dr david beeton - international energy agency€¦ · dr david beeton operating agent task ......

TRANSCRIPT

Market deployment of

hybrid & electric vehicles

Dr David Beeton

Operating Agent Task XVIII

IEA Implementing Agreement Hybrid & Electric Vehicles

Technology Portfolio Issues: Smart Cities

Eskom Megawatt Park, Sandton, S.Africa

6th July 2011

Structure of Presentation

1. IEA Implementing Agreement on Hybrid & Electric Vehicles

3. EV Ecosystems: Preparing for Mass Adoption of EVs

2. EVs in a Smart City Context

4. Emerging Challenges in Creating EV Ecosystems

5. A Big Question for EVs in Smart Cities

Implementing Agreement

Hybrid & Electric Vehicles

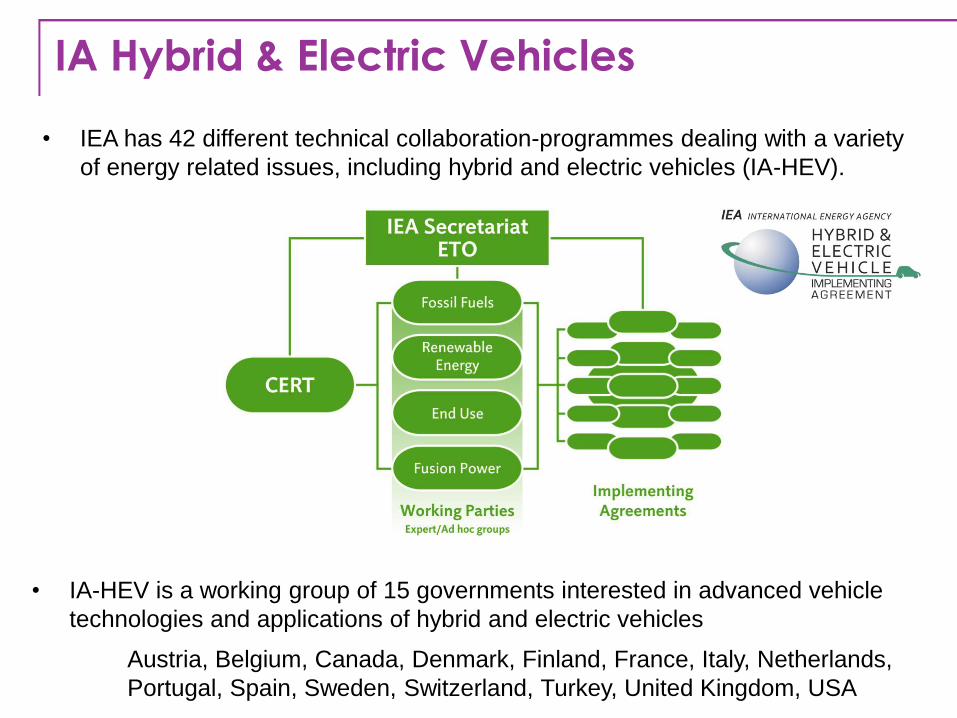

IA Hybrid & Electric Vehicles

• IEA has 42 different technical collaboration-programmes dealing with a variety

of energy related issues, including hybrid and electric vehicles (IA-HEV).

• IA-HEV is a working group of 15 governments interested in advanced vehicle

technologies and applications of hybrid and electric vehicles

Austria, Belgium, Canada, Denmark, Finland, France, Italy, Netherlands,

Portugal, Spain, Sweden, Switzerland, Turkey, United Kingdom, USA

IA-HEV Task Forces (1994-2011) • Information Exchange (Task I)

• Environment Issues of EVs and components (Task II)

• Infrastructure of electric vehicles (Task III)

• Batteries and super capacitors (Task V)

• Hybrid Vehicles (Task VII)

• Deployment Strategies (Task VIII)

• Clean City Vehicles (Task IX)

• Electrochemical Systems (Task X)

• Electric cycles (Task XI)

• Heavy-Duty Hybrid Vehicles (Task XII)

• Fuel Cell Vehicles (Task XIII)

