economics by jeff rubin & strategy -...

TRANSCRIPT

JeffreyRubin AveryShenfeld BenjaminTal PeterBuchanan WarrenLovely DavidBezic (416)594-7357 (416594-7356 (416)956-3698 (416)594-7354 (416)594-7359 (416)956-3219

CIBC World Markets Inc. • PO Box 500, 161 Bay Street, BCE Place, Toronto, Canada M5J 2S8 • Bloomberg @ WGEC1 • (416) 594-7000C I B C W o r l d M a r k e t s C o r p • 3 0 0 M a d i s o n A v e n u e , N e w Yo r k , N Y 1 0 0 1 7 • ( 2 1 2 ) 8 5 6 - 4 0 0 0 , ( 8 0 0 ) 9 9 9 - 6 7 2 6

Strategecon

Economics & Strategy

http://research.cibcwm.com/res/Eco/EcoResearch.html

JeffreyRubin(416)594-7357

AveryShenfeld(416)594-7356

BenjaminTal(416)956-3698

PeterBuchanan(416)594-7354

MenyGrauman(416)956-6527

KrishenRangasamy(416)956-3219

Recent announcements from OPEC andChinawon’tbesufficienttoholdoilpricesincheck.Theadditional200,000barrelsperdaypledgedfromSaudiArabiaisapittancecomparedtothefourmillionbarrelsperdaythatdepletionwillhiveoffworldproductionthisyear.Whatlittle increaseinproductionSaudi is capable of will probably all begobbledupbythatcountry’sownvoraciousappetite for energy. Nor is the $145 pertonnecut (48centspergallon) inChinesefuelsubsidieslikelytodentdemandmuch.MostNorthAmericanswouldgladlylineupatthepumpsforChina’snow$3.25agallongas,particularlythoseofuswholivenorthoftheborder.

With half of the world’s population neverhaving topayworldoilprices, it shouldn’tcome as a great surprise that $130 perbarrelcrudepriceshaveyettoquashworlddemand. And the only supply response todate has been yet another round of costoverrunsandlengthyprojectdelaysrunningthe gamut from Canadian oil sands todeepwaterGulfofMexicowells.

Withthebasiclawsofsupplyanddemandnolongeroperativeincrudeoilmarkets,wearecompelledtoonceagainraiseourtargetprices for oil.Weare liftingour target forWestTexas Intermediateby$20perbarreltoanaveragepriceof$150nextyearandby $50 per barrel to an average price of$200perbarrelby2010.Underprevailingrefinerymargins, thatshouldtranslate intoanear-$7pergallonpumppricewithintwoyears,a70%increasefromtoday’salreadyrecordlevels.

HigheroilpricesspellstagflationfortheUSeconomy next year, and we have markeddown our GDP growth forecast to barelyover1%for2009(pages9-11).Thebiggestimpactswillbeintransportandnonegreaterthantheadjustmentsontheroad.Afterall,America is the quintessential land of thecar.

Asgasolinepricesclimbinexorably,Americandrivinghabitsaregoingtohavetoundergoa massive change, mimicking the drivinghabitslongadoptedbyEuropeanswhohavefacedmuchhighergasprices.Averagemilesdriven will likely fall by as much as 15%,whilethemarketshareoflighttrucks,SUVsand vans will be literally halved, reversingthe trendof the lastfifteen years.But themost fundamental, and unprecedentedchangewillbeinthenumberofvehiclesontheroad.

Over the next four years, we are likely towitnessthegreatestmassexodusofvehiclesoffAmerica’shighwaysinhistory.By2012,there should be some 10 million fewervehiclesonAmerican roadways than therearetoday—adeclinethatdwarfsallpreviousadjustmentsincludingthoseduringthetwoOPEC oil shocks (see pages 4-8). Many ofthose in the exit lane will be low incomeAmericans from households earning lessthan $25,000 per year. Incredibly, over 10millionofthoseAmericanhouseholdsownmorethanonecar.

Soontheywon’townany.

“Over the next four years, we are likely to witness the greatest mass exodus of vehicles o f f A m e r i c a ’ s h i g h w a y s i n history. By 2012, there should be some 10 million fewer vehicles on American roadways than there are today ...”

Heading for the Exit LanebyJeffRubin

June 26, 2008

CIBC World Markets InC. StrategEcon - June 26, 2008

2

MARKET CALL

INTEREST & FOREIGN EXCHANGE RATES

Upwardrevisionstoourcallforstill-higheroilpriceswilladdtothepressureontheFedtocalminflationexpectationsbyraisingrates.BestbetsforthefirstmovearerightaftertheNovemberelections.Withinflationrunningata4%clip,takingtherealfundsratetozerowillrequirea200-bptighteningbyautumn2009,amovetheFedwillbeforcedintoevenifitmeansleavingtheeconomygrowingataslowcrawl.

TheCanadianyieldcurvepricesinalaterstartforBankofCanadatightening,whichlooksappropriategiventhehigherstartingpointforyieldsandthelowerstartingpointforCPI.ButbothinflationandrateswillbeheadedhigherastheshelteringimpactonCPIfromearlierhugeC$gainsbeginstowane.AsintheUS,ratehikeswillbegetexpectationsformoretocome,puttingpressurefurtheroutthecurve.

TheECBseemsdeterminedtothrowinaquarter-pointratehiketoshowitscoloursasaninflationfighter,amovethatmighttemporarilylifttheeurowhiletheFedbidesitstime.Butoverall,2009willbeabetteryearfortheUSdollarastheFedreducesthedollar’syielddisadvantage.TheBankofCanada’smoremodestratehikeswouldn’tdomuchfortheC$ontheirown,butshouldliftthelooniethroughparitywhenbuttressedbysoaringoilandgaspricesandrelatedM&Ainflows.

