economic and steel market outlook 2015-2016 based on information available as of 17th april, 2015...

TRANSCRIPT

1) Based on information available as of 17

th April, 2015

23rd April 2015

Economic and Steel Market Outlook 2015-2016

Q2-2015 Report from EUROFER’s Economic Committee 1)

EU macro-economic overview (y-o-y change in %)

EUROFER Forecast April 2015

EU

2013

2014 (e)

2015 (f)

2016 (f)

GDP 0.0 1.3 1.9 2.0

Private consumption -0.1 1.3 2.0 1.8

Government

consumption 0.2 1.0 0.8 0.6

Investment -1.2 2.1 2.0 3.3

Investment in mach. equip.

-0.9 3.8 3.9 4.0

Investment in construction

-2.8 0.8 1.6 2.9

Exports 2.2 3.5 4.3 4.9

Imports 1.2 4.1 4.2 4.9

Unemployment rate 11.2 10.6 10.1 9.4

Inflation 1.5 0.6 0.2 1.4

Industrial

production -0.3 1.4 2.1 2.5

(e) = estimate (f) = forecast

I. EU Macro-economic overview

Indicators gaining further strength Private consumption to take the lead Investment is lagging, for now Modest support from public spending Mild rebound EU industrial activity Euro to remain low against the US$ Inflation to turn positive later in 2015 EU economy turning the corner? Outlook improved but risks still loom Economic growth showed a slight acceleration in the final quarter of 2014. GDP in the EU rose by 0.4% quarter-on-quarter and in the Eurozone by 0.3% following a sputtering economic performance in the second and third quarter of last year. The improvement was mainly driven by a mild rebound in investment in combination with continued support from private consumption and net trade. Meanwhile, only the reduction in inventories acted as a drag on growth. Particularly in Germany, Spain and Sweden the economic rebound gained traction in the final quarter of last year. GDP growth remained robust in the UK and Poland whereas the economic situation in France and Italy - the main laggards of the Eurozone recovery - appears to have stabilised with France registering a tepid 0.1% q-o-q growth and Italy’s 0% change moving the country out of recession. The resulting 1.3% GDP growth in the EU over the whole year 2014 basically reflects headwinds from disappointing investment growth preventing domestic demand to gain more traction and the

2

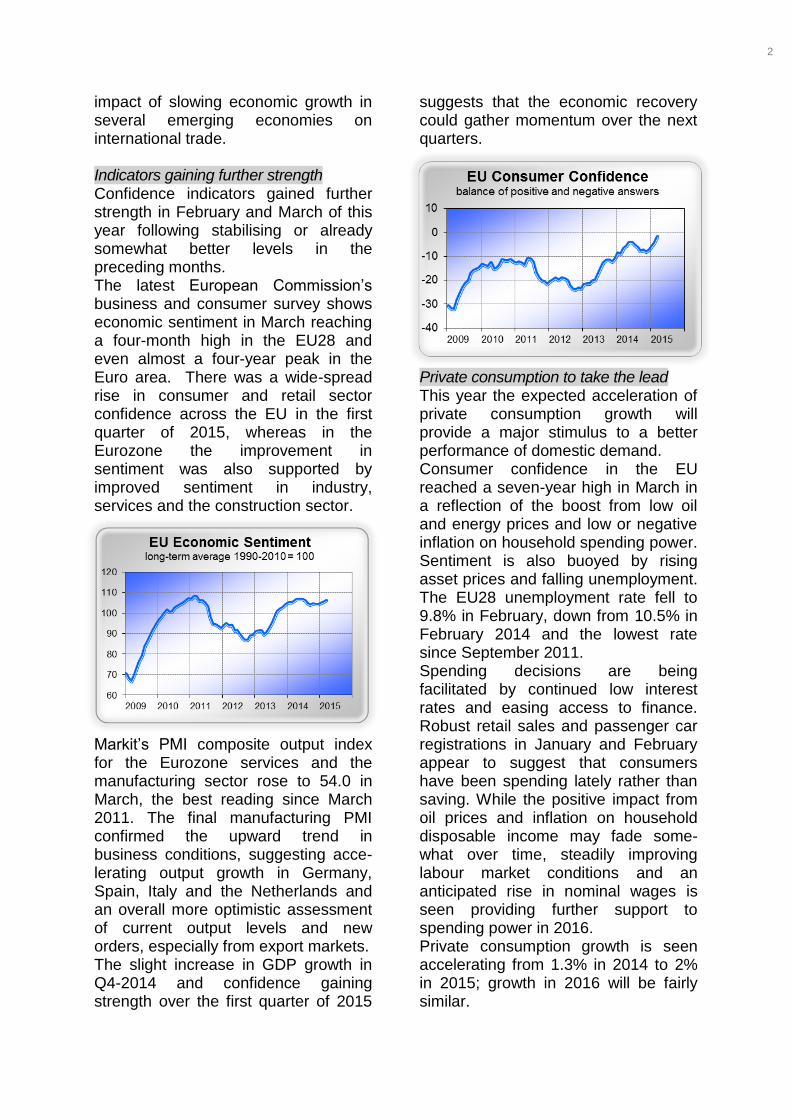

impact of slowing economic growth in several emerging economies on international trade. Indicators gaining further strength Confidence indicators gained further strength in February and March of this year following stabilising or already somewhat better levels in the preceding months. The latest European Commission’s business and consumer survey shows economic sentiment in March reaching a four-month high in the EU28 and even almost a four-year peak in the Euro area. There was a wide-spread rise in consumer and retail sector confidence across the EU in the first quarter of 2015, whereas in the Eurozone the improvement in sentiment was also supported by improved sentiment in industry, services and the construction sector.

