european custom procedure trays markets m16f-54€¦ · cardiology 2-1 cataract 2-1 ... sterile...

TRANSCRIPT

European Custom Procedure Trays Markets

M16F-54

#M16F-54 © 2007 Frost & Sullivan www.frost.com August 2007

Publications Division – Terms and Conditions of Business

1. Frost & Sullivan takes no responsibility for any incorrect information supplied by manufacturers or users.

Quantitative market information is based primarily on interviews and therefore is subject to fluctuation.

2. Frost & Sullivan reports are limited publications containing valuable market information provided to a select

group of customers in response to orders. Our customers acknowledge when ordering that Frost & Sullivan

reports are for our customers’ internal use and not for general publication or disclosure to third parties.

3. No part of any Frost & Sullivan report may be given, lent, resold, or disclosed to third parties without written

permission. Third parties include subsidiary companies, other legal entities, customers, suppliers or any other

organisation or associate of the purchasing company.

4. Furthermore, the report in full or in part may not be reproduced, stored in a retrieval system, or transmitted in

any form or by any means, electronic, mechanical, photocopying, recording, or otherwise, without the

permission of the publisher or where covered by a corporate licence agreement or where sold under the terms of

a Frost & Sullivan Online contract.

5. Payment is due upon receipt of invoice.

6. Prices quoted verbally or in writing are valid for thirty days. Invoices must be paid in the currency quoted and

shown on the invoice.

7. Standard delivery time is 14 days from date of receipt of an official purchase order.

8. Draft (pre-press) reports are sold prior to checking and editing and are therefore subject to later correction.

Orders for draft reports will be invoiced with delivery of the draft report. Draft reports must be returned to the

address below on receipt of the final copy.

9. Extra copies of a report are available for $500 if ordered together with the initial copy. Usage and distribution

of extra report copies are subject to the same terms and conditions as the initial report. Corporate and Online

licences which allow worldwide use of multiple copies of reports and unlimited distribution within one

organisation are available.

For further information, write to:

European Sales Manager

Frost & Sullivan Ltd

4 Grosvenor Gardens

London

SW1W 0AH

#M16F-54 © 2007 Frost & Sullivan www.frost.com August 2007 iii

Table of Contents

C h a p t e r 1

Executive Summary

Summary 1-1

Executive Summary of the European Custom Procedure Trays Market 1-1

C h a p t e r 2

Glossary of Terms

Definition of terms 2-1

Procedure Definition 2-1

Cardiology 2-1

Cataract 2-1

Coronary Angiography 2-1

Coronary Artery Bypass Graft (CABG) 2-1

Custom Procedure Tray (CPT) 2-2

Customer Adapted Set (CAS) 2-2

Diagnosis Related Groups (DRGs) 2-2

Minimally Invasive Surgery 2-2

Non-wovens 2-2

Obstetrics 2-2

Percutaneous Transluminal Coronary Angioplasty (PTCA) 2-3

Reusable Product 2-3

Single-use Product 2-3

Sterile Field 2-3

Sterilisation 2-3

#M16F-54 © 2007 Frost & Sullivan www.frost.com August 2007 iv

C h a p t e r 3

Industry Challenges

Identification of Challenges Facing the European Custom Procedure Trays Market 3-1

Industry Challenges 3-1

Issues on Effective Supply Chain Management 3-2

Increasing Product Awareness 3-2

Customized Sourcing 3-2

Dedicated Sales and Marketing Channel 3-3

C h a p t e r 4

European Custom Procedure Trays Market

European CPT Market 4-1

Market Overview 4-1

Market Engineering Measurements 4-3

Market Drivers 4-3

Increased Emphasis on Infection Control Measures 4-4

Reduction in Procurement Costs and Time 4-4

Product Bundling 4-5

Benefits of Customization 4-5

Improved Clinical and Staff Efficiency 4-5

Government Regulations to Advance Single Use Products 4-5

Constant Rise in the Number of Surgeries 4-6

Cost Control Model 4-6

Market Restraints 4-6

Pricing Pressure 4-7

Growth of New Procedures 4-7

Brand Allegiance 4-7

Lack of Standardization Amongst Geographical Regions 4-8

Customer Perception 4-8

Long-term Contracts for Medical Device Components 4-8

Market Forecasts 4-8

Pricing Trends 4-10

#M16F-54 © 2007 Frost & Sullivan www.frost.com August 2007 v

Trends by Geographic Region 4-11

Trends by Product Type 4-12

Competitive Structure 4-14

Angiography CPT Market for Europe 4-15

Market Overview 4-15

Market Engineering Measurements 4-16

Market Forecasts 4-16

Pricing Trends 4-18

Trends by Geographic Region 4-18

Market Share Analysis 4-19

Ophthalmic CPT Market for Europe 4-22

Market Overview 4-22

Market Engineering Measurements 4-22

Market Forecasts 4-23

Pricing Trends 4-25

Trends by Geographic Region 4-25

Market Share Analysis 4-26

Operating Room CPT Market for Europe 4-28

Market Overview 4-28

Market Engineering Measurements 4-29

Market Forecasts 4-30

Pricing Trends 4-32

Trends by Geographic Region 4-32

Market Share Analysis 4-34

Anaesthesia Room CPT Market for Europe 4-36

Market Overview 4-36

#M16F-54 © 2007 Frost & Sullivan www.frost.com August 2007 vi

Market Engineering Measurements 4-37

Market Forecasts 4-37

Pricing Trends 4-39

Trends by Geographic Region 4-39

Market Share Analysis 4-40

C h a p t e r 5

Market Engineering Research for German Custom Procedure Trays Market

German CPT Market Forecast 5-1

Market Overview 5-1

Market Engineering Measurements 5-2

Market Forecasts 5-2

Angiography CPT Market 5-4

Ophthalmic CPT Market 5-5

Operating Room CPT Market 5-7

Anaesthesia Room CPT Market 5-8

C h a p t e r 6

Market Engineering Research for the French Custom Procedure Tray Market

French CPT Market Forecast 6-1

Market Overview 6-1

Market Engineering Measurements 6-1

Market Forecasts 6-2

Angiography CPT Market 6-4

Ophthalmic CPT Market 6-5

Operating Room CPT Market 6-7

Anaesthesia Room CPT Market 6-8

#M16F-54 © 2007 Frost & Sullivan www.frost.com August 2007 vii

C h a p t e r 7

Market Engineering Research for The United Kingdom Custom Procedure Trays Market

The United Kingdom CPT Market Forecast 7-1

Market Overview 7-1

Market Engineering Measurements 7-2

Market Forecasts 7-3

Angiography CPT Market 7-4

Ophthalmic CPT Market 7-5

Operating Room CPT Market 7-7

Anaesthesia Room CPT Market 7-8

C h a p t e r 8

Market Engineering Research for Italian and Spanish Custom Procedure Trays Market

Italian and Spanish CPT Market Forecast 8-1

Market Overview 8-1

Market Engineering Measurements 8-2

Market Forecasts 8-2

Angiography CPT Market 8-4

Ophthalmic CPT Market 8-5

Operating Room CPT Market 8-7

Anaesthesia Room CPT Market 8-8

#M16F-54 © 2007 Frost & Sullivan www.frost.com August 2007 viii

C h a p t e r 9

Market Engineering Research for Benelux and Scandinavia Custom Procedure Trays Market

