eaapac-sadcopac workshop on committees inquiries juba, south sudan - 6-8 feb 2013 resource person:...

TRANSCRIPT

EAAPAC-SADCOPAC Workshop on

Committees InquiriesJuba, South Sudan - 6-8

Feb 2013Resource Person: Mitchell O’Brien,

Team Lead – Parliament Program, World Bank Institute

Objective: To Strengthen the capacity of PACs to use committee hearings to scrutinize implementation of the budget.

Sub-themes1. Introducing the Budget

2. The Budget ProcessDraftingEnactment ImplementationExternal Audit

3. Parliamentary Audit

4. The Changing World of PACs

1 – Introducing the budget We look at the definition of the budget

and its components, including revenues, expenditures and the deficit, as well as some of the main objectives of budgeting.

Definition of the budget

“It’s got a lot of numbers in it.” (George W. Bush) “…budgeting is concerned with the translation of

financial resources into human purposes.” (Aaron Wildavsky)

“The budget is a document which forecasts and authorizes the annual receipts and expenditures of the State…” (French Decree of 1862)

An itemized summary of estimated or intended expenditures for a given period along with proposals for financing them.

Components of the budget:Revenues Direct taxes: A tax paid directly to the government, for

example a tax imposed on the income of individuals or companies.

Indirect taxes: A tax paid to a second party, for example a shop owner, who then passes it on to the government. Examples are value added tax and custom duties.

Progressive versus regressive taxation: A progressive tax increases as a percentage of income as one’s income increases.

Other sources of government income might consist of user charges for certain services, foreign aid, and income from investments or commercial activities.

Components of the budget:Expenditures

Spending to fulfill a government obligation, generally by issuing a check or disbursing cash.

Capital expenditures are investments in physical assets,such as a roads and buildings that can be used for a number of years.

Current expenditures reflect spending on wages, benefit payments, and other goods or services that are consumed immediately.

Functional classification: According to various activities and policy objectives, such as health care,education, defense or justice.

Components of the budget:The budget balance Deficit: The difference produced when spending

exceeds revenues in a fiscal year. Surplus: The amount by which revenues exceed outlays

or expenditures (not common). Changes in the deficit do not have to be the result of a

shift in fiscal policy, but can also reflect the business cycle, for instance.

Consistently growing deficits, however, give cause for concern: Pressure on interest rates and ‘crowding out’ Rising debt servicing costs Inflationary pressures Unfair for future generations to have to pay for today’s

consumption

Some principles of good budgeting Comprehensiveness: The budget must cover

all the fiscal operations of government. Predictability: Spending agencies should have

certainty about their allocations in the medium term to enable them to plan ahead.

Contestability: No item in the budget should have an automatic claim to funding.

Transparency: Accurate, timely, reliable and comprehensive information.

Periodicity: The budget should cover a fixed period of time, and follow a clear schedule. However, should seek to achieve medium term objectives

Objectives of budgeting (Schick 1998)

Fiscal discipline: Budget totals should be the result of explicit, enforced decisions; they should not merely accommodate spending demands.

Allocative efficiency: Expenditures should be based on government priorities and on effectiveness of public programs (need to listen to the recommendations of the PAC).

Operational efficiency: Agencies should produce goods and services at a cost that achieves ongoing efficiency gains.

These objectives are interrelated!

Concluding remarks

Public resources are always limited and inevitably fall short of meeting all the needs of society.

A well-functioning budget process helps to assess competing claims on the budget and facilitates difficult tradeoffs.

Meeting this challenge successfully requires that budgeting achieves: Affordable budget totals Strategic prioritization of public funds Sound operational management

2 – The Budget Process The budget cycle in government

typically involves a number of different actors and follows a sequence of essential steps.

We introduce the main participants of the budget process and present a simplified and generalized outline of planning, approving, implementing and auditing expenditures.

Key actors in the budget process The finance ministry or treasury is to coordinate and

drive the budget process in accordance with schedule. Spending departments are ultimately responsible for

expenditures within their jurisdiction. President/Prime Minister and Cabinet make

fundamentally political decisions about tradeoffs. The role of the legislature is to scrutinize and authorize

revenues and expenditures. Independent supreme audit institutions audit

government accounts for compliance and performance. Other actors may include the media, civil society

organizations, donors and international financial institutions.

B u d g e t t a b l e d i n t h el e g i s l a t u r e

C o n s i d e r a t i o n b yp a r l i a m e n t a r yc o m m i t t e e ( s )

P a r l i a m e n t a c c e p t s ,a m e n d s o r r e j e c t s t h eb u d g e t

F i n a n c e m i n i s t r y o rt r e a s u r y i s s u e sg u i d e l i n e s t o s p e n d i n gd e p a r t m e n t s o r a g e n c i e s

S p e n d i n g d e p a r t m e n t ss u b m i t d r a f t b u d g e t s

N e g o t i a t i o n a n d f i n a ld e c i s i o n s b y e x e c u t i v e

D r a f t i n g L e g i s l a t i v e I m p l e m e n t a t i o n A u d i t

F u n d s a p p o r t i o n e d t os p e n d i n g d e p a r t m e n t s t oi m p l e m e n t a c t i v i t i e s

