double tax treaty between latvia and the russian federation remi troch, riga 8 june 2011

TRANSCRIPT

Double Tax Treaty between Latvia and the Russian Federation

Remi Troch, Riga 8 June 2011

Double Tax Treaty between Latvia and the Russian Federation The treaty was signed in December 2010.

So far, it has not yet gone through the whole ratification process (such as: Approval in the Saeima and the Russian Parliament).

Based on the obtained information, the treaty is currently being reviewed by the Russian Ministry of Justice for approximately a month. Their conclusion should be issued within the next couple of days.

.

Double Tax Treaty between Latvia and the Russian Federation

After this stage, the draft of the legislative act on the ratification of the treaty shall be passed to the Russian Government and then, after being approved by the Governmental Commission, sent to the State Duma for approbation.

It is impossible to estimate the timeframes for the described procedures.

It seems therefore unlikely that it will enter into force on 1 January 2012, as is generally expected.

Double Tax Treaty between Latvia and the Russian Federation The Treaty contains 31 articles.

Protocol with 4 points on 4 different articles.

Done in English, Latvian and Russian; in case of dispute, the English text shall prevail.

More liberal in assessing the criteria for the existence of a Permanent Establishment (“PE”) than the Latvian Corporate Income tax Law and the Law on Taxes and Duties.

Double Tax Treaty between Latvia and the Russian Federation The term “Latvian Republic” and “Russian Federation” include its

exclusive economic zone and continental shelf as defined in accordance

with international law, including the 1982 UN Law on the Sea Convention.

The term "international traffic" means any transport by ship, aircraft, road

or rail transport vehicle operated by an enterprise of a Contracting State

except when the vessel, aircraft, vehicle or railway vehicle is operating

solely between places in the other contracting State.

Double Tax Treaty between Latvia and the Russian Federation Permanent establishment (article 5):

Today, a Russian company which carries out construction works (including repairs) assembly, and similar activity in Latvia could face the existence of a PE. The Latvian law on Taxes and Duties is much more restrictive than the not yet ratified Latvian-Russian DTT: where the latter stipulates that a construction site only constitutes a PE when it last longer than 9 months, the internal law does not contain such a clause, so that the tax authorities can conclude to the existence of a PE as soon as a construction, assembly, etc. work has started.

There is however a time criterion for services: 30 days in any six months period; however there is not necessarily an analogy between the two.

Double Tax Treaty between Latvia and the Russian Federation Income from immovable property (article 6):

Income derived by a resident of a Contracting State derives from immovable property (including income from agriculture or forestry) situated in the other Contracting State may be taxed in that other State.

Ships, aircraft, auto and railway vehicles shall not be regarded as immovable property.

Double Tax Treaty between Latvia and the Russian Federation International traffic (article 8):

Profits derived by a resident of a Contracting State from the operation of ships, aircraft, road or railway vehicles in international traffic shall be taxable only in that State.

Profits from the use of said vehicles in international traffic includes:a) profits from the bareboat lease of ships, aircraft, auto or rail vehicle, andb) profits from the use, maintenance or lease of containers (including trailers and similar equipment for transportation of containers), for the transportation of goods or merchandise,

Double Tax Treaty between Latvia and the Russian Federation International traffic (article 8), Ctd:

where such use, maintenance or rental , as the case may be, is incidental to the operation of ships, aircraft, road or railway vehicles by the enterprise in international traffic.

The provisions of paragraph 1 and 2 shall also apply to profits from the participation in a pool, a joint business or in an international operating agency.

