eur excess liquidity to decline - euro donwtrend -parisbas dec 2010

TRANSCRIPT

Market Economics | Interest Rate Strategy | Forex Strategy 16 December 2010

Market Mover We wish all our readers Happy Holidays and a Happy New Year.

The next edition of Market Mover will be published on 6 January 2011

IMPORTANT NOTICE. Please refer to important disclosures found at the end of this report. Some sections of this report have been written by our strategy teams (shown in blue). Such reports do not purport to be an exhaustive analysis and may be subject to conflicts of interest resulting from their interaction with sales and trading which could affect the objectivity of this report. www.GlobalMarkets.bnpparibas.com

Market Outlook 2-3Fundamentals 4-30

Global: Fire and Ice 4-5

US FOMC: Pricing Out Japan 6-7

US: A Curious Case of Consumer Deleveraging

8-10

ECB: Room at the Top 11-15

UK: HMS QE2 Sunk Before It Was Launched

16-17

SNB: Governing Two Economies 18

Sweden: Further Tightening 19-20

Norway: Hawkish Tone 21-22

Turkey: Reserving Judgement 23-25

Japan: Tankan Points to Soft Patch 26-28

Japan: Marking Up 2010 Growth Forecast

29-30

Interest Rate Strategy 31-59 Bonds: Forecast Update 31-32

USD Rates Outlook in Q1 33-36

US: Ideal Timing for LT Bullish Hedges

37

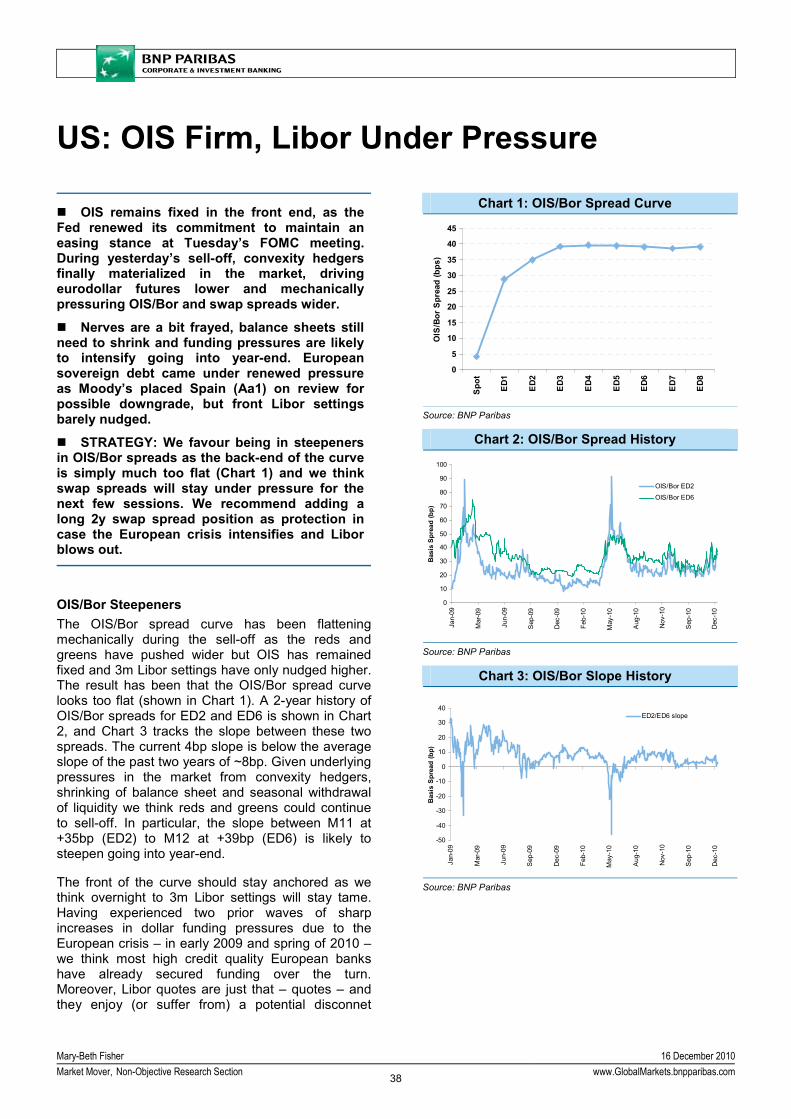

US: OIS Firm, Libor Under Pressure 38-39

MBS: 2011 Outlook – Status Quo 40-42

EUR: Flattening Trend Will Resume 43

EUR: Excess Liquidity to Decline Next Week

44

EUR: Euribor Red/Greens Opportunities

45

EUR: 2011 EGB Issuance Preview 46-47

Gilts: Strategic Trades for 2011 48

JGBs: Watch the Corporate Sector 49

Global Inflation Watch 50-53

Inflation: Post Mortem 2010 54-56

Technical Analysis 57-58

IR Strategy: Track Record for 2010 59FX Strategy 60-65

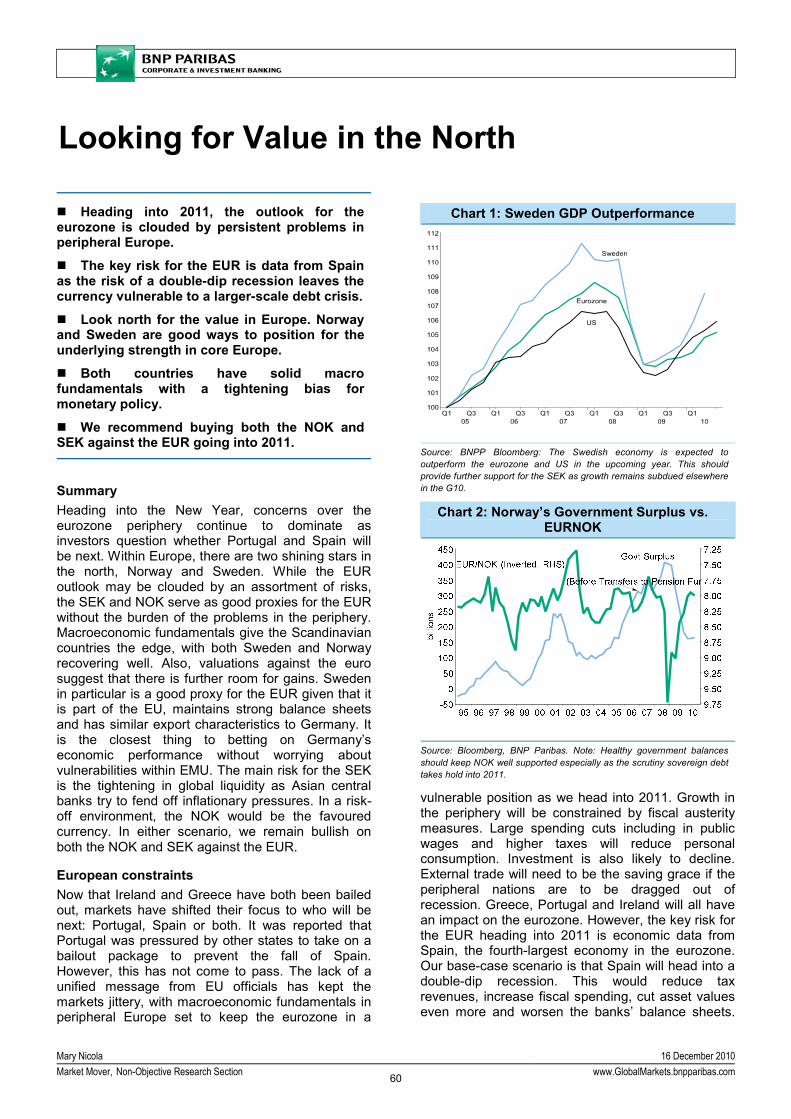

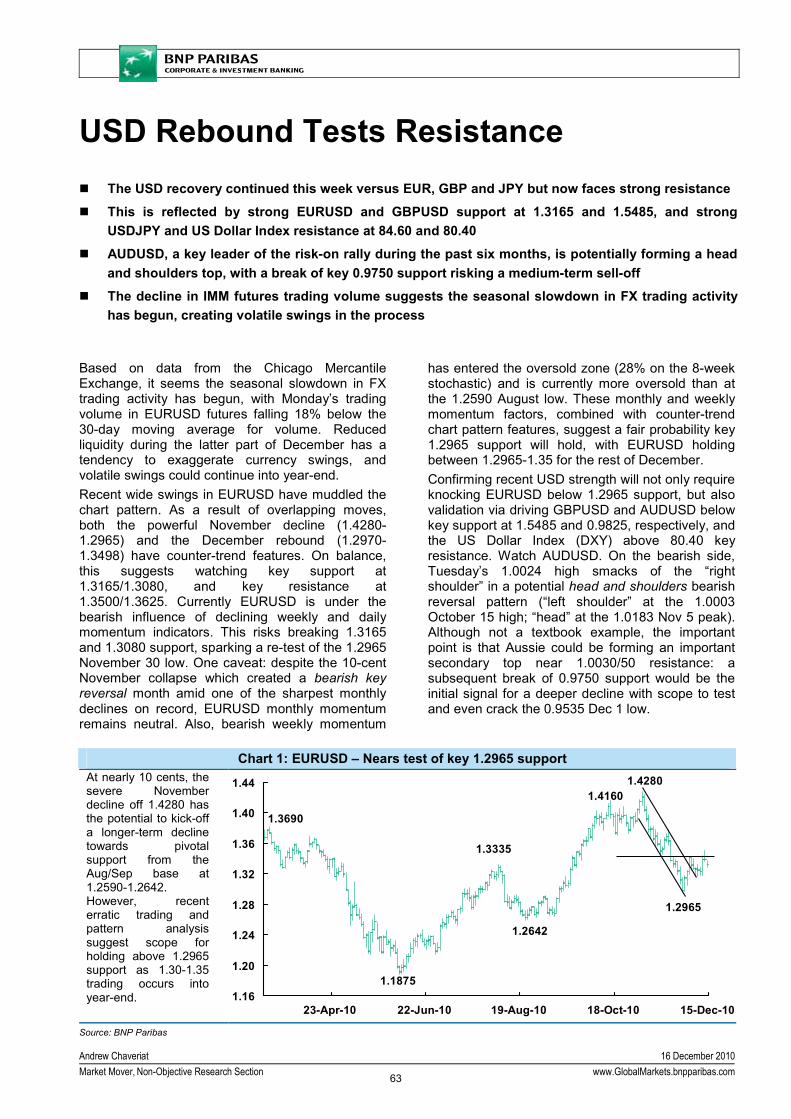

Looking for Value in the North 60-62

Technical Strategy: USD Rebound Tests Resistance

63-64

Trading Positions 65

Forecasts & Calendars 66-80 2 Week Economic Calendar 66-67

Key Data Preview 68-74

4 Week Calendar 75

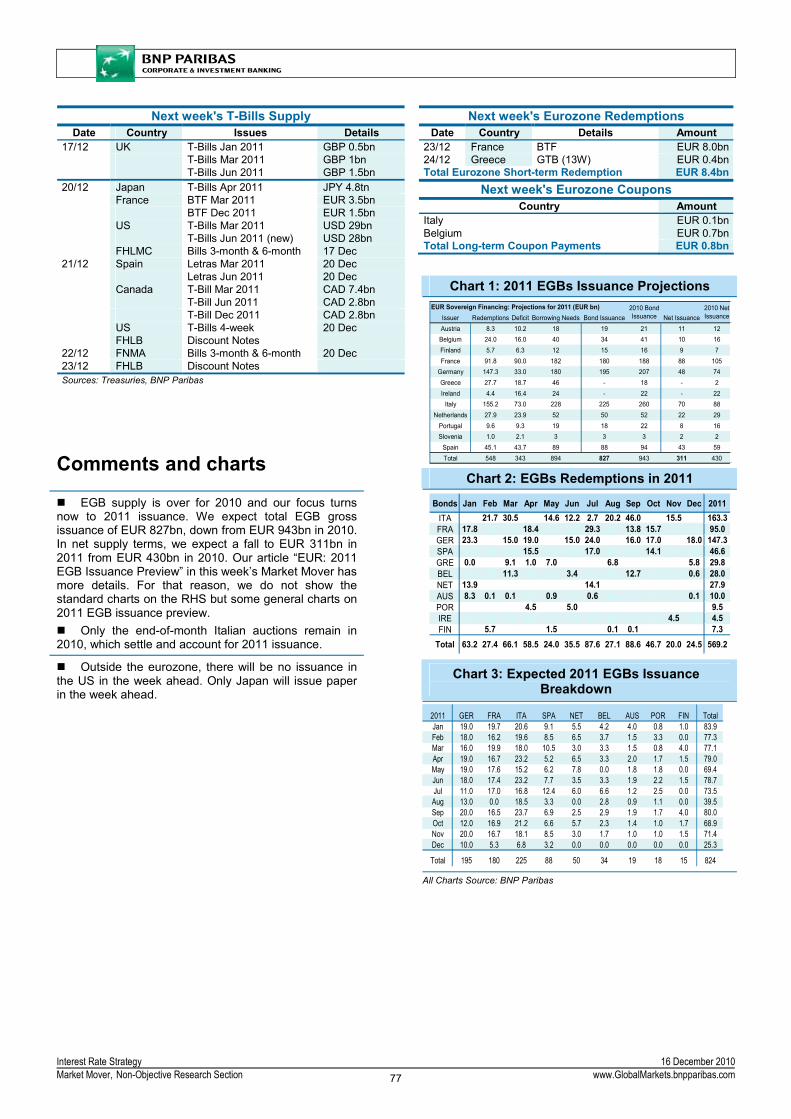

Treasury & SAS Issuance 76-77

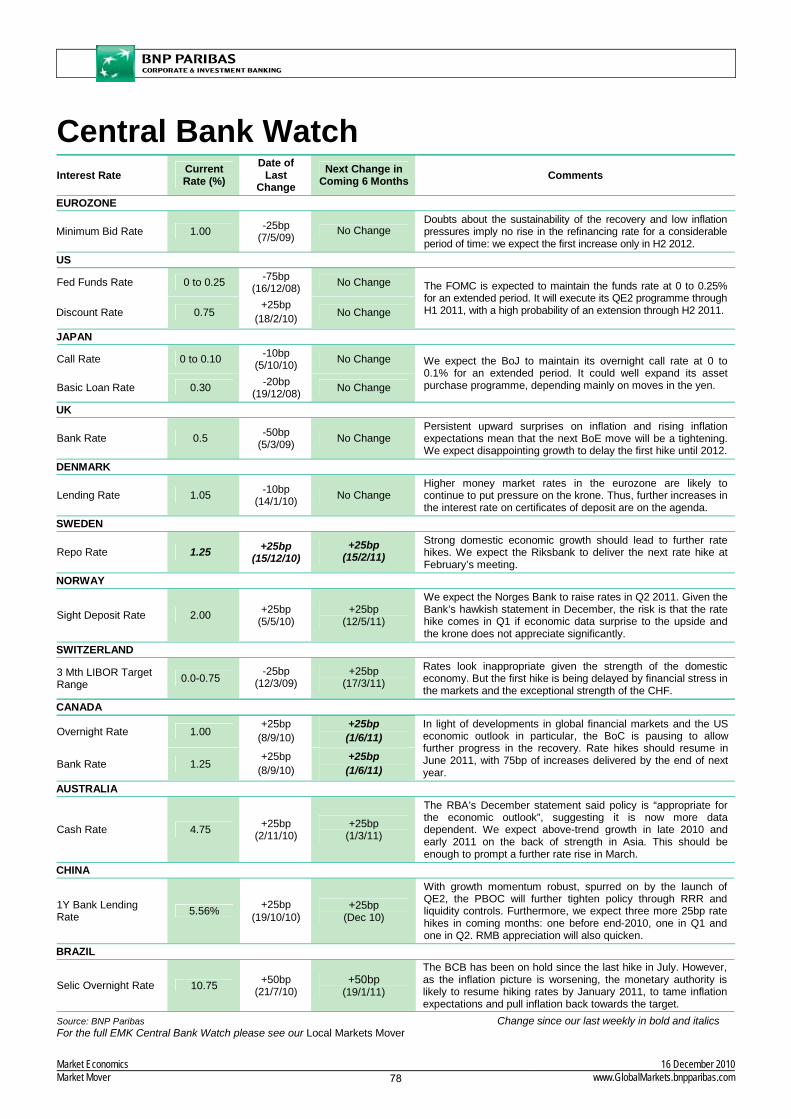

Central Bank Watch 78

Economic & Interest Rate Forecasts 79

FX Forecasts 80

Contacts 81

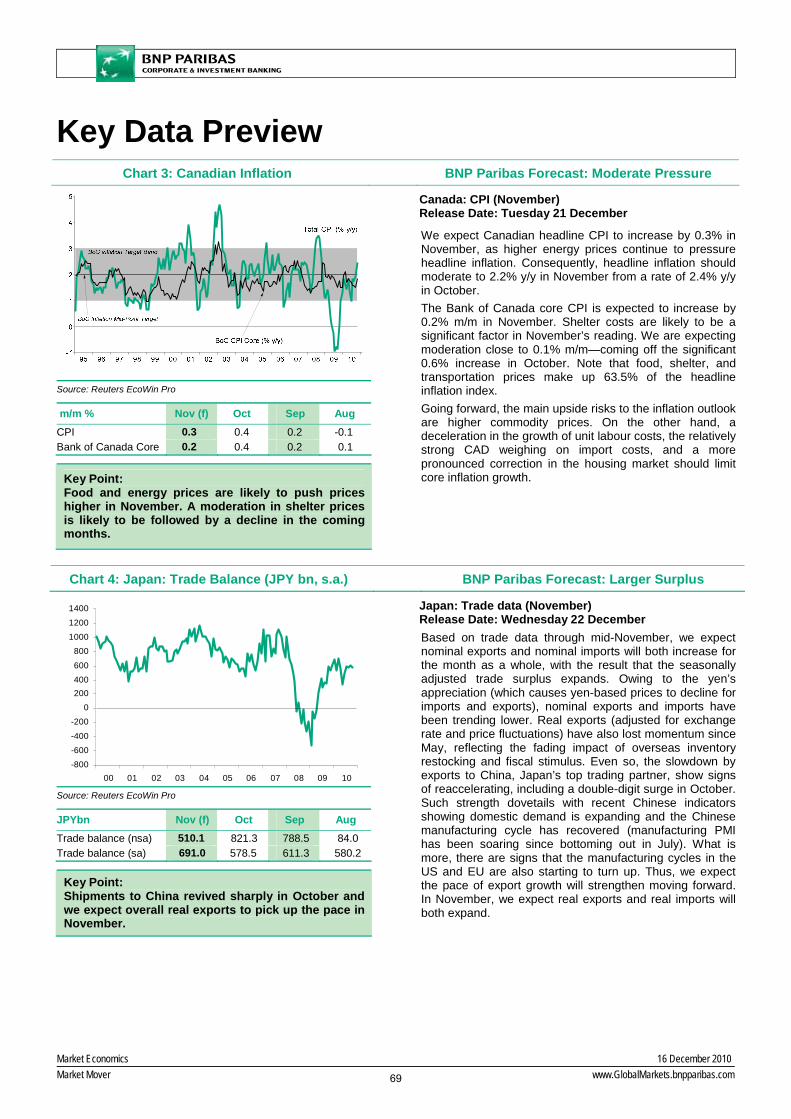

Bond markets are desperately seeking support. Any rebound continues to prove short-lived and the market action shows little sign of a lasting reversal before the turn of the year.

The market is oversold. Although better-than-expected economic data have been fuelling the sharp sell-off, poor year-end liquidity conditions have been a key factor exacerbating the move.

