export services in postindustrial society

TRANSCRIPT

THIRTY-FIRST NORTH AMERICAN MEETINGS OF THE REGIONAL SCIENCE ASSOCIATION

EXPORT SERVICES IN POSTINDUSTRIAL SOCIETY

William B. Beyers Department of Geography University of Washington Seattle, Washington 91985

Michael J. Alvine Central Puget Sound Economic Development District Seattle, Washington

ABSTRACT While it is evident that employment in services now dominates the U.S. economy, we still have relatively little understanding of the spatial structure of trade in services. This situation is in part a legacy of our historic tendency to focus on the markets of manufacturing and primary production sectors on the theory that they are "basic." However, the great expansion of services employment in our economy in recent decades means this assumption needs reexamination. This paper reports the results of interviews with 2,200 service sector firms in the Central Puget Sound region, exploring their degree of export orientation. These interviews show a striking degree of export orientation within these sectors. This study suggests that interregional trade in services is probably extremely important in the economic base of all major metropolitan regions.

1. INTRODUCTION While it is evident that employment in services now dominates the U.S.

economy, we still have relatively little understanding of the spatial structure of trade in services. There is disagreement among scholars as to the degree of interregional trade in services. Some feel that trade of services is largely defined by central place hierarchical positions of places, while others have argued for the essential substitution of service sectors for the primary and secondary sectors as the driving forces in regional economies.

This paper presents selected results from a study of service sector firms in the Central Puget Sound region. These results indicate that interregional trade in services is significant and growing, and they imply the need for a reorientation of our view of the growth-inducing role of the services in "postindustrial society"

Given the relative stagnation of manufacturing sector employment in this country in recent years, it has become popular to think of our society as "postindustrial" meaning that traditional manufacturing industry is no longer the only key agent in regional economic change. Writers such as Daniel Bell (1973) emphasize the expanding power of new elements in the industrial order - - the tertiary, quaternary, quinary sectors - - including activities that did not exist a decade or two ago and that have come to be regarded as bellweathers of economic change in advanced economies. Information processing, design, com- munications management, organizational management, software, etc. are ex- amples of these sectors, which contrast with the "industrial" society driven by manufacturing and primary processing activities.

A variety of forces are responsible for the growth of industrial society. These forces include the development of more narrowly defined product lines and consequent regional specialization, technological change in products and pro- cesses, and the development of more complex organizations for management and product distribution. But to what extent have elements of the "postindustrial"

34 PAPERS OF THE REGIONAL SCIENCE ASSOCIATION, VOL. 57, 1985

economy also demonstrated these same growth properties? To what extent is the postindustrial society, composed of highly specialized organizations delivering their output to clients, located with the same spatial diversity as is the case for goods producers in the "industrial" society? We really do not have a body of empirical evidence on trading structures, or a location theory developed for this class of activities, which can help us answer this question very elegantly. We recognize that the Central Administrative Office (CAO) functions of large (usually manufacturing) corporations are located typically in the laborsheds of our largest cities, and that the suppliers of inputs to these organizations are agglomerated near these headquarter cities. But beyond this top of the hierarchy layer, and beyond the specialized services cities such as Washington, D.C. or Las Vegas, what is the degree of interregional trade in the more "normal" complement of these activities which are found in almost every metropolitan region?

2. SELECTED TREATMENT OF SERVICES EXPORTS IN THE LITERATURE A considerable literature haS developed in regional science, geography,

economics, and planning regarding the economic base of communities, a literature which makes various assumptions about trade in different industries. Let us review some of this literature vis-~t-vis trade in services.

At one end of the spectrum, there are those who regard interregional trade in services to be an insignificant activity. This group acknowledges that services are exported, but argues that their trade is governed by central place principles. Reifler (1976) has taken this position, arguing that exports from larger metro- politan centers filter to places farther down the hierarchy. Using data for Bureau of Economic Analysis (BEA) urban-focused regions, he finds an association between services earning per capita and size of place, and he interprets this as evidence of increased export activity in services from large size places. But what of exports to other large size places, internationally, or into smaller places in another subregion in the lattice of places of a given size: " . . . these activities are likely to respond to, but not initiate, regional growth" (Reifler 1976, p. 100). Hence, in this view we should expect that service exports, if any, from a region such as the Seattle area would be localized in nature, flowing to nearby (BEA) regions.

Riefler's analysis was national in scale. However, the same posture is evident in many studies at the regional scale. This has been a convenient means of accomplishing economic base analyses for agencies without the resources to conduct survey research on the structure of their regional economies. Recently produced studies in the Pacific Northwest by the Northwest Power Planning Council (1983) and the State of Washington Emergency Commission on Eco- nomic Development and Job Creation (1983) are exemplary of this posture.

In some ways it is curious that this tradition has developed, since some of the earliest empirical work on the nature of the regional economic base empha- sized the prospective contribution of any sector to this component of any regional economy (Tiebout 1962; Blumenfeld 1955; Alexander 1954).

In striking contrast to the work of scholars taking a pessimistic view of the role of services in the regional economic base is the work of scholars such as Noyelle (1983, 1984), Stanback and Noyelle (1982), Stanback, Bearse, Noyelle and Karasaek (1981), Pred (1977), Polese (1982), and Ullman and Dacey (1960).

Pred undertook an analysis of "job-control" in large corporations, head- quartered in a sample of western United States metropolitan centers in the 1970s. He reasoned from their organizational structure to probable interregional

BEYERS AND ALVINE: EXPORT SERVICES 35

trading relationships, and was struck by the nonhierarchical nature of the locations of jobs "controlled" from his sample of cities. Smaller places such as Boise, Idaho were endowed with headquarters of some very large corporations. On a per capita basis, Pred argued that an equal amount of this type of employment was found in Boise as in the biggest of places. Pred reasoned that much services trade was associated with these headquarters functions, but he did not exploit the possibility that linked services sectors are also highly externalized (although he did not foreclose the prospect of such interaction).

