elite commercial reit - alanyeo.files.wordpress.com

TRANSCRIPT

ed: JS / sa: PY, CS

BUY (Initiating Coverage)

Last Traded Price ( 21 Jul 2021): S$0.67 (STI : 3,119.00) Price Target 12-mth: S$0.80 (20% upside)

Potential Catalyst: Uplift in valuations and rentals

Analyst

Singapore Research Team [email protected].

Dale LAI +65 66823715 [email protected]

Price Relative

Forecasts and Valuation

FY Dec (GBPm) 2020A 2021F 2022F 2023F

Gross Revenue 21.0 33.4 36.8 39.7 Net Property Inc 20.4 32.5 35.8 38.5 Total Return 23.4 19.1 20.7 22.6 Distribution Inc 14.8 23.7 25.8 28.1 EPU (S cts) N/A 4.72 4.35 4.71 EPU Gth (%) nm nm (8) 8 DPU (S cts) 4.43 5.00 5.41 5.82 DPU Gth (%) nm 13 8 8 NAV per shr (S cts) 64.9 65.2 64.6 64.0 PE (X) N/A 14.1 15.3 14.1 Distribution Yield (%) 6.7 7.5 8.1 8.8 P/NAV (x) 1.0 1.0 1.0 1.0 Aggregate Leverage (%) 33.7 43.7 43.7 43.7 ROAE (%) N/A 7.2 6.7 7.3 Consensus DPU (S cts): 9.4 9.6 10.3 Other Broker Recs: B: 3 S: 0 H: 0 GICW Industry : Real Estate GIC Sector: Equity Real Estate Investment (REITs) Principal Business: Elite Commercial REIT is a Singapore real estate investment trust ("REIT") established with the investment strategy of principally investing, directly or indirectly, in commercial assets and real estate-related assets in the UK.

Source of all data on this page: Company, DBS Bank, Bloomberg Finance

L.P.

At A Glance Issued Capital (m shrs) 470

Mkt. Cap (S$m/US$m) 313 / 229

Major Shareholders (%)

Partner Reinsurance Co Ltd 22.4

Ho Lee Group Trust 7.6

Sunway Re Cap Pte Ltd 5/8

Free Float (%) 59.5

3m Avg. Daily Val (US$m) 0.09

DBS Group Research . Equity

22 Jul 2021

Singapore Company Focus

Elite Commercial REIT Bloomberg: ELITE SP | Reuters: ELIE.SI Refer to important disclosures at the end of this report

High Yield, Low (UK Sovereign) Risk

• Initiate coverage with a BUY recommendation and TP of

GBP0.80; attractive yields of 7.6%/8.2% in FY21F/FY22F

• 93% leased to the UK’s Department for Work and

Pensions (DWP), which is counter-cyclical and resilient

• Full occupancy and long WALE of 7.2 years provide

strong income visibility

• Rental uplift of c.8% for majority of portfolio assets in

FY23 to drive a re-rating

Initiate coverage with BUY, TP of GBP0.80, implying upside of 21% with attractive yields of 7.6%/8.2% for FY21F/FY22F. Elite Commercial REIT occupies a unique position in the REITs space, where it functions as social infrastructure, given its 99% exposure to the UK government. We like its resilient and counter-cyclical portfolio that provides stable cash flows through the economic cycles. The REIT enjoys 100% portfolio occupancy and a weighted average lease expiry (WALE) of c.7.2 years, offering strong visibility to distributions.

Potential uplift in valuations in 2022. Current book value is conservative and assumes that half of the break options will be exercised, an unlikely scenario. We thus expect to see significant uplift in valuations when the breaks are not exercised by Mar 2022, bringing P/NAV down to <1.0x. We think it is unlikely for the primary tenant, Department for Work and Pensions (DWP), to break the leases as properties are strategically chosen to serve the local communities and provide crucial public services to c.30% of the UK population.

Built-in upside from inflation-linked rental uplift every five years. The leases to the UK government have rent reviews every five years pegged to the UK Consumer Price Index (“CPI”), subject to an annual minimum increase of 1.0% and maximum of 5.0%. This provides the portfolio with an embedded rental growth profile. The next rent review in Apr 2023 could see c.8% rental growth for selected leases, resulting in c.7.4% rental growth for the portfolio in that year.

Valuation: Our target price of GBP0.80 is based on DCF with a WACC of 5.5% and terminal growth rate of 1.00%.

Key Risks to Our View: Tenant risks, lease break option in 2023 for most agreements, country risks, interest rate risks and regulatory risks.

89

109

129

149

169

189

209

0.6

0.6

0.6

0.6

0.6

0.7

0.7

0.7

0.7

0.7

0.7

Mar-21 Jun-21

Relative IndexS$

Elite Commercial REIT (LHS) Relative STI (RHS)

DBS is supported by the Research Talent Development Grant Scheme

which aims to groom research talent to expand research coverage of

small-mid cap SGX listed companies

Page 2

Company Focus

Elite Commercial REIT

Table of Contents

Investment Summary 3

Peers Comparison 4

Valuation 6

Key Risks 7

SWOT Analysis 8

Resilience of Portfolio a Positive 9

Potential Upside 10

Environment, Social & Governance (ESG) 11

Portfolio Overview 12

Financials 19

Company Background 23

Management 24

Page 3

Company Focus

Elite Commercial REIT

Investment Summary

We are initiating coverage on Elite Commercial REIT with a

BUY recommendation and TP of GBP0.80, implying 21%

upside.

Only UK-focused REIT listed on SGX; counter cyclical

portfolio. Elite Commercial REIT is the only UK-focused

listed REIT in Singapore, with over 99% of gross floor area

leased to the AA-rated UK government. Its portfolio, valued

at £515.3m, comprises 155 predominantly freehold quality

commercial buildings located across the UK, with a total

net internal area of c.3.9m square feet. The properties are

geographically diversified across the UK, located in densely

populated areas and primarily in town centres close to

public transport nodes, ensuring accessibility.

Assets Under Management (AUM) expanded by 67% and

market capitalisation increased by 57% from maiden

acquisition. The 58 properties acquired on 9 Mar 2021 are

100% occupied, with more than 99% of the rental income

coming from the UK government. This reinforces the REIT’s

strategy of focusing on high credit quality tenants while

simultaneously diversifying the tenant base by adding

other UK government tenants other than Department for

Work and Pensions (DWP).

Tenant Breakdown by 1Q21 Gross Rental Income

Source: Company

High occupancy of 100% and long WALE of 7.2 years as at

Mar 2021. The portfolio is fully occupied with a long WALE.

Assuming the tenant does not terminate its lease on the

permissible break dates, 93.2% of total portfolio rent will

only expire in 2028. We think that it is unlikely for DWP, the

primary tenant, to exercise the option to break the lease as

the properties in the portfolio are crucial infrastructure

integral to UK’s social fabric and are relevant in meeting

social security needs of the UK in the long run. Tenant DWP

has also invested in the maintenance and upkeep of the

properties, suggesting a lower probability of breaking the

lease.

Potential significant uplift in valuations if breaks are not

exercised. Approximately 64.5% of total portfolio rent have

lease break options that will come into effect in Mar 2023.

The leases will continue till Mar 2028 if break options are

not exercised by Mar 2022 as tenants have to give a one-

year notice, which we understand have not been served.

Our current book values are conservative as we have

assumed that half of the break options will be exercised.

Given that it is highly unlikely that the tenants will exercise

this break option, we can expect to see a significant uplift in

book valuations, bringing P/NAV down to <1.0x once we

confirm that the option is not exercised by Mar 2022.

Embedded rental growth from inflation-linked rental

escalations. The leases to the UK government have rent

reviews every five years based on the UK Consumer Price

Index (“CPI”), subject to an annual minimum increase of

1.0% and maximum of 5.0%. This provides the portfolio

with built-in upside from the rental uplifts. With the next

rent review in Apr 2023, we can expect to see an increase

of c.8% in rental growth for leases with rent review,

resulting in c.7.4% rental growth for the portfolio.

Resilient portfolio provides stable returns. DWP, its primary

tenant, is UK government’s largest public service

department. It is responsible for welfare, pensions, and

child maintenance for c.20m claimants, which is c.30% of

the UK population. As claimant count is highly correlated

with unemployment, DWP is a unique counter-cyclical

occupier, which implies stability throughout economic

cycles. The REIT has also consistently achieved c.100% of

rent collection in advance since listing, notwithstanding UK

lockdowns and Brexit as the portfolio maintains 99%

exposure to AA-rated UK government with low default risk.

Alignment of interest and support from Sponsors. The

Sponsors, Elite Partners Holdings Pte. Ltd. (“EPH”), Ho Lee

Group Pte. Ltd. (“HLG”) and Sunway RE Capital Pte. Ltd.

(“Sunway”), have each provided Elite Commercial REIT a

right of first refusal (ROFR) over all future UK commercial

acquisitions. The Manager believes it will be able to

leverage on the Sponsor Group’s extensive expertise and

strong sourcing capabilities, to pursue DPU, value and

quality-accretive acquisition opportunities for Elite

Commercial REIT to grow its portfolio. These opportunities

are available to the REIT through the ROFR pipeline from

Sponsors and open market supply.

