1

2

Forward-Looking Statements October 30, 2008This presentation contains forward-looking statements including, among other things, management's outlook, estimates of future performance, revenue, earnings per share, and growth objectives. The forward-looking statements contained herein are based on our current expectations and are subject to a number of risks and uncertainties that could cause us to fail to achieve our current financial projections and other expectations, such as changes in the demand for the V.A.C. resulting from increased competition, the seasonal slowing of V.A.C. unit growth in the fourth and first quarter of each year, changes in payer reimbursement policies, our ability to achieve expected benefits from our recent acquisition of LifeCell and our ability to protect our intellectual property rights. All information set forth in this presentation is as of today’s date. We undertake no duty to update this information. More information about potential factors that could cause our results to differ or adversely affect our business and financial results is included in our Annual Report on Form 10-K for the fiscal year ended December 31, 2007 and in our Quarterly Report on Form 10-Q for the quarterly period ended June 30, 2008, including, among other sections, under the captions, "Risk Factors" and "Management's Discussion and Analysis of Financial Condition and Results of Operations." These reports are on file with the SEC and available at the SEC's website at www.sec.gov. Additional information will also be set forth in those sections in our Quarterly Report on Form 10-Q for the quarterly period ended September 30, 2008, which will be filed with the SEC in early November 2008.

TRADEMARKS

The following trademarks are proprietary to KCI Licensing, Inc. and/or LifeCell Corporation, their affiliates and/or licensors and may be used in this presentation: ActiV.A.C., AlloDerm, AlloDermGBR, Conexa, Cymetra, GranuFoam, InfoV.A.C., KCI, KCI The Clinical Advantage, Kinetic Concepts, LifeCell, RotoProne, SensaT.R.A.C., Strattice, T.R.A.C., V.A.C., V.A.C. ATS, V.A.C. Freedom, V.A.C. GranuFoam Silver, V.A.C. Instill, and V.A.C. Therapy. The absence of a trademark or service mark or logo from this list does not constitute a waiver of trademark or other intellectual property rights of KCI Licensing, Inc. and/or LifeCell Corporation.

3

Time Topic Presenter

8:00 am Strategic OverviewWound Healing Overview Cathy Burzik, President and CEO

9:00 am Regenerative Medicine Lisa Colleran, Global President, LifeCell

9:20 am Therapeutic Support Systems Lynne Sly, Global President, TSS

9:30 am Research & Development Dr. Todd Fruchterman, Sr. VP & CTODr. John Harper, VP Clinical Sciences

10:30 am Break

10:40 am Financial Overview Marty Landon, Sr. VP & CFO

11:00 am Q&A Panel KCI Management

11:30 am Lunch speaker Dr. John Pryor, Trauma Program Director, University of Pennsylvania Health System

12:30 pm KCI Tours

Today’s Agenda

4

Strategic OverviewClinically focused…Outcomes driven

Cathy BurzikPresident & CEO

5

To advance the power of innovative therapies, advanced wound healing and regenerative medicine.

KCI at a GlanceOur Mission

6

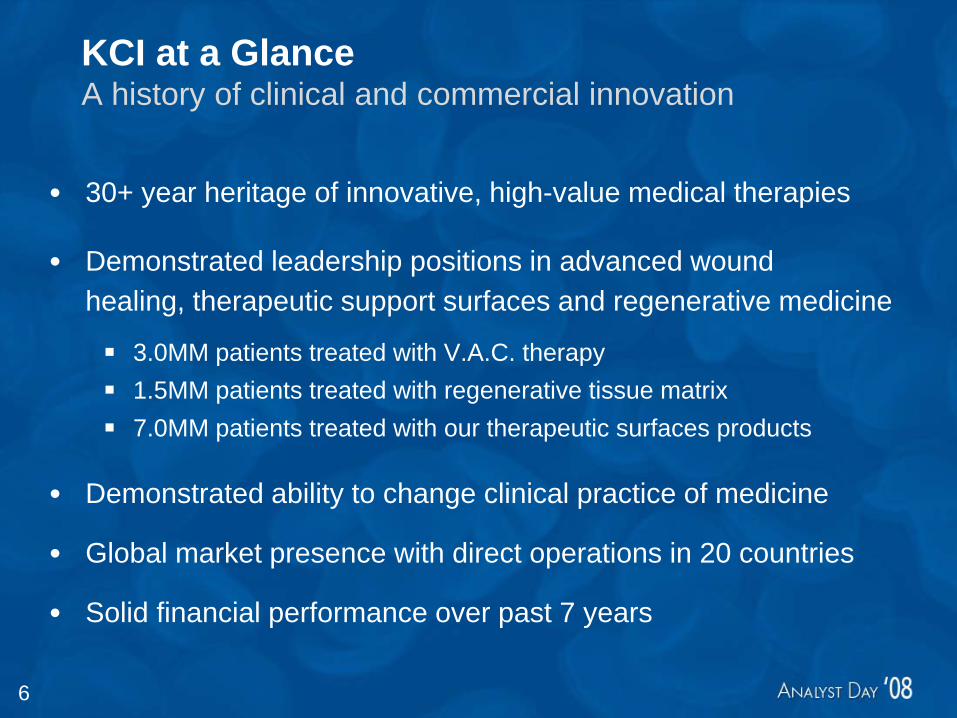

KCI at a GlanceA history of clinical and commercial innovation

• 30+ year heritage of innovative, high-value medical therapies

• Demonstrated leadership positions in advanced wound healing, therapeutic support surfaces and regenerative medicine