•

•

•

2008 2009

END OF PERIOD: 25-Jun Sep Dec Mar Jun Sept Dec

CDA Overnight target rate 3.00 3.00 3.00 3.25 3.50 4.00 4.0098-Day Treasury Bills 2.62 2.70 2.80 3.20 3.35 3.75 3.70Chartered Bank Prime 4.75 4.75 4.75 5.00 5.25 5.75 5.752-Year Gov't Bond (3.75% 6/10) 3.23 3.40 3.60 3.85 3.95 4.30 4.3510-Year Gov't Bond (4% 06/17) 3.71 3.85 3.95 4.00 4.10 4.35 4.4030-Year Gov't Bond (5% 06/37) 4.06 4.20 4.25 4.30 4.30 4.60 4.65

U.S. Federal Funds Target 2.00 2.00 2.25 2.75 3.25 3.75 4.0091-Day Treasury Bills 1.80 1.95 2.10 2.55 2.95 3.50 3.602-Year Gov't Note (2.875% 6/10) 2.82 2.95 3.05 3.10 3.40 3.85 4.0010-Year Gov't Note (3.875% 05/18) 4.11 4.20 4.30 4.35 4.45 4.60 4.6530-Year Gov't Bond (4.375% 02/38) 4.65 4.75 4.80 4.80 4.80 4.80 4.90

Canada - US T-Bill Spread 0.82 0.75 0.70 0.65 0.40 0.25 0.10Canada - US 10-Year Bond Spread -0.40 -0.35 -0.35 -0.35 -0.35 -0.25 -0.25

Canada Yield Curve (30-Year — 2-Year) 0.83 0.80 0.65 0.45 0.35 0.30 0.30US Yield Curve (30-Year — 2-Year) 1.83 1.80 1.75 1.70 1.40 0.95 0.90

EXCHANGE RATES — (US¢/C$) 99.0 100.0 103.1 105.3 101.5 102.0 101.5— (C$/US$) 1.011 1.000 0.970 0.950 0.985 0.980 0.985— (Yen/US$) 108 105 108 102 97 96 94— (US$/euro) 1.57 1.59 1.56 1.50 1.49 1.49 1.50— (US$/pound) 1.98 1.99 1.96 1.90 1.90 1.88 1.90— (US¢/A$) 95.9 96.5 93.0 92.5 91.0 92.0 93.0

CIBC World Markets InC. StrategEcon - June 26, 2008

�

STRATEGY AND EARNINGS OUTLOOK

•

•

•

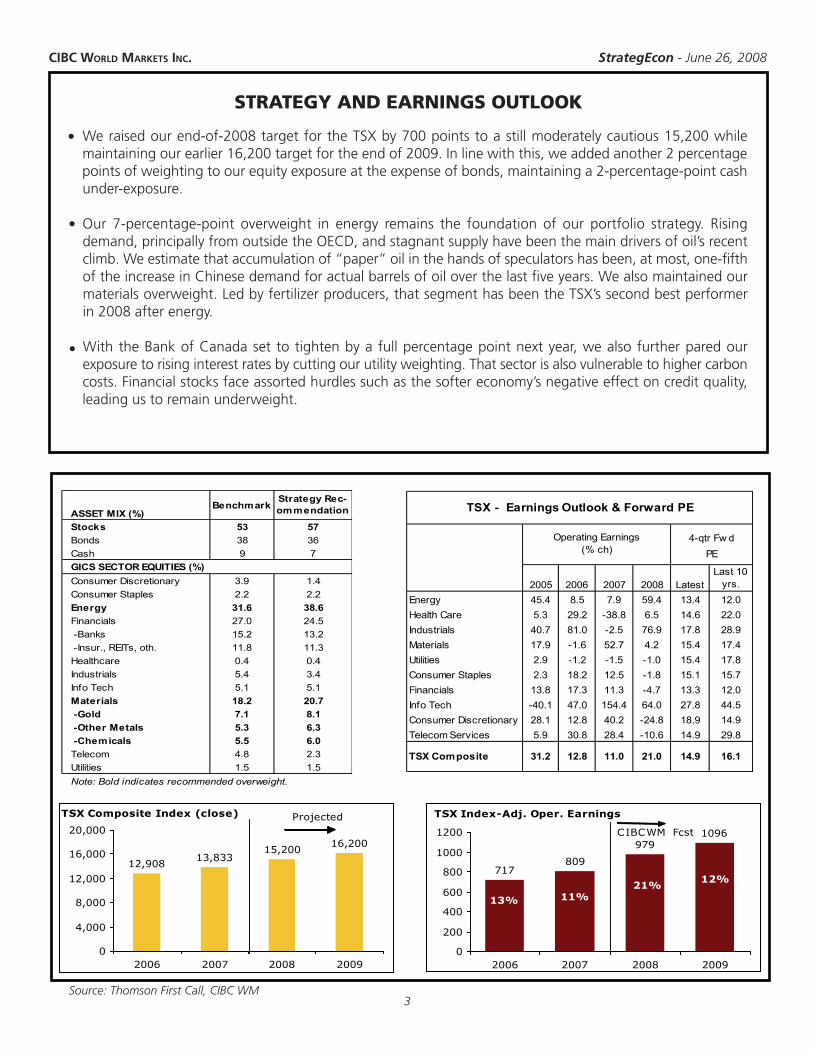

Weraisedourend-of-2008targetfortheTSXby700pointstoastillmoderatelycautious15,200whilemaintainingourearlier16,200targetfortheendof2009.Inlinewiththis,weaddedanother2percentagepointsofweightingtoourequityexposureattheexpenseofbonds,maintaininga2-percentage-pointcashunder-exposure.

Our 7-percentage-point overweight in energy remains the foundation of our portfolio strategy. Risingdemand,principallyfromoutsidetheOECD,andstagnantsupplyhavebeenthemaindriversofoil’srecentclimb.Weestimatethataccumulationof“paper”oilinthehandsofspeculatorshasbeen,atmost,one-fifthoftheincreaseinChinesedemandforactualbarrelsofoiloverthelastfiveyears.Wealsomaintainedourmaterialsoverweight.Ledbyfertilizerproducers,thatsegmenthasbeentheTSX’ssecondbestperformerin2008afterenergy.

WiththeBankofCanadasettotightenbyafullpercentagepointnextyear,wealsofurtherparedourexposuretorisinginterestratesbycuttingourutilityweighting.Thatsectorisalsovulnerabletohighercarboncosts.Financialstocksfaceassortedhurdlessuchasthesoftereconomy’snegativeeffectoncreditquality,leadingustoremainunderweight.

Source: Thomson First Call, CIBC WM

2005 2006 2007 2008 LatestEnergy 45.4 8.5 7.9 59.4 13.4Health Care 5.3 29.2 -38.8 6.5 14.6Industrials 40.7 81.0 -2.5 76.9 17.8Materials 17.9 -1.6 52.7 4.2 15.4Utilities 2.9 -1.2 -1.5 -1.0 15.4Consumer Staples 2.3 18.2 12.5 -1.8 15.1Financials 13.8 17.3 11.3 -4.7 13.3Info Tech -40.1 47.0 154.4 64.0 27.8Consumer Discretionary 28.1 12.8 40.2 -24.8 18.9Telecom Services 5.9 30.8 28.4 -10.6 14.9

TSX Composite 31.2 12.8 11.0 21.0 14.9

Last 10 yrs.