Page 4

Company Focus

Elite Commercial REIT

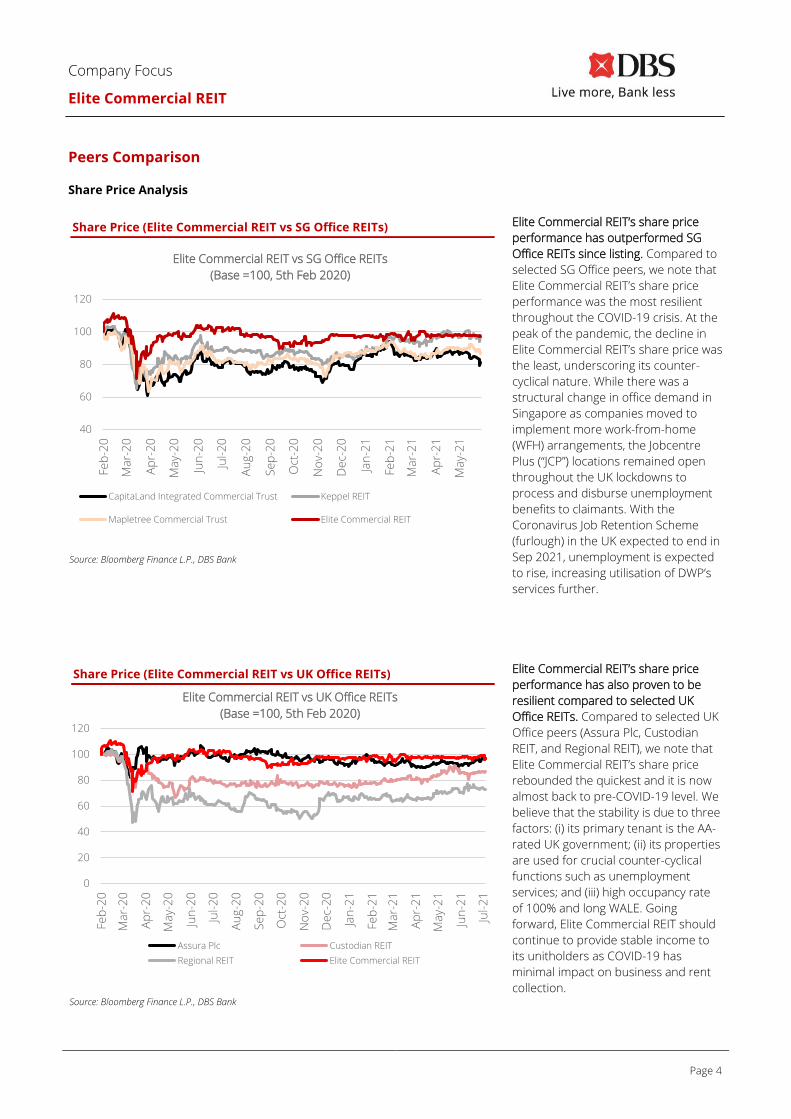

Peers Comparison Share Price Analysis

Source: Bloomberg Finance L.P., DBS Bank

Elite Commercial REIT’s share price

performance has outperformed SG

Office REITs since listing. Compared to

selected SG Office peers, we note that

Elite Commercial REIT’s share price

performance was the most resilient

throughout the COVID-19 crisis. At the

peak of the pandemic, the decline in

Elite Commercial REIT’s share price was

the least, underscoring its counter-

cyclical nature. While there was a

structural change in office demand in

Singapore as companies moved to

implement more work-from-home

(WFH) arrangements, the Jobcentre

Plus (“JCP”) locations remained open

throughout the UK lockdowns to

process and disburse unemployment

benefits to claimants. With the

Coronavirus Job Retention Scheme

(furlough) in the UK expected to end in

Sep 2021, unemployment is expected

to rise, increasing utilisation of DWP’s

services further.

Source: Bloomberg Finance L.P., DBS Bank

Elite Commercial REIT’s share price

performance has also proven to be

resilient compared to selected UK

Office REITs. Compared to selected UK

Office peers (Assura Plc, Custodian

REIT, and Regional REIT), we note that

Elite Commercial REIT’s share price

rebounded the quickest and it is now

almost back to pre-COVID-19 level. We

believe that the stability is due to three

factors: (i) its primary tenant is the AA-

rated UK government; (ii) its properties

are used for crucial counter-cyclical

functions such as unemployment

services; and (iii) high occupancy rate

of 100% and long WALE. Going

forward, Elite Commercial REIT should

continue to provide stable income to

its unitholders as COVID-19 has

minimal impact on business and rent

collection.

Share Price (Elite Commercial REIT vs SG Office REITs)

Share Price (Elite Commercial REIT vs UK Office REITs)

40

60

80

100

120

Feb

-20

Ma

r-2

0

Ap

r-2

0

Ma

y-2

0

Jun

-20

Jul-

20

Au

g-2

0

Se

p-2

0

Oct

-20

No

v-2

0

De

c-2

0

Jan

-21

Feb

-21

Ma

r-2

1

Ap

r-2

1

Ma

y-2

1

Elite Commercial REIT vs SG Office REITs

(Base =100, 5th Feb 2020)

CapitaLand Integrated Commercial Trust Keppel REIT

Mapletree Commercial Trust Elite Commercial REIT

0

20

40

60

80

100

120

Feb

-20

Ma

r-2

0

Ap

r-2

0

Ma

y-2

0

Jun

-20

Jul-

20

Au

g-2

0

Se

p-2

0

Oct

-20

No

v-2

0

De

c-2

0

Jan

-21

Feb

-21

Ma

r-2

1

Ap

r-2

1

Ma

y-2

1

Jun

-21

Jul-

21

Elite Commercial REIT vs UK Office REITs

(Base =100, 5th Feb 2020)

Assura Plc Custodian REIT

Regional REIT Elite Commercial REIT

Page 5

Company Focus

Elite Commercial REIT

P/NAV Analysis

S-REITs are currently trading at a weighted average P/NAV

multiple of 1.05x. REITs with predominantly overseas

assets usually trade at a discount to their Singapore-

focused counterparts. As investors usually perceive higher

risks with a portfolio that is based overseas, S-REITs

typically trade at a slight premium to S-REITs with

predominantly overseas assets.

Given that Elite Commercial REIT’s portfolio is entirely made

up of overseas assets, we believe that overseas office S-

REITs are better peer comparisons. We select Prime US

REIT and IREIT Global as they have portfolios that are

based entirely overseas. UK-listed Assura Plc also works

well as a peer comparison for Elite Commercial REIT, as it is

the closest competitor in the social infrastructure space in

the UK.

The three identified peers are currently trading at P/NAV

multiples of between 1.0x to 1.3x. Given Elite Commercial

REIT’s relatively comparable exposure and high degree of

diversification, our target P/NAV multiple values Elite

Commercial REIT at 1.2x. We believe that this valuation is

undemanding as the identified peers are trading within the

1.0x to 1.3x range. Moreover, Elite Commercial REIT's

portfolio is 99% leased to UK Government linked entities

and we expect it to have minimal risks.

Yield Comparison

As vaccination rates ramp up and the number of COVID-19

cases trend downwards, economies are expected to

rebound from the lows of FY20. Similarly, S-REITs’ earnings

are expected to recover and the average forward yields for

the sector are now 6.0% and 6.6% for FY21F and FY22F

respectively.

Compared to their Singapore-focused peers, S-REITs with

predominantly overseas assets are generally expected to

offer higher yields. Prime US REIT, which is a pure-play US

office REIT, is projected to generate forward yields of 7.8%

and 8.0% in FY21F and FY22F respectively. IREIT, which

invests in office properties in Europe, is forecast to deliver

forward yields of between 5.9% and 7.0% in the next two

years. Assura Plc’s forward yields are 3.8% and 3.9% in

FY21F and FY22F respectively.

Using these three REITs as a peer comparison set, we

believe that Elite Commercial REIT should be priced at a

level where its forward yields fall between 3.8% and 8.0%

over the next two years. Based on our valuations, Elite's

target yield of 6.3% and 6.8% is well within the range where

its peers are trading at now. Having a significantly smaller

market cap than Assura, we expect Elite Commercial REIT

to trade at a premium to Assura's yields. However, when

compared to Prime's and IREIT's yields, we believe that

Elite's target yield is undemanding. Again, Elite's leases are

almost entirely leased to the DWP (UK government linked

entity) and we believe that the stable and visible cash flows

from its portfolio warrants it to trade at a yield that is at

least comparable to its overseas S-REIT peers. On a yield

comparison basis, the average of the three identified peers’

FY21F/FY22F forward yields are 5.8% and 6.3%. Hence, we

believe that a forward FY21F yield of 7.6% is a fair target.

REIT

Mkt

Cap

(S$’bn)

Geographical Exposure Share

Price

Current Yield Current

P/NAV

Target Yield Target

P/NAV Singapore UK /

Europe Others FY21 FY22 FY21 FY22

Assura Plc 3.85 0% 100% 0% 76.55 3.8% 3.9% 1.3x 3.5% 3.6% 1.4x

Manulife US REIT 1.71 0% 0% 100% 0.80 7.4% 7.8% 1.1x 6.6% 6.9% 1.2x

Prime US REIT 1.33 0% 0% 100% 0.85 7.8% 8.0% 1.0x 6.6% 6.8% 1.2x

Keppel Pacific Oak REIT 1.03 0% 0% 100% 0.81 7.5% 7.7% 1.0x 7.1% 7.3% 1.0x

IREIT 0.61 0% 100% 0% 0.64 5.9% 7.0% 1.4x 5.0% 5.9% 1.6x

Elite Commercial REIT 0.58 0% 100% 0% 0.67 7.6% 8.2% 1.0x 6.3% 6.8% 1.2x

Average 6.6% 7.1% 1.1x 5.8% 6.2% 1.3x

Average of three

identified peers 5.8% 6.3% 1.2x 5.0% 5.5% 1.4x

Source: Bloomberg Finance L.P., DBS Bank

Page 6

Company Focus

Elite Commercial REIT

Valuation

Discounted cash flow (DCF) valuation method. We have

assessed Elite Commercial REIT’s fair value using the DCF

valuation method, given its relatively stable and visible

cashflows due to the portfolio’s high occupancy rates and

long WALE. The triple-net leases will also limit large

fluctuations to expenses. As such, we believe that the DCF

method would be an appropriate valuation tool.

We derive a fair value of GBP0.80. Our DCF analysis has

factored in a normalised risk-free rate of 2.0%, market

return of 9.4% and beta of 0.78x. The 5.5% WACC reflects

cost of equity of 7.8% and post-tax cost of debt of 2.0%.

Assuming terminal growth rate of 1.0%, we derive a fair

value of GBP0.80 using DCF. This implies a yield of

7.6%/8.2% for FY21F/FY22F.

Sensitivity analysis. Elite Commercial REIT’s valuation is

more sensitive to changes in WACC than terminal growth.

For every 1-ppt change in WACC, our DCF valuation would

move by c.46% while a 1-ppt shift in terminal growth would

result in a c.28% shift in DCF value.

Source: DBS Bank Estimates

DCF Analysis

FY Dec (GBPm) FY21F FY22F FY23F FY24F FY25F FY26F FY27F FY28F FY29F FY30F Terminal Value

EBIT 28.3 31.3 33.8 34.0 34.0 34.0 34.0 36.8 36.9 37.0

Depreciation 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0

Tax Provision (4.5) (4.9) (5.3) (5.3) (5.3) (5.3) (5.3) (5.9) (5.9) (5.9)

Capex (215.9) 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0

Chngs to Wkg Cap 5.6 5.4 5.7 5.3 5.4 5.3 5.3 6.2 5.8 5.8

FCF to the Firm (186.5) 31.8 34.2 34.0 34.0 34.0 34.0 37.1 36.8 36.9 720.0

PV of FCF 51.5

PV of Terminal Value 423.0

Net Cash / (Debt) (81.8)

Equity Value (GBPm) 392.7

Price per Share (GBP) 0.80

Risk Free Rate (Rf) 2.0%

Market Return 9.4%

Beta 0.78

Cost of Equity (Ke) 7.8%

% of debt financing 40.0%

After-tax cost of debt 2.0%

WACC 5.5%

Terminal Growth 1.0%

Source: DBS Bank Estimates

Terminal Growth

0.50% 0.75% 1.00% 1.25% 1.50%

WA

CC

4.5% 1.02 1.09 1.18 1.28 1.39

5.0% 0.84 0.90 0.96 1.03 1.11

5.5% 0.71 0.75 0.80 0.85 0.91

6.0% 0.59 0.63 0.66 0.70 0.75

6.5% 0.50 0.53 0.56 0.59 0.62

Sensitivity of DCF to changes in Terminal Growth Rate

Page 7

Company Focus

Elite Commercial REIT

Key Risks Tenant risks. Elite Commercial REIT is dependent on the UK

government for over 99% of rental payments. If the

government agencies do not renew a significant portion of

their leases, and no replacement tenants are found, this

may have an adverse impact on the financial condition and

results of operations of Elite Commercial REIT, as well as

the ability of the REIT to make regular distributions to

unitholders.

