economic conditions in the sacramento region uli real estate outlook 2013 december 6, 2012 ryan...

TRANSCRIPT

Economic Conditions in the Sacramento Region

ULI Real Estate Outlook 2013December 6, 2012

CSER PublicationsPresented By

Ryan Sharp, CEcDCSER Director

ECONOMIC & DEMOGRAPHIC PROFILES

SITE SELECTION RESEARCH & INFORMATION

RESEARCH VALIDATION & PEER REVIEW

ECONOMIC & TAX IMPACT STUDIES

INDUSTRY STUDIES

WORKFORCE STUDIES

ECONOMIC DEVELOPMENT STRATEGIES

MARKET & FEASIBILITY ANALYSES

POLICY ANALYSIS & PROGRAM EVALUATION SUPPORT

INF

OR

MA

TIO

N

EV

AL

UA

TIO

N

CO

NS

ULT

AT

ION

CORE SKILLS:

• Economic & demographic analysis & forecasting • Regional economics & economic development

practices • Market & feasibility analysis

• Econometric & input-output modeling • Social science research & survey design

• Strategic planning & collaborative processes • Performance measurement

• Geographic Information Systems

Current Conditions

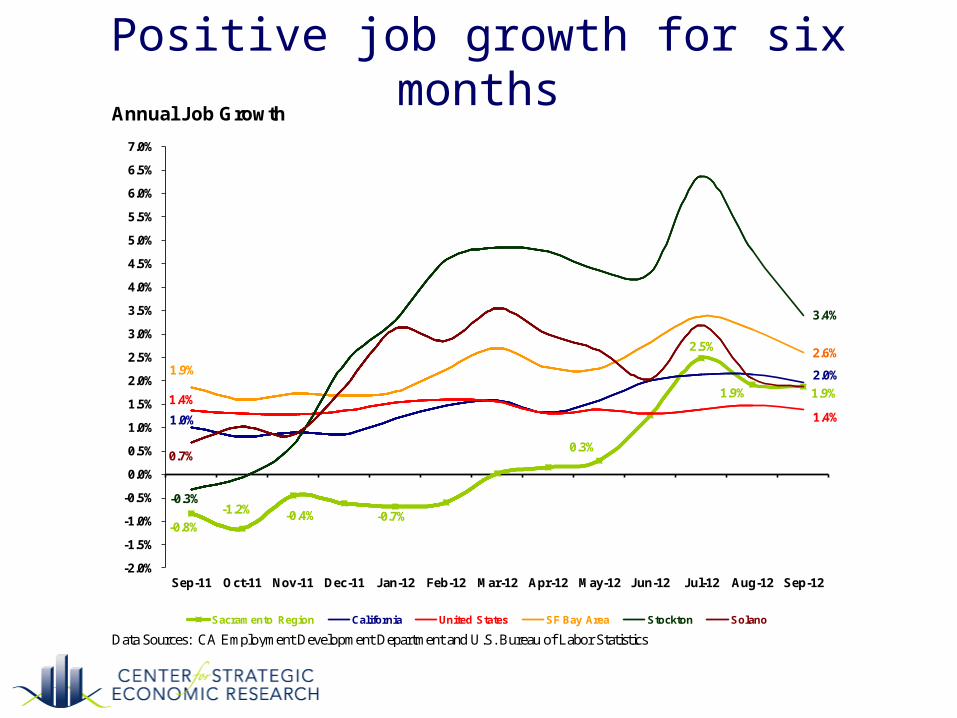

Positive job growth for six monthsAnnual Job Growth

Data Sources: CA Employment Development Department and U.S. Bureau of Labor Statistics

-0.8%

-1.2% -0.4% -0.7%

0.3%

2.5%

1.9% 1.9%

1.0%

2.0%

1.4%

1.4%

1.9%2.6%

-0.3%

3.4%

0.7%

-2.0%

-1.5%

-1.0%

-0.5%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

5.0%

5.5%

6.0%

6.5%

7.0%

Sep-11 Oct-11 Nov-11 Dec-11 Jan-12 Feb-12 Mar-12 Apr-12 May-12 Jun-12 Jul-12 Aug-12 Sep-12

Sacramento Region California United States SF Bay Area Stockton Solano

Most large sectors added jobs in past yearSacramento Region Largest Sector Annual Job Growth

Data Source: CA Employment Development Department

-1.5%-0.8%

3.9%

-0.7%

3.1%

0.8%

3.3% 3.0%

-6.0%

-5.0%

-4.0%

-3.0%

-2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

Sep-11 Oct-11 Nov-11 Dec-11 Jan-12 Feb-12 Mar-12 Apr-12 May-12 Jun-12 Jul-12 Aug-12 Sep-12

Government Prof. & Business Svcs. Trade, Trans., & Util. Leisure & Hospitality Edu. & Health Svcs.

