ecag volume 12

TRANSCRIPT

Financial OutlookISSUE

12MAY- AUGUST

2016

GCC ECONOMIC UPDATES

UAE SHIFTS FROM BORROWERSTO A LENDERS MARKET

HOW VAT WILL IMPACTUAE BUSINESSES

5

13

10

Created by

2

COVERSTORY FINANCIAL OUTLOOK

BREXIT:BRITaIn LEavEs ThE EU

3

COnTEnTFINANCIAL OUTLOOK

CONTENTEDITOR’S DESK

VAT IN THE UAE:WHAT DObUSINESSESNEED TO DO?

bANKING FEATURE:UAE SHIFTS FROM bORROWERS TO A LENDERS MARKET

WILL PRICES OF PRODUCTS AND SERVICES GO UP IN THE UAE?

yOUR qUESTIONS,ANSWERED

HOW DOESVAT WORK?

UAE FINANCE NEWS

4

GCC ECONOMICUPDATES13

5

7

8

19

12

10

4

EDITOR’S DESK FINANCIAL OUTLOOK

Dear Readers,

We are happy to inform you that we have given our newsletter a complete makeover. It has a new name, looks great, and the content is amazing. It has happened only because of your continuous support and guidance. Our newsletter from the Emirates Chartered

Accountants Group (12th edition onwards) will henceforth be known as Financial Outlook. We expect your continuous association with us for all our future issues as well.

On June 23rd, 2016, the people in the UK voted to exit from the European Union. In the aftermath of Brexit, uncertainty is the only certainty. The global market immediately lost $2.1 trillion in value. Still, most of the economists concluded that this phenomenon would not lead to a major economic downturn.

If we look into the GCC perceptive, the top three concerns are the value of the British Pound, its effect on the investments made in the UK and trade relations between the GCC and the UK. British currency fell down to a 30 years record low against USD, the peg for GCC currencies. GCC-based investors made a lot of investments in the UK, especially in its property market. The decrease in currency value will lead to a substantial decline in value of investments and return from such investments. But if we look into the trade between UK and GCC, imports to GCC is more than double of the exports. In this context, the weaker British Pound will help the importers to improve their business by introducing high quality of products with better price. Since UK has lost its free trade access with EU, it will be focusing to build trade ties with wealthier and more safe countries in the Middle East i.e. GCC. So, if we look into the overall impact of Brexit on GCC, it seems that the positive impact is higher than the negative facts.

For the cover story of this newsletter, we will be talking about the upcoming VAT in the UAE, its likely effects on the UAE economy and counteractive measures for the business community. My partner Pradeep Sai has written an article on changes seen recently in the money lending market in the UAE under the article “UAE shifts from borrowers market to lenders market”. Partner Ragesh Mattummal has answered queries related to the company incorporation in the UAE. In addition to this, there are summarized GCC economic updates as well as latest news updates in the UAE.

I am sure the new version of our newsletter “Financial Outlook” which covers more analysis on the latest trends on the business world will definitely help you in your day-to-day business activities. We expect your continued support. I wish everyone to have a good read ahead.

E D I T O R ’ S D E S K

CA. Manu Nair, FCA, CMACEO, Emirates Chartered

Accountants Group

5

VAT In ThE UAEWhaT do BUsInEssEs nEEd To do?

Value Added Tax (VAT) is a tax on consumption and it applies to almost all goods and services. Most managements are aware that the GCC

governments have decided to adopt VAT as an effort to diversify the economy and generate revenue. UAE will also adopt VAT which applies to almost all goods and services except basic food items, healthcare and education. So, it will not only impact consumers but also businesses across the region.

VAT is a widely discussed topic among business owners that raises an important query – how should they be prepared for VAT before it hits them? Their concern is the impact of increase in cost of doing

business in the region. It might require more time for business owners to get accustomed with the new system and make a shift from the existing operating structure. They may have to screen their existing suppliers and invest more in manpower to ensure that the right talent is available in the organization.

Though the burden normally lies on the ultimate consumer, the business entities need to change the systems, processes and procedures to comply with the new legal requirement expected to be implemented by the government effective from 1st Jan 2018.

COVER STORYFINANCIAL OUTLOOK

In the UAE, the SME business sector does’nt

have a stringent financial system and operating policies. SMEs are going to face challenges implementing the new tax laws as compared to the larger organizations which are operated with proper operating policies and structures.

Normal requirements under VAT system that companies need to comply with:

• At the time of purchase of goods or availing of services – ensure that in case of taxable items, the tax has been properly charged (input tax) by the supplier and details given in the invoices.

• At the time of sale or provision of services – apply the rate on the sale value and reduce the amount of input tax to arrive at the amount to be paid.

• Pay the tax due to the Govt. within the stipulated time.

• File VAT returns with the Govt. authorities by providing relevant information requested within the stipulated period.

• Maintain proper stock, invoices, accounts, VAT returns and other relevant records to justify the tax paid at the time of purchase.

The above requirements demand more control and safety on stock, invoices and records, ensure proper filing system, modification/ upgradation of software, compliance of due dates for collection, payment and remittance of tax, filing of VAT returns to Govt. etc.

In the UAE, the SME business sector does not have a stringent financial system and operating policies. As a result, SMEs are going to face challenges implementing the new tax laws as compared to the larger organizations which are normally operated with proper operating policies and structures. It will be a massive effort for the SMEs to cope with the requirements of the provisions of the new law. Every businessman need to maintain proper books

6

FINANCIAL OUTLOOK

Every business will needto maintain proper books of

accounts and will need to incorporate VAT into their accounting systems. They will need to keep accurate records to demonstrate that they have correctly applied the VAT rules.

of accounts and incorporate VAT into their accounting systems. They need to keep accurate records to demonstrate that they have applied the VAT rules correctly. The role of the accountant will be very important for the compliance of VAT. Maintenance of accounts and records is very important as per new the commercial company law.

Information System will have to take an important role in this. Accounting software needs to comply for ease of business flow and maintain a stringent legal compliance.

Every organization should properly educate their employees, well in advance before VAT is imple-mented.