However, this risk is mitigated as each of the existing lease

agreements with The Secretary of State for Housing,

Communities and Local Government contains a clause that

requires a one-year notice period for termination, which

provides the Manager sufficient time to source and secure

new tenants.

Concentration risks. The majority of lease agreements are

due to expire in 2028, with certain lease agreements

containing an option for termination in 2023. Such

properties which have lease agreements that contain the

option for the tenant to terminate in 2023 account for

c.70% of the total revenue of Elite Commercial REIT.

Revenue may be adversely affected if majority of these

leases are not renewed or if suitable replacement tenants

are not found.

However, the properties are well-located and close to

amenities and public transportation, hence they may be

easily converted to other uses.

Country risks. Elite Commercial REIT is exposed to country

risk including economic changes, political changes or policy

changes in the UK where all of its properties are located. As

the UK economy is affected by global economic conditions,

a change in the strength of the global economy might

result in a downturn in the economy in the UK which might

negatively affect tenant demand for Elite Commercial REIT’s

properties. This in turn could negatively impact income and

distributions to unitholders of Elite Commercial REIT.

Interest rate risks. While interest rates are still relatively low

currently, inflationary pressures might build up due to

extremely dovish policies. If interest rates go up, Elite

Commercial REIT might face higher borrowing costs and

increased interest rate risk going forward, which could

negatively impact its distributions. However, we

understand that Elite Commercial REIT has already entered

into interest rate hedges for c.63% of its borrowings which

will mitigate such risks in the medium term.

Regulatory risks. The properties are based in the UK, with a

holding company in the British Virgin Islands (“BVI”). The

laws and regulations in Singapore, UK and BVI, as well as

the International Financial Reporting Standards (“IFRS”) are

subject to change, Should there be any changes, this may

affect the current REIT structure and ability to repatriate

cash in a tax efficient manner, potentially negatively

affecting distributions paid to unitholders.

Page 8

Company Focus

Elite Commercial REIT

SWOT Analysis

Strengths Weakness

• Diversified portfolio across the UK. The portfolio is

geographically diversified across the UK, with a particular

concentration in areas of higher population density and/or

close to major urban and metropolitan areas. The

properties used for Jobcentre Plus centres are also close to

public transport and other amenities, hence easily

accessible to the general population.

• Stable cash flow backed by AA-rated UK government, its

primary tenant. Over 99% of the portfolio’s gross rental

income in FY2020 was derived from the current leases with

primary tenant, DWP. This has enabled the REIT to

consistently achieve approximately 100% of rent collection

in advance since listing, notwithstanding UK lockdown and

Brexit.

• Embedded rental growth from inflation-linked rental

escalations. The leases to the UK government have rent

reviews every five years based on the UK Consumer Price

Index (“CPI”), subject to an annual minimum increase of

1.0% and maximum of 5.0%. As a result, there is upside

built into the lease agreements.

• Concentration risk. The portfolio is based entirely in

the UK and used primarily for office purposes. This

exposes Elite Commercial REIT to the risk of an economic

downturn in the UK in general, which may lead to a

decline in occupancy and rental income.

• Regulatory risk. The properties are based overseas in

the UK, with a holding company in the British Virgin

Islands (“BVI”). The laws and regulations in Singapore, UK

and BVI, as well as the International Financial Reporting

Standards (“IFRS”) are subject to change, potentially

affecting Elite Commercial REIT.

Opportunities Threats

• Growth from acquisition opportunities in UK, the most

liquid real estate market in Europe. Elite Commercial REIT is

able to leverage on its sponsors’ extensive expertise and

strong sourcing capabilities in the UK. They have each

provided Elite Commercial REIT a right of first refusal over

all future UK acquisitions.

• Resilience of a counter-cyclical portfolio. Should the

economic impact from Covid-19 worsen, unemployment

rate and claimant count will rise, increasing utilisation of

DWP’s services. However, it will have minimal impact on

Elite Commercial REIT’s operations and rent collection.

• Properties with lease agreements that contain an

option for tenant to terminate in 2023 account for c.70%

of total revenue. Revenue may be adversely affected if

majority of these leases are not renewed or if Elite

Commercial REIT is unable to source for suitable

replacement tenants.

• Gearing level is rising. Current aggregate leverage of

42.1% leaves little available debt headroom. Funding

restrictions may be imposed should the limit breach the

50% mark set by Monetary Authority of Singapore (MAS).

Source: DBS Bank

Page 9

Company Focus

Elite Commercial REIT

Resilient Portfolio

Unique counter-cyclical occupier provides stable cash flows

even in economic downturns. Elite Commercial REIT’s

primary tenant is the Department for Work and Pensions

(“DWP”), UK’s largest public service department. For the 12

months ended 31 Mar 2020, the DWP served over 20m

claimants and customers with a budget of £191bn in

benefits. DWP plays a vital role in the delivery of public

services to more than 66m UK citizens, supporting those

who depend on government measures, especially with

COVID-19 that has weakened the UK economy and raised

unemployment.

Within the portfolio, 123 out of 155 properties function as

Jobcentre Plus (part of the DWP), which is a government-

funded employment agency and social security office whose

aim is to help people of working age find employment in the

UK. Assistance provided include career advisory services,

unemployment benefits arrangements and job-matching

services. Hence, in an economic downturn like now, the

portfolio is especially resilient given that claimant counts, job

centre footfall and DWP benefit spending are all highly

correlated to unemployment. Even during nationwide

lockdowns from COVID-19, Jobcentre Plus locations

remained open and operational with minimal disruption,

demonstrating DWP’s uniquely counter-cyclical operations.

Going forward, we expect footfall to DWP offices to increase

as the Coronavirus Job Retention Scheme (furlough) ends in

Sep 2021, with 4.7m people on furlough as of 31 Jan 2020.

With the unemployment rate rising, these Jobcentre Plus

offices are even more crucial to UK’s social fabric.

Usage of properties ties in with social security needs of the

UK, ensuring relevance in the long run. Aside from

unemployment services, other crucial DWP services will help

to address the challenges the UK will face: (i) UK’s

population is ageing, and it is projected that one in four

people in the UK will be aged 65 years and older by 2050, an

increase from approximately one in five just two years ago,

according to the Office for National Statistics. This drives

long-term structural demand growth for pension services,

which is one of the services provided; (ii) Child maintenance

services, which will be required regardless of economic

conditions; and (iii) Disability services, which will also be

required regardless of economic conditions. The portfolio

represents crucial public infrastructure for the provision of

DWP services and will continue to be needed in the long

run.

Portfolio maintains 99% exposure to AA-rated UK

government with low default risk. Over 99% of the portfolio’s

gross rental income in FY2020 was derived from leases from

the AA-rated (by S&P) UK government. The occupier mix is

now diversified to include other government agencies as

well, such as the Ministry of Defence, National Records of

Scotland, Her Majesty’s Courts and Tribunals Service,

National Resources of Wales and Environmental Agency.

This has enabled the REIT to consistently achieve

approximately 100% of rent collection in advance since

listing, notwithstanding UK lockdowns and Brexit.

Over 99% of gross rental income derived from full repairing

and insuring (triple net) leases. The responsibility for the

repair of the external, internal, and structural format of the

property is placed with the tenant. Elite Commercial REIT, as

the landlord, has no repairing or insuring liability and will not

be required to bear the costs of material repairs to the

properties, if any. This helps to reduce risks caused by

damages to the properties and limit large fluctuations to

capex requirements.

Built-in upside from inflation-linked rental uplifts. The leases

to the UK government have rent reviews every five years

based on the UK Consumer Price Index (“CPI”), subject to an

annual minimum increase of 1.0% and maximum of 5.0%.

This provides the portfolio with an embedded rental growth

profile that benefits from rent escalation; the upcoming rent

review will be in Apr 2023. The Bank of England forecasts

CPI to be 1.7%/2.3% in FY21F/22F. However, we have taken

a slightly more conservative stance and assumed 1.5%/1.9%

for FY21F/22F, bringing the cumulative five-year CPI forecast

to 8%. We have thus assumed that the rental growth will be

c.8% in 2023 for leases that have rent reviews, which is

majority of the portfolio, resulting in c.7.4% rental growth in

the portfolio.

2018 2019 2020 2021F 2022F Cumulative

Bank of

England

Forecast 2.5% 1.5% 0.6%

1.7% 2.3% 8.6%

DBS

Forecast 1.5% 1.9% 8.0%

Source: Bank of England, DBS Bank Estimates

Strong acquisition pipeline. Elite Commercial REIT plans to

acquire £250-300m in assets annually. The Manager

believes it will be able to leverage on the Sponsor group’s

extensive expertise and strong sourcing capabilities, to

pursue DPU, value and quality-accretive acquisition

opportunities for Elite Commercial REIT to grow its portfolio.

These opportunities are available to the REIT through a

pipeline from Sponsors, who have provided Elite

Commercial REIT a right of first refusal (ROFR) over all future

UK commercial acquisitions. Target properties to be

acquired can be obtained from the open market or third

parties as well.

Page 10

Company Focus

Elite Commercial REIT

Upside Potential

Significant uplift in valuations if breaks not exercised.

Approximately 64.5% of the REIT’s portfolio have lease

break options that will come into effect in Mar 2023. The

leases will continue till Mar 2028 if break options are not

exercised by Mar 2022 as tenants have to give a one-year

notice. Current valuations assume that half of the break

options will be exercised. However, we think that it is

unlikely for tenants to exercise the break option as these

properties are assets that provide crucial DWP services to

c.30% of the UK population. In FY20, there was a £3.0m

valuation uplift from £3.6m to £6.6m (84% uplift in value)

after the removal of the lease break clause for Lodge

House, Bristol. Hence, we can expect to see a huge

increase in valuations if the breaks are not exercised by

Mar 2022.

Asset Enhancement Potential. The Manager expects to

improve the rental income generation ability and value of

the portfolio through accretive asset enhancements. At the

time of the IPO, they identified Peel Park in Blackpool as an

asset with strong potential for asset enhancement. The

property sits on c.11.7 hectares of undeveloped grassland

which provides the opportunity to either work with DWP to

increase its footprint on site or carve out a portion of the

land for alternative uses in the future. We believe that the

Manager will be opportunistic when embarking on any

asset enhancement initiative.

The Manager is also keen to revamp the buildings and

upgrade the properties as part of the asset enhancement

initiative. They are looking at improving the Energy

Performance Certificate (EPC) ratings on the current

buildings as the buildings are not new, although very

functional.

Source: Company

Asset recycling. While acquisitions will be made to grow the

portfolio, the Manager will also explore options such as

divesting underperforming properties or re-letting

properties out as commercial properties, to redeploy

assets and optimise the portfolio. This will allow Elite

Commercial REIT to recycle proceeds from the divestments

into acquiring properties that meet its investment criteria.

