earnings management and annual report readability · pdf file1 earnings management and annual...

TRANSCRIPT

1

Earnings management and annual report readability

Kin Lo* Sauder School of Business

The University of British Columbia Vancouver, BC, Canada

Felipe Ramos FUCAPE Business School

Vitoria, ES, Brazil

and

Rafael Rogo Sauder School of Business

The University of British Columbia Vancouver, BC, Canada

September 2014

Abstract We explore how the readability of annual reports varies with earnings management. Using the Fog Index to measure readability (Li 2008), and focusing on the management discussion and analysis section of the annual report (MD&A), we predict and find that firms that are most likely to have managed earnings to beat the prior year’s earnings have MD&As that are more difficult to read. In addition, we find that readability has marginal but incremental power in predicting financial misstatements when added to the F-Score model of Dechow et al. (2011) Key Words: Annual report readability, profitability, earnings management JEL Classification: D82; G14; G18; M41; M45

We appreciate the helpful comments from our colleagues at UBC. Funding was provided in part by the Institute of Chartered Accountants of BC and the Social Sciences and Humanities Research Council. * Contact author: Ph. 604-822-8430; Email: [email protected]; Mail: 2053 Main Mall, Vancouver, BC, Canada, V6T 1Z2

2

1. INTRODUCTION

The seminal work of Li (2008) explored the relationship between the readability of annual

reports and financial performance. Borrowing the Fog Index from computation linguistics, where

a higher reading on the Fog Index indicates disclosures that are more difficult to understand, Li

finds a negative relationship between Fog and the level of earnings. It is unclear whether this

result is due to managers providing complex disclosures to obfuscate bad performance or that

bad news is simply harder to be communicated (Bloomfield, 2008). To further explore these two

explanations and to better understand managers’ use of complex disclosures, we look at instances

in which firms are more likely to have managed earnings upwards to meet or beat an earnings

benchmark (Burgstahler and Dichev, 1997). When financial performance is achieved partly by

earnings management, we expect the explanations management provides for that performance

will be less readable than explanations provided by firms not engaging in earnings management.

In other words, we expect that when reported performance differs from underlying fundamentals,

we expect managers to try to make it harder for investors to identify such earnings management

behavior. Our results suggest that the readability level of financial disclosures goes beyond the

one derived from the ontological explanation of good vs. bad news being disclosed. Instead, we

find that managers strategically use corporate disclosure to mislead or to influence investors’

understanding of firm’s value.

Our study is motivated by the importance and richness of the textual component of

financial disclosures—an average of 80% of an annual report, for instance. The SEC highlighted

the importance of textual disclosures when it issued a set of rules requiring plain English

disclosures. Christopher Cox, Chairman of the SEC, went further and suggested “just as the

Black-Scholes model is commonplace when it comes to compliance with the stock option

compensation rules, we may soon be looking to the Gunning-Fog and Flesch-Kincaid models to

3

judge the level of compliance with the plain English rules.” If readability is going to be used as a

measure of compliance, then we should understand the factors that affect it how managers

choose it.

Our analysis focuses on the readability of the management discussion and analysis

(MD&A) section of the annual report—a section in which managers have discretion on how to

present an explanation of the company’s business, financial conditions, and results of operation.

The earnings benchmark we use is the prior year’s earnings because anecdotal evidence suggests

that management’s discussions in the annual report are more likely to compare and contrast

performance in the current fiscal year with that in the prior year or years. Forecasted earnings,

whether by sell-side analysts or by management, are seldom referenced in annual reports.

Our findings are consistent with our hypotheses. Controlling for the relationship between

Fog and the overall earnings level as well as other known factors, we find robust evidence that

Fog is higher for firms that meet or just beat prior year’s earnings (MBE). We further identify

firms in the MBE sample that are more likely to have managed accruals and find consistently

higher Fog for this subgroup but not for other MBE firms.

In addition to exploring whether firms that manage earnings have less readable financial

reports, we turn the analysis on its head and test whether readability predicts financial

misstatements along the lines of Dechow et al. (2011). We find that the Fog Index is a marginal

but statistically significant predictor when added to the F-score model of Dechow et al.

Our contribution to the literature is two-fold. First, we refine the overall relationship

between readability and financial performance. While the overall pattern documented by Li

(2008) is one where higher earnings associates with lower Fog, we provide evidence that this

relationship is discontinuous (or at least non-monotonic) around the benchmark of the prior

4

year’s earnings, particularly for firms that are likely to have managed accruals. Second, we show

that earnings management, that is, using accounting discretion with the aim of concealing

underlying performance, manifests itself as more complex disclosures. Our evidence is

consistent with managers strategically choosing higher reporting complexity in conjunction with

earnings management in an attempt to conceal the latter, which is a new finding in the literature.

Overall, we add to a more complete understanding of the relationship between financial report

readability and reported performance.

The remainder of this paper is organized as follows. The next section describes our

hypotheses. Sections 3 and 4 contain our analyses of the first and second hypotheses,

respectively. Section 4 concludes.

2. HYPOTHESIS DEVELOPMENT

In computational linguistics, the Gunning Fog Index, or just Fog Index, is a function of the

number of words per sentence plus the percentage of words that are complex (i.e., having three

or more syllables). This sum is scaled by a constant (0.4) such that the Fog value approximates

the number of years of formal education required to understand the text.

The Fog Index was first brought into the accounting literature by Li (2008), who

examined how readability of annual reports varies with financial performance. Li found a

negative relationship between profitability and Fog (i.e., profitable firms have more readable

reports compared with firms with losses). He also found that firms with more persistent positive

earnings have lower Fog.

In the discussion of Li (2008), Bloomfield (2008) provides a number of potential

explanations for the observed relationships between readability and financial performance. Two

are particularly salient here. First is obfuscation—that managers try to hide bad news by writing

5

text that is more difficult to decipher. Second is ontology—that bad news is inherently more

difficult to communicate.

Bloomfield provides two other potential explanations that could also be considered

variation of ontology. He suggests that loss firms need to provide more explanation as a result of

“management by exception.” He also suggests that the nature of accounting conservatism—

recognizing bad news in a more timely fashion than good news—requires managers to provide

more explanation about the future when there are losses. In sum, obfuscation requires conscious

actions to affect readability, whereas the ontological explanations suggest that readability is

inherently a function of the circumstances. As will be seen below, our analyses will have bearing

on these two explanations.

With regard to financial performance, there is a substantial literature documenting the

frequency, motivations, and benefits that accrue to firms that are able to meet or beat

benchmarks. In recent decades, some two-third to three-quarters of firms will meet or beat

expectations in the capital market (as proxied by analyst forecasts). The rewards of doing so are

higher stock returns, lower information asymmetry, and lower cost of capital (Bartov et al., 2002;

Brown et al., 2009). These firm-level effects translate into personal benefits via executive

compensation directly through higher stock and option value or indirectly through discretionary

bonuses.

The incentives for management to meet or beat earnings benchmarks also lead some

managers to use their accounting discretion to achieve their performance. For instance,

Burghstahler and Dichev (1997) document unusually low (high) frequencies of firms reporting

small earnings decreases (increases) and small losses (profits), suggesting that earnings

management is the source of these irregular distributions of earnings outcomes.

6

Depending on the context, some benchmarks will be more salient than others. In the

capital market context, the expectations in the market is the most relevant—meeting or falling

short of the market’s expectations is what determines changes in stock prices. In other instances,

zero earnings is the relevant benchmark—maintaining a positive level of earnings is important

for reasons of contractual provisions and general loss aversion, for examples. A third benchmark

is the prior year’s performance, which is equivalent to a benchmark of zero change in earnings.