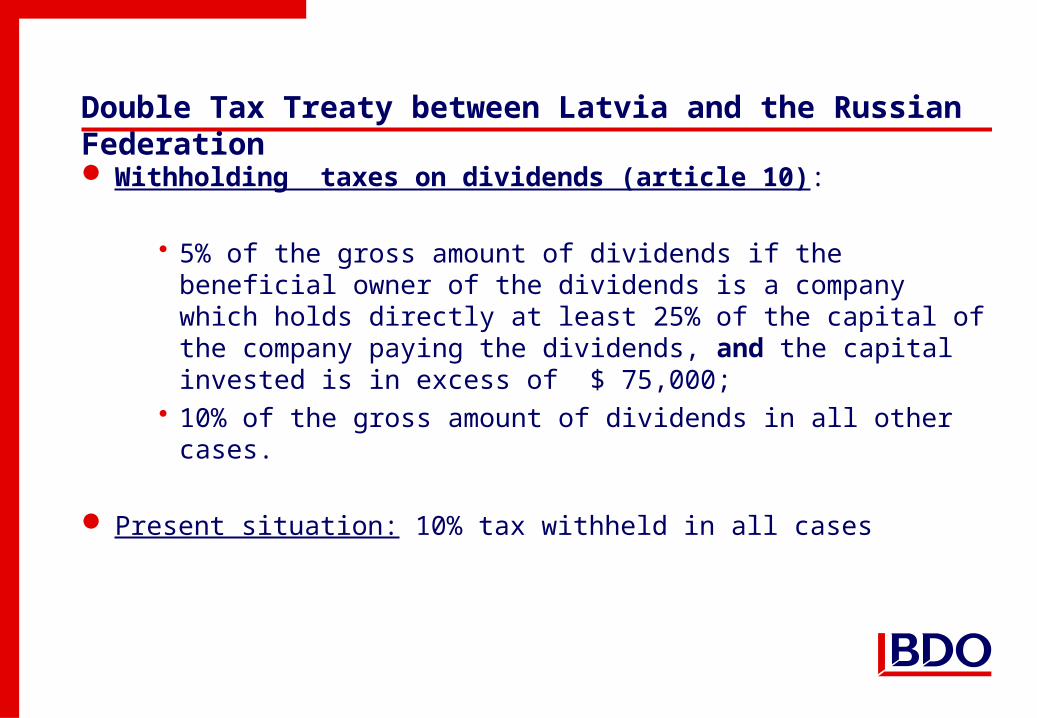

Double Tax Treaty between Latvia and the Russian Federation Withholding taxes on dividends (article 10):

5% of the gross amount of dividends if the beneficial owner of the dividends is a company which holds directly at least 25% of the capital of the company paying the dividends, and the capital invested is in excess of $ 75,000;

10% of the gross amount of dividends in all other cases.

Present situation: 10% tax withheld in all cases

Double Tax Treaty between Latvia and the Russian Federation Other withholding taxes (article 11 and 12):

Interest: - 5% on interest on loans between financial institutions of the two States,

- 10% in all other cases, except on loans guaranteed by a Government: 0%.

- present situation: 10% on interest paid to an associated non-resident company

• Royalties: - 5%

- present situation: 5%; 15% on copyright to literary or artistic works

Double Tax Treaty between Latvia and the Russian Federation

Other withholding taxes, Ctd:

Currently, management and consultancy fees are subject to a 10% withholding tax; if

the tax was not withheld, the taxable income will be increased by the amount of the

expense.

Under the Treaty (Non-discrimination clause: article 25) no withholding tax on

management and consultancy fees, can be levied, provided a residence certificate is

submitted to the tax authorities.

Double Tax Treaty between Latvia and the Russian Federation Capital gains (article 13):

Gains derived by a resident of a Contracting State from the alienation of shares deriving more than 50 per cent of their value directly or indirectly from immovable property situated in the other Contracting State may be taxed in that other State.

Gains derived by an enterprise of a Contracting State - which is engaged in the international traffic of ships, aircraft, road or railway vehicles - from the alienation of such ships, aircraft, road or rail transport or movable property pertaining to such vessels, aircraft , road or railway vehicles, shall be taxable only in that State.

Double Tax Treaty between Latvia and the Russian Federation Income from dependent services (i.e. salary) (article 15):

Remuneration derived by a resident of a Contracting State in respect of an employment exercised in the other Contracting State shall be taxable only in the first-mentioned State if:

a) the recipient is present in the other State for a period or periods not exceeding in the aggregate 183 days in any twelve month period commencing or ending in the fiscal year concerned, and

b) the remuneration is paid by, or on behalf of, an employer who is not a resident of the other State, and

c) the remuneration is not borne by a permanent establishment which the employer has in the other State.

