equity story - dnb · 2017-12-15 · average equity (lhs) roe roe ambition roe using peer average...

TRANSCRIPT

December 2017

Equity story

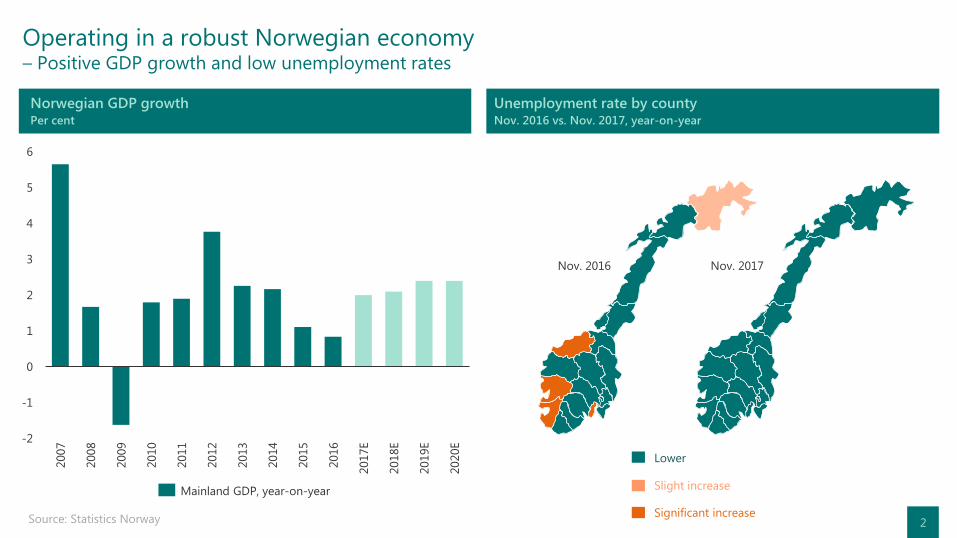

Operating in a robust Norwegian economy – Positive GDP growth and low unemployment rates

2 Source: Statistics Norway

Norwegian GDP growth Per cent

Unemployment rate by county Nov. 2016 vs. Nov. 2017, year-on-year

Significant increase

Slight increase

Lower

-2

-1

0

1

2

3

4

5

6

2007

2010

2014

2012

2011

2008

2009

2013

2015

2016

2017E

2018E

2019E

2020E

Mainland GDP, year-on-year

Nov. 2016 Nov. 2017

-200

0

200

400

600

800

1,000

1,200

1,400

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

2001 2003 2005 2007 2009 2011 2013 2015 2017

Market value of fund (lhs)

Net cash flow from oil-related industries (rhs)

Financial returns incl. dividends (rhs)

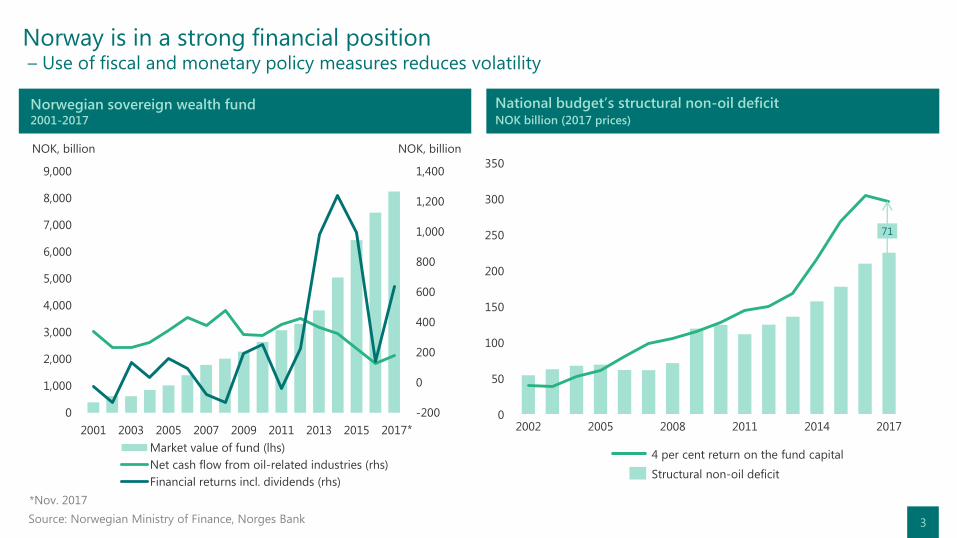

Norway is in a strong financial position – Use of fiscal and monetary policy measures reduces volatility

Source: Norwegian Ministry of Finance, Norges Bank

Norwegian sovereign wealth fund 2001-2017

National budget’s structural non-oil deficit NOK billion (2017 prices)

