earnings management in family firms ear050512 v3 and real... · accounting and real earnings...

TRANSCRIPT

ACCOUNTING AND REAL EARNINGS MANAGEMENT

IN FAMILY FIRMS

Ann-Kristin Achleitner

Center for Entrepreneurial and Financial Studies (CEFS) Technische Universität München

Nina Fichtl Center for Entrepreneurial and Financial Studies (CEFS)

Technische Universität München [email protected]

Christoph Kaserer*

Center for Entrepreneurial and Financial Studies (CEFS) Technische Universität München

*Corresponding Author Center for Entrepreneurial and Financial Studies (CEFS)

TUM School of Management │ Technische Universität München Arcisstr. 21 │ 80333 München

Tel: + 49 (0)89 289 – 25489 │ Fax: + 49 (0)89 289 – 25488

Accounting and Real Earnings Management in Family Firms

ABSTRACT

This paper starts from the presumption that firms follow multiple earnings management

strategies simultaneously, i.e. they engage in accounting (AEM) and real earnings

management (REM) at the same time. We hypothesize that the outcome of this trade-off is

driven by earnings management motives influenced by the ownership structure of the firm and

the institutional environment. In order to test this hypothesis, we use a large hand-collected

panel data set of listed German firms over the period 1998 to 2008. Specifically, we test the

hypothesis that firms owned by their founding families should engage more in AEM and less

in REM activities as compared to their non-family counterparts. In a nutshell, this is because

at the one side control motives are a strong driver for AEM in family firms, whereas at the

other side, family shareholders tend to dislike REM because of its negative performance

impact. Our results clearly support this hypothesis, even when we control for a potential

selection bias.

JEL Classification: G32, M4, M41, M48

Keywords: family firms, accounting earnings management, real earnings management,

earnings quality, ownership structures, Germany.

2

1. Introduction

In this paper we scrutinize the trade-off between accounting earnings management (AEM)

and real earnings management (REM). It is agreed in the literature that AEM refers to the

way in which the discretion granted by accounting standards is exploited, whereas REM

affects the timing and structuring of business activities. Hitherto, the overwhelming part of

the literature focuses on drivers of AEM (for surveys cf. e.g. Healy and Wahlen, 1999;

Armstrong et al., 2010, Kothari et al., 2010). Some recent papers investigate drivers of

REM (e.g. Gunny 2010; Roychowdhury, 2006), whereby only very few papers take an

integrated view by looking at both earnings management mechanisms simultaneously

(Cohen et al., 2008; Cohen and Zarowin 2010; Zang, 2012). However, such an integrated

view is a prerequisite for understanding earnings manipulation, as these papers point out

that firms engage in multiple earnings management strategies at the same time. Such an

understanding is important for any discussion about accounting choices and enforcement.

In this paper we make a contribution to this strand of literature by scrutinizing the impact

of ownership structures on both AEM as well as REM. More specifically, we hypothesize

that by taking the specific benefits of earnings manipulation as well as the incentive

structures governing the firms into account, closely-held firms should be less inclined to

use REM, but more inclined to use AEM as compared to widely-held firms. We test this

hypothesis by analyzing earnings management in family-owned firms.

Our hypothesis is based on two pillars. First, we follow Cohen and Zarowin (2010) and

Zang (2012) in pointing out that the choice between AEM and REM is, among others,

determined by the specific motivation that is pursued. Such motivation for earnings

management can be related to (i) meeting capital market expectations, (ii) influencing

3

management compensation, (iii) avoiding the breach of debt covenants or (iv) influencing

payout levels. While for motives (iii) and (iv) no direct preference for either AEM or REM

arises (as long as the costs of these instruments are not taken into account), a management

pursuing motivations (i) or (ii) might prefer REM over AEM. This is because as far as

earnings smoothing is concerned, it could be argued that the capital market, e.g. financial

analysts, is able to look behind the veil of financial accounting policy. For example,

Graham et al. (2005) report that 80% of surveyed managers would decrease discretionary

spending on R&D or maintenance in order to meet formerly published earnings targets.

Moreover, to the extent that these REM actions have an impact on the stock price, REM is

also an instrument to influence stock-based compensation in the short-term.

Actually, both family and non-family firms are interested in earnings management.

However, the underlying motives are quite different. While in widely-held firms earnings

management is mostly driven by the desire to smooth earnings and to influence

management compensation, the dominant motive in family-owned firms is to stay in

control of the company, i.e. to avoid the breach of covenant clauses (Prencipe et al., 2008),

and to pay smooth dividends (Schmid et al., 2010). Hence, from the benefit side family-

owned firms are, at best, indifferent between AEM and REM, while non-family firms may

have a clear preference for REM.

Second, for getting the whole picture about the trade-off between AEM and REM also the

costs of these two instruments have to be taken into account (Zang, 2012). While AEM is

based on pure accounting choices and, therefore, has no cash flow consequences, this does

not hold to be true for REM. By definition, REM implies a deviation from normal business

practices with the goal to avoid the reporting of a loss or to smooth earnings.

4

Roychowdhury (2006) shows that this effect is obtained by boosting earnings through

increased price discounts, overproduction in order to allocate less overhead costs to the

cost of goods sold and aggressively reducing discretionary expenses such as R&D,

advertising and SG&A expenses. Therefore, it is not surprising , that REM has a negative

impact on future performance (Gunny, 2010). As a consequence, the propensity to use

REM instead of AEM is related to the degree of interest alignment between shareholders

and management.

Therefore, from the cost side perspective we would expect closely-held firms, e.g. family

firms, to prefer AEM over REM as in these firms a stronger alignment between the interest

of shareholders and managers can be assumed. For firms with atomistic shareholder

structures this alignment may be less effective so that the negative performance

consequences of REM are given a lower weight.

The results presented in this paper clearly support our hypothesis that family firms are less

inclined to use REM, but more inclined to use AEM as compared to widely-held firms.

More specifically, our findings can be summarized as follows. First, while all firms use

AEM as well as REM simultaneously, there is strong evidence that family-owned firms use

more AEM and less REM compared to their non-family counterparts. Second, this result is

not driven by family management, i.e. the fact that members of the founding family hold

positions in the board. This is what we would expect according to our theoretical

reasoning, as the motives for earnings management are related to the position of the

founding family as a blockholder in the company. Third, this reasoning is further supported

by the fact that we also find non-family firms with significant insider ownership to rely

5

more heavily on AEM. It should be noted that the results are robust against a potential self-

selection bias.

The paper contributes to the literature along several dimensions. First, while accounting

earnings management in family firms has been addressed by previous research (e.g. Wang,

2006; Ali et al,. 2007; Prencipe et al., 2008; Tong, 2007, Jaggi et al., 2009; Bar-Yosef and

Prencipe, 2011), this paper to the best of our best knowledge studies the effects of family

involvement on the trade-off between AEM and REM for the first time. Second, the paper

corroborates former studies indicating that control considerations are an important motive

for earnings management in family firms (Prencipe et al., 2008; Bar-Yosef and Prencipe,

2011). In this sense, it raises some doubts against other studies concluding that because of

higher interest alignment earnings quality is superior in family firms (Wang, 2006).

Without taking into account the trade-off between AEM and REM, it is quite difficult to

get a complete picture about earnings management activities in family firms.

Fourth, the paper offers a potential explanation why evidence on AEM in family firms

hitherto is mixed. While evidence on US and UK firms commonly suggests that family and

managerial ownership is negatively associated with accounting earnings management

(Warfield et al., 1995; Peasnell et al., 2005; Wang, 2006; Ali et al., 2007; Tong, 2007),

results on European and Asian firms indicate that family influence increases the level of

accounting earnings management (Gabrielsen et al., 2002; Jara-Bertin and Lopez Iturriaga,

2008; Jaggi et al., 2009). If the trade-off between AEM and REM depends, among others,

on ownership structures and the institutional framework, the optimal choice between AEM

and REM is likely to differ across countries.

6

Third, beyond the family-firm literature, we also add some evidence to the literature on the

interaction between AEM and REM, especially because we relate this trade-off to

ownership structures. This issue has not yet been scrutinized in the literature (Cohen and

Zarowin, 2010; Zang, 2012).

The rest of the paper is organized as follows. Section 2 develops the theoretical framework

and discusses related literature. Section 3 presents the empirical models, while section 4

reports the sample and descriptive statistics. Results of the analyses are presented in

section 5. Section 6 concludes the paper and points out to avenues for future research.

2. Related Literature and Hypotheses

Earnings management can be defined as “a purposeful intervention in the external financial

reporting process, with the intent of obtaining some private gain.” (Schipper, 1989: 92).

Thereby, earnings management comprises AEM and REM. While the former is the

outcome of accounting choices, the latter results from cash flow choices including

operating, financing and investment decisions (e.g. Schipper, 1989; Roychowdury, 2006;

Dechow and Skinner, 2000). Typical examples for REM activities include the deferral of

discretionary expenses such as marketing or R&D expenses (e.g. Baber et al., 1991;

Dechow and Sloan, 1991; Holthausen et al., 1995; Bushee, 1998; Bens et al., 2003), the

sale of profitable assets or timing of income recognition from the disposal of a long-lived

asset (Bartov 1993; Herrmann et al., 2003), inventory management (e.g. Hunt et al., 1996;

Thomas and Zhang, 2002) or the cutting of prices to boost sales in the current period and

other means to accelerate sales (Jackson and Wilcox, 2000).

