experience / expertise / excellence the changing landscape …€¦ · · 2017-06-01experience /...

TRANSCRIPT

1 Experience / Expertise / Excellence www.plgconsulting.com

Experience / Expertise / Excellence

THE CHANGING LANDSCAPE FOR ENERGY SHALE OIL & GAS OUTLOOK

Prepared for

Southwest Association of Rail Shippers October 8, 2015 – Dallas, TX Graham Brisben CEO, PLG Consulting

2 Experience / Expertise / Excellence www.plgconsulting.com

Experience ! Delivering value to over 200

clients since 2001

! Real-world, industry veterans

! Logistics, engineering & supply chain experts with operational experience

Core Expertise ! Bulk Logistics

! Freight Rail

! Logistics Infrastructure Design

! Energy & Chemical Markets

! Investment Advisory and Corporate Development

Partial Client List

Services ! Diagnostic assessments &

optimization

! Supply chain design & operational improvement

! Investment strategy, target identification, due diligence, post-transactional support

! Crude by rail (CBR) and rail tank car (RTC) forecasts

! Independent technology assessment & implementation

! Hazmat training, auditing & risk assessment

THE CHANGING LANDSCAPE FOR ENERGY: SHALE OIL & GAS OUTLOOK

3 Experience / Expertise / Excellence www.plgconsulting.com

Source: EIA, May 2014

US Shale

Source: CAPP, About Oil Sands

Western Canadian (WC) Oil Sands

Source: www.epmag.com

SAGD Horizontal Drilling & Hydraulic Fracturing

Source: Marathon, February 2014

“MOORE’S LAW” Exponential advances in technology, resulting in:

-Declining costs

-Surging production of natural gas,

crude oil, and HGLs

4 Experience / Expertise / Excellence www.plgconsulting.com

MMb/d B

cf/d

0

10

20

30

40

50

60

70

80

90

Jan-

2011

M

ar-2

011

May

-201

1 Ju

l-201

1 S

ep-2

011

Nov

-201

1 Ja

n-20

12

Mar

-201

2 M

ay-2

012

Jul-2

012

Sep

-201

2 N

ov-2

012

Jan-

2013

M

ar-2

013

May

-201

3 Ju

l-201

3 S

ep-2

013

Nov

-201

3 Ja

n-20

14

Mar

-201

4 M

ay-2

014

Jul-2

014

Sep

-201

4 N

ov-2

014

Jan-

2015

M

ar-2

015

May

-201

5 Ju

l-201

5 S

ep-2

015

Nov

-201

5 Ja

n-20

16

Mar

-201

6 M

ay-2

016

Jul-2

016

Sep

-201

6 N

ov-2

016

0

2

4

6

8

10

12

Domestic Crude, HGLs, and Dry Gas Production

Crude Oil Production (MMb/d) HGL Production from Processing Plants (MMb/d) Dry Gas Production (Bcf/d)

Source: EIA, October 2015

5 Experience / Expertise / Excellence www.plgconsulting.com

THE CHANGING LANDSCAPE FOR ENERGY: SHALE OIL & GAS OUTLOOK

Source: Petrochemical Update, September 2015

US Oil Production 1950-2015 Canadian Oil Sands Production and Forecast

Source: BMO Capital Markets, September 2015

6 Experience / Expertise / Excellence www.plgconsulting.com

Source: IEA, August 2015

Historical Front Month Oil Futures Prices

Source: EIA STEO, September 2015

U.S. Natural Gas Prices and Storage

Source: EIA STEO, October 2015

7 Experience / Expertise / Excellence www.plgconsulting.com

Pullback in Drilling Rigs, Well Completion

Retrenchment began in earnest 1Q 2015

! Rig count decline of 50% since beginning of the year

! Eliminated exploratory drilling – R&D budgets down by 30-50% for 2015

However, productivity advances from 2013-2014 continue to support production

! Higher yields per well ! Drilling “sweet spots” only ! Focusing on perfecting latest,

