© 2005 The McGraw-Hill Companies, Inc., All Rights ReservedMcGraw-Hill/Irwin

Slide 1

CHAPTER ELEVEN

INVESTMENT ANALYSIS AND TAXATION OF INCOME

PROPERTIES

© 2005 The McGraw-Hill Companies, Inc., All Rights ReservedMcGraw-Hill/Irwin

Slide 2

Motivation For Investing

Rate of return Price appreciation Diversification Tax benefits

© 2005 The McGraw-Hill Companies, Inc., All Rights ReservedMcGraw-Hill/Irwin

Slide 3

Hierarchy of Investment Strategies

1. Sector or Industry

2. Type of property in the industry

© 2005 The McGraw-Hill Companies, Inc., All Rights ReservedMcGraw-Hill/Irwin

Slide 4

Investment StrategiesA. Property sector investingB. Contrarian investing

Major economic, technological and other factors would make a property of poor type.

C. Market timingD. Growth investingE. Value investing

A. Overlooked by investors

© 2005 The McGraw-Hill Companies, Inc., All Rights ReservedMcGraw-Hill/Irwin

Slide 5

Investment Strategies

F. Size of property

G. Strategy as to tenants

H. Arbitrage investing

I. Turn around/ special situation

J. Blue chip properties

© 2005 The McGraw-Hill Companies, Inc., All Rights ReservedMcGraw-Hill/Irwin