Remember that VAT is going to be considered all across the region but at different dates. That’s why companies operating in other GCC countries should keep track of VAT and understand the tasks that need to undertake for a smooth transition. They must examine the impact of the special rules on intra-GCC supplies and ascertain whether the current business models need to be restructured according to the provisions of the VAT rules.

VAT can add an extra cost to the business. There can be instances where the VAT paid to suppliers is not refunded from the supply chain downstream. Furthermore, non-compliance with tax laws may also attract severe penalties. All businesses must undertake a review of their current contracts to determine if VAT has been appropriately addressed or not.

An implementation of VAT law would require a complete revamp of present practices and will insist on a higher degree of financial transparency and accounting discipline.

COVER STORY

7

COVER STORYFINANCIAL OUTLOOK

WILL PRICEs oF PRodUCTsand sERvICEs Go UP In ThE UaE?

The first question that comes up whenever the introduction of VAT is discussed among the UAE residents is whether their cost of living will go

up.

According to a recent survey conducted by CFA Society Emirates, the association for financial and investment professionals in the UAE, the introduction of VAT in the UAE by 2018 is likely to lead to higher inflation rates. The hike in price depends upon the sector of the product and service which is taken into account. The burden of VAT or any other form of taxation needs to be borne either by the business or consumers or both. The market will decide whether the consumer will bear the cost or the trader/manufacturer. In sellers’ market, traders will automatically impose the tax burden on the end consumers as a result of which, the cost of living of the individuals will go up. But, in the case of buyers’ market, the cost of VAT will have to be borne by the trader/manufacturer and cannot be passed on to the consumers.

WILL VAT BE A COST TO THE BUSINESS? If you are engaged in the supply of goods or services that are subjected to VAT (including at the zero rate) you will be entitled to reclaim VAT you incur on costs. If you are engaged in activities that are exempt from VAT and you cannot reclaim VAT incurred on costs, VAT will be a cost to your business (as suppliers will charge VAT that you cannot reclaim).

WILL IT AffECT prICES/mArgINS? VAT is a tax on consumption and is levied on the price charged to the customer. Therefore, it is expected that prices will increase by the amount of VAT. However, it is ultimately the suppliers who determine the price of their goods/services. The price needs to take account of VAT, i.e. whether you charge 100 or 105, the amount will be deemed to include VAT. For example, if a supplier charges 105 now and 105 after the introduction of VAT (at say

8

COVER STORY FINANCIAL OUTLOOK

hoW doEsvaT WoRk?

VAT is leVied AT eAch sTAge in The chAin of producTion And disTribuTion And is collecTed by

businesses on behAlf of The VAT AuThoriTies. VAT is ulTimATely pAid by The end consumer.

5%), then the supplier will only retain 100 after the introduction as 5 would be due as VAT to the tax authority. If the supplier wants to retain 105, then the price needs to be increased by the amount of VAT (say 5%) to 110.25. If the supplier does not increase the selling price when VAT is introduced, then this will affect margins as VAT will be due on the amount received.

CONCLUSION:VAT will increase prices for the end consumer at least by the amount that the VAT rate is specified by the Government. It may increase further if the suppliers decide to include the cost of administration and compliance into the end price. The longer the supply chain of any product or service, the more the price will go up.

9

FINANCIAL OUTLOOK

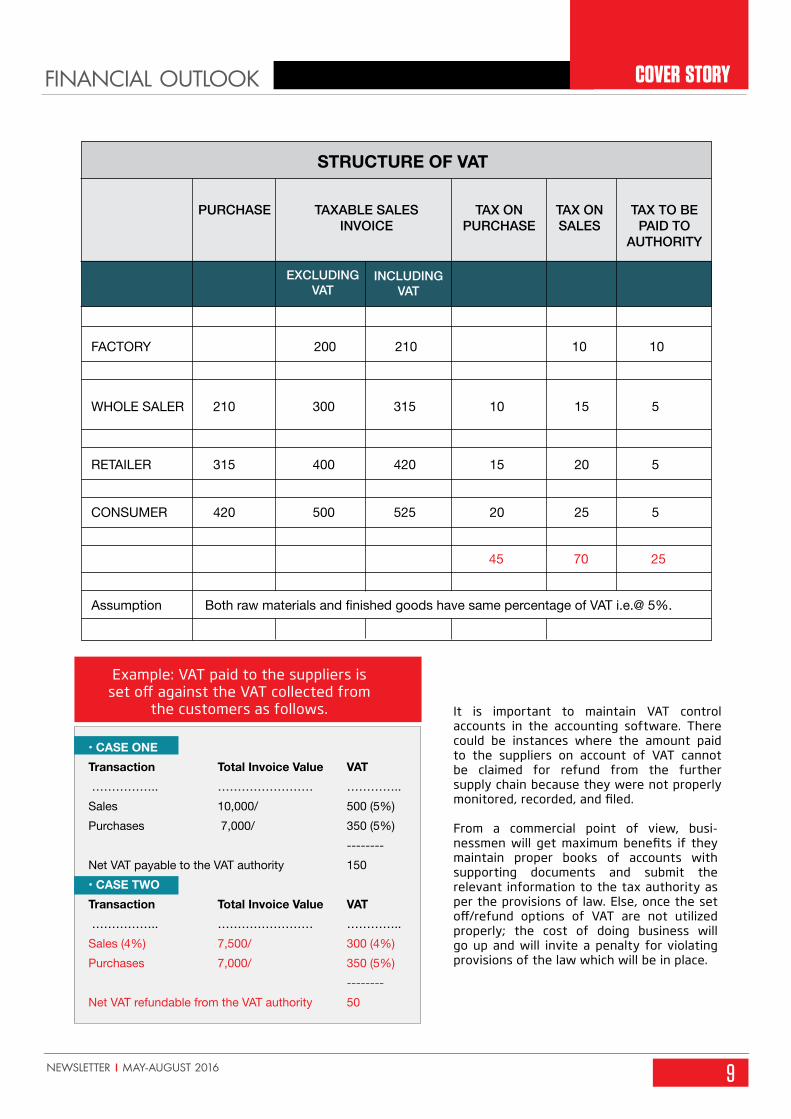

• CASE ONETransaction Total Invoice Value VAT …………….. …………………… …………..Sales 10,000/ 500 (5%)Purchases 7,000/ 350 (5%) --------Net VAT payable to the VAT authority 150• CASE TWOTransaction Total Invoice Value VAT …………….. …………………… …………..Sales (4%) 7,500/ 300 (4%) Purchases 7,000/ 350 (5%) --------Net VAT refundable from the VAT authority 50

STRUCTURE OF VAT

PURCHASE

200 210 10 10

210 300 315 10 15 5

315 400 420 15 20 5

420 500 525 20 25 5

45 70 25

FACTORY

WHOLE SALER

RETAILER

CONSUMER

Assumption Both raw materials and finished goods have same percentage of VAT i.e.@ 5%.

