effect of ifrs adoption on performance of banks in …

TRANSCRIPT

International Journal of Social Sciences and Humanities Reviews Vol.9 No.1, January 2019; p.207 – 219, (ISSN: 2276-8645)

207

EFFECT OF IFRS ADOPTION ON PERFORMANCE OF BANKS IN NIGERIA

OFOR THERESA NKECHI (PhD)

Faculty of Management Sciences,

Anambra State University,

Igbariam, Nigeria.

Email: [email protected]

Tel: +2348066230755

&

EMEKA OBIORA PETERS

Staff of Management Sciences,

Anambra State University,

Igbariam, Nigeria.

ABSTRACT

In the light of globalization, where remote speculations have turned out to be popular, looking at of articulation of money related places of Nigerian firms against different firms over the world has turned into

a worry. Nigeria organizations were ordered to embrace the international Financial Reporting Standards

(IFRS) in their monetary reports. This research will x-beam the effect which the appropriation of IFRS announcing standard will have on the

detailed execution of Nigerian banks recorded on the Nigerian Stock Exchange. Eight (8) out of the fourteen

(14) cited banks have been selected for the exploration. The four files of execution received in this inquiry are, liquidity utilizing complete store to add up to credit, benefit utilizing the arrival on, advance advances

and after that advertise value which was determined by profit proportion for the period (2011 and 2012). 2011 represented commonly acknowledged bookkeeping methodology period, while 2012 represents IFRS

selection.

A comparability index for the banks was determined utilizing the Excel Spreadsheet for every one of the banks on every factor. At that point the One Test was received for the further investigations. Mean was

utilized to react to the research questions while the t-insights tried the hypothesis. The outcome holds that

mean figures delivered for market , productivity and liquidity are more prominent in the GAAP time (2011) than in the IFRS routine (2012), while advance give was higher for the IFRS period (2012). The t-tried

maintain the way that none of the factors had obvious effect. In this way, the pursuit maintained that IFRS received does not have noteworthy impact on bank execution

detailed in 2011 and 2012. The investigation at that point prescribes that the open selection of IFRS for all

organizations, cum cooption of IFRS rule in expert preparing ought to be a necessary Government strategy.

KEYWORDS: IFRS, GAAP, Corporate execution, Liquidity, Profitability.

International Journal of Social Sciences and Humanities Reviews Vol.9 No.1, January 2019; p.207 – 219, (ISSN: 2276-8645)

208

INTRODUCTION

Since the 1960's business has turned out to be seriously globalized. Nigeria business is making increasingly

universal exchanges now. The internationalization of firms and account has uncovered the requirement for

the utilization of a uniform arrangement of announcing framework. The improvement of internationally

worthy Standard started abnitio in 1973 thus of the combination of a gathering of ensured bookkeeping

experts of real countries to frame International Accounting Standard Committee (IASC).

These countries are Ireland, Mexico, United States, Australia, UK, France, Germany, Japan, Canada, and

Netherland. The attention was on Creating and improving a general financial standard which will improve

satisfactory and adequate divulgences and supplant neighborhood norms, blend the errors in financial related

report due to decent varieties in lawful frameworks, organization structures, charge frameworks, and so on,

cultivate cross outskirt exchanges and improve comparability of data.

Henceforth, the clients of budgetary data can sufficiently contrast reports of funds to diverse organizations

which assess their monetary execution and position. In April 2001, the IASC was supplanted by International

Accounting Standard Board (IASB) and are mindful for creating bookkeeping standard known as IFRS

(Garba, 2013). The reception of IFRS in Nigeria was initiated in September 2010 .

Furthermore, this reception necessitated that all open recorded organizations should utilize IFRS for the

introduction of their budget summaries by first January, 2012. Different elements with open intrigue are

required to soak up IFRS by first January, 2013 while medium and little scale estimated substances are

required to Change to IFRS by first January, 2014.

Be that as it may, preceding soaking up of IFRS in Nigeria, banks throughout the years show powerless

divulgences in financial reportage, operational wasteful aspects, under capitalization and feeble corporate

administration practice that obstructs their execution and makes it hard to identify issues effectively, in the

financial part. The quality and standard of money related detailing in Nigeria banking part appears not to

coordinate the elevated requirement of announcing in the banking space of created nations (Garba, 2013)

until Nigeria embraces IFRS.

It is trusted that the switch over into IFRS from GAAP could improve likeness, responsibility, honesty and

straightforwardness in budgetary reporting (Akpani, 2011). Numerous researchers trusted that IFRS

reception in Nigeria will manage the emergency in the monetary part which added to the decrease in the

nation's foreign direct investment (FDI) in the oil furthermore, gas segment to a country, for example, Ghana

who accepted to have an improved money related detailing. Ironkwe and Oglekwu (2016) led contemplate

on the impact of IFRS on corporate execution. Muhammed (2012) analyzed the impact of IFRS selection on

the execution of organizations in Nigeria. Eneje et al, (2016) looked into the impacts of IFRS reception on

the mechanics of credit misfortune provisioning for banks in Nigerian.

Ugbede et al, (2014) have explored the IFRSs opposite the nature of banks fiscal summary data proof from

a developing showcase – Nigerian. Okoye, Okoye and Ezejiofor (2014) dug into a top to bottom appraisal

of effect of IFRSs on securities exchange development and the degree at which it can improve the situation

of corporate associations in the Nigerian capital market. Among these examinations, none have explored

IFRS impact on bank execution subsequently, the hole this examination filled in learning. The Objectives of

this Study is to decide the impact of IFRS reception on corporate execution of chose Nigeria banks. The

specialist in this way centered around looking at the consequence of Nigeria banks preceding and post

appropriation of IFRS. Key outcome pointers as far as liquidity, productivity, market value and loan grants

of the sampled banks were embraced to quantify the effect of the pre and post reception of IFRS in Nigeria.