Markit’s PMI composite output index for the Eurozone services and the manufacturing sector rose to 54.0 in March, the best reading since March 2011. The final manufacturing PMI confirmed the upward trend in business conditions, suggesting acce-lerating output growth in Germany, Spain, Italy and the Netherlands and an overall more optimistic assessment of current output levels and new orders, especially from export markets. The slight increase in GDP growth in Q4-2014 and confidence gaining strength over the first quarter of 2015

suggests that the economic recovery could gather momentum over the next quarters.

Private consumption to take the lead This year the expected acceleration of private consumption growth will provide a major stimulus to a better performance of domestic demand. Consumer confidence in the EU reached a seven-year high in March in a reflection of the boost from low oil and energy prices and low or negative inflation on household spending power. Sentiment is also buoyed by rising asset prices and falling unemployment. The EU28 unemployment rate fell to 9.8% in February, down from 10.5% in February 2014 and the lowest rate since September 2011. Spending decisions are being facilitated by continued low interest rates and easing access to finance. Robust retail sales and passenger car registrations in January and February appear to suggest that consumers have been spending lately rather than saving. While the positive impact from oil prices and inflation on household disposable income may fade some-what over time, steadily improving labour market conditions and an anticipated rise in nominal wages is seen providing further support to spending power in 2016. Private consumption growth is seen accelerating from 1.3% in 2014 to 2% in 2015; growth in 2016 will be fairly similar.

3

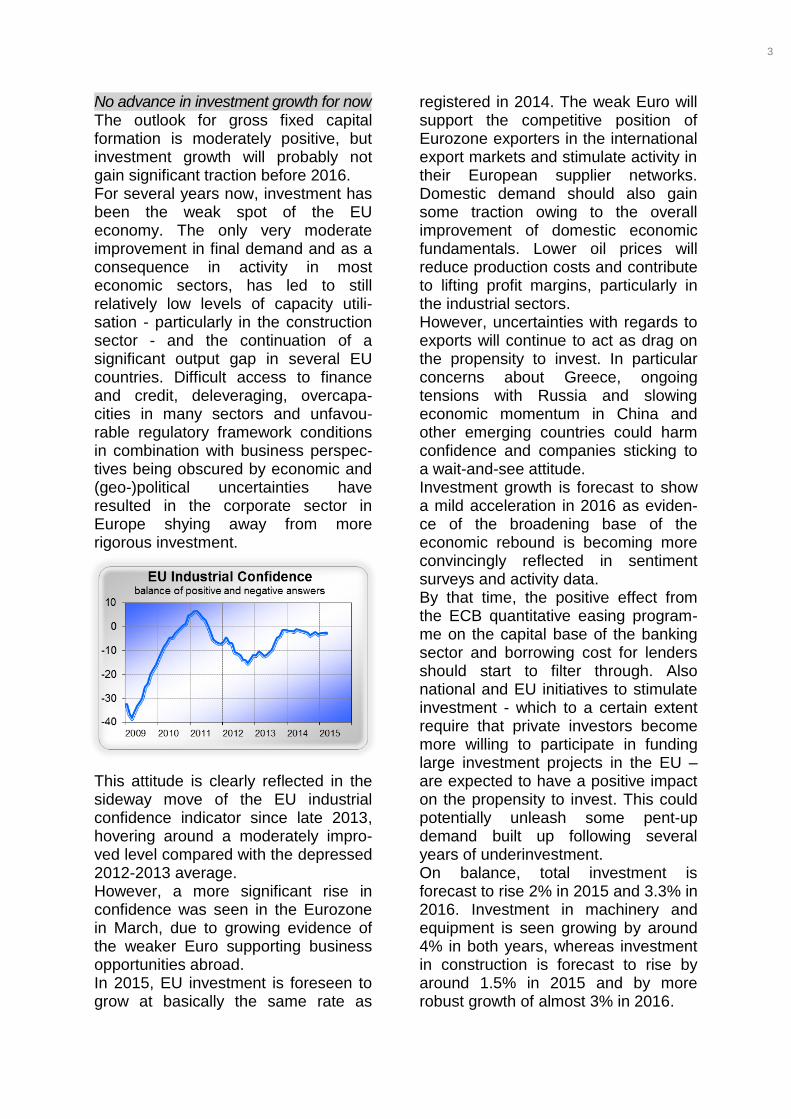

No advance in investment growth for now The outlook for gross fixed capital formation is moderately positive, but investment growth will probably not gain significant traction before 2016. For several years now, investment has been the weak spot of the EU economy. The only very moderate improvement in final demand and as a consequence in activity in most economic sectors, has led to still relatively low levels of capacity utili-sation - particularly in the construction sector - and the continuation of a significant output gap in several EU countries. Difficult access to finance and credit, deleveraging, overcapa-cities in many sectors and unfavou-rable regulatory framework conditions in combination with business perspec-tives being obscured by economic and (geo-)political uncertainties have resulted in the corporate sector in Europe shying away from more rigorous investment.