*

*Nov. 2017

NOK, billion NOK, billion

0

50

100

150

200

250

300

350

2017 2002 2014 2005 2008 2011

4 per cent return on the fund capital

Structural non-oil deficit

71

3

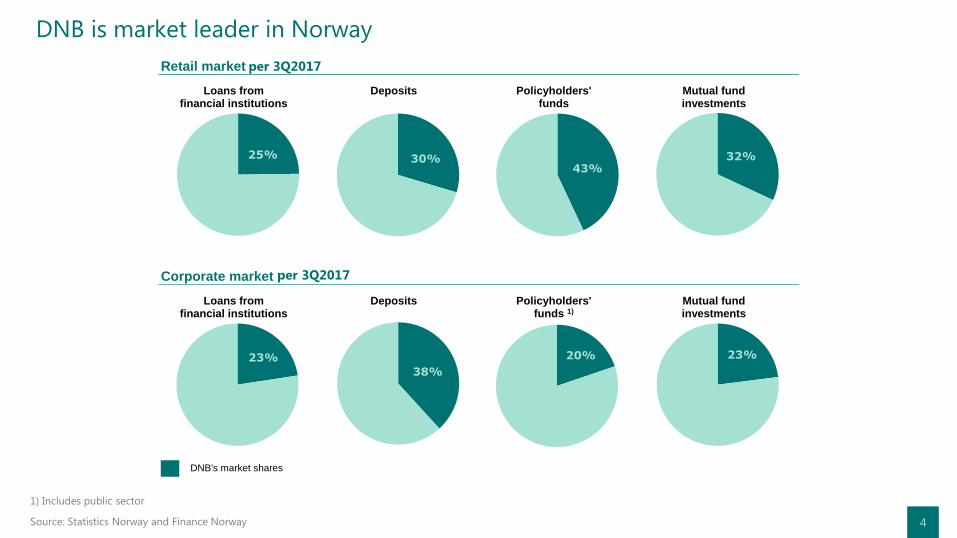

DNB is market leader in Norway Oppdatert

22.10 Retail market

Corporate market

DNB's market shares

1) Includes the public sector.

Source: Statistics Norway and Finance Norway

Loans fromfinancial institutions

25%

Deposits

30%

Policyholders'funds

43%

Mutual fundinvestments

32%

Loans fromfinancial institutions

23%

Deposits

38%

Policyholders'funds 1)

20%

Mutual fundinvestments

23%

per 3Q2017

per 3Q2017

1) Includes public sector

Source: Statistics Norway and Finance Norway 4

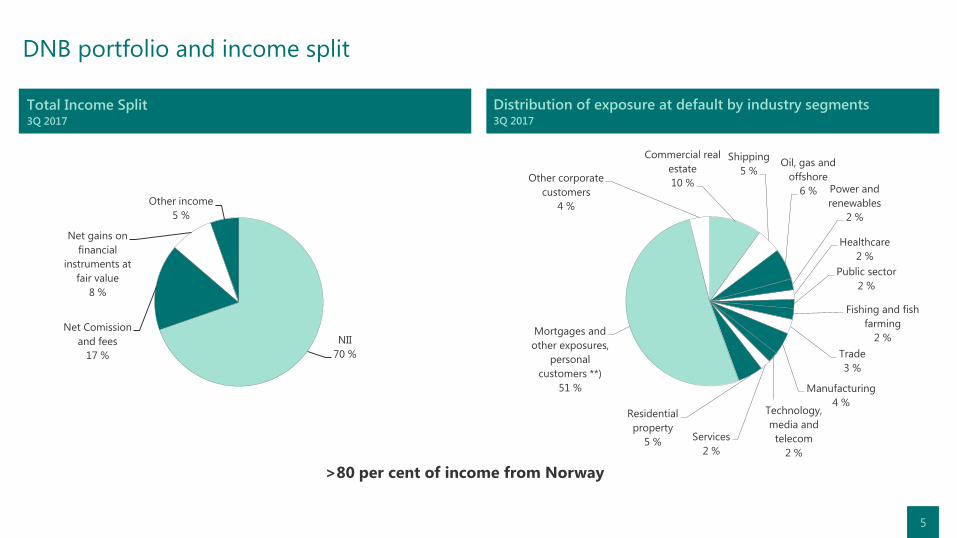

DNB portfolio and income split

5

Distribution of exposure at default by industry segments 3Q 2017

Total Income Split 3Q 2017

Commercial real

estate

10 %

Shipping

5 % Oil, gas and

offshore

6 % Power and

renewables

2 %

Healthcare

2 %

Public sector

2 %

Fishing and fish

farming

2 %

Trade

3 %

Manufacturing

4 % Technology,

media and

telecom

2 %

Services

2 %

Residential

property

5 %

Mortgages and

other exposures,

personal

customers **)