F i n a n c e m i n i s t r ym o n i t o r s s p e n d i n g

R e q u e s t f o r l e g i s l a t i v ea p p r o v a l o f a d j u s t m e n tb u d g e t i f n e c e s s a r y

S u p r e m e a u d i t i n s t i t u t i o na s s e s s e s d e p a r t m e n t a la c c o u n t s a n dp e r f o r m a n c e

A u d i t r e p o r t s p u b l i s h e da n d r e v i e w e d b yp a r l i a m e n t

B e f o r e b e g i n n i n g o f r e l e v a n t f i s c a l y e a r F i s c a l y e a r s t a r t s a n d e n d s F o l l o w i n g e n d o f f i s c a l y e a r

S t a g e s o f t h e a n n u a l b u d g e t p r o c e s s

Stage 1 - Drafting Concerned with compiling a draft budget that

can be submitted to the legislature. Mostly internal to the executive, secretive. The first step is to set fiscal policy and estimate

available revenues based on macroeconomic projections in order to establish the total resource envelope (the estimates).

Finance ministry issues guidelines to spending departments.

Submission of draft budget requests from spending departments.

Negotiations at bureaucratic and political levels.

Stage 2 – Enactment

Budget tabled in the legislature. Consideration by parliamentary

committee(s). Parliament accepts, rejects or amends the

budget.

Access to information

Legislative decision making needs to be based on comprehensive, accurate, appropriate and timely information.

In a number of countries, the budget document itself contains little narrative that outlines the policies underlying tax and spending proposals.

Many budgets do not sufficiently relate expenditures to policy objectives.

Parliamentary budget offices are important sources of independent expertise.

The OECD has developed Best Practices for Budget Transparency that deal with the availability of budget information.

Budgeting for the medium term Many aspects of budgeting require more than an annual time

horizon, e.g. large scale capital projects or restructuring of service delivery.

The purpose of a Medium Term Expenditure Framework (MTEF) is to indicate the size of the financial resources needed during the medium term, usually between three to five years, in order to carry out existing policy.

Differs from multiyear budgeting, which involves fixed appropriations for a number of fiscal years.

Usually, only the first year of an MTEF is approved by the legislature as the annual budget, whereas the outer years are nonbinding projections of the future cost of existing policy.

MTEFs will be discussed in detail in a separate session. However, this is essential criteria for PACs determining whether

government programming achieved its objectives

Does the annual central government budget documentation submitted to the legislature contain multi-year expenditure estimates?

Number of countries

Percentage of total

Yes 28 70% No 12 30% Total 40 100% Source: OECD (2003), http://ocde.dyndns.org/

Stage 3 - Implementation Funds are apportioned to departments in order

to implement activities. Finance ministry monitors spending. Request for legislative approval of adjustment

budget if necessary. Fiscal risks are inherent in a continuously

changing economic environment – purpose of contingency reserves.

In-year adjustment decisions should be transparent and thoroughly scrutinized.

OECD Recommendations A comprehensive budget includes performance data and medium

term projections. A pre-budget report states explicitly the government’s long-term

economic and fiscal policy objectives, and its economic assumptions and fiscal policy intentions for the medium term.

Monthly reports show progress in implementing the budget, including explanations of any differences between actual and forecast amounts.

A mid-year report provides a comprehensive update on the implementation of the budget, including an updated forecast of the budget outcome for the medium term.

A year-end report should be audited by the audit institution and released within six months of the end of the fiscal year.

A pre-election report illuminates the general state of government finances immediately before an election.

A long-term report assesses the long-term sustainability of current government policies.

Stage 4 – External Audit

Supreme audit institution assesses departmental accounts and performance.

Audit reports should be published promptly and submitted to parliament.

We will look at this stage in more detail in a later session.

Concluding remarks For parliamentary budget researchers and committee

staff thorough acquaintance with the actors and process of budgeting is essential.

This unit looked at a simplified and generalized summary of budgeting in the public sector.

Most budget processes in the public sector go through drafting, legislative, implementation, and audit stages.

Medium term budgeting frameworks are increasingly used to guide annual budgeting and to provide a broader planning horizon.

Political dynamics

Budgeting takes place in a broader political context.

Secure legislative majorities enhance the predictability of voting outcomes.

Minority and coalition governments may have to make more concessions in order to ensure legislative support.

Party majorities only ensure predictability of legislative voting behavior when they are matched with tight party discipline.

Role of electoral system.

3. Parliamentary Audit Audit and the ‘chain of accountability’ Types of supreme audit institutions The Lima Declaration Types of audit Interaction between auditors and

parliament What do PACs look like globally

Voters Parliament

PrimeMinister

Cabinet

Departments

AccountingOfficers

Confer authority on Confers authority on Establish and appoint

Account toAre accountable toIs accountable to

Audit and the chain of accountability in parliamentary systems

Reports toAppoints

Auditor General

Supreme Audit Institution Audits and evaluates

Types of supreme audit institutions A supreme audit institution is a public organization that is

independent of government and has responsibility for auditing and reporting on the government’s financial operations.

Audit courts are independent of both the legislative and executive branches of government and an integral part of the judiciary. Napoleon put in place the cour des comptes in 1807. Found in Latin countries in Europe, South America and West Africa.

Auditor generals are independent bodies that report directly to parliament and have no judicial function. In the UK, the Exchequer and Audit Departments Act of 1866 required

annual appropriation accounts to be investigated by the Comptroller and Auditor General.

