energy and reserve market designs with explicit

TRANSCRIPT

8/13/2019 Energy and Reserve Market Designs With Explicit

http://slidepdf.com/reader/full/energy-and-reserve-market-designs-with-explicit 1/7

IEEE TRANSACTIONS ON POWER SYSTEMS, VOL. 18, NO. 1, FEBRUARY 2003 53

Energy and Reserve Market Designs With ExplicitConsideration to Lost Opportunity Costs

Deqiang Gan and Eugene Litvinov

Abstract—The primary goal of this work is to investigate thebasic energy and reserve dispatch optimization (cooptimization)in the setting of a pool-based market. Of particular interest is themodeling of lost opportunity cost introduced by reserve allocation.We derive the marginal costs of energy and reserves under a va-riety of market designs. We also analyze existence, algorithm, andmultiplicity of optimal solutions. The results of this study are usedto support the reserve market design and implementation in ISONew England control area.

Index Terms—Electricity market, marginal pricing, optimiza-tion, power systems, spinning reserve.

NOMENCLATURE

Node energy demand, a vector.

System reserve demand (or requirement), a scalar.

Unit vector, every elements of is unity.

Lost opportunity cost function.

Transmission thermal limit vector.

Index set of generators (consists of 1, 2, 3, …).

Lost opportunity cost price.

Energy bid price/generation.

Reserve bid price/allocation.

Generation sensitivity factor matrix.

Equals to 1 or 0 indicating if a generator incurs lost

opportunity cost.Energy nodal price vector.

Reserve clearing price.

I. INTRODUCTION

THERE EXIST two school of thoughts for market design asderegulation in power industry proceeds. They are com-

monly known as pool model and bilateral model [1], [2]. ISONew England (ISO-NE) control area electricity market followsthe concept of pool model [3] and [4].

In a pool-based market, energy and reserves are centrally andoptimally allocated based on volunteer bids (in this paper re-

serve refers to 10-min spinning reserve). Under two-settlementdesign [4], the allocation of energy and reserves is implemented

in two steps—day-ahead scheduling and real-time dispatch. The

optimization concepts of the two steps are, broadly speaking,similar. In this study, we focus on the market design issues inthe real-time dispatch setting.

Manuscript received January 23, 2002; revised June 21, 2002.D. Gan was with ISO New England, Inc., Holyoke, MA 01040 USA.

He is now at Zhejiang University, Zhejiang 310027, China (e-mail:[email protected]).

E. Litvinov is with ISO New England, Inc., Holyoke, MA 01040 USA(e-mail: [email protected]).

Digital Object Identifier 10.1109/TPWRS.2002.807052

While the idea of locational marginal pricing advocated in

[5]–[7] seemingly dominates the pool-based energy markets,

there is little consensus on how to structure reserve markets.

In fact, the design of reserve markets is often a debatable

topic. Discussions on this topic can be found in, say, [8]–[12],

[22].

One of the current major tasks in the ISO New England, Inc. is

to study and possibly improve the existing reserve market. Aside

from a long-term forward market, which will not be discussed

here, the following four alternative designs received attention in

this effort:

• generators receive availability payments—model (A);

• generators receive lost opportunity cost payments—model

(L);

• generators receive availability and lost opportunity cost

payments—model (A L);

• generators receive either availability or lost opportunity

cost payment—model (A L).

Availability payment refers to the payment to generators that

offer reserve capability to the market. The definition of lost op-

portunity cost incurred in reserve allocation can be found in the

next section. More details about it can be found in New York,

PJM, or the New England ISO website. The existing ISO-NE

market, which is undertaking a major revision, follows model(A L). The revised market design will likely follow a variant

of model (A L) as outlined in [23]. We will briefly discuss this

revised market design subsequently.

The three electricity markets in the Northeastern U.S. all have

or will have energy and reserve markets where lost opportu-

nity costs are explicitly compensated. Whether or not generator

lost opportunity cost should be compensated is a policy issue. If

under certain market design generators do receive lost opportu-

nity cost compensation, then energy, reserve, and lost opportu-

nity cost are cooptimized. This is at present a common practice.