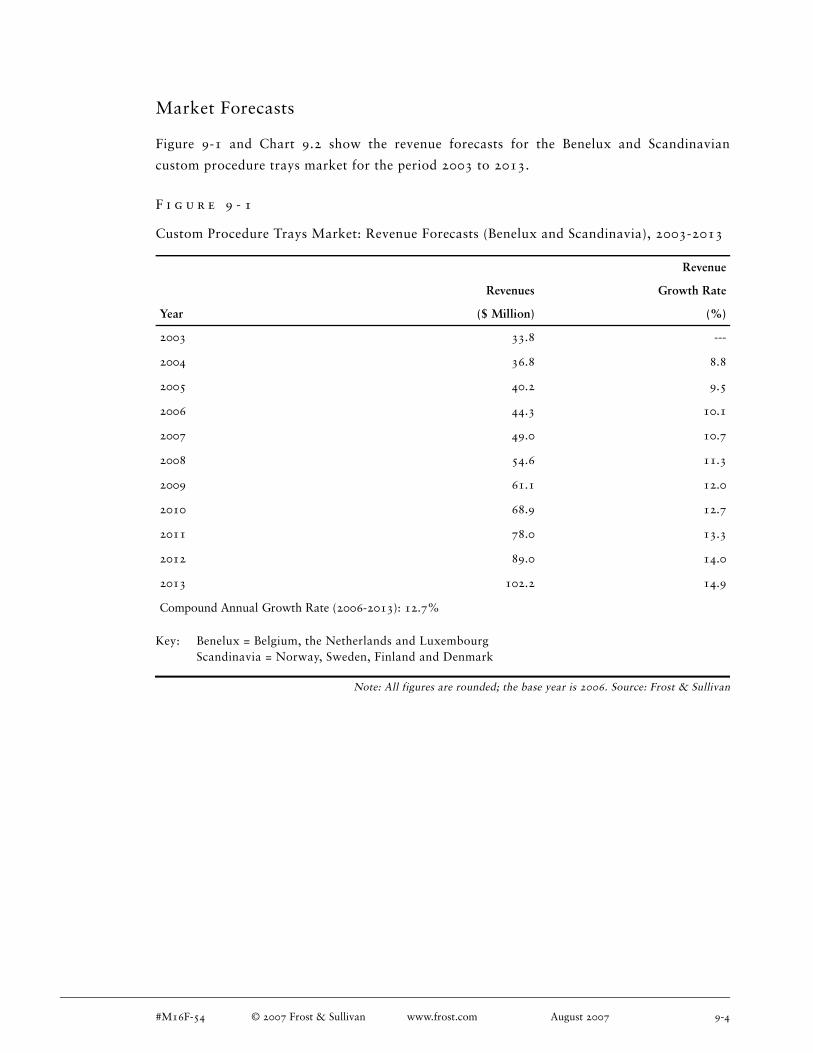

Benelux and Scandinavia CPT Market Forecast 9-1

Market Overview 9-1

Healthcare System in Belgium 9-1

Healthcare System in The Netherlands 9-1

Healthcare System in Denmark 9-2

Healthcare System in Sweden 9-2

Healthcare System in Finland 9-2

Healthcare System in Norway 9-2

Market Engineering Measurements 9-3

Market Forecasts 9-4

Angiography CPT Market 9-5

Ophthalmic CPT Market 9-7

Operating Room CPT Market 9-8

Anaesthesia Room CPT Market 9-10

C h a p t e r 1 0

Market Engineering Strategy

Strategic Recommendations for European Custom Procedure Trays Market 10-1

Strategic Recommendations 10-1

Effective Supply Chain Management 10-2

Competent Supplier Partnership 10-3

Continuous Customer Evaluation 10-3

Vendor-managed Inventory 10-4

Outsourcing Sterilization Facilities 10-4

Entrance of Single-use Surgical Product Manufacturers 10-4

#M16F-54 © 2007 Frost & Sullivan www.frost.com August 2007 ix

C h a p t e r 1 1

Database of Key Industry Participants

Key Industry Participants 11-1

Industry Participants 11-1

C h a p t e r 1 2

Decision Support Databases

Demographics 12-1

Total Population 12-1

Prevalence of Cardiovascular Diseases 12-3

Procedures 12-5

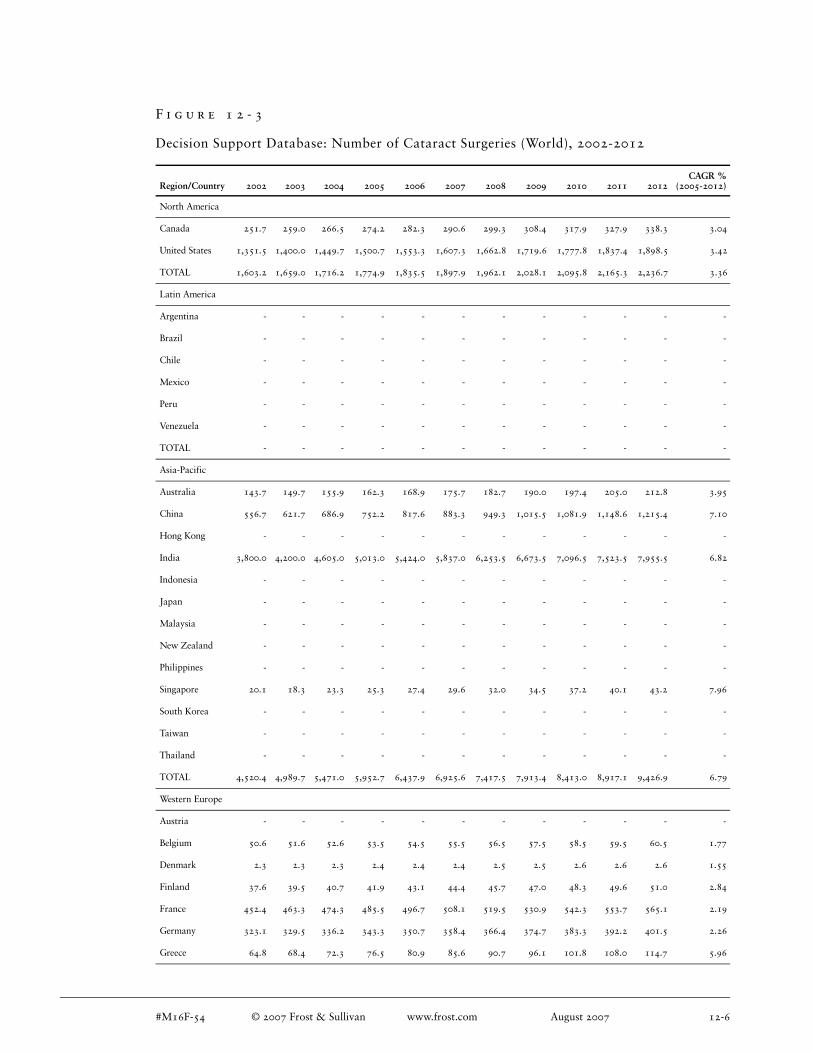

Number of Cataract Surgeries 12-5

Expenditure 12-8

Total Healthcare Expenditure 12-8

Government Healthcare Expenditure 12-10

Private Healthcare Expenditure 12-12

#M16F-54 © 2007 Frost & Sullivan www.frost.com August 2007 x

List of Figures

C h a p t e r 3

Industry Challenges

3-1 Custom Procedure Trays Market:

Impact of Top Four Industry Challenges (Europe), 2007-2013 3-1

C h a p t e r 4

European Custom Procedure Trays Market

4-1 Custom Procedure Trays Market:

Market Drivers Ranked in Order of Impact (Europe), 2007-2013 4-4

4-2 Custom Procedure Trays Market:

Market Restraints Ranked in Order of Impact (Europe), 2007-2013 4-6

4-3 Custom Procedure Trays Market:

Revenue Forecasts (Europe), 2003-2013 4-9

4-4 Custom Procedure Trays Market:

Pricing Trends (Europe), 2003-2013 4-10

4-5 Custom Procedure Trays Market:

Per cent of Revenues by Geographic Region (Europe), 2003-2013 4-11

4-6 Custom Procedure Trays Market:

Per cent of Revenues by Product Type (Europe), 2003-2013 4-13

4-7 Custom Procedure Trays Market:

Competitive Structure (Europe), 2006 4-14

#M16F-54 © 2007 Frost & Sullivan www.frost.com August 2007 xi

4-8 Angiography CPT Market:

Revenue Forecasts (Europe), 2003-2013 4-17

4-9 Angiography CPT Market:

Per cent of Revenues by Geographic Region (Europe), 2003-2013 4-18

4-10 Angiography CPT Market:

Company Market Share by Revenues (Europe), 2006 4-20

4-11 Ophthalmic CPT Market:

Revenue Forecasts (Europe), 2003-2013 4-24

4-12 Ophthalmic CPT Market:

Per cent of Revenues by Geographic Region (Europe), 2003-2013 4-25

4-13 Ophthalmic CPT Market:

Company Market Share by Revenues (Europe), 2006 4-27

4-14 Operating Room CPT Market:

Revenue Forecasts (Europe), 2003-2013 4-31

4-15 Operating Room CPT Market:

Per cent of Revenues by Geographic Region (Europe), 2003-2013 4-33

4-16 Operating Room CPT Market:

Company Market Share by Revenues (Europe), 2006 4-34

4-17 Anaesthesia Room CPT Market:

Revenue Forecasts (Europe), 2003-2013 4-38

4-18 Anaesthesia Room CPT Market:

Per cent of Revenues by Geographic Region (Europe), 2003-2013 4-39

4-19 Anaesthesia Room CPT Market:

Company Market Share by Revenues (Europe), 2006 4-40

#M16F-54 © 2007 Frost & Sullivan www.frost.com August 2007 xii

C h a p t e r 5

Market Engineering Research for German Custom Procedure Trays Market

5-1 Custom Procedure Trays Market:

Revenue Forecasts (Germany), 2003-2013 5-3

5-2 Angiography CPT Market:

Revenue Forecasts (Germany), 2003-2013 5-4

5-3 Ophthalmic CPT Market:

Revenue Forecasts (Germany), 2003-2013 5-6

5-4 Operating Room CPT Market:

Revenue Forecasts (Germany), 2003-2013 5-7

5-5 Anaesthesia Room CPT Market:

Revenue Forecasts (Germany), 2003-2013 5-9

C h a p t e r 6

Market Engineering Research for the French Custom Procedure Tray Market

6-1 Custom Procedure Trays Market:

Revenue Forecasts (France), 2003-2013 6-3

6-2 Angiography CPT Market:

Revenue Forecasts (France), 2003-2013 6-4

6-3 Ophthalmic CPT Market:

Revenue Forecasts (France), 2003-2013 6-6

6-4 Operating Room CPT Market:

Revenue Forecasts (France), 2003-2013 6-7

6-5 Anaesthesia Room CPT Market:

Revenue Forecasts (France), 2003-2013 6-9

#M16F-54 © 2007 Frost & Sullivan www.frost.com August 2007 xiii

C h a p t e r 7

Market Engineering Research for The United Kingdom Custom Procedure Trays Market

7-1 Custom Procedure Trays Market:

Revenue Forecasts (The United Kingdom), 2003-2013 7-3

7-2 Angiography CPT Market:

Revenue Forecasts (The United Kingdom), 2003-2013 7-4

7-3 Ophthalmic CPT Market:

Revenue Forecasts (The United Kingdom), 2003-2013 7-6

7-4 Operating Room CPT Market:

Revenue Forecasts (The United Kingdom), 2003-2013 7-7

7-5 Anaesthesia Room CPT Market:

Revenue Forecasts (The United Kingdom), 2003-2013 7-9

C h a p t e r 8

Market Engineering Research for Italian and Spanish Custom Procedure Trays Market

8-1 Custom Procedure Trays Market:

Revenue Forecasts (Italy and Spain), 2003-2013 8-3

8-2 Angiography CPT Market:

Revenue Forecasts (Italy and Spain), 2003-2013 8-4

8-3 Ophthalmic CPT Market:

Revenue Forecasts (Italy and Spain), 2003-2013 8-6

8-4 Operating Room CPT Market:

Revenue Forecasts (Italy and Spain), 2003-2013 8-7

8-5 Anaesthesia Room CPT Market:

Revenue Forecasts (Italy and Spain), 2003-2013 8-9

#M16F-54 © 2007 Frost & Sullivan www.frost.com August 2007 xiv

C h a p t e r 9

Market Engineering Research for Benelux and Scandinavia Custom Procedure Trays Market

9-1 Custom Procedure Trays Market:

Revenue Forecasts (Benelux and Scandinavia), 2003-2013 9-4

9-2 Angiography CPT Market:

Revenue Forecasts (Benelux and Scandinavia), 2003-2013 9-6

9-3 Ophthalmic CPT Market:

Revenue Forecasts (Benelux and Scandinavia), 2003-2013 9-7

9-4 Operating Room CPT Market:

Revenue Forecasts (Benelux and Scandinavia), 2003-2013 9-9

9-5 Anaesthesia Room CPT Market:

Revenue Forecasts (Benelux and Scandinavia), 2003-2013 9-10

C h a p t e r 1 2

Decision Support Databases

12-1 Decision Support Database:

Total Population in Million (World), 2002-2012 12-1

12-2 Decision Support Database:

Prevalence of Cardiovascular Diseases in Million (World), 2002-2012 12-3

12-3 Decision Support Database:

Number of Cataract Surgeries (World), 2002-2012 12-6

12-4 Decision Support Database:

Total Healthcare Expenditure in Billion USD (World), 2002-2012 12-8

12-5 Decision Support Database:

Government Healthcare Expenditure in Billion USD (World), 2002-2012 12-10

12-6 Decision Support Database:

Private Healthcare Expenditure in Billion USD (World), 2002-2012 12-12

#M16F-54 © 2007 Frost & Sullivan www.frost.com August 2007 xv

List of Charts

C h a p t e r 4

European Custom Procedure Trays Market

4.1 Custom Procedure Trays Market:

Market Engineering Measurements (Europe), 2006 4-3

4.2 Custom Procedure Trays Market:

Revenue Forecasts (Europe), 2003-2013 4-9

4.3 Custom Procedure Trays Market:

Per cent of Revenues by Geographic Region (Europe), 2003-2013 4-12

4.4 Custom Procedure Trays Market:

Per cent of Revenues by Product Type (Europe), 2003-2013 4-13

4.5 Angiography CPT Market:

Market Engineering Measurements (Europe), 2006 4-16

4.6 Angiography CPT Market:

Revenue Forecasts (Europe), 2003-2013 4-17

4.7 Angiography CPT Market:

Per cent of Revenues by Geographic Region (Europe), 2003-2013 4-19

4.8 Angiography CPT Market:

Company Market Share by Revenues (Europe), 2006 4-20

4.9 Ophthalmic CPT Market:

Market Engineering Measurements (Europe), 2006 4-23

4.10 Ophthalmic CPT Market:

Revenue Forecasts (Europe), 2003-2013 4-24

#M16F-54 © 2007 Frost & Sullivan www.frost.com August 2007 xvi

4.11 Ophthalmic CPT Market:

Per cent of Revenues by Geographic Region (Europe), 2003-2013 4-26

4.12 Ophthalmic CPT Market:

Company Market Share by Revenues (Europe), 2006 4-27

4.13 Operating Room CPT Market:

Market Engineering Measurements (Europe), 2006 4-30

4.14 Operating Room CPT Market:

Revenue Forecasts (Europe), 2003-2013 4-31

4.15 Operating Room CPT Market:

Per cent of Revenues by Geographic Region (Europe), 2003-2013 4-33

4.16 Operating Room CPT Market:

Company Market Share by Revenues (Europe), 2006 4-35

4.17 Anesthesia Room CPT Market:

Market Engineering Measurements (Europe), 2006 4-37

4.18 Anaesthesia Room CPT Market:

Revenue Forecasts (Europe), 2003-2013 4-38

4.19 Anaesthesia Room CPT Market:

Per cent of Revenues by Geographic Region (Europe), 2003-2013 4-40

4.20 Anaesthesia Room CPT Market:

Company Market Share by Revenues (Europe), 2006 4-41

C h a p t e r 5

Market Engineering Research for German Custom Procedure Trays Market

5.1 Custom Procedure Trays Market:

Market Engineering Measurements (Germany), 2006 5-2

5.2 Custom Procedure Trays Market:

Revenue Forecasts (Germany), 2003-2013 5-3

#M16F-54 © 2007 Frost & Sullivan www.frost.com August 2007 xvii

5.3 Angiography CPT Market:

Revenue Forecasts (Germany), 2003-2013 5-5

5.4 Ophthalmic CPT Market:

Revenue Forecasts (Germany), 2003-2013 5-6

5.5 Operating Room CPT Market:

Revenue Forecasts (Germany), 2003-2013 5-8

5.6 Anaesthesia Room CPT Market:

Revenue Forecasts (Germany), 2003-2013 5-9

C h a p t e r 6

Market Engineering Research for the French Custom Procedure Tray Market

6.1 Custom Procedure Trays Market:

Market Engineering Measurements (France), 2006 6-2

6.2 Custom Procedure Trays Market:

Revenue Forecasts (France), 2003-2013 6-3

6.3 Angiography CPT Market:

Revenue Forecasts (France), 2003-2013 6-5

6.4 Ophthalmic CPT Market:

Revenue Forecasts (France), 2003-2013 6-6

6.5 Operating Room CPT Market:

Revenue Forecasts (France), 2003-2013 6-8

6.6 Anaesthesia Room CPT Market:

Revenue Forecasts (France), 2003-2013 6-9

#M16F-54 © 2007 Frost & Sullivan www.frost.com August 2007 xviii

C h a p t e r 7

Market Engineering Research for The United Kingdom Custom Procedure Trays Market

7.1 Custom Procedure Trays Market:

Market Engineering Measurements (The United Kingdom), 2006 7-2

7.2 Custom Procedure Trays Market:

Revenue Forecasts (The United Kingdom), 2003-2013 7-3

7.3 Angiography CPT Market:

Revenue Forecasts (The United Kingdom), 2003-2013 7-5

7.4 Ophthalmic CPT Market:

Revenue Forecasts (The United Kingdom), 2003-2013 7-6

7.5 Operating Room CPT Market:

Revenue Forecasts (The United Kingdom), 2003-2013 7-8

7.6 Anaesthesia Room CPT Market:

Revenue Forecasts (The United Kingdom), 2003-2013 7-9

C h a p t e r 8

Market Engineering Research for Italian and Spanish Custom Procedure Trays Market

8.1 Custom Procedure Trays Market:

Market Engineering Measurements (Italy and Spain), 2006 8-2

8.2 Custom Procedure Trays Market:

Revenue Forecasts (Italy and Spain), 2003-2013 8-3

8.3 Angiography CPT Market:

Revenue Forecasts (Italy and Spain), 2003-2013 8-5

8.4 Ophthalmic CPT Market:

Revenue Forecasts (Italy and Spain), 2003-2013 8-6

#M16F-54 © 2007 Frost & Sullivan www.frost.com August 2007 xix

8.5 Operating Room CPT Market:

Revenue Forecasts (Italy and Spain), 2003-2013 8-8

8.6 Anaesthesia Room CPT Market:

Revenue Forecasts (Italy and Spain), 2003-2013 8-9

C h a p t e r 9

Market Engineering Research for Benelux and Scandinavia Custom Procedure Trays Market

9.1 Custom Procedure Trays Market:

Market Engineering Measurements (Benelux and Scandinavia), 2006 9-3

9.2 Custom Procedure Trays Market:

Revenue Forecasts (Benelux and Scandinavia), 2003-2013 9-5

9.3 Angiography CPT Market:

Revenue Forecasts (Benelux and Scandinavia), 2003-2013 9-6

9.4 Ophthalmic CPT Market:

Revenue Forecasts (Benelux and Scandinavia), 2003-2013 9-8

9.5 Operating Room CPT Market:

Revenue Forecasts (Benelux and Scandinavia), 2003-2013 9-9

9.6 Anaesthesia Room CPT Market:

Revenue Forecasts (Benelux and Scandinavia), 2003-2013 9-11

C h a p t e r 1 0

Market Engineering Strategy

10.1 Custom Procedure Trays Market:

Competitive Rivalry (Europe), 2006 10-2

#M16F-54 © 2007 Frost & Sullivan www.frost.com August 2007 1-1

1Executive Summary

S u m m a r y

Executive Summary of the European Custom Procedure Trays Market

Slides 1 to 8 provide an overview of the European custom procedure trays market from

2003 to 2013.

1

!"#$%&'()*"+,$-).#$/&0"#&)1#'2+)3'#4&,+

356789:

;"<"+,)=>>?

! "##$%&'()*%+%,-../0123%4..%'/56*)%'7)7'0783%96/)%8(:-;72*%:(2*1/2)%6/56.<%:(2=/872*/1.%/2=(';1*/(2%128%/)%*67%)(.7%>'(>7'*<%(=%&'()*%+%,-../0123%?(%>1'*%(=%/*%;1<%@7%:/':-.1*78A%B-(*78A%:(>/78%('%(*67'C/)7%'7>'(8-:78%C/*6(-*%*67%C'/**72%1>>'(01.%(=%&'()*%+%,-../0123

#M16F-54 © 2007 Frost & Sullivan www.frost.com August 2007 1-2

DEF&GHI !%"##$%&'()*%+%,-../012A%4..%'/56*)%'7)7'078%CC3='()*3:(; "

4%87*1/.78%=/212:/1.%121.<)/)%(=%*67%J-'(>712%%K-)*(;%L'(:78-'7%9'1<)%

D1'M7*)%/)%>'7)72*78%/2%*6/)%'7)71':6%)7'0/:73%967%121.<)/)%/)%@1)78%(2%=(-'%

M7<%=1:*(')N

43 &('7:1)*%;1'M7*%8<21;/:)

O3 D1'M7*%,61'7)

K3 ,75;72*%'7072-7)

P3%Q75/(21.%*'728)

3;@A!1 B*

C

;

J-'(>712%%K-)*(;%L'(:78-'7%9'1<)%D1'M7*)

DEF&GHI !%"##$%&'()*%+%,-../012A%4..%'/56*)%'7)7'078%CC3='()*3:(; R

D&$<#'%EF/'G)@&<F$(+H(F,&0)AF(<0$-)

D&#-'(2

7#'(/&

I,'G2)J)K%'F(

C&(&G"LMM)J)K/'(0F('NF'M)S%,:128/210/1%T%,C7872A%&/2.128A%?('C1<

128%P72;1'M

SS%O727.-U%T%O7.5/-;A%*67%?7*67'.128)%128%

V-U7;@(-'5

7$#&/'+,).&#F$0

C'+&)O&'#P)=>>6))