We focus on the third benchmark for two reasons. First, our analysis of readability

focuses on annual reports, and the MD&A section in particular. MD&A is a disclosure required

by the Securities and Exchange Commission (SEC).1 As a regulated disclosure, it is reasonable

to expect management to discuss facts and figures that are already contained in the audited

financial statements and elsewhere in the annual report rather than information from the capital

markets, such as analyst forecasts, which can change frequently. Second, the requirement to

comment on trends suggests that management would rather have a zero or positive earnings

change rather than having to explain a decline in earnings, which could arguably be interpreted

as the beginning of a downward trend. Third, we focus on the zero earnings change benchmark

rather than the zero earnings benchmark to obtain more time-series variation in meeting/beating

vs. missing the benchmark. That is, there are some firms that are persistently profitable while

others are persistently not.

While the relationship between Fog and earnings levels documented by Li (2008) is

overall negative, we expect that firms at or just above the zero earnings change benchmark will

tend to show a different relationship. First, if at least some of the firms in this region of earnings

performance are able to do so via upward earnings management, then the underlying

1 The MD&A disclosure is required by SEC Regulation S-K, Item 303. Among other things, it requires registrants to discuss financial condition, results of operation, and “currently known trends, events, and uncertainties …” (Securities Act Release No. 6835, May 18, 1989).

7

performance that they would have otherwise reported would have been lower, which would have

a commensurately higher Fog. That is, all else equal, the readability for the underlying

performance is lower than for the reported performance. Second, earnings management involves

degrees of untruth. Within the accounting discretion available, management makes biased

choices to increase earnings. In some cases the earnings management falls outside acceptable

levels and is considered (fraudulent) misrepresentation. In either case, management must try to

hide the deception so as not to be discovered. Deceptive communication is linguistically more

complex and also cognitively more demanding.2

Based on the above discussion, our first hypothesis is as follows (stated in alternative

form):

H1: Firms that have managed earnings have annual report disclosures that are less readable, ceteris paribus.

Beyond this general hypothesis, we have three subsidiary hypotheses with increasing specificity:

H1A: Firms with zero or slightly positive earnings changes will have annual report disclosures that are less readable, ceteris paribus.

H1B: Firms with (i) zero or slightly positive earnings changes and (ii) positive discretionary accruals will have annual report disclosures that are less readable, ceteris paribus.

H1C: Firms with (i) zero or slightly positive earnings changes and (ii) high positive discretionary accruals will have annual report disclosures that are less readable, ceteris paribus.

The idea that deception results in more complex writing leads to our second hypothesis.

Dechow et al. (2011) used the sample of firms reporting restatements in Accounting and

Auditing Enforcement Releases (AAER) published by the SEC to estimate a model that

produced a likelihood of financial misstatement (“F-Score”). Along with this model, we

2 “… from a cognitive perspective, truth tellers should be able to discuss exactly what did and did not happen because they were actually there to witness the event being discussed. Liars, on the other hand, would be forced to keep track of what they have previously said to avoid contradicting themselves later” (Hancock et al., 2007).

8

hypothesize that writing complexity can be used as a factor to help identify firms misstating

financial statements. Our second hypothesis is as follows:

H2: Firms with less readable financial reports are more likely to have misstated financial statements.

In the next two sections, we describe our empirical analyses and results of testing these

two hypotheses.

3. TEST OF HYPOTHESIS 1

To test the first hypotheses, we use a sample of firm-years with available data between 2000 and

2012. We require financial data from Computat as well as MD&A disclosures on the SEC’s

Edgar system. Details of required financial data items will be provided below. We exclude firms

in the utilities and financial services industries (SIC 4400-5000 and 6000-6999). Table 1 shows

the results of the sample selection procedure. The final sample consists of 26,967 firm-years and

4,855 unique firms.

The first hypothesis concerns the influence of earnings management on readability. To

test this hypothesis, we require measures of readability, earnings management, and control

variables that are known to affect readability. Therefore, the general form of equation we use to

test this hypothesis is as follows:

𝑅𝑒𝑎𝑑𝑎𝑏𝑖𝑙𝑖𝑡𝑦 = 𝛽! + 𝛽!𝐸𝑀 + 𝛽!𝐶𝑜𝑛𝑡𝑟𝑜𝑙! + 𝜀 (1)

where EM refers to the earnings management proxy. The follow discussion provides additional

details for this equation.

3.1 Readability

We use the Gunning Fox Index to measure readability. As mentioned above, the Fog Index is

computed as follows:

9

𝐹𝑜𝑔 = 0.4 × 𝑤𝑜𝑟𝑑𝑠 𝑝𝑒𝑟 𝑠𝑒𝑛𝑡𝑒𝑛𝑐𝑒 + 𝑝𝑒𝑟𝑐𝑒𝑛𝑡 𝑜𝑓 𝑐𝑜𝑚𝑝𝑙𝑒𝑥 𝑤𝑜𝑟𝑑𝑠 . (2)

The number of words per sentence is computed as the ratio of the total number of words divided

by the number of sentences. Complex words are those having three or more syllables. Longer

sentences and a higher proportion of complex words increase Fog, meaning a reduction in

readability. The Fog Index has been used widely and has seen increasing usage in the accounting

literature (e.g., Miller, 2010; Lehavy et al., 2011).

3.2 Earnings management

We use a number of different proxies for earnings management. Our first and simplest measure

uses the approach of Burgstahler and Dichev (1997): we identify firms having a higher

likelihood of managing earnings as those firms with earnings in the neighborhood of meeting or

just beating past year’s earnings. We conduct our main tests using earnings per share (EPS), but

we also present results for earnings deflated by total assets. In either case, we measure earnings

before extraordinary items. We define the variable MBE = 1 if ΔEPS falls in the neighborhood

from zero to a small positive number; otherwise MBE = 0. We use a range of values to define the

“small positive number” to ensure robustness of results.

Our second measure of earnings management uses the sign of discretionary accruals. In

our main tests, we use the Jones (1991) model:

𝐷𝐴 = 𝛼! + 𝛼!(1 𝑇𝐴!!!)+𝛼! ΔRev! 𝑇𝐴!!! + 𝛼!(𝑃𝑃𝐸! 𝑇𝐴!!!). (3)

where ΔRevt is the change in revenues from year t-1 to t, PPEt is gross property, plant, and

equipment, and TAt-1 is total assets at the end of year t-1. In supplementary tests, we also use the

modified Jones model from Dechow et al. (1995) and the performance-matched model of

Kothari et al. (2005) with similar results as reported below. We estimate each model cross-

sectionally by industry and year, and require at least 15 observations.

10

Discretionary accrual models have large amounts of measurement error and suffer from

low power (Dechow et al., 1995). We do not simply use the discretional accrual measure as our

proxy for earnings management. Rather, we interact discretionary accruals with our first

measure, MBE, to increase the power of detecting firms that have managed earnings.

Furthermore, managing earnings to meet or beat past earnings presumably involves upward

earnings management, so we focus on positive discretionary accruals, which we label as PosDA

(and the complement is NegDA). Therefore, our second measure to identify firms that are likely

to have managed earnings upwards is MBE × PosDA.

Our third measure of earnings management refines the second one just described but

using not only the sign of discretionary accruals, but also the magnitude. We separate firms with

positive discretionary accruals into high and low partitions using the median value, resulting in

HighPosDA and LowPosDA. Our third measure of firms most likely to have managed earnings

upwards is thus MBE × HighPosDA.

3.3 Control variables

Our list of control variables derives from Li (2008). The most important of these in our context

are the earnings-related variables. The first is Earnings, which is the level of earnings reported,

which is expected to be negatively associated with Fog (i.e., firm-years with high earnings have

more readable MD&A) based on Li (2008). Depending on the specification, Earnings is either

EPS before extraordinary items, or earnings before extraordinary items deflated by beginning

total assets. Closely related in the variable NegEarnChg, which equals 1 if the change in

Earnings is negative.

We include all of the 12 other control variables used in Li (2008). We provide details for

these variables in Appendix A.