A systematic treatment on the formulation, solution algorithm,

and pricing analysis of cooptimization becomes a timely issue.

The primary goal of this work is to study the basic princi-ples of cooptimization, laying down the engineering founda-

tions of energy/reserve market design. The results can also be

valuable for market implementation. We do not investigate how

to choose the optimal market design which would require sub-

stantial economic analysis [13]–[15], [24]. Of particular interest

in this work is to present a general approach for modeling lost

opportunity cost. In the context of cooptimization, we derive

the formulae for calculating marginal costs under a variety of

market designs. We also investigate such issues as solution ex-

istence, algorithm, and multiplicity of cooptimization.

0885-8950/03$17.00 © 2003 IEEE

8/13/2019 Energy and Reserve Market Designs With Explicit

http://slidepdf.com/reader/full/energy-and-reserve-market-designs-with-explicit 2/7

8/13/2019 Energy and Reserve Market Designs With Explicit

http://slidepdf.com/reader/full/energy-and-reserve-market-designs-with-explicit 3/7

GAN AND LITVINOV: ENERGY MARKET DESIGNS WITH CONSIDERATION TO LOST OPPORTUNITY COSTS 55

A. Optimization Formulation and Solution Existence

Let us define a constant vector as follows:

(8)

we have

(9)

The graph of a lost opportunity cost function is illustrated in

Fig. 2. Obviously, it is nondifferentiable but it is continuous.

The problem of energy and reserve dispatch with considera-

tion of lost opportunity cost is as follows:

(10-1)

(10-2)

(10-3)

(10-4)

(10-5)

(10-6)

(10-7)

The above model corresponds to market design model

(A L). To obtain the optimization model for market design

model (A), one only needs to assume that in the above

model. To obtain the optimization model for market design,

model (L), one needs to assume that in the above model.

In the recent proposal [23], generators that are able to provide

reserves are classified as tier 1 and tier 2 resources. In a nutshell,

tier 1 resources do not incur lost opportunity cost while tier 2 re-

sources do. The optimization formulation for tier 1 resource is

simply an energy-only optimization, and the optimization for-mulation for tier 2 resources is similar to that of model (A L).

By the continuity of objective function of the above problem,

the answer to the question of solution existence is a qualified

“yes,” provided the feasible set of the problem is nonempty [16,

Weierstrass Theorem].

Now let us briefly discuss the optimization formulation for

model (A L). It can be stated as follows:

(11-1)

(11-2)

(11-3)

(11-4)

(11-5)

(11-6)

(11-7)

The 0–1 variables are introduced to enforce the condition

that a generator either receives reserve availability payment or

lost opportunity cost payment. Mathematically, this model is

similar to model (A L), so we will not discuss it further. But the

results to be presented can be extended to deal with this model.

Before proceeding to study the solution algorithm, we note

that locational reserve requirements are not discussed here

Fig. 2. Lost opportunity cost function when a constant price is used.

but theoretically they could be incorporated into the presented

framework without conceptual difficulty using methods pre-

sented in the literature [17], [18].

B. Solution Algorithm

This section suggests a solution algorithm for the optimiza-

tion problem (10). First, let us convert the nondifferentiable lostopportunity cost function into a discrete function as follows:

(12)

With the above manipulations, the energy and reserve dispatch

problem can be reformulated as a 0–1 mixed integer program-

ming problem as

(13-1)

(13-2)(13-3)

(13-4)

(13-5)

(13-6)

(13-7)

(13-8)

The above 0–1 problem can be solved using the standard

branch- and-bound method [19]. Note that the integer variables

are associated with generators with reserve capabilities only. In

ISO-NE, the number of generators is approximately 350, but the

number of generators that have reserve capability is only about

50.

Whether or not the standard branch-and-bound algorithm can

meet the requirement of real-time application is out of the scope

of this study. However, the formulation (13) allows us to inves-

tigate the pricing issues of energy and reserves.

