1

LOKMAN HEKİM ENGÜRÜSAĞ SAĞLIK, TURİZM,

EĞİTİM HİZMETLERİ VE İNŞAAT TAAHHÜT A.Ş.

CONSOLIDATED FINANCIAL STATEMENTS FOR THE INTERIM PERIOD

1 JANUARY – 30 JUNE 2018

TOGETHER WITH THE AUDITOR’S REVIEW REPORT

(CONVENIENCE TRANSLATION INTO ENGLISH OF THE CONSOLIDATED FINANCIAL STATEMENTS

TOGETHER WITH THE INDEPENDENT AUDITOR’S REVIEW REPORT ORIGINALLY ISSUED IN TURKISH)

2

LOKMAN HEKİM ENGÜRÜSAĞ SAĞLIK, TURİZM,

EĞİTİM HİZMETLERİ VE İNŞAAT TAAHHÜT A.Ş.

CONSOLIDATED FINANCIAL STATEMENTS FOR THE INTERIM PERIOD

1 JANUARY – 30 JUNE 2018 TOGETHER WITH THE AUDITOR’S REVIEW REPORT

To The Board of Directors of

Lokman Hekim Engürüsağ Sağlık, Turizm, Eğitim Hizmetleri ve İnşaat Taahhüt A.Ş.

Introduction

We have reviewed the accompanying statement of financial position of Lokman Hekim Engürüsağ

Sağlık, Turizm, Eğitim Hizmetleri ve İnşaat Taahhüt A.Ş. (the “Group” or the “Company”), as at

30 June 2018, the consolidated statement of income, the consolidated statement of other

comprehensive income, changes in equity, consolidated cash flows and other explanatory notes

for the three-month period then ended. The management of the Group is responsible for the

preparation and fair presentation of this condensed consolidated interim financial information in

accordance with Turkish Accounting Standard 34 (“IAS 34”) “Interim Financial Reporting”. Our

responsibility is to express a conclusion on this condensed consolidated interim financial

information based on our review.

Scope of Review

We conducted our review in accordance with International Standard on Review Engagements

2410, “Review of Interim Financial Information Performed by the Independent Auditor of the

Entity”. A review of interim financial information consist of making inquiries, primarily of persons

responsible for financial and accounting matters, and applying analytical and other review

procedures. A review is substantially less in scope than an audit conducted in accordance with

International Standards on Auditing and consequently does not enable us to obtain assurance

that we would become aware of all significant matters that might be identified in an audit.

Accordingly, we do not express an audit opinion.

Conclusion

Based on our review, nothing has come to our attention that causes us to believe that the

accompanying interim consolidated financial information as at 30 June 2018 is not prepared, in

all material respects, in accordance with IAS 34, “Interim Financial Reporting”.

17 August 2018, Ankara

Vezin Bağımsız Denetim A.Ş.

Member Firm of HLB International

Harun AKTAŞ, CPA

Auditor in Charge

3

TABLE OF CONTENTS

CONSOLIDATED STATEMENT OF FINANCIAL POSITION...................................................4-5

CONSOLIDATED STATEMENT OF INCOME.......................................................................6

CONSOLIDATED STATEMENT OF CHANGES IN SHAREHOLDER’S EQUITY..............................7

CONSOLIDATED STATEMENT OF CASH FLOW STATEMENT.................................................8

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS...............................................9-51

LOKMAN HEKİM ENGÜRÜSAĞ SAĞLIK, TURİZM, EĞİTİM HİZMETLERİ VE İNŞAAT TAAHHÜT A.Ş.

Consolidated Statement of Financial Position at 30 June 2018

(Amounts are expressed in Turkish Lira (TRY) unless otherwise stated.)

4

Notes

30 June 2018

31 December 2017

ASSETS

Current Assets 95,583,297 83,267,354

Cash and Cash Equivalents [4] 2,293,323 1,957,355

Trade Receivables 60,442,759 58,766,734

- Related Parties [31] 1,581,326 2,923,110

- Other [6] 58,861,433 55,843,624

Other Receivables [7] 70,189 284,812

Inventories [8] 17,630,052 13,013,651

Prepaid Expenses [19] 12,770,978 5,690,157

Assets Related to Current Period Tax [18] 365,529 988,797

Other Current Assets [17] 2,010,467 2,565,848

Non-Current Assets 164,451,018 148,560,823

Other Receivables [7] 254,941 112,177

Biological Assets [9] 16,176,967 13,991,900

Investment Property 6,400,000 6,400,000

Tangible Assets [10] 94,032,133 89,998,909

- Tangible Assets Acquired Through Financial Leasing

9,539,878

10,334,138

- Other Tangible Assets

84,492,255

79,664,771

Intangible Assets 25,402,610 25,277,631

- Goodwill [13] 1,848,336 1,848,336

- Other Intangible Assets [11] 23,554,274 23,429,295

Prepaid Expenses [19] 10,627,264 1,303,293

- Related Parties 10,419,627 861,792

- Other 207,637 441,501

Deferred Tax Assets [29] 11,557,103 11,476,913

Total Assets 260,034,315 231,828,177

LOKMAN HEKİM ENGÜRÜSAĞ SAĞLIK, TURİZM, EĞİTİM HİZMETLERİ VE İNŞAAT TAAHÜT A.Ş.

Consolidated Statement at Financial Position at 30 June 2018

(Amounts are expressed in Turkish Lira (TRY) unless otherwise stated.)

5

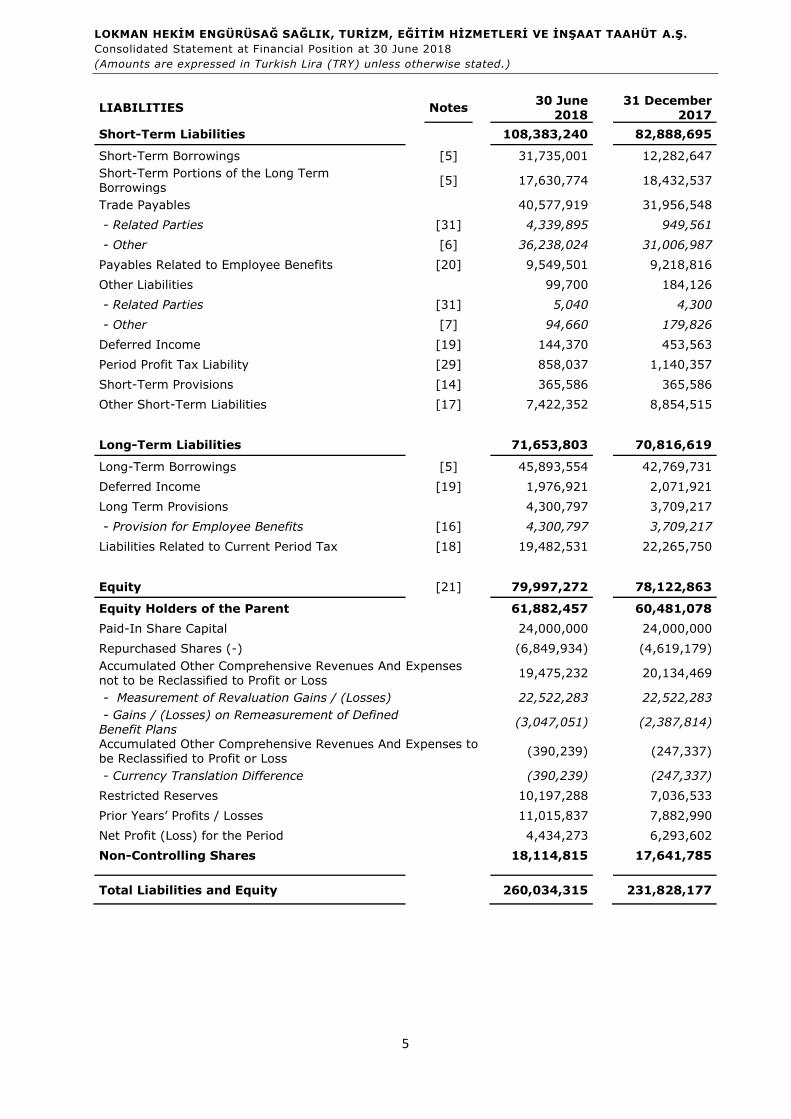

LIABILITIES

Notes

30 June 2018

31 December 2017

Short-Term Liabilities 108,383,240 82,888,695

Short-Term Borrowings [5] 31,735,001 12,282,647

Short-Term Portions of the Long Term Borrowings

[5]

17,630,774

18,432,537

Trade Payables 40,577,919 31,956,548

- Related Parties [31] 4,339,895 949,561

- Other [6] 36,238,024 31,006,987

Payables Related to Employee Benefits [20] 9,549,501 9,218,816

Other Liabilities 99,700 184,126

- Related Parties [31] 5,040 4,300

- Other [7] 94,660 179,826

Deferred Income [19] 144,370 453,563

Period Profit Tax Liability [29] 858,037 1,140,357

Short-Term Provisions [14] 365,586 365,586

Other Short-Term Liabilities [17] 7,422,352 8,854,515

Long-Term Liabilities 71,653,803 70,816,619

Long-Term Borrowings [5] 45,893,554 42,769,731

Deferred Income [19] 1,976,921 2,071,921

Long Term Provisions 4,300,797 3,709,217

- Provision for Employee Benefits [16] 4,300,797 3,709,217

Liabilities Related to Current Period Tax [18] 19,482,531 22,265,750

Equity [21] 79,997,272 78,122,863

Equity Holders of the Parent 61,882,457 60,481,078

Paid-In Share Capital 24,000,000 24,000,000

Repurchased Shares (-) (6,849,934) (4,619,179)

Accumulated Other Comprehensive Revenues And Expenses not to be Reclassified to Profit or Loss

19,475,232

20,134,469

- Measurement of Revaluation Gains / (Losses) 22,522,283 22,522,283

- Gains / (Losses) on Remeasurement of Defined Benefit Plans

(3,047,051)

(2,387,814)

Accumulated Other Comprehensive Revenues And Expenses to be Reclassified to Profit or Loss

(390,239)

(247,337)

- Currency Translation Difference (390,239) (247,337)

Restricted Reserves 10,197,288 7,036,533

Prior Years’ Profits / Losses 11,015,837 7,882,990

Net Profit (Loss) for the Period 4,434,273 6,293,602

Non-Controlling Shares 18,114,815 17,641,785

Total Liabilities and Equity

260,034,315

231,828,177

LOKMAN HEKİM ENGÜRÜSAĞ SAĞLIK, TURİZM, EĞİTİM HİZMETLERİ VE İNŞAAT TAAHÜT A.Ş.