TAXABLE SALESINVOICE

EXCLUDINGVAT

INCLUDINGVAT

TAX ONPURCHASE

TAX ONSALES

TAX TO BEPAID TO

AUTHORITY

From a commercial point of view, busi-nessmen will get maximum benefits if they maintain proper books of accounts with supporting documents and submit the relevant information to the tax authority as per the provisions of law. Else, once the set off/refund options of VAT are not utilized properly; the cost of doing business will go up and will invite a penalty for violating provisions of the law which will be in place.

It is important to maintain VAT control accounts in the accounting software. There could be instances where the amount paid to the suppliers on account of VAT cannot be claimed for refund from the further supply chain because they were not properly monitored, recorded, and filed.

COVER STORY

10

BAnKInG FEATURE FINANCIAL OUTLOOK

UaE shIFTs FRoM BoRRoWERs To a LEndERs MaRkET

If we look into the UAE banking sectors in the year 2016, it is quite clear that compared to previous years, banks are now prefering asset

based fundings. They have become more prudent in lending as deposits have shrunk which is primarily because of a prolonged period of lower oil prices and increasing bad debts. The main focus of banks are now controlling operating costs and maintaining asset levels and quality rather than targeting growth in their business portfolios.

Analysis reveals that a drop in deposits is also promoting a more conservative lending policy and

hence the profit margin for the banks will be harder to sustain. As a result of this policy, the market in general and the SME sector in particular will be adversely impacted as they are more volatile to banking norm fluctuations.

If we look at recent history, subsequent to the global financial downturn during the 2008-2010 period, liquidity began to flow back into the banking system in 2010- 2011, aided by the strong price of oil. For the past four to five years, UAE banks have had a consistent growth run, in which they have had no substantial credit losses, a better asset quality and

Pradeep Sai,Partner, Emirates Chartered Accountants Group

11

FINANCIAL OUTLOOK

Banks have tightened their credit policy for customers in the current year and choose their customers after a stringent screening process.

funding as well as growing profits.

pLUNgE IN DEpOSITSThe UAE is the world’s sixth-largest oil producer. It uses revenue from sale of crude oil to fund more than 60% of the federal budget. Since the year 2014, the price of crude oil has come down by more than 70% of its peak value and the slowdown in economic growth resulted in less demand and more supply. The reduction of oil prices also resulted in less spending on infrastructure compared to previous years. Referring to central bank statistics, S&P noted that government and public sector deposits fell 14.2% to $94.1 billion (Dh 346 billion) towards end of 2015 from $109.7 billion (Dh 403 billion) in the previous year. This has been a key factor in tightening business lending.

SCrEENINg BOrrOWErSBanks are now more risk-averse when choosing who to lend to avoid credit losses. They have tightened their credit policy for customers in the current year and choose their customers after a stringent screening process. The UAE Central Bank said in the beginning of the year; “In the past, the main challenge for the banks was that they had a lot of liquidity in place and they had to place it into yield-earning assets, which was why the retail side of the business was strong.” But now the situation is different. Banks are now more conservative since it is harder to pump in liquidity into the system.

Tightening liquidity will probably lead to higher interest rates as the amount of money in banks

decreases. Local interest rates are dependent on two things — an increase in US dollar

rates, it flows into this region because the dirham is pegged to the dollar and

the Federal Reserve’s monetary policy. In addition to this, the rates also reflect

current liquidity conditions in the local market.

Though economic headwinds are strengthening, the experience of UAE banks in implementing stringent controls during global financial meltdown in 2008-10 gives them confidence. UAE is in the process of paradigm shift from oil driven economy to non-oil driven, consumption oriented economy. The results of this have already started reflecting in different sectors and this will help the banks to regain their lending swagger within a short period of time when liquidity increases.

BAnKInG FEATURE

need not have an office space or even a residential visa under this license with this cost.

As of now, the authorities of UAQ Free Trade Zone & Dubai South Free Zone do not insist the shareholders holding employment visa to submit an NOC from their existing employers. All other free zones ask for it.

Are side agreements between the partners of LLC companies valid? I have an LLC company registered in Dubai and hold 49% of its shares.

The UAE national is not an active partner and has made no investment in the company. I pay a fixed amount as a sponsorship fee to him every year. Can we make a side agreement stating the same, so that all company assets belong to me? Can I do notary attestation of this agreement? Suresh Kumar, Sharjah

A: Any agreements between the partners of the company outside the MOA of the company commonly called as side agreements are valid; provided it doesn’t violate the provisions of the law, i.e. UAE Commercial Company Law.

As per the UAE Commercial Company Law (now New CCL), the MOA of the company should be in accordance with the provisions of the CCL. However, if you draft an agreement stating that the entire assets of the company belong to only one shareholder and the other doesn’t have any right on the assets and no value for his share, it is clearly against the provisions of the law and therefore, invalid. So you cannot make such an agreement and no question arises about a notary attestation of the same.

Notary attestation is possible only for those agreements which are within the provisions of the law. However, if you have any concern on the long term business relationship with your existing partner, you can look for another UAE national as the major shareholder or a company 100% owned by UAE national/s. Of course, he should be willing to sell his 51% shares of the company and sign in presence of a notary to mark his consent.