Slide 6

Real Estate Investment Analysis

Investment Strategy Investment philosophy

Investment objectives

Investment policies

© 2005 The McGraw-Hill Companies, Inc., All Rights ReservedMcGraw-Hill/Irwin

Slide 7

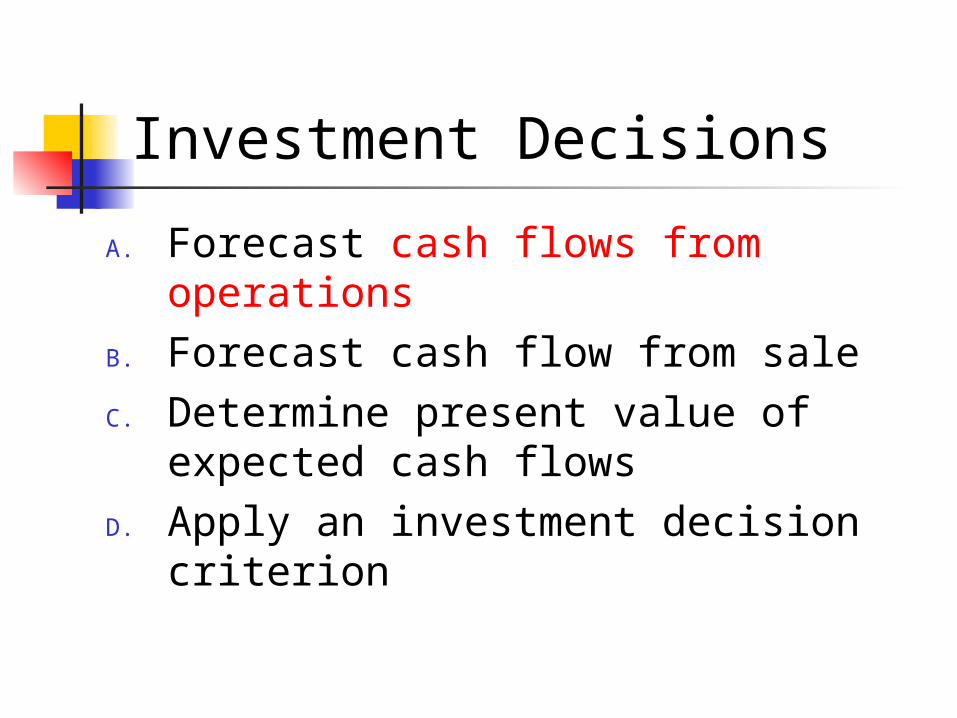

Investment Decisions

A. Forecast cash flows from operations

B. Forecast cash flow from saleC. Determine present value of

expected cash flowsD. Apply an investment decision

criterion

© 2005 The McGraw-Hill Companies, Inc., All Rights ReservedMcGraw-Hill/Irwin

Slide 8

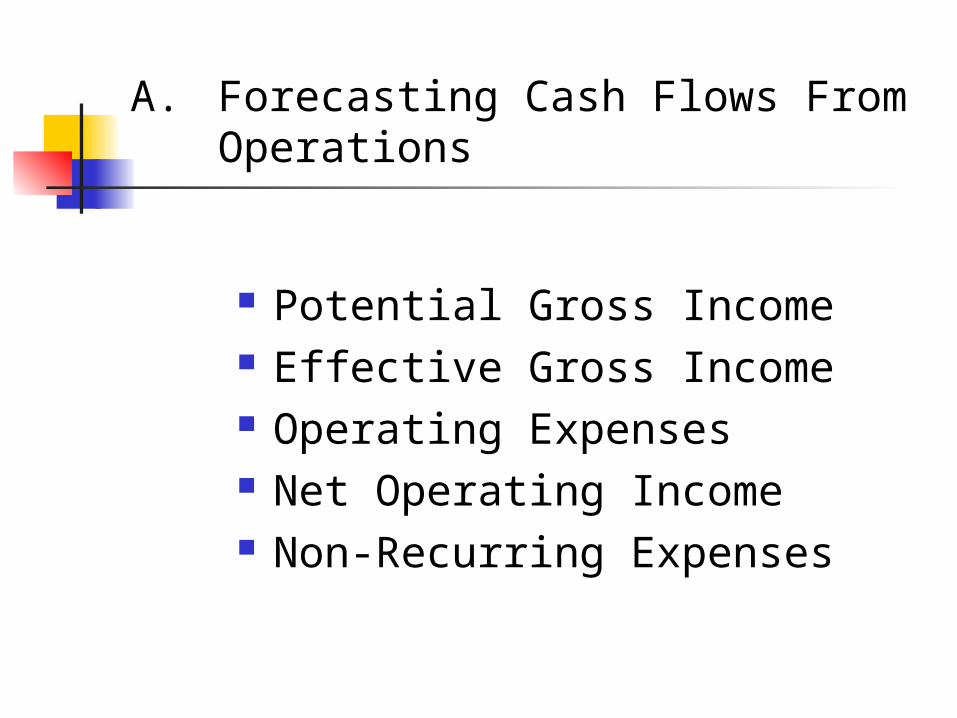

A. Forecasting Cash Flows From Operations

Potential Gross Income Effective Gross Income Operating Expenses Net Operating Income Non-Recurring Expenses

© 2005 The McGraw-Hill Companies, Inc., All Rights ReservedMcGraw-Hill/Irwin

Slide 9

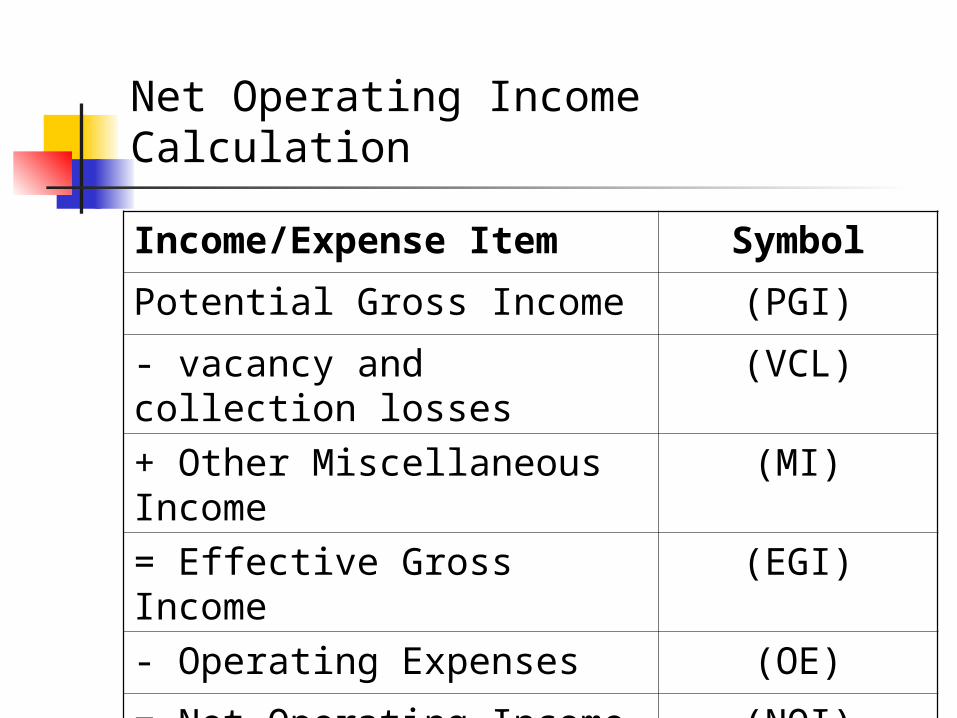

Net Operating Income Calculation

Income/Expense Item Symbol

Potential Gross Income (PGI)

- vacancy and collection losses

(VCL)

+ Other Miscellaneous Income

(MI)

= Effective Gross Income (EGI)

- Operating Expenses (OE)

= Net Operating Income (NOI)