Used in most of the Commonwealth. The International Organisation of Supreme Audit Institutions

(INTOSAI) has put down fundamental standards for national audit in the Lima Declaration of Guidelines on Auditing Precepts.

Lima DeclarationThe supreme audit institution should… Be independent from the audited entity and

protected against outside influence. Have functional and organizational independence,

guaranteed by the constitution. Have the financial means to accomplish its tasks. Self-determine its audit program. Have members with prerequisite qualifications and

moral integrity. Report annually and independently to Parliament. Produce reports that are objective, clear, limited to

essentials, precise and easy to understand. Audit all public financial operations.

Are the findings of the national audit body available to the public? Number of

countries Percentage of

total Always 20 50% Generally, but with some exceptions*

18 45%

Never or rarely 2 5% Total 40 100%

Source: OECD (2003), http://ocde.dyndns.org/ Note: * For example audits of the military.

Types of audit Financial audit is the traditional focus of public sector auditing. In the auditor general model, financial audit focuses on the

accounts of government departments in order to present a judgment about the accuracy and fairness of an organization’s financial statements. Because it is impossible to check every single transaction, auditors use sampling techniques.

In the audit court model, the emphasis of financial audit is on certifying the legality of spending, to see whether government revenue and spending have been authorized and used for approved purposes, and whether departments and agencies have conformed to all pertinent laws and regulations.

In addition, many audit institutions increasingly perform value for money or performance audits. This is a comparatively recent development over the last twenty to thirty years.

The term value for money captures the ‘Three Es’ of economy, efficiency and effectiveness.

Interaction with parliament

relationship between parliament and the audit institution varies between systems.

In the court model tradition, parliament uses audit information for a formal vote on the execution of a budget.

In the Westminster tradition there is no formal vote on budget execution, and parliamentary review serves primarily to generate recommendations for improving public spending.

In a number of countries supreme audit institutions have established parliamentary liaison offices and accompany audit related work of parliament on an ongoing basis.

More recently, many supreme audit institutions have also developed a more ad hoc advisory function.

Role of parliamentary committees A few legislatures do not consider audit findings in detail,

but most parliaments use committees to do so. In some legislatures the same committee that is

responsible for approving the budget is also tasked with considering audit reports.

Another option that is closely linked to the auditor general model of public audit is to use a dedicated public accounts committee for the scrutiny of audit findings.

Other parliaments involve sectoral committees, such as those responsible for health, education or defense, to scrutinize relevant audit findings.

Other parliaments have a hybrid model.

Public accounts committees First modern PAC in Denmark in 1856 followed

by the UK in 1861 Strong linkage with Auditor General Policy-neutral: focus on implementation Cross-partisan: opposition chairperson in 67% of

PACs in the Commonwealth Hearings with accounting officers Increasing importance of value for money audit But: evidence that this system does not work

well in many developing countries Delayed reporting Poor quality of reports Government non-response

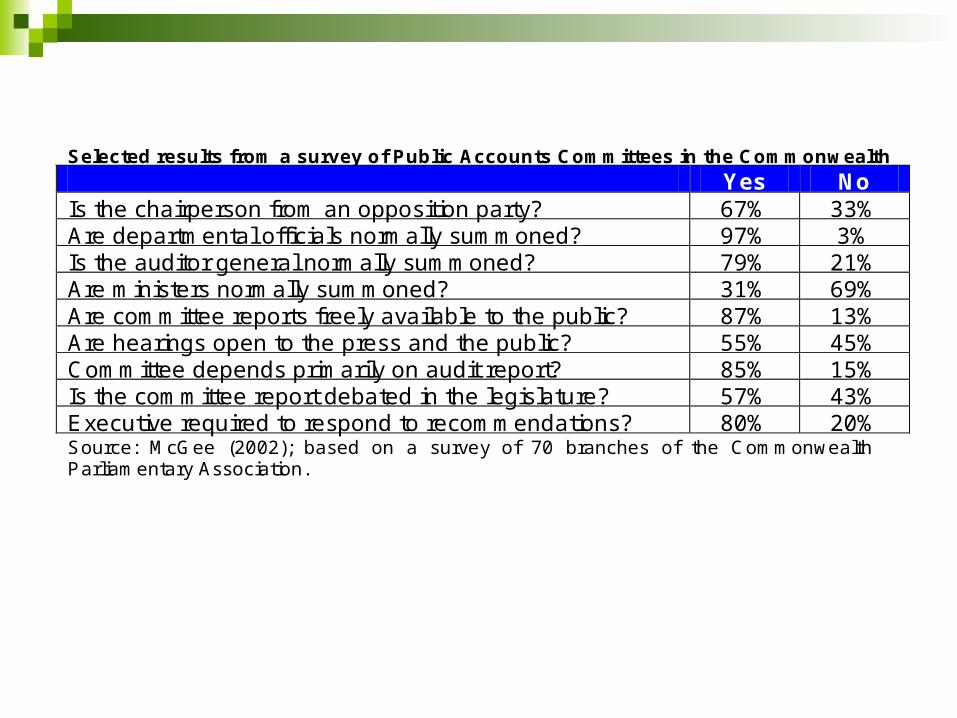

Selected results from a survey of Public Accounts Committees in the Commonwealth Yes No Is the chairperson from an opposition party? 67% 33% Are departmental officials normally summoned? 97% 3% Is the auditor general normally summoned? 79% 21% Are ministers normally summoned? 31% 69% Are committee reports freely available to the public? 87% 13% Are hearings open to the press and the public? 55% 45% Committee depends primarily on audit report? 85% 15% Is the committee report debated in the legislature? 57% 43% Executive required to respond to recommendations? 80% 20% Source: McGee (2002); based on a survey of 70 branches of the Commonwealth Parliamentary Association.

