Filing Information: December 2011, IDC #CA12CAS11, Volume: 1, Tab: Vendors

Canadian Cloud and Application Services: Competitive Analysis

C O M P E T I T I V E A N A L Y S I S

I D C M a r k e t S c a p e : C a n a d i a n S A P I m p l e m e n t a t i o n E c o s y s t e m 2 0 1 0 – 2 0 1 1 V e n d o r A n a l y s i s

Jim Westcott

I D C O P I N I O N

This IDC study represents a vendor assessment of the 2011 SAP-based systems

integration (SI) market through the IDC MarketScape model. This assessment

discusses both quantitative and qualitative characteristics that define success in the

SAP implementation market. This MarketScape covers a variety of vendors

participating in the SAP implementation market. The evaluation is based on a

comprehensive and rigorous framework that assesses each vendor relative to the

criteria and to one another. The framework highlights the factors expected to be the

most influential for success in the market in both the short term and the long term.

Key findings include:

The Canadian SAP implementation services market is highly competitive, and

the list of capable service providers is long. Buyers looking at implementing SAP

technology have a large field from which to choose a provider, increasing the

likelihood of finding an ideal partner and ensuring project success.

There are several IT service providers whose Canadian operations are above

average in terms of market share or customer penetration relative to other

geographies. These service provider firms are leaders in the Canadian

marketplace and help drive the brand image of the firms throughout the world.

Growth in new SAP license sales indicates that the implementation services

market is a strong growth market for IT services providers and will continue to be

a growth market for the foreseeable future. IT service providers are working with

SAP to develop a strong road map for emerging technology solutions and focus

areas (including mobility, analytics, in-memory computing, and cloud computing)

to sustain growth beyond the current forecast period.

33 Y

onge S

t., S

uite 4

20, T

oro

nto

, O

nta

rio C

anada, M

5E

1G

4

#CA12CAS11 ©2011 IDC

T A B L E O F C O N T E N T S

P

In This Study 1

Methodology ............................................................................................................................................. 2

Situat ion Overview 2

IDC MarketScape Vendor Inclusion Criteria ............................................................................................. 6

Market Size and Growth ........................................................................................................................... 6

Market Strategies .............................................................................................................................. 6

Future Out look 12

Market Analysis ........................................................................................................................................ 13

Vendor Summary Analysis ....................................................................................................................... 14

Accenture .......................................................................................................................................... 14

Description of Offerings.............................................................................................................. 14

Strengths .................................................................................................................................... 15

Key Findings and Opportunities ................................................................................................. 15

Capgemini ......................................................................................................................................... 15

Description of Offerings.............................................................................................................. 15

Strengths .................................................................................................................................... 16

Key Findings and Opportunities ................................................................................................. 16

CGI .................................................................................................................................................... 17

Description of Offerings.............................................................................................................. 17

Strengths .................................................................................................................................... 17

Key Findings and Opportunities ................................................................................................. 18

Deloitte .............................................................................................................................................. 18

Description of Offerings.............................................................................................................. 18

Strengths .................................................................................................................................... 18

Key Findings and Opportunities ................................................................................................. 19

HCL ................................................................................................................................................... 19

Description of Offerings.............................................................................................................. 19

Strengths .................................................................................................................................... 20

Key Findings and Opportunities ................................................................................................. 20

HP ..................................................................................................................................................... 20

Description of Offerings.............................................................................................................. 20

Strengths .................................................................................................................................... 21

Key Findings and Opportunities ................................................................................................. 21

IBM .................................................................................................................................................... 22

Description of Offerings.............................................................................................................. 22

Strengths .................................................................................................................................... 22

Key Findings and Opportunities ................................................................................................. 22

TCS ................................................................................................................................................... 23

Description of Offerings.............................................................................................................. 23

Strengths .................................................................................................................................... 23

Key Findings and Opportunities ................................................................................................. 23

Essent ial Guidance 24

©2011 IDC #CA12CAS11 1

I N T H I S S T U D Y

This study uses the IDC MarketScape vendor assessment model to evaluate the

Canadian SAP implementation services market. This research enables analysis of

quantitative and qualitative characteristics to provide metrics and context for end

users evaluating the use of SAP implementation services. It will also help in analyzing

a vendor's current comparative success in the marketplace and in anticipating a

vendor's evolution (and ascendancy). The main user focus areas for this market

include, among other factors, evaluation of depth and breadth of SAP implementation

service portfolios, flexibility and range of service delivery models, pricing options,

implementation methodology frameworks, sales and marketing strategies, go-to-

market strategies, and delivery model capabilities and overall competitiveness.

IDC's SAP implementation evaluation is based on a comprehensive framework and

set of parameters to assess vendors relative to one another and to those factors

expected to be most conducive to user demand and to market success for the short

term and the long term. The IDC MarketScape strategies axis represents a three- to

five-year period and future perspective, while the capabilities axis represents current

SAP implementation services offered and go-to-market execution. Despite the

regional focus of this study, IDC Canada has opted to keep the strategies and

capabilities weighting at 1:1. Often strategic direction is set at a corporate level which,

in most cases, lies outside of Canada. However, equal weighting of these two factors

was maintained due to the uniqueness of the Canadian IT services market and the

need for a balanced approach to serving existing customers and acquiring new

customers.

Market share of each vendor is indicated by the size of the circle representing the

vendor, and the vendor's year-over-year growth rate is indicated by a (+), (=), or (-)

icon next to the vendor name, representing growth in excess of, the same as, or at a

slower pace than the entire market.

This study is made up of four key sections. The first section provides definitions and

descriptions of the various IT services categories that are included in the vendor

analysis. The second provides definitions, descriptions, and weighting for the

characteristics IDC analysts believe enable a successful SAP implementation service

that is highly responsive and adaptable to user demand. These characteristics are

based on buyer and vendor surveys and analyst observations of the evolving market

and industry practices.

The third section is a visual aggregation of multiple vendors into bubble chart format

(refer to Figure 2), accompanied by written analysis. The diagram concisely display

and quantify scores of the eight reviewed vendors weighted across the SAP

implementation services market. This particular approach was chosen based on IDC's

assessment of evolving market demand and user input.

2 #CA12CAS11 ©2011 IDC

M e t h o d o l o g y

IDC MarketScape criteria selection, weightings, and vendor scores represent well-

researched IDC judgment about the market and selected vendors. IDC analysts tailor

the range of standard characteristics by which vendors are measured through

structured discussions, surveys, and interviews with market leaders, participants, and

end users. Market weightings are based on user interviews, buyer surveys, and the

input of a review board of IDC experts in each market. IDC analysts base individual

vendor scores, and ultimately vendor positions within the IDC MarketScape, on

detailed surveys and interviews with the vendors, publicly available information, and

end-user experiences in an effort to provide an accurate and consistent assessment

of each vendor's characteristics, behavior, and capability.

S I T U A T I O N O V E R V I E W

The SAP implementation market covers the design, build, and integrate functions of

the design-build-run function chain (see Figure 1). The design phase includes both IT

and business consulting. The analysis in this document excludes the "run" function

illustrated as it consists of outsourcing services activities.

F I G U R E 1

I D C ' s D e s i g n - B u i l d - R u n F u n c t i o n C h a i n

Source: IDC, 2011

©2011 IDC #CA12CAS11 3

IT consulting is defined as any professional services activity around information

technology. It is the delivery of advice to customers aimed at managing their IT

organization and at improving their IT performance, infrastructure, and related

processes. IT consulting includes two main areas:

IT strategy consulting assists an IT executive with designing an IT vision and

goals for the entire organization and then aligning resources accordingly. This

includes IT strategic planning (including human resources, facilities, and financial

planning), IT road map design, governance, systems, enterprise application, and

infrastructure strategy.