11

3.4 Descriptive statistics

Table 2 shows the sample statistics. The mean and median value of Fog is around 18, meaning

that the typical MD&A requires two years beyond an undergraduate degree. This value is similar

to that reported in Li (2008), where the mean and median were 18.23 and 17.98, respectively. On

average, firms increase EPS by five to six cents year-over-year.

Table 3 shows the correlation matrix for the variables. Fog negatively correlates with

firm size (Size) and number of geographic segments (NGSeg) and positively correlates with

market-to-book (MTB), with magnitude around 10%. The signs of these correlations are

consistent with Li (2008).3 While there are many correlations among the variables that are

statistically significant due to our large sample size, the magnitudes are mostly modest and

should not pose a problem with multicollinearity.

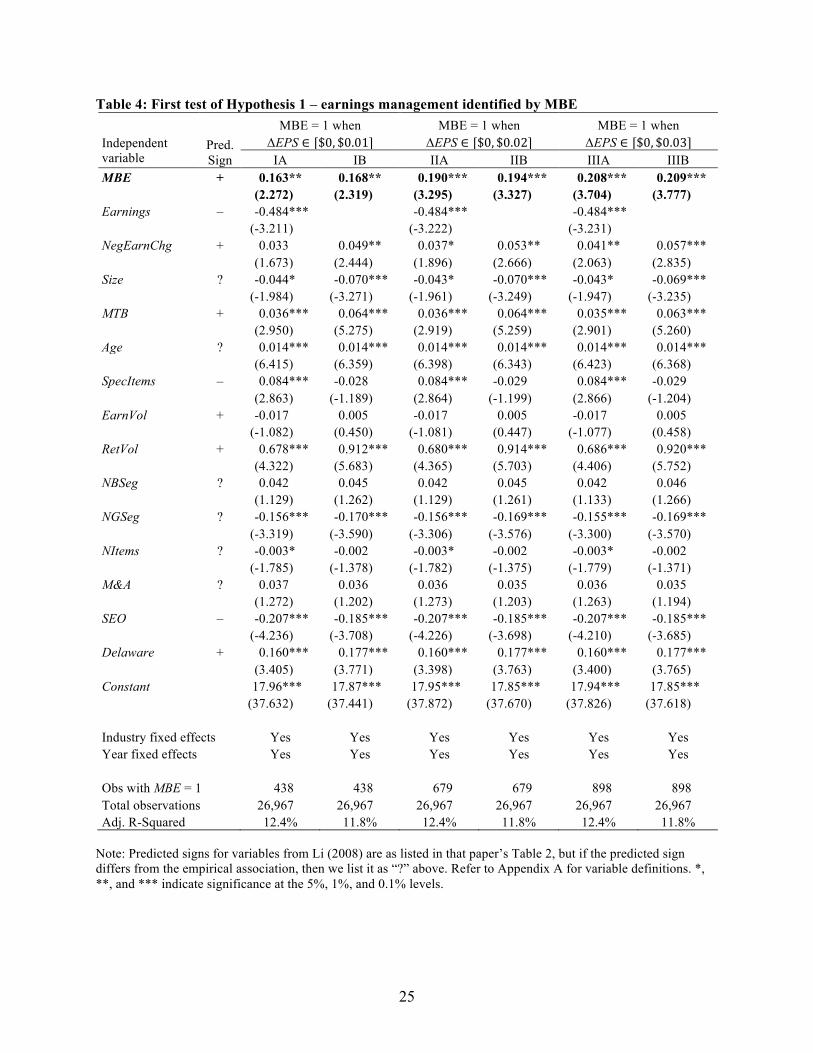

3.5 Results – Test of Hypothesis 1A

Table 4 presents our first test of Hypothesis 1. The definition of EM in Equation (1) in this

analysis is whether a firm met or beat past year’s earnings. That is, we identify firms with zero or

small positive earnings changes as having a higher likelihood of having managed earnings. We

use three different definitions of “small positive,” being one, two, or three cents of EPS before

extraordinary items.

The key variable is MBE, which has a significantly positive coefficient (coefficient =

0.163 to 0.209, t = 2.27 to 3.78). Firms that met or just beat prior year’s EPS had MD&A that

were more complex to read by about a fifth or sixth of a year of formal education. This analysis

controls for other determinants of Fog identified in Li (2008, Table 2) as well fixed effects for

industry and year. Standard errors are clustered by industry as in Li (2008). We also control for

3 Li (2008) did not report a correlation table. We use the multivariate regression report in Li’s Table 2 to compare with out bivariate correlations, even though strictly they are not comparable.

12

whether a firm had a negative earnings change (NegEarnChg); missing the benchmark of the

past year’s earnings is bad news and the results from Li (2008) suggest that bad news is

associated with more complex reports. The coefficient on this variable is significantly positive as

expected (coefficient = 0.033 to 0.057, t = 1.67 to 2.84), but more modest in magnitude

compared with the coefficient on MBE. In addition, we control for the level of earnings with the

variable Earnings. However, since this analysis in Table 4 uses EPS, undeflated, the magnitudes

for this variable are difficult to interpret because of varying share sizes, so we show results with

the Earnings variable in three columns and without in the other three. As expected, the

coefficient is negative, meaning that more profitable firms have less complex MD&A.

Overall, this first result, at least for MBE firms, is inconsistent with a purely ontological

explanation, given that firms with relatively good news have MD&A section that is less readable

than firms disclosing worse news.

To address the scale issue related to using EPS, we show results of measuring

profitability as earnings before extraordinary items deflated by total assets. Table 5 Panel A

shows the results of this analysis, with MBE defined to equal 1 when deflated earnings is from

zero to 0.4%, 0.5% or 0.6%. For brevity, we do not report the coefficients for the control

variables. Similar to Table 4, we find results as expected. The coefficient on MBE ranges from

0.127 to 0.137, somewhat smaller than in Table 4 but significant at the 1% level or better (t =

2.75 to 3.44). The coefficient on NegEarnChg is also positive as expected, but again

substantially smaller in magnitude compared with the coefficient on MBE.

We also conduct a placebo test to confirm that the results found are not spurious. In

particular, we want to reduce the possibility that some unmodelled factors omitted from our

analysis but correlated with the propensity to meet/beat explain the variation in MD&A

13

readability. To this end, we include MBEt-1 to see if meeting or beating in the prior year is at all

associated with current MD&A readability. Table 5 Panel B shows that the coefficient on MBEt-1

is not significantly different from zero (t = 0.445), while the coefficient on MBEt continues to be

significantly positive and with similar magnitudes as in Table 4.

Overall, the adjusted R-squared values in both Tables 4 and 5 are around 12%, which are

similar but slightly higher than the 10% reported in Li (2008). The results so far support

Hypothesis 1A. We find consistent evidence that, while falling short of past year’s earnings is

associated with slightly more complex MD&A, meeting or just beating is associated even more

complex reports. The ontology explanation suggests that it is possible and even likely that bad

new is inherently more difficult to explain. Our evidence suggests that the good new of meeting

or just beating past earnings is even harder to explain, which is contrary to the ontological

explanation. This result could arise if the good news is artificial and some amount of obfuscation

is required to make the underlying performance less transparent. We investigate this possibility

further in the next tests of H1B and H1C.

3.6 Results – tests of Hypotheses 1B and 1C

Considering only whether a firm met of just beat the prior year’s earnings as we did in the test of

H1A involves misclassifying firms that would have met or just beat prior year’s earnings without

any earnings management. To improve the identification of firms that are more likely to have

managed earnings, we consider also estimates of firms’ discretionary accruals in addition to

whether it met or beat prior earnings. Table 6 shows the results of regressing Fog on MBE

interacted with PosDA (positive discretionary accruals), as well as the main effect for PosDA and

control variables. The results are as predicted: MBE × PosDA is significantly positive

(coefficient = 0.299 to 0.335, t = 3.56 to 5.25). Firms that are likely to have used earnings-

14

increasing discretionary accruals to meet or beat prior earnings have less readable MD&A. The

magnitudes of the coefficient are about 1.5 to 2 times as large as those estimated in Table 4 for

MBE. Consistent with this larger magnitude, we find the coefficient for MBE × NegDA to be

insignificant; that is, the effect found in Table 4 is concentrated in the subset with positive

discretionary accruals. Firms that met or just beat prior earnings but have negative discretionary

accruals do not exhibit more complex MD&A. This evidence supports Hypothesis 1B.