C. Optimality Conditions and Marginal Costs

Suppose we find the optimal integer solution . Now it is

straightforward to derive the marginal costs of energy and re-

serve. As usual, let , , , and be Lagrangian multipliers

8/13/2019 Energy and Reserve Market Designs With Explicit

http://slidepdf.com/reader/full/energy-and-reserve-market-designs-with-explicit 4/7

56 IEEE TRANSACTIONS ON POWER SYSTEMS, VOL. 18, NO. 1, FEBRUARY 2003

of constraints in equations (15)–(17), we form the Lagrangian

function as follows:

(14)

If the th generatorhas lost opportunity cost, then we have that

, . By the standard Kuhn–Tucker optimality

conditions, we have that , and

(15-1)

(15-2)

The nodal energy prices are given by the marginal cost vector

[5], [6]. The reserve price is also set to the

marginal cost .

If the th generator does not have lost opportunity cost, we

have , . By the standard Kuhn–Tucker

optimality theory, . It follows that:

(16-1)

(16-2)

The energy price is again the marginal cost .

The reserve price is still given by . In the next section, we will

present a pricing analysis based on equations (15) and (16).

V. PRICING ANALYSIS FOR ALTERNATIVE MARKET DESIGNS

In this section, we present a pricing analysis for each of the

models mentioned in the previous section. Whenever possible,

we will indicate if multiple solutions exist.

A. Model (A)

Under this simple model, . The reserve clearing priceequals to the reserve availability price of the most expensive

generator that is designated to supply reserve. The past expe-

rience gained in ISO-NE is that bid prices for reserves are often

zero because for many generators reserve costs are sunk costs

and they are ensured lost opportunity costs. Under model (A), it

is less likely that generators will ask for zero reserve prices be-

cause they do not receive lost opportunity cost. However, there

is no guarantee that most generators will ask for reserve prices

that are greater than zero.

When the bid prices for reserves of many generators are equal

to zero (under uniform price auction many generators do bid

zero prices), then it is likely that and, generally, there are

multiple solutions in reserve allocation. In fact, there is a con-

tinuum of reserve solutions. For instance, consider the following

problem:

(17-1)

(17-2)

(17-3)

(17-4)

The optimal energy dispatch is , , but any

reserve dispatch that meets is an optimal reserve

dispatch. To find an unique solution, one method is to designate

reserve contributions to the generators with lowest energy bid

prices.

A major concern about this model is that when cheaper and

fast-start generators are backed down to provide reserve, they

have a disincentive to follow ISO dispatch instructions.

B. Model (L)

Under thismodel, . Let usconsider two situations. Inthefirst situation, the optimal dispatch does not require paying gen-

erators lost opportunity cost. This is just the situation in model

(A) when the bid prices for reserves are all equal to zero. So it is

quite possible that there are multiple solutions for reserve allo-

cation. To resolve this problem, again, one could designate re-

serve contributions to generators with lowest energy bid prices.

Now let us consider the second situation where, in the optimal

dispatch, some generators are paid lost opportunity cost. In the

sequel, we show that the marginal cost of producing reserves,

, can still be greater than zero. To get a feel of what could

be, let us derive an alternative expression of from equations

(15-1)–(15-2)

(18)

When there is no congestion, it is obvious that . Since

,

(19)

Recall that the marginal cost of a product is equal to the

change of production cost as the demand increases by a small

amount [20]. Based on this principle, let us verify the result (19)