It is agreed in the theoretical and empirical literature that AEM and REM are complements

rather than substitutes (Ewert and Wagenhofer, 2005; Cohen and Zarowin, 2010; Zang,

7

2012). Therefore, there is a trade-off between the two instruments the outcome of which

depends on the associated benefits and costs. This trade-off most likely depends on the

ownership structure of a company. Actually, given that the family is concerned about the

longevity of the firm, family firms are presumed to be less subject to managerial myopia

and more inclined to invest into positive NPV projects rather than boost current earnings

by engaging in risky projects (James, 1999). Hence, there is more interest alignment

between the shareholders and the management in a family-owned firm as compared to

widely-held firms. The long-term investment horizon of family shareholders reduces the

capital market pressure to meet short-term earnings targets such as analyst or management

forecasts (Graham et al., 2005).

While the alignment of interests is considered to reduce the level of earnings management,

family firms could exhibit higher levels of earnings management due to conflicts between

family and minority shareholders. Previous studies argue that family firms may ‘mask’

performance to conceal expropriation of minority shareholders (Leuz et al., 2003; Wang,

2006; Jara-Bertin and Lopez Iturriaga 2008; Jaggi et al., 2009). Moreover, long-term

orientation does not only mitigate agency costs arising from short-termism but also results

in the wish to maintain a controlling position in the firm and risk aversion. Family firms

could have incentives to engage in earnings management in order to conceal ‘true’

economic performance with the purpose of defending financial and non-financial private

benefits of control from owning the company.

Two important goals pursued by the family blockholder should be mentioned in this

context. First, family firms could make use of accounting policy discretion to meet debt-

related earnings targets, i.e. debt covenants (Prencipe et al., 2008). Second, it should not be

8

forgotten that families often have an interest to smooth earnings in order to smooth

dividend payouts (Kasanen et al., 1996; García Lara et al., 2005; Schmid et al., 2010).

However, these family-specific goals can be pursued by pure AEM. There is not so much

need to engage in REM, especially since the latter is associated with negative performance

consequences (Gunny, 2010). Indeed, family firms as long-term investors may have lower

incentives to sacrifice firm value to meet short-term earnings targets (Hutton, 2007;

Salvato and Moores, 2010). As opposed to that, the management in a widely-held firm may

engage in REM rather than AEM because the latter is more easily detected by the market.

In fact, financial analysts at least to some extent may be able to look behind the veil of

financial accounting policy (Graham et al., 2005). As managers are considered to have

strong incentives to manage earnings for compensation and reputation purposes (e.g.

(Healy, 1985; Holthausen et al., 1995; Bergstresser and Philippon 2006), they would use

REM instead of AEM instruments.

Because of these interacting effects between AEM and REM, it is not surprising that

previous evidence on AEM in family firms is mixed. While evidence on US and UK firms

commonly suggests that family and managerial ownership is negatively associated with

accounting earnings management (Dhaliwal et al., 1982; Warfield et al., 1995; Peasnell et

al., 2005; Wang, 2006; Ali et al., 2007; Tong, 2007), results on European and Asian firms

indicate that insider ownership and family influence tend to increase the level of

accounting earnings management (Gabrielsen et al. 2002; Jara-Bertin and Lopez Iturriaga,

2008; Jaggi et al., 2009).

According to our main hypothesis these differences can be well explained by differences in

the institutional framework and in the level of family ownership. The outcome of the trade-

9

off between AEM and REM is driven by two mechanisms. First, the level of family

ownership is relevant as it determines the degree of interest alignment. As ownership

structures in Asian and European countries tend to be more concentrated as compared to

the US or the UK we expect, on the margin, AEM to be less attractive relative to REM in

the latter countries as compared to the former ones. It should be noted that the level of

family ownership in our sample is 36% as compared to an average of 10% in the sample of

S&P 500 firms in Wang (2006).

Second, investor protection rights should set a limit to the degree of AEM put in place by

the management. In fact, as far as AEM is concerned, it is well known that it is confined by

the level of investor protection (Ball et al., 2000, 2003; Leuz et al., 2003). Therefore, we

can expect that this influences the level of REM. As a consequence, it could be that in

countries with higher investor protection rights, the management of widely-held firms has

less discretion in implementing AEM making REM relatively more attractive.

As an additional aspect, Wang (2006) points out that there could be a non-linear

relationship between family ownership and AEM. Incentives to manage earnings in family

firms are likely to change with the level of ownership. Previous studies point out that

incentives to defend private benefits of control are particularly pronounced at medium

levels of managerial or family ownership (Morck et al., 1988; Himmelberg et al., 1999;

Anderson and Reeb, 2003). We are able to observe a high heterogeneity regarding the level

of family ownership in our sample of German listed firms and test if there is a non-linear

relationship between family ownership and earnings management.

Family members have different possibilities to influence earnings depending on whether

they only act as shareholders or are involved in the board. Germany is characterized by a

10

two-tier board structure. Compared to unitary board systems, dual board systems separate

distinctly between the management and the supervision of a company. We take this effect

into account by analyzing the impact of family ownership and the impact of family

management separately. According to our reasoning family ownership should be the

driving factor for AEM. However, it may well be that control incentives are more

pronounced in those firms where the family is also active in the management. Therefore, it

will be interesting to see whether the existence of a family-CEO has an additional impact

on AEM activities.

To sum up, the main hypotheses tested in our paper are as follows:

(i) By taking the specific benefits of earnings manipulation as well as

differences in the incentive structures into account, family-owned firms

should be less inclined to use REM, but more inclined to use AEM as

compared to widely-held firms. This should at least hold to be true in a

German corporate governance context with relatively weak investor

protection rights.

(ii) Earnings management activities in family firms should be driven by family

ownership and not by family management.

(iii) While we have no clear prediction as far as the impact of the ownership

level on the degree of AEM is concerned, we expect REM to be the lower

the larger the ownership stake of the family is.

(iv) We expect family firms where the founder is appointed as the CEO to

engage in more AEM because of the long-term control motive of the

founder.

11

3. Research Design

3.1 Measurement of Family Involvement

The family firm definition used in this study follows the founding family concept used in

the literature (Anderson and Reeb, 2003). Accordingly, firms classify as family firms when

the founder or a member of his/her family by either blood or marriage serve as directors in

the management and/or supervisory board or act as blockholder, either individually or as a

group (Villalonga and Amit, 2006). In order to account for the more concentrated

ownership, studies related to the German capital market set the threshold for a family

blockholding at 25% of voting rights (Andres, 2008; Ampenberger et al., 2012). In this

study we follow this approach. It should also be noted that according to the German Stock

Corporation Act, important corporate decisions can be blocked with 25% of the voting

rights.

According to this definition, we use the dichotomous variable Dummy_FF indicating

whether a specific firm is a family or non-family firm. However, we also use other proxies

measuring family involvement. Family ownership FF_OWN corresponds to the percentage

of common shares controlled by the founding family, while FMB is a dummy variable

which indicates the presence of the founding family in the management board. Moreover,

in order to analyze the role of the CEO, we include the following indicator variables in the

regression model: a dummy variable indicating whether the CEO is a founder of the

company (F_CEO), a descendant of the founding family (D_CEO), or an outside hired

CEO (H_CEO). The presence of a founding family member as a chairman in the

supervisory board is indicated by the dummy variable FF_Chair.

12

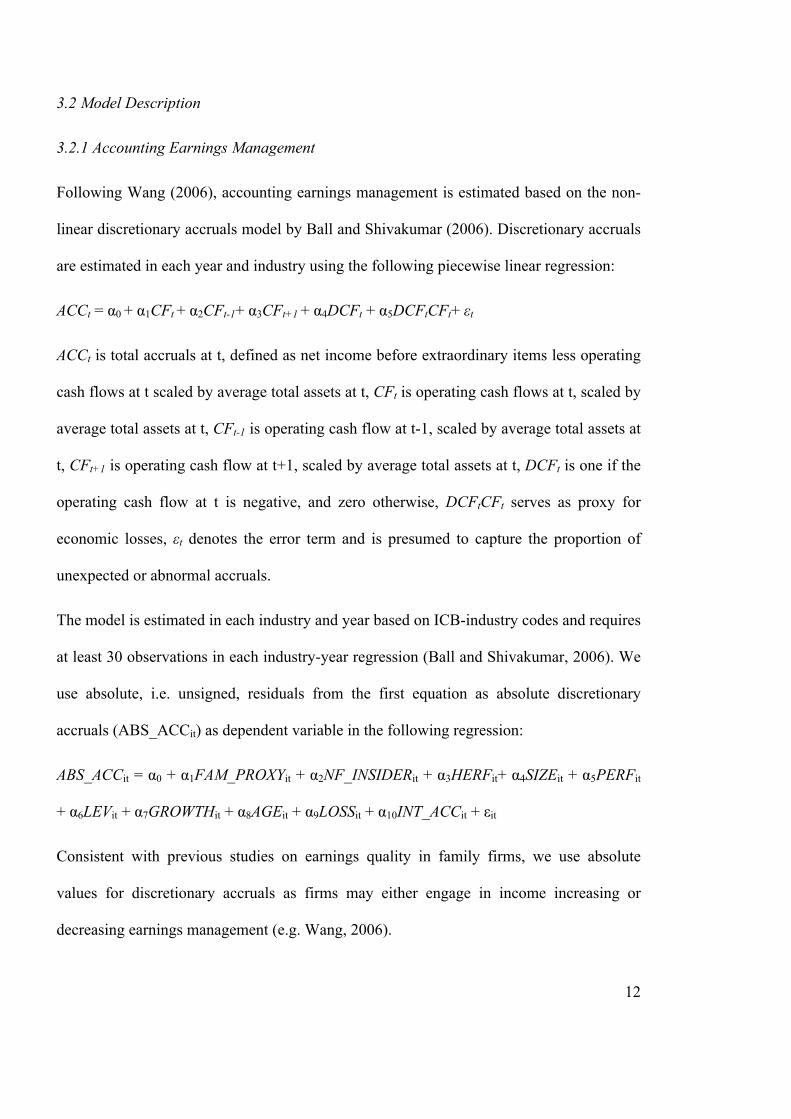

3.2 Model Description

3.2.1 Accounting Earnings Management

Following Wang (2006), accounting earnings management is estimated based on the non-

linear discretionary accruals model by Ball and Shivakumar (2006). Discretionary accruals

are estimated in each year and industry using the following piecewise linear regression:

ACCt = α0 + α1CFt + α2CFt-1+ α3CFt+1 + α4DCFt + α5DCFtCFt+ εt

ACCt is total accruals at t, defined as net income before extraordinary items less operating

cash flows at t scaled by average total assets at t, CFt is operating cash flows at t, scaled by

average total assets at t, CFt-1 is operating cash flow at t-1, scaled by average total assets at

t, CFt+1 is operating cash flow at t+1, scaled by average total assets at t, DCFt is one if the

operating cash flow at t is negative, and zero otherwise, DCFtCFt serves as proxy for

economic losses, εt denotes the error term and is presumed to capture the proportion of

unexpected or abnormal accruals.