© 2005 The McGraw-Hill Companies, Inc., All Rights ReservedMcGraw-Hill/Irwin

Slide 10

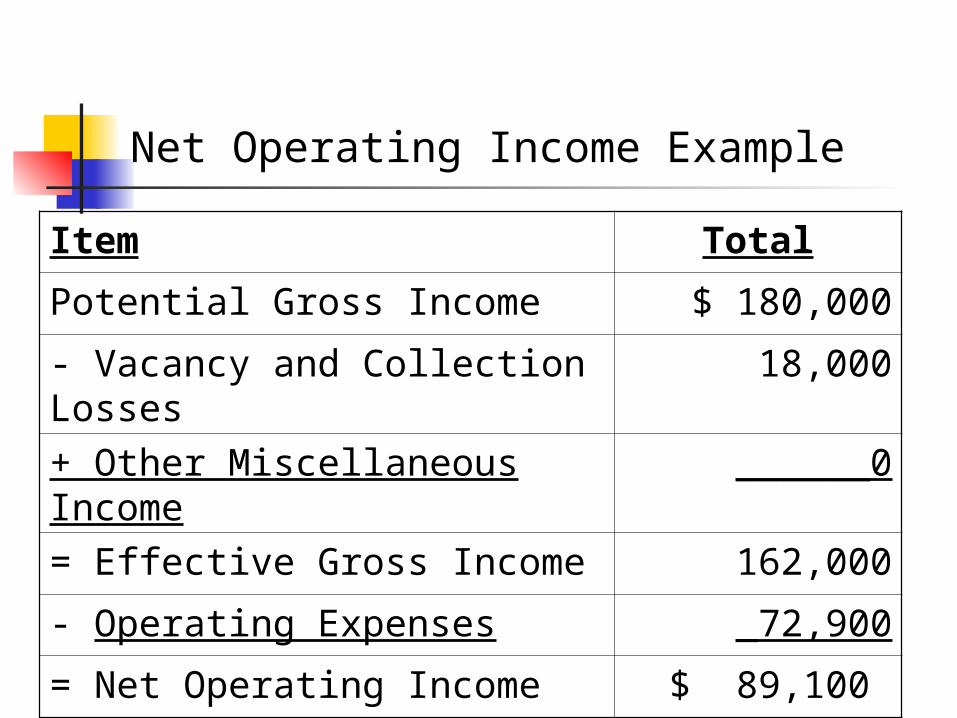

Net Operating Income Example

Item Total

Potential Gross Income $ 180,000

- Vacancy and Collection Losses

18,000

+ Other Miscellaneous Income

______0

= Effective Gross Income 162,000

- Operating Expenses _72,900

= Net Operating Income $ 89,100

© 2005 The McGraw-Hill Companies, Inc., All Rights ReservedMcGraw-Hill/Irwin

Slide 11

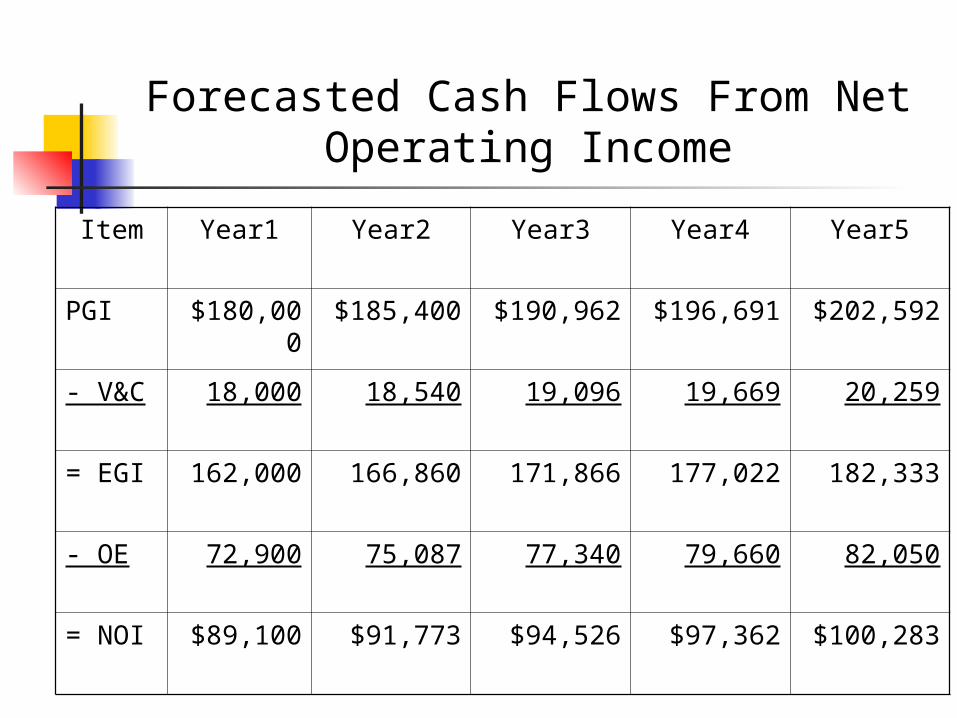

Forecasted Cash Flows From Net Operating Income

Item Year1 Year2 Year3 Year4 Year5

PGI $180,000

$185,400 $190,962 $196,691 $202,592

- V&C 18,000 18,540 19,096 19,669 20,259

= EGI 162,000 166,860 171,866 177,022 182,333

- OE 72,900 75,087 77,340 79,660 82,050

= NOI $89,100 $91,773 $94,526 $97,362 $100,283