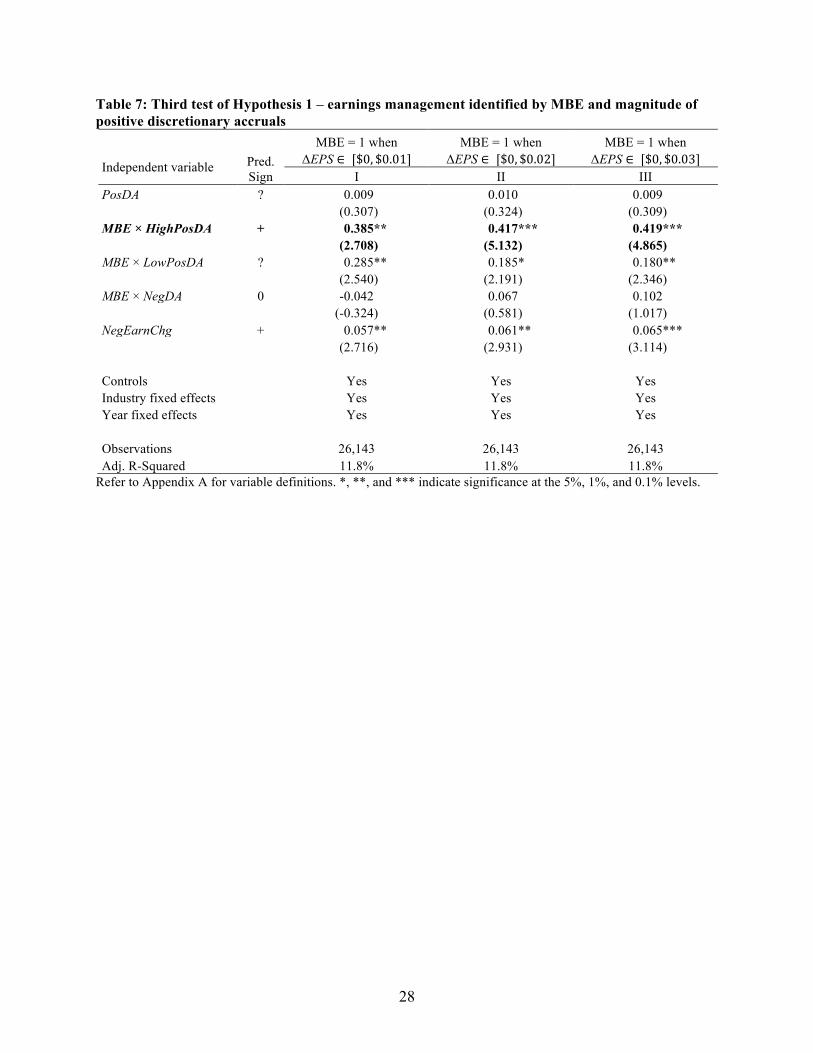

We further refine the definition of earnings management by identifying firms that have

highly positive vs. less positive discretionary accruals by splitting at the median value of PosDA,

resulting in HighPosDA and LowPosDA. Table 7 shows these results. The coefficients for MBE

× HighPosDA are significantly positive (coefficient = 0.385 to 0.419, t = 2.71 to 5.13),

supporting H1C. The magnitudes are larger than the corresponding coefficients from Table 6 by

about one-third, consistent with our expectations. The coefficients for MBE × LowPosDA are

also significantly positive, with smaller magnitudes than for the firms with high positive

discretionary accruals (less than half as large in two of the three specifications). These results

suggest that those firms most likely to have used income-increasing discretionary accruals to

meet or beat prior performance have MD&A reports that are more complex by about 40% of a

year of formal education, which is a material difference.

3.7 Supplemental robustness tests

We conduct three robustness checks to confirm our results above. For brevity, we present results

based on the most specific definition of earnings management we just used to test H1C (i.e.,

using MBE × HighPosDA). Table 8 shows these results. Panel A shows regression estimates

when we include firm-level fixed effects. This specification is likely to be overly conservative if

firms repeatedly manage earnings and that activity is reflected in lower readability, bringing up

15

the average Fog value for such firms. Nevertheless, the magnitude of the coefficient on MBE ×

HighPosDA decreases but remains significantly positive. The coefficient on MBE × LowPosDA

is no longer significant. Panel B uses the modified Jones model of Dechow et al. (1995) to

measure discretionary accruals, and the results remain essentially the same as those reported in

Table 7, which uses the simpler Jones (1991) model. Panel C uses the performance-matched

accrual model of Kothari et al. (2005). Again, the results are very similar to those reported in

Table 7 except that the coefficient on MBE × LowPosDA is no longer significant, which is

similar to what was found with firm-level fixed effects in Panel A.

In sum, we find consistent and robust evidence supporting Hypothesis 1 with different

definitions of earnings management, different accrual models, controlling for different fixed

effects, and using a placebo test. Next we examine whether readability is predictive of financial

misstatements.

4. TEST OF HYPOTHESIS 2

Hypothesis 2 predicts that firm-years with less readable financial reports are more likely to have

misstated financial statements. To test this hypothesis, we continue to focus on the readability of

MD&A as above. For the misstatements, we use the information provided in Accounting and

Auditing Enforcement Releases (AAER) issued by the SEC. Table 9 shows how we obtain the

216 firm-years of misstatement observations used in out tests. The frequency of the

misstatements peaked at 39 cases in the year 1999, and has been markedly less frequent in the

latter years.

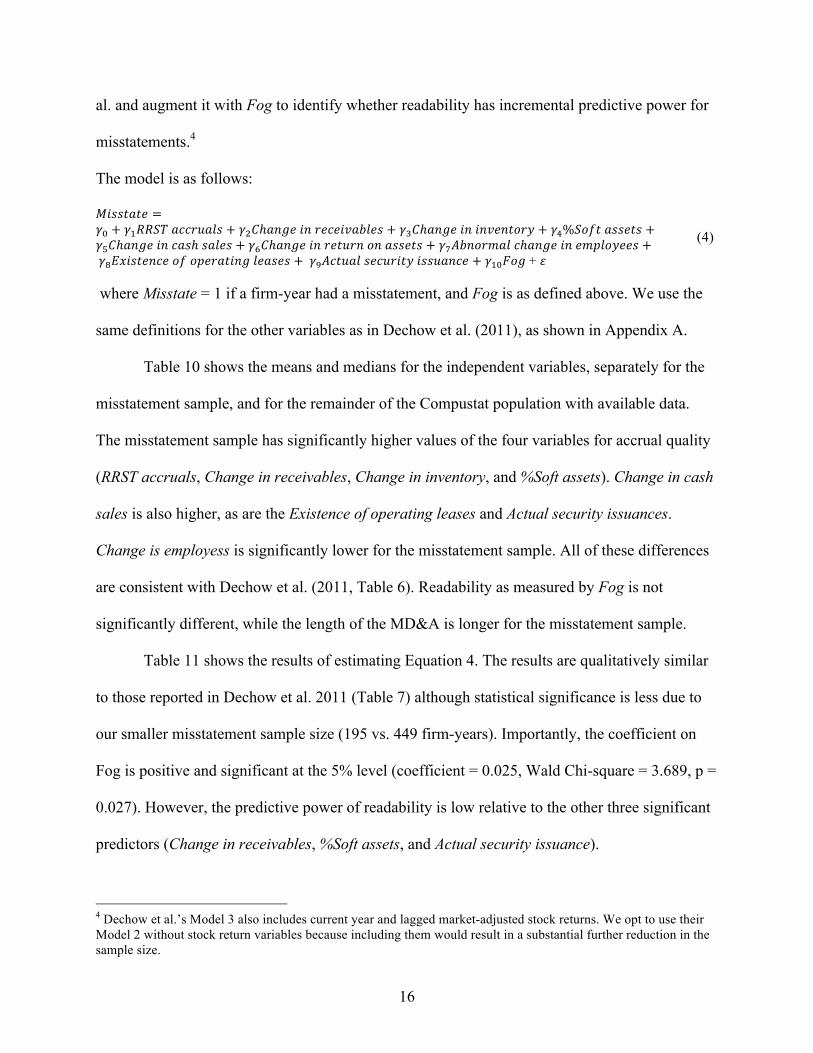

4.1 Model of misstatement

To test whether low readability is predictive of misstatements, we use the model F-Score model

of Dechow et al. (2011). Specifically, we use the variables in Model 2 of Table 7 of Dechow et

