© 2018 Experian Information Solutions, Inc. All rights reserved. Experian and the marks used herein are service marks or registered trademarks of Experian Information Solutions, Inc. Other product and company names mentioned herein are the trademarks of their respective owners. No part of this copyrighted work may be reproduced, modified, or distributed in any form or manner without the prior written permission of Experian. Experian Public.

www.experian.com/automotive

State of the Automotive Finance Market

A look at loans and leases in Q4 2017Presented by: Melinda Zabritski | Sr. Director, Financial Solutions

2 © Experian

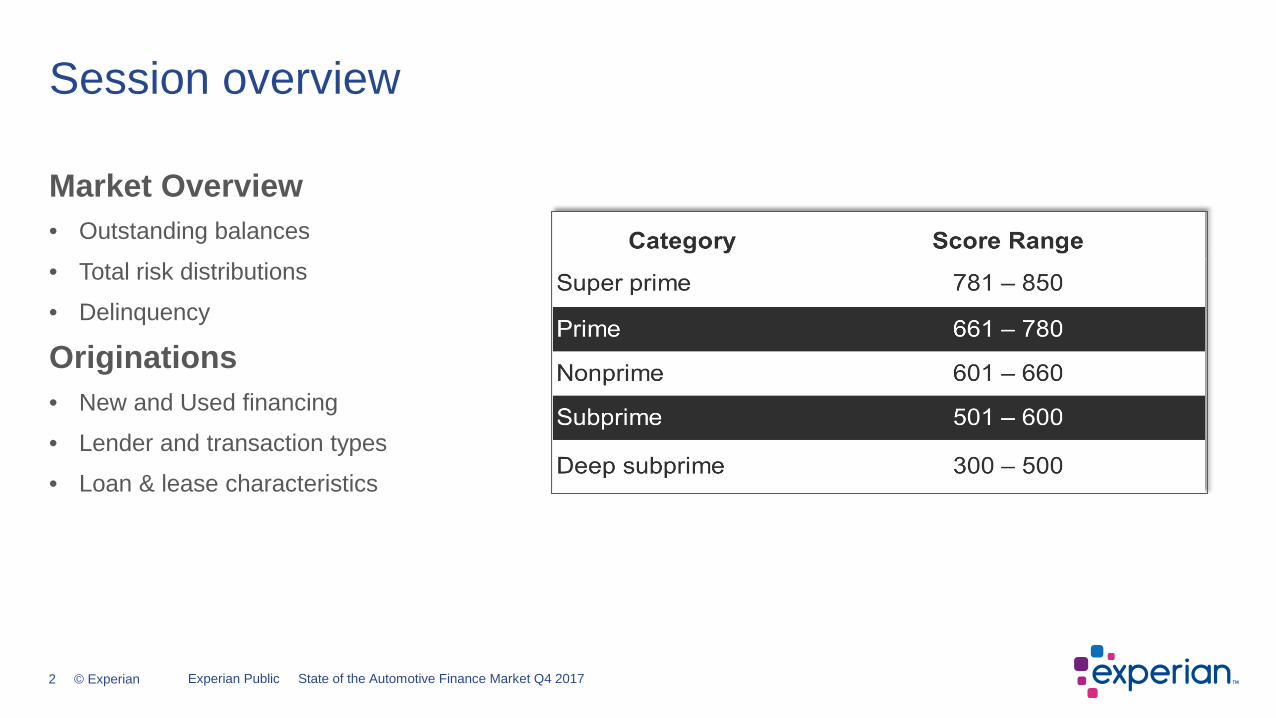

Market Overview• Outstanding balances

• Total risk distributions

• Delinquency

Originations• New and Used financing

• Lender and transaction types

• Loan & lease characteristics

Session overview

Experian Public State of the Automotive Finance Market Q4 2017

3 © Experian

A review of all open automotive loans & leases

Overall Automotive Finance Market

Experian Public State of the Automotive Finance Market Q4 2017

4 © Experian

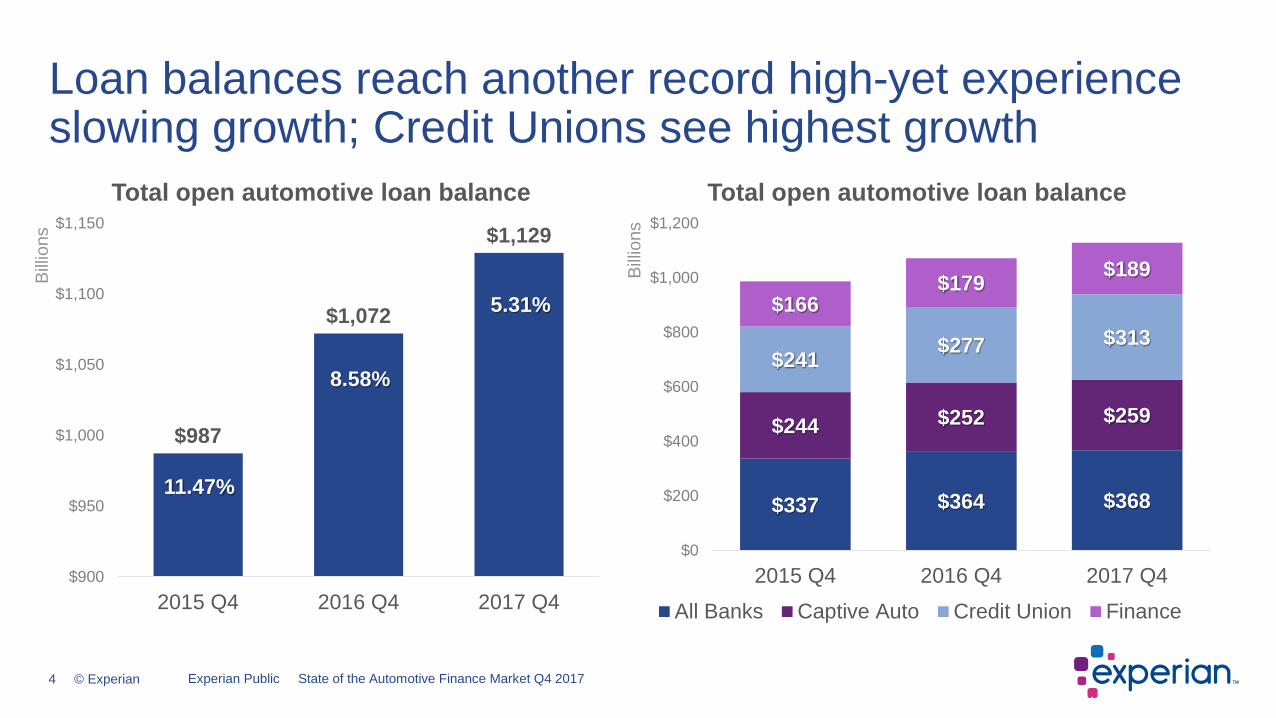

$987

$1,072

$1,129

$900

$950

$1,000

$1,050

$1,100

$1,150

2015 Q4 2016 Q4 2017 Q4

Bill

ions

Total open automotive loan balance

Loan balances reach another record high-yet experience slowing growth; Credit Unions see highest growth

Source: Experian-Oliver Wyman Market Intelligence Reports

$337 $364 $368

$244 $252 $259

$241 $277 $313$166

$179 $189

$0

$200

$400

$600

$800

$1,000

$1,200

2015 Q4 2016 Q4 2017 Q4

Bill

ions

Total open automotive loan balance

All Banks Captive Auto Credit Union Finance

Experian Public State of the Automotive Finance Market Q4 2017

11.47%

8.58%

5.31%

5 © Experian

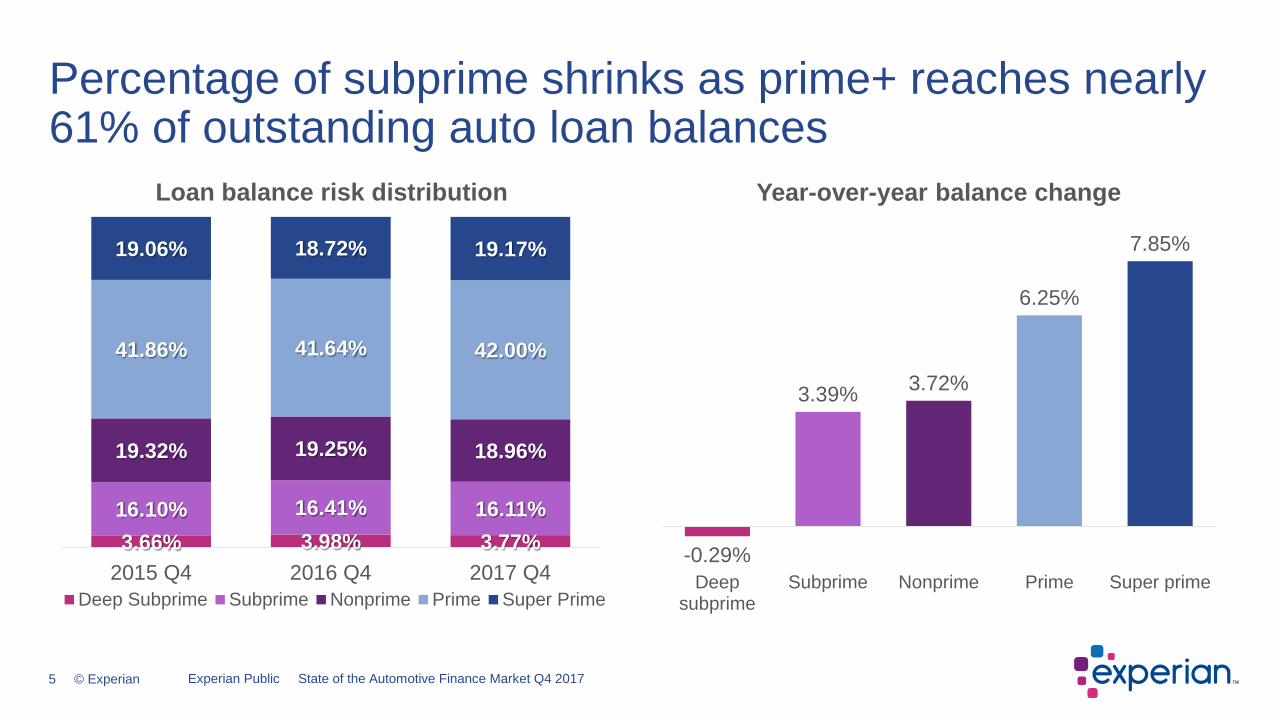

3.66% 3.98% 3.77%16.10% 16.41% 16.11%

19.32% 19.25% 18.96%

41.86% 41.64% 42.00%

19.06% 18.72% 19.17%

2015 Q4 2016 Q4 2017 Q4

Loan balance risk distribution

Deep Subprime Subprime Nonprime Prime Super Prime

Percentage of subprime shrinks as prime+ reaches nearly 61% of outstanding auto loan balances