Consolidated Statement of Income for the period 1 January – 30 June 2018

(Amounts are expressed in Turkish Lira (TRY) unless otherwise stated.)

6

Notes

1 January 30 June

2018

1 April 30 June

2018

1 January 30 June

2017

1 April 30 June

2017

Income Statement

Revenue [22] 136,913,630 68,292,863 116,838,696 56,854,945

Cost of Sales (-)

[22] (117,450,434) (60,158,727) (104,989,119)

(53,256,059)

Gross Profit (Loss) 19,463,196 8,134,136 11,849,577 3,598,886

General Administrative Expenses (-) [23] (4,566,492) (2,452,106) (3,706,006) (1,838,681)

Marketing, Sales and Distribution Expenses (-) [23] (1,391,025) (630,791) (1,685,563) (906,102)

Other Operating Income [24] 191,635 38,738 349,076 224,585

Other Operating Expenses (-)

[25] (558,690) (158,740) (1,171,158)

(591,320)

Operating Profit (Loss) 13,138,624 4,931,237 5,635,926 487,368

Income From Investment Activities

[26] 276,458 154,602 249,523

140,135

Operating Profit (Loss) Before Financial Expenses

13,415,082 5,085,839 5,885,449

627,503

Financial Income [27] 2,939,912 654,735 2,023,814 72,165

Financial Expenses (-)

[29] (8,272,127) (3,635,641) (5,343,350)

(2,168,160)

Profit (Loss) Before Tax 8,082,867 2,104,933 2,565,913 (1,468,492)

Tax Income (Expenses) [29] (725,564) 863,784 2,336,203 2,158,202

Period Tax Expense (619,815) (282,772) (537,932) 33,591

Deferred Tax Income (Expense)

(105,749) 1,146,556 2,874,135

2,124,611

Net Profit (Loss) for the Period

7,357,303 2,968,717 4,902,116

689,710

Distribution of Profit (Loss) 7,357,303 2,968,717 4,902,116 689,710

Non-Controlling Shares 2,923,030 1,082,584 3,179,187 1,441,375

Parent Company Shares 4,434,273 1,886,133 1,722,929 (751,665)

Earnings Per Share [30] 0.184761 0.078589 0.071789 (0.031319)

Other Comprehensive Income Statement 1 January

30 June 2018

1 April

30 June 2018

1 January 30 June

2017

1 April 30 June

2017

Net Profit (Loss) for the Period 7,357,303 2,968,717 4,902,116

689,710

Items not to be Reclassified to Profit or Loss

[21] (659,237) (425,907) (199,498)

(197,930)

- Gains/Losses on Remeasurement of Defined Benefit Plans

(845,176) (546,035) (154,686)

(247,415)

Tax Income/Expenses 185,939 120,128 (44,812) 49,485

Items to be Reclassified to Profit or Loss (142,902) (219,316) (5,912) (74,733)

Currency Translation Differences (142,902) (219,316) (5,912) (74,733)

Other Comprehensive Income (After Tax) (802,139) (645,223) (205,410) (272,663)

Total Comprehensive Income 6,555,164 2,323,494 4,696,706

417,047

Distribution of Total Comprehensive Income 6,555,164 2,323,494 4,696,706 417,017

Non-Controlling Shares 2,923,030 1,082,584 3,179,187 1,441,375

Equity Holders of the Parent 3,632,134 1,240,910 1,517,519 (1,024,328)

LOKMAN HEKİM ENGÜRÜSAĞ SAĞLIK, TURİZM, EĞİTİM HİZMETLERİ VE İNŞAAT TAAHÜT A.Ş.

Consolidated Statement of Changes in Shareholder’s Equity for the period 1 January – 30 June 2018

(Amounts are expressed in Turkish Lira (TRY) unless otherwise stated.)

7

Other Comprehensive

Income/Expenses not to be

Reclassified to Profit or Loss

Other Comprehensive

Income/Expenses

to be Reclassified

to Profit or Loss

Retained Earnings

Notes Paid-In Share

Capital

Repurchased

Shares (-)

Tangible

Assets Revaluation

Increase/

(Decrease)

Gains/ (Losses)

on Remeasurement

of Defined

Benefit Plans

Currency

Translation

Differences

Restricted

Reserves Prior Years’

Profits/Losses

Net Profit/Loss

for the

Period

Non-

controlling

Shares

Total

1 January 2017 [22] 24,000,000 (3,022,141) 26,427,590 (1,312,039) 206,703 4,497,027 4,383,102 7,113,164 13,830,104 76,123,510

Adjustment related to Prior Years 10,879 593,677 (219,541) (604,556) (219,541)

Transfers 586,995 6,306,628 (6,893,623) -

Currency Translation Differences (5,912) (5,912)

Gains/(Losses) on Remeasurement

ofDefined Benefit Plans (154,686) (154,686)

Tangible Assets Revaluation

Increase/(Decrease) -

Tax Income/Expense (44,812) (44,812)

Repurchased Shares (459,220) 459,220 (459,220) (459,220)

Cash Dividend Distribution (2,450,000) (2,450,000)

Non-controlling Shares -

Net Profit/Loss for the Period 1,722,929 3,179,187 4,902,116

30 June 2017 24,000,000 (3,481,361) 26,427,590 (1,511,537) 211,670 5,543,242 10,824,187 1,722,929 13,954,735 77,691,455

1 January 2018 [22] 24,000,000 (4,619,179) 22,522,283 (2,387,814) (247,337) 7,036,533 7,882,990 6,293,602 17,641,785 78,122,863

Transfers 930,000 5,363,602 (6,293,602) -

Currency Translation Differences (142,902) (142,902)

Gains/(Losses) on Remeasurement

of Defined Benefit Plans (845,176) (845,176)

Tangible Assets Revaluation Increase/(Decrease)

-

Tax Income/Expense 185,939 185,939

Repurchased Shares (2,230,755) 2,230,755 (2,230,755) (2,230,755)

Cash Dividend Distribution (2,450,000)

Non-controlling Shares (2,450,000) -

Net Profit/Loss for the Period 4,434,273 2,923,030 7,357,303

30 June 2018 24,000,000 (6,849,934) 22,522,283 (3,047,051) (390,239) 10,197,288 11,015,837 4,434,273 18,114,815 79,997,272

LOKMAN HEKİM ENGÜRÜSAĞ SAĞLIK, TURİZM, EĞİTİM HİZMETLERİ VE İNŞAAT TAAHÜT A.Ş.

Consolidated Statement of Cash Flow for the period 1 January – 30 June 2018

(Amounts are expressed in Turkish Lira (TRY) unless otherwise stated.)

8

Notes

1 January 30 June

2018

1 January 30 June

2017

A. Cash Flows From Operating Activities (11,113,830) (1,821,403)

Profit (Loss) for the Period 4,434,273 1,722,929

Adjustments to Reconcile Net Profit (Loss) for the Period 4,634,248 385,452

Adjustments to Depreciation and Amortization Expense [10-11] 4,588,763 4,489,640

Adjustments to Impairment (Cancellation) 98,612 398,932

- Adjustments to Impairment (Cancellation) in Receivables [6] 98,612 398,932

Adjustments to Provisions 591,580 123,800

- Adjustments to (Cancellation) Provisions related with Employee Benefits

[20] 591,580 123,800

Adjustments to Unrealized Currency Translation Diffirences [21] (142,902) (5,912)

Adjustments to Tax (Income) Expenses [29] (80,190) (2,829,323)

Other Adjustments Related to Non-Cash Items [17] (421,615) (1,791,685)

Changes in Working Capital (17,732,351) (1,479,784)

Adjustments to Decrease (Increase) in Trade Receivables (1,353,022) (2,042,932)

- Adjustments to Decrease (Increase) in Trade Receivables from Related Parties

[31] 1,341,784 (617,417)

- Adjustments to Decrease (Increase) in Trade Receivables from Third Parties

[7] (2,694,806) (1,425,515)

Adjustments to Decrease (Increase) in Other Receivables related with Operations

71,859 361,342

- Adjustments to Decrease (Increase) in Other Receivables from Related Parties related with Operations

[33] 220,132 369,920

- Adjustments to Decrease (Increase) in Other Receivables from Third Parties related with Operations

[7] (148,273) (8,578)

Adjustments to Decrease (Increase) in Stocks [8] (6,801,468) (1,208,114)

Adjustments to Decrease (Increase) in Prepaid Expenses [19] (16,638,656) (1,916,888)

Adjustments to Increase (Decrease) in Trade Payables 8,651,385 (4,309,372)

- Increase (Decrease) in Trade Payables to the Related Parties [31] 3,390,334 (9,502)

- Increase (Decrease) in Trade Payables to the Third Parties [6] 5,261,051 (4,299,870)

Increase (Decrease) in Payables related to Employee Benefit [20] 330,685 (1,714,347)

Increase (Decrease) in Other Payables related with Operations (84,426) 32,475

- Increase (Decrease) in Other Payables to the Related Parties related with Operations

[31] 740 (1)

- Increase (Decrease) in Other Payables to the Third Parties related with Operations

[7] (85,166) 32,476

Increase (Decrease) in Deferred Income [29] (309,193) (65,404)

Other Adjustments to Other Increase (Decrease) in Working Capital (1,599,515) 9,383,456

- Decrease (Increase) in Other Assets related with Operations 1,412,513 1,250,548

- Increase (Decrease) in Other Liabilities related with Operations (3,012,028) 8,132,908

Cash Flows from Operations (8,663,830) 628,597

Paid Dividends (2,450,000) (2,450,000)

B. Cash Flows from Investing Activities (8,705,926) (8,021,342)

Cash Outflows from Acquiring Tangible-Intangible Assets [10,11] (8,705,926) (8,021,342)

C. Cash Flows from Financing Activities 20,155,724 9,986,246

Cash Inflows from Borrowings [4] 89,793,679 82,681,533

- Cash Inflows from Loans 89,793,679 82,681,533

Cash Outflows from Repayments of Borrowings [4] (69,637,955) (72,695,287)

- Cash Outflows from Loan Repayments (69,637,955) (72,695,287)

Net Increase (Decrease) on Cash and Cash Equivalents Before the

Effect of Currency Translation Differences 335,968 143,501

D. Effect of Currency Translation Differences on Cash and Cash Equivalents

- -

Net Increase (Decrease) on Cash and Cash Equivalents 335,968 143,501

E. Cash and Cash Equivalents at the Beginning of the Period [4] 1,957,355 793,820

F. Cash and Cash Equivalents at the End of the Period(A+B+C+D+E) [4] 2,293,323 937,321

LOKMAN HEKİM ENGÜRÜSAĞ SAĞLIK, TURİZM, EĞİTİM HİZMETLERİ VE İNŞAAT TAAHÜT A.Ş.

