dtf econ study opening slides - diesel technology forum · 27/09/2011 · – johnson matthey –...

TRANSCRIPT

9/27/2011

1

Welcome to the National Press ClubWelcome to the National Press ClubWashington, DC

September 28, 2011

Today’s Event

• Introductions

• Opening Remarks – DTF Executive Director Allen Schaeffer

• Presentation of Study Findings – Dr. Richard McCann, Aspen Environmental Group

• Questions

Copyright © 2011 Diesel Technology Forum

Dieselforum.org

Questions

• Luncheon

9/27/2011

2

Members of Diesel Technology Forum

– Amyris– BASF – BorgWarner

BOSCH

– Ford Motor Company– General Motors – Honeywell

– BOSCH– BP– Caterpillar Inc. – Chrysler– Corning– Cummins Inc. – Daimler – Deere & Company

– Johnson Matthey– Mazda North American Operations– MTU– Navistar – Terra Environmental Technologies– Umicore– Volkswagen of America– Volvo Group

Copyright © 2011 Diesel Technology Forum

Dieselforum.org

Deere & Company– Delphi Automotive– Donaldson Company– Dow Automotive

Volvo Group

Allied Members– Association of Diesel Specialists– Western States Petroleum

Association

Aspen Environmental Group

Environmental services focused on energy infrastructure› Contracts with many state and federal agencies› Reviewed environmental studies for most of

California’s large renewable and fossil-fueled power plants

Integrated Energy Analysis and Planning Division› Statewide and West-wide energy plans and

regulatory analyses

Copyright © 2011 Diesel Technology Forum

Dieselforum.org

regulatory analyses› Focused on AB 32 implementation

9/27/2011

3

M.Cubed

• Policy consulting on energy and environmental issues

• Addressed transportation and air quality regulations• Conducted regional economic impact studies

• Prepared 2003 assessment of diesel technology in California economy– Dr. Richard McCann and Mr. Steve Moss previously

partners at M.Cubed• Dr McCann and Mr Moss have been consulting

Copyright © 2011 Diesel Technology Forum

Dieselforum.org

Dr. McCann and Mr. Moss have been consulting on energy policy issues for 25 years

Study Findings

Dr. Richard McCann Aspen Environmental Group

9/27/2011

Aspen Environmental Group 1

Richard McCann MPP PhDRichard McCann, MPP, PhDAspen Environmental Group

with M.CubedFor the Diesel Technology Forum

September 28, 2011

9/27/2011

Aspen Environmental Group 2

Diesel’s Advantages Energy efficientEnergy efficient

Power output

Durability and reliability

Portability

Fuel handling characteristics

Fuel flexibility Fuel flexibility

Highlights of Findings Diesel technology is ubiquitous, powering all sectors Diesel technology is ubiquitous, powering all sectors

of the economy particularly those that are fundamental

Diesel technology supersector about same size as all utilities (energy, water and telecommunications)

Adding diesel‐reliant sectors, produces as much national income as the information sector

Diesel industries generate high economic value

Jobs pay well above the national average

Produce disproportionate share of exports

9/27/2011

Aspen Environmental Group 3

Highlights of Diesel Importance to Specific Sectors

90% of agriculture’s $1.2 trillion in shipments used 90% of agriculture s $1.2 trillion in shipments used diesel vehicles

98.5% of construction and mining fuel use is diesel

85% of transit vehicles and 49% of transit passenger‐miles were diesel powered

83% of Army and Marine vehicles and engines are 3 y gdiesel powered

Many Public Sector Functions Rely on Diesel

Virtually all emergency vehicles, such as ambulances, Virtually all emergency vehicles, such as ambulances, fire engines and tow trucks use diesel engines

Hospitals, data centers, air traffic control towers, pipelines and other critical service sectors often rely on diesel generators for emergency standby power

National defense relies on diesel to move material, munitions and weapons, both between theatres and on the battlefield

Non‐rail transit mostly diesel powered

9/27/2011

Aspen Environmental Group 4

Scope Assessment of economic value delivered by diesel Assessment of economic value delivered by diesel technology to the U.S. economy

“State of the World” report

Focus on:

Diesel technology production and fuels industries, plus diesel support services

Diesel‐reliant industries in resource extraction, agriculture, construction, freight‐hauling