-0.29%

3.39% 3.72%

6.25%

7.85%

Deepsubprime

Subprime Nonprime Prime Super prime

Year-over-year balance change

Experian Public State of the Automotive Finance Market Q4 2017

6 © Experian

1.99% 2.32%1.43%

4.65%

2.44%1.82%

2.39%1.34%

4.48%

2.36%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

Bank Captive Credit Union Finance Total

% of loans & leases 30 dpd2016 Q4 2017 Q4

30 day delinquency rates are improving

Source: Experian-Oliver Wyman Market Intelligence Reports

1.81%2.85%

1.28%

5.21%

2.48%1.66%

2.92%

1.17%

5.12%

2.39%

0.0%

2.0%

4.0%

6.0%

Bank Captive Credit Union Finance Total

% of loan balances 30 dpd2016 Q4 2017 Q4

Experian Public State of the Automotive Finance Market Q4 2017

7 © Experian

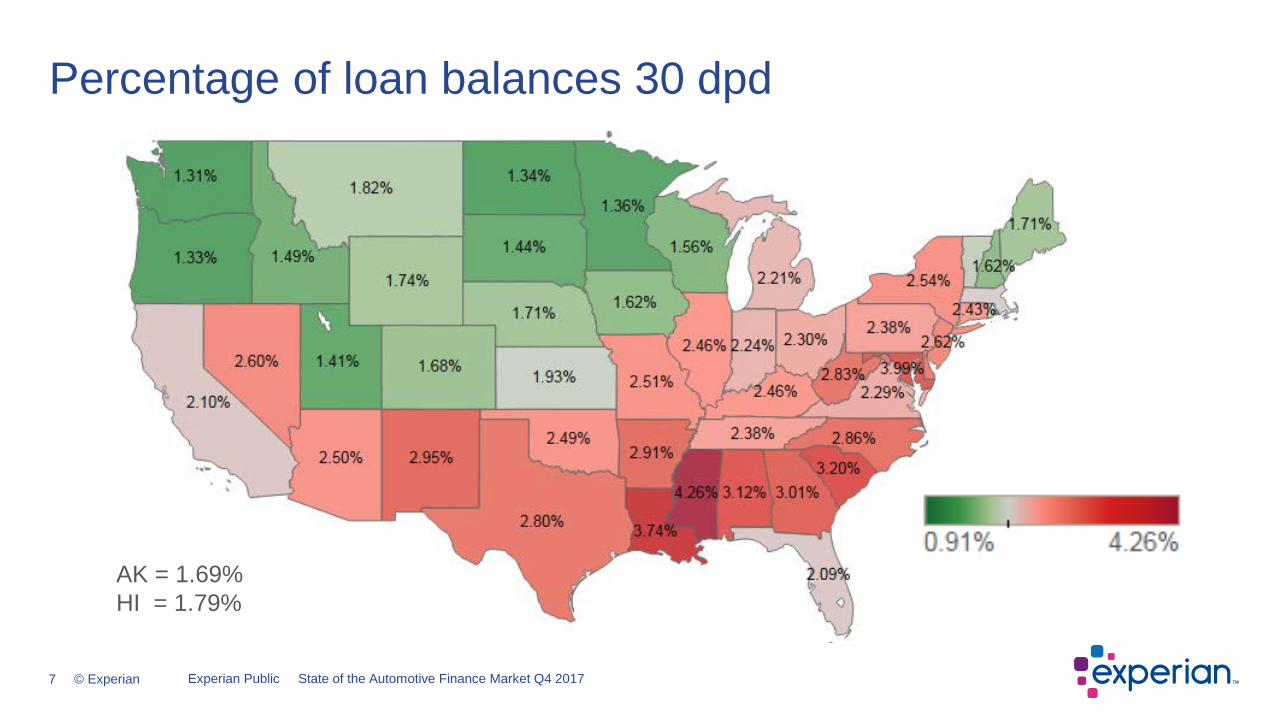

Percentage of loan balances 30 dpd

Experian Public State of the Automotive Finance Market Q4 2017

AK = 1.69%HI = 1.79%

8 © Experian

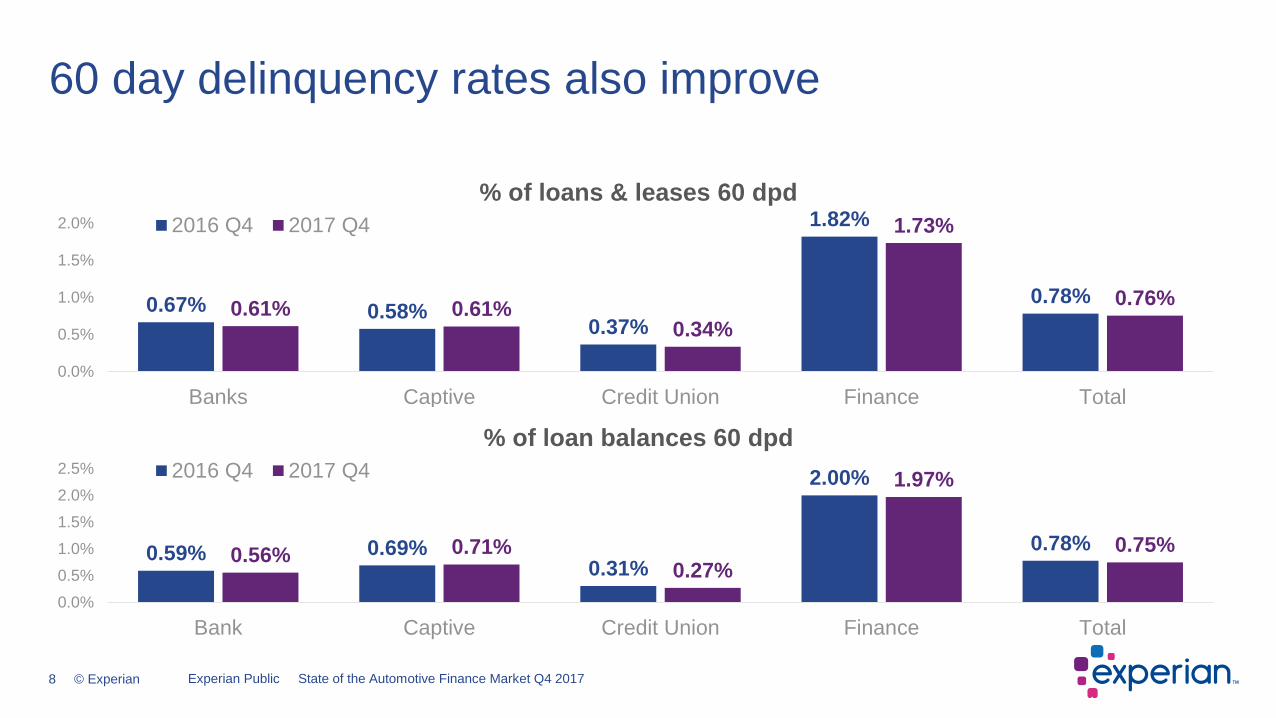

0.67% 0.58%0.37%

1.82%

0.78%0.61% 0.61%0.34%

1.73%

0.76%

0.0%

0.5%

1.0%

1.5%

2.0%

Banks Captive Credit Union Finance Total

% of loans & leases 60 dpd2016 Q4 2017 Q4