Substantial gains in four major sectors

Major Sector Annual Job Gains and Losses

Data Source: CA Employment Development Department

Sacramento SF BaySector Region California Area Stockton Solano

Total Nonfarm 15,700 276,100 72,500 6,400 2,200Private Sector 17,500 318,300 76,200 6,900 2,500Public Sector -1,800 -42,200 -3,700 -500 -300Trade, Trans., & Util. 4,300 45,300 10,900 1,700 700Prof. & Business Svcs. 4,100 88,500 20,900 900 400Construction 3,488 25,400 7,200 200 300Edu. & Health Svcs. 3,200 56,700 16,100 1,800 500Financial Activities 1,600 21,700 -1,600 400 200Manufacturing 700 -9,000 1,100 1,200 -200Leisure & Hospitality 700 67,500 13,600 700 700Mining & Logging 12 -100 0 0 0Information -200 25,700 7,900 100 0Other Services -400 -3,400 100 -100 -100Government -1,800 -42,200 -3,700 -500 -300

September 2011-2012

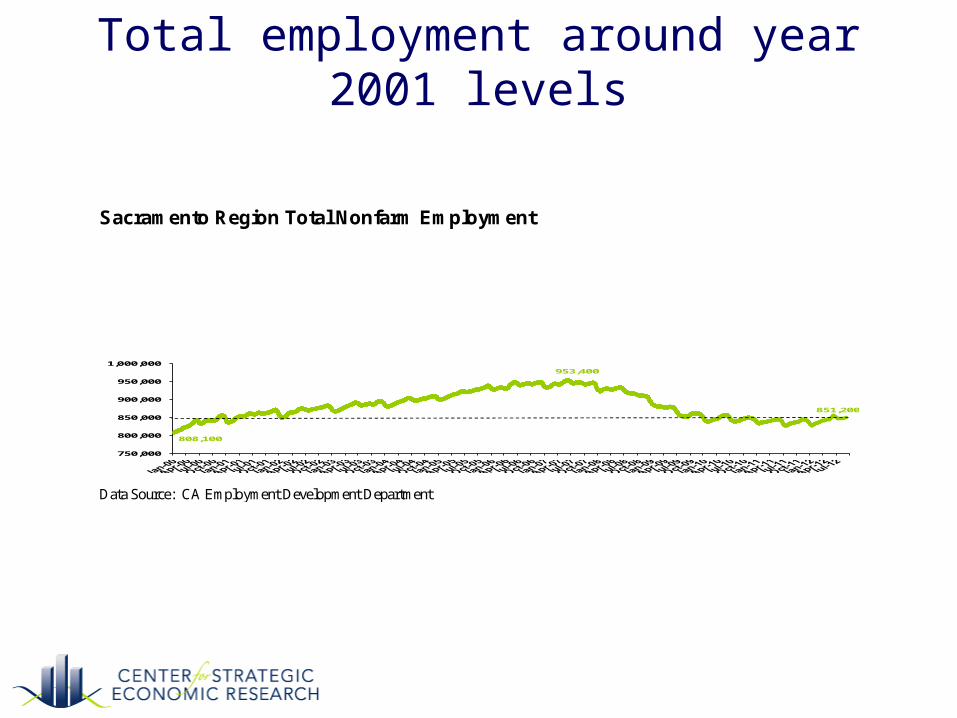

Total employment around year 2001 levels

Sacramento Region Total Nonfarm Employment

Data Source: CA Employment Development Department

808,100

953,400

851,200

750,000

800,000

850,000

900,000

950,000

1,000,000

Unemployment rate above statewide averageUnemployment Rate (Seasonally Adjusted Annual Average)

Data Sources: CA Employment Development Department and U.S. Bureau of Labor Statistics

12.8

%

12.6

%

11.3

%12.3

%

12.0

%

10.8

%

9.7%

9.2%

8.3%

10.6

%

9.9%

8.6%

17.0

%

17.2

%

15.4

%

11.9

%

11.8

%

10.4

%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

11.0%

12.0%

13.0%

14.0%

15.0%

16.0%

17.0%

18.0%

19.0%

Sep-10 Sep-11 Sep-12

Sacramento Region California United States SF Bay Area Stockton Solano

Job growth ranks in middle of state regionsAnnual Job Growth and Unemployment Rate Change