3.0MM patients treated with V.A.C. therapy1.5MM patients treated with regenerative tissue matrix7.0MM patients treated with our therapeutic surfaces products

• Demonstrated ability to change clinical practice of medicine

• Global market presence with direct operations in 20 countries

• Solid financial performance over past 7 years

7

KCI at a GlanceLTM 09/08 Business Summary

WoundHealing (WH)

Therapeutic Support Systems

(TSS)

Regenerative Medicine (RM)

Market Size& Growth

KCI MarketPosition

KCI Revenue (1)(LTM Q3)

~$4.5 Billion(Advanced Wound Care)

5 to 6% Growth

~ $1 Billion 18 to 22% Growth

~ $2.5 Billion 2 to 3% Growth

#1 #1 #2

$1,391 Million13.3%

Y-o-Y Growth

CurrentMarket

• Surgical, trauma & chronic wounds

• Acute & Post-Acute

• Challenging Hernia• Breast Reconstruction

• Complications of immobility

• Pulmonary & skin integrity

• Patient handling

$227 Million27.7%

Y-o-Y Growth

$339 Million5.9%

Y-o-Y Growth

Revenue Mix (1) 71% 12% 17%

(1) On a Proforma basis as if LifeCell was owned by KCI the entire period

8

KCI at a GlanceGlobal Sales Force Footprint

9

Cathy BurzikPresident & CEO

Marty LandonSVP & CFO

Steve SeidelSVP & Gen Counsel

Lisa ColleranGlobal President,

LifeCell

Lynne SlyGlobal President,

TSS

Todd Fruchterman SVP & CTO

Rohit KashyapSVP

Corporate Development

Michael SchneiderSVP

Manufacturing& Operations

TLV KumarPresident,

EMEA

Patrick LohPresident,

APAC

Jim CravensSVP

Human Resources

David RamseySVP & CIO

KCI at a GlanceLeadership Team

10

Superior Product

Superior Outcomes

Extensive Global Distribution Network200 Service Centers

24/7/365 Clinical SupportAdvantage Center

Billing & Collections

TSS Manufacturing Facility-San Antonio

V.A.C. Manufacturing Facility

Athlone, Ireland

LifeCell Headquar

ters

LifeCell HeadquartersBranchburg, New JerseyPic of

articles

Substantial Clinical Evidence900 Journal articles

15 V.A.C. Clinical trials17 TSS Clinical trials20+ LifeCell clinical

trials/studies

KCI at a GlanceThe Clinical Advantage

1,000+ Innovative & Leading Patents

KCI Headquarters

KCI Headquarters

San Antonio, Texas

11

Strategic Vision2008 through 2013

• Sustain growth higher than market growth in all business segments

• Incremental growth through innovation and global expansion

• Build leadership position in biologics based on acquisition of LifeCell

• Focused execution to improve operating margins

• Strong business fundamentals enabling earnings growth higher than revenue growth and strong cash flows

A growth-oriented, diversified med-tech leader with best-in-class therapeutic platforms

Target Revenue Growth

8-11% CAGR

Target Earnings Growth

15-19% CAGR

Target Free Cash Flow

Growth16-20% CAGR

12

Wound Healing Beyond 2013Basis of competition beyond expiry of base patents

Market expansion

• $7B (2008) to $12B (2013)

Sustainable market leadership

• Novel next generation technologies extend patent portfolio to 2020 and beyond

• Operating leverage in model generates predictable, stable, sustainable operating profit