The model is estimated in each industry and year based on ICB-industry codes and requires

at least 30 observations in each industry-year regression (Ball and Shivakumar, 2006). We

use absolute, i.e. unsigned, residuals from the first equation as absolute discretionary

accruals (ABS_ACCit) as dependent variable in the following regression:

ABS_ACCit = α0 + α1FAM_PROXYit + α2NF_INSIDERit + α3HERFit+ α4SIZEit + α5PERFit

+ α6LEVit + α7GROWTHit + α8AGEit + α9LOSSit + α10INT_ACCit + εit

Consistent with previous studies on earnings quality in family firms, we use absolute

values for discretionary accruals as firms may either engage in income increasing or

decreasing earnings management (e.g. Wang, 2006).

13

The experimental variable FAM_PROXY denotes the variables that proxy for family

involvement as explained above. Following Wang (2006) and other prior literature, the

following control variables are included in the model: firm size (SIZE) measured as natural

logarithm of total assets, profitability (PERF) measured as net income scaled by average

total assets, leverage (LEV) defined as debt to total assets, a dummy variable that indicates

if the firm exhibits a loss in the observation period (LOSS), growth (GROWTH) measured

as sales growth and age (AGE) measured as observation year less founding year.

Our observation period covers the years 1998 to 2008 and is hence characterized by the

internationalization of accounting standards in Germany. To control for differences in the

accounting standard applied, we include a dummy variable INT_ACC in our analysis that

equals one if international accounting standards (IFRS or US GAAP) are applied in the

respective observation period and zero if financial statements are prepared according to

German GAAP.

We differentiate between effects of family ownership and ownership concentration by

including the Herfindahl index (HERF) for ownership concentration. Furthermore, non-

family insider ownership (NF_INSIDER) is added as a control variable to examine if

effects are due to insider or family ownership (Wang, 2006).

3.2.2 Real Earnings Management

Following Roychowdhury (2006), we use discretionary cash flows to analyze effects of

family ownership and management on real earnings management.

Discretionary cash flows are presumed to result from sales manipulation. Managers may be

tempted to temporarily increase sales. Increased sales from price discounts are presumed to

vanish when the firm returns to its old prices. As a consequence, the cash inflow per sale

14

net of price discount is lower because margins decrease. Roychowdhury (2006) expects

that sales management activities are reflected in lower current period cash flows from

operations and higher production costs as compared to levels common for the respective

sales level.

The estimation model for discretionary cash flows is expressed by the following regression

equation:

CFOt/At-1=α0 + α1 (1/At-1) + α2 (St/At-1) + α3 (ΔSt /At-1) + εt

All variables used in the model are scaled by lagged total assets (At-1). CFOt is cash flows

from operating activities in t, St is sales in t, ΔSt is change in sales from t-1 to t. The

regression is run cross-sectionally for each industry and year with a minimum of 15

observations per industry-year based on ICB codes. The residuals are presumed to capture

the amount of discretionary cash flows (Discr_CF). Higher levels of discretionary cash

flows are interpreted as lower levels of real earnings management.

Effects of family influence on discretionary cash flows are examined based on the

following regression model:

Discr_CFit = α0 + α1FAM_PROXYit + α2NF_INSIDERit + α3HERFit+ α4SIZEit + α5PERFi +

α6LEVit + α7GROWTHit + α8AGEit + α9LOSSit + α10INT_ACCit + εit

Experimental and control variables in the models on real earnings management are as

defined in our models on accounting earnings management. All models are calculated

based on pooled OLS and between effects models.

15

4. Data and Descriptive Statistics

4.1 Sample Selection

Our sample covers eleven years of panel data for the period from 1998 to 2008. We start

our sample selection process by identifying all German corporations whose common stock

is listed in the CDAX in the respective year. In this way, we get 7,642 firm-year

observations. The CDAX corresponds to the market segment that comprises the EU

regulated market of the German stock exchange. We eliminate observations of financial

firms based on the ICB industry classification in Thomson Financial Datastream.

Observations are only included if full information regarding the founder, ownership

structures and/or board structures as well as the accounting standard applied in the

respective year is available. Outliers are eliminated based on the top and bottom 1%-

percentile. Based on this sampling procedure, we include 4,937 firm-year observations of

non-financial firms (708 cross-sections) in our analysis (2,335 observations for family

firms and 2,602 observations for non-family firms).

Data on ownership and board structures is derived from Hoppenstedt Aktienführer which

publishes annual data on ownership structures of listed German firms. This information is

verified using several further databases including Bureau van Dijk’s Amadeus database,

Commerzbank’s Wer gehört zu wem, the director dealings database of the Bundesanstalt

für Finanzdienstleistungsaufsicht (BaFin) and web research. Data on the founder is derived

from Hoover’s Online Profile, Factiva, LexisNexis as well as web-based research.

Accounting data comes from the Worldscope database. Data on accounting standards is

verified by hand using annual reports of the respective observation year.

16

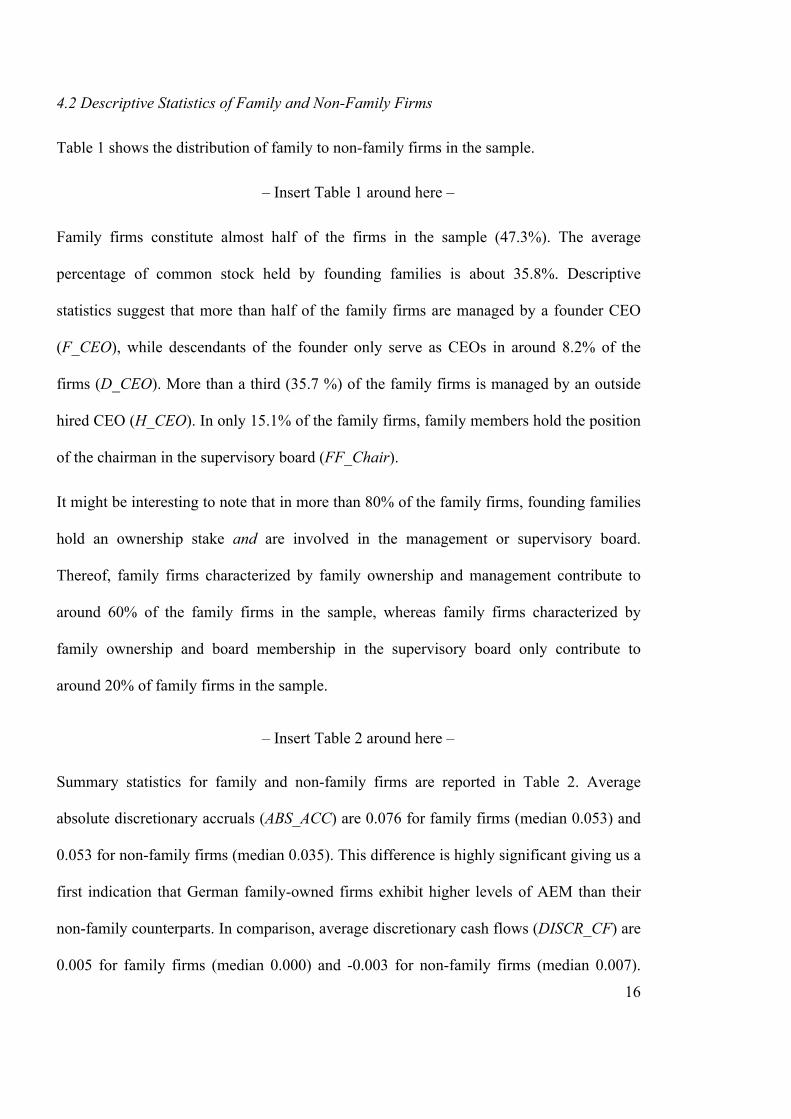

4.2 Descriptive Statistics of Family and Non-Family Firms

Table 1 shows the distribution of family to non-family firms in the sample.

– Insert Table 1 around here –

Family firms constitute almost half of the firms in the sample (47.3%). The average

percentage of common stock held by founding families is about 35.8%. Descriptive

statistics suggest that more than half of the family firms are managed by a founder CEO

(F_CEO), while descendants of the founder only serve as CEOs in around 8.2% of the

firms (D_CEO). More than a third (35.7 %) of the family firms is managed by an outside

hired CEO (H_CEO). In only 15.1% of the family firms, family members hold the position

of the chairman in the supervisory board (FF_Chair).

