economic and institutional factors affecting business ... et al... · economic and institutional...

TRANSCRIPT

1

Economic and Institutional Factors Affecting Business Environmental Management

David Ervin, JunJie Wu, Madhu Khanna, Cody Jones, Teresa Wirkkala and Patricia Koss

Professor Ervin, Dr. Jones and Professor Koss are with the Departments of Economics and Environmental Science and Management, P.O. Box 751, Portland State University, Portland, OR 97207-0751 Professor Wu and Ms. Wirkkala (formerly Hall) are with the Department of Agricultural and Resource Economics, 200 Ballard Extension Hall, Oregon State University, Corvallis, OR 97331-3601 Professor Khanna is with the Department of Agricultural and Consumer Economics, University of Illinois, 326 Mumford Hall, MC-710, 1301 West Gregory Drive, Urbana, IL 61801-3605

Correspondence Address:

David Ervin Department of Economics

241 M Cramer Hall Portland State University Portland, OR 97207-0751

Office: 503-725-3935 Fax: 503-725-3945

Email: [email protected]

2

Economic and Institutional Factors Affecting Business Environmental Management

Abstract. Two different conceptual frameworks, profit maximization and institutional theory,

have been used to analyze why firms voluntarily undertake environmental management. The

neoclassical economic approach centers on rationalizing environmental management decisions

based on their potential to decrease cost, increase revenue and improve the manager’s utility.

Institutional theory takes a broader view and emphasizes how external pressures from market

and non-market constituents shape the firm’s environmental efforts. Studies of business

environmental management often adopt one or the other framework. We view the two

approaches as complementary, since institutional pressures can influence upper management’s

view of what is in the firm’s economic interest and help explain environmental efforts that go

beyond compliance. Therefore we postulate a model that includes both types of motivations to

analyze environmental management actions by small, medium and large facilities in Oregon’s

major manufacturing and service sectors. Survey data are used to estimate the magnitude and

significance of economic and institutional factors in a facility’s choice of environmental practice

routines and pollution-prevention operational activities. Our findings support the hypothesized

model built using both conceptual frameworks. Specifically, the results show significant

influences by firm factors, including cost barriers, upper management attitudes toward

environmental stewardship, and parent company ownership, and by external institutional forces

including regulatory, investor and competitor pressures. The robust coefficient on the proxy for

upper management’s environmental attitudes suggests that explanatory models should go beyond

profit maximization theory to include this important behavioral influence. Taken as a whole, the

findings imply that a multifaceted policy strategy extending beyond public regulation and

incentives can advance environmental management by facilities in Oregon, and likely elsewhere.

Key words: Environmental practices; pollution-prevention activities; management

environmental attitudes; economic factors; institutional theory

1

I. Introduction

Expanding markets for ‘green’ products and stocks, tighter pollution standards, and the

growing likelihood of greenhouse gas regulation have elevated environmental management to a

strategic level for many businesses. It has been suggested that such firms increasingly view pro-

active environmental management as an opportunity not simply to minimize the expense of

complying with regulations, but to control risks, lower operating costs, respond to stakeholders,

enhance revenues, and improve their competitive advantage (Esty and Winston, 2006). Insights

about the significant factors influencing these efforts can enhance the cost-effectiveness of the

next generation of public and private environmental policies.

Observing this shift in strategy for many firms, scholars from multiple disciplines have

contributed to an extensive literature on voluntary environmental management since the early

1990s (Alberini and Segerson, 2002; deLeone and Rivera 2009; Khanna, 2001; Lyon and

Maxwell, 2004; Reinhardt, 2005). Some early work advanced a conceptual framework that

incorporated the constraints imposed by the natural environment into strategic business

management, termed a natural resource-based view of the firm (e.g., Hart, 1995). This

framework focused attention on strategies for key firm resources, e.g., R&D capacity, that

contribute to sustained comparative advantage. In a second body of work, management scholars

have applied institutional and neo-institutional theory to understand business’ environmental

management actions, such as adopting environmental management systems (EMS) (e.g., Darnall

et al, 2008; Delmas and Toeffel, 2004, 2008; Rivera, deLeon and Koerber, 2009). Delmas and

Toeffel (2004;210) note:

“However, the institutional perspective does not address the fundamental issue of

business strategy: why do organizations subject to the same level of institutional pressure

pursue different strategies?”

2

The authors theorize the differing responses reflect divergences in ‘objective’ and ‘perceived’

pressures, the latter being influenced by the management’s perspectives on the impact of various

institutional pressures on a firm’s financial and environmental performance which in turn depend

on the firm’s organizational structure other characteristics.

Economists have mostly sought to explain business environmental decisions using a

profit maximization framework that emphasizes the influences of external market and regulatory

forces and internal firm characteristics on expected costs and returns (Konar and Cohen, 1997,

2001; Khanna and Brouhle, 2009). This approach considers internal firm decisions and variables

under the control of managers to affect such actions, e.g., production process innovations as well

as external factors that affect profit, e.g., certification and marketing expense to differentiate

products, that may be influenced by the external pressures defined by institutional theory (Wu,

2009). A few economists have advanced a utility maximization approach in which managers

holding strong environmental values receive the equivalent of a monetary incentive from

increased environmental action by their firms (e.g., Baron, 2001; Nakamura, et al., 2001).

Several studies have empirically analyzed the effects of various institutional pressures

from market actors, government and non-governmental organizations, the effects of leadership

values and managerial attitudes and the influence of various departments within the organization

(see review in Delmas and Toeffel, 2004; Delmas and Toeffel, 2008; Cordano and Frieze, 2000).

Other studies have used observed facility characteristics and various proxies for economic

incentives to explain firm participation in voluntary environmental programs (VEPs), such as

ISO 14001, WasteWise, and the National Environmental Performance Track (Arora and Cason,

1995; DeCanio and Watkins, 1998; Innes and Sam, 2008; Khanna and Damon, 1999, Nishitani,

2009; Videras and Alberini, 2000); and the adoption of selected environmental management

practices (EMPs) (Anton, et al., 2004; Dasgupta, at al., 2000; Henriques and Sadorsky, 1996;

3

Johnstone and Labone, 2009; Khanna and Anton, 2002). Nakamura, et al., 2001) applied a

utility maximization approach to examine the effect of managerial attitudes towards

environmental stewardship on voluntary environmental action by their firms. In general, these

studies show that a relatively small set of factors appear to influence such decisions, including

regulatory intensity, firm size and economic performance while the effects of public recognition

are mixed (Alberini and Segerson, 2002; Cohen, 1997; Johnstone and Labone, 2009; Khanna,

2001, Khanna and Brouhle, 2009; Harrington et al., 2008).

As pointed out by Delmas and Toeffel (2004), a comprehensive framework that combines

both objective pressures and perceived pressures and allows for the evaluation of their

differential influences on environmental management actions is lacking. Available data often

limit analysis of the full spectrum of motivations for business environmental initiatives,

including the role of management’s values. Further, many of the empirical tests cover only

publicly-traded and large manufacturing firms, leaving out private firms, small- and medium-

sized enterprises (SMEs), and the service sector. Therefore, our understanding of drivers and

their effects on firm decisions remains partial and limits insights into effective policy approaches

for these industry segments. Analyses of business environmental management decisions should

ideally include all relevant motivations and barriers, and be tested across the full range of

facilities to best inform public and private policies.

The research reported here takes a first step in combining the economic and institutional

frameworks as suggested by Delmas and Toeffel (2004). With this more comprehensive model,

we enlarge the domain of empirical analysis on the internal and external factors that affect

business environmental actions. We use survey data from facilities in six major Oregon

industries to shed new light on what is driving green business behavior in a state with a strong

environmental tradition. SMEs and large facilities in manufacturing and service sectors populate

4

the database, which more closely mirrors national patterns of industrial activity than many other

samples. By focusing on one state, the analysis holds constant some policy and unobservable

factors that can confound analyses of environmental management drivers and impacts across

states. We develop a utility maximization model that also includes perceived external

institutional pressures to analyze facilities’ reported environmental management practices (EMP)

and pollution-prevention activities (P2). The two-equation model is tested over alternative

specifications of facility and institutional explanatory variables to ascertain robustness.

An early analysis of the survey data examined differences in the types of facilities that

are likely to participate in voluntary environmental programs (VEPs) and those likely to adopt

EMPs using Poisson and ZIP models with counts of EMPs and VEPs as the dependent variables

(Khanna et al, 2007). That paper examined the effect of observed facility characteristics on the

number of VEPs in which a firm participated and the number of EMPs it adopted. The main

findings of that study were that facilities that faced environmental regulations for a larger

number of environmental impacts and those that considered the environment to be a significant

issue for the facility were more likely to engage in VEPs and EMPs. It also found that larger

facilities are more likely to participate in VEPs while innovative facilities, as measured by R&D

capacity, are more likely to adopt more EMPs.