most productive fracking techniques

Source: Bentek Energy, September 2015

8 Experience / Expertise / Excellence www.plgconsulting.com

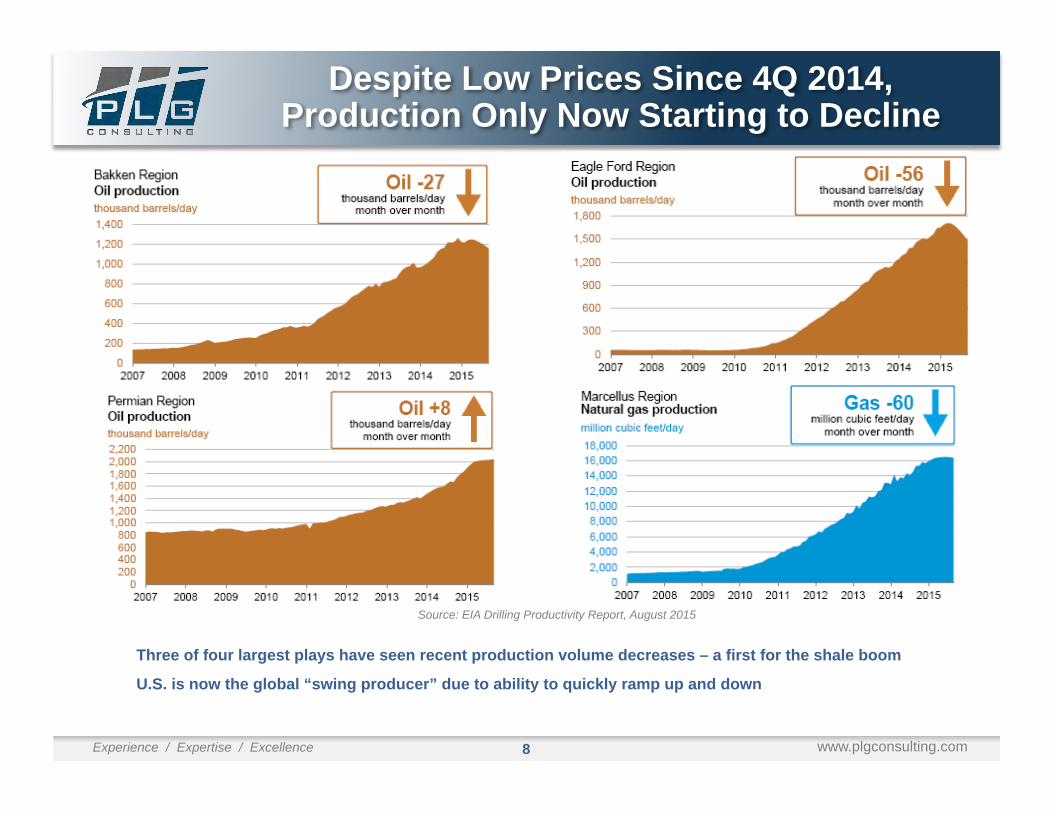

Despite Low Prices Since 4Q 2014, Production Only Now Starting to Decline

Three of four largest plays have seen recent production volume decreases – a first for the shale boom

U.S. is now the global “swing producer” due to ability to quickly ramp up and down

