electric power european power daily - s tender for new gas-fired power capacity eligible for ......

TRANSCRIPT

Volume 15 / Issue 164 / August 23, 2013

www.platts.com

[ELECTRIC POWER ]

EUROPEAN POWER DAILY

Platts European Power AssessmentsAt-A-Glance Day-Ahead Baseload Comparisons

August 22, 2013 (Eur/MWh) Change (%)

Platts PEP Index 49.5065 -2.08%Platts Conti Index 46.3975 -3.24%Platts UK Power Index 55.1000 0.35%Platts Mid Germany 44.7500 -2.72%Platts Mid Switzerland 45.2500 -1.09%Platts Mid France 43.2500 -4.95%Platts Mid Netherlands 50.7500 -1.93%Platts Mid Belgium 46.1500 -0.43%Platts Mid Spain 54.1000 -0.28%

Platts Indices: Platts Pan-European Power (PEP) Index and the Continental Power (Conti) Index are demand-weighted (Source: ENTSO-E), baseload indices to indicate trends in the free European electricity market as a whole. The Conti Index is based upon assessments in Germany, Switzerland, France, Belgium and the Netherlands. The PEP Index is based on these six assessments plus the UK’s GTMA day-ahead market and Spanish bilateral day-ahead assessments.

(Eur/MWh)

Central & Eastern Europe September base

Source: Platts

32

35

38

41

44

22-Aug19-Aug14-Aug9-Aug6-Aug1-Aug

German Czech Hungarian Polish

ThE MArkET

Belgian gas plant tender to include open cycleBelgium’s tender for new gas-fired power capacity eligible for state support has been widened to include open cycle as well as combined cycle units, according to an economy ministry document seen by Platts.

The terms of the tender have not yet been publicly disclosed but the latest version of a specifications document is in circulation among interested parties.

A Belgian energy ministry spokeswoman Thursday said that relevant texts are still under review by the cabinet, after a proposed royal decree on implementation was approved July 19 at the final cabinet meeting before the summer recess.

“We’re waiting for the cabinet’s comments in September,” the spokeswoman said.

The specifications confirm the amount of new capacity called for through the tender, capped at 800 MW.

Financial terms outlined in the document stipulate that the maximum annual support that can be requested for each megawatt installed is Eur44,471 ($59,336) for open cycle gas plants, while the maximum for closed-cycle CCGTs is higher at Eur89,330. State payments will not be subject to tax.

The financial modeling behind the support proposed evaluates the profitability of a hypothetical gas plant over 25 years to allow for a 7.5% annual return on investment.

The level of support requested by a candidate project will account for 70% of the final decision, with projects submitting the lowest maximum annual support level rated highest.

The weightings for the remaining selection criteria are: 15% based on start-up date, with open cycle projects “ready to run” on January 1, 2016 and closed cycle CCGTs on January 1, 2017 scoring the highest ratings; 10% based on a project’s contribution to “effective market functioning,” scored inversely based on an owner-operator’s existing proportion of production capacity ownership; and 5% on technical quality, of which half based on plant flexibility.

With flexibility accounting for a weighting of just 2.5% of the selection criteria, it is unclear whether the draft specifications will receive a favorable outcome from energy regulator CREG, which in a May report slammed the proposed call for tender on a number of counts, including failure to ensure flexible capacity. That version of the tender document did not include open cycle plants, which are more flexible than CCGTs.

The latest ministry draft says that both gas plant technologies will need to prove an ability to participate in ancillary services and balancing. Flexible response from new gas plants is considered crucial if gas generation is to be used to back up intermittent renewables as Belgium phases out nuclear power by 2025.

Other criteria are that CCGTs must have minimum installed capacity of 400 MW, while the restriction for OCGTs is smaller, at 100 MW. Required plant efficiencies at low heat rate are 57% and 40% respectively.

Both technology types must have available capacity of 80%

European Power Market highlights

�� Continental European prompt power prices slid lower Thursday amid typically lower Friday demand while the UK prompt remained stable as lower demand and stronger wind generation was partially offset by lower nuclear generation and rising NBP gas prices, sources said.

�� UK day-ahead baseload was last heard midday at GBP47/MWh, flat on day, while peakload power eased back 65 pence to GBP54/MWh.

�� With no new developments on the nuclear front, French day-ahead prices moved lower after Wednesday’s upwards surge. Friday base closed Eur2.25 lower on the day at Eur43.25/MWh, with peakload down 25 euro cent at Eur51.25/MWh .

�� Despite strengthening winds in Germany, plant outages and a lower solar forecast kept supply tight, with German day-ahead baseload last heard at Eur44.75/MWh, Eur1.25 lower on the day, while day-ahead peakload dropped 60 euro cent to Eur51.25/MWh.

�� Further forward, German Cal 14 baseload was last heard trading OTC at Eur36.70/MWh, just 10 euro cent higher on the day.

EuropEan powEr Daily august 23, 2013

2Copyright © 2013 McGraw Hill Financial

German Platts Power Index (PPI)

22-Aug-13 ChangeMidday assessments

PPI (Month-ahead - Eur/MWh) 37.800 +0.050 ▲PPI (Quarter-ahead - Eur/MWh) 38.600 +0.100 ▲PPI (Year-ahead - Eur/MWh) 36.650 +0.050 ▲PPI Midday (Eur/MWh) 37.090 +0.060 ▲

End of day assessments

PPI (Month-ahead - Eur/MWh) 37.800 +0.000 —PPI (Quarter-ahead - Eur/MWh) 38.700 +0.100 ▲PPI (Year-ahead - Eur/MWh) 36.700 +0.050 ▲PPI EoD (Eur/MWh) 37.140 +0.050 ▲

Platts Power Index (PPI): The PPI is a weighted forward power index, based on German front-month, front-quarter and front-year base load wholesale prices to indicate curve movements in continental Europe’s benchmark power market. Front-month is weighted singularly, front-quarter three-fold and front-year 12-fold. The midday PPI index compares changes with the last end of day PPI, and the last end of day PPI compares changes with the last Midday PPI.

Platts Uk Assessments (GTMA, GBP/MWh)August 22, 2013 Euro Equivalents Baseload Peak Baseload PeakDay-ahead 46.80 - 47.20 53.50 - 54.50 54.87 - 55.33 62.72 - 63.89Weekend 43.50 - 44.50 51.00 - 52.17Week Ahead 45.25 - 46.25 53.50 - 53.90 53.05 - 54.22 62.72 - 63.19Week Ahead+1 46.25 - 46.40 53.75 - 55.75 54.22 - 54.40 63.01 - 65.36Sep 46.30 - 47.30 54.40 - 55.40 54.28 - 55.45 63.77 - 64.95Oct 48.15 - 49.15 56.00 - 57.00 56.45 - 57.62 65.65 - 66.82Nov 51.65 - 52.65 60.50 - 61.50 60.55 - 61.72 70.93 - 72.10Q4 13 51.35 - 52.35 59.85 - 60.85 60.20 - 61.37 70.16 - 71.34Q1 14 55.00 - 56.00 63.25 - 64.25 64.48 - 65.65 74.15 - 75.32Winter 13/14 53.20 - 54.20 61.50 - 62.50 62.37 - 63.54 72.10 - 73.27Summer 14 48.50 - 49.50 56.05 - 57.05 56.86 - 58.03 65.71 - 66.88Winter 14/15 54.70 - 55.70 63.95 - 64.95 64.13 - 65.30 74.97 - 76.14Summer 15 52.00 - 53.00 60.05 - 61.05 60.96 - 62.13 70.40 - 71.57Winter 15/16 58.30 - 59.30 68.95 - 69.95 68.35 - 69.52 80.83 - 82.00April 14 Annual 51.60 - 52.60 60.00 - 61.00 60.49 - 61.66 70.34 - 71.51

Baseload=2300-2300, Peak=0700-1900

Daily indices

GBP/MWh Eur/MWh Change D-1 (GBP/MWh)Day-ahead 47.00 55.10 +0.00Weekend 44.00 51.58 +1.15Sep 46.80 54.87 +0.50

Index definitions are published in the Platts methodology guide available on the Platts website.

Platts Central European Spot Assessments (Eur/MWh)August 22, 2013 Baseload Peak

Day-Ahead (Germany) 44.60 - 44.90 51.10 - 51.40Day-Ahead (Switzerland) 44.75 - 45.75 50.80 - 51.80Swiss Franc equivalent 55.09 - 56.32 62.53 - 63.77Week Ahead (Germany) 40.75 - 41.25 54.75 - 55.25Weekend (Germany) 28.15 - 28.65

Baseload = 0000-2400, Peak = 0800-2000.

Swiss Franc equivalents are for Swiss prices.

Platts French Assessments (Eur/MWh)August 22, 2013 Baseload Peak

D/A 43.00 - 43.50 51.00 - 51.50Weekend 28.50 - 29.00Week Ahead 41.75 - 42.25 55.60 - 56.10Sep 13 37.90 - 38.40 49.45 - 51.45Oct 13 44.70 - 45.70 57.35 - 59.35Nov 13 49.15 - 50.15 64.95 - 66.95Q4 2013 47.05 - 47.55 61.50 - 62.00Q1 2014 52.25 - 52.75 64.50 - 65.50Cal 2014 41.65 - 42.15 54.95 - 56.95Cal 2015 41.35 - 42.35 55.20 - 57.20Cal 2016 41.65 - 42.15 57.95 - 59.95

based on a pre-determined number of annual operating hours for each plant, the document said. Minimum efficiency is 57% for CCGTs and 40% for OCGTs.

Positive clean spark spreads assumedSeparately, the draft royal decree outlining procedures for implementation of the tender states that the financial support model is based on the assumption that open cycle plants operate for 847 hours per year while closed cycle units operate for 2602 hours until 2025.

Average capital expenditure is assumed at Eur354,000/MW in 2011 currency for open cycle plants and Eur795,500/MW for CCGTs, the document shows.

The version of the decree seen by Platts, dated July 6, also assumes positive clean spark spreads — of Eur41.09/MWh in 2011 currency for open cycle technology during plant operating hours and Eur35.07/MWh for closed cycle plants, based on average efficiencies at high heat rate of 36% and 53% respectively. Clean spark spreads are the theoretical measure of a gas plant’s profitability accounting for the cost of feedstock gas and carbon permits.

In its May report, CREG said that the ministry’s clean spark spread assumptions were too high.

Platts spark spread assessment data shows a Belgian quarter-ahead clean spark spread of just 47 euro cent/MWh baseload on Thursday for a 60% efficient gas plant.

Tight timelinesDavid Haverbeke, Partner for Field Fisher Waterhouse LLP, told Platts that a tender process would need to be finalized by the end of the year to enable contracted capacity to enter into service by the draft decree’s deadline of January 1, 2016 for open cycle and January 1, 2017 for combined cycle plant.

“The list of potential candidates is quite short - there are five or six [with large CCGT proposals], although the inclusion of open cycle units may change the picture as these are generally smaller, between 100 MW and 200 MW,” Haverbeke said.

Noting that the draft was focused solely on gas-fired generation, opening it to legal challenge, Haverbeke said it might be hard to get the proposal finalized in time to meet the 2016/2017 deadlines.

“If the draft was sent to the [European Commission] in late July, that takes us to the end of the year before the EC has to rule on it,” he said. “The draft itself needs finalizing and placing in the Official Journal. Only two months after that will we know if it will be challenged under Belgian proceedings.”

As the country’s dominant nuclear generator, Haverbeke said Electrabel might consider challenging the auction as discriminatory against other fuel types.

As to the structure of support, Haverbeke said the duration of the subsidy was potentially problematic. “The price requested will cover 70% of the selection criteria, so that is important, but 10 years is a really short time for project financing and is likely to create problems for developers.”

The draft documents indicate financial support for projects until 2025/2026, although a six-year support limit is also mentioned. The energy ministry spokeswoman was not able to provide further comment Thursday.

The best that potential bidders could hope for was that energy minister Melchior Wathelet lined up an approved auction process ahead of elections in Belgium next May, Haverbeke said.