16

al. and augment it with Fog to identify whether readability has incremental predictive power for

misstatements.4

The model is as follows:

𝑀𝑖𝑠𝑠𝑡𝑎𝑡𝑒 =𝛾! + 𝛾!𝑅𝑅𝑆𝑇 𝑎𝑐𝑐𝑟𝑢𝑎𝑙𝑠 + 𝛾!𝐶ℎ𝑎𝑛𝑔𝑒 𝑖𝑛 𝑟𝑒𝑐𝑒𝑖𝑣𝑎𝑏𝑙𝑒𝑠 + 𝛾!𝐶ℎ𝑎𝑛𝑔𝑒 𝑖𝑛 𝑖𝑛𝑣𝑒𝑛𝑡𝑜𝑟𝑦 + 𝛾!%𝑆𝑜𝑓𝑡 𝑎𝑠𝑠𝑒𝑡𝑠 +𝛾!𝐶ℎ𝑎𝑛𝑔𝑒 𝑖𝑛 𝑐𝑎𝑠ℎ 𝑠𝑎𝑙𝑒𝑠 + 𝛾!𝐶ℎ𝑎𝑛𝑔𝑒 𝑖𝑛 𝑟𝑒𝑡𝑢𝑟𝑛 𝑜𝑛 𝑎𝑠𝑠𝑒𝑡𝑠 + 𝛾!𝐴𝑏𝑛𝑜𝑟𝑚𝑎𝑙 𝑐ℎ𝑎𝑛𝑔𝑒 𝑖𝑛 𝑒𝑚𝑝𝑙𝑜𝑦𝑒𝑒𝑠 + 𝛾!𝐸𝑥𝑖𝑠𝑡𝑒𝑛𝑐𝑒 𝑜𝑓 𝑜𝑝𝑒𝑟𝑎𝑡𝑖𝑛𝑔 𝑙𝑒𝑎𝑠𝑒𝑠 + 𝛾!𝐴𝑐𝑡𝑢𝑎𝑙 𝑠𝑒𝑐𝑢𝑟𝑖𝑡𝑦 𝑖𝑠𝑠𝑢𝑎𝑛𝑐𝑒 + 𝛾!"𝐹𝑜𝑔 + 𝜀

(4)

where Misstate = 1 if a firm-year had a misstatement, and Fog is as defined above. We use the

same definitions for the other variables as in Dechow et al. (2011), as shown in Appendix A.

Table 10 shows the means and medians for the independent variables, separately for the

misstatement sample, and for the remainder of the Compustat population with available data.

The misstatement sample has significantly higher values of the four variables for accrual quality

(RRST accruals, Change in receivables, Change in inventory, and %Soft assets). Change in cash

sales is also higher, as are the Existence of operating leases and Actual security issuances.

Change is employess is significantly lower for the misstatement sample. All of these differences

are consistent with Dechow et al. (2011, Table 6). Readability as measured by Fog is not

significantly different, while the length of the MD&A is longer for the misstatement sample.

Table 11 shows the results of estimating Equation 4. The results are qualitatively similar

to those reported in Dechow et al. 2011 (Table 7) although statistical significance is less due to

our smaller misstatement sample size (195 vs. 449 firm-years). Importantly, the coefficient on

Fog is positive and significant at the 5% level (coefficient = 0.025, Wald Chi-square = 3.689, p =

0.027). However, the predictive power of readability is low relative to the other three significant

predictors (Change in receivables, %Soft assets, and Actual security issuance).

4 Dechow et al.’s Model 3 also includes current year and lagged market-adjusted stock returns. We opt to use their Model 2 without stock return variables because including them would result in a substantial further reduction in the sample size.

17

5. DISCUSSION AND CONCLUSION

This paper extends the readability analysis of Li (2008). Beyond the overall negative relations

between the Fog Index and financial performance (i.e., the positive relationship between

readability and performance), we hypothesize and document a disruption to that overall pattern.

In the region where a firm meets or just beats the prior year’s earnings, the Fog score increases

and readability deteriorates. The effect is larger when we focus on subsets of firms within this

neighborhood of earnings performance that are more likely to have engaged in accruals

management to increase earnings. Overall, we find consistent and robust evidence that firms that

are likely to have managed earnings to meet or beat the benchmark of the prior year’s earnings

on average have more complex MD&A reports. Using the F-Score model of Dechow et al.

(2011), we also show that the Fog Index has marginal predictive power incremental to known

predictors.

If the ontological explanation proposed by Bloomfield (2008) were a sufficient

explanation (i.e., that good performance is inherently easier to communicate than bad

performance), then we should not observe the pattern we found. Our evidence suggests that, at

least for firms that are most suspected of having managed earnings, obfuscation is involved in

making the financial report more difficult to read.

Our results are also consistent with the commonly held belief, supported by empirical

evidence, that telling the truth is easier than telling lies (Hancock et al., 2007). Lying is difficult

if it is to be convincing because the communicator has to ensure the consistency of the supposed

“facts.” While earnings management in many cases do not outright fall into the category of lying,

the activity does involve some active efforts on the part of management to bias the financial

statements through accruals or other means. Such actions create a discrepancy between

unmanaged performance and reported performance which can make it mentally more taxing to

18

explain reported performance when management knows the underlying unmanaged performance.

Earnings management also challenges managers’ ethical standards, which again can cause

cognitive stress, which can be indirectly connected to readability of their written words.

Further research can go beyond readability and explore how the specific content of the

MD&A relates to benchmark beating and earnings management. For instance, do firms suspected

of having managed earnings use a more passive writing style or different pronouns? Another

avenue is to investigate other earnings benchmarks and the corresponding disclosures that would

focus on those benchmarks (e.g., meeting or beating market expectations and conference calls).

19

Appendix A Variable definitions

Readability variables

Fog = 0.4 × (words per sentence + percent of complex words).

Length = natural log of the number of words in the MD&A section of the annual report.

Variables in test of Hypothesis 1

ΔEPS = change in EPS from year t-1 to t.

MBE = 1 if ΔEPS falls in the neighborhood from zero to a small positive number; 0 otherwise. (The small positive number is identified in each test.)

PosDA = 1 if discretionary accruals ≥ 0; otherwise 0. Discretionary accruals are estimated using the Jones (1991) model, the modified Jones model of Dechow et al. (1995), or the performance-matched model of Kothari et al. (2005).

HighPosDA = 1 if DA > median(DA | DA≥0); otherwise 0.

Earnings = EPS before extraordinary items (or earnings before extraordinary items deflated by total assets)

NegEarnChg = 1 if ΔEarnings < 0.

Size = log of market value of equity at fiscal year-end.

MTB = (market value of equity + book value of liabilities) / book value of total assets, measured at the end of the fiscal year.

Age = number of years since a firm first appears in the CRSP monthly stock return file.

SpecItems = amount of special items divided by total assets.