Notes to the Consolidated Financial Statements for the Period 1 January – 30 June 2018

(Amounts are expressed in Turkish Lira (TRY) unless otherwise stated.)

9

1. COMPANY’S ORGANIZATION AND MAIN ACTIVITY

Lokman Hekim Engürüsağ Sağlık, Turizm, Eğitim Hizmetleri ve İnşaat Taahhüt A.Ş. (“Parent

Company”, “Group”, or “Company”) was established in Ankara in 1996. Firstly, it started to operate

sale of medical stuff and procurement of medical equipment.

Company amended the main contract in the meeting which was conducted on 23 May 2010 after

the 2009 Ordinary General Assembly Meeting. Company’s tittle of “Engürüsağ Sağlık, Turizm, Eğitim

Hizmetleri ve İnşaat Taahhüt A.Ş.” has been changed as “Lokman Hekim Engürüsağ Sağlık, Turizm,

Eğitim Hizmetleri ve İnşaat Taahhüt A.Ş.” relying on this amendment.

Company’s recorded address is General Tevfik Sağlam Caddesi No: 119 Etlik/Ankara.

Main partnership capital and partnership structure is;

30 June 2018 31 December 2017

Amount (TRY) % Amount (TRY) %

A Category 193,208 0.81 193,208 0.81

B Category 23,806,792 99.19 23,806,792 99.19

Total 24,000,000 100 24,000,000 100

A category shares are registered and cannot be sold in the stock exchange market. They cannot be

transferred partially to 3rd parties. A category shareholder has priority for sale of shares relying on

real value (the value which is set jointly between parties). In the situation of conflict, revaluation

of share will be made during a month by independent auditing firm which is jointly decided. At the

transfers of a category share, in the situation that there is one or more than one A category

shareholder which will take over, shares are transferred equally. When there is no A category

shareholder to take over A category shares which are settled its value, shareholder is free to sell

his shares to 3rd parties over its settled value.

Affairs and management of the Company are conducted by board of directors consisted of minimum

7 or 9 people which are elected by General Board. If board of directors will consist of 7 people

elected by General Board, 5 of them; and if board of directors will consist of 9 people, 6 of them

will be elected by General Board between candidates jointly nominated by shareholders who have

more than 51 percent of A category shares.

There is no granted privilege to B category shares.

Subsidiaries which are in the group, are subjected to consolidation, are direct, and sphere of

activities of these subsidiaries with its rate of share are like below;

Company

Principle Activity

Participation Rate (%)

30 June

2018

31 December

2017

Lokman Hekim Van Sağlık Hizmetleri ve İnşaat Taahhüt A.Ş.

Healthcare

51

51

Hay Süt ve Süt Ürünleri Hayvancılık Gıda

İth. İhr. A.Ş.

Livestock,

Dairy

73.62

73.62

Engürüsağ Genel Ticaret Ltd. Şti. (Erbil)

Healthcare

95

95

Lokman Hekim Tıp Merkezleri A.Ş.* Healthcare 100 100

(*) The Company has 49% of the shares owned by the company and 66% of the management

representation and 100% of the profit share. Therefore, the company have been included into

financial statements by fully consolidation method.

LOKMAN HEKİM ENGÜRÜSAĞ SAĞLIK, TURİZM, EĞİTİM HİZMETLERİ VE İNŞAAT TAAHÜT A.Ş.

Notes to the Consolidated Financial Statements for the Period 1 January – 30 June 2018

(Amounts are expressed in Turkish Lira (TRY) unless otherwise stated.)

10

Lokman Hekim Etlik Hospital

In Etlik district in Ankara, five-storey hospital building that has 2,900 m² of indoor area has been rented

for 15 years in 1999 and rental contract have been extended 5+5 years in 2014. There are 2 operating

rooms, 2 delivery rooms, 3 newborn intensive care incubators, 3 intensive care beds, 31 inpatient beds

with a total capacity of 37 beds.

The company has purchased the independent sections on the side of the hospital to grow the hospital,

and the projecting and rebuilding works have been started with-in the year 2017 and this additional

section is planned to bring into service in 2019.

The hospital has TUV-CERT ISO 9001:2008 Certificate of Quality Management System and it supports

the project of Baby-Friendly Hospital which is conducted by UNICEF and Ministry of Health. In this scope,

hospital has Certificate of Baby-Friendly Hospital.

Lokman Hekim Ankara Hospital

Hospital building that has 8 floors and 17,500 m² indoor areas in Sincan district in Ankara, is The Group’s

own asset. The hospital has 6 full-fledged operation rooms and one heliport for air ambulance. The

hospital has 51 intensive care rooms, 6 intensive care units for cardiology department, 1 coronary room

with 4 beds and 21 newborn intensive care incubators and 134 patient beds with a total capacity of 216

beds.

The hospital has a Baby-Friendly Hospital certificate from a project of UNICEF and Ministry of Health.

Lokman Hekim Akay Hospital

In Çankaya, Ankara, the 11-storey hospital built on 18,000 m² total area was rented for 15 years and

started its operation in 1 August 2016. The hospital has a total bed capacity of 126 beds, including 3

beds internal intensive care, 4 beds coronary intensive care, 3 beds surgical intensive care, 6 newborn

intensive care incubators, 9 beds KVC intensive care units and 101 patient beds.

Lokman Hekim Akay Hospital supports TQCSI ISO 9001: 2008 Quality Management System Standards

document and Ministry of Health and Baby Friendly Hospital Project carried out by UNICEF and has Baby

Friendly Hospital certificate.

Lokman Hekim Van Hospital

In Van city center the 9-storey hospital building with 12,500 m² indoor area, the hospital has 5 fully-

fledged operating rooms, 16 internal intensive care beds, 15 surgical intensive care beds, 5 beds for

intensive care for cardiology department, 17 coronary rooms, 64 newborn intensive care incubators and

99 patient beds with a total capacity of 216 beds.

Lokman Hekim Hayat Hospital

In the center of Van, there are 2 operating rooms, 13 beds medical and surgical intensive care units,

26 newborn intensive care units and 30 patient beds in a 5-storey hospital which is installed in a closed

area of approximately 4,500 m² and has a total capacity of 69 beds.

Engürüsağ General Trading Limited Company

The center was established to provide imaging and diagnostic facilities in Erbil, Iraq in 2013.The group

has 95% percent of the shares and titled as co-founder. The company operates in an indoor area of

approximately 2,000 m² which includes radiology and laboratory units located in the center.

Hay Süt ve Süt Ürünleri Hayvancılık Gıda İth. İhr. A.Ş.

73.62% of the shares were owned by The Company established in the Haymana district of Ankara on

23 August 2007 with a capital of TRY 1,000,000. On 29 March 2011 the company's capital was increased

to TRY 2,100,000. Hay Süt produces milk at European standards.

LOKMAN HEKİM ENGÜRÜSAĞ SAĞLIK, TURİZM, EĞİTİM HİZMETLERİ VE İNŞAAT TAAHÜT A.Ş.

Notes to the Consolidated Financial Statements for the Period 1 January – 30 June 2018

(Amounts are expressed in Turkish Lira (TRY) unless otherwise stated.)

11

Lokman Hekim Demet Tıp Merkezleri A.Ş.

It has been established in the Demetevler district of Yenimahalle in Ankara with a capital of TRY 50,000

on 12 April 2016 to provide a closed area of 2,400 m², outpatient treatment and health services.

Licensing and furnishing studies of the Lokman Hekim Demet Medical Center were completed and patient

admission started on 11 October 2016.

According to the Regulations Regarding Private Health Establishments Diagnosed and Treated Out of

the Company, the share of the company's capital has been limited to 49%. Preemtive right with (49%)

Group A shares that The Company have as founder shareholder and (51%) shares that was paid in the

course of establishment; The Company’s share rate is 100%. The absolute amount of profit share

belongs to The Company.

Laboratories

The laboratories located in the hospitals are members of the ONEWORLD ACCURACY and the reliability

of the laboratory instruments and the measurement results are regularly checked with the External

Quality Control Programs.

Medical Units

Anesthesia and Reanimation, Nutrition and Diet, Brain and Neurosurgery, Radiology, Child Care and

Pediatric, Child Neurology, Dermatology, Physical Med and Rehabilitation, Gastroenterology, General

Surgery, Pulmonology, Hematology, Eye Diseases, Internal Diseases, Gynecological Diseases and

Delivery, Cardiology, Cardiovascular Surgery, Otorhinolaryngology, Neurology, Nephrology Orthopedics

and Traumatology, Urology, Endocrinology, Psychiatry, Pediatric Surgery, Plastic Reconstructive and

Aesthetic Surgery, Emergency Medicine, Biochemistry, Microbiology, Infectious Diseases, Pathology,

Interventional Radiology, Medical Oncology.

Personnel

Position 30 June 2018

31 December 2017

Doctor 270 263

Health Services 838 791

Health Support Services 470 446

Management Support Services 446 402

Management 108 106

Veterinary and Laborers 14 14

Total 2,146 2,022

2. PRINCIPALS REGARDING TO THE PRESENTATION OF FINANCIAL STATEMENTS

2.1. Main Principles Regarding to the Presentation

2.1.1 Legal Books and Financial Statements

Within the scope of standards as IAS/IFRS respectively; Turkish Accounting Standards and Turkish

Financial Reporting System, Public Oversight, Accounting and Auditing Standards Authority (“POA”),

5411 numbered Banking Law, Turkish Capital Markets Board of Turkey (“CMB”) 6362 numbered

Capital Markets Law and with 5684 numbered Insurance Law and also 4683 numbered Individual

Retirement and Investment Law are published on 20 May 2013, on Official Journal in 28652.