60 day delinquency rates also improve

Source: Experian-Oliver Wyman Market Intelligence Reports

0.59% 0.69%0.31%

2.00%

0.78%0.56% 0.71%0.27%

1.97%

0.75%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

Bank Captive Credit Union Finance Total

% of loan balances 60 dpd2016 Q4 2017 Q4

Experian Public State of the Automotive Finance Market Q4 2017

9 © Experian

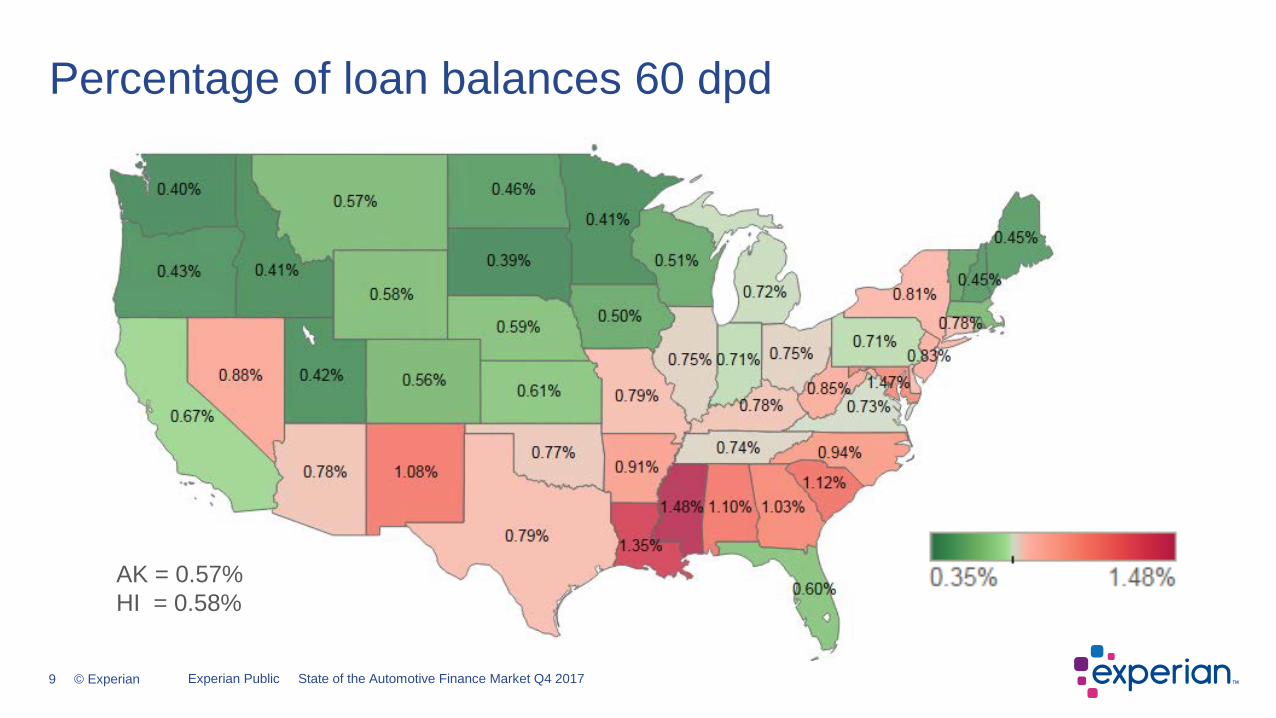

Percentage of loan balances 60 dpd

Experian Public State of the Automotive Finance Market Q4 2017

AK = 0.57%HI = 0.58%

10 © Experian

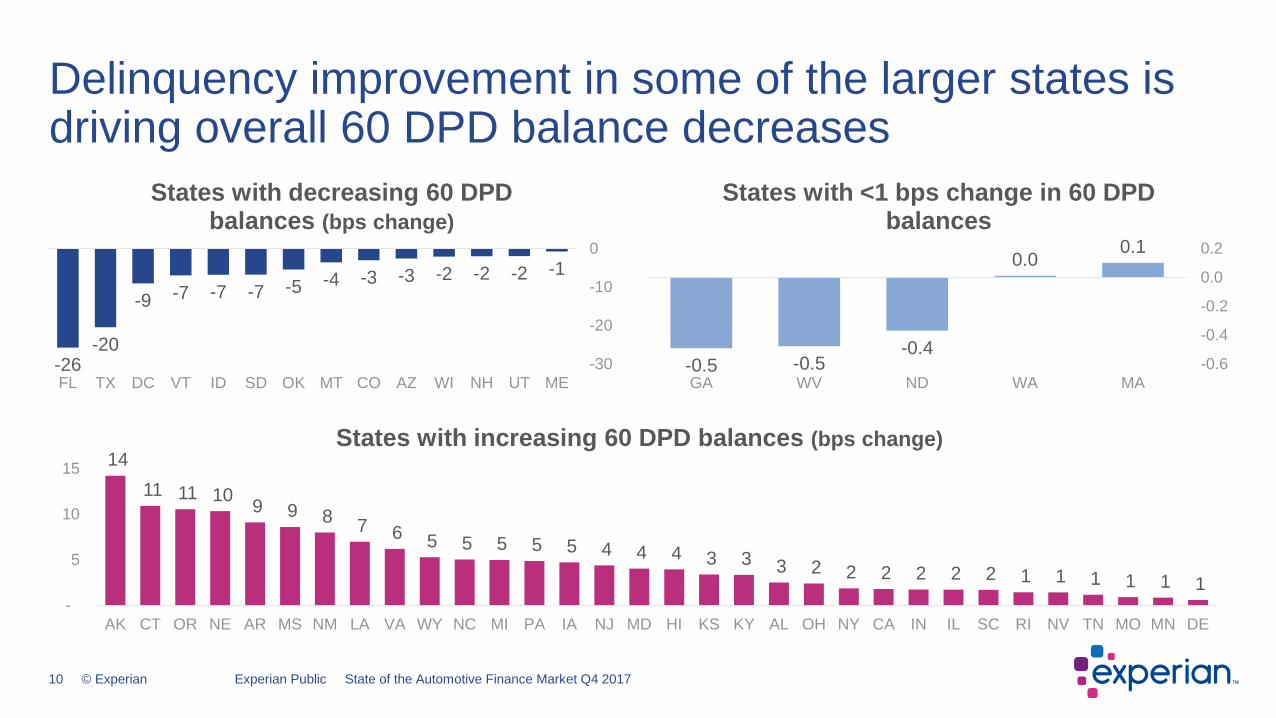

Delinquency improvement in some of the larger states is driving overall 60 DPD balance decreases

Experian Public State of the Automotive Finance Market Q4 2017

14 11 11 10 9 9 8 7 6 5 5 5 5 5 4 4 4 3 3 3 2 2 2 2 2 2 1 1 1 1 1 1

-

5

10

15

AK CT OR NE AR MS NM LA VA WY NC MI PA IA NJ MD HI KS KY AL OH NY CA IN IL SC RI NV TN MO MN DE

States with increasing 60 DPD balances (bps change)

-1-2-2-2-3-3-4-5-7-7-7-9

-20-26 -30

-20

-10

0

MEUTNHWIAZCOMTOKSDIDVTDCTXFL

States with decreasing 60 DPD balances (bps change)