TSX - Earnings Outlook & Forward PE

PE4-qtr Fw dOperating Earnings

(% ch)

12.022.028.917.4

14.929.8

16.1

17.815.712.044.5

717809

9791096

0

200

400

600

800

1000

1200

2006 2007 2008 2009

CIBCWM Fcst

TSX Index-Adj. Oper. Earnings

12%

13%

21%11%

15,20016,200

12,90813,833

0

4,000

8,000

12,000

16,000

20,000

2006 2007 2008 2009

TSX Composite Index (close) Projected

ASSET MIX (%)Benchmark

Strategy Rec-ommendation

Stocks 53 57Bonds 38 36Cash 9 7GICS SECTOR EQUITIES (%)Consumer Discretionary 3.9 1.4Consumer Staples 2.2 2.2Energy 31.6 38.6Financials 27.0 24.5 -Banks 15.2 13.2 -Insur., REITs, oth. 11.8 11.3Healthcare 0.4 0.4Industrials 5.4 3.4Info Tech 5.1 5.1Materials 18.2 20.7 -Gold 7.1 8.1 -Other Metals 5.3 6.3 -Chemicals 5.5 6.0Telecom 4.8 2.3Utilities 1.5 1.5Note: Bold indicates recommended overweight.

CIBC World Markets InC. StrategEcon - June 26, 2008

�

We stand at a turning point for US transport. Realgasoline prices have already surpassed the peak levelsthat followed the second OPEC oil shocks, and evenwhenadjustedforpotentialfuelefficiencyimprovements,haveincreasedtothepointwheretheywilldramaticallychangedrivingbehaviourinAmerica.

The some 57 million Americans who own a car andhavedirect access topublic transportationwill start toactmoreandmorelikeEuropeans,whohavelongpaidmuch higher gasoline prices. By 2012, average milesdriven will have shrunk by more than 15%. SUV andother light trucksales,whichuntil2006accountedforalmost 60% of total motor vehicles, will plummet toless thanhalf that level, reversing the lastfifteenyearsgrowthinmarketshare.

More fundamentally, the freeways are about to getless congested. Not only will the number of vehicleregistrations in the United States not grow over thenextfouryears,butby2012thereshouldberoughly10millionfewervehiclesontheroadinAmericathantherearetoday.

Forthepasthalfcentury,Americahasspentthebulkofits infrastructuremoneyonbuildinghighways—onlytoseethatsoon,$7pergallongasolinepriceswillleadtofewerandfewerpeopleusingthem.

GettingOfftheRoad:Adjustingto$7perGallonGasinAmerica

JeffRubinandBenjaminTal

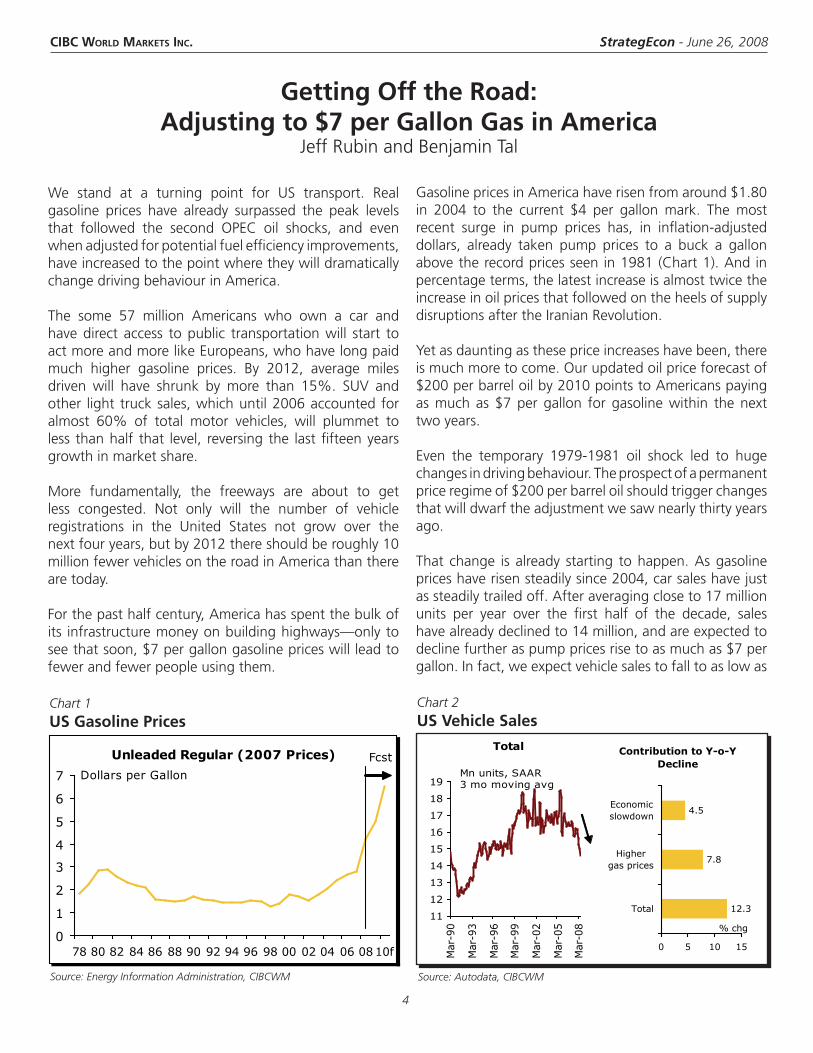

GasolinepricesinAmericahaverisenfromaround$1.80in 2004 to the current $4 per gallon mark. The mostrecent surge in pump prices has, in inflation-adjusteddollars, already taken pump prices to a buck a gallonabovetherecordpricesseenin1981(Chart1).Andinpercentageterms,thelatestincreaseisalmosttwicetheincreaseinoilpricesthatfollowedontheheelsofsupplydisruptionsaftertheIranianRevolution.

Yetasdauntingasthesepriceincreaseshavebeen,thereismuchmoretocome.Ourupdatedoilpriceforecastof$200perbarreloilby2010pointstoAmericanspayingasmuchas$7pergallon forgasolinewithin thenexttwoyears.