IT operations consulting assists an IT executive with optimizing the company's

IT infrastructure and architecture, and its use of specific technologies. This

includes infrastructure management; IT road map implementation; hardware,

software, and services procurement; vendor relationship management; IT

infrastructure performance; and performance engineering.

Business consulting involves advisory and implementation services related to

management issues. It involves defining an organization's strategy and goals and

designing and implementing the structures and processes that help the organization

reach its goals. Business consulting includes three main areas:

Strategy consulting assists an executive with defining a vision and goals for the

business, and acquiring and aligning resources to reach its objectives. This

includes competitive analysis, market analysis, advice-on-market entry and/or

exit strategy, product portfolio management, alliance strategy, strategic planning,

strategic road map development, and advice on corporate acquisition or

divestment choices.

Operational improvement consulting helps clients become more competitive

through process and operational changes by addressing the process and

business/industry or functional content dimensions of business transformation.

Operational improvement consulting can be viewed by core business processes

(e.g., manufacturing, marketing, sales, order fulfillment, and customer care) or by

support functions (e.g., finance processes, human resources, and

marketing/communications) excluding IT. Operational improvement consulting

services include process reengineering, sales force effectiveness, procurement

improvement, pricing strategy, cross-functional initiatives/program management

or support for all growth initiatives (including product launch, new business

implementation, and pre- and postmerger integration), and advice on risk,

security, and compliance. Operational improvement consulting also includes

process and business performance measurement through executive dashboard

and scorecard design and implementation. Examples of support functions

consulting include:

Finance and accounting (F&A) consulting serves the finance function in

client organizations. Consulting services to the finance function include

strategy and organization design for finance and accounting processes,

4 #CA12CAS11 ©2011 IDC

financial assessment, budgeting, finance management and controls

(including treasury, trading, and tax operations), transactional processes and

process and service delivery, and financial performance management and

measurement.

Governance, risk, and compliance (GRC) consulting reflects an

integrated approach to governance, risk, and compliance for organizations.

GRC is a comprehensive and holistic view of all three components

(governance, risk, and compliance) from both operational and strategic

perspectives; it is a process that promotes the operation, management, and

high performance levels of a business while ensuring the reduction of

uncertainty. Specific skills used in this service include integrating enterprise;

governance; and risk management, risk and vulnerability assessment,

business sustainability, regulatory compliance, compliance cost optimization,

change management and learning as related to risk in an organization,

performance measurement, and monitoring and incident management.

Internal audit consulting services assist organizations in assessing,

building, transforming, and sourcing their own internal audit departments.

The ultimate goal is to establish internal audit departments that are of

strategic and high value to organizations. Consulting activities include

benchmarking the internal audit function, measurement of internal audit

performance and value, quality assurance reviews including identification of

internal audit weaknesses based on stakeholder needs and organizational

risk management priorities, Sarbanes-Oxley services, the development of

internal audit career profiles and human resource models, and to determine

whether to outsource some or all of the internal audit function.

Change and organization consulting focuses on building the case for business

change and on the actions required to create the momentum to implement a

business change. Change and organization consulting also addresses the

human dimension of business transformation including organization design. This

includes helping executives align organizational elements with a new strategy

and mobilizing an organization to achieve improvement goals. Change initiatives

may include various facilitation and internal communication techniques, usually

tied to strategy and business improvement initiatives:

Change management is a structured approach to transitioning individuals,

teams, and organizations from a current state to a desired future state. It

includes both organizational change management processes and individual

change management models, which together are used to manage the

people side of change.

Organizational consulting focuses on the human dimension of business

transformation. This includes helping executives align organizational elements

with a new strategy. Organizational consulting contains several dimensions:

Human capital management. Advice related to compensation,

employee rewards and incentive programs, talent acquisition and talent

management, and development planning

©2011 IDC #CA12CAS11 5

Health and benefits. Designing or describing optimal employee health

plans with providers

Mergers and acquisitions. Assessing and proposing responses to

issues relating to cultural fit, job type, employee transition, and so forth

Communication. Strategies and tactics for disseminating corporate

information to the employee population and collecting insight into

employee attitudes, satisfaction, engagement, and other employee

behaviors, and interpreting that information

The build and integrate functions include systems integration, defined as a process

that includes the planning, design, implementation, and project management of a

technical solution that addresses a customer's specific technical or business needs

(SAP in this case). It involves IT site preparation, IT project management, test and

debug, system configuration, IT installation, software reengineering, custom software

development, packaged software customization, application interfacing and

integration, IT relocation services, systems migration, IT documentation, and user

experience design and analysis.

SI projects typically involve different platforms and technologies. The solution may

include hardware, software, and services. An SI project is formalized by a contract

that is constructed around solution specifications and often demands certain levels of

performance against technical or business goals. The end result of an SI project is

the delivery of a system that meets a stated objective and fulfills solution

specifications. It is difficult to place a minimum dollar limit, but SI projects in this

category usually exceed $100,000.

This study does not assess the run components of the SAP ecosystem. These are

services that involve a long-term, contractual arrangement in which a service provider

takes ownership of and responsibility for managing all or part of a client's IS

infrastructure and operations based on a service-level agreement (SLA). Services are

provided in a one-to-one model. These contracts would typically include the following

services provided in a discrete or bundled format, post-implementation:

Local area network (LAN) and wide area network (WAN) operations

management

Help desk support

Application management

Hosted application management

Disaster recovery services

Hosting services

Datacentre operations (either mainframe based or through a server farm)

6 #CA12CAS11 ©2011 IDC

I D C M a r k e t S c a p e V e n d o r I n c l u s i o n C r i t e r i a

For a vendor to be considered for inclusion in this study, the vendor's services must

have been significantly evaluated for purchase within a recent deal with which IDC is

familiar. Further research and due diligence were then conducted to narrow the list of

vendors to only those that had won deals and that IDC viewed as legitimate

contenders for future SAP implementation deals within the Canadian IT services

market. At the outset, 13 vendors were invited to participate in this study, the

following eight accepted:

Accenture

Capgemini

CGI

Deloitte

HCL

HP

IBM

Tata Consultancy Services (TCS)

The five vendors that declined to participate were Bell Canada, Fujitsu, Infosys,

TELUS, and Wipro.

M a r k e t S i z e a n d G r o w t h

From an implementation services standpoint, IDC Canada estimates that SAP-related

services accounted for approximately $1.2 billion in 2010, with a projected growth rate

of approximately 20% in 2011, producing an estimated 2011 spending total of $1.4

billion. From an ecosystem perspective, adding outsourcing and IT training and

education spending would add a further $1.2 billion to $1.5 billion (in 2010) bringing

the SAP-related IT services spending ecosystem into the $2.4 billion to $2.7 billion

range.

The following sections provide a detailed view of the criteria and subcriteria used by

IDC Canada to evaluate vendors active in the SAP implementation services market.

The analysis includes descriptions and quantitative values for both the strategies and

the capabilities vectors.

