externally financed project funds management, accounting and reporting zaza rukhaia 27-29 february,...

TRANSCRIPT

EXTERNALLY FINANCED PROJECT FUNDS MANAGEMENT, ACCOUNTING AND

REPORTING

Zaza Rukhaia27-29 February, 2012

SYSTEM OF SETTLEMENT OF ACCOUNTS OF THE TREASURY

• Consolidated Treasury Account and accounting and reporting of budget receipts;

• Management of the consolidated multi-currency account;

• Management of sub-accounts of donor funded investment projects

Externally financed project funds management, accounting and reporting

TOPICS

• The State Treasury has one account in national currency – consolidated treasury account

• Receipts of the country - regional as well as local budget receipts - are deposited to the consolidated treasury account

• All budget payments are made from the consolidated treasury account

• Treasury performs only clearing settlement with clients of the Treasury; all transactions go through commercial banks

Externally financed project funds management, accounting and reporting

CONSOLIDATED TREASURY ACCOUNT

CONSOLIDATED TREASURY ACCOUNT AND ACCOUNTING AND REPORTING OF BUDGET RECEIPTS

CONSOLIDATED TREASURY ACCOUNT AND ACCOUNTING AND REPORTING OF BUDGET RECEIPTS

• Operations of the consolidated treasury account are carried out “in real time regime via inter-banks system of settlement of accounts” (RTGS - Real Time Gross Settlement), updated system of which was introduced in 2010

• Treasury is connected to the RTGS system as an independent participant and is granted a BIC code - TRESGE22.

• In 2010 the Georgian banking system introduced international standard of accounts IBAN

Externally financed project funds management, accounting and reporting

RTGS / IBAN

CONSOLIDATED