The Manager has shared that, as a social REIT, their first

and primary intent is to keep the government tenants, so

that it can provide stable cashflows to investors. Should

break clauses be exercised, the Manager will then assess

the property to consider disposal or reconfigure the use

for another commercial tenant.

Aerial view of Peel Park

Page 11

Company Focus

Elite Commercial REIT

Environment, Social & Governance (ESG)

Elite Commercial REIT understands the importance of

delivering sustainable value in communities where the REIT

operates to make a positive contribution to stakeholders.

Environment: Elite Commercial REIT recognises that the

quality and environmental credentials of the portfolio are

crucial to maintaining the resilience of its business. Hence,

they actively explore ways to improve the energy rating of

buildings and condition of properties. Some of the

initiatives include introducing new ground source or air

source heating systems, which would reduce power usage.

They are also working with the tenant to allow for new

glazing and energy saving lighting systems, which will

improve energy efficiency. Management has shared that

they are willing to allocate a portion of the uplift in

valuations to improvement works.

Social: The properties in Elite Commercial REIT’s portfolio

are assets used to support social welfare. Over 99% of the

portfolio’s gross rental income in FY20 was derived from

DWP, a government agency that plays a crucial role in UK’s

social infrastructure with the provision of unemployment

services, pension services, child maintenance services and

disability services.

Page 12

Company Focus

Elite Commercial REIT

Portfolio Overview

Predominantly freehold office assets that are

geographically diversified across the UK and conveniently

located. The portfolio value as of Mar 2021 is £515.3m. Of

the 155 properties, 150 properties are freehold and five

are on long leasehold tenures. The portfolio is

geographically diversified across the UK, located in densely

populated areas and primarily in town centres close to

public transport nodes, ensuring accessibility.

High occupancy of 100% and long weighted average lease

expiry (WALE) of 7.2 years as at Mar 2021. The portfolio is

fully occupied with long WALE. Assuming the tenant does

not terminate lease on the permissible break dates, 93.2%

of the portfolio rent expires in 2028. We think it is unlikely

for DWP, the primary tenant, to exercise the option to

break the lease as they have invested in the maintenance

and upkeep of the properties.

Geographical Spread of 155 Properties Across UK

Source: Company

Lease Expiry Profile as at 31 Mar 2021

WALB: Weighted Average Lease To Break

Source: Company

Page 13

Company Focus

Elite Commercial REIT

Salient Details of Properties in the Portfolio

No. Property Function Net Internal

Area (sqft)

Valuation

(GBP)

2020 Gross

Revenue

(GBP)

Occupancy

Rate as of

31 Mar 2021

Tenure as

of 31 Dec

2020

London and South East

1 Beaufort House, Harlow Jobcentre Plus 28,170 6,735,000 433,899 100% Freehold

2 Broadlands House, Newport (IOW) Jobcentre Plus 31,930 7,980,000 468,311 100% Freehold

3 Crown Building, Banbury Jobcentre Plus 25,051 3,930,000 253,085 100% Freehold

4 Crown Buildings, Colchester Jobcentre Plus 19,152 3,655,000 204,330 100% Freehold

5 Crown House, Chatham Jobcentre Plus 30,317 6,710,000 432,326 100% Freehold

6 Crown House, Worthing Jobcentre Plus 31,503 5,825,000 326,711 100% Freehold

7 East Street, Epsom Jobcentre Plus 8,687 2,415,000 143,158 100% Freehold

8 Gloucester House, Bognor Regis Jobcentre Plus 21,254 2,885,000 214,083 100% Freehold

9 High Road, Ilford Jobcentre Plus 18,741 6,535,000 356,394 100% Freehold

10 Nutwood House, Canterbury Back Office 27,673 9,160,000 512,000 100% Freehold

11 Palting House, Folkestone Jobcentre Plus 36,566 4,585,000 268,840 100% Freehold

12 Rishton House, Lowestoft Jobcentre Plus 41,656 2,890,000 214,530 100% Freehold

13 South Western House, Aldershot Jobcentre Plus 19,924 2,555,000 164,174 100% Freehold

14 St Andrew's House, Bury St Edmunds Jobcentre Plus 28,863 3,320,000 229,930 100% Freehold

15 The Forum, Stevenage Jobcentre Plus /

Retail 18,609 5,010,000 272,522 100% Freehold

16 Wyvern House, Bedford Jobcentre Plus 23,803 3,160,000 187,741 100% Freehold

17 Crown House Jobcentre Plus 34,729 12,200,000 - 100% Freehold

18 Medina Road Jobcentre Plus 15,366 6,400,000 - 100% Freehold

19 Raydean House Jobcentre Plus 21,958 8,300,000 - 100% Freehold

20 Oates House Jobcentre Plus 14,659 8,600,000 - 100% Freehold

21 Collyer Court Jobcentre Plus 15,586 8,400,000 - 100% Freehold

22 Peckham High Street Jobcentre Plus 17,967 9,600,000 - 100% Freehold

23 Broadway House Jobcentre Plus 17,218 10,900,000 - 100% Freehold

24 Finchley Lane Jobcentre Plus 15,424 5,600,000 - 100% Freehold

25 Kilner House Jobcentre Plus 13,145 6,300,000 - 100% Freehold

26 Tonbridge Crown Buildings Jobcentre Plus 10,549 3,000,000 - 100% Freehold

27 Medwyn House Jobcentre Plus 23,218 6,000,000 - 100% Freehold

28 St. Cross House Jobcentre Plus 42,985 5,500,000 - 100% Freehold

Source: Company

Page 14

Company Focus

Elite Commercial REIT

No. Property Function Net Internal

Area (sqft)

Valuation

(GBP)

2020 Gross

Revenue

(GBP)

Occupancy

Rate as of

31 Mar 2021

Tenure as

of 31 Dec

2020

South West

1 Brendon House, Taunton Jobcentre Plus 41,750 5,705,000 381,723 100% Freehold

2 Cotswold House, Torquay Back Office 21,895 3,110,000 206,540 100% Freehold

3 Cyppa Court, Chippenham Jobcentre Plus 12,299 2,100,000 - 100% Freehold

4 Hanover House, Bridgwater Jobcentre Plus 21,598 2,100,000 - 100% Freehold

5 Kent Street, Bristol Jobcentre Plus 6,339 1,075,000 95,083 100% Freehold

6 Lodge House, Bristol* Back Office 25,979 6,550,000 366,588 100% Freehold

7 Monks Park Avenue, Bristol Jobcentre Plus 10,183 2,070,000 115,477 100% Freehold

8 Queen's House, Plymouth Jobcentre Plus 14,094 1,400,000 - 100% Freehold

9 Regent House, Weston Super Mare Jobcentre Plus /

Retail 21,704 2,685,000 212,637 100% Freehold

10 Spring Gardens House, Swindon Jobcentre Plus 47,918 8,035,000 617,373 100% Freehold

11 St Paul's House, Chippenham Back Office 16,207 3,675,000 272,877 100% Freehold

12 Summerlock House, Salisbury Jobcentre Plus 17,136 2,775,000 185,327 100% Freehold

*Lodge House, Bristol – break option not exercised, lease will expire on 31 March 2028

Source: Company

No. Property Function Net Internal

Area (sqft)

Valuation

(GBP)

2020 Gross

Revenue

(GBP)

Occupancy

Rate as of

31 Mar 2021

Tenure as

of 31 Dec

2020

Midlands

1 Acacia Walk, Nottingham Jobcentre Plus 4,306 785,000 57,656 100% Freehold

2 Beecroft Road, Cannock Jobcentre Plus 31,517 1,850,000 137,015 100% Freehold

3 Bristol Road South, Birmingham Jobcentre Plus 18,996 4,300,000 - 100% Freehold

4 Crown Buildings, Ilkeston Jobcentre Plus 18,352 1,430,000 112,904 100% Freehold

5 Crown House, Burton On Trent Jobcentre Plus 45,897 1,790,000 128,185 100% Freehold

6 Crown House, Grantham Jobcentre Plus 24,962 2,535,000 141,407 100% Freehold

7 George Street, Corby Jobcentre Plus 8,847 1,300,000 - 100% Freehold

8 High Street, Bliston Jobcentre Plus 10,779 1,700,000 - 100% Freehold

9 Holborn House, Derby Call Centre 35,120 6,300,000 452,639 100% Freehold

10 Lothersdale House, Wellingborough Jobcentre Plus 32,113 4,120,000 262,055 100% Freehold

11 Saxon Mill Lane, Tamworth Jobcentre Plus 10,698 1,400,000 - 100% Freehold

12 Scotland House, Stourbridge Jobcentre Plus 12,452 1,800,000 - 100% Freehold

13 St Katherine's House, Northampton Back Office 27,745 2,100,000 - 100% Freehold

14 Tannery House, Alfreton Jobcentre Plus 10,226 1,100,000 86,499 100% Freehold

15 Temple House, Wolverhampton Jobcentre Plus 27,523 3,000,000 - 100% Freehold

16 Upper Huntbach Street, Stoke On Trent Jobcentre Plus 21,540 2,830,000 209,815 100% Freehold

17 Washwood Heath Road, Birmingham Jobcentre Plus 14,922 1,000,000 - 100% Freehold

Source: Company

Page 15

Company Focus

Elite Commercial REIT

No. Property Function Net Internal

Area (sqft)

Valuation

(GBP)

2020 Gross

Revenue

(GBP)

Occupancy

Rate as of

31 Mar 2021

Tenure as

of 31 Dec

2020

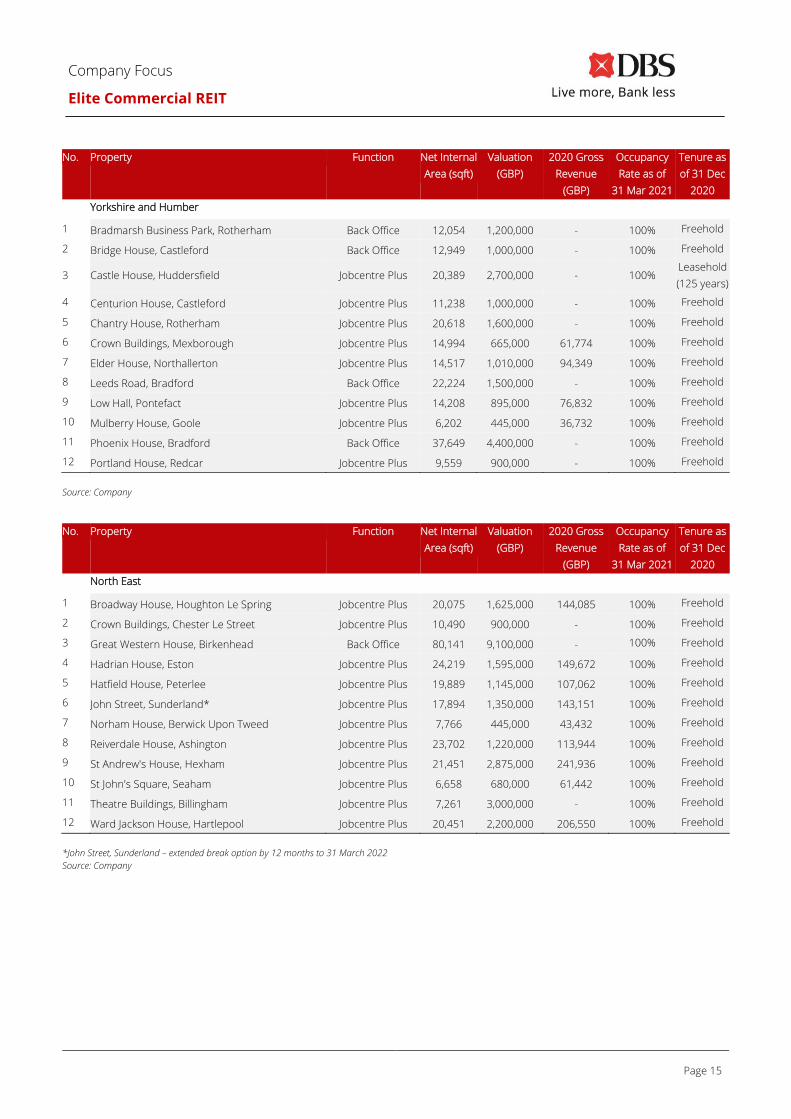

Yorkshire and Humber

1 Bradmarsh Business Park, Rotherham Back Office 12,054 1,200,000 - 100% Freehold

2 Bridge House, Castleford Back Office 12,949 1,000,000 - 100% Freehold

3 Castle House, Huddersfield Jobcentre Plus 20,389 2,700,000 - 100% Leasehold

(125 years)