It might be interesting to note that in more than 80% of the family firms, founding families

hold an ownership stake and are involved in the management or supervisory board.

Thereof, family firms characterized by family ownership and management contribute to

around 60% of the family firms in the sample, whereas family firms characterized by

family ownership and board membership in the supervisory board only contribute to

around 20% of family firms in the sample.

– Insert Table 2 around here –

Summary statistics for family and non-family firms are reported in Table 2. Average

absolute discretionary accruals (ABS_ACC) are 0.076 for family firms (median 0.053) and

0.053 for non-family firms (median 0.035). This difference is highly significant giving us a

first indication that German family-owned firms exhibit higher levels of AEM than their

non-family counterparts. In comparison, average discretionary cash flows (DISCR_CF) are

0.005 for family firms (median 0.000) and -0.003 for non-family firms (median 0.007).

17

Even though this difference is only weakly significant, it nevertheless is in line with our

hypothesis that non-family firms engage more actively in REM than family firms. It should

be noted that the level of REM decreases in discretionary cash flows.

Results emerging from Table 2 indicate that family firms tend to be significantly smaller in

terms of total assets (SIZE). They exhibit lower return on assets (PERF) and leverage

(LEV). Family firms appear to have higher sales growth (GROWTH) than non-family

firms. Consistent with lower ownership concentration in family firms than in non-family

firms (HERF), untabulated statistics indicate that large block holdings of non-family

insiders, financial investors or other shareholder groups can be found more frequently in

non-family than in family firms. This evidence indicates that founding families tend to be

the dominant shareholder in listed family firms in Germany.

Descriptive statistics on the industry distribution are displayed in Table 3 and show that

family firms are represented in all industries among German listed firms but are

particularly concentrated in the health care, the consumer services, the telecommunication

and the technology industry.

– Insert Table 3 around here –

Pearson correlation coefficients between the variables used in the analysis are displayed in

Table 4. Abnormal accruals (ABS_ACC) are significantly negatively correlated with

discretionary cash flows (DISCR_CF). This relation can possibly be explained by the fact

that firms engage in accounting and real earnings management at the same time, i.e. they

use multiple earnings management strategies. This is consistent with the results in

Roychowdhury (2006).

– Insert Table 4 around here –

18

5. Results

5.1 Family Firms and Accounting Earnings Management

Table 5 shows the results from the pooled ordinary least squares (OLS) regression on

accounting earnings management with absolute abnormal discretionary accruals

(ABS_ACC) as dependent variable. Results from the pooled OLS regression are consistent

with results from between effects models which are therefore not tabulated.

– Insert Table 5 around here –

First of all, all model specifications indicate that family firms have significantly higher

levels of discretionary accruals than non-family firms, regardless how family involvement

is measured. Moreover, model 3 suggests that family ownership – not family management

– is the main driver of AEM in family firms. The coefficient on family ownership

(FF_OWN) is much more relevant than the coefficient on family board management

(FMB) from a statistical as well as an economic point of view. This corroborates our

hypothesis that the private interests of the founding family are driving the AEM activities.

In line with this result, we find in model 4 that AEM is particularly prevalent in family

firms where either the founder or an external manager is appointed as the CEO (F_CEO,

H_CEO). As far as the founding CEO is concerned, this is not surprising as the motives for

earnings management, especially to stay in control of the firm, may be strongly developed

also in this case. Moreover, the founding CEO may also be driven by socio-emotional

factors arising from being in control of the firm (Stockmans et al., 2010).

What is probably more intriguing is the fact that also externally hired CEOs engage

strongly in AEM, if they are hired by a family firm. However, our primary hypothesis also

delivers an explanation for that. The externally hired CEO, similarly to the CEO in a

19

widely-held firm, has an incentive to influence his compensation by earnings management

activities. However, as opposed to the widely-held firm, where REM may be a preferred

instrument for doing that, in the family-owned firm there may be strong limits set to such

REM activities because of the tight control exercised by the family. Therefore, the

externally hired CEO in a family firm has a different trade-off rate between AEM and

REM as the CEO in a widely-held firm leading him to engage more in AEM. As an

additional explanation one should take into account that variable compensation in family

firms tends to be rather accounting than stock based as compared to non-family firms

(Cheng and Firth, 2006; Young and Tsai, 2008; Gomez-Mejia et al., 2003). Therefore,

there is an additional incentive for the external manager to prefer AEM over REM.

The coefficient on ownership concentration (HERF) is negative and significant in models 2

and 3. This result may indicate that earnings management on average decreases with

increasing ownership concentration. One explanation might be that the existence of other

large shareholders sets a limit to the AEM activities, which is in line with our reasoning

that the degree of earnings management is confined by the degree of corporate control.

To assess the robustness of our results on AEM, we use the model applied by DeFond and

Jiambalvo (1994), Kasznik (1999) and Cohen and Zarowin (2010) among others to

estimate discretionary accruals. Since this alternative measure produces consistent results

with the Ball and Shivakumar (2006) model, results are not tabulated.

5.2 Family Firms and Real Earnings Management

Consistent with the analysis on accounting earnings management, four models are

examined to analyze effects of founding family involvement on real earnings management

based on pooled OLS and between effects models. The results in Table 6 are from the

20

pooled OLS regressions. Results are largely consistent with results derived from the

between effects models which are therefore not tabulated.

– Insert Table 6 around here –

According to the results presented in Table 6 we find some indication that REM is less

pronounced in family firms. Regardless of the model specification, coefficients are positive

indicating that there is a lower level of REM in family-owned firms. However, one has to

admit that from a statistical point of view the evidence is rather weak, as only in three

models the coefficients are statistically significant. Two of these three significant

coefficients measure family ownership, which corroborates our reasoning that family

ownership has a dampening impact on REM. The third coefficient relates to the

appointment of an externally hired CEO. As already explained in the preceding section, we

expect that such an externally hired CEO should have an incentive to engage in AEM

rather than in REM. However, by splitting up the impact into family ownership and family

management variables, we do not get any significant results.

As an alternative measure for real earnings management, we use discretionary expenses.

Results are consistent with those presented in Table 6 and indicate that REM is

significantly lower in family firms. Due to limited space, results are not tabulated.

5.3 Additional Analyses

5.3.1 Earnings Management and Self-Selection Bias

Two objections against our results could be raised. First, one could argue that AEM and

REM should be analyzed in an integrated framework as it has been presumed that firms are

using both instruments simultaneously. Second, and more importantly, it may well be that

firms self-select into the group of family or non-family firms. As has already been shown

21

in Table 3 the industry distribution of family firms is quite different from the distribution

of non-family firms. For different industries, however, the earnings management incentives

as well as constraints may be totally different. Therefore, it may well be that other firm

characteristics are responsible for forming this selection effect, which are much harder to

control for.

We therefore repeat our analysis by taking into account these two objections. For that

purpose we estimate a two-stage model using the Heckman (1979) method. In the first

stage, we explain total earnings management (Total_EM), i.e. AEM and REM, by a model

that takes economic variables into account that are expected to explain earnings

management activities with the exception of ownership variables (Cohen and Zarowin,

2010). In the second stage we explain, conditional on the results in the first stage, the

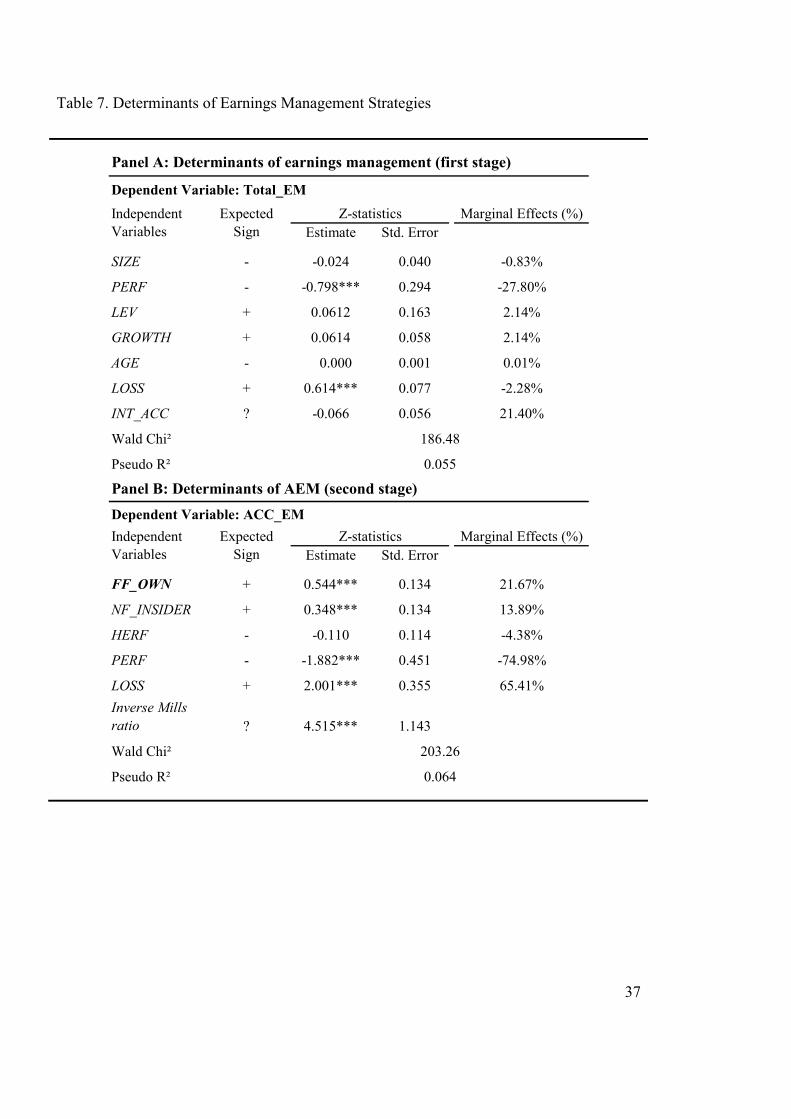

preference for either AEM or REM. Results are presented in Table 7.