This analysis expands upon the earlier study in several respects. First, our EMP measure

expands beyond the count of practices to capture the reported level of their use based on a five-

point Likert scale. Second, we add another dimension of environmental management, the

amount of pollution-prevention (P2) activity, an indicator of the facility’s actions to avoid

pollution and other environmental harms. Including the P2 measures allows us to capture a fuller

spectrum of environmental initiatives. Third, perhaps more importantly, our unique, primary data

allow us to introduce an expanded suite of economic and institutional explanatory variables,

5

including several perceived market and non-market pressures, that have been hypothesized by

the utility maximization and the institutional theories to play important roles, but have been

rarely tested in the previous studies. These additions allow us to probe the roles of institutional

forces alongside management values and observed facility characteristics in shaping the

organization’s environmental management efforts. In particular, building on the findings in

Khanna et al. (2007) our analysis sheds light on some of the perceived institutional pressures that

could be correlated with the facility viewing the environment to be a significant issue for them

and that increase the likelihood of adoption of EMPs and P2 activities. Two other studies that use

this survey data focus on examining firms’ motivations for environmental violations and

overcompliance, without examining firms’ adoption of environmental management practices or

policies (Wu and Wirkkala, 2009; Wu, 2009).

The remainder of this article is organized as follows. In the next section, we develop a

simple conceptual model that draws on economics and management concepts to guide our

empirical analysis. Section III describes the sample and the survey, and summarizes the data

collected. Section IV reports the variables created and hypotheses, and section V presents

econometric results. The final section draws conclusions and policy implications for advancing

business environmental management efforts.

II. Conceptual Framework

We develop a framework that draws upon the existing literature and views a facility

manager’s utility as depending on the facility’s profits, its environmental performance and

managerial attitudes that influence the impact of the first two factors on his/her utility. This

approach is based on the view posited by institutional theory that external social and cultural

pressures exerted on organizations in a common field create and diffuse a common set of values,

6

norms and rules that influence their practices and structures beyond mere profit maximization

motives (Scott, 1992). Institutional pressures on firms’ environmental decisions could be

imposed by shareholders, suppliers, competitors, industry (trade) associations, government

regulators, consumers, community groups, and environmental activists (Delmas and Toeffel,

2004). These institutional pressures can change the way firms view the cost and benefits of

environmental management by transforming the marketplace environment in which firms operate

and facilitate the emergence of external benefits from such actions (Auld et al. 2008).1 However,

we expect that the same set of institutional pressures will have a differential impact on a

facility’s environmental management actions due to differences in the way these pressures are

perceived by the facility management and the way they affect the facility’s profitability (Wu,

2009). For example, investor preferences for stronger environmental programs could reduce the

firm’s cost of raising external capital. Facilities differ in these impacts due to heterogeneity in

their characteristics and the attitudes of the management. Managers’ views are shaped by

prevailing social and cultural environments and their desire to ensure legitimacy of their firm.

A facility motivated solely by a desire to maximize profits would only undertake a

voluntary environmental activity, either as an internal initiative or in response to external

institutional pressures, if it results in higher profits. Upper managers who hold altruistic

preferences obtain additional value from the facility preventing environmental harm. They can

be expected to lead the organization to voluntarily improve its environmental performance even

if the actions are not profit maximizing (Marshall, Cordano and Silverman, 2005).

1While institutional theory predicts fairly homogeneous responses to market and non-market pressures by organizations in the same field, observations in the real world suggest heterogeneous firm environmental management actions occur in any field. New institutional theory attributes such heterogeneity to variations in firm structure and culture. For example, various functional departments, such as legal affairs or marketing, receive pressures from different sources and have varying capacity to translate them into environmental actions in different firms (Delmas and Toeffel, 2008).

7

Voluntary environmentally-friendly actions may serve to increase a firm’s profitability in

response to internal initiatives and external pressures. Such actions can lead to increased demand

and higher prices for the firm’s output through product differentiation. Such actions can also lead

to increased efficiency of the production system, reduced waste in the use of inputs, and lower

operating costs. As noted above, such efforts may also lower costs of financial capital. A facility

may also benefit by improving its corporate reputation, gaining consumer and community

goodwill, lowering expenses for obtaining permits for expanding their facilities and preventing

boycotts by environmental interest groups. Voluntary environmental actions may also lower

transaction costs in dealing with regulatory authorities and preempt the threat of anticipated

regulations, thereby limiting future financial liabilities. Of course, such actions can impose added

expense in the form of employee training, change in production and pollution control methods.

Improvements in environmental performance of a facility may be achieved by adopting

EMPs and/or by taking P2 actions. While the former involves changes in routine operating

policies and procedures, such as setting environmental goals and policies, training employees

and undertaking environmental auditing and reporting, the latter includes changes in the methods

of pollution control. The extent to which the above motivations drive facilities to adopt EMPs or

P2 can be expected to differ depending on the effectiveness of EMP and P2 in achieving the

particular objectives driving their adoption and in being observable and credible signals of the

facility’s environmental responsibilities to consumers, other stakeholders and the government.

We represent these motivations using the following model in which we hypothesize that

the facility manager’s utility is a function of profit (π) and environmental performance (EP):

U(π, EP; α), where α is a parameter denoting the manager’s attitudes and values toward

environmental management. Environmental performance (EP) in a facility depends on its

8

environmental practices (EMP), pollution-prevention activities (P2), and a vector of exogenous

facility characteristics (X), such as multinational operations and R&D capacity and α:

EP = E(EMP, P2, X; α). (1)

Profit (π) depends on the product price (p), the quantity of sales (Q), and the cost of

production (C): π = pQ -C. Thus, to understand how a manager makes her environmental

decisions, we must also specify how EMP and P2 actions affect the price (p), the quantity of

sales (Q), and the cost of production (C). We assume that, given the external institutional

pressures for environmental management such as consumers’ willingness to pay for

environmentally-friendly products, investor and other stakeholder concerns, and regulatory

pressures, both the price and sales of a facility, as well as its cost of production, are potentially

affected by its environmental efforts and performance because both of them may enhance the

firm’s public image and resource efficiency. Adoption of EMPs and P2 may reduce costs of

production by increasing efficiency of resource use or they may increase costs of production

because they involve more employee training and effort and new equipment. Formally,

p = p(EMP, P2, EP│ I, B, X), (2)

Q = Q(EMP, P2, EP│ I, B, X), (3)

C = C(EMP, P2, EP│ I, B, X), (4)

where I is a vector of perceived external institutional pressures, including those by consumers,

investors, competitors, environmental interest groups, and regulators; and B is a vector of

internal barriers (e.g., upfront cost, downtime risks) to adopting EMP and carrying out P2

actions.

The manager’s objective is to maximize her utility by choosing EMP and P2:

Max U(π, EP; α), (5)

s.t. expressions (1) - (4).

9

The first-order condition defines the facility’s optimal choice of environmental management

policy and pollution-prevention actions through these two reduced form equations:

EMP* = f(I, B, X, α) (6)

P2* = g(I, B, X, α) (7)

Based on the conceptual framework using utility maximization and institutional theories, we set

forth three hypotheses about factors that motivate the adoption of EMPs and P2 by facilities.

Hypothesis I: The stronger the threat of regulatory pressures faced by a facility, the greater the

extent of adoption of EMPs and P2.

Several theoretical studies suggest that the potential to preempt environmental regulations

and shape future regulations provides incentives for adopting voluntary environmental

initiatives. Segerson and Miceli (1998) show that an anticipated regulatory threat could lead

firms to undertake voluntary abatement in order to preempt regulation that would otherwise

involve higher abatement costs and transactions. In a test of this proposition, Delmas and Toeffel

(2008) find that facilities more receptive to nonmarket pressures, including regulatory factors,

were significantly more likely to participate in voluntary government environmental programs.

Lutz et al. (2000) show that firms have an incentive to voluntarily produce goods with improved

environmental attributes if it can be used to influence the minimum quality standards likely to be

set by the government.

Hypothesis II: The stronger the pressures to be environmentally responsible from consumers,

interest groups, investors and competitors, the greater the extent of adoption of EMPs and P2.