Data Sources: CA Employment Development Department and U.S. Bureau of Labor Statistics

1.4%

1.5%

1.7%

1.9%

1.9%

2.0%

2.3%

2.3%

2.6%

3.4%

-0.9%

-1.4%

-1.0%

-1.4%

-1.4%

-1.2%

-1.0%

-1.2%

-1.3%

-1.8%

-3.0% -2.0% -1.0% 0.0% 1.0% 2.0% 3.0% 4.0%

United States

Inland Empire

Los Angeles

Solano

Sacramento Region

California

San Diego

Fresno

SF Bay Area

Stockton

Unemployment Rate Change Sep 11-12 Job Growth Sep 11-12

Sacramento among fastest-growing large metro areas nationally

Moderate but declining competitive position

Economic Outlook

Leading indicators improving for nation and state

Stable growth expected for state

Regional business sentiment tapering offSacramento Region Business Confidence Index—Third Quarter 2012

Data Source: Center for Strategic Economic Research-Sacramento Business Journal Business Confidence Survey conducted between September 13, 2012 and October 3, 2012—participants were asked to provide their assessment of the Sacramento Region’s business climate and their industry for the previous and upcoming six months Note: Responses to the questions are scaled from 0 to 100 in the following manner: Substantially Better = 100; Moderately Better = 75; Same = 50; Moderately Worse = 25; Substantially Worse = 0.

37

4648

49

52

49

49

56

55

50

46

55 57

54 52

26

5153

23

5149

20

25

30

35

40

45

50

55

60

65

Q1 2009

Q2 2009

Q3 2009

Q4 2009

Q1 2010

Q2 2010

Q3 2010

Q4 2010

Q1 2011

Q2 2011

Q3 2011

Q4 2011

Q1 2012

Q2 2012

Q3 2012

Ind

ex S

core

0 t

o 1

00 (

Ove

r 50

= P

osi

tive

Per

cep

tio

ns)

Sacramento Region Business Confidence Index

BCI Industry conditions vs. 6 mo. ago

Industry conditions 6 mo. from now Sac Region conditions vs. 6 mo. ago

Sac Region conditions 6 mo. from now

Job growth expected to improveSacramento Region Annual Job Growth Outlook October 2012 to September 2013 Forecast

Data Sources: Historical from CA Employment Development Department; Forecast from CSER Business Forecast model

-0.8%

1.9%

2.8%

-1.5%

-1.0%

-0.5%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

Past 12 MonthsAverage = 0.4%

Next 12 MonthsAverage = 2.2%

Only four major sectors with negative job growth forecast

Major Sector Annual Average Job Growth Outlook Q4-12 to Q3-13 Forecast, Sorted by Sector Size

Data Sources: Historical from CA Employment Development Department; Forecast from CSER Business Forecast model

Past 12 Next 12Sector Months Months Q4-12 Q1-13 Q2-13 Q3-13

Total Nonfarm 0.4% 2.2% 1.8% 2.2% 2.4% 2.6%Government -0.7% -0.3% -0.2% -0.3% -0.6% -0.2%Trade, Trans., & Util. 1.3% 2.5% 1.9% 1.7% 2.9% 3.5%Edu. & Health Svcs. 3.4% 2.4% 1.7% 2.3% 2.0% 3.4%Prof. & Business Svcs. 0.9% 2.9% 3.8% 3.3% 2.8% 1.8%Leisure & Hospitality -2.2% 3.0% 1.9% 4.7% 2.5% 2.9%Financial Activities 2.0% 5.2% 3.3% 5.1% 6.5% 6.1%Construction -0.3% 14.3% 10.0% 16.2% 18.9% 12.0%Manufacturing -0.6% 1.1% 0.9% -0.9% 1.2% 3.4%Other Services -0.4% -0.5% -0.1% -1.6% 0.2% -0.4%Information -1.0% -1.1% -2.1% -1.3% -0.3% -0.5%Mining & Logging 0.5% -7.0% -3.5% -23.2% -4.4% 3.0%

Notable declines in unemployment anticipatedSacramento Region Unemployment Rate Outlook (Seasonally Adjusted Annual Average) October 2012 to September 2013 Forecast