The lows in yields are behind us. We have updated our forecasts to take into account recent moves and the reduction in downside risks to growth as well as upward surprises in inflation in several developed economies.

As real money flows return, we expect yields to decline at the start of 2011, before resuming their rise later in the year.

Curves remain mostly directional as do US/EUR spreads which have widened in the recent sell-off.

JGBs continue to partly resist the sell-off in Treasuries. We expect the belly of the curve to underperform in the near term.

Sterling remains extremely vulnerable. We expect GBPUSD to target the 1.5300/1.5200 area.

USDJPY has not (yet) reacted to the sharp move of the US curve. A rally is likely if US data remain on the strong side.

We expect EURUSD to resume its downtrend going into 2011.

Market Views Current 1 Week 1 Month

UST 10y T-note Yield (%) 3.52 ↔ ↓ 2y/10y Spread (bp) 285 ↔ ↓ EGB 10y Bund Yield (%) 3.06 ↔ ↓ 2y/10y Spread (bp) 199 ↔ ↓ JGB 10y JGB Yield (%) 1.28 ↔ ↔ 2y/10y Spread (bp) 105 ↔ ↔ Forex EUR/USD 1.3218 ↓ ↓ USD/JPY 84.30 ↑ ↑

Cyril Beuzit 16 December 2010Market Mover www.GlobalMarkets.bnpparibas.com

Market Outlook

Analysing the bond market sell-off has not been an easy exercise and, going into the year-end, it remains unclear whether we have seen a fundamental shift or an overdone correction – the reality probably lying in between. As discussed in last week’s Market Mover, the recent sharp sell-off reflects a mix of bad positioning, central bank and political news (US fiscal deal), better economic data (except US payrolls) and year-end market conditions. The difficulty lies in attaching weights to these different factors but, so far, the QE2 sell-off looks similar to the QE1 sell-off seen in the spring of 2009. The recent market action and the risk that upcoming data will continue to surprise to the upside indicate that the lows in yields are behind us (see our updated forecasts in the “Forecasts & Calendars” section). However, although it may remain tough to fight the reflation trade going into 2011, the big picture still favours a low-yield environment. The economic picture does not look as bad as it did six months ago but the US output gap continues to be unusually wide, final demand growth has been lacklustre and the economic recovery faces substantial headwinds. In addition, underlying inflation is very weak and will remain so for some time – the trough on core inflation is still to come. Against this backdrop, policy rates will remain exceptionally low in 2011 with QE2 targeting a rise in inflation expectations.