51 %

Other corporate

customers

4 %

NII

70 %

Net Comission

and fees

17 %

Net gains on

financial

instruments at

fair value

8 %

Other income

5 %

>80 per cent of income from Norway

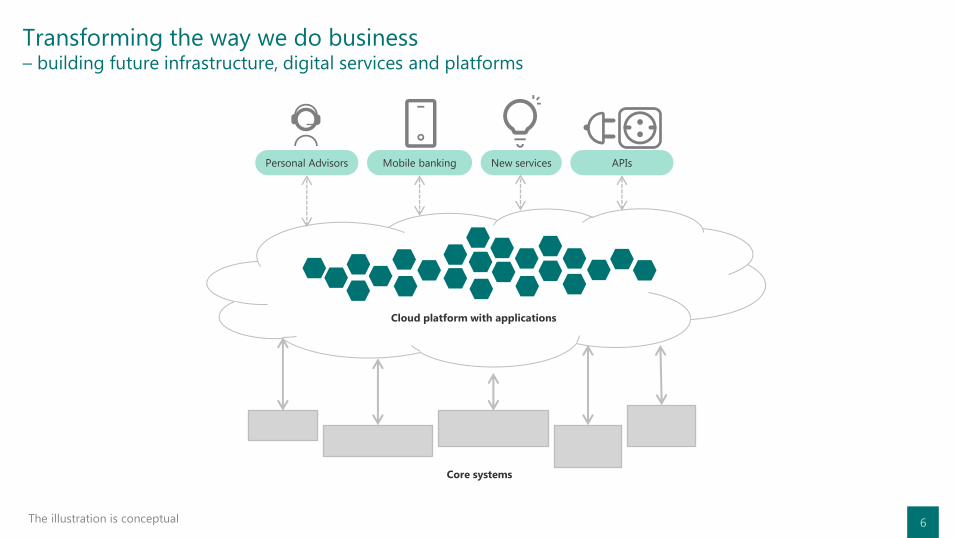

Transforming the way we do business – building future infrastructure, digital services and platforms