Even the temporary 1979-1981 oil shock led to hugechangesindrivingbehaviour.Theprospectofapermanentpriceregimeof$200perbarreloilshouldtriggerchangesthatwilldwarftheadjustmentwesawnearlythirtyyearsago.

That change isalready starting tohappen.Asgasolinepriceshaverisensteadilysince2004,carsaleshavejustassteadilytrailedoff.Afteraveragingcloseto17millionunits per year over the first half of the decade, saleshavealreadydeclinedto14million,andareexpectedtodeclinefurtheraspumppricesrisetoasmuchas$7pergallon.Infact,weexpectvehiclesalestofalltoaslowas

Chart 2USVehicleSales

Chart 1USGasolinePrices

Source: Energy Information Administration, CIBCWM Source: Autodata, CIBCWM

Unleaded Regular (2007 Prices)

0

1

2

3

4

5

6

7

78 80 82 84 86 88 90 92 94 96 98 00 02 04 06 08 10f

Dollars per Gallon

FcstTotal

11

12

13

14

15

16

17

18

19

Mar

-90

Mar

-93

Mar

-96

Mar

-99

Mar

-02

Mar

-05

Mar

-08

Mn units, SAAR3 mo moving avg

Contribution to Y-o-Y Decline

12.3

7.8

4.5

0 5 10 15

Total

Highergas prices

Economicslowdown

% chg

CIBC World Markets InC. StrategEcon - June 26, 2008

�

Chart �SurgingGasolineCosts

11millionunitsby2012,thelowestlevelsincetheearly1980s.While someof the currentweakness in vehiclesalescanbeattributedtotheeconomicslowdown,weestimate that higher gasoline prices have had almosttwicetheeffect(Chart2).

Tumblingcarsalesandmoreprudentdrivinghabitsarealready starting to hit fuel demand. Overall gasolinedemandintheUnitedStateshasfallensharplysincethebeginningoftheyearandisheadedforthefirstannualdrop in 17 years. Per capita consumption has fallenby close to5%since2004 (Chart 3), and, like vehiclesales,willcontinuetodeclineaslongasgasolinepricescontinuetorise.

WhileAmericansarebuyinglessgasoline,unfortunately,the reduction in quantity is not keeping up with theincrease in price. Hence, even with chastened drivinghabits, most Americans are spending more on fillingtheirtanksandlessoneverythingelse.Overthelastfouryears,gasolinesaleshavegrownfivetimesasmuchasthe rest of retail sales in the United States (Chart 4)1.And at that rate, gasoline will take over grocery storespending2asthelargestiteminhouseholds’non-vehicleretailspendingbylatenextyear(Chart5).

USversusEurope

Atthesoon-to-be$6to$7pergallonrangeforgasolinepriceswecanexpecttoseesomequantumshiftsindrivingbehaviourinAmerica.Andtoseewherethoseshiftswillbegoing is relativelyeasy.Allwehavetodo is lookat

Chart �GasolineConsumptionPerCapita

Europe,whereevenattoday’sworldoilprices,driversarealreadypayingtheequivalentofthosegasolinepricesormore.Infact,inmanyplacesinEurope,theyarepayingwellabovethatandhavebeenforsometime.

Compare for example, drivingbehaviour in theUnitedKingdom with driving behaviour in the United States.Over90%ofAmericanhouseholdsuseacartogettowork,whileover60%ofUShouseholdsowntwocarsor more (Table 1). By comparison, just 60% of Britishhouseholdsuseacartogettowork,whilelessthan25%owntwoormorecars.Moreover,Americansdrivetheircarsmore.TheymakefourdrivingtripsadaywhileBrits

Source: Consumer Federation of America, CIBCWM

Source: US Census Bureau, Federal Highway Administration, CIBCWM

1st Quarter

96

100

104

108

112

97 98 99 00 01 02 03 04 05 06 07 08

Index 1997=100

Retail Sales

90

110

130

150

170

190

04 05 06 07 08

Gasoline Others

Index 2004=100

Spending on Gasoline Per Vehicle

0.4

0.9

1.4

1.9

2.4

2.9

3.4

92 94 96 98 00 02 04 0608f10f

$000s

Fcst

Chart �GasolineSpendingWillSoonOvertakeGroceries(monthlyaverages)

Source: US Census Bureau, CIBCWM

10

20

30

40

50

60

70

80

03 04 05 06 07 08 09f 10f 11f 12f

Gasoline Stations Food & Beverage Stores

$ Billion

CIBC World Markets InC. StrategEcon - June 26, 2008

6

Source: EMBARQ, CIBCWM

makehalf of thatperday.And last, butbynomeansleast,some30%ofBritsdon’tevenhaveacar.IntheUSlessthan10%ofhouseholdsdon’townacar.

Gasoline consumption is ultimately about how manypeople drive, the distance they drive and the type ofvehiclestheydrive.OnallthreecountsAmericanfaceamassivechange.

Adding the first two factors we get an index of milesdriven.Andpercapita,Americansdrive twiceasmuchasdrivers inSweden,UK,Germany,andFrance,wheregasolinepricesarenowover$8pergallon(Chart6).

Ofcoursetheflipsideofthisequationispublictransit.America’s obsession with the car is mirrored in itsavoidanceofpublictransit.Whenitcomestotakingthetrain,bus,orsubway,theUSranksthelowestamongOECDcountries, just as it ranks the highest among the samegroupwhenitcomestotheuseofthecar(Chart7).

DrivingLessinSmallerVehicles

Higher oil prices will make drivers use their cars less.While Americans are already driving 11 billion fewermiles than they did last year, a decline of 4.3%, theystilldrive todayabout30%more thantheydidbeforetheOPECoilshocks.Theelasticityofdrivingtogasolinepricesisestimatedtobearoundthe0.06.Thatmeansa10%riseingasolinepriceswilleventuallyleadtoa0.6%reductioninmilesdriven.Usingthatruleofthumb,the280%cumulativerise ingasolinepricesbetween2004andourtarget$7pergallontargetpriceshouldinducemorethan15%reduction inmilesdrivenonAmericanroads(Chart8).Thatwillturnbacktheclocktothemid1980sasfarasaveragemileagedrivenisconcerned.