According to the Principles of Financial Reporting in Capital Markets Notification (II-14.1) of Capital

Markets Board of Turkey (“CMB”), financial market institutions, with exclusion of exported capital

market tools, the transactions in the stock market of investment funds and partnership, housing

finance and asset finance funds, has to prepare its financial statement appropriately to the

IAS/IFRS.

LOKMAN HEKİM ENGÜRÜSAĞ SAĞLIK, TURİZM, EĞİTİM HİZMETLERİ VE İNŞAAT TAAHÜT A.Ş.

Notes to the Consolidated Financial Statements for the Period 1 January – 30 June 2018

(Amounts are expressed in Turkish Lira (TRY) unless otherwise stated.)

12

In the number of the meeting 20/670 of Capital Markets Board of Turkey (“CMB”), the number of

notification II-14.1 for the financial market institutions, with exclusion of exported capital market

tools, the transactions in the stock market of investment funds and partnership, housing finance

and asset finance funds after the interim periods of 31 March 2013, the methods came into force.

This methods announced in the weekly newsletter at the date 07 June 2013 and in the number of

2013/19. The company prepares its consolidated financial statements after 30 June 2013 according

to these standards.

CMB, with its resolution dated 17 March 2005, announced that all publicly traded entities operating

in Turkey was not obliged to apply inflationary accounting effective from 1 January 2005. In

accordance with this resolution, IAS 29 “Financial Reporting in Hyperinflationary Economies” is not

applied to the consolidated financial statements since 1 January 2005.

The Group prepares its Financial Statements in according to Turkish Commercial Code (“TCC”) and

Ministry of Finance Standards and used the currency is Turkish Lira(s).

The consolidated financial statements are prepared in accordance with the historical cost basis

records for the purpose of fair presentation in accordance with Turkish Accounting Standards and

Turkish Financial Reporting System (IAS/IFRS).

2.1.2 Principles of Consolidation;

Company

Principle Activity

Participation Rate (%)

30 June 2018

31 December

2017

Lokman Hekim Van Sağlık Hizmetleri ve İnşaat Taahhüt A.Ş.

Healthcare

51

51

Hay Süt ve Süt Ürünleri Hayvancılık Gıda

İth. İhr. A.Ş.

Livestock,

Dairy

73.62

73.62

Engürüsağ Genel Ticaret Ltd. Şti. (Erbil)

Healthcare

95

95

Lokman Hekim Tıp Merkezleri A.Ş.* Healthcare 100 100

(*) Preemtive right with (49%) Group A shares that The Company have as founder shareholder and

(51%) shares that was paid in the course of establishment; The Company’s share rate is 100%. The

absolute amount of profit share belongs to The Company. All the companies above are consolidated

in accordance with the principles below.

Consolidation Method

• Consolidated balance sheets and income statement items of the partnerships are consolidated

through adding up to each other. Book values of the shares owned by Main Partnership in

consolidated subsidiaries are set off from the shareholders’ equity accounts of the subsidiary.

• Receivables and payables, sale of good and services and income and loss items resulting

from the transactions between the partnerships from each other which are within the scope of

consolidation are set off.

• Tangible and intangible assets purchased between the partnerships which are subject to

consolidation method are presented in the consolidated balance sheet through their costs of

acquisition after the necessary adjustments are made.

• The amounts equal to the external shares of main partnership and subsidiaries are deducted

from all shareholders’ equity items, including the paid/issued capitals of the subsidiaries which

are within the scope of consolidation, and are presented as “Non-controlling Interests” before

the shareholders’ equity account group in the balance sheet.

LOKMAN HEKİM ENGÜRÜSAĞ SAĞLIK, TURİZM, EĞİTİM HİZMETLERİ VE İNŞAAT TAAHÜT A.Ş.

Notes to the Consolidated Financial Statements for the Period 1 January – 30 June 2018

(Amounts are expressed in Turkish Lira (TRY) unless otherwise stated.)

13

• Cost of acquisition of shares in the capital of subsidiary by main partnership as of the date

when the partnership within the scope of consolidation become subsidiary and just for the one

time for the following share purchases, is set off from the value in the shareholders’ equity in

the re-valued balance sheet of the subsidiary based on the fair value as of the purchase date.

• Acquisition of the Group is accounted through purchase method. In this method, acquisition

is registered based on cost. The group, starting from the acquisition date, includes the operation

results of the company which is acquired in its income statement and also presents each

definable asset and liability of the acquired company as well as the goodwill or negative goodwill

aroused as result of the acquisition in the balance sheet as of this date.

2.1.3. Functional Currency

Functional currency of the Group is Turkish Lira (TRY) and attached consolidated financial statements

and notes to consolidated financial statements are presented in Turkish Lira (TRY).

2.1.4. Declaration of Conformity

Attached financial statements of Group have been confirmed by the Board of Directors of the Company

as of 14 August 2018. The right to change the attached consolidated financial statements belongs to

the General Assembly of the Company or legal authorities.

2.1.5. Netting / Set Off

Financial assets and liabilities are presented at their net values in cases of a required legal right, related

assets and liabilities are intended to be netted or acquisition of assets are followed by the performing of

the liabilities.

2.1.6. Financial Statement of Partnerships Operating in Foreign Countries

Financial statements of partnerships and subsidiaries in foreign countries are prepared in accordance

with the host countries’ standards and law. The accounting principles of the Group are adjusted

according to these laws and standards.

If the currencies of the Group companies are different from reporting currency, then the translation

method is below;

All the assets and liabilities are translated with the exchange rate on the date of balance sheet.

Revenues and expenses are translated with the exchange rate on the date of balance sheet and

the difference of translation is stated in the comprehensive income statement.

2.1.7. New and Revised Turkish Accounting / Financial Reporting Standards

The Group applied new and revised standards which are published by Public Oversight Authority (“POA”)

in the current period and related to its field of business.

(a) New Standards, Amendments and Interpretations Applicable as at 1 January 2017

IAS 7 “Statement of Cash Flows” (Amendments)

Amendments to IAS 7, ‘Statement of cash flows’; on disclosure initiative effective from annual periods

beginning on or after 1 January 2017. These amendments introduce an additional disclosure that will

enable users of financial statements to evaluate changes in liabilities arising from financing activities.

LOKMAN HEKİM ENGÜRÜSAĞ SAĞLIK, TURİZM, EĞİTİM HİZMETLERİ VE İNŞAAT TAAHÜT A.Ş.

Notes to the Consolidated Financial Statements for the Period 1 January – 30 June 2018

(Amounts are expressed in Turkish Lira (TRY) unless otherwise stated.)

14

IAS 12 “Income Taxes: Recognition of Deferred Tax Assets for Unrealised

Losses” (Amendments)

Amendments to IAS 12, effective from annual periods beginning on or after 1 January 2017. The

amendments clarify the accounting for deferred tax where an asset is measured at fair value and that

fair value is below the asset’s tax base. It also clarify certain other aspects of accounting for deferred

tax assets. These amendments will be not effective on the Company’s financial position or its

performance.

Annual improvements for the period 2014-2016; Effective for annual reporting periods beginning on or

after January 1, 2018. These changes includes;

- IFRS 1, ‘First time adoption of IFRS’, regarding the deletion of short-term exemptions for first-time

adopters regarding IFRS 7, IAS 19 and IFRS 10. Amendments to IFRS1, effective from annual

periods beginning on or after 1 January 2018.

- IFRS 12, ‘Disclosure of interests in other entities’; regarding clarification of the scope of the

standard. These amendments should be applied retrospectively for annual periods beginning on or

after 1 January 2017. This amendment clarifies that the disclosures requirement of IFRS 12 are

applicable to interest in entities classified as held for sale except for summarized financial

information.

- IFRS 28, ‘Investments in Associates and Joint Ventures’; The amendment enable when an

investment in an associate or a joint venture is held by, or is held indirectly through, an entity that

is a venture capital organization, or a mutual fund, unit trust and similar entities including

investment-linked insurance funds, the entity may elect to measure that investment at fair value

through profit or loss in accordance with IFRS 9.

(b) Standards Issued but not yet Effective

Standards, interpretations and amendments to existing standards that are issued but not yet effective

up to the date of issuance of the consolidated financial statements are as follows. The Group will make

the necessary changes if not indicated otherwise, which will be affecting the consolidated financial

statements and disclosures, after the new standards and interpretations become in effect.

IFRS 15 - Revenue from Contracts with Customers

The standard replaces existing IFRS guidance and introduces a new control-based revenue recognition

model for contracts with customers. In the new standard, total consideration measured will be the

amount to which the Company expects to be entitled, rather than fair value and new guidance have

been introduced on separating goods and services in a contract and recognizing revenue over time. The

standard is effective for annual periods beginning on or after 1 January 2018, with early adoption

permitted. These amendments will be not effective on the Company’s financial position or its

performance.

IFRS 9 - Financial Instruments

The final version of IFRS 9 brings together all three aspects of the accounting for financial instruments

project: classification and measurement, impairment and hedge accounting. IFRS 9 is built on a logical,

single classification and measurement approach for financial assets that reflects the business model in

which they are managed and their cash flow characteristics. Built upon this is a forward-looking expected

credit loss model that will result in more timely recognition of loan losses and is a single model that is

applicable to all financial instruments subject to impairment accounting. In addition, IFRS 9 addresses

the so-called ‘own credit’ issue, whereby banks and others book gains through profit or loss as a result

of the value of their own debt falling due to a decrease in credit worthiness when they have elected to

measure that debt at fair value.

LOKMAN HEKİM ENGÜRÜSAĞ SAĞLIK, TURİZM, EĞİTİM HİZMETLERİ VE İNŞAAT TAAHÜT A.Ş.

Notes to the Consolidated Financial Statements for the Period 1 January – 30 June 2018

(Amounts are expressed in Turkish Lira (TRY) unless otherwise stated.)

15

The Standard also includes an improved hedge accounting model to better link the economics of risk

management with its accounting treatment. IFRS 9 is effective for annual periods beginning on or after

January 1, 2018, with early application permitted by applying all requirements of the standard.

Alternatively, entities may elect to early apply only the requirements for the presentation of gains and

losses on financial liabilities designated as FVTPL without applying the other requirements in the

standard. The Group does not expect that these amendments will have significant impact on the

consolidated financial position or performance of the Group.