– Insert Table 7 around here –

From a technical perspective, it should be noted that Total_EM is our measure whether a

firm-year observation is classified as an earnings management firm-year observation or

not. It is an indicator variable that equals one if either discretionary accruals are above or

discretionary cash flows are below the median in the respective year, and zero otherwise.

In the first stage, we get the expected result that earnings management activities are driven

by profitability (negative impact) and the existence of a loss (positive impact). In the

second stage, we see that these variables are still significant. However, on top of that also

the ownership structure becomes relevant. In fact, it clearly emerges that AEM is higher in

family firms, but also in insider-held firms, while REM is lower in these two types of

firms. Moreover, the coefficients are highly significant in all models. This is also true for

22

the coefficient on the inverse Mills ratio strongly indicating that there might be a selection

bias in the data.

To sum up, even by correcting for a potential selection bias and by taking an integrated

view on AEM as well as REM, we find results strongly corroborating our hypotheses that

family firms engage more in AEM and less in REM as compared to their non-family

counterparts.

5.3.2 Non-linear Effects of Family Ownership on Earnings Management

We test for non-linearity between family ownership and earnings management in three

ways. Following Wang (2006), we generate three indicator variables, one for family firms

without family ownership but presence of family members on one of the boards

(No_FAM), one for weak (W_FAM) and one for strong family ownership (S_FAM). The

indicator variable on strong family ownership (S_FAM) equals one if the percentage of

common stock owned by family members is greater than or equal to the median of family

ownership in the respective year (about 30%), and zero otherwise. Accordingly, the

dummy variable on weak family ownership (W_FAM) equals one if the percentage of

common stock owned by the family is below the median value of family ownership in the

respective year, and zero otherwise. In a second model, we add the square of family

ownership to the models for accounting earnings management (FF_OWN and FF_OWN²).

In a third model, we include dummy variables for family ownership according to the

different control thresholds in German listed firms (FF_1 to FF_4): An ownership level

between zero and 25% (blocking minority, FF_1), between 25% and 50% (simple

majority, FF_2), between 50% and 75% (qualified majority, FF_3) and above the qualified

majority of 75% (FF_4).

Results are presented in table 8. Again, our results corroborate the hypotheses that AEM

activities are driven by family ownership and not by family management. In fact, while the

23

coefficients on weak family ownership (W_FAM) and strong family ownership (S_FAM)

are positive and statistically significant, we do not find any impact in those firms where

families do not have significant ownership stakes but are present in the supervisory or

management board (No_FAM).

– Insert Table 8 around here –

As far as different levels of ownership are concerned, our hypothesis does not make a clear

prediction. Nevertheless, one might expect that the impact on AEM is the larger the larger

the ownership stake of the family is. While the result in model 2 is not against this

presumption, this is not true for the results of model 3 in Table 8. In fact, according to

these results AEM activities do not seem to strongly depend on the ownership stake held

by the founding family. This is at least true for ownership stakes of up to 75% of voting

rights. Beyond this level the coefficient on family ownership is not significantly different

from zero. This could be an indication that incentives to manage accounting earnings are

particularly pronounced for medium levels of family ownership. However, it should be

taken into account that this result may also be driven by data issues, as the number of

family firms in which the family holds more than 75% of the voting rights becomes very

small (4.5% of family firms).

– Insert Table 9 around here –

As far as REM is concerned, our hypothesis predicts that these activities should be less

pronounced the larger the ownership stake of the family is. This is true, at least, if we

assume that the cost of REM activities gets more strongly weighted the more this cost is

borne by the family. The results presented in Table 9 slightly corroborate this hypothesis.

In fact, REM is less pronounced in firms with strong family ownership (S_FAM), whereas

24

the coefficients on weak or no family influence are not significantly different from zero

according to model 1. The results in model 2, however, are not in accordance with our

hypothesis, while the results in model 3 only partially support it.

4.3.2 Presence of Other Large Shareholders

As a final remark, it should be noted that results are robust when variables that can be used

as proxy for the presence of other blockholders are included in the models. At first, we add

the percentage held by outside blockholders, i.e. shareholders owning more than 5% of

shares in the firm. Secondly, we control for other types of large shareholders that may

affect earnings characteristics, i.e. banks, strategic shareholders, private equity and

institutional investors. Untabulated results suggest that the presence of these types of

outside blockholders is not systematically associated with AEM or REM and does not

affect our results.

5. Summary and Conclusion

When engaging in earnings management firms are faced with a trade-off between AEM

and REM. While there are several papers investigating the two mechanisms on an isolated

basis, only few studies have taken an integral view. This paper aimed to shed new light on

the understanding of this trade-off.

Specifically, we have argued that the outcome of this trade-off is driven by the motives

driving earnings management, the ownership structure of the firm and the institutional

environment. In order to test this hypothesis, we have used a large panel data set of listed

German firms over the period 1998 to 2008. Our ownership variable of interest was related

to the founding family concept. We hypothesized that firms owned by their founding

families should engage more in AEM and less in REM activities. In a nutshell, this is

25

because at the one side they engage in earnings management not because of capital market

pressures, but because of control motives (i.e. avoiding the breach of covenant clauses or

influencing the dividends). At the other side, because of their large ownership stakes they

dislike REM because of its negative performance impact.

Our results corroborate this hypothesis. We find clear evidence that family firms engage

more actively in AEM compared to their non-family counterparts, while they engage less

in REM. This result is robust against a potential selection bias. In fact, by applying a two-

stage Heckman selection model we can clearly corroborate these results. Moreover, by

splitting-up the family involvement into a family ownership and a family management

component, it can be shown that the effect is driven by family ownership. However, with

respect to the question whether ownership has a linear or non-linear impact on earnings

management activities the findings are rather mixed.

Our findings also shed some light on the question why evidence on AEM in family firms

presented hitherto was mixed. We argue that the ownership structures as well as the

institutional environment, especially the level of investor protection, influence the trade-off

between AEM and REM. As this impact is different for family and non-family firms it may

well be that the relative level of AEM changes across countries.

26

References

Ali, A., Chen, T.-Y. and Radhakrishnan, S. (2007) Corporate disclosures by family firms,

Journal of Accounting and Economics, 44(1-2), pp. 238–286.

Ampenberger, M., Schmid, T., Achleitner, A.-K., Kaserer, C. (2012) Capital structure

decisions in family firms: empirical evidence from a bank-based economy, Review of

Managerial Sciences, Forthcoming.

Anderson, R. C. and Reeb, D. M. (2003) Founding-Family Ownership and Firm

Performance: Evidence from the S&P 500, The Journal of Finance, 58(3), pp. 1301–

1328.

Andres, C. (2008) Large shareholders and firm performance – An empirical examination of

founding-family ownership, Journal of Corporate Finance, 14 (4), pp. 431–445.

Armstrong, C. S., Guay, W.R. and Weber, J.P. (2010) The Role of Information and

Financial Reporting in Corporate Governance and Debt Contracting, Journal of

Accounting and Economics, 50(2-3), pp. 179–234.

Baber, W. R., Fairfield, P. M. and Haggard, J. A. (1991) The Effect of Concern about

Reported Income on Discretionary Spending Decisions: The Case of Research and

Development, The Accounting Review, 66(4), pp. 818–829.

Ball, R., Kothari, S. P. and Robin, A. (2000) The effect of international institutional factors

on properties of accounting earnings, Journal of Accounting and Economics, 29(1),

pp. 1–51.

Ball, R., Robin, A. and Wu, J. S. (2003) Incentives versus standards: properties of

accounting income in four East Asian countries, Journal of Accounting and

Economics, 36(1-3), pp. 235–270.

Ball, R. and Shivakumar, L. (2006) The Role of Accruals in Asymmetrically Timely Gain

and Loss Recognition, Journal of Accounting Research, 44(2), pp. 207–242.

Bar-Yosef, S. and Prencipe, A. (2011) Earnings Management and Corporate Governance

in Family-Controlled Companies, Journal of Accounting, Auditing and Finance,

26(2), pp. 199–227.

27

Bartov, E. (1993) The Timing of Asset Sales and Earnings Manipulation, The Accounting

Review, 68(4), pp. 840–855.

Bens, D. A., Nagar, V., Skinner, D. J. and Wong, M. H. F. (2003) Employee stock options,

EPS dilution, and stock repurchases, Journal of Accounting and Economics, 36(1-3),

pp. 51–90.

Bergstresser, D. and Philippon, T. (2006) CEO incentives and earnings management,

Journal of Financial Economics, 80(3), pp. 511–529.

Bushee, B. (1998) The influence of institutional investors on myopic R&D investment

behavior, The Acounting Review, 73(3), pp. 305–333.

Cheng, S. and Firth, M. (2006) Family Ownership, Corporate Governance, and Top

Executive Compensation, Managerial and Decision Economics, 27(7), pp. 549–561.