Both Real and Nominal Yields Should Drop in Q1

-0 .5

0 .0

0 .5

1 .0

1 .5

2 .0

2 .5

3 .0

Ja n-0 3 Jan-05 Jan-07 Jan-09 Ja n-111 .5

2 .0

2 .5

3 .0

3 .5

4 .0

4 .5

5 .0

5 .5C ore , 6m th a headC o re C P I, L H S

core

U S 10y N o min a l

0.0

0 .5

1 .0

1 .5

2 .0

2 .5

3 .0

10y R e al Y ie ld

RY

Source: BNP Paribas

The different measures of inflation expectations indicate that there has not (yet) been a fundamental shift in expectations. The US 5y5y forward breakeven has been rising over the past couple of months while the EUR one has fallen but both remain in the ‘neutral’ zone. The flat(er) 10/30y spreads in both the US and Europe also support this view. Risk appetite remains solid and is still supported by ample global liquidity conditions. Some recent data suggest that investment funds have been switching their allocation from bonds to stocks. But, despite the collapse of the bond market, there has been no acceleration of the bullish momentum in equities. This highlights that, beyond some asset switches, the bond market sell-off has, so far, more to do with wrong positioning − the latest surveys suggest that the market may have to sell off more before reaching a turning point. This probably also indicates concerns about possible political decisions, rising inflation pressures in the emerging world as well as a decoupling between the main western equity indices and the domestic economy (household confidence) which is unlikely to last. Overall, judging from the very poor liquidity in the bond market, year-end pressures to cut balance sheets appear to be a significant factor exacerbating the recent move on Treasuries. The move so far has been primarily cash driven but, over the past couple of sessions, the attendant

Further capitulation by bond markets

Risk appetite remains solid

Looking for signs of a stabilisation on Treasuries

2

Cyril Beuzit 16 December 2010Market Mover www.GlobalMarkets.bnpparibas.com

swap spread widening indicates that convexity hedging flows have also played a role. Peak mortgage negative convexity is in the 3.25 to 3.50% range, which suggests that we may have seen most of the adjustment. From this point onward, convexity flows should become a more modest force. With mortgages finding support, the Treasury market should also become less volatile, which should mark the beginning of the end to this sell-off. Both the 2y and the 5y parts of the curve have cheapened on a forward basis to levels close to the top end of their ranges of the past two years. For instance, the 5y5y rate is around 5.28% within 20bp of the top since end-2008. Therefore, the belly of the curve will offer a buying opportunity… but probably not before the year-end. In Europe the focus will remain on peripheral markets in coming weeks with a big question mark about demand for early 2011 auctions (see “EUR: 2011 EGB Issuance Preview”). Spreads remain off their November highs but renewed tensions look likely with Moody’s putting Spain’s rating on review for a possible downgrade. It is unclear exactly how much progress will be made towards deciding on a permanent rescue framework at the EU Heads of State Summit given the extent of the divergence in views among the individual EU members. We remain neutral on EGBs going into 2011. Regarding the curve, directionality is less significant on rebounds, as the short end has some potential to rally at current levels of yields and the long end is still under pressure in line with the Treasury market. This leads us to see the near-term bias for the curve as neutral to slightly steeper − receiving the 2-10y will be one of our key strategic trades for 2011. The JGB market continues to follow the global bear trend in bond prices, with the 10y yield now just below the psychologically important 1.3% level. Correction pressures appear to have abated slightly, however, with many investors prepared to buy into weakness at current levels. The super-long sector has moved back into its historical range and the 10y sector has also experienced a significant sell-off. Much is now likely to depend on the extent to which yields rise for the short- to medium-term JGBs that constitute the core of banks' bond portfolios. The BoJ Monetary Policy Board will meet on Monday and Tuesday (20-21 December), but is not expected to announce any new measures. Monetary policy still looks likely to remain highly accommodative for quite some time to come and JGB market participants will therefore be focusing most of their attention on rising stock prices (fuelled by an improvement in economic sentiment) and the move in overseas rate markets. Sterling is now in an extremely vulnerable position as the negative mix of higher inflation and slower growth dynamics in the UK economy leave the BoE in a difficult position. Indeed, the sharp spike higher in the BoE’s Inflation Expectations Survey is a particular concern suggesting that sterling is now set to come under increasing pressure. We see GBPUSD as at significant risk as the US continues to produce positive data surprises which, together with the rise in yields, is providing the USD significant support. We expect GBPUSD to target the 1.5300/1.5200 area. However, it is interesting to note that USDJPY, which is traditionally the currency pair most closely correlated with the US yield curve, has remained in a range over the past couple of weeks despite the sharp rise in yields. This seems to be the result of Japanese investors’ continued hedging of their bond portfolios. However, if US data remain strong, this could be enough to encourage investors to unwind their hedges, triggering a sharp move higher in USDJPY. The EUR is also expected to remain weak as the latest data provide further evidence of increasing economic divergence within the eurozone. We expect EURUSD to extend the major down trend into the end of the year and through the first half of 2011 with the USD set to embark on a broad-based rebound.

Early 2011 buying opportunities

Renewed stress on EMU peripherals

JGBs are still outperforming in the sell-off

GBP is at risk

EURUSD to resume its downward trend

USDJPY to push higher

3

Marcelo Carvalho 16 December 2010Market Mover www.GlobalMarkets.bnpparibas.com

Global: Fire and Ice Some say the world will end in fire, some

say in ice.

The pendulum is swinging between these two extremes.

Market attention may shift from fears that things are getting too cold in developed economies…

…to worries that things are getting too hot in emerging markets.

The problem is that policy stimulus in developed economies is fuelling overheating in emerging markets, which are resisting FX appreciation.

To quote from a poem by Robert Frost, “Some say the world will end in fire, Some say in ice.” Earlier in the year, observers feared that things might get too cold in developed economies. But as double-dip fears fade, attention may shift to concerns that emerging markets are getting too hot. Ultra-loose policies in developed economies are fuelling capital flows into emerging markets. But as EM policymakers are resisting FX appreciation, inflation pressures will intensify if central banks fall behind the curve and let their economies overheat. In all, are we moving from concerns of recession ice in developed economies to worries of inflation fire in emerging markets?

Hot and cold The cold front from the North seems mostly behind us now. Earlier in the year, many feared a double dip in growth performance, particularly in the US. However, in part on the heels of further policy accommodation in developed economies, global growth seems to be finding a better footing. Double-dip fears have faded, notwithstanding concerns about sovereign risk in some eurozone economies.

But the Fed's monetary easing is affecting markets well beyond the US. Along with a weaker USD and rising commodity prices, capital flows to emerging markets (EM) have intensified. The resulting currency appreciation across emerging markets has prompted policymakers to introduce measures to cool these inflows, and to tighten monetary policy by less than domestic demand considerations in EM alone would dictate. In many cases, EM policymakers are increasingly resorting to measures other than outright rate hikes (such as higher reserve

requirements and credit restrictions), perhaps fearing the currency implications of rate increases. Specific experiences vary from country to country, but the broader theme seems the same across emerging markets, from Turkey to China, including Brazil.

How will it play out? Our take: global liquidity remains abundant, with policies accommodative in the developed world. Capital flows to emerging markets remain strong. Pressures for FX appreciation in EM persist. But EM policymakers are resisting these FX pressures, and many EM central banks are falling behind the curve. Policies remain too loose for too long. Inflation pressures are building across EM. The question is how policymakers will ultimately respond.

In all, market attention may well swing from fears that things could get too cold in developed economies to worries that things are getting too hot in emerging markets. No one wants a repeat of the great depression of the 1930s. But the inflationary 1970s were not that great either.

Hell is other people At the heart of this ice-and-fire global policy dilemma are the tensions between what is seen as best for developed economies at the current stage of the global business cycle and what is seen as best for emerging markets – especially when countries fail to fully consider the global implications of their individual choices. In that context, each country thinks it is pursuing its own best interests, oblivious to international spillovers. Hell is others.

The US judges it is doing what is best for the US economy (QE). If others (such as China) don't let their currencies appreciate against the USD, that is their problem. For the US, the problem is lack of FX flexibility in EM. My currency, your problem. Hell is emerging markets.

By contrast, EM policymakers judge they should not just allow ultra-loose monetary conditions in developed economies to fuel bubbles in their markets. Emerging market countries do not want FX to appreciate beyond what they judge is consistent with fundamentals. They cannot – and will not – allow their policies to be dictated by Washington DC. Hell is the US.

As often in economic debates, there is some truth on both sides. The US is right: it is harder and more painful to engineer global rebalancing if EM policymakers resist FX adjustment. But EMs are also

4

Marcelo Carvalho 16 December 2010Market Mover www.GlobalMarkets.bnpparibas.com

right: it is hard to rely on the USD as a reliable reserve currency for the international monetary system when the cornerstone country is pursuing domestic policies which are not optimal for others.

Real FX adjustments tend to prevail in the long run – if not via nominal appreciation, then via higher inflation. The problem with the inflation route is that it is much more painful – and probably more destabilising.

In a nutshell, can EM policymakers deliver stability without a credible and steady US policy anchor as the centre of the international monetary system? What happens if things fall apart and the centre cannot hold?

Conclusion Market attention may well start to swing from one extreme to the other – from concerns of recession ice in developed economies to worries of inflation fire in emerging markets. At the heart of the matter: policy stimulus in the developed world is fuelling overheating in emerging markets while EM policymakers are resisting currency appreciation. All claim that hell is other people.

5

Julia Coronado 16 December 2010Market Mover www.GlobalMarkets.bnpparibas.com

US FOMC: Pricing Out Japan

Bold moves by US policymakers have led investors to price out the Japan scenario, suggesting that higher rates are here to stay.

The FOMC confirmed its resolve by interpreting incoming data conservatively and signalling its commitment to QE2 in the December FOMC statement.

That said, we think the FOMC is correct in being cautious about incoming data. With the strong patch in spending yet to show reliable follow-through to job creation, forecasts of significantly above-trend growth and fears of inflation being built into longer-term rates are probably overdone.

Interest rates continued their steady march higher after the December FOMC meeting as markets continued to price out any possibility the US could get stuck in a Japanese-style scenario. US policymakers have shown a remarkable commitment to stimulate the US economy; incoming data suggests some they are getting some traction. The FOMC made only minor changes to its policy statement and stayed the course on QE2. The 10-year Treasury is up more than 100 basis points since the announcement of QE2 (see Chart 1). However, that only puts it back at the levels seen in April, when the recovery looked to be on a moderate but reasonably steady track. Meanwhile, equities are up more than 3% since the November FOMC meeting and nearly 11% for the year. The rise is helping to offset house price declines and keep the recovery in household net worth on track. November retail sales represented yet another data point suggesting we will get a solid gain in GDP in Q4. We have revised up our forecast to 2.6% q/q saar.

The data flow on balance has been encouraging. But we have yet to see good follow-through to job growth, something the FOMC emphasised in its statement. Consumers have maintained a saving rate just under 6% throughout the recovery. Thus the recent data will prove to be a fleeting firm patch unless we see hiring pick up. We think consumer spending and jobs are likely to meet in the middle, with consumer spending growth continuing to post moderate gains (rather than accelerating) and the jobs picture improving gradually. While some of the volatility in rates markets owes to technical factors,

the message from US policymakers has been clear. They will prevent a Japanese scenario at all costs and the market is reacting accordingly. This enthusiasm from investors is not without its risks. Higher rates threaten the recovery in an already-fragile housing market and higher headline inflation will erode some of the stimulus. Nonetheless, we seem to have left the Japanese scenario behind for now.

There were very few changes to the December FOMC statement. The Fed chose a conservative interpretation of recent data following the recent back-up in the unemployment rate. In November, the FOMC said that information received since the last meeting confirmed that the "pace of the recovery in output and employment continues to be slow". In the latest statement, it indicated that information received since the last meeting confirms that the "recovery is continuing, though at a rate that has been insufficient to bring down unemployment”.

Chart 1: Rates Rising Rapidly

Source: Reuters EcoWin Pro

Chart 2: Retail Sales Firm, Need Follow-Through to Jobs

Source: Reuters EcoWin Pro

6

Julia Coronado 16 December 2010Market Mover www.GlobalMarkets.bnpparibas.com

Other changes were also modest. While the Fed previously noted that housing starts continue to be depressed, this time it said the housing sector continues to be depressed. This broader reference includes the decline in prices we have seen of late. Having previously said that measures of underlying inflation have trended lower in recent quarters, this time it said that these measures “have continued to trend downward”. This perhaps suggests a slightly more entrenched dynamic. There were few to no changes in the policy paragraphs and the parameters of the QE2 programme are virtually unchanged. As expected, the Fed remains cautious and sought to send a signal of steady policy.