International Journal of Social Sciences and Humanities Reviews Vol.9 No.1, January 2019; p.207 – 219, (ISSN: 2276-8645)

209

LITERATURE REVIEW

IFRS is an all inclusive motivation to upgrade a brought together limit in monetary data announcing

framework crosswise over universal regions with the attention on producing speedier energy for

improvement financially. They are standards – based measures by the IASB.

This single lot of worldwide financial measures has been under improvement for more than three decades

since the IASC was set up in 1973. Today the suite of benchmarks contains International Accounting

Standard (IAS) which was created by IASC and the IFRS , issued by IASB.

Theory of Benchmark. This paper is tied down on value expansion theory of Jensen (2001). This theory

holds that the essential destinations and motivation behind an existing firm is to take advantage of investors

riches in the long run. As indicated by .Jensen (2001), these speculations clarify that all the authoritative

exercises whether magnanimous or something else, are essentially looking to make benefit. This hypothesis

additionally holds that budgetary inquirers like obligation and warrant holders on the long run, will be

augmentation of different partners (Abdul-Baki et al, 2014).

The specialist therefore noticed the basic purpose behind displaying a company's financial report in the

instructed arrangement regarding IFRS is to boost its long haul value, accomplish straightforwardness,

responsibility and budget reports similarity. Observational Studies of Okoye and Akenbor (2014) opined

that it is convenient for Nigeria to embrace a international standard on the grounds that numerous Nigerian

organizations have securities of outside organizations.

Subsequently, IFRS will result to a superior choice about the progression of financial capital. Various

specialists have additionally distinguished the advantage IFRS is considered to deliver. As per Mary, Okoye

and Adediran (2013) the presentation and appropriation of IFRS in Nigeria will make and support open doors

for a bigger money change for firm and upturn the centralization of economies of scale. Taiwo and Adejare

(2014) recommended from their investigation that IFRS will upgrade money related execution and nature of

bookkeeping records. It will likewise upgrade business proficiency, help assets distribution and execution

arranging in organizations.

This is pair with Ocansey and Enahoro (2014) that the selection of IFRS in Nigeria needs a decent corporate

administration framework and new set of ability and skill. Obviously, if governments , institutional

condition, administrative bodies, governing body, review panels, partners and every other gathering can

assume their jobs fittingly,

IFRS will finish in an improved data quality particularly for banks. Irokwe and Oglekwu (2016) did an

investigation on IFRS and corporate execution of recorded organizations in Nigeria. Individual meeting and

poll techniques were embraced in the investigation as the significant methods for essential information

gathering. Information gathered were broke down utilizing both illustrative strategies, for example, tables,

frequencies and rate s and inferential measurements of chi-square and ANOVA individually.

The investigation held that relationship between the appropriation of IFRS and the monetary execution is

unequivocally positive due to cost decrease of an association. IFRS reception improves business profitability

and effectiveness for more prominent and powerful business result. The reception of IFRS spares worldwide

partnerships the cost of setting up various arrangement of records for different eco national units and offices.

Shehu (2015), explored on IFRS reception and income quality in recorded store cash banks in Nigeria. He

examines company's properties from the points of view of structure, observing, execution components also,

the nature of income of recorded store cash banks in Nigeria.

The investigation received connection look into structure with adjusted board information of 14 banks as

test of the investigation, utilizing various relapse as an apparatus of examination.

International Journal of Social Sciences and Humanities Reviews Vol.9 No.1, January 2019; p.207 – 219, (ISSN: 2276-8645)

210

The outcome uncovers that organizations highlights, for example, bank development, Leverage, liquidity,

benefit, bank measure impact income nature of recorded store cash banks in Nigeria after the reception of

IFRS, while the pre period demonstrates that the chosen organizations traits have no observable effect on

income quality. It is in this way maintained the selection of IFRS is convenient and practical. Abata (2015)

contemplated the effect of IFRS selection on monetary detailing practice in the Nigeria banking division.

The particular goals of the examination was to find out if the subjective contrasts in the explanation of money

related position arranged by Nigerian recorded banks under IFRS and NGAAP are factually critical or not.

Optional information were utilized in this examination.

These information were gathered from the yearly reports of fourteen Nigerian sampled banks. One

speculation was created and tried at 5% dimension of Hugeness. Discoveries recommended that the

quantitative contrasts in the budget report arranged under NGAAP and IFRS are measurably huge. The

investigation in this way presumes IFRS affect the budgetary position announcing in the Nigerian financial

area. Sani and Umar (2014) evaluated how much the Nigerian banking industry has consented to these

prerequisites as caught in IFRS 1: First time reception of IFRS. Utilizing ex-post facto and review examine

plans, the investigation sourced information from organized poll and late examined budgetary reports of the

inspected banks. Subjective Grading System (QGS) was utilized in learning the degree of consistence by the

banks while multivariate relapse and chi-square test were utilized in estimation of the impact of the elements

in charge of such consistence and distinguished plausible troubles in the process separately. The examination

held that the business agreed (semi-unequivocally) with the desires for IFRS-system, in any case, the process

is as yet loaded with some grinding which include: absence of top to bottom IFRS information from the

money related columnists.