This attitude is clearly reflected in the sideway move of the EU industrial confidence indicator since late 2013, hovering around a moderately impro-ved level compared with the depressed 2012-2013 average. However, a more significant rise in confidence was seen in the Eurozone in March, due to growing evidence of the weaker Euro supporting business opportunities abroad. In 2015, EU investment is foreseen to grow at basically the same rate as

registered in 2014. The weak Euro will support the competitive position of Eurozone exporters in the international export markets and stimulate activity in their European supplier networks. Domestic demand should also gain some traction owing to the overall improvement of domestic economic fundamentals. Lower oil prices will reduce production costs and contribute to lifting profit margins, particularly in the industrial sectors. However, uncertainties with regards to exports will continue to act as drag on the propensity to invest. In particular concerns about Greece, ongoing tensions with Russia and slowing economic momentum in China and other emerging countries could harm confidence and companies sticking to a wait-and-see attitude. Investment growth is forecast to show a mild acceleration in 2016 as eviden-ce of the broadening base of the economic rebound is becoming more convincingly reflected in sentiment surveys and activity data. By that time, the positive effect from the ECB quantitative easing program-me on the capital base of the banking sector and borrowing cost for lenders should start to filter through. Also national and EU initiatives to stimulate investment - which to a certain extent require that private investors become more willing to participate in funding large investment projects in the EU – are expected to have a positive impact on the propensity to invest. This could potentially unleash some pent-up demand built up following several years of underinvestment. On balance, total investment is forecast to rise 2% in 2015 and 3.3% in 2016. Investment in machinery and equipment is seen growing by around 4% in both years, whereas investment in construction is forecast to rise by around 1.5% in 2015 and by more robust growth of almost 3% in 2016.

4

Modest support from public spending Public spending will continue to provide moderate support to GDP growth over the forecast period. Several countries will have to continue their strict budget policies in order fulfil the criteria agreed in the Maastricht treaty and to reduce high levels of public indebtedness. Nevertheless, improving economic growth should result in higher tax income, while lower government bond yields and reduced energy bills will curtail expenses. This should lead to a continuation of growth rates of public investment in the range of 0.5 to 1% per annum in 2015 and 2016. Mild rebound EU industrial activity EU industrial production data for the whole year 2014 data underpin that the growth pace of activity remained rather sluggish over the year. Eurostat data signal that total industrial production grew by just 1.1% last year.

January 2015 data show industrial activity moving sideways at the level reached at the end of last year while activity in February improved slightly. For 2015 and 2016 somewhat higher growth rates of industrial activity are foreseen. Improving domestic economic funda-mentals with private consumption taking the lead as main engine of growth of internal demand in the EU in combination with the overall positive outlook for exports which will be

supported by the weaker Euro are expected to boost industrial production growth. Concerns remain, however, with regards to slowing trade with Russia and its negative impact on EU countries with traditionally strong business connections in Russia. Nevertheless, the global economy gaining momentum in 2015 and 2016 is expected to gradually boost dynamics of international trade. The improved competitiveness of Eurozone exporters should ensure that net trade will continue to provide solid support to the industrial performance of EU industry. Industrial production is forecast to increase 2.1% in 2015 and 2.5% in 2016. Euro to remain low against the US$ The Euro stood over the first half of April at a rate of 1.07 against the US$, compared with 1.08US$ for March. The common currency had touched a twelve-year low of just under 1.06 US$ by mid-March following the start of bond purchases under the ECB quantitative easing programme on 9 March. Since May 2014 the Euro has lost around 25% of its value against the dollar.

The key factor behind this sharp depreciation has been the strong divergence between economic and monetary policies of the EU and the US. For the moment, the dollar looks

5

set to strengthen mildly further as the FED is moving closer towards introducing stepwise interest rate hikes which most likely will start from mid-2015. At the same time, the ECB asset purchases and uncertainty about Greece will for the moment keep downward pressure on the Euro. Over time, these divergences are foreseen to diminish to a certain extent as the EU economy picks up speed, boosted by the weak Euro and low oil prices. Should the US economy fail to rebound as expected after the weather-related slowdown in Q1-2015 and as a consequence the Fed postponing its monetary tightening schedule, the Euro bounce-back could start sooner rather than later. Inflation to turn positive later in 2015 In addition to boosting economic growth via a weaker Euro and cheaper cost of and easier access to financing, the ECB’s quantitative easing programme has also been introduced to anchor inflation expectations. Inflation in the Euro area remained in negative territory during the first quarter of 2015, albeit with a rising trend, increasing from -0.6% in January to -0.1% in March due to the initial sharp decline of energy prices easing somewhat going forward and rising prices for services, food and tobacco. Under the current economic conditions low or negative inflation is providing a welcome additional boost to economic growth, as both businesses and private households have the potential to use the increase in purchasing power – at least partially – for spending purposes. On the longer term, low or even negative inflation becoming entrenched in the expectations of enterprises and private consumers would work counter-productive on investment decisions. Core inflation is expected to turn slightly positive in the second half of