Retail sales posted a solid gain in November, rising 0.8% after an upward-revised 1.7% increase in October. As shown in Chart 2, gains in consumer spending have not come at the expense of a lower saving rate. Therefore any acceleration in consumer spending growth will likely be dependent on continued improvement in the labour market. We expect that to be forthcoming but gradual. The US

economy lacks the cyclical turbo boosters of manufacturing, construction and finance that fuelled job growth early in prior recoveries; another engine of job creation has yet to come forward.

One encouraging sign on the jobs front came from the NFIB survey of small businesses for November. This reported that a net 4% of small companies are planning to hire. This may sound small, and it is. However, it is up from the record low of -10% reached in March 2009 and has been rising steadily in recent months. Small businesses have been another sector weighing on the recovery. Thus a move into positive territory confirms that the economy is making headway in its healing process and downside risks are diminishing.

The pricing out of Japan likely means that higher rates are here to stay. However, we think the forecasts of significantly above-trend growth and fears of inflation being built into longer-term Treasury rates are probably overdone.

7

Yelena Shulyatyeva 16 December 2010Market Mover www.GlobalMarkets.bnpparibas.com

US: A Curious Case of Consumer Deleveraging

The Q3 Flow of Funds Accounts indicate a

pick-up in household net worth. This was driven by capital gains on equity, partially offset by losses in real estate wealth on the back of house price declines. Also boosting net worth were continued declines in both consumer credit and net mortgage borrowing.

The recent pick-up in retail spending has been supported by gradual improvement in the labour market. However, consumer deleveraging still represents a speed limit.

Three main factors appear to have contributed to ongoing declines in revolving credit: households continue to default on their obligations; they are paying off a larger share of their balances each month; and they are financing less of their new spending with credit.

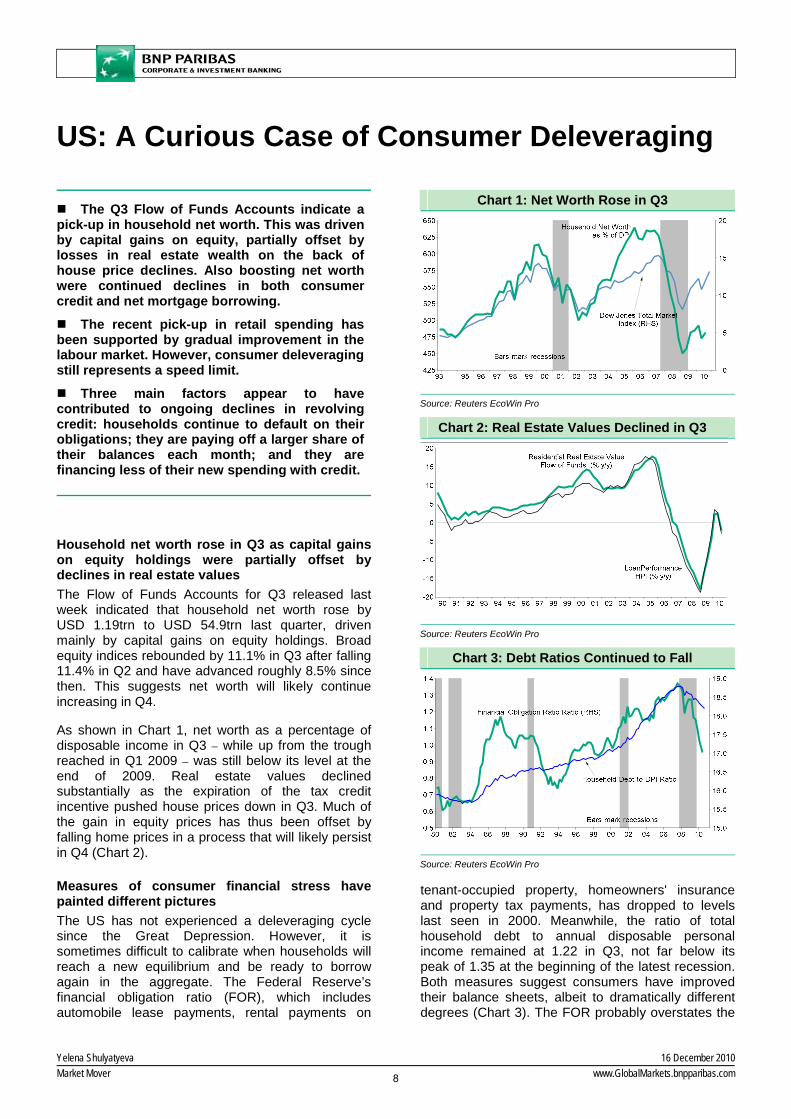

Household net worth rose in Q3 as capital gains on equity holdings were partially offset by declines in real estate values The Flow of Funds Accounts for Q3 released last week indicated that household net worth rose by USD 1.19trn to USD 54.9trn last quarter, driven mainly by capital gains on equity holdings. Broad equity indices rebounded by 11.1% in Q3 after falling 11.4% in Q2 and have advanced roughly 8.5% since then. This suggests net worth will likely continue increasing in Q4.

As shown in Chart 1, net worth as a percentage of disposable income in Q3 – while up from the trough reached in Q1 2009 – was still below its level at the end of 2009. Real estate values declined substantially as the expiration of the tax credit incentive pushed house prices down in Q3. Much of the gain in equity prices has thus been offset by falling home prices in a process that will likely persist in Q4 (Chart 2).

Measures of consumer financial stress have painted different pictures The US has not experienced a deleveraging cycle since the Great Depression. However, it is sometimes difficult to calibrate when households will reach a new equilibrium and be ready to borrow again in the aggregate. The Federal Reserve’s financial obligation ratio (FOR), which includes automobile lease payments, rental payments on

tenant-occupied property, homeowners' insurance and property tax payments, has dropped to levels last seen in 2000. Meanwhile, the ratio of total household debt to annual disposable personal income remained at 1.22 in Q3, not far below its peak of 1.35 at the beginning of the latest recession. Both measures suggest consumers have improved their balance sheets, albeit to dramatically different degrees (Chart 3). The FOR probably overstates the

Chart 1: Net Worth Rose in Q3

Source: Reuters EcoWin Pro

Chart 2: Real Estate Values Declined in Q3

Source: Reuters EcoWin Pro

Chart 3: Debt Ratios Continued to Fall

Source: Reuters EcoWin Pro

8

Yelena Shulyatyeva 16 December 2010Market Mover www.GlobalMarkets.bnpparibas.com

progress consumers have made as it assumes consumers can refinance all their debt at current low rates. We know this is not the case, owing to tight credit and underwater mortgages. But as some people have been able to take advantage of low rates to reduce their debt burdens, the true picture probably lies somewhere between the two measures.

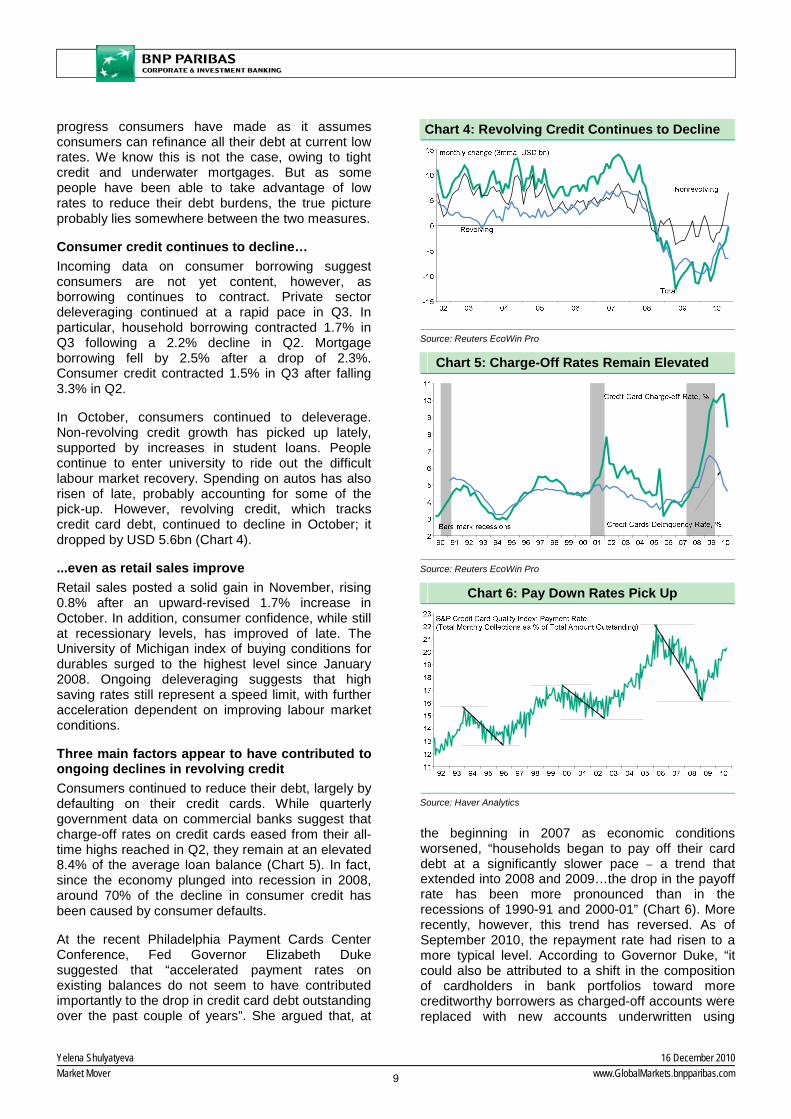

Consumer credit continues to decline… Incoming data on consumer borrowing suggest consumers are not yet content, however, as borrowing continues to contract. Private sector deleveraging continued at a rapid pace in Q3. In particular, household borrowing contracted 1.7% in Q3 following a 2.2% decline in Q2. Mortgage borrowing fell by 2.5% after a drop of 2.3%. Consumer credit contracted 1.5% in Q3 after falling 3.3% in Q2.

In October, consumers continued to deleverage. Non-revolving credit growth has picked up lately, supported by increases in student loans. People continue to enter university to ride out the difficult labour market recovery. Spending on autos has also risen of late, probably accounting for some of the pick-up. However, revolving credit, which tracks credit card debt, continued to decline in October; it dropped by USD 5.6bn (Chart 4).

...even as retail sales improve Retail sales posted a solid gain in November, rising 0.8% after an upward-revised 1.7% increase in October. In addition, consumer confidence, while still at recessionary levels, has improved of late. The University of Michigan index of buying conditions for durables surged to the highest level since January 2008. Ongoing deleveraging suggests that high saving rates still represent a speed limit, with further acceleration dependent on improving labour market conditions.

Three main factors appear to have contributed to ongoing declines in revolving credit Consumers continued to reduce their debt, largely by defaulting on their credit cards. While quarterly government data on commercial banks suggest that charge-off rates on credit cards eased from their all-time highs reached in Q2, they remain at an elevated 8.4% of the average loan balance (Chart 5). In fact, since the economy plunged into recession in 2008, around 70% of the decline in consumer credit has been caused by consumer defaults.