IFRS 4 - Insurance Contracts (Amendments)

Amendments to IFRS 4, ‘Insurance contracts’ regarding the implementation of IFRS 9, ‘Financial

Instruments’; effective from annual periods beginning on or after 1 January 2018. These amendments

introduce two approaches: an overlay approach and a deferral approach. The Group does not expect

that these amendments will have significant impact on the consolidated financial position or performance

of the Group.

IFRIC 22 - Foreign Currency Transactions and Advance Consideration

The amendments clarifies the accounting for transactions that include the receipt or payment of advance

consideration in a foreign currency. The Interpretation covers foreign currency transactions when an

entity recognizes a non-monetary asset or non-monetary liability arising from the payment or receipt

of advance consideration before the entity recognizes the related asset, expense or income. The date

of the transaction, for the purpose of determining the exchange rate, is the date of initial recognition of

the non-monetary prepayment asset or deferred income liability. If there are multiple payments or

receipts in advance, a date of transaction is established for each payment or receipt. The amendment

is effective for annual reporting periods beginning on or after 1 January 2018 with earlier application is

permitted. The Group does not expect that these amendments will have significant impact on the

consolidated financial position or performance of the Group.

IFRS 2 - Share-Based Payment

IFRS 2 Share-Based Payment has been amended to improving consistency and resolve some long-

standing ambiguities in share-based payment accounting. The amendments cover three accounting

areas:

i) measurement of cash-settled share-based payments

ii) classification of share-based payments settled net of tax withholdings

iii) accounting for modification of a share-based payment from cash-settled to equity-settled

The amendments are effective for periods beginning on or after 1 January 2018, with earlier application

permitted. The Group does not expect that these amendments will have significant impact on the

consolidated financial position or performance of the Group.

IAS 28 Investments in Associates and Joint Venture (Amendments)

Amendment to IAS 28, ‘Investments in associates and joint venture’; effective from annual periods

beginning on or after 1 January 2019. These amendments clarify that companies account for long-term

interests in associate or joint venture to which the equity method is not applied using IFRS 9. These

amendments will be not effective on the Company’s financial position or its performance.

LOKMAN HEKİM ENGÜRÜSAĞ SAĞLIK, TURİZM, EĞİTİM HİZMETLERİ VE İNŞAAT TAAHÜT A.Ş.

Notes to the Consolidated Financial Statements for the Period 1 January – 30 June 2018

(Amounts are expressed in Turkish Lira (TRY) unless otherwise stated.)

16

IAS 40 Investment Property (Amendments)

Amendment to IAS 40, ‘Investment Property’ relating to transfers of investment property; effective from

annual periods beginning on or after 1 January 2018. These amendments clarify that to transfer to, or

from, investment properties there must be a change in use. To conclude if a property has changed use

there should be an assessment of whether the property meets the definition. This change must be

supported by evidence.

IFRS - 10 and IAS 28: Sale or Contribution of Assets between an Investor and its

Associate or Joint Venture (Amendments)

In December 2017, the POA postponed the effective date of this amendment indefinitely pending the

outcome of its research project on the equity method of accounting. Early application of the amendments

is still permitted.

(c) The New Standards, Amendments and Interpretations that are Issued by The

International Accounting Standards Board (IASB) but not Issued by (“POA”)

IASB issued Annual Improvements to IFRSs - 2015–2017 Cycle. The amendments are effective as of 1

January 2019. Earlier application is permitted. The Group will make the necessary changes after

adjustments are made from POA.

Annual Improvements to IFRS’s 2015-2017 Cycle

- IFRS 3 “Business Combinations” and IFRS 11 “Joint Arrangements” — IFRS 3 and IFRS 11 are

amended to clarify how a company accounts for increasing its interest in a joint operation that meets

the definition of a business. If a party obtains control, then the transaction is a business combination

achieved in stages and the acquiring party re-measures the previously held interest at fair value. If a

party maintains (or obtains) joint control, then the previously held interest is not re-measured.

- IAS 12 “Income Taxes” — IAS 12 is amended to clarify that all income tax consequences of dividends

(including payments on financial instruments classified as equity) are recognized consistently with the

transactions that generated the distributable profits – i.e. in profit or loss, other comprehensive income

or equity.

- IAS 23 “Borrowing Costs” — IAS 23 is amended to clarify that the general borrowings pool used to

calculate eligible borrowing costs excludes only borrowings that specifically finance qualifying assets

that are still under development or construction. Borrowings that were intended to specifically finance

qualifying assets that are now ready for their intended use or sale – or any non-qualifying assets – are

included in that general pool.

These amendments will be not effective on the Company’s financial position or its performance.

Changes and Mistakes in the Accounting Policies

An enterprise can only changes its accounting policies only in case of following conditions and apply

backwards;

Required by a standard or an interpretation

If it is in a character which provides a more appropriate and trustable way to present the effects of

the transactions and events on the financial statement, performance or cash flow of the enterprise

Parties who use the financial statements should have the opportunity to compare the financial

statements throughout the time in order to find out the trends of the financial position, performance

and cash flow. Therefore, as long as a change in an accounting policy does not meet one of the criteria

described above, same accounting policies should be used in every period and financial period. Financial

cost for inventories have not been calculated for this period. Necessary adjustments have been

made on prior periods’ financial statements.

LOKMAN HEKİM ENGÜRÜSAĞ SAĞLIK, TURİZM, EĞİTİM HİZMETLERİ VE İNŞAAT TAAHÜT A.Ş.

Notes to the Consolidated Financial Statements for the Period 1 January – 30 June 2018

(Amounts are expressed in Turkish Lira (TRY) unless otherwise stated.)

17

Comparative Information and Restatement of Prior Period Financial Statements

The accompanying financial statements is presented in comparison with the previous year in order to

identify the Group's financial condition, trends in performance and cash flows. In terms of comparative

information to conform to presentation in the current period financial statements are reclassified, where

necessary, and describes important differences.

2.2. Summary of Important Accounting Policies

2.2.1. Revenue;

Revenue means – in exchange of the health services provided – invoice amount of the invoiced services,

the amount to be invoiced for the performed but not invoiced services and the amount calculated based

on the completion level for not invoiced but still continuing services, less returns and discounts.

In case an uncertainty arises to collect a revenue amount which was presented in the financial

statements, uncollectable or the amount which becomes impossible to collect be considered as cost in

the financial statements rather than adjusting the first registered revenue.

2.2.2. Inventories;

Costs of inventories are compromise of cost of all purchases, conversion costs and other costs burdened

to perform the current position and condition of the inventories. For the inventory purchases with interim

payments, the differences between the cash value and future value are recognized as finance costs in

the period it occurred.

Inventory method is weighted average cost method.

Inventories are valued with the lowest of cost and net realizable value. Net realizable value is the value

expected sales value under normal conditions less the total of expected costs of completion and expected

sales costs in order to perform the sale.

It is assumed that the production activities would be at normal capacity on the distribution of fixed

general production costs to conversion costs. Normal capacity is the expected average production

amount under normal conditions within one or a few periods or sessions considering the loss of capacity

due to the planned repair and maintenance works. If the real production level is close to the normal

capacity, then this capacity is considered as normal capacity. If the actual production level is

continuously below from the pre-determined normal capacity, then the normal capacity is accepted as

realized actual capacity and all the fixed production costs add into the production costs of services.

The Company's actual capacity in Ankara Hospital of Sincan continued for periods, and has been

accepted as the normal capacity and this capacity calculations were made accordingly. Therefore,

the cost of an idle capacity has not been occurred.

2.2.3. Biological Assets

Biological assets are recognized initially at cost. They are valued at fair value at the end of each

reporting period. In cases where fair value cannot be calculated or determined clearly, so-called

biological asset is re-valued through its cost less all related accumulated depreciation and accumulated

provisions for loss. Gains or losses on the values are linked with the period profit or loss.

2.2.4. Tangible Assets

Tangible assets which are expected to be used within the company for more than one year are registered

with their costs at the time of purchase. In the following periods, revaluation method for lands and

buildings are revaluated based on the method for cost of other tangible assets. Costs of other tangible

assets which were purchased prior to 01 January 2005 are costs which are adjusted for inflation effects.

LOKMAN HEKİM ENGÜRÜSAĞ SAĞLIK, TURİZM, EĞİTİM HİZMETLERİ VE İNŞAAT TAAHÜT A.Ş.

Notes to the Consolidated Financial Statements for the Period 1 January – 30 June 2018

(Amounts are expressed in Turkish Lira (TRY) unless otherwise stated.)

18

The group used pro rata depreciation for tangible assets according to normal depreciation method. When

the Group determines the depreciation lives for its tangible assets, it considers the useful life of the

asset.

Costs of tangible assets which are purchased through leasing are the costs less the interest and foreign

exchange difference. Interests and foreign exchange differences are registered as financial costs in the

relevant period.

Group’s beneficial life for tangible assets are;

Buildings 50 Years

Machinery, plants and equipment 5 – 20 Years

Vehicles 5 Years

Fixtures 2 – 20 Years

Assets Purchased Through Leasing 5 – 20 Years

Other intangible assets 5 – 20 Years

2.2.5. Intangible Assets

Intangible assets which are expected to be used within the company for more than one year are

registered with its costs at the time of purchase. They are re-valued based on the cost model in the

following periods. Cost of Intangible assets which were purchased prior to 01 January 2005 are costs

which are adjusted for the inflation effect.

“Doctor Staff and Medical Licence Fee” is reported in Intangible assets as Rights for Lokman Hekim

Akay Hospital, Lokman Hekim Demet Hospital, Lokman Hekim Van Hospital and Lokman Hekim

Hayat Hospital,

According to the issued change in the Official Journal in 11 July 2013, transfer of staff and license

is allowed with article 6 of Private Hospital Regulation.

The Group takes the useful lives of the assets into consideration when determining the depreciation

lives of the Intangible assets. The Group determined useful lives for its Intangible assets 3 to 15 years.

2.2.6. Goodwill

Purchase price burdened related to the purchase of a company is distributed to the identifiable assets,

liabilities and conditional liabilities at the time of purchase of the purchased company. The difference

between purchase price and fair value of the identifiable assets, liabilities and conditional liabilities of

the purchased company is registered as goodwill in the consolidated financial statements. In the

mergers, assets, Intangible assets and conditional liabilities which are not stated in the financial

statements of the purchased company/enterprise but can be separated from the goodwill are reflected

to the consolidated financial statements with their fair values. Goodwill in the financial statements of

purchased company is not considered as identifiable assets.