When consumers prefer products produced using environmentally-friendly practices or

possess certain environmental attributes, firms may be able to charge premium prices or increase

market shares at existing prices by differentiating their products through adoption of EMPs

10

and/or P2s. Arora and Gangopadhyay (1995) examine the conditions under which firms produce

high-quality environmental products to differentiate themselves from other firms and gain

market share in the presence of consumer willingness to pay premiums for environmentally-

friendly products and firm desire to relax price competition. Henriques and Sadorsky (1996) find

that customer pressure was the second most cited source of pressure to adopt an environmental

management plan by Canadian firms, and Florida and Davison (2001) found that firms that were

more actively engaged with community stakeholders were more likely to institute pollution

prevention programs.

Firms may also have incentives to undertake voluntary adoption to preempt consumer

groups from lobbying for more stringent abatement regulations, particularly when it is not very

costly for consumer groups to organize themselves and influence the political process (Maxwell

et al., 2000). Baron (2001) shows the conditions under which an activist group can create

incentives for a facility to be socially responsible and that these incentives increase if the facility

faces greater competitive pressures or if the management has stronger altruistic preferences.

Delmas and Toeffel (2004) hypothesize that market-related groups, including consumers,

suppliers, investors and others exert pressure through corporate marketing departments. Delmas

and Toeffel (2008) found that increased receptivity to environmental interest group pressure by

the legal affairs department had a significant positive effect on a facility’s participation in

voluntary government environmental programs.

In addition to consumers and interest groups, investors can also influence a facility’s

decisions about environmental management. The capital markets pressure firms to increase their

value. Firms that undertake environmental management to increase their profits can benefit by

facing a lower cost of raising capital. Kristrom and Lundgren (2003) show that a firm’s value is

linked to its stock of “green goodwill” and that a firm can increase that stock by investing in

11

environmentally-friendly projects. However, capital markets can also pressure firms to avoid

environmental management that is driven by altruistic motives and is unprofitable. Thus the

impact of investor pressures on incentives for adopting EMPs and P2 is ambiguous. Delmas and

Toeffel (2008) find that pressures from consumers, investors and suppliers are stronger if they

have strong preferences for improved environmental management and the facility’s marketing

department has influence over facility decisions.

Several scholars theorize that less competitive or more concentrated industries are more

likely to undertake voluntary environmental efforts because their profit margins are larger (Brau

and Cararro 1999) and there are weaker incentives for free riding (Maxwell, Lyon and Hackett

2000). This may also be the case because firms in these industries face lower costs of inter-firm

coordination (Glachant 1999) and have greater market power and ability to differentiate products

(Arora and Gangopadhyay 1995; Garvie 1997). An industry dominated by a few big firms is also

more effective in inducing its suppliers to adopt environmental management practices as

compared to an industry that is fragmented; this could be a major reason why automotive

suppliers in the US adopted similar environmental management practices (Delmas and Toeffel,

2004).

Hypothesis III: The stronger the moral motivations of the managers toward the environment, the

greater the extent of adoption of EMPs and P2.

Several case studies of firms suggest that managers’ attitudes and commitment play an

important role in filtering, interpreting and prioritizing the signals they receive from the external

environment and in facilitating or impeding proactive environmental management (Nash, 2000).

Baron (2001) develops a formal model to show that altruistic managerial preferences can lead a

facility to go further in adopting socially-responsible practices than is profit maximizing.

Cordano and Frieze (2000) find that managerial attitudes influenced preferences for source

12

reduction activities, suggesting that when a manager’s attitudes toward a behavior become more

favorable, the intention and effort exerted to perform the behavior are likely to increase. Neo-

institutional scholars argue that business firms are not exclusively bound to profit maximization

and also seek social legitimacy for their long term survival (Rivera, deLeon and Koerber 2009).

This motive could translate into positive attitudes by managers toward environmental

stewardship that mirror public opinion. As noted above, Nakumura, Takahashi, and Vertinsky

(2001) found empirical support for the influence of managers’ attitudes toward environmental

stewardship on related management actions by a sample of Japanese firms.

Next, we discuss the survey design and the data that are used to estimate equations (6)

and (7) and test the above hypotheses.

III. Data

The sample comprised all facilities in Oregon employing at least 10 employees2 (R3.7),

operating primarily in one of the following sectors3: Construction of Buildings (Construction;

NAICS 236), Food Manufacturing (Food; NAICS 311), Wood Product Manufacturing (Wood;

NAICS 321), Computer and Electronic Product Manufacturing (Electronics; NAICS 334), Truck

Transportation (Transport; NAICS 484), and Accommodation (Accommodation; NAICS 721).

The chosen sectors accounted for nearly 33% of employment, 30% of all facilities, and 30% of

corporate tax revenues in Oregon industry in 2004 (DOR, 2004; Graham Slater, OED

2 The lower limit was arbitrarily set at 10 employees on the reasoning that facilities with fewer than 10 workers likely would not have enough resources to implement a formal environmental program. Setting it at a higher level, such as 50 workers, would have eliminated the majority of the sample facilities. 3 Facility name, location, number of employees and primary industry classification were obtained from the Oregon Employment Department (OED), which is authorized by Oregon Revised Statutes (ORS) 657.665(3) to release information to state agencies for the purposes of socioeconomic analysis. No individual persons are identified, and information is provided subject to strict confidentiality rules (State of Oregon, 2005a, 2005b, 2005c; Graham Slater, personal communication, 2005). The North American Industry Classification System (NAICS) replaces the earlier Standard Industry Classification (SIC) system. NAICS codes contain up to six digits; however, sectors were defined at the 3-digit level in this study.

13

unpublished data 2005; USCB, 2003). These six sectors constitute some of Oregon’s major

industries and include both manufacturing and service sectors. Facilities were selected as the

appropriate business unit to survey because studies suggest that environmental management can

vary substantially across facilities within a company; environmental permits are typically issued

at the facility level, and; emission data are typically reported at the facility level (DEQ, 2006;

Rivera and De Leon, 2004; Rivera, De Leon and Koerber, 2006).

To ensure a high response rate, each facility in the sample was contacted by telephone to

verify its mailing address and identify the individual who was most knowledgeable about

environmental management. These contacts resulted in a list of 1,964 eligible facilities after

eliminating facilities that had discontinued business. A description of the sampling and survey

procedures is given in Jones (2007).

Appendix A describes the development of the survey instrument and presents the version

sent to wood products, electronics, and food manufacturing facilities. The sections of the survey

include: (1) environmental management motivations (e.g., investor, regulatory, and

competitiveness pressures) and barriers/costs; (2) environmental management practices (EMPs,

e.g., environmental goals, documented environmental policy, regular environmental audits); (3)

P2 activities (e.g., emphasizing pollution prevention, reducing spills, and choosing raw materials

to reduce impacts); (4) environmental performance (e.g., amounts and changes in waste water

discharged, solid waste landfilled, hazardous/toxic wastes generated); and (5) general

information (e.g., annual facility revenue and publicly traded versus privately owned status).

The survey structure was the same for all sectors; only the performance measures and examples

of voluntary environmental programs were tailored to the individual sectors. Ordered response

and Likert scales were designed in accordance with accepted empirical methods (Fowler, 1995;

Smith and Albaum, 2005).

14

The mail survey was conducted from October 2005 through March 2006. A series of

reminders and additional mailings were sent to improve the response rate. A randomly-selected

subgroup of the mailings was sent Priority Mail with a $5 incentive to increase responses. An