7$#&/'+,).&#F$0)F+)=>>?Q=>5R

@&+&'#/E)K/$%&

,*'1*75/:%421.<)/)%(=%*67%J-'(>712%%K-)*(;%L'(:78-'7%9'1<)%D1'M7*)

@&+&'#/E)3&,E$0$G$<2

! .#F-'#2)#&+&'#/E)SF,E)F(0"+,#2)%'#,F/F%'(,+

! 7#$+,)J)K"GGFN'()%"TGF+E&0)#&+&'#/E)+&#NF/&+

! B&/F+F$()+"%%$#,)0','T'+&+

! *$"(,#2)F(0"+,#2)U$#&/'+,+

! .#$%#F&,'#2)0','T'+&+

*"##&(/2*"##&(/2)UF<"#&+)'#&)F()HK)0$GG'#+!"#$P))))V5)!"#$)W)HKX5YR5

W4)%(2%E"*6 4>'/.A%"##$X

#M16F-54 © 2007 Frost & Sullivan www.frost.com August 2007 1-3

DEF&GHI !%"##$%&'()*%+%,-../012A%4..%'/56*)%'7)7'078%CC3='()*3:(; I

K&<-&(,',F$()T2).#$0"/,)12%&

*.1

;(<F$<#'%E2*.1

Z%E,E'G-$G$<2)*.1

Z%&#',F(<)@$$-)*.1

;('&+,E&+F')*.1

Y7<N%KL9%T%K-)*(;%L'(:78-'7%9'1<)%

DEF&GHI !%"##$%&'()*%+%,-../012A%4..%'/56*)%'7)7'078%CC3='()*3:(; H

I(0"+,#2)*E'GG&(<&+QZN&#NF&S)

" I++"&+)$()&UU&/,FN&)+"%%G2)/E'F()-'('<&-&(," I(/#&'+F(<)%#$0"/,)'S'#&(&++" *"+,$-F[&0)+$"#/F(<" B&0F/',&0)')+'G&+)'(0)-'#4&,F(<)/E'((&G))

!"#$%&'()*"+,$-).#$/&0"#&)1#'2+\3'#4&,)I(0"+,#2)/E'GG&(<&+

#M16F-54 © 2007 Frost & Sullivan www.frost.com August 2007 1-4

DEF&GHI !%"##$%&'()*%+%,-../012A%4..%'/56*)%'7)7'078%CC3='()*3:(; F

!"#$%&'()*"+,$-).#$/&0"#&)1#'2+)3'#4&,\3'#4&,)

B#FN&#+)'(0)@&+,#'F(,+

]'/4)$U)K,'(0'#0F[',F$()'-$(<+,)D&$<#'%EF/'G)

@&<F$(+

^ID^]Z_ 3!BIH3

@!K1@;I`1K

B@Ia!@K

D#$S,E)$U)`&S).#$/&0"#&+

*$(+,'(,)#F+&)F()

`"-T&#)$U)

K"#<&#F&+.#$0"/,)C"(0GF(<)

I(/#&'+&0)!-%E'+F+)

$()I(U&/,F$()*$(,#$G)

3&'+"#&+)

C&(&UF,+)$U)

*"+,$-F[',F$(

.#F/F(<).#&++"#&

I-%#$N&0)*GF(F/'G)

'(0)K,'UU)!UUF/F&(/2

@&0"/,F$()F()

.#$/"#&-&(,)*$+,+)

'(0)1F-&

D$N&#(-&(,)

@&<"G',F$(+),$)

;0N'(/&)KF(<G&)H+&)

.#$0"/,+Y)

C#'(0);GG&<F'(/&

*.18;)*$+,)*$(,#$G)

3$0&G

*"+,$-&#).&#/&%,F$(

]$(<)1&#-)*$(,#'/,+)U$#)3&0F/'G)B&NF/&)

*$-%$(&(,+

DEF&GHI !%"##$%&'()*%+%,-../012A%4..%'/56*)%'7)7'078%CC3='()*3:(; $

K,#',&<F/)@&/$--&(0',F$(+

a&(0$#8-'('<&0)

I(N&(,$#2

*$(,F("$"+)

*"+,$-&#)

!N'G"',F$(

*$-%&,&(,)

K"%%GF&#)

.'#,(&#+EF%

#!UU&/,FN&)K"%%G2)*E'F()3'('<&-&(,

KF(<G&)H+&)3'("U'/,"#&#+)

/$"G0).&(&,#',&)*.1)

3'#4&,

Z",+$"#/F(<)K,&#FGF[',F$()7'/FGF,F&+

#M16F-54 © 2007 Frost & Sullivan www.frost.com August 2007 1-5

DEF&GHI !%"##$%&'()*%+%,-../012A%4..%'/56*)%'7)7'078%CC3='()*3:(; Z

*$(/G"+F$(+

[ 967%KL9%:(2:7>*%/)%7U*'7;7.<%>(>-.1'%/2%*67%\2/*78%,*1*7)A%128%J-'(>7%/)%=('7:1)*%*(%7B-1.%*61*%/2%*67%:(;/25%<71')3%967'7%61)%@772%1%)-@)*12*/1.%5'(C*6A%>1'*/:-.1'.<%/2%:7'*1/2%:(-2*'/7)3%967%;1/2%>'(:78-'7)%C67'7%KL9%61)%@7:(;7%>(>-.1'%1'7%125/(5'1>6<%128%(>6*61.;/:%)-'57'<3%P'/0/25%KL9%/)%12%/2:'71)78%87)/'7%=('%:(2072/72:7A%)>778%128%'7./1@/./*<%/2%*7';)%(=%*67%;78/:1.%8/)>()[email protected])%-)78%=('%)-'57'<3%K(;>.7*7%:-)*(;/)1*/(2%128%(>*/;/)1*/(2%(=%'7)(-':7)%/)%*67%M7<%8'/07'%/2%=-*-'7

[ 96/)%'7)71':6%)7'0/:7%>'(0/87)%12%/2G87>*6%121.<)/)%(=%*67%J-'(>712%K-)*(;%L'(:78-'7%9'1<)%D1'M7*A%128%>'(0/87)%)*'1*75/:%'7:(;;7281*/(2)%*(%)-::778%/2%*67%/2:'71)/25.<%:(;>7*/*/07%720/'(2;72*

#M16F-54 © 2007 Frost & Sullivan www.frost.com August 2007 2-1

2Glossary of Terms

D e f i n i t i o n o f t e r m s

Procedure Definition

C a r d i o l o g y

The study of the heart and its functions. Invasive cardiology is the theory and practice of

diagnostic and therapeutic cardiac procedures such as cardiac catheterization, coronary angi-

oplasty or electrophysiologic studies that involve the entry into the heart or central

circulation.

C a t a r a c t

An opacity in the eye lens, which progressively reduces visual functioning. Cataract rates

increase significantly with age, with the large unmet need in elderly people. Cataract surgery

is a highly effective procedure, improving visual acuity and functioning in 80 to 95 per cent

of patients.

C o r o n a r y A n g i o g r a p h y

The diagnostic procedure that enables the radiographic visualisation of the coronary blood

vessels. It is used to diagnose coronary heart disease, and is therefore essential before coro-

nary angioplasty or coronary artery bypass surgery.

C o r o n a r y A r t e r y B y p a s s G r a f t ( C A B G )

This is a surgery in which the narrowing of a coronary artery is by-passed with a vein or

artery is removed from another part of the patient's body—typically the leg or the chest.

#M16F-54 © 2007 Frost & Sullivan www.frost.com August 2007 2-2

C u s t o m P r o c e d u r e T r a y ( C P T )

The bundling of medical disposables required for particular surgical procedures, supplied in

a sterile package, usually on some form of 'tray'. These medical devices typically include

drapes and gowns, swabs, sutures, knives, syringes, and so on. A CPT essentially includes at

least 90 per cent of the single-use products that are required for a particular procedure. It

excludes products for minor procedures such as basic anaesthesia and suturing kits. It also

excludes products in which non-woven components account for the majority of the contents

of the pack.

C u s t o m e r A d a p t e d S e t ( C A S )

Customer adapted sets essentially contain only drapes, gowns or certain standard items, and

are not assembled to suit particular customer requirements. CAS was developed by the

companies that supply drapes and gowns to hospitals. Occasionally, these companies have

also supplied certain low-value commodity items such as swabs. This supply has increasingly

developed in certain countries such as Germany and Italy.

D i a g n o s i s R e l a t e d G r o u p s ( D R G s )

DRGs shift the responsibility of financing healthcare from tax revenues to health insurance

funds, wherein healthcare costs are reimbursed on the basis of a fixed cost per procedure.

M i n i m a l l y I n v a s i v e S u r g e r y

An invasive procedure is any operation that pierces the skin or mucous membranes, or enters

a body cavity or organ. Minimally invasive surgery seeks to minimise the extent to which this

is necessary.

N o n - w o v e n s

Products made from the formation of fibres directly into a textile web, eliminating the

weaving process used in traditional textile manufacture. The most notable healthcare prod-

ucts made from this material are surgical drapes and gowns.

O b s t e t r i c s

The branch of medicine that deals with the management of pregnancy, labour and

puerperium.

#M16F-54 © 2007 Frost & Sullivan www.frost.com August 2007 2-3

P e r c u t a n e o u s T r a n s l u m i n a l C o r o n a r y A n g i o p l a s t y

( P T C A )

A procedure to treat coronary heart disease. A narrow tube (a cardiac catheter) is passed

through the skin of the groin or elbow into an artery and threaded into the coronary arteries.

When the tip of the catheter is in the narrowed section of the coronary artery, the small

balloon at the tip of the catheter is inflated, thus dilating the narrowed section of the coro-

nary artery. A stent is often inserted into the dilated artery to act as a scaffolding to help keep

it open.

R e u s a b l e P r o d u c t

A product intended to be reprocessed and reused. For example, some drapes and gowns are

made from cotton and poly cotton. Newer 'high tech' reusable products tend to be made of

chemically-modified poly cotton, with an additional membrane to provide an improved

barrier. For many of the single-use products used in procedure trays, there is no reusable

alternative.

S i n g l e - u s e P r o d u c t

A product that the manufacturer intends to be used only once.