The investigation additionally found managability, globalization and reactions to client's needs is factors

which has huge effect on the dimension of consistence of

Nigerian saves money with IFRS-system. Eneje, Obidike and Chukwujekwu (2016) basically analyzed the

impact of IFRS appropriation on the systems of provisioning for credit misfortune in Nigerian banks. They

broke down how the adjustment in the acknowledgment and estimation of advance misfortune arrangement

influences the bookkeeping nature of banks in this manner lessening the imagination in salary bookkeeping

conduct of the cash stores in banks.

In the model indicated, accommodating loss of advance and advances in the present year was conveyed as

the variable which is reliant while non-performing credits of the start of the year, current changes in non-

performing credits, current changes in all out advances, income before charges and advance misfortune

arrangements nearby with IFRS were utilized as the free factors.

In accordance with the points of this investigation, acquired information were optional in nature

from the cash store banks yearly budgetary position reports and records covering the period from 2005 to

2015. Descriptive statistics and the ordinary

least square multiple regression analytical system were deployed for the

data analysis. It was discovered that the confinement to perceive as it were acquired misfortunes under IAS

39 essentially lessens pay smoothing also, postpones acknowledgment of future anticipated future loses.

In view of the examined bank informational index and results, this paper has appeared that the post-IFRS

has had increased effect on the systems of advance provisioning contrasted with the pre-IFRS period in the

Nigerian cash store banks. Ugbede, Mohd and Ahmed (2014), examined IFRS also, the nature of banks fiscal

summary data: proof from developing business sector Nigeria. The research checks budget summary data

quality utilizing profit the executives, practicality of misfortune acknowledgment and significance. An

aggregate of twenty (20) Nigerian banks covering a time of six years were researched. An outcome uncovers

that IFRS selection is related with insignificant profit the executives and convenient acknowledgment of

misfortunes.

The outcome got uncovers a minuet backing to IFRS selection as its related with high

International Journal of Social Sciences and Humanities Reviews Vol.9 No.1, January 2019; p.207 – 219, (ISSN: 2276-8645)

211

significance of accounting data. Capital market misrepresentation for the most part incites importance

results. It was the accept of the examination that IFRS appropriation induces high caliber of banks financial

position reports data in comparism to the officially existing GAAP Asian and Dike (2015) examined the

distinctions in the nature of bookkeeping data pre-and-post IFRS appropriation by assembling firms in

Nigeria extending a five-year time frame. Numerous relapse investigation was performed on bookkeeping

quality factors and t-test was conveyed out for uniformity of intend to analyze pre-and-post IFRS. Results

demonstrate utilizing profit the board, importance and opportune misfortune acknowledgment a autonomous

factors bookkeeping quality delivered a declining bend.

Book estimation of and profit less value important and opportune misfortune acknowledgment is less in

post-IFRS contrasted with pre-IFRS period.

Okoye, Okoye and Ezediofor (2014) evaluated the effect of IFRS on securities exchange development and

the degree at which it can improve the position of corporate association in Nigerian capital market. They

embraced graphic structure utilizing the stock cost and offers exchanged amid the stock cost and offers

exchanged amid two years that is all.

SPSS version 7.0 was additionally used to get the mean, fluctuation and standard deviation. It has been seen

that the reception of IFRS in Nigeria will upgrade trustworthy budget summaries that will likewise give a

reason for the quality of a corporate substance in capital market, henceforth is an invited advancement in the

Nigerian economy.

The investigation uses optional information to test the impacts of appropriation of IFRS on the execution of

the chose firms in Nigeria. In investigating the information acquired, T-test and Logic relapse were utilized

in the examination. The examination finds that fluctuation of profit has diminished from a normal of 32624.4

to 14432.2, which recommends that there was low fluctuation in profit in the post appropriation period.

Auspicious acknowledgment of misfortune is the measure for pervasiveness of vast negative

results propose that the misfortune acknowledgment isn't opportune in the post-reception period. He

observed LNEG to be sure, which connotes that IFRS administrator organizations perceive misfortunes less

in the pre-appropriation period more oftentimes than they do in the post-reception that is all. The examination

along these lines infers that bookkeeping quality improved after of IFRS was presented and received.

Besides, under IFRS, firms were probably going to show higher qualities on a number of lists utilized in

estimating benefit , for example, income per share (EPS). Strategy for Data Analysis

This investigation quantitatively estimated its variable to have the capacity to learn the degree to which fiscal

reports arranged under IFRS and NGAAP can be thought about. In compatibility to accomplish this, an

adjusted variant of the Grays Conservatism Index (Comparability Index) was embraced. Dim (1980, is

referred to in Cardozzo, 2008) at first presented the list of conservatism in benefits similarity of a few nations

as a quantitative proportion of contrasts between bookkeeping rehearses.

The consider adjusted this equivalence file by applying it to other key components of the fiscal summaries,

for example, credit concede, productivity, liquidity, and market value arranged under IFRS and NGAAP.

This record is determined underneath:

1. Total Comparability Index =

1 – Profit IFRS – Profit NGAAP

Profit IFRS

2. Total Comparability Index =

1 – Liquidity IFRS– Liquidity NGAAP

Liquidity IFRS

3. Total Comparability Index =

1 – Loan grant IFRS– Loan grant NGAAP

Loan grant IFRS

4. Total Comparability Index

International Journal of Social Sciences and Humanities Reviews Vol.9 No.1, January 2019; p.207 – 219, (ISSN: 2276-8645)

212

1 –Market IFRS– Market NGAAP

Market IFRS

The gainfulness liquidities, advance give and market value revealed under IFRS are picked as the

denominators so as to get with the impact of IFRS on corporate execution. Introduction of Data; The

information gathered were introduced underneath in two tables, table no.1 for banks

benefit, liquidity, advance concede and market an incentive for year 2011 utilizing GAAP technique while

table No.2 used to show banks benefit, liquidity, advance granted and market for year 2012 utilizing IFRS

technique.