“That would leave a final decision to his successor, just about allowing already-approved CCGT projects to be built by the 2017 deadline — but it will be down to whether turbine suppliers can

EuropEan powEr Daily august 23, 2013

3Copyright © 2013 McGraw Hill Financial

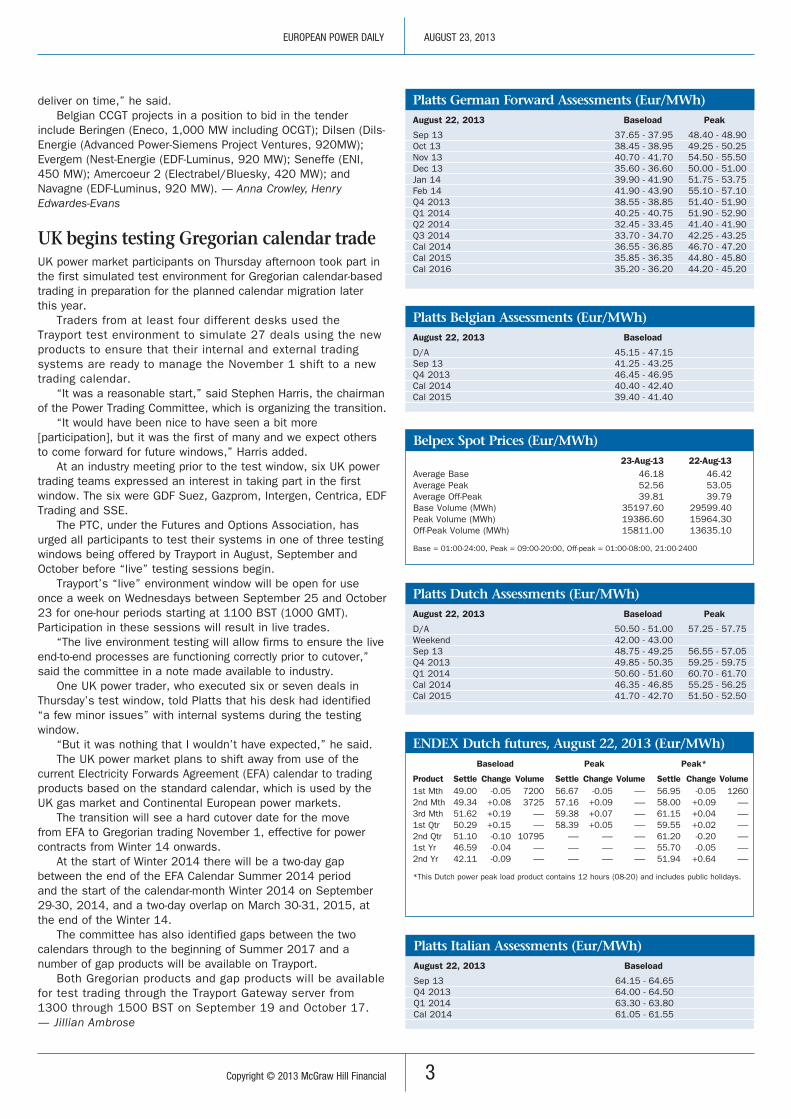

Platts German Forward Assessments (Eur/MWh)August 22, 2013 Baseload Peak

Sep 13 37.65 - 37.95 48.40 - 48.90Oct 13 38.45 - 38.95 49.25 - 50.25Nov 13 40.70 - 41.70 54.50 - 55.50Dec 13 35.60 - 36.60 50.00 - 51.00Jan 14 39.90 - 41.90 51.75 - 53.75Feb 14 41.90 - 43.90 55.10 - 57.10Q4 2013 38.55 - 38.85 51.40 - 51.90Q1 2014 40.25 - 40.75 51.90 - 52.90Q2 2014 32.45 - 33.45 41.40 - 41.90Q3 2014 33.70 - 34.70 42.25 - 43.25Cal 2014 36.55 - 36.85 46.70 - 47.20Cal 2015 35.85 - 36.35 44.80 - 45.80Cal 2016 35.20 - 36.20 44.20 - 45.20

Platts Belgian Assessments (Eur/MWh)August 22, 2013 Baseload

D/A 45.15 - 47.15Sep 13 41.25 - 43.25Q4 2013 46.45 - 46.95Cal 2014 40.40 - 42.40Cal 2015 39.40 - 41.40

Platts Dutch Assessments (Eur/MWh)August 22, 2013 Baseload Peak

D/A 50.50 - 51.00 57.25 - 57.75Weekend 42.00 - 43.00Sep 13 48.75 - 49.25 56.55 - 57.05Q4 2013 49.85 - 50.35 59.25 - 59.75Q1 2014 50.60 - 51.60 60.70 - 61.70Cal 2014 46.35 - 46.85 55.25 - 56.25Cal 2015 41.70 - 42.70 51.50 - 52.50

Platts Italian Assessments (Eur/MWh)August 22, 2013 Baseload

Sep 13 64.15 - 64.65Q4 2013 64.00 - 64.50Q1 2014 63.30 - 63.80Cal 2014 61.05 - 61.55

Belpex Spot Prices (Eur/MWh) 23-Aug-13 22-Aug-13Average Base 46.18 46.42Average Peak 52.56 53.05Average Off-Peak 39.81 39.79Base Volume (MWh) 35197.60 29599.40Peak Volume (MWh) 19386.60 15964.30Off-Peak Volume (MWh) 15811.00 13635.10

Base = 01:00-24:00, Peak = 09:00-20:00, Off-peak = 01:00-08:00, 21:00-2400

ENDEX Dutch futures, August 22, 2013 (Eur/MWh) Baseload Peak Peak*

Product Settle Change Volume Settle Change Volume Settle Change Volume1st Mth 49.00 -0.05 7200 56.67 -0.05 —- 56.95 -0.05 12602nd Mth 49.34 +0.08 3725 57.16 +0.09 —- 58.00 +0.09 —-3rd Mth 51.62 +0.19 —- 59.38 +0.07 —- 61.15 +0.04 —-1st Qtr 50.29 +0.15 —- 58.39 +0.05 —- 59.55 +0.02 —-2nd Qtr 51.10 -0.10 10795 —- —- —- 61.20 -0.20 —-1st Yr 46.59 -0.04 —- —- —- —- 55.70 -0.05 —-2nd Yr 42.11 -0.09 —- —- —- —- 51.94 +0.64 —-

*This Dutch power peak load product contains 12 hours (08-20) and includes public holidays.

deliver on time,” he said.Belgian CCGT projects in a position to bid in the tender

include Beringen (Eneco, 1,000 MW including OCGT); Dilsen (Dils-Energie (Advanced Power-Siemens Project Ventures, 920MW); Evergem (Nest-Energie (EDF-Luminus, 920 MW); Seneffe (ENI, 450 MW); Amercoeur 2 (Electrabel/Bluesky, 420 MW); and Navagne (EDF-Luminus, 920 MW). — Anna Crowley, Henry Edwardes-Evans

Uk begins testing Gregorian calendar tradeUK power market participants on Thursday afternoon took part in the first simulated test environment for Gregorian calendar-based trading in preparation for the planned calendar migration later this year.

Traders from at least four different desks used the Trayport test environment to simulate 27 deals using the new products to ensure that their internal and external trading systems are ready to manage the November 1 shift to a new trading calendar.

“It was a reasonable start,” said Stephen Harris, the chairman of the Power Trading Committee, which is organizing the transition.

“It would have been nice to have seen a bit more [participation], but it was the first of many and we expect others to come forward for future windows,” Harris added.

At an industry meeting prior to the test window, six UK power trading teams expressed an interest in taking part in the first window. The six were GDF Suez, Gazprom, Intergen, Centrica, EDF Trading and SSE.

The PTC, under the Futures and Options Association, has urged all participants to test their systems in one of three testing windows being offered by Trayport in August, September and October before “live” testing sessions begin.

Trayport’s “live” environment window will be open for use once a week on Wednesdays between September 25 and October 23 for one-hour periods starting at 1100 BST (1000 GMT). Participation in these sessions will result in live trades.

“The live environment testing will allow firms to ensure the live end-to-end processes are functioning correctly prior to cutover,” said the committee in a note made available to industry.

One UK power trader, who executed six or seven deals in Thursday’s test window, told Platts that his desk had identified “a few minor issues” with internal systems during the testing window.

“But it was nothing that I wouldn’t have expected,” he said.The UK power market plans to shift away from use of the

current Electricity Forwards Agreement (EFA) calendar to trading products based on the standard calendar, which is used by the UK gas market and Continental European power markets.

The transition will see a hard cutover date for the move from EFA to Gregorian trading November 1, effective for power contracts from Winter 14 onwards.

At the start of Winter 2014 there will be a two-day gap between the end of the EFA Calendar Summer 2014 period and the start of the calendar-month Winter 2014 on September 29-30, 2014, and a two-day overlap on March 30-31, 2015, at the end of the Winter 14.

The committee has also identified gaps between the two calendars through to the beginning of Summer 2017 and a number of gap products will be available on Trayport.

Both Gregorian products and gap products will be available for test trading through the Trayport Gateway server from 1300 through 1500 BST on September 19 and October 17. — Jillian Ambrose

EuropEan powEr Daily august 23, 2013

4Copyright © 2013 McGraw Hill Financial

Platts to refocus Spanish power assessments

Following a period of consultation, Platts has decided to refocus its Spanish power assessments by concentrating on contract periods with higher liquidity. Effective October 1, 2013, Platts will launch a daily assessment of weekend baseload power and discontinue the existing daily assessments of the less liquid balance-of-month and balance-of-year contracts. Please send comments or questions to [email protected] with copy to [email protected].

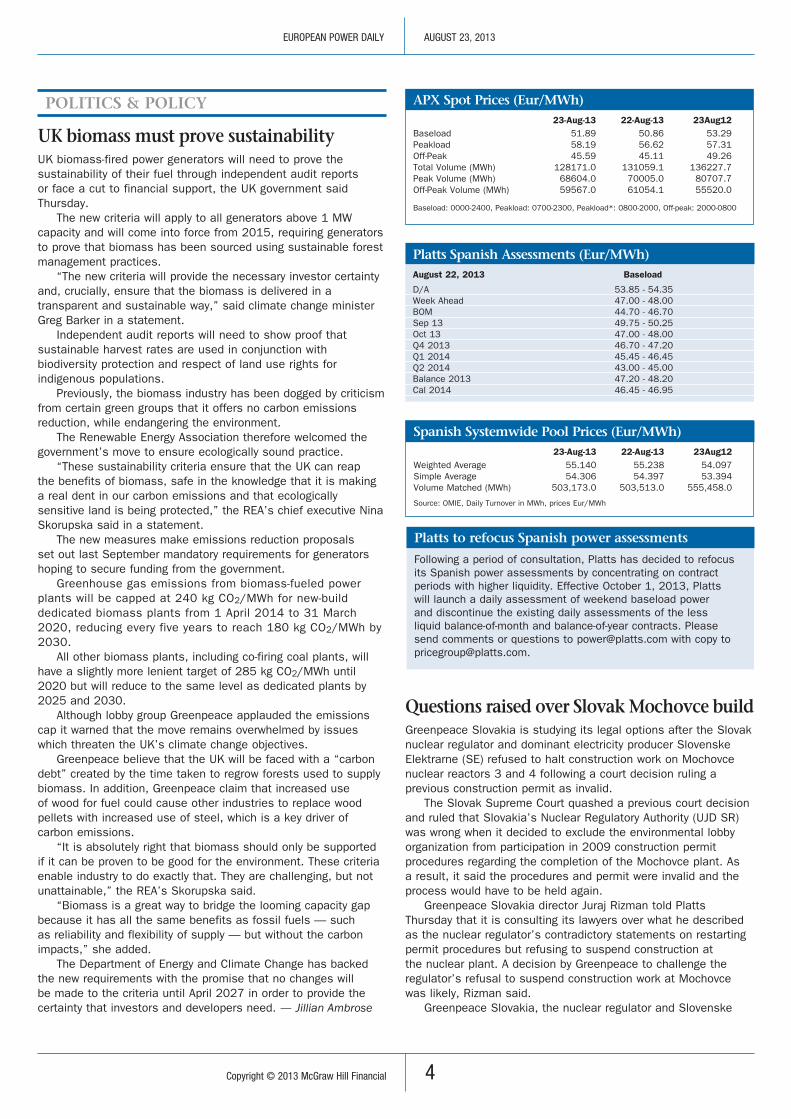

Platts Spanish Assessments (Eur/MWh)August 22, 2013 Baseload

D/A 53.85 - 54.35Week Ahead 47.00 - 48.00BOM 44.70 - 46.70Sep 13 49.75 - 50.25Oct 13 47.00 - 48.00Q4 2013 46.70 - 47.20Q1 2014 45.45 - 46.45Q2 2014 43.00 - 45.00Balance 2013 47.20 - 48.20Cal 2014 46.45 - 46.95