Source: EIA Drilling Productivity Report, August 2015

9 Experience / Expertise / Excellence www.plgconsulting.com

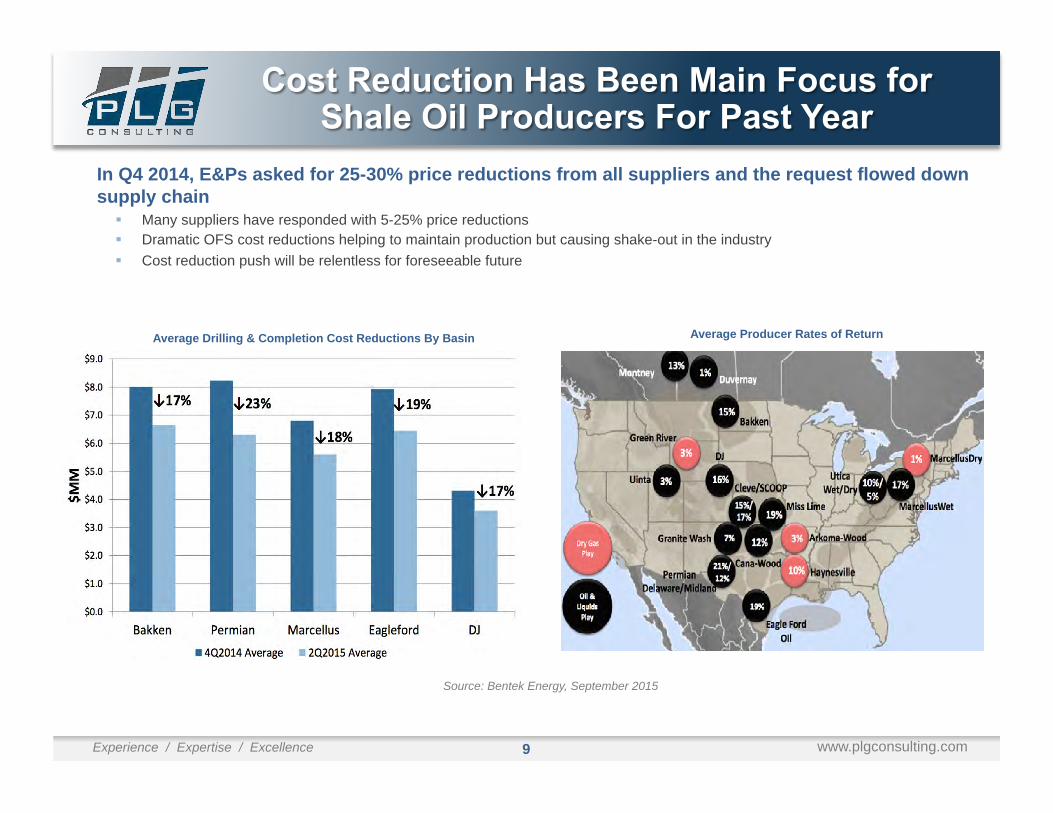

In Q4 2014, E&Ps asked for 25-30% price reductions from all suppliers and the request flowed down supply chain

! Many suppliers have responded with 5-25% price reductions ! Dramatic OFS cost reductions helping to maintain production but causing shake-out in the industry ! Cost reduction push will be relentless for foreseeable future

Average Drilling & Completion Cost Reductions By Basin

Source: Bentek Energy, September 2015

Average Producer Rates of Return

10 Experience / Expertise / Excellence www.plgconsulting.com

Feedstock (Ethane)

Byproduct (Condensate)

Home Heating (Propane)

Other Fuels

Other Fuels

Gasoline

Gas

NGLs

Crude

Proppants

OCTG

Chemicals

Water

Cement

Generation

Process Feedstocks

All Manufacturing

Steel

Fertilizer (Ammonia)

Methanol

Chemicals

Petroleum Products

Petrochemicals

Inputs Wellhead Direct Output Thermal Fuels Raw Materials

THE NEXT WAVE Manufacturing renaissance in the US based on

abundant, low cost energy and feedstocks

IMPACTS TO-DATE INCLUDE Dramatic reduction in crude imports, lower electricity costs, lower gasoline prices, increased refined products exports

Downstream Products

Significant rail impacts noted in red

11 Experience / Expertise / Excellence www.plgconsulting.com

0

500

1,000

1,500

2,000

2,500

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

U.S. QUARTERLY CARLOADS ORIGINATED FOR INDUSTRIAL SAND AND U.S. LAND RIGS

U.S. Quarterly Carloads Originated for Industrial Sand (STCC 14413)

U.S. Land Rigs

Shale Gas Boom

Rig Shift from Gas to Liquids

Shale Oil Boom

Oil Price Collapse

Note: PLG utilizes rail car origination loads as the best way to track sand industry volume trends

High Intensity Fracking

Carloads Rigs

Source: Baker Hughes and

Surface Transportation

Board, September

2015

12 Experience / Expertise / Excellence www.plgconsulting.com

Price Pressure Impacts on Sand Sourcing and Transportation

Source: NavPort and Headwaters MB, September 2015

Traditional source areas for Northern White (WI, MN, IL) began to lose market share in 2014