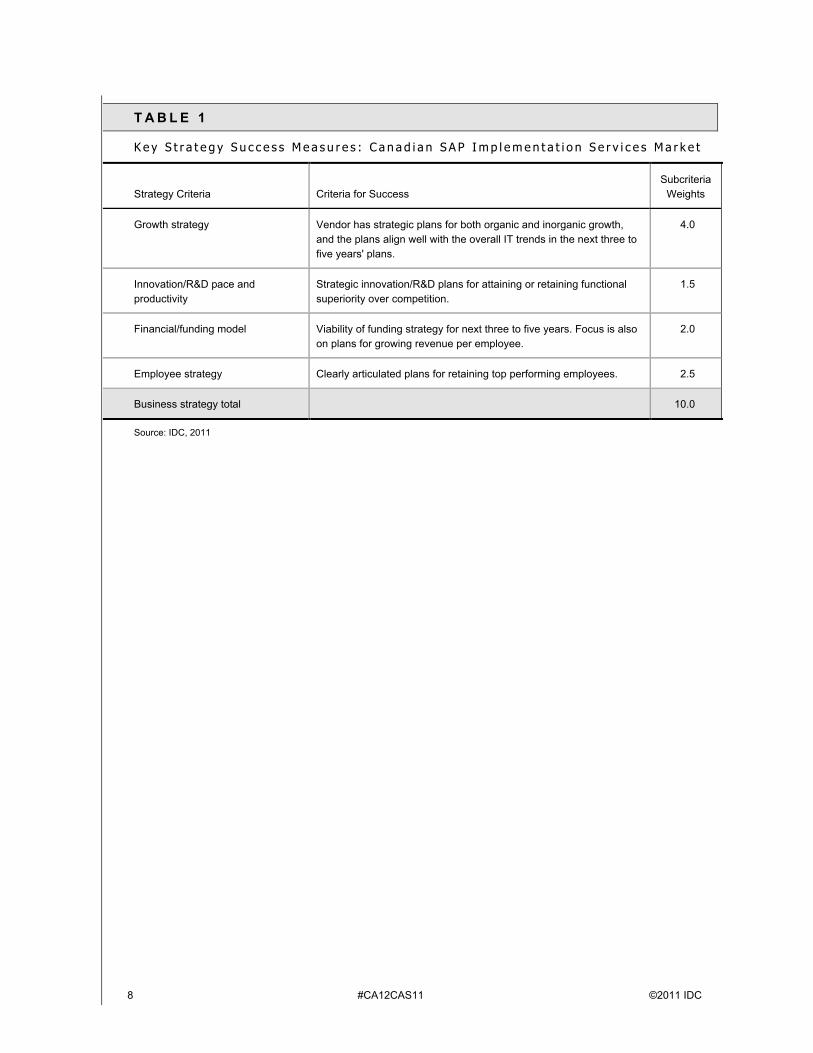

Market Strategies

There are several criteria that are most influential in predicting success in SAP

implementation services. There are service elements that providers must take into

consideration when crafting a future strategy and in leveraging existing capabilities to

best advantage. Factors for future strategy are found in Table 1, with factors for

leveraging existing capabilities in Table 2. The factors were weighted because IDC

believes that some are more important than others in maximizing market opportunity

and realizing market success in the Canadian marketplace.

©2011 IDC #CA12CAS11 7

T A B L E 1

K e y S t r a t e g y S u c c e s s M e a s u r e s : C a n a d i a n S A P I m p l e m e n t a t i o n S e r v i c e s M a r k e t

Strategy Criteria Criteria for Success

Subcriteria

Weights

Offering strategy Current development of offerings that will be relevant and attractive

to customers over the next three to five years.

Functionality or offering road map Excellence is marked by plans to offer a complete suite of SAP

solutions either through organic development, through partnership, or

through acquisition.

2.0

Delivery model Excellence is marked by plans to support emerging architectures,

such as SOA, and the ability to provide nontraditional service delivery

options, such as SaaS.

3.5

Cost management strategy Superior service calls for ways by which the vendor can help clients

justify expenditures, including ROI models, and by providing clear

paths by which the client can lower costs.

2.0

Portfolio strategy A true portfolio strategy ensures that the client makes most effective

use of the technology for business transformation and focuses on

services offered in support of SI services including emerging services

areas such as SI services around cloud computing.

2.5

Offering strategy total 10.0

Go-to-market strategy These are strategies that will maximize the connection between the

offering and the customers, including choosing to target customer

segments that offer the greatest opportunity over the next three to

five years.

Pricing model Superior planning for future pricing alignment with market direction,

and pricing plans that will encourage adoption of full SAP suite.

2.0

Sales/distribution strategy Excellence is demonstrated by plans to serve new markets such as

SMB for enterprise suppliers, or enterprise for SMB suppliers, or

specific industries. Also, the strategy to use partners including SAP

to reach these new market segments is also taken under

consideration.

3.0

Marketing strategy This involves clear, differentiation strategy and messaging of

vendor's SAP practice.

2.0

Customer service strategy Whatever the current client retention rate, superior firms have a well-

articulated plan for lowering client churn.

3.0

Go-to-market strategy total 10.0

Business strategy To be successful, vendors need to have strategies to grow the

business that are aligned with market trends and future opportunities

over the next three to five years.

8 #CA12CAS11 ©2011 IDC

T A B L E 1

K e y S t r a t e g y S u c c e s s M e a s u r e s : C a n a d i a n S A P I m p l e m e n t a t i o n S e r v i c e s M a r k e t

Strategy Criteria Criteria for Success

Subcriteria

Weights

Growth strategy Vendor has strategic plans for both organic and inorganic growth,

and the plans align well with the overall IT trends in the next three to

five years' plans.

4.0

Innovation/R&D pace and

productivity

Strategic innovation/R&D plans for attaining or retaining functional

superiority over competition.

1.5

Financial/funding model Viability of funding strategy for next three to five years. Focus is also

on plans for growing revenue per employee.

2.0

Employee strategy Clearly articulated plans for retaining top performing employees. 2.5

Business strategy total 10.0

Source: IDC, 2011

©2011 IDC #CA12CAS11 9

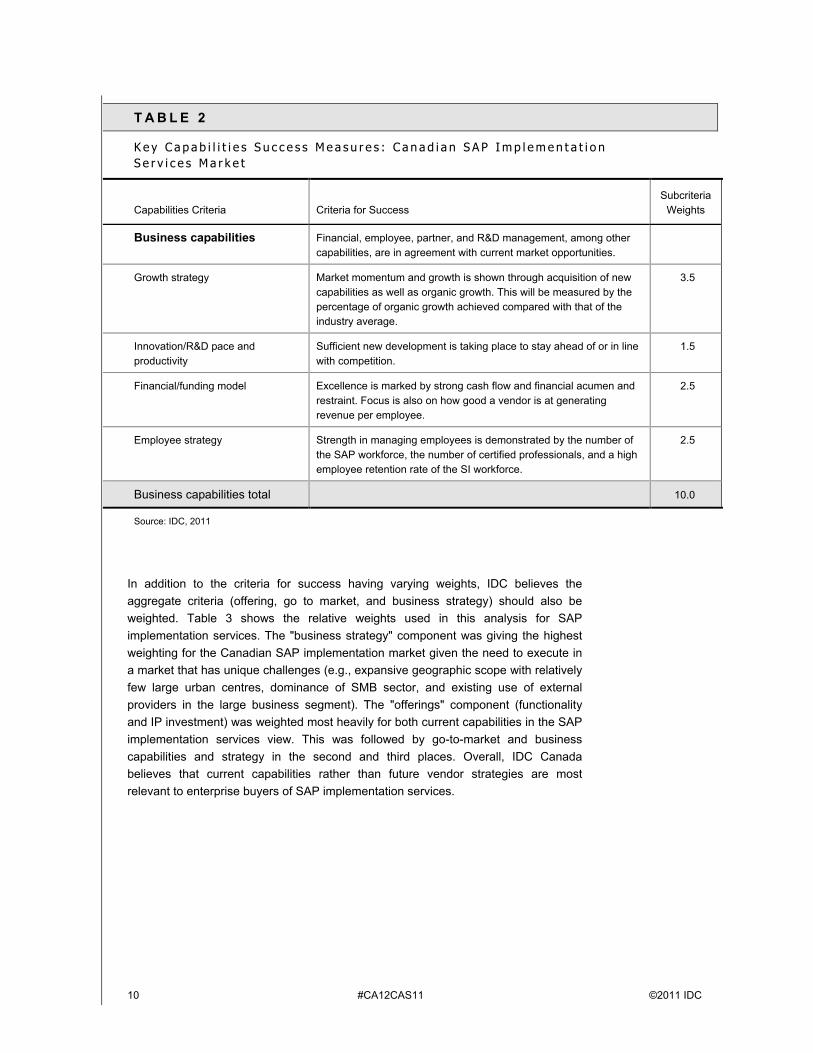

T A B L E 2

K e y C a p a b i l i t i e s S u c c e s s M e a s u r e s : C a n a d i a n S A P I m p l e m e n t a t i o n

S e r v i c e s M a r k e t

Capabilities Criteria Criteria for Success

Subcriteria

Weights

Offering capabilities The offering's capabilities align well with current market needs and

demands.