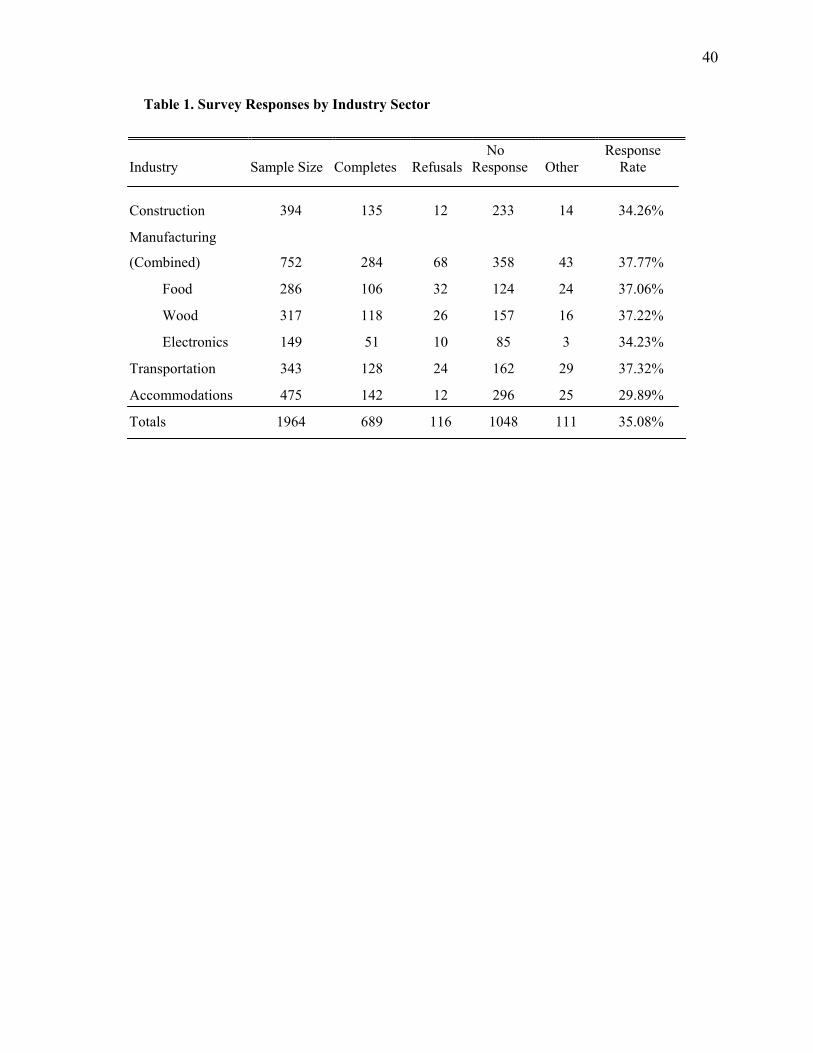

overall response rate of just over 35 percent and 689 responses allows reliable multivariate

analysis and testing (see Table 1).

Self-selection bias is a concern in environmental management surveys because facilities

with stronger environmental programs may be more inclined to respond than those with weak

records. To test for potential bias, we conducted a telephone survey of 900 non-respondents,

selected at random from among all non-respondents. We received responses from 370 facilities

that did not complete the mail survey, for a response rate of just over 41 percent. The survey

included seven questions regarding the firm’s characteristics, environmental regulatory actions,

and reasons for not responding. An analysis of the responses indicated that the non-respondents

did not differ significantly from responding facilities with regard to facility size in terms of

employment levels or environmental regulatory actions: approximately 2 percent of respondents

and non-respondents alike reported receiving an infraction such as a notice of violation or

penalty. The most frequently cited reason for not responding was that the survey was too long

and required too much time, a comment also received by several respondents. In addition, the

non-respondents did not differ significantly from respondents with respect to geographic location

or facility size based on the number of employees (Jones, 2007).4 These findings together

provide a reasonable indication that our results are not significantly affected by substantial non-

response bias. 4 Surveys were sent to facilities in 34 Oregon counties, and responses were received from 31 counties. Among responding counties, the proportions of the state’s population and the proportions of responding facilities varied by no more than 1.1%, and reflected the state’s population distribution. A total of 10 surveys (0.5% or the sample) were sent to the counties that did not respond. These counties comprise 0.5% of Oregon’s population.

15

In summary, the sample is dominated by small, independently-operated facilities, with 69

percent employing fewer than 50 individuals, and 95 percent employing fewer than 250

individuals. Facilities were also primarily independent; just 21 percent reported being owned by

a parent firm. Under 22 percent reported that either the facility or the parent firm had a research

and development (R&D) department, with the vast majority in manufacturing sectors. Less than

one-half of respondents (42 percent) reported selling directly into retail markets (Q24 in

Appendix A). The median number of close competitors reported was six (Q25).

IV. Variables

The following variables used in the econometric analyses were constructed from responses to

survey questions. As such, the quantitative measures used in the empirical analysis represent

responses by facility representatives who were most knowledgeable of their environmental

affairs. In some cases, the responses require subjective assessments, such as rating the strength

of various perceived motivations, while others require objective data to complete. Following the

survey protocols in the Dillman Tailored Design method, including maintaining strict

confidentiality, minimizes the potential for error or bias from the true population measure.

Summary statistics for each variable are presented in Table 2.

Dependent variables

1. Environmental management practices (EMP) – the extent and degree of EMP is

measured with an index constructed using Principal Component Analysis (PCA) of the responses

to Q12a-Q12k (see the Questionnaire in Appendix). PCA optimally weights chosen observed

variables and combines them linearly to create new principal component variables (Kennedy,

2003). Example practice dimensions include the following (for a complete list of practices, see

Appendix A):

16

• Our environmental goals guide operational decisions.

• We conduct environmental audits for our own performance goals, not just for

compliance.

• We require our suppliers to pursue environmentally friendly practices.

This, and the indexes of other motivations constructed using PCA discussed below, are scaled to

range between zero and one, where zero suggests the action or motivation is not present and one

suggests full implementation or a complete motivational force (Hall, 2006).

2. Pollution prevention activities (P2) – the level of pollution prevention actions is

measured with an index of the responses to Q14a-Q14f, constructed using PCA. Example

pollution prevention actions include the following (for a list of all actions, see Appendix A):

• Efforts have been made to reduce spills and leaks of environmental contaminants.

• We choose raw materials that minimize environmental impacts.

• We have modified our production systems to reduce waste and environmental

impacts.

Insufficient survey responses precluded an analysis of the facilities’ environmental

performance.5

5 Extensive efforts were made both to collect data on actual performance outcomes from the survey respondents, and also to supplement responses with secondary data from publicly available sources. These efforts did not generate a sufficient quantity and quality of usable data. Secondary data was collected for those facilities which reported to the US EPA’s Toxic Release Inventory (TRI), or which held one or more environmental regulatory permits. In this sample, only 24 respondents reported to the TRI, and only 240 held an environmental regulatory permit. Regarding primary data, the large numbers of missing responses to the survey questions resulted in a substantial loss of observations, and where responses were received, much of the data could not be considered sufficiently reliable. Regarding missing data, although 95% of respondents answered the compliance questions (questions 15a through 15e in the appendix), and 70 percent responded to at least one question regarding changes in impact levels (question 17a through 17h in the appendix), only 56 percent responded to one or more of the outcome questions (questions 16a through 16h in the appendix). However, performance questions were industry specific, and not all questions could be combined in multi-sector analysis. Within sectors, response rates were low (ranging from 2 to 54 percent, depending on the question), and sample sizes too small, to generate meaningful results that could be extrapolated to the larger marketplace.

17

Explanatory variables

We now describe the specific explanatory variables that are included to estimate the

reduced form equations for EMP and P2 obtained from the general theoretical framework posited

in section II. Each equation is a function of all the exogenous variables in the model.

Institutional (I) pressures

1. Issue: Environmental issues were a significant concern for the facility (yes = 1, no = 0

to Q1). We hypothesize that facilities that recognize that their operations face significant

environmental issues are more likely to implement EMPs. We also hypothesize that this

recognition could lead to more P2 activities. A similar variable indicating the perception of a

significant erosion control problem on farms was significant in explaining the number and extent

of soil conservation practices by farmers (Ervin and Ervin, 1982). Khanna et al (2007) find that

this factor has a significant effect in motivating adoption of a larger number of environmental

management practices (EMP) using count data methods, in a model that excluded reported

institutional pressures, management attitudes and barriers.

2. Consumer pressures – measured with an index constructed using PCA of Q3a-Q3c

We hypothesize that higher levels of perceived pressures by consumers for environmentally-

friendly products and processes are directly related to increased levels of EMP and P2.

Henriques and Sadorsky (1996) found that consumer pressures were a significant motivator in

the adoption of an environmental plan. Khanna and Anton (2002) also found firms facing more

consumer pressures adopt more comprehensive environmental management systems.

3. Interest group pressures – measured with an index constructed using PCA of Q3d-Q3f

We hypothesize that higher levels of pressure by environmental interest groups will increase

EMP and P2. Previous studies have found evidence of this hypothesized effect. Maxwell, Lyon

18

and Hackett (2000) estimated that changes in company emission levels reported to the EPA’s

Toxics Release Inventory (TRI) between 1988 and 1992 were lower in states with more active

environmental organizations. McClelland and Horowitz (1999) found that a sample of paper

mills generally exceeded water pollution regulatory standards and attributed the overcompliance

to community pressures to be a ‘good neighbor’. Henriques and Sadorsky (1996) found that

perceived pressures from lobby groups and neighborhood and community groups were

significant in motivating voluntary actions, while Khanna and Damon (1999) found a similar

effect by trade associations. Most of these studies concerned behavior by larger public firms.