0.10.0

-0.4-0.5-0.5 -0.6

-0.4

-0.2

0.0

0.2

MAWANDWVGA

States with <1 bps change in 60 DPD balances

11 © Experian

Trends in automotive loan and lease originations

Originations in Q4 2017

Experian Public State of the Automotive Finance Market Q4 2017

12 © Experian

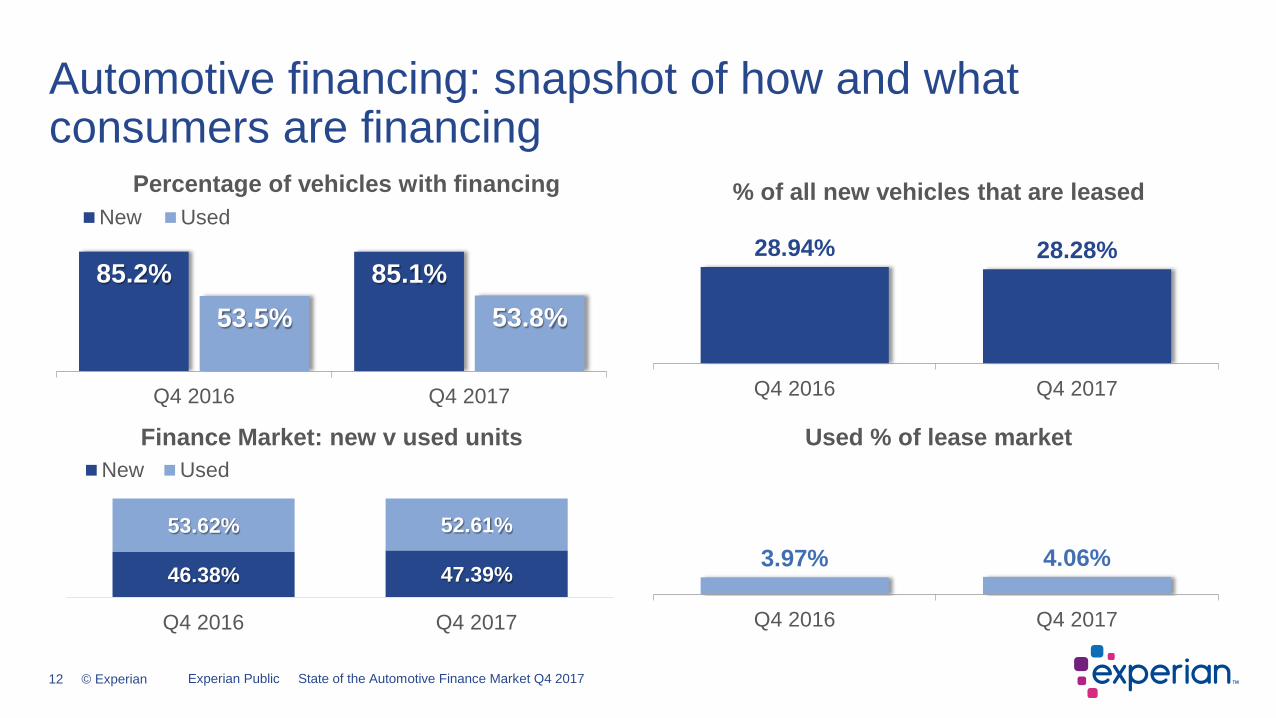

85.2% 85.1%53.5% 53.8%

Q4 2016 Q4 2017

Percentage of vehicles with financingNew Used

Automotive financing: snapshot of how and what consumers are financing

28.94% 28.28%

Q4 2016 Q4 2017

% of all new vehicles that are leased

46.38% 47.39%

53.62% 52.61%

Q4 2016 Q4 2017

Finance Market: new v used units New Used

3.97% 4.06%

Q4 2016 Q4 2017

Used % of lease market

Experian Public State of the Automotive Finance Market Q4 2017

13 © Experian

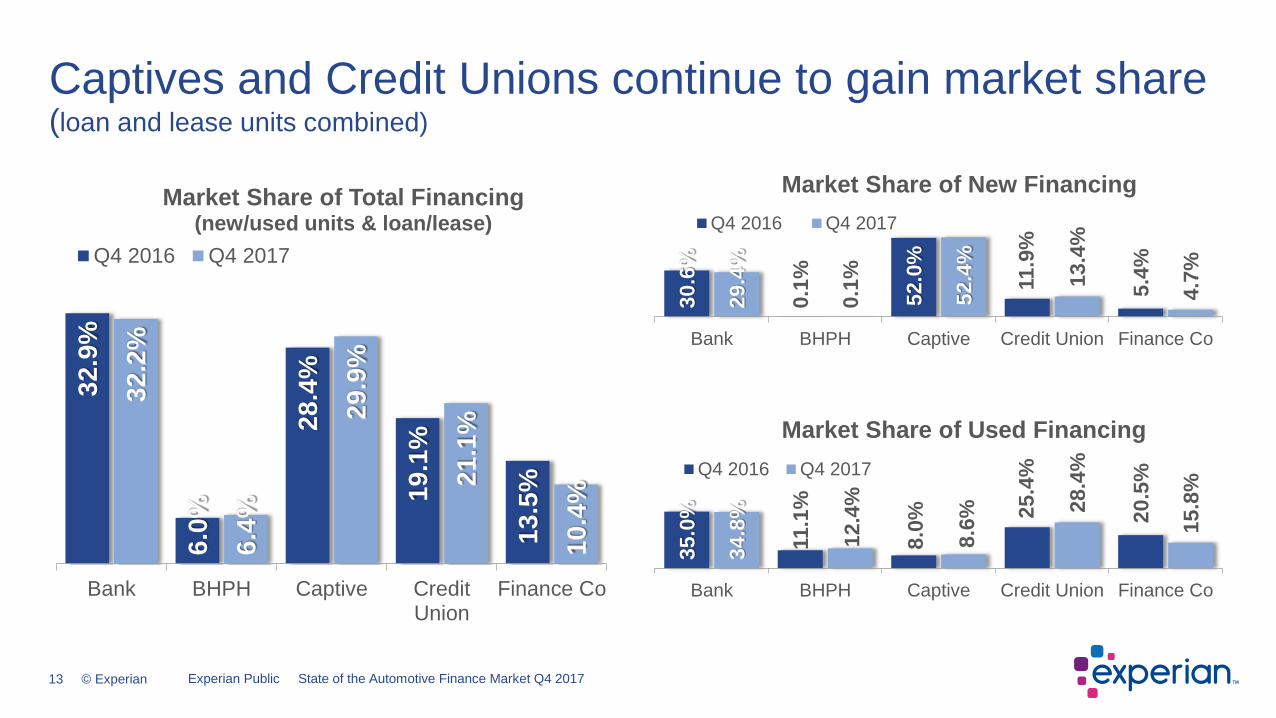

32.9

%

6.0%

28.4

%

19.1

%

13.5

%

32.2

%

6.4%

29.9

%

21.1

%

10.4

%Bank BHPH Captive Credit

UnionFinance Co

Market Share of Total Financing(new/used units & loan/lease)

Q4 2016 Q4 2017

Captives and Credit Unions continue to gain market share (loan and lease units combined)

30.6

%

0.1%

52.0

%

11.9

%

5.4%

29.4

%

0.1% 52.4

%

13.4

%

4.7%

Bank BHPH Captive Credit Union Finance Co

Market Share of New FinancingQ4 2016 Q4 2017

35.0

%

11.1

%

8.0% 25

.4%

20.5

%

34.8

%

12.4

%

8.6%

28.4

%

15.8

%

Bank BHPH Captive Credit Union Finance Co

Market Share of Used FinancingQ4 2016 Q4 2017

Experian Public State of the Automotive Finance Market Q4 2017

14 © Experian

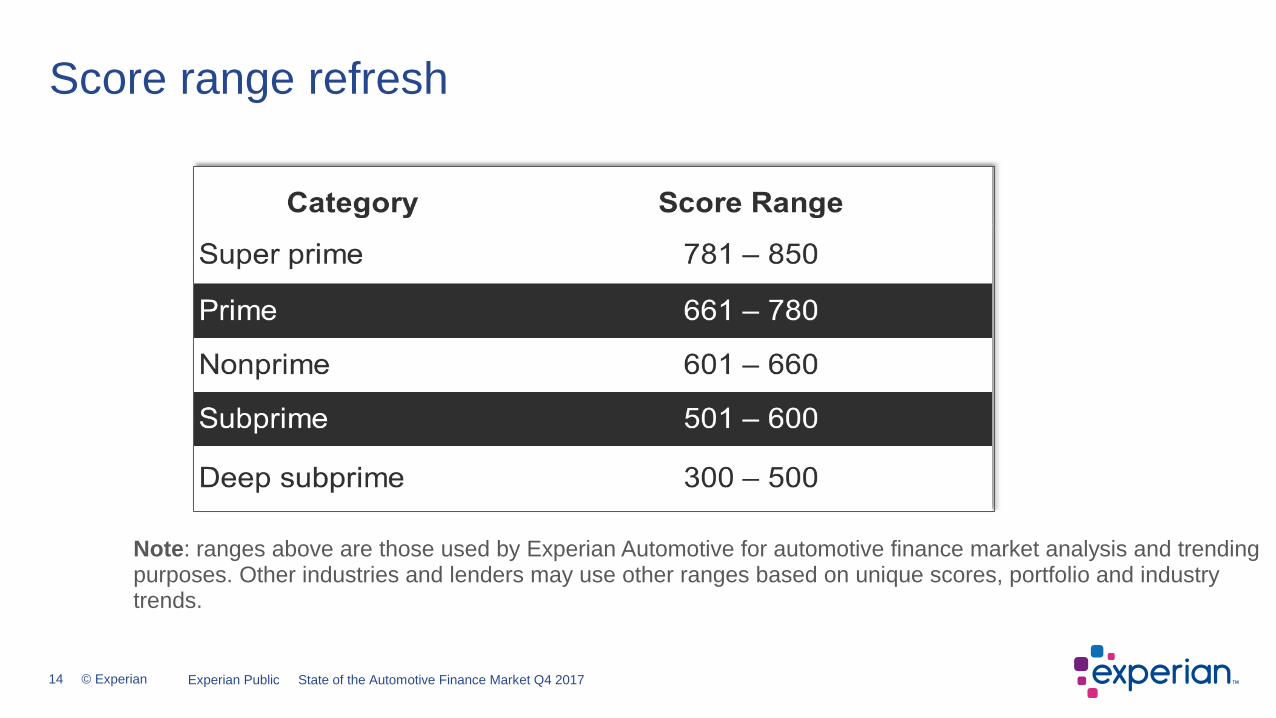

Score range refresh

Note: ranges above are those used by Experian Automotive for automotive finance market analysis and trending purposes. Other industries and lenders may use other ranges based on unique scores, portfolio and industry trends.