Not only will Americans drive less but they will startto drive very different vehicles from the ones they arecurrently driving. Light trucks, which include vans andtheubiquitousSUV,accountedforasmuchas60%oftotalvehiclesalesinAmericabackin2006.That’salmosta doubling in its market share since the early 1990s(Chart9).Butevenat$4pergallongasoline,SUVsalesareplunging.At$7pergallonpumpprices,theirshareoftotalvehiclesales,alongwithother lighttrucks,will

Chart 7PrivateVehiclesversusPublicTransit

Chart 6GasPricesandDriving—AnInternationalPerspective

Table 1DailyTravelCharacteristics

Source: Giuliano & Dargay (200�), CIBCWM

United States

United Kingdom

Used car to get to work (%) 90.4 61.8

Total distance travelled (miles) 20.9 7.0

Number of trips 4.0 2.0

No cars in household (%) 8.0 30.6

2 cars or more in household (%) 61.9 24.7

0

2

4

6

8

10

12

14

4 5 6 7 8 9 10 11

Gasoline Prices ($/Gallon)

Avera

ge T

ravel Per

Vehic

le

(mile

s)

US

Canada

Australia

Germany/UK

Sweden

France

Source: OECD, US Census Bureau, CIBCWM

Rail, Buses & Coaches

-50 50 150 250

Japan

Italy

Sweden

France

Germany

Spain

UK

US

mn passenger

miles/100,000 Persons

Private Vehicles

0 500 1000 1500

US

Italy

France

UK

Sweden

Germany

Spain

Japan

mn passenger

miles/100,000 Persons

1,338

CIBC World Markets InC. StrategEcon - June 26, 2008

7

haveevenfallenbelowlevelsseenoverfifteenyearsago.While therewill stillbehouseholdswhowillbuy thesevehicles,allof thegains inmarketshareseenover thelastdecadewillhavebeenfullyreversed.

GettingOfftheRoad

Inpart,Americanswillrespondtorecordhighgasolinepricesbydriving lessandbydrivingmorefuelefficientvehicles.Butthemostdramaticresultwillbethatroughlytenmillionvehicleswillcomerightofftheroad.

Aswithoil,thereisadepletionrateinautos.It’scalledthe scrappage rate, and it refers to the percentage ofexistingvehiclesthateveryyearareretiredfromservice.

Lastyearthescrappageratewas5.2%3,resultinginsome12millionvehiclescomingofftheroad.Thatmeansnewvehiclesaleshadtoriseby12millionunitsjusttokeepthe stock of passenger vehicles unchanged. We knowfrom history that the scrappage rate rises with surgesinoilprices,becauseoldercars typicallyaveragemuchpoorerfueleconomythannewercarsandthusbecomeincreasinglyexpensivetorunaspumppricesrise.At$7pergallongasolinewehaveassumedthatthescrapraterisesmodestlyto6%.

A 6% scrappage rate would take roughly 14 millionvehicles off the road every year. For the number ofvehicle registrations to remain constant in the faceof that decline, there would have to be an offsettingnumberofnewvehicle sales that year. Butgiven theirlinktofuelprices,newvehiclesaleswillbeatleastthreemillionbelow thatnumberby2012.Ourprojected11mnvehicle sales in2012will be the lowest level sincetheearly1980s.Summingupthecumulativedifferencebetween new sales and scrappage over that periodsuggeststhatsomewhere intheneighbourhoodoftenmillionAmericanswillbecomingofftheroadoverthenext4½years(Chart10).

Isthisarealisticestimate?While$7pergallongasolineprices certainly took people off the road in Europe,you cannot simply impose Europe on America. MostEuropeanshave access topublic transport by virtueofthe broad infrastructure policies European countrieshavepursued.Inmarkedcontrast,Americabuiltmassivehighwaysandfreewaysforapopulationthatownedandusedtheirowncarstogetaround.

Chart 10NumberofVehiclesToFallby10Millionby2012

Chart 9PlungingSUVSales

Source: R.L. Polk Co., Federal Highway Administration, CIBCWMSource: Autodata Corporation, CIBCWM

Chart 8AmericansWillSoonDriveLess

Source: Federal Highway Administration, CIBCWM

8.0

8.5

9.0

9.5

10.0

10.5

11.0

11.5

12.0

12.5

70 76 82 88 94 00 06 12f

Fcst

Average travel per vehicle('000 miles)

Auto Scrapping vs. Sales

8

10

12

14

16

18

05 07 09f 11f

Number of cars scrappedNew auto sales

million

cumulativegap = 10 mn cars

Number of Vehicles

120

140

160

180

200

220

240

80 84 88 92 96 00 04 08 12f

million

Fcst

Light truck as a share of Total Vehicle Sales

2630343842465054586266

92 94 96 98 00 02 04 06 08 10f 12f

%

CIBC World Markets InC. StrategEcon - June 26, 2008

8

Chart 12CarOwnershipandSpendingByIncome

Source: Consumer Federation of America, BTS, CIBCWM

Chart 11AccessToPublicTransportation

Hencewemustnarrowour focuson thoseAmericanswhereaEuropeanstyleshiftindrivinghabitsiscurrentlyfeasible.Peoplecan’t simplyabandon theircars if theyhavenoothermeansofgettingaround,particularly intermsofgettingwork.Theremustbeat leastapublictransportalternative.

Asitturnsout,roughly57millionAmericanhouseholdsthat own a vehicle have reasonable access to publictransit4, slightly more than half of the number ofhouseholdswhoownavehicle(Chart11)5.Andapplyingthe80%vehicleownershiprateseen inEuropetothistarget group suggests a 10 million reduction in thenumberofregisteredvehiclesintheUS.

Wherewillthisdeclinecomefrom?Thefocusisonthosewho can least afford to operate a car when gasolinecosts $7per gallon.No less than80%of low incomeAmericans (or roughly24millionhouseholds)with lessthan$25,000annual incomeownacar.Withgasolinebillssurgingtorecordhighs,theywillbethefirsttocomeofftheroad.

OneinfiveofthoselowincomeAmericans,orroughlyfivemillionhouseholds,willprobablystopdrivingorgiveupthesecondvehicle6.Andagoodpartofthepreviouslynotedincreaseinthescrappagerateislikelytocomefromthis group, particularly the 30% of households under$25,000annual incomewhoownasecondcar,whichis likelyagas-guzzlingnear-wreck.Thevastmajorityof

these individualswill live in thecityasopposed to thesuburbs,giventheirmuchgreateraccesstopublictransit(Chart12)7.

Ouranalysissuggeststhatabouthalfofthenumberofcarscomingoff theroad in thenext fouryearswillbefromlowincomehouseholdswhohaveaccesstopublictransit.Attheircurrentdrivinghabits,fillingupthetankwillhaverisenfromabout7%oftheirincometo20%,anincreasethatwillseemanystarttakingthebus.