6 The illustration is conceptual

Core systems

Cloud platform with applications

Personal Advisors Mobile banking New services APIs

7

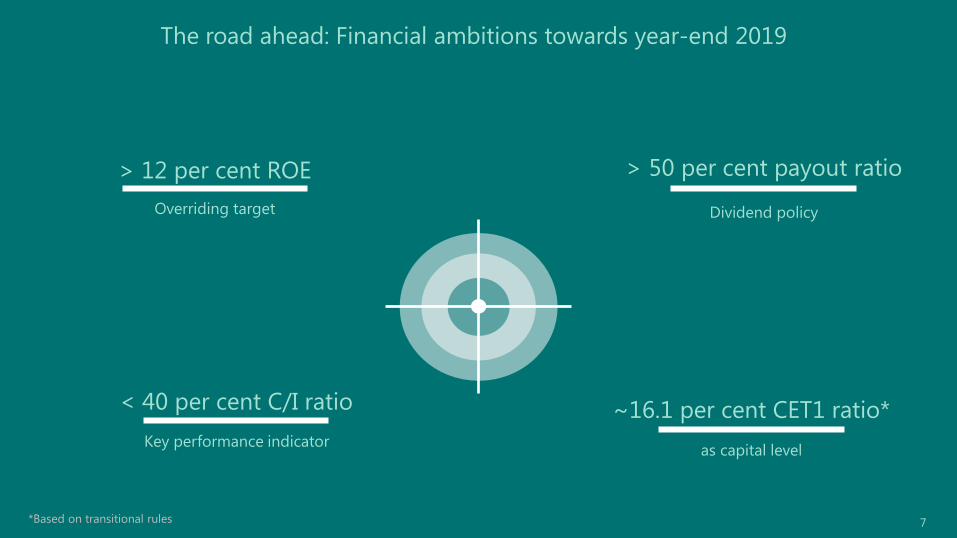

The road ahead: Financial ambitions towards year-end 2019

*Based on transitional rules

~16.1 per cent CET1 ratio*

as capital level

> 50 per cent payout ratio

Dividend policy

> 12 per cent ROE

Overriding target

< 40 per cent C/I ratio

Key performance indicator

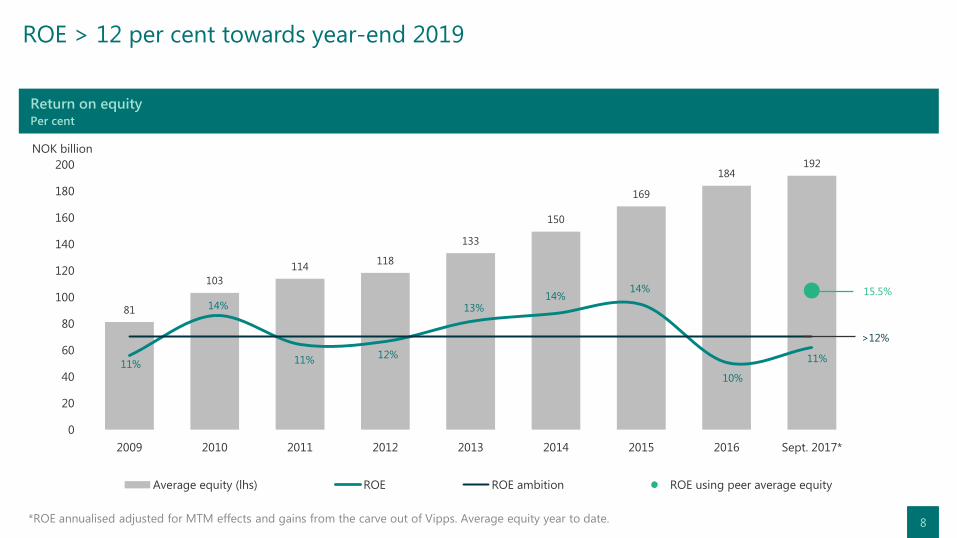

81

103

114 118

133

150

169

184 192

>12%

15.5%

0

20

40

60

80

100

120

140

160

180

200

2009 2010 2011 2012 2013 2014 2015 2016 Sept. 2017*

Average equity (lhs) ROE ROE ambition ROE using peer average equity

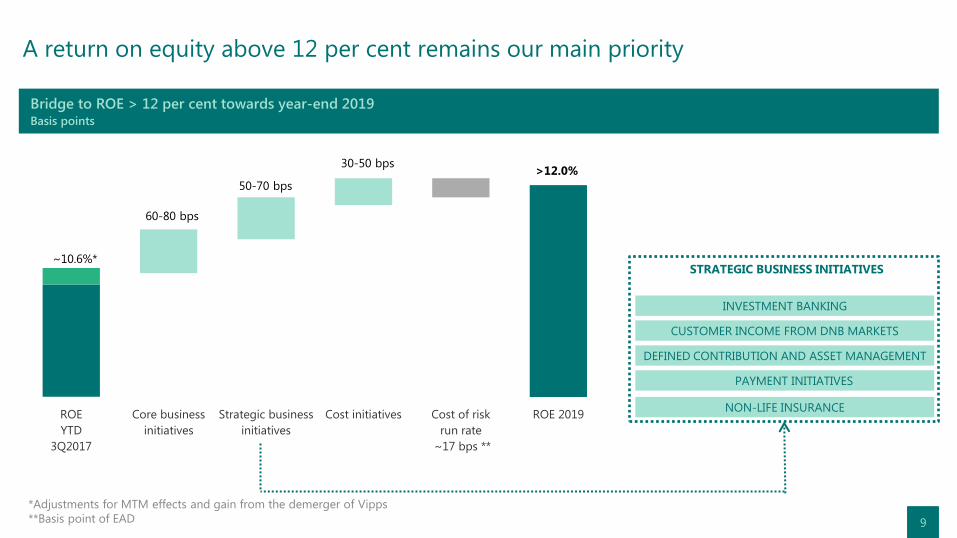

ROE > 12 per cent towards year-end 2019

*ROE annualised adjusted for MTM effects and gains from the carve out of Vipps. Average equity year to date. 8