• Market Deployment – Lessons learned (Task XIV)

• Plug-in Hybrid Electric Vehicles (Task XV)

• Technology Alternatives for buses (Task XVI)

• BEV system integration and optimization (Task XVII)

• EV Ecosystems (Task XVIII)

International cooperation

Creating EV

ecosystems

Advancing

technology &

manufacturing

Vehicle

trials

Infrastructure

pilots

Public

sector

Private

sector

Removing

barriers

to mass

adoption

Accelerating

early

market growth

Smart Cities

Business Models

Innovation

Skills

Mass Adoption

Immediate Challenges

North East England EV Programme

Smart Cities

For the first time in human history more

people live in cities than in rural areas

Over the next 20 years the urban

population will grow from 3.5 billion to

5.0 billion

The social, environmental and

economic challenges of this

transformation will shape the 21st

century.

Opportunity:

• Improve the lives of citizens

• Limit the impact on the

environment

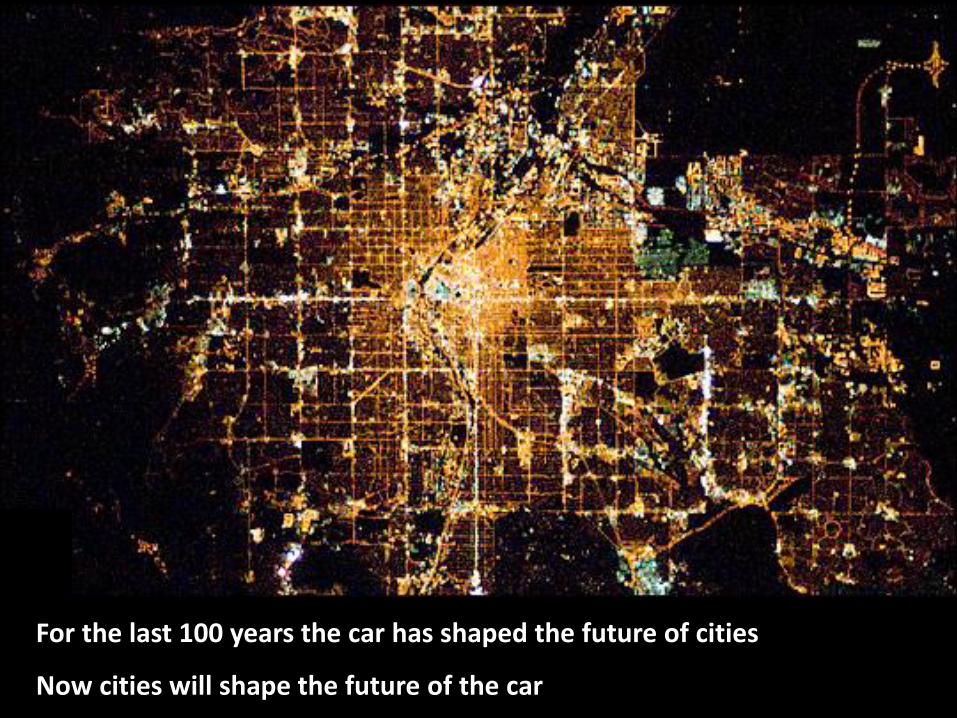

For the last 100 years the car has shaped the future of cities

Now cities will shape the future of the car

EV Ecosystems

International cooperation

Creating EV

ecosystems

Advancing

technology &

manufacturing

Vehicle

trials

Infrastructure

pilots

Public

sector

Private

sector

Removing

barriers

to mass

adoption

Accelerating

early

market growth

Smart Cities

Business Models

Innovation

Skills

Mass Adoption

Immediate Challenges

North East EV Programme

EV Ecosystems

• ‘Total environments’ to support operation of thousands of vehicles

‘Hard Infrastructure’

e.g. recharging points, smart grids,

buildings, transport systems

‘Soft Infrastructure’