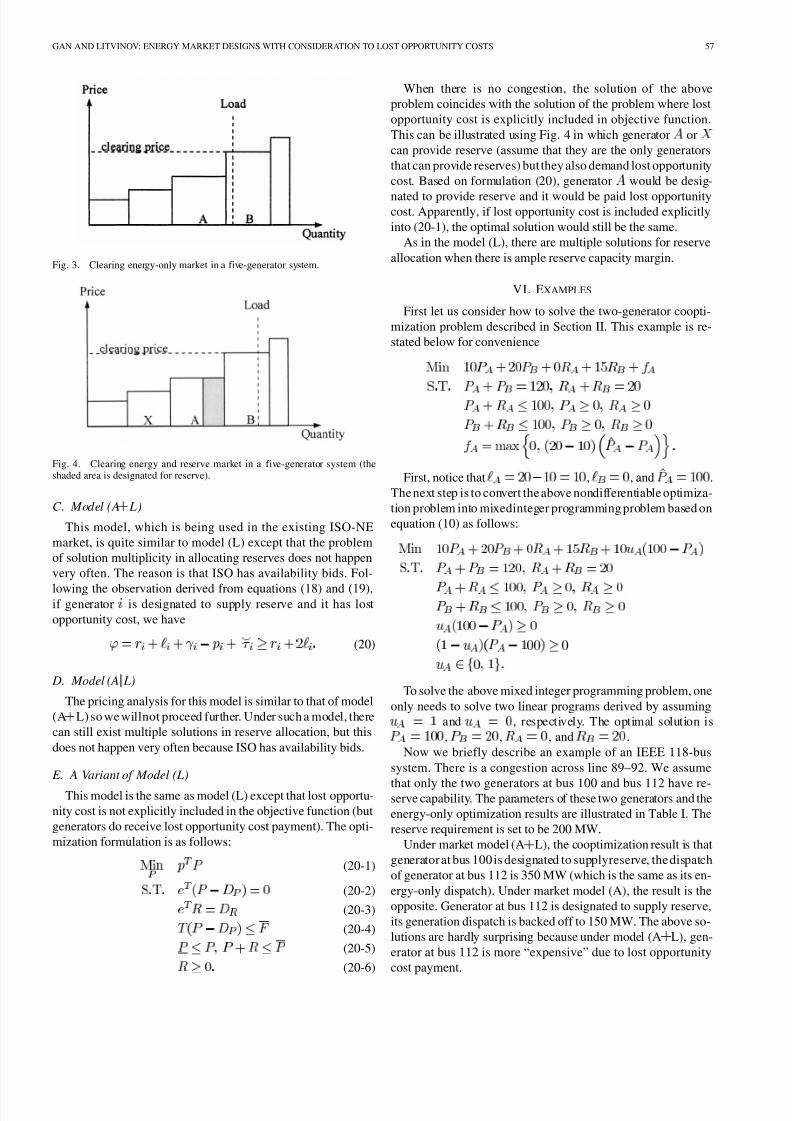

by looking at an example noncongested five-generator system as

illustrated in Figs. 3 and 4.

Suppose reserve requirement is increased by a infinitesimal .

Suppose generator is the only one that is capable of supplying

reserve, the change of total production cost would consist of

three components

• energy cost increase of generator , which is ;

• energy cost decrease of generator , which is ;

• lost opportunity cost increase of generator , which is

.

Note that happens to be equal to the clearing price. The

change of production cost would be

. This indicates that the reserve marginal cost is equal to

which is consistent with the result in (19) if one considers

that and in this example.

8/13/2019 Energy and Reserve Market Designs With Explicit

http://slidepdf.com/reader/full/energy-and-reserve-market-designs-with-explicit 5/7

GAN AND LITVINOV: ENERGY MARKET DESIGNS WITH CONSIDERATION TO LOST OPPORTUNITY COSTS 57

Fig. 3. Clearing energy-only market in a five-generator system.

Fig. 4. Clearing energy and reserve market in a five-generator system (theshaded area is designated for reserve).

C. Model (A L)

This model, which is being used in the existing ISO-NE

market, is quite similar to model (L) except that the problem

of solution multiplicity in allocating reserves does not happen

very often. The reason is that ISO has availability bids. Fol-

lowing the observation derived from equations (18) and (19),if generator is designated to supply reserve and it has lost

opportunity cost, we have

(20)

D. Model (A L)

The pricing analysis for this model is similar to that of model

(A L) so we willnot proceed further. Under such a model, there

can still exist multiple solutions in reserve allocation, but this

does not happen very often because ISO has availability bids.