the year and hold steady, until the base effect of the oil price begins to fade during the final quarter of 2015. This should trigger a rising trend in inflation in 2016. EU economy turning the corner? The April 2015 outlook from EUROFER’s Economic Committee suggests that the economic recovery in the EU will find a more solid footing in 2015 and 2016. The slight improvement in GDP growth in Q4-2014 combined with the recent uptrend in economic indicators bode well for a more broad-based gain in economic momentum. The weaker Euro and low oil price will provide a major boost to domestic demand and exports. Private consumption looks set to take the lead as the key driver of economic growth in 2015. Investment is expected to take over this role in 2016 as evidence of the broadening base of the economic rebound is becoming more convincingly reflected in a further improvement of sentiment and hard data and business conditions improve further. Against the background of encouraging signals from indicators and hard data, the outlook for economic growth in the EU has been revised slightly upwards. GDP in the EU is seen growing by 1.9% in 2015 and 2% in 2016. Outlook improved but risks still loom The key internal risk for the economic recovery of the EU would be an exit of Greece from the Eurozone. Should Greece fail to start the austerity and reform process within the requested timeframe as agreed in the deal to extend the country's rescue programme, political tensions would rise further with eventually a Greek exit being an evident possibility. While a Greek exit would have particularly severe repercussions on

6

the Greek economy, the negative impact on the EU should not be underestimated despite the fact that the EU banking sector is now better prepared to limit turbulence arising from events such as a Grexit owing to the introduction of the European Stability Mechanism and a reduced exposure to Greek debt. Nevertheless, borrowing costs in several other Euro area economies would most likely rise, following initially huge impairments on loans to Greek banks. Uncertainty about financial and economic stability in the Euro area would flare up again and confidence would take a severe hit, thereby dampening especially investment growth perspectives. Another internal risk remains the divergence in economic performance at the country level. The extent to which EU member states will benefit from the current economic setting depends to a large extent on the pace of implementation of the necessary reforms with regards to the labour market, tax system, banking sector and functioning of public institutions. Despite tentative signs of improve-ment, France and Italy will continue to lag the economic recovery foreseen for the other large Euro area economies. With regards to external risks, a significant deterioration of the Russian economy due to an escalation of the conflict in Eastern Ukraine leading to the EU and other countries stepping up sanctions, would damage exports and confidence. Geopolitical unrest in the Middle East remains a topic of concern as well, particularly with regards to the negative impact of political and economic instability on confidence. The instable situation in Yemen since the Shiite rebels launched a power grab last February could affect oil supply via a disruption of shipments via the Bab el-Mandeb Strait. So far, however,

continued evidence of a global supply glut has tempered upward pressure on the oil price, which remained in a fairly narrow bandwidth around 55US$ per barrel of Brent in early April. Another risk would be weaker than expected growth of the US economy in 2015. Harsh weather and the labour conflict at the west coast affected economic activity at the start of the year, whereas several indicators are not as strong as expected. Should the dollar strengthen significantly further, US exports may be hurt and drag down GDP growth. This in turn may affect international trade. Also the recent weakness in several emerging economies remains a reason for concern. While for 2015 and 2016 a modest rebound in global economic growth appears to be a plausible scenario, it is also clear that the emerging economies may no longer contribute to global growth the way they have done in recent years. Meanwhile, chances have grown that EU economic growth could surprise on the upside this year. Positive economic and business fundamentals have become more firmly established in the early stages of 2015 than previously foreseen. Should the ECB’s monetary policy measures result in a faster than expected improvement of the invest-ment climate in the EU, possibly also supported by the Juncker’s investment plan, domestic demand could grow more vigorously than currently expected. A stronger depreciation of the Euro exchange rate and lower oil prices would also provide an additional boost to GDP growth in the EU.

7

USA Rather weak GDP growth in Q1’15 Rebound foreseen from Q2 US economy on track for stronger

economic momentum in 2015-2016 GDP growth in Q4-2014 was revised downwards twice, to just 2.6% at an annualised rate, a marked slowdown compared with more dynamic growth rates in Q2 and Q3. The slowdown reflects a downturn in federal government spending, slower non-residential investment and a smaller contribution from inventory investment. Relatively weak growth seems to have persisted in Q1-2015. Some data in early 2015 such as retail sales came in weaker than expected, suggesting rather sluggish private consumption. Harsh weather conditions affected activity in the Northeast and Midwest, with the labour dispute at west coast ports disrupting supply. Also oil industry investment is reported to have been weak. Meanwhile, the stronger dollar is weighing down on US exports. March indicators, however, support the expectation of a rebound of GDP growth from Q2 onwards. The manufacturing PMI index picked up to 55.3, with robust levels of output and new orders boding well for a rebound of economic growth over the coming quarters. However, the survey also showed exports orders dropping for the first time since November 2014. Job creation was strong in January and February. Robust employment growth will be supportive to rising wages; the lower energy bill will provide further support to private consumption in 2015. The stronger dollar and weak energy prices will keep inflation low for the time being. This suggests that the Fed will increase interest rates only gradually. Rising wages and low interest will be supportive to a modest housing market revival. On balance, the US remains on track for developing stronger economic momentum in 2015 and 2016. GDP is forecast to grow by on average 3% per annum.