! Change in fracking techniques called for more 100 mesh from IL, MO

! New source areas allowed for barge shipments and more single-line rail hauls

Price pressure encouraging more mines closer to shale plays

! Logistics is by far the biggest cost

! Rail pricing has not followed same cost reductions as other parts of the supply chain

Expect continued innovation in the field to enable lower cost proppants

13 Experience / Expertise / Excellence www.plgconsulting.com

Source: NavPort and Headwaters MB, September 2015

Frac sand industry volume is close to bottoming out…near term volume recovery is unlikely

! Overall volume likely down >30% since 2014 peak

! Excessive capacity throughout each link in the supply chain

! Consolidation among players is expected

Sand and all services in supply chain remain under heavy price pressure

! 20-25% price reductions are “normal” in many areas

Logistics cost are >2/3 of the total delivered cost of sand

! Heavy focus on reducing rail costs

Small covered hopper market in a state of disarray

Impact of Price Collapse on Frac Sand Demand

14 Experience / Expertise / Excellence www.plgconsulting.com

Current market conditions ! Lots of cars in storage starting in Q4 2014

! Minimal outright cancellations of car orders – very difficult contractually; some moving out of new-build delivery schedules

! New-build production schedules are full through 2016 – many new cars direct to storage

Cement consumption is expected to grow by 8%+ in 2015 ! Cement also utilizes small covered hoppers; small help to the

market - may be build/lease opportunities for cement cars with frac sand downturn

Plastic pellet cars market growing and may allow some small hopper car buyers to shift orders to large covered hopper cars

Major questions surround small covered hopper market after backlog build out in 2016

! Gas market growth slowed by low gas prices resulting in low gas rig count; oil price level will be key driver on future oil rig counts and sand usage

! Frac sand industry consolidation will further rationalize the car market

! Industry will continue to slowly move to more unit trains – improved cycle time reduces car volume requirement

