Download - Guide to freelancing

Guide to Freelancing 1

Guide to Freelancing

Welcome to the IPSE Guide to Freelancing. Please bear in mind this guide is aimed at UK freelancers, so any tax issues and other legalities mentioned here are governed by British rules. All content within this guide is correct at time of print and relates to figures for the financial year 2013/14.

Contents01 Section 1 Introduction

» About this guide » About freelancing » If you do nothing else, do this.

05 Section 2 Setting up your freelance business

» Setting up in business » Limited company: why you might want one » Alternatives to a limited company

16 Section 3 The Books: Handling the business finances

» Accountants » Bookkeeping » Money in the bank » Money in your pocket » Money out

30 Section 4 Paying the taxman: What to pay, how and when

» Value Added Tax (VAT) » Taxation of limited companies » Taxation of sole traders, partnerships and LLP’s

37 Section 5 Running the show: How to manage a successful business

» Where is your HQ? » Winning work » Managing the workload » Financial planning

53 Section 6 Risk prevention: Insurance and protective measures

» Assessing risk » Compulsory insurance » Worth considering

Guide to Freelancing 1

Section 1

IntroductionThis section covers:1. About this guide Who it’s for and how to use it

2. About freelancing Career paths and how to go about it

3. If you do nothing else, do this. The freelance checklist

About this guideHello and thank you for choosing the IPSE Guide to Freelancing. Please bear in mind this guide is aimed at UK freelancers, so any tax issues and other legalities mentioned here are governed by British rules. All content within this guide is correct at time of print and relates to figures for the financial year 2013/14.

If you’re just starting out...Are you thinking of starting up as a freelancer, contractor or consultant? Some of the heavier tax and regulatory matters can seem rather daunting if you’re not familiar with them – but it doesn’t all have to be done in one go. Give the whole guide a quick scan first and then come back to individual chapters later, scheduling a separate chunk of time for each section. If you put things in practice bit by bit, you will become much more fluent over time – developing that broad business savvy is one of the most rewarding parts of being your own boss.

If you’re already established...The guide is a useful reference source to keep abreast of current regulations.

Either way, don’t skip... The freelance checklist at the end of this section. If you’re just starting out it will help you plan your launch and if you’re already established it will help you to review your current set up.

Guide to Freelancing 2

Taking the plunge...

“It’s easy to delay and make excuses about not being sufficiently prepared. I’d say if you have a clear idea of what you want to be

doing, the skills to do it, and you have a financial buffer in place, just jump in and give it a go. I honestly think one of the biggest hurdles to starting out is worrying too much about being prepared. It can’t hurt

to read a few guides and talk to people, but when it comes down to it if you’re suited to freelancing, you’ll soon find out. If not then you

can always just find yourself a regular job – nothing wrong with that. Long story short, just get out there and do it.”

Frank G. Freelancer

And don’t forget, we’re here if you need us IPSE is the UK’s only not-for-profit association dedicated to supporting, representing and protecting the freelance community. So far 22,000 UK freelancers have joined IPSE because it helps them get ahead in business. To find out more visit www.ipse.co.uk

About freelancing“I can’t tell you how much admiration I have for people who leave

the comfort of a regular wage to strike out on their own. It takes a lot of courage, and without that courage this country would be a much

poorer place,”Prime Minister David Cameron

Freelancers play a pivotal role in Britain’s 21st century innovation-driven economy and are increasingly being recognised as key drivers of wealth creation in the country. You no longer have to belong to a large company to be credible. In fact, big brands are fragmenting and the personal brand is emerging as the force of the future. Experts are saying that, in the networked economy of today and tomorrow, individuals are as important as a big company.

Different ways of freelancing‘Freelancer’ is a broad term covering many different ways of working independently. Some people work on long term contracts, doing a full week at a single client site for several months until the contract is finished or renewed. Others work with several clients at a time or on a series of fast turnaround projects.

Freelancers use different terms to describe what they are, e.g. freelancer, contractor, consultant, independent professional, interim, portfolio worker, self-employed, business owner. They use a range of legal forms to run their businesses, including limited companies, sole traderships, partnerships, umbrella companies and others. They might brand themselves using their own name, or else create a completely separate business brand and logo, presenting themselves as a small business rather than an individual. Some work through agencies, others directly with their clients. Some charge by the hour, some by day or week, and others give a fixed project fee. The unifying factor is that freelancers are their own bosses and have commercial, business-to-business relationships with their clients.

Guide to Freelancing 3

To go freelance, you don’t necessarily have to work in the traditional areas associated with freelancing such as media or IT. More and more people are finding creative ways to exploit their skills in all sorts of areas such as business development, environmental consulting or even offering training in niche areas, for example selling to government departments.

Building your own career ladderFreelancing is not for everyone. There are risks. It’s not an easy option. In fact, the survey conducted by IPSE in 2010 showed that the general population was happier with working hours, time for themselves and time with family, than freelancers.

However, with risk comes reward. In the same survey, freelancers were shown to be happier overall than the general population. IPSE’s annual membership surveys consistently show that most people go into it because they want to, not because they are forced into it through redundancy, while only three percent plan to use it as a stopgap while they find a permanent position. Moreover, two thirds of freelancers continue to work as freelancers because of the autonomy it gives them.

Anyone choosing the independent route will need to build their own career ladder and work out how to structure their business in a way that frees up their full potential. The business will also need to be supported by some kind of promotional activity to ensure a sustainable level of work. And when it comes to deciding which marketing technique works best, there is no magic wand. There are almost as many views on effective marketing as there are freelancers. As with so many things, you have to take what works for you, adapting the techniques that best fit your style and industry – the section in this guide on winning work will give you some ideas to try out.

It is certainly worth experimenting with different approaches until you are able to narrow down those that deliver the best results for you.

It’s a good idea to revisit your goals and long term plans regularly, benchmarking your journey and adjusting course if necessary. There is nothing wrong with switching business models or re-inventing yourself completely at different points in your career. For example, someone starting out as a programmer can later morph into a project manager and eventually into a management consultant charging a premium fee.

“Just as travel broadens the mind, a freelancer will have a broader and more colourful experiential mind-set than executives or owner-

managers”Tony Lahert CEO, Step Solutions, Argos Direct The Role of Freelancers in the 21st Century British Economy).

If you do nothing else, do this...Time estimate THE GRAND STRATEGY Check

About a day Do a simple business plan. Template available to IPSE members

Couple of hours Do a financial forecast. Template available to IPSE members

Under an hour Write down a cash flow strategy to mitigate against late payments or income gaps.

Time estimate ADMIN MATTERS Check

Couple of hours Decide whether to set up as a sole-trader, limited liability partnership, limited company, or under a PAYE umbrella.

Big decision. Allow a day or so.

Source an accountant (unless you went the umbrella route). Ask for recommendations and referrals on the IPSE legal & accounting forum. Check whether the service includes a basic record keeping and invoicing system.

An hour or less If your accountant doesn’t provide one, source a record keeping and invoicing system. Ask for recommendations on the IPSE legal & accounting forum.

Guide to Freelancing 4

Time estimate ADMIN MATTERS Check

A few days Get a bank account set up in your company/business name.

Couple of hours Send relevant forms to HMRC (ask accountant for assistance). If in doubt, call the IPSE tax helpline.

An hour or less Consider the VAT Flat Rate Scheme – discuss merits with accountant and if applicable, apply.

Time estimate IT & SYSTEMS Check

Can take weeks Install internet and email. Ask for help on the IPSE technical forum.

1 week Get business phone line, mobile phone and, if necessary, a fax.

A few days Source computer/s, printer, backup system and any other equipment needed - ask for help on the IPSE technical forum.

Several hours Install software.

Half a day Set up a professional base to work from.

Time estimate THE BUSINESS DRIVE Check

Half a day Review business plan and decide which business model, price bracket and marketing tactic to focus on.

A few weeks Launch a new business drive based on the above.

A few days Follow up hot leads.

Several hours on and off

Review results and decide whether to continue or switch tactics. Swap ideas with others on the IPSE contracting issues forum or at IPSE Real Life Meetings (RLMs).

Time estimate GETTING READY TO DELIVER Check

20 minutes Understand the project lifecycle from the client’s perspective.

Couple of hours Develop a project briefing template to send to clients to help them specify objectives, deliverables and project milestones.

About an hour Understand the concept of a business-to-business working relationship and draft a policy (for own record) establishing how this will be achieved with potential clients. If in doubt, call the IPSE tax and contract helpline.

A few minutes Understand the concept of a business-to-business working relationship and draft a policy (for own record) establishing how this will be achieved with potential clients. If in doubt, call the IPSE tax and contract helpline.

Under an hour Download Terms and Conditions template and customise so it is ready to append to proposals and quotations.

A few minutes Download Mutual Secrecy Agreement template for any projects that might have confidentiality issues.

Guide to Freelancing 5

Section 2

Setting up your freelance business

Working out the right trading structureThis section covers:4. Setting up in business Important rules and regulations, including IR35 and Employment Status

5. Limited company: why you might want one Why many freelancers decide to set one up, what the implications are and how to go about it – also what to do if you eventually want to close the company down

6. Alternatives to a limited company Other options explained, including sole trader, partnership, limited liability partnership and umbrella company

Setting up in businessOnce you go freelance, you enter a new realm of laws and regulations.

The word ‘freelance’ is a layman’s term, not an official category used by the Government to classify workers. Therefore, ‘going freelance’ actually means setting yourself up as a business by establishing a trading structure and letting the tax authorities know what you’re up to.

These are the trading structures through which you can operate:

Trading structure Legal category* Your tax status

Limited company Incorporated Company director and/or employee of your company

Sole trader Unincorporated Self-employed

Partnership Unincorporated Self-employed

Limited liability partnership Incorporated Self-employed

Umbrella company Incorporated Employee of the umbrella

* An incorporated business is a separate legal entity. You can think of it as being like a separate person – it can own things, have bank accounts in its own name, and it can be liable for debts or lawsuits. If you are unincorporated it means that you and the business are one and the same – there is no legal separation.

Each of these structures has its own tax and legal implications. All of them can be set up fairly quickly, but some are quicker and easier to set up and run than others (see the following chapters). Whichever way you chose to operate it’s essential to start thinking in terms of the business, not you as an individual. You should think about having a business telephone line installed separately from your private line and/or using a business mobile phone. If you already own a desk, computers and other office equipment, you should consider ‘selling’ these to your business, initially recording the value as a personal loan to the business from you, in the form of set-up expenses.

Guide to Freelancing 6

Avoiding problems with the taxman: ‘Employment Status’Employment status is an important issue to understand fully as it could influence decisions regarding your set-up.

Your employment status decides whether you should be treated as employed or self-employed for tax purposes. You might think you are freelance or self-employed, but that doesn’t necessarily mean that the taxman will agree with you. The tax authorities can challenge your employment status on any particular client contract if they think that you are behaving as if you were that client’s employee – in other words, not a real business. This is known as ‘deemed employment’. If you do all your work for one client, or if you have very long contracts with particular clients, you could be vulnerable.

The implications of being ‘deemed employed’ can be expensive because HMRC will seek to recover the higher levels of tax and NIC that are payable by employees. Who they choose to recover the tax from, depends on your chosen business structure.

In addition your employment status also has an effect on other laws such as the Agency Workers Directive for more information visit IPSE’s policy website pages.

Implications for sole traders and ordinary partnershipsSole traders and ordinary partnerships are known as unincorporated businesses – in other words, you are self-employed as opposed to having a separate corporate structure. As a result sole traders and partners in a business report their income on their own income tax self-assessment return. Sole traders will complete a self-employment page and the individual partners will complete a partnership page.

If, as a sole trader or partnership you are ‘deemed employed’ then your client will be liable for tax and NICs on the fees they have paid you. This can be charged retrospectively for as long as the engagement took place, even if that means several years. It can be very expensive and probably won’t do your client relationship much good if the situation should arise.

Implications for limited liability partnerships (LLP)Under an LLP structure the Intermediaries Legislation (IR35) will apply and thus if the engagement is deemed by HMRC to be ‘employment’, the partnership itself will be liable for the extra tax and NIC’s both employer’s and employee’s.

Implications for limited companiesIf you are the director of your own limited company through which you bill your client(s), and the taxman says you are ‘deemed employed’, then the IR35 legislation can kick in, allowing HMRC to reclassify the engagement between you and your client as ‘IR35 caught’.

If you are working with more than one client you are less likely to be caught by IR35 however it is not impossible for IR35 to apply to one or more of them since IR35 is assessed engagement by engagement.

The typical relationship involving a freelancer trading through a limited company is:

Engaging organisation (the client) – limited company service provider (your company/the “intermediary”) – the worker (you), and there may be an agency between your company and the client.

What the IR35 Intermediaries legislation allows HMRC to do is create a ‘hypothetical contract’ which asks the question: “If the intermediary (your company) was removed from the business relationship and the worker (you) were engaged directly by the end client what would that relationship be?”

If HMRC can successfully argue that the relationship would most closely represent a contract of service (employment), then only for tax purposes and only for the engagement(s) in question, you will be deemed an employee. And in this scenario, you can only be deemed an employee of … your own company!

Guide to Freelancing 7

The taxman will then insist that your own limited company should have deducted PAYE tax and NICs on the all of the fees paid by the client, as if the fees were salary payments. The additional tax due can be charged retrospectively going back up to six years. They may also charge interest and penalties, and there are likely to be accountancy fees to sort it all out. That’s how contractors can find themselves owing tens of thousands and sometimes even hundreds of thousands in tax and NIC’s that they weren’t expecting.

How HM Revenue & Customs assesses your employment statusCurrently HM Revenue & Customs (HMRC) use three key employment status indicators called ESIs) to decide whether you are a genuine business or whether you are in fact a ‘disguised employee’ of your client. The principle is that if you have an engagement where you have to provide your personal service, where there is an obligation to offer and accept work and where you can be controlled by the engager, then a contract of service (employment) exists.

Where any one of these three elements is missing, then it cannot be a contract of employment and so logically it must be a contract for services (self-employment). In an ideal world, it would be best to “pass” all three key tests, but “passing” two is better than one. But where these status indicators are inconclusive, one should also consider ‘in business’ factors or factors which show that a freelancer is taking the kind of financial risk that would not be required of an employee. In essence, the more factors in your favour the better.

Being in business can be most easily demonstrated by the type of expenditure you incur; for example, most employees do not need to invest in office equipment and stationery to do their job. It is highly unlikely that an employee would need liability insurances or to submit invoices in order to get paid. Also most employees will receive some form of employment benefits and have the protection of employment law. If you are IBOYOA (in business on your own account) you will have to make provision for all of these things and face the prospect of contracts terminating at short notice and with no guarantee of finding future work etc.

The key is to think of yourself as a business and act as one. This goes beyond business structure - it’s a principle that actually starts in your head. You are you, and the service you offer is your business. In short, genuine freelancers are in business on their own account and bear the responsibility for the success or failure of their business. They are not ‘disguised employees’.

Ultimately, a number of factors can come together to create a whole ‘picture’ of your employment status. So rather than relying on any single factor to protect you from being wrongly accused of being an employee, make sure the whole picture of your status can reasonably be said to be that of a business. For more information, IPSE provides a wealth of resources for its members, including tax and legal helplines, and specific guides to IR35 and the Agency Workers Regulations.

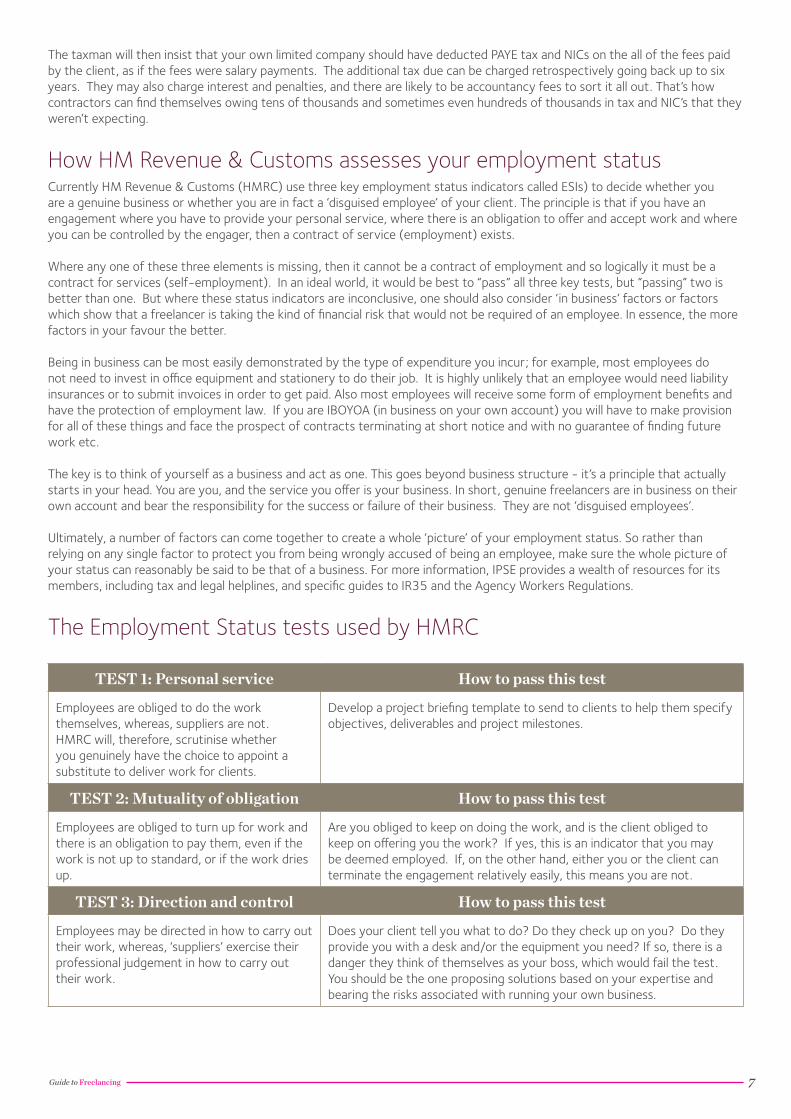

The Employment Status tests used by HMRC

TEST 1: Personal service How to pass this test

Employees are obliged to do the work themselves, whereas, suppliers are not. HMRC will, therefore, scrutinise whether you genuinely have the choice to appoint a substitute to deliver work for clients.

Develop a project briefing template to send to clients to help them specify objectives, deliverables and project milestones.

TEST 2: Mutuality of obligation How to pass this test

Employees are obliged to turn up for work and there is an obligation to pay them, even if the work is not up to standard, or if the work dries up.

Are you obliged to keep on doing the work, and is the client obliged to keep on offering you the work? If yes, this is an indicator that you may be deemed employed. If, on the other hand, either you or the client can terminate the engagement relatively easily, this means you are not.

TEST 3: Direction and control How to pass this test

Employees may be directed in how to carry out their work, whereas, ‘suppliers’ exercise their professional judgement in how to carry out their work.

Does your client tell you what to do? Do they check up on you? Do they provide you with a desk and/or the equipment you need? If so, there is a danger they think of themselves as your boss, which would fail the test. You should be the one proposing solutions based on your expertise and bearing the risks associated with running your own business.

Guide to Freelancing 8

Specify your working relationship by means of a contractIn a dispute the courts will look at the contract between your business and your client to infer whether or not you are actually an employee by another name. Therefore, it’s essential to draw up a contract for any large project you take on. Furthermore, it should be a contract for services with your business, not a contract of service with you personally. This contract should accurately reflect the relationship between parties, and should include clauses that demonstrate your ability to send substitutes, the lack of mutuality of obligation, and that you have direction and control over your work.

It is really important to have one professionally drawn up. IPSE members can download a template ‘contract for services’ at www.ipse.co.uk/resources

IPSE members can download a comprehensive guide to IR35 from www.ipse.co.uk/resources.

Case study: Experiencing a tax investigationRobert is a freelance project manager and infrastructure consultant. Out of the blue he was contacted by HM Revenue & Customs (HMRC) who wanted to review the PAYE records of the limited company he operates to check he was paying proper tax and NI. As a IPSE member he knew straight away what they were really interested in – checking his contracts to see if they could deem him to be ‘IR35 caught’. HMRC suggested he call them, but instead he called the IPSE help-line which advised him on his next steps.

The tax inspector asked to see his books and records for the last six years and spent two hours going through them. He wanted a complete breakdown of expenses and asked Robert to highlight any mobile phone calls that were personal. Robert duly went through them and found £4 of personal phone calls out of receipts totalling hundreds of pounds. Assuming the inspector would dismiss this as an insignificant amount, Robert was surprised to hear him say “I’ll have to think what to do about that”. Then the request came to view his client contracts for the previous five years. As expected, the inspector announced that they were being passed to the IR35 compliance department.

IPSE provided Robert with an expert adviser, Jacqui Mann from Abbey Tax Protection. As a former tax inspector, Jacqui advised Robert and his accountant throughout the IR35 investigation process and dealt with the authorities on Robert’s behalf. The cost of this representation was covered thanks to his IPSE Standard membership. In the end the case was closed without Robert being liable for additional tax or penalties.

“I felt very panicky at the beginning, but being a IPSE member has definitely helped the situation”, says Robert. “Having Jacqui to represent me was very reassuring, and on top of that I was able to discuss it on the IPSE forums with others who have been through the same experience.”

For more information on what to expect from a tax enquiry visit www.ipse.co.uk/resources

In a nutshell: Setting up in business » ‘Going freelance’ essentially means that you are setting yourself up as a business. To do this, you have to formally

set up a legal business structure and let the tax authorities know how you are operating

» Freelancers can operate as a limited company, sole trader, partnership, limited liability partnership (LLP) or umbrella company

» The tax authorities scrutinise your client relationships and can challenge your employment status if they think you are not genuinely in business on your own account

» If you are the director of your own limited company or operate as an LLP, through which you bill your client(s), you need to be aware of the risks of IR35

» Working relationships with clients should be specified by means of a professionally drafted ‘contract for services’ – IPSE members can use the IPSE template contract

» IPSE members are covered for tax investigations – if a revenue officer asks to meet for an informal chat, you are under no legal obligation to do so – instead ring the IPSE help-line for advice

» Please visit IPSE website policy pages for more information about employment status and Agency Workers Regulations

Guide to Freelancing 9

Limited company: why you might want one Although it’s perfectly possible to freelance as a sole trader or partnership, a large proportion of freelancers prefer to ‘incorporate’ – in other words, to set up a limited company.

One of the main reasons for this is that some clients are wary of working with unincorporated businesses because it puts them at risk under the employment status rules. However, it’s not the only reason. Having a limited company lends certain credibility. It is a separate legal entity, which helps to create a division between the person and the business. It also protects any personal assets – if the company goes bust or gets sued, creditors can’t take your possessions as long as you haven’t acted fraudulently or negligently, in which case they might be able to seize your personal assets (as specified in The Companies Act 2006).

ImplicationsA limited company is a distinct legal entity in its own right. It has rights and responsibilities and can own property or equipment. This means that there are more rules and regulations to running a limited company than an unincorporated business. A number of returns need to be made within a strict time limit:

» Company tax return

» Company accounts and a computation of taxable profits

» Form P35 in relation to salaries including directors remuneration

» A form P11D (return of taxable benefits and expenses) for each director/employee

» Personal tax return for the company directors

However, with the help of a good accountant, this isn’t unduly onerous. It will cost you a bit more than running an unincorporated business, but on the other hand a company gives you a certain amount of control over when and how you pay tax which can result in legitimate savings.

Guide to Freelancing 10

Weighing up the benefits of a Limited CompanyPros Cons

•Overcomes the hurdle of clients who won’t deal with sole traders or partnerships

•Personal assets are protected against company debts*

•You can control how you pay yourself to ensure tax efficiency

•If you are working through a recruitment agency, the agency or the client can pay your limited company gross. A recruitment agency must pay all others as if they were employees by applying PAYE

•It’s easier to set up trade accounts with suppliers

•Owner managers can get Statutory Sick Pay, Statutory Maternity Pay and similar benefits**

•Entitled to R&D tax credits

•Can have occupational pension scheme and NIC relief for pension payments

•A limited company can raise funds through Venture Capital, Enterprise Investment Schemes or sale of equity

•There are more rules and regulations

•If you get hit with IR35, you get stung with the bill, not the client

•There is more admin due to the legal reporting requirements and number of returns that have to be made

•Accountancy fees tend to be slightly higher for a limited company

•The penalties for getting it wrong or submitting returns late are greater than for sole traders

•You can’t just withdraw money from the business without formally recording it as salary, dividend or loan

•Your company must pay a 25% tax on any money you borrow from your company if you don’t repay it within nine months of the year end (this is repayable after the loan has been repaid), HMRC will also charge interest on the unpaid amount

•The company has to pay corporation tax on gains made if you sell company assets.

* As long as you haven’t given any personal guarantees or acted negligently** 10% of Statutory Maternity Pay is paid to small employers, so the owner managed company can claim the cost back from the Government with a 5% margin. As the cost is borne by the company and then recovered, the margin remains within the company. Sole traders cannot claim Statutory Maternity Pay but if you are registered self-employed and are paying Class 2 National Insurance Contributions (NICs), you will be eligible for Maternity Allowance (MA) for 39 weeks. This pays a standard weekly rate of 90 per cent of your average gross weekly earnings (before tax) for the first six weeks. For the following 33 weeks you will get either the standard rate of £135.45, or 90 per cent of your average gross weekly earnings, whichever is the smaller. For more information about maternity pay please visit http://www.nidirect.gov.uk/statutory-maternity-pay.htm

The Rules » The company must have at least one director and a registered office, and must have “Limited” or “Ltd” after its name.

» Private limited companies are not obliged to appoint a company secretary unless the company’s articles contain a reference to the company having a secretary.

» Ownership in terms of the split of shares in the company is up to you but many freelancers split the shares with their spouses. HMRC have previously attempted to challenge this type of set up, in particular, with the infamous Arctic Systems case, which HMRC lost at the House of Lords. Following the case HMRC proposed a new set of rules to combat what they called ‘income shifting’; however, these are still on hold. In general, it is considered best to make the split when the company is first formed and in the case of a husband and wife, ensure that the shares subscribed for or provided to the spouse are full ordinary shares. IPSE members can download the guide to Family Business Tax for more information.

» The registered office is the company’s legal address and it can be your accountant’s office, your own office premises or your home office. In the case of a home office, it is important to check the terms of any lease or mortgage agreement to make sure there are no restrictions regarding commercial operations.

» The registered office must be within the jurisdiction in which the company was incorporated. So a company formed in Scotland must have a registered office in Scotland and a company formed in England or Wales must have its registered office in England or Wales. Legally, a plaque or sign must be displayed outside the building to show that this is the company registered office, although IPSE does not know of any freelancers who

Guide to Freelancing 11

have been prosecuted or investigated for failing to comply.

» A limited company must file annual accounts with Companies House and also a corporation tax return accompanied with the accounts to HMRC. The limited company must also complete an annual return to Companies House. This document confirms details of the shareholders and directors of the company.

» Finally, any company with an annual turnover in excess of £77,000 from April 2012 must register for VAT. More information on the requirement to register is given in the VAT section.

The role of the Company DirectorsAs a company director you are legally responsible for making sure the company is run properly, according to the law and in the interests of the shareholders. The latter shouldn’t be too hard given that you and/or your spouse are probably the only shareholders.

A director of a limited company is not strictly an employee of that company unless he/she has a contract of employment. Although not a legal obligation, some freelancers draw up a contract of employment as it can help make the case that you are not IR35 caught. However, bear in mind that ‘employment’ leads to such responsibilities as the provision of the minimum wage and other statutory benefits. Your accountant may have a standard contract that you can tailor to your specific needs or it may require you to engage the services of an employment law contract specialist to create one.

Questions to ask yourself » How long are you intending to freelance or contract for? (If it’s just a few months, it’s probably not worth setting

up a limited company)

» Can you handle the legal responsibility of being a company director?

» Can you set up proper business to business relationships with your clients so as to avoid being IR35 caught?

» Can you simplify the admin with the help of a good accountant?

How to set up the Limited CompanySome freelancers consider putting some of their own personal money into the business as a loan from you to the business. This can be repaid later as the business begins to generate income. If your business subsequently folds you may then lose your investment.

The easiest way to set up a limited company is to ask an accountant to set one up for you, or to use the IPSE Start-up package. Accountants usually charge around £100-£150, although some do it for free by absorbing the cost into your ongoing monthly fee.

You can also do it yourself, which can be a bit cheaper - around £40 (or £100 for a same day service).You can find out more about this in the guidance booklets available via the Companies House websitewww.companieshouse.gov.uk.

What to do if you want to close the companyIf, for whatever reason, you decide you want to close down your company, you will need to complete a ‘Striking Off Application (DS01)’ form available on the Companies House website (www.companieshouse.gov.uk) – you need to have stopped trading at least three months before.

If there are any funds left in the company, you need to decide how to take it out. There are three options: 1) take it out as dividends or 2) take it out as capital 3) make a company pension contribution. Option 2 should, in a typical scenario, be the more attractive than Option 1. Check with an accountant, financial planner or tax planner to make sure the principle works with your specific situation.

Guide to Freelancing 12

Option 1: Take all the money out as dividendsAll remaining funds in the company after payment of all liabilities are treated as a final dividend distribution and allotted to the shareholders as usual. As of 2012/13, all dividend income at or below the £34,370 basic rate tax limit is taxed at 10%. Dividend income at or below the £150,000 higher rate tax limit is charged at 32.5% and the higher rate dividend tax rate is now 42.5%. Careful planning is required here as you might not know what other income you will receive in the rest of the tax year.

Option 2: Take all the money out as capitalTo do this you need to let HMRC know that you intend to make a claim under ‘Extra Statutory Concession ESC C16’. Essentially this concession treats the final distribution of the company as capital, rather than revenue and is therefore subject to Capital Gains Tax (CGT) rules.

There are two useful reliefs for CGT:

1. The first £10,600 of annual capital gains are exempt from tax, and this applies to each taxpayer. 2. There is also Entrepreneurs Relief. Normally, gains between £10,600 and £34,370 are charged at 18% and gains above £34,370 are charged at 28%. However, with Entrepreneurs Relief the tax rate on the gain is only 10%.

You can claim this relief if:

» the company is your ‘personal company’, i.e. you own a minimum of five percent of the voting shares, and are an employee/director of the company

» the company is a qualifying trading company. There are limits on the amount of non-business assets the company can hold in order to meet the criteria – accumulated reserves count as non-business assets.

Option 3: Make a company pension contributionIf you have a pension shortfall, you can make a lump sum contribution of up to £50,000 into a pension. From the tax year 2014-15 onwards, this will be reduced to £40,000. This should reduce your Corporation Tax bill for your last year of trading, as they are an allowable expense under the revenue’s “Wholly and exclusively” rules. It will also reduce the CGT bill in Option 2 as the lump sum will be taken out of the business before it is closed down.

Comparison betweendividend and capital distributionA husband and wife are both 50/50 shareholders of their limited company, so the funds are divided equally. They decide to close the company and there is £75,000 left in the company after all liabilities have been paid. They have no other capital gain occurring in the year and are eligible for Entrepreneurs Relief. Therefore, they are able to create significant savings by distributing the funds as capital rather than dividends.

The dividend route The capital route

Dividends £75,000 Capital £75,000

Taxable amount £75,000 Taxable amount after allowance of £21,200(£10,600 x 2)

£53,800

Tax liabilityIf at 25% rateIf at 36.11% rate

£18,750£27,082

Tax liability10% if claiming Entrepreneurs Relief

£5,380

Important note: HMRC can enquire into a company tax return up to two years after the end of the accounting period. If you are an IPSE member and you have decided to stop freelancing, you are, therefore, advised to maintain your membership to cover the two year window in order to remain protected in case of a tax investigation.

Guide to Freelancing 13

In a nutshell: Limited Companies » ‘Incorporating’ or operating as a limited company is a popular route for freelancers - many clients have a policy of

not working with sole traders

» Because of the admin involved, it is not worth setting up a limited company if you only plan to freelance for a few months

» Running a limited company is a big responsibility – you need to understand the rules

» An accountant can help you set the company up

» HMRC can investigate company accounts up to two years after the end of the accounting period, including the accounts for the year you cease to trade.

Alternatives to a limited companySole TraderA sole trader, or sole proprietor, is defined as a business that is owned and controlled by one person who takes all the decisions, responsibility and profits from the business which they run. Sole traders were previously referred to as ‘schedule D workers’. The schedule system no longer exists so sole traders are now technically known as self-employed.

Operating as a sole trader is more straightforward than a limited company because there is less paperwork. You pay tax and NIC’s on the business profit, regardless of how much you draw, so the accounting side of your business is very straightforward.

As a sole trader you are protected from the risk of IR35 because, if HMRC decides that you are ‘deemed employed’, they will hit your client with the tax bill, not you. However, for precisely that reason, clients might refuse to engage you, so you could be limiting your market. In some industry sectors this is more of an issue than others – it’s a good idea to compare notes with other freelancers in your field.

Another potential disadvantage of the sole trader route is if you work via an agency and the agency settles your bill then they must by law pay you as an employee. This can be problematic because you pay tax under PAYE as an employee but without receiving employee benefits such as holiday or sickness pay. This makes it harder to build the financial buffers required to weather the risks of being self-employed.

Finally, be aware that personal assets, including your home, are potentially at risk because you are personally liable for any business debts, including lawsuits – it’s advisable to mitigate these risks with suitable insurance cover, such as Professional Indemnity. Sole traders pay tax twice a year under the self-assessment system known as ‘payment on account’.

If you do decide that the relative simplicity of being a sole trader is the way to go then you must register as self-employed. This can be done online at the HMRC website: http://www.hmrc.gov.uk/selfemployed/register-selfemp.htm. You must register within three months of the commencement of business or you will be fined!

Sole trader is a good choice if... » You’re working on your own

» You don’t want the responsibility of being a company director

» Your actual or prospective clients don’t mind working with an unincorporated business

» Your fees aren’t paid by a recruitment agency

» Your activities aren’t likely to put your personal assets at risk

» You protect your personal assets by taking out adequate insurance cover, for example Professional Indemnity in case of a lawsuit.

To set yourself up as a sole trader, visit http://www.hmrc.gov.uk/selfemployed/register-selfemp.htm

Guide to Freelancing 14

PartnershipsA partnership is a simple way for two or more people to work together.

There are two types of partnership that you can set up:1. Ordinary partnership 2. Limited liability partnership

Ordinary partnershipsLike a sole trader, an ordinary partnership is an unincorporated business. This means that the business is not a separate legal entity and the partners are personally liable for the business debts. Partners are jointly and severally liable so, if you’re in business with someone with no personal assets then you could also find yourself liable for their share of any business debts.

A partnership can continue even if one partner resigns or dies as long as there are at least two other existing partners left. If there is only one partner left, the partnership must be dissolved, however, the remaining partner can continue on the trade as a sole trader. If one partner takes on a debt, all the partners are jointly liable for repayment of the debt. If one of the partners resigns, dies or goes bankrupt, the remaining partners will still be personally liable for any outstanding debts. However, for tax purposes each partner is taxed on their own share of the profits and therefore, each partner is personally responsible for ensuring they pay the correct amount of tax on time through their own tax returns.

Limited liability partnershipAn LLP is different from a traditional partnership in that it is a legal person separate from its members. It has “members” rather than partners and must be formally incorporated to exist. Like a limited company, an LLP has to submit accounts and an annual return to Companies House each year. This requirement is more demanding than for normal partnerships and specific accounting rules may lead to different profits from those of a normal partnership. However, unlike a limited company there are no requirements for board meetings or decision making by formal resolution, nor does an LLP have a memorandum or articles of association.

Partners and members of an LLP can join and leave at any time without the partnership being dissolved. However, to be a partnership there would have to be a minimum of two partners/members present.

How partners are paid and taxedFor tax purposes an LLP is treated exactly the same as an ordinary partnership despite having limited liability. Each partner is taxed personally on their share of profits through their own self-assessment tax returns which will be subject to income tax and class 4 NICs.

Whether you are a partner in an ordinary partnership or a member of a limited liability partnership, you are classed as self-employed and taxed on your share of any profit made by the business*. Your drawings from the business are not subject to PAYE and do not need to be processed through a payroll system.

* For this to apply to LLPs, the business must carry out a trade or profession rather than being simply an investment vehicle. Setting one upAlthough it is not a legal obligation, partnerships should have a comprehensive member agreement in place and take legal or professional advice about the issues covered in the agreement.

As a member of a partnership you need to register as self-employed, which can be done online via the HMRC website. See www.hmrc.gov.uk/partnerships.

To set up an LLP you also need to incorporate the partnership – you can find out more here: http://www.companieshouse.gov.uk/about/gbhtml/gpllp1.shtml

Alternatively you can appoint an accountant as your agent – they can advise you on the implications and handle the set-up process for you.

A partnership is a good choice if... » Your current or prospective clients don’t mind working with an unincorporated business

» Your fees aren’t paid by a recruitment agency

» Your activities aren’t likely to put your personal assets at risk

Guide to Freelancing 15

» You protect your personal assets by taking out adequate insurance cover, for example Professional Indemnity in case of a lawsuit

» You don’t want the responsibility of being a Company Director

» You and your partners have compatible skills and a clear, shared vision

» All of the partners have high levels of trust in each other

» You have a partnership agreement professionally drawn up

A limited liability partnership is a good choice if...

» You want the reassurance of having your personal assets protected

» You don’t mind the extra admin involved in sending accounts to Companies House

» You don’t want the extra responsibility of running a limited company

Find out more at www.hmrc.gov.uk/partnerships or appoint an accountant to set one up for you

Umbrella CompanyAn umbrella company is a service for people who don’t want to or need to run their own limited company. By joining an umbrella service you’re handing over the responsibilities and admin to a service provider. You become an employee of the umbrella company – the umbrella then bills your client through its own limited company structure and pays you a salary, with PAYE tax deducted at source, based on the work you do for your clients. You still have to land your own work, but they do the rest, such as payroll, debt collection and paperwork. It’s very easy, saves time, and removes the need to be aware of the legal requirements and risks involved with running a limited company.

The downside is that it’s not your own company and, therefore, it’s harder to build your own brand. It’s also less tax efficient because all the money is paid as employment income. However, if you are intending to contract for a short period, say a few months, this could prove to be the best option. If you are unavoidably ‘IR35 caught’ it may also represent a good choice – IR35 becomes irrelevant because the fees you earn from the client have the full PAYE tax deducted at source when they are paid to you as salary.

Make sure that the umbrella company you choose is a PAYE Umbrella. Any providers that claim to be able to pay you gross, without deducting tax at source, are likely to get you into hot water with the tax authorities. If you decide to go the umbrella company route do your research, seek peer recommendations and consider carrying out credit checks. You should also be very wary of any offshore solutions - IPSE has a policy of advising against aggressive tax avoidance schemes.

Will an offshore company protect me from IR35? Some freelancers have been told that they can use an offshore company to avoid IR35. It does not matter where your company is incorporated as this does not affect how HMRC determines IR35 status. There are freelancers working in the UK with companies incorporated in countries such as Ireland, the Netherlands and so on. There are reciprocal legal and tax agreements between the UK and these countries. However, some agents and clients are nervous about dealing with foreign companies.

Certain offshore schemes have used an umbrella structure and divert bonuses or other income into loans or employee benefit trusts, whilst IPSE cannot comment on specific cases, arrangements of this nature are subject to very close scrutiny by HMRC (particularly since the June 2010 Budget and the subsequent anti avoidance legislation that has either been passed or proposed) and indeed some schemes have been successfully challenged by HMRC with retrospective taxation applied. Careful investigation should be applied before entering into any of these arrangements, schemes of this nature are not covered under IPSE’s tax investigations insurance policy.

An umbrella company is a good choice if... » You don’t want the responsibility of being a company director or the hassle of handling your own business admin

» You are only planning to freelance for a short time

» You are unavoidably IR35 caught

» If you wish to have a taste of freelancing without committing to setting yourself up in business

Guide to Freelancing 16

Section 3

THE BOOKSHandling the business

financesThis section covers:7. Accountants Why it pays to get one, what to look for and where to find one

8. Bookkeeping How and why it is important to maintain proper records

9. Money in the bank Setting up a business account, how to submit invoices and tips for chasing outstanding debts

Money in your pocket How to pay yourself from the business

10. Money out What you can and can’t claim as a legitimate business expense

AccountantsWhy it pays to get oneLegally there is nothing stopping you from keeping your own accounts if you so wish, using an accounting package such as Sage or QuickBooks. Sole traders, for example, may be less inclined to get an accountant. However, many freelancers do prefer to have their accounts done by a professional, so they can get on with doing what they do best. At the end of the day it is your legal responsibility to make sure your accounts are correct, so it really is worth the cost. Using a qualified professional also helps show the tax authorities that you are taking extra steps to comply with the rules.

An accountant can provide tax advice, complete the relevant tax returns and, if you have a limited company, produce the mandatory end of year accounts, which includes the P&L and balance sheet. Some accountants may also offer additional services, such as bookkeeping, including recording and processing of receipts and expenses and invoicing.

For the basic service, a good business accountant will usually charge between £60 and £120 plus VAT per month to draw up the end of year accounts and tax returns for a limited company. VAT returns are sometimes included in this fee as well. If you operate as a sole trader or partnership, your accountancy needs may be moresimple and you could therefore be charged less.

Tax is a complex area and the rules for freelancers can change from one year to the next. Good accountants are an excellent source of advice. For complex issues, it’s often worth getting a second opinion as well - IPSE members can contact the tax and legal help-lines with any queries.

Guide to Freelancing 17

Where to find a good accountantGo to www.ipse.co.uk and browse the list of IPSE Accredited Accountants – they have been given specialist training in freelance-specific issues and have undertaken and passed an exacting training and assessment programme. If you are an IPSE member, you can also ask for recommendations from other freelancers on the IPSE forums – people tend to reply very quickly, sometimes within minutes.

What to look for in an accountantDo they understand freelancing?Don’t be afraid to ask about the firm’s experience of freelancing. Also, question the accountant’s knowledge about specific freelance regulation, such as IR35. It is important that you feel confident in the service they provide.

Do they suit your individual business requirements? Consider how you prefer to work and then ask relevant questions in order to make sure the service is suited to your specific needs. You may wish to enquire about typical response times, how contact will be maintained, who will manage your account and act as your main contact. Run through your business plan and detail any areas in which you would like the accountant to be involved, such as business advice, financial reporting, tax and auditing work. Find out if they offer any additional services you may require, such as management accounts, cash flow forecasting, advice in respect of other business activities/investments or tax planning.

Do they come well recommended?If possible ask to speak to freelance clients who are currently on their books. Other freelancers in your network can also provide vital insight that will help you avoid potential pitfalls when choosing an accountant.

Do they belong to one of the Chartered Institutes?This will offer you more protection against malpractice. Remember that anybody can call themselves an accountant but the main professional bodies all insist that their members carry adequate Professional Indemnity insurance, as well as running their own strict disciplinary schemes (including dispute resolution).

Do they charge fixed fees, monthly or hourly?You need to know what you’ll be charged so that you’re not caught by hidden extras. Make sure you are clear about what is included in your package and any additional charges that you might incur. Fixed fees are becoming increasingly common although some accountants do charge on an hourly or monthly basis. If possible try and meet your new accountant face-to-face. It will help build the relationship, moving the arrangement beyond being simply ‘an accounts processing service.’

“You simply can’t be a one-man accountant, lawyer and all the rest, and do the thing that you’re very good at doing.” Michael Darby, Freelance branding consultant

In a nutshell: Accountants » Use an accountant – it’s a more efficient use of time, resource and expertise

» Shop around carefully for the right accountant – it’s an important decision

» Don’t forget you are the client – ask questions until you are satisfied with the answers

» Budget between £700 and £1500 plus VAT per year for accounting, depending on whether you’re a sole trader or running a limited company

» Visit www.ipse.co.uk to source specialist freelancer accountants

If you’re a IPSE member, it can often be worth getting a second opinion from the IPSE tax and legal help-lines.

Guide to Freelancing 18

BookkeepingSetting up a systemBookkeeping is the first stage in the overall accounting process and is usually done by the freelancer, although it is possible to outsource it to your accountant. Bookkeeping involves recording, analysing and filing all the financial information generated by the business, such as income generated through invoices, expenses and bank transactions. Not only does this provide essential figures to help you stay on top of your business – you also need it so that you or your accountant can complete the relevant accounts and tax returns. And if you are inspected by the tax authorities, you need to show that you have a proper system in place.

Your accountant may provide you with a system. Alternatively, there are a number of excellent systems available that allow you to do everything from project estimating, timesheets and invoicing, through to calculating VAT and producing profit and loss and balance sheet statements (see next page). If you’re a IPSE member, ask for recommendations on the forums.

The implications of not keeping proper recordsA new approach to BRC started on 1 November 2012. Customers who are more likely to be at risk of having inadequate records will be contacted by letter to arrange for HMRC to call them to go through a short questionnaire.

Depending on the outcome of this call, HMRC will confirm to some customers that no further action is required. Where some issues are identified, customers will be offered targeted self-help education options. Customers who are assessed as being at risk of keeping inadequate records will be referred for a BRC visit.

As of July 2011, HM Revenue & Customs (HMRC) will be investigating up to 50,000 SMEs a year to seek out what it refers to as “poor record keeping”. Penalties include fines of up to £3,000 imposed for “significant record keeping failures.” You can keep up to speed with any changes via the IPSE newsletter.

A selection of bookkeeping systems for freelancers can be found here on the IPSE website.

As well as being a legal requirement, proper financial records help you stay on top of your business. There are many useful systems on the market to help you keep your paperwork in order.

Keeping RecordsWhat records should be kept? The short answer is, keep everything. The law doesn’t prescribe what records to create, but does say that if you create any records in your business, these should be retained. You may not always get evidence, such as a receipt, for small cash expenses, but if this happens, make a brief note of the amount you spent, when you spent it and what it was for. The record must be made contemporaneously, in other words near the time of the event rather than retrospectively.

If tax authorities were to inspect your records, they might ask to see any of the following:

» A list of all sales income and other business receipts as they come in, plus supporting records, for example, invoices, bank statements and paying-in slips to show where the income came from

» A list of all purchases and other expenses as they arise, with supporting receipts or invoices (unless the amounts are very small)

» All purchases and sales of assets used in your business

» All amounts taken out of the business bank account, or in cash, for your own or your family’s personal use

» Business diaries, mileage logs, minutes of Board Meetings, i.e. supporting records as well as the primary accounting records

» All amounts paid into the business from personal funds, for example, the proceeds of a life assurance policy.

Do they have to be kept in paper form?You don’t have to keep hard copies of the records if you don’t want to accumulate a warehouse full of physical receipts. HMRC says the following about scanning or storing records electronically:

Guide to Freelancing 19

“You can keep most records on a computer or use any storage device such as CD-ROM, USB memory stick or a network drive. You may not need to keep the original paper records as long as the method you use captures all the information ( front and back) on the document and allows the information to be presented to us in a readable format, if requested.”How long records need to be keptThe law specifies different time periods according to the type of record. These are the main ones:

Payments cash book 6 years (Companies Act)

Purchase invoices (revenue items) 6 years (Companies Act)

Purchase invoices (capital items) 10 years (Companies Act)

Purchase ledger 6 years (Companies Act)

Petty cash records 7 years (Companies Act, VAT)

Bank paying in counterfoils 6 years (Statute of Limitations)

Bank statements 6 years (Statute of Limitations)

Receipts cash book 10 years (Companies Act)

Sales ledger 10 years (Statute of Limitations)

Remittance advices 6 years (Statute of Limitations)

Deeds of covenant 12 years (Statute of Limitations)

Income tax and NI records 6 years (Taxes Management Act)

Payroll and payroll control account 7 years (Statute of Limitations)

Staff personnel records 7 years after cessation of employment(Statute of Limitations)

Expense accounts and records 7 years (Statute of Limitations)

Title deeds, leases, searches etc 12 years after interest in property ceases(Statute of Limitations)

Fixed assets register Indefinite (Companies Act)

Agreements (under seal) 12 years after expiry (Statute of Limitations)

Agreements (other) 6 years after expiry (Statute of Limitations)

In a nutshell: Bookkeeping » You can be fined up to £3,000 for each year you fail to keep proper records

» Keep all records you generate – any receipts you claim, invoices you send out, bills you receive, payslips, dividend vouchers

» Records can be computer based – you don’t need paper versions of receipts and invoices as long as all the information is there and readable

» Use one of the many systems available to keep everything organised.

Guide to Freelancing 20

Money in the bankGet a business bank accountBefore charging any money to clients, you need a dedicated business bank account. If you have a limited company, then ‘you’ are not the same in legal terms as ‘the company’, so ‘the company’ needs an account in its own name. The money in that account doesn’t belong to you until it is formally paid to you by the company.

Sole traders also benefit from having a separate business bank account. Although a sole trader’s business is not a separate legal entity in the same way that a limited company is, you still need to keep your personal affairs separate from those of the business. Having a separate business bank account will help you do that.

Choosing a bankSome people prefer to have the accounts in separate banks so that the bank can’t use knowledge about your business to make decisions regarding your personal finances. However, others prefer to develop a relationship with a particular bank. This can also make it easier to transfer money between personal and business accounts.

You don’t need to choose a bank with a local branch. There are specialist small business accounts and high-rate business savings accounts available over the internet and from non-high street banks. A bank that offers internet banking can also be very convenient – check whether you can download statements in a .csv or Excel format – that could speed up your bookkeeping as you won’t have to enter transactions manually.

Many freelancers choose to run two accounts – a business current account for everyday transactions and a business deposit account to set aside money for tax and VAT. Look for accounts that offer free banking and a good rate of interest on cash savings – you may be keeping thousands of pounds of tax money in there. Rates vary but should be within a couple of percentage points of the current Bank of England rate.

Issuing InvoicesWhat to put on the invoice

1. A clear header saying ‘invoice’.

2. A unique identification number – if your business is VAT registered, it is advisable that this needs to be a sequential number, in other words, part of a series, so that the next invoice follows on from the last.

3. The name that you regularly use for the business. If it’s a limited company you also need to include the full name of the company as it appears in the certificate of incorporation (you can put the main brand name at the top and the officially registered name as small print in the footer). Limited companies can, if they want to, include the names of the company directors on their invoices, as long as all the directors’ names are included.

4. Your business address. This must be an address where any legal documents can be delivered to you. If your business is a limited company and the business address is different to the registered address, then the registered address should also be included in the small print.

5. Your company registration number if your business is a limited company.

6. Your VAT registration number if your business is VAT registered.

7. The company name and address of the customer you are invoicing.

8. The date that the invoice is being issued (the tax date).

9. A clear description of what goods and/or services were delivered.

10. The date the goods or services were provided (supply date).

11. A column showing the number of units of the goods or services supplied (for example 3 hours), a column showing the price/rate per unit and a column showing the total for each item without VAT.

Guide to Freelancing 21

12. If your business is VAT registered, then add three more columns: the percentage of VAT that applies to each item, the total amount of VAT payable per item and then the total amount of each item including VAT.

13. At the bottom show a grand total of all items without VAT, the total amount of VAT owed and finally, a grand total of everything including VAT.

Many agencies will ask you to sign a “self-billing” agreement. This just means that they will prepare a combined invoice and payment confirmation for you, based on your timesheet. This saves you the bother of having to bill them.

Many electronic bookkeeping systems include an invoicing function that lets you customise a template, generate invoice numbers, issue invoices and track payments. IPSE members can also download an invoice template from www.ipse.co.uk

Invoicing clients outside the UKIf you’re supplying services to a client outside the UK, there’s the issue of what to do about VAT. Here’s what to do if your business is based in the UK and you are invoicing a client with an address in the EU:

1. Don’t include any VAT on the invoice, irrespective of the fact that you are VAT registered in the UK

2. Put the letters ‘GB’ either before your invoice number or in front of your VAT Registration Number

3. Include the recipient’s EU VAT registration number on the invoice. If they don’t have one you need to prove it is a business transaction by asking them to send you a purchase order or official company request, which you keep on file in case you are ever challenged

4. Include the following phrase on the invoice: ‘These services are outside the scope of UK VAT and are subject to reverse charge arrangements’

Guide to Freelancing 22

5. Bear in mind these principles apply to the supply of most traditional freelance services – if it’s not a business to business transaction, or if you’re supplying goods, then that will change things and you should seek advice (if you’re a IPSE member the tax help-line is a good port of call).

Invoices sent to clients in countries outside the EU can be slightly more complex. They are also outside the scope of UK VAT, so in theory whatever local VAT is payable is the client’s problem. However, some countries may have special rules that could make it your problem as well. For non-EU countries it’s therefore best to double check with that country’s tax authorities. As a starting point, try the IPSE forums as members work all over the world and there is usually someone who can point you in the right direction.

Staying on top of cash flowFor any business, cash flow is extremely important. Every year lots of profitable businesses go bankrupt because they don’t have cash at the right time. A good invoice system and easy to understand payment terms are key to healthy cash flow. These are some tactics to consider:

» Send out your invoices promptly, and ensure that they are sufficiently clear and detailed, and that they reflect the terms of your contract, so that the client does not have any reason to query the invoice or delay or withhold payment

» Make sure that your terms and conditions are clearly outlined in your contract with the client, and that there is no scope for ambiguity

» Ask for a deposit payment in advance, of 20% or 50%, for example

» Don’t assume that you have to offer 30 day payment terms – try offering 14 days instead, and where third party expenses recharged at cost are involved, insist on repayment within seven days

» Offer early discount settlements

» Chase outstanding invoices and keep dated notes of all conversations

Getting the terms and conditions rightTo protect yourself from late payment make your credit terms clear in the original contract. It’s also a good idea to vet new clients that don’t have a visible track record. This could mean asking for references from some of the client’s other suppliers, or doing a professional credit check. IPSE members can get discounted rates on credit checking from Creditsafe.

Your terms and conditions should cover your costs, your delivery arrangements and your payment terms. For example, do you want full or part payment in advance or payment in arrears? If you are prepared to give credit – say 30 days, then say so here. Many businesses give credit to clients, but if you’re not certain that the client will pay up then you can ask for payment upfront.

You can also state your right to charge interest on late payments and to claim compensation for debt recovery costs. You need to make your client aware of, and agree to, your terms and conditions at the outset and give the client the opportunity to discuss any problems they may have before you submit your invoice. Make sure your terms and conditions are also sent out with the invoice once the work is complete.

IPSE members can download template terms and conditions from www.ipse.co.uk

Tackling late payments“Credit vetting, terms of trade, accurate invoices and a good rapport should all form part of the structured approach you take when dealing with your customers,” says Philip King, director general of the Institute of Credit Management.

However, even with a good system in place, sooner or later most freelancers and contractors will have to chase up a late payment. When that does happen, it helps to be armed with the latest information on your clients’ legal requirements.

Since November 1998, small companies have been able to charge business customers interest on late payments, under the Late Payment of Commercial Debts (Interest) Act 1998. Small businesses can charge other businesses interest at eight percent plus the Bank of England base rate. If you have not specified a credit period in your contract it will be assumed to be 30 days from delivery or invoice, whichever is later. If payment is not forthcoming, after the credit period is up you need to follow up the invoice with reminders, which can be phone calls, letters, emails or faxes.

Remember, when it comes to tackling late payments you generally deal with the accounts department rather than your direct client so it can make the process less awkward.

Guide to Freelancing 23

During the collection process you may encounter customers who either can’t or won’t pay. You may need to impose collection sanctions such as stopping supply, reviewing the credit limit, imposing interest, use of a collection agency or legal action.

“For customers who genuinely can’t pay, it is important to determine the cause of the problem and how serious it is, what is being done to

resolve it, what you can do to help and what, if any, assurances can be offered in return for your help,”

suggests King.

It may be in your interest to negotiate a settlement such as a payment plan. For customers who simply ignore requests for payment, or make endless promises to pay you may need to threaten, or even take legal action. Take the advice of a solicitor before taking legal action.

Debt collection top tipsBe courteousRemember that every contact you make with your client can add to your existing relationship. A professional but friendly approach can earn your debtor’s respect and cement loyalty.

Convey urgencyEmails and faxes are useful tools in the collection armoury as they convey urgency and often beat defensive barriers when letters are being ignored or phone calls diverted.

Be systematicIncorporate phone calls into your collection strategy. A good strategy will timetable appropriate dates for issuing invoices, making phone calls and issuing reminders.

Be prepared Check that the information relating to the outstanding debt is correct and that the information is readily available when making phone calls – i.e. the account number, the invoice date and the balance due.

Be organisedLog the details of the phone call to remind you what action to take next, but make sure that you do not log any information that contravenes the Data Protection Act 1998. The website of the Office of Public Sector Information includes further details on this Act.

For further information see also CreditSafe’s fee recovery service and IPSE’s guide to Credit Management and Control

“With new clients I often call the accounts department before an invoice is due to check that it’s in the system. Many organisations have fixed days when they do payment runs – I time my invoicing

accordingly. It tends to be the suppliers who are politely persistent who get paid first.”

Charlie Bradburn, copywriter/consultant

Guide to Freelancing 24

In a nutshell: Money in the bank » Set up a dedicated business bank account - for a list of possible providers

visit www.ipse.co.uk

» Make your credit terms clear in your initial client contract. Terms do not need to necessarily be 30 days

» Create an invoice template which meets all legal requirements

» Different rules apply when invoicing clients outside the UK

» Errors on invoices are likely to delay payment, check the details with the client before submitting your invoice

» Send invoices promptly and have a system in place for following up on late payments

Money in your pocketOnce clients have paid their invoices, there are various things you can do with the money sitting in the business account:1. Use it to pay bills, expenses or taxes.2. Keep it in the business for a rainy day or to invest in growth.3. Extract it from the business for your personal use.

Extracting money: Sole traders and partnershipsExtracting money from the business is straightforward if you’re an unincorporated business (i.e. you’re self-employed rather than a company). Any profit left over after tax can be drawn from the business account if you wish.

To calculate the taxable profit:A. Add up your invoices (excluding VAT).B. Add up all your legitimate business expenses (excluding VAT).C. Subtract the expenses total from the invoice total – that’s your profit.

Set aside any money for tax and bills that you owe (plus VAT if applicable – see the section on VAT). Any money left over is yours.

Note that partners in a partnership are taxed on their share of the profit.

Guide to Freelancing 25

Extracting money: Limited companiesIf you run a limited company, the money received by the business isn’t yours. It still belongs to the company. To transfer any profits to your personal bank account you need to formally record the transaction as either a salary or a dividend. There are tax implications when doing this.

Paying yourself a salaryWhen you receive a salary, your salary is subject to certain taxes that must be accounted for by your limited company. They are:

» PAYE (Pay As You Earn) Income Tax.

» Employee’s National Insurance Contributions (NICs).

» Employer’s National Insurance Contributions (NICs).

The process for paying yourself is as follows:

1. Decide how much to pay yourself each month. They can be varying amounts, but usually people set a monthly amount payable on a fixed date - this can be topped up by one-off bonuses as needed.

2. Transfer the amount from the business to the personal account on the agreed date.

3. Record the transaction as salary on your bookkeeping system, including the date and the amount.

4. Tell your accountant what salary you paid yourself each month – the accountant will issue a monthly pay slip showing the tax deductions.

5. Pay all three taxes (PAYE, Employee’s NICs and Employer’s NICs) to HMRC from the business bank account – this is usually done monthly by direct debit. Your accountant can advise on the due dates. These payments must be made electronically and the cleared funds need to be in HMRC’s bank account by the 19th day of the month after the salary was paid.

Paying yourself a dividendDividends can be paid to the owners (shareholders) of a company from the retained (post tax) profit provided that the correct procedures are followed. This involves the Board of Directors having a meeting, formally voting the dividend and providing a written record of that decision. There must also be documentation in the form of a dividend voucher which is then issued to the shareholder(s). Dividend paperwork must conform to the law – IPSE members can download a dividend voucher from the freelance toolkit section of www.ipse.co.uk.

The advantage of paying yourself dividends is that neither employee nor employer NICs are payable. However, the total paid out in dividends cannot exceed the retained profits of the company. Your accountant can assist you with calculating funds available for distribution and preparation of the appropriate paperwork.

Dividends can be declared as often as you like, although if you are paying yourself regular dividends of the same amount (e.g. £1,000 once a month) there is a risk that the taxman could reclassify the payments as salary, which would negate any benefit from receiving dividends upon which neither employee nor employer NICs are payable.