Return on equity Per cent

11%

14% 14%

14%

11% 12%

13%

10%

11%

NOK billion

ROE

YTD

3Q2017

Core business

initiatives

Strategic business

initiatives

Cost initiatives Cost of risk

run rate

~17 bps **

ROE 2019

~10.6%*

>12.0%

60-80 bps

30-50 bps

50-70 bps

A return on equity above 12 per cent remains our main priority

*Adjustments for MTM effects and gain from the demerger of Vipps

**Basis point of EAD

INVESTMENT BANKING

CUSTOMER INCOME FROM DNB MARKETS

DEFINED CONTRIBUTION AND ASSET MANAGEMENT

PAYMENT INITIATIVES

STRATEGIC BUSINESS INITIATIVES

Bridge to ROE > 12 per cent towards year-end 2019 Basis points

NON-LIFE INSURANCE

9

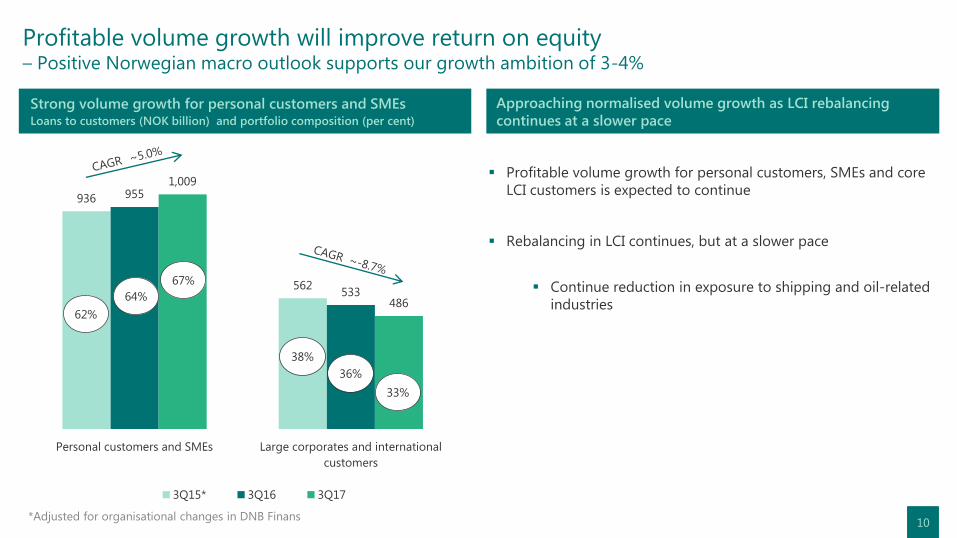

936

562

955

533

1,009

486

Personal customers and SMEs Large corporates and international

customers

3Q15* 3Q16 3Q17

Profitable volume growth will improve return on equity – Positive Norwegian macro outlook supports our growth ambition of 3-4%

*Adjusted for organisational changes in DNB Finans

Strong volume growth for personal customers and SMEs Loans to customers (NOK billion) and portfolio composition (per cent)

Approaching normalised volume growth as LCI rebalancing

continues at a slower pace

Profitable volume growth for personal customers, SMEs and core

LCI customers is expected to continue

Rebalancing in LCI continues, but at a slower pace

Continue reduction in exposure to shipping and oil-related

industries

62%

64%

67%

38%

36%

33%

10

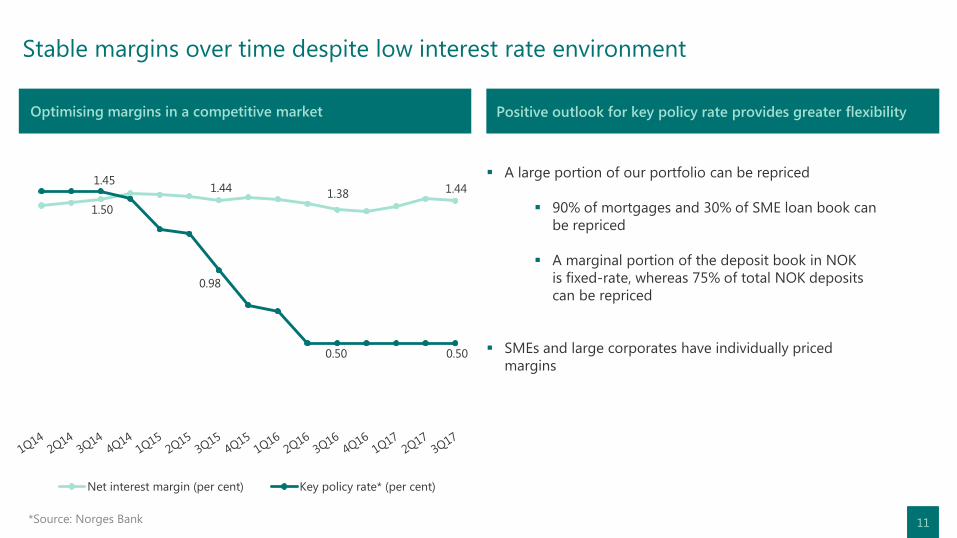

Stable margins over time despite low interest rate environment

Optimising margins in a competitive market Positive outlook for key policy rate provides greater flexibility

A large portion of our portfolio can be repriced

90% of mortgages and 30% of SME loan book can

be repriced

A marginal portion of the deposit book in NOK

is fixed-rate, whereas 75% of total NOK deposits

can be repriced

SMEs and large corporates have individually priced

margins

1.44 1.38 1.44

1.45

0.50 0.50

0.98

1.50

Net interest margin (per cent) Key policy rate* (per cent)