! These negative factors could cause extended difficult market conditions

0

1

2

3

4

5

6

0

10,000

20,000

30,000

40,000

Backlog

Orders

Deliveries

Order/Del'y Ratio

Source: Chicago Freight Car Leasing, RSI, March 2015

Small Cube Hopper Car Orders

15 Experience / Expertise / Excellence www.plgconsulting.com

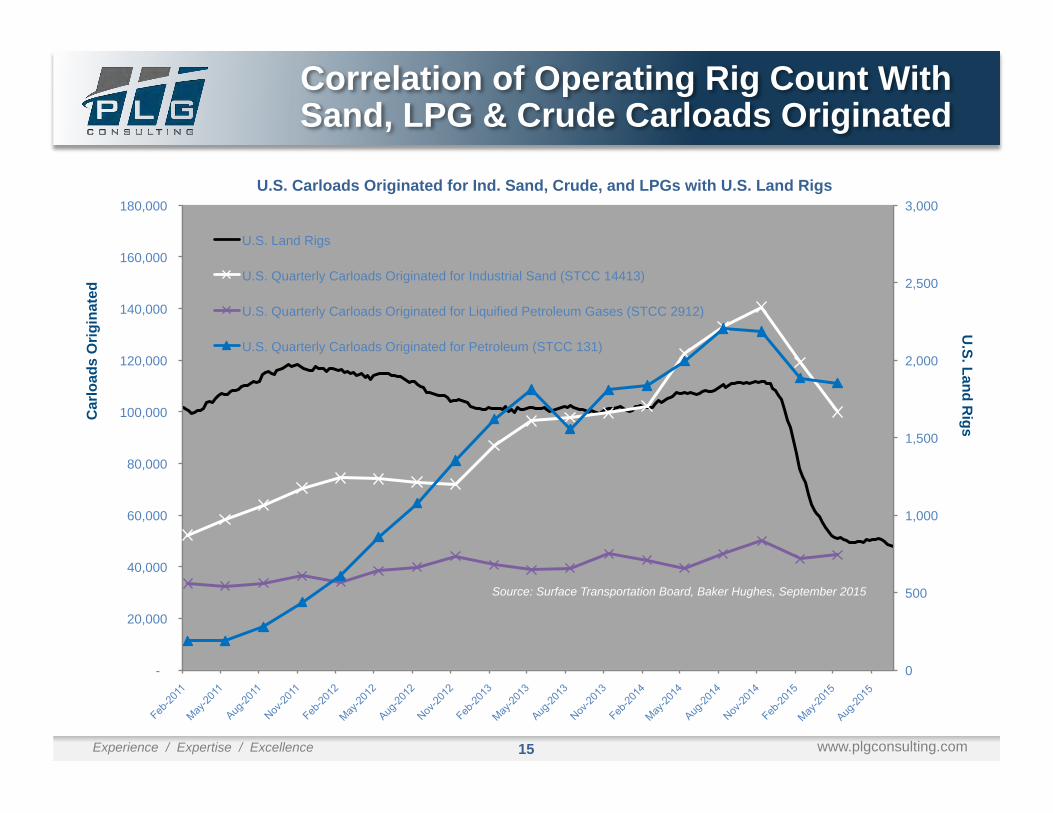

Correlation of Operating Rig Count With Sand, LPG & Crude Carloads Originated

-

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

180,000

0

500

1,000

1,500

2,000

2,500

3,000 U.S. Carloads Originated for Ind. Sand, Crude, and LPGs with U.S. Land Rigs

U.S. Land Rigs

U.S. Quarterly Carloads Originated for Industrial Sand (STCC 14413)

U.S. Quarterly Carloads Originated for Liquified Petroleum Gases (STCC 2912)

U.S. Quarterly Carloads Originated for Petroleum (STCC 131)

Car

load

s O

rigin

ated

U

.S. Land Rigs

Source: Surface Transportation Board, Baker Hughes, September 2015

16 Experience / Expertise / Excellence www.plgconsulting.com

US Crude-by-Rail (CBR) Growth

Source: EIA, March 2015

Bakken play the primary origin area for US CBR ! Rail volumes have flattened since 2014 due to increased

pipeline capacity and smaller Brent-WTI differentials

0

200

400

600

800

1,000

1,200

1,400

Jan-

10

Apr

-10

Jul-1

0 O

ct-1

0 Ja

n-11

A

pr-1

1 Ju

l-11

Oct

-11

Jan-

12

Apr

-12

Jul-1

2 O

ct-1

2 Ja

n-13

A

pr-1

3 Ju

l-13

Oct

-13

Jan-

14

Apr

-14

Jul-1

4 O

ct-1

4 Ja

n-15

A

pr-1

5 Ju

l-15

Oct

-15

Bakken Region Production (kb/d)

PADD 2 Crude by Rail (kb/d)

Source: Data from EIA DPR and EIA Crude Oil by Rail, September, 2015

US Bakken Region Crude Production & PADD 2 CBR (k/bpd)

17 Experience / Expertise / Excellence www.plgconsulting.com

NA Crude Logistics Today

THE CHANGING LANDSCAPE FOR ENERGY: SHALE OIL & GAS OUTLOOK

Light/Sweet

Heavy/Sour

Permian

Bakken

Eagle Ford

Oil Sands

GOM

Light/Sweet

Heavy/Sour

LA Gulf Coast Refiners

TX Gulf Coast Refiners

PADD 3 Demand 8,550

kbpd

Midwest Refiners

PADD 2 Demand 3,575 kbpd

East Coast Refiners

PADD 1 Demand 1,100 kbpd

Pacific Northwest Refiners

California Refiners

PADD 5 Demand

2,525 kbpd

Sources: EIA, PLG analysis (Google Earth)

Rail

Pipeline

Marine

Imports Coming Back?