APX Spot Prices (Eur/MWh) 23-Aug-13 22-Aug-13 23Aug12Baseload 51.89 50.86 53.29Peakload 58.19 56.62 57.31Off-Peak 45.59 45.11 49.26Total Volume (MWh) 128171.0 131059.1 136227.7Peak Volume (MWh) 68604.0 70005.0 80707.7Off-Peak Volume (MWh) 59567.0 61054.1 55520.0

Baseload: 0000-2400, Peakload: 0700-2300, Peakload*: 0800-2000, Off-peak: 2000-0800

Spanish Systemwide Pool Prices (Eur/MWh) 23-Aug-13 22-Aug-13 23Aug12Weighted Average 55.140 55.238 54.097Simple Average 54.306 54.397 53.394Volume Matched (MWh) 503,173.0 503,513.0 555,458.0

Source: OMIE, Daily Turnover in MWh, prices Eur/MWh

PolITICS & PolICy

Uk biomass must prove sustainabilityUK biomass-fired power generators will need to prove the sustainability of their fuel through independent audit reports or face a cut to financial support, the UK government said Thursday.

The new criteria will apply to all generators above 1 MW capacity and will come into force from 2015, requiring generators to prove that biomass has been sourced using sustainable forest management practices.

“The new criteria will provide the necessary investor certainty and, crucially, ensure that the biomass is delivered in a transparent and sustainable way,” said climate change minister Greg Barker in a statement.

Independent audit reports will need to show proof that sustainable harvest rates are used in conjunction with biodiversity protection and respect of land use rights for indigenous populations.

Previously, the biomass industry has been dogged by criticism from certain green groups that it offers no carbon emissions reduction, while endangering the environment.

The Renewable Energy Association therefore welcomed the government’s move to ensure ecologically sound practice.

“These sustainability criteria ensure that the UK can reap the benefits of biomass, safe in the knowledge that it is making a real dent in our carbon emissions and that ecologically sensitive land is being protected,” the REA’s chief executive Nina Skorupska said in a statement.

The new measures make emissions reduction proposals set out last September mandatory requirements for generators hoping to secure funding from the government.

Greenhouse gas emissions from biomass-fueled power plants will be capped at 240 kg CO2/MWh for new-build dedicated biomass plants from 1 April 2014 to 31 March 2020, reducing every five years to reach 180 kg CO2/MWh by 2030.

All other biomass plants, including co-firing coal plants, will have a slightly more lenient target of 285 kg CO2/MWh until 2020 but will reduce to the same level as dedicated plants by 2025 and 2030.

Although lobby group Greenpeace applauded the emissions cap it warned that the move remains overwhelmed by issues which threaten the UK’s climate change objectives.

Greenpeace believe that the UK will be faced with a “carbon debt” created by the time taken to regrow forests used to supply biomass. In addition, Greenpeace claim that increased use of wood for fuel could cause other industries to replace wood pellets with increased use of steel, which is a key driver of carbon emissions.

“It is absolutely right that biomass should only be supported if it can be proven to be good for the environment. These criteria enable industry to do exactly that. They are challenging, but not unattainable,” the REA’s Skorupska said.

“Biomass is a great way to bridge the looming capacity gap because it has all the same benefits as fossil fuels — such as reliability and flexibility of supply — but without the carbon impacts,” she added.

The Department of Energy and Climate Change has backed the new requirements with the promise that no changes will be made to the criteria until April 2027 in order to provide the certainty that investors and developers need. — Jillian Ambrose

Questions raised over Slovak Mochovce buildGreenpeace Slovakia is studying its legal options after the Slovak nuclear regulator and dominant electricity producer Slovenske Elektrarne (SE) refused to halt construction work on Mochovce nuclear reactors 3 and 4 following a court decision ruling a previous construction permit as invalid.

The Slovak Supreme Court quashed a previous court decision and ruled that Slovakia’s Nuclear Regulatory Authority (UJD SR) was wrong when it decided to exclude the environmental lobby organization from participation in 2009 construction permit procedures regarding the completion of the Mochovce plant. As a result, it said the procedures and permit were invalid and the process would have to be held again.

Greenpeace Slovakia director Juraj Rizman told Platts Thursday that it is consulting its lawyers over what he described as the nuclear regulator’s contradictory statements on restarting permit procedures but refusing to suspend construction at the nuclear plant. A decision by Greenpeace to challenge the regulator’s refusal to suspend construction work at Mochovce was likely, Rizman said.

Greenpeace Slovakia, the nuclear regulator and Slovenske

EuropEan powEr Daily august 23, 2013

5Copyright © 2013 McGraw Hill Financial

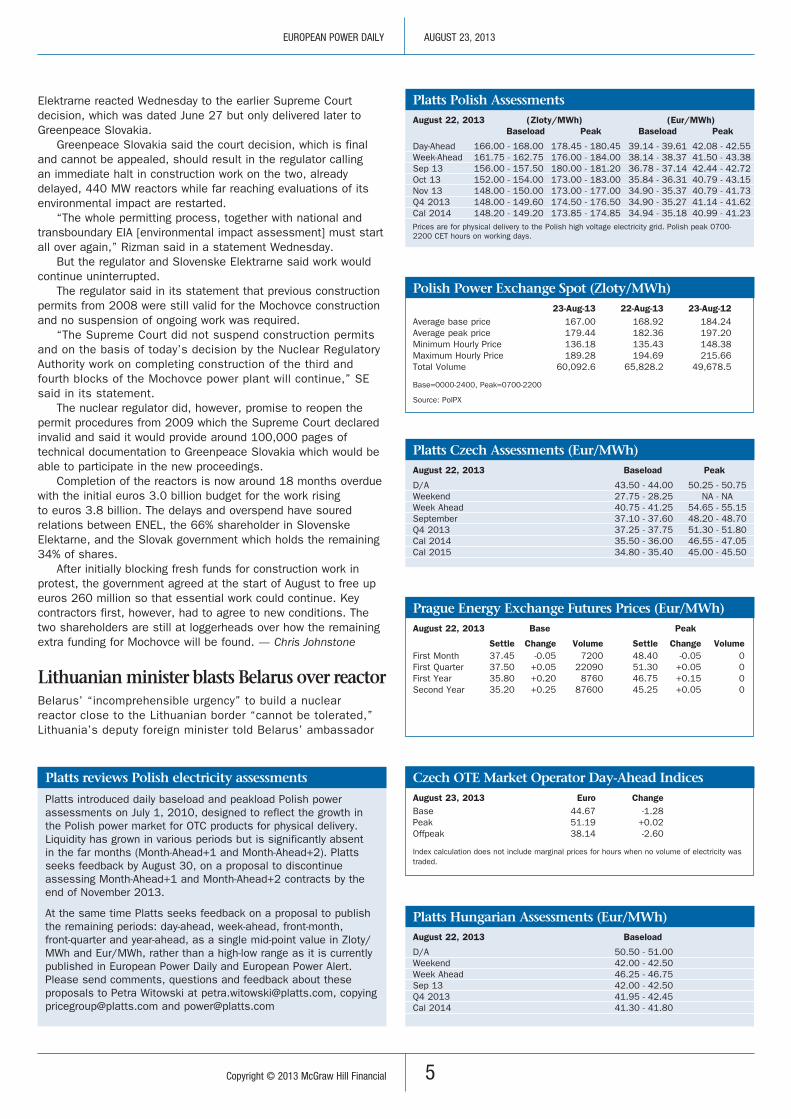

Platts Polish AssessmentsAugust 22, 2013 (Zloty/MWh) (Eur/MWh) Baseload Peak Baseload Peak

Day-Ahead 166.00 - 168.00 178.45 - 180.45 39.14 - 39.61 42.08 - 42.55Week-Ahead 161.75 - 162.75 176.00 - 184.00 38.14 - 38.37 41.50 - 43.38Sep 13 156.00 - 157.50 180.00 - 181.20 36.78 - 37.14 42.44 - 42.72Oct 13 152.00 - 154.00 173.00 - 183.00 35.84 - 36.31 40.79 - 43.15Nov 13 148.00 - 150.00 173.00 - 177.00 34.90 - 35.37 40.79 - 41.73Q4 2013 148.00 - 149.60 174.50 - 176.50 34.90 - 35.27 41.14 - 41.62Cal 2014 148.20 - 149.20 173.85 - 174.85 34.94 - 35.18 40.99 - 41.23Prices are for physical delivery to the Polish high voltage electricity grid. Polish peak 0700-2200 CET hours on working days.

Platts Czech Assessments (Eur/MWh)August 22, 2013 Baseload Peak

D/A 43.50 - 44.00 50.25 - 50.75Weekend 27.75 - 28.25 NA - NAWeek Ahead 40.75 - 41.25 54.65 - 55.15September 37.10 - 37.60 48.20 - 48.70Q4 2013 37.25 - 37.75 51.30 - 51.80Cal 2014 35.50 - 36.00 46.55 - 47.05Cal 2015 34.80 - 35.40 45.00 - 45.50

Platts hungarian Assessments (Eur/MWh)August 22, 2013 Baseload

D/A 50.50 - 51.00Weekend 42.00 - 42.50Week Ahead 46.25 - 46.75Sep 13 42.00 - 42.50Q4 2013 41.95 - 42.45Cal 2014 41.30 - 41.80

Polish Power Exchange Spot (Zloty/MWh) 23-Aug-13 22-Aug-13 23-Aug-12Average base price 167.00 168.92 184.24Average peak price 179.44 182.36 197.20Minimum Hourly Price 136.18 135.43 148.38Maximum Hourly Price 189.28 194.69 215.66Total Volume 60,092.6 65,828.2 49,678.5

Base=0000-2400, Peak=0700-2200

Source: PolPX

Prague Energy Exchange Futures Prices (Eur/MWh)August 22, 2013 Base Peak

Settle Change Volume Settle Change VolumeFirst Month 37.45 -0.05 7200 48.40 -0.05 0First Quarter 37.50 +0.05 22090 51.30 +0.05 0First Year 35.80 +0.20 8760 46.75 +0.15 0Second Year 35.20 +0.25 87600 45.25 +0.05 0

Czech oTE Market operator Day-Ahead IndicesAugust 23, 2013 Euro ChangeBase 44.67 -1.28Peak 51.19 +0.02Offpeak 38.14 -2.60

Index calculation does not include marginal prices for hours when no volume of electricity was traded.

Elektrarne reacted Wednesday to the earlier Supreme Court decision, which was dated June 27 but only delivered later to Greenpeace Slovakia.

Greenpeace Slovakia said the court decision, which is final and cannot be appealed, should result in the regulator calling an immediate halt in construction work on the two, already delayed, 440 MW reactors while far reaching evaluations of its environmental impact are restarted.

“The whole permitting process, together with national and transboundary EIA [environmental impact assessment] must start all over again,” Rizman said in a statement Wednesday.

But the regulator and Slovenske Elektrarne said work would continue uninterrupted.

The regulator said in its statement that previous construction permits from 2008 were still valid for the Mochovce construction and no suspension of ongoing work was required.

“The Supreme Court did not suspend construction permits and on the basis of today’s decision by the Nuclear Regulatory Authority work on completing construction of the third and fourth blocks of the Mochovce power plant will continue,” SE said in its statement.