12

Q&A FINANCIAL OUTLOOK

A UK national, residing in the UK, wants to set up a company in Dubai. Can he do it without coming to the UAE? And if so, how can you

help us register a company in the Dubai Free Zone? David Christopher, Dubai

A: Dear David, there are many options to set up companies in the UAE without the physical presence of the shareholders. The physical presence of the shareholder is not mandatory in any of the UAE offshores to set up offshore companies. Moreover, Umm Al Quwain Free Trade Zone and Dubai South Free Zone allow investors to set up companies without them being physically present there. However, physical presence is mandatory for opening bank accounts in the UAE. But, if he can provide us the power of attorney (certified and attested by the UAE embassy or the consulate in UK) in someone’s name who is physically present here, we can set up the company both in main land as well as in all other free zones.

For setting up a company in Dubai, we will prepare the entire documentation such as Application for opening the company, Memorandum of Association, Articles of Association, Specimen Signature, Cards etc. and get it signed from the shareholders. Then they can send these back to us through courier for submitting to the free zone. In certain free zones we can complete the whole procedure within 24 working hours.

I am working as a Sales Manager in one of the private companies in Dubai. Can you please tell me in which Free Zone in the UAE, I can set up

a company at lowest cost and how much will it cost? Also, should I submit a no objection certificate (NOC) from my existing employer?Hussain Shaikh, Abu Dhabi

A: There are more than 50 free zones in all over the UAE as of now. The selection of a free zone to start a company depends upon many factors, mainly on the activity which you are planning to do under the license. However, to answer your question, in UAQ Free Trade Zone and RAK Free Trade Zone you can set up a company at a cost of around AED 15,000. The license can be a trade license or a service license; it depends on your requirements. You can also operate bank accounts under this license. You

yoUR qUEsTIons, ansWEREd Ragesh Mattummal,

Partner,Emirates Chartered Accountants Group

13

ECOnOMYFINANCIAL OUTLOOK

GCC EConoMIC UPdaTEs

HOW DO CrEDIT rATINg AgENCIES LOOK AT gCC COUNTrIES?

Credit agencies have restated their rating outlooks on the GCC countries. Moody's Investors Service has downgraded the Government of Saudi Arabia's long-term issuer ratings to A1 from Aa3 and assigned a stable outlook. It is the first ever downgrade since it commenced rating the country over 20 years back. The reason cited by Moody’s was a deepening concern over the country’s precarious fiscal position and ability to diversify away from oil revenues. The rating looks stable, which means there is no imminent danger of a further downgrade. Oman came down from A3 to Baa1 and is just three points above a junk rating - the reason being the negative impact that Oman’s sovereign credit profile faced due to an extended period of low crude oil prices. It's the second time that Oman has fallen after a

downgrade in February from A1 to A3. Bahrain’s rating fell further into junk territory to Ba2 with a negative outlook. The other three GCC countries, Qatar, Kuwait and the UAE, were put on a negative watch, meaning that there can be a cut in their rating in the next 18 months if the credit profile weakens further. Moody’s expects that the Abu Dhabi government’s vast reserves will help the UAE government face the challenges of a slow economy.

The Credit Sentiment Survey released by the UAE Central Bank shows that the demand for credit has rebounded, both for personal and business, in the first quarter of 2016. Though the corporates and small businesses showed an increased interest in credit, financial institutions were unwilling to extend their business loans. It is a typical phenomenon in economic cycles where banks become extremely cautious in lending during slumps and are a bit laid-back during upturns. On the retail side, individual

demands showed an increase, reflecting a positive sentiment after a dip in demand in Q4 of 2015.

Further, the World Bank revised its growth forecast for the UAE by 1.1% to 2% this year in the midst of low oil prices and budgetary spending cutbacks. Initially, the growth was estimated @ 3.4%. As per the World Bank, the Arabian Gulf nations'

The only month when prices were set higher was in August last year. The prices showed an upward trend again in April 2016.

14

ECOnOMY FINANCIAL OUTLOOK

efforts to raise cash to make up for the budgetary shortfalls would not block the gap completely. Though an attempt to expand revenue have also been implemented, including raising corporate and consumption taxes (including VAT), that would not be able to cover up the losses from the oil price immediately. In short, the governments will rely on domestic and international debt to fund the deficits.

OIL SECTOrFuel prices are poised for a sharp jump of over 10% in April as per the pricing details announced by the Ministry of Energy. UAE announced deregulation of prices in July 2015, and we have witnessed seven consecutive months of decline in prices, spurred by a fall in global crude oil prices. The only month, when prices were higher, was in August 2015, and April 2016 will be only the second month with high prices. The UAE’s economy minister is expecting the crude oil price to reach $60 this year with demand and production moving more in line. It is a very positive sign for the region. However, if the oil price remains lower than $75 per barrel, Bank of America Merrill Lynch (BAML) estimates that the peak global oil demand will rise only beyond 2050.

CL*1:48.52

2000000

1000000

Vol: 99210654.00

52.00

50.00

48.52

46.00

44.00

42.00

40.00

38.00

36.00

34.00

Mar 16 Apr May Jun Jul Aug

CLU16 - Crude Oil WTI (NYMEX)

BANKINg SECTOr

The fall in crude oil revenues, the primary source of liquidity in the GCC region, has led to a slight liquidity crunch. Banks across the region are collecting loans from the market to bolster funding. The UAE interbank EIBOR rates have tightened with the one-year rate increasing from 1.48% to 1.62% in Jan this year. This change may not impact borrowing costs for corporates as several banks in the UAE had included their internal cost of funding to the EIBOR rates during the financial crisis, most of which persist till now. The Loan to Deposit rates have gone over 100% for the system as a whole indicating a stress in the system itself.

National Bank of Abu Dhabi, the largest bank by assets in the UAE, has reported an 11% drop in net profits for its first quarter. The impact of the slowing economy has resulted in higher provisions for bad debts and a lower non-net interest income. The Abu Dhabi Commercial Bank reported an 18% drop in net profits in its first quarter resulted by higher provisions for bad loans and a compressed net interest rate margin. First Gulf Bank, the third largest bank in Abu Dhabi, also reported a 6% drop in its Q1 profits, primary reasons being lower fees and commission income with provisions just a little better. Big banks are constantly under pressure to hold on to profit levels. As a result, in a slowing environment, both retail and corporate clients, feel the pressure of higher credit costs; more so in the coming months when banks set aside larger amounts for bad debt provisions. Banks in the UAE have also cut jobs, though marginal, to limit costs.