Table no 1: Banks Performance Indicators Using GAAP Method, 2011

Bank Profitability

(N’000)

Liquidity

(N’000)

Loan Grant

(N’000)`

Market

(N’000)

Access Bank 7.36 88.62 217,634,811.00 65.79

Diamond Bank 14.78 62.72 344,397,331.00 176.74

Eco Bank 23.92 45.54 410,150.00 113.04

Fidelity Bank Nig. 6.03 45.49 255,257.00 414.29

First Bank Plc 10.52 62.34 1,144,461.00 329.58

FCMB -9.91 77.43 319,020,875.00 144.12

UBA Plc 13.65 41.12 607,486.00 93.18

Zenith Bank 15.36 44.86 707,586.00 2016.50

Source: Nigerian Stock Exchange Website

Table no 2: Banks Performance Indicators Using IFRS Method, 2012

Table no 2: Banks Performance Indicators Using IFRS Method, 2012

Bank Profitability

(N’000)

Liquidity

(N’000)

Loan Grant

(N’000)`

Market

(N’000)

Access Bank 15.26 143.62 237,624,211.00 22.62

Diamond Bank 17.39 62.96 523,374,608.00 120.37

Eco Bank 3.40 51.36 546,873.00 207.14

Fidelity Bank Nig. 121.13 33.01 152,257.00 122.58

First Bank Plc 22.38 60.10 1,316,407.00 111.47

FCMB 9.41 54.40 350,489,990.00 154.55

UBA Plc 24.95 46.71 795,254.00 152.81

Zenith Bank 21.47 49.69 895,354.00 95.07

Source: Nigerian Stock Exchange Website.

FINDINGS. The examination of the investigation depended on bank comparable record. The comparability index on

factors are appeared on tables 3,4,5 and 6 for gainfulness, liquidity, credit and market value

separately.

International Journal of Social Sciences and Humanities Reviews Vol.9 No.1, January 2019; p.207 – 219, (ISSN: 2276-8645)

213

Table no. 3: Banks Computed Comparability Index for Profitability

Bank GAAP Method

2011 (N’000)

IFRS Method

2012 (N’000)

Difference Comparability

Index

Access Bank 7.36 15.26 7.9 0.48230668

Diamond Bank 14.78 17.39 2.61 0.84991374

Eco Bank 23.92 3.40 -20.52 7.0352941

Fidelity Bank Nig. 6.03 121.13 115.1 0.04978123

First Bank Plc 10.52 22.38 11.86 0.47006256

FCMB -9.91 9.41 19.32 -1.053135

UBA Plc 13.65 24.95 11.3 0.54709419

Zenith Bank 15.36 21.47 6.11 0.71541686

Source: Nigerian Stock Exchange Website.

Table no.4: Banks Computed Comparability Index for Liquidity

Bank GAAP Method

2011 (N’000)

IFRS Method

2012 (N’000)

Difference Comparability

Index

Access Bank 88.62 143.62 55 0.61704498

Diamond Bank 62.72 62.96 0.24 0.99618806

Eco Bank 45.54 51.36 5.82 0.88668224

Fidelity Bank Nig. 45.49 33.01 -12.48 1.37806725

First Bank Plc 62.34 60.10 -2.24 1.03727121

FCMB 77.43 54.40 -23.03 1.42334559

UBA Plc 41.12 46.71 5.59 0.88032541

Zenith Bank 44.86 49.69 4.83 0.90279734

Source: Nigerian Stock Exchange Website.

Table no.5: Banks Comparability Index for Loan Grant

Bank GAAP Method

2011 (N’000)

IFRS Method

2012 (N’000)

Difference Comparability

Index

Access Bank 217,634,811.00 237,624,211.00 19989400 0.9158781

Diamond Bank 344,397,331.00 523,374,608.00 178977277 0.65803217

Eco Bank 410,150.00 546,873.00 136723 0.74999131

Fidelity Bank

Nig.

255,257.00 152,257.00 -103000 1.67648778

First Bank Plc 1,144,461.00 1,316,407.00 171946 0.86938234

FCMB 319,020,875.00 350,489,990.00 31469115 0.91021394

UBA Plc 607,486.00 795,254.00 187768 0.76388927

Zenith Bank 707,586.00 895,354.00 187768 0.7902863

Source: Nigerian Stock Exchange Website.

International Journal of Social Sciences and Humanities Reviews Vol.9 No.1, January 2019; p.207 – 219, (ISSN: 2276-8645)