• KCI Clinical Advantage is unique – not easily replicated

Care givers

Infrastructure

Clinical evidence

Best-in-class products & innovation

KCI The Clinical Advantage

13

Realizing the VisionClinically focused…Outcomes driven

14

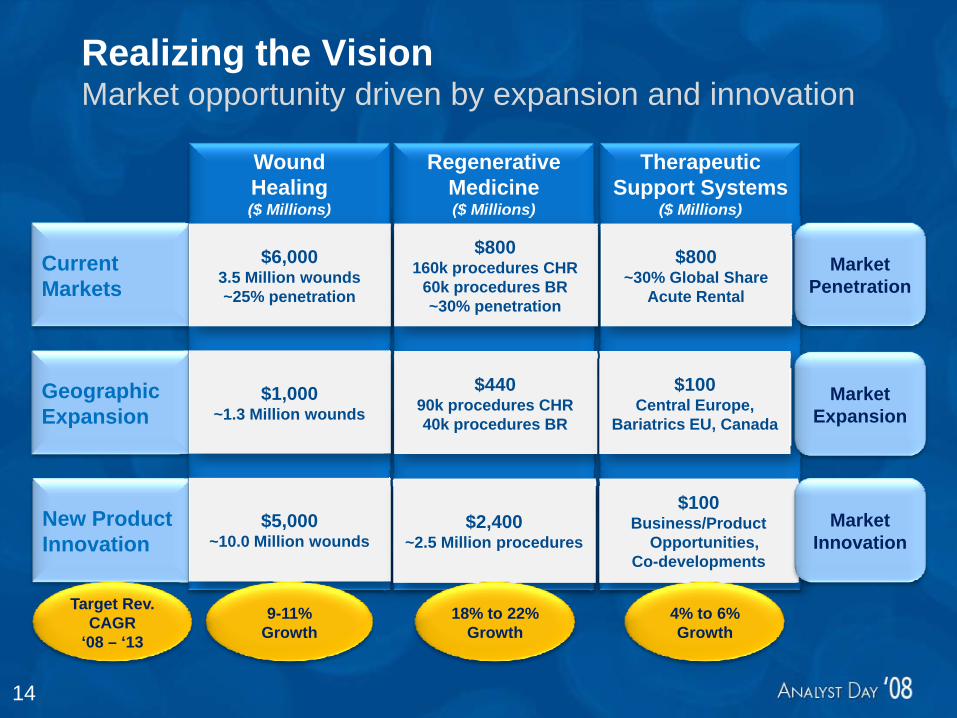

Realizing the VisionMarket opportunity driven by expansion and innovation

New ProductInnovation

GeographicExpansion

CurrentMarkets

WoundHealing ($ Millions)

$6,0003.5 Million wounds~25% penetration

$1,000~1.3 Million wounds

$5,000~10.0 Million wounds

9-11% Growth

Regenerative Medicine($ Millions)

$800160k procedures CHR

60k procedures BR~30% penetration

$44090k procedures CHR40k procedures BR

$2,400~2.5 Million procedures

18% to 22% Growth

Therapeutic Support Systems

($ Millions)

$800~30% Global Share

Acute Rental

$100Central Europe,

Bariatrics EU, Canada

$100Business/Product

Opportunities,Co-developments

4% to 6% Growth

Market Penetration

Market Expansion

Market Innovation

Target Rev. CAGR

‘08 – ‘13

16

WoundHealing

Regenerative Medicine

Therapeutic Support Systems

New ProductInnovation

GeographicExpansion

CurrentMarkets

Realizing the VisionChallenges

• Medicare• Competitive pricing pressure• Inferior competitor products• Health technology assessments

• Business model• Price realization• Regulatory/reimbursement approvals

• Surgeon adoption• Competition

15

New ProductInnovation

GeographicExpansion

CurrentMarkets

Realizing the VisionOpportunities

WoundHealing

Regenerative Medicine

Therapeutic Support Systems

• Increase V.A.C. penetration (2008 to 2013)US 35% to 50+%; EMEA 13% to 20+%

• Expand target market with reimbursement (Germany)

• APAC marketJapan opportunity: >250k wounds, >$500 Million China, India: >1 Million wounds

• Expand NPWT (Lower acuity wounds ~4.5 Million; Complex infected ~350k)• Leverage NPTP (Surgical incision ~5.2 Million, Vacuum Assisted Regenerative

Medicine ~110k)

17

WoundHealing

Regenerative Medicine

Therapeutic Support Systems

New ProductInnovation

GeographicExpansion

CurrentMarkets

Realizing the VisionOpportunities

• Increase market penetration (2008-2013) from 30% to 60%• Drive Strattice conversion to maintain leadership position• Invest in clinical studies, sales force and medical education

• Launch Strattice in EU markets – current market opportunity $440MM• Investment in clinical studies, KOL development & sales force• Develop APAC regions

• Execute on new applications – market opportunity $2.4B• Apply unique processing technology to other tissue types• Exploit combination of NPWT and Regenerative Tissue Matrix