The nuclear regulator did, however, promise to reopen the permit procedures from 2009 which the Supreme Court declared invalid and said it would provide around 100,000 pages of technical documentation to Greenpeace Slovakia which would be able to participate in the new proceedings.

Completion of the reactors is now around 18 months overdue with the initial euros 3.0 billion budget for the work rising to euros 3.8 billion. The delays and overspend have soured relations between ENEL, the 66% shareholder in Slovenske Elektarne, and the Slovak government which holds the remaining 34% of shares.

After initially blocking fresh funds for construction work in protest, the government agreed at the start of August to free up euros 260 million so that essential work could continue. Key contractors first, however, had to agree to new conditions. The two shareholders are still at loggerheads over how the remaining extra funding for Mochovce will be found. — Chris Johnstone

lithuanian minister blasts Belarus over reactorBelarus’ “incomprehensible urgency” to build a nuclear reactor close to the Lithuanian border “cannot be tolerated,” Lithuania’s deputy foreign minister told Belarus’ ambassador

Platts reviews Polish electricity assessments

Platts introduced daily baseload and peakload Polish power assessments on July 1, 2010, designed to reflect the growth in the Polish power market for OTC products for physical delivery. Liquidity has grown in various periods but is significantly absent in the far months (Month-Ahead+1 and Month-Ahead+2). Platts seeks feedback by August 30, on a proposal to discontinue assessing Month-Ahead+1 and Month-Ahead+2 contracts by the end of November 2013.

At the same time Platts seeks feedback on a proposal to publish the remaining periods: day-ahead, week-ahead, front-month, front-quarter and year-ahead, as a single mid-point value in Zloty/MWh and Eur/MWh, rather than a high-low range as it is currently published in European Power Daily and European Power Alert. Please send comments, questions and feedback about these proposals to Petra Witowski at [email protected], copying [email protected] and [email protected]

EuropEan powEr Daily august 23, 2013

6Copyright © 2013 McGraw Hill Financial

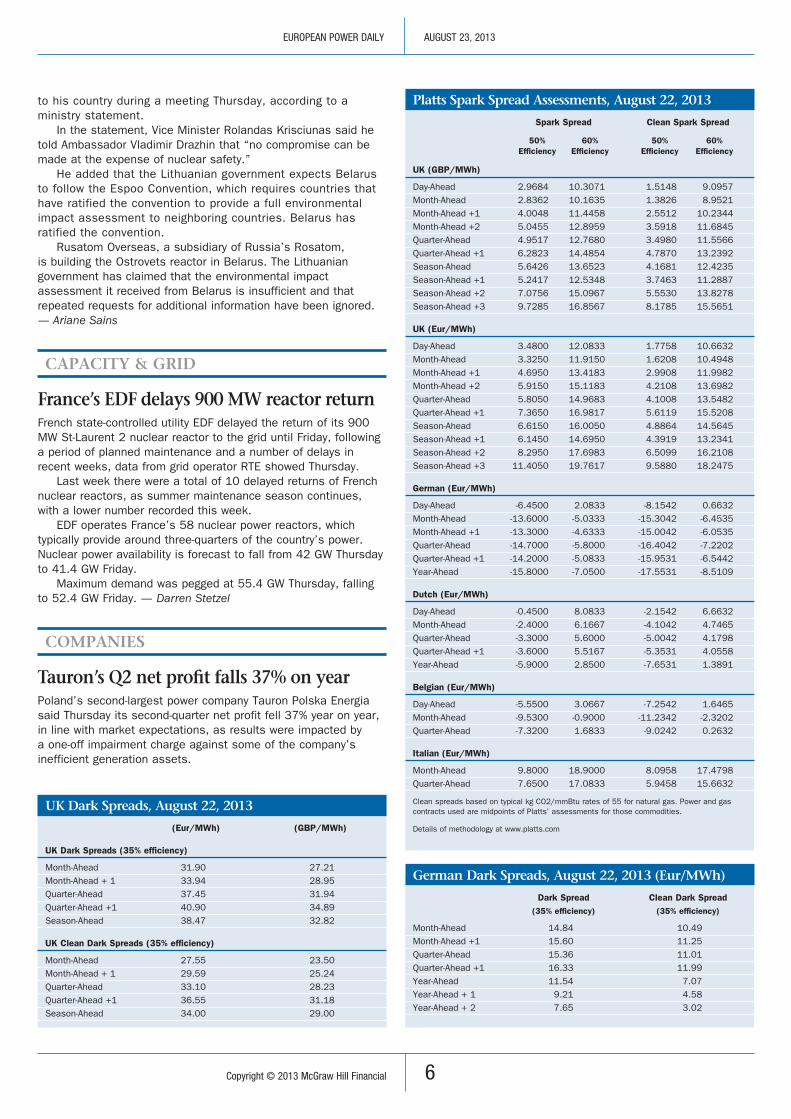

Platts Spark Spread Assessments, August 22, 2013

Spark Spread Clean Spark Spread

50% 60% 50% 60% Efficiency Efficiency Efficiency Efficiency

UK (GBP/MWh)

Day-Ahead 2.9684 10.3071 1.5148 9.0957Month-Ahead 2.8362 10.1635 1.3826 8.9521Month-Ahead +1 4.0048 11.4458 2.5512 10.2344Month-Ahead +2 5.0455 12.8959 3.5918 11.6845Quarter-Ahead 4.9517 12.7680 3.4980 11.5566Quarter-Ahead +1 6.2823 14.4854 4.7870 13.2392Season-Ahead 5.6426 13.6523 4.1681 12.4235Season-Ahead +1 5.2417 12.5348 3.7463 11.2887Season-Ahead +2 7.0756 15.0967 5.5530 13.8278Season-Ahead +3 9.7285 16.8567 8.1785 15.5651

UK (Eur/MWh)

Day-Ahead 3.4800 12.0833 1.7758 10.6632Month-Ahead 3.3250 11.9150 1.6208 10.4948Month-Ahead +1 4.6950 13.4183 2.9908 11.9982Month-Ahead +2 5.9150 15.1183 4.2108 13.6982Quarter-Ahead 5.8050 14.9683 4.1008 13.5482Quarter-Ahead +1 7.3650 16.9817 5.6119 15.5208Season-Ahead 6.6150 16.0050 4.8864 14.5645Season-Ahead +1 6.1450 14.6950 4.3919 13.2341Season-Ahead +2 8.2950 17.6983 6.5099 16.2108Season-Ahead +3 11.4050 19.7617 9.5880 18.2475

German (Eur/MWh)

Day-Ahead -6.4500 2.0833 -8.1542 0.6632Month-Ahead -13.6000 -5.0333 -15.3042 -6.4535Month-Ahead +1 -13.3000 -4.6333 -15.0042 -6.0535Quarter-Ahead -14.7000 -5.8000 -16.4042 -7.2202Quarter-Ahead +1 -14.2000 -5.0833 -15.9531 -6.5442Year-Ahead -15.8000 -7.0500 -17.5531 -8.5109

Dutch (Eur/MWh)

Day-Ahead -0.4500 8.0833 -2.1542 6.6632Month-Ahead -2.4000 6.1667 -4.1042 4.7465Quarter-Ahead -3.3000 5.6000 -5.0042 4.1798Quarter-Ahead +1 -3.6000 5.5167 -5.3531 4.0558Year-Ahead -5.9000 2.8500 -7.6531 1.3891

Belgian (Eur/MWh)

Day-Ahead -5.5500 3.0667 -7.2542 1.6465Month-Ahead -9.5300 -0.9000 -11.2342 -2.3202Quarter-Ahead -7.3200 1.6833 -9.0242 0.2632

Italian (Eur/MWh)

Month-Ahead 9.8000 18.9000 8.0958 17.4798Quarter-Ahead 7.6500 17.0833 5.9458 15.6632

Clean spreads based on typical kg CO2/mmBtu rates of 55 for natural gas. Power and gas contracts used are midpoints of Platts’ assessments for those commodities.

Details of methodology at www.platts.com

German Dark Spreads, August 22, 2013 (Eur/MWh)

Dark Spread Clean Dark Spread (35% efficiency) (35% efficiency)

Month-Ahead 14.84 10.49Month-Ahead +1 15.60 11.25Quarter-Ahead 15.36 11.01Quarter-Ahead +1 16.33 11.99Year-Ahead 11.54 7.07Year-Ahead + 1 9.21 4.58Year-Ahead + 2 7.65 3.02

Uk Dark Spreads, August 22, 2013

(Eur/MWh) (GBP/MWh)

UK Dark Spreads (35% efficiency)

Month-Ahead 31.90 27.21Month-Ahead + 1 33.94 28.95Quarter-Ahead 37.45 31.94Quarter-Ahead +1 40.90 34.89Season-Ahead 38.47 32.82

UK Clean Dark Spreads (35% efficiency)

Month-Ahead 27.55 23.50Month-Ahead + 1 29.59 25.24Quarter-Ahead 33.10 28.23Quarter-Ahead +1 36.55 31.18Season-Ahead 34.00 29.00

to his country during a meeting Thursday, according to a ministry statement.

In the statement, Vice Minister Rolandas Krisciunas said he told Ambassador Vladimir Drazhin that “no compromise can be made at the expense of nuclear safety.”

He added that the Lithuanian government expects Belarus to follow the Espoo Convention, which requires countries that have ratified the convention to provide a full environmental impact assessment to neighboring countries. Belarus has ratified the convention.

Rusatom Overseas, a subsidiary of Russia’s Rosatom, is building the Ostrovets reactor in Belarus. The Lithuanian government has claimed that the environmental impact assessment it received from Belarus is insufficient and that repeated requests for additional information have been ignored. — Ariane Sains

CAPACITy & GrID

France’s EDF delays 900 MW reactor returnFrench state-controlled utility EDF delayed the return of its 900 MW St-Laurent 2 nuclear reactor to the grid until Friday, following a period of planned maintenance and a number of delays in recent weeks, data from grid operator RTE showed Thursday.

Last week there were a total of 10 delayed returns of French nuclear reactors, as summer maintenance season continues, with a lower number recorded this week.

EDF operates France’s 58 nuclear power reactors, which typically provide around three-quarters of the country’s power. Nuclear power availability is forecast to fall from 42 GW Thursday to 41.4 GW Friday.

Maximum demand was pegged at 55.4 GW Thursday, falling to 52.4 GW Friday. — Darren Stetzel

CoMPANIES

Tauron’s Q2 net profit falls 37% on yearPoland’s second-largest power company Tauron Polska Energia said Thursday its second-quarter net profit fell 37% year on year, in line with market expectations, as results were impacted by a one-off impairment charge against some of the company’s inefficient generation assets.