214

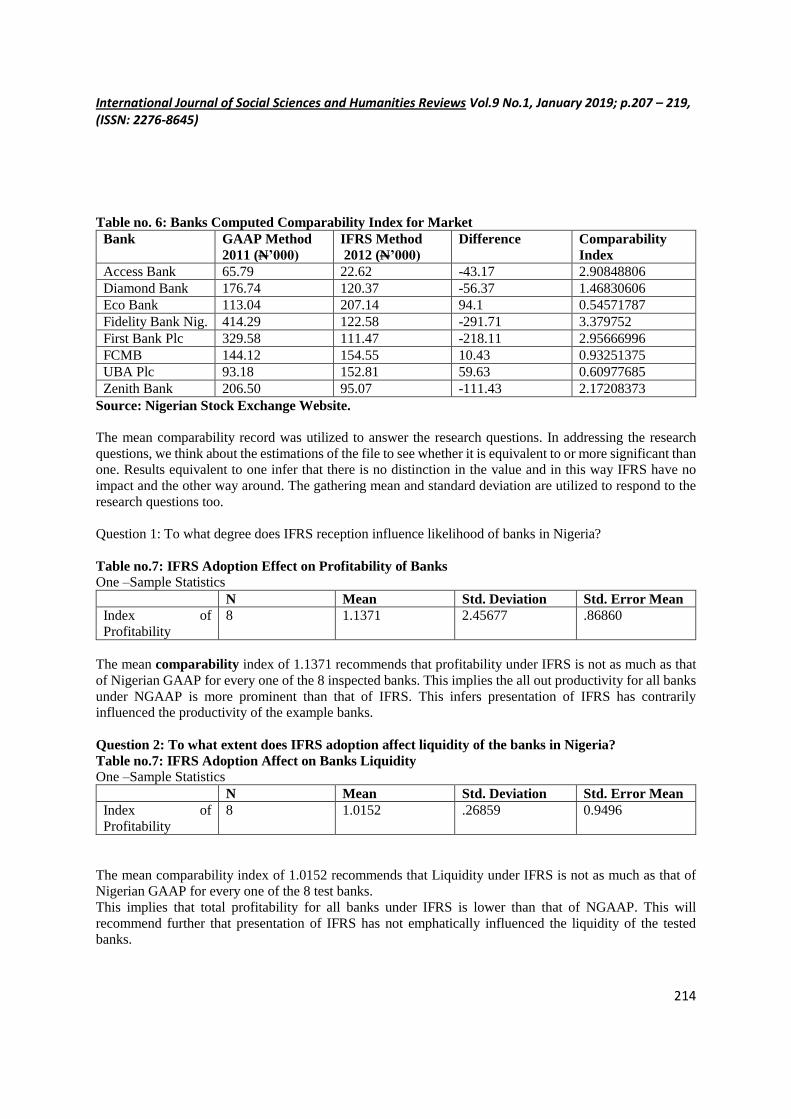

Table no. 6: Banks Computed Comparability Index for Market

Bank GAAP Method

2011 (N’000)

IFRS Method

2012 (N’000)

Difference Comparability

Index

Access Bank 65.79 22.62 -43.17 2.90848806

Diamond Bank 176.74 120.37 -56.37 1.46830606

Eco Bank 113.04 207.14 94.1 0.54571787

Fidelity Bank Nig. 414.29 122.58 -291.71 3.379752

First Bank Plc 329.58 111.47 -218.11 2.95666996

FCMB 144.12 154.55 10.43 0.93251375

UBA Plc 93.18 152.81 59.63 0.60977685

Zenith Bank 206.50 95.07 -111.43 2.17208373

Source: Nigerian Stock Exchange Website.

The mean comparability record was utilized to answer the research questions. In addressing the research

questions, we think about the estimations of the file to see whether it is equivalent to or more significant than

one. Results equivalent to one infer that there is no distinction in the value and in this way IFRS have no

impact and the other way around. The gathering mean and standard deviation are utilized to respond to the

research questions too.

Question 1: To what degree does IFRS reception influence likelihood of banks in Nigeria?

Table no.7: IFRS Adoption Effect on Profitability of Banks

One –Sample Statistics

N Mean Std. Deviation Std. Error Mean

Index of

Profitability

8 1.1371 2.45677 .86860

The mean comparability index of 1.1371 recommends that profitability under IFRS is not as much as that

of Nigerian GAAP for every one of the 8 inspected banks. This implies the all out productivity for all banks

under NGAAP is more prominent than that of IFRS. This infers presentation of IFRS has contrarily

influenced the productivity of the example banks.

Question 2: To what extent does IFRS adoption affect liquidity of the banks in Nigeria?

Table no.7: IFRS Adoption Affect on Banks Liquidity

One –Sample Statistics

N Mean Std. Deviation Std. Error Mean

Index of

Profitability

8 1.0152 .26859 0.9496

The mean comparability index of 1.0152 recommends that Liquidity under IFRS is not as much as that of

Nigerian GAAP for every one of the 8 test banks.

This implies that total profitability for all banks under IFRS is lower than that of NGAAP. This will

recommend further that presentation of IFRS has not emphatically influenced the liquidity of the tested

banks.

International Journal of Social Sciences and Humanities Reviews Vol.9 No.1, January 2019; p.207 – 219, (ISSN: 2276-8645)