EarnVol = standard deviation of operating earnings during the prior five years.

RetVol = standard deviation of monthly stock returns in the prior year.

NBSeg = natural log of the number of business segments.

NGSeg = natural log of the number of geographic segments.

NItems = number of items in Compustat with non-missing values.

M&A = 1 for firm-years in which a company is an acquirer according to SDC Platinum M&A database.

20

SEO =1 for firm-years in which a company has a seasoned equity offering according to SDC Global New Issues database; 0 otherwise.

Delaware = 1 if the firm is incorporated in Delaware; 0 otherwise.

Variables in test of Hypothesis 2

Variable Calculation Accrual quality variables RSST accruals (ΔWC + ΔNCO + ΔFIN) / Average total assets, where

WC = [Current Assets (DATA 4) – Cash and Short-term Investments (DATA 1)] – [Current Liabilities (DATA 5) – Debt in Current Liabilities (DATA 34)];

NCO = [Total Assets (DATA 6) – Current Assets (DATA 4) – Investments and Advances (DATA 32)] – [Total Liabilities (DATA 181) – Current Liabilities (DATA 5) – Long-term Debt (DATA 9)];

FIN = [Short-term Investments (DATA 193) + Long-term Investments (DATA 32)] – [Long-term Debt (DATA 9) + Debt in Current Liabilities (DATA 34) + Preferred Stock (DATA 130)]; following Richardson et al. 2005.

Change in receivables

ΔAccounts Receivable (DATA 2) / Average total assets

Change in inventory

ΔInventory (DATA 3) / Average total assets

%Soft assets (Total Assets (DATA 6) - PP&E (DATA 8) - Cash Equivalent (DATA 1)) / Total Assets (DATA 6)

Performance variables Change in cash sales

Percentage change in cash sales [Sales (DATA 12) – ΔAccounts Receivable (DATA 2)]

Change in return on assets

[Earningst (DATA 18) / Average total Assetst] - [Earningst-1 (DATA 18) / Average total Assetst-1]

Market-related incentives Actual security issuance

An indicator variable coded 1 if firm issued securities during year t (i.e., an indicator variable coded 1 if DATA 108 > 0 or DATA 111 > 0)

Nonfinancial variables Abnormal change in employees

Percentage change in the number of employees (DATA 29) – Percentage change in Assets (DATA 6)

Off-balance-sheet variables Existence of operating leases

An indicator variable coded 1 if future operating lease obligations are greater than zero

Note: “RSST” refers to the accrual model of Richarson, Sloan, Soliman, and Tuna (2005).

21

References Bartov, E., D. Givoly, C. Hayn, 2002. The rewards to meeting or beating earnings expectations.

Journal of Accounting and Economics 33, 173-204.

Bloomfield, R.J., 2008.Discussion of “Annual report readability, current earnings, and earnings persistence”. Journal of Accounting and Economics 45, 248-252.

Bradshaw, M., S. Richardson, R.G. Sloan, 2001. Do analysts and auditors use information in accruals? Journal of Accounting Research 39, 45-74.

Brown, S., S.A. Hillegeist, K. Lo, 2009. The effect of earnings surprises on information asymmetry. Journal of Accounting and Economics 47, 208-225.

Burgstahler, D., I. Dichev, I., 1997. Earnings management to avoid earnings decreases and losses. Journal of Accounting and Economics 24, 99-126.

Dechow, P.M., I. Dichev, 2002. The quality of accruals and earnings: the role of accrual estimation errors. The Accounting Review 77, 35-39.

Dechow, P.M., W. Ge, C.R. Larson, R.G. Sloan, 2011. Predicting material accounting misstatements. Contemporary Accounting Research 28, 17-82.

Dechow, P., R.G. Sloan, A. Sweeney, 1995. Detecting Earnings Management. The Accounting Review 70, 193-225.

Hancock, J.T., L.E. Curry, S. Goorha, M. Woodworth, 2007. On lying and being lied to: A linguistic analysis of deception in computer-mediated communication. Discourse Processes 45, 1-23.

Jones, J., 1991. Earnings management during import relief investigation. Journal of Accounting Research 29, 193-228.

Kothari, S.P., A.J. Leone, C.E. Wasley, 2005. Performance matched discretionary accrual measures. Journal of Accounting and Economics 39, 163-197.

Lang, M., R. Lundholm, 2000. Voluntary disclosure and equity offerings: reducing information asymmetry or hyping the stock? Contemporary Accounting Research 17, 623-62.

Lehavy, R., F. Li, and K. Merkley, 2011. The effect of annual report readability on analyst following and the properties of their earnings forecasts. The Accounting Review 86, 1087-1115.

Li, F., 2008. Annual report readability, current earnings, and persistence. Journal of Accounting and Economics 45, 221-247.

Miller, B.P., 2010. The effects of reporting complexity on small and large investor trading. The Accounting Review 85, 2107-2143.

22

Richardson, S.R., R. Sloan, M. Soliman, and I. Tuna, 2005. Accrual reliability, earnings persistence, and stock prices. Journal of Accounting and Economics 39, 437-85.

Roychowdhury, S., 2006. Earnings management through real activities manipulation. Journal of Accounting and Economics 42, 335-370.

Schrand, C., B. Walther, 2000. Strategic benchmarks in earnings announcements: the selective disclosure of prior-period earnings components. The Accounting Review 75, 151-177.

23

Table 1: Sample selection Observations All Compustat firm-years 2000-2012 109,197 Less: observations in utilities or financial services (24,507) Less: firm-years with insufficient data (57,723) Number of firm-years used in tests of Hypothesis 1 26,967 Number of firms 4,855

Table 2: Descriptive statistics for variables used to test Hypothesis 1 (n = 26,967)

Variable Mean S.D. Q1 Median Q3 Fog 18.020 1.613 16.880 17.907 19.048 ΔEPS 0.049 40.521 -0.390 0.060 0.460 Size 5.768 2.058 4.292 5.774 7.156 MTB 1.999 1.757 1.100 1.496 2.242 Age 15.576 11.853 6.000 12.000 22.000 SpecItems -0.032 0.248 -0.016 -0.001 0.000 EarnVol 0.063 1.045 0.001 0.002 0.010 RetVol 0.158 0.099 0.090 0.131 0.194 NBSeg 1.032 0.531 0.693 0.693 1.386 NGSeg 1.057 0.647 0.693 1.099 1.609 NItems 278.878 29.838 255.000 283.000 301.000 M&A 0.398 0.489 0.000 0.000 1.000 SEO 0.061 0.239 0.000 0.000 0.000 Delaware 0.653 0.476 0.000 1.000 1.000

Note: Refer to Appendix A for variable definitions.

24

Table 3: Correlation matrix with Pearson (Spearman) values above (below) the main diagonal Variable (1) (2) (3) (4) (5) (6) (7) (8) (9) (10) (11) (12) (13) (14)

(1) Fog 1.00 0.00 -0.10 0.12 -0.02 -0.02 0.04 0.10 -0.02 -0.09 0.01 -0.03 -0.01 0.06

(2) ΔEPS 0.00 1.00 0.01 0.00 0.00 0.01 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00

(3) Size -0.11 0.10 1.00 0.17 0.29 0.08 -0.05 -0.40 0.13 0.26 0.28 0.34 0.07 0.08

(4) MTB 0.09 0.15 0.38 1.00 -0.12 -0.01 0.18 0.08 -0.11 -0.06 -0.01 -0.04 0.07 0.07

(5) Age -0.02 0.02 0.24 -0.08 1.00 0.06 -0.03 -0.29 0.20 0.16 0.23 0.09 -0.09 -0.20

(6) SpecItems -0.02 0.27 0.01 0.10 0.05 1.00 0.00 -0.11 0.01 0.01 0.01 0.00 0.01 -0.02

(7) EarnVol 0.19 0.04 -0.38 0.20 -0.25 -0.02 1.00 0.06 -0.03 -0.03 -0.01 -0.01 0.01 0.02