Data Sources: Historical from CA Employment Development Department; Forecast from CSER Business Forecast model

12.8% 12.6%

11.3%

9.4%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

Sep-10 Sep-11 Sep-12 Sep-13

Regional Strategic Planning

nexteconomycapitalregion.org

• Leaders from Valley Vision, the Metro Chamber, SACTO, and SARTA sparked Next Economy in response to the severe regional recession

• Objective is to identify catalytic strategies along with specific actions and champions to accelerate new job creation, investment, and innovation

• The core research agenda and related findings drove the collaborative planning process

• Collaborative structure includes a leadership group, a steering committee, various work groups, three regional forums, and targeted outreach

• Tied into California Economic Summit to leverage regions in reigniting the state’s economy (caeconomy.org)

PROJECT BACKGROUND

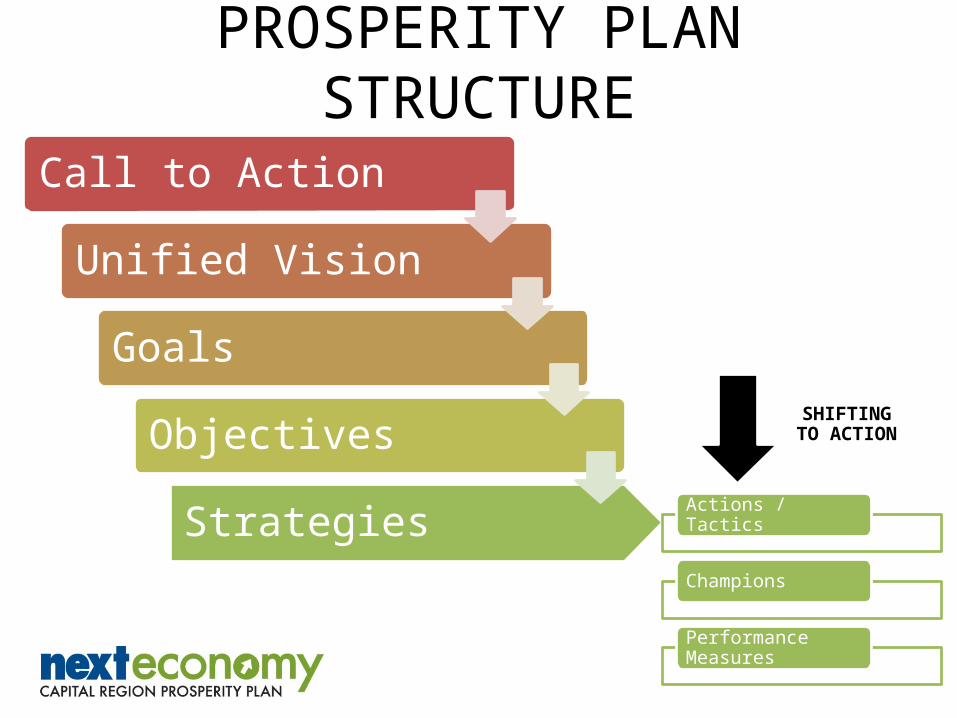

PROSPERITY PLAN STRUCTURE

Call to Action

Unified Vision

Goals

Objectives

Strategies Actions / Tactics

Champions

Performance Measures

SHIFTING TO ACTION

UNIFIED VISIONWithin five years the Capital Region

will be widely regarded as a:

Sought-after place for business

growth, investment, and

entrepreneurship

Desirable place for a quality

workforce and young

professionals to live, study, work,

and play

Diverse economy renowned for its

core business clusters and

driven in large part by export

activity

GOALS

Foster a strong innovation environment

Amplify the Region’s global market transactions

Diversify the economy through growth and support of core business clusters

Grow and maintain a world-class talent base

Improve the regional business climate for economic growth

CORE BUSINESS CLUSTERS

•37,000 jobs

•$3.5 billion output

Agriculture & Food

•11,000 jobs

•$1.7 billion output

Advanced Manufacturing

•3,000 jobs

•$850 million output

Clean Energy Technology

•17,000 jobs

•$1.1 billion output

Education & Knowledge Creation

•31,000 jobs

•$9.7 billion output

Information & Communications Technology

•99,000 jobs

•$8.6 billion output

Life Sciences & Health Services

Thank You!

Regional economic conditions have improved

Moderate competitive position

Forecast shows uptick in next 12 months

Next Economy aimed at accelerating job growth and investment