Note:

1. The AAA 2007 edition of “Your Driving Cost” concluded that the cost of owning a car has reached a record high in 2007. Given that this estimate was based on a cost of only $2.9� per gallon, the current figure is most likely higher.

2. Food and beverage stores only.

�. Source: R. L. Polk & Co. “The Vehicle Population Report 2007”. Note that the median age of a passenger car is currently 9 years—tying a record high in 2006.

�. Usually a reasonable access is defined as less than half a mile distance from a bus or train station.

�. Based on statistics obtained from the US Census Bureau, METRANS and Bureau of Transportation Statistics.

6. These estimates are consistent with survey-based findings published by METRANS regarding the role of public transportation in the mobility of low income households.

7. Based on US Census Bureau. Also see The Center on Urban and Metropolitan Policy discussion regarding “The State of Low-Wage Workers”.

Spending on Gasoline BY Household Income

0

5

10

15

20

25

99 01 03 05 07 09e

<$25k $100k+

Fcst% of income

No. of vehicles <$25k $100k+

% %

0 19.5 1.3

1 47.9 9.6

2 22.2 48.2

3 or more 10.4 40.9

Household Income

Source: US Census Bureau, METRANS, Bureau of Transportation Statistics, CIBCWM

%withAccessto

PublicTransport

75%

50%

25%

No. of Households with Cars

0 20 40 60

Metro

Suburb

Rural

mn

Totalno.of

Households

withCars

andAccess

toPublic

Transport

=57.4mn

CIBC World Markets InC. StrategEcon - June 26, 2008

9

It’s hard to be sanguine about America’s economicoutlook in the faceof ever increasing fuel costs.Afterall, nine out of the last 10 US recessions have beenaccompaniedby sharp spikes in thepriceof crudeoil.True,theeconomydidmanagetoweatherthestormofrisingoilpricesfrom2001to2005,aperiodinwhichthepriceofpetroleumshotupbyroughly180%evenastheUSeconomygrewbycloseto3%ayear.Somesawthisasasignofalastingbreakdowninoil’sthreattogrowth,citingthemoreefficientuseofenergyresources,deeperfinancialmarkets,andmoreflexiblelaboragreements.

Butthemorerecentoilupturn,inwhichcrudepriceshaveclimbedbyover130%sincethebeginningof2007,lookstobetakingavisiblebiteoutofgrowth(Chart1).Andamorecarefulanalysisofthepastrelationshipbetweenoil andgrowth suggests that thereweregood reasonsfortheeconomy’sinitialresilience,andthatmostoftheeconomicshockliesahead,puttingtheUSeconomyontrackforacaseofstagflationin2009evenasthehousingshockpetersout.

RedefininganOilShock

Oilpricesandeconomicgrowtharenotpartofasimpleone-way causal relationship. As was true of the largeoilspikesofthe1970sandearly1980s,thetimingand

OilandGrowth:That70sShowRe-RunAveryShenfeldandMenyGrauman

Chart 1OilPricesHelpSlowUSRealGDPGrowth

magnitudeoftheshocktogrowthisaffectedbythestateoftheeconomyatthetimeithits,themonetarypolicyresponse,thepaceofoil’sclimb,andasnotedbyenergyeconomist JamesHamilton, thedegreetowhichpricesbegintoeclipsepeaklevelsoverthepriorthreeyears.

Hamiltonshowedthatincreasesinoilpricesthatsimplyreversepreviousdeclinesdonothavethesameeconomicimpact as identical price gains from already elevatedlevels.Bythisstandard,someverylargespikesinoilpricesoverthelast50yearsdonotreallyqualifyasoilshocksatall (Chart2),beingsimplyreboundsfromtemporarycrudepricedipsthathadyettofiltertheirwayintotheeconomyatlarge.Forexample,althoughoilpricesshotupmorethan25%inthefirstquarterof1989,theywerestillbelowtheirpreviousthree-yearhigh.

Similarly, the economic hit during oil’s rise in the firsthalf of2007wasminimizedas crude’s climb from thenear$50/bbllevelsimplyreverseditsearlierdip.Instead,Hamilton’smodelsuggeststhatgiventhetypicalresponselags,thegreater impactongrowthliesaheadin2009.Theselagscapturenotonlythespreadingimpactoftheinitialshocktoothersectorsashigheroilcostsaffectjobcreationinthemostsensitivesectors,butalsotheimpactofthesubsequentinterestratehikesasthecentralbankrespondstotheinflationthreatbyraisinginterestrates.

Recessions are shaded.

Chart 2SomeOilPriceGainsDidn'tSetNewHighs

-30

-20

-10

0

10

20

30

2Q1982 1Q1989 2Q1994 1Q2003

Unadjusted (q/q % change)Adjusted (% change versus previous 3-year high)

WTI oil prices

0.0

1.0

2.0

3.0

4.0

04 05 06 07 08 090

20

40

60

80

100

120

140

160

Real GDP Growth, % (LHS)

Avg WTI Oil, $US/bbl (RHS)

CIBC World Markets InC. StrategEcon - June 26, 2008

10

the $150 bn in planned direct consumer stimulus willhavegonetopayforhighercosts for fuel, ratherthanincreasesinoverallspendingvolumes(Chart5).

Moreover,oneoftheearlierargumentsforwhyoilmightmatter less these days is rapidly disappearing. Untilrecently, it was commonplace to dismiss the oil shockby pointing to the fact that the US economy, with itsshift intoservices,hadbecomesignificantly lessenergyintensivethanitwasinthe1970s,whenoilshocksdidsomuchdamage.ButalthoughUScrudeoilexpendituresmadeuponly4%ofGDPlastyear,thissharewillgrowto9.5%overthenextthreeyearsascrudepriceshitanaverageof$200/bblin2010(Chart6).Intermsofoil’sshare of spending, we’re right back where we startedfrom.

As a result, applying that model shows that after aminimalshockto2008growth,ourforecastforafurtherclimbtoanaverage$150/bblnextyearwillpare2009realGDPgrowthby2.0-2.5%points,relativetoabasecaseofflatoilpricesandaresultingmoremoderatecourseforinterestrates.Thatwillturnwhatmighthavebeenabrisk3%+recovery fromthisyear’shousing-related troublesintoananemicexpansion.