e.g. regulation, business models,

incentives, skills, community

engagement

EV Ecosystems

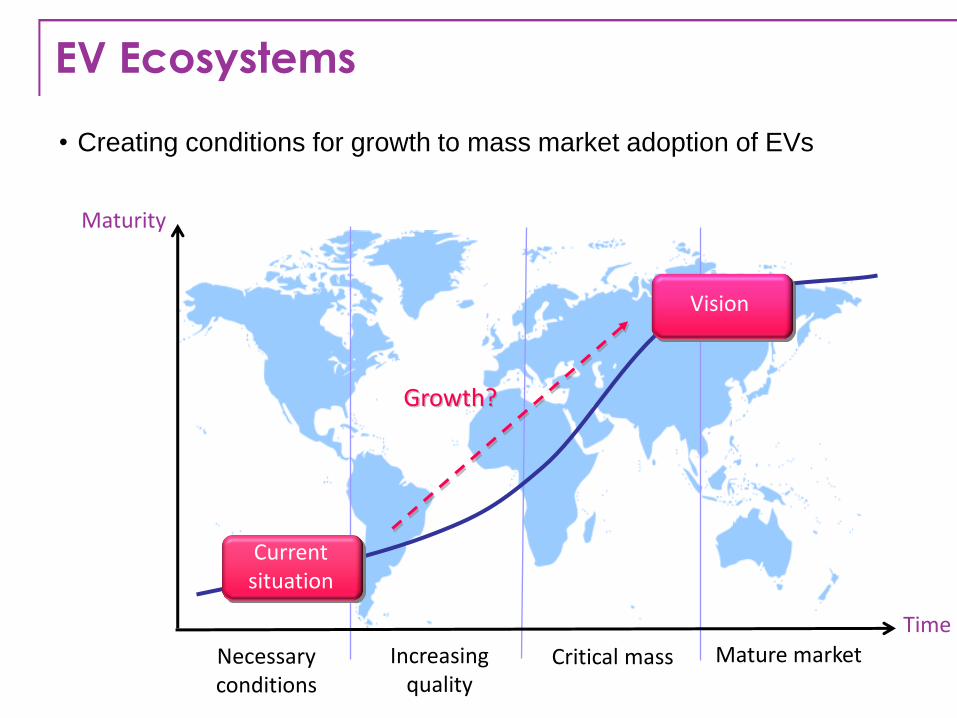

• Creating conditions for growth to mass market adoption of EVs

Time

Maturity

Necessary conditions

Increasing quality

Critical mass Mature market

Growth?

Vision

Current situation

EV Ecosystems

• What comes after the pilots?

Incentives

Innovation and cost reduction → Vehicles → Recharging infrastructure

Mass market adoption

Infrastructure provision

Energy & parking

Third party services

Mobility services

1st generation investments

2nd generation investments

Capital

Time

Revenue

Task XVIII: EV Ecosystems

Preparing World Cities for Mass Adoption

Lessons learned

Problem solving

Best practice

Web portal

Roadmapping

workshops

20 world cities

and regions

Congresses of cities

and businesses

City Roadmaps

International Roadmap

• Roadmapping workshops in 20 pioneering world cities, assembling experts from

municipalities, regional authorities, governments and industry

• A global community of pioneering cities for policy exchange and problem solving

• International Roadmap will establish a blueprint for development of EV Ecosystems