4. The Changing World of PACs

The traditional PAC was described by Yamamoto (2007) and McGee (2002)

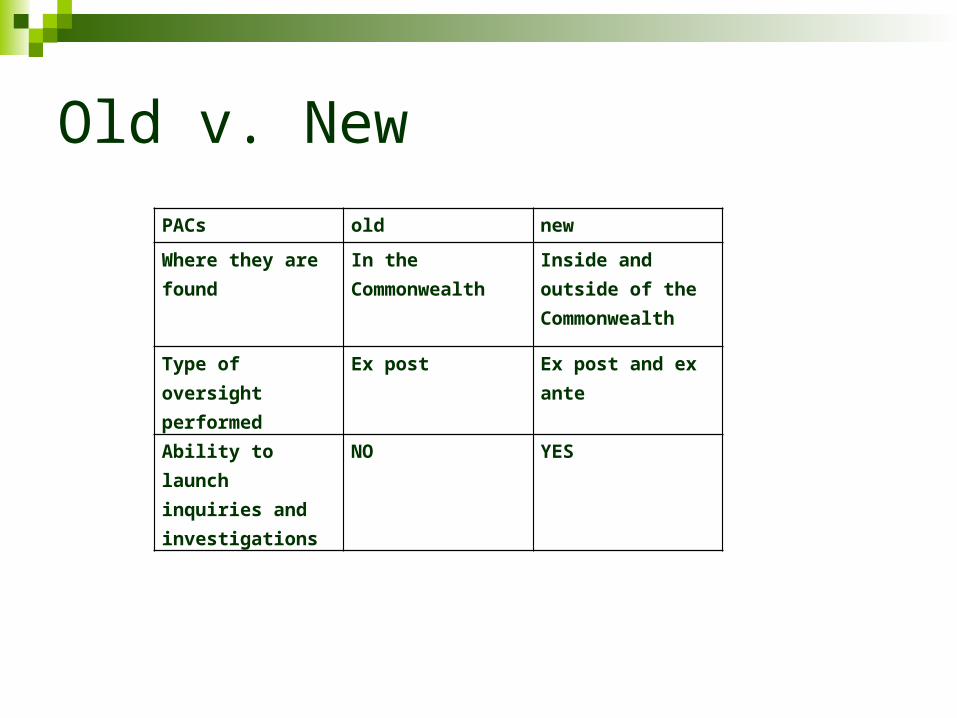

PACs are now set up outside the Commonwealth (Ethiopia, South Sudan, Rwanda, Liberia, Indonesia, Bhutan, Thailand …)

They oversee ex post and ex ante They can launch their own investigation

Old v. New

PACs old new

Where they are found In the Commonwealth Inside and outside of the Commonwealth

Type of oversight performed

Ex post Ex post and ex ante

Ability to launch inquiries and investigations

NO YES

Snapshot of a Modern PAC

Examine:

a. Membership and leadership

b. Staffing

c. Powers and responsibility

d. Activity

a. Membership and leadership

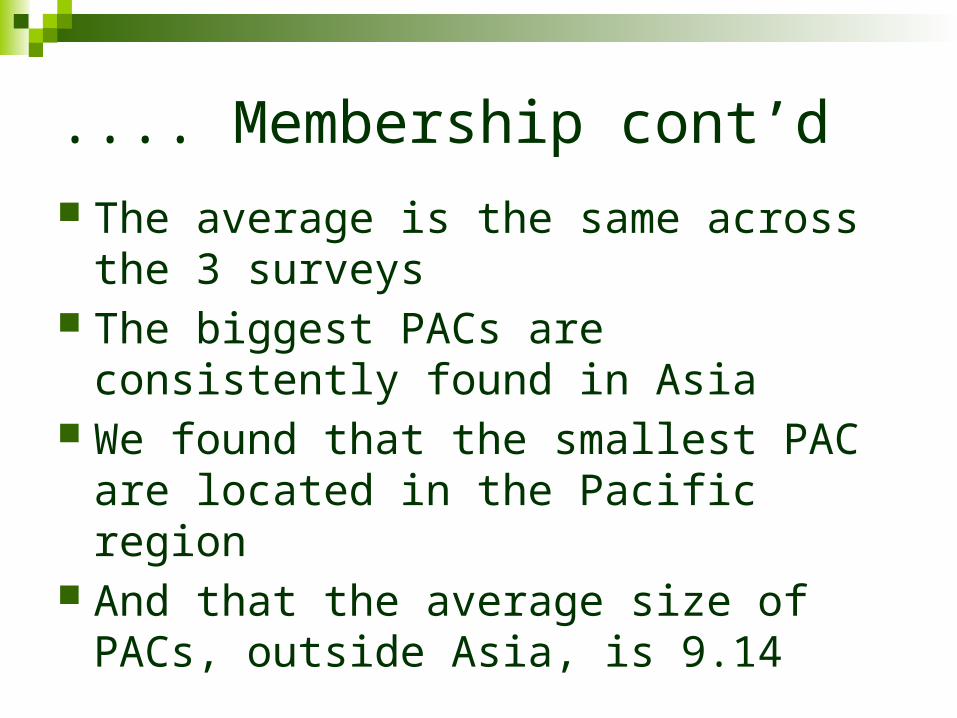

.... Membership cont’d The average is the same across the 3

surveys The biggest PACs are consistently found

in Asia We found that the smallest PAC are

located in the Pacific region And that the average size of PACs,

outside Asia, is 9.14

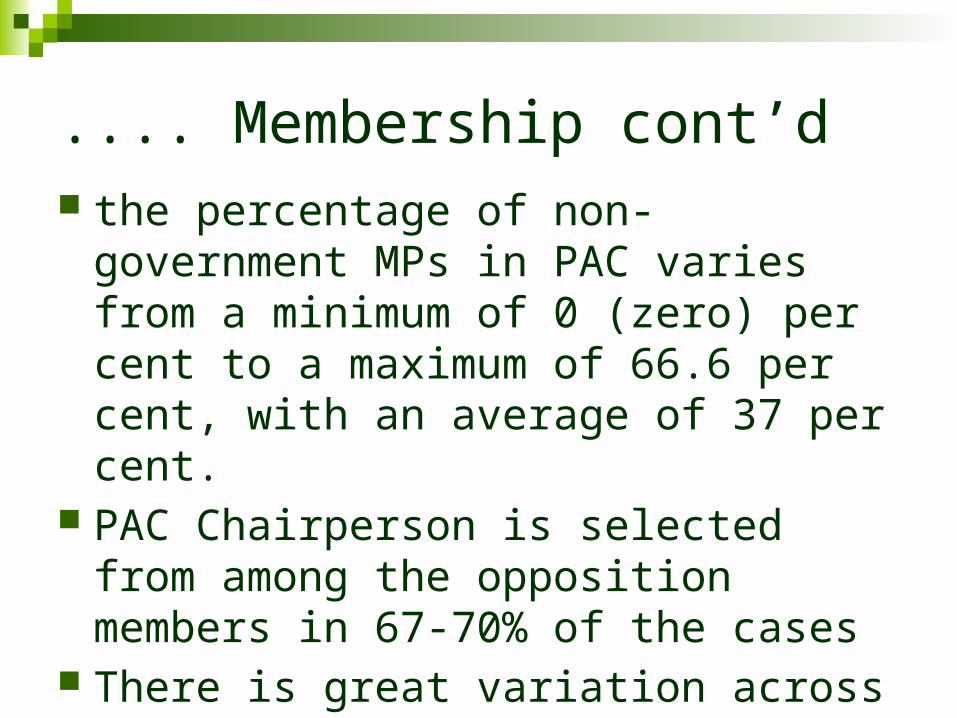

.... Membership cont’d the percentage of non-government MPs in

PAC varies from a minimum of 0 (zero) per cent to a maximum of 66.6 per cent, with an average of 37 per cent.

PAC Chairperson is selected from among the opposition members in 67-70% of the cases

There is great variation across regions.

b. Staffing

The size of the staff at the disposal of PACs is a very important variable

McGee (2002) said that lack of staff is what prevents larger PACs from performing effectively

Pelizzo and Stapenhurst (2012) found that the size of staff is strong and significant predictor of the number of reports produced by a PAC

...... Staffing cont’d The size of the staff at the disposal of

PACs is an important variable McGee (2002) said that lack of staff is

what prevents larger PACs from performing effectively

Pelizzo and Stapenhurst (2012) found that the size of staff is strong and significant predictor of the number of reports produced by a PAC