© 2005 The McGraw-Hill Companies, Inc., All Rights ReservedMcGraw-Hill/Irwin

Slide 12

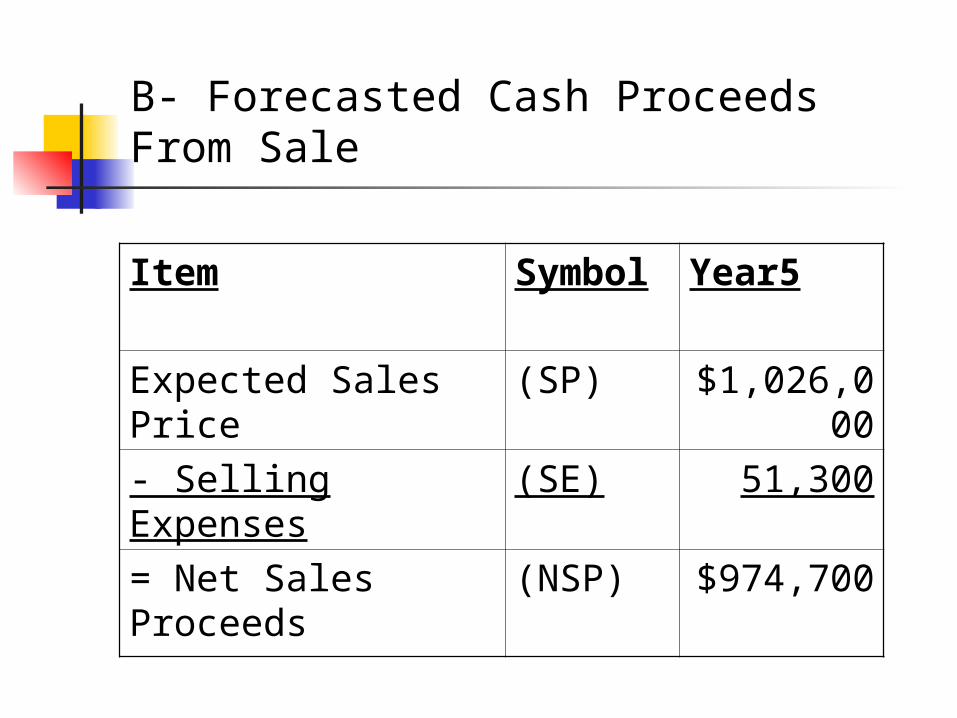

B- Forecasted Cash Proceeds From Sale

Item Symbol Year5

Expected Sales Price

(SP) $1,026,000

- Selling Expenses (SE) 51,300

= Net Sales Proceeds

(NSP) $974,700

© 2005 The McGraw-Hill Companies, Inc., All Rights ReservedMcGraw-Hill/Irwin

Slide 13

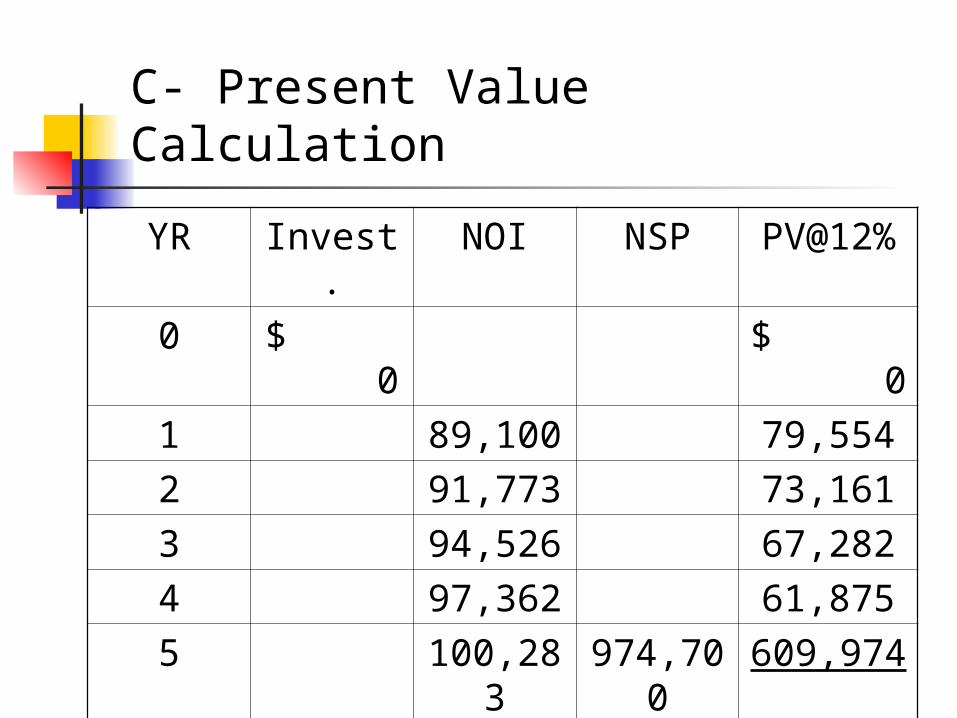

C- Present Value Calculation

YR Invest. NOI NSP PV@12%

0 $ 0

$ 0

1 89,100 79,554

2 91,773 73,161

3 94,526 67,282

4 97,362 61,875

5 100,283

974,700

609,974

PV= $891,846

© 2005 The McGraw-Hill Companies, Inc., All Rights ReservedMcGraw-Hill/Irwin

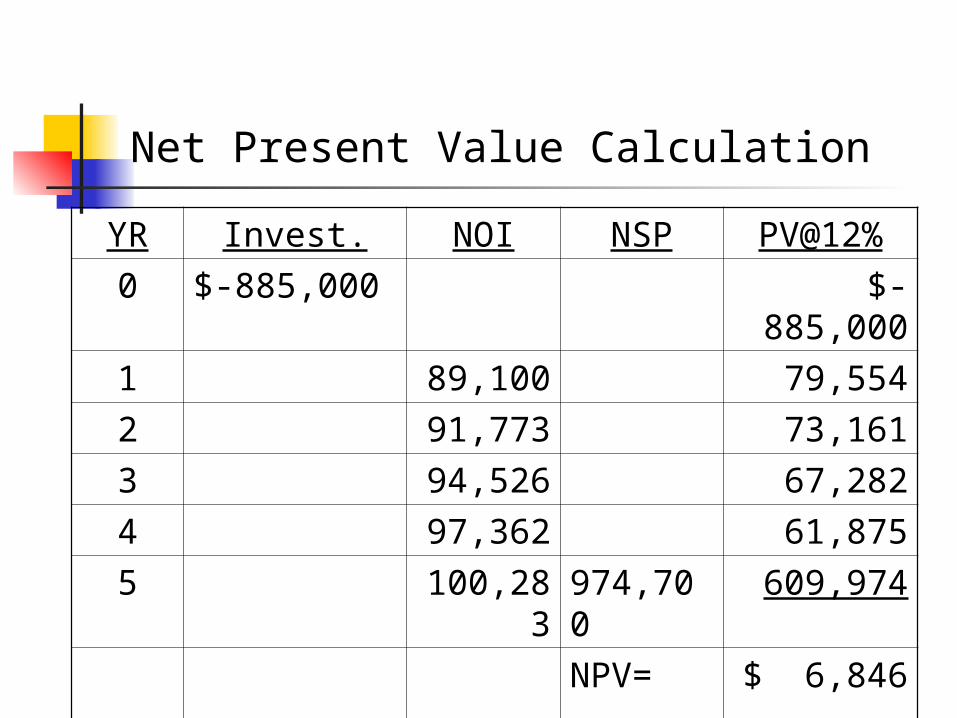

Slide 14

Net Present Value (NPV)

The net present value is the present value of a project’s cash inflows, minus the present value of the cash outflows.