S t e r i l e F i e l d

The area considered to be free of micro-organisms during a surgical procedure.

S t e r i l i s a t i o n

The process that eliminates micro-organisms (including bacterial endospores) from surgical

instruments, gowns, drapes and other items.

#M16F-54 © 2007 Frost & Sullivan www.frost.com August 2007 3-1

3Industry Challenges

I d e n t i f i c a t i o n o f C h a l l e n g e s F a c i n g t h e

E u r o p e a n C u s t o m P r o c e d u r e T r a y s M a r k e t

Industry Challenges

The first phase of the Market Engineering methodology is the identification of the key chal-

lenges facing the industry. These challenges have an impact on, and are integrated into, every

phase of the Market Engineering system. An industry challenge is an issue that can affect the

development of the market or the competitors in the marketplace. Challenges include

customer issues, regulatory programmes, economic trends, market measurement trends,

competitive strategies, new technologies, sales and marketing strategies, new market oppor-

tunities and market threats.

Figure 3-1 presents the impact of the top four industry challenges for the European custom

procedure trays market from 2007 to 2013.

Source: Frost & Sullivan

F i g u r e 3 - 1

Custom Procedure Trays Market: Impact of Top Four Industry Challenges (Europe),

2007-2013

Challenge 1-2 Years 3-4 Years 5-7 Years

Issues on effective supply chain management High Medium Low

Increasing product awareness Medium Medium Low

Customized sourcing Medium Medium Low

Dedicated sales and marketing channel Medium Medium Low

#M16F-54 © 2007 Frost & Sullivan www.frost.com August 2007 3-2

These challenges have been identified and ranked on the basis of their impact on the market.

I s s u e s o n E f f e c t i v e S u p p l y C h a i n M a n a g e m e n t

Effective and efficient management of the supply chain is essential in the CPT market. Hence,

it is very important for CPT companies to closely keep track of the hospitals and their needs.

It is critical to understand the importance of selecting the appropriate components for inclu-

sion within a procedure tray. End users such as surgeons are generally highly brand

conscious, and the failure to provide the desired brand may result in business failure. Hence,

adequate training should be provided to the theatre staff about the benefits and usage of a

company's products.

Stock out of raw materials and production parts would shut down an operation and prove

extremely costly in terms of lost production, escalation of operating costs due to fixed costs

and inability to satisfy delivery promises to customers. One way to ensure uninterrupted

material flow is to hold a large inventory. Nevertheless, inventory requires the capital, which

cannot be invested elsewhere; the cost of carrying inventory may reach 20 to 50 per cent of

the total value per year. Therefore, it is important for the supply department to keep inven-

tory investment and loss at a minimum.

I n c r e a s i n g P r o d u c t A w a r e n e s s

Since the CPT market is a complex mix of various components, it is essential to train and

brief end users and theatre staff on product benefits. CPT companies need to make end users

aware of the benefits of purchasing individual components against the cost of purchasing a

CPT. The best method for the same at present is to provide hospitals with on-line facilities for

stock ordering and management activities. Data repeated from the first sentence.New and

innovative methods need to be adopted for training purposes. Educational support tools,

product samples brochures and on-line training sessions could be adopted.

C u s t o m i z e d S o u r c i n g

The idea of 'customization' means offering customers whatever they want. Hospitals often

have special requirements for procedure kits. Choices vary with doctors and even amongst

theatre staff, posing a huge challenge for stock holding for a CPT company. Hence, it is crit-

ical for these companies to have the ability to source various products from a number of

suppliers. The challenge is to segment the products in a CPT into a range of categories and

develop distinct strategies for each type.

#M16F-54 © 2007 Frost & Sullivan www.frost.com August 2007 3-3

Constant customer research is vital to sustain the companies' position in the competitive

market. It helps in understanding the needs of the end user through a broader perspective.

This creates an interesting power play between end users, hospital procurement personnel,

CPT companies and suppliers. The surgeon may wish to use one type of sutures, while the

hospital procurement personnel might be supporting the idea of CPT, but want a competitive

price. CPT companies will want to win the business by supplying the required brands, but

will also wish to do so in a profitable way. A company such as Ethicon is therefore under

pressure to supply CPT companies. In order to manage these relationships effectively, it is

critical that CPT companies should fully understand the importance that customers attach to

brands for specific products.

D e d i c a t e d S a l e s a n d M a r k e t i n g C h a n n e l

Since customer needs have to be closely evaluated and observed, it becomes an important

challenge to employ a dedicated sales and distribution channel for CPT. The employees in

these channels would closely work with the theatre staff, who also contribute significantly to

the decision-making process of procedure packs in hospitals. Customizing kits based on their

suggestions regarding the packing pattern, packing material, product specifications and

delivery specifications is a major challenge. There also exists the need for CPT companies to

be able to communicate the intricate cost comparisons and provide methodologies for

customers to help them understand this process.

#M16F-54 © 2007 Frost & Sullivan www.frost.com August 2007 4-1

4European Custom Procedure Trays Market

E u r o p e a n C P T M a r k e t

Market Overview

Custom Procedure Tray (CPT) is a customized solution for specific hospital procedures. It

contains a bundle of disposable products, which would be required for a particular proce-

dure. Procedure trays meet the surgical user's needs for single-use components in one sterile

pack and provide a convenient way of managing surgical interventions. Since a number of

components are added to a pack, they are sourced from a wide and diverse supplier base,

tailored to meet individual needs including delivery options that will meet the users operating

requirements. The provision of all the single-use components in one pack helps save the time

involved in setting up, reduces packaging waste and benefits the environment, reducing

inventory and associated costs.

The kits consist of dressing material, operating room (OR) drapes and various disposable

products for the daily OR requirements like syringes, cannulae, suture material and others.

Disposable products such as patient drapes, surgical staff clothing and surgical dressings

account for approximately 20 to 30 per cent of the contents in a normal tray. The remaining

products include instruments, sutures, tubes, bowls and various other single-use products are

sourced from different suppliers.

The European CPT market is growing at a fast pace, though not as rapid as the United States.

Many regional participants have recently entered this market. Other single-use product firms

have also extended their product line and included procedure packs in their offering. Large

players in the United States are not able to penetrate this market, unlike other medical

devices.

This research service covers the following segments:

! Angiography custom procedure trays

! Ophthalmic custom procedure trays

! OR custom procedure trays

! Anaesthesia room custom procedure trays

#M16F-54 © 2007 Frost & Sullivan www.frost.com August 2007 4-2

The study period is from 2003 to 2013. The base year is 2006. The forecast period is from

2007 to 2013. Angiography and ophthalmic surgery are the segments that make the

maximum use of custom procedure trays at present. Hence, they have been analysed as

distinct segments. The OR segment combines all other surgical procedures, as the European

market has not yet developed substantially in this area. It excludes ophthalmic procedures

but includes areas such as cardiac surgery, orthopaedic surgery, obstetrics, ENT surgery and

neurosurgery. This segment clearly has the largest overall market potential. Anaesthesia CPT

is a relatively new market, which is still in its infancy stage, with a huge growth potential. It

is expected to experience high growth rates during the forecast period.

The European countries considered in this study comprise a total population of

349.3 million. Germany is the largest country, with almost 24 per cent of this population.

The United Kingdom, France and Italy are very similar in population size, each accounting

for approximately 17 per cent of the total population. Spain has a smaller population, with

the proportion being 11 per cent. Benelux and Scandinavia are similar in size, accounting for

8 and 7 per cent of the total population, respectively.

The elderly population is ever increasing in Europe, as life expectancy is increasing due to

medical advances. The proportion of the population aged above 65 is 16.0 per cent. This is

significant for two reasons. Firstly, the ratio of elderly people to working people (who pay

the taxes that fund healthcare) is increasing, thereby exerting strain on healthcare funding.

Secondly, elderly people are more likely to require surgical procedures, a factor that directly

influences the demand for the products in this market.

In 2006, the European CPT market was valued at $380.4 million, and the revenues are

growing at a very high rate. The potential of the market is greatly ahead of the current

market size. The market is highly fragmented, with a large number of participants in the CPT

business. The increased need for convenience, speed of operations and more efficient hospital

management are driving the customer demand. The market is propelled by the increasing

popularity of outsourcing and the realization of infection risks in hospitals and possible ways

to reduce this problem. A number of companies are expected to enter this market in the

future, with the likelihood of merger and acquisition activity over the next five years being

extremely high. Any company wishing to succeed in the European market must be fully

aware of the complexities of the various healthcare systems in Europe, and possess the neces-

sary sales, marketing, operational and supply chain management skills to succeed.

#M16F-54 © 2007 Frost & Sullivan www.frost.com August 2007 4-3

Market Engineering Measurements

Chart 4.1 presents the market engineering measurements for the European custom procedure

trays market in 2006.

C h a r t 4 . 1

Custom Procedure Trays Market: Market Engineering Measurements (Europe), 2006

Market Engineering Drives Market

Strategy and Planning

MarketEngineer

ChallengeIdentification

MarketResearch

MarketEngineering

System

Implementation

MarketPlanning

MarketStrategy

Note: All figures are rounded. Source: Frost & Sullivan

Market Drivers

Figure 4-1 presents the market drivers ranked in order of impact for the European custom

procedure trays market from 2007 to 2013.

Measurement Name Measurement Trend

Market age Growth stage ---

Revenues $380.4 million Increasing

Potential revenues (maximum future market size) $1,580.5 million Increasing

Base year market growth rate 17.5% Increasing

Compound annual growth rate 22.6% ---

Price sensitivity High Increasing

Average price $39 Increasing

#M16F-54 © 2007 Frost & Sullivan www.frost.com August 2007 4-4

Source: Frost & Sullivan

I n c r e a s e d E m p h a s i s o n I n f e c t i o n C o n t r o l M e a s u r e s

The Government of United Kingdom has formed a 'Trust infection control committee', which

has formulated specific standards for the degree of sterility to be adhered to inside an opera-

tion theatre. The committee has also laid down specifications to prevent infection in other

minimally invasive procedures like ophthalmic procedures, which would require minimum

downtime. Usage of prepacked, sterilized kits would greatly contribute to the reduction of

any nosocomial and iatrogenic infections.