215

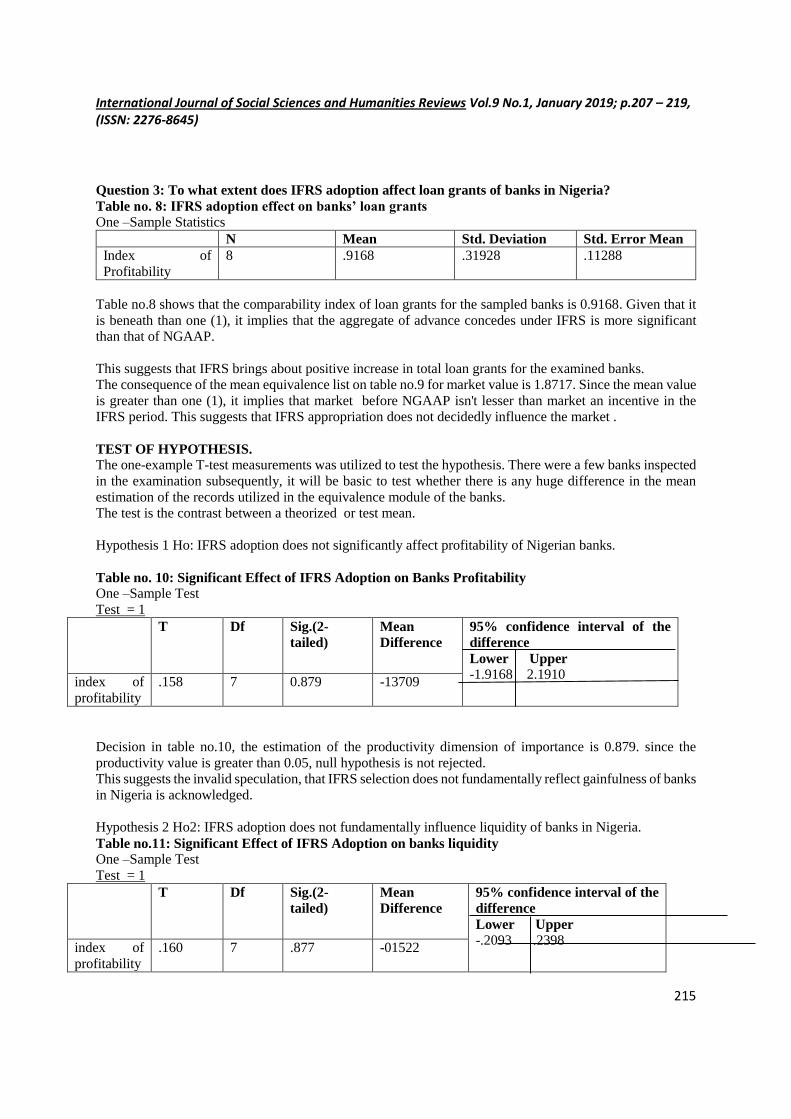

Question 3: To what extent does IFRS adoption affect loan grants of banks in Nigeria?

Table no. 8: IFRS adoption effect on banks’ loan grants

One –Sample Statistics

N Mean Std. Deviation Std. Error Mean

Index of

Profitability

8 .9168 .31928 .11288

Table no.8 shows that the comparability index of loan grants for the sampled banks is 0.9168. Given that it

is beneath than one (1), it implies that the aggregate of advance concedes under IFRS is more significant

than that of NGAAP.

This suggests that IFRS brings about positive increase in total loan grants for the examined banks.

The consequence of the mean equivalence list on table no.9 for market value is 1.8717. Since the mean value

is greater than one (1), it implies that market before NGAAP isn't lesser than market an incentive in the

IFRS period. This suggests that IFRS appropriation does not decidedly influence the market .

TEST OF HYPOTHESIS. The one-example T-test measurements was utilized to test the hypothesis. There were a few banks inspected

in the examination subsequently, it will be basic to test whether there is any huge difference in the mean

estimation of the records utilized in the equivalence module of the banks.

The test is the contrast between a theorized or test mean.

Hypothesis 1 Ho: IFRS adoption does not significantly affect profitability of Nigerian banks.

Table no. 10: Significant Effect of IFRS Adoption on Banks Profitability One –Sample Test

Test = 1

T Df Sig.(2-

tailed)

Mean

Difference

95% confidence interval of the

difference

Lower Upper -1.9168 2.1910

index of

profitability

.158 7 0.879 -13709

Decision in table no.10, the estimation of the productivity dimension of importance is 0.879. since the

productivity value is greater than 0.05, null hypothesis is not rejected.

This suggests the invalid speculation, that IFRS selection does not fundamentally reflect gainfulness of banks

in Nigeria is acknowledged.

Hypothesis 2 Ho2: IFRS adoption does not fundamentally influence liquidity of banks in Nigeria.

Table no.11: Significant Effect of IFRS Adoption on banks liquidity One –Sample Test

Test = 1

T Df Sig.(2-

tailed)

Mean

Difference

95% confidence interval of the

difference

Lower Upper

-.2093 .2398 index of

profitability

.160 7 .877 -01522

International Journal of Social Sciences and Humanities Reviews Vol.9 No.1, January 2019; p.207 – 219, (ISSN: 2276-8645)

216

Decision

The outcome on table No.11 demonstrates that the profitability is 0.877. Since the productivity value is

more noteworthy than the 0.05 value embraced in this research, we will acknowledge the null hypothesis

which expresses that IFRS selection does not essentially influence liquidity of banks in Nigeria.

Hypothesis 3 Ho3: IFRS selection does not essentially influence credit stipends of the banks in Nigeria.

Table No.12: Significant Effect of IFRS Adoption on Banks Loan Grants

One –Sample Test

Test = 1

T Df Sig.(2-

tailed)

Mean

Difference

95% confidence interval of the

difference

Lower Upper -.3502 .1837

index of

profitability

-.737 7 .485 -.08323

The outcome from table No.12 demonstrates that the estimation of the benefit dimension of importance is

0.485. Since the likelihood value is more significant than 0.05, the invalid speculation that IFRS reception

does not essentially influence credit stipends of the banks in Nigeria isn't rejected.

Hypothesis 4 Ho: IFRS appropriation does not essentially influence the market value of the banks in Nigeria.

Table No.13: Significant Effect of IFRS Adoption on Banks Market

One –Sample Test

Test = 1

T Df Sig.(2-

tailed)

Mean

Difference

95% confidence interval of the

difference

Lower Upper -.07691 .8203

index of

profitability

2.173 7 0.66 .87166

Decision The outcome from table No.13 demonstrates a profitability value of 0.66. Since the likelihood value is more

significant than 0.05, the null hypothesis that IFRS reception does not essentially influence the market value

of the banks in Nigeria isn't rejected.

This suggests the IFRS selection contrarily influenced the market.