18 Experience / Expertise / Excellence www.plgconsulting.com

Crude Oil Price Forecast

Crude oil prices forecasted to improve as supply contracts, global demand increases over several years

2015 and 2016 are and will be very challenging

Return of $100/bbl. oil: Don’t hold your breath

“New normal” of $60-$70/bbl. expected to maintain after 2017

Brent-WTI differential expected to continue to be challenging for CBR volumes

THE CHANGING LANDSCAPE FOR ENERGY: SHALE OIL & GAS OUTLOOK

$0

$10

$20

$30

$40

$50

$60

$70

$80

$90

2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

WTI (Cushing) Forecast Pricing Brent - WTI Brent (Sullom Voe) WTI (Cushing)

Source: Turner Mason, October 2015

19 Experience / Expertise / Excellence www.plgconsulting.com

Selected Major Pipeline Projects

Source: CAPP, PLG analysis

Enbridge Mainline

Expansion

Sunoco-ETP Permian Express Phase II

ETP Dakota Access

Enbridge Flanagan South &

Seaway Twin Expansions

Enbridge Line 9

Reversal

Enterprise Midland-to-

Houston

Spectra Platte Twin

KM Trans-Mountain

Expansion & Enbridge Northern Gateway

TransCanada Keystone XL

TransCanada Energy East

20 Experience / Expertise / Excellence www.plgconsulting.com

THE CHANGING LANDSCAPE FOR ENERGY: SHALE OIL & GAS OUTLOOK

CBR share of production expected to decrease due to new pipeline capacity coming online, trend to pipelines in lower price environment, and narrow

WTI-Brent price differentials

-

200

400

600

800

1,000

1,200

1,400

2014 2015 2016 2017 2018 2019 2020

Bakken Takeaway Forecast (kbpd)

Crude by Rail Forecast

Pipeline Forecast

Local Refinery Forecast

Note: Based on $52-64 WTI price

Source: PLG Crude by Rail & Tank Car Forecast, Oct. 2015

Bakken Production and Takeaway Share

21 Experience / Expertise / Excellence www.plgconsulting.com

Western Canada Production and Takeaway Share

THE CHANGING LANDSCAPE FOR ENERGY: SHALE OIL & GAS OUTLOOK

-

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

2014 2015 2016 2017 2018 2019 2020

Western Canada Takeaway Forecast (kbpd)

CBR Forecast

Pipeline Forecast

Local Refinery Forecast

Source: PLG Crude by Rail & Tank Car Forecast, Oct. 2015

Proportion of production handled by rail expected to ramp up through 2016 and then drop back as pipeline capacity starts to develop

Note: Based on $52-64 WTI price

22 Experience / Expertise / Excellence www.plgconsulting.com

North American CBR Forecast Overview

THE CHANGING LANDSCAPE FOR ENERGY: SHALE OIL & GAS OUTLOOK

Source: PLG Crude by Rail & Tank Car Forecast, Oct. 2015

Bakken & Oil Sands are main drivers of CBR volumes

-

100

200

300

400

500

600

700

800

2014 2015 2016 2017 2018 2019 2020

North America Crude by Rail Volume Forecast (kbpd)

Bakken

Western Canada

Niobrara

Permian

Note: Based on $52-64 WTI price

23 Experience / Expertise / Excellence www.plgconsulting.com

DOT 117 Car Specification

Source: AllTranstek LLC

New rules were issued by U.S. DOT on May 1st, and effective July 7, 2015, covering the areas of:

! Tank Car standards for both new and existing cars used in High Hazard Flammable trains

! Enhanced braking systems requirements

! Classification of unrefined petroleum based products

! Rail Routing risk assessments and information

! Rail Network operating speeds

Implementation schedule by car type/commodity that “feathers in” need for new/retrofitted car by up to 10 years vs. NPRM of up to 3 years for PG I and PG II – largely focused on crude and ethanol

Electronically Controlled Pneumatic (“ECP”) braking system requirement for HHFUTs is most contentious area of ruling

U.S. and Canada rules are largely harmonized

Retrofit standard is less than new standard (7/16” shell for retrofit vs. 9/16” shell for new)

2Q 2015 tank car orders down 29% vs. 1Q 2015 and 70% vs. 2Q 2014

Current backlog at ~46,000 cars, down 11% since start of year

Lease rates between $500-$1,000 per car per month based on spec

Similar to small cube hoppers, significant oversupply exists with some new builds going straight into storage

More cars expected to be scrapped than retrofitted ! Soft market conditions and regulatory grace period resulting in