It’s unclear whether the effect extends to environmental action by smaller and private firms.

4. Investor pressures – measured with an index constructed using PCA of Q4a-Q4c

We hypothesize that greater pressure by investors increases facility environmental management.

Alberini and Segerson (2002) and Khanna (2001) conclude that empirical studies have generally

found that stock prices are sensitive to a firm’s environmental performance and, by inference, to

its environmental management effort. By implication, publicly traded firms will undertake more

EMP and P2 than privately owned facilities. It’s possible that investors and their advisers can

more readily screen facility environmental practices than P2 activities, and therefore the effect on

EMP may be stronger.

5. Regulatory pressures – measured with an index constructed using PCA of Q4d-Q4h

We hypothesize that higher perceived pressure from current and future environmental

regulations result in higher levels of EMP and P2. Reviews generally conclude that regulatory

pressure exerts a robust positive effect on environmental management efforts (Alberini and

Segerson, 2002; Khanna, 2001). Our index of regulatory pressures tilts more toward future or

anticipated regulations than current (3 of 5 elements), and therefore may show more influence on

P2 activities.

19

6. Competitive pressures – measured with an index constructed using PCA of Q5a-Q5f

Some investigators hypothesize that increases in various market pressures to keep up with

competitors, reduce costs, differentiate products, and increase productivity lead to higher levels

of environmental management policy and pollution prevention actions (Arora and Cason 1995;

Khanna and Damon 1999). Empirical studies have found mixed effects of competitiveness

influences on environmental management (see survey in Khanna 2001).

Management attitudes toward the environment (α)

7. We measure these with an index constructed using PCA of Q7 a,b,d and f. Elements c

and e of Q7 were not included in this index because their content was more economic in nature.

We hypothesize that upper management attitude supportive of facility environmental stewardship

translates into higher levels of EMP and P2, similar to Nakamura, Takahashi and Vertinsky

(2001). As in that study, we assume that these attitudes are primarily exogenous. The survey did

not set out to collect information to explain the potential causes of these attitudes.

Perceived Facility Barriers (B)

8. Barriers are measured with an index constructed using PCA of Q8a-Q8h. The

potential barriers include high upfront expense, lack of availability of knowledgeable staff, high

day-to-day costs, significant upfront time commitment, uncertain future benefits of

environmental actions, risks of downtime or delivery interruptions during implementation,

contributions to environmental performance not included in performance appraisals, and

employees not being rewarded for contributions to facility environmental performance. These

factors represent either added costs in materials, equipment or staff, resource impediments,

increased risks for operations, or incentive incompatible management policies. Therefore, we

hypothesize that lower levels of the PCA index of perceived barriers will lead to increasing a

20

facility’s environmental friendliness. Environmental management studies have rarely measured

and tested the effects of such barriers to environmental management behavior. Alberini and

Segerson (2002) discuss the information costs associated with gathering information on pollution

abatement techniques and the added transaction costs of voluntary agreements. Nakamura,

Takahashi and Vertinsky (2001) include debt ratio in their analysis to estimate the effect of

increased costs of capital and employee age to capture the slower learning effect of older

workers on implementing environmental management.

Observed Facility characteristics (X)

9. Parent Ownership: Facility was owned by a parent company (yes = 1, no = 0 to Q18).

We hypothesize that parent company ownership makes more resources available to the facility to

develop its environmental policy and strategy, perhaps in the form of templates and guidance on

various EMPs. The parent company may also have information and experience on EMPs and

P2 activities that would make them more attractive to the facility.

10. Multinational: Facility or parent company was a multinational corporation (yes = 1,

no = 0 to Q21). Multinational firms face a more complex environmental management

environment in complying with a mosaic of regulations in multiple countries. This complexity

introduces greater risks from being found in non-compliance. We hypothesize that these risks

lead the facility to adopt higher levels of EMP than facilities that operate solely in the U.S.,

ceteris paribus. Multinationals also may be exposed to a wider array of environmental

management technologies because of their operations in a variety of countries and therefore may

be aware of more EMP and P2 that offer net benefits.

11. Private: Facility or parent company was privately owned (versus publicly traded or

other; yes = 1, no = 0 to Q22). We hypothesize that companies that are privately owned have

21

fewer incentives to adopt environmental practices and pollution-prevention actions than their

publicly traded counterparts because they are not subject to stock market pressures from

environmentally-conscious investors and other stakeholders. This rationale was also articulated

during the pre-survey interviews by a private firm engaged in voluntary environmental

management.

12. Facility R&D or Parent R&D: Facility had its own R&D department (Q23A) or

parent company has an R&D department (Q23B), (base is no R&D capacity). Adoption of P2

practices may also be influenced by a firm’s technological capabilities because strategies to

prevent pollution need to be customized to the particular production processes and products of

the adopting firm. Therefore, pollution prevention is likely to require technical expertise and

related experience. Cohen and Levinthal (1994) refer to these inputs as “complementary internal

expertise.” Indeed, surveys of firms suggest that adopters of pollution prevention techniques are

more innovative in general, with higher R&D intensity and a history of more frequent new

product introductions and product design changes (Florida and Jenkins, 1996). Therefore we

hypothesize that facilities with their own or parent company R&D capacity will adopt higher

levels of P2 practices. It’s also possible that the P2 activities could carry over to adopting more

EMPs to help facilitate their implementation.

13. Facility (Sales) Revenue: Total 2004 facility revenue was less than $25 million

(small, Q28A), or $25- $100 million (medium, Q28B), (base > $100 million; large). Several

investigators have hypothesized that larger firms have more incentive to participate in VEPs than

smaller firms because of economies of scale and more personnel that lower the costs of

participation and the threat of increased exposure to liability because of ‘deep pockets’ (Arora

and Cason, 1995; Khanna, 2001; Lyon and Maxwell, 2004; Videras and Alberini, 2000). We

assume these reasons carry beyond VEP participation to the adoption of EMP. We also

22

hypothesize that larger facilities have more resources to undertake P2 activities that often require

up-front investments than smaller facilities, ceteris paribus. The empirical evidence of the effect

of firm size on environmental effort is mixed and often insignificant. If the analysis does not

control for other motivations and barriers, firm size may be correlated with those factors and

capture some of their influences.

14. Management age: Average age of facility upper management was 20-40 years

(Q29A), or 41-60 (Q29B), (base > 60). Very few studies have examined the effect of

management age on firm environmental management behavior. Nakamura, Takahashi and

Vertinsky (2001) theorize that a lower average age of firm employees may increase firm

environmental actions because younger employees have a higher learning capacity. However,

their measure extends beyond managers to all employees. We hypothesize that older managers

have acquired more human capital over time to become proficient in all aspects of management,

and therefore are more likely to implement higher level of EMPs and to undertake more P2

activities that bring net benefits to the facility.

15. Industry sector: We include dummy variables for each manufacturing and service

sector to capture any sectoral effects on EMP and P2 not reflected by the motivations, barriers

and facility characteristic variables. A dummy variable is also included for those facilities that

did not identify a sector. The base sector for interpreting the coefficients is accommodations.

V. Econometric Results

We estimate reduced form equations for environmental management practices (EMP) and

pollution prevention actions (P2) based on equations (6) and (7) from the theoretical model.

Other studies of the factors affecting facility environmental management actions have used this

econometric approach, e.g., Johnstonne and Labonne (2009); Nakamura, Takahashi and

23

Vertinsky (2001). The equations allow an assessment of the size and significance of the effect of

a hypothesized explanatory variable on the dependent variables while controlling for the

influences of other exogenous factors. Specifically, the following two equations are estimated

using seemingly unrelated regression (SUR) estimation methods:

EMPi =β1’Ii + β2’ Bi + β3’ Xi + β4 αi + ε1i (8)

P2i = γ1’Ii, + γ2’ Bi + γ3’ Xi + γ4 αi + ε2i (9)

where εi’s are error terms.