It’snot that thishasbeen the steepest shock to crudeoilonrecord.Indeed,measuredagainstarollingthree-year high, so far this year oil prices have not climbedat anywhere near the speed that they did during theearly 1970s (Chart 3). But past shocks were oftenshort-lived, as they related to temporary disruptions insupply,includingthoseengineeredbyOPEC.Thismorefundamentally driven oil upsurge should prove to bemuchmorepersistentthanatanyothertimeinhistoryasbothrealandnominaloilpricescontinuetobreakalltimerecords(Chart4).ThelongestrunningcontinuousoilspikeinUShistorylastedsevenquarters,whileweexpectoilprices,atleastonatrendbasis,tobeheadedhigherrightthrough2012.

BehindtheMath

While the model’s forecast of a 2-2.5%-point growthshock simply reflects past sensitivities, on the groundrealitiesalsoareconsistentwithsluggishgrowthaheadfor 2009. Note that this year, consumer spending isbeingtemporarilyproppedupbybillionsintaxrebates.Butdon’texpectthatone-offmeasuretohavealastingimpactongrowth,inpartbecauseit’sbeingcannibalizedbyrisinggasolineprices.Alreadythisyear,nearlyhalfof

Chart �GasolineSpendingTakesHalfofStimulusFunds

0

20

40

60

80

100

120

140

160

Jan.

08

Feb.

08

Mar.0

8

Apr.0

8

May.0

8

June

.08

Stim

ulus

Pac

kage

$ bn, cummulative increase in gasoline spending

Chart �OilPriceSetsRecordinRealTerms(2008$s)

-

20

40

60

80

100

120

140

160

Q1.60 Q1.67 Q1.74 Q1.81 Q1.88 Q1.95 Q1.02

Real WTI oil Nominal WTI oil

$US/bbl, quarterly avg.

$92

Q2f:$122

Chart �ALongerRunofNewHighsinOilthisTime

-

5

10

15

20

25

30

35

40

Q1.70 Q1.77 Q1.84 Q1.91 Q1.98 Q1.05

chg in WTI oil price from 3-yr high, %

Fcst90

85

CIBC World Markets InC. StrategEcon - June 26, 2008

11

Chart 6OilIntensityisOntheRise

Indeed, it’s not just how much oil drains initially fromconsumerorbusinessfinancesorreducesenergyuse,buttheadjustmentcoststotheeconomyfromtheresultingsharpchangesinbehavior.That’salreadybeingseenashundreds of thousands of auto-related jobs disappearwiththemeltdowninlighttrucksales, longbeforetheeconomy can replace them with activity in producingmoreenergy-efficienttransportationalternatives.Theoilshockwillsimilarlyhaverippleeffectsonairlines,tourismandothersectors.

Another‘thistimewillbedifferent’argumentnotesthatthe1970soilshockswerecausedbysupplydisruptionsthathurtglobalgrowth,whilethepresentcrudeoilrun-upwasinitiallydrivenbyhealthyglobalgrowththatisinitselfabenefittotheUSeconomy.Todate,thathasforthemostpartbeenthecase,andhasbeenreflectedinabullmarketforUSexports.

But in addition to rapid economic growth in thedeveloping world, recent crude prices also capture anoutrightdeclineincrudeoilsupplyfrom2005to2007,and much more limited medium term supply growthprospects than were available in earlier decades (seeOccasional Report #6�).SupplydisruptionsinNigeriaanddecliningRussianproductionwill easilyoutweighwhatSaudiArabiaplans toadd in thenear term.Moreover,whileweexpectgrowthtoholdupwellinthedevelopingworld,theoilshockwill,withsimilarlags,takeabiteoutofactivityinUStradingpartnersinEurope.

OilTakesHousing’sPlace

Butthemostimportantreasonforthinkingthatthemajorhittogrowthliesaheadrestsontheresponseinmonetarypolicy.Asanumberofprominenteconomists,includingBen Bernanke himself, have pointed out, the impactof some of the biggest oil shocks were exacerbatedby aggressive Fed tightening. The 1973-74 oil shock,inparticular,wasmadeworseby the Fed’sdecision tobelatedly raise the fed funds rateby830bpsover thespanoflessthanthreeyears(Chart7,left).Thelast30yearslargelycoincidedwithstableinflationexpectations,whichmeantthatcentralbankerscouldavoidaggressivelyraising rates in the face of climbing energy prices.Unfortunately,forthefirsttimesincetheearly1980s,thatappearstobechanging,asconsumerinflationcontinuestoheatupandtheFedcomesunderincreasingpressuretoact.

At a minimum, once the worst of the housing shockpasses,theFedwillbeforcedtoraiserealinterestratesbacktozeroinordertopreventanimprovingeconomyfromallowingwagesandotherpricestocatchuptooil.With CPI trending at an energy- and food-driven 4%,thatwillentail200basispointsintighteningtogettoa4%fundsratebytheendofnextyear.Asaresultofourupwardrevisedcallforbothoilandinterestrates,we’vechoppedourUSgrowthforecastfor2009fromjustover2%asoftwomonthsago,tolittleover1%,nobetterthan this year’shousing-bluntedperformance. TheUSeconomyhasmanagedtoavoidfeelingthefullbruntofoilpricesoverthelastfewyears,but2009willbetheyearthatitsluckrunsout(Chart7,right).

Chart 7OilShocksPushInterestRatesHigher

0%

2%

4%

6%

8%

10%

1973 1977 1981 1985 1989 1993 1997 2001 2005 2009

Fcst

US oil expenditures as share of GDP

2

4

6

8

10

12

14

Q4.70

Q3.71

Q2.72

Q1.73

Q4.73

Q3.74

Effective fed funds rate

WTI oil, $US qtly avg

%

0

1

2

3

4

5

Q1.08 Q3.08 Q1.09 Q3.0980

100

120

140

160

180

Target fed funds rate (LHS)

WTI oil, $US qtly avg (RHS)