100 big ideas

Case studies

Future vision

Outputs: High Level City Roadmap

Outputs: High Level City Roadmap

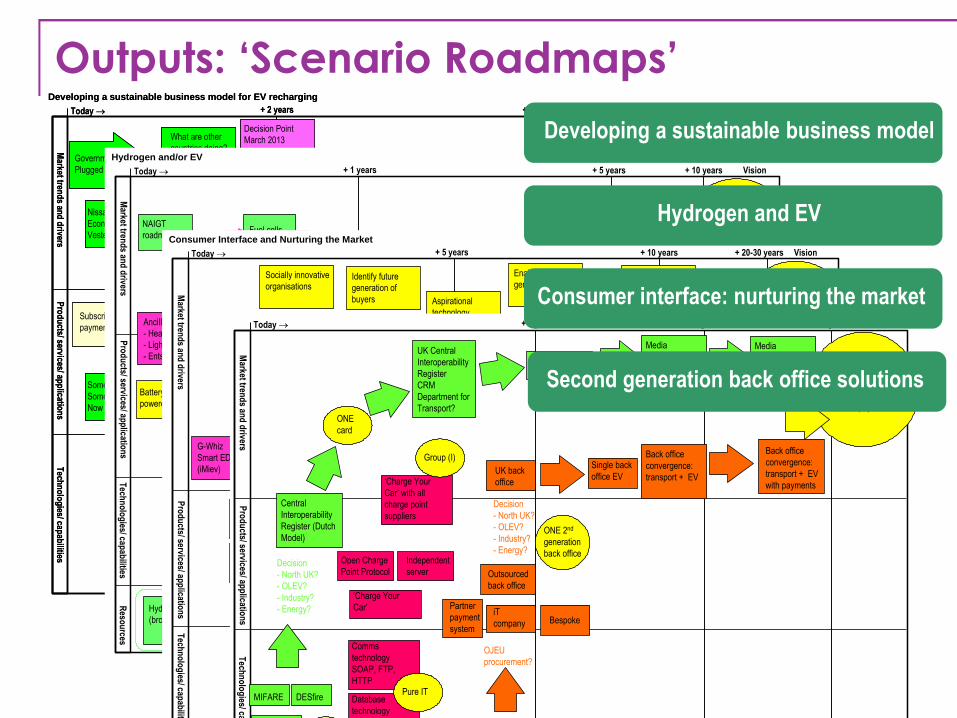

Outputs: ‘Scenario Roadmaps’ Developing a sustainable business model for EV recharging

Today + 2 years

Market tren

ds an

d d

riversP

rod

ucts/ services/ ap

plicatio

ns

Tech

no

log

ies/ capab

ilities

Vision+ 5 years + 10 years

Subscription

payment

What are other

countries doing?

Decision Point

March 2013

Year 2 – 10

Not enough

vehicles to sustain

business model

Government drivers

Plugged in Places

Nissan/ Regional

Economy

Vested Interest

Require integrated

EV strategies

EV = zero emission

Destroys previous

work – issue with

managing

commuter travel

Someone

Something

Now

Inducement for

public charging!

Park and ride

Not many cars –

how do we decide?Charge for parking

Number of vehicles

Valley of death

Capital funding runs

out

Sell data

No revenue

Charge for:

- parking

- energy

Charge for other

things

No need for

infrastructure

No further local

authority estate

growth

Vision: Viable and self-

sustainable business

model for EV recharging

infrastructure – until no

longer required

Back office

provided by a

commercial entity

No back office

Power company

owns posts (buys

posts). Revenue

from ground rent

No back office

Power company

rents posts

New partnership:

private state and

public estate

merger

Commuter parking

sales targets (i.e.

post rented for a

year)

Options?

Private expansion

of post estate

Planning legislation

to expand post

estate

Plugged in Places

dies

No network

No interoperabilityN

cars?

10 years

A BRevenue

Ins??? costs

Vehicle

numbers

30 pence/ ???

Key

Enabler

Opportunity

Barrier

Risk

Option

Developing a sustainable business model for EV recharging

Today + 2 years

Market tren

ds an

d d

riversP

rod

ucts/ services/ ap

plicatio

ns

Tech

no

log

ies/ capab

ilities

Vision+ 5 years + 10 years

Subscription

payment

What are other

countries doing?

Decision Point

March 2013

Year 2 – 10

Not enough

vehicles to sustain

business model

Government drivers

Plugged in Places

Nissan/ Regional

Economy

Vested Interest

Require integrated

EV strategies

EV = zero emission

Destroys previous

work – issue with

managing

commuter travel

Someone

Something

Now

Inducement for

public charging!

Park and ride

Not many cars –

how do we decide?Charge for parking

Number of vehicles

Valley of death

Capital funding runs

out

Sell data

No revenue

Charge for:

- parking

- energy

Charge for other

things

No need for

infrastructure

No further local

authority estate

growth

Vision: Viable and self-

sustainable business

model for EV recharging

infrastructure – until no

longer required

Back office

provided by a

commercial entity

No back office

Power company

owns posts (buys

posts). Revenue

from ground rent

No back office

Power company

rents posts

New partnership:

private state and

public estate

merger

Commuter parking

sales targets (i.e.

post rented for a

year)

Options?