(8) RetVol 0.10 -0.04 -0.44 -0.08 -0.33 -0.13 0.43 1.00 -0.10 -0.09 -0.21 -0.18 0.07 0.06

(9) NBSeg -0.04 0.01 0.13 -0.10 0.19 -0.04 -0.19 -0.12 1.00 0.14 0.02 0.11 -0.03 -0.04

(10) NGSeg -0.08 0.02 0.27 0.03 0.15 -0.11 -0.09 -0.09 0.14 1.00 0.20 0.14 -0.04 0.02

(11) NItems 0.00 0.02 0.27 0.05 0.23 -0.11 -0.13 -0.19 0.03 0.20 1.00 0.08 0.01 0.03

(12) M&A -0.03 -0.02 0.34 0.05 0.07 -0.06 -0.19 -0.20 0.12 0.14 0.08 1.00 0.00 0.03

(13) SEO -0.01 0.04 0.08 0.09 -0.10 0.02 0.05 0.07 -0.03 -0.04 0.01 0.00 1.00 0.06

(14) Delaware 0.07 0.02 0.08 0.08 -0.21 -0.04 0.10 0.07 -0.05 0.03 0.04 0.03 0.06 1.00 Bolded coefficients are statistically significant at the 1% level.

25

Table 4: First test of Hypothesis 1 – earnings management identified by MBE MBE = 1 when MBE = 1 when MBE = 1 when Independent variable

Pred. Sign

ΔEPS ∈ [$0, $0.01] ΔEPS ∈ [$0, $0.02] ΔEPS ∈ [$0, $0.03] IA IB IIA IIB IIIA IIIB

MBE + 0.163** 0.168** 0.190*** 0.194*** 0.208*** 0.209***

(2.272) (2.319) (3.295) (3.327) (3.704) (3.777)

Earnings – -0.484***

-0.484***

-0.484***

(-3.211)

(-3.222)

(-3.231)

NegEarnChg + 0.033 0.049** 0.037* 0.053** 0.041** 0.057*** (1.673) (2.444) (1.896) (2.666) (2.063) (2.835) Size ? -0.044* -0.070*** -0.043* -0.070*** -0.043* -0.069***

(-1.984) (-3.271) (-1.961) (-3.249) (-1.947) (-3.235)

MTB + 0.036*** 0.064*** 0.036*** 0.064*** 0.035*** 0.063***

(2.950) (5.275) (2.919) (5.259) (2.901) (5.260)

Age ? 0.014*** 0.014*** 0.014*** 0.014*** 0.014*** 0.014***

(6.415) (6.359) (6.398) (6.343) (6.423) (6.368)

SpecItems – 0.084*** -0.028 0.084*** -0.029 0.084*** -0.029

(2.863) (-1.189) (2.864) (-1.199) (2.866) (-1.204)

EarnVol + -0.017 0.005 -0.017 0.005 -0.017 0.005

(-1.082) (0.450) (-1.081) (0.447) (-1.077) (0.458)

RetVol + 0.678*** 0.912*** 0.680*** 0.914*** 0.686*** 0.920***

(4.322) (5.683) (4.365) (5.703) (4.406) (5.752)

NBSeg ? 0.042 0.045 0.042 0.045 0.042 0.046

(1.129) (1.262) (1.129) (1.261) (1.133) (1.266)

NGSeg ? -0.156*** -0.170*** -0.156*** -0.169*** -0.155*** -0.169***

(-3.319) (-3.590) (-3.306) (-3.576) (-3.300) (-3.570)

NItems ? -0.003* -0.002 -0.003* -0.002 -0.003* -0.002

(-1.785) (-1.378) (-1.782) (-1.375) (-1.779) (-1.371)

M&A ? 0.037 0.036 0.036 0.035 0.036 0.035

(1.272) (1.202) (1.273) (1.203) (1.263) (1.194)

SEO – -0.207*** -0.185*** -0.207*** -0.185*** -0.207*** -0.185***

(-4.236) (-3.708) (-4.226) (-3.698) (-4.210) (-3.685)

Delaware + 0.160*** 0.177*** 0.160*** 0.177*** 0.160*** 0.177***

(3.405) (3.771) (3.398) (3.763) (3.400) (3.765)

Constant

17.96*** 17.87*** 17.95*** 17.85*** 17.94*** 17.85***

(37.632) (37.441) (37.872) (37.670) (37.826) (37.618)

Industry fixed effects Yes Yes Yes Yes Yes Yes Year fixed effects Yes Yes Yes Yes Yes Yes Obs with MBE = 1 438 438 679 679 898 898 Total observations 26,967 26,967 26,967 26,967 26,967 26,967 Adj. R-Squared 12.4% 11.8% 12.4% 11.8% 12.4% 11.8%

Note: Predicted signs for variables from Li (2008) are as listed in that paper’s Table 2, but if the predicted sign differs from the empirical association, then we list it as “?” above. Refer to Appendix A for variable definitions. *, **, and *** indicate significance at the 5%, 1%, and 0.1% levels.

26

Table 5: First test of Hypothesis 1 – earnings management identified by MBE – supplemental results Panel A: MBE defined using earnings deflated by total assets instead of EPS MBE = 1 when MBE = 1 when MBE = 1 when

Independent variable Pred. Sign

ΔEarnings ∈ [0, 0.4%] ΔEarnings ∈ [0, 0.5%] ΔEarnings ∈ [0, 0.6%] I II III

MBE + 0.136** 0.137*** 0.127**

(2.745) (3.442) (3.048)

NegEarnChg + 0.051** 0.051** 0.052** (2.574) (2.593) (2.614)

Controls Yes Yes Yes Industry fixed effects Yes Yes Yes Year fixed effects Yes Yes Yes

Observations with MBE = 1 1040 1321 1595 Total observations 26,967 26,967 26,967 Adj. R-Squared 11.8% 11.8% 11.8%

Panel B: Placebo test with MBE in prior year MBE = 1 when MBE = 1 when MBE = 1 when

Independent variable Pred. Sign

ΔEPS ∈ [$0, $0.01] ΔEPS ∈ [$0, $0.02] ΔEPS ∈ [$0, $0.03] I II III

MBEt + 0.168** 0.193*** 0.207*** (2.325) (3.355) (3.806) MBEt-1 0 0.040 0.061 0.070 (0.445) (1.031) (1.495) NegEarnChg + 0.049*** 0.053*** 0.057*** (2.451) (2.654) (2.813)

Controls Yes Yes Yes Industry fixed effects Yes Yes Yes Year fixed effects Yes Yes Yes Observations with MBE = 1 438 679 898 Total observations 26,967 26,967 26,967 Adj. R-Squared 12.2% 12.1% 12.0%

Refer to Appendix A for variable definitions. *, **, and *** indicate significance at the 5%, 1%, and 0.1% levels.

27

Table 6: Second test of Hypothesis 1 – earnings management identified by MBE and sign of discretionary accruals MBE = 1 when MBE = 1 when MBE = 1 when

Independent variable Pred. Sign

ΔEPS ∈ [$0, $0.01] ΔEPS ∈ [$0, $0.02] ΔEPS ∈ [$0, $0.03] I II III

PosDA ? 0.009 0.010 0.009 (0.307) (0.324) (0.307) MBE × PosDA + 0.335*** 0.301*** 0.299*** (3.563) (4.920) (5.248) MBE × NegDA 0 -0.042 0.067 0.102 (-0.324) (0.581) (1.016) NegEarnChg + 0.102*** 0.115*** 0.113*** (4.631) (4.528) (4.349)

Controls Yes Yes Yes Industry fixed effects Yes Yes Yes Year fixed effects Yes Yes Yes

Observations 26,143 26,143 26,143 Adj. R-Squared 11.8% 11.8% 11.8%

Refer to Appendix A for variable definitions. *, **, and *** indicate significance at the 5%, 1%, and 0.1% levels.