Emirates NBD’s UAE Purchasing Managers Index (PMI) rebounded in March to 54.5, up from February’s 53.1. Overall, as a reflection of the slowdown in Q1, improvement in business conditions was the weakest at 53.4. There were positives in the report with increased employment in UAE’s non-oil private sector. Equities have posted a strong rebound over the last two months after posting lows in late January. The

rETAIL SECTOr

A.T. Kearney's 2016 Global Retail Development Index (GRDI) places the UAE and Saudi Arabia among the world's top 10 developing retail markets. The UAE, led by Dubai, is 7th on the list and has the highest sales per capita in the region making it an attractive and relatively low-risk market for the retailers. According to CBRE’s latest Global Shopping Centre Development Report, Abu Dhabi and Dubai are together in the top 17 of most active cities for shopping centre development. In the global rankings for shopping centres developed over the last year, Dubai and Muscat are in the top 30, with Muscat paving the way for the GCC region. The 2016 report confirms that the Middle East retail market is a very attractive destination for international brands. Dubai, with its high per capita income, significant growth potential and a high spending consumer base, is ranked second for international brand presence.

Dubai has always maintained its high position by attracting the rest of the world for tourism and shopping. The Emirate has retained its position as the second most important international shopping destination for the fifth consecutive year, closely behind London. This information was shared by real estate consultancy firm CBRE and reported by Arabian Business recently.

15

ECOnOMYFINANCIAL OUTLOOK

DFM Index is up 31% from its low of 2590.72 traded on Jan 21 as crude oil prices have recovered to around $40 a barrel level.

Not done with the sovereign rating, credit agency Moody’s projected an outlook of negative for five Abu Dhabi banks while retaining their ratings. NBAD remains at Aa3, ADCB, UNB and Al Hilal Bank at A1 and ADIB at A2. The turtle-pace of the GCC economy (due to lower crude oil prices) is getting to the banking sector. The banking industry, which is a representation of a nation's economic growth, is faltering from lower deposit accretion. On the other hand, with the economy slowing down, bad debts have started to increase putting pressure on bank balance sheets. Moody’s mentions the capacity and willingness of the Emirate of Abu Dhabi that has helped the banks in retaining their ratings.

As per the UAE Central Bank data, loans in the banking industry has increased by Dhs11.80 billion ($3.21 billion) with the loans to the private sector increasing by Dhs8.2 billion ($2.23 billion). In the first two months of the year, loans have increased by Dhs18.20 billion ($4.96 billion). Deposits in the system were stagnant and in the first two months it has fallen marginally by Dhs0.50 million. The impact of low crude oil prices and a consequent plunge in government spending, which is the key factor for deposit accretion, is pretty evident in the current system. The loan to deposit ratio in the system has increased further to 102.22%, and the tighter liquidity is feeding through higher rates in the system. Interbank EIBOR rates have steadily increased over the last year with the one year EIBOR rate increasing to 1.57% from 1.02% at the beginning of 2015.

Some small business owners that had fled the country fearing imprisonment due to unpaid debt have begun to return following a concerted effort by lenders. According to a top banker, “In some

cases [when a business defaults], there’s not much the banks can do, and in other cases the banks have obviously tried very hard to work together to address those cases, particularly when you can see that this is not a case of a company that was doing anything wrong – they’ve just got impacted by the overall market."

rEAL ESTATE

Saudi reSidential market Slowdown continueS:

Saudi Arabia's residential real estate remains slow in 2016, though transaction volumes and sale prices are declining at a slower rate compared to 2015. A reduction in government spending, due to the drop in oil prices, will most likely impact the financing of real estate projects. Many projects have been delayed and scaled back which will further aggravate the minimal availability of housing across the kingdom. As per Knight Frank’s Saudi Arabia Residential Market Report:

• Main Saudi Arabian cities have seen a shift in demand from sales to rentals

• Rental rates have increased in 2015 and are

16

ECOnOMY FINANCIAL OUTLOOK

expected to maintain their growth levels in 2016.

• A 2.5% white land tax and a revised mortgage law are expected to increase demand in sales.

• 2016 might see a re-prioritization of projects with an emphasis on affordable housing.

Dubai apartment prices continued to drop marginally during April, bringing the annual values down by 7.3%. ReidIn's Dubai Residential Property Sales Price Index decreased from 259.0 to 257.6, a difference of 1.4 points last month, which represents a decrease of 0.53%. The report showed that apartment sales prices fell 0.75% during the month and by 7.3% year-on-year while Villa sales prices registered an

increase in April of 0.40% but decreased 8.2% annually.

“However, in the UAE real estate market, there is a trend of shift from rented apartments or commercial buildings to owning a property. As per experts, the upward trends are witnessed in the month of June.”

Source: Colliers International /globalproperty.com HISTORY OF PROPERTY PRICE IN UAE.(http://www.globalpropertyguide.com/Middle-East/United-Arab-Emirates/Price-History)

In the UAE real estate market, there is a trend of

shift from rented apartments or commercial buildings to owning a property.

17

ECOnOMYFINANCIAL OUTLOOK

prOJECTS, INfrASTrUCTUrE & OTHEr DEVELOpmENTS

Qatar, uae among moSt inveStment-friendly StateS:

A key report from Arcadis, a leading global design and consultancy firm says that despite low oil prices are hindering investment into infrastructure Qatar, and the UAE are the second and third most attractive countries for infrastructure investment globally. Nations with secure business environments, stable financial sectors, and strong growth potentials remain the top most attractive markets for infrastructure investors. The top 10 countries of 2016 for long-term infrastructure investment are: Singapore, Qatar, UAE, Canada, Malaysia, Norway, Sweden, US, UK and The Netherlands.