Stanback and Noyelle have recently published a number of papers focusing on the services in the context of urban change (Stanback, Bearse, Noyelle, and Karasek 1981; Noyelle 1983, 1984; Stanback and Noyelle 1982). They have repeatedly argued that services have become more important elements in the economic base of large cities, particularly those that they refer to as the "complex of corporate activities" Included in this set are Central Administrative Offices (CAO's) of manufacturing firms and primary producers, finance, insurance and real estate, business services, legal services, membership organizations, miscel- laneous services, and social services. While not presenting data on trade, they make interesting arguments regarding the growth of these sectors in an export context.

Noyelle and Stanback argue that as the economy has grown, services inputs to producers and CAO's have grown rapidly. R&D, planning, engineering, customizing, stylizing, corporate management, etc. are described as examples of these enlarged input streams from the services. In a sense, they argue that these services have grown as indirect exports, arguing that their rise has been stimulated primarily by the expansion in demand for them by increased purchases as inputs to other sectors which are in turn exporting. Noyelle and Stanback also present a classification of cities, based on an analysis of the structure of their economies, to bolster arguments regarding their vision of the possibility of an impending polarization of the nation's urban places. They conclude that the potential exists for the very largest of places to capture much of the expansion of the traded services, with some disenfranchisement of the set of places below the level of the diversified service centers from this new era of trade in services in advanced societies (Stanback and Noyelle 1982).

In considering structural change, they see advanced services as becoming more important in community economic bases:

Until recently, manufacturing had been a principal component of the export base of many of the current diversified and specialized service centers. Increasingly, however, it is advanced services that constitute the vital sector of their economies (Noyelle 1983, p. 286).

It should be noted that these authors provide no data on trade to confirm their arguments.

Writers on the economic base concept have also sometimes included services in their "basic sector" Ullman and Dacey's work on the minimum requirements concept is probably the best example of this, in that every sector is to some degree basic or exporting (except in the place that is the observed minimum for a sector) (Ullman and Dacey 1960). Similarly, input-output accounts make no assumptions about such bifurcations; any sector may be selling locally or nonlocally in empirically observed proportions. Mulligan and Gibson (1984) provide similar evidence for a set of small places in Arizona.

It is instructive to review evidence from the survey-based input-output

36 PAPERS OF THE REGIONAL SCIENCE ASSOCIATION, VOL. 57, 1985

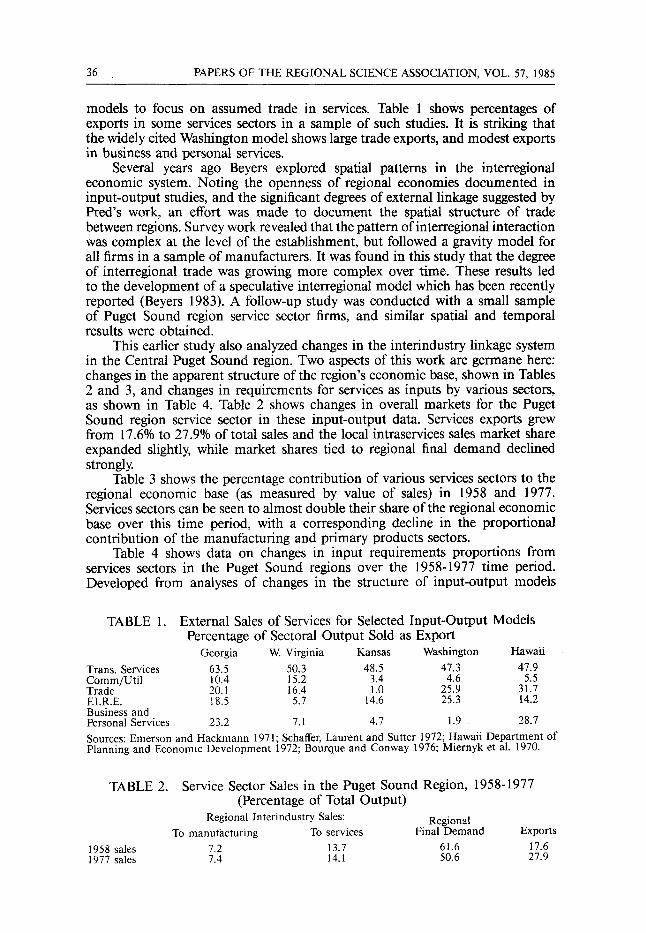

models to focus on assumed trade in services. Table 1 shows percentages of exports in some services sectors in a sample of such studies. It is striking that the widely cited Washington model shows large trade exports, and modest exports in business and personal services.

Several years ago Beyers explored spatial patterns in the interregional economic system. Noting the openness of regional economies documented in input-output studies, and the significant degrees of external linkage suggested by Pred's work, an effort was made to document the spatial structure of trade between regions. Survey work revealed that the pattern ofinterregional interaction was complex at the level of the establishment, but followed a gravity model for all firms in a sample of manufacturers. It was found in this study that the degree of interregional trade was growing more complex over time. These results led to the development of a speculative interregional model which has been recently reported (Beyers 1983). A follow-up study was conducted with a small sample of Puget Sound region service sector firms, and similar spatial and temporal results were obtained.