At the recent Philadelphia Payment Cards Center Conference, Fed Governor Elizabeth Duke suggested that “accelerated payment rates on existing balances do not seem to have contributed importantly to the drop in credit card debt outstanding over the past couple of years”. She argued that, at

the beginning in 2007 as economic conditions worsened, “households began to pay off their card debt at a significantly slower pace – a trend that extended into 2008 and 2009…the drop in the payoff rate has been more pronounced than in the recessions of 1990-91 and 2000-01” (Chart 6). More recently, however, this trend has reversed. As of September 2010, the repayment rate had risen to a more typical level. According to Governor Duke, “it could also be attributed to a shift in the composition of cardholders in bank portfolios toward more creditworthy borrowers as charged-off accounts were replaced with new accounts underwritten using

Chart 4: Revolving Credit Continues to Decline

Source: Reuters EcoWin Pro

Chart 5: Charge-Off Rates Remain Elevated

Source: Reuters EcoWin Pro

Chart 6: Pay Down Rates Pick Up

Source: Haver Analytics

9

Yelena Shulyatyeva 16 December 2010Market Mover www.GlobalMarkets.bnpparibas.com

stricter criteria”. Regardless of the cause, consumer credit is currently being paid down at an aggressive rate, particularly when one considers that the uptrend in pay downs between 2003 and 2007 owed in large part to the substitution of home equity debt for credit card borrowing. Both home equity and credit card balances are declining.

Indeed, there has been a recent surge in “cash-in” refinancing whereby homeowners have been reducing their principal balances through a refinancing transaction. This could be the result of tighter lending standards and declining home values, with lenders requiring homeowners to reduce their loan balances to access lower mortgage rates. However, it stands in stark contrast to the peak of the housing bubble in 2006 when “cash-outs” (refinances resulting in loan amounts that were at least 5% greater than the amortised unpaid principal balance of the original loan) accounted for almost 90% of all refinancing transactions. As the housing bubble burst and home values dropped, the cash-out ratio dropped to 18.5% as of Q3 2010 – the lowest level since Freddie Mac records began in 1985. In contrast, the proportion of cash-ins surged to 33% in Q3 (Chart 7).

Some of the deleveraging can be attributed to a reduction in new borrowing. According to the Federal Reserve Board’s quarterly Senior Loan Officer Opinion Survey, despite a modest easing in lending standards, demand for consumer loans remains weak (Chart 8). According to the quarterly report on household debt and credit from the New York Fed, the number of inquiries for new consumer credit is significantly down from its pre-recession levels (Chart 9 – I).

Supply factors have also likely contributed to the decline in overall credit card outstanding balances. Households may be charging less because they had less credit available. Indeed, the same survey shows a significant decline in credit card limits since the peak in mid-2008 (Chart 9 – II).

The relationship between consumers and credit is undergoing a fundamental change. While a solid holiday shopping season should help keep the recovery on track, there are no indications that credit will soon become the accelerator it once was.

Chart 7: Cash-In Refinances Surged This Year

Source: Reuters EcoWin Pro

Chart 8: Demand for Credit Remains Sluggish

Source: Haver Analytics

Chart 9: Supply Factors Also Limit Credit Increases

Source: Reuters EcoWin Pro

10

Dominique Barbet/Ken Wattret 16 December 2010Market Mover www.GlobalMarkets.bnpparibas.com

ECB: Room at the Top The ECB will have a new president from the

beginning of November 2011.

As the process of choosing a new president is lengthy, speculation over who it will be could continue for some time yet.

A German president remains the most likely outcome, with Axel Weber the front runner. But alternative candidates are also in the frame.

Uncertainty over the change of leadership, plus increased divergence within the eurozone, implies a more uncertain policy outlook.

The structure The Governing Council of the ECB is made up of six Executive Board members and the heads of each of the national central banks (NCBs) in the eurozone. The number of NCBs currently stands at 16 but will expand to 17 from the start of 2011 when Estonia joins the eurozone.

The six members of the Executive Board of the ECB serve a non-renewable eight-year term. They can be removed only in the case of incapacity or serious misconduct. The names of the current members are in Table 1, along with the expiry dates for their terms.

Jean-Claude Trichet’s eight-year term as president of the ECB will expire on 31 October 2011. Choosing his replacement may be a lengthy process (Table 2). Who will get the job, when we will find out and what this means for future policy are obviously a source of considerable interest for markets.

The nomination process According to the ECB statutes, the members of the Executive Board should be persons of "recognised standing and professional experience in monetary and banking matters" (Article 283 of the EU Treaty, effective since the ratification of the Lisbon Treaty). The Executive Board members are chosen by the European Council, voting on a qualified majority basis, on the recommendation of the Council and after the European Parliament and the Governing Council of the ECB have expressed their opinions.

The timetable for choosing Mr Trichet to be president of the ECB back in 2003 offers a template for how the procedure will evolve this time. Mr Trichet’s term began in November 2003. The European Council officially chose him in mid-July that year. By the end

of July, the ECB had adopted a positive opinion on his nomination. The European Parliament approved the choice on 23 September, less than two weeks after the EU Commission for Economic and Monetary Affairs had heard the candidate.

Table 1: Executive Board Members

Name Nationality Term Ends J-C Trichet France President 31/10/2011 V Constancio Portugal V/President 31/05/2018 G Tumpel-Gugerell Austria Member 31/05/2011 J-M Gonzales-Paramo Spain Member 31/05/2012 L Bini-Smaghi Italy Member 31/05/2013 J Stark Germany Member 31/05/2014 Source: ECB

Table 2: Timetable for Naming the New ECB President

Steps Likely timing

Heads of State discussions May-June 2011

European Council official approval of Candidate June-July 2011

ECB expresses opinion July 2011

Monetary & Economic Affairs Commission of EU Parliament hears the candidate September 2011

EU Parliament expresses opinion September 2011

European Council formal nomination September 2011

New ECB President takes up duties 1 November 2011

Source: BNP Paribas

Table 3: Governing Council Membership

Country NCB Head Total Number of

GC Members % of

Members% of

Capital KeyGermany A Weber 2 9.1 27.1 France C Noyer 2 9.1 20.4

Italy M Draghi 2 9.1 17.9 Spain MF Ordoñez 2 9.1 11.9

Netherlands N Wellink 1 4.5 5.7 Belgium G Quaden 1 4.5 3.5 Greece G Provopoulos 1 4.5 2.8 Austria E Nowotny 2 9.1 2.8

Portugal C Costa 2 9.1 2.5 Finland E Liikanen 1 4.5 1.8 Ireland P Honohan 1 4.5 1.6

Slovakia J Makuch 1 4.5 1.0 Slovenia M Kranjek 1 4.5 0.5

Luxembourg Y Mersch 1 4.5 0.3 Cyprus A Orphanides 1 4.5 0.2 Malta M Bonello 1 4.5 0.1

Source: ECB, BNP Paribas

11

Dominique Barbet/Ken Wattret 16 December 2010Market Mover www.GlobalMarkets.bnpparibas.com

On the basis of the 2003 timetable, it is most likely that the new president of the ECB will be chosen at the Heads of State and Government meeting in May or June next year. It is likely that the nomination will seep through to the public domain before this as the European Council will want to ensure the candidate has sufficient support beforehand. Negative opinions from the ECB or the European Parliament would not necessarily block the appointment but would be very damaging to the authority of the proposed president and to the credibility of the ECB.

An earlier indication of who will be the new president is also possible. This is because the term of current Executive Board member Mrs Tumpel-Gugerell will come to an end in May next year, so a successor will have to be nominated soon. This could be discussed as soon as the EU Summit on 16-17 December.

The nationality of the proposed successor to Mrs Tumpel-Gugerell may be an indication of the likely nationality of the new president. Media reports have suggested that Germany and France will discuss the choice of the new Executive Board member and the new president in tandem. The suggestion is that a deal could be struck in favour of the ECB president being German as long as a France national fills the vacancy on the Executive Board, replacing Mrs Tumpel-Gugerell but with a high-profile portfolio (such as the responsibility for economic analysis).

The role of ECB president The ECB president has just one vote like the other members but has considerably more influence given his or her position in setting the agenda and chairing the Governing Council meetings. The ECB president is obliged to present and explain the policy decisions of the Governing Council in the press conference that follows the policy-setting meetings (which usually occur on the first Thursday of each month). This is a key part of the job and an important issue for who is chosen – discussed below.

The president also has to deliver a testimony, and answer questions, in the European Parliament twice a year. He or she will usually attend the meetings of finance ministers of the eurozone, an opportunity to make recommendations to finance ministers about other aspects of economic policy. One of the features of Mr Trichet’s ECB presidency has been less public disagreement between the two camps.

Who is in the frame? In theory, any person from the eurozone who meets the relevant criteria can be president. But in practice, choosing a President is a complicated process given the horse-trading between member states over the key roles and responsibilities within the eurozone.

What we know is that both previous presidents were experienced heads of national central banks at the time of their nomination. Having run a central bank is an obvious advantage. But it is not a necessity.

Nationality is probably the more important issue. The presidency of the ECB has not been held by the largest economy, Germany, which is one reason why the initial focus of speculation over who will be the new president centred on the Bundesbank’s current president, Axel Weber.

At the time of writing, we see four main scenarios for the choice of the new president of the ECB which we discuss in turn below. The probabilities which we have attached to each outcome are very fluid given the political nature of the decision.

Box 1: ECB Governing Council - Voting Rights The principle for voting at the Governing Council is one member, one vote. However, with the increasing number of new eurozone members, the ECB has secured specific voting rules insuring that no more than 21 people take part in the voting (the voting system is described in the Article 10 of Protocol 4 annexed to the EU Treaty).

Since January 2009, the number of eurozone member states has exceeded 15 and the new set of rules can apply. However, the Governing Council can decide to stick to the simple one member one vote system as long as the number of member countries remains below 18.

The system works as follows:

Every Executive Board member always has a voting right.

The Governors of the NCBs in the main five countries have at least four permanent voting rights. The main five countries are defined according to two criteria: the size of GDP (with a weighting of 5/6); and the size of the national financial system (for the remaining 1/6 weighting). The so-called first group is currently composed of Governors from Germany, France, Italy, Spain and the Netherlands.

The second group is composed of the Governors from the other central banks and they share the remaining 10 or 11 vote rights on a rotating basis. The frequency of rotation of the first group cannot be lower than that of the second group. As a result the first group currently has 5 voting rights and the second group only 10. From January next year, 10 of the 12 members of the second group will have a voting right. Only when an 18th country joins EMU will the first group lose the fifth voting right it currently holds.

Different rules, with three groups of Governors, will apply from the day the monetary union reaches 22 member countries. These rules are also defined in Article 10. They are intended to prevent the voting rights of the largest countries being overly diluted as the monetary union expands its membership.

Source: EU Treaty, effective since the ratification of the Lisbon Treaty

12

Dominique Barbet/Ken Wattret 16 December 2010Market Mover www.GlobalMarkets.bnpparibas.com

Scenario 1: Axel Weber (40%)

The initial front runner for the position and a very credible candidate in many respects, Mr Weber has the requisite experience of having running a central bank, is a highly respected economist and is, of course, German. The suggestion is that, should Mr Weber secure the presidency, the current Executive Board member Jürgen Stark would then return to the Bundesbank to become its new president.

There have never been two people from the same country on the ECB Executive Board simultaneously, though there is no formal obstacle to this happening. Indeed, as Table 3 highlights, the larger countries are under-represented in relation to their contributions to the ECB’s capital.

At one stage, a Weber presidency was perceived by some to be a ‘done deal’, with Chancellor Merkel a strong supporter of his candidacy. It has looked less of a certainty recently, however, related in part to Mr Weber’s tendency to express a different view to that of the Governing Council as a whole. His dissent has been most vocal in relation to the Securities Markets Programme (or SMP).

His reputation as a ‘hawk’ is also a concern for the countries in most economic and financial distress given the potential implications for future monetary policy. The reservations over Mr Weber have led to speculation of an alternative outcome…

Scenario 2: Another German (20%)

Germany feels that, as the largest economy in the eurozone, it is its turn to hold the ECB presidency. If Mr Weber is too controversial a candidate, then an option would be for another German to take the role. A potential alternative is the current ECB Executive Board member Jürgen Stark. Though he has never been the head of a central bank, he has extensive experience in senior roles at the Bundesbank and the ECB.