Experian Public State of the Automotive Finance Market Q4 2017

15 © Experian

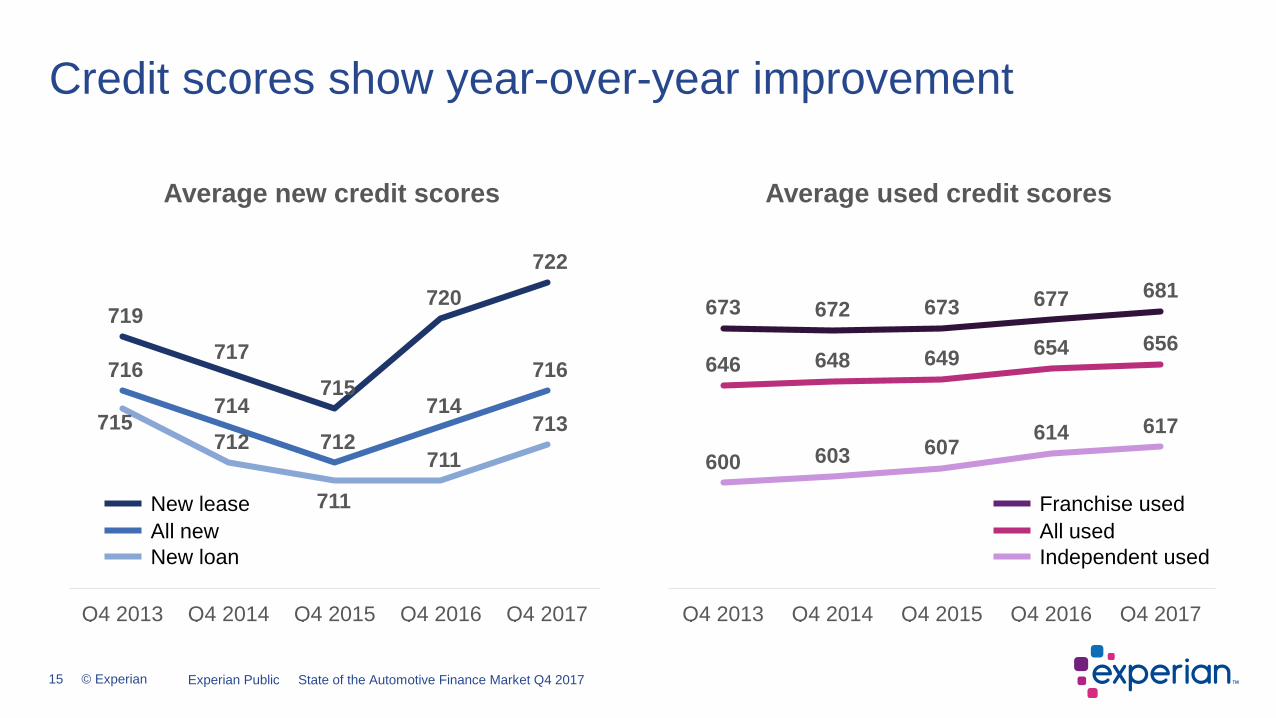

Credit scores show year-over-year improvement

646 648 649 654 656673 672 673 677 681

600 603 607614 617

Q4 2013 Q4 2014 Q4 2015 Q4 2016 Q4 2017

Average used credit scores

Franchise usedAll usedIndependent used

New leaseAll newNew loan

Experian Public State of the Automotive Finance Market Q4 2017

715 712

711

711 713

716 714

712 714

716

719 717

715

720 722

Q4 2013 Q4 2014 Q4 2015 Q4 2016 Q4 2017

Average new credit scores

16 © Experian

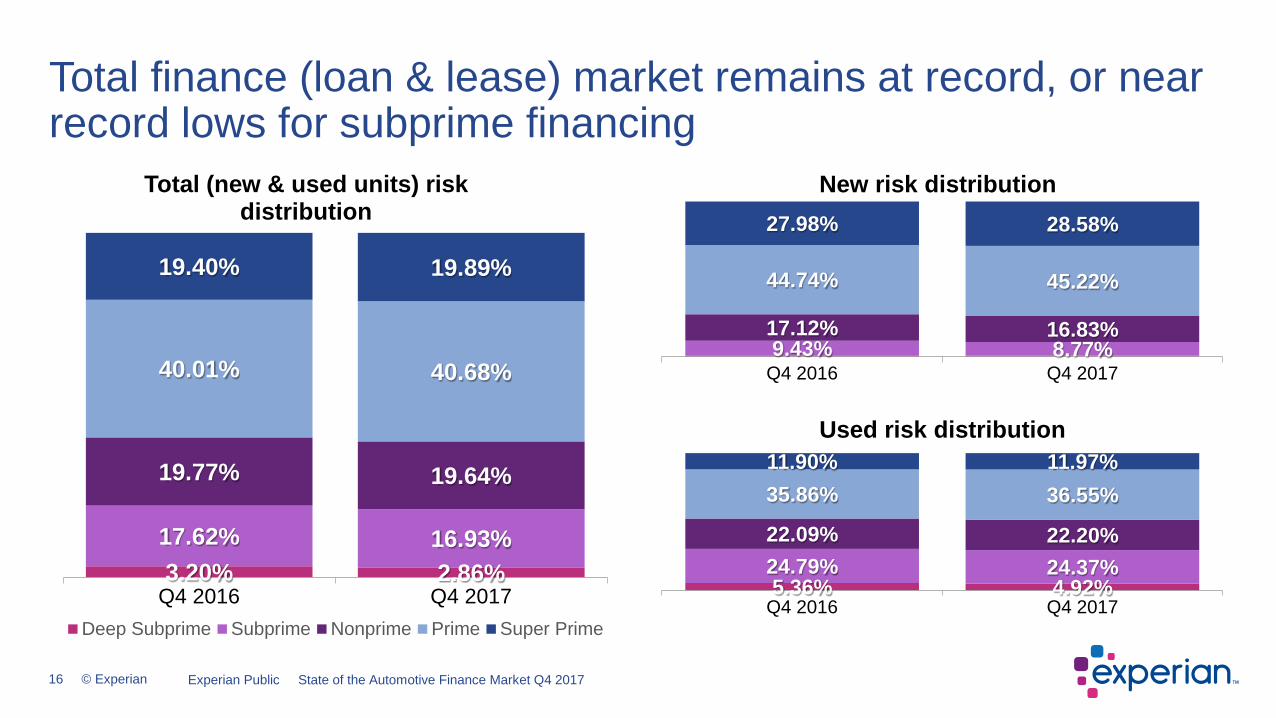

Total finance (loan & lease) market remains at record, or near record lows for subprime financing