Double Tax Treaty between Latvia and the Russian Federation Income from dependent services (i.e. salary), Ctd:

Notwithstanding the preceding provisions of this Article, remuneration derived in respect of paid employment (salaried work) performed on the vessels, aircraft, auto or rail used in international traffic, and which belong to the company registered in the Contracting State, may be taxed in that State.

Double Tax Treaty between Latvia and the Russian Federation PENSIONS (article 18):

Pensions and other similar remuneration derived by a resident of a Contracting State in consideration of past employment shall be taxable only in that State.

• However such pensions and other similar remuneration paid by the other Contracting State or a political subdivision or local authority, or who are paid from funds created by the State or a political subdivision, shall be taxable only in that other State.

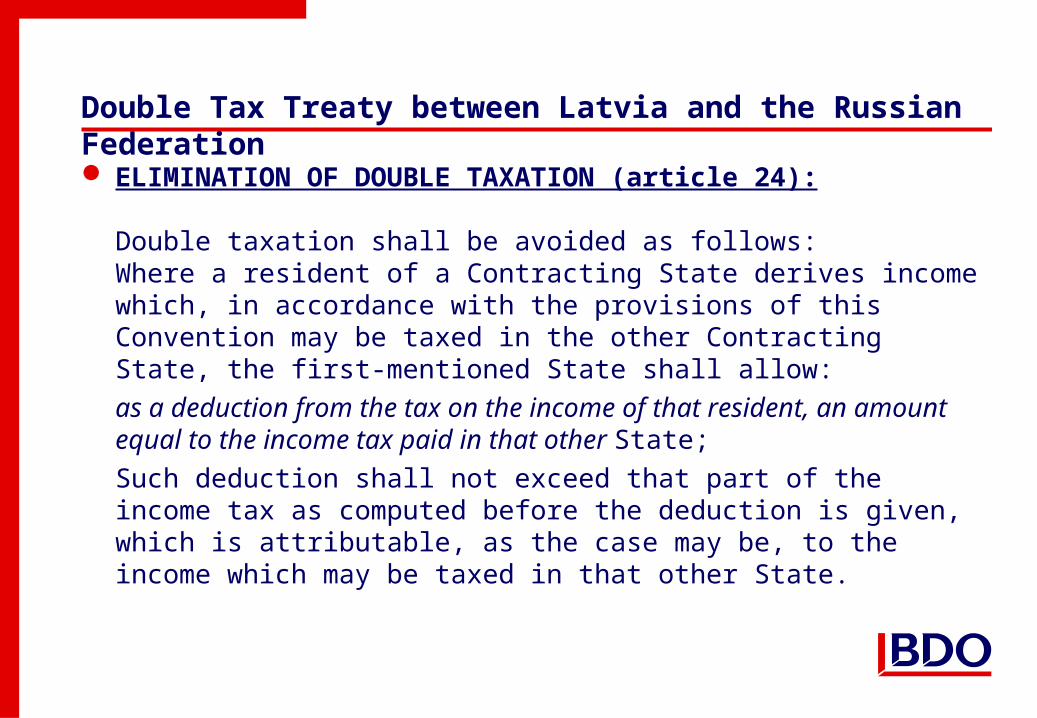

Double Tax Treaty between Latvia and the Russian Federation ELIMINATION OF DOUBLE TAXATION (article 24):

Double taxation shall be avoided as follows:Where a resident of a Contracting State derives income which, in accordance with the provisions of this Convention may be taxed in the other Contracting State, the first-mentioned State shall allow:

as a deduction from the tax on the income of that resident, an amount equal to the income tax paid in that other State;

Such deduction shall not exceed that part of the income tax as computed before the deduction is given, which is attributable, as the case may be, to the income which may be taxed in that other State.

Double Tax Treaty between Latvia and the Russian Federation NON- DISCRIMINATION (article 25):

Nationals of a Contracting State shall not be subjected in the other Contracting State to any taxation or any requirement connected therewith, which is other or more burdensome than the taxation and connected requirements to which nationals of that other State in the same circumstances, in particular with respect to residence, are or may be

subjected. NO withholding tax on fees

The taxation of a PE which an enterprise of a Contracting State has in the other Contracting State shall not be less favourable than the taxation levied on enterprises of that other State carrying on the same activities.