Functionality/offering delivered The ideal solution offers solutions along the full life cycle of a SAP-

based application integration process without partnership (i.e.,

capable of providing the design, build, implement, sustain, upgrade).

The vendor should be able to market these offerings as a standalone

offering.

1.5

Delivery model appropriateness

and execution

The buyer is given flexibility in delivery to meet its culture and needs

with options including onshore, nearshore, offshore, and

geographical reach. Focus is also on the size of the offshore

practice.

3.0

Cost competitiveness Pricing must reflect volume discounts and must be competitive with

the market. Focus is on blended SAP integration rates.

2.0

Portfolio benefits delivered The offerings are well supported and enhanced by a portfolio of

complementary offerings such as business consulting, application

management, and support services. That is, the vendor has the

capability to provide end-to-end services solutions and not just

integration services.

3.5

Offering capabilities total 10.0

Go-to-market capabilities These are capabilities that will maximize the connection between

offerings and customers, such as delivery, partnerships, pricing,

distribution, marketing, sales, and service.

Pricing model Flexible pricing arrangements that allow clients to navigate through

the costs of undertaking implementation projects.

3.0

Sales/distribution How well the vendor is able to reach customers using a combination

of both direct selling and an efficient partnership ecosystem. The

right partners/partnership ecosystem will include subcontracting or

collaboration with other SIs, strategic relationships with ISVs that

have strong expertise in certain domain or industry-specific areas

and, of course, strong relationships with SAP. Focus is also on the

size of the SAP-dedicated sales force.

2.5

Marketing Focus is on the size and importance of the SAP-dedicated marketing

spend within the enterprise. Looking at a marketing campaign that is

geared toward a well-defined audience. The message is concise and

appropriate for each of the target markets.

1.5

Customer service Focus is on the size of the SAP implementation client base as well as

how well the vendor is able to keep the current clients engaged.

3.0

Go-to-market strategy total 10.0

10 #CA12CAS11 ©2011 IDC

T A B L E 2

K e y C a p a b i l i t i e s S u c c e s s M e a s u r e s : C a n a d i a n S A P I m p l e m e n t a t i o n

S e r v i c e s M a r k e t

Capabilities Criteria Criteria for Success

Subcriteria

Weights

Business capabilities Financial, employee, partner, and R&D management, among other

capabilities, are in agreement with current market opportunities.

Growth strategy Market momentum and growth is shown through acquisition of new

capabilities as well as organic growth. This will be measured by the

percentage of organic growth achieved compared with that of the

industry average.

3.5

Innovation/R&D pace and

productivity

Sufficient new development is taking place to stay ahead of or in line

with competition.

1.5

Financial/funding model Excellence is marked by strong cash flow and financial acumen and

restraint. Focus is also on how good a vendor is at generating

revenue per employee.

2.5

Employee strategy Strength in managing employees is demonstrated by the number of

the SAP workforce, the number of certified professionals, and a high

employee retention rate of the SI workforce.

2.5

Business capabilities total 10.0

Source: IDC, 2011

In addition to the criteria for success having varying weights, IDC believes the

aggregate criteria (offering, go to market, and business strategy) should also be

weighted. Table 3 shows the relative weights used in this analysis for SAP

implementation services. The "business strategy" component was giving the highest

weighting for the Canadian SAP implementation market given the need to execute in

a market that has unique challenges (e.g., expansive geographic scope with relatively

few large urban centres, dominance of SMB sector, and existing use of external

providers in the large business segment). The "offerings" component (functionality

and IP investment) was weighted most heavily for both current capabilities in the SAP

implementation services view. This was followed by go-to-market and business

capabilities and strategy in the second and third places. Overall, IDC Canada

believes that current capabilities rather than future vendor strategies are most

relevant to enterprise buyers of SAP implementation services.

©2011 IDC #CA12CAS11 11

T A B L E 3

A g g r e g a t e C r i t e r i a W e i g h t i n g f o r t h e C a n a d i a n S A P I m p l e m e n t a t i o n

S e r v i c e s M a r k e t

Strategy Criteria Weighting Capabilities Criteria Weighting

Offerings strategy 3.0 Offerings capabilities 5.0

Go-to-market strategy 3.0 Go-to-market capabilities 3.0

Business strategy 4.0 Business capabilities 2.0

Subtotal 10.0 Subtotal 10.0

Source: IDC, 2011

Consequently, based on these weightings, there are several criteria that are most

influential in predicting success (for definitions of these areas, refer back to Tables 1

and 2):

Offerings. SAP implementation offerings are the most vital aspect of success for

vendors participating in the Canadian SAP implementation market. Services

providers should be able to provide a full range of SAP-based services and

solutions by leveraging all available SAP capabilities and resources. Services

providers should possess implementation capabilities around key functional

areas such as financial management, customer relationship management, supply

chain management, HR, business analytics, and any new initiative on the SAP

horizon including mobility and cloud computing. Key metrics include the number

and the types of offerings, the offering road map, and the portfolio strategy.

Complementary offerings such as outsourcing and operation-related services,

training, and support services also improve a provider's position in the ecosystem

(although not measured in this analysis).

Growth strategy. Organic and inorganic growth is important in the Canadian

market (as it is globally) due to the relative size of the market and the

concentration in revenue at the top of the market. Nontraditional providers,

including the offshore providers, are growing significantly faster than the overall

market average and sustaining these growth rates will be challenging, but it also

demonstrates the pressure that incumbent providers are facing. Overall, the SAP

implementation services market is vibrant and healthy and providers' not keeping

pace with the growth will have to reevaluate their strategies and execution in the

Canadian marketplace.

12 #CA12CAS11 ©2011 IDC

Delivery model and cost competitiveness. For the most part, Canadian

companies are comfortable using the offshore services delivery model although

application of the model will vary by business. There are some businesses, even

large Canadian businesses that are engaged in first-generation offshore resource

usage (for both project-based and outsourcing-based services), which typically

serves to restrict the use of offshore resources in favour of onsite resources. The

analysis is clear that global sourcing is a key component in providing SAP

implementation services to Canadian customers and having an appropriate mix

on onsite and offshore resources will be of critical importance as well as having

an offshore bench that can assign an even higher percentage of resources to

Canadian customer projects.

F U T U R E O U T L O O K

The IDC vendor assessment for the Canadian SAP-based systems implementation

market represents IDC's opinion on which vendors are well positioned today through

current capabilities and which are best positioned to gain market share over the next

few years. For the purposes of discussion, IDC divides potential key strategy

measures for success into two primary categories: capabilities and strategy.

Positioning in the upper right of the grid indicates that vendors have a strong

combination of capabilities to ensure success in today's ecosystem and have the right

set of strategic initiatives to maintain and grow their future position in the market.

Positioning on the y-axis reflects the vendor's current capabilities and menu of

services and how well it is aligned to customer needs. The capabilities category

focuses on the capabilities of the company and its services today. In this category,

IDC analysts look at how well a vendor is building, pricing, positioning, and/or

delivering capabilities that enable it to execute its chosen strategy in the market. On

the y-axis, a position toward the top (north of centre) indicates a strong set of

differentiated capabilities to be successful in today's market.

Positioning on the x-axis or strategy axis indicates how well the vendor's future

strategy aligns with what customers will require in three to five years. The strategy

category focuses on high-level strategic decisions and underlying assumptions about

road maps for offerings, customer segmentation, business, and go-to-market plans

for the future, which in this case is defined as the next three to five years. In this

category, analysts look at whether or not a supplier's strategies in various areas are

aligned with customer requirements in terms of spending, procurement, and delivery

over a defined future time period. On the x-axis, a position toward the right (east of

centre) indicates a strategy that not only is well aligned with customer requirements

but is agile and differentiated from the pack.