28

Table 7: Third test of Hypothesis 1 – earnings management identified by MBE and magnitude of positive discretionary accruals MBE = 1 when MBE = 1 when MBE = 1 when

Independent variable Pred. Sign

ΔEPS ∈ [$0, $0.01] ΔEPS ∈ [$0, $0.02] ΔEPS ∈ [$0, $0.03] I II III

PosDA ? 0.009 0.010 0.009 (0.307) (0.324) (0.309) MBE × HighPosDA + 0.385** 0.417*** 0.419*** (2.708) (5.132) (4.865) MBE × LowPosDA ? 0.285** 0.185* 0.180** (2.540) (2.191) (2.346) MBE × NegDA 0 -0.042 0.067 0.102 (-0.324) (0.581) (1.017) NegEarnChg + 0.057** 0.061** 0.065*** (2.716) (2.931) (3.114)

Controls Yes Yes Yes Industry fixed effects Yes Yes Yes Year fixed effects Yes Yes Yes

Observations 26,143 26,143 26,143 Adj. R-Squared 11.8% 11.8% 11.8%

Refer to Appendix A for variable definitions. *, **, and *** indicate significance at the 5%, 1%, and 0.1% levels.

29

Table 8: Third test of Hypothesis 1 – earnings management identified by MBE and magnitude of positive discretionary accruals – supplemental robustness tests Panel A – Including firm-level (instead of industry) fixed effects MBE = 1 when MBE = 1 when MBE = 1 when

Independent variable Pred. Sign

ΔEPS ∈ [$0, $0.01] ΔEPS ∈ [$0, $0.02] ΔEPS ∈ [$0, $0.03] I II III

PosDA ? 0.013 0.013 0.014 (0.951) (0.952) (1.007) MBE × HighPosDA + 0.166* 0.195** 0.136* (1.780) (2.331) (1.939) MBE × LowPosDA ? -0.049 -0.073 -0.064 (-0.562) (-1.029) (-1.017) MBE × NegDA 0 0.050 0.059 0.059 (0.614) (0.847) (0.985) NegEarnChg + 0.034** 0.035** 0.036** (2.538) (2.605) (2.611)

Controls Yes Yes Yes Firm fixed effects Yes Yes Yes Year fixed effects Yes Yes Yes

Observations 26,143 26,143 26,143 Adj. R-Squared 69.4% 69.4% 69.4%

Panel B – Discretionary accruals estimated using modified Jones model of Dechow et al. (1995) MBE = 1 when MBE = 1 when MBE = 1 when

Independent variable Pred. Sign

ΔEPS ∈ [$0, $0.01] ΔEPS ∈ [$0, $0.02] ΔEPS ∈ [$0, $0.03] I II III

PosDA ? 0.013 0.015 0.013 (0.495) (0.551) (0.505) MBE × HighPosDA + 0.357** 0.372*** 0.394*** (3.039) (5.949) (5.226) MBE × LowPosDA ? 0.269* 0.169* 0.185* (2.280) (2.300) (2.308) MBE × NegDA 0 0.002 0.117 0.126 (0.015) (1.075) (1.360) NegEarnChg + 0.057** 0.061** 0.065*** (2.740) (2.957) (3.136)

Controls Yes Yes Yes Industry fixed effects Yes Yes Yes Year fixed effects Yes Yes Yes

Observations 26,143 26,143 26,143 Adj. R-Squared 11.8% 11.8% 11.8%

30

Panel C – Discretionary accruals estimated using performance matching of Kothari et al. (2005) MBE = 1 when MBE = 1 when MBE = 1 when

Independent variable Pred. Sign

ΔEPS ∈ [$0, $0.01] ΔEPS ∈ [$0, $0.02] ΔEPS ∈ [$0, $0.03] I II III

PosDA ? 0.009 0.010 0.009 (0.287) (0.305) (0.283) MBE × HighPosDA + 0.307* 0.347*** 0.401*** (2.108) (4.571) (5.954) MBE × LowPosDA ? 0.067 0.052 0.059 (0.619) (0.410) (0.577) MBE × NegDA 0 0.178 0.195* 0.199** (1.612) (2.122) (2.407) NegEarnChg + 0.058** 0.062** 0.066** (2.706) (2.880) (3.034)

Controls Yes Yes Yes Industry fixed effects Yes Yes Yes Year fixed effects Yes Yes Yes

Observations 26,038 26,038 26,038 Adj. R-Squared 11.9% 11.9% 11.9%

Refer to Appendix A for variable definitions. *, **, and *** indicate significance at the 5%, 1%, and 0.1% levels.

31

Table 9: Sample of AAER observations Observations AAER firm-years with gvkey available 588 Less: observations in utilities or financial services (193) Less: observations without MD&A available on Edgar (179) Number of firm-years in misstatement sample used in tests of Hypothesis 2 216 Number of firms 110

Misstatement sample by year Firm-years Percentage 1996 24 11.11% 1997 33 15.28 1998 31 14.35 1999 39 18.06 2000 17 7.87 2001 22 10.19 2002 17 7.87 2003 19 8.80 2004 9 4.17 2005 5 2.31 Total 216 100.00%

32

Table 10: Descriptive statistics for misstatement sample and Compustat population

Misstatement sample Compustat population Misstate – Compustat

Variable N Mean Median N Mean Median Diff. in means t-stat

Accruals quality variables RSST accruals 211 0.091 0.051 26,545 0.038 0.028 0.053 2.84

Change in receivables 214 0.049 0.028 28,629 0.020 0.011 0.030 5.36

Change in inventory 213 0.025 0.000 28,498 0.008 0.000 0.017 4.51

% Soft assets 215 0.670 0.690 28,861 0.557 0.588 0.113 6.34

Performance variables Change in cash sales 211 0.348 0.200 27,941 0.187 0.084 0.161 2.44

Change in return on assets 211 -0.010 -0.005 28,304 -0.005 0.000 -0.005 -0.39

Nonfinancial variables Abnormal change in employees 199 -0.155 -0.077 26,271 -0.083 -0.033 -0.073 -2.08

Off-balance-sheet variables Existence of operating leases 216 0.894 1.000 29,032 0.811 1.000 0.083 3.09

Market-related variables Actual security issuance 216 0.972 1.000 29,032 0.868 1.000 0.104 4.52

Readability proxies Fog 216 18.440 18.208 29,032 18.278 18.022 0.161 0.80

Length (for info only – not used in tests) 216 8.476 8.592 29,032 8.357 8.418 0.118 1.95

Refer to Appendix A for variable definitions.

33

Table 11: Test of Hypothesis 2 Logistic regression where the dependent variable is equal to 1 if the firm-year had a misstatement; 0 otherwise.

Model 1 Model 2

Variable Pred. Sign Coefficient Wald Chi-

square Coefficient Wald Chi-

square Intercept -7.696*** 174.707 -8.203*** 158.240

RSST accruals + 0.333 0.962 0.337 0.991

Change in receivables + 2.594*** 8.021 2.573** 7.926

Change in inventory + 1.697 1.923 1.750 2.046

% Soft assets + 2.071*** 34.592 2.103*** 35.475

Change in cash sales + 0.085 1.028 0.082 0.974

Change in return on assets – -0.382 0.874 -0.377 0.860

Actual security issuance + 1.293*** 6.496 1.298*** 6.536

Abnormal change in employees – -0.104 0.550 -0.103 0.537

Existence of operating leases + 0.228 0.832 0.248 0.971

Fog + 0.025* 3.689

Misstating firm-years 195 195 Non-misstating firm-years 24712 24712

Note: The sample of misstatement firms was reduced from 216 to 195 firm-years due to the unavailability of data for some of the regressions variables (number of employees in particular). Refer to Appendix A for variable definitions. *, **, and *** indicate significance at the 5%, 1%, and 0.1% levels.