9.43% 8.77%17.12% 16.83%

44.74% 45.22%

27.98% 28.58%

Q4 2016 Q4 2017

New risk distribution

5.36% 4.92%24.79% 24.37%22.09% 22.20%

35.86% 36.55%11.90% 11.97%

Q4 2016 Q4 2017

Used risk distribution

Experian Public State of the Automotive Finance Market Q4 2017

3.20% 2.86%17.62% 16.93%

19.77% 19.64%

40.01% 40.68%

19.40% 19.89%

Q4 2016 Q4 2017

Total (new & used units) risk distribution

Deep Subprime Subprime Nonprime Prime Super Prime

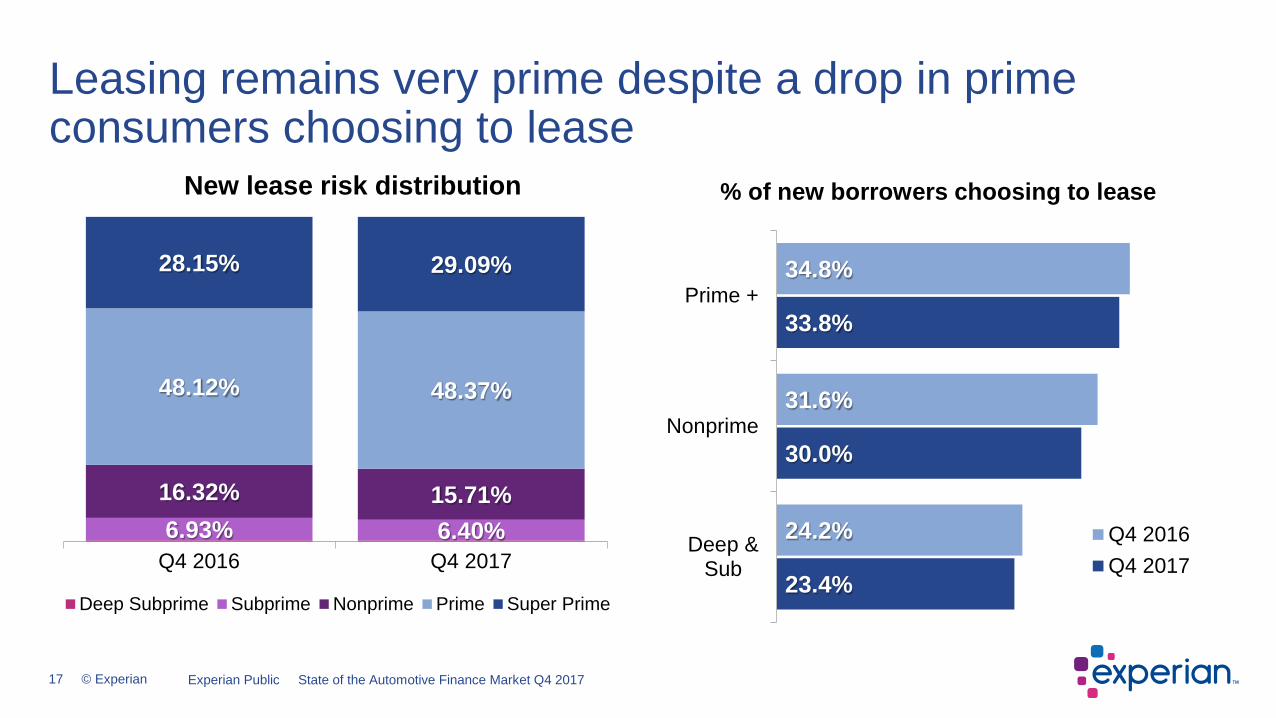

17 © Experian

6.93% 6.40%16.32% 15.71%

48.12% 48.37%

28.15% 29.09%

Q4 2016 Q4 2017

New lease risk distribution

Deep Subprime Subprime Nonprime Prime Super Prime

Leasing remains very prime despite a drop in prime consumers choosing to lease

23.4%

30.0%

33.8%

24.2%

31.6%

34.8%

Deep &Sub

Nonprime

Prime +

% of new borrowers choosing to lease

Q4 2016Q4 2017

Experian Public State of the Automotive Finance Market Q4 2017

18 © Experian

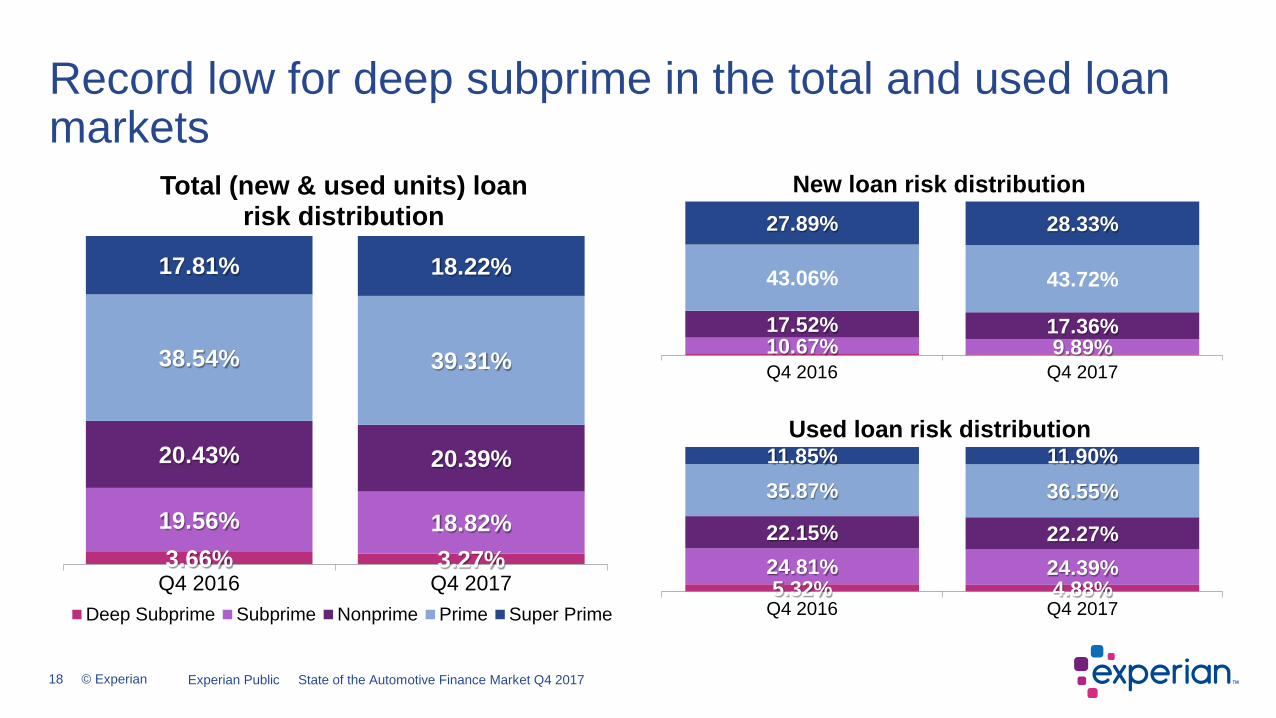

3.66% 3.27%19.56% 18.82%

20.43% 20.39%

38.54% 39.31%

17.81% 18.22%

Q4 2016 Q4 2017

Total (new & used units) loan risk distribution

Deep Subprime Subprime Nonprime Prime Super Prime

Record low for deep subprime in the total and used loan markets

10.67% 9.89%17.52% 17.36%

43.06% 43.72%

27.89% 28.33%

Q4 2016 Q4 2017

New loan risk distribution

5.32% 4.88%24.81% 24.39%22.15% 22.27%

35.87% 36.55%11.85% 11.90%

Q4 2016 Q4 2017

Used loan risk distribution

Experian Public State of the Automotive Finance Market Q4 2017

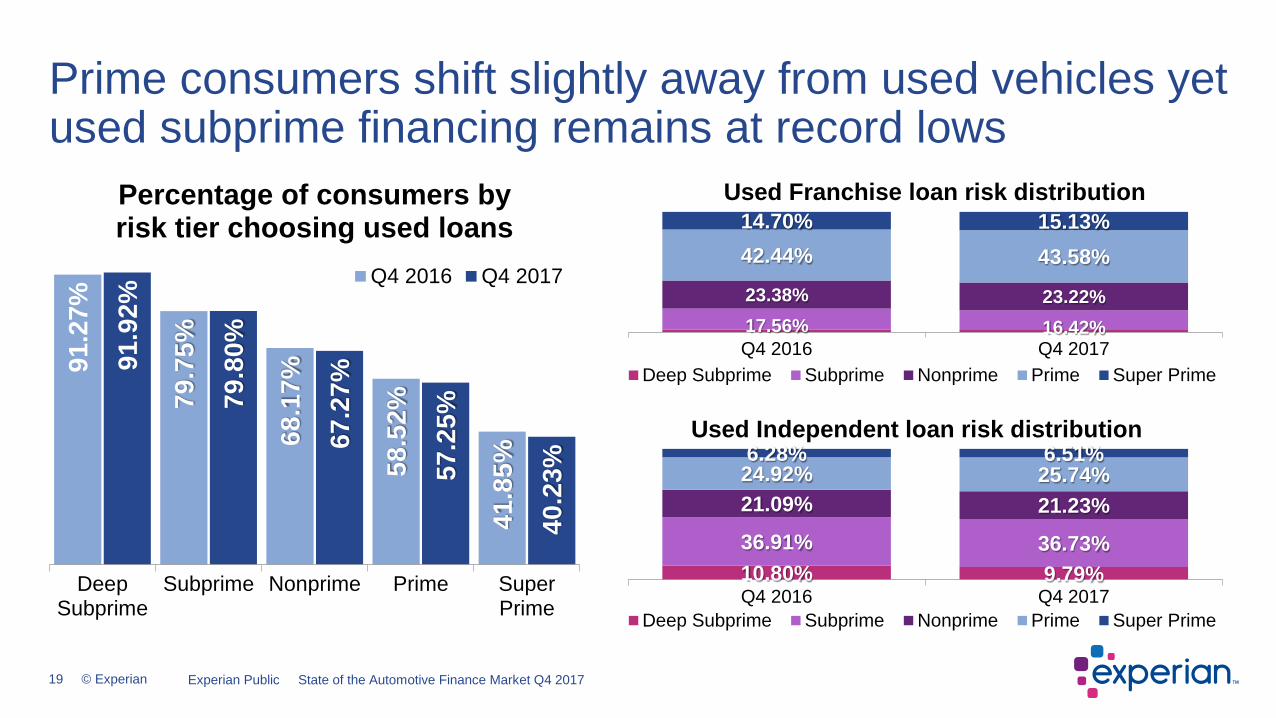

19 © Experian

91.2

7%

79.7

5%

68.1

7%

58.5

2%

41.8

5%

91.9

2%

79.8

0%

67.2

7%

57.2

5%

40.2

3%Deep

SubprimeSubprime Nonprime Prime Super

Prime

Percentage of consumers by risk tier choosing used loans

Q4 2016 Q4 2017

Prime consumers shift slightly away from used vehicles yet used subprime financing remains at record lows