9/27/2011

Aspen Environmental Group 5

Methodology Use regional impact assessment approach Use regional impact assessment approach

› Rely on IMPLAN and U.S. economic data sources

Identify relationships of diesel technology and fuel industries to key economic sectors

› Assign economic output causation from diesel use

Assess share of U.S. GDP and employment produced p y pwhen using diesel = technology enabled activity

Diesel Industries Covered Diesel Fuel Diesel Fuel

› Oil production and refining

Diesel Technology Manufacturing

› Auto and truck

› Rail

› Shipsp

› Tractors and other off‐road and industrial equipment

› Military vehicles, ships and equipment

Diesel Servicing

9/27/2011

Aspen Environmental Group 6

Key Diesel‐Reliant Industries AgricultureAgriculture

Mining

Oil and Gas Production

Construction

Trade and Freight Hauling

Utilities Utilities

Passenger Transport

Government Services

9/27/2011

Aspen Environmental Group 7

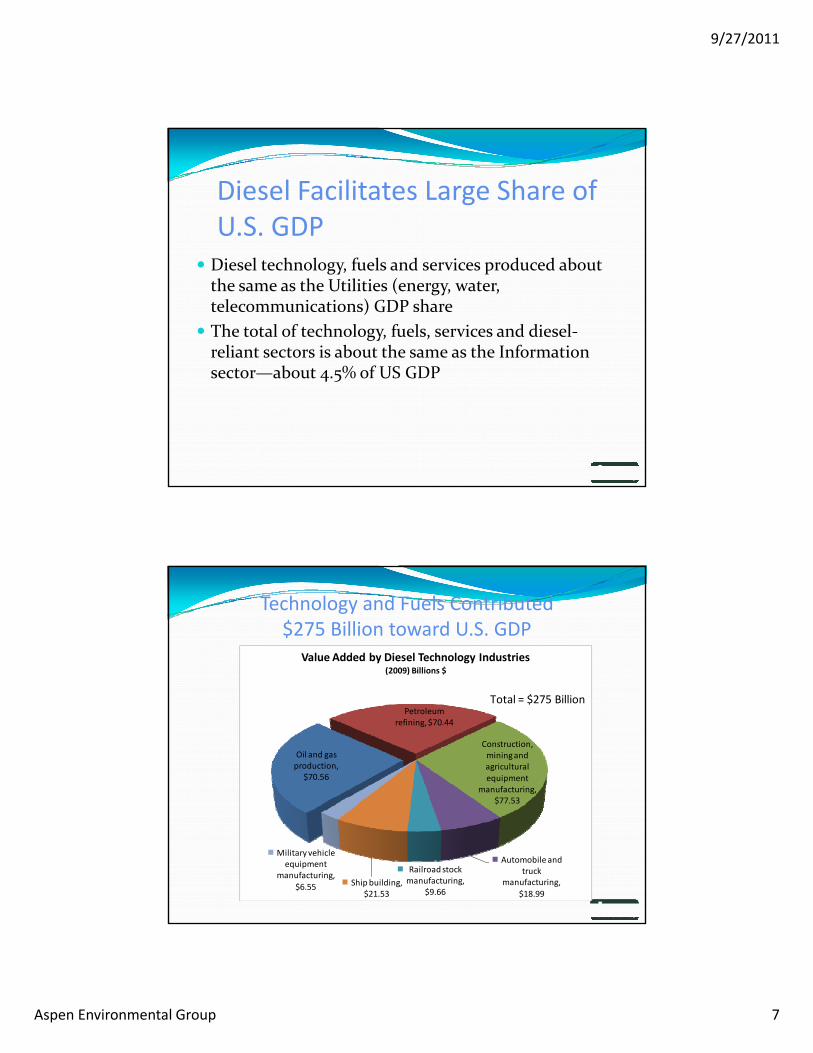

Diesel Facilitates Large Share of U.S. GDP

Diesel technology, fuels and services produced about the same as the Utilities (energy, water, telecommunications) GDP share