...... Staffing cont’d

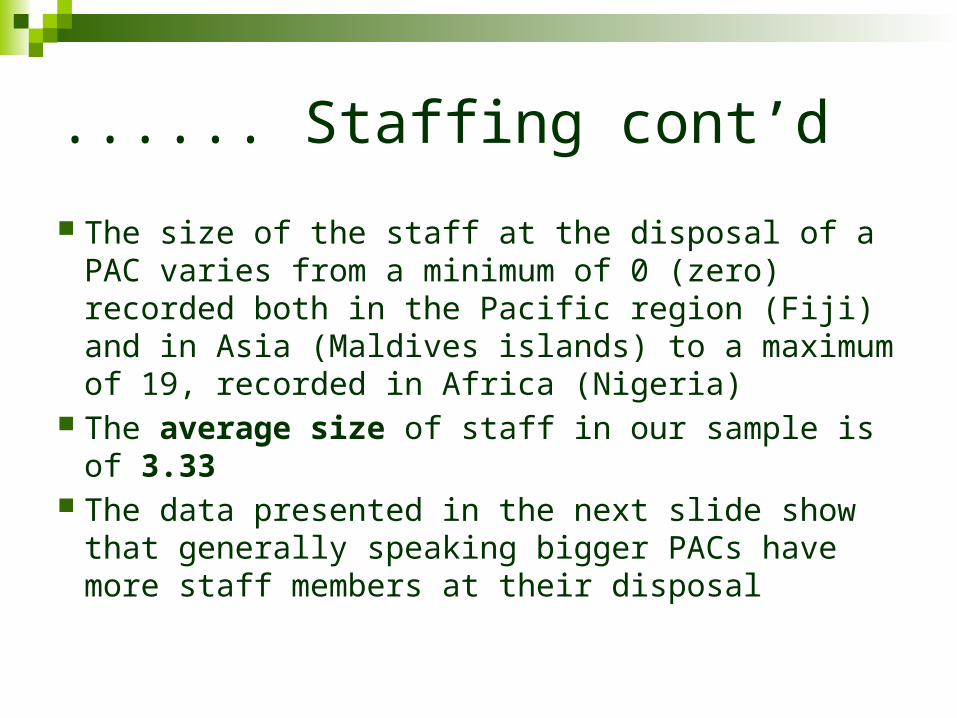

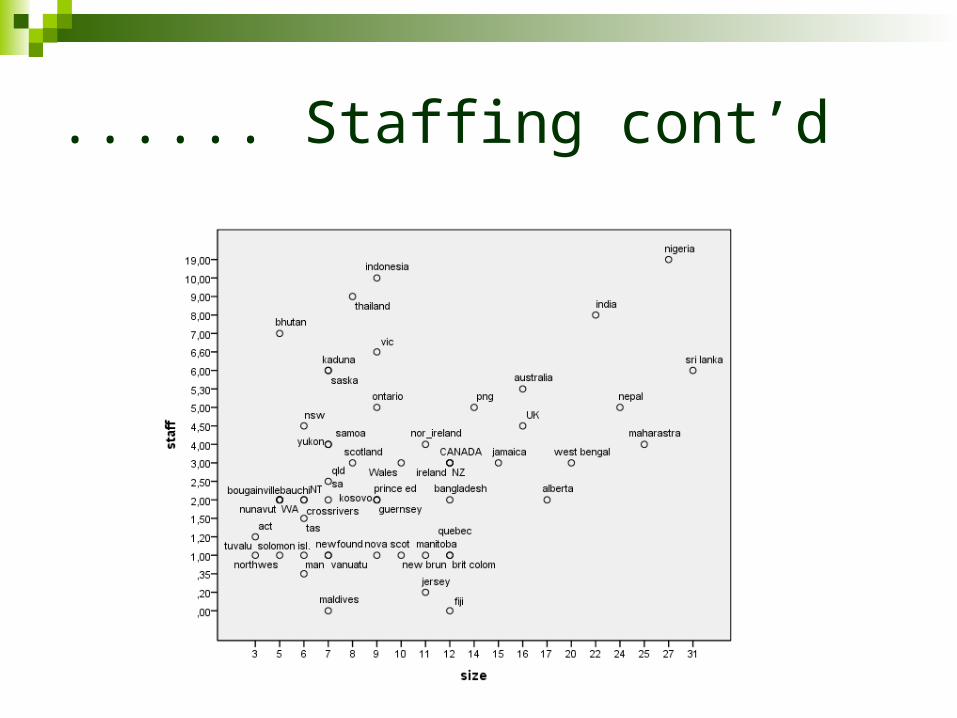

The size of the staff at the disposal of a PAC varies from a minimum of 0 (zero) recorded both in the Pacific region (Fiji) and in Asia (Maldives islands) to a maximum of 19, recorded in Africa (Nigeria)

The average size of staff in our sample is of 3.33 The data presented in the next slide show that

generally speaking bigger PACs have more staff members at their disposal

...... Staffing cont’d

c. Powers and Responsibilities

WBI conducted a survey in 2009 sought information on the scope of their mandate.

Responses can be grouped into three categories:

i. Right of access

ii. Accounts and operations

iii. AG reports

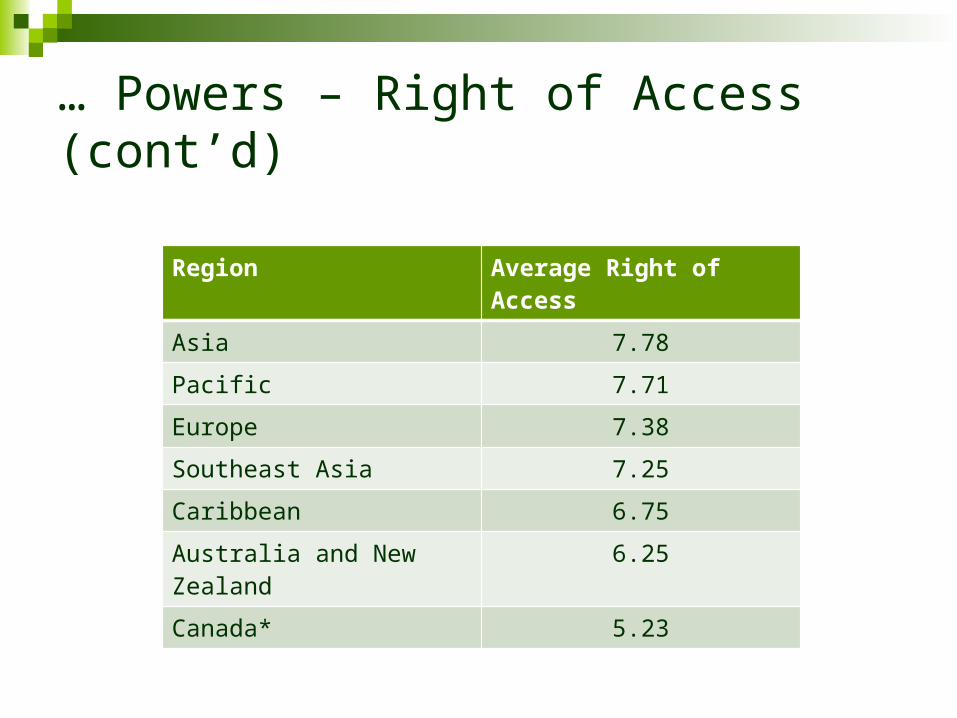

… Powers – Right of Access

… Powers – Right of Access (cont’d)

Region Average Right of Access

Asia 7.78

Pacific 7.71

Europe 7.38

Southeast Asia 7.25

Caribbean 6.75

Australia and New Zealand 6.25

Canada* 5.23

… Powers – Accounts and Operations

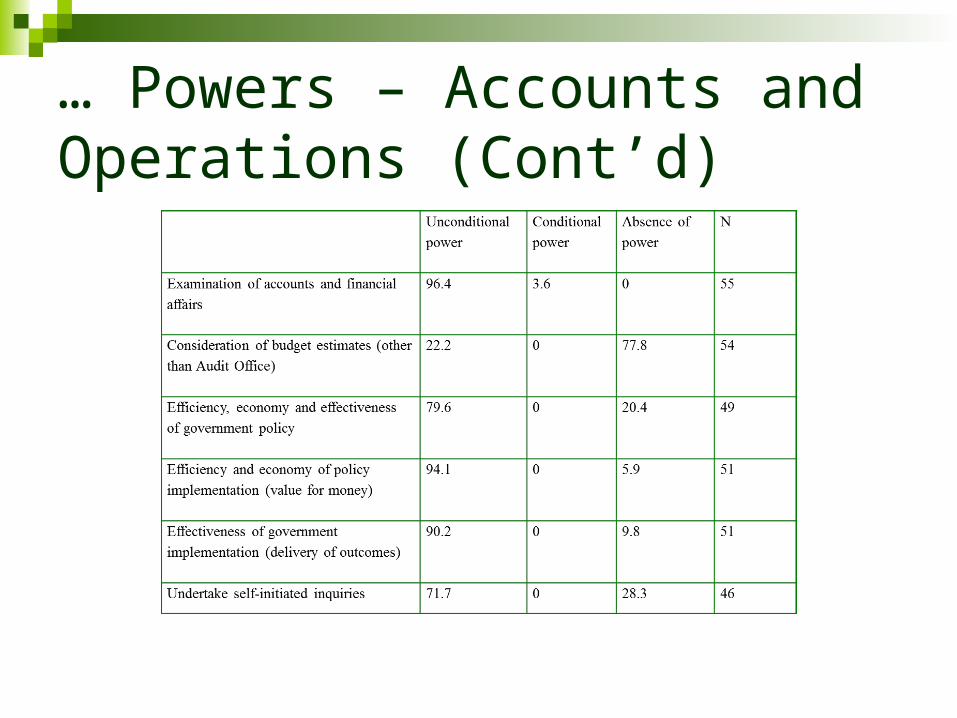

Powers in this category pertain to the ability to:

i. Examine accounts

ii. Consider budget estimates

iii. Assess the efficiency, economy and effectiveness of a given policy

iv. Assess the efficiency and the economy of policy implementation

v. Assess the effectiveness of policy implementation; and

vi. Undertake self-initiated inquiries.

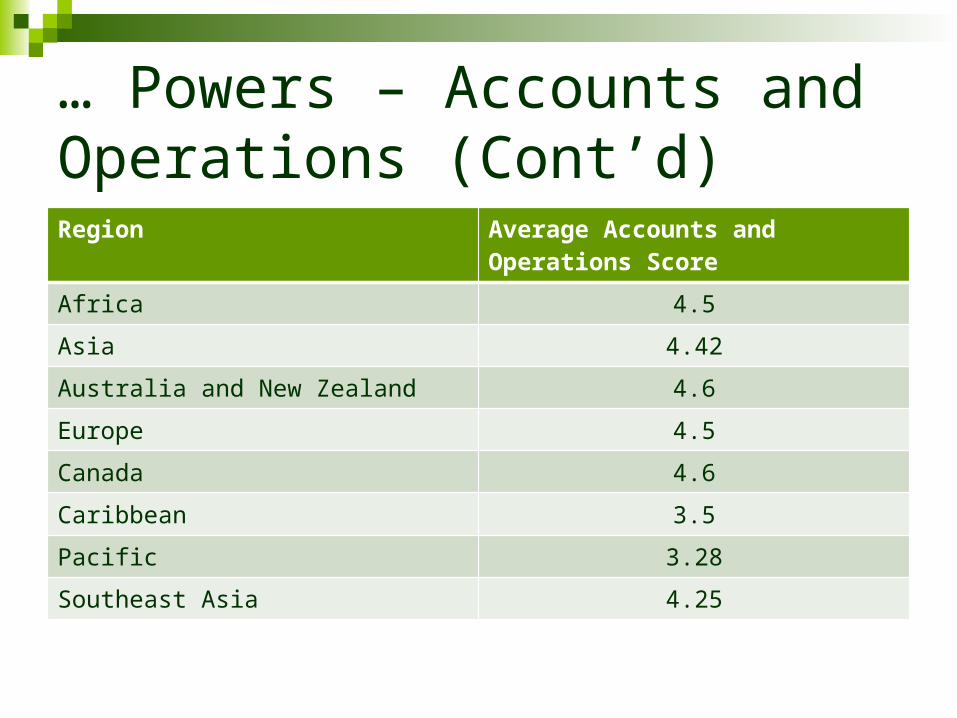

… Powers – Accounts and Operations (Cont’d)