“wait and see” approach

! Backlog of cars will be built to new 117 standard

Tank Car Regulatory and Market Dynamics

24 Experience / Expertise / Excellence www.plgconsulting.com

Regulation & Shale Gas Supply Contributing to Reduced Coal Demand

Source: EIA and Carbon Brief, September 2015

Source: Petrochemical Update, September 2015

US Shale Gas Production

25 Experience / Expertise / Excellence www.plgconsulting.com

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

1,600,000

1,800,000

U.S. QUARTERLY CARLOADS ORIGINATED

STCC 14413 - Industrial sand and gravel (includes frac sand)

STCC 131 - Crude Petroleum and Natural Gas

STCC 1121 - Bituminous coal

4 Qtr. Avg. 1,754,908

4 Qtr. Avg. 1,466,184

4 Qtr. Avg. 77,644

4 Qtr. Avg. 245,012

-288,724

+167,368

Source: Surface Transportation Board

26 Experience / Expertise / Excellence www.plgconsulting.com

THE CHANGING LANDSCAPE FOR ENERGY: SHALE OIL & GAS OUTLOOK

US gas demand will grow due to: ! Coal-fired generation plant converting to gas

! More industrial use – steel, fertilizer, methanol

! Mexican export via pipeline and LNG export overseas

! Increasing use as transportation fuel

US gas cost competitiveness is sustainable ! 30+ year supply at ~$4 mm/btu; cost of production

decreasing ! Supply will overwhelm demand as prices

approach $5/

Low-cost gas and NGLs driving US industrial “renaissance”

Source: EIA, September 2015

Source: EIA for historical and CME Group Oct 2, 2015 settlements for futures

60

65

70

75

80

85

2013 2014 2015 2016

U.S. Natural Gas Production (Bcf/day)

Historical Projections

0 2 4 6 8

10 12 14

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Natural Gas Price at Henry Hub ($/MMBTU)