The total of technology, fuels, services and diesel‐reliant sectors is about the same as the Information

b % f US GDPsector—about 4.5% of US GDP

Technology and Fuels Contributed $275 Billion toward U.S. GDP

Value Added by Diesel Technology Industries (2009) Billions $

Oil and gas production,

$70.56

Petroleum refining, $70.44

Construction, mining and agricultural equipment

manufacturing, $77.53

Total = $275 Billion

Automobile and truck

manufacturing,

$18.99

Railroad stock manufacturing,

$9.66Ship building,

$21.53

Military vehicle equipment

manufacturing,

$6.55

9/27/2011

Aspen Environmental Group 8

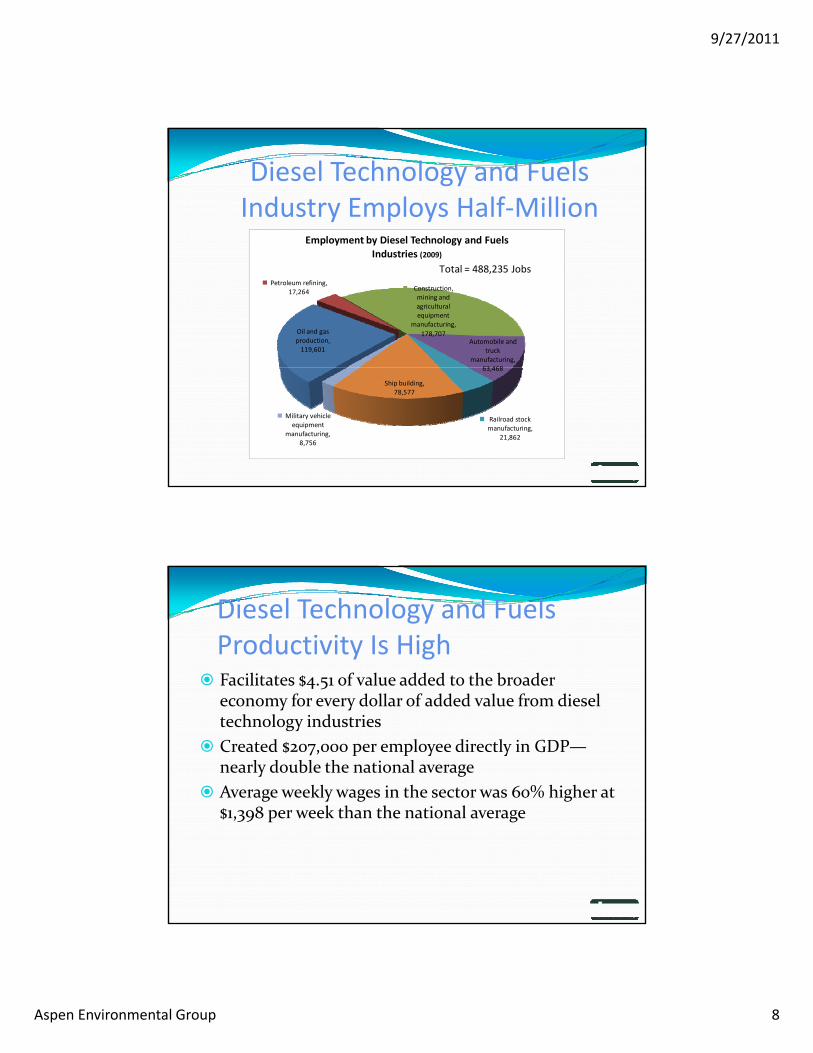

Diesel Technology and Fuels Industry Employs Half‐Million

Employment by Diesel Technology and Fuels

Oil and gas production, 119,601

Petroleum refining, 17,264 Construction,

mining and agricultural equipment

manufacturing,

178,707Automobile and

truck manufacturing,

63 468

Industries (2009)

Total = 488,235 Jobs

63,468

Railroad stock manufacturing,

21,862

Ship building, 78,577

Military vehicle equipment

manufacturing, 8,756

Diesel Technology and Fuels Productivity Is High

Facilitates $4.51 of value added to the broader Facilitates $4.51 of value added to the broader economy for every dollar of added value from diesel technology industries

Created $207,000 per employee directly in GDP—nearly double the national average

Average weekly wages in the sector was 60% higher at $1,398 per week than the national average

9/27/2011

Aspen Environmental Group 9

Diesel Services Employ Three Quarters of a Million Diesel services support deployment, operations and Diesel services support deployment, operations and maintenance of diesel vehicles and equipment, often embedded in other related industries

Added $82 billion directly and $207 billion in total to the U.S. economy.