*Source: Norges Bank 11

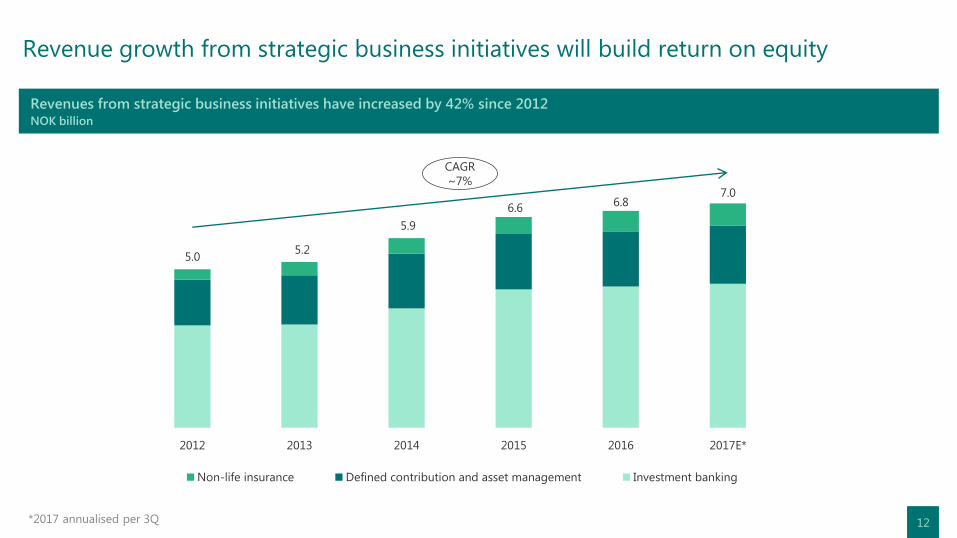

Revenue growth from strategic business initiatives will build return on equity

*2017 annualised per 3Q

Revenues from strategic business initiatives have increased by 42% since 2012 NOK billion

5.0 5.2

5.9

6.6 6.8

7.0

2012 2013 2014 2015 2016 2017E*

Non-life insurance Defined contribution and asset management Investment banking

CAGR

~7%

12

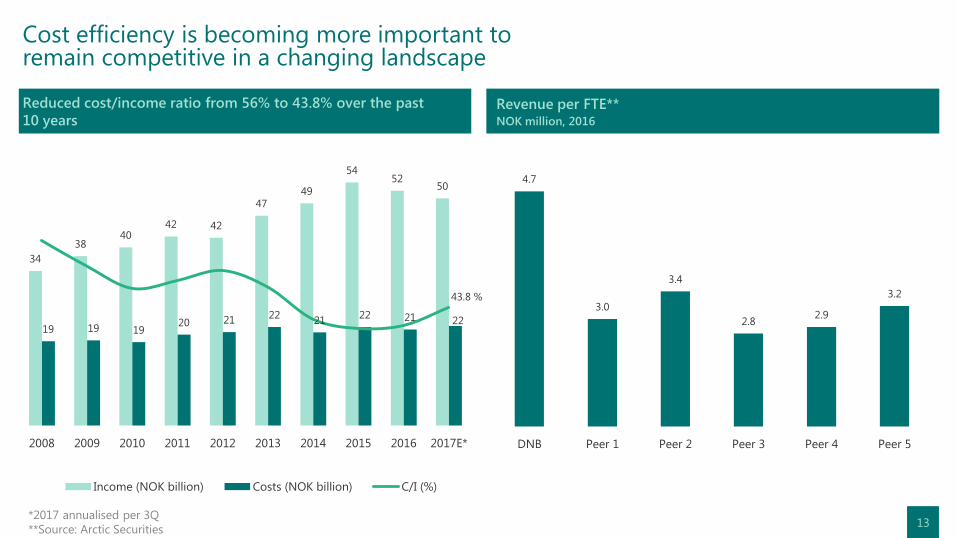

Cost efficiency is becoming more important to remain competitive in a changing landscape

*2017 annualised per 3Q

**Source: Arctic Securities

Reduced cost/income ratio from 56% to 43.8% over the past

10 years Revenue per FTE** NOK million, 2016

4.7

3.0

3.4

2.8 2.9

3.2

DNB Peer 1 Peer 2 Peer 3 Peer 4 Peer 5

34

38 40

42 42

47 49

54 52

50

19 19 19 20 21 22

21 22 21 22

43.8 %

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017E*

Income (NOK billion) Costs (NOK billion) C/I (%)