Figure 2 shows each vendor's position in the vendor assessment chart. Vendor

market share is represented by the size of the circles. Vendor year-over-year growth

rate relative to the given market is indicated by a plus, neutral, or minus icon next to

the vendor name. Spatial position is also represented on the x- and y-axes.

©2011 IDC #CA12CAS11 13

F I G U R E 2

I D C M a r k e t S c a p e S A P I m p l e m e n t a t i o n S e r v i c e s V e n d o r A s s e s s m e n t

Source: IDC, 2011

M a r k e t A n a l y s i s

As a whole, the vendors covered in this analysis are established players, all with

strengths in service, innovation, and delivery. This analysis indicates an intense

competition among the players as vendor ratings were very close for the majority of

the vendors in most subcriteria. The need to differentiate will become even more

important in the next three to five years.

The analysis also reveals certain areas of high performance and somewhat weaker

categories for players as a group within the SAP implementation ecosystem.

14 #CA12CAS11 ©2011 IDC

Relationship with SAP. The vendors profiled in this document have strong

relationships with SAP at the corporate level, and these relationships have been

reinforced at the Canada level. Vendors that have a weaker relationship with

SAP will be at a disadvantage relative to competitors.

Vertical market capabilities. All of the profiled vendors are aligned

organizationally by vertical market or have cultivated strong capabilities for

selected verticals.

Tactical market approach. Relatively few vendors are cultivating reputations as

thought leaders in Canada. In this market, emphasizing real-world experience

and tactical competency is a better strategy, and it is best to leverage thought

leadership from corporate or headquarter sources.

Global resource leverage. Global resourcing has become table stakes for

vendors operating in Canada, allowing for the reuse of methodologies, IP, and

qualified resources. Most buyers are now comfortable augmenting onsite and on-

shore resources with offshore resources, including employees brought onsite

from offshore locations.

Managed innovation. SAP has laid out its investment road map for emerging

solutions areas including mobility, in-memory computing, and cloud computing.

Implementation partners are keenly aware of these emerging opportunities and

many are already working with SAP in codeveloping solutions. In Canada,

vendors have to balance these emerging markets with existing solutions

offerings, the bulk of the opportunity in this country.

V e n d o r S u m m a r y A n a l y s i s

Accenture

Descr ipt ion of Offer ings

P r e s e n c e i n C a n a d a

Accenture has been one of the leading IT services providers' active in Canada.

Accenture's Canadian workforce exceeds 4,500, and it has offices and delivery

centres in major metropolitan centres across the country. Accenture is a Leader in

this IDC MarketScape document.

O r g a n i z a t i o n

While a significant proportion of Accenture's Canadian revenue has come from

outsourcing over the past few years, the SAP implementation practice accounts for

more than 10% of revenue in Canada and numbers in excess of 500 local resources.

Even in comparison with the other vendors profiled in this document, Accenture has a

very strong relationship with SAP, and it has reinforced this relationship with the

creation of an Accenture Innovation Center for SAP in Toronto, one of a group of

centres distributed globally. Accenture's Global Delivery Network has in excess to

16,000 SAP resources.

©2011 IDC #CA12CAS11 15

T a r g e t s f o r S A P S e r v i c e s

Accenture's SAP resources are largely held in Toronto and Montreal, but it worked on

two dozen projects across Canada in 2010/2011 across a wide range of industries

including retail, financial services, utilities, and high tech. Accenture can provide SAP

services across the entire application life cycle from consulting to implementation and

application outsourcing. The creation of the Accenture Innovation centre for SAP in

Toronto will allow Accenture an opportunity to provide Canadian customers with a

local option for assessing SAP capabilities and project options.

Strengths

A r e a s W h e r e t h e C o m p a n y E x c e l s o r I s A b l e t o D i f f e r e n t i a t e I t s e l f

Accenture, in addition to its service delivery capabilities, has cultivated strong C-level

relationships with companies across Canada. Accenture both globally and in Canada

has positioned itself as a thought leader in the IT services market, and this positioning

has raised the company's profile and gives it an advantage in terms of getting

recognition for its delivery capabilities, codevelopment initiatives, and its platform

solution for SAP implementation.

R e a s o n s f o r I t s S u c c e s s

Accenture was a pioneer in organizing its services practices by vertical market, and

this continues to be one of its strengths in the SAP implementation services market.

Accenture can provide vertical expertise and industry templates and solutions for SAP

products including horizontal product offerings (i.e., HCM).

Key F indings and Opportunit ies

R e a s o n s f o r i t s P o s i t i o n i n g o n t h e C h a r t

Accenture's positioning in the Canadian SAP implementation services market

straddles Major Player and Leader, making it a Leader in the market. Accenture is

well positioned from a customer and revenue perspective, but its growth rate has

some room to match some of its smaller rivals.

W a y s i n W h i c h t h e F i r m C a n I m p r o v e I t s P o s i t i o n i n t h e M a r k e t p l a c e

Accenture is one of the largest and best-regarded IT and business services provider

operating in Canada. The company has a strong relationship with SAP, and it

continues to demonstrate its commitment to the platform with new investments. In the

Canadian marketplace, Accenture has to balance its thought leadership initiatives and

its outsourcing/annuity revenue business with its consulting/systems integration

business.

Capgemini

Descr ipt ion of Offer ings

P r e s e n c e i n C a n a d a

Capgemini Canada is a top 10 IT and business service provider in Canada, operating

as part of the North America business unit. Using the North America operating model,

16 #CA12CAS11 ©2011 IDC

Capgemini has just short of 9,000 total resources of which close to 1,500 working in

Canada. Capgemini is a Major Player in this IDC MarketScape document.

O r g a n i z a t i o n

Capgemini has concentrated its SAP resource base (totaling 200) in central Canada,

specifically Toronto and Montreal. Capgemini can augment these in-country

resources with more than 4,000 SAP resources distributed in 22 global delivery

centres.

T a r g e t s f o r S A P S e r v i c e s

In Canada, Capgemini generates a disproportionately high percentage of its revenue

from outsourcing (in comparison with other geographies). From a target perspective,

Capgemini focuses its resources (including its SAP implementation resources) on the

utilities sector, manufacturing businesses, and retail entities. Capgemini is also

leveraging SAP's All-in-One certification program to scale SAP solutions for small and

medium-sized businesses.

Strengths

A r e a s W h e r e t h e C o m p a n y E x c e l s o r I s A b l e t o D i f f e r e n t i a t e I t s e l f

Capgemini has aggressively built solutions for the SAP platform including OnePath

(SaaS-based solutions for HCM, SCM, and procurement). Capgemini offers HCM

EDGE a proprietary solution that delivers templates and tools for SAP HCM solution.

Capgemini also offers its CRESCENT solution for consumer products and wholesale/

distribution companies. These are certified SAP All-in-One offerings. Drawing on its

success in the energy sector, Capgemini offers EnergyPath, also an SAP All-in-One

solution for energy services companies.

R e a s o n s f o r I t s S u c c e s s

Capgemini has, over the course of the past few years, shifted to an annuity revenue-

generation model, the result of winning large outsourcing contracts. This shift has

concentrated Capgemini's resources and expertise in a handful of industries, and this

has contributed to its success in the SAP implementation services market.

Key F indings and Opportunit ies

R e a s o n s f o r I t s P o s i t i o n i n g o n t h e C h a r t

Capgemini is positioned as a Major Player in the Canadian SAP implementation

services market. Despite the significant shift toward outsourcing taken by Capgemini

in Canada, the firm still has strong assets in the implementation services market and

a strong global relationship with SAP that continues to fuel opportunities in the local

Canadian market.