Private expansion

of post estate

Planning legislation

to expand post

estate

Plugged in Places

dies

No network

No interoperabilityN

cars?

10 years

A BRevenue

Ins??? costs

Vehicle

numbers

30 pence/ ???

Key

Enabler

Opportunity

Barrier

Risk

Option

Hydrogen and/or EV

Today + 1 years

Market tren

ds an

d d

riversP

rod

ucts/ services/ ap

plicatio

ns

Tech

no

log

ies/ capab

ilitiesR

esou

rces

Vision+ 5 years + 10 years

NAIGT

roadmap

Battery

powered EV

Companies

manufacture

parts

RangePower/ Energy

density

Ancilliaries

- Heating

- Lighting

- Ents

“HyPower”

direct

injections

Hydrogen

distribution

H2 from

renewables

Hydrogen

storageHydrogen

“clean up”

Plasma

reforming

(QinwtiQ)

Amonia as H2

source

Use

subsystem

to develop

Vision: Economic

development in North

East England i.e.

production in region

Fuel cellsHydrogen

internal

combustion

engine

Hydrogen

(brown)

Nissan in

region

Wessington

Cryogenics

tanks

Inova on board

hydrogen

generation

Renew Tech

fuel cells

Dominick

Hunter/ Parker

Fuel Cells

North East

Universities

North East

England

existing

expertise

HICE Gen

Sets

Fuel cells

Chemical H2

generation

Consumer Interface and Nurturing the Market

Today + 5 years

Market tren

ds an

d d

riversP

rod

ucts/ services/ ap

plicatio

ns

Tech

no

log

ies/ capab

ilities

Vision+ 10 years + 20-30 years

Vision: Electric vehicles

are commonplace in the

minds of the public

G-Whiz

Smart ED

(iMiev)

Car dealers lack

knowledge of new

technologies

Benefits of low

driving costs

Socially innovative

organisationsIdentify future

generation of

buyers

Engage cultural

icons

Quality premium

tag

Aspirational

technology

Air quality benefits

Transport

governance

Enable future

generationCarbon markets

Cost of electricity

generation

Increasing

emphasis on

demand reduction

Plug-in hybrids

E-mobility

integrated with

lifestyle activities

e.g. easyJet,

Premier Inn

Visible innovationUltra-low

maintenance

Increasing battery

capacity

Ease of use of

technology

Intelligent transport

systems

Demonstration of

new charging

systems

Dealers need to

work it!

Fuel cell extended

range vehicles

Demonstrations/

simulations/

visualisations

Demonstration

projects for each

market segment

Today + 2 years

Market tren

ds an

d d

riversP

rod

ucts/ services/ ap

plicatio

ns

Tech

no

log

ies/ capab

ilitiesR

esou

rces

Vision+ 5 years + 10 years

DESfire EV

one media

Real time

comms

MIFARE DESfire

ONE

card

Central

Interoperability

Register (Dutch

Model)

Decision

- North UK?

- OLEV?

- Industry?

- Energy?

ONE

card

UK Central

Interoperability

Register

CRM

Department for

Transport?

Single media EV

Media

convergence:

transport + EV Vision: 2020-2025Single

UK/ EU interoperable

system for EV, transport,

banks and payment

Media

convergence:

transport + EV

with payments

(bank)

„Charge Your

Car‟ with one

charge point

supplier

Database

technology

others

Oracle/ SQL

Comms

technology

SOAP, FTP,

HTTPPure IT

„Charge Your

Car‟

Independent

server

Open Charge

Point Protocol

„Charge Your

Car‟ with all

charge point

suppliers

Group (I)

Payment back

office missing

Tech (MySQL)

Oracle/ SAP

OJEU

procurement?

Partner

payment

systemBespoke

iT

company

Outsourced

back office

Decision

- North UK?

- OLEV?

- Industry?

- Energy?

