exploring charitable giving - bmo bank of montreal · exploring charitable giving ... choosing...

TRANSCRIPT

Financial Planning Update

Exploring Charitable GivingIncluding donor-advised funds vs. private foundations

In many cases, the donors believe in and want to support a specific nonprofit organization’s mission. Still others use charitable giving as a way to teach the next generation about empathy and generosity. If you are considering charitable giving, there are a variety of ways that you can support the charities you believe in. The following are some of the options available.

Donate directly. Donate cash or other assets to a charity’s general fund for unrestricted use, or to a restricted fund for a specific project.

Donate through your will or trust. Make testamentary gifts in your will or trust by giving a set dollar amount or a portion of your estate or trust to a charity.

Designate a charity as the beneficiary of your Individual Retirement Account (IRA). Naming a charity as the beneficiary of your IRA is beneficial because a charity does not pay income tax on amounts distributed to it from an IRA.

Create a charitable trust. Use a charitable remainder trust to make payments to a noncharitable beneficiary for a specified period of time and then distribute the remainder of the trust to one or more charities. (See more details below.) Use a charitable lead trust to distribute a portion of the trust’s income to one or more charities for a specified period of time and then distribute the remainder of the trust to a noncharitable beneficiary.

Establish a donor-advised fund (DAF) or your own private foundation (PF). Both offer an immediate income tax deduction in the year of the gift and enable the donor to distribute the funds for grant making over an extended period of time.

Choosing Between a DAF and a PFBelow are some high-level guidelines to help you compare a DAF and a PF. Your financial advisor can help you determine if one of these vehicles is right for you.

A DAF may make sense if you are:

• Making a minimum contribution of approximately $5,000 – $50,000

• Seeking a simple, fast and inexpensive way to form a charitable giving vehicle

• Looking to maximize your charitable giving income tax deductions

• Contributing closely held stock, publicly traded stock or real estate that has appreciated in value, especially if you want a larger tax deduction

• Seeking greater flexibility in the annual amount of your grant making, including the ability to not make any grants in some years

• Looking for greater privacy in your grant making, including keeping the balance of your charitable giving vehicle private

In exchange for lower administrative and management fees, more favorable deduction limitations and asset valuations, and no excise tax, a DAF generally provides less control in the areas of grant making and investing than a PF. A sponsoring charity of a DAF typically offers two to seven investment pools into which a donor may allocate the funds in the account for investment (although most sponsoring charities will permit independent and active management of a DAF account if it has a minimum balance of $250,000 to $5 million). Because a PF is not limited to a selection of investment pools, the donor has complete control over the investment of its funds within the PF rules.

Charitable giving is an important goal for many investors. Some donors seek to improve their community, while others, who are financially secure, simply want to give back.

BMO Private Bank April 2016

Continued

Financial Planning Update

BMO Private Bank April 2016

2

In addition, a donor to a PF exercises full control over grant making. With a DAF, the sponsoring charity has the legal right to approve or deny a grant and makes all the final decisions. However, it’s important to note that donors can make recommendations and, in practical application, the sponsoring charity generally approves recommendations for grants to 501(c)(3) organizations.

Finally, a donor to a PF may appoint its board members, including family members, providing the opportunity for a family’s future generations to participate in its legacy through philanthropy. A PF may operate in perpetuity, and successive generations may serve on the board. A PF continues to exist until its board votes to dissolve and unwind its operations.

See table below for a more detailed comparison of the two vehicles.