E. A Variant of Model (L)

This model is the same as model (L) except that lost opportu-

nity cost is not explicitly included in the objective function (but

generators do receive lost opportunity cost payment). The opti-

mization formulation is as follows:

(20-1)

(20-2)

(20-3)

(20-4)

(20-5)

(20-6)

When there is no congestion, the solution of the above

problem coincides with the solution of the problem where lost

opportunity cost is explicitly included in objective function.

This can be illustrated using Fig. 4 in which generator or

can provide reserve (assume that they are the only generators

that can provide reserves) but they also demand lost opportunity

cost. Based on formulation (20), generator would be desig-

nated to provide reserve and it would be paid lost opportunitycost. Apparently, if lost opportunity cost is included explicitly

into (20-1), the optimal solution would still be the same.

As in the model (L), there are multiple solutions for reserve

allocation when there is ample reserve capacity margin.

VI. EXAMPLES

First let us consider how to solve the two-generator coopti-

mization problem described in Section II. This example is re-

stated below for convenience

First, notice that , , and .

The next step is to convert the above nondifferentiable optimiza-

tion problem into mixedinteger programming problem based on

equation (10) as follows:

To solve the above mixed integer programming problem, one

only needs to solve two linear programs derived by assumingand , respectively. The optimal solution is

, , , and .

Now we briefly describe an example of an IEEE 118-bus

system. There is a congestion across line 89–92. We assume

that only the two generators at bus 100 and bus 112 have re-serve capability. The parameters of these two generators and the

energy-only optimization results are illustrated in Table I. The

reserve requirement is set to be 200 MW.

Under market model (A L), the cooptimization result is that

generator at bus 100 is designated to supplyreserve, the dispatch

of generator at bus 112 is 350 MW (which is the same as its en-

ergy-only dispatch). Under market model (A), the result is the

opposite. Generator at bus 112 is designated to supply reserve,

its generation dispatch is backed off to 150 MW. The above so-

lutions are hardly surprising because under model (A L), gen-

erator at bus 112 is more “expensive” due to lost opportunity

cost payment.

8/13/2019 Energy and Reserve Market Designs With Explicit

http://slidepdf.com/reader/full/energy-and-reserve-market-designs-with-explicit 6/7

58 IEEE TRANSACTIONS ON POWER SYSTEMS, VOL. 18, NO. 1, FEBRUARY 2003

TABLE IPARAMETERS OF TWO GENERATORS OF 118-BUS TEST SYSTEM

VII. FORMULATION WHEN VARIABLE PRICE IS USED IN

CALCULATING LOST OPPORTUNITY COST

In this section, we assume that lost opportunity cost function

takes the most general form (6). This optimization is self-ref-

erential because the lost opportunity cost depends on variable

price which is not known until the final solution is obtained.

In this section, we suggest a method to get around this impasse.

Let us suppose temporarily that the reserve dispatch is given,

let itbe . Then, itis trivialto compute optimal energy dispatchand resultant energy prices

(21-1)

(21-2)

(21-3)

(21-4)

The Lagrangian function of the above optimization problem

is easily obtained as

(22)The spot prices are given by . The key to

solving the problem is to find out an energy dispatch that is

optimized taking into account reserve requirements. Consider

the following bilevel optimization problem:

(23-1)

(23-2)

(23-3)

(23-4)

(23-5)

(23-6)

(23-7)

(23-8)

In the above formulation, is a variable in the upper-level

optimization and a parameter in the lower-level optimization.

stays in the lower-level optimization subproblem. The primal

solution of the above bilevel optimization problem is the desired

optimal dispatch of energy and reserves. The dual solution con-

tains locational marginal prices.

In what follows we describe briefly how to solve the bilevel

optimization problem (23). By the standard theory of linear

programming, the primal and dual solutions of the lower-level

subproblem depend on the optimal basis of the lower-level

subproblem, that is

(24-1)

(24-2)

where is the right-hand-side of the lower-level sub-

problem, it is a linear function of .