Key emerging regions Positive outlook for India, but

prospects for the other BRIC countries are subdued

China's GDP growth in Q1-2015 came in at 7.0%, 0.3 %-points lower than the Q4’14 reading (annualised rate). Falling imports and muted industrial activity in January and February indicate that domestic demand weakened further. The housing market is the key factor behind this slowdown. Housing prices and residential construction activity continued their downward trend. Net trade is expected to have partially offset the drag from domestic demand on GDP growth. The outlook for the remainder of 2015 and for 2016 is obscured by potential risks in the Chinese economy. The housing sector correction looks set to continue, reflecting excess inventories in the residential sector. Private and public government debt is high and off-balance-sheet borrowing by local authorities has sparked fears of hidden credit risks in the banking sector. GDP growth could slow to below 7% in 2015 and to around 6% in 2016. The Indian economy grew 7.5% y-o-y in Q4-2014; a similar rate is foreseen for 2015 and 2016. The Modi government made encouraging progress on regula-tory and tax reforms, but further work is needed on reforming the labour market and investment climate. Low inflation will enable the Reserve bank to lower interest rates further. Sentiment is quite positive, which will be supportive to domestic demand growth. Brazil returned to growth (0.3% q-o-q) in Q4-2014, but prospects for 2015-2016 are muted due to the negative impact from falling prices and weak demand for commodities and from high inflation and high interest rates on investment. In due time, the weakened Real should support exports. GDP may grow 1% in 2015 and 2% in 2016. Russian economic conditions deterio-rated rapidly in early 2015 due to the impact of low oil prices, trade sanctions and the sharp Ruble devaluation. With no indications for a short-term improve-ment, GDP is now foreseen to fall 4% in 2015, followed by 0% growth in 2016.

8

1) As of 2013, “steel structures” is no longer a separate sector but is included in the construction sector. Shipbuilding activity is now included in “other transport” which includes all non-automotive transport equipment such as railway material, air & spacecraft and motorcycles

II. The EU Steel Market

Overview Steel Using Sectors

Development of the main steel using sectors – EUROFER forecast April 2015 % change year-on-year in the SWIP (Steel Weighted Industrial Production) index1)

% share in total

Consumption

Year 2014

Q115 Q215 Q315 Q415 Year 2015

Q116 Q216 Q316 Q416 Year 2016

Construction 35 1.4 -1.6 1.4 1.9 2.5 1.2 1.1 2.5 3.3 3.3 2.6

Mechanical engineering

14 1.2 1.4 2.2 1.1 2.7 1.9 3.0 3.2 3.5 3.4 3.2

Automotive 18 5.1 3.1 4.7 4.9 5.0 4.4 4.3 2.7 2.5 2.4 3.0

Domestic appliances 3 -0.3 -0.1 1.6 3.8 3.4 2.2 2.6 3.3 2.3 2.4 2.6

Other Transport 2 0.4 2.8 4.6 3.8 3.3 3.6 3.6 2.7 3.9 3.4 3.4

Tubes 13 2.4 0.4 0.3 1.1 -1.1 0.2 0.1 1.7 2.8 4.1 2.1

Metal goods 14 2.7 0.3 1.8 2.8 4.5 2.3 2.8 3.4 2.8 2.2 2.8

Miscellaneous 2 1.8 0.8 1.7 2.3 3.3 2.1 2.9 3.4 2.7 2.6 2.9

TOTAL 100 2.2 0.6 2.2 2.6 3.2 2.2 2.3 2.7 2.9 3.0 2.7

2014 ended on a weak note Steady growth SWIP 2015-2016 Investment key driver from 2016 Q4-2014 data for the EU steel using sectors confirm that activity ended last year on a weak note. The SWIP index increased by just 0.5% y-o-y, in line with the weak momentum suggested by industrial indicators for that period. Total activity over the whole year 2014 still grew 2.2%. This was primarily the result of strong growth in the first quarter of 2014 as a result of the weather-related base year effect compared with Q1-2013. Prospects for this year and next are moderately positive with fairly similar growth of activity expected for 2015 and somewhat stronger growth pencilled in for 2016. The economic framework at the start of

this year is rather positive. The weak Euro will provide a welcome boost to exports whereas lower energy bills will stimulate domestic demand. The sharp rise in consumer confidence over the past few months suggests that particularly private consumption growth could strengthen in 2015. Growth in Q1

will be modest, however, as construc-tion output will fall slightly compared with the high level of Q1-2014. The remainder of the year will see a gradual rise in activity across almost all sectors, resulting in total growth of around 2% in the whole year 2015. Activity growth in 2016 is foreseen to become more investment-driven as the investment climate in the EU will get support from easing financing condi-tions and EU policy measures. Exports will continue to boost output as well. The SWIP index is forecast to rise by 2.7% in 2016.

9

Construction

Output 2014 +1.4% Activity seen rising in 2015-2016 Residential activity key driver in 2015,

more broad-based growth in 2016 EU construction output in Q4-2014 continued the downward trend in activity registered in Q3; output fell 0.5% y-o-y. Total output in 2014 grew 1.4%, as a result of strong - weather-related - growth in the first quarter of last year and sluggish momentum in the remainder of the year. This growth figure, however, hides widely diverging trends at the country level. While the performance of the construction sector in Germany, the UK, Sweden and Hungary remained robust in Q4 and - including Poland -over the year as a whole, elsewhere in the EU activity remained lacklustre with most countries on a downward trend or at best moving sideways. The outlook for 2015 and 2016 is for construction activity to gradually gain momentum in most EU countries. Production in the first quarter of 2015 is expected to be down on the weather-related high level of output in the same period of 2014. The remainder of the year looks set to register a strengthening trend in the performance of the construction sector across the EU. However, France and Italy are foreseen to lag the modest pick-up in activity in the other EU countries due to both countries trailing