His candidacy, however, is complicated by a couple of issues. First, his reputation as a policy hawk. If this is an obstacle to Mr Weber securing the position, then the same reservations may apply to Mr Stark. However, as he has not showed the same degree of public dissent as Mr Weber, he is probably viewed as more of a team player. A second problem is his role on the Executive Board. His eight-year term does not expire until mid-2014. While responsibilities within the Executive Board can be switched around, starting a new term as the president is a different issue.

Our understanding, having spoken to the ECB, is that it would not be possible to nominate an existing Executive Board member for another position on the

Board until his or her current term had expired. A former Executive Board member could, however, be nominated to be president.

Other high-profile German nationals have also been floated as possible candidates, including the current CEO of the EFSF, Klaus Regling. He has extensive experience in the financial sector, including at the German Finance Ministry and the IMF. But he has not run a central bank, or even had a senior position at a central bank, which is an issue. Another is the practical constraint of his current role at the EFSF.

The implication of the probabilities attached to the first two scenarios is that we believe it is more likely than not that a German will be the next president of the ECB. But it is not a done deal. Another member state of the eurozone may yet take the top job. This leads us to the third scenario…

Scenario 3: A Compromise Candidate (20%)

Contrary to perceptions before the formation of the ECB that its first president would be a German, the job went to the Netherlands. The head of the Dutch central bank, Wim Duisenberg, got the job, though only for half a term (i.e. four years). Germany took the role of Chief Economist for the highly influential Otmar Issing.

Mr Duisenberg was a compromise option. He was a highly experienced central banker, from a core member state and sufficiently hawkish to placate Germany.

Such a compromise option is also possible this time. Indeed, there is a long tradition in Europe of a ‘small country’ compromise candidate emerging late in the day when there has been insufficient support for the ‘big country’ front runner. It happened only recently with the choice of Herman Van Rompuy as president of the EU Council.

As the outgoing president is French, another French national is highly unlikely to secure the role. To some extent this also applies to the Netherlands, given the nationality of the first ECB president. Would it really be fair that a country representing just 6% of total eurozone output accounted for two of the first three ECB presidents? This would seem to rule out the current head of the Netherlands central bank, Nout Wellink, who would otherwise be seen as a credible candidate for the compromise option.

That the newly appointed vice president of the ECB, the former head of the Central Bank of Portugal, Mr Constancio, is from southern Europe is an additional complication. This makes it more likely that the new president will be from a northern European country, a

13

Dominique Barbet/Ken Wattret 16 December 2010Market Mover www.GlobalMarkets.bnpparibas.com

key reason why Germany apparently pushed hard for Mr Constancio to get the job of vice president.

With so many member states seemingly out of the running, this has led to speculation that the current head of Finland’s central bank, Mr Liikanen, could become the next president of the ECB. He has the requisite experience of running a central bank and is from a ‘neutral’ part of the eurozone. He also worked for the European Commission from 1995 to 2004, so has plenty of EU experience.

But is he the right fit given the specific requirements of the role? Mr Duisenberg often struggled in dealing with the media. The position of ECB president needs someone who can deal effectively and comfortably with a bombardment of questions on a variety of issues very shortly after the conclusion of what are likely to be, given increasing divergence within the eurozone, difficult discussions on the Governing Council. Does he have the experience required to steer the Governing Council in these difficult times?

The same question marks also apply to other ‘small country’ names which have periodically cropped up in speculation, largely centred on Benelux countries. One could argue, however, that these countries are already over-represented in senior EU positions.

The best compromise option would be for Mr Trichet to stay in the role. The advantages of continuity in these highly uncertain times are obvious. How about extending his term for another four years, say, given the exceptional circumstances? There are, however, procedural obstacles. The terms of Executive Board members are non-renewable which would appear to rule this option out.

The nationality of the current ECB vice president is one of the obstacles in the way of the last of our four scenarios…

Scenario 4: Mario Draghi (20%)

In a number of respects, Mr Draghi is a very credible candidate for the ECB presidency. He ticks many of the most important boxes. He has been a highly effective head of the Banca D’Italia, is the president of the Financial Stability Board, earned a doctorate in economics from MIT, worked at the World Bank for many years and unlike most of the candidates, has extensive private sector experience also.

In contrast to some on the ECB Governing Council, he has kept a remarkably low profile in his near five-year spell running the Banca D’Italia. A key issue in the way of his candidacy is the national politics associated with choosing the leadership of the ECB. Having two Southern Europeans at the helm is not acceptable for some.

Tough call Given the issues highlighted above, predicting who will get the job is not straightforward. Weighing up all the information available, our bottom line assumption is that the most probable outcome is that the next president of the ECB will come from Germany. We are aware that Mr Weber’s candidacy has been damaged by his outspokenness. But given the lack of practical alternatives, we still believe that a Weber presidency is the single most likely outcome.

It is unlikely in our view that the next president of the ECB will come from southern Europe. This is not a refection of Mr Draghi’s candidacy. As stated above, his credentials are impressive. Rather, it reflects the politics of the eurozone.

Policy implications An obvious worry is that if a German with a hawkish reputation takes the presidency, this will lead to a tighter than otherwise monetary policy stance – much too tight potentially for the periphery. This is more of a concern now than in the past. In the early days of EMU, the German economy struggled. Now, it looks structurally strong. The unemployment rate is at its lowest in almost two decades and skill shortages in fast growing sectors risk generating upward pressure on labour costs and inflation.

While the ECB sets monetary policy for the eurozone as a whole it is reasonable to assume that members of the Governing Council will be influenced by what is happening in their own countries or those near by. There is some historical experience of this in respect of German influence on ECB policy.

That the German economy was going strong in early 2008 – GDP surged by over 5% annualised in Q1 – and wage pressures were building, were contributory factors behind the ECB’s decision to raise rates in July 2008 in the eye of the financial storm. Germany had pushed hard – rightly, in our opinion at the time – for a faster pace of tightening in 2006 and 2007 and this frustration was instrumental in the decision to hike in summer 2008.

Germany was also highly influential on policy in the early 2000s but in the other direction. Taylor Rule analysis suggests that rates were low in relation to eurozone needs in the early years of EMU (Chart 1), when the German economy was performing poorly. This contributed to the formation of asset price bubbles in other countries which have now burst with such devastating consequences.

More divided ECB policy is not determined by the president alone. But inasmuch as the president shapes the agenda for Governing Council meetings and is influential in

14

Dominique Barbet/Ken Wattret 16 December 2010Market Mover www.GlobalMarkets.bnpparibas.com

determining how the decisions will be made – on the basis of consensus-building like Mr Trichet, on the basis of simple voting or guided more strongly by the Executive Board – the choice of the new president is highly significant. The president’s style is also going to be important when it comes to how the ECB will interact with other policymakers, like governments, during a crisis.

A less consensus-driven approach could result in a more responsive ECB, with faster decision-making. But it could also lead to more dissent if members of the Governing Council feel frustrated that they are not being heard. Looking ahead, with the eurozone looking increasingly divergent growth-wise, greater dissent and a higher degree of difficulty in forging a consensus are to be expected. This implies a need for strong leadership - but preferably a leadership style which can persuade the Governing Council to stick together rather than creating dissent.

Shifting to second A likely consequence of a German presidency would be an increased emphasis on the second pillar of the ECB’s monetary policy strategy – monetary analysis. If ECB policy were to become less sensitive to short run determinants of inflation (e.g. the balance of supply and demand) and more sensitive to medium-term trends as signalled by the money and credit analysis, this would also lean towards higher ECB policy rates earlier.

Broad money and credit growth rates are not normal at present but they are in the process of normalising. If this continues, growth rates will look increasingly out of kilter with the emergency level of policy rates currently in place (Chart 2).

There is also likely to be a greater tendency at a German-run ECB to 'lean against the wind' when it comes to potential asset price bubbles. This was a prominent theme of Mr Stark’s contributions to the ECB’s conference last month on the causes and consequences of the global financial crisis. In this context, the speeches of Mr Weber suggesting that the costs of too late an exit from monetary policy accommodation would be greater than the costs of too early an exit are also significant.

Another salient issue given recent developments is how sensitive, or otherwise, a German-led ECB would be to problems in the peripheral economies. From a purely arithmetical perspective, the solidity of the core member states is far more important than the problems in the periphery. The combined output share of Greece, Ireland and Portugal is around 6%, less than a quarter of that for Germany alone. An increased emphasis on the solidity of the core was, until recently, the direction in which the speeches of

those most keen on ‘normalisation’, including from Mr Weber and Mr Stark, were leaning.

Forecast implications Our forecast remains for the refinancing rate to stay at 1% until spring 2012, consistent with low domestic price pressures and subdued growth in the eurozone as a whole. Market developments will also be key to maintaining policy accommodation, as was evident in the recent decision to maintain full allotment for all refinancing operations through Q1 2011.

Looking to the longer-term, under Scenarios 1 and 2 the bias would be towards tighter policy and a flatter yield curve. Under Scenario 4, this is also possible. With the ECB led by southern Europeans there could be a desire to reinforce the anti-inflation credibility of the ECB by raising interest rates earlier and more quickly than otherwise.

The bottom line is that we are entering an uncertain era for ECB policy. The vice president is new to the job and all members of the Executive Board will see their terms expire within two and a half years of the next president taking up the role. Add the increased internal divergence to the mix and forecasting ECB policy is unlikely to be straightforward.

Chart 1: ECB Policy & Taylor Rule

-2.0

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

98 99 00 01 02 03 04 05 06 07 08 09 10

ECB Refi

Eurozone

-2.0

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

98 99 00 01 02 03 04 05 06 07 08 09 10

ECB Refi

Eurozone

Sources: Reuters EcoWin Pro & BNP Paribas

Chart 2: ECB Policy & Lending Growth

97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12-1

0

1

2

3

4

5

6

7

8

9

10

11

12

13

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

5.5

Bank Lending (% y/y, 18M th Lag RHS)

ECB Refi Rate (% )

Sources: Reuters EcoWin Pro

15

Alan Clarke and Paul Mortimer-Lee 16 December 2010Market Mover www.GlobalMarkets.bnpparibas.com

UK: HMS QE2 Sunk Before It Was Launched

We have changed our Bank of England

monetary policy forecast.

Given higher than expected inflation and the threat this poses to inflation expectations, we no longer expect the Bank to engage in a second round of quantitative easing.

Given our view that GDP will grow much more slowly during 2011 than the BoE’s central projection, we still believe that the first interest rate hike is a long way off (2012).

Nonetheless, if inflation expectations rise abruptly and upside risks to wage inflation emerge, there is a risk that the BoE will hike Bank Rate during 2011.

Enough is enough We have revised our BoE monetary policy forecast. We had expected downward surprises on GDP growth during 2011 to provoke a downward revision to the Bank’s medium-term inflation outlook, opening the door to a second phase of quantitative easing. However, Tuesday’s upward surprise on inflation was the final nail in the coffin.

CPI inflation accelerated by 0.1pp to 3.3% y/y, contrary to earlier indications that we might have seen a slight deceleration. It was a bad number which is only likely to get worse in the coming months. Rising utility bills and petrol prices will add to inflation in December, before the VAT hike to 20% pushes inflation even higher in January. We had expected CPI inflation to peak at 3.6% y/y in February. However, following this week’s surprise, the peak is likely to be 3.8% y/y with a significant risk of 4% y/y.

There have been persistent upward surprises on current inflation over the last two years. While it is typically the medium-term outlook for inflation that matters most for BoE policy, near-term inflation is posing an ever-bigger threat to inflation expectations and wages – with implications for inflation further ahead. The fact remains that around 1pp of current inflation is related to increases in indirect taxes including VAT. The latter will eventually drop out of the y/y calculation. Nonetheless, when this happens (in 2012), the likely undershoot relative to target is looking more and more marginal as time passes.