To attack the bilevel optimization problem, observe that and

do not depend on the specific value of , rather they depend

on which constraints are included in optimal basis only. As a

result, suppose temporarily that the optimal basis is known,

then energy prices are known. Let it be and be as defined

based on (8). Now the bilevel optimization problem can be cast

as

(25-1)

(25-2)

(25-3)

(25-4)

The above problem possesses a structure that is similar to that

of (10). It can be solved using the general algorithm described

in Section IV-B.

The question remains to be how to find out the optimal basis.

One obvious solution is to enumerate all of the combinations

of bases of the lower-level subproblem. For example, in the

five-generator system illustrated in Fig. 3, where each gener-

ator is required to submit a single block bid, there are only five

possible energy prices. A better solution is to apply a standardbranch-and-bound algorithm [19]. Since a branch-and-bound al-

gorithm is fairly familiar to the power engineering audience,

we will not discuss it here. The readers are referred to [ 19] for

details.

VIII. FINAL REMARKS

In this paper, we studied four alternative energy/reserve

market designs that received attention in ISO-NE. We presented

a fairly detailed analysis on the basic formulation, solution

algorithm, and pricing formulae of cooptimization under these

market designs. The results of the research have been used

to support, from engineering perspective, the reserve marketdesign and implementation in ISO-NE. Many of the questions

raised during discussions on reserve market design at ISO-NE

are answered. The main finding is that energy, reserve, and lost

opportunity cost cooptimization are, in general, a nondifferen-

tiable and possibly bilevel optimization problem. This problem

can be further converted into a mixed integer programming

problem. A standard algorithm for solving these problems is

that of branch and bound. This algorithm can be efficient or

exceedingly slow, depending upon the size of the problem.

Whether or not a standard branch-and-bound algorithm can

meet engineering requirements is thus a subject of additional

research.

8/13/2019 Energy and Reserve Market Designs With Explicit

http://slidepdf.com/reader/full/energy-and-reserve-market-designs-with-explicit 7/7

GAN AND LITVINOV: ENERGY MARKET DESIGNS WITH CONSIDERATION TO LOST OPPORTUNITY COSTS 59

ACKNOWLEDGMENT

The authors have benefitted from the discussions in ISO-NE

Reserve Market Design Working Group. The opinions described

in the paper do not necessarily reflect those of ISO New Eng-

land, Inc. The authors remain solely responsible for errors.

REFERENCES

[1] H. Singh, S. Hao, and A. Papalexopoulos, “Transmission congestionmanagement in competitive electricity markets,” IEEE Trans. Power Syst., vol. 13, pp. 672–680, May 1998.

[2] F. F. Wu and P. Varaiya, “Coordinated multilateral trades for electricpower networks: Theory and implementation,” Int. J. Elect. Power En-ergy Syst., vol. 21, no. 2, 1999.

[3] K. W. Cheung, P. Shamsollahi, D. Sun, J. Milligan, and M. Potishnak,“Energy and ancillary service dispatch for the interim ISO New Englandelectricity market,” IEEE Trans. Power Syst., vol. 15, pp. 968–974, Aug.2000.

[4] D. Gan and Q. Chen, “Locational marginal pricing: New England per-spective, presentation summary for panel session flow-gate and locationbased pricing approaches and their impacts,” in Proc. IEEE Power Eng.Soc. Winter Meeting, Columbus, OH, Jan. 2001.

[5] M. C. Caramanis, R. E. Bohn, and F. C. Schweppe, “Optimal spotpricing: Practice and theory,” IEEE Trans. Power App. Syst., vol.

PAS–101, pp. 3234–3245, Sept. 1982.[6] M. L. Baughman andS. N. Siddiqi, “Real timepricing ofreactive power:

Theory and case study results,” IEEE Trans. Power Syst., vol. 6, pp.23–29, Feb. 1991.

[7] W. W. Hogan, “Contract networks for electric power transmission,” J. Regulator Econ., vol. 4, pp. 211–242, 1992.

[8] D. Chattopadhyay, B. B. Chakrabarti, and E. G. Read, “Pricing forvoltage stability,” in Proc. PICA, Melbourne, Australia, May 2001.

[9] E. H. Allen and M. D. Ilic, “Reserve markets for power systems relia-bility,” IEEE Trans. Power Syst., vol. 15, pp. 228–233, Feb. 2000.