%

CIBC World Markets InC. StrategEcon - June 26, 2008

12

CANADA

ECONOMIC UPDATE

UNITED STATES

ConflictsofInterest:CIBCWorldMarkets’analystsandeconomistsarecompensatedfromrevenuesgeneratedbyvariousCIBCWorldMarketsbusinesses,includingCIBCWorldMarkets’InvestmentBankingDepartment.CIBCWorldMarketsmayhavealongorshortpositionordealasprincipalinthesecuritiesdiscussedherein,relatedsecuritiesorinoptions,futuresorotherderivativeinstrumentsbasedthereon.Thereadershouldnotrelysolelyonthisreportinevaluatingwhetherornottobuyorsellthesecuritiesofthesubjectcompany.LegalMatters:Thisreportisissuedandapprovedfordistributionby(i)inCanadabyCIBCWorldMarketsInc.,amemberoftheIDAandCIPF,(ii)intheUK,CIBCWorldMarketsplc,whichisregulatedbytheFSA,and(iii)inAustralia,CIBCWorldMarketsAustraliaLimited,amemberoftheAustralianStockExchangeandregulatedbytheASIC(collectively,“CIBCWorldMarkets”).ThisreportisdistributedintheUnitesStatesbyCIBCWorldMarketsInc.andhasnotbeenreviewedorapprovedbyCIBCWorldMarketsCorp.,amemberoftheNewYorkStockExchange(“NYSE”),NASDandSIPC.ThisreportisintendedfordistributionintheUnitedStatesonlytoMajorInstitutionalInvestors(assuchtermisdefinedinSEC15a-6andSection15oftheSecuritiesExchangeActof1934,asamended)andisnotintendedfortheuseofanypersonorentitythatisnotamajorinstitutionalinvestor.MajorInstitutionalInvestorsreceivingthisreportshouldeffecttransactionsinsecuritiesdiscussedinthereportthroughCIBCWorldMarketsCorp.Thisreportisprovided,forinformationalpurposesonly,toinstitutionalinvestorandretailclientsofCIBCWorldMarketsinCanada,anddoesnotconstituteanofferorsolicitationtobuyorsellanysecuritiesdiscussedhereininanyjurisdictionwheresuchofferorsolicitationwouldbeprohibited.ThisdocumentandanyoftheproductsandinformationcontainedhereinarenotintendedfortheuseofprivateinvestorsintheUnitedKingdom.SuchinvestorswillnotbeabletoenterintoagreementsorpurchaseproductsmentionedhereinfromCIBCWorldMarketsplc.ThecommentsandviewsexpressedinthisdocumentaremeantforthegeneralinterestsofclientsofCIBCWorldMarketsAustraliaLimited.Thisreportdoesnottakeintoaccounttheinvestmentobjectives,financialsituationorspecificneedsofanyparticularclientofCIBCWorldMarketsInc.Beforemakinganinvestmentdecisiononthebasisofanyinformationcontainedinthisreport,therecipientshouldconsiderwhethersuchinformationisappropriategiventherecipient’sparticularinvestmentneeds,objectivesandfinancialcircumstances.CIBCWorldMarketsInc.suggeststhat,priortoactingonanyinformationcontainedherein,youcontactoneofourclientadvisersinyourjurisdictiontodiscussyourparticularcircumstances.Sincethelevelsandbasesoftaxationcanchange,anyreferenceinthisreporttotheimpactoftaxationshouldnotbeconstruedasofferingtaxadvice;aswithanytransactionhavingpotentialtaximplications,clientsshouldconsultwiththeirowntaxadvisors.Pastperformanceisnotaguaranteeoffutureresults.Theinformationandanystatisticaldatacontainedhereinwereobtainedfromsourcesthatwebelievetobereliable,butwedonotrepresentthattheyareaccurateorcomplete,andtheyshouldnotberelieduponassuch.Allestimatesandopinionsexpressedhereinconstitutejudgementsasofthedateofthisreportandaresubjecttochangewithoutnotice.AlthougheachcompanyissuingthisreportisawhollyownedsubsidiaryofCanadianImperialBankofCommerce(“CIBC”),eachissolelyresponsibleforitscontractualobligationsandcommitments,andanysecuritiesproductsofferedorrecommendedtoorpurchasedorsoldinanyclientaccounts(i)willnotbeinsuredbytheFederalDepositInsuranceCorporation(“FDIC”),theCanadaDepositInsuranceCorporationorothersimilardepositinsurance,(ii)willnotbedepositsorotherobligationsofCIBC,(iii)willnotbeendorsedorguaranteedbyCIBC,and(iv)willbesubjecttoinvestmentrisks,includingpossiblelossoftheprincipalinvested.TheCIBCtrademarkisusedunderlicense.(c)2008CIBCWorldMarketsInc.Allrightsreserved.Unauthorizeduse,distribution,duplicationordisclosurewithoutthepriorwrittenpermissionofCIBCWorldMarketsInc.isprohibitedbylawandmayresultinprosecution.

AnearlierprojectedstarttoNorthAmericanratehikeshasustrimmingourCanadianrealgrowthoutlookfor2009,withsomewhatlessgrowthcomingfromrealexports(althoughnominalexportswillremainhealthy)andinterestsensitivebusinessandresidentialinvestment.Inflationhasmovedontothesharplyclimbingtrackthatwehavebeenanticipatingforseveralmonths,andweaddedabittotheheadlineratefor2009inlinewithanupgradedoilpricecall.

We’ve raised our economic growth forecast for the remainder of the year to reflect a more resilient USconsumer,andtocapturethepositiveimpactof$150bninfederaleconomicstimulus.Lookingtonextyearthough,wehavetakendownourrealGDPforecastbyroughly1%-ptasaresultofourhigheroutlookforoilpricesandamorehawkishFed.AsinCanada,ourinflationforecasthasbeenedgedhigheronthebackofanupwardrevisiontoourforecastclimbinenergyprices.

CANADA 08Q1A 08Q2F 08Q3F 08Q4F 2007 2008F 2009F

Real GDP Growth (AR) -0.3 0.7 1.2 3.0 2.7 1.1 1.9

Real Final Domestic Demand (AR) 2.3 2.7 2.8 3.0 4.2 3.7 3.0

All Items CPI Inflation (Y/Y) 1.8 2.2 3.0 3.5 2.1 2.6 3.3

Core CPI Ex Indirect Taxes (Y/Y) 1.4 1.5 1.6 2.3 2.1 1.7 2.1

Unemployment Rate (%) 5.9 6.2 6.4 6.3 6.0 6.2 6.3

Merchandise Trade Balance (C$ Bn) 52.8 53.8 35.1 34.7 48.8 44.1 40.9

U.S.

Real GDP Growth (AR) 0.9 -0.2 -0.4 2.9 2.2 1.3 1.3

Real Final Sales (AR) 0.7 -1.0 -0.5 2.2 2.5 1.2 1.3

All Items CPI Inflation (Y/Y) 4.1 4.1 4.7 4.8 2.9 4.4 4.1

Core CPI Inflation (Y/Y) 2.4 2.3 2.2 2.3 2.3 2.3 2.8

Unemployment Rate (%) 4.9 5.3 5.5 5.6 4.6 5.3 5.3