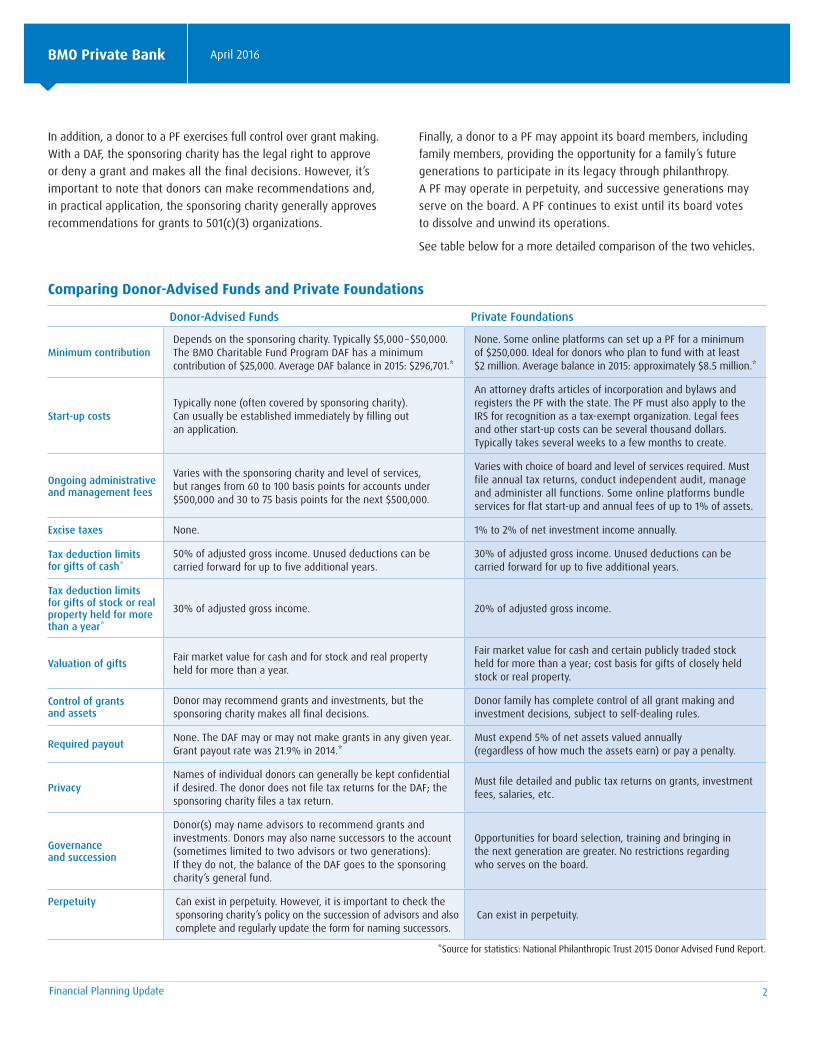

Comparing Donor-Advised Funds and Private Foundations

Donor-Advised Funds Private Foundations

Minimum contributionDepends on the sponsoring charity. Typically $5,000 – $50,000. The BMO Charitable Fund Program DAF has a minimum contribution of $25,000. Average DAF balance in 2015: $296,701.*

None. Some online platforms can set up a PF for a minimum of $250,000. Ideal for donors who plan to fund with at least $2 million. Average balance in 2015: approximately $8.5 million.*

Start-up costsTypically none (often covered by sponsoring charity). Can usually be established immediately by filling out an application.

An attorney drafts articles of incorporation and bylaws and registers the PF with the state. The PF must also apply to the IRS for recognition as a tax-exempt organization. Legal fees and other start-up costs can be several thousand dollars. Typically takes several weeks to a few months to create.

Ongoing administrative and management fees

Varies with the sponsoring charity and level of services, but ranges from 60 to 100 basis points for accounts under $500,000 and 30 to 75 basis points for the next $500,000.

Varies with choice of board and level of services required. Must file annual tax returns, conduct independent audit, manage and administer all functions. Some online platforms bundle services for flat start-up and annual fees of up to 1% of assets.

Excise taxes None. 1% to 2% of net investment income annually.

Tax deduction limits for gifts of cash*

50% of adjusted gross income. Unused deductions can be carried forward for up to five additional years.

30% of adjusted gross income. Unused deductions can be carried forward for up to five additional years.

Tax deduction limits for gifts of stock or real property held for more than a year*

30% of adjusted gross income. 20% of adjusted gross income.

Valuation of gifts Fair market value for cash and for stock and real property held for more than a year.

Fair market value for cash and certain publicly traded stock held for more than a year; cost basis for gifts of closely held stock or real property.

Control of grants and assets

Donor may recommend grants and investments, but the sponsoring charity makes all final decisions.

Donor family has complete control of all grant making and investment decisions, subject to self-dealing rules.

Required payout None. The DAF may or may not make grants in any given year. Grant payout rate was 21.9% in 2014.*

Must expend 5% of net assets valued annually (regardless of how much the assets earn) or pay a penalty.

PrivacyNames of individual donors can generally be kept confidential if desired. The donor does not file tax returns for the DAF; the sponsoring charity files a tax return.

Must file detailed and public tax returns on grants, investment fees, salaries, etc.

Governance and succession

Donor(s) may name advisors to recommend grants and investments. Donors may also name successors to the account (sometimes limited to two advisors or two generations). If they do not, the balance of the DAF goes to the sponsoring charity’s general fund.

Opportunities for board selection, training and bringing in the next generation are greater. No restrictions regarding who serves on the board.

Perpetuity Can exist in perpetuity. However, it is important to check the sponsoring charity’s policy on the succession of advisors and also complete and regularly update the form for naming successors.

Can exist in perpetuity.

*Source for statistics: National Philanthropic Trust 2015 Donor Advised Fund Report.

Financial Planning Update

BMO Private Bank April 2016

3

What is a Charitable Remainder Trust (CRT)?A CRT is a tax-exempt irrevocable trust designed to reduce a donor’s taxable income and estate taxes. The trust first distributes a fixed amount or percentage of income to the donor, the donor’s spouse or children, or other noncharitable beneficiaries for a specified period of time (up to 20 years) or for the duration of one or more lives. After that, the remainder of the trust transfers to one or more designated charities.

The donor can contribute cash or, more commonly, highly appreciated assets with a very low tax basis. When the charity sells the low-cost basis assets, it owes no capital gains taxes and can then reinvest the proceeds into a more diversified portfolio if desired.

There are two main types of CRTs:A Charitable Remainder Annuity Trust (“CRAT”) pays the noncharitable beneficiary an annuity—a fixed amount equal to between 5% and 50% of the fair market value of the original funding amount.