Dubai’s diversification into tourism and aviation through its well-connected Dubai International Airport continues to provide results. In February, passenger traffic increased to 6.38 million (an increase of 6.9% annually). For the first two months of 2016, the total passenger traffic was at 13.7 million which is up 6.5% for the same period in 2015. The benefits of this passenger traffic accrue to the tourism and retail sector, which are holding up in spite of the broad slowdown across the region due to lower crude oil prices.

new SolutionS reQuired to fund gcc capital projectS:

Lower oil prices will limit the amount of funding available to the GCC governments to back capital projects, forcing them to make tough choices such as cuts in public spending and an introduction of structural reforms and developments. “Spending in the region will need to be better prioritized in order to ensure it meets social and economic development. Governments will have to seek for

Quarterly House Price Change (%)

Overall Apartment Villa Townhouse

Source: Collier International

50403020100-10-20'07 '08

the private sector involvement, innovate and find alternative funding sources to fund their project requirements,” explained Cynthia Corby, Audit partner and the Middle East Infrastructure and Capital Projects leader at Deloitte, a leading provider of audit, consulting, financial advisory, risk management, tax and related services. She was speaking about Deloitte Middle East’s newly released annual publication: “GCC Powers of Construction 2016: The funding equation." The report acts as a comprehensive review of the construction industry in particular for the sector’s leaders and shareholders. It is based on data collected from surveys and supported by interviews with some of the most prominent leaders from the construction industry as well as articles and interviews examining key industry trends.

$2 trillion projectS in the pipeline in gcc:

The pipeline of projects planned in the Gulf Cooperation Council (GCC) states amounts to $2 trillion, as of May 2016. It was revealed at a summit of construction sector leaders in Dubai, UAE. Leading professional services firm Deloitte informed that Saudi Arabia leads the region in terms of the value of projects in the pre-execution stage, with 38.91% of the total value, followed by the UAE with 34.84%. Qatar is next with 8.57% and Kuwait with 8.22%. Oman follows with 6.48% with Bahrain having a 2.97% share of the market. Besides the oil price slump, the growth of the projects sector depends on several factors, like the speed of enacting legislation, restructuring, project plans prioritization, and the ability to secure funding, says Ed James, Director of content and analysis, Meed Projects. “But more importantly, governments’ commitment to maintain spending in the face of

18

ECOnOMY FINANCIAL OUTLOOK

falling revenues to keep the economy moving will be a key factor in driving the industry forward through the challenging times,” he said. Experts predict that there still will be huge project investments between now and the end of this decade. The ever-growing economies across the Gulf region require improved infrastructure for cities to function and expand as planned, but there's also the need to explore innovative financing models to fulfill the funding gaps that may arise due to deficits in the government budget.

Gulf governments expected to raise $390bn in funding by 2020: Gulf governments are expected to raise between $255bn to $390bn by 2020 by selling both local and international debt as low oil price continues to put pressure on public finances. The GCC countries are expected to post a total fiscal deficit of $318 billion between 2015 and 2016, according to the GCC Sovereign Debt 2016 Report. Despite spending cuts announced across the GCC, Qatar expects to post a deficit of $13 billion this year, its first budget deficit in 15 years; while Saudi Arabia reached a deficit of $99 billion in 2015, with an estimate of $88 billion for 2016. Qatar will seek to raise up to $5 billion from a planned bond sale as early as this month, its first since 2011, Bloomberg reported. Meanwhile, Abu Dhabi expects to post a wider budget deficit of $10.1 billion in 2016 and plans to minimize the gap mainly with international bond issues.

Saudi arabia forgeS ahead with $442bn conStruction projectS:

Saudi Arabia’s project market in 2016 boasts of $500 billion worth of schemes in the pre-execution phase covering the power and water, transport, hydrocarbons and construction sectors, said a report. Under the ambitious reform agenda being driven by Deputy Crown Prince Mohammed bin Salman, within its recently announced Vision 2030 framework, Saudi Arabia is seeking to drive the non-oil economy and stimulate private investment in state activities, reported Arab News, citing a study by Meed, a leading source of Middle East business

19

ECOnOMYFINANCIAL OUTLOOK

intelligence. A report, "Saudi Arabia Strategies 2016: Adapting to a new economic reality" provides precise information about the kingdom’s plans to execute these projects and also observes how its latest Vision 2030 strategy will change the business landscape of the country.

dubai launcheS international centre for 3d printing:

Dubai Holding has launched the International Center for 3D printing which aims to make Dubai an international destination for 3D printing by the year 2030. The project, situated at Dubai Industrial City, will create a suitable atmosphere and provide the best infrastructure to bring a network of design and technology suppliers as well as factories under a single roof. It will include laboratories and research centres for testing materials used in 3D printed products within an integrated environment dedicated for construction, medicine, and consumer products sectors. It will also involve the academic sector, which will add innovation and educational value to this initiative through research and development.

Saudi arabia 2030 viSion:

Saudi Arabia announced its blueprint for “Saudi Arabia 2030” which will give its economy a makeover and make it less dependent on crude oil. The kingdom plans to increase the share of non-oil exports in GDP with large scale privatization and create the world’s largest sovereign fund with assets of over $3 trillion. The move away from oil will involve amongst other initiatives; use of renewable energy, focus on industrial equipment and mining sector and creating high-quality tourist attractions. To quote the website quantumauditing.com, "There is also a plan to have a “green card” for overseas workers. Deputy Crown Prince Mohammed bin Salman addressed a press conference where he mentioned that to achieve this vision a price of $30 a barrel will be sufficient. The IPO of Aramco is part of this plan and less than 5% of its stake is expected to be sold to investors and this could be as early as next year. Currently, Apple has the

largest market cap globally at around $500 billion (was $580 before the poor results this week), in comparison Aramco which controls about 15% of global crude oil reserves is estimated to have a market cap of over $2 trillion. The world’s largest oil company Exxon Mobil has a market cap of about $365 billion. Aramco’s IPO when it happens in Q4 this year or sometime next year will take center stage in global financial markets and make it the world’s largest company."

With the fall in crude oil prices, Saudi Arabia gave some indication that they are ready to buckle down for the long run, with large changes in the anvil for the economy. Last week, Saudi Deputy Crown Prince’s announced the proposed $2 trillion Public Investment Fund (PIF) which will be the source of future revenues for the Saudi government. This week Saudi Capital Market Authority Chairman, Mohammed Al Jadaan stated that the number of listed companies will increase to 250 from about 170 now, and the market cap would grow to equal the size of Saudi GDP in seven years’ time. The market cap at about $385 billion is just under 60% of Saudi Arabia’s GDP. The first of these listings is expected to be Saudi oil giant Aramco which controls about 15% of all crude oil reserves globally. New listings will come from a combination of privately owned companies as well as divestment of stakes in Government owned entities. The interesting part in this was the intention to develop new products like derivatives trading in the equity & debt markets. This could be a path breaking event when implemented as today most GCC markets are “long only” markets & with no Index futures available for trading, it is quite expensive and impractical to short the market using instruments structured by private institutions. In a move to attract foreign investors the Capital Markets Authority is also working on rules and regulations to give easier access to foreign investors.