4 Centurion House, Castleford Jobcentre Plus 11,238 1,000,000 - 100% Freehold

5 Chantry House, Rotherham Jobcentre Plus 20,618 1,600,000 - 100% Freehold

6 Crown Buildings, Mexborough Jobcentre Plus 14,994 665,000 61,774 100% Freehold

7 Elder House, Northallerton Jobcentre Plus 14,517 1,010,000 94,349 100% Freehold

8 Leeds Road, Bradford Back Office 22,224 1,500,000 - 100% Freehold

9 Low Hall, Pontefact Jobcentre Plus 14,208 895,000 76,832 100% Freehold

10 Mulberry House, Goole Jobcentre Plus 6,202 445,000 36,732 100% Freehold

11 Phoenix House, Bradford Back Office 37,649 4,400,000 - 100% Freehold

12 Portland House, Redcar Jobcentre Plus 9,559 900,000 - 100% Freehold

Source: Company

No. Property Function Net Internal

Area (sqft)

Valuation

(GBP)

2020 Gross

Revenue

(GBP)

Occupancy

Rate as of

31 Mar 2021

Tenure as

of 31 Dec

2020

North East

1 Broadway House, Houghton Le Spring Jobcentre Plus 20,075 1,625,000 144,085 100% Freehold

2 Crown Buildings, Chester Le Street Jobcentre Plus 10,490 900,000 - 100% Freehold

3 Great Western House, Birkenhead Back Office 80,141 9,100,000 - 100% Freehold

4 Hadrian House, Eston Jobcentre Plus 24,219 1,595,000 149,672 100% Freehold

5 Hatfield House, Peterlee Jobcentre Plus 19,889 1,145,000 107,062 100% Freehold

6 John Street, Sunderland* Jobcentre Plus 17,894 1,350,000 143,151 100% Freehold

7 Norham House, Berwick Upon Tweed Jobcentre Plus 7,766 445,000 43,432 100% Freehold

8 Reiverdale House, Ashington Jobcentre Plus 23,702 1,220,000 113,944 100% Freehold

9 St Andrew's House, Hexham Jobcentre Plus 21,451 2,875,000 241,936 100% Freehold

10 St John's Square, Seaham Jobcentre Plus 6,658 680,000 61,442 100% Freehold

11 Theatre Buildings, Billingham Jobcentre Plus 7,261 3,000,000 - 100% Freehold

12 Ward Jackson House, Hartlepool Jobcentre Plus 20,451 2,200,000 206,550 100% Freehold

*John Street, Sunderland – extended break option by 12 months to 31 March 2022

Source: Company

Page 16

Company Focus

Elite Commercial REIT

No. Property Function Net Internal

Area (sqft)

Valuation

(GBP)

2020 Gross

Revenue

(GBP)

Occupancy

Rate as of

31 Mar 2021

Tenure as

of 31 Dec

2020

North West

1 Beech House, Hyde Jobcentre Plus 39,550 2,375,000 223,037 100% Freehold

2 Blackburn Road, Burnley Call Centre 46,405 5,605,000 472,113 100% Freehold

3 Duchy House, Preston Back Office 43,805 4,000,000 244,825 100% Freehold

4 Heron House, Stockport Jobcentre Plus 43,271 4,070,000 322,490 100% Freehold

5 Hilden House, Warrington Back Office 50,841 7,065,000 560,215 100% Freehold

6 Hougoumont House, Liverpool Jobcentre Plus 17,082 1,255,000 105,091 100% Freehold

7 Lee-Moran House, Burnley Jobcentre Plus 17,886 2,030,000 170,407 100% Freehold

8 Mitre House, Lancaster Jobcentre Plus 64,597 4,335,000 409,806 100% Freehold

9 Palatine House, Preston Back Office 36,257 3,385,000 207,079 100% Freehold

10 Peel Park, Blackpool Back Office 156,542 26,900,000 1,695,000 100% Freehold

11 Roskell House, Fleetwood Jobcentre Plus 5,863 535,000 46,800 100% Freehold

12 Roydale House, Leigh Jobcentre Plus 21,022 1,300,000 118,550 100% Freehold

13 Silver Street, Bury Jobcentre Plus 9,352 945,000 79,106 100% Freehold

14 Springfield House, Liverpool Jobcentre Plus 10,534 1,175,000 104,253 100% Freehold

15 St Martin's House, Bootle Back Office 85,453 3,915,000 387,592 100% Freehold

16 Wilmslow Road Jobcentre Plus 20,807 2,485,000 196,557 100% Freehold

17 Speke Road, Garston Jobcentre Plus 8,317 700,000 - 100% Freehold

18 Openshaw Job Centre, Manchester Jobcentre Plus 12,925 800,000 - 100% Freehold

19 Premier House, Liverpool Jobcentre Plus 9,476 800,000 - 100% Freehold

20 Great Moore Street, Bolton Jobcentre Plus 13,842 1,300,000 - 100% Freehold

21 Cardwell Place, Lancashire Back Office 15,386 1,000,000 - 100% Freehold

22 Brunswick House, Birkenhead Jobcentre Plus 27,956 2,100,000 - 100% Freehold

23 Tomlinson House, Blackpool Norcross Lane Back Office 89,179 1,000,000 - 100% Freehold

24 Chantry House, Chester Jobcentre Plus 34,847 5,300,000 - 100% Freehold

25 Dallas Court Units 1-2, Salford Back Office 16,044 1,500,000 - 100% Leasehold

(91 years)

Source: Company

Page 17

Company Focus

Elite Commercial REIT

No. Property Function Net Internal

Area (sqft)

Valuation

(GBP)

2020 Gross

Revenue

(GBP)

Occupancy

Rate as of

31 Mar 2021

Tenure as

of 31 Dec

2020

Scotland

1 Atlas Road, Glasgow Jobcentre Plus 49,788 4,010,000 397,111 100% Freehold

2 Bayfield Road, Portree Jobcentre Plus 1,943 240,000 24,901 100% Freehold

3 Bowling Green Street, Bellshill Jobcentre Plus 23,512 2,810,000 277,847 100% Freehold

4 Castlestead House, Montrose Jobcentre Plus 4,246 410,000 41,363 100% Freehold

5 Claverhouse Industrial Park, Dundee Call Centre 48,269 2,995,000 281,392 100% Freehold

6 Coustonholm Road, Glasgow Jobcentre Plus 36,124 3,070,000 303,446 100% Freehold

7 Crown Building, Kilmarnock Jobcentre Plus 36,696 3,050,000 301,762 100% Freehold

8 Discovery House, Stornoway Jobcentre Plus 7,276 865,000 93,259 100% Freehold

9 Flemington House, Motherwell Jobcentre Plus 29,381 2,540,000 263,779 100% Freehold

10 Glasgow Benefits Centre, Glasgow Back Office 137,287 30,290,000 1,940,350 100% Freehold

11 Hall Street, Campbeltown Jobcentre Plus 8,288 585,000 59,758 100% Freehold

12 Heron House, Falkirk Jobcentre Plus 25,454 2,650,000 262,181 100% Freehold

13 High Street, Dingwall Jobcentre Plus 3,438 320,000 30,808 100% Freehold

14 Parklands, Falkirk Back Office 81,350 6,570,000 683,789 100% Freehold

15 Pollokshaws Road, Glasgow Jobcentre Plus 15,812 1,570,000 154,722 100% Freehold

16 St John Steet, Stranraer Jobcentre Plus 6,402 610,000 65,646 100% Freehold

17 Trinity Road, Elgin Jobcentre Plus 17,427 1,450,000 142,946 100% Freehold

18 Waggon Road, Leven Jobcentre Plus 4,901 290,000 27,637 100% Freehold

19 Wallacetoun House, Ayr Jobcentre Plus /

Medical Centre 28,299 2,870,000 283,747 100% Freehold

20 Whitburn Road, Bathgate Jobcentre Plus 31,484 2,695,000 266,327 100% Freehold

21 South Muirhead Road, Glasgow Jobcentre Plus 9,097 900,000 - 100% Freehold

22 Irish Street, Dumfries Jobcentre Plus 12,303 1,400,000 - 100% Freehold

23 New River House, Galashiels Jobcentre Plus 21,216 2,800,000 - 100% Freehold

24 Victoria Road, Fife Jobcentre Plus 45,884 4,500,000 - 100% Freehold

25 Ladywell House, Edinburgh Back Office 54,622 7,400,000 - 100% Freehold

26 Lindsay House, Dundee Back Office 38,803 4,700,000 - 100% Freehold

27 Sidlaw House, Dundee Call Centre 61,250 6,000,000 - 100% Freehold

Source: Company

Page 18

Company Focus

Elite Commercial REIT

No. Property Function Net Internal

Area (sqft)

Valuation

(GBP)

2020 Gross

Revenue

(GBP)

Occupancy

Rate as of

31 Mar 2021

Tenure as

of 31 Dec

2020

Wales

1 Bridge Street, Llangefni Jobcentre Plus 9,601 725,000 63,990 100% Freehold

2 Cleddau Bridge Business Park, Pembroke Dock Call Centre 19,418 1,275,000 119,460 100% Freehold

3 Crown Buildings, Aberdare Jobcentre Plus /

Back Office 24,290 1,050,000 102,662 100% Freehold

4 Crown Buildings, Abertillery Jobcentre Plus 9,159 405,000 37,117 100% Freehold

5 Crown Buildings, Bridgend Jobcentre Plus 46,058 3,975,000 376,304 100% Freehold

6 Crown Buildings, Caerphilly Back Office 21,000 1,400,000 124,374 100% Freehold

7 Dock Street, Porthcawl Jobcentre Plus 3,023 285,000 25,699 100% Freehold

8 Hannah Street, Porth Jobcentre Plus 7,018 680,000 64,763 100% Freehold

9 High Street, Swansea Jobcentre Plus 19,609 1,995,000 188,006 100% Freehold

10 Maengwyn Street, Machynlleth Jobcentre Plus 3,655 145,000 12,421 100% Freehold

11 Oldway House, Swansea Jobcentre Plus 14,575 1,120,000 104,611 100% Freehold

12 Parc Menai, Bangor Call Centre

31,674 3,670,000 384,196

100% Leasehold

(235 years)