17.56% 16.42%23.38% 23.22%

42.44% 43.58%14.70% 15.13%

Q4 2016 Q4 2017

Used Franchise loan risk distribution

Deep Subprime Subprime Nonprime Prime Super Prime

10.80% 9.79%36.91% 36.73%

21.09% 21.23%24.92% 25.74%6.28% 6.51%

Q4 2016 Q4 2017

Used Independent loan risk distribution

Deep Subprime Subprime Nonprime Prime Super Prime

Experian Public State of the Automotive Finance Market Q4 2017

20 © Experian

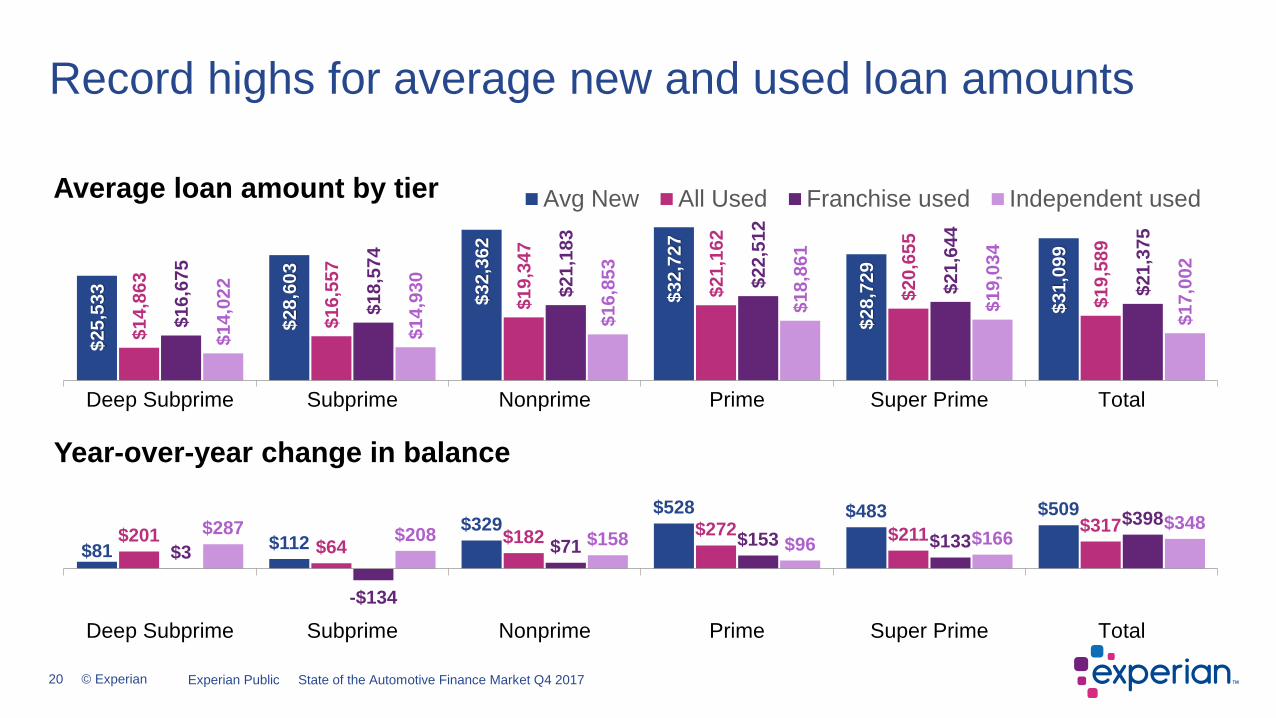

Record highs for average new and used loan amounts

$81 $112$329

$528 $483 $509$201 $64 $182 $272 $211 $317

$3

-$134

$71 $153 $133$398$287 $208 $158 $96 $166

$348

Deep Subprime Subprime Nonprime Prime Super Prime Total

Year-over-year change in balance

$25,

533

$28,

603

$32,

362

$32,

727

$28,

729

$31,

099

$14,

863

$16,

557

$19,

347

$21,

162

$20,

655

$19,

589

$16,

675

$18,

574

$21,

183

$22,

512

$21,

644

$21,

375

$14,

022

$14,

930

$16,

853

$18,

861

$19,

034

$17,

002

Deep Subprime Subprime Nonprime Prime Super Prime Total

Average loan amount by tier Avg New All Used Franchise used Independent used

Experian Public State of the Automotive Finance Market Q4 2017

21 © Experian

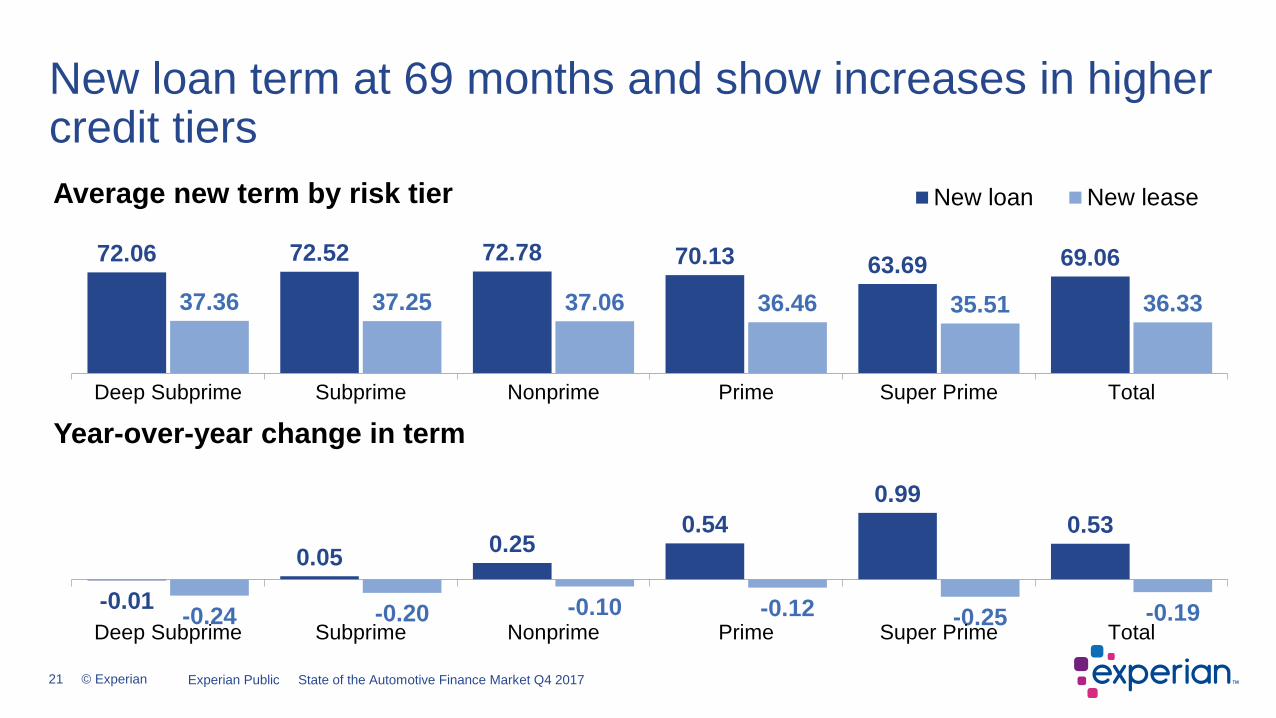

72.06 72.52 72.78 70.13 63.69 69.06

37.36 37.25 37.06 36.46 35.51 36.33

Deep Subprime Subprime Nonprime Prime Super Prime Total

Average new term by risk tier New loan New lease

New loan term at 69 months and show increases in higher credit tiers

-0.01

0.05 0.250.54

0.990.53

-0.24 -0.20 -0.10 -0.12 -0.25 -0.19Deep Subprime Subprime Nonprime Prime Super Prime Total

Year-over-year change in term

Experian Public State of the Automotive Finance Market Q4 2017

22 © Experian

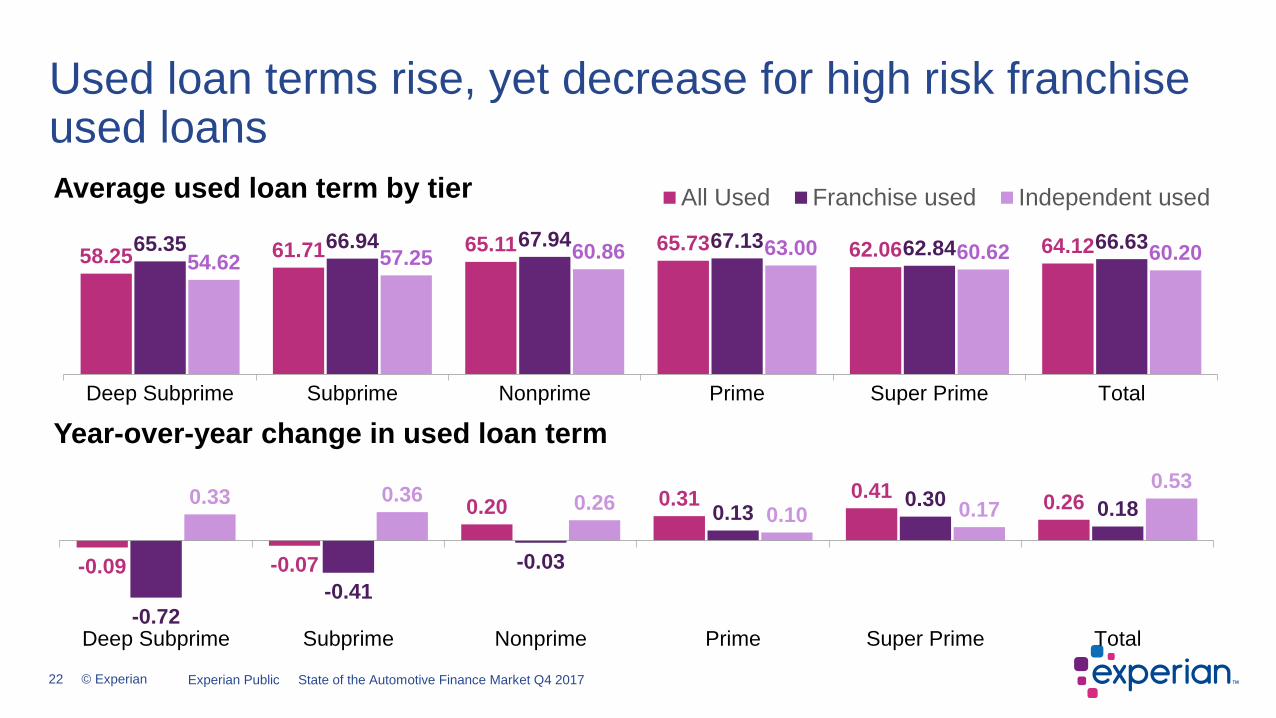

Used loan terms rise, yet decrease for high risk franchise used loans

58.25 61.71 65.11 65.73 62.06 64.1265.35 66.94 67.94 67.13 62.84 66.6354.62 57.25 60.86 63.00 60.62 60.20