Historical Futures

27 Experience / Expertise / Excellence www.plgconsulting.com

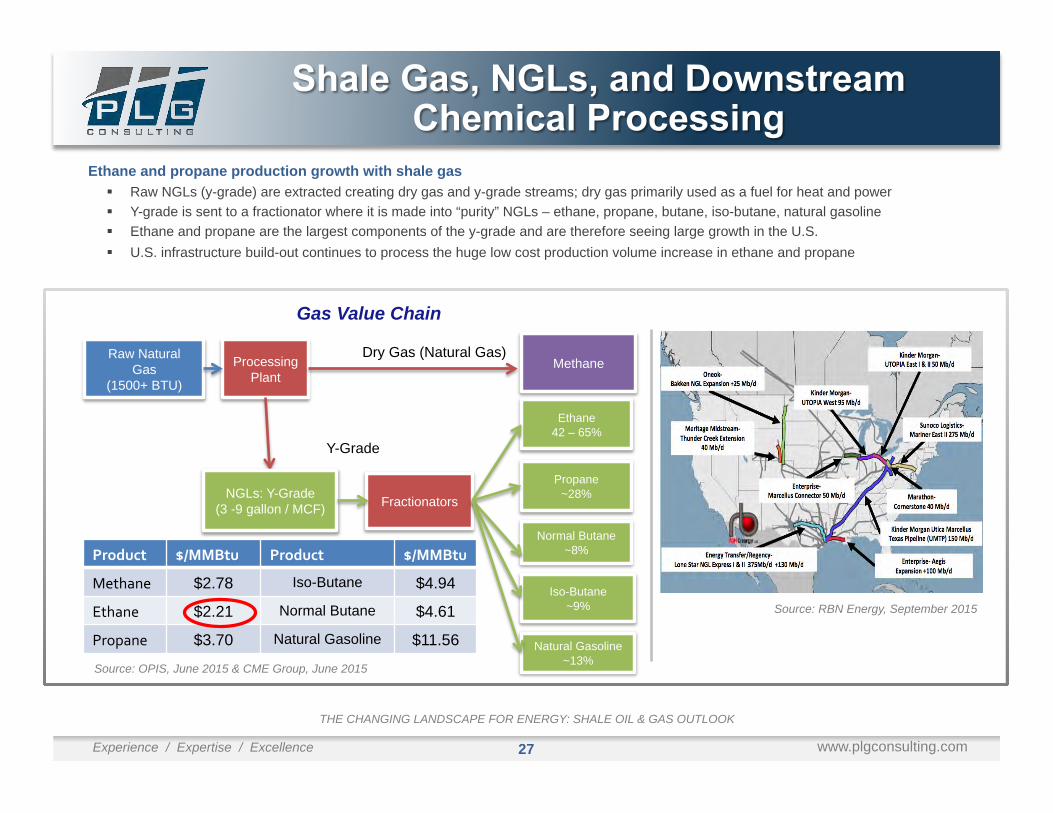

Ethane and propane production growth with shale gas ! Raw NGLs (y-grade) are extracted creating dry gas and y-grade streams; dry gas primarily used as a fuel for heat and power ! Y-grade is sent to a fractionator where it is made into “purity” NGLs – ethane, propane, butane, iso-butane, natural gasoline ! Ethane and propane are the largest components of the y-grade and are therefore seeing large growth in the U.S. ! U.S. infrastructure build-out continues to process the huge low cost production volume increase in ethane and propane

Source: OPIS, June 2015 & CME Group, June 2015

Gas Value Chain

Dry Gas (Natural Gas) Raw Natural Gas

(1500+ BTU)

Processing Plant

Methane

Ethane 42 – 65%

Propane ~28%

Normal Butane ~8%

Iso-Butane ~9%

Natural Gasoline ~13%

Fractionators NGLs: Y-Grade (3 -9 gallon / MCF)

Y-Grade

Product $/MMBtu Product $/MMBtu

Methane $2.78 Iso-Butane $4.94

Ethane $2.21 Normal Butane $4.61

Propane $3.70 Natural Gasoline $11.56

THE CHANGING LANDSCAPE FOR ENERGY: SHALE OIL & GAS OUTLOOK

Source: RBN Energy, September 2015

28 Experience / Expertise / Excellence www.plgconsulting.com

Abundant feedstock, structural cost advantages, and domestic market growth driving US petrochemical industry expansion

Rate of expansion growth will be slowed by ! Volatility of market prices – some based on oil prices

! Lack of EPC capacity

! Shortage of craft labor resources in the U.S. Gulf Coast

! Increasing regulatory hurdles and delays

Expansion peak will be dampened and overall build-out will take longer than announced schedules

! 2nd wave possible early next decade

U.S. chemical industry is entering a historic growth period with incredible growth opportunities and challenges

Sou

rce:

Pet

roch

emic

al U

pdat

e, S

epte

mbe

r 201

5

Oil to Gas Prices

U.S. Ethane Supply Balance

Natural Gas HH Spot Brent Oil

29 Experience / Expertise / Excellence www.plgconsulting.com

Ethylene and Propylene

Ammonia and Deriva=ves

Methanol

Polymers and Resins

Chlor-‐alkali

Other

Source: American Chemistry Council and PLG analysis

PLG’s SHIELD Database

• Shale gas Industrial Expansion Logistics Database

• Interactive information on over 150 projects at launch

• Includes PLG chemical industry expert insights on logistics volumes per project

• Expected release Fall 2015

THE CHANGING LANDSCAPE FOR ENERGY: SHALE OIL & GAS OUTLOOK

30 Experience / Expertise / Excellence www.plgconsulting.com

Shale gas Industrial Expansion Logistics Database (SHIELD) is the first comprehensive, searchable database that provides detailed project information on all the announced shale gas industrial expansion projects. Additionally, PLG’s petrochemical industry experts provide SHIELD’s subscribers with projected logistics volumes by mode for each project.

Features include: ! User-friendly, interactive database with mapping to display

facility locations

! Advanced search and query functionality

! Real time alerts on project updates per subscriber preference

Sample product categories include: ! Ammonia and derivatives

! Ethylene and Propylene

! Methanol

! Polymers and resins

Beta version will be released November 16, 2015 with over 150 projects included

Representative Sample

Sample of searchable fields

31 Experience / Expertise / Excellence www.plgconsulting.com

Thank You!

For follow up questions and information, please contact:

Taylor Robinson President

+1 (508) 982-1319 | [email protected]