Double Tax Treaty between Latvia and the Russian Federation MUTUAL AGREEMENT PROCEDURE (article 26):

Where a person considers that the actions of one or both of the Contracting States result or will result for him in taxation not in accordance with the provisions of this Convention, he may, irrespective of the remedies provided by the domestic law of those States, present his case to the competent authority of the Contracting State of which he is a

resident .

The case must be presented within three years from the first notification of the action resulting in taxation not in accordance with the provisions of the Convention.

Double Tax Treaty between Latvia and the Russian Federation INFORMATION EXCHANGE (article 27):

The competent authorities of the Contracting States shall exchange such

information as is necessary for carrying out the provisions of this

Agreement or of the domestic laws of the Contracting States concerning

taxes of every kind and description imposed on behalf of the Contracting

States, or of their political subdivisions or local authorities, insofar as the

taxation thereunder is not contrary to the Agreement. The exchange of

information is not restricted by Articles 1 and 2 (i.e. also VAT and other

indirect taxes).

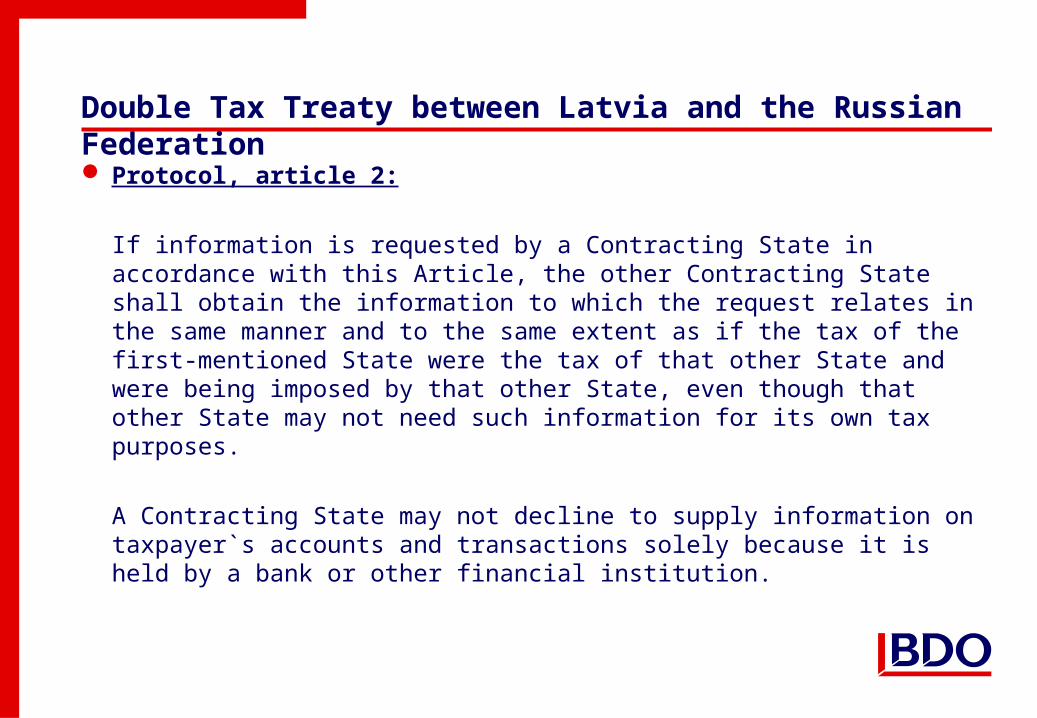

Double Tax Treaty between Latvia and the Russian Federation Protocol, article 2:

If information is requested by a Contracting State in accordance with this Article, the other Contracting State shall obtain the information to which the request relates in the same manner and to the same extent as if the tax of the first-mentioned State were the tax of that other State and were being imposed by that other State, even though that other State may not need such information for its own tax purposes.

A Contracting State may not decline to supply information on taxpayer`s accounts and transactions solely because it is held by a bank or other financial institution.