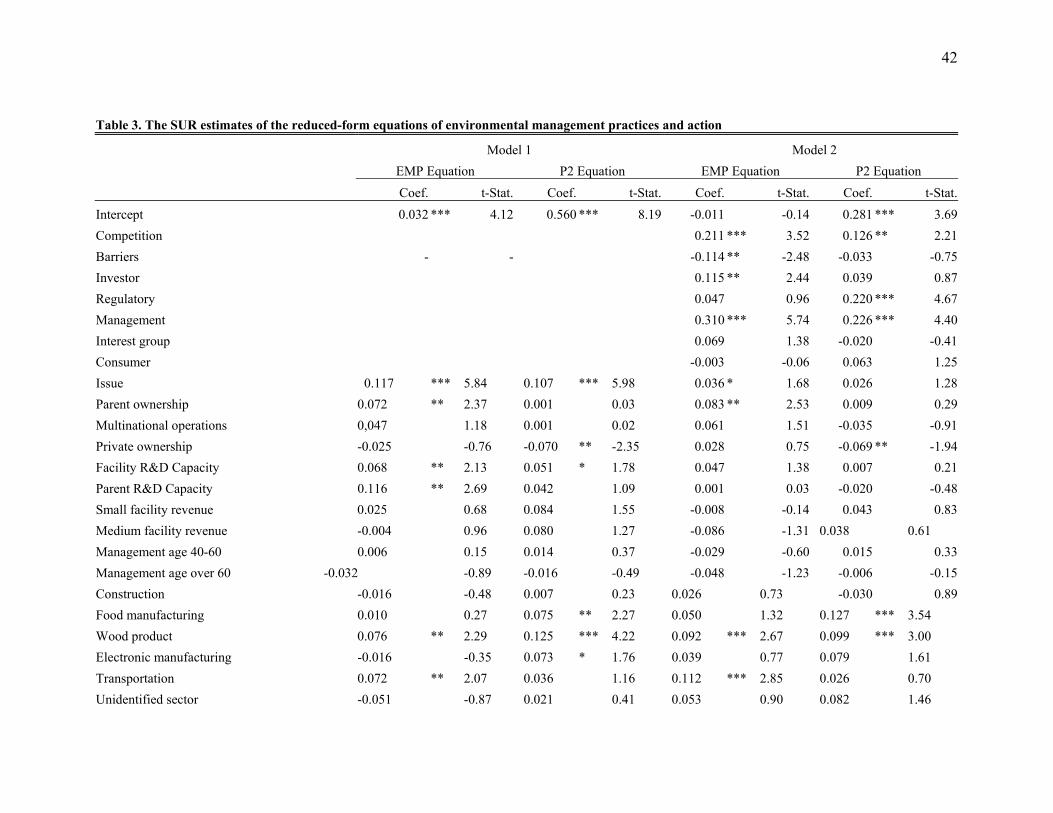

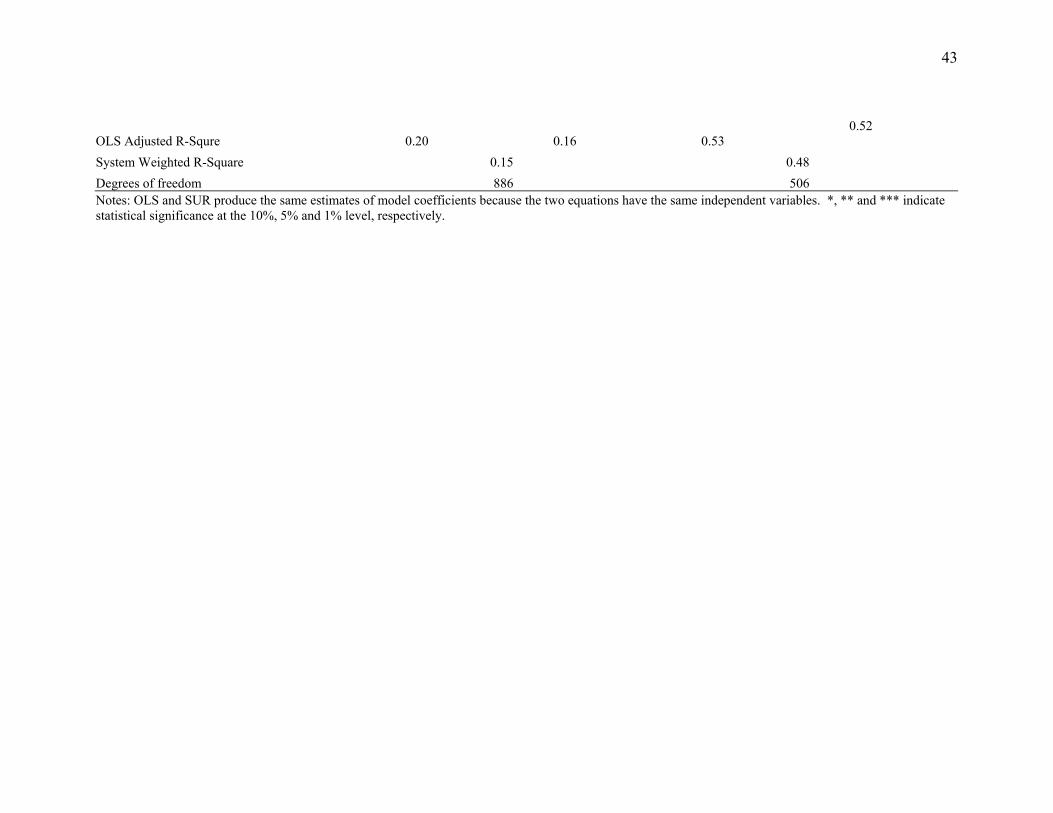

Table 3 reports the estimations of three specifications of the reduced form equations to

check the robustness of the estimated results. Model 1 includes only the observed facility

characteristics and Issue and is similar to the specification included in Khanna et al. (2007). In

Model 2 we expand upon Model 1 to analyze the influences of perceived institutional pressures

and barriers along with the Issue and facility characteristics. To examine the possibility that

facilities that see the environment as a significant issue for them were also the ones that

perceived greater pressures from the sources described above, we estimate Model 3 while

excluding the variable Issue but including all the other variables in Model 2. We use this to

examine the robustness of the effect of the motivational and barrier variables. All models include

the sector dummies to control for structural differences across sectors that might affect the

decisions of firms to adopt EMP or P2. As more explanatory variables are included in the

model, the system weighted R2 increases from 0.15 to 0.48.

The estimation results for model 1 show that the facilities with Issue equal to one were

more likely to choose a higher level of EMPs and a higher level of P2 activities. Moreover,

facilities owned by a parent company and having an R&D department in the facility or the parent

company were statistically significantly more likely to have a higher level of EMPs. These

findings are consistent with those in Khanna et al. (2007). Additionally, we also find that

24

facilities that were publicly traded and therefore possibly faced greater institutional pressure

from shareholders, as well as those that had their own R&D department had a higher level of P2

activities.

Model 2 shows that with the inclusion of the suite of perceived institutional pressures, the

variable Issue is statistically less significant in explaining the level of EMPs and has an

insignificant effect on the level of P2 activities. Instead we find that a facility is more likely to

adopt more EMPs and P2 activities if a) it believes that a higher level of EMPs will increase its

competitive advantage and b) its upper management has a positive attitude toward environmental

stewardship. The perception that investors value reduced environmental risk is associated with

more EMP activities but not with more P2 activities. On the other hand, a facility is more likely

to take P2 actions if it states that its management desires to improve compliance with existing

and anticipated regulations and to preempt regulations. A facility is less likely to adopt EMPs if

it faces large barriers to environmental management such as high up-front costs, substantial time

investments, and a lack of knowledgeable personnel; however, concerns about such barriers had

an insignificant effect on the adoption of P2 activities. Facilities owned by a parent corporation

are more likely to adopt EMPs, while publicly traded facilities are more likely to engage P2

activities. After controlling for all external pressures, the Issue variable are no longer statistically

significant, suggesting some degree of correlation between Issue and the institutional factors

considered here. It is possible that the facilities for which environmental issues are significant are

those that recognize the market-based and non-market pressures for reducing environmental risks

and improving environmental performance. This model shows that the inclusion of perceived

influences by external stakeholders and upper management attitudes adds to our understanding of

the mechanisms through which institutional pressures, social norms and economic concerns

25

could be playing a role in the extent to which a facility undertake various types of environmental

management.

In Model 3, we exclude Issue but include all the other variables included in Model 2. We

find that signs and significances of the other variables are qualitatively unchanged suggesting

that our results are robust across the various specifications considered here. Specifically, all

models provide robust evidence that pro-environment management attitudes increase the

likelihood of a firm undertaking a higher level of EMP and P2 activities. The uniform

significance and size of the coefficient on the management attitudes variable suggest that a utility

maximization approach can help explain corporate environmental actions. The construct derived

from the four stewardship-related elements in question 7 affirms the importance of these

personal values in business environmental management. It significantly increases the likelihood

of P2 activities suggesting that the influence of upper management attitudes does not end with

the adoption of EMPs, but extends to P2 activities as well.