with regards to the implementation of reforms to remedy weak government finances, bureaucracy, high unemploy-ment and poorly functioning labour markets. These factors will prevent the two countries to return to growth before 2016. Meanwhile, activity in Spain is foreseen to recover from a low level following a multi-year slump. With regards to drivers of growth of activity, new and renovation projects in the residential sector will provide the main boost in 2015. Construction in Poland, however, will remain largely driven by infrastructure projects. Construction investment growth is expected to strengthen going into 2016, on a par with improving confi-dence levels and the expected easing of access to finance and continued low cost of borrowing. Also national and EU investment initiatives, supported by funding from the private sector, are expected to feed through in construction activity, with most likely a modestly positive impact on public and private funding for new infrastructure projects. Continued weakness in France and Italy will limit growth of EU construction activity to 1.2% in 2015. Output in 2016 is forecast to grow by around 2.5% as the construction sector fundamentals improve further, both at the sector and country level.

10

Automotive

Robust EU automotive sales in early 2015 but exports falter

Solid prospects for 2015-2016 Exports obscured by risks and

uncertainties The EU automotive market started 2015 on a positive note. Passenger car sales grew 8.6% y-o-y in the first quarter of 2015, with all large EU markets - Spain in particular - on an uptrend. Commercial vehicle sales rose 8.5% y-o-y over the January-February period. With the exception of France, demand improved in all major markets. Growth was very strong in Spain and the UK and in most Central European markets. Exports of premium segment cars lost momentum in the first months of this year. UK exports fell 9% y-o-y over the January-February period, whereas German Q1’15 exports stabilised at the year earlier level; this partly reflects the negative impact of weaker sales in Russia due to the 32% collapse of the market. Total automotive output grew 2.8% in the final quarter of last year; only in the UK and Sweden was slightly down on the year earlier level. First data and indicators for Q1-2015 signal that output in the EU continued to expand at a growth rate of around 2.5%. Germany, France and the UK bucked this trend and saw output falling moderately compared with the year earlier level; this basically reflects

weakening exports and OEMs switching to new model series. Meanwhile, output in Italy and Spain grew rather vigorously. Prospects for 2015 and 2016 remain rather upbeat. The EU car market is expected to benefit from the positive impact of low oil prices on disposable income and other factors such as improving labour markets boosting consumer confidence. Also commercial vehicle sales look set to remain on an uptrend owing to easing financing conditions and the positive impact of strengthening economic fundamentals and lower fuel prices on demand for road transport. The outlook for car exports is obscured by uncertainty. Hard data confirm that the light vehicle market in Russia collapsed at the start of this year, with sales falling by more than 30% y-o-y. Clearly, several producers are hit by weakening export demand, also because of slowing sales in other emerging markets. It remains to be seen how long and to what extent this may affect sector activity in 2015 and 2016. Total automotive output – including production of parts and components - is expected to increase by around 4.5% in 2015. Only in France activity is expected to remain under pressure. Automotive activity is forecast to expand by around 3% in 2016.

11

Mechanical Engineering

Output grew slightly in 2014 Weak Euro is seen boosting

exports EU investment picking up in 2016 In Q4-2014, EU mechanical engineering activity maintained the rate of expansion – almost 1.5% y-o-y - registered in the third quarter. Total activity in the whole year 2014 grew 1.2%. At the country level, fundamentals were rather robust in the UK, the Netherlands and Central Europe. Meanwhile, output in Germany and France grew slightly, whereas production in Italy, Spain and Sweden registered a decline. Export demand from third countries rather than the EU domestic market has been driving growth, although in several EU markets tentative signs of a modest recovery of investment in machinery and equipment could be observed. The mechanical engineering sector is expected to gain modestly further strength in 2015, whereas business conditions in 2016 will most likely see a more pronounced improvement. The key factors in the outlook for this sector are confidence and access to and cost of financing and credit. While since late 2014 indications that economic fundamentals underpinning the expectation of the recovery of the EU economy gaining traction have

become stronger, supported by the weaker Euro and low oil prices, the improvement in industrial confidence remained unconvincing. This can at least partly be explained by the fact that business prospects remained obscured by uncertainties with regards to demand from Russia and other emerging economies, internal stability in the EU and the lack of hard evidence of the recovery in the EU gaining momentum. Meanwhile, financing conditions impro-ved steadily, but particularly small and medium sized companies still report rather difficult access to credit. For 2015 a modest improvement in activity is on the cards, basically owing to the weak Euro boosting competiti-veness of Eurozone exporters on the international markets. EU demand is expected to strengthen only modestly. EU mechanical engineering output is forecast to rise almost 2% in 2015. A more robust rise of activity is predicted for 2016 in line with streng-thening sentiment as the recovery in the EU gains further traction, financing conditions ease further and the corporate sector is becoming less risk aversive. By then, the sector could tap into pent-up demand accrued over years of underinvestment. Activity is forecast to rise by around 3%.