Usage of procedure packs reduces linen and other operating room accessories handling,

thereby preventing chances of infection. Usage of disposable drapes and gowns, which

contribute a major portion of the procedure pack, also decreases the spread of contamination

and reduces lint in operating theatres.

R e d u c t i o n i n P r o c u r e m e n t C o s t s a n d T i m e

The growing diversity of operating procedures and surgical preferences requires the procure-

ment of a massive variety and volume of supporting clinical products. There is also the need

to reduce stockholding space, manage costs and meet emergency requirements. The time,

costs, inconvenience and stress of supplying single-use products to the operating team needs

to be minimized by the most effective purchasing departments. Usage of procedure packs

reduces administrative issues and minimizes the need to liaise with non-core suppliers.

It also enables inventory reduction, easier control on storage and simplified delivery sched-

ules. Procedure kits create an opportunity to standardize contract items and control costs.

F i g u r e 4 - 1

Custom Procedure Trays Market: Market Drivers Ranked in Order of Impact (Europe),

2007-2013

Rank Driver 1-2 Years 3-4 Years 5-7 Years

1 Increased emphasis on infection control measures High High High

2 Reduction in procurement costs and time High High Medium

3 Product bundling Medium High High

4 Benefits of customization Medium High High

5 Improved clinical and staff efficiency Medium Medium High

6 Government regulations to advance single use products Medium Medium Medium

7 Constant rise in the number of surgeries Medium Medium Medium

8 Cost control model Medium Medium Low

#M16F-54 © 2007 Frost & Sullivan www.frost.com August 2007 4-5

P r o d u c t B u n d l i n g

This driver pertains particularly to large companies that aim to become a single supplier fortheir customers. In addition to their specialized products, companies could also consider prepacking the components for a particular procedure. These companies could supply theircapital equipment along with other disposables used during a surgery. This enables compa-nies to overcome competition and build strong relationships with customers. This strategy ismostly used by companies in the ophthalmic and interventional cardiology market.

B e n e f i t s o f C u s t o m i z a t i o n

The foremost benefit of implementing custom procedure packs is the advantage of custom-izing according to the customers' needs, resulting in customer satisfaction. The end usershave the choice to design a component guideline that best suits the kind of procedure orsurgery performed. They also have the option of using products manufactured by a singlefirm or combine products of their choice. The end product, CPT, will only contain the prod-ucts that are specified by the user, from the specified suppliers, packed and deliveredaccording to the users' requirements.

I m p r o v e d C l i n i c a l a n d S t a f f E f f i c i e n c y

Usage of procedure packs improves efficiency by significantly reducing the clinical andadministrative workload, minimizing waste and associated costs, while supporting profes-sional choice. The delivery, selection, collection, checking and aseptic preparation ofnecessary single-use items is a major task. Procedure packs ensure easier aseptic transfer andquicker set-up time. They also enable the performance of additional procedures and reducesession time. The ordering and stock control of single-use products used in surgical interven-tions also require the attention of nursing staff, which are in increasingly short supply. Thebest-run operating department works to avoid unnecessary time, indirect costs, inconven-ience and stress involved in preparing for a procedure.

G o v e r n m e n t R e g u l a t i o n s t o A d v a n c e S i n g l e U s e

P r o d u c t s

The Medical Device Directive of 1993 has been a very important development in the Euro-pean healthcare sector. A series of standards are being developed, categorising medicaldevices according to their criticality in terms of patient protection, providing standard testsand criteria for products to be introduced in the European market with CE (ConformitéEuropéenne) marking. One of these standards is likely to stimulate the demand for single-useproducts, thereby increasing the need for custom procedure trays.

The European Standard prEN 13795-1 addresses surgical drapes and gowns. This standardcovers infection control aspects in the form of essential properties for reusable and single-usedrapes and clothing. The requirements of this standard have to be fulfilled when products areintroduced and, for reusable products, after each reprocessing. This acts as a major driver forCPT, since it has all components which are pre sterilized and packed which single use prod-ucts pertaining to that particular procedure or surgery.

#M16F-54 © 2007 Frost & Sullivan www.frost.com August 2007 4-6

C o n s t a n t R i s e i n t h e N u m b e r o f S u r g e r i e s

Europe has a higher share of aging population than any other continent. Almost 20 per cent

of Europe's population is aged above 55. The average life expectancy is also increasing in

Europe. Men at the age of 60 can expect to live for an additional 17 years and women can

expect another 22 years of life. Europe's aging profile has a significant impact on the number

of surgeries that could be performed, which acts as a market opportunity for custom proce-

dure trays. It is proven that the elderly account for a disproportionate amount of surgical

procedures. This impacts the operating and ophthalmic CPT market, since the number of

cataract surgeries have raised in Europe.

C o s t C o n t r o l M o d e l

Decision-making process becomes a lot easier through the implementation of CPT. It enables

in comparing component costs (linen and other operating room components), operating

theatre and clinical time costs (picking time/opening and preparation time), CSSD

(Central Sterile Supply Department) savings, procurement and inventory savings (order/

invoice processing/inventory holding/internal logistics), waste cost and potential revenue

increase due to operating room efficiency.

Market Restraints

Figure 4-2 show the market restraints ranked in order of impact for the European custom

procedure trays market from 2007 to 2013.

Source: Frost & Sullivan

F i g u r e 4 - 2

Custom Procedure Trays Market: Market Restraints Ranked in Order of Impact (Europe),

2007-2013

Rank Restraint 1-2 Years 3-4 Years 5-7 Years

1 Pricing pressure High Medium Low

2 Growth of new procedures Medium Medium High

3 Brand allegiance Medium Medium Medium

4 Lack of standardization amongst geographical regions Medium Medium Medium

5 Customer perception Medium Medium Low

6 Long-term contracts for medical device components Low Low Low

#M16F-54 © 2007 Frost & Sullivan www.frost.com August 2007 4-7

Frost & Sullivan expects the magnitude of these restraints to be outweighed by the drivers,

thus resulting in significant market growth.

P r i c i n g P r e s s u r e

Similar to other growing markets, the CPT market also faces intense price wars among

participants to increase market penetration and market share.The CPT market being highly

fragmented, many companies face pressure due to the presence and superior sales volumes of

leading companies. The market leaders have admirable bargaining powers, which pressurise

the smaller firms.

G r o w t h o f N e w P r o c e d u r e s

Most of the surgeries currently have an alternative less invasive treatment available for sake

of patients' convenience. Minimally invasive surgery is a new kind of surgery, which is

becoming increasingly common. In addition, most ophthalmic procedures are being done

using laser rays, which might potentially replace cataract surgeries. Henceforth, the usage of

procedure kits for such surgeries will be minimum, which poses a threat to the CPT market.

B r a n d A l l e g i a n c e

Convincing doctors to adapt new products or techniques. Usually, they are very particular

about the type and brand of product used for a procedure. CPT, which has a combination of

different components and of various brands.

Although it is rare, brand loyalty can even exist for very 'simple' products such as syringes

and swabs, wherein price is the usual barometer. For example, a few surgeons have even been

known to specify either a Terumo or Becton Dickinson syringe. This is a major barrier for

CPT companies in their attempt to attract hospitals.Hence, existing companies in this market

and potential entrants need to spend a lot of time and resources on the hospital and theatre

staff to exactly understand their needs and specifications to tailor make their product

accordingly.

#M16F-54 © 2007 Frost & Sullivan www.frost.com August 2007 4-8

L a c k o f S t a n d a r d i z a t i o n A m o n g s t G e o g r a p h i c a l R e g i o n s

Key differences exist in the healthcare budgets and purchasing patterns of medical compo-

nents among various countries within Europe. It is important for companies to understand

the peculiarities of the different healthcare systems with regard to all types of healthcare

products. However, this is a major issue to companies wishing to sell custom procedure trays,

as end users are involved in a complicated purchasing decision-making process.

C u s t o m e r P e r c e p t i o n

Very appropriately communicating the benefits of using a CPT becomes a big challenge for

companies who are in this market. Usually in hospitals, traditions are very deep rooted. So it

is only sufficient to brief the theatre staff and the doctors about the benefits of procedure

packs. The purchasing department also needs to be clearly elaborated upon the cost benefit

model upon uptake of CPT this is mainly because the purchasers and theatre staff have

different priorities. The purchasers are the cost controllers and very seldom understand the

workflow of the nurses in the operating theatres, which are constantly under intense time

pressure. It is crucial that the doctors, the nurse management and the administrative manage-

ment work closely with each other on the decision making process.

A detailed cost benefit model needs to be drawn up by the CPT company, explaining in detail

comparing the current costs involved in the hospital and cost saving after concept of Custom

Procedure Packs would be implemented. Currently hospitals work on a budget, and it also

becomes very essential for CPT companies to price the product competitively.

L o n g - t e r m C o n t r a c t s f o r M e d i c a l D e v i c e C o m p o n e n t s

The buying process of healthcare institutions in most European countries is tender based and

these contracts are usually meant for long terms. Particularly, supply of single-use products

are procured on a long-term tender basis, which acts as a restraint for new entrants that

prefer to bid amongst other competitors for tenders. In addition, since these single-use prod-

ucts are the key components of CPTs, it will result in the inability of hospitals to adopt the

benefits of CPT without a significant financial penalty.

Market Forecasts

Figure 4-3 and Chart 4.2 present the revenue forecasts for the European custom procedure

trays market from 2003 to 2013.