A Charitable Remainder Unitrust (“CRUT”) pays the noncharitable beneficiary a fixed percentage of the fair market value of the trust’s assets, valued annually.

The donor receives income tax and gift tax charitable deductions in the year of the contribution, based on the actuarial value of the remainder interest for the charity. The income tax deduction is limited to 50% of AGI for gifts of cash and 30% of AGI for gifts of long-term capital gain property. Like DAFs and PFs, there is a five-year carryover for unused deductions.

Neither a CRAT nor CRUT is taxed on trust income. Instead, the noncharitable beneficiaries pay taxes on the portion of the trust’s taxable income included in their annuity or unitrust distribution in this order: (1) ordinary income, (2) capital gains, (3) other income (including tax-exempt income) and (4) return of principal.

If you’re interested in creating a CRT, speak with your financial advisor, CPA and attorney to review your assets, discuss tax consequences and draft the trust agreement.

Benefits of Donating Appreciated Publicly Traded Stock Held for More Than a YearWhen you donate appreciated publicly traded stock that you have held for more than a year rather than cash, you pay no capital gains taxes, and neither does the charity that receives the donation when it sells the stock.

For example, suppose you want to donate $50,000 to a DAF and have the choice of donating cash or appreciated publicly traded stock held for more than a year worth $50,000 (with a cost basis of $10,000). Assume you are in the 39.6% and 20% federal income tax brackets for ordinary income and capital gains, respectively.

Here are your options:

Scenario 1: Donate cash

• Your gift totals $50,000.

• You receive a $50,000 charitable deduction (subject to certain limitations, including the 50% of AGI and Pease limitations).

• Your resulting federal income tax savings totals $19,800 and the net cost of your gift is $30,200 (or 60.4% of the gifted amount).

Scenario 2: Donate the appreciated stock

• The value of your gift totals $50,000, but it is made with appreciated stock rather than cash.

• You still receive the $50,000 charitable deduction (however, in this case, subject to 30% of AGI).

• You have the added benefit of paying no capital gains tax on the donated securities (resulting in $8,000 in federal tax savings).

• In this example, the net cost of your gift is $22,200 ($50,000 – $8,000 – $19,800) (or 44.4% of the gifted amount).

While each investor’s situation is unique, the example above illustrates that there may be times when donating appreciated stock is advantageous relative to donating cash.

There are two main types of CRTs:

• Charitable Remainder Annuity Trust (CRAT)

• Charitable Remainder Unitrust (CRUT)

Susanna Poon is the Director of Philanthropy Services with CTC | myCFO, an integrated wealth management provider that serves ultra-affluent individuals, families and family offices across their tax, estate, investment, philanthropic, risk and family capital needs.

Ms. Poon earned a BA in Political Science and a BS in Communication Studies from Boston University, where she graduated magna cum laude. She earned her JD from the UCLA School of Law in Los Angeles, California.

BMO Private Bank April 2016

BMO Harris Bank N.A. (BMO Harris Bank) has worked in collaboration with National Philanthropic Trust (NPT) to establish the BMO Charitable Fund Program, a donor-advised fund program that is administered and sponsored by National Philanthropic Trust, a 501(c)(3), an independently operated public charity serving a national constituency. The BMO Charitable Fund Program is not a separate legal entity and is not a charitable organization. The BMO Charitable Fund Program is a service provided by BMO in collaboration with NPT to assist clients who have selected a donor-advised fund as a means to facilitate their philanthropic giving. Neither BMO nor any of its affiliates is the sponsor of the donor-advised funds created through the BMO Charitable Fund Program. The National Philanthropic Trust is the sponsor of the donor-advised funds created through the BMO Charitable Fund Program and the legal owner of assets transferred to such donor-advised funds.BMO Wealth Management is a brand name that refers to BMO Harris Bank N.A. and certain of its affiliates that provide certain investment, investment advisory, trust, banking, securities, insurance and brokerage products and services.BMO Private Bank is a brand name used in the United States by BMO Harris Bank N.A. Member FDIC. Not all products and services are available in every state and/or location.This information is being used to support the promotion or marketing of the planning strategies discussed herein. This information is not intended to be legal advice or tax advice to any taxpayer and is not intended to be relied upon. BMO Harris Bank N.A. and its affiliates do not provide legal advice to clients. You should review your particular circumstances with your independent legal and tax advisors.Investment Products are: NOT FDIC INSURED l NOT BANK GUARANTEED l MAY LOSE VALUE.© BMO Financial Group (04/16)

In conclusionCharitable giving can be complex. Whether you support a specific organization or simply want to give back, there may be a number of options available—each with unique characteristics and benefits. For help deciding which planning tools can best facilitate charitable giving that meets your goals, consult your financial advisor.

Feel confident about your futureBMO Private Bank — its professionals, its disciplined approach, its comprehensive and innovative advisory platform — can provide financial peace of mind.

For greater confidence in your future, call your BMO Private Bank Advisor today.

www.bmoprivatebank.com