Deep Subprime Subprime Nonprime Prime Super Prime Total

Average used loan term by tier All Used Franchise used Independent used

-0.09 -0.07

0.20 0.31 0.41 0.26

-0.72-0.41

-0.03

0.13 0.30 0.180.33 0.36 0.26 0.10 0.170.53

Deep Subprime Subprime Nonprime Prime Super Prime Total

Year-over-year change in used loan term

Experian Public State of the Automotive Finance Market Q4 2017

23 © Experian

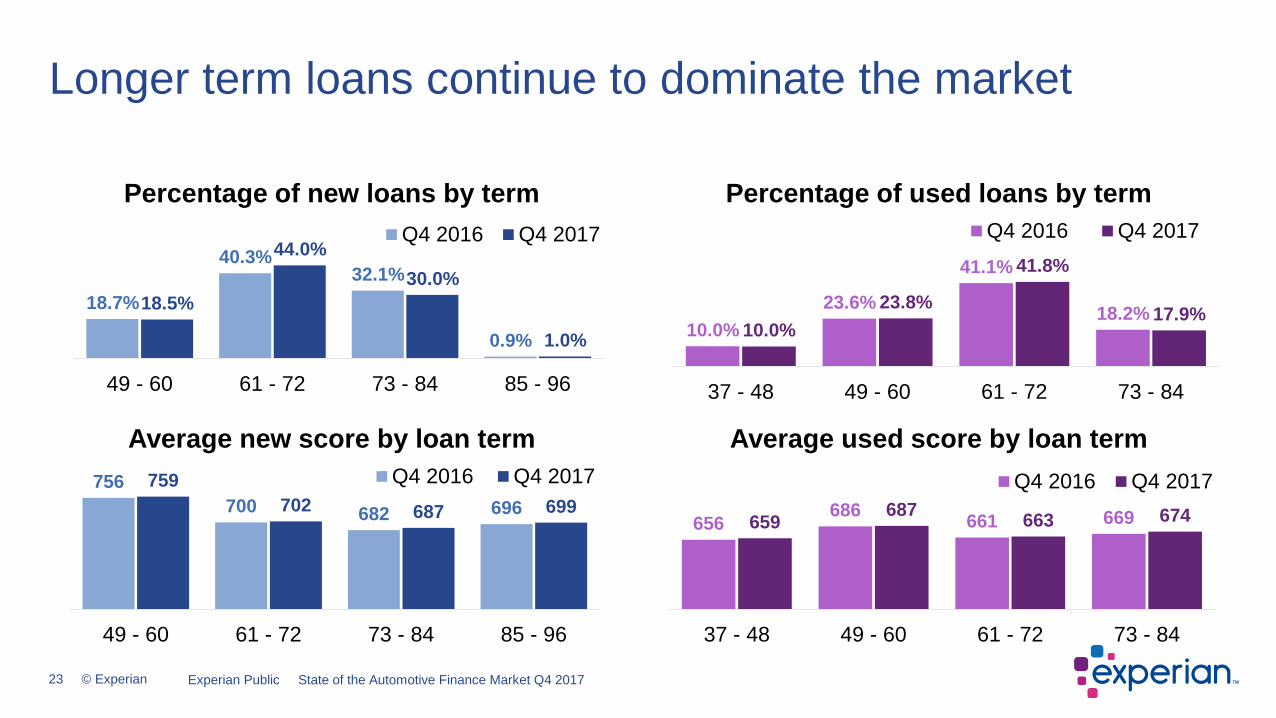

18.7%

40.3%32.1%

0.9%

18.5%

44.0%30.0%

1.0%

49 - 60 61 - 72 73 - 84 85 - 96

Percentage of new loans by termQ4 2016 Q4 2017

Longer term loans continue to dominate the market

10.0%23.6%

41.1%

18.2%10.0%

23.8%

41.8%

17.9%

37 - 48 49 - 60 61 - 72 73 - 84

Percentage of used loans by termQ4 2016 Q4 2017

756700 682 696

759702 687 699

49 - 60 61 - 72 73 - 84 85 - 96

Average new score by loan termQ4 2016 Q4 2017

656686 661 669659 687 663 674

37 - 48 49 - 60 61 - 72 73 - 84

Average used score by loan termQ4 2016 Q4 2017

Experian Public State of the Automotive Finance Market Q4 2017

24 © Experian

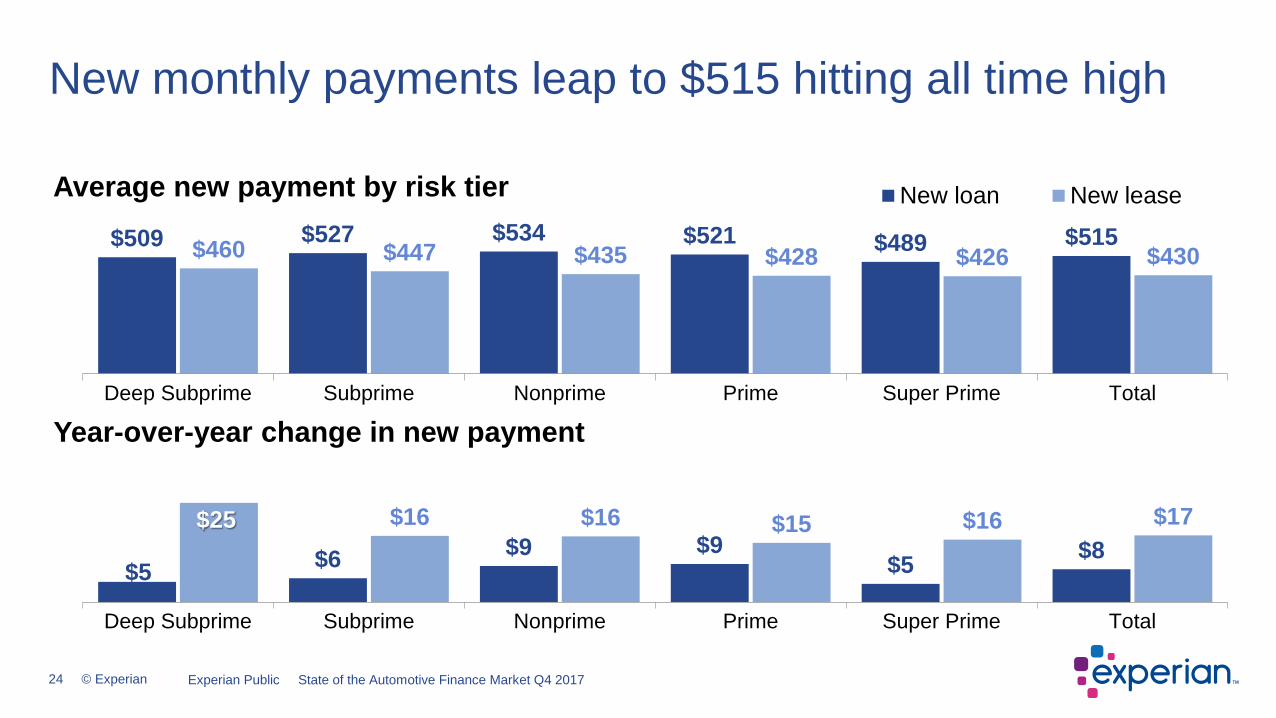

$509 $527 $534 $521 $489 $515$460 $447 $435 $428 $426 $430

Deep Subprime Subprime Nonprime Prime Super Prime Total

Average new payment by risk tier New loan New lease

New monthly payments leap to $515 hitting all time high

$5 $6 $9 $9$5 $8

$25 $16 $16 $15 $16 $17

Deep Subprime Subprime Nonprime Prime Super Prime Total

Year-over-year change in new payment

Experian Public State of the Automotive Finance Market Q4 2017

25 © Experian

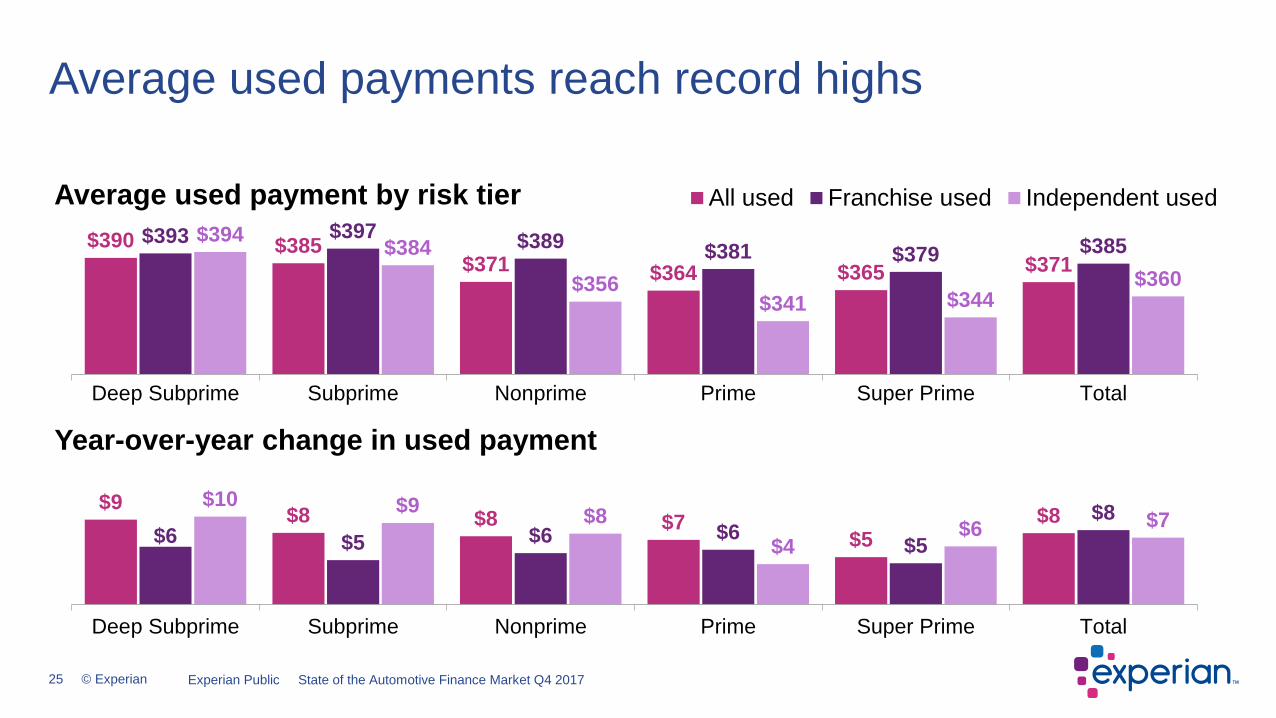

$390 $385$371 $364 $365 $371

$393 $397 $389 $381 $379 $385$394 $384$356

$341 $344$360

Deep Subprime Subprime Nonprime Prime Super Prime Total

Average used payment by risk tier All used Franchise used Independent used

Average used payments reach record highs

$9 $8 $8 $7$5

$8$6 $5 $6 $6 $5

$8$10 $9 $8$4

$6 $7

Deep Subprime Subprime Nonprime Prime Super Prime Total

Year-over-year change in used payment

Experian Public State of the Automotive Finance Market Q4 2017

26 © Experian

Rates rise across the entire automotive loan market13

.76%

10.9

8% 6.79

%

4.03

%

3.17

%

5.11

%

19.3

2%

16.2

7% 10.0

1%

5.48

%

3.80

% 8.84

%

18.1

0%

14.8

4% 9.24

%

5.28

%

3.76

% 7.68

%

20.2

8%

18.0

2% 11.8

3%

6.14

%

3.90

% 11.4

8%

Deep Subprime Subprime Nonprime Prime Super Prime Total

Average loan rates by tier Avg New All Used Franchise used Independent used

1728 36 43

543729

58 5239 41

3048

6646 40 41

1811

4257

37 46

11

Deep Subprime Subprime Nonprime Prime Super Prime Total

Year-over-year change (bps) in loan rate

Experian Public State of the Automotive Finance Market Q4 2017

27 © Experian

• Outstanding loan balances continue to set record highs

• Delinquency rates beginning to improve

• Leasing remains strong with over 28% of all new consumer vehicle sales

• Credit scores improve as lending continues to shift into more prime segments

• Deep subprime reaches record lows in used lending

• Loan amounts and payments reach record highs for both new and used vehicle financing

• While longer term loan remain the norm, there’s a decrease in 72-84 month loans in both new and used financing; while new sees slight growth in 85+

Summary

Experian Public State of the Automotive Finance Market Q4 2017