Double Tax Treaty between Latvia and the Russian Federation ASSISTANCE IN COLLECTION (article 28):

The Contracting States undertake to provide each other assistance in the

collection of a taxpayer’s unpaid taxes to the extent that this amount is

finally determined in accordance with laws and regulations of the

requesting Contracting State.

Double Tax Treaty between Latvia and the Russian Federation ENTRY INTO FORCE (article 30):

As of today, the treaty is not yet ratified and hence the provisions are not applicable. Each Contracting State through diplomatic channels in writing notifies the other State on the completion of the procedure prescribed by the internal law for entry into force of this Agreement.It shall enter into force on the date of the last notification and its provisions in both Contracting States are applicable to:a) in relation to taxes withheld at source - income received on the first day of January or thereafter in the calendar year following the year in which the Agreement enters into force;b) in respect of other taxes on income - taxes chargeable for any fiscal year beginning on the first day of January or thereafter in the calendar year following the year in which the Agreement enters into force.

Double Tax Treaty between Latvia and the Russian Federation

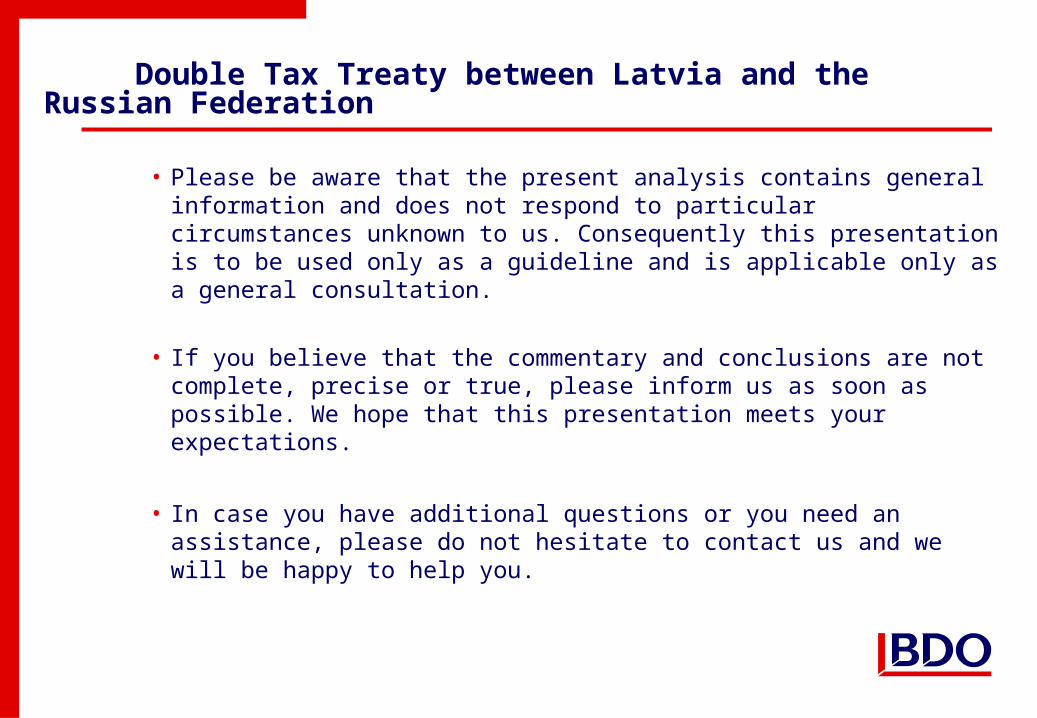

• Please be aware that the present analysis contains general information and does not respond to particular circumstances unknown to us. Consequently this presentation is to be used only as a guideline and is applicable only as a general consultation.

• If you believe that the commentary and conclusions are not complete, precise or true, please inform us as soon as possible. We hope that this presentation meets your expectations.

• In case you have additional questions or you need an assistance, please do not hesitate to contact us and we will be happy to help you.

Remi Troch

Director International taxes“BDO Zelmenis & Liberte”Attorneys at lawAlberta street 1-2, Riga, LV-1010Phone: (+371) 67222237Fax: (+371) 67222236E-mail: [email protected]

CONTACTS