… Powers – Accounts and Operations (Cont’d)Region Average Accounts and Operations

Score

Africa 4.5

Asia 4.42

Australia and New Zealand 4.6

Europe 4.5

Canada 4.6

Caribbean 3.5

Pacific 3.28

Southeast Asia 4.25

… Powers – AG Reports

The three powers that belong to this category are:

i. Perform an examination of Auditor General compliance reports,

ii. Conduct an examination of Auditor General Performance reports; and

iii. Refer matters to the Auditor General for investigation

… Powers – AG Reports (Cont’d) The power to examine the AG’s

performance report is enjoyed unconditionally by 90.7 per cent of PACs (9.3% of the PACs lack this power)

The power to examine the AG’s compliance reports is enjoyed unconditionally by 94.4 per cent of PACs (5.6 per cent of PACs this power)

… Powers – AG Reports (Cont’d) Various studies show the success of PACs depends on

the quality of the work carried out by the SAIs Various jurisdictions have lamented that AG, once

appointed, are not terribly active and dynamic. Therefore, its important PACs have the power to initiate

their own inquiries and to refer matters to the AG for investigation

However, referring matters to the A-G is the least common power (conditional in 7.4% of the PACs; unconditional in 83.3% of PACs; and 9.3% of PACs lack this power)

d. Activity

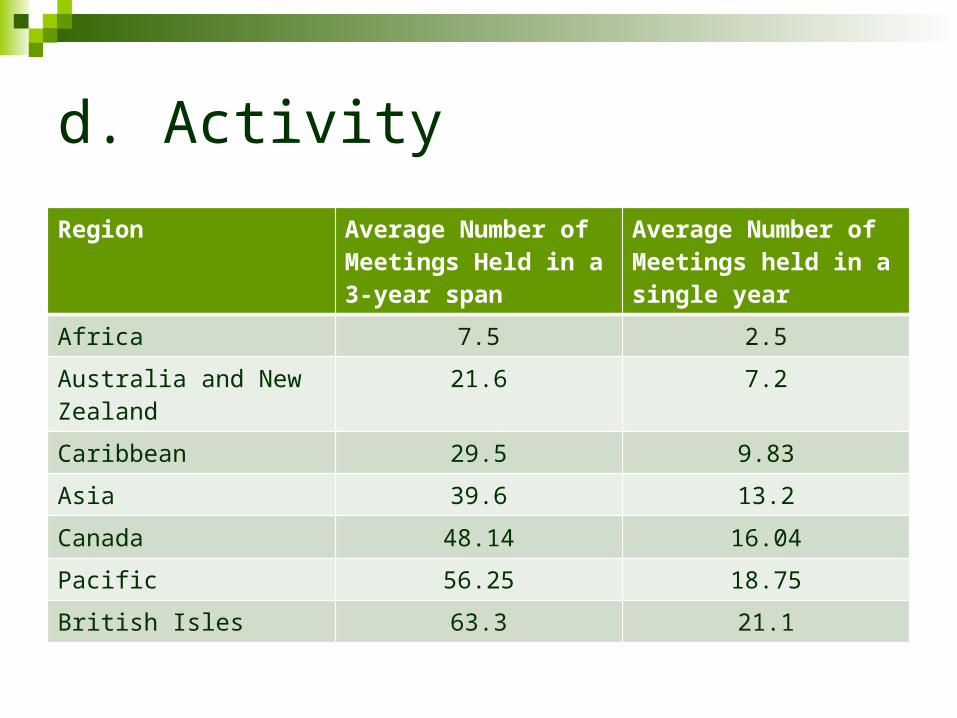

Region Average Number of Meetings Held in a 3-year span

Average Number of Meetings held in a single year

Africa 7.5 2.5

Australia and New Zealand

21.6 7.2

Caribbean 29.5 9.83

Asia 39.6 13.2

Canada 48.14 16.04

Pacific 56.25 18.75

British Isles 63.3 21.1

… Activity (Con’td)

We’ll hear tomorrow how many committee hearings and reports are produced by PACs

Concluding remarks

External audit and parliamentary scrutiny of audit findings are fundamental for holding government to account.

Supreme audit institutions have evolved according to different traditions. The audit court and auditor general models are the two main types, but there are variations and hybrids.

The independence of supreme audit institutions has been recognized as a core fundamental of effective audit.

Parliament can engage with audit findings most effectively through dedicated committee capacity.

Devising sound review and follow-up mechanisms is important for parliament to ensure that recommendations are actually implemented to improve public spending and administration.