EuropEan powEr Daily august 23, 2013

7Copyright © 2013 McGraw Hill Financial

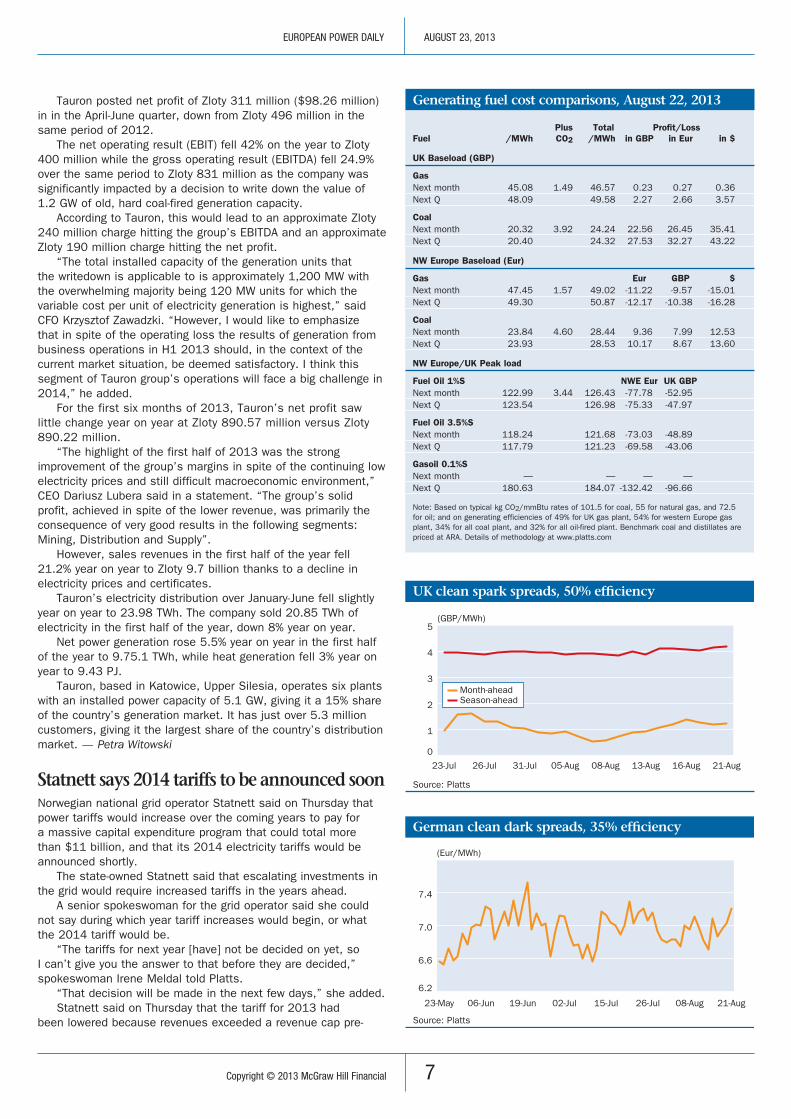

Generating fuel cost comparisons, August 22, 2013

Plus Total Profit/LossFuel /MWh CO2 /MWh in GBP in Eur in $

UK Baseload (GBP)

GasNext month 45.08 1.49 46.57 0.23 0.27 0.36Next Q 48.09 49.58 2.27 2.66 3.57

CoalNext month 20.32 3.92 24.24 22.56 26.45 35.41Next Q 20.40 24.32 27.53 32.27 43.22

NW Europe Baseload (Eur)

Gas Eur GBP $Next month 47.45 1.57 49.02 -11.22 -9.57 -15.01Next Q 49.30 50.87 -12.17 -10.38 -16.28

CoalNext month 23.84 4.60 28.44 9.36 7.99 12.53Next Q 23.93 28.53 10.17 8.67 13.60

NW Europe/UK Peak load

Fuel Oil 1%S NWE Eur UK GBPNext month 122.99 3.44 126.43 -77.78 -52.95Next Q 123.54 126.98 -75.33 -47.97

Fuel Oil 3.5%SNext month 118.24 121.68 -73.03 -48.89Next Q 117.79 121.23 -69.58 -43.06

Gasoil 0.1%SNext month — — — —Next Q 180.63 184.07 -132.42 -96.66

Note: Based on typical kg CO2/mmBtu rates of 101.5 for coal, 55 for natural gas, and 72.5 for oil; and on generating efficiencies of 49% for UK gas plant, 54% for western Europe gas plant, 34% for all coal plant, and 32% for all oil-fired plant. Benchmark coal and distillates are priced at ARA. Details of methodology at www.platts.com

(Eur/MWh)

German clean dark spreads, 35% efficiency

Source: Platts

6.2

6.6

7.0

7.4

21-Aug08-Aug26-Jul15-Jul02-Jul19-Jun06-Jun23-May

Tauron posted net profit of Zloty 311 million ($98.26 million) in in the April-June quarter, down from Zloty 496 million in the same period of 2012.

The net operating result (EBIT) fell 42% on the year to Zloty 400 million while the gross operating result (EBITDA) fell 24.9% over the same period to Zloty 831 million as the company was significantly impacted by a decision to write down the value of 1.2 GW of old, hard coal-fired generation capacity.

According to Tauron, this would lead to an approximate Zloty 240 million charge hitting the group’s EBITDA and an approximate Zloty 190 million charge hitting the net profit.

“The total installed capacity of the generation units that the writedown is applicable to is approximately 1,200 MW with the overwhelming majority being 120 MW units for which the variable cost per unit of electricity generation is highest,” said CFO Krzysztof Zawadzki. “However, I would like to emphasize that in spite of the operating loss the results of generation from business operations in H1 2013 should, in the context of the current market situation, be deemed satisfactory. I think this segment of Tauron group’s operations will face a big challenge in 2014,” he added.

For the first six months of 2013, Tauron’s net profit saw little change year on year at Zloty 890.57 million versus Zloty 890.22 million.

“The highlight of the first half of 2013 was the strong improvement of the group’s margins in spite of the continuing low electricity prices and still difficult macroeconomic environment,” CEO Dariusz Lubera said in a statement. “The group’s solid profit, achieved in spite of the lower revenue, was primarily the consequence of very good results in the following segments: Mining, Distribution and Supply”.

However, sales revenues in the first half of the year fell 21.2% year on year to Zloty 9.7 billion thanks to a decline in electricity prices and certificates.

Tauron’s electricity distribution over January-June fell slightly year on year to 23.98 TWh. The company sold 20.85 TWh of electricity in the first half of the year, down 8% year on year.

Net power generation rose 5.5% year on year in the first half of the year to 9.75.1 TWh, while heat generation fell 3% year on year to 9.43 PJ.

Tauron, based in Katowice, Upper Silesia, operates six plants with an installed power capacity of 5.1 GW, giving it a 15% share of the country’s generation market. It has just over 5.3 million customers, giving it the largest share of the country’s distribution market. — Petra Witowski

Statnett says 2014 tariffs to be announced soonNorwegian national grid operator Statnett said on Thursday that power tariffs would increase over the coming years to pay for a massive capital expenditure program that could total more than $11 billion, and that its 2014 electricity tariffs would be announced shortly.

The state-owned Statnett said that escalating investments in the grid would require increased tariffs in the years ahead.

A senior spokeswoman for the grid operator said she could not say during which year tariff increases would begin, or what the 2014 tariff would be.

“The tariffs for next year [have] not be decided on yet, so I can’t give you the answer to that before they are decided,” spokeswoman Irene Meldal told Platts.

“That decision will be made in the next few days,” she added.Statnett said on Thursday that the tariff for 2013 had

been lowered because revenues exceeded a revenue cap pre-

(GBP/MWh)

UK clean spark spreads, 50% efficiency

Source: Platts

0

1

2

3

4

5

21-Aug16-Aug13-Aug08-Aug05-Aug31-Jul26-Jul23-Jul

Month-ahead Season-ahead

EuropEan powEr Daily august 23, 2013

8Copyright © 2013 McGraw Hill Financial

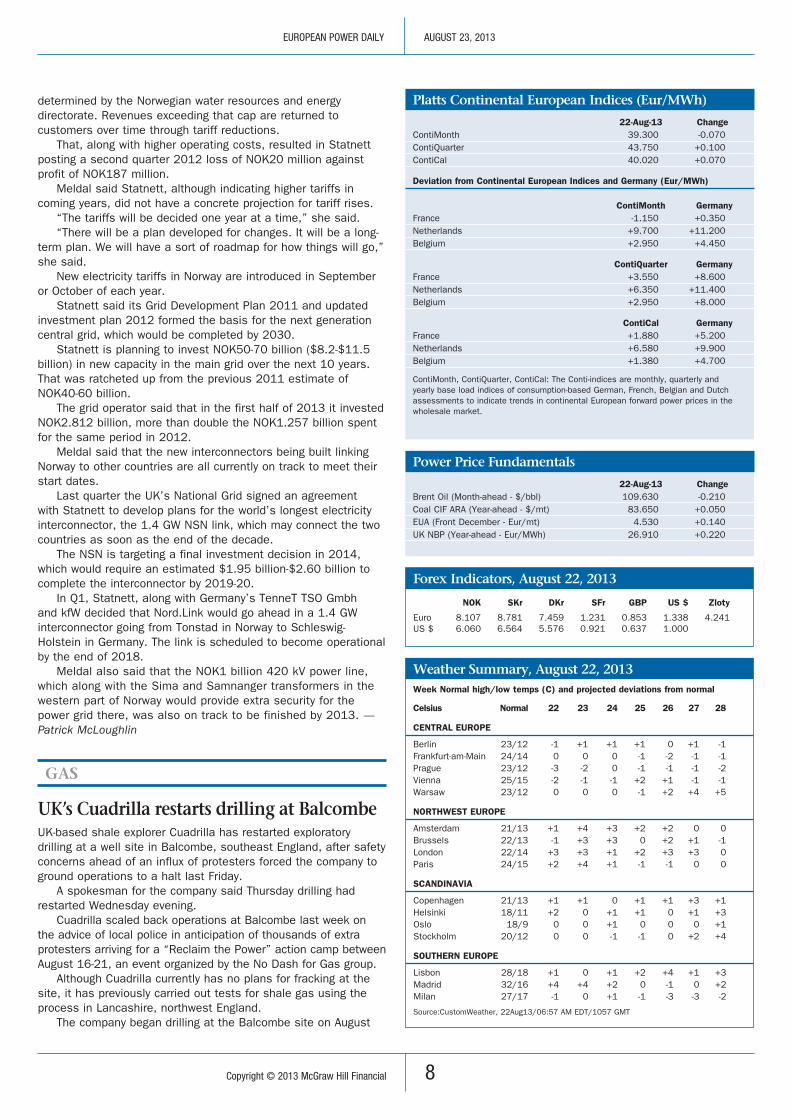

Platts Continental European Indices (Eur/MWh)

22-Aug-13 ChangeContiMonth 39.300 -0.070ContiQuarter 43.750 +0.100ContiCal 40.020 +0.070

Deviation from Continental European Indices and Germany (Eur/MWh)

ContiMonth GermanyFrance -1.150 +0.350Netherlands +9.700 +11.200Belgium +2.950 +4.450

ContiQuarter GermanyFrance +3.550 +8.600Netherlands +6.350 +11.400Belgium +2.950 +8.000

ContiCal GermanyFrance +1.880 +5.200Netherlands +6.580 +9.900Belgium +1.380 +4.700

ContiMonth, ContiQuarter, ContiCal: The Conti-indices are monthly, quarterly and yearly base load indices of consumption-based German, French, Belgian and Dutch assessments to indicate trends in continental European forward power prices in the wholesale market.

Forex Indicators, August 22, 2013

NOK SKr DKr SFr GBP US $ Zloty

Euro 8.107 8.781 7.459 1.231 0.853 1.338 4.241US $ 6.060 6.564 5.576 0.921 0.637 1.000

Weather Summary, August 22, 2013Week Normal high/low temps (C) and projected deviations from normal

Celsius Normal 22 23 24 25 26 27 28

CENTRAL EUROPE

Berlin 23/12 -1 +1 +1 +1 0 +1 -1Frankfurt-am-Main 24/14 0 0 0 -1 -2 -1 -1Prague 23/12 -3 -2 0 -1 -1 -1 -2Vienna 25/15 -2 -1 -1 +2 +1 -1 -1Warsaw 23/12 0 0 0 -1 +2 +4 +5

NORTHWEST EUROPE

Amsterdam 21/13 +1 +4 +3 +2 +2 0 0Brussels 22/13 -1 +3 +3 0 +2 +1 -1London 22/14 +3 +3 +1 +2 +3 +3 0Paris 24/15 +2 +4 +1 -1 -1 0 0

SCANDINAVIA

Copenhagen 21/13 +1 +1 0 +1 +1 +3 +1Helsinki 18/11 +2 0 +1 +1 0 +1 +3Oslo 18/9 0 0 +1 0 0 0 +1Stockholm 20/12 0 0 -1 -1 0 +2 +4

SOUTHERN EUROPE

Lisbon 28/18 +1 0 +1 +2 +4 +1 +3Madrid 32/16 +4 +4 +2 0 -1 0 +2Milan 27/17 -1 0 +1 -1 -3 -3 -2

Source:CustomWeather, 22Aug13/06:57 AM EDT/1057 GMT

determined by the Norwegian water resources and energy directorate. Revenues exceeding that cap are returned to customers over time through tariff reductions.