18

WoundHealing

Regenerative Medicine

Therapeutic Support Systems

New ProductInnovation

GeographicExpansion

CurrentMarkets

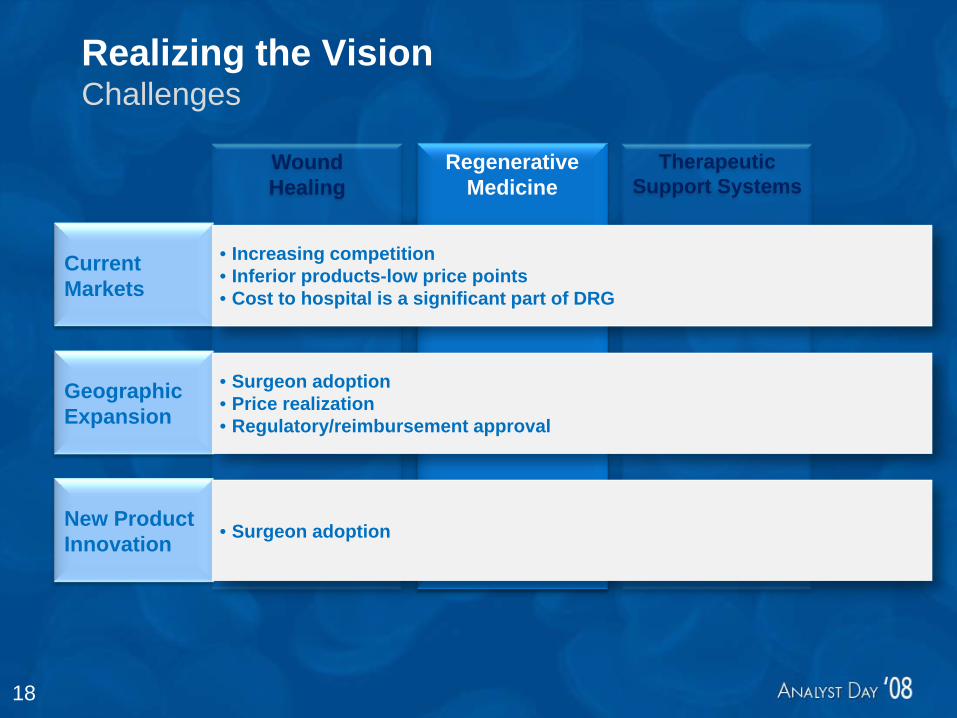

Realizing the VisionChallenges

• Increasing competition• Inferior products-low price points• Cost to hospital is a significant part of DRG

• Surgeon adoption• Price realization• Regulatory/reimbursement approval

• Surgeon adoption

19

WoundHealing

Regenerative Medicine

Therapeutic Support Systems

New ProductInnovation

GeographicExpansion

CurrentMarkets

Realizing the VisionOpportunities

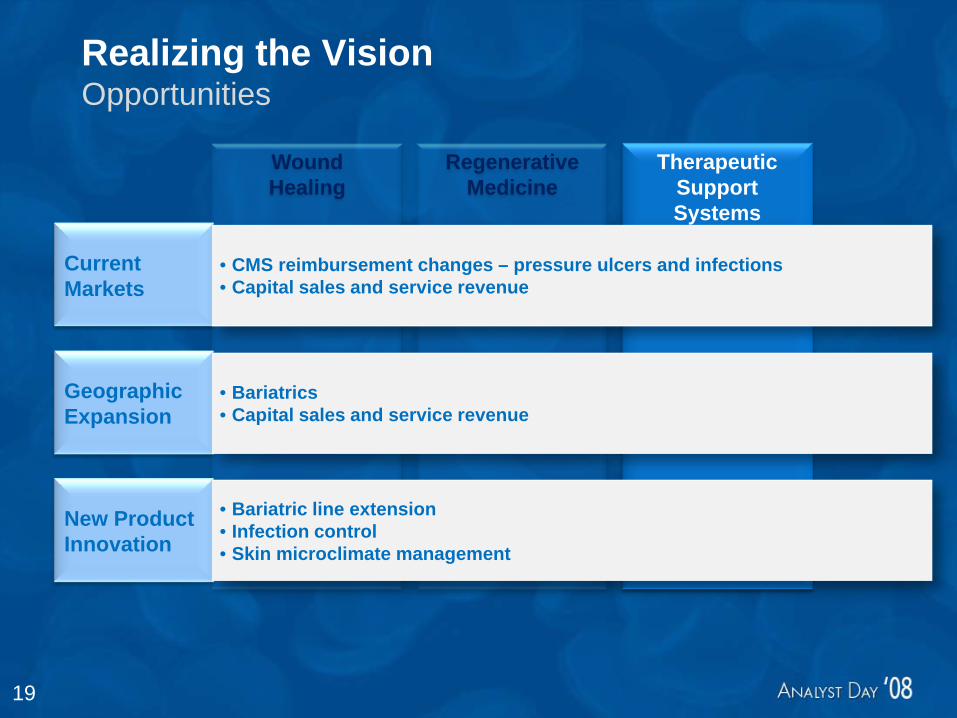

• CMS reimbursement changes – pressure ulcers and infections• Capital sales and service revenue

• Bariatrics• Capital sales and service revenue

• Bariatric line extension• Infection control• Skin microclimate management

20

WoundHealing

Regenerative Medicine

Therapeutic Support Systems

New ProductInnovation

GeographicExpansion

CurrentMarkets

Realizing the VisionChallenges

• Shift in business mix• Competitive GPO environment• Commoditization of selected products

• Low price points in local markets

• Mature market with limited opportunities• Product mix shifting to surfaces vs. frames

21

Realizing the VisionMarket opportunity driven by expansion and innovation

New ProductInnovation

GeographicExpansion

CurrentMarkets

WoundHealing ($ Millions)

$6,0003.5 Million wounds~25% penetration

$1,000~1.3 Million wounds

$5,000~10.0 Million wounds

9-11% Growth

Regenerative Medicine($ Millions)