13

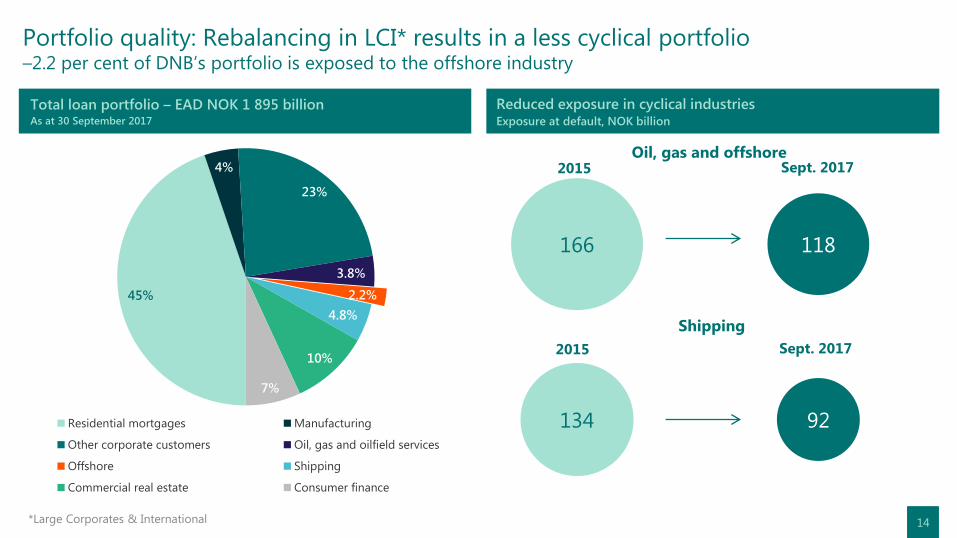

Portfolio quality: Rebalancing in LCI* results in a less cyclical portfolio –2.2 per cent of DNB’s portfolio is exposed to the offshore industry

*Large Corporates & International

Total loan portfolio – EAD NOK 1 895 billion As at 30 September 2017

Reduced exposure in cyclical industries Exposure at default, NOK billion

166

134

118

92

Oil, gas and offshore

Shipping

2015 Sept. 2017

2015 Sept. 2017

45%

4%

23%

3.8%

2.2%

4.8%

10%

7%

Residential mortgages Manufacturing

Other corporate customers Oil, gas and oilfield services

Offshore Shipping

Commercial real estate Consumer finance

14

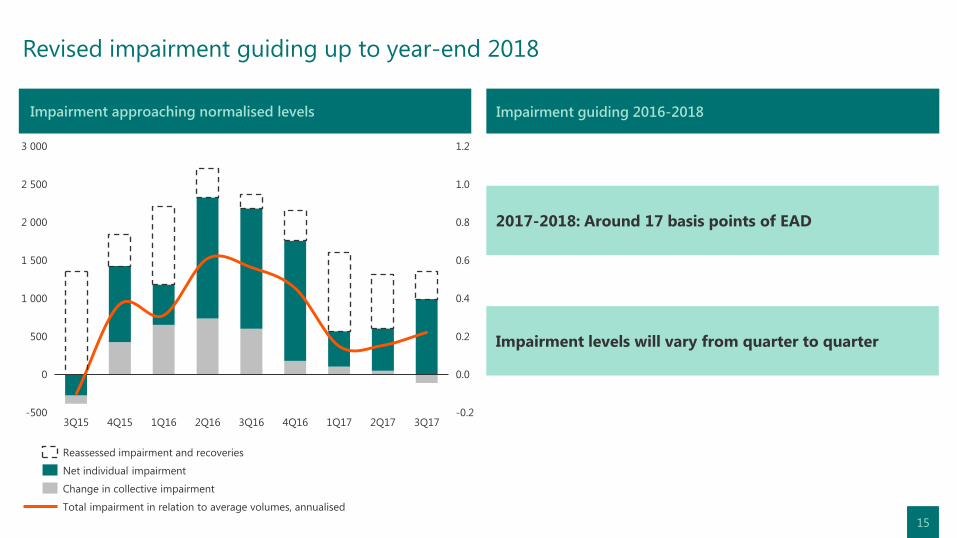

Revised impairment guiding up to year-end 2018

Impairment approaching normalised levels Impairment guiding 2016-2018

2 500

-500

1 500

1.0

0

1 000

2 000

0.6

1.2

500

0.8

3 000

-0.2

0.0

0.2

0.4

1Q17 1Q16 4Q16 3Q15 4Q15 2Q16 3Q16 3Q17 2Q17

Total impairment in relation to average volumes, annualised

Reassessed impairment and recoveries

Net individual impairment

Change in collective impairment

2017-2018: Around 17 basis points of EAD

Impairment levels will vary from quarter to quarter

15

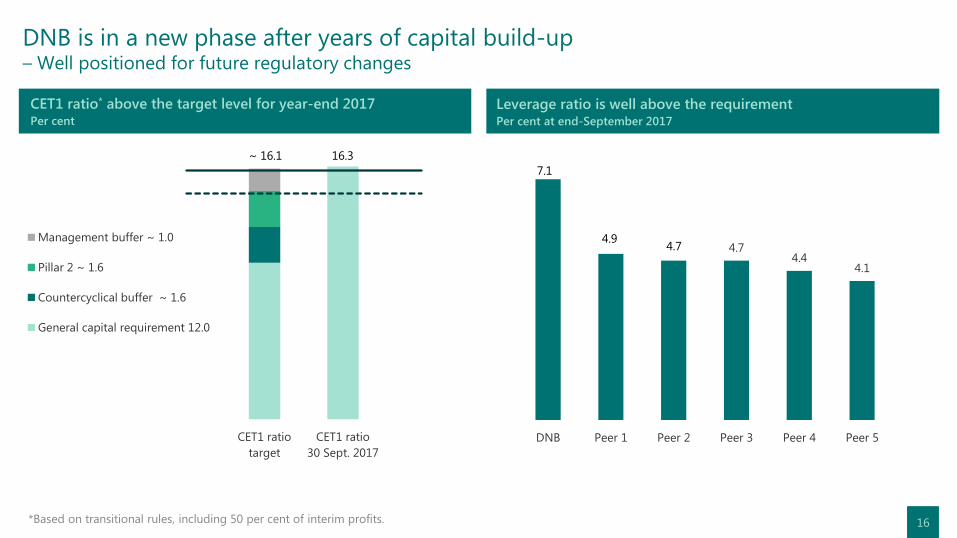

DNB is in a new phase after years of capital build-up – Well positioned for future regulatory changes