#M16F-54 © 2007 Frost & Sullivan www.frost.com August 2007 4-9

Note: All figures are rounded; the base year is 2006. Source: Frost & Sullivan

C h a r t 4 . 2

Custom Procedure Trays Market: Revenue Forecasts (Europe), 2003-2013

Note: All figures are rounded; the base year is 2006. Source: Frost & Sullivan

F i g u r e 4 - 3

Custom Procedure Trays Market: Revenue Forecasts (Europe), 2003-2013

Revenue

Revenues Growth Rate

Year ($ Million) (%)

2003 244.3 ---

2004 279.5 14.4

2005 323.6 15.8

2006 380.4 17.5

2007 452.2 18.9

2008 543.3 20.1

2009 660.1 21.5

2010 810.2 22.7

2011 1,003.2 23.8

2012 1,253.6 25.0

2013 1,580.5 26.1

Compound Annual Growth Rate (2006-2013): 22.6%

0

200

400

600

800

1000

1200

1400

1600

1800

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Year

Rev

enue

s ($

Mill

ion)

0

5

10

15

20

25

30

Gro

wth

Rat

e (%

)

Revenues ($ Million) Growth Rate (%)

#M16F-54 © 2007 Frost & Sullivan www.frost.com August 2007 4-10

The market amounted to $380.4 million in 2006. This has grown by 30.2 percent in

2006 experiencing a growth rate of 17.5 per cent over 2005. The largest markets at present

are Germany, Italy and Spain. However, most of the European countries have witnessed

significant growth since 2003, with further growth expected during the forecast period.

Pricing Trends

The total number of procedures in Europe, including angiographies, amounted to

44.7 million in 2006. The number of angiographies have reduced since 2004 due to the

advent of 64 slice CT scanning 64 slice CT is a radiological procedure that produces the 3D

image of the heart, and is less invasive as well.The number of total procedures per

100,000 people is significantly high in countries such as Germany, United Kingdom, Italy and

France, and is relatively lower in Spain and the Scandinavian countries.

Figure 4-4 shows the pricing trends of the European custom procedure trays market from

2003 to 2013.

Note: All figures are rounded; the base year is 2006. Source: Frost & Sullivan

F i g u r e 4 - 4

Custom Procedure Trays Market: Pricing Trends (Europe), 2003-2013

Average Price Price Change

Year ($) (%)

2003 39 ---

2004 40 2

2005 42 5

2006 43 2

2007 43 0

2008 44 2

2009 45 2

2010 46 2

2011 47 2

2012 46 (2)

2013 46 0

#M16F-54 © 2007 Frost & Sullivan www.frost.com August 2007 4-11

The average selling price in 2006 was $43, increasing from $39 in 2003. Prices are slightly

higher in certain countries. For example, prices in United Kingdom, the Netherlands and

Scandinavia are higher than Spain, Italy, France and Belgium. Overall, the average price has

remained relatively stable, despite slight reductions in the prices of angiography and

ophthalmic procedure trays. However, the overall average price is likely to strengthen slightly

over the coming years due to the increasing penetration of higher-valued OR CPTs and the

realisation by market participants that price competition cannot be stressed upon if a viable

business model is to be maintained.

Trends by Geographic Region

Figure 4-5 and Chart 4.3 provide the per cent of revenues by geographic region for the Euro-

pean custom procedure trays market from 2003 to 2013.

Key: Benelux = Belgium, the Netherlands and Luxembourg Scandinavia = Norway, Sweden, Finland and Denmark

Note: All figures are rounded; the base year is 2006. Source: Frost & Sullivan

F i g u r e 4 - 5

Custom Procedure Trays Market: Per cent of Revenues by Geographic Region (Europe),

2003-2013

Germany France United Kingdom Italy and Spain Benelux and Scandinavia

Year (%) (%) (%) (%) (%)

2003 32.5 15.9 23.2 14.5 13.8

2004 33.2 15.8 22.8 15.0 13.2

2005 34.1 15.5 22.4 15.6 12.4

2006 35.2 15.2 21.9 16.0 11.6

2007 36.5 14.9 21.4 16.4 10.8

2008 37.9 14.5 20.9 16.7 10.0

2009 39.5 14.0 20.3 16.9 9.3

2010 41.0 13.6 19.8 17.1 8.5

2011 42.5 13.2 19.2 17.3 7.8

2012 44.1 12.8 18.7 17.3 7.1

2013 45.7 12.4 18.1 17.3 6.5

#M16F-54 © 2007 Frost & Sullivan www.frost.com August 2007 4-12

C h a r t 4 . 3

Custom Procedure Trays Market: Per cent of Revenues by Geographic Region (Europe),

2003-2013

Note: All figures are rounded; the base year is 2006. Source: Frost & Sullivan

Germany represented the largest market, accounting for 35.2 per cent of the total European

revenues in 2006. This was due to two reasons. Firstly, it is the market with the largest

overall market potential, since it experiences the highest number of surgical procedures in

Europe. Secondly, it has a high CPT penetration rate. While this rate lags behind the

United Kingdom and Holland in the OR segment, it has increased exponentially in the anaes-

thesia and ophthalmic segments. The United Kingdom account for the second largest market

in Europe. This is because of the relatively high number of procedures and participants

existent in UK.

The proportion of the market accounted for by France is high due to the population, high

rate of surgery and sophistication of the healthcare system. The Benelux and Scandinavian

market accounted for 11.6 per cent of total European market revenues in 2006. This is rela-

tively high, given that the population of Belgium and Holland account for only 7.5 per cent

of Europe's population. CPT companies like Kimal increased their market potential in the

Netherlands due to home-town advantage.

Trends by Product Type

Figure 4-6 and Chart 4.4 show the per cent of revenues by product type for the European

custom procedure trays market from 2003 to 2013.

0%

20%

40%

60%

80%

100%

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Benelux and Scandinavia

Italy and Spain

United Kingdom

France

Germany

#M16F-54 © 2007 Frost & Sullivan www.frost.com August 2007 4-13

Key: OR = Operating Room includes Orthopedic surgery, Cardiac surgery, General surgery, Neurosurgery, ENT/Maxillo facial surgery, Obstetrics/Gynecology

Note: All figures are rounded; the base year is 2006. Source: Frost & Sullivan

C h a r t 4 . 4

Custom Procedure Trays Market: Per cent of Revenues by Product Type (Europe), 2003-2013

Note: All figures are rounded; the base year is 2006. Source: Frost & Sullivan

The OR segment accounted for the largest revenue, valuing at 46.8 per cent in 2006. This is

due to the fact that this segment includes all the different types of surgery.

F i g u r e 4 - 6

Custom Procedure Trays Market: Per cent of Revenues by Product Type (Europe), 2003-2013

Angiography Ophthalmology OR Anaesthesiology

Year (%) (%) (%) (%)

2003 32.1 31.8 33.3 2.8

2004 30.2 29.6 37.5 2.6

2005 28.2 27.4 42.0 2.4

2006 26.0 25.0 46.8 2.2

2007 23.8 22.6 51.7 2.0

2008 21.5 20.2 56.5 1.8

2009 19.3 17.9 61.2 1.6

2010 17.2 15.7 65.7 1.4

2011 15.1 13.7 70.0 1.2

2012 13.2 11.8 74.0 1.1

2013 11.4 10.0 77.6 0.9

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Anaesthesiology

Operating Room

Ophthalmology

Angiography

#M16F-54 © 2007 Frost & Sullivan www.frost.com August 2007 4-14

The penetration of CPT is not as high in the angiography and ophthalmology segments due to

the lesser number of procedures. The angiography segment contributed 26.0 per cent and the

ophthalmology segment contributed 25.0 per cent to the total market during the base year.

Anaesthesia CPT, market is a relatively new concept of packaging which has been recently

introduced, accounted for 2.2 per cent of the total CPT market in 2006. The trends vary from

one region to another. For example, CPT trays have the maximum penetration in angiog-

raphy procedures in Germany since it has the highest number of cardiovascular cases,

whereas in countries such as the United Kingdom, the OR segment is more popular than

angiography and ophthalmology.

Competitive Structure

Figure 4-7 shows the competitive structure of the European custom procedure trays market

in 2006.

Source: Frost & Sullivan

F i g u r e 4 - 7

Custom Procedure Trays Market: Competitive Structure (Europe), 2006

Number of Companies in the Market 32

Tiers of Competition Tier 1: Alcon, Cardinal,KimalTier 2: Angiokard, PVB, Medex Medical, B BraunMedica Europe, Hartmann, Becton Dickinson, Bausch & Lomb, Rocialle, Pennine,Lohmann & RauscherTier 3: Domilens, Cordis, AMO, Sengewald, 3M, Kimberly Clark, Molnlycke, Meditalia, Deroyal, Medtronic, Caledonian Medical,Beldico, 3S Medical, Hydrex, JP Medical, Allergan, Ioltech, Interster

Notable Acquisitions, Mergers 2001—Molnlycke acquired J & J's Barrier brand2002—Sengewald acquired MSP Schmeiser2002—In Health Group took over Allegiance-name changed to Cardinal2002—In Health Group acquires Rocialle2003—Maxxim an independent European company2004—Name changed to Medica Europe

Key End-user Groups SurgeonsSurgical staffPurchasing department

Competitive Factors Effective supply chain management, customized packaging solutions

#M16F-54 © 2007 Frost & Sullivan www.frost.com August 2007 4-15

There were 32 active participants in the market in 2006. There were three tiers of competi-tion and Alcon, Cardinal and Kimal were the tier 1 participants.

Alcon is the leader in the supply of ophthalmic trays throughout Europe, having a consider-able lead over the other vendors. However, in the overall market, the share of Alcon is muchlower, as the potential of the ophthalmology segment is smaller than the other segments.Cardinal is the market leader in both angiography and OR trays. Kimal holds the secondposition in the angiography CPT market.

Tier 2 includes Angiokard, B Braun and Medex Medical in the angiography segment,

Paul Hartmann, Pennine and Lohmann & Rauscher in the OR segment, Becton Dickinson

and Bausch & Lomb in the ophthalmology segment and participants such as In health Group

and Medica Europe are present in more than one segment.

A n g i o g r a p h y C P T M a r k e t f o r E u r o p e

Market Overview

Cardiovascular (CV) diseases are a major source of morbidity and mortality in western Euro-

pean countries. There is no epidemiological information available on the impact of CV

morbidity and mortality at the entire European level, but in the United Kingdom for instance,

the mortality due to CV diseases in men under 65 is 42 per cent, compared to 32 per cent for

cancer (British Heart Foundation, www.dphpc.ox.ac.uk/bhfhprg/stats/). Hence, CV thera-

peutic classes represent approximately one quarter of the worldwide pharmaceutical sales.