13 Quay Street, Haverfordwest Jobcentre Plus 8,603 805,000 75,000 100% Freehold

14 Thistle House, Tonypandy Jobcentre Plus 14,650 1,140,000 112,044 100% Freehold

15 Station Road, Port Talbot Jobcentre Plus 8,793 800,000 - 100% Freehold

16 Rhyl High Street Jobcentre Plus 9,452 900,000 - 100% Freehold

17 Windsor Road, Neath Jobcentre Plus 15,817 1,500,000 - 100% Freehold

18 Afon House, Newtown Jobcentre Plus 19,160 1,700,000 - 100% Freehold

19 Charles Street, Newport Jobcentre Plus 18,334 2,200,000 - 100% Freehold

20 Newport Road, Cardiff Back Office 33,749 4,900,000 - 100% Freehold

Source: Company

No. Property Function Net Internal

Area (sqft)

Valuation

(GBP)

2020 Gross

Revenue

(GBP)

Occupancy

Rate as of

31 Mar 2021

Tenure as

of 31 Dec

2020

East

1 Blackburn House, Norwich Back Office 9,302 1,500,000 - 100% Leasehold

(83 years)

2 Great Oaks House, Basildon Back Office 54,432 9,000,000 - 100% Leasehold

(983 years)

Source: Company

Page 19

Company Focus

Elite Commercial REIT

Financials

Steady growth in revenue driven by portfolio growth. Gross

revenue grew by 87.6% y-o-y to £6.6m in 1Q21 from £3.5m

in 1Q20 (from listing on 6 Feb to 31 Mar), boosted by

contributions from its newly acquired portfolio on 9 Mar

2021. These properties combined are projected to

contribute c.£10.4m to FY21F (from 9 Mar to 31 Dec 2021)

revenues, and c.£13.7m (full year) in FY22F.

Revenue from FY20 – FY22F (£m)

Source: Company

Revenue from FY20 – FY22F (£m)

Source: Company, DBS Bank Estimates

Strong balance sheet. Elite Commercial REIT employs

prudent capital management to drive long-term

sustainable growth. It has a healthy debt maturity profile

with a bridge loan of £9m due in FY22 and an average

weighted debt maturity of 2.8 years. The REIT' has low

borrowing cost of c.1.9%, sound interest coverage ratio

(ICR) of 7.4x and 61% of its assets are unencumbered.

Although its gearing ratio is slightly high at 42.1%,

management has expressed that they are proactively

looking at ways to bring down the gearing to their comfort

level of below 40% in the long run and has plans in the

pipeline to achieve this.

Debt Maturity Profile (£m)

Source: Company

DPU has outperformed IPO forecast every quarter.

Actual DPU has exceeded IPO forecast consistently

every quarter from 1Q20 to 1Q21 despite the

challenging environment, demonstrating resilience of

Elite Commercial REIT. Going forward, we believe that

the REIT will continue to provide stable returns to

unitholders given its unique counter-cyclical

positioning.

Actual DPU vs DPU projection

1Q20 2Q20 3Q20 4Q20 1Q21

DPU

(pence) 0.74 1.22 1.23 1.26 1.22

DPU

projection

(pence)

0.73 1.20 1.21 1.21 1.20

% change +1.2% +1.5% +1.6% +4.4% +1.7%

Source: Company

3.5

5.8 5.8 5.86.6

0.000

2.000

4.000

6.000

8.000

1Q20 2Q20 3Q20 4Q20 1Q21

21.0 23.1 23.1

10.4 13.7

0.0

10.0

20.0

30.0

40.0

FY20 FY21F FY22F

Initial Portfolio Acquisitions

Page 20

Company Focus

Elite Commercial REIT

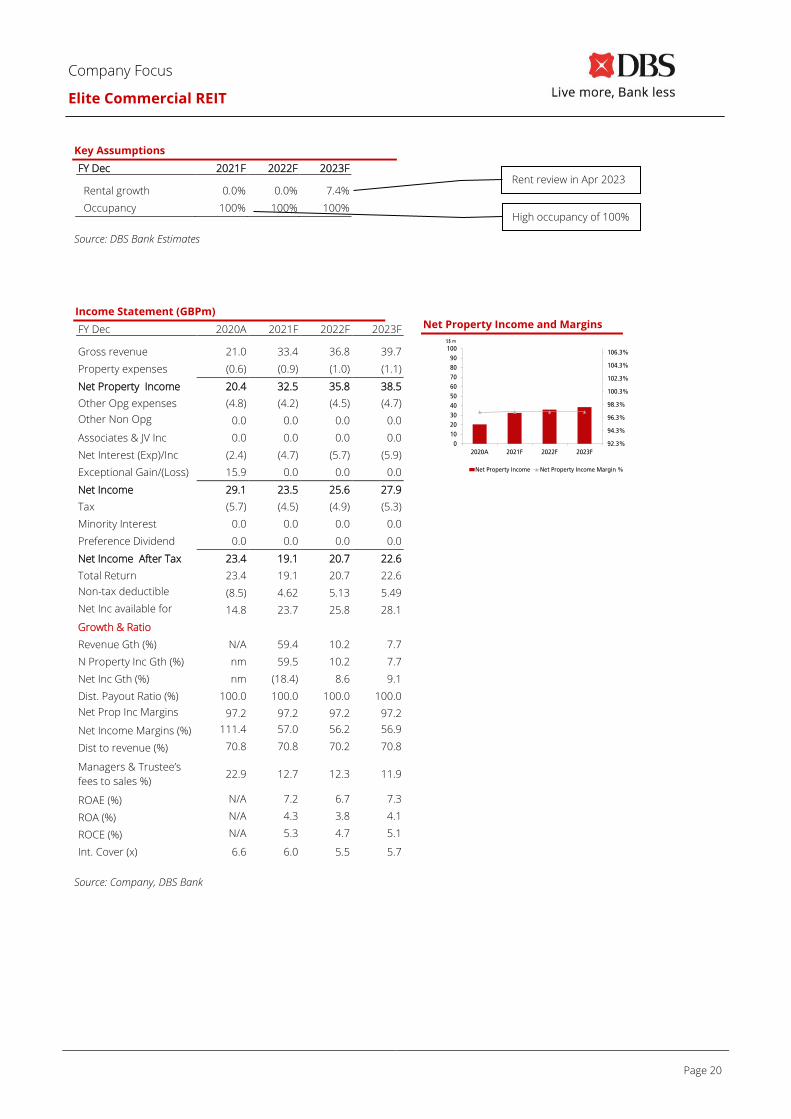

Key Assumptions

FY Dec 2021F 2022F 2023F

Rental growth 0.0% 0.0% 7.4%

Occupancy 100% 100% 100%

Source: DBS Bank Estimates

Income Statement (GBPm)

FY Dec 2020A 2021F 2022F 2023F Gross revenue 21.0 33.4 36.8 39.7

Property expenses (0.6) (0.9) (1.0) (1.1)

Net Property Income 20.4 32.5 35.8 38.5

Other Opg expenses (4.8) (4.2) (4.5) (4.7)

Other Non Opg

(Exp)/Inc 0.0 0.0 0.0 0.0

Associates & JV Inc 0.0 0.0 0.0 0.0

Net Interest (Exp)/Inc (2.4) (4.7) (5.7) (5.9)

Exceptional Gain/(Loss) 15.9 0.0 0.0 0.0

Net Income 29.1 23.5 25.6 27.9

Tax (5.7) (4.5) (4.9) (5.3)

Minority Interest 0.0 0.0 0.0 0.0

Preference Dividend 0.0 0.0 0.0 0.0

Net Income After Tax 23.4 19.1 20.7 22.6

Total Return 23.4 19.1 20.7 22.6

Non-tax deductible

Items (8.5) 4.62 5.13 5.49

Net Inc available for

Dist. 14.8 23.7 25.8 28.1

Growth & Ratio

Revenue Gth (%) N/A 59.4 10.2 7.7

N Property Inc Gth (%) nm 59.5 10.2 7.7

Net Inc Gth (%) nm (18.4) 8.6 9.1

Dist. Payout Ratio (%) 100.0 100.0 100.0 100.0

Net Prop Inc Margins

(%) 97.2 97.2 97.2 97.2

Net Income Margins (%) 111.4 57.0 56.2 56.9

Dist to revenue (%) 70.8 70.8 70.2 70.8

Managers & Trustee’s

fees to sales %) 22.9 12.7 12.3 11.9

ROAE (%) N/A 7.2 6.7 7.3

ROA (%) N/A 4.3 3.8 4.1

ROCE (%) N/A 5.3 4.7 5.1

Int. Cover (x) 6.6 6.0 5.5 5.7

Source: Company, DBS Bank

Net Property Income and Margins

92.3%

94.3%

96.3%

98.3%

100.3%

102.3%

104.3%

106.3%

0

10

20

30

40

50

60

70

80

90

100

2020A 2021F 2022F 2023F

S$ m

Net Property Income Net Property Income Margin %

Rent review in Apr 2023

High occupancy of 100%

Page 21

Company Focus

Elite Commercial REIT

Balance Sheet (GBPm)

FY Dec 2020A 2021F 2022F 2023F Investment Properties 312 528 528 528

Other LT Assets 0.0 0.0 0.0 0.0

Cash & ST Invts 20.2 21.1 21.4 21.6

Inventory 0.0 0.0 0.0 0.0

Debtors 0.88 1.40 1.55 1.67

Other Current Assets 0.0 0.0 0.0 0.0

Total Assets 333 550 551 551

ST Debt

0.0 0.0 0.0 0.0

Creditor 2.54 4.05 4.46 4.81

Other Current Liab 5.36 5.36 5.36 5.36

LT Debt 102 226 226 226

Other LT Liabilities 5.92 5.92 5.92 5.92

Unit holders’ funds 217 309 309 309

Minority Interests 0.0 0.0 0.0 0.0

Total Funds & Liabilities 333 550 551 551

Non-Cash Wkg. Capital (7.0) (8.0) (8.3) (8.5)

Net Cash/(Debt) (81.8) (205) (205) (205)