W a y s i n W h i c h t h e F i r m C a n I m p r o v e I t s P o s i t i o n i n t h e M a r k e t p l a c e

Capgemini has to continue to expand its presence beyond central Canada into high

growth regions and areas of the country that complement its existing strategy and

industry focus. The recent (outsourcing) contract win in British Columbia provides a

foundation from which the firm can grow in western Canada.

©2011 IDC #CA12CAS11 17

CGI

Descr ipt ion of Offer ings

P r e s e n c e i n C a n a d a

CGI is a Canadian success story having started in Quebec in the 1970s to become a

$4+ billion global IT and business services provider. IDC Canada has, in the past,

analysed CGI's distributed business model, but it has resulted in CGI having a strong

presence throughout Canada and it gives local business units the expertise to win

new business and maintain existing business with customers based on regional

requirements and industry expertise. CGI is a Major Player in this IDC MarketScape

document.

O r g a n i z a t i o n

CGI generates approximately 50% of its revenue from Canada and globally, about

one-third of revenue comes from consulting, systems integration, and application

development. As a percentage of revenue, SAP does not account for an

overwhelming majority as CGI has strong capabilities in packaged enterprise

applications and custom developed applications.

T a r g e t s f o r S A P S e r v i c e s

From a top-line Canadian perspective, CGI is well diversified across the entire

country. In terms of its SAP implementation capabilities, CGI has strong roots in the

eastern half of Canada, extending from Atlantic Canada to Ontario. Western Canada

is considered a growth market opportunity. CGI has a diverse customer base as well,

with SAP projects completed or under way in many vertical markets including

telecom, utilities, healthcare, public sector, retail, and manufacturing.

Strengths

A r e a s W h e r e t h e C o m p a n y E x c e l s o r I s A b l e t o D i f f e r e n t i a t e I t s e l f

In comparison with the other vendors profiled in this document, CGI has two

interesting points of differentiation. First, CGI prefers to use its own project

management framework (as opposed to a customer or a SAP-based methodology).

This allows the company to improve the monitoring of projects as well as lower

project risk by owning and overseeing all aspects of the project. Second, CGI does

not focus its IP on codeveloping SAP solutions. Rather, it focuses its innovation of

improving the productivity and interoperability of SAP solutions.

R e a s o n s f o r I t s S u c c e s s

CGI's business model allows local business units to get very close to its customers

and to develop strong vertical market skills based on the composition of that market.

To this foundation, CGI has, through M&A activities, extended its reach across North

America, Europe, and Asia, giving it onshore, nearshore, and offshore delivery

capabilities.

18 #CA12CAS11 ©2011 IDC

Key F indings and Opportunit ies

R e a s o n s f o r I t s P o s i t i o n i n g o n t h e C h a r t

CGI's positioning as a Major Player in the SAP implementation services market

underscores its presence in Canada as a first tier IT and business services provider.

CGI is well positioned from a revenue perspective, but it has to remain diligent not to

lose market share to new entrants.

W a y s i n W h i c h t h e F i r m C a n I m p r o v e I t s P o s i t i o n i n t h e M a r k e t p l a c e

In the Canadian marketplace, CGI is encouraged to raise its profile in SAP

implementation market, both with SAP as a partner and within the end-user

community. Unlike all of the other providers evaluated in this document, CGI does not

seek awards for its SAP work yet this could be a lost opportunity and something that

could hinder CGI's ability to market itself to new and potential customers.

Deloitte

Descr ipt ion of Offer ings

P r e s e n c e i n C a n a d a

Deloitte is one of the world's largest partner-owned IT and business consultancies,

and it has a well established operating history in Canada. In addition to its consulting

practice (which includes technology, human capital, strategy and operations, and

services quality), Deloitte Canada provides Tax, Financial Advisory Services, and

Enterprise Risk Services as part of its portfolio. Deloitte is a Leader in this IDC

MarketScape document.

O r g a n i z a t i o n

Deloitte's technology practice has experienced strong growth over the past few years,

and IDC Canada estimates that services related to SAP accounts for approximately

20% of revenue for the group.

T a r g e t s f o r S A P S e r v i c e s

Deloitte has a wide range of customers across all industries; however, it generates a

higher proportion of its Canadian revenue from tactical industries (i.e., financial

services, energy, and manufacturing) and strategic industries (i.e., public sector,

healthcare, and utilities). As a reseller of SAP's Business All In One solution, Deloitte

also targets small and medium enterprises. Globally, Deloitte derives a significant

proportion of its revenue from the SME sector through its SAP partnership.

Strengths

A r e a s W h e r e t h e C o m p a n y E x c e l s o r I s A b l e t o D i f f e r e n t i a t e I t s e l f

In the Canadian marketplace, one of the ways in which Deloitte has demonstrated its

capabilities is through the development of two SAP COEs, one in Victoria, British

Columbia, the result of a project with the British Columbia Government focused on

revenue management and the other in Winnipeg, Manitoba, with expertise in loan

management and CRM.

©2011 IDC #CA12CAS11 19

R e a s o n s f o r I t s S u c c e s s

Deloitte has resources to match many of the other top players with respect to global

delivery: the ability to draw from a pool of more than 10,000 SAP resources around

the globe. Deloitte has also cultivated a strong relationship with SAP, codeveloping

ASAP as an example, as well as using its methodologies (Enterprise Value Delivery)

and IndustryPrint to streamline project delivery and utilize best practices developed

from other SAP engagements.

Key F indings and Opportunit ies

R e a s o n s f o r I t s P o s i t i o n i n g o n t h e C h a r t

Deloitte occupies a position in the Leaders area, placing the firm at the top end of the

market in terms of IDC Canada's evaluation. Coupled with its audit, tax, and advisory

businesses, Deloitte matches up well with all of the other major vendors and their

Canadian and international capabilities.

W a y s i n W h i c h t h e F i r m C a n I m p r o v e I t s P o s i t i o n i n t h e M a r k e t p l a c e

Deloitte is very effective at demonstrating its thought leadership abilities in the

Canadian market, and this has positively reflected on the Deloitte brand. The firm is

also encouraged to raise its public profile by announcing contract wins to the market,

even in generic terms, in order to promote its practical capabilities in SAP

implementation services.

HCL

Descr ipt ion of Offer ings

P r e s e n c e i n C a n a d a

HCL is relatively new to Canada, having a local market presence (Toronto,

Vancouver, Montreal) since 2008. HCL accelerated its stake in the SAP

implementation services market in Canada (and North America) with the acquisition

of AXON in 2008. HCL is a Major Player in this IDC MarketScape document.

O r g a n i z a t i o n

In Canada, HCL generates the majority of its revenue from Enterprise Application

Services, the division of HCL that largely accounts for AXON's revenue. The vast

majority of HCL's revenue in Canada comes from application services and SAP

generates the lion share.

T a r g e t s f o r S A P S e r v i c e s

In a very short period of time, HCL has been able to acquire several high-profile

customers in the utilities (Hydro One, Fortis), transportation (Canadian National

Railway, Canadian Pacific Railway), and oil and gas (ConocoPhillips, Suncor)

sectors. HCL has established a development centre for the transportation industry

(based on its contracts with CPR and CNR) as well as its iCREW (SAP-certified

solution for HCM in regulated transportation industries) and its iLINE asset

management solution.

20 #CA12CAS11 ©2011 IDC

Strengths

A r e a s W h e r e t h e C o m p a n y E x c e l s o r I s A b l e t o D i f f e r e n t i a t e I t s e l f

HCL has defined itself as a fast follower in the Canadian market, using its asset base

tested in other geographies to establish itself in Canada in a relatively short period of

time. There is a strong vertical market orientation to HCL's strategy, and it will

continue to build on this foundation.