In case of the buyers’ share of the fair values of the purchased identifiable assets, liabilities and

conditional liabilities exceeds the purchase price, then the difference is linked with the consolidated

income statement. In case any value decline in the goodwill amount, its effect is reflected to the period

results. Testing for the value decline at the same time every year to determine whether there is a value

decline in the goodwill amount or not.

Legal mergers among the enterprises which are under the control of the Group are considered within

the scope of UFRS 3. Therefore, no goodwill is calculated in such mergers. Moreover, transactions

occurred during legal mergers are subject to adjustment process during the preparation of consolidated

financial statements.

LOKMAN HEKİM ENGÜRÜSAĞ SAĞLIK, TURİZM, EĞİTİM HİZMETLERİ VE İNŞAAT TAAHÜT A.Ş.

Notes to the Consolidated Financial Statements for the Period 1 January – 30 June 2018

(Amounts are expressed in Turkish Lira (TRY) unless otherwise stated.)

19

2.2.7. Decline in the Values of Assets

According to IAS 36 – Decline in the Values of Assets standard, book values of tangible and intangible

assets and their recoverable values can be compared if it is deemed necessary due to domestic and

international economic indications. If it is forecasted that the book value of the asset exceeds the

recoverable value, then it is accepted that there is decline in the value of the asset.

Recoverable value is the lesser of the exercise price and market price. Forecasted decline in the value

is registered as loss at the term in which it is determined.

2.2.8. Financial Instruments

a) Cash and Cash Equivalents

Cash on hand of the Group consists of cash and bank deposits. Cash equivalents consist of receivables

from credit card. Bank deposit balances of foreign currencies are re-valued from the foreign exchange

rate of T.R. Central Bank at the date of balance sheet. Current values of the cash in the balance sheet

and deposits in the bank and receivables from credit card are the fair value of these assets.

b) Trade Receivables and Payables

Trade receivables and payables resulting from providing a service to a customer by the Group or

purchasing a good or service from a supplier are presented after clarified from deferred financing

revenues and costs.

It is assumed that the discounted values of trade receivables and provision for doubtful receivables are

equivalent to the fair values of the assets.

The group, in case there is an objective proof that the collecting is impossible, makes provisions for

doubtful receivables. The amount of this provision is registered value of the receivable less the

guarantees and warrantees.

Following making a provision for the doubtful receivables, in case all or a portion of the doubtful

receivable is not collected, the collected amount is written off from doubtful receivables and registered

as other revenues.

c) Other Receivables, Payables and Liabilities

Registered based on accrual basis and it is assumed that the registered values are equivalent to fair

values.

2.2.9. Benefits for Employees / Termination Indemnity

According to applicable Labor Law, the company shall pay a termination indemnity not less than 30 days

for each year for the employee who is fired from the company except those fired due to bad behaviors.

For this reason, the company has to estimate the total cost to be paid and discount the estimated

payments so that find the net present value. Therefore, the company reports its total liability at the

date of balance sheet which is discounted to net present value.

It is assumed that man who has worked 25 years and woman who has worked 20 years would be retired

and termination indemnity would be paid at that time. Accordingly, the company tries to find out the

expected termination indemnity liability which it would pay at the time of retirement or firing its

employees in the future. Net present value of the portion of the termination indemnity right hold by the

employee at the date of balance sheet within this total liability which is expected to be paid is registered

into the balance sheet as provision for termination indemnity. It is assumed that ratio of the number of

employees who were fired or leave the company in the previous periods without getting any termination

indemnity to the total number of employees would be the same in the following periods and total liability

is declined at this rate.

LOKMAN HEKİM ENGÜRÜSAĞ SAĞLIK, TURİZM, EĞİTİM HİZMETLERİ VE İNŞAAT TAAHÜT A.Ş.

Notes to the Consolidated Financial Statements for the Period 1 January – 30 June 2018

(Amounts are expressed in Turkish Lira (TRY) unless otherwise stated.)

20

The difference of the total termination indemnity between the two periods is distributed to cost of

interest, cost of service for the current period and actuarial income / loss. Cost of interest is the cost of

use of the liability in the previous period’s balance sheet during the period and equals to the liability

amount at the beginning of the period for the employees who are still working multiplied by discount

rate used in that year.

The cost of service for the current period is the portion of the termination indemnity at the time of it is

going to be paid which the employees get the right for termination indemnity for their services at the

time of balance sheet through discount rate. All other differences are reflected to actuarial income and

loss. Actuarial income / loss, cost of interest and cost of services for the current period are presented

in the comprehensive income statement.

Except from the wages, bonuses and other social benefits provided to employees, there is not any

contribution plan to be paid after the retirement or resigning period.

2.2.10. Taxation

Tax payable in the attached financial statements is consist of tax provision for the current period and

deferred tax. The provision for the liabilities regarding to the corporate tax to be resulted from the

activities in the current period is set based on the legal tax rates at the time of balance sheet. Deferred

tax asset/liability is the difference between account value and tax value (timing difference). Current tax

rate is considered on the calculation of deferred tax asset.

Deferred tax liability is presented in the financial statements for all taxable or deductible provisional

differences but deferred tax asset is presented in the financial statements provided that there are

taxable profits are possible from which the deductible provisional differences can be set off. Net deferred

tax assets resulting from the timing differences are reduced at the rate of the tax deductions provided

that it is not certain that they can be used in the following years according to the information on hand.

2.2.11. Related Parties

Parallel to the aim of these financial statements, related parties are considered and defined as the

companies which are linked to the shareholders, important managerial employees and board members,

their families and controlled by them or related to them, subsidiary and partnerships and minority

partners of the affiliates.

Shareholders, major managers of these companies and members of the board of the Company and their

families are also considered as related parties. Transactions made with the related parties are generally

in accordance with the market conditions. Key managerial employees are also defined as the related

parties of the company.

2.2.12. Costs of Borrowing

Bank loans with interest are registered at their net amounts after deducting the cost of borrowing.

Revenues or costs which are arising at the time of amortization or registration of the liabilities are linked

to income statement. Costs of borrowings are also registered based on accruals even if the maturities

have not become due yet at the time they arise.

2.2.13. Earnings (Loss) Per Share

Earnings (Loss) per share are calculated through net profit or loss of the period divided by the weighted

average of the number of common shares in the current period.

In Turkey, companies can increase their owners’ equity by distributing accumulated profits arise from

inflation adjustments with shares (free) to their existing stockholders.

LOKMAN HEKİM ENGÜRÜSAĞ SAĞLIK, TURİZM, EĞİTİM HİZMETLERİ VE İNŞAAT TAAHÜT A.Ş.

Notes to the Consolidated Financial Statements for the Period 1 January – 30 June 2018

(Amounts are expressed in Turkish Lira (TRY) unless otherwise stated.)

21

2.2.14. Events after the Balance Sheet Date

In case there are some events after the balance sheet date which requires adjustment entries, these

amounts in the financial statements are adjusted according to the new situation; but in case there are

events after the balance sheet date which does not require any adjustment entry, there are explanations

in the related period if the events are important.

2.2.15. Provisions, Conditional Liabilities and Conditional Assets

Provisions;

Provisions are the accruals provided that there would be a liability (legal or structural liability) resulting

from the events happened in the past, and it is probable that this liability will cause a decline in the

asset items and the liability amount can be determined reliably. Accured provisions are reviewed in

every balance sheet period and revised in order to reflect the current expectations.

Conditional Liabilities and Conditional Assets;

Transactions which cause commitment and conditional liability mean the conditions which are linked to

the result of one or more than one event that may happened in the future. Therefore, since some

transactions have possible damage, risk and uncertainty in the future, they are defined as items out of

balance sheet. In case there is a forecast for possible obligations or losses to be occurred in the future,

these liabilities are considered as costs and debt for the Company. However, income and profits which

are probable to occur in the future are presented in the financial statements.

2.2.16. Assets and Liabilities In terms of Foreign Currency

Assets in the balance sheet in terms of foreign currencies are converted to Turkish Lira based from

buying rate of foreign exchange and liabilities from selling rate of foreign exchange published by T.R.

Central Bank. Transactions with foreign currencies within the period are converted to Turkish Lira from

the actual rates at the date of transaction. Foreign exchange gains and losses arising from these

transactions are presented in the income statements. Rates used in the financial statements in 30 June

2018 and 31 December 2017 reports are as follows;

2.2.17. Important Accounting Review, Forecast and Assumptions

Preparation of financial statements requires management to apply policies and make decisions, forecasts

and assumptions which affect the assets, liabilities, incomes and losses which are reported. Real

outcomes may be different from these forecasts.

Forecasts and assumptions which are the basis of the forecasts should be revised all the time.

Important forecasts and assumptions used by the Company during the preparation of the financial

statements are as follows;

Useful lives of tangible and intangible assets

Discount rates used for trade receivables and payables

Provision rates for the receivables from Social Security Institutions (“SSI”)

Regarding to the employee benefits, retirement term, increase rate, discount rate, rate for not to

get any termination indemnity

Rates used for deferred tax calculation

Estimated operation results related to coming years as long as goodwill is based on the

impairment test

Income accurals arising from ongoing patient cares and progress payments

30 June 2018 31 December 2017

Buying Selling Buying Selling

USD 4.5607 4.5690 3.7719 3.7787

EUR 5.3092 5.3188 4.5155 4.5237

LOKMAN HEKİM ENGÜRÜSAĞ SAĞLIK, TURİZM, EĞİTİM HİZMETLERİ VE İNŞAAT TAAHÜT A.Ş.

Notes to the Consolidated Financial Statements for the Period 1 January – 30 June 2018

(Amounts are expressed in Turkish Lira (TRY) unless otherwise stated.)

22

3. OPERATION SEGMENT

Details of sales and receivables are calculated based on its sources such as hospitals, customers,

kind of treatment.