Discussion on Findings

The study demonstrates that the presentation of IFRS has decreased the benefit of banks however it doesn't

have significant impact on the profitability of the banks in Nigeria. This recommends that the value of the

profitability was lower when reported utilizing the IFRS accounting rules.

This suggests IFRS presentation realized an insignificant fall in bank's benefit. Hence, it tends to be said that

the monetary reports of banks give moderately a similar data in the two arrangements: IFRS and GAAP.

Subsequently, the utilization of IFRS did not upset money related position of the banks.

International Journal of Social Sciences and Humanities Reviews Vol.9 No.1, January 2019; p.207 – 219, (ISSN: 2276-8645)

217

This study countered the Jensen's (2001) value expansion hypothesis where in firms may embrace one

bookkeeping standards or rules to boost investors riches. This present examination battles that organizations

won't profit by the utilization of shifting bookkeeping standards of distinctive bookkeeping periods. The

outcomes are in tanderm with past discoveries in Nigeria.

As this examination uncovers decreased monetary development for banks in Nigerian (liquidity, showcase

value ,low benefit and higher advance figure), the past contemplate concurred that IFRS implies negligible

profit the board and auspicious acknowledgment of misfortunes (Ugbede et al., 2014; Eneje et al., 2016),In

these cases, IFRS reception has made conceivable an increasingly solid money related report regime.(Okoye

et al., 2014).

Moreover, the presentation and selection of IFRS demonstrates characteristic of lower liquidity of banks in

Nigeria. it in any case, does not have significant impact on the liquidity of the banks in Nigeria. This

advocates that the dimension of banks liquidity will generally be equivalent to in IFRS money related report

in 2012 IFRS reception. As liquidity is a major variable that guides the bank in gathering its financial

obligations on demand deposits and loan advances, More so, the introduction and adoption of IFRS

heightened the loan advances of banks.

All the more along these lines, the presentation and reception of IFRS increased the advance advances of

banks.

However, it doesn't have critical impact on the credit gifts of the banks in Nigeria. This is demonstrative that

IFRS presentation did not change the monetary places of the bank credit announced in fiscal reports. An

advance concede from bank mirrors their dimension of money related intermediation.

The presentation of IFRS caused increment in banks credit and advances (however not noteworthy), bank

budgetary intermediation is required to improve. This couldn't help contradicting the Jensen's (20001) value

Maximization Theory, this means that banks can't again improve budgetary position on bank advances by

changing from NGAAP to IFRS. The market value of banks were at long last diminished, however it doesn't

have critical impact on available value of the banks in Nigeria.

This proposes IFRS and NGAAP sees on the budgetary position of the banks in Nigeria are not a long way

from one another. This refuted the statement of the Jensen's (2011) value Maximization Theory where in

firms can utilize one accounting standards or rules to boost

investors wealth. In this way it is demonstrated that the utilization of IFRS did not modify the market value

of banks.

In clear difference to the present study, was the discoveries which holds that IFRS appropriation has

emphatically affected a few factors in the banks budgetary reports of banks, for instance benefit and

development potential (Yahaya, Yusuf and Dania, 2015). This investigation sets that IFRS results in higher

reportage for bank benefit as against the discoveries of the past

thought. The situation of this study lines up with the perspective on chose observational works in Nigeria.

As this investigation found decreased money related wellbeing for Nigerian banks (low benefit, liquidity and

market value and higher credit value) , the past investigation concurred that IFRS implies negligible income

the board and auspicious acknowledgment of loses (Ugbede et al, 2014; Eneje et al; 2016).

IFRS selection in every one of these researches, has enthroned solid financial related reporting. (Okoye et

al; 2014).

CONCLUSION

The study has demonstrated that the equivalence indices of Nigerian banks tested uncovers a slight high

mean. This proposes banks execution under IFRS seemed lower than NGAAP. Be that as it may, these higher

estimations of mean regarding NGAAP don't have significant effect on the banks execution.

This proposes banks execution isn't influenced by the presentation and appropriation of IFRS in Nigeria. The

investigation has appeared Nigerian conditions can without much of a stretch absorb the presentation of the

IFRS in the banking framework. The decreased budgetary wellbeing for Nigerian banks (low benefit,

International Journal of Social Sciences and Humanities Reviews Vol.9 No.1, January 2019; p.207 – 219, (ISSN: 2276-8645)

218

liquidity, advertise value and higher advance figure) implies that IFRS implies auspicious acknowledgment

of misfortunes and negligible income the executives.

Recommendation

In accordance with the discoveries of the study and conclusion proffered, it ends up basic that certain

suggestions ought to be made to fill in as a guide for pragmatic activities. Since the selection of IFRS is

observed to be factually huge in influencing bank liquidity however did not change bank benefit, liquidity,

advance and market , revealed in resulting year, it is prescribed that the utilization of IFRS ought to be

supported in Nigeria as its utilization results to Nigeria banks use of international accounting standards and

procedures in financial reporting.

REFERENCE Abdul-Baki, Z., Uthman, B., and Sanni M. (2014). Financial ratios as performance measure: A

comparison of IFRS and Nigerian GAAP. Accounting and Management Information

Systems. 13(1), 82–97.

Adam, M. (2014). Evaluating the Financial Performance of Banks using financial ratios- A case

study of Erbil Bank for Investment and Finance. European Centre for Research Training

and Development UK. 2(2), 156 – 170.

Adam, M. (2009). Nigerian banks: The Challenges of Adopting International Financial

Reporting Standards. Zenith Economic Quarterly, .4, (2), 17.

Agrawal, N. (2008). The Impact of IFRS on Corporate Governance. Available at

www.livemint.com.