Saudi Arabia’s net foreign assets declined by 1.7% in February to $548 billion - lowest since May 2012. From an all-time high of $737 billion in August 2014 it is down to 21% or about $153 billion in a year and a half. At this rate, reserves could be precariously low in two years. The situation can only be reversed with higher oil prices or if the Saudi government cuts some of the huge subsidies in the economy. The Saudi Central Bank also operates as its Sovereign Wealth Fund and these assets are being liquidated to cover the large budget deficit, which in turn has been due to lower crude oil prices. In a move to boost revenue, every passenger leaving the UAE from any of Dubai’s airports will be charged Dhs35 ($9.52). With 85 million passengers expected to use the airport, this charge could garner about $400 million in 2016 with the move being effective from June 30.

20

nEWS FINANCIAL OUTLOOK

CrEDIT BUrEAU USErSDOUBLE IN 2015

The number of institutions using the services of Al Etihad Credit Bureau (AECB) doubled during 2015, with a significant increase in credit data enquiries

UaE FInanCE nEWs

also being noted.

“The number of subscribers with Al Etihad Credit Bureau doubled in 2015 to reach a total of 59, whilst the average monthly enquiries tripled in the fourth quarter of 2015 compared to the first quarter of of the same year,” said Marwan Ahmad Lutfi, CEO of Al Etihad Credit Bureau at its first annual subscriber forum held recently. Officials from the bureau as well as a number of representatives from the banking and financial services sector attended the forum.According to Manoj Chawla, chief risk officer at Emirates NBD, “Underwriting has become more informed, thereby substantially adding to efficiency and also managing risk and serving the customer. Al Etihad Credit Bureau has helped banks in better managing the risk-reward equation and can be seen as driving a responsible behaviour in the market that is beneficial overall for all participants. The bureau’s reports have become one of the key drivers in the retail underwriting process.”

21

nEWSFINANCIAL OUTLOOK

gCC INTrODUCTION Of VAT TO CrEATE 5,000 NEW TAx JOBS

Gulf Arab states’ introduction of value-added tax (VAT) in 2018 will create more than 5,000 new jobs for tax and accountancy executives, with some large consultancy firms already starting to increase their headcount, according to industry experts.

Finance ministers from the six Gulf Cooperation Council (GCC) countries formally agreed on June 16 at a meeting in Jeddah to introduce tax across the bloc from 2018. The full details of the process have not been announced and it is not yet clear whether all the countries will introduce VAT on January 2018.

The United Arab Emirates (UAE) and Qatar will be the first to adopt the new tax regime, but all six members of the GCC, which also includes Kuwait, Saudi Arabia, Oman and Bahrain, are expected to implement VAT by the end of 2018, according to a tax alert issued in February by consultancy firm EY.

In preparation for this, many of the ‘Big 4’ international accountancy firms – including PwC, Deloitte, EY and KPMG – have already started hiring in order to have enough staff in place to manage their clients’ tax obligations.

prIVATE WEALTH IN THE UAE pOISED TO rEACH $1Tr IN 2020

Private wealth in the UAE is projected to post a compound annual growth rate (CAGR) of 14.1 per cent to reach almost $1 trillion in 2020; over the next five years, private wealth held by ultra-high-net-worth households in the Emirates is also expected to increase by a staggering 20 per cent, according to a new report by The Boston Consulting Group (BCG).

In the UAE, the growth of private wealth was driven

primarily by cash and deposits. In fact, between 2014 and 2015, the amount of wealth held in cash and deposits increased by 16.7 per cent across the nation, compared with 0.7 per cent for bonds, and 3.8 per cent for equities according to BCG’s report, Global Wealth 2016: Navigating the New Client Landscape.

Based on BCG’s study, the UAE is set to show solid growth in the next five years, with the wealth breakdown anticipated to be 19.2 per cent in equities, 12.1 per cent in cash and deposits, and 4.8 per cent in bonds.

“Segmentation approaches based mainly on wealth level continue to be used by the majority of wealth managers, neglect what clients are truly willing to pay for,” said Markus Massi, Partner & Managing Director of BCG Middle East’s Financial Services practice. “Such approaches no longer allow wealth managers to capitalise on the full potential of the market.”

ABU DHABI gOVErNmENT TO mErgE mUBADALA AND IpIC

Abu Dhabi plans to merge state investment funds Mubadala Development Company and International Petroleum Investment Company. The combined fund would have assets worth around $135 billion, according to Reuters calculations based on both funds' latest financial statements.

"The merger of the two companies augments the investment advantages and economic revenue for Abu Dhabi, and creates a body capable of achieving the highest level of integration and growth in

22

FINANCIAL OUTLOOK

multiple sectors, including energy, technology and space industry," the agency said.

NBAD-fgB mErgEr TO LEAD TO SUBSTANTIAL COST SAVINgS

The merger of Abu Dhabi’s NBAD and FGB banks could lead to cost savings of 28 percent, according to a senior banker.

Sanjay Uppal, who helped oversee Emirates NBD’s merger in 2007, said: “When we look at domestic mergers, we typically look at revenue synergies of somewhere in the region of 6 to 12 percent and cost synergies of somewhere in the region of 15-25 to 28 percent.”

Uppal, who was CFO when Emirates Bank and National Bank of Dubai merged to form Emirates NBD in 2007, told Bloomberg TV that NBAD and FGB “should be targeting synergies somewhere close to these benchmarks.”

National Bank of Abu Dhabi and First Gulf Bank held preliminary talks on a merger that would create the largest bank by assets in the Middle East and Africa.

ABU DHABI fINANCIAL grOUp TO ACqUIrE SHUAA CApITAL STAKE

Alternative investment firm Abu Dhabi Financial Group has reached an agreement to acquire Dubai Banking Group’s 48.36 percent stake in Shuaa Capital.