12

Tubes

Total output 2014 rose 2.4% Market prospects for line pipe

and OCTG clouded by reduced investment oil & gas sector

Other tube demand seen rising Slight rise tube output in 2016 EU steel tube output fell 4% y-o-y in the final quarter of 2014. Total production over the whole of last year increased 2.4%. The sector performance at the country level diverged widely, depending on factors such as product range and end-user segment, the balance between domestic and export sales and exposure to international competition. Output in France fell sharply, whereas the rate of expansion of activity was stronger than average in Poland, the Czech and Italy. Output in the other countries was not too far from the 2013 level. The outlook for the steel tube sector in the EU is rather dim. To a large extent this can be attributed to uncertainties regarding market prospects for large welded tubes, oil country tubular goods and other market segments related to oil and gas exploration and exploi-tation. The sharp drop in oil prices has resulted in oil and gas companies cutting back on their investments. Competition in the commodity grade OCTG market is foreseen to remain

fierce due to ample supply from international suppliers. Following the suspension of the Southstream project last year, line pipe mills are reported to be waiting for the possible re-start of the project under a new name. It remains to be seen whether EU producers will benefit should this happen. For the moment also the outlook for US shale gas projects is less benign than a year ago. On balance, weak demand from these market segments and continued fierce competition from international suppliers in the commodity segment due to global overcapacity will act as a drag on total tube production activity in the EU. Meanwhile, market prospects for the main client sectors of small welded and seamless steel tubes such as the construction sector, the automotive and metal goods industry remain moderately positive. Activity in these sectors is expected to gradually gain momentum in 2015 and 2016 which should result in an increase in demand. However, also in these market segments competition from abroad will remain fierce. EU production of steel tubes is expected to stabilise around the year earlier level in 2015 and to increase by around 2% in 2016.

13

Domestic Appliances

Output fell slightly in 2014 - diverging trends at the country level

Prospects for 2015-2016 more favourable

Support from private consumption growth and residential sector

Activity in the electric domestic appliances sector in the EU grew 2.9% y-o-y in the fourth quarter of 2014, following a weak Q2 and Q3. On balance, total activity in 2014 fell by 0.3%. Output declined in most EU countries, with particularly a sharp contraction in France, the UK and Sweden. In contrast, production activity strengthened significantly in the Czech Republic and Slovakia owing to capacity expansions installed in preceding years coming further into operation. Fierce competition in a mature market largely dominated by replacement sales have led to domestic appliances manufacturers relocating production plants to lower-wage countries and reducing capacity in Western Europe. Demand for electric household appliances remained sluggish due to the persisting weakness of residential property markets in several EU countries - particularly so in France, Italy and Spain – and overall rather depressed levels of consumer sentiment.

Prospects for 2015 and 2016 are somewhat more positive owing to the expected mild acceleration of private consumption growth in 2015 and the recovery in the construction sector gaining traction. Particularly the residential property sector looks set to gain more momentum across the EU. Consumer confidence in the EU reached a seven-year high in March in a reflection of the boost from low oil and energy prices and low or negative inflation on household spending power. Sentiment is also buoyed by rising asset prices and the improving labour market. The segment of eco-friendly appliances which perform also competitively in terms of non-environmental attributes such as innovative design and styling is likely to show the highest growth rate of demand. Nevertheless, price competition and margin pressure in this sector will remain fierce as the internet retail channel accounts for an increasing share of total sales. In 2015, production in the EU is foreseen to increase by around 2%, followed by around 2.5% growth in 2016. Best prospects are foreseen for Germany, Spain and most Central European countries.

14

1) steel intensity is the ratio of steel consumption to steel weighted production in the steel using industries (SWIP)

Real Consumption

Forecast for real consumption - % change year-on-year

Period Year 2014

Q115 Q215 Q315 Q415 Year 2015

Q116 Q216 Q316 Q416 Year 2016

2.1 0.4 1.6 2.0 2.3 1.6 1.8 2.3 2.5 2.5 2.3

Real steel consumption rose 2.1% in 2014

Construction stopped acting as a drag on final demand growth

2015-2016: steady growth real consumption

Real steel consumption in the EU increased by around 2% y-o-y in the final quarter of 2014. This resulted in total real steel consumption over the whole year increasing by 2.1%, in line with a fairly similar moderate rise in activity of the steel using sectors. The automotive sector showed the strongest momentum over the year. Equally important for the growth of final steel demand is the fact that the construction sector finally turned the corner in the 2014 and stopped acting

as a drag on real steel consumption. The outlook for 2015 and 2016 is for a continuation of the moderate recovery of real steel consumption in the EU. The plausibility of this growth scenario has strengthened owing to the fact the fact that the business environment for most steel using sectors in the EU has

become more favourable owing to the weak Euro and low oil prices. While in 2015 private consumption growth looks set to be the major growth driver, investment is seen strengthening more robustly in 2016. Exports will continue to provide support to economic growth as well. As a consequence, activity in the steel using sectors is expected to rise by around 2% in 2015 and by almost 3% in 2016. Steel intensity is expected to have only a moderately negative impact on real steel consumption in 2015 and 2016. On balance, real steel consumption is forecast to increase by 1.6% in 2015 and 2.3% in 2016.