That, along with higher operating costs, resulted in Statnett posting a second quarter 2012 loss of NOK20 million against profit of NOK187 million.

Meldal said Statnett, although indicating higher tariffs in coming years, did not have a concrete projection for tariff rises.

“The tariffs will be decided one year at a time,” she said.“There will be a plan developed for changes. It will be a long-

term plan. We will have a sort of roadmap for how things will go,” she said.

New electricity tariffs in Norway are introduced in September or October of each year.

Statnett said its Grid Development Plan 2011 and updated investment plan 2012 formed the basis for the next generation central grid, which would be completed by 2030.

Statnett is planning to invest NOK50-70 billion ($8.2-$11.5 billion) in new capacity in the main grid over the next 10 years. That was ratcheted up from the previous 2011 estimate of NOK40-60 billion.

The grid operator said that in the first half of 2013 it invested NOK2.812 billion, more than double the NOK1.257 billion spent for the same period in 2012.

Meldal said that the new interconnectors being built linking Norway to other countries are all currently on track to meet their start dates.

Last quarter the UK’s National Grid signed an agreement with Statnett to develop plans for the world’s longest electricity interconnector, the 1.4 GW NSN link, which may connect the two countries as soon as the end of the decade.

The NSN is targeting a final investment decision in 2014, which would require an estimated $1.95 billion-$2.60 billion to complete the interconnector by 2019-20.

In Q1, Statnett, along with Germany’s TenneT TSO Gmbh and kfW decided that Nord.Link would go ahead in a 1.4 GW interconnector going from Tonstad in Norway to Schleswig-Holstein in Germany. The link is scheduled to become operational by the end of 2018.

Meldal also said that the NOK1 billion 420 kV power line, which along with the Sima and Samnanger transformers in the western part of Norway would provide extra security for the power grid there, was also on track to be finished by 2013. — Patrick McLoughlin

GAS

Uk’s Cuadrilla restarts drilling at BalcombeUK-based shale explorer Cuadrilla has restarted exploratory drilling at a well site in Balcombe, southeast England, after safety concerns ahead of an influx of protesters forced the company to ground operations to a halt last Friday.

A spokesman for the company said Thursday drilling had restarted Wednesday evening.

Cuadrilla scaled back operations at Balcombe last week on the advice of local police in anticipation of thousands of extra protesters arriving for a “Reclaim the Power” action camp between August 16-21, an event organized by the No Dash for Gas group.

Although Cuadrilla currently has no plans for fracking at the site, it has previously carried out tests for shale gas using the process in Lancashire, northwest England.

The company began drilling at the Balcombe site on August

Power Price Fundamentals

22-Aug-13 Change Brent Oil (Month-ahead - $/bbl) 109.630 -0.210Coal CIF ARA (Year-ahead - $/mt) 83.650 +0.050EUA (Front December - Eur/mt) 4.530 +0.140UK NBP (Year-ahead - Eur/MWh) 26.910 +0.220

EuropEan powEr Daily august 23, 2013

9Copyright © 2013 McGraw Hill Financial

To reach Platts

E-mail:[email protected]

North America

Tel:800-PLATTS-8

Latin America

Tel:+54-11-4121-4810

Europe & Middle East

Tel:+44-20-7176-6111

Asia Pacific

Tel:+65-6530-6430

European Power Daily is published daily Monday-Friday except for UK public holidays, by Platts, a division of McGraw Hill Financial, registered office: 20 Canada Square, Canary Wharf, England, E14 5LH.

Officers of the Corporation: Harold McGraw III, Chairman, President and Chief Executive Officer; Kenneth Vittor, Executive Vice President and General Counsel; Jack F. Callahan, Jr., Executive Vice President and Chief Financial Officer; Elizabeth O’Melia, Senior Vice President, Treasury Operations.

Prices, indexes, assessments and other price information published herein are based on material collected from actual market participants. Platts makes no warranties, express or implied, as to the accuracy, adequacy or com-pleteness of the data and other information set forth in this publication (‘data’) or as to the merchantability or fitness for a particular use of the data. Platts assumes no liability in connection with any party’s use of the data. Corporate policy prohibits editorial personnel from holding any financial interest in companies they cover and from disclosing information prior to the publication date of an issue.

Copyright © 2013 by Platts, McGraw Hill Financial

Permission is granted for those registered with the Copyright Clearance Center (CCC) to photocopy material herein for internal reference or personal use only, provided that appropriate payment is made to the CCC, 222 Rosewood Drive, Danvers, MA 01923, phone (978) 750-8400. Reproduction in any other form, or for any other purpose, is forbidden without express permission of McGraw Hill Financial. For article reprints contact: The YGS Group, phone +1-717-505-9701 x105. Text-only archives available on Dialog File 624, Data Star, Factiva, LexisNexis, and Westlaw.

Power EditorsAnna Crowley, Andreas Franke, Petra Witowski, Jillian Ambrose, Darren Stetzel, Beatrice Bedeschi

Emissions EditorFrank Watson

London [email protected]

Global Editorial Director, PowerSarah Cottle

Manager, Advertisement SalesKacey Comstock

Volume 15 / Issue 164 / August 23, 2013

Vice President, EditorialDan Tanz

Platts PresidentLarry Neal

ISSN:

Advertising

Tel : +1-720-548-5508

Platts is a trademark of McGraw Hill Financial

1556-3243

EUROPEAN POWER DAILY

2, targeting possible shale oil resources. It has all the relevant permits to conduct its exploratory operations at Balcombe.

The test drilling has, however, attracted protesters to the area who have attempted to delay or halt operations by blocking deliveries to the site, with some supergluing themselves to each other at the entrance.

A spokeswoman for No Dash for Gas said Thursday the ongoing protest camp outside the drilling site will continue, despite the big Reclaim the Power camp having been taken down.

“We expect a lot of people who were at the Reclaim the Power [camp] and our supporters to come back to Balcombe in the coming months and continue supporting the local opposition to dangerous drilling,” she added.

No Dash for Gas has previously said it shares “serious concerns about the environmental and social impact of fossil fuel extraction in the area,” adding that Balcombe was a test for the fracking industry and could lead to “an estimated two-thirds of the UK being covered by fracking rigs.”

Anti-fossil fuel activists also forced their way into Cuadrilla’s head office on Monday and targeted the company’s PR firm in an effort to step up their resistance against fracking. — Geraldine Anderson

MArkET CoMMENT

European Power Markets

Uk prompt holds firm on lower nuclearPrompt prices held steady Thursday as lower demand and stronger wind generation will be partially offset by lower nuclear power generation and rising NBP gas prices, market sources said.

On the OTC market day-ahead baseload was last heard midday at GBP47/MWh, flat on day, while peakload power eased back 65 pence to GBP54/MWh.

The N2EX day-ahead baseload power auction was also relatively unchanged on day, outturning at GBP47.22/MWh from Wednesday’s GBP47.23/MWh result.

EDF Energy transparency data show that its 550 MW Dungeness B-22 unit will have an availability of 203 MW Friday as it lowers output for planned offload refuelling, which will reduce total nuclear power generation from near maximum levels

of over 9 GW seen over the past week turning the generation mix towards increased use of more expensive gas-fired power.

Lower nuclear output on Friday will offset the expected increase in wind generation from below 300 MW midday Thursday to above 1.5 GW forecast for Friday.

Power prices were also supported by rising NBP gas prompt prices as the supply-side tightened with lower gas imports from the Netherlands via the BBL gas pipeline.

The within-day gas contract at 09:30 BST was valued at 64.60 pence/therm, having gained 0.60 p/th from Wednesday’s close, and the day-ahead price had pushed up by 0.30 p/th to 64.50 p/th.

Weekend gas prices were also higher, driving 65 pence gains on the weekend baseload contract which was last heard at GBP43.50/MWh at midday.

Gains persisted through the forward curve with September baseload rising 50 pence to GBP46.80/MWh while Winter 13 base gained 25 pence to GBP53.70/MWh.

German September near five-month highGerman day-ahead power prices inched lower Thursday on the back of the typical drop in demand on a Friday afternoon and increased wind power output, while planned and unplanned plant outages and a lower solar forecast kept supply tight, especially during late morning hours, according to sources.

Day-ahead baseload was last heard trading at Eur44.75/MWh, Eur1.25 lower on the day, while day-ahead peakload dropped 60 euro cent to Eur51.25/MWh.

The Epex Spot exchange cleared day-ahead prices above OTC, but down on the day at Eur45.94/MWh baseload and Eur52.56/MWh peakload.

Hours 8-11 were most expensive on the exchange, clearing above Eur60/MWh, compared to none above Eur60/MWh in the previous three sessions.

EEX transparency data showed overall stable baseload availability day-on-day, with 17 GW at Germany’s lignite plants Friday, 10.5 GW at the country’s hard coal units and 9.3 GW at the nuclear fleet with a number of unplanned nuclear and lignite outages expected to last into next week.

In renewables supply, wind power generation was forecast to more than double to 2.7 GW for average baseload hours Friday, while solar output was estimated to drop to a peakload average

EuropEan powEr Daily august 23, 2013

10Copyright © 2013 McGraw Hill Financial

of 10 GW, according to market sources.On the curve, September baseload added just 5 euro cent

on the day to Eur37.80/MWh, still the highest close for a front-month contract since late March, Platts data shows.

At the far end, Cal 14 base firmed 10 euro cent to Eur36.70/MWh, its highest close in a week.

In power-related commodities, EUA emissions allowances moved up 14 euro cent to Eur4.53/mt for the Dec 13 contract, while year-ahead coal into Europe added $0.15 to close at $83.75/mt.

French prompt lower after surge WednesdayFrench prompt power prices moved lower Thursday after an upward surge in Wednesday’s session, while the supply situation remained steady on the day with no new developments on the nuclear front and typically lower Friday prices added a little extra weight, market sources said.

Baseload power for delivery Friday closed Eur2.25 lower on the day at Eur43.25/MWh Thursday, with peakload down 25 euro cent at Eur51.25/MWh. Epex Spot settled the same contracts at Eur45.26/MWh and Eur52.31/MWh.

Traders said the downward move was a natural reaction to a strong upward move the previous day, and that it is also not unusual for the price for Friday to weaken ahead of the weekend.

The latest RTE data showed that EDF has delayed the return of its 900 MW St-Laurent 2 nuclear reactor to the grid by one day until Friday, following a period of planned maintenance and a number of delays in recent weeks.

Nuclear power availability is forecast to fall from 42 GW Thursday to 41.4 GW Friday, with maximum demand pegged at 55.4 GW Thursday, falling to 52.4 GW Friday.

The latest CustomWeather data showed that temperatures in Paris will rise by 2 degrees Celsius overnight to 4 C above the 15-25 C seasonal norm Friday, and increasing by 3 C to 4 C above the seasonal norm of 13-21 C in Amsterdam, the Netherlands.

The Dutch day-ahead baseload contract closed Eur1 lower than the previous close at Eur50.75/MWh, while peakload was up 75 euro cent at Eur57.50/MWh. APX settled the same contracts at Eur51.89/MWh and Eur58.19/MWh.

Further forward, baseload power for delivery in September was down 25 euro cent on the day at Eur38.15/MWh, while the Dutch price closed flat at Eur49/MWh. The French front-quarter was unchanged at Eur47.30/MWh, and the Dutch contract was down by just 5 euro cent at Eur50.10/MWh.

Meanwhile, core contract German Cal 14 was up 10 euro cent on the day at Eur36.70/MWh, and the French equivalent was up 5 euro cent to Eur41.90/MWh. The Dutch contract was up 5 euro cent to Eur46.60/MWh.

CEE prompt down on plant return, wind boostCzech and Hungarian day-ahead power prices eased Thursday as the expected return of a Hungarian power block and strengthening wind power output boosted supply, sources said.

Hungarian day-ahead base changed hands OTC at Eur50.75/MWh, Eur2.50 lower on the day but remained at a Eur7 premium to its Czech counterpart.