Cohen, D. A., Dey, A. and Lys, T. Z. (2008) Real and accrual-based earnings management

in the pre- and post-sarbanes-oxley periods, The Accounting Review, 83(3), pp. 757–

787.

Cohen, D.A. and Zarowin, P. (2010) Accrual-based and real earnings management

activities around seasoned equity offerings, Journal of Accounting and Economics,

50(1), pp. 2–19.

Dechow, P. M. and Skinner, D. J. (2000) Earnings Management: Reconciling the Views of

Accounting Academics, Practitioners, and Regulators, Accounting Horizons, 14(2),

pp. 235–250.

Dechow, P. M. and Sloan, R. (1991) Executive incentives and the horizon problem: an

empirical investigation, Journal of Accounting and Economics, 14(1), pp. 15–89.

DeFond, M. L. and Jiambalvo, J. (1994) Debt covenant violation and manipulation of

accruals, Journal of Accounting and Economics, 17(1-2), pp.145–176.

Dhaliwal, D. S., Salamon, G. L. and Dan Smith, E. (1982) The effect of owner versus

management control on the choice of accounting methods, Journal of Accounting

and Economics, 4(1), pp. 41–53.

28

Ewert, R. and Wagenhofer, A. (2005) Economic Effects of Tightening Accounting

Standards to Restrict Earnings Management, The Accounting Review, 80(4), pp.

1101–1124.

Gabrielsen, G., Gramlich, J. D. and Plenborg, T. (2002) Managerial Ownership,

Information Content of Earnings, and Discretionary Accruals in a Non-US Setting,

Journal of Business Finance & Accounting, 29(7/8), pp. 967–988.

García Lara, J. M., García Osma, B. and Araceli, M. (2005) The Effect of Earnings

Management on the Asymmetric Timeliness of Earnings, Journal of Business

Finance & Accounting, 32(3/4), pp. 691–726.

Gomez-Mejia, L. R., Larraza-Kintana, M. and Makri, M. (2003) The Determinants of

Executive Compensation in Family-Controlled Public Corporations, The Academy of

Management Journal, 46(2), pp. 226–237.

Graham, J. R., Harvey, C. R. and Rajgopal, S. (2005) The economic implications of

corporate financial reporting, Journal of Accounting and Economics, 40(1-3), pp. 3–

73.

Gunny, K. (2010) The Relation between Earnings Management Using Real Activities

Manipulation and Future Performance: Evidence from Meeting Earnings

Benchmarks', Contemporary Accounting Research, 27 (3), pp. 855–888.

Healy, P. M. (1985) The effect of bonus schemes on accounting decisions, Journal of

Accounting and Economics, 7(1-3), pp. 85-107.

Healy, P. M. and Wahlen, J. M. (1999) A Review of the Earnings Management Literature

and Its Implications for Standard Setting, Accounting Horizons, 13(4), pp. 365–383.

Herrmann, D., Inoue, T. and Thomas, W. B. (2003) The Sale of Assets to Manage

Earnings in Japan, Journal of Accounting Research, 41(1), pp. 89–108.

Himmelberg, C. P., Hubbard, R. G. and Palia, D. (1999) Understanding the determinants of

managerial ownership and the link between ownership and performance, Journal of

Financial Economics, 53(3), pp. 353–384.

Holthausen, R. W., Larcker, D. F. and Sloan, R. G. (1995) Annual bonus schemes and the

manipulation of earnings, Journal of Accounting and Economics, 19(1), pp. 29–74.

29

Hunt, A., Moyer, S. E. and Shevlin, T. (1996) Managing interacting accounting measures

to meet multiple objectives: A study of LIFO firms, Journal of Accounting and

Economics, 21(3), pp. 339–374.

Hutton, A. P. (2007) A discussion of 'corporate disclosure by family firms', Journal of

Accounting and Economics, 44(1-2), pp. 287–297.

Jackson, S. and Wilcox, W. (2000) Do managers grant sales price reductions to avoid

losses and declines in earnings and sales?, Quarterly Journal of Business and

Economics, 39(4), pp. 3–20.

Jaggi, B., Leung, S. and Gul, F. (2009) Family control, board independence and earnings

management: Evidence based on Hong Kong firms, Journal of Accounting & Public

Policy, 28(4), pp. 281–300.

James, H. S. (1999) Owner as manager, extended horizons and the family firm,

International Journal of the Economics of Business, 6(1), pp. 41–55.

Jara-Bertin, M. A. and Lopez Iturriaga, F. J. (2008) Earnings Management and Contest to

the Control: An Analysis of European Family Firms, Corporate Governance: An

International Review, 16(3), pp. 146–159.

Kasanen, E., Kinnunen, J. and Niskanen, J. (1996) Dividend-based earnings management:

Empirical evidence from Finland, Journal of Accounting and Economics, 22(1-3),

pp. 283–312.

Kasznik, R. (1999) On the Association between Voluntary Disclosure and Earnings

Management, Journal of Accounting Research, 37(1), pp. 57–81.

Kothari, S. P., Ramanna, K. and Skinner, D. J. (2010) Implications for GAAP from an

analysis of positive research in accounting, Journal of Accounting and Economics,

50 (2-3), pp. 246–286.

Leuz, C., Nanda, D. and Wysocki, P. D. (2003) Earnings management and investor

protection: an international comparison, Journal of Financial Economics, 69(3), pp.

505–527.

30

Morck, R., Shleifer, A. and Vishny, R. W. (1988) Management Ownership and Market

Valuation - An Empirical Analysis, Journal of Financial Economics, 20 (1-2), pp.

293–315.

Peasnell, K., Pope, P. and Young, S. (2005) Board Monitoring and Earnings Management:

Do Outside Directors Influence Abnormal Accruals?, Journal of Business Finance &

Accounting, 32(7-8), pp. 1311–1346.

Prencipe, A., Markarian, G. and Pozza, L. (2008) Earnings Management in Family Firms:

Evidence from R&D Cost Capitalization in Italy, Family Business Review, 21(1), pp.

71–88.

Roychowdury, S. (2006) Earnings management through real activities manipulation,

Journal of Accounting and Economics, 42(3), pp. 335–370.

Salvato, C. and Moores, K. (2010) Research on Accounting in Family Firms: Past

Accomplishments and Future Challenges, Family Business Review, 23(3), pp. 193–

215.

Schipper, K. (1989) Commentary on Earnings Management, Accounting Horizons 3(4),

pp. 91–102.

Schmid, T., Ampenberger, M., Kaserer, C. and Achleitner, A.-K. (2010) Controlling

Shareholders and Payout Policy: Do Founding Families Have a Special 'Taste for

Dividends'?, CEFS Working Paper No. 2010-01, Technische Universität München.

Stockmans, A., Lybaert, N. and Voordeckers, W. (2010) Socioemotional Wealth and

Earnings Management in Private Family Firms, Family Business Review, 23(3), pp.

280–294.

Thomas, J. K. and Zhang, H. (2002) Inventory changes and future returns, Review of

Accounting Studies, 7(2-3), 163–187.

Tong, Y. H. (2007) Financial Reporting Practices of Family Firms, Advances in

Accounting, 23(1), pp. 231–261.

Villalonga, B. and Amit, R. (2006) How do family ownership, control and management

affect firm value?, Journal of Financial Economics, 80(2), pp. 385–417.

31

Wang, D. (2006) Founding Family Ownership and Earnings Quality, Journal of

Accounting Research, 44(3), pp. 619–656.

Warfield, T. D., Wild, J. J. and Wild, K. L. (1995) Managerial ownership, accounting

choices, and informativeness of earnings, Journal of Accounting and Economics,

20(1), pp. 61–91.

Young, C.-S. and Tsai, L.-C. (2008) The sensitivity of compensation to social capital:

Family CEOs vs. nonfamily CEOs in the family business groups, Journal of

Business Research, 61(4), pp. 363-374.

Zang, A. (2012) Evidence on the Trade-Off between Real Activities Manipulation and

Accrual-Based Earnings Management, The Accounting Review, 87 (2), pp. 675–703.

32

Table 1.Distribution of Family Firms and Family Firm Characteristics

Year No. of Firms

No. of Family Firms

Percentage of Family Firms

Family Ownership

Family Management

F_CEO D_CEO H_CEO FF_Chair

46.15% 17.95% 35.90% 12.09%1998 305 99 32.46% 45.33% 68.69% 46.15% 17.95% 35.90% 12.09%1999 418 175 41.87% 43.01% 76.00% 60.93% 9.93% 29.14% 12.50%2000 557 291 52.24% 38.59% 77.32% 60.70% 7.39% 31.91% 12.95%2001 542 291 53.69% 37.31% 73.54% 57.63% 7.25% 35.11% 13.72%2002 499 248 49.70% 37.48% 69.76% 56.64% 6.19% 37.17% 14.17%2003 469 232 49.47% 37.81% 68.53% 57.41% 6.48% 36.11% 15.49%2004 442 214 48.42% 34.57% 68.22% 55.10% 7.65% 37.24% 17.70%2005 436 205 47.02% 30.83% 69.76% 53.97% 8.99% 37.04% 17.59%2006 434 206 47.47% 29.58% 68.93% 51.79% 9.74% 38.46% 16.92%2007 436 198 45.41% 30.33% 69.19% 55.61% 8.56% 35.83% 16.49%2008 399 176 44.11% 31.83% 65.34% 52.98% 7.74% 39.29% 15.70%56.05% 8.24% 35.72% 15.08%

Total 4,937 2,335 47.30% 35.80% 70.88% 56.05% 8.24% 35.72% 15.08%

Note: Family Ownership refers to the mean of common stock held by the founding family in family firms. Family Management presents the percentage of family firms in which one or more members of the founding family hold positions in the management board. F_CEO represents the percentage of founding CEOs, D_CEO the percentage of descendant CEOs and H_CEO the percentage of hired CEOs in family firms.