15

Apparent Consumption

Forecast for apparent consumption - % change year-on-year

Period Year 2014

Q115 Q215 Q315 Q415 Year 2015

Q116 Q216 Q316 Q416 Year 2016

3.9 -1.1 2.6 1.9 4.0 1.8 2.2 2.5 1.5 3.6 2.4

Destocking curtailed Q4-2014 demand

3.9% rise apparent consumption in 2014 absorbed by imports

EU steel market to strengthen mildly further in 2015-2016

EU mills concerned about imports gaining further market share

Apparent steel consumption in Q4-2014 fell 1.3% y-o-y following rather robust growth in the first 3 quarters of last year. The slight decline in demand basically reflects the usual destocking in the steel distribution chain and rather uncertain business expectations for end-users in the final quarter of the year. Meanwhile, imports increased 5.5% y-o-y in Q4-2014, which resulted in domestic deliveries by EU mills falling by 2.5% and a further loss of market share for domestic steel producers. This trend characterised the whole of the year 2014. While the EU steel market recovered from the slump in the 2012-2013 period, the 3.9% rise in steel demand benefited mostly third country steel suppliers. Total imports

rose almost 12% in 2014, whereas domestic shipments from EU producers rose by less than 2%. The EU steel market is expected to steadily strengthen in 2015 and 2016. The outlook for real steel consumption is moderately positive, owing to activity in most steel using sectors gaining traction. Higher activity levels at down-stream steel users imply that inven-tories in the supply chain and at end-users will need to be raised slightly. The key uncertainty for EU steel producers, however, is whether third country imports will prevent them from benefiting from the mildly positive trend in EU steel demand. For 2015 it is expected that imports will continue to rise and only in 2016 take a step back. As a consequence, domestic deliveries from EU suppliers will most likely see hardly any growth in 2015, before picking up by around 3% in 2016. All in all, apparent steel consumption in the EU is forecast to increase by almost 2% in 2015 and by around 2.5% in 2016.

EU Apparent Consumption

in million tonnes per annum

2008 187

2009 122

2010 148

2011 158

2012 141

2013 141

2014 146

2015 (f) 149

2016 (f) 153

16

Imports

Total 3rd country imports rose

12% in 2014 – finished product imports 19% up

Early 2015: imports rising further Chinese supply glut find its way

to the international markets Imports seen rising 4% in 2015 Final customs data confirm the rising trend of steel imports in Q4-2014, despite a mild reduction in actual volumes compared with the preceding quarter and a more moderate year-on-year growth rate. Total imports including semis rose 5% y-o-y, whereas finished product imports increased 9% with flat product imports 12% up and long products 1% up compared with the same period of 2013. Total steel imports in 2014 rose 12%. While semis’ imports fell 3%, finished steel imports increased 19%, with flat products rising 15% and long products 32% up compared with 2013. Imports from China, Russia, the Ukraine, South Korea and India accounted for 75% of

total finished product imports. First customs data for 2015 signal that imports in the first two months of this year remained at an elevated level. While imports in January were lower than in the same month of 2014, February imports showed again an

increase. Total finished product imports over the first two months of 2015 increased 5% y-o-y, but were 25% up on the monthly average of Q4-2014 and 7% higher than the monthly average of the whole year 2014. Particularly flat product imports were on a rising trend, rising 12% y-o-y and 31% compared with the monthly average of Q4-2014 and 12% compared with the monthly average of 2014. Especially imports from China and South Korea were on a rising trend in the first two months of this year. Finished product imports from China rose 38% compared with the monthly average of 2014, whereas imports from South Korea grew by 18%. These data clearly fuel concerns about imports remaining at an elevated level as long as excess production - mainly originating in China - is being pushed into the international markets at cut-

rate prices, thereby distorting traditional steel trade flows. As such, China’s supply glut is hurting the profitability of the global steel sector. Third country imports are foreseen to rise by almost 4% per annum in 2015. 2016 may see imports declining by almost 3%.

17

Exports

Total exports grew by just 1% in 2014

EU remained net exporter but surplus smaller than in 2013

Exports forecast to increase slightly in 2015-2016 – some support from weaker Euro

Total steel exports from the EU to third countries grew by 8% y-o-y in the final quarter of 2014. While semis exports decreased by 16% y-o-y, finished product exports were 12% up on the year earlier level as a result of a 10% rise in flat product exports and a 16% increase in long product exports. Total exports in 2014 increased by just 1%, hiding diverging trends at the product level. Semis exports decreased by 7% compared with the preceding year, while finished products exports rose 2% as a result of a 6% increase in flat product exports and a 3% drop in long product exports. Similar to the situation in 2012 and 2013, the EU was also a net exporter in 2014. However, the trade surplus narrowed to 347,000 tonnes per month compared with 556,000 tonnes per month in 2013. As in the preceding years, the trade surplus resulted from a deficit in semis (301,000 tonnes per

month), a slight surplus in flat products (118,000 tonnes) and a surplus of 530,000 tonnes per month in long products. The reduction in the net trade volume in 2014 is explained by lower net exports of both flat and long products owing to the modest improvement of demand in the EU steel market. Rebar, wire rod and beams were the most exported long steel products. The key destination for EU exports of long products was Algeria. The outlook for 2015 and 2016 is for a slight rise of EU exports to third countries. The weakened Euro is contributing to a better competitive position of Eurozone exporters on the international markets. However, the scale of potential sales is limited by fierce global competition and extremely low price levels resulting from the current distortion of traditional trade flows. This situation is seen persisting over the coming two years. EU exports are forecast to increase by around 1% in 2015 and 2% in 2016.