[10] H. Singh and A. Papalexopoulos, “Competitive procurement of ancillaryservices by an independent system operator,” IEEE Trans. Power Syst.,vol. 14, pp. 498–504, May 1999.

[11] M. Flynn, W. P. Sheridan, J. D. Dillon, and M. J. O’Malley, “Reliabilityand reserve in competitive electricity market scheduling,” IEEE Trans.Power Syst., vol. 16, pp. 78–87, Feb. 2001.

[12] X. Ma, D. Sun, and K. Cheung, “Energy and reserve dispatch in a

multi-zone electricity market,” IEEE Trans. Power Syst., vol. 14, pp.913–919, Aug. 1999.[13] D. Gan and D. V. Bourcier, “Locational market power screen and con-

gestion management: Experience and suggestions,” IEEE Trans. Power Syst., vol. 17, pp. 180–185, Feb. 2002.

[14] R. J. Green, “Competition in generation: The economic foundations,”Proc. IEEE , vol. 88, pp. 128–139, Feb. 2000.

[15] R. Zimmerman, R. Thomas, D. Gan, and C. Murillo-Sanchez, “A web-based platform for experimental investigation of electric power auc-tions,” Decision Support Syst., vol. 24,no. 3&4, pp.193–205, Jan. 1999.

[16] M. S. Bazaraa, H. D. Sherali, and C. M. Shetty, Nonlinear Program-ming—Theory and Algorithms, 2nd ed. New York: Wiley, 1993.

[17] S. Hao and D. Shirmohammadi, “Clearing prices computation for in-tegrated generation, reserve and transmission markets,” in Proc. PICA,Sydney, Australia, May 2001.

[18] M. Aganagic, K. H. Abdul-Rahman, and J. G. Waight, “Spot pricing

of capacities for generation and transmission of reserve in an extendedpoolco model,” IEEE Trans. Power Syst., vol. 13, pp. 1128–1134, Aug.1998.

[19] J. F. Bard, Practical Bilevel Optimization—Algorithms and Applica-tions. Norwell, MA: Kluwer, 1998.

[20] P. R. Gribik, G.A. Angelidis,and R. R. Kovas, “Transmissionaccessandpricing with multiple separate energy forward markets,” IEEE Trans.Power Syst., vol. 14, pp. 865–876, Aug. 1999.

[21] A. Jayantilal, K. W. Cheung, P. Shamsollahi, and F. S. Bresler, “Marketbased regulation for thePJM electricity market,” in Proc. PICA, Sydney,Australia, May 2001.

[22] N. S. Rau, “Optimal dispatch of a system based on offers and bids—Amixed integer LP formulation,” IEEE Trans. Power Syst., vol. 14, pp.274–279, Feb. 1999.

[23] PJM Interconnection, L.L.C. (2001, July) Spinning Reserve MarketBusiness Rules. [Online]. Available: http://www.pjm.com.

[24] K. Seeley, J. Lawarree, and C.-C. Liu, “Analysis of electricity market

rules and their effects on strategic behavior in a noncongestive grid,” IEEE Trans. Power Syst., vol. 15, pp. 157–162, Feb. 2000.

Deqiang Gan received the Ph.D.degree in electrical engineering from XianJiaotong University, Xian, China, in 1994.

Currently, he is with Zhejiang University, Zhejiang, China. He was a SeniorAnalyst in ISO New England, Inc., Holyoke, MA, where he worked on is-sues related to the design, implementation, and economic analysis of electricitymarkets. Prior to joining ISO New England, Inc., he held research positions atseveral universities in the U.S. and Japan.

Eugene Litvinov obtained the B.S. and M.S. degrees from the Technical Uni-versity, Kiev, Ukraine, U.S.S.R., and the Ph.D. degree from Urals PolytechnicInstitute, Sverdlovsk, Russia.

Currently, he is a Director of Technology with the ISO New England,Holyoke, MA. His main interests are power system market clearing models,system security, computer applications to power systems, and informationtechnology.