Czech baseload power for Friday delivery was heard trading OTC at Eur43.75/MWh before midday London time, down Eur1.50 euro on the day, while the corresponding peakload contract was unchanged on the day at Eur50.50/MWh.

Meanwhile, exchange settlements outturned above OTC in

both markets with OTE and OKTE clearing Czech and Slovakian day-ahead base Eur44.67/MWh and peak Eur51.19/MWH, while HUPX settled Hungarian day-ahead base at Eur52.02/MWh and peak Eur63.60/MWh.

“Borders are open and wind power is in good condition,” said a Czech trader. According to a market source, German wind power generation was forecast to rise to nearly 3 GW Friday while solar output was set to fall to 10 GW for average peakload hours.

Prices remain at a slight premium in Hungary as plant outages continue to tighten supply, although a 232 MW Matra-5 coal-fired power plant unit is scheduled to return to the grid Friday morning after shutting down in an unplanned outage Tuesday, according to Mavir data. In addition, a 500 MW reactor at Hungary’s 2 GW nuclear power plant Paks remained offline with no indication of when the reactor is likely to return to service, although one market source said it may return to the grid by the end of the week.

While capacity flows from Austria into Hungary remain at healthy levels, prices have eased from the highs seen earlier in the week, peaking at Eur14.91/MWh for hour 20, CAO data shows.

CustomWeather pegged temperatures in Prague up to 2 degrees Celsius below seasonal norms of 12/23 C Friday through to next Wednesday, while temperatures in Budapest were forecast to rise from the seasonal norm of 14/27 C Friday to 5 C above the average by Tuesday.

Further out on the prompt, week-ahead prices saw little change after strong gains Wednesday, which surprised many traders.

“Next week the weather will be a little lower so consumption should not be so high,” said a Hungarian trader. Hungarian baseload power for week 35 traded flat on the day at Eur46.50/MWh while its Czech counterpart eased 60 euro cent to Eur41/MWh, still around 2 euros above where the contracts where trading Monday.

On the curve, September baseload contracts softened 15 euro cent in both markets to Eur42.25/MWh in Hungary and Eur37.35/MWh in the Czech Republic.

Further forward, year-ahead power prices gained 15 euro cent to close at Eur41.55/MWh in Hungary and Eur35.75/MWh in the Czech market.

Polish September hits fresh highPolish power prices for September delivery continued to climb to fresh highs Thursday on the back of the bullish prompt amid revised weather forecasts, sources said.

September base was valued at Zloty 156.75/MWh, up 50 grosz on the day and more than a Zloty higher than where the contract was trading on Monday.

The September peakload contract moved 60 grosz higher on the day to Zloty 180.60/MWh, rising more than 3 Zloty this week.

In addition, front-month contracts closed at a seven-month-high, Platts data shows, triggered by bullish prompt prices seen this month.

“Prices on the spot have risen and there’s the possibility of additional exports,” said a trader, adding that “the weather may also be warmer and there may be less wind”.

Meanwhile, prompt power prices softened Thursday as strong power exports to neighboring markets were offset by typically lower Friday demand, sources said.

With no day-ahead trades heard OTC, Poland’s POLPX settled Friday base at Zloty 167/MWh, nearly 2 Zloty lower on the day, while day-ahead peak cleared at Zloty 179.45/MWh, nearly 3 Zloty lower on the day.

EuropEan powEr Daily august 23, 2013

11Copyright © 2013 McGraw Hill Financial

“Exports are still profitable, especially to Germany,” said a trader. “It’s all going to Germany, which is sending more power to France because there’s some tightness there”.

Power exports allocated in the daily auction to neighboring countries were expected to reach up to 1,600 MW Friday morning before receding back to 400-500 MW during peak midday hours, data from the grid operator shows, narrowing capacity supply margins below 1 GW during hours of peak demand, which was pegged at 20 GW for hour 13.

Wind power generation was forecast to rise from negligible levels Thursday to 450 MW Friday, according to a market source.

Meanwhile, CustomWeather pegged temperatures in Warsaw in line with the seasonal average of 12/23 degrees Celsius Friday and Saturday but would rise up to 5 C above the norm by Wednesday.

Also on the prompt, week-ahead base was heard trading in a single clip at Zloty 162.25/MWh, up Zloty 1.25 higher on the day.

Further forward, Cal 14 base gained 30 grosz on the day to close at Zloty 148.70/MWh while the peakload contract was heard 35 grosz higher at Zloty 174.35/MWh.

Prompt holds above Eur50/MWh as wind dipsSpanish prompt power prices held firmly above Eur50/MWh Thursday as wind was forecast below 1 GW during peak demand hours, offsetting weaker Friday demand, with costlier coal and CCGT generation continuing to make up the shortfall, sources said.

Baseload power for next-day delivery was little changed day-on-day, assessed 15 euro cent lower at Eur54.10/MWh. The OMIE exchange settled Friday contracts a touch above OTC at Eur54.31/MWh.

Red Electrica data showed forecast wind generation falling below a gigawatt Friday morning and into the early afternoon, pegged between 705-MW and 930 MW for hours 10-14.

Peak demand was seen around 900 MW lower day-on-day, grid data showed, estimated at 34.2 GW for hour 14 Friday, against 35.1 GW for the same hour Thursday.

Changing fundamentals expected over the weekend and into week 35 saw a downward shift in week-ahead baseload prices, which shed a euro on the day to close at Eur47.50/MWh amid below-average volumes.

“Demand will start to tick up going into September and wind will be above 6 GW on Saturday and Sunday so maybe we’ll have a bit more wind next week,” a trading source said.

Further forward, prices were little moved on the day with the stable day-ahead market resulting in a largely stagnant curve. September baseload was unchanged by close at Eur50/MWh.

“The spot has been more or less in line with OTC expectations so we’re not seeing much change,” the trader said.

At the far end, Cal 14 was assessed 10 euro cent below Wednesday’s close at Eur46.70/MWh.

low PUN weighs on Italian front-monthItalian power prices were mixed Thursday, with the front-month falling in line with IPEX and the curve rising, lifted by movements in the euro-dollar exchange rate, according to trading sources.

The September edged 35 euro cent lower to close at Eur64.40/MWh. The Q4’13 and Cal 14 contracts posted gains of 10 and 5 euro cent respectively, ending the trading session at Eur64.25/MWh and Eur61.30/MWh, while Q1’14 was assessed flat at Eur63.55/MWh.

“August has delivered lower than expected” one trader said, adding that as a consequence the September was losing value.

Gains on the curve contradicted slightly bearish oil prices, as the Brent October crude fell by $0.21/barrel to close at $109.63/barrel.

The PUN - single national purchasing day-ahead price - was little changed on IPEX’s exchange, rising by just around 80 euro cent and settling at Eur64.63/MWh, with minimum and maximum hourly price of Eur53.31/MWh and Eur93/MWh.

That brought the average August PUN to Eur65.64/MWh, down by Eur1.22 on-month.

Zonal selling prices in the centre-north, centre-south, south and Sardinia settled at Eur60.45/MWh, in the north at Eur60.86/MWh and in Sicily at Eur110.55/MWh.

On the coupled northern Italy-Slovenia market zone, the maximum hourly price in northern Italy was Eur85.03/MWh for hour 21, in the Slovenian BSP market Eur71.85/MWh for the same hour.

Power demand was expected to reach an hourly peak of 35.61 GW for 21, according to GME’s forecasts.

Temperatures in Milan and Rome were expected to be between 19/29 and 21/31 degrees Celsius on Friday, the weather forecast of Italian newswire ANSA reported.

EUA Market

Dec 13 EUAs at 2 week high of Eur4.53/mtEU Allowances broke out of tightly rangebound trade over previous trading sessions to rally to two week highs Thursday as speculative market participants covered short positions amid rising commodity prices, market sources said.

December 2013 EUAs opened the day just slightly higher than Wednesday’s Eur4.39/mt close and remained a touch above the Eur4.40 mark over much of the morning until a bullish auction result spurred pricing levels higher.

The EU sold 1.7685 million carbon dioxide allowances at auction for Eur4.43/mt ($5.62/mt) through Germany’s European Energy Exchange, on behalf of 24 EU member state governments.

The minimum and maximum bids in the auction were Eur1.99/mt and Eur4.50/mt, respectively, according to EEX data.

The total number of bids received was enough to cover 10.398 million EUAs, giving a cover ratio of 5.88, the exchange said, well above an average of 2.97 based on all EU auctions so far this year.

“The auction cleared several cents above the market and [attracted] a very healthy bid to cover,” a carbon trader told Platts.

Pricing levels on the Dec 13 contract rallied from Eur4.41/mt to Eur4.47/mt on ICE in the 5 minutes following the auction, and remained at strong levels before breaking through the Eur4.50 mark late in the session.

The trader attributed the bullish day to positioning among speculative market players.

“Perhaps part of the speculative community expected us to break [below] Eur4.30/mt which has been a strong support level in recent weeks. It didn’t happen so [this] could be some short covering,” he said.

Another trader pointed to the uptick in energy commodity prices as key drivers of the day’s gains.

“It’s still fairly rangebound though,” he added.The Dec 13 EUA contract lifted to Eur4.53/mt by close, up 14

cents on day, and the strongest close since the contract closed at the same level August 6, Platts data shows.

EuropEan powEr Daily august 23, 2013

12Copyright © 2013 McGraw Hill Financial 12

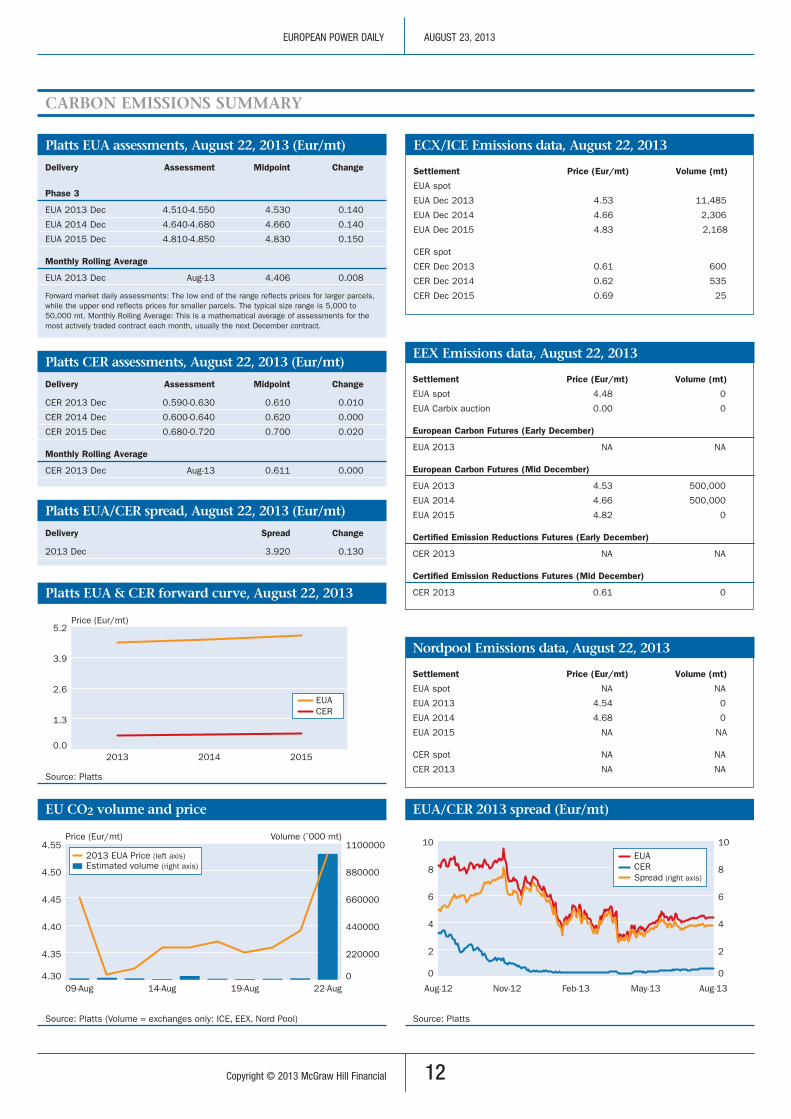

Carbon emissions summary

Platts EUA assessments, August 22, 2013 (Eur/mt)

Delivery Assessment Midpoint Change

Phase 3

EUA 2013 Dec 4.510-4.550 4.530 0.140

EUA 2014 Dec 4.640-4.680 4.660 0.140

EUA 2015 Dec 4.810-4.850 4.830 0.150

Monthly Rolling Average

EUA 2013 Dec Aug-13 4.406 0.008

Forward market daily assessments: The low end of the range reflects prices for larger parcels, while the upper end reflects prices for smaller parcels. The typical size range is 5,000 to 50,000 mt. Monthly Rolling Average: This is a mathematical average of assessments for the most actively traded contract each month, usually the next December contract.