Currently, coronary angiography is the gold standard to diagnose coronary artery disease and

the basis to perform percutaneous coronary intervention. Angioplasty, also known as balloon

angioplasty and Percutaneous Transluminal Angioplasty (PCTA), is a medical procedure used

to open narrowed or clogged blood vessels of the heart. A thin balloon is threaded through a

blood vessel in the groin or arm into a heart (coronary) artery. The balloon is inflated to

compress the blockage and stretch the artery open.

This segment is different from the other segments as this procedure is non-interventional. It

includes radiography procedures, which are also performed in the cathlab. The main compo-

nent in the CPT for angiography is the fluid management system, which is created by a

Boston Scientific company called North American Medical Instrument Corporation

(NAMIC). Various kit packing companies have tie-ups with NAMIC in different regions.

There exists a high level of standardisation in cardiac trays, allowing companies to produce a

few standard kits in addition to the customised kits. Specialist companies such as Cordis,

Kimal, BBraun and Medex Medical are quite strong in this market.

#M16F-54 © 2007 Frost & Sullivan www.frost.com August 2007 4-16

Market Engineering Measurements

Chart 4.5 presents the market engineering measurements for the European angiography CPT

market in 2006.

C h a r t 4 . 5

Angiography CPT Market: Market Engineering Measurements (Europe), 2006

Market Engineering Drives Market

Strategy and Planning

MarketEngineer

ChallengeIdentification

MarketResearch

MarketEngineering

System

Implementation

MarketPlanning

MarketStrategy

Note: All figures are rounded. Source: Frost & Sullivan

Market Forecasts

Figure 4-8 and Chart 4.6 provide the revenue forecasts for the European angiography CPT

market from 2003 to 2013.

Measurement Name Measurement Trend

Market age Growth stage ---

Market revenues $99.0 million Increasing

Potential revenues (maximum future market size) $180.3 million Increasing

Base year market growth rate 8.5% Increasing

Compound annual growth rate 8.9% ---

Active participants 19 Stable

Average price $50 Increasing

#M16F-54 © 2007 Frost & Sullivan www.frost.com August 2007 4-17

Note: All figures are rounded; the base year is 2006. Source: Frost & Sullivan

C h a r t 4 . 6

Angiography CPT Market: Revenue Forecasts (Europe), 2003-2013

Note: All figures are rounded; the base year is 2006. Source: Frost & Sullivan

The European angiography CPT market was worth $99.0 million in 2006. This segment,

which has grown by 15.6 per cent since 2003, is currently reaching maturity.

F i g u r e 4 - 8

Angiography CPT Market: Revenue Forecasts (Europe), 2003-2013

Revenue

Revenues Growth Rate

Year ($ Million) (%)

2003 78.5 ---

2004 84.5 7.6

2005 91.3 8.0

2006 99.0 8.5

2007 107.5 8.6

2008 117.0 8.8

2009 127.7 9.1

2010 139.5 9.2

2011 152.0 8.9

2012 165.5 8.9

2013 180.3 8.9

Compound Annual Growth Rate (2006-2013): 8.9%

0

20

40

60

80

100

120

140

160

180

200

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Year

Rev

enue

s ($

Mill

ion)

0

1

2

3

4

5

6

7

8

9

10

Gro

wth

Rat

e (%

)

Revenues ($ Million) Growth Rate (%)

#M16F-54 © 2007 Frost & Sullivan www.frost.com August 2007 4-18

The German market has an extremely high number of angiography procedures and highpenetration of angiography CPTs. Hence, the country accounts for almost half of the totalEuropean angiography CPT market revenues. It is the largest market in Europe, despiteprices being quite low due to the competition resulting from a large number of participants.Nevertheless, the market for angiographies is expected to decline due to technologicaladvances.

Pricing Trends

The average selling price in 2006 was $50. This has increased from $35.01 in 1998, andprices are likely to continue to increase, but at a lesser rate of approximately 2 per cent peryear. The high number of competitors in the European angiography CPT market creates asignificant degree of price competition. Although price per unit increases, the number ofangiographies are likely to reduce due to the advent of new technologies like 64 slice CTscan.

Trends by Geographic Region

Figure 4-9 and Chart 4.7 provide the per cent of revenues by geographic region for the Euro-pean angiography CPT market from 2003 to 2013.

Key: Benelux = Belgium, the Netherlands and Luxembourg Scandinavia = Norway, Sweden, Finland and Denmark

Note: All figures are rounded; the base year is 2006. Source: Frost & Sullivan

F i g u r e 4 - 9

Angiography CPT Market: Per cent of Revenues by Geographic Region (Europe), 2003-2013

Germany France United Kingdom Italy and Spain Benelux and Scandinavia

Year (%) (%) (%) (%) (%)

2003 35.7 22.8 28.0 2.5 10.7

2004 34.1 23.9 27.8 2.6 10.6

2005 34.2 24.9 27.6 2.7 10.4

2006 33.5 25.1 27.3 2.8 10.3

2007 32.8 27.0 27.0 2.9 10.1

2008 32.0 28.2 26.7 3.0 9.9

2009 31.3 29.3 26.4 3.1 9.7

2010 30.6 30.5 26.0 3.2 9.5

2011 29.8 31.7 25.7 3.3 9.4

2012 28.1 32.9 25.3 3.4 9.3

2013 28.1 34.2 24.8 3.5 9.2

#M16F-54 © 2007 Frost & Sullivan www.frost.com August 2007 4-19

C h a r t 4 . 7

Angiography CPT Market: Per cent of Revenues by Geographic Region (Europe), 2003-2013

Note: All figures are rounded; the base year is 2006. Source: Frost & Sullivan

Germany represents an extremely large proportion of the European revenues. In Germany

alone, the total number of angiographic procedures rose by 45 per cent from 1995 to 2000,

while the fraction of interventional procedures remained low at about 30 per cent.

[Z. Kardiol. 90 (2001) 665].

This country leads the way in terms of cardiology, creating future market potential. Further-

more, the penetration of CPT is also very high in the German market, creating a large market

size. This is despite the relatively low prices in Germany caused by a high level of

competition.

France is the country with the second largest potential market. However, the penetration of

CPT for angiography in France is slightly lower than the European average. This is the reason

for the country accounting for 25.96 per cent of the European revenues. Belgium and

Norway follow the same trend as that of Germany, witnessing an above average number of

procedures and a relatively high level of penetration.

Market Share Analysis

Figure 4-10 and Chart 4.8 show the company market share by revenues for the European

angiography CPT market during 2006.

0%

20%

40%

60%

80%

100%

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Benelux and Scandinavia

Italy and Spain

United Kingdom

France

Germany

#M16F-54 © 2007 Frost & Sullivan www.frost.com August 2007 4-20

Note: Others include Medtronic, Caledonian Medical, Beldico, 3S Medical, Hydrex and JP Medical

Note: All figures are rounded; the base year is 2006. Source: Frost & Sullivan

C h a r t 4 . 8

Angiography CPT Market: Company Market Share by Revenues (Europe), 2006

Note: All figures are rounded; the base year is 2006. Source: Frost & Sullivan

F i g u r e 4 - 1 0

Angiography CPT Market: Company Market Share by Revenues (Europe), 2006

Company Market Share (%)

Cardinal 24.4

Kimal 22.4

B Braun 16.8

Angiokard 10.2

Medica Europe 8.0

Vygon 5.0

In Health Group (Rocialle) 3.9

Deroyal 2.3

Others 7.0

TOTAL 100.0

B Braun16.8%

Kimal22.4%

Angiokard10.2%

Deroyal2.3%

Others7.0%

Medica Europe8.0%

Cardinal24.4%

Vygon5.0%

In Health Group (Rocialle)3.9%

#M16F-54 © 2007 Frost & Sullivan www.frost.com August 2007 4-21

There is no dominant market participant in the European angiography CPT market. Most

countries in Europe have domestic participants in this segment.

However, none of the companies have managed to create a strong foothold across all the

major European countries.

Cardinal is the key participant, with 24.4 per cent market share in 2006. The company has

its European production headquartered in France. The capacity of this production facility is

currently being expanded. The main competitive advantage for Cardinal is its very strong

brand name in drapes and gowns.

Kimal followed closely with a share of 22.4 per cent in 2006. Kimal is a UK company,

focusing mainly on the cardiology and radiology area, having angiography CPT sales in a

number of European countries. The company has been very successful in the

United Kingdom, wherein it is the market leader. It has also developed an extremely domi-

nant position in the Scandinavian countries and a good position in Italy. This company has

grown substantially since 2001 due to persistent campaigning and partnering. Kimal also has

a tie-up with Boston Scientific for its NAMIC fluid management systems in the

United Kingdom, Scandinavia, Portugal, Holland, Norway, Sweden, Denmark, Austria,

Hungary and a few eastern European countries.

B Braun had a market share of 16.8 per cent in 2006. It has a relatively strong position in the

German market, has achieved sales in Scandinavia and is building a market presence in the

United Kingdom.

Angiokard is also strong in Germany, but has not yet achieved significant sales outside its

home country.

Medica Europe had a market share of 8.0 per cent in 2006. Maxxim Medical, Europe had a

management buy-out in April 2003 and it became an independent European company head-

quartered in Holland. In May 2004, it acquired the name Medica Europe. Medica was the

former name of the company before it was bought by Maxxim, USA, in 1995. Maxxim has

plans of becoming a Pan European vendor and has its assembling unit located in the

Netherlands.

Vygon had a market share of 5.0 per cent and is the market leader in France.

#M16F-54 © 2007 Frost & Sullivan www.frost.com August 2007 4-22

O p h t h a l m i c C P T M a r k e t f o r E u r o p e

Market Overview

Cataract surgery is the most common type of eye surgery. It accounts for approximately

two-thirds of all the eye procedures. In many countries, it is the highest volume surgical

procedure performed, which makes it attractive for the sale of procedure trays. The following

three factors of the ophthalmic market are critical to the likely uptake of CPT:

! High volume of the number of procedures performed

! High standardisation (the procedure is subject to very little variation)

! High propensity to use single-use products (particularly true for eye surgery because of

the risk of infection)

The ophthalmic CPT segment has specific market participants that focus on ophthalmology,

offering a wide range of ophthalmology products. This is one of the reasons that it has been