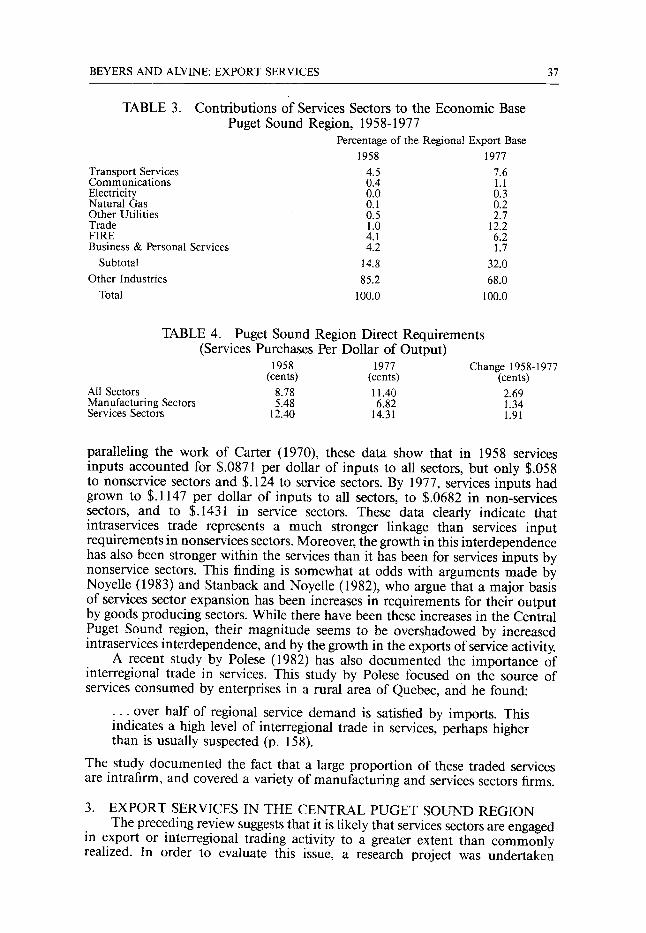

This earlier study also analyzed changes in the interindustry linkage system in the Central Puget Sound region. Two aspects of this work are germane here: changes in the apparent structure of the region's economic base, shown in Tables 2 and 3, and changes in requirements for services as inputs by various sectors, as shown in Table 4. Table 2 shows changes in overall markets for the Puget Sound region service sector in these input-output data. Services exports grew from 17.6% to 27.9% of total sales and the local intraservices sales market share expanded slightly, while market shares tied to regional final demand declined strongly.

Table 3 shows the percentage contribution of various services sectors to the regional economic base (as measured by value of sales) in 1958 and 1977. Services sectors can be seen to almost double their share of the regional economic base over this time period, with a corresponding decline in the proportional contribution of the manufacturing and primary products sectors.

Table 4 shows data on changes in input requirements proportions from services sectors in the Puget Sound regions over the 1958-1977 time period. Developed from analyses of changes in the structure of input-output models

TABLE 1.

Trans. Services Comm/Util Trade EI.R.E. Business and Personal Services

External Sales of Services for Selected Input-Output Models Percentage of Sectoral Output Sold as Export

Georgia W. Virginia Kansas Washington Hawaii 63.5 50.3 48.5 47.3 47.9 10.4 15.2 3.4 4.6 5.5 20.1 16,4 1.0 25,9 31.7 18.5 5.7 14.6 25.3 14.2

23.2 7.1 4.7 1.9 28.7 Sources: Emerson and Hackmann 1971; Schaffer, Laurent and Sutter 1972; Hawaii Department of Planning and Economic Development 1972; Bourque and Conway 1976; Miernyk et al. 1970.

TABLE 2.

1958 sales 1977 sales

Service Sector Sales in the Puget Sound Region, 1958-1977 (Percentage of Total Output)

Regional Interindustry Sales: Regional To manufacturing To services Final Demand Exports

7.2 13.7 61.6 17.6 7.4 14.1 50.6 27.9

BEYERS AND ALVINE: EXPORT SERVICES 37

TABLE 3. Contributions of Services Sectors to the Economic Base Puget Sound Region, 1958-1977

Percentage of the Regional Export Base 1958 1977

Transport Services 4.5 7.6 Communications 0.4 1.1 Electricity 0.0 0.3 Natural Gas 0.1 0.2 Other Utilities 0.5 2.7 Trade 1.0 12.2 FIRE 4.1 6.2 Business & Personal Services 4.2 1.7

Subtotal 14.8 32.0 Other Industries 85.2 68.0

Total 100.0 100.0

TABLE 4. Puget Sound Region Direct Requirements (Services Purchases Per Dollar of Output)

1958 1977 Change 1958-1977 (cents) (cents) (cents)

All Sectors 8.78 11.40 2.69 Manufacturing Sectors 5.48 6.82 1.34 Services Sectors 12.40 14.31 1.91

paralleling the work of Carter (1970), these data show that in 1958 services inputs accounted for $.0871 per dollar of inputs to all sectors, but only $.058 to nonservice sectors and $. 124 to service sectors. By 1977, services inputs had grown to $.1147 per dollar of inputs to all sectors, to $.0682 in non-services sectors, and to $.1431 in service sectors. These data clearly indicate that intraserviees trade represents a much stronger linkage than services input requirements in nonservices sectors. Moreover, the growth in this interdependence has also been stronger within the services than it has been for services inputs by nonservice sectors. This finding is somewhat at odds with arguments made by Noyelle (1983) and Stanback and Noyelle (1982), who argue that a major basis of services sector expansion has been increases in requirements for their output by goods producing sectors. While there have been these increases in the Central Puget Sound region, their magnitude seems to be overshadowed by increased intraservices interdependence, and by the growth in the exports of service activity.

A recent study by Polese (1982) has also documented the importance of interregional trade in services. This study by Polese focused on the source of services consumed by enterprises in a rural area of Quebec, and he found:

. . . over half of regional service demand is satisfied by imports. This indicates a high level of interregional trade in services, perhaps higher than is usually suspected (p. 158).

The study documented the fact that a large proportion of these traded services are intrafirm, and covered a variety of manufacturing and services sectors firms.

3. EXPORT SERVICES IN THE CENTRAL PUGET SOUND REGION The preceding review suggests that it is likely that services sectors are engaged

in export or interregional trading activity to a greater extent than commonly realized. In order to evaluate this issue, a research project was undertaken

38 PAPERS OF THE REGIONAL SCIENCE ASSOCIATION, VOL. 57, 1985

involving a broad cross-section of service sector establishments in the Central Puget Sound region.

This section of the paper provides selected findings from this project. More detailed findings are available in Beyers, Alvine, and Johnsen (1985).

The desire in this project was to undertake "exploratory analysis" focusing on sectors which have been previously more or less overlooked. Thus, retail and wholesale trade activity was not focused upon because it has been the subject of so many central place market studies, and tourism-related sectors were bypassed because of the relative wealth of information about this activity. A set of (business) service sectors was identified at a four-digit SIC level of detail which we felt was likely to have export markets.

We obtained a list of firm names in these sectors from Contacts Influential, a private firm that collects information on individual business establishments primarily for market research purposes. Almost 19,000 establishments were identified in the study region in the four-digit SIC codes selected for study. This was a much larger sample than we could interview, so we chose to contact all firms with six or more employees, and 5% of firms with five or fewer employees. This led to a sample size of about 5,000 establishments. Almost 2,200 of these firms were contacted by telephone, and probed about their degree of export market orientation. We chose to conduct detailed interviews with those reporting more than 10% of their business in export markets, and sought limited information from the balance of the sample. About 1,105 firms met the 10% export threshold; these firms employed approximately 85,000.persons, while the other approxi- mately 1,100 firms employed about 35,000 persons. (About 5% of the firms contacted refused cooperation in the survey.) The in-depth interviews probed the level of export business, its dynamics, factors associated with the firms choice of location in the region, changes in location, and factors affecting business success. Interviews were conducted by students with key executives in these firms. It appears as though our overall sample size is about 40% of employment in the sectors which we chose to study, a very large level of coverage by survey research standards.

Location of Markets Respondents to the in-depth interviews had nonlocal sales of more than

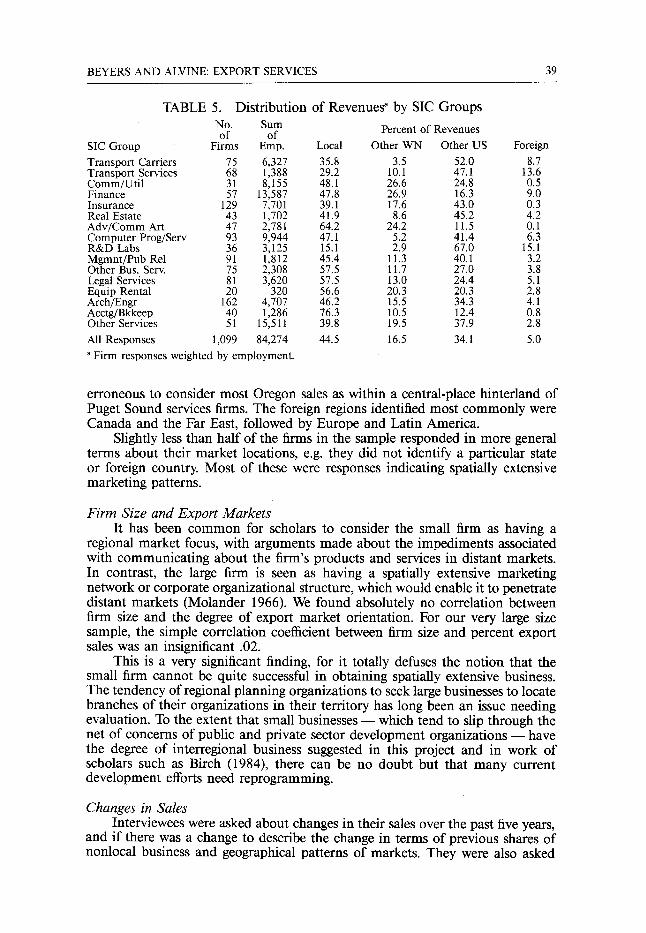

55% of their revenues. Table 5 shows the size of this sample by broad SIC groups, and the location of revenues for these establishments. In almost every grouping, the nonlocal revenue proportion is significant; in about a third of these categories the non-Washington sales component was over half of their business.

Sectors with particularly striking export proportions include transportation services, research and development labs, insurance, and real estate services. In contrast, a more local orientation is evident in advertising, commerical photog- raphy and art services, and bookkeeping services. Beyond these extremes, it is fascinating to note the almost generic strong ties to external markets in a variety of sectors heretofore considered largely local in their focus: communications, banking, and computer services.

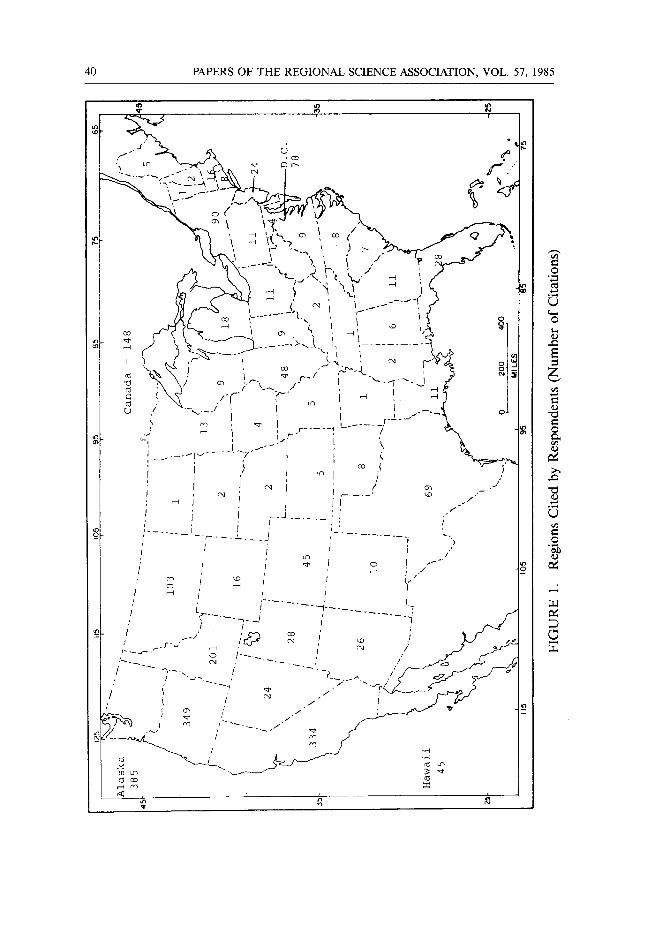

The tally of regions identified is shown in Figure 1 for domestic regions. While the pattern shows a dominance of ties to Alaska, Oregon, and California, this regional focus should not be interpreted as a central place like market structure. One would be hard pressed to consider California to be in Washington's hinterland. Portland, Oregon is a metropolitan place in the national settlement system only slightly smaller than Seattle. And as with California, it is probably

BEYERS AND ALVINE: EXPORT SERVICES 39

Distribution of Revenues a by SIC Groups TABLE 5.

No. Sum Percent of Revenues of of

SIC Group Firms Emp. Local Other WN Other US Foreign

Transport Carriers 75 6,327 35.8 3.5 52.0 8.7 Transport Services 68 1,388 29.2 10.1 47.1 13.6 Comm/Util 31 8,155 48.1 26.6 24.8 0.5 Finance 57 13,587 47.8 26.9 16.3 9.0 Insurance 129 7,701 39.1 17.6 43.0 0.3 Real Estate 43 1,702 41.9 8.6 45.2 4.2 Adv/Comm Art 47 2,781 64.2 24.2 11.5 0.1 Computer Prog/Serv 93 9,944 47.1 5.2 41.4 6.3 R&D Labs 36 3,125 15.1 2.9 67.0 15.1 Mgmnt/Pub Rel 91 1,812 45.4 11.3 40.1 3.2 Other Bus. Serv: 75 2,308 57.5 11.7 27.0 3.8 Legal Services 81 3,620 57.5 13.0 24.4 5.1 Equip Rental 20 320 56.6 20.3 20.3 2.8 Arch/Engr 162 4,707 46.2 15.5 34.3 4.1 Acctg/Bkkeep 40 1,286 76.3 10.5 12.4 0.8 Other Services 51 15,511 39.8 19.5 37.9 2.8

All Responses 1,099 84,274 44.5 16.5 34.1 5.0

a Firm responses weighted by employment.

erroneous to consider most Oregon sales as within a central-place hinterland of Puget Sound services firms. The foreign regions identified most commonly were Canada and the Far East, followed by Europe and Latin America.

Slightly less than half of the firms in the sample responded in more general terms about their market locations, e.g. they did not identify a particular state or foreign country. Most of these were responses indicating spatially extensive marketing patterns.

Firm Size and Export Markets It has been common for scholars to consider the small firm as having a

regional market focus, with arguments made about the impediments associated with communicating about the firm's products and services in distant markets. In contrast, the large firm is seen as having a spatially extensive marketing network or corporate organizational structure, which would enable it to penetrate distant markets (Molander 1966). We found absolutely no correlation between firm size and the degree of export market orientation. For our very large size sample, the simple correlation coefficient between firm size and percent export sales was an insignificant .02.

This is a very significant finding, for it totally defuses the notion that the small firm cannot be quite successful in obtaining spatially extensive business. The tendency of regional planning organizations to seek large businesses to locate branches of their organizations in their territory has long been an issue needing evaluation. To the extent that small businesses - - which tend to slip through the net of concerns of public and private sector development organizations - - have the degree of interregional business suggested in this project and in work of scholars such as Birch (1984), there can be no doubt but that many current development efforts need reprogramming.

Changes in Sales Interviewees were asked about changes in their sales over the past five years,

and if there was a change to describe the change in terms of previous shares of nonlocal business and geographical patterns of markets. They were also asked

4 0 P A P E R S O F T H E R E G I O N A L S C I E N C E A S S O C I A T I O N , V O L . 57, 1985

J " L] ~

" ~ - " ~ - .'~".; - ~ , ' ~ { ~ ~t "~ " m ', ,,'--,,

! Z~, . t -

un I O0 ~

' I1 , " ( I ,

( " f z ~ ' " ,~ ~ ,.-4

." m ; ' ~ I _ L . . . . . . ) 3 , J '~ I i , - - " . . . . - ~ - - I ~ ,

I I ' ' , } " I i ~ I l

, #

- - - - T - - - - : . _ _ J , - . . . . . . . . ~ ' L , .

I I I i / ' I'

I .~ I ~ I / " ~ "

,-4 / i t

: L i ........ H ..... L, , -~ . . . . . -~-4 ; - . . . . . . . q j ' -

.. , . , - - / ,!4~ ~ , .o :, " - ' ~ - ,,~ . . . . . . " ~ o ~ / - - - , ~ ../ / _ . z / -

I ,L.-._ j o~ / / " i / '~

/ .,H

l . q r ~ I < ~ �9 �9 ,j., ,~

~o

0

z

. . 0

(..)

0

_"2

BEYERS AND ALVINE: EXPORT SERVICES 41

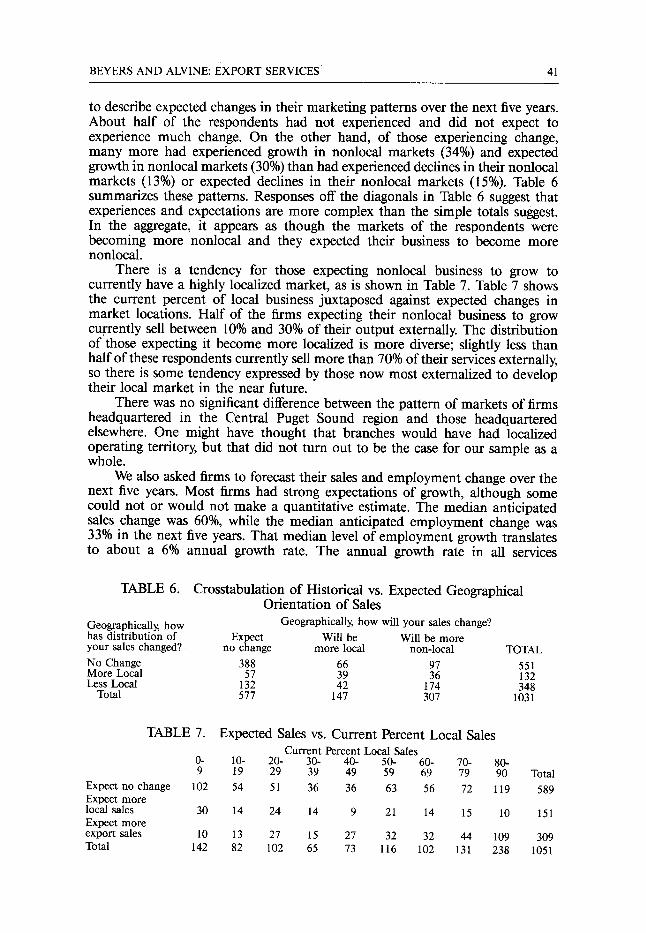

to describe expected changes in their marketing patterns over the next five years. About half of the respondents had not experienced and did not expect to experience much change. On the other hand, of those experiencing change, many more had experienced growth in nonlocal markets (34%) and expected growth in nonlocal markets (30%) than had experienced declines in their nonlocal markets (13%) or expected declines in their nonlocal markets (15%). Table 6 summarizes these patterns. Responses off the diagonals in Table 6 suggest that experiences and expectations are more complex than the simple totals suggest. In the aggregate, it appears as though the markets of the respondents were becoming more nonlocal and they expected their business to become more nonlocal.

There is a tendency for those expecting nonlocal business to grow to currently have a highly localized market, as is shown in Table 7. Table 7 shows the current percent of local business juxtaposed against expected changes in market locations. Half of the firms expecting their nonlocal business to grow currently sell between 10% and 30% of their output externally. The distribution of those expecting it become more localized is more diverse; slightly less than half of these respondents currently sell more than 70% of their services externally, so there is some tendency expressed by those now most externalized to develop their local market in the near future.

There was no significant difference between the pattern of markets of firms headquartered in the Central Puget Sound region and those headquartered elsewhere. One might have thought that branches would have had localized operating territory, but that did not turn out to be the case for our sample as a whole.

We also asked firms to forecast their sales and employment change over the next five years. Most firms had strong expectations of growth, although some could not or would not make a quantitative estimate. The median anticipated sales change was 60%, while the median anticipated employment change was 33% in the next five years. That median level of employment growth translates to about a 6% annual growth rate. The annual growth rate in all services

TABLE 6. Crosstabulation of Historical vs. Expected Geographical Orientation of Sales

Geographically, how Geographically, how will your sales change? has distribution of Expect Will be Will be more your sales changed? no change more local non-local TOTAL

No Change 388 66 97 551 More Local 57 39 36 132 Less Local 132 42 174 348

Total 577 147 307 1031

TABLE 7. Expected Sales vs. Current Percent Local Sales Current Percent Local Sales

0- 10- 20- 30- 40- 50- 60- 70- 80- 9 19 29 39 49 59 69 79 90 Total

Expect no change 102 54 51 36 36 63 56 72 119 589 Expect more local sales 30 14 24 14 9 21 14 15 10 151 Expect more export sales 10 13 27 15 27 32 32 44 109 309 Total 142 82 102 65 73 116 102 131 238 1051

42 PAPERS OF THE REGIONAL SCIENCE ASSOCIATION, VOL. 57, 1985

employment in the Central Puget Sound region was 4.5% per annum over the 1958-1977 time period.

The firms we interviewed were probed for information on their mobility. Given that many had grown rapidly, it should be expected that they have had a dynamic locational history. This was borne out by the interviews. Fully half had moved in the last five years, mostly to gain space or to be nearer to sites important to principal officers in the firm. Most of the firms we interviewed were young - - half had been started since 1971, and one quarter since 1978. They were small - - median size was only fifteen employees - - hence it is likely that they were short of space as they were and are growing. Most moved only short distances, and interestingly many fewer anticipated not having to move in the next five years than had recently moved (additional detail can be found in Beyers, Alvine, and Johnsen 1985).

Other Establishments. The preceding discussion has referred to those firms meeting our interview

screen of 10% export business; this sample must be placed in context of all firms in the services sectors in this survey to get a more accurate image of overall interregional trade in services. Firms with less than 10% export business were asked their export sales percentage, and their level of employment.

In striking contrast to the 1,100 firms that met our 10% screen, the approximately 1,000 firms which we interviewed by telephone had only about 2% of their business in export markets. These firms tended to be slightly smaller than the median size of firms in the in-depth interview sample, and collectively had about 35,000 employees. Extrapolation of the results for the sample of firms meeting our export-sales screen and the sample with less than 10% export sales as a whole in the Contacts Influential listing leads to a level of export orientation in the 33%-37% range. This level is well above those reported in Table 1 for the various input-output studies in the sector focused upon in this survey. While this is the case, these studies are somewhat dated, and given the growth in export-market sales reported by firms in our interviews, there is good reason to expect higher export-service estimates than found in these earlier research efforts.

The contrasting levels of export orientation of firms in the same four-digit SIC codes in our sampling plan is a major finding of this study. Why is it that firms in narrowly defined categories of services studied here have highly varying degrees of export market ties? Expressed alternatively, what determines what degree of the business activity is export-tied in given sectors?

4. CONCLUSIONS The data presented in this paper indicate that service sectors probably have

significant export markets in larger metropolitan regions. The linkages found in the Central Puget Sound region service sectors to larger urban regions (e.g. New York, San Francisco and Los Angeles) are contrary to central place theory notions that Puget Sound region service firms' exports are exclusively to their surrounding periphery. Many service sectors have a base of income which is as external and spatially diverse as many sectors traditionally considered key to the local economy. This finding means that many state and local economic devel- opment initiatives need rethinking, even in the absence of changes in federal programs. Clearly, one of the most important results of the project reported here is documentation of the fact that a broad cross section of service sectors are strongly dependent upon interregional t r a d e - trade in distant parts of the United States and in foreign countries. Moreover, these are growing sectors in

BEYERS AND ALVINE: EXPORT SERVICES 43

the national economic context, and the degree of their external trade is also growing. This is clear not only from the recent history of sales of respondents but from their expectations of changes in sales relationships.

The data presented in this paper tend to support analyses of structural change using input-output data, but do not necessarily support some more qualitatively oriented interpretations of studies of structural change. In this regard, the work of NoyeUe and Stanback deserves reexamination. Noyelle and Stanback argue that much of the growth of the local services (wherever) is due to their greater input requirements by the "key" (i.e., export) sectors found in each region. Yet the data presented in this paper suggest that while the significance of these inputs has risen, proportionally they did not increase as much as intraservices input purchases. The survey research reported here also suggested a strong market tie within the services: more than half of the contacts reported by our respondents were with services or public sector markets. Evidence gathered in this paper suggests that growth of services exports was not primarily associated with the movement of goods, or because of export market linkages to goods producing or moving sectors. Rather, the growth of the services seems to be more tied to complex intraservices sector demands, and final demands for services by consumers and government. The research results presented here lead to a number of research needs.

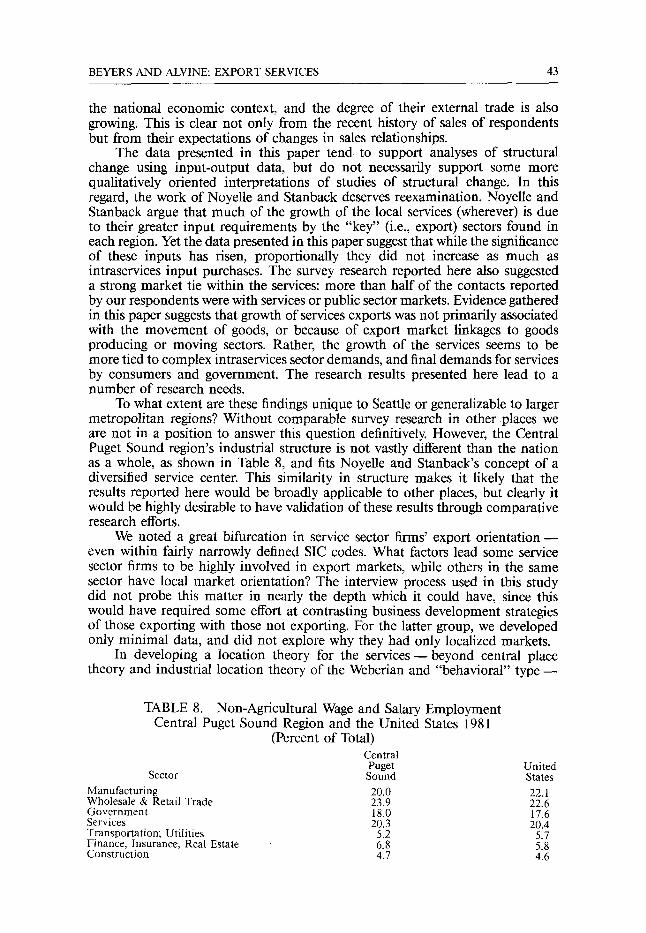

To what extent are these findings unique to Seattle or generalizable to larger metropolitan regions? Without comparable survey research in other places we are not in a position to answer this question definitively. However, the Central Puget Sound region's industrial structure is not vastly different than the nation as a whole, as shown in Table 8, and fits Noyelle and Stanback's concept of a diversified service center. This similarity in structure makes it likely that the results reported here would be broadly applicable to other places, but clearly it would be highly desirable to have validation of these results through comparative research efforts.

We noted a great bifurcation in service sector firms' export orientation even within fairly narrowly defined SIC codes. What factors lead some service sector firms to be highly involved in export markets, while others in the same sector have local market orientation? The interview process used in this study did not probe this matter in nearly the depth which it could have, since this would have required some effort at contrasting business development strategies of those exporting with those not exporting. For the latter group, we developed only minimal data, and did not explore why they had only localized markets.

In developing a location theory for the s e r v i c e s - beyond central place theory and industrial location theory of the Weberian and "behavioral" t y p e -

TABLE 8. Non-Agricultural Wage and Salary Employment Central Puget Sound Region and the United States 1981

(Percent of Total) Central Puget United

Sector Sound States

Manufacturing 20.0 22.1 Wholesale & Retail Trade 23.9 22.6 Government 18.0 17.6 Services 20.3 20.4 Transportation; Utilities 5.2 5.7 Finance, Insurance, Real Estate 6.8 5.8 Construction 4.7 4.6

44 PAPERS OF THE REGIONAL SCIENCE ASSOCIATION, VOL. 57, 1985

we really need to have a micro level understanding of the location factors of significance to these sectors. This means a comparative evaluation of the importance of various input factors. Given the significance of labor costs to these sectors it is likely that qualities of labor would figure centrally in the development of a location theory for service export firms. Given the small size of many of these establishments, and the apparent key role of their founder in their siting decision (or nondecision?), any such theorizing about their location must have a focus on these entrepreneurs.

Many current regional development program efforts seem typically focused on attracting manufacturing industry; industrial policy discussion has largely focused on manufacturing to the exclusion of much consideration of the role of the services as basic industry in a national or regional context. The data presented in this paper indicate that this view must be augmented. Given the continuing growth of employment in services through the recent recession, and given the data provided to us by the respondents about their recent history of growth, it is clear that structural change in the export base of the Central Puget Sound region has continued as suggested in Tables 2 and 3. This suggests the need for careful consideration of service sectors in any national or regional industrial policy.

The results presented in this paper are exploratory. While they need verifi- cation in other settings to confirm their generality, there is good reason to believe that the spatially extensive characteristics of the markets of services firms in the study region are common to most large metropolitan regions, and may also characterize many smaller regions' economic base in "postindustrial" society. Hopefully, regional scientists, geographers, planners, economists and others interested in understanding forces leading the growth and development of our economy will help in obtaining the understanding we need of the role of export service activity in contemporary economic development processes. At the same time, new perspectives are probably necessary on location theory for the services, and in "industrial policy" for America in the 1980s.

ACKNOWLEDGMENTS Funding for the research reported in this paper was provided by the Economic

Development Administration, Grant No. 07-15-11071, and by the College of Arts and~Sciences at the University of Washington. The views expressed are those of the authors; they do not necessarily represent the views of the supporting institutions. The assistance of J. Scott MacCready, Dean Hansen, John W. Tofflemire, Barney Warf, David Baltz, Jonathan Van Wyk and Nancy White, in conducting interviews is gratefully acknowledged. Mr. Erik Johnsen, Executive Director of the Central Puget Sound Economic Development District, was instrumental in the development of this project. Support from the National Science Foundation under Grant No. SES 8109290 to William Beyers also played a critical role in this project.

REFERENCES Alexander, J. W. 1954. The basic-nonbasic concept of urban economic functions. Economic

Geography 30: 246-61. Bell, D. 1973. The coming of postindustrial society: a venture in social forecasting. New York:

Basic Books. Beyers, W. B. 1983. The interregional structure of the U.S. economy. International Regional Science

Review 8: 213-31. Beyers, W. B., Alvine, M. J., and Johnsen, E. 1985. The service economy: export of services in the

Central Puget Sound Region. Seattle: Central Puget Sound Economic Development District.

BEYERS AND ALVINE: EXPORT SERVICES 45

Birch, D. 1984. The changing rules of the game, finding a niche in the thoughtware economy. Economic Development Commentary 8, 1: 12-16.

Blumenfeld, H. 1955. The economic base of the metropolis. Journal of the American Institute of Planners 21:114-32.

Bourque, P. J. and Conway, R. S., Jr. 1976. The input-output structure of Washington state. Seattle: Graduate School of Business Administration, mimeographed.

Carter, A. 1970. Structural change in the American economy. Cambridge, MA: Harvard University Press.

Emerson, M. J. and Hackmann, D. G. 1971. The 1969 Kansas input-output study. Topeka: Kansas Department of Economic Development, Planning Division.

Hawaii Department of Planning and Economic Development. 1972. Interindustry study of the Hawaiian economy.

Miernyk, W. H., Shellhamer, K. L., Brown, D. M., Coccari, R. L., Gallagher, C. J., and Wineman, W. H. 1970. Simulating regional economic development. Lexington, MA: D.C. Heath and Company.

Molander, J. D. 1966. Geographic isolation and market area expansion; a study of small Washington state firms attempting to sell in the national market. D.B.A. dissertation, Graduate School of Business Administration, University of Washington.

Mulligan, G. and Gibson, L. 1984. Regression estimates of economic base multipliers for small communities. Economic Geography 60: 225-37.

Northwest Power Planning Council. 1983. Economic and Demographic Assumptions, mimeo- graphed.

Noyelle, T. J. 1983. The rise of advanced services. American Planning Association Journal 49, 3: 280-90.

Noyelle, T. J. 1984. The service era, focussing public policy on people and places. Economic Development Commentary 8, 2: 12-17.

Polese, M. 1982. Regional demand for business services and interregional service flows in a small Canadian region. Papers, Regional Science Association 50:151-63.

Pred, A. 1977. City-systems in advanced economies. New York: Wiley & Sons. Riefler, R. 1976. Implications of service industry growth for regional development strategies. Annals

of Regional Science 10: 88-103. Schaffer, W. A., Laurent, E. A., and Sutter, E. M., Jr. 1972. Introducing the Georgia economic

model. Atlanta: The Georgia Department of Industry and Trade. Stanback, T. M., Jr. and Noyelle, T. J. 1982. Cities in transition. Totowa, NJ: Allenheld, Osmun. Tiebout, C. M. 1962. The community economic base study. New York: Committee on Economic

Development. Ullman, E. L. and Dacey, M. J. 1960. The minimum requirements approach to the regional

economic base. Papers, Regional Science Association. 6:175-94. Washington State. 1983. Report of the emergency commission on economic development and job

creation. Volume III.