During first half of the year 2018 and same period of 2017, details of service sales based on The

Group’s each medical unit are as follows;

Service Sales/Hospitals 1 January - 30 June 2018

1 January - 30 June 2017

Amount % Amount %

Etlik Hospital Service Sales 17,505,592 13 14,888,006 13

Ankara Hospital Service Sales 40,328,763 31 33,273,061 29

Van Hospital Service Sales 28,589,433 22 28,041,342 25

Hayat Hospital Service Sales 9,982,380 8 8,157,579 7

Irbil Diagnostic Center Service Sales 1,254,749 1 1,642,267 2

Akay Hospital Service Sales 30,886,190 23 26,070,985 23

Demet Medical Center Service Sales 3,501,835 2 1,259,657 1

Total Sales 132,048,942 100 113,332,897 100

The summary of sales to Social Security Institution (SSI) and other sales are as follows;

Service Sales/Institution 1 January - 30 June

2018

1 January - 30 June

2017 Amount % Amount %

Sales to SSI* 65,222,429 49 62,987,760 56

Other Sales 66,826,513 51 50,345,137 44

Total Sales 132,048,942 100 113,332,897 100

As of 30 June 2018, details of trade receivables from Social Security Institution (SSI) and other

receivables are as follows;

Trade Receivables/Institution 30 June 2018 31 December 2017

Amount % Amount %

Receivables from SSI* 41,596,425 69 41,377,716 71

Other Receivables 18,846,334 31 17,389,018 29

Total 60,442,759 100 58,766,734 100

(*) Major customer of The Group is Social Security Institution (SSI).

Sales details based on treatment kind are as follows;

1 January - 30 June 2018 1 January - 30 June 2017

Number of

Patient Net Sales (%) Number of

Patient Net Sales (%)

Outpatient 535,361 59,379,971 45 486,932 48,417,457 43

Inpatient 31,319 72,668,971 55 29,680 64,915,440 57

Total 566,680 132,048,942 100 516,612 113,332,897 100

LOKMAN HEKİM ENGÜRÜSAĞ SAĞLIK, TURİZM, EĞİTİM HİZMETLERİ VE İNŞAAT TAAHÜT A.Ş.

Notes to the Consolidated Financial Statements for the Period 1 January – 30 June 2018

(Amounts are expressed in Turkish Lira (TRY) unless otherwise stated.)

23

4. CASH AND CASH EQUIVALENTS

The position of cash and cash equivalents as of end of the period is as follows;

30 June 2018

31 December 2017

Cash 549,391 506,949

Banks 1,743,932 1,450,406

Total 2,293,323 1,957,355

5. FINANCIAL LIABILITIES

The summary of short-term liabilities as of balance sheet date is as follows;

Short-Term Financial Liabilities 30 June

2018

31 December

2017

Short-Term Borrowings 29,280,663 9,613,490

Short-Term Portion of Long-Term Borrowings 17,630,774 18,432,537

Financial Leasing Debts 2,454,338 2,669,157

- Financial Leasing Debts 2,993,130 3,389,436

- Deferred Interest Cost (538,792) (720,279)

Total 49,365,775 30,715,184

The summary of long-term financial liabilities is as follows;

Long-Term Financial Liabilities 30 June 2018

31 December 2017

Long-Term Borrowings 43,641,304 39,336,037

Financial Leasing Debts 2,252,250 3,433,694

- Financial Leasing Debts 2,572,864 3,980,744

- Deferred Interest Cost (320,614) (547,050)

Total 45,893,554 42,769,731

Redemption schedule of bank borrowings is as follows;

Bank Borrowings 30 June

2018

31 December 2017

0 - 3 Months 8,736,378 4,780,769

3 - 12 Months 38,175,059 23,565,257

1 - 5 Years 37,917,606 34,701,609

More Than 5 Years 5,723,698 4,334,427

Total 90,552,741 67,382,062

Redemption schedule of financial leasings is as follows;

Financial Leasing 30 June 2018

31 December 2017

0 - 3 Months 709,044 724,533

3 - 12 Months 1,745,294 1,944,624

1 - 5 Years 2,252,250 3,433,694

Total 4,706,588 6,102,851

Mortgage amounting to TRY 102,665,001 has been given for bank borrowings.

(31 December 2017: TRY 92,935,001).

LOKMAN HEKİM ENGÜRÜSAĞ SAĞLIK, TURİZM, EĞİTİM HİZMETLERİ VE İNŞAAT TAAHÜT A.Ş.

Notes to the Consolidated Financial Statements for the Period 1 January – 30 June 2018

(Amounts are expressed in Turkish Lira (TRY) unless otherwise stated.)

24

6. TRADE RECEIVABLES AND TRADE PAYABLES

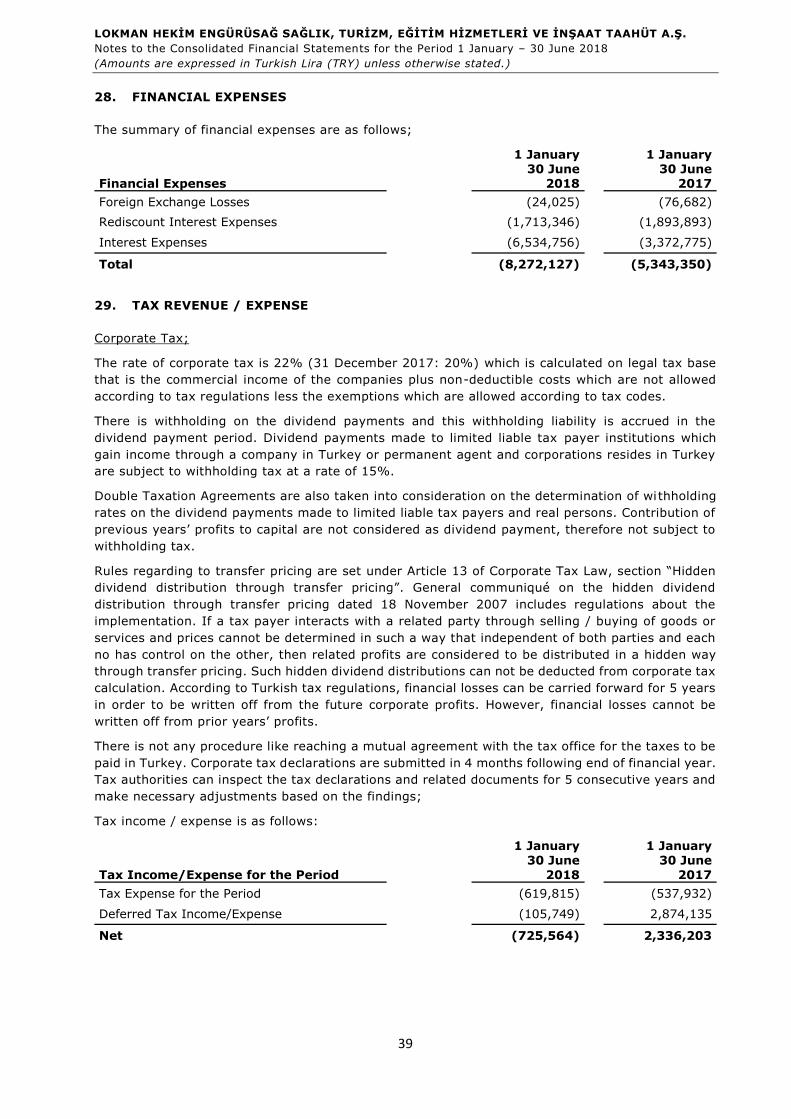

The summary of trade receivables as of end of the periods is as follows;

30 June 2018

31 December 2017

Trade Receivables 49,681,446 47,081,601

Notes Receivables 18,362 34,615

Rediscounts on Receivables (1,199,131) (1,205,643)

Doubtful Trade Receivables 2,703,803 2,605,191

Provision for Doubtful Trade Receivables (2,703,803) (2,605,191)

Credit Card Receivables 593,091 587,001

Trade Receivables from Related Parties 1,581,326 2,923,110

Income Accruals* 9,767,665 9,346,050

Total 60,442,759 58,766,734

(*) The total amount of income accruals is arising from ongoing patient cares.

The interest rate used for discounting receivables is 17% Average maturity for credit card

receivables is 40 days.

Transactions related to doubtful trade receivables with-in the period are as follows;

Doubtful Trade Receivables 30 June 2018

31 December 2017

Beginning of the Period 2,605,191 903,571

Worthless Receivables, Collections/Cancelation (300,910) (698,039)

Additions with-in the Period 399,522 2,399,659

End of the Period 2,703,803 2,605,191

Details of trade receivables from Social Security Institution (SSI) and others are as follows;

Trade Receivables/Institution 30 June 2018 31 December 2017

Amount % Amount %

Receivables from SSI* 41,596,425 69 41,377,716 71

Other Receivables 18,846,334 31 17,389,018 29

Total 60,442,759 100 58,766,734 100

(*) Major customer of The Group is Social Security Institution (SSI).

The summary of trade payables as of end of the periods is as follows;

30 June 2018

31 December 2017

Trade Payables 15,481,873 13,276,061

Notes Payables* 21,138,907 17,921,683

Rediscount on Payables (976,492) (1,030,920)

Other Trade Payables 279,775 496,188

Trade Payables to Related Parties 4,339,895 949,561

Expense Accruals 313,961 343,975

Total 40,577,919 31,956,548

The interest rate used for discounting payables is 17%.

(*) The amount of TRY 6,137,035 included in notes payables is composed of notes with 31 July

2018 maturity related to Akay Hospital (31 December 2017: TRY 6,137,035).

LOKMAN HEKİM ENGÜRÜSAĞ SAĞLIK, TURİZM, EĞİTİM HİZMETLERİ VE İNŞAAT TAAHÜT A.Ş.

Notes to the Consolidated Financial Statements for the Period 1 January – 30 June 2018

(Amounts are expressed in Turkish Lira (TRY) unless otherwise stated.)