$800160k procedures CHR

60k procedures BR~30% penetration

$44090k procedures CHR40k procedures BR

$2,400~2.5 Million procedures

18% to 22% Growth

Therapeutic Support Systems

($ Millions)

$800~30% Global Share

Acute Rental

$100Central Europe,

Bariatrics EU, Canada

$100Business/Product

Opportunities,Co-developments

4% to 6% Growth

Market Penetration

Market Expansion

Market Innovation

Target Rev. CAGR

‘08 – ‘13

22

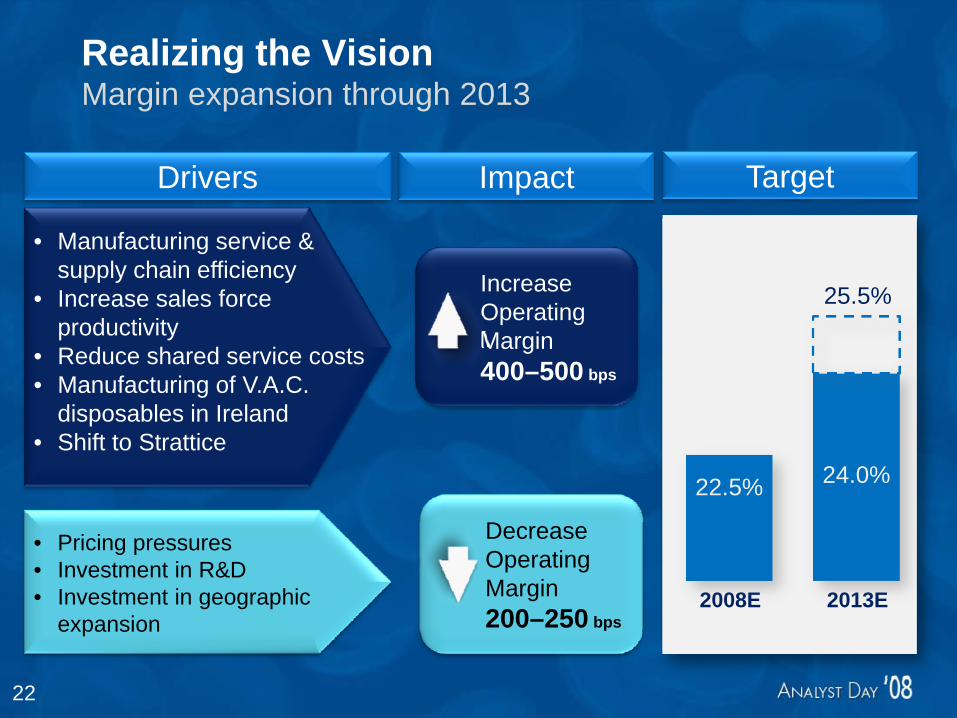

Realizing the VisionMargin expansion through 2013

• Pricing pressures• Investment in R&D• Investment in geographic

expansion

Drivers Impact

2008E 2013E

22.5% 24.0%

25.5%

Target

Decrease Operating Margin200–250 bps

Increase Operating Margin400–500 bps

• Manufacturing service & supply chain efficiency

• Increase sales force productivity

• Reduce shared service costs• Manufacturing of V.A.C.