Ahmed Zakari& Co - Chartered Accountants and Entop Consulting Ltd UK. (2011).

International Financial Reporting Standards (IFRS): An Essential course for Getting to

“KNOW IFRS”.

Akinleye, G.T.(2016). Effect of international financial reporting standards (IFRS) adoption on

the performance of money deposit banks in Nigeria. European Journal of Business,

Economics and Accountancy, 4(4), ): 87-95.

Akiwi,(2010).Adoption of international financial reporting standards in developing countries –

The case of Ghana. Business Economics and Tourism. VAASA Ammatikorkeakoulu

University of Applied Sciences Bachelor of Business Administration .

Alp, A., & Ustuntag, S. (2009).Financial reporting transformation the experience of Turkey.

Critical Perspective on Accounting, 20, 680-699.

http://dx.doi.org/10.1016/j.cpa.2007.12.005

Anyanwu, C. (2010). Overview of Current Banking Sector Reforms and Real Sector in

Nigerian Economy”, Central Bank of Nigeria Economic and Financial review 48(4) 31-59.

Asian, A. U. & Dike, A.(2015). IFRS adoption and accounting quality of quoted manufacturing

firms in Nigeria: a cross sectional study of brewery and cement manufacturing

firms..International Journal of Business and Management Review, 3(6), :

61-77.

Bala, M. (2013). Effect of IFRS Adoption on the Financial Reports of Nigeria Listed entities:

The Case of Oil and Gas Companies.TheMacrotheme Review 2(7), 9-26.

Barth, M.,(2008). Global Financial Reporting, Implications for US Academics. The Accounting

Review. 83(5),): 1159-1179. Beke, J. (2011).

How can International Accounting Standards Support Business Management? International

Journal of Management and BusinessResearch.1(1), 25-34

Benzacar; K. (2008). IFRS: the next accounting revolution: A publication of CMA management

June . Eneje,

B., Obidike, C. & Chukwujekwu, P.(2016). The Effect of IFRS Adoption on the Mechanics of

International Journal of Social Sciences and Humanities Reviews Vol.9 No.1, January 2019; p.207 – 219, (ISSN: 2276-8645)

219

Loan Loss Provisioning For Nigerian Banks. IOSR Journal of Business and Management,

18(6), : 45-52.

Garba, S. (2013). IFRS and Bank Performance in Nigeria. https://www.academia.edu.

Godwin, J., Karman A., & Heanly, R. (2009). Corporate Governance and the Prediction of the

Impact of AIFRS Adopting. Abacus 45, 124-145.

Https://en.wikipedia.org/wiki/List_of_International_Financial_Reporting_Standards

Ironkwe, U. I. & Oglekwu, M.(2016). International Financial Reporting Standards (IFRSs) and

Corporate Performance of Listed Companies in Nigeria.” IIARD International Journalof

Banking and Finance Research, (2)3):1-13.

Iyoha, F. O; & Jimoh, J. (2011). Institutional Infrastructure and the adoption of International

Financial Reporting Standards in Nigeria. SSRN publications pp 17-23. Mary, J., The effect

of International Financial Reporting Standards (IFRS)adoption on the performance of firms

in Nigeria. Journal of Administrative and Economic Sciences Qassim University,

5(2),:133-157.

Ocansey, E.,& Enahoro, J. (2014). Comparative Study of the International Financial Reporting

Standards Implementation in Ghana and Nigeria. European Scientific Journal.10(13), 529-

546.

Odia, J.,& Ogiedu, K. (2013). IFRS Adoption: Issues, Challenges and Lessons for Nigeria and

other Adopters. Mediterranean Journal of SocialSciences. 4(3), 389-399.

Okoye, P., & Akenbor, C. (2014). Financial Reporting Framework in Nigeria and the Adoption

of the IFRS. International Journal of Business and Economic Development 2(1), 52- 63.

Okoye,P.V.C., Okoye, J. F. N. &Ezejiofor, R.A.(2014). Investigated the impact of the IFRS

adoption on stock market movement in Nigerian corporate organization.” International

Journal of Academic Research in Business and Social Sciences, 4(9), : 202-218.

Okpala, K. (2012). Adoption of IFRS and the Financial Statement Effects. The Perceived

Implication on Foreign Direct Investment and Nigeria Economy. Australian Journal of

Business and Management Research. 2. 76- 83.

Sani, S. & Umar, D.(2014). An assessment of compliance with IFRS framework at first-time

adoption by the quoted banks in Nigeria.” Journal of Finance and Accounting,

2(3),): 64-73.

Shehu, U.H.(2015). Adoption of international financial reporting standards and earnings quality

in listed deposit money banks in Nigeria. Procedia Economics and Finance, 28, : 92-101.

Taiwo, F., & Adejare, A. (2014). Empirical Analysis of the Effect of International Financial

Reporting Standards (IFRS) Adoption on Accounting Practices

in Nigeria.Archives of Business Research, 2(2), 1-14.

Tanko, M. (2012). The Effect of IFRS Adoption on the Performance of Firms in Nigeria.

Journal of Administrative and Economic Sciences, 5(2), 133-157.

Ugbede, O.,Mohd, L. & Ahmad, K.(2014). International Financial Reporting Standards and the

quality of banks financial statement information: evidence from an emerging market-

Nigeria.” European Journal of Business and Social Sciences, 3(8),: 243-255.

Yahaya, O. A., Yusuf, M. J. & Dania, I.S(2015). International financial reporting standards’

adoption and financial statement effects: Evidence from listed deposit money banks in

Nigeria. Research Journal of Finance and Accounting, 6(12), : 107-122.