End-of-year appraisal Given the time of year, it is worthwhile assessing what the BoE has done well and what it has done badly. To its credit, QE1 worked. The economy has recovered more swiftly than expected and unemployment is lower than feared. Contrary to concerns that the economy might flirt with the risk of deflation, the UK seems about the furthest from deflation of the industrialised economies.

However, what the BoE hasn’t done particularly well is forecast inflation. Chart 1 shows where inflation has actually been compared with the BoE’s projection 2 years earlier. The shaded bars show that it is incredibly rare for inflation to be lower than the Bank projects. In fact, on average inflation has been around 0.75pp points higher than the Bank’s projection. Given this, there should be a tendency for the Bank to aim a little higher at the medium-term horizon.

US lessons The key reason the BoE hasn't begun QE2 already is worries about inflation expectations. If inflation stays above 2% for a long time, people will doubt it is truly aiming at 2%. If we go to 4%, they definitely won't believe it.

Also, the Bank will have learned from the Fed's experience that QE can have a perverse effect on bond yields through inflation expectations, with breakevens having risen considerably since Bernanke made his Jackson Hole speech (by around 50bp). Rising inflation expectations are the last thing the BoE needs.

Chart 1: BoE CPI Inflation Forecasting Error 2-Years Ahead

Source: Reuters EcoWin Pro, BoE

16

Alan Clarke and Paul Mortimer-Lee 16 December 2010Market Mover www.GlobalMarkets.bnpparibas.com

Nominal GDP has been increasing at close to a 6% y/y pace over the last year, and it is questionable whether the Bank would want to boost this further. The labour market in recent months has seen very good job growth, and there is anecdotal evidence of pay freezes being less widespread than before. Wage growth will probably pick up.

Faster-than-expected inflation seems to reflect to an important degree a bigger pass-through of the exchange rate shock from sterling's depreciation. Why has this happened? It could be that inflationary expectations have held up better than normal, possibly as a result of BoE policy. It may be that the output gap is a lot smaller than the fall in output might suggest. Neither argues for more QE.

Conclusion Despite our view that GDP growth will disappoint expectations during 2011, the obstruction to further QE now looks too big. Hence we no longer expect QE2 to be launched. We continue to believe that disappointing growth will prevent the first interest rate hike from being delivered any time soon (not until 2012). In particular, the Bank has aimed high with regard to near-term inflation. Nonetheless, if inflation expectations do rise appreciably and there are signs that this is pushing wage inflation higher, there is clearly a risk that the MPC begins to tighten policy during 2011.

17

Eoin O’Callaghan 16 December 2010Market Mover www.GlobalMarkets.bnpparibas.com

SNB: Governing Two Economies

As widely expected, the SNB left the policy target unchanged in December.

The central bank remains extremely sensitive to the strength of the franc and the stress in the euro area periphery.

The SNB continues to expect a marked slowdown in the coming quarters and has revised its inflation forecast down further.

We think growth will surprise to the upside but a hike as soon as March looks very challenging.

The timing of the first hike remains dependent on the exchange rate.

As widely expected, the SNB left the policy target and band unchanged in December. The strength of the franc continues to delay policy normalisation. The dilemma for the SNB is setting a single policy variable for two sectors of the economy that are experiencing very different monetary conditions. For the domestic economy, policy looks too loose. But monetary conditions are tight for exporters. The two sectors’ performance will diverge accordingly – domestic demand will contribute more to growth than in the past, net trade less. If any of the franc’s current strength reflects rate hike expectations, the SNB clearly doesn’t want to validate them. Despite the strength of the economic data since the last meeting, the SNB continues to expect a marked slowdown in growth in 2011. The monetary authority expects growth to slow to 1.5% in 2011 from 2.5% this year. We see risk to the upside of that 2011 forecast (we have 2%). Sectors focused on the domestic market are in a strong position to respond to the SNB’s zero interest rate policy – employment growth is rising and neither the private nor public sector is characterised by the imbalances evident in many parts of Europe. In addition, while net trade should contribute less to growth on the combination of a strong franc and robust domestic demand growth, Swiss exports will benefit vibrant emerging-market demand. The SNB also revised down the medium-term outlook for inflation further. 2012 inflation is now expected at 1% rather than 1.2%. We are less sanguine about medium-term inflation. With a smaller output gap than elsewhere in Europe (we put it at c.0.5%), closing more quickly, the drag from spare capacity is fading quite rapidly. The prospect of stronger inflation in the future is evident in the SNB’s

preferred gauge of core inflation – dynamic factor inflation – which rose from 0.1% y/y in October 2009 to 1.0% last month. Shorter-term measures of momentum in the GDP deflator are also picking up. With the franc delivering monetary tightening independent of SNB policy, the outlook for policy is dependent on the outlook for the exchange rate. Were the franc to depreciate significantly, then given the strength of domestic fundamentals, we would expect the SNB to hike. But if the franc stays strong, the first increase will come later as the SNB awaits further evidence on the robustness of the economy. Since July, we have had the first hike in March 2011. That now looks very challenging, particularly given the subdued level of the SNB’s medium-term inflation forecast. It is also tricky to think of reasons to expect the franc to soften between now and then; there are widespread expectations of an escalation in market tensions early in 2011 when a large amount of euro area sovereign debt supply comes onto the market. We will revisit our call first thing in the New Year – but the risk is clearly that the first hike comes later in 2011.

Chart 1: SNB Policy Rates

Source: Reuters EcoWin Pro

Chart 2: SNB Inflation Forecasts

Source: Reuters EcoWin Pro

18

Gizem Kara 16 December 2010Market Mover www.GlobalMarkets.bnpparibas.com

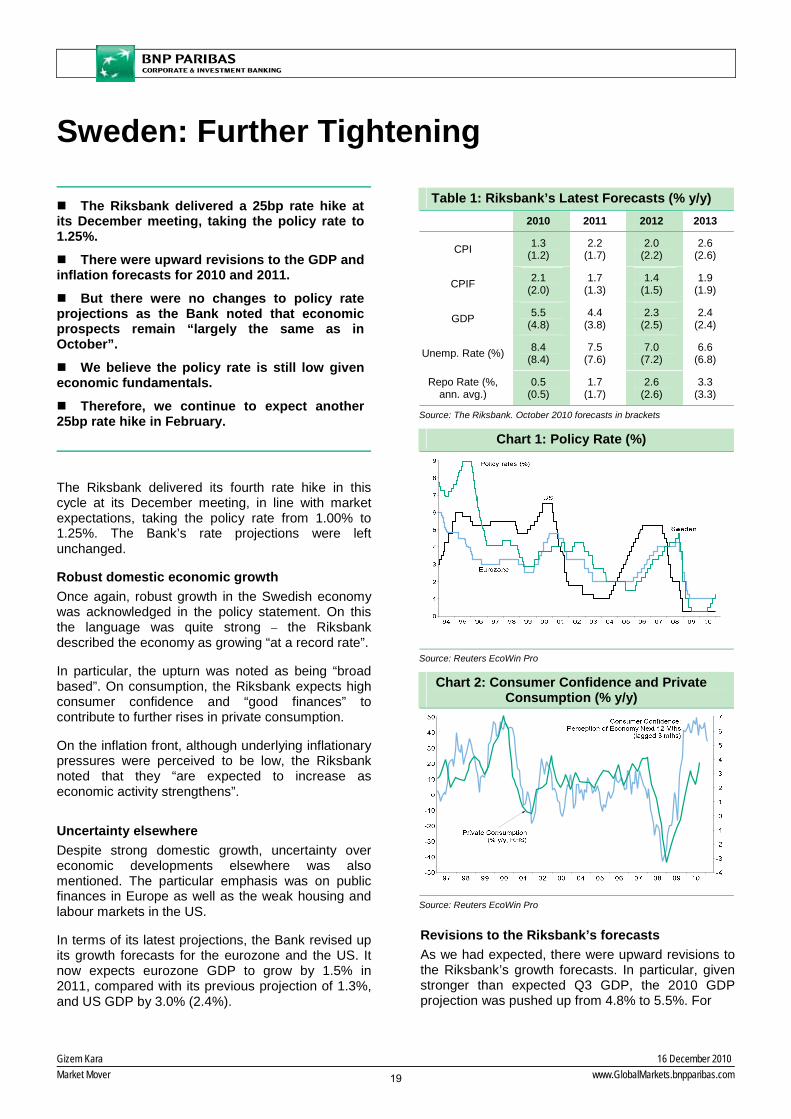

Sweden: Further Tightening The Riksbank delivered a 25bp rate hike at

its December meeting, taking the policy rate to 1.25%.

There were upward revisions to the GDP and inflation forecasts for 2010 and 2011.

But there were no changes to policy rate projections as the Bank noted that economic prospects remain “largely the same as in October”.

We believe the policy rate is still low given economic fundamentals.

Therefore, we continue to expect another 25bp rate hike in February.

The Riksbank delivered its fourth rate hike in this cycle at its December meeting, in line with market expectations, taking the policy rate from 1.00% to 1.25%. The Bank’s rate projections were left unchanged.

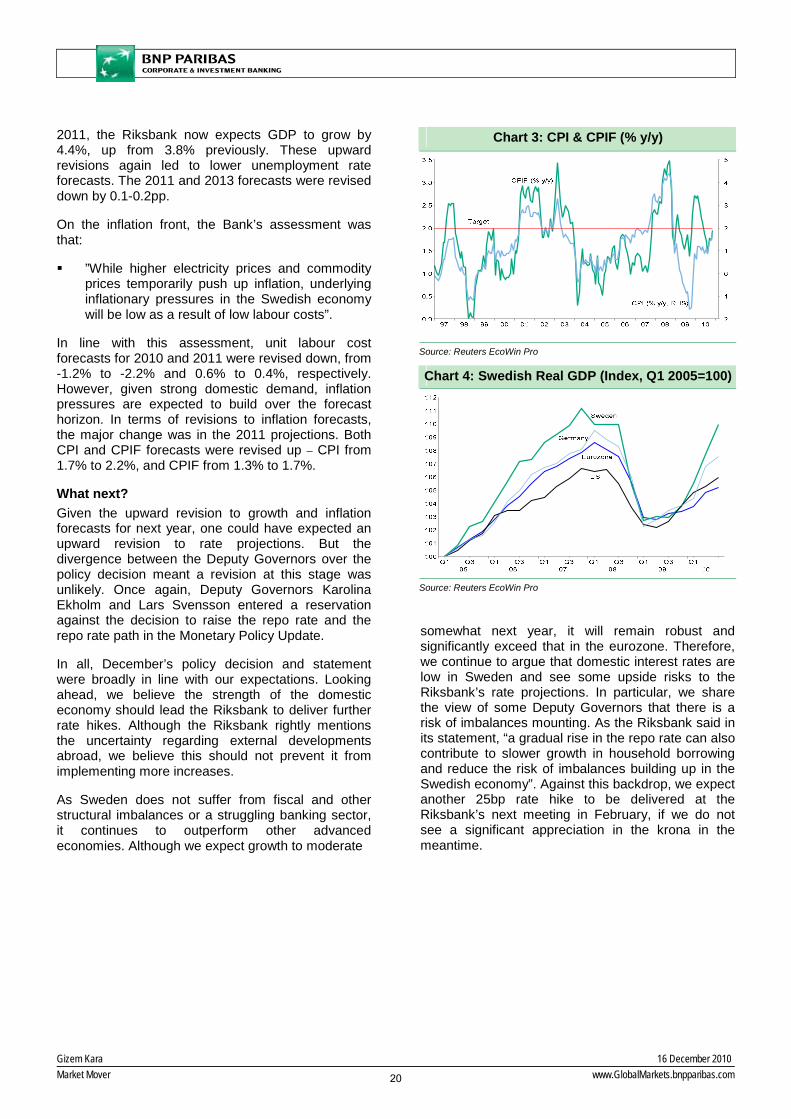

Robust domestic economic growth Once again, robust growth in the Swedish economy was acknowledged in the policy statement. On this the language was quite strong – the Riksbank described the economy as growing “at a record rate”.