25

7. OTHER RECEIVABLES AND OTHER PAYABLES

The Group’s other short-term receivables are as follows;

Other Short-Term Receivables

30 June 2018

31 December 2017

Deposits and Guarantees Given 60,793 55,284

Other Receivables 9,396 229,528

Total 70,189 284,812

Other long-term receivables are consist of deposits and guarantees given;

Other Long-Term Receivables

30 June

2018

31 December

2017

Deposits and Guarantees Given 254,941 112,177

Total 254,941 112,177

Other payables of The Group are short-term;

Other Payables

30 June 2018

31 December 2017

Due to Shareholders 5,040 4,300

Other Payables 94,660 179,826

Total 99,700 184,126

8. INVENTORIES

30 June 2018

31 December 2017

Medical Inventories 13,293,221 8,118,840

Feed Stocks 3,761,913 4,232,704

Other Stocks 574,918 662,107

Total 17,630,052 13,013,651

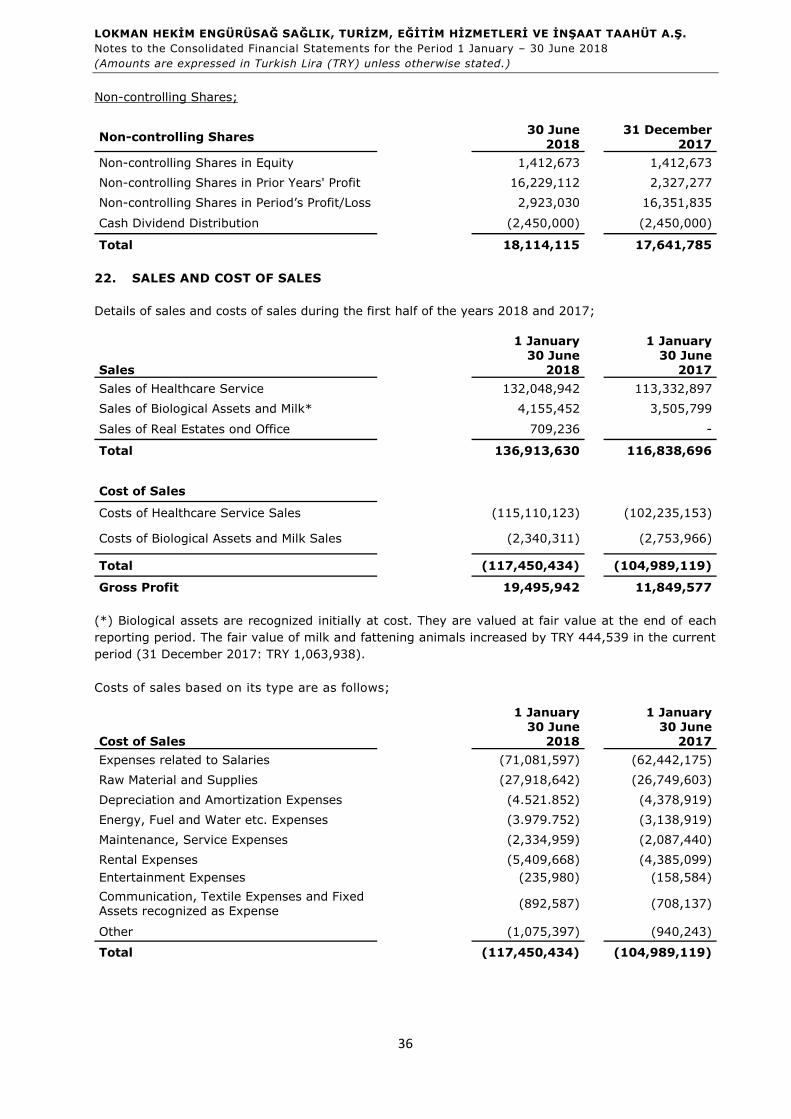

9. BIOLOGICAL ASSETS

Biological Assets

30 June 2018

31 December 2017

Book Value 15,343,729 12,927,962

Changes in the Fair Value 833,238 1,063,938

Total 16,176,967 13,991,900

Biological assets are recognized initially at cost. They are valued at fair value at the end of each

reporting period. The fair value of milk and fattening animals increased by TRY 444,539 in the

current period (31 December 2017: TRY 1,063,938).

As of 30 June 2018, the number of biological assets of the company is 1,406 (31 December 2017:

1,555).

The total amount of insurance on biological assets is TRY 1,867,500

(31 December 2017: TRY 4,008,000)

LOKMAN HEKİM ENGÜRÜSAĞ SAĞLIK, TURİZM, EĞİTİM HİZMETLERİ VE İNŞAAT TAAHÜT A.Ş.

Notes to the Consolidated Financial Statements for the Period 1 January – 30 June 2018

(Amounts are expressed in Turkish Lira (TRY) unless otherwise stated.)

26

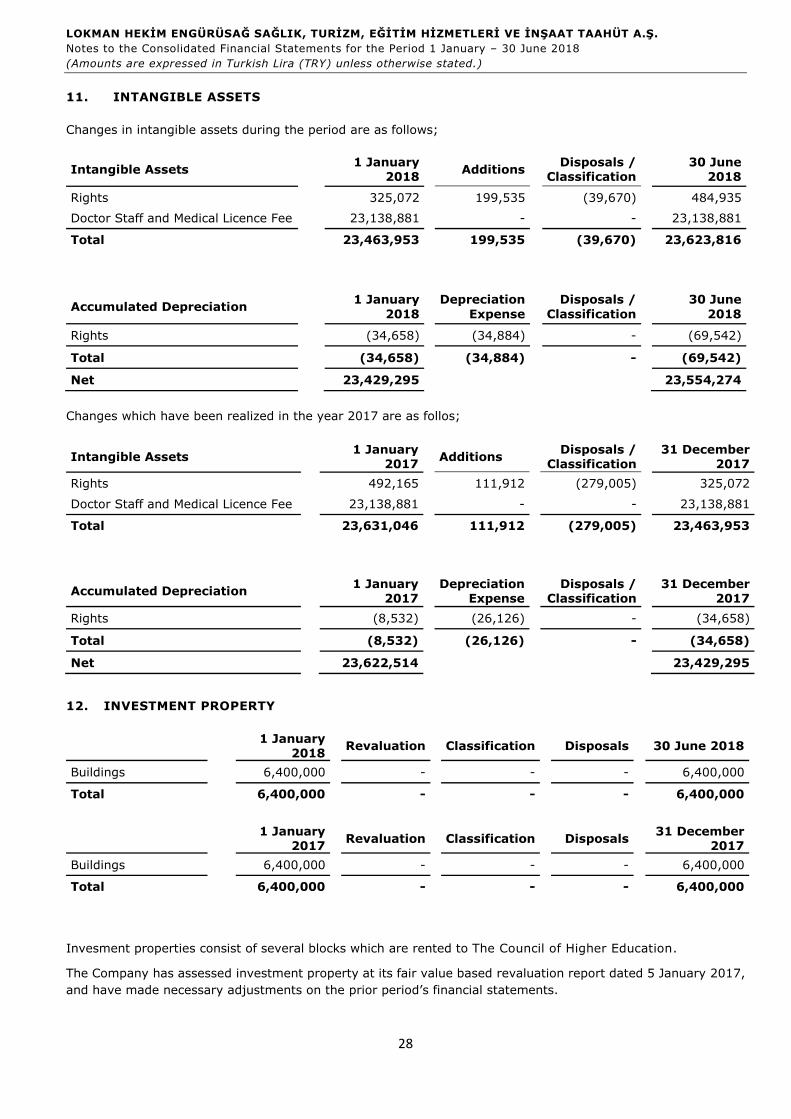

10. TANGIBLE ASSETS

Changes in the tangible assets during first half of the year are as follows;

Tangible Assets

1 January

2018 Additions

Classification

Disposals

30 June

2018

Lands 11,262,750 - - - 11,262,750

Buildings 33,675,197 350,130 - - 34,025,327

Machinery, Equipment and Installations 18,847,421 2,393,938 - (1,622) 21,239,737

Vehicles 724,771 - - - 724,771

Furniture and Fittings 29,474,476 1,058,882 - (45,598) 30,487,760

Assets Acquired Through Financial Leases 19,516,618 - - - 19,516,618

Special Costs 8,460,935 521,336 - - 8,982,271

Other Tangible Assets 2,039,125 17,923 - - 2,057,048

Construction in Progress 7,003,502 4,251,074 - - 11,254,576

Total 131,004,795 8,593,283 - (47,220) 139,550,858

Accumulated Depreciation

1 January

2018

Depreciation

Expense Classification

Disposals

30 June

2018

Buildings (697,911) (355,107) - - (1,053,018)

Machinery, Equipment and Installations (8,224,436) (884,082) - - (9,108,518)

Vehicles (328,159) (58,204) - - (386,363)

Furniture and Fittings (18,171,662) (1,795,533) - 41,040 (19,926,155)

Assets Acquired Through Financial Leases (9,182,479) (794,260) - - (9,976,739)

Special Costs (3,622,887) (537,168) - - (4,160,055)

Other Tangible Assets (778,352) (129,525) - - (907,877)

Total (41,005,886) (4,553,879) - 41,040 (45,518,725)

Net 89,998,909 94,032,133

LOKMAN HEKİM ENGÜRÜSAĞ SAĞLIK, TURİZM, EĞİTİM HİZMETLERİ VE İNŞAAT TAAHÜT A.Ş.

Notes to the Consolidated Financial Statements for the Period 1 January – 30 June 2018

(Amounts are expressed in Turkish Lira (TRY) unless otherwise stated.)

27

Changes in the tangible assets with-in the 2017 are as follows;

Tangible Assets

1 January 2017

Additions

Classification

Disposals

31 December 2017

Lands 6,343,750 1,194,000 3,725,000 - 11,262,750

Buildings 36,986,250 413,947 (3,725,000) - 33,675,197

Machinery, Equipment and Installations 15,707,538 3,147,883 - (8,000) 18,847,421

Vehicles 602,315 244,660 - (122,204) 724,771

Furniture and Fittings 26,979,087 2,503,938 - (8,549) 29,474,476

Assets Acquired Through Financial Leases 14,709,430 4,807,188 - - 19,516,618

Special Costs 6,743,670 1,717,265 - - 8,460,935

Other Tangible Assets 2,001,628 37,497 - - 2,039,125

Construction in Progress 406,268 6,597,234 - - 7,003,502

Total 110,479,936 20,663,612 - (138,753) 131,004,795

Accumulated Depreciation

1 January 2017

Depreciation Expense

Classification

Disposals

31 December 2017

Buildings - (697,911) - - (697,911)

Machinery, Equipment and Installations (6,704,623) (1,527,413) - 7,600 (8,224,436)

Vehicles (341,357) (80,319) - 93,517 (328,159)

Furniture and Fittings (14,528,996) (3,642,881) - 215 (18,171,662)

Assets Acquired Through Financial Leases (7,613,878) (1,568,601) - - (9,182,479)

Special Costs (2,410,544) (1,212,343) - - (3,622,887)

Other Tangible Assets (515,622) (262,730) - - (778,352)

Total (32,115,020) (8,992,198) - 101,332 (41,005,886)

Net 78,364,916 89,998,909

The total insurance amount on tangible assets is TRY 203,755,000 (31 December 2017: TRY 136,030,500).