Created 764,000 jobs

Diesel a Prime U.S. Export Exports 9% of output, five times higher than national Exports 9% of output, five times higher than national

average for manufacturing industries

4.4% of all U.S. exports

9/27/2011

Aspen Environmental Group 10

In Key Diesel‐Reliant Sectors, Creates $455 Billion for GDP

Value Added from Diesel Contribution in Key Sectors (2009) Billions $

T t l $455 Billi

Agriculture, $40.3Nonresidential

Construction, $49.3

Manufacturing, $161.4

Warehousing, $3.6

Water and Sewage Utilities, $0.5

Wholesale Trade, $51.9

Total = $455 Billion

Coal Mining, $4.4

Electric Power Utilities, $47.0

Mineral Mining, $4.9

Air Transport, $9.5Oil and Gas

Production, $25.1

Couriers and Messengers, $8.5

Residential Construction,

$21.4

US Postal Service, $7.4

Government, $15.1

Scenic and Sightseeing,

$5.2

9/27/2011

Aspen Environmental Group 11

83% of Freight Value Shipped Using Diesel

U.S. Freight Shipments: Value by Mode 1997‐2007

$4,000

$5,000

$6,000

$7,000

$8,000

$9,000

$10,000

$6 848$7,546

$8,772

$98

$103

$115

(Billion 2007 dollars)

Air

Pipeline

Water

$0

$1,000

$2,000

$3,000

1997 2002 2007

$6,848

Value

Land (truck + rail)

Bureau of Transportation Statistics, Commodity Flow Surveys

Diesel Share of Highway Fuel Use Has Grown 50% Since 1980

9/27/2011

Aspen Environmental Group 12

Diesel Fuel Use and GDP Growth Highly Correlated

Comparison of U.S Heavy Duty Truck Fuel Consumption and Gross Domestic Product

(1970‐2008)

$6,000

$8,000

$10,000

$12,000

$14,000

1,000

1,500

2,000

2,500

3,000

omestic Product (B

illions 2005$)

ck Fuel Use (Thousand Gallons per Day)

( )

1970‐2008 Growth Rates:GDP = 3.0%

Truck Fuel Use = 3 1%

$0

$2,000

$4,000

0

500

Gross Do

Heavy Duty Truc

Heavy Duty Truck Fuel Use U.S. Gross Domestic Product

Transportation Energy Data Book, 2009, Table 1.14

Bureau of Economic Affairs, 2011.

Truck Fuel Use = 3.1%

Non‐Highway Diesel‐Powered Freight Modes IncreasedFreight Modes Increased Dramatically

Locomotive efficiency improved more than doubled from 235 ton‐miles / gal in 1980 to 480 in 2009

Rail ton‐miles more than doubled from 1981 to 2008Rail ton miles more than doubled from 1981 to 2008