ONE 2nd

generation

back office

UK back

office

Single back

office EV

Back office

convergence:

transport + EV

Back office

convergence:

transport + EV

with payments

Developing a sustainable business model

Hydrogen and EV

Consumer interface: nurturing the market

Second generation back office solutions

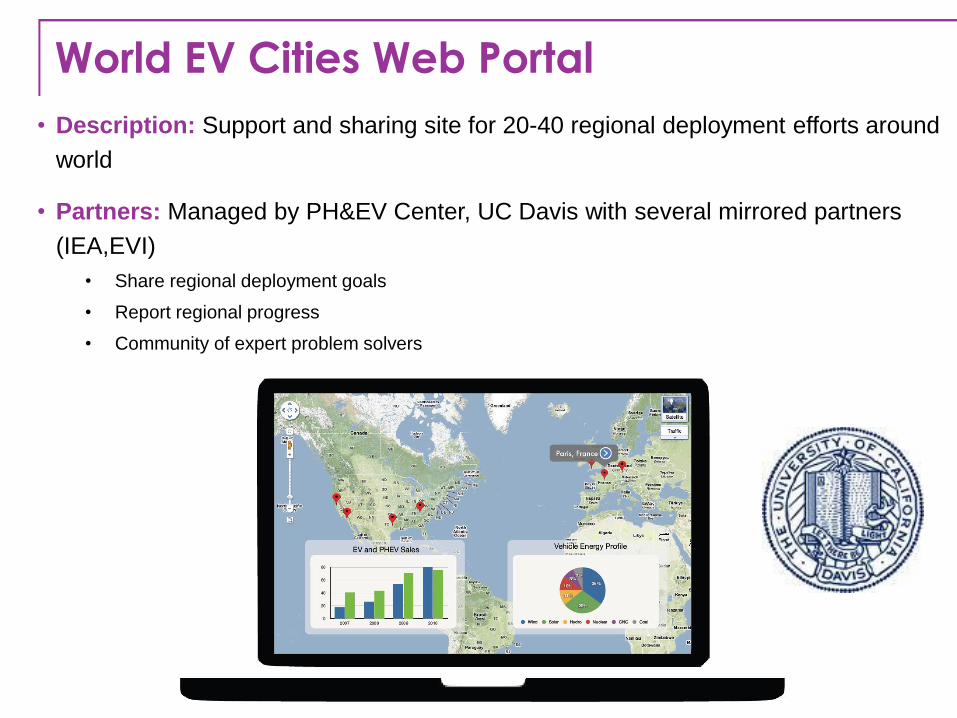

World EV Cities Web Portal

• Description: Support and sharing site for 20-40 regional deployment efforts around

world

• Partners: Managed by PH&EV Center, UC Davis with several mirrored partners

(IEA,EVI)

• Share regional deployment goals

• Report regional progress

• Community of expert problem solvers

Founding Partners

World Cities Pioneering EV Ecosystems

Join Us!

Emerging Challenges

Business

opportunity Functionality

Volume opportunity

and data

Revenue collection

and data

Vehicles Core and value-

added services

Co-marketing Co-marketing

Interoperability Interoperability

Integration

Integrated

service

provision

Mobility

services

Recharging

services

Energy,

parking &

third-party

services

Future Business Models

Understanding Market Dynamics and

Necessary Social Change

Time

Product

performance

attributes ICE vehicles

Electric

vehicles

High-end customer

requirements

Low-end customer

requirements

L1

L2

L3

L4

t4 t3 t2 t1

Unlocking Opportunities Beyond

Recharging Batteries

BIG question for smart cities

Arterial Management

Crash Prevention &

Safety

Commercial Vehicle Ops

Electronic Payment & Pricing

Emergency Management

Highway Management

Information Management

Intelligent Vehicles

Road Weather

Management

Roadway Operations & Maintenance

Traffic Incident Management

Transit Management

Traveler Information

Transportation Management

Center

Electric Vehicle Charging

Is EV Just Another Silo?

Or a

potential

source of

unifying

intelligence?

Thank You

For more information please contact:

Dr David Beeton

Operating Agent Task XVIII

IEA Implementing Agreement Hybrid & Electric Vehicles

Email: [email protected]