As noted, institutional forces operating through capital markets in the form of investor

pressures and competitiveness concerns, and perceived facility barriers also exert positive effects

on EMP. The significance of the investor and competitiveness variables in the EMP equation

conforms to findings in several other studies (Dasgupta, Hettige and Wheeler, 2000; Henriques

and Sadorsky, 1996; Khanna and Anton, 2002; Videras and Alberini, 2000). The significance of

the competitiveness variable in the EMP equation suggests that interest in product and process

innovations and other cost-saving or differentiation strategies spread across the industries

surveyed, not just manufacturing. The composite measure of potential barriers, e.g., upfront time

commitment, significantly decreases EMPs. This finding suggests that responding facilities

perceive some significant impediments to improving the environmental friendliness of their

processes, products, and services. The barriers receiving the highest average ratings included

26

high upfront expense, high day-to-day costs, significant upfront time commitment, and uncertain

future benefits (Jones 2007). As noted, few other studies have had the data to conduct

quantitative analysis of the effects of such barriers.

The positive impact of having a parent company suggests those facilities can tap larger

reservoirs of resources to implement EMP than their independently-operated counterparts. The

implications for the design of future environmental policy are important, as only a very small

minority of facilities were owned by parent companies. Finally, facilities operating in the wood

products manufacturing and transportation sectors had significantly higher levels of EMP than

the base sector of accommodations.

In contrast to the level of EMP, a narrower set of factors motivates P2 actions. In

addition to management’s environmental attitudes, perceived regulatory pressure and

competiveness concerns are statistically significant in the P2 equation. This finding supports the

influential role of regulation on environmental activity hypothesized in this and other studies.

However, the impact of regulation does not extend back to more EMP for our sample of

facilities. P2 is more responsive to regulatory pressure than EMP perhaps because P2 has a

more direct effect on environmental compliance than EMP. The significant positive effect of

competitiveness concerns on P2 activities suggests that the sample facilities perceive these

actions as important in maintaining their economic viability. One facility characteristic, public

ownership, significantly increases P2 actions relative to private operations. This significant

effect only occurred in model 3, and therefore should not be considered as robust as the

influences of management attitudes, regulatory pressure and competitiveness concerns. The

finding that privately owned facilities practice significantly fewer P2 techniques supports our

hypothesis that they experience less pressure from environmentally conscious investors and other

stakeholders than their publicly traded counterparts. Finally, the wood products and food

27

manufacturing sectors exhibited significantly higher P2 activities than the accommodations

sector, ceteris paribus. This may reflect the more pollution reduction experience and

opportunities in the two manufacturing sectors that experience broad regulation of their wastes.

Surprisingly, the perceived pressures from consumers and environmental interest groups

and a variety of facility characteristics (e.g., size) are insignificant in the EMP equations. The

insignificance of consumer pressures accords with recent reviews that conclude this factor has

not exerted a large effect on environmental management to date (Alberini and Segerson, 2002;

Khanna, 2001). Environmental interest group pressure also has an insignificant effect on EMPs

and P2 activities. The significant coefficients on the wood products and transportation sector

dummies in the EMP model may be pulling some explanatory power from the interest group

variable. Several studies have found that such groups and environmentally-supportive political

jurisdictions are significantly associated with increased environmental activity (Innes and Sam,

2008). For example, Nisitami (2009) estimated that these stakeholders’ environmental

preferences/pressures influenced Japanese firms’ decisions to adopt ISO 14001.

The insignificance of facility size, measured by annual sales categories, on EMP and P2

intensity contrasts with other studies, which have found that large firms are more likely to

participate in a voluntary environmental program (Arora and Cason, 1995; Dasgupta, Hettige and

Wheeler, 2000; DeCanio and Watkins, 1998; King and Lenox, 2000; Videras and Alberini,

2000).6 Other studies have found facility size plays a significant role in adopting environmental

management systems. For example, Johnstone and Labonne (2009) find that the firms’

motivations for adopting EMSs can be divided into achieving better compliance or improved

6 We also ran the models with firm size defined based on the number of employees. The results stayed the same, that is, all variables that were significant before stayed significant, while variables that were insignificant before remained insignificant. This holds regardless whether small facilities are defined as those with 15, 20, or 25 employees or less and medium facilities are defined as those with 50, 75 or 100 employees or less.

28

performance, and signaling good environmental behavior to other market participants or

regulators. They found the relative importance of these motivations varies systematically by

facility size. Cost factors held more importance for smaller facilities in adopting EMSs, while

signaling exerted a significant influence for larger facilities. Our earlier analysis also found that

larger facilities, measured in terms of employment, were more likely to participate in voluntary

environmental programs, and adopt larger numbers of EMPs, but only if they saw environmental

issues as a serious concern (Khanna et al, 2007).

IV. Conclusions and Policy Implications

The popular press often reports stories of companies that transform their operations to

become more environmentally friendly. A growing number of studies have investigated the

factors that motivate firms to make these transformations. This study adds to that literature by

testing an enlarged set of potential motivations and barriers from both utility maximization and

institutional theories with survey data from a wide spectrum of manufacturing and service

businesses in an environmentally progressive state. We also use two measures of facility action,

environmental management routines and pollution prevention activities, to conduct the tests.

The results provide evidence that a broad suite of market and nonmarket institutional

pressures and internal factors explain business proactive environmental management. The results

also suggest that a combination of economic and institutional theories provides a sound

conceptual base to understand the mechanisms leading firms to adopt EMPs and P2. One of our

most robust findings is that a pro-environmental attitude towards the environment by upper

managers is strongly correlated with higher facility EMP and P2 activities. This result suggests a

utility maximization approach in addition to institutional theory can help understand business

29

environmental activities, similar to what Nakamura, Takahashi and Vertinsky (2001) found for

ISO program adoptions in Japanese firms.

The tests also suggest different sets of influences for the two environmental actions. We

find that surveyed facilities facing more intense competitive pressure for environmental

performance, lower costs (barriers) of adopting responsible environmental management and

greater pressure from investors have implemented higher levels of EMP. Facilities that report

environmental issues as a significant concern also have significantly higher EMP. On the other

hand, facilities reporting a higher level of regulatory pressure and competition and having a

positive attitude toward the environment are more likely to adopt P2 activities. Although our

survey would not permit such a test, the different sets of influences may reflect differing

institutional pressures on the facility departments most interested in each action as theorized by

Delmas and Toffel (2008).

An overarching policy implication flows from the empirical finding of substantially

different sets of significant factors in the EMP and P2 equations. As noted, both internal facility

characteristics and various institutional market factors are statistically significant in the EMP

equation. The diversity suggests that relying principally on a narrow strategy to advance EMP,

especially regulation, will not fare well. Indeed, policy attempts to influence the trajectory of

environmental management by altering just one factor may miss policy targets or be offset by

simultaneous changes in the other forces. For example, offering technical and financial

assistance to lower barriers to environmental management practice adoption may be offset if

these or other policies weaken competitiveness and investor pressures.

Another policy implication is that a facility is more likely to take pollution prevention

actions when it perceives higher regulatory pressures in the future. In an earlier analysis of these

data, regulatory intensity also significantly increased the probability of a facility participating in

30

voluntary environmental programs (Khanna et al, 2007). That finding, coupled with the

significant influence on P2 found in this study, implies that regulatory pressure is a complement

to voluntary environmental effort rather than a substitute for it. The two findings provide robust

support for the importance of perceived regulatory pressure because the two analyses differed in

significant ways, as noted earlier. In this study, the models included management attitudes and

pollution prevention as an added dimension of environmental management, and yet in both sets

of models, regulatory pressure remains a significant variable. The influential role of regulation

supports other theoretical and empirical studies that find credible regulatory threats are necessary

to advance voluntary environmental actions (Alberini and Segerson, 2002; Khanna, 2001; Lyon

and Maxwell, 2004; Segerson and Miceli, 1998). Without the threats, political appeals to

increase voluntary environmental management likely will fall short of public goals for pollution

control and other environmental stewardship objectives.

The study’s findings also provide insight into the roles of institutional pressures outside

of public environmental regulation and internal factors. Key market forces, particularly

competitiveness and investor pressures, along with cost barriers, are statistically significant in the

the environmental management practice equation. This provides evidence that public and private

policy actions to improve the quality of information about facility environmental management

and performance for investors, distribute reliable data on costs and returns of environmental

management practices, advance green technological innovations that aid competitiveness, and

technical assistance and educational programs to lower barriers could accelerate voluntary

environmental activity.