Platts CEr assessments, August 22, 2013 (Eur/mt)

Delivery Assessment Midpoint Change

CER 2013 Dec 0.590-0.630 0.610 0.010

CER 2014 Dec 0.600-0.640 0.620 0.000

CER 2015 Dec 0.680-0.720 0.700 0.020

Monthly Rolling Average

CER 2013 Dec Aug-13 0.611 0.000

Platts EUA/CEr spread, August 22, 2013 (Eur/mt)

Delivery Spread Change

2013 Dec 3.920 0.130

ECX/ICE Emissions data, August 22, 2013

Settlement Price (Eur/mt) Volume (mt)

EUA spot

EUA Dec 2013 4.53 11,485

EUA Dec 2014 4.66 2,306

EUA Dec 2015 4.83 2,168

CER spot

CER Dec 2013 0.61 600

CER Dec 2014 0.62 535

CER Dec 2015 0.69 25

EEX Emissions data, August 22, 2013

Settlement Price (Eur/mt) Volume (mt)

EUA spot 4.48 0

EUA Carbix auction 0.00 0

European Carbon Futures (Early December)

EUA 2013 NA NA

European Carbon Futures (Mid December)

EUA 2013 4.53 500,000

EUA 2014 4.66 500,000

EUA 2015 4.82 0

Certified Emission Reductions Futures (Early December)

CER 2013 NA NA

Certified Emission Reductions Futures (Mid December)

CER 2013 0.61 0

Nordpool Emissions data, August 22, 2013

Settlement Price (Eur/mt) Volume (mt)

EUA spot NA NA

EUA 2013 4.54 0

EUA 2014 4.68 0

EUA 2015 NA NA

CER spot NA NA

CER 2013 NA NASource: Platts

Platts EUA & CER forward curve, August 22, 2013

Price (Eur/mt)

0.0

1.3

2.6

3.9

5.2

201520142013

EUACER

Source: Platts

EUA/CER 2013 spread (Eur/mt)

0

2

4

6

8

10

Aug-13May-13Feb-13Nov-12Aug-12

0

2

4

6

8

10EUACERSpread (right axis)

Source: Platts (Volume = exchanges only: ICE, EEX, Nord Pool)

EU CO2 volume and price

Price (Eur/mt) Volume (’000 mt)

0

220000

440000

660000

880000

1100000

4.30

4.35

4.40

4.45

4.50

4.55

22-Aug19-Aug14-Aug09-Aug

Estimated volume (right axis)2013 EUA Price (left axis)

EuropEan powEr Daily august 23, 2013

13Copyright © 2013 McGraw Hill Financial

ExchangE summary

EPEX France Spot Auction Day-Ahead (Eur/MWh) 23-Aug-13 22-Aug-13 23Aug12Minimum Hourly Price 23.58 13.92 36.89Maximum Hourly Price 61.62 57.63 64.93Average Base Price 45.26 45.42 52.59Average Peak Price 52.31 53.05 57.24Total Volume (MWh) 148,514.0 140,484.0 153,191.0

EEX French Power Futures (Eur/MWh)August 22, 2013 Base Peak

Month Settle Change Volume Settle Change VolumeFirst Month 38.25 -0.25 3600 50.50 0.00 6300Second Month 44.88 0.13 0 57.88 -0.50 0Third Month 50.00 0.75 0 66.25 0.25 0First Quarter 47.13 -0.12 2209 61.88 0.25 0Second Quarter 52.65 0.21 0 64.75 0.00 0Third Quarter 33.25 0.00 0 47.75 0.00 0Fourth Quarter 33.00 -0.04 0 48.75 0.00 0First Year 41.93 0.00 0 56.00 0.00 0Second Year 41.93 0.00 0 56.25 0.00 0Third Year 41.93 0.00 0 58.88 -0.12 0

APX Power Uk Daily Market Bulletin - 22-Aug-13

APX Power UK Spot Market Statistics for 22-Aug

(Half Hourly Contracts)Traded contracts (MW) 17508Total volume (MWh) 8754Highest price (GBP/MWh) 80.00Lowest price (GBP/MWh) 30.00

Data includes trades made between 00.00 and 18.00 22-Aug for all half hourly contracts.

Previous day total spot volume (MWh) 58977

Includes all spot and prompt trades between 00.00.00 and 23.59.59 21-Aug

Nord Pool Average Spot Prices (Eur/MWh) 23Aug13 22Aug13 23Aug12Oslo 31.55 30.56 26.47Bergen 31.55 30.56 25.11Molde 35.37 35.30 32.44Trondheim 35.37 35.30 32.44Tromso 35.37 35.30 32.44Kristiansand 31.55 30.56 26.47Lulea 46.37 52.59 32.57Malmo 46.37 52.59 32.57Stockholm 46.37 52.59 32.57Sundsvall 46.37 52.59 32.57Finland 46.37 52.59 45.16West Denmark 46.31 52.62 43.43East Denmark 46.40 52.62 53.29Systemwide 36.17 36.82 30.41

Nord Pool Futures

Contract Close Change High Low VolumeDay ahead (Eur/MWh) 36.60 -0.28 36.60 36.60 100First Week (Eur/MWh) 36.10 +0.40 36.10 35.80 437Second Week (Eur/MWh) 35.85 —- 35.85 35.70 80Third Week (Eur/MWh) 36.40 +0.27 —- —- —-First Month (Eur/MWh) 36.65 +0.40 36.70 36.50 101Second Month (Eur/MWh) 37.40 +0.60 37.40 37.00 39Third Month (Eur/MWh) 38.60 +0.55 38.65 38.30 22Fourth Month (Eur/MWh) 39.80 +0.45 39.85 39.60 22Fifth Month (Eur/MWh) 41.50 +0.40 41.50 41.50 10Sixth Month (Eur/MWh) 41.20 +0.17 —- —- —-First Quarter (Eur/MWh) 38.70 +0.60 38.80 37.95 675Second Quarter (Eur/MWh) 40.33 +0.43 40.35 40.00 106Third Quarter (Eur/MWh) 33.05 +0.37 33.10 32.95 29Fourth Quarter (Eur/MWh) 31.00 +0.25 —- —- —-First Year (Eur/MWh) 35.33 +0.40 35.30 35.10 47Second Year (Eur/MWh) 33.91 +0.26 33.96 33.80 25Third Year (Eur/MWh) 32.75 +0.25 32.75 32.65 8

EPEX Germany/Austria spot Auction (Eur/MWh) 23-Aug-13 22-Aug-13 23Aug12Phelix base 45.94 47.15 53.29Phelix peak 52.56 53.29 57.31Total Volume (MWh) 614,006.8 666,918.7 600,461.6

Base = 0000-2400, Peak = 0800-2000

Source: EEX

EEX Phelix Futures (Eur/MWh)August 22, 2013 Base Peak

Month Settle Change Volume Settle Change VolumeFirst Month 37.67 -0.25 242640 48.64 0.13 18648Second Month 38.65 0.15 10430 49.91 0.15 4140Third Month 41.10 -0.05 0 54.82 0.00 0Fourth Month 36.10 -0.13 0 50.38 0.20 3960Fifth Month 40.88 0.18 0 52.75 0.10 0Sixth Month 42.88 0.18 0 56.15 0.10 0Total 253,070 26,748

Quarter Settle Change Volume Settle Change VolumeFirst Quarter 38.59 -0.01 289379 51.63 0.12 31680Second Quarter 40.53 0.01 205105 52.35 0.20 53760Third Quarter 32.92 0.04 21840 41.56 0.19 0Fourth Quarter 34.20 0.10 0 42.78 0.19 0Total 516,324 85,440

Year Settle Change Volume Settle Change VolumeFirst Year 36.67 0.07 770880 46.88 0.17 68904Second Year 36.01 0.08 560640 45.25 0.19 0Third Year 35.70 0.14 333792 44.70 0.25 18792Fourth Year 36.23 0.08 61320 45.80 0.15 0Fifth Year 37.30 -0.15 0 47.30 0.07 0Sixth Year 38.30 -0.05 0 49.05 0.17 0Total 1,726,632 87,696

Austria EXAA Power Exchange (Eur/MWh) 23-Aug-13 22-Aug-13 23-Aug-12Minimum Hourly Price 28.93 29.93 37.24Maximum Hourly Price 57.38 56.12 65.48Baseload 43.89 45.35 52.90Peakload 50.50 50.55 58.29Total Volume (MWh) 26,058.3 24,232.6 33,016.4

Elexon Uk Balancing Prices (GBP/MWh)

Sell - Buy Sell - Buy Sell - Buy Sell - BuyP1 31.44 - 31.44 P13 32.16 - 37.99 P25 57.78 - 60.39 P37 63.52 - 96.51P2 29.75 - 31.19 P14 35.00 - 41.64 P26 57.16 - 63.20 P38 62.39 - 73.50P3 30.74 - 53.84 P15 38.18 - 49.55 P27 56.40 - 58.51 P39 40.93 - 59.36P4 30.63 - 53.86 P16 40.18 - 48.57 P28 53.06 - 53.06 P40 40.62 - 59.83P5 28.62 - 29.36 P17 48.48 - 57.16 P29 56.44 - 57.08 P41 60.76 - 88.72P6 27.50 - 28.22 P18 50.26 - 72.03 P30 54.17 - 54.17 P42 67.13 - 107.29P7 27.50 - 27.80 P19 50.61 - 77.08 P31 53.62 - 53.62 P43 61.99 - 88.02P8 27.54 - 53.50 P20 51.96 - 80.00 P32 60.56 - 66.63 P44 40.17 - 57.26P9 27.16 - 53.50 P21 52.33 - 71.27 P33 62.09 - 84.55 P45 53.41 - 62.00P10 27.66 - 53.21 P22 52.99 - 69.80 P34 66.57 - 89.72 P46 52.44 - 62.26P11 38.18 - 53.06 P23 56.73 - 65.62 P35 66.81 - 96.58 P47 46.99 - 65.05P12 38.16 - 38.16 P24 57.23 - 61.37 P36 68.62 - 94.65 P48 43.14 - 65.18

Delivery date: August 21, 2013

Source: Elexon, BM Reporting

28 October - 1 November 2013

Part of Principal Sponsor Associate Sponsor

Celebrate the unveiling of the 2013 Platts Top 250 Global Energy Company RankingsTM

29 October 2013 • The Fullerton, Singapore

Advertising and sponsorship opportunities available, contact:Sam Tang at +65 6530 6510 or [email protected] more information on Singapore International Energy Week, visit: www.siew.sg

For more information, visit: www.Top250.platts.com

Join us at the Platts Top 250 Asia Awards Dinner where we will recognize the outstanding accomplishments of the top performing energy companies in Asia and around the globe. We will reveal the 2013 Platts Top 250 Global Energy Company RankingsTM and recognize leaders in the Asia region. Being awarded a ranking in the Platts Top 250 is an accomplishment of prestige and honor in the energy industry.

Plan now to take advantage of this remarkable opportunity to network with the industry’s most infl uential executives. Yearly 300 top energy industry leaders from around the world as well as other key industry executives who are attending Singapore International Energy Week (SIEW) are inattendance at this elite event.

ASIA AWARDS DINNER