33

Table 2.Summary Statistics for Family and Non-Family Firms

Sample Period: 1998-2008

Variable

FF NF FF NF FF NF FF NF Mean Median

Governance Characteristics

FF_OWN 0.358 0.006 0.376 0.000 0.250 0.028 2,335 2,602 *** ***FMB 0.709 0.000 1.000 0.000 0.454 0.000 2,335 2,602 *** ***NF_INSIDER 0.070 0.141 0.000 0.000 0.139 0.243 2,335 2,602 *** ***HERF 0.217 0.345 0.171 0.257 0.181 0.310 2,335 2,602 *** ***Firm Characteristics

ABS_ACC 0.076 0.053 0.053 0.035 0.070 0.057 1,670 1,765 *** ***DISCR_CF 0.005 -0.003 0.000 0.007 0.118 0.864 2,066 2,436 * n.s.SIZE 4.982 5.487 4.862 5.358 0.684 0.874 2,268 2,514 *** ***PERF -0.039 0.004 0.020 0.026 0.178 0.120 2,186 2,512 *** ***LEV 0.200 0.219 0.154 0.194 0.184 0.172 2,012 2,329 *** ***GROWTH 0.210 0.095 0.089 0.040 0.515 0.367 2,217 2,508 *** ***AGE 30.15 67.82 16.00 60.00 38.55 54.54 2,335 2,602 *** ***LOSS 0.393 0.281 0.000 0.000 0.488 0.450 2,235 2,559 ***1 -INT_ACC 0.794 0.601 1.000 1.000 0.405 0.490 2,335 2,602 ***1 -

Mean Median Std. Deviation Observations Sign. of Diff.

Notes: FF refers to family firms, whereas NF refers to non-family firms. FF_OWN is family ownership, FMB is a dummy variable and one if one or more members of the founding family hold positions in the management board and zero otherwise, NF_INSIDER is non-family insider ownership, HERF is a Herfindahl index on ownership concentration at a firm and year level, ABS_ACC is absolute abnormal accruals, DISCR_CF is discretionary cash flows, SIZE is natural logarithm of total assets, PERF is net income scaled by average total assets, LEV is debt to total assets, GROWTH is sales growth, AGE is firm age since incorporation, LOSS is one if net income is negative and zero otherwise, INT_ACC is one if financial statements are prepared according to IFRS or US GAAP and zero if prepared under German GAAP (HGB). Significance of differences is assessed based on t-tests (mean) and Wilcoxon/Man-Whitney tests (median). 1denotes that significance of differences in dummy variables is assessed based on Chi² tests.

Table 3.Industry Distribution of Family and Non-Family Firms

ICB-Code Industry DescriptionNon-Family

Firms Family FirmsFamily Firms per

Industry [%]1 Basic Materials 254 64 20.13%2 Industrials 829 454 35.39%3 Consumer Goods 572 260 31.25%4 Health Care 134 256 65.64%5 Consumer Services 325 355 52.21%6 Telecommunication 28 35 55.56%9 Technology 334 864 72.12%

34

Tab

le 4

.Cor

rela

tion

Mat

rix

Variables

12

34

56

78

910

1112

1314

1516

1718

19

1AB

S_AC

C1

2D

ISC

R_C

F-0

.058

***

1

3D

umm

y_FF

0.17

4***

0.02

7*1

4FF

_OW

N0.

0801

***

0.05

83**

*0.

7124

***

1

5FM

B0.

0824

***

-0.0

30**

0.14

07**

*0.

7124

***

10.

1613

*6

FF_O

WN

x F

MB

0.02

64-0

.010

60.

1394

***

0.14

07**

* 0

.770

7***

1

7F_

CEO

0.16

13**

*0.

026*

0.59

46**

*0.

1394

***

0.01

43-0

.006

91

0.52

17*

8D

_CEO

-0.0

514*

**0.

013

0.20

24**

*0.

5946

***

-0.0

279*

*-0

.027

*-0

.108

2***

1

9H

_CEO

0.06

94**

*0.

000

0.52

17**

*0.

2024

***

0.1

743*

** 0

.195

2***

-0.2

788*

** -0

.094

7***

1

10FF

_Cha

ir0.

0341

**0.

002

0.29

30**

* 0

.240

1***

-0.0

050.

0106

-0.0

338*

*0.

0198

0.3

995*

**1

11N

F_IN

SID

ER0.

017

0.01

1-0

.197

***

-0.2

957*

** 0

.101

4***

-0.0

28**

-0.0

874*

** -0

.096

6***

-0.1

092*

**-0

.049

0***

1

12H

ERF

-0.0

82**

*0.

003

-0.2

43**

* -0

.047

8***

-0.0

546*

**0.

0119

-0.2

004*

**0.

0335

** -0

.105

1***

-0.0

667*

**0.

0285

**1

13SI

ZE-0

.275

***

-0.0

19-0

.304

***

-0.1

823*

**-0

.122

6***

-0.0

504*

**-0

.312

8***

-0.0

015

-0.0

458*

**-0

.054

2***

-0.1

440*

** 0

.108

4***

1

14PE

RF-0

.364

***

0.33

3***

-0.1

43**

*-0

.032

** -0

.106

5***

-0.0

548*

** -0

.157

8***

0.0

540*

** -0

.037

8***

0.02

190.

000

0.1

196*

** 0

.286

2***

1

15LE

V-0

.057

***

-0.0

94**

*-0

.052

***

-0.0

105

0.0

500*

** 0

.074

2***

-0.1

534*

**0.

0308

** 0

.083

7***

0.0

586*

** 0

.090

6***

-0.0

762*

* 0

.089

7***

-0.0

566*

**1

16G

ROW

TH-0

.001

0.03

6**

0.12

8***

0.0

903*

**-0

.003

3-0

.015

4 0

.159

3***

-0.0

257*

0.00

20.

0091

0.0

251*

-0.0

802*

**-0

.064

0***

0.0

552*

** -0

.101

6***

117

AGE

-0.2

27**

*-0

.02

-0.3

67**

* -0

.209

2***

-0.1

371*

** -0

.082

0***

-0.

3959

***

0.0

827*

** -0

.073

9***

-0.0

739*

**-0

.015

9 0

.255

6***

0.4

722*

** 0

.216

8***

0.0

453*

** -0

.164

9***

1

18LO

SS0.

318*

**-0

.258

***

0.11

8***

0.0117

0.0

884*

** 0

.029

5**

0.1

514*

** -

0.07

80**

*0.

0245

-0.0

059

0.0

315*

*-0

.108

0***

-0.3

080*

** -0

.692

5***

0.0

837*

**-0

.049

4***

-0.2

332*

**1

19IN

T_AC

C0.

065*

**0.

037*

*0.

208*

** 0

.073

8***

0.0

724*

** 0

.032

4**

0.2

295*

** -

0.07

87**

* 0

.051

0***

0.0

436*

**-0

.033

4**

-0.2

861*

**-0

.061

1***

-0.0

891*

** -

0.11

32**

* 0

.080

1***

-0.2

822*

**0.

0656

***

1

*, *

*, *

** s

igni

fican

tly d

iffer

ent f

rom

zer

o at

the α

= 0.

1, 0

.05

and

0.01

leve

l, re

spec

tivel

y.

35

Table 5.Effects of Family Involvement on Discretionary Accruals

Dependent Variable: ABS_ACC

Estimate Std. Error Estimate Std. Error Estimate Std. Error Estimate Std. Error

Intercept ? 0.109*** 0.011 0.114*** 0.011 0.110*** 0.012 0.111*** 0.012

Dummy_FF ? 0.008*** 0.003

FF_OWN ? 0.012** 0.006 0.015** 0.007

FMB ? 0.007 0.006

FF_OWN X FMB ? -0.014 0.012

F_CEO ? 0.008* 0.004

D_CEO ? -0.003 0.006

H_CEO ? 0.011*** 0.004

Family_Chair ? 0.001 0.006

NF_INSIDER ? 0.005 0.006 0.005 0.006 0.006 0.006 0.005 0.006

HERF ? -0.007 0.005 -0.009** 0.005 -0.008** 0.005 -0.006 0.005

SIZE - -0.008*** 0.002 -0.008*** 0.002 -0.008*** 0.002 -0.008*** 0.002

PERF - -0.126*** 0.021 -0.128*** 0.021 -0.126*** 0.021 -0.126*** 0.022

LEV + -0.024*** 0.008 -0.025*** 0.008 -0.024*** 0.008 -0.025*** 0.008

GROWTH + -0.003 0.004 -0.003 0.004 -0.004 0.004 -0.004 0.004

AGE - -0.000*** 0.000 -0.000*** 0.000 -0.000*** 0.000 -0.000*** 0.000

LOSS + 0.013*** 0.004 0.013*** 0.004 0.0131*** 0.004 0.013*** 0.004

INT_ACC ? -0.002 0.003 -0.001 0.003 -0.002 0.003 -0.003 0.003

F-Value

p-value F-test

Adj R²

N

30.12

0.000

0.179

3,008

Model 4

27.85

0.000

0.181

2,948

35.47

0.179

0.000

36.35

0.000

Independent Variables

Expected Sign

Model 1 Model 2 Model 3

0.180

3,0083,008 Notes: Results are derived from pooled OLS models. ABS_ACC denotes absolute abnormal accruals; Dummy_FF is an indicator variable that equals one if the founding family holds more than 25% of ordinary shares or positions in the management or supervisory board; FF_OWN is the percentage of common shares held by the family; FMB is a dummy variable and equals on if a family member is involved in the management of the firm and zero otherwise. F_CEO is one if one of the founders serves as CEO, D_CEO is one if there is a descendant CEO, H_CEO is one if there is an external CEO in a family firm. NF_INSIDER is the percentage of common shares held by non-founding family insiders; HERF is a Herfindahl index and corresponds to ownership concentration; SIZE is the natural logarithm of total assets; PERF is net income before extraordinary items scaled by average total assets; LEV is total debt to total assets; GROWTH is sales growth; LOSS is an indicator variable which equals one if net income is negative and zero otherwise; INT_ACC is an indicator variable that equals 1 if consolidated financial statements are prepared according to IFRS or US GAAP and zero otherwise. Standard errors are clustered on a year and firm level following Petersen (2009). *** / ** / * indicate a two-tailed significance level at 99% / 95% / 90%. Mean VIFs are between 1.35 and 1.59, max. VIF 2.46 (FF_OWN X FMB).