International trade by ship almost doubled from 1983 to 2008

9/27/2011

Aspen Environmental Group 13

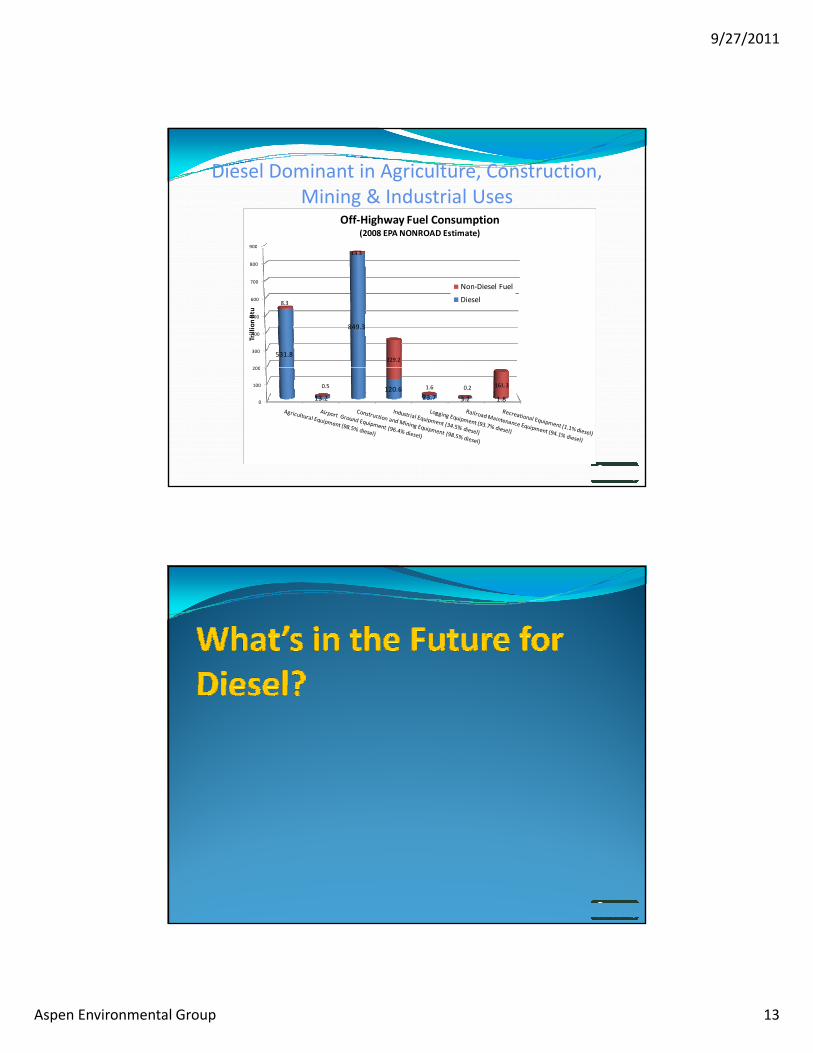

Diesel Dominant in Agriculture, Construction, Mining & Industrial Uses

900

Off‐Highway Fuel Consumption (2008 EPA NONROAD Estimate)

200

300

400

500

600

700

800

900

531.8

849.3

8.3

13.3

229.2

Trillion Btu

Non‐Diesel Fuel

Diesel

0

100

200

13.2120.6

23.7 3.2 1.8

0.5 1.6 0.2 161.3

9/27/2011

Aspen Environmental Group 14

Diesel Fits with Environmental Goals Diesel 20‐40% more efficient than spark‐ignition Diesel 20 40% more efficient than spark ignition technologies

50% of European auto market

Fuel economy standards will favor diesel technologies

Federal and state policies lead to clean diesel technologies that use a range of fuels, including g g gbiofuels

U.S. energy R&D has a 60:1 benefit‐cost ratio

Diesel retrofit programs return a 13:1 benefit‐cost ratio

9/27/2011

Aspen Environmental Group 15

Diesel Industry Contributions

Diesel Industry S b t

Total Output Value Added EmploymentDiesel Technology and Fuels Industry Statistics

SubsectorVehicle, Equipment & Engine Manufacturing

$178.2 billion $45.7 billion 349,000

Oil Production & Refining

$218.6 billion $55.3 billion 137,000

Sales, Repair & $120.7 billion $82.1 billion 764,000ServicingTotal $517.5 billion $183.0 billion 1,252,000 Multiplier Effect $300.1 billionTotal Value Added $483.1 billion

Diesel Reliance and 2009 U.S. GDPDiesel GDP Share

($ billions)Agriculture 35.0% $40.30 Sectors

% Diesel Contribution or Influence

g cu tu e 35 0% $ 0 30Coal Mining 26.8% $4.40 Electric Power Utilities 24.6% $47.00 Mineral Mining 17.0% $4.90 Air Transport 16.8% $9.50 Oil and Gas Production 15.9% $25.10 Couriers and Messengers 15.2% $8.50 Residential Construction 14.0% $21.40 US Postal Service 13.7% $7.40 Government 13.3% $15.10 Scenic and Sightseeing 12.4% $5.20 Nonresidential Construction 11.7% $49.30 Manufacturing 10.5% $161.40 Warehousing 8.8% $3.60 Water and Sewage Utilities 7.0% $0.50 Wholesale Trade 6.8% $51.90 Total for Diesel Reliant Sectors $455

9/27/2011

Aspen Environmental Group 16

Conclusions Diesel technology is ubiquitous throughout the U.S. Diesel technology is ubiquitous throughout the U.S. economy—key to producing fundamental resources and goods, and prime mover of four‐fifths of all freight

Technology and fuels sectors are twice as productive and wages are three‐fifths higher than U.S. average

Exports five times more of sector output than national average, over 4% of national exports

Richard McCann, Aspen [email protected](530) 757‐6363

[email protected] Technology Forum301‐668‐7230