The cash flows are discounted at the investor’s required rate of return– in the example 12 percent.

© 2005 The McGraw-Hill Companies, Inc., All Rights ReservedMcGraw-Hill/Irwin

Slide 15

Net Present Value Calculation

YR Invest. NOI NSP PV@12%

0 $-885,000 $-885,000

1 89,100 79,554

2 91,773 73,161

3 94,526 67,282

4 97,362 61,875

5 100,283

974,700 609,974

PV = NPV=

$891,846$ 6,846

© 2005 The McGraw-Hill Companies, Inc., All Rights ReservedMcGraw-Hill/Irwin

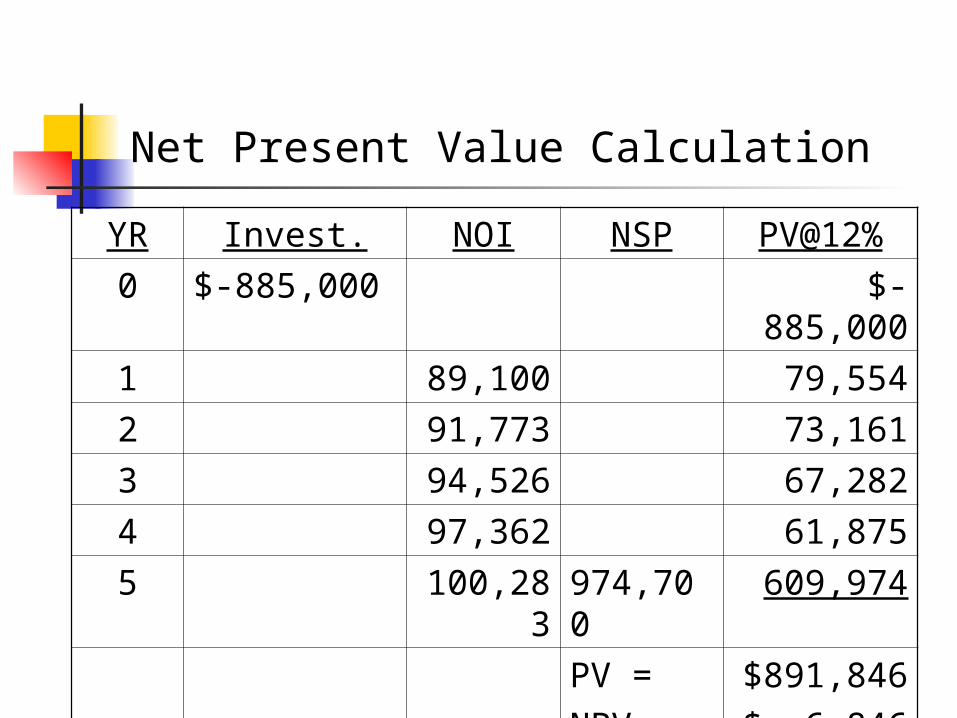

Slide 16

Net Present Value Calculation

YR Invest. NOI NSP PV@12%

0 $-885,000 $-885,000

1 89,100 79,554

2 91,773 73,161

3 94,526 67,282

4 97,362 61,875

5 100,283

974,700 609,974

NPV= $ 6,846

© 2005 The McGraw-Hill Companies, Inc., All Rights ReservedMcGraw-Hill/Irwin

Slide 17

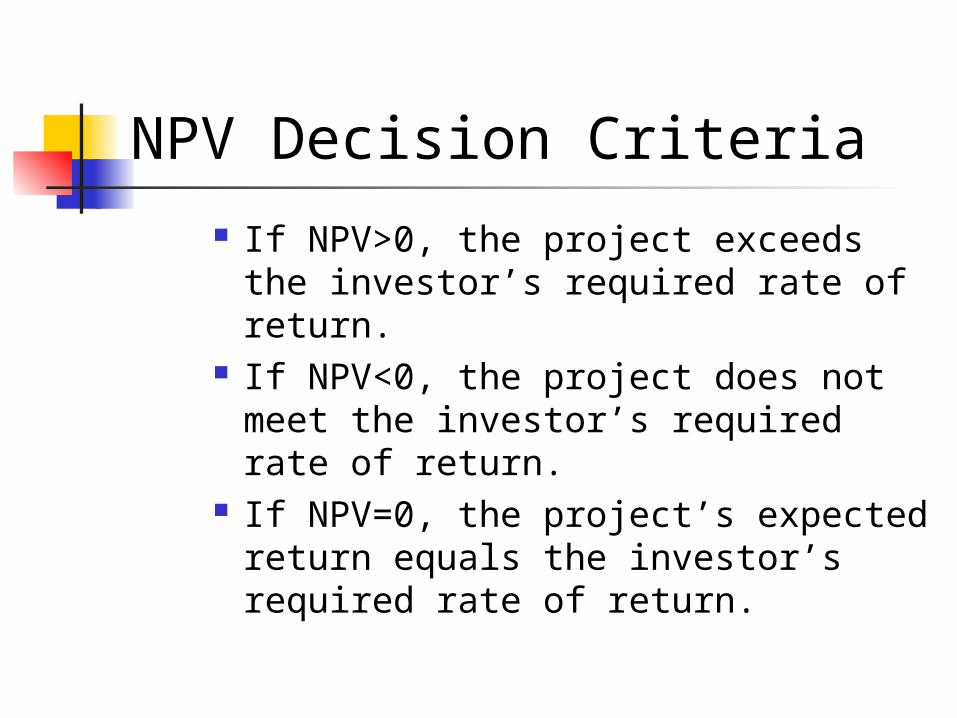

NPV Decision Criteria

If NPV>0, the project exceeds the investor’s required rate of return.