In closing, we identify two lines of inquiry that merit more attention. First, the robust role

of management attitudes toward the environment suggests that they should be an integral

element of business environmental management studies. Our survey was not designed to gather

31

information about the influential forces that explain the formation of such attitudes. This type of

intelligence would help understand the potential roles of private and public educational and other

measures to encourage a larger number of managers to pursue cost-effective voluntary actions.

Second, the integration of utility maximization and institutional theories appears to offer a more

powerful framework for understanding business environmental behaviors than one without the

other. We made a modest first attempt at this integration but believe carefully designed surveys

could provide richer details on the interaction of the two sets of forces. Findings from both lines

of inquiry would contribute to an improved understanding of effective strategies to induce

greater voluntary environmental effort by industry.

Acknowledgments

We are grateful for the valuable comments of three anonymous Journal reviewers whose

insights and suggestions significantly improved the content and clarity of this paper. The

research reported here comes from the project “Oregon Business Decisions for Environmental

Performance” funded by the U.S. Environmental Protection Agency (EPA) Program on

Corporate Environmental Behavior and Effectiveness of Government Intervention, June 2003 –

June 2007. Ervin and Wu are the senior co-authors of this paper. The authors thank Cameron

Speir for his valuable contributions to the survey development and enumeration and database

construction. Ervin acknowledges the helpful comments from seminar participants at Michigan

State University’s Elton R. Smith lecture series, the College of William and Mary, Reed College,

and the Organization for Economic Cooperation and Development, the valuable technical editing

assistance by Karen Carskadon, and helpful statistical support by Xixi Wang. Any opinions

expressed here are the authors’ and do not reflect the views or policies of the EPA.

32

References

Alberini, A. and K. Segerson, 2002. Assessing voluntary programs to improve environmental

quality. Environmental and Resource Economics 22(1-2): 157-184.

Anton, W., G. Deltas, and M. Khanna, 2004. Environmental management systems: Do they

improve environmental performance? Journal of Environmental Economics and

Management 48(1): 632-654.

Arora, S. and T. N. Cason, 1995. An experiment in voluntary environmental regulation:

Participation in EPA’s 33/50 Program. Journal of Environmental Economics and

Management 28(3): 271-287.

Arora, S. and S. Gangopadhyay, 1995. Toward a theoretical model of voluntary

overcompliance. Journal of Economic Behavior and Organization 28(3): 289-309.

Auld, G. S. Bernstein, and B. Cashore, 2008 “The New Corporate Social Responsibility”

Annual Review of Environment and Resources, Vol. 33: 413-435.

Baron, D.P. 2001. Private politics, corporate social responsibility, and integrated strategy.

Journal of Economics and Management Strategy 10(1): 7-45

Brau, R. and C. Carraro, 1999. Voluntary approaches, market structure and competition. CAVA

Working Paper 99/08/1. Paris, CERNA (Centre d’Économie Industrielle).

Cohen, M.A., 1997. “Firm Response to Environmental Regulation and Environmental

Pressures.” Managerial and Decision Economics 18:417-420.

Cohen, W. and D. Levinthal, 1994. Fortune favors the prepared firm. Management Science

40(2): 227-251.

Cordano, M and I.H. Frieze, 2000. “Pollution Reduction Preferences of U.S. Environmental

Managers: Applying Ajzen’s Theory of Planned Behavior” Academy of Management

Journal, 43 (4): 627-641.Dasgupta, S., H. Hettige, and D. Wheeler, 2000. What improves

33

environmental compliance? Evidence from Mexican industry. Journal of Environmental

Economics and Management 39(1): 39-66.

Darnall, N., I. Henriques and P. Sadorsky. 2008. “Do Environmental Management Systems

Improve Business Performance in an International Setting?” Journal of International

Management (14): 364-376.

DeCanio, S. J. and W. E. Watkins, 1998. Investment in energy efficiency: Do the characteristics

of firms matter? Review of Economic Statistics 80(1): 95-107.

deLeone, P. and J. Rivera, editors. 2009. Voluntary Environmental Programs: A Policy

Perspective. Plymouth (UK): Lexington.

Delmas, M. and M. W. Toffel. 2004. Stakeholders and environmental management practices:

An institutional framework. Business Strategy and the Environment 13(4): 209-222.

Delmas, M. and M. W. Toffel. 2008. Organizational responses to environmental demands:

Opening the Black box,” Strategic Management Journal., 29: 1027–1055.

Dillman, D., 2000. Mail and Internet Surveys: The Tailored Design Method, Second Edition.

New York, John Wiley & Sons, 464 pp.

Ervin, C. and D. Ervin, 1982. Factors affecting the use of soil conservation practices:

Hypotheses, evidence, and policy implications. Land Economics 58(3): 277-292.

Esty, D. C. and A. S. Winston, 2006. Green to gold: How smart companies use environmental

strategy to innovate, create value, and build competitive advantage. New Haven, Yale

University Press, 366 pp.

Florida, R. and P. D. Jenkins,1996. Adoption of organizational innovations by Japanese

transplants. Heinz School Working Paper. Pittsburg: Carnegie Mellon University.

34

Florida R, Davison D. 2001. Gaining from green management: environmental

management systems inside and outside the factory. California Management Review

43: 64.

Fowler, F. J., 1995. Improving survey questions: Design and evaluation. Thousand Oaks,

California: Sage Publications, 190 pp.

Garvie, D., 1997. Self-regulation of pollution: The role of market structure and consumer

information. Fondazione Eni Enrico Mattei (FEEM) Working Paper 59.97. Milan: FEEM.

Glachant, M., 1999. The cost efficiency of voluntary agreements for regulating industrial

pollution: A Coasean approach. In: Cararo, F. Lévêque (Editors), Voluntary Approaches in

Environmental Policy, Fondazione Eni Enrico Mattei (FEEM) Series on Economics, Energy,

Environment. C. S. Dordrecht, Kluwer Academic Publishers, pp. 75-90.

Greene, W. H. 2003. Econometric Analysis, Fifth Edition. New York: Macmillan Publishing

Company, 1026 pp.

———, 2002. Greene, W. H., 2002. Econometric modeling guide, volumes 1 and 2. New York:

Econometric Software, Inc.

Hall, T., 2006. Business decisions for voluntary environmental management:

motivations, actions and outcomes. Masters thesis. Corvallis, Oregon, Oregon State

University.

Henriques, I. and P. Sadorsky, 1996. The determinants of an environmentally responsive firm:

An empirical approach. Journal of Environmental and Economics and Management 30(3):

381-395.

Innes, R. and A. G. Sam, 2008. Voluntary pollution reductions and the enforcement of

environmental law: An empirical study of the 33/50 Program. Journal of Law and

35

Economics 51(2): 271-296.

Johnstone, N. and J. Labonne, 2009. Why do manufacturing facilities introduce environmental

management systems? Improving and/or signaling performance. Ecological Economics

68(2009): 719-730.

Jones, C. 2007. Voluntary environmental program participation in selected Oregon

manufacturing, construction, accommodation, and transport sectors: Perceived influences on

participation and effects on effort and outcomes. Master’s project. Portland, Oregon,

Portland State University.

Jones, Cody. 2008. What’s regulation got to do with it? Examining the impact of regulatory

intensity on facility environmental management and performance. Doctoral dissertation.

Portland State University: Portland, OR Kennedy, P., 2003. A guide to econometrics, Fifth

Edition. Cambridge, Massachusetts, MIT Press.

Khanna, M., 2001. Nonmandatory approaches to environmental regulation: A survey. Journal

of Economic Surveys 15(3): 291-324.

Khanna, M. and W. R. Q. Anton, 2002. Corporate environmental management: Regulatory and

market-based pressures. Land Economics 78(4): 539-558.

Khanna, M. and L. Damon, 1999. EPA’s Voluntary 33/50 Program: Impact on toxic releases

and economic performance of firms. Journal of Environmental and Economics and

Management 37(1): 1-25.

Khanna, M., P. Koss, C. Jones, and D. Ervin, 2007. Motivations for voluntary environmental

management. Policy Studies Journal 35(4): 751-772.

King, A. and M. J. Lenox, 2000. Industry self-regulation without sanctions: The chemical

industry’s Responsible Care Program. Academy of Management Journal 43(4): 698-716.

36

Konar, S., and M.A. Cohen. 1997. “Information as regulation: The effect of community right to

know laws on toxic emissions.” Journal of Environmental Economics and Management

32:109-124.

Konar, S., and M.A. Cohen. 1997. “Does the Market Value Environmental Performance?.” The