Ratio

Current Ratio (x) 2.7 2.4 2.3 2.3

Quick Ratio (x) 2.7 2.4 2.3 2.3

Aggregate Leverage (%) 33.7 43.7 43.7 43.7

Source: Company, DBS Bank

Page 22

Company Focus

Elite Commercial REIT

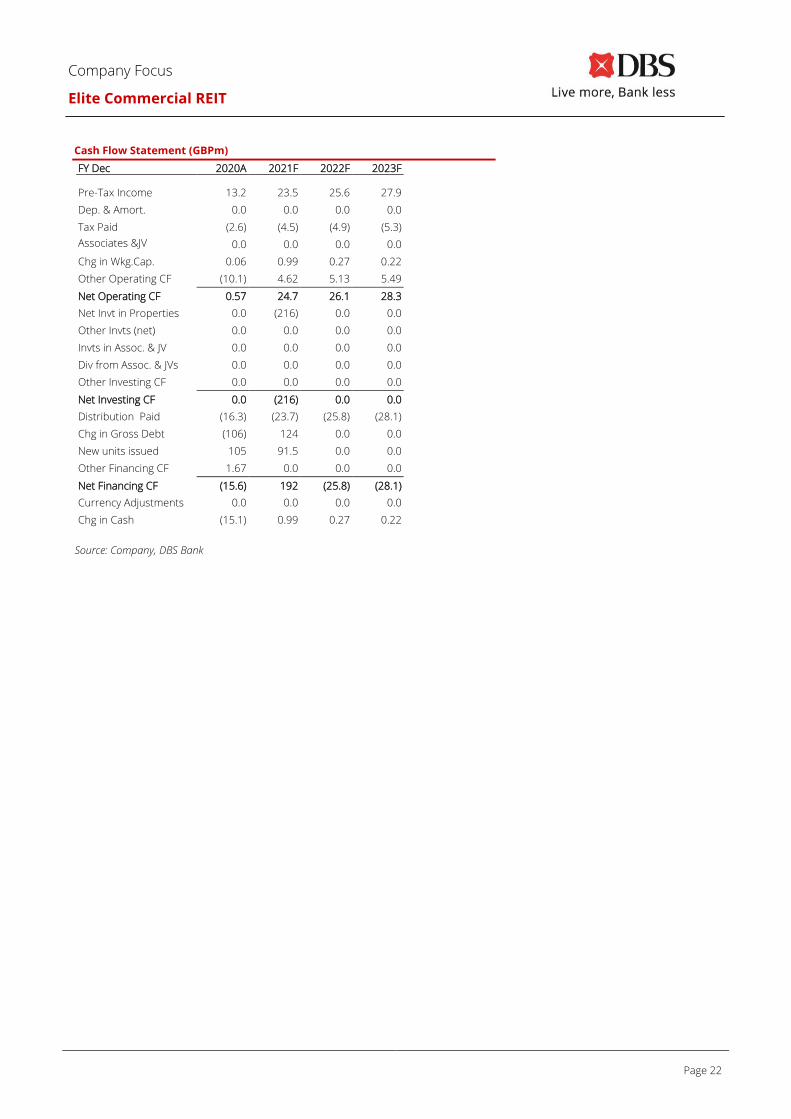

Cash Flow Statement (GBPm)

FY Dec 2020A 2021F 2022F 2023F Pre-Tax Income 13.2 23.5 25.6 27.9

Dep. & Amort. 0.0 0.0 0.0 0.0

Tax Paid (2.6) (4.5) (4.9) (5.3)

Associates &JV

Inc/(Loss) 0.0 0.0 0.0 0.0

Chg in Wkg.Cap. 0.06 0.99 0.27 0.22

Other Operating CF (10.1) 4.62 5.13 5.49

Net Operating CF 0.57 24.7 26.1 28.3

Net Invt in Properties 0.0 (216) 0.0 0.0

Other Invts (net) 0.0 0.0 0.0 0.0

Invts in Assoc. & JV 0.0 0.0 0.0 0.0

Div from Assoc. & JVs 0.0 0.0 0.0 0.0

Other Investing CF 0.0 0.0 0.0 0.0

Net Investing CF 0.0 (216) 0.0 0.0

Distribution Paid (16.3) (23.7) (25.8) (28.1)

Chg in Gross Debt (106) 124 0.0 0.0

New units issued 105 91.5 0.0 0.0

Other Financing CF 1.67 0.0 0.0 0.0

Net Financing CF (15.6) 192 (25.8) (28.1)

Currency Adjustments 0.0 0.0 0.0 0.0

Chg in Cash (15.1) 0.99 0.27 0.22

Source: Company, DBS Bank

Page 23

Company Focus

Elite Commercial REIT

Company Background

The only UK-focused Singapore REIT. Elite Commercial

REIT is a Singapore real estate investment trust (“REIT”)

established with the investment strategy of principally

investing, directly or indirectly, in commercial assets and

real estate-related assets in the United Kingdom (“UK”).

Listed on Singapore Exchange Securities Trading Limited

(SGX-ST) on 6 February 2020, Elite Commercial REIT is the

only UK-focused listed REIT in Singapore. Elite Commercial

REIT’s portfolio comprises 155 predominantly freehold

quality commercial buildings located across the UK, with a

total net internal area of c.3.9m square feet.

Established Sponsors with alignment of interest. The

sponsors of Elite Commercial REIT are Elite Partners

Holdings Pte. Ltd. (“EPH”), Ho Lee Group Pte. Ltd. (“HLG”)

and Sunway RE Capital Pte. Ltd. (“Sunway”). They have an

aggregate of close to 20% interest in the REIT, aligning

their interests with Unitholders.

Trust Structure. The following diagram illustrates the

relationship, among others, between Elite Commercial

REIT, the Manager, the Trustee, the Property Manager,

and the Unitholders.

Structure of Elite Commercial REIT

Source: Company, DBS Bank

Page 24

Company Focus

Elite Commercial REIT

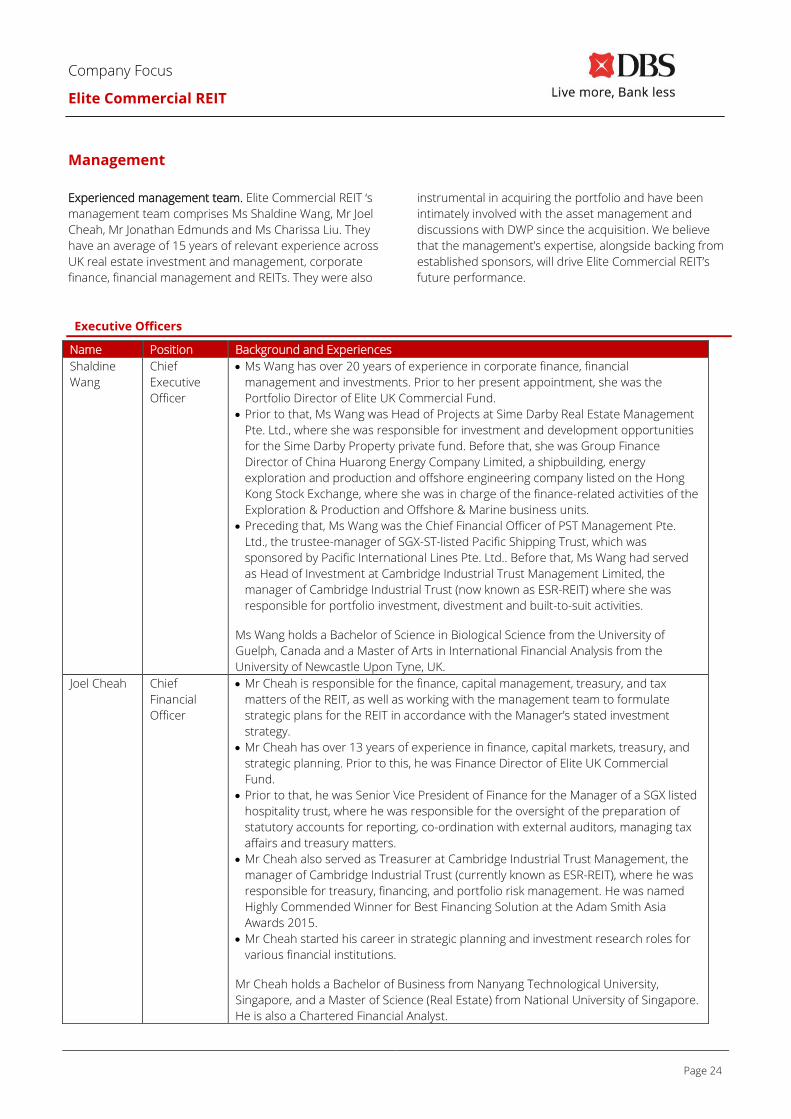

Management

Experienced management team. Elite Commercial REIT ‘s

management team comprises Ms Shaldine Wang, Mr Joel

Cheah, Mr Jonathan Edmunds and Ms Charissa Liu. They

have an average of 15 years of relevant experience across

UK real estate investment and management, corporate

finance, financial management and REITs. They were also

instrumental in acquiring the portfolio and have been

intimately involved with the asset management and

discussions with DWP since the acquisition. We believe

that the management’s expertise, alongside backing from

established sponsors, will drive Elite Commercial REIT’s

future performance.

Executive Officers

Name Position Background and Experiences

Shaldine

Wang

Chief

Executive

Officer

• Ms Wang has over 20 years of experience in corporate finance, financial

management and investments. Prior to her present appointment, she was the

Portfolio Director of Elite UK Commercial Fund.

• Prior to that, Ms Wang was Head of Projects at Sime Darby Real Estate Management

Pte. Ltd., where she was responsible for investment and development opportunities

for the Sime Darby Property private fund. Before that, she was Group Finance

Director of China Huarong Energy Company Limited, a shipbuilding, energy

exploration and production and offshore engineering company listed on the Hong

Kong Stock Exchange, where she was in charge of the finance-related activities of the

Exploration & Production and Offshore & Marine business units.

• Preceding that, Ms Wang was the Chief Financial Officer of PST Management Pte.

Ltd., the trustee-manager of SGX-ST-listed Pacific Shipping Trust, which was

sponsored by Pacific International Lines Pte. Ltd.. Before that, Ms Wang had served

as Head of Investment at Cambridge Industrial Trust Management Limited, the

manager of Cambridge Industrial Trust (now known as ESR-REIT) where she was

responsible for portfolio investment, divestment and built-to-suit activities.

Ms Wang holds a Bachelor of Science in Biological Science from the University of

Guelph, Canada and a Master of Arts in International Financial Analysis from the

University of Newcastle Upon Tyne, UK.

Joel Cheah Chief

Financial

Officer

• Mr Cheah is responsible for the finance, capital management, treasury, and tax

matters of the REIT, as well as working with the management team to formulate

strategic plans for the REIT in accordance with the Manager’s stated investment

strategy.

• Mr Cheah has over 13 years of experience in finance, capital markets, treasury, and

strategic planning. Prior to this, he was Finance Director of Elite UK Commercial

Fund.

• Prior to that, he was Senior Vice President of Finance for the Manager of a SGX listed

hospitality trust, where he was responsible for the oversight of the preparation of

statutory accounts for reporting, co-ordination with external auditors, managing tax

affairs and treasury matters.