If NPV<0, the project does not meet the investor’s required rate of return.

If NPV=0, the project’s expected return equals the investor’s required rate of return.

© 2005 The McGraw-Hill Companies, Inc., All Rights ReservedMcGraw-Hill/Irwin

Slide 18

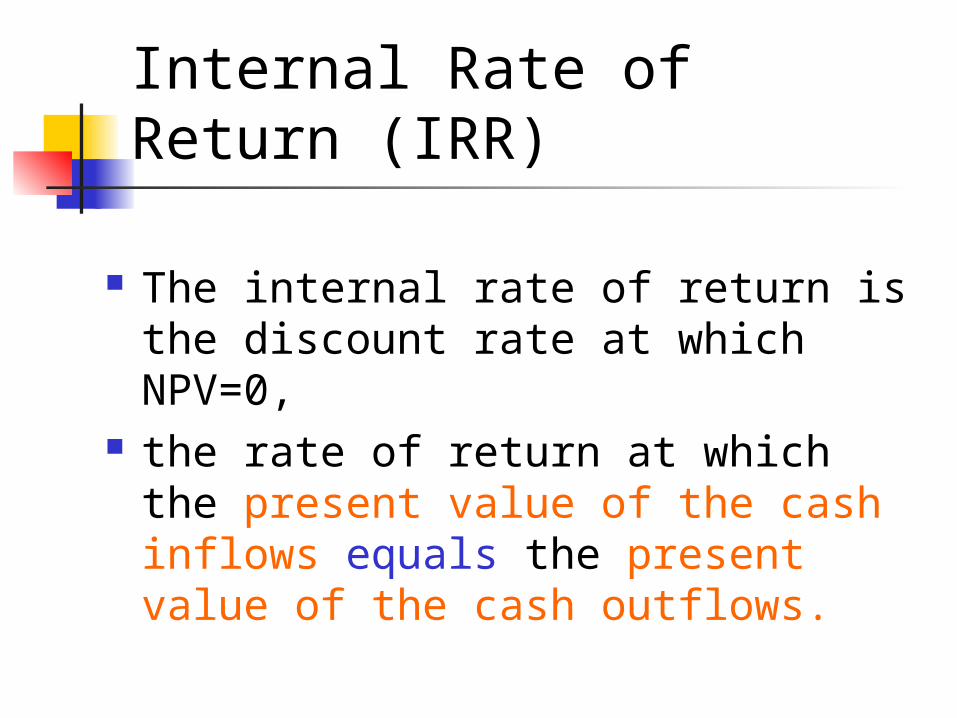

Internal Rate of Return (IRR)

The internal rate of return is the discount rate at which NPV=0,

the rate of return at which the present value of the cash inflows equals the present value of the cash outflows.

© 2005 The McGraw-Hill Companies, Inc., All Rights ReservedMcGraw-Hill/Irwin

Slide 19

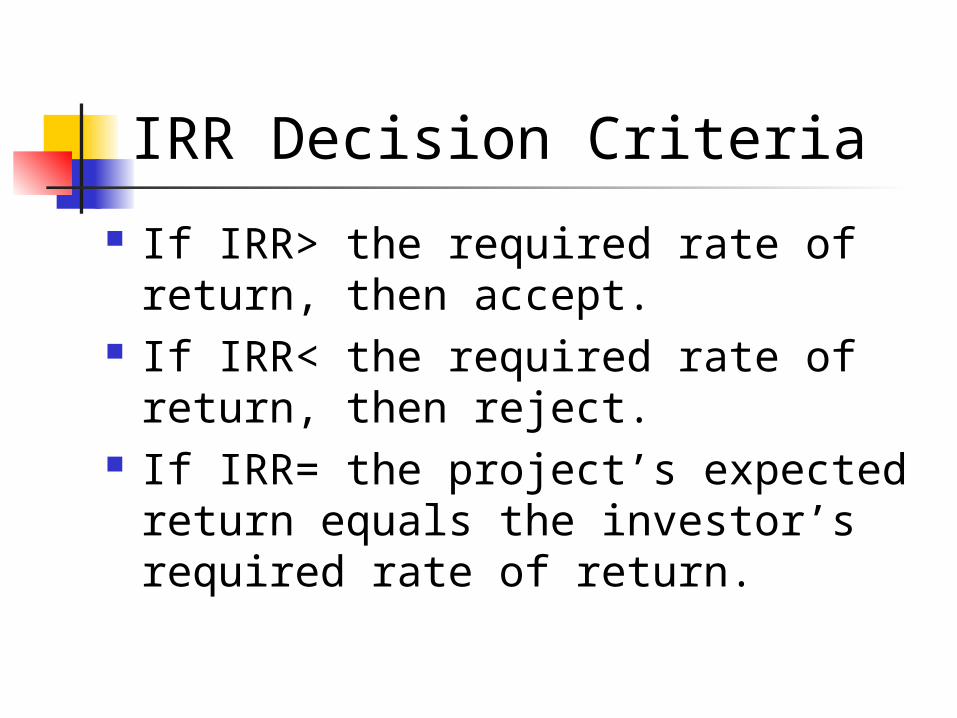

IRR Decision Criteria

If IRR> the required rate of return, then accept.