36

Table 6.Effects of Family Involvement on Discretionary Cash Flows

Dependent Variable: Discr_CF

Estimate Std. Error Estimate Std. Error Estimate Std. Error Estimate Std. Error

Intercept ? 0.090*** 0.022 0.089*** 0.021 0.0895*** 0.021 0.089*** 0.022

Dummy_FF ? 0.009 0.006

FF_OWN ? 0.026** 0.012 0.0280* 0.016

FMB ? -0.001 0.011

FF_OWN X FMB ? -0.001 0.026

F_CEO ? 0.010 0.009

D_CEO ? 0.008 0.014

H_CEO ? 0.014* 0.008

Family_Chair ? -0.009 0.011

NF_INSIDER ? 0.010 0.011 0.015 0.012 0.015 0.012 0.010 0.012

HERF ? -0.003 0.009 -0.006 0.009 -0.006 0.009 -0.001 0.009(0.00895)SIZE - -0.017*** 0.004 -0.016*** 0.004 -0.0163*** 0.004 -0.016*** 0.004

PERF - 0.312*** 0.027 0.310*** 0.027 0.310*** 0.027 0.315*** 0.028

LEV + -0.034** 0.014 -0.036** 0.014 -0.0362** 0.014 -0.033** 0.015

GROWTH + -0.009 0.007 -0.009 0.007 -0.008 0.007 -0.007 0.007

AGE - 0.000 0.000 0.000 0.000 0.000 0.000 0.000 0.000

LOSS + -0.015** 0.007 -0.015** 0.007 -0.0145** 0.007 -0.015** 0.007

INT_ACC ? 0.017*** 0.005 0.017*** 0.005 0.017*** 0.005 0.014*** 0.005

F-Value

p-value F-test

Adj R²

N

27.64

Model 4Independent Variable

Expected Sign

Model 1 Model 2 Model 3

23.66

0.000

0.132

3,767

32.64

0.000

0.133

3,859

30.12

0.134

0.000

3,859

0.134

3,859

0.000

Notes: Results are derived from pooled OLS models. Discr_CF denotes discretionary cash flows; Dummy_FF is an indicator variable that equals one if the founding family holds more than 25% of ordinary shares or positions in the management or supervisory board; FF_OWN is the percentage of common shares held by the family; FMB is a dummy variable and equals on if a family member is involved in the management of the firm and zero otherwise. F_CEO is one if one of the founders serves as CEO, D_CEO is one if there is a descendant CEO, H_CEO is one if there is an external CEO in a family firm. NF_INSIDER is the percentage of common shares held by non-founding family insiders; HERF is a Herfindahl index and corresponds to ownership concentration; SIZE is natural logarithm of total assets; PERF is net income before extraordinary items scaled by average total assets; LEV is total debt to total assets; GROWTH is sales growth; LOSS is an indicator variable which equals one if net income is negative and zero otherwise; INT_ACC is an indicator variable that equals 1 if consolidated financial statements are prepared according to IFRS or US GAAP and zero otherwise. Standard errors are clustered on a year and firm level following Petersen (2009). *** / ** / * indicate a two-tailed significance level at 99% / 95% / 90%. Mean VIFs are between 1.33 and 1.57, max. VIF 2.46 (FF_OWN X FMB).

37

Table 7. Determinants of Earnings Management Strategies

Dependent Variable: Total_EMMarginal Effects (%)

Estimate Std. Error

SIZE - -0.024 0.040 -0.83%

PERF - -0.798*** 0.294 -27.80%

LEV + 0.0612 0.163 2.14%

GROWTH + 0.0614 0.058 2.14%

AGE - 0.000 0.001 0.01%

LOSS + 0.614*** 0.077 -2.28%

INT_ACC ? -0.066 0.056 21.40%

Wald Chi²

Pseudo R²

Dependent Variable: ACC_EMMarginal Effects (%)

Estimate Std. Error

FF_OWN + 0.544*** 0.134 21.67%

NF_INSIDER + 0.348*** 0.134 13.89%

HERF - -0.110 0.114 -4.38%

PERF - -1.882*** 0.451 -74.98%

LOSS + 2.001*** 0.355 65.41%Inverse Mills ratio ? 4.515*** 1.143

Wald Chi²

Pseudo R²

Dependent Variable: Real_EMMarginal Effects (%)

Estimate Std. ErrorM Z-statisticsFF_OWN - -0.275** 0.129 -10.98%

NF_INSIDER - -0.206 0.148 -8.20%

HERF ? 0.112 0.106 0.0447

PERF - -0.422 0.446 -16.83%

LOSS + -1.448*** 0.350 -51.77%Inverse Mills ratio ? -5.629*** 1.137

Wald Chi²

Pseudo R² 0.067

Independent Variables

Expected Sign

Z-statistics

Z-statistics

Z-statistics

Panel C: Determinants of REM (second stage)

Independent Variables

Expected Sign

Z-statistics

203.26

0.064

205.78

Independent Variables

Expected Sign

Z-statistics

Panel A: Determinants of earnings management (first stage)

186.48

0.055

Panel B: Determinants of AEM (second stage)

38

Table 7. Determinants of Earnings Management Strategies (continued)

Dependent Variable: Real_EMMarginal Effects (%)

Estimate Std. ErrorM Z-statisticsFF_OWN - -0.275** 0.129 -10.98%

NF_INSIDER - -0.206 0.148 -8.20%

HERF ? 0.112 0.106 0.0447

PERF - -0.422 0.446 -16.83%

LOSS + -1.448*** 0.350 -51.77%Inverse Mills ratio ? -5.629*** 1.137

Wald Chi²

Pseudo R² 0.067

Independent Variables

Expected Sign

Z-statistics

Z-statistics

Z-statistics

Panel C: Determinants of REM (second stage)

205.78

Notes: This table presents the results of two probit models. For Panel A, the dependent variable Total_EM takes the value of 1 if either the level of absolute discretionary accruals (REM) is below or the level of discretionary accruals (AEM) is above the median value and zero otherwise. For Panel B, the dependent variable Real_EM takes the value of 1 if the discretionary expenses multiplied by negative one is above the median and zero otherwise. For Panel C, the dependent variable ACC_EM takes the value of 1 if absolute abnormal accruals are above median in the respective year and zero otherwise. SIZE is the natural logarithm of total assets; PERF is net income before extraordinary items scaled by average total assets; LEV is total debt to total assets; GROWTH is sales growth; LOSS is one if net income is negative and zero otherwise; INT_ACC is one if financial statements are prepared according to IFRS or US GAAP and zero otherwise. FF_OWN is founding family ownership; NF_INSIDER non-founding family insider ownership; HERF is a Herfindahl index and corresponds to ownership concentration. Standard errors are clustered on a year and firm level following Petersen (2009). *** / ** / * indicate a two-tailed significance level at 99% / 95% / 90%.

39

Table 8.Non-linearity between Family Ownership and Discretionary Accruals

Dependent Variable: ABS_ACC

Estimate Std. Error Estimate Std. Error Estimate Std. Error

Intercept ? 0.106*** 0.011 0.110*** 0.011 0.109*** 0.011

No_FAM ? 0.008 0.005

W_FAM ? 0.011*** 0.004

S_FAM ? 0.010** 0.004

FF_OWN + 0.041** 0.020

FF_OWN² - -0.045 0.028

FF_1 ? 0.008* 0.005

FF_2 ? 0.012*** 0.005

FF_3 ? 0.007* 0.004

FF_4 ? 0.004 0.008

NF_INSIDER ? -0.006 0.005 0.006 0.006 -0.005 0.005

HERF ? 0.006 0.006 -0.007 0.005 0.006 0.006

SIZE - -0.008*** 0.002 -0.008*** 0.002 -0.008*** 0.002

PERF - -0.126*** 0.021 -0.128*** 0.021 -0.127*** 0.021

LEV + -0.024*** 0.008 -0.024*** 0.008 -0.024*** 0.008

GROWTH + -0.004 0.004 -0.003 0.004 -0.003 0.004

AGE - -0.000*** 0.000 -0.000*** 0.000 -0.000*** 0.000

LOSS + 0.013*** 0.004 0.013*** 0.004 0.013*** 0.004

INT_ACC ? -0.002 0.003 -0.002 0.003 -0.002 0.003

F-Value

p-value F-test

Adj. R²

N

0.000

3,008 3,008

0.000

0.180

0.000

0.180

30.39

3,008

0.181

Model 3

32.33 27.43

Expected Sign

Model 2Model 1Independent Variable