In particular, the upturn was noted as being “broad based”. On consumption, the Riksbank expects high consumer confidence and “good finances” to contribute to further rises in private consumption.

On the inflation front, although underlying inflationary pressures were perceived to be low, the Riksbank noted that they “are expected to increase as economic activity strengthens”.

Uncertainty elsewhere Despite strong domestic growth, uncertainty over economic developments elsewhere was also mentioned. The particular emphasis was on public finances in Europe as well as the weak housing and labour markets in the US.

In terms of its latest projections, the Bank revised up its growth forecasts for the eurozone and the US. It now expects eurozone GDP to grow by 1.5% in 2011, compared with its previous projection of 1.3%, and US GDP by 3.0% (2.4%).

Revisions to the Riksbank’s forecasts As we had expected, there were upward revisions to the Riksbank’s growth forecasts. In particular, given stronger than expected Q3 GDP, the 2010 GDP projection was pushed up from 4.8% to 5.5%. For

Table 1: Riksbank’s Latest Forecasts (% y/y) 2010 2011 2012 2013

CPI 1.3 (1.2)

2.2 (1.7)

2.0 (2.2)

2.6 (2.6)

CPIF 2.1 (2.0)

1.7 (1.3)

1.4 (1.5)

1.9 (1.9)

GDP 5.5 (4.8)

4.4 (3.8)

2.3 (2.5)

2.4 (2.4)

Unemp. Rate (%) 8.4 (8.4)

7.5 (7.6)

7.0 (7.2)

6.6 (6.8)

Repo Rate (%, ann. avg.)

0.5 (0.5)

1.7 (1.7)

2.6 (2.6)

3.3 (3.3)

Source: The Riksbank. October 2010 forecasts in brackets

Chart 1: Policy Rate (%)

Source: Reuters EcoWin Pro

Chart 2: Consumer Confidence and Private Consumption (% y/y)

Source: Reuters EcoWin Pro

19

Gizem Kara 16 December 2010Market Mover www.GlobalMarkets.bnpparibas.com

2011, the Riksbank now expects GDP to grow by 4.4%, up from 3.8% previously. These upward revisions again led to lower unemployment rate forecasts. The 2011 and 2013 forecasts were revised down by 0.1-0.2pp.

On the inflation front, the Bank’s assessment was that:

”While higher electricity prices and commodity prices temporarily push up inflation, underlying inflationary pressures in the Swedish economy will be low as a result of low labour costs”.

In line with this assessment, unit labour cost forecasts for 2010 and 2011 were revised down, from -1.2% to -2.2% and 0.6% to 0.4%, respectively. However, given strong domestic demand, inflation pressures are expected to build over the forecast horizon. In terms of revisions to inflation forecasts, the major change was in the 2011 projections. Both CPI and CPIF forecasts were revised up – CPI from 1.7% to 2.2%, and CPIF from 1.3% to 1.7%.

What next? Given the upward revision to growth and inflation forecasts for next year, one could have expected an upward revision to rate projections. But the divergence between the Deputy Governors over the policy decision meant a revision at this stage was unlikely. Once again, Deputy Governors Karolina Ekholm and Lars Svensson entered a reservation against the decision to raise the repo rate and the repo rate path in the Monetary Policy Update.

In all, December’s policy decision and statement were broadly in line with our expectations. Looking ahead, we believe the strength of the domestic economy should lead the Riksbank to deliver further rate hikes. Although the Riksbank rightly mentions the uncertainty regarding external developments abroad, we believe this should not prevent it from implementing more increases.

As Sweden does not suffer from fiscal and other structural imbalances or a struggling banking sector, it continues to outperform other advanced economies. Although we expect growth to moderate

somewhat next year, it will remain robust and significantly exceed that in the eurozone. Therefore, we continue to argue that domestic interest rates are low in Sweden and see some upside risks to the Riksbank’s rate projections. In particular, we share the view of some Deputy Governors that there is a risk of imbalances mounting. As the Riksbank said in its statement, “a gradual rise in the repo rate can also contribute to slower growth in household borrowing and reduce the risk of imbalances building up in the Swedish economy”. Against this backdrop, we expect another 25bp rate hike to be delivered at the Riksbank’s next meeting in February, if we do not see a significant appreciation in the krona in the meantime.

Chart 3: CPI & CPIF (% y/y)

Source: Reuters EcoWin Pro

Chart 4: Swedish Real GDP (Index, Q1 2005=100)

Source: Reuters EcoWin Pro

20

Gizem Kara 16 December 2010Market Mover www.GlobalMarkets.bnpparibas.com

Norway: Hawkish Tone The Norges Bank left its policy rate at 2.00%

at its December meeting, in line with market expectations.

The statement accompanying the policy decision was hawkish compared to October’s.

We expect the Norges Bank to deliver a rate hike in Q2 2011, but a hawkish statement overall has increased the chances of a hike in Q1.

If the krone does not appreciate significantly and economic data turn out to be stronger than the Bank’s expectations, a rate hike is likely in Q1.

Rates on hold The Norges Bank kept its policy rate at 2.00% at its December meeting, in line with market expectations.

In the opening paragraph of the statement, the Bank mentioned that “underlying inflation has been approximately as expected” and “growth has picked up”. But the level of activity was perceived to be “probably still somewhat lower than normal”. In terms of external developments, the Bank said that “growth has been unexpectedly high among several of Norway’s most important trading partners”. We believe this mainly reflects stronger-than-expected growth in Sweden in Q3. Another positive factor noted was the increase in oil prices, which provides a boost to the economy overall.

Less positively, there was acknowledgement of the uncertainty regarding developments in Europe due to fiscal concerns. The Norges Bank noted the high level of borrowing rates in peripheral eurozone countries. That said, the emphasis was still that “contagion to other markets has so far been limited”.

Overall, while the Norges Bank kept its policy rate unchanged, it noted that “the consideration of guarding against the risk of future financial imbalances that may disturb activity and inflation somewhat further ahead suggests that the key policy rate should not be kept low for too long”. This was broadly the same as in the Norges Bank’s in-depth assessment back in October. In all, compared to its predecessor, the statement had a hawkish tone.

Risks around the policy outlook In terms of policy, in its in-depth assessment, the

Norges Bank noted that:

“Both the consideration of bringing consumer price inflation up to target and the consideration of stabilising developments in output and employment imply a low key policy rate”.

Although it again mentioned that “the low interest rate level has not triggered an increase in household debt growth so far”, there was particular emphasis on

Chart 1: Policy Rates (%)

Source: Reuters EcoWin Pro

Chart 2: Real GDP (% y/y)

Source: Reuters EcoWin Pro

Chart 3: Private Consumption & Retail Sales

Source: Reuters EcoWin Pro

21

Gizem Kara 16 December 2010Market Mover www.GlobalMarkets.bnpparibas.com

the rise in house prices and consumer spending. Against this backdrop, the Norges Bank remains aware of the risk of financial imbalances building up in the economy. Therefore, rates are not expected to remain low “for too long”.

Policy ahead Overall, the policy statement signalled that we might see an upward revision to the Norges Bank’s rate projections at its March meeting, when the new Monetary Policy Report will be published. As we noted before, recent domestic developments suggest growth will pick up in the quarters ahead. Given the key policy rate is still low compared to what the neutral rate should be in Norway, we expect rate hikes. We expect the next hike to come in Q2, but the hawkish statement has increased the risk of a rate hike in Q1.

At the press conference after the policy decision, Deputy Governor Qvigstad mentioned that he sees no reason to change the Bank’s policy rate projections (the quarterly rate projections in the October Monetary Policy Report suggested the Bank intends to deliver a rate hike, at the earliest, in summer 2011). However, developments in the period ahead will be key for the timing of the hike.

In particular, if we do not see a signicant appreciation in the currency, economic data surprises to the upside and house prices increase markedly, the Norges Bank is likely to deliver a rate hike in Q1. But if tensions in financial markets intensify going into next year due to concerns over the eurozone, the Bank will wait until Q2.

Chart 4: Credit To Households and Non-Financial Corporations (% y/y)

Source: Reuters EcoWin Pro

Chart 5: Import-Weighted NOK

Source: Reuters EcoWin Pro

22

Paul Mortimer-Lee / Selim Cakir 16 December 2010Market Mover www.GlobalMarkets.bnpparibas.com

IMPORTANT DISCLOSURE: This analysis has been produced jointly by employees of BNP Paribas S.A. ("BNPP") and Turk Ekonomi Bank A.S. (“TEB”). It has been separately reviewed and approved by BNPP and TEB. BNPP is an indirect shareholder of TEB with 42.125% stake. This analysis does not contain investment research recommendations.

Turkey: Reserving Judgement The Turkish central bank’s deputy governor,

Erdem Başçı, this week suggested that the CBT could cut interest rates and increase reserve requirements.

This would be designed to maintain monetary discipline in the economy while avoiding undue appreciation of the exchange rate.

We have serious doubts about the effectiveness of such a policy without support from fiscal policy.

We believe the current suggested policy mix is likely to result in real exchange rate appreciation through higher inflation and would do little to bolster financial stability in the event of a reversal of inflows.

The Turkish central bank’s deputy governor, Erdem Başçı, this week stated that to achieve the dual objectives of “price stability” and “financial stability”, the optimal policy choice was to reduce the policy rate to curb FX inflows and to tighten domestic conditions through use of tools other than the interest rate (read: reserve requirements).

Turkey is not alone in its endeavour. An increasing number of emerging market countries are looking for ways to manage monetary policy by avoiding outright rate hikes because they fear FX appreciation. They have adopted measures to discourage speculative inflows and address potential financial instability. These measures are sometimes called macro-prudential regulation, which sounds a lot less coarse than capital controls.

Emerging markets’ worries are understandable We have sympathy with the authorities in emerging markets where achieving domestic balance requires higher interest rates but where achieving external balance argues against that. One of the main effects of ultra-easy US monetary policy is on inflation abroad. These effects are often manifested in oil and other commodity prices (e.g. food).

However, the Fed's inflation objective excludes food and energy. There are two things wrong with this. First, it treats a big chunk of US inflation as exogenous whereas we all know it is endogenous

and is affected by US policy. Second, the inflation target is inconsistent with the US' obligations as issuer of THE reserve currency.

Is the US shock temporary or more lasting? Clearly, in many countries, the level of interest rates is far below nominal growth when the economy is at potential, which appears too loose. If one believes that the US output gap is transitory and US inflation is low on a temporary basis, then keeping rates down

Chart 1: Credit Growth1 and Reserve Requirement Ratios in Selected EMs

RRR, %

Credit Growth, y/y, %

0

5

10

15

20

25

30

35

40

Czech

R.

S. Kore

a

Russia

Poland

Turkey

India

Indon

esia

Peru

Argenti

naChin

aBraz

il

Source: ReutersEcowinPro, local authorities. (1) Latest available data.

Chart 2: Required Reserves and Their Remuneration

Market overnight rate

Remuneration Rate of RR

Cost of RR( Policy rate-RR)

RRR (RHS)

-10

-5

0

5

10

15

20

25

Jan-

08

Mar

-08

May

-08

Jul-0

8

Sep-

08