If IRR< the required rate of return, then reject.

If IRR= the project’s expected return equals the investor’s required rate of return.

© 2005 The McGraw-Hill Companies, Inc., All Rights ReservedMcGraw-Hill/Irwin

Slide 20

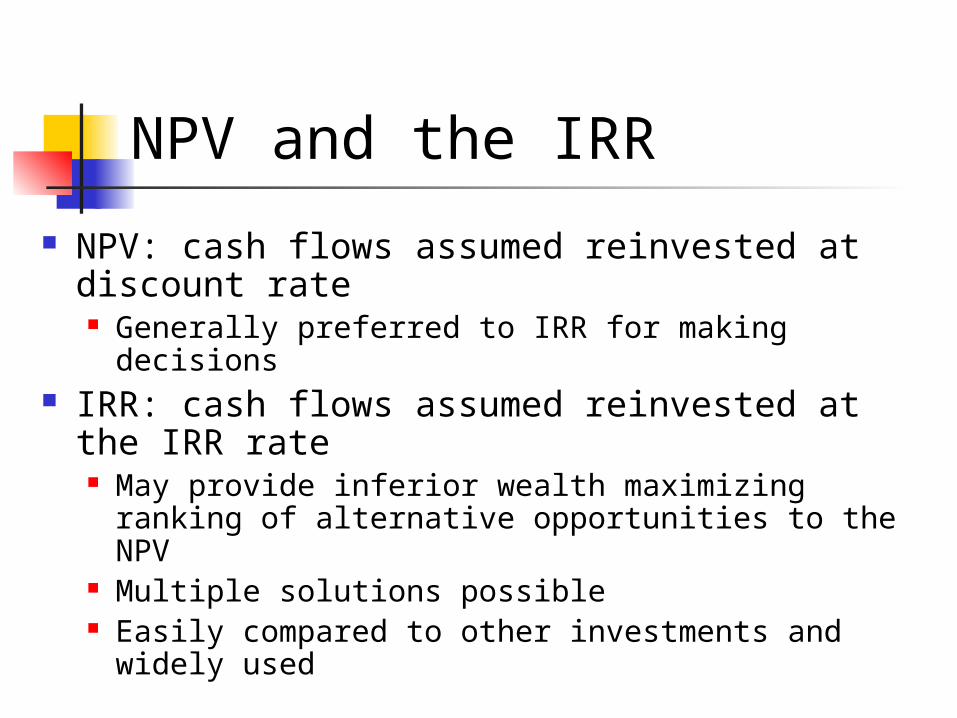

NPV and the IRR

NPV: cash flows assumed reinvested at discount rate Generally preferred to IRR for making decisions

IRR: cash flows assumed reinvested at the IRR rate May provide inferior wealth maximizing ranking of

alternative opportunities to the NPV Multiple solutions possible Easily compared to other investments and widely

used

© 2005 The McGraw-Hill Companies, Inc., All Rights ReservedMcGraw-Hill/Irwin

Slide 21

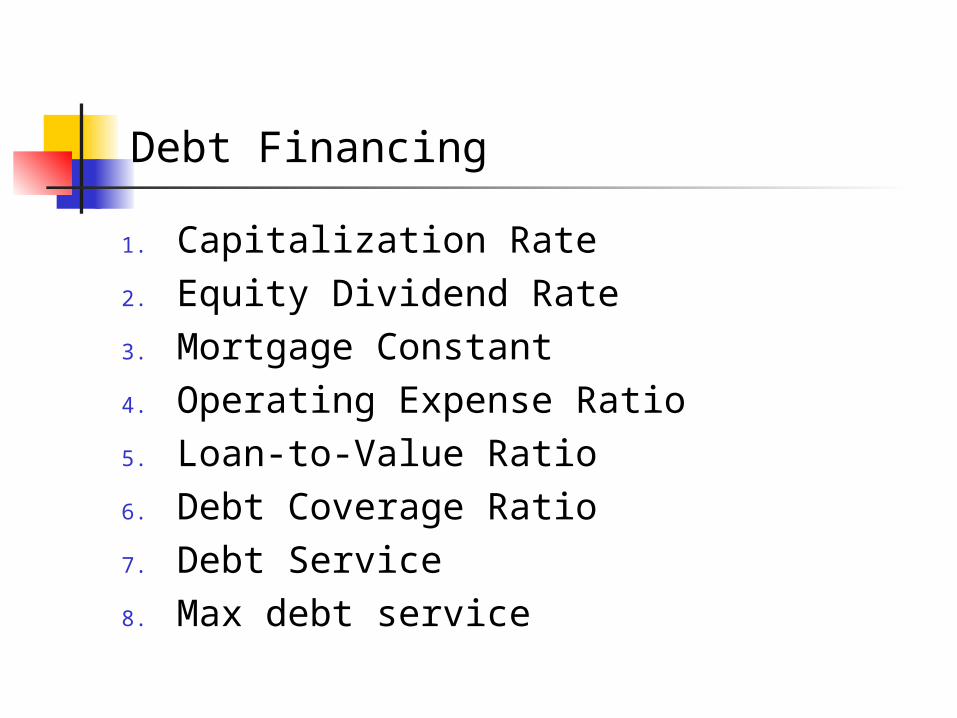

Debt Financing

1. Capitalization Rate2. Equity Dividend Rate3. Mortgage Constant4. Operating Expense Ratio5. Loan-to-Value Ratio6. Debt Coverage Ratio7. Debt Service8. Max debt service