In a bourse statement, Shuaa confirmed the deal saying it was subject to regulatory approval. No value for the transaction was given.

Reuters reported at the end of last month that ADFG, Al Mal Capital and Arqaam Capital were among the bidders for the stake.

It said the stake was worth around $91m based on the company’s closing price on May 31.

The stake sale comes as the Dubai Group subsidiary looks to sell assets to help fun repayments on a $10bn debt restructuring.

DUBAI BANK EmIrATES NBD IN DHS 500m DIgITAL pUSH

Dubai’s biggest bank Emirates NBD announced that it will invest Dhs 500m over the next three years into improving its digital services.

The bank’s investment will focus on five areas including: end to end process transformation; faster and more responsive customer interface; omnichannel experience, fortification of cyber security and anti-fraud capabilities; and enhancement of data management and analytics.Emirates NBD also revealed plans to launch the United Arab Emirates’ first so-called ‘digital bank’ targeted at millennials.

The initiative will use digitisation and social inputs to offer customers self-service money management with useful tools and applications, a statement said.Emirates NBD group chief executive officer Shayne Nelson said: “We are making a commitment to the future with our digital transformation plan.

“Our focus on technology innovation and adoption to create digital-only products is creating a new paradigm in the way people bank in the UAE.”

Currently, the bank offers digital banking initiatives such as e-payment capabilities for 25 service providers including telecom, utilities, transportation, card schemes and education providers.

nEWS

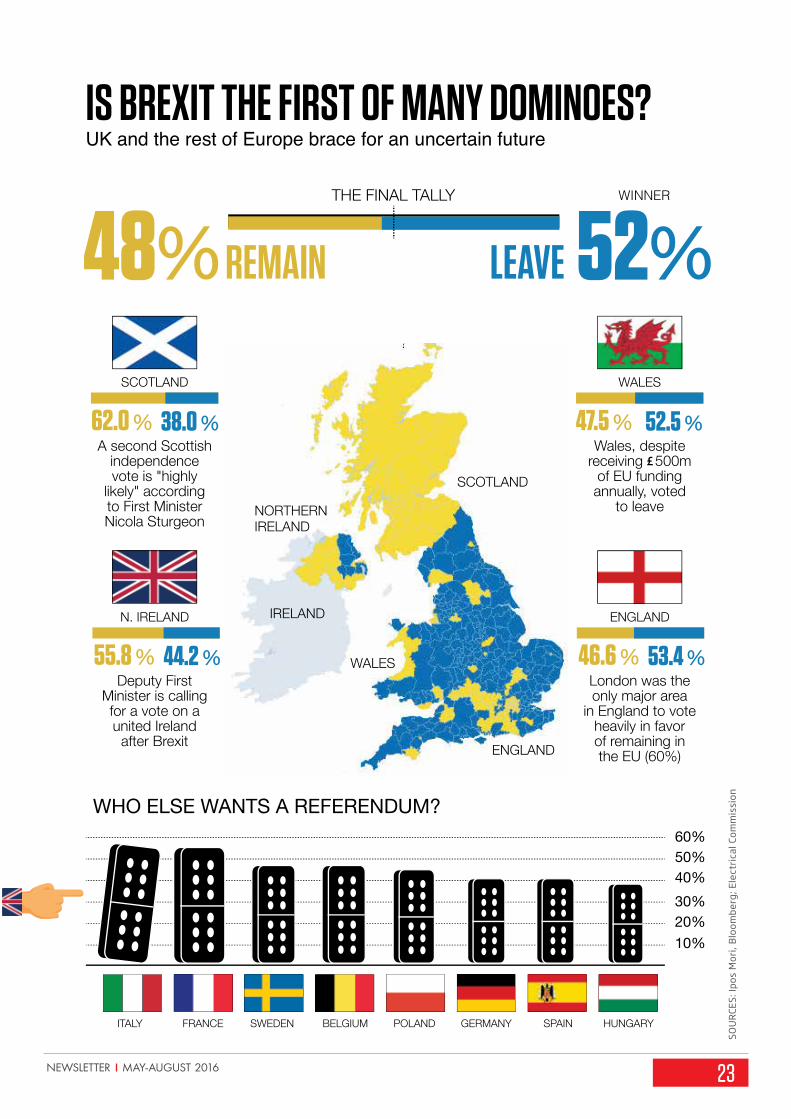

IS BREXIT THE FIRST OF MANY DOMINOES?UK and the rest of Europe brace for an uncertain future

THE FINAL TALLY

WHO ELSE WANTS A REFERENDUM?

WINNER

48% 52%REMAIN LEAVE

NORTHERNIRELAND

SCOTLAND

ENGLAND

IRELAND

WALES

47.5 % 52.5 %

46.6 % 53.4 %

WALES

Wales, despitereceiving 500m

of EU fundingannually, voted

to leave

ENGLAND

ITALY FRANCE SWEDEN BELGIUM POLAND GERMANY SPAIN HUNGARY

London was theonly major area

in England to voteheavily in favorof remaining inthe EU (60%)

60%50%40%30%20%10%

62.0 % 38.0 %

55.8 % 44.2 %

SCOTLAND

A second Scottishindependencevote is "highly

likely" accordingto First MinisterNicola Sturgeon

N. IRELAND

Deputy FirstMinister is callingfor a vote on aunited Ireland

after Brexit

23

SOU

RCE

S: Ip

os M

ori,

Blo

ombe

rg; E

lect

rica

l Com

mis

sion

Locations: Dubai, Sharjah, Ajman, RAK, Abu Dhabi, London

Corporate Office: Suite 503, Wasl Business Central, Port Saeed, P.O. Box: 122957, Dubai, UAE.Tel: +971 4 2500290 Fax: +971 4 2500291 Email: [email protected] www.emiratesca.com

Disclaimer: The views and opinions expressed in the Financial Outlook Newsletter are those of authors onlyand not necessarily the opinion of Emirates Chartered Accountants Group.

For Private Circulation only.

The Group Entities: United Auditing, IEC Emirates Chartered Accountants Co., Emirates Chartered Accountants, Emirates Accounts Services UK.