*Based on transitional rules, including 50 per cent of interim profits.

16

CET1 ratio* above the target level for year-end 2017 Per cent

Leverage ratio is well above the requirement Per cent at end-September 2017

CET1 ratio

target

CET1 ratio

30 Sept. 2017

Management buffer ~ 1.0

Pillar 2 ~ 1.6

Countercyclical buffer ~ 1.6

General capital requirement 12.0

16.3 ~ 16.1

4.7 4.4

4.1

DNB Peer 1 Peer 2 Peer 3 Peer 4 Peer 5

7.1

4.7 4.9

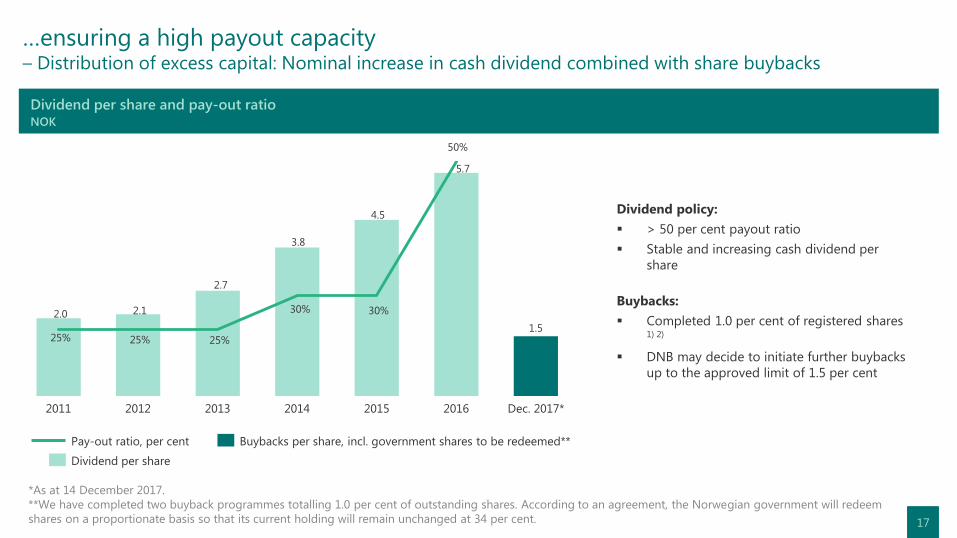

…ensuring a high payout capacity – Distribution of excess capital: Nominal increase in cash dividend combined with share buybacks

*As at 14 December 2017.

**We have completed two buyback programmes totalling 1.0 per cent of outstanding shares. According to an agreement, the Norwegian government will redeem

shares on a proportionate basis so that its current holding will remain unchanged at 34 per cent.

17

Dividend per share and pay-out ratio NOK

1.5

2011 Dec. 2017* 2014 2012 2013 2015 2016

Dividend per share

Pay-out ratio, per cent Buybacks per share, incl. government shares to be redeemed**

25% 25% 25%

30% 30%

50%

2.0 2.1

2.7

3.8

4.5

5.7

Dividend policy:

> 50 per cent payout ratio

Stable and increasing cash dividend per

share

Buybacks:

Completed 1.0 per cent of registered shares 1) 2)

DNB may decide to initiate further buybacks

up to the approved limit of 1.5 per cent

DISCLAIMER - CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

The statements contained in this presentation may include forward-looking statements such as statements of future

expectations. These statements are based on the management’s current views and assumptions and involve both known and

unknown risks and uncertainties.

Although DNB believes that the expectations reflected in any such forward-looking statements are reasonable, no assurance

can be given that such expectations will prove to have been correct.

Actual results, performance or events may differ materially from those set out or implied in the forward-looking statements.

Important factors that may cause such a difference include, but are not limited to: (i) general economic conditions, (ii)

performance of financial markets, including market volatility and liquidity (iii) the extent of credit defaults, (iv) interest rate

levels, (v) currency exchange rates, (vi) changes in the competitive climate, (vii) changes in laws and regulations, (viii)

changes in the policies of central banks and/ or foreign governments, or supra-national entities.

DNB assumes no obligation to update any forward-looking statement.

19