© 2005 The McGraw-Hill Companies, Inc., All Rights ReservedMcGraw-Hill/Irwin

Slide 22

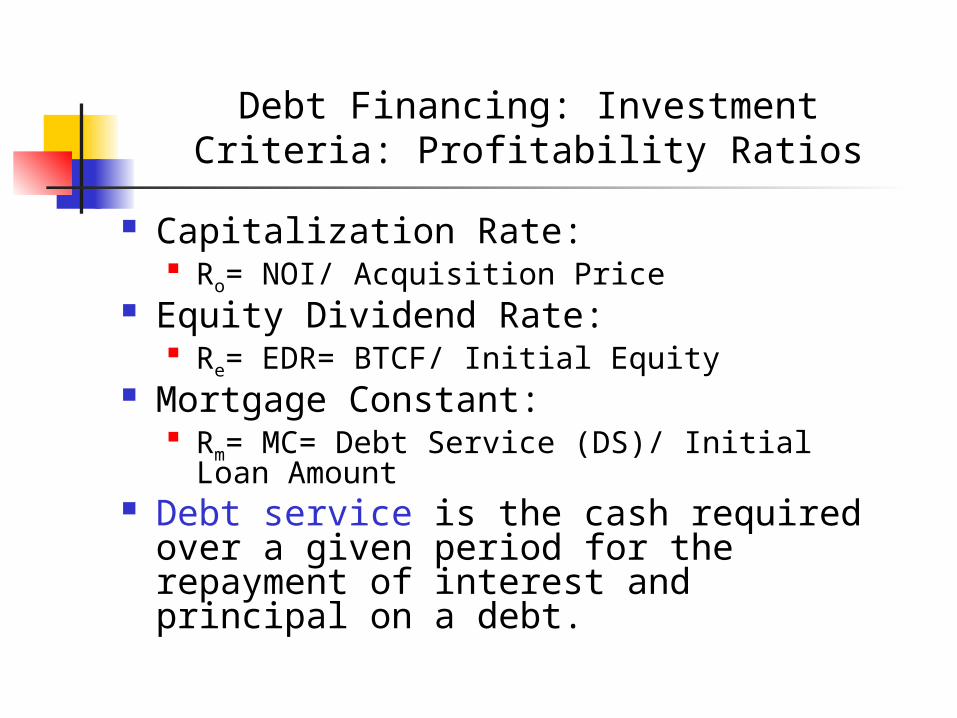

Debt Financing: Investment Criteria: Profitability Ratios

Capitalization Rate: Ro= NOI/ Acquisition Price

Equity Dividend Rate: Re= EDR= BTCF/ Initial Equity

Mortgage Constant: Rm= MC= Debt Service (DS)/ Initial Loan

Amount Debt service is the cash required over

a given period for the repayment of interest and principal on a debt.

© 2005 The McGraw-Hill Companies, Inc., All Rights ReservedMcGraw-Hill/Irwin

Slide 23

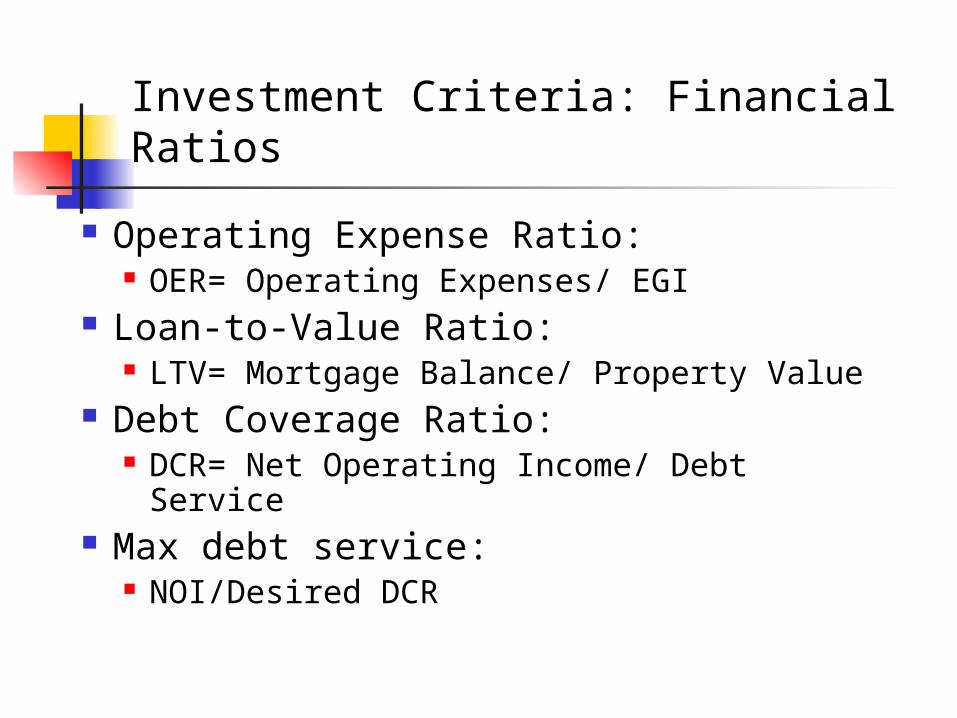

Investment Criteria: Financial Ratios

Operating Expense Ratio: OER= Operating Expenses/ EGI

Loan-to-Value Ratio: LTV= Mortgage Balance/ Property Value

Debt Coverage Ratio: DCR= Net Operating Income/ Debt

Service Max debt service:

NOI/Desired DCR

© 2005 The McGraw-Hill Companies, Inc., All Rights ReservedMcGraw-Hill/Irwin

Slide 24

End of chapter!