• Mr Cheah also served as Treasurer at Cambridge Industrial Trust Management, the

manager of Cambridge Industrial Trust (currently known as ESR-REIT), where he was

responsible for treasury, financing, and portfolio risk management. He was named

Highly Commended Winner for Best Financing Solution at the Adam Smith Asia

Awards 2015.

• Mr Cheah started his career in strategic planning and investment research roles for

various financial institutions.

Mr Cheah holds a Bachelor of Business from Nanyang Technological University,

Singapore, and a Master of Science (Real Estate) from National University of Singapore.

He is also a Chartered Financial Analyst.

Page 25

Company Focus

Elite Commercial REIT

Executive Officers (cont’d)

Jonathan

Edmunds

Chief

investment

Officer

• Mr Edmunds has more than 18 years of experience in the real estate industry,

focusing on real estate investment and management across various sectors globally.

Previously, he was Investment and Asset Management Director of Elite UK

Commercial Fund.

• Preceding that, Mr Edmunds was Director of the Real Estate department of AEP

Investment Management Pte. Ltd., where he was responsible for strategic investment

and transaction management for their UK, Australia, and Singapore mandates. He

was also a lead manager of Basil Property Trust and was responsible for investments,

fund acquisitions and structuring.

• Mr Edmunds had previously worked in the UK and Switzerland. He was Vice

President of the Real Estate department in Beaumont Partners where he was

responsible for fund raising, acquisitions, structuring, reporting, and managing the

Global Student Housing and Multi-Family investment strategy. He also completed the

analysis, structuring and closing of acquisitions for the company’s European and

North American credit income strategies. Prior to that, Mr Edmunds served as

Director of the Real Estate department of WW Advisors Ltd, managing a US$250

million equity mandate to acquire income-producing assets in the UK and Europe.

He originated and managed the acquisition of a portfolio of assets as well as

structured and arranged the debt capital, implemented interest rate hedges and

managed asset performance for the portfolio.

• Earlier in his career, Mr Edmunds was an associate at Lazard, a Corporate Finance

Advisory firm in the UK. He started off as an Associate of Deutsche Bank AG’s Real

Estate Debt Markets department.

Mr Edmunds graduated from University of the West of England with a BA (Hons)

Business Studies. He also holds a Master of Arts in Property Valuation and Law from

The City University in London, UK.

Source: Company, DBS Bank

Page 26

Company Focus

Elite Commercial REIT

DBS Bank recommendations are based an Absolute Total Return* Rating system, defined as follows:

STRONG BUY (>20% total return over the next 3 months, with identifiable share price catalysts within this time frame)

BUY (>15% total return over the next 12 months for small caps, >10% for large caps)

HOLD (-10% to +15% total return over the next 12 months for small caps, -10% to +10% for large caps)

FULLY VALUED (negative total return i.e. > -10% over the next 12 months)

SELL (negative total return of > -20% over the next 3 months, with identifiable catalysts within this time frame)

Share price appreciation + dividends

Completed Date: 22 Jul 2021 06:31:08 (SGT)

Dissemination Date: 22 Jul 2021 06:36:33 (SGT)

Sources for all charts and tables are DBS Bank unless otherwise specified.

GENERAL DISCLOSURE/DISCLAIMER

This report is prepared by DBS Bank Ltd. This report is solely intended for the clients of DBS Bank Ltd, its respective connected and

associated corporations and affiliates only and no part of this document may be (i) copied, photocopied or duplicated in any form or by any

means or (ii) redistributed without the prior written consent of DBS Bank Ltd.

The research set out in this report is based on information obtained from sources believed to be reliable, but we (which collectively refers to

DBS Bank Ltd, its respective connected and associated corporations, affiliates and their respective directors, officers, employees and agents

(collectively, the “DBS Group”) have not conducted due diligence on any of the companies, verified any information or sources or taken into

account any other factors which we may consider to be relevant or appropriate in preparing the research. Accordingly, we do not make any

representation or warranty as to the accuracy, completeness or correctness of the research set out in this report. Opinions expressed are

subject to change without notice. This research is prepared for general circulation. Any recommendation contained in this document does

not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. This document

is for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should

obtain separate independent legal or financial advice. The DBS Group accepts no liability whatsoever for any direct, indirect and/or

consequential loss (including any claims for loss of profit) arising from any use of and/or reliance upon this document and/or further

communication given in relation to this document. This document is not to be construed as an offer or a solicitation of an offer to buy or sell

any securities. The DBS Group, along with its affiliates and/or persons associated with any of them may from time to time have interests in

the securities mentioned in this document. The DBS Group, may have positions in, and may effect transactions in securities mentioned

herein and may also perform or seek to perform broking, investment banking and other banking services for these companies.

Any valuations, opinions, estimates, forecasts, ratings or risk assessments herein constitutes a judgment as of the date of this report, and

there can be no assurance that future results or events will be consistent with any such valuations, opinions, estimates, forecasts, ratings or

risk assessments. The information in this document is subject to change without notice, its accuracy is not guaranteed, it may be incomplete

or condensed, it may not contain all material information concerning the company (or companies) referred to in this report and the DBS

Group is under no obligation to update the information in this report.

This publication has not been reviewed or authorized by any regulatory authority in Singapore, Hong Kong or elsewhere. There is no

planned schedule or frequency for updating research publication relating to any issuer.

The valuations, opinions, estimates, forecasts, ratings or risk assessments described in this report were based upon a number of estimates

and assumptions and are inherently subject to significant uncertainties and contingencies. It can be expected that one or more of the

estimates on which the valuations, opinions, estimates, forecasts, ratings or risk assessments were based will not materialize or will vary

significantly from actual results. Therefore, the inclusion of the valuations, opinions, estimates, forecasts, ratings or risk assessments

described herein IS NOT TO BE RELIED UPON as a representation and/or warranty by the DBS Group (and/or any persons associated with

the aforesaid entities), that:

(a) such valuations, opinions, estimates, forecasts, ratings or risk assessments or their underlying assumptions will be achieved, and

(b) there is any assurance that future results or events will be consistent with any such valuations, opinions, estimates, forecasts, ratings or

risk assessments stated therein.

Please contact the primary analyst for valuation methodologies and assumptions associated with the covered companies or price targets.

Page 27

Company Focus

Elite Commercial REIT

Any assumptions made in this report that refers to commodities, are for the purposes of making forecasts for the company (or companies)

mentioned herein. They are not to be construed as recommendations to trade in the physical commodity or in the futures contract relating

to the commodity referred to in this report.

DBSVUSA, a US-registered broker-dealer, does not have its own investment banking or research department, has not participated in any

public offering of securities as a manager or co-manager or in any other investment banking transaction in the past twelve months and does

not engage in market-making.

ANALYST CERTIFICATION

The research analyst(s) primarily responsible for the content of this research report, in part or in whole, certifies that the views about the

companies and their securities expressed in this report accurately reflect his/her personal views. The analyst(s) also certifies that no part of

his/her compensation was, is, or will be, directly or indirectly, related to specific recommendations or views expressed in the report. The

research analyst (s) primarily responsible for the content of this research report, in part or in whole, certifies that he or his associate1 does

not serve as an officer of the issuer or the new listing applicant (which includes in the case of a real estate investment trust, an officer of the

management company of the real estate investment trust; and in the case of any other entity, an officer or its equivalent counterparty of

the entity who is responsible for the management of the issuer or the new listing applicant) and the research analyst(s) primarily

responsible for the content of this research report or his associate does not have financial interests2 in relation to an issuer or a new

listing applicant that the analyst reviews. DBS Group has procedures in place to eliminate, avoid and manage any potential conflicts of

interests that may arise in connection with the production of research reports. The research analyst(s) responsible for this report operates

as part of a separate and independent team to the investment banking function of the DBS Group and procedures are in place to ensure

that confidential information held by either the research or investment banking function is handled appropriately. There is no direct link of

DBS Group's compensation to any specific investment banking function of the DBS Group.

COMPANY-SPECIFIC / REGULATORY DISCLOSURES

1. DBS Bank Ltd, DBS HK, DBS Vickers Securities (Singapore) Pte Ltd (''DBSVS'') or their subsidiaries and/or other affiliates have proprietary

positions in Manulife US Real Estate Inv, Prime US REIT, Keppel Pacific Oak US REITl, Mapletree Commercial Trust, CapitaLand Integrated

Commercial Trust, Keppel REIT, recommended in this report as of 30 Jun 2021.

2. Neither DBS Bank Ltd nor DBS HK market makes in equity securities of the issuer(s) or company(ies) mentioned in this Research Report.

3. DBS Bank Ltd, DBS HK, DBSVS, their subsidiaries and/or other affiliates have a net long position exceeding 0.5% of the total issued share

capital in Manulife US Real Estate Inv, Prime US REIT, Keppel Pacific Oak US REITl, Mapletree Commercial Trust, recommended in this

report as of 30 Jun 2021.

4. DBS Bank Ltd, DBS HK, DBSVS, DBSVUSA or their subsidiaries and/or other affiliates beneficially own a total of 1% of any class of

common equity securities of Manulife US Real Estate Inv, Prime US REIT, Keppel Pacific Oak US REITl, as of 30 Jun 2021.

Compensation for investment banking services:

5. DBS Bank Ltd, DBS HK, DBSVS, their subsidiaries and/or other affiliates of DBSVUSA have received compensation, within the past 12

months for investment banking services from IREIT Global, CapitaLand Integrated Commercial Trust, as of 30 Jun 2021.

6. DBS Bank Ltd, DBS HK, DBSVS, their subsidiaries and/or other affiliates of DBSVUSA, within the next 3 months, will receive or intend to

seek compensation for investment banking services from Prime US REIT, as of 30 Jun 2021.

.

1 An associate is defined as (i) the spouse, or any minor child (natural or adopted) or minor step-child, of the analyst; (ii) the trustee of a trust

of which the analyst, his spouse, minor child (natural or adopted) or minor step-child, is a beneficiary or discretionary object; or (iii) another

person accustomed or obliged to act in accordance with the directions or instructions of the analyst.

2 Financial interest is defined as interests that are commonly known financial interest, such as investment in the securities in respect of an

issuer or a new listing applicant, or financial accommodation arrangement between the issuer or the new listing applicant and the firm or

analysis. This term does not include commercial lending conducted at arm's length, or investments in any collective investment scheme

other than an issuer or new listing applicant notwithstanding the fact that the scheme has investments in securities in respect of an issuer

or a new listing applicant.

Page 28

Company Focus

Elite Commercial REIT

7. DBS Bank Ltd, DBS HK, DBSVS, their subsidiaries and/or other affiliates of DBSVUSA have managed or co-managed a public offering of

securities for IREIT Global, Keppel REIT, CapitaLand Integrated Commercial Trust, in the past 12 months, as of 30 Jun 2021.

8. DBSVUSA does not have its own investment banking or research department, nor has it participated in any public offering of securities

as a manager or co-manager or in any other investment banking transaction in the past twelve months. Any US persons wishing to

obtain further information, including any clarification on disclosures in this disclaimer, or to effect a transaction in any security discussed

in this document should contact DBSVUSA exclusively.