R e a s o n s f o r I t s S u c c e s s

Similar to other IT service providers, HCL has a vertical market structure and

alignment, and this has clearly lead to its success in Canada as it has used its global

experience to win Canadian business in a relatively short period of time. HCL has

also focused on larger deals (a highly competitive market that is difficult to unseat

incumbents), and it has cultivated relationships with sourcing advisors in addition to

its internal pursuit resources to increase its profile in large accounts.

Key Findings and Opportunit ies

R e a s o n s f o r I t s P o s i t i o n i n g o n t h e C h a r t

If this document had been authored in 2010 or early, HCL would have likely appeared

as a Contender. As it stands today, IDC considers HCL a Major Player as it has

managed to capture a significant amount of revenue and a number of marquee

customers in a relatively short amount of time. HCL has done a good job of exploiting

its capabilities to reach Canadian customers in specific vertical markets, and it has

built a foundation upon which it can generate future success.

W a y s i n W h i c h t h e F i r m C a n I m p r o v e I t s P o s i t i o n i n t h e M a r k e t p l a c e

HCL is something of an unknown quantity in the Canadian IT services market, and

the company has a relatively low level of awareness with Canadian end-user

businesses. HCL has the opportunity to increase its profile and awareness in the

market of Canadian customers and move itself higher up the market share ladder.

HP

Descr ipt ion of Offer ings

P r e s e n c e i n C a n a d a

HP is one of the largest and most diversified IT services provider in Canada with well

over $1 billion in revenue. HP's Canadian IT and business services revenue is

generated across the country, strengthened by the EDS acquisition and its strong

presence in British Columbia. HP is a Leader in this IDC MarketScape document.

O r g a n i z a t i o n

The largest share of HP's services revenue is generated through IT outsourcing.

Implementation services, confined to systems integration, comprise less than 10% of

the HP's revenue (IDC Canada estimate). Within these confines, SAP is a focus area

for HP and it does account for a sizeable share of SI spending in Canada. HP has

four SAP capability centres in Canada: two in the east (Ontario and Quebec) and two

in the west (Manitoba and Alberta).

©2011 IDC #CA12CAS11 21

T a r g e t s f o r S A P S e r v i c e s

HP has customer relationships in the major Canadian vertical market segments with a

strong heritage in the public sector, manufacturing, retail, and oil and gas. In addition

to its already strong presence in Ontario and British Columbia, HP is targeting

Quebec and Alberta for future growth. HP is also targeting the SMB sector as a

complement to its capabilities in the large business segment, a reflection of the

composition of the Canadian business landscape and its stated objective to grow IT

services revenue.

Strengths

A r e a s W h e r e t h e C o m p a n y E x c e l s o r I s A b l e t o D i f f e r e n t i a t e I t s e l f

HP has a pragmatic approach to SAP implementation services: Canadian customers

benefit from consistent methodologies, resources, and pricing based on standardized

policies as well as leveraging multiple COEs located throughout the world (5 of the 12

SAP COE's are located in the western hemisphere).

R e a s o n s f o r I t s S u c c e s s

Application services had a strong heritage in EDS prior to the acquisition and,

postacquisition, HP has continued to emphasize this business as part of its IT

services growth strategy. HP can leverage its existing success with SAP

implementation around the world to continue building the Canadian practice.

Key F indings and Opportunit ies

R e a s o n s f o r I t s P o s i t i o n i n g o n t h e C h a r t

HP's position on the IDC MarketScape chart mirrors that of the other top-rated

vendors: the border between Major Player and Leader. HP has competitive

capabilities across the entire IT services life cycle and a healthy SAP services

business, particularly with the inclusion of EDS' legacy services operations.

W a y s i n W h i c h t h e F i r m C a n I m p r o v e I t s P o s i t i o n i n t h e M a r k e t p l a c e

HP has a very strong Canadian presence yet its focus on North America as the

operating unit takes some of the focus away from its capabilities in the domestic

Canadian market and veils its presence to some degree. HP can improve its

positioning in the SAP implementation services market by raising its capabilities (and

giving it the same level of investment as it has for Java and .Net) as well as adding a

Canadian SAP COE to its existing global delivery system.

IBM

Descr ipt ion of Offer ings

P r e s e n c e i n C a n a d a

IBM is the largest IT provider in Canada with over 20,000 in-country employees and

annual revenue in excess of $5 billion. IT services revenue is estimated to exceed $4

billion annually. IBM is a Leader in this IDC MarketScape document.

22 #CA12CAS11 ©2011 IDC

O r g a n i z a t i o n

IBM's Canadian SAP capabilities are integrated in IBM's Americas business unit,

which accounts for approximately 25% of IBM's global SAP workforce. IBM also

operates an SAP Innovation and Delivery centre in Toronto.

T a r g e t s f o r S A P S e r v i c e s

IBM's strong presence across Canada has given the company a wide customer base

that includes all of the major sectors. IBM continues to target the midmarket or SMB

sector in Canada as a growth market.

Strengths

A r e a s W h e r e t h e C o m p a n y E x c e l s o r I s A b l e t o D i f f e r e n t i a t e I t s e l f

IBM has several areas in which it is able to differentiate itself from its competitors. Its

primary advantage stems from its scale in Canada, as well as the scope of its

offerings, in particular its outsourcing capabilities. IBM can also leverage its

partnership with SAP globally, described as SAP's largest partnership.

R e a s o n s f o r I t s S u c c e s s

IBM's success stems from the strength and depth of its SAP bench as well as the

reach of its sales force. IBM can also bring a strong vertical market focus, industry

templates for SAP projects, a host of software assets for automating and managing

SAP applications, and a robust methodology for managing SAP projects.

Key F indings and Opportunit ies

R e a s o n s f o r I t s P o s i t i o n i n g o n t h e C h a r t

IBM is positioned as a Leader in the Canadian SAP implementation market because

of its overall size of the practice and the breadth and depth of its capabilities.

W a y s i n W h i c h t h e F i r m C a n I m p r o v e I t s P o s i t i o n i n t h e M a r k e t p l a c e

As previously mentioned, IBM can benefit from establishing a stronger foothold in the

SMB sector or at least the high end of the medium-sized business market. This is a

growth area for some of its competitors and a source revenue that currently goes to

small and niche providers.

TCS

Descr ipt ion of Offer ings

P r e s e n c e i n C a n a d a

TCS was among the first wave of India-based providers to open an office in Canada,

and now it is the leading offshore provider in Canada in terms of revenue. Throughout

its evolution in Canada, TCS has grown its core business activities centered on

application services and expanded into complementary markets in IT infrastructure

services and BPO. TCS is a Leader in this IDC MarketScape document.

©2011 IDC #CA12CAS11 23

O r g a n i z a t i o n

In 2010, TCS restructured its organization and consolidated and its application

services business in an Enterprise Solutions group. This allows TCS to share

knowledge, expertise, toolsets, and resources around the globe. Application services

accounts for approximately 90% of TCS's revenue in Canada and SAP is a large

focus for TCS, particularly for new license sales and implementations.

T a r g e t s f o r S A P S e r v i c e s

TCS supports a wide range of SAP products in Canada from an implementation

services, with strong capabilities in ABAP, BOBJ, and logistics. From a vertical

market perspective, TCS has implemented SAP projects in the manufacturing, retail,

utilities, life sciences, travel, and transportation sectors. TCS is targeting buyers in the

financial services and telecom sectors in addition to expanding its presence in

established verticals.

Strengths

A r e a s W h e r e t h e C o m p a n y E x c e l s o r I s A b l e t o D i f f e r e n t i a t e I t s e l f

One of TCS's advantages lies in its global delivery model, the Global Network

Delivery Model (GNDM) that combines nearshore, regional, and offshore solutions

centres. From a customer perspective, the GNDM offering provides access to a

globally integrated resource base, using common processes and standard

infrastructure components.

R e a s o n s f o r I t s S u c c e s s

At least part of its success in the SAP implementation services market is based on

the strong relationship TCS has built with SAP. It was the first India-based SI to be an

SAP global service partner and one of the first Global Run SAP partner.