disposables in Ireland• Shift to Strattice

23

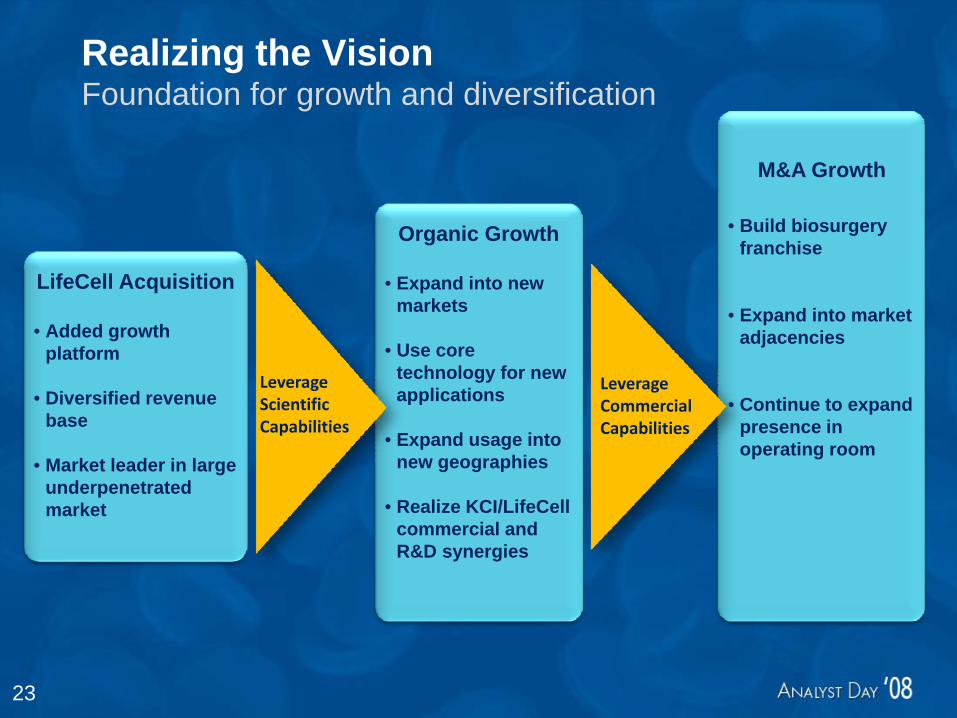

Leverage CommercialCapabilities

M&A Growth

• Build biosurgeryfranchise

• Expand into market adjacencies

• Continue to expand presence in operating room

Leverage ScientificCapabilities

Organic Growth

• Expand into new markets

• Use core technology for new applications

• Expand usage into new geographies

• Realize KCI/LifeCell commercial and R&D synergies

LifeCell Acquisition

• Added growth platform

• Diversified revenue base

• Market leader in large underpenetrated market

Realizing the VisionFoundation for growth and diversification

24

Strategic Vision2008 through 2013

• Sustain growth higher than market growth in all business segments

• Incremental growth through innovation and global expansion

• Build leadership position in biologics based on acquisition of LifeCell

• Focused execution to improve operating margins

• Strong business fundamentals enabling earnings growth higher than revenue growth and strong cash flows

A growth-oriented, diversified med-tech leader with best-in-class therapeutic platforms

Target Revenue Growth

8-11% CAGR

Target Earnings Growth

15-19% CAGR

Target Free Cash Flow

Growth16-20% CAGR

25

Wound HealingClinically focused…Outcomes driven

26

Traumatic Degloving

InfectedAbdominal

Initial Wound 7 days V.A.C. Therapy

18 days V.A.C. Therapy with STSG

Sacral PressureUlcer withNecrotizing Fasciitis

Post-debridement 28 days V.A.C. Therapy; 2 weeks Post-Flap

Initial Wound 24 days V.A.C. Therapy

30 days V.A.C. Therapy2-3 weeks post-STSG

14 days V.A.C. Therapy

Surg

ical

Trau

ma

Chr

onic

Wou

nds

Wound HealingV.A.C. Therapy: significant unmet medical need

27

• Acute (surgical and trauma) and chronic wounds

• Complex, hard to heal wounds• Wounds treated across care settings

• 20+MM complex, hard to heal wounds

4.8MM V.A.C. appropriate wounds$7B target NPWT market2x size of AWC market

Target Market

InfoV.A.C.for Acute Care

ActiV.A.C.for Home Care

Advanced DressingsUnique Mechanism of Action

Product Portfolio

Wound HealingV.A.C. Therapy: highly differentiated and clinically proven

28

• 30,000 institutions• >100,000 caregivers globally

• 1,300 sales/support personnel• 1,300 Advantage Center U.S.

representatives• 1,600 service organization associates

• 15 RCTs• >400 Journal articles

• 3rd generation NPWT V.A.C. Therapy• GranuFoam dressing – mechanism of

action

Care givers

Infrastructure

Clinical evidence

Best-in-class products & innovation

Wound HealingCompetitive clinical advantage

29

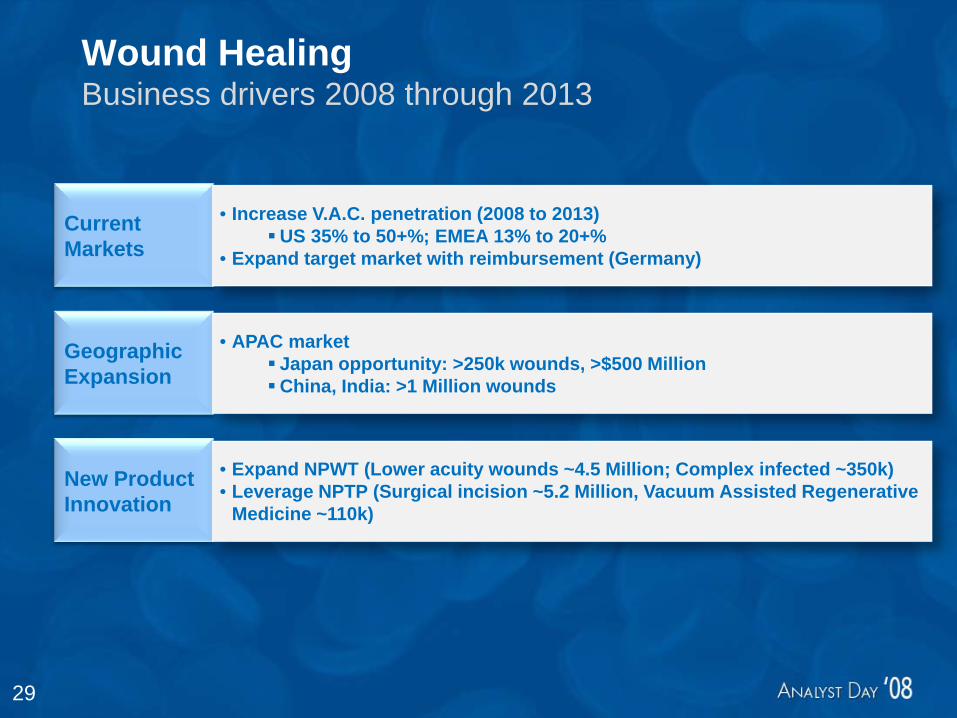

Wound HealingBusiness drivers 2008 through 2013

New ProductInnovation

GeographicExpansion

CurrentMarkets

• Increase V.A.C. penetration (2008 to 2013)US 35% to 50+%; EMEA 13% to 20+%

• Expand target market with reimbursement (Germany)

• APAC marketJapan opportunity: >250k wounds, >$500 MillionChina, India: >1 Million wounds

• Expand NPWT (Lower acuity wounds ~4.5 Million; Complex infected ~350k)• Leverage NPTP (Surgical incision ~5.2 Million, Vacuum Assisted Regenerative

Medicine ~110k)

30

Wound HealingCurrent Market

US EMEA

1.5 MMwounds

2.0 MMwounds

35%13%

2008 V.A.C. Penetration

• New differentiated products

• Targeted sales force expansion

• Flexible business models

• Evidence-based selling

US EMEA

1.7 MMwounds

2.2 MMwounds

50-55%20-25%

2013 V.A.C. Target Penetration

UnpenetratedPenetrated

31

Wound HealingCurrent Market

2008-2011 2012 -2013

Driv

ers

Growth & Market Share

NPWT Growth: >2.0x AWC market• Competition gains low single-digit

share/yr• Pricing decline: low single-digit

NPWT Growth: ~1.5x AWC market• Competition gains: low-to-mid

single-digit share/yr• Pricing decline: mid single-digit

Commercial• Targeted sales force expansion• Flexible business & service models• Evidence based selling

• Value added services • Build Installed base

Other • German reimbursement (2010) • Additional homecare reimbursement

Target Launch DFU Bridge Dressing

Simplace Dressing

Gen IV V.A.C. Gen V V.A.C.

2009 2010 2011 2012 2013

32

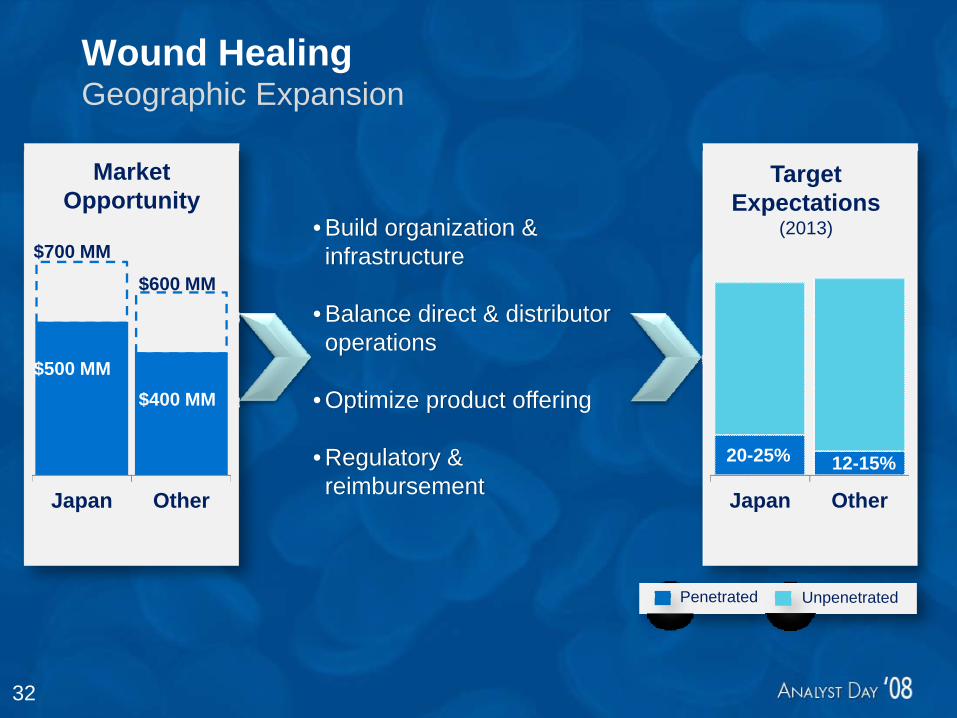

Japan Other

20-25%

Target Expectations

(2013)

12-15%

Japan Other

Wound HealingGeographic Expansion

$700 MM

Market Opportunity

$600 MM

$500 MM$400 MM

• Build organization & infrastructure

• Balance direct & distributor operations

• Optimize product offering

• Regulatory & reimbursement

UnpenetratedPenetrated

33

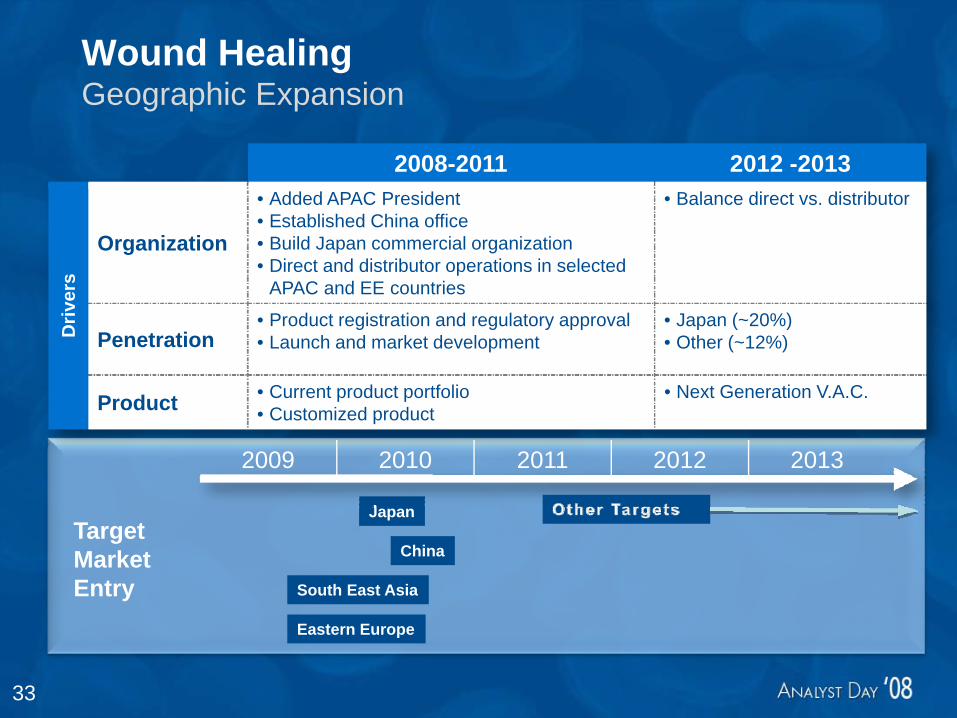

Wound HealingGeographic Expansion

Target MarketEntry

China

Japan

South East Asia

Eastern Europe

2008-2011 2012 -2013

Driv

ers

Organization

• Added APAC President• Established China office• Build Japan commercial organization • Direct and distributor operations in selected

APAC and EE countries

• Balance direct vs. distributor

Penetration• Product registration and regulatory approval• Launch and market development

• Japan (~20%)• Other (~12%)

Product • Current product portfolio• Customized product

• Next Generation V.A.C.

2009 2010 2011 2012 2013

34

Clinical Need

• Soft tissue repair and regeneration

• Hard tissue repair and regeneration

Wound HealingNew Product Innovation

• Lower acuity wounds that need only some of the benefits of V.A.C.

• Wounds that require therapy in addition to V.A.C.

VING

• Management of high risk surgical incisions; cosmesis

• Management of open abdomen

Negative Pressure

RegenerativeMedicine(NPRM)

Negative PressureSurgical

Management(NPSM)

Negative PressureWound Therapy(NPWT)

Futura

SWMS

Ab-System

TE-Wound

TE- Ortho

Neg

ativ

e P

ress

ure

Tech

nolo

gy P

latfo

rm

Soft tissue repair and regeneration

Hard tissue repair and regeneration

Lower acuity wounds that need only some of the benefits of V.A.C.

Wounds that require therapy in addition to V.A.C.

Management of high risk surgical incisions; cosmesis

Management of open abdomen

35

Wound HealingNew Product Innovation

2008-2011 2012 -2013

Driv

ers

Commercial • V.A.C. sales force• LifeCell sales force

• New sales force (TE-Ortho)

Target Penetration

• Mid to high single digit penetration• Some minor cannibalization of V.A.C.

(<2% of total)

Planning Cycle Penetration• SWMS – I (7% to10%)• Ab-System (15% to 20%)• TE-Wound (12% to 15%)• SWMS-A (10% to 12%)

Anticipatedproduct launch

Ab-System

SWMS -I

TE - Wound

Futura

SWMS-A

VING TE-Ortho

2009 2010 2011 2012 2013

R & D Planned Pipeline

36

7.0%

9.5%

9.0% 0.5%2.0%

12.5%

1.0%

2.5%

CurrentMarkets

GeographicExpansion

NewProducts

Overall

Revenue Growth (‘08-’11) Revenue Growth (‘11-’13)

3.0%

7.5%4.0% 1.5%

3.0%

10.0%

2.0%

4.0%

CurrentMarkets

GeographicExpansion

NewProducts

Overall

Wound HealingGrowth through innovation and market leadership

37

Beyond 2013Basis of competition beyond expiry of base patents

Market expansion

• $7B (2008) to $12B (2013)

Sustainable market leadership

• Novel next generation technologies extend patent portfolio to 2020 and beyond

• Operating leverage in model generates predictable, stable, sustainable operating profit

• KCI Clinical Advantage is unique – not easily replicated

Care givers

Infrastructure

Clinical evidence

Best-in-class products & innovation

KCI The Clinical Advantage