Key F indings and Opportunit ies

R e a s o n s f o r I t s P o s i t i o n i n g o n t h e C h a r t

TCS is positioned as a Leader in the Canadian SAP implementation services market.

TCS is the leading offshore provider active in Canada, and it continues to significantly

outperform the market average in both project-based IT services and SAP

implementation services. Canadian companies have become increasingly

comfortable in including offshore providers in RFI and RFP proposals and TCS is, as

the largest offshore player active in Canada, often sought after for a contribution.

W a y s i n W h i c h t h e F i r m C a n I m p r o v e I t s P o s i t i o n i n t h e M a r k e t p l a c e

TCS should continue to exploit its leadership position in the market and expand its

capabilities across Canada. TCS has expanded into Western Canada recently, and

this effort should be intensified to expand its presence in the west. TCS should,

wherever possible, demonstrate its success in the SAP implementation market with

public announcements to improve its brand recognition and demonstrate its

capabilities in this growing market.

24 #CA12CAS11 ©2011 IDC

E S S E N T I A L G U I D A N C E

The key finding of this research is the overall strength of the capabilities of the

majority of the vendors. While there are areas in which many vendors strive to

differentiate themselves through strategies and capabilities, there is also a great deal

of commonality among the vendors. This section highlights some of the ways in which

competitive positioning can be strengthened for vendors active in the SAP

implementation services market:

Find niche markets or service offerings to establish an exceptional

relationship with SAP. All of the service providers profiled in this document

have strong relationships with SAP and strong ties to SAP's Canadian leadership

team. Given the existence of a relatively even playing field, there are

opportunities for implementation partners to distinguish themselves through the

development of expertise or competencies in specific vertical markets or

components of the SAP solution.

Carefully balance innovation with practical, near-term service offerings.

Vendors in Canada have to walk a fine line in demonstrating thought leadership

and innovative strategies with a more practical approach to solving real-world

enterprise application issues. By and large, Canadian businesses place thought

leadership lower on the buying criteria checklist. Many of the profiled vendors

have done a good job of leveraging IP and thought leadership material from other

geographies while focusing on tactical issues in Canada. As the market for

implementation services evolves and incorporates cloud computing options,

balancing these two aspects will be challenging and leveraging existing assets

will be even more important.

Strengthen the "partnership" model with customers. Buyers have become

very sophisticated and knowledgeable, and they have a very strong

understanding of their requirements and what they expect from service providers.

In a buyers' market, vendors will have to demonstrate a commitment to flexibility

and the willingness to adapt to buyer requirements in order to be successful. This

message was consistently mentioned and reinforced by end-user interviews and

vendor flexibility and the willingness to embrace the partnership model was often

the key selection issue and separated winning bidders from losing bidders.

Find ways to selectively implement alternative pricing strategies. Vendors

have created a wide range of pricing options from which buyers can choose, and

this has clearly had a positive effect on new license sales and implementation

projects. The vast majority of customers interviewed for this study opted for

traditional fixed-price contracts, but there is still an opportunity for vendors to

establish the applicability of value-based pricing, risk-reward pricing, and other

pricing mechanisms. While some buyers may prefer the relative certainty of

traditional pricing methods, vendors can benefit from demonstrating how other

customers leveraged alternative pricing strategies.

©2011 IDC #CA12CAS11 25

This research project included a customer or an end-user dimension, and there are

numerous items buyers should consider including:

If your business is thinking about implementing SAP technology, there is at

least one service provider operating in Canada that will be a good fit. As

buyers go through the process of selecting enterprise applications, one of the

choices is the use of internal resources, the services resources of the ISV, or

opting for an IT services vendor. This research project has clearly demonstrated

that while there is commonality in service offerings and capabilities, there are

many vendors that take a unique approach to providing SAP implementation

services. Buyers are encouraged to cast a wide net for implementation partners,

and the chances of identifying an ideal match will be higher and be one of the

key factors in producing a success result.

Plan ahead and take advantage of economies of scale and scope. There are

definite advantages for taking a piece-meal approach to enterprise application

implementation, not the least of which is managing expenditures. Conversely,

there are advantages to consider current and future needs for SAP technology

and part of the consideration lies in the ability of vendors to bundle services, and

passing on cost savings on to customers. Vendors are generally willing to

accommodate a variety of project configurations to reflect the comfort level of

buyers and the benefit of bundled solutions and pricing discounts should be

factored into the equation.

Work with SAP to identify a potential service provider. As the chosen ISV,

SAP can work with buyers to identify implementation solution providers that have

specific expertise or experience in a specific area. SAP has invested

considerable time and effort in cultivating and enhancing relationships with

implementation partners, and there are areas where partners work hand in hand

with SAP developing IP, industry templates and solutions, module add-ons, and

supported methodologies. To protect the investment in SAP technologies, buyers

that don't already have a strong relationship with an implementation provider can

leverage SAP as knowledgeable advisor.

Closely evaluate vendors for specific criteria including vertical expertise

and module or functional expertise. Vertical market expertise and "knowledge

of my business" are consistently issues that affect project success, and there are

SAP implementation providers that have cultivated exceptional strength in select

vertical markets or SAP functional modules. Buyers are encouraged to seek out

this expertise, from around the globe, and engage with Canadian providers that

can leverage their global expertise on local projects as a means of improving the

odds and scale of successful outcomes.

26 #CA12CAS11 ©2011 IDC

L E A R N M O R E

R e l a t e d R e s e a r c h

IT Services Firms in Canada: Awareness, Selection Criteria, and Brand

Perception (IDC #CA10CAS11, December 2011)

IT Consulting Services in Canada: Mining 2011 Growth Opportunities (IDC

#CA4CAS11, July 2011)

Canadian Enterprise Applications 2011–2015 Forecast (IDC #CA5ECA11, June

2011)

Canada Professional Services 2011–2015 Forecast (IDC #CA6CAS11, May

2011)

Business Consulting Services in Canada: End-Users Sound Off On Usage Plans

and Opportunities (IDC #CA13CAS11, March 2011)

IDC's Worldwide Services Taxonomy, 2011 (IDC #226877, March 2011)

S y n o p s i s

This IDC study represents a vendor assessment of the SAP-based systems

integration ecosystem through the IDC MarketScape model. This assessment

discusses both quantitative and qualitative characteristics that explain success in the

SAP implementation market in Canada. This MarketScape covers a variety of

vendors participating in the SAP implementation space. The evaluation is based on a

comprehensive and rigorous framework that assesses vendors relative to the criteria

and one another and highlights the factors expected to be the most influential for

success in the market in both the short term and the long term.

"There is no question that SAP is a dynamic force in the Canadian enterprise

application market and one of the leading ISVs active in Canada. One of the key

findings of this research project is that the SAP partner ecosystem is equally as

vibrant and that there are many provider active in Canada that have an excellent mix

of strategic intent and delivery capabilities" says Jim Westcott, research manager,

Application Services at IDC Canada. "It is also apparent that the SAP implementation

services market is highly competitive and that differentiation, while difficult to attain,

will be based on cultivating and maintaining customer relationships and the further

development of industry expertise and functional SAP expertise."

©2011 IDC #CA12CAS11 27

C o p y r i g h t N o t i c e

This IDC research document was published as part of an IDC continuous intelligence

service, providing written research, analyst interactions, telebriefings, and

conferences. Visit www.idc.com to learn more about IDC subscription and consulting

services. To view a list of IDC offices worldwide, visit www.idc.com/offices. Please

contact the IDC Hotline at 800.343.4952, ext. 7988 (or +1.508.988.7988) or

[email protected] for information on applying the price of this document toward the

purchase of an IDC service or for information on additional copies or Web rights.

Copyright 2011 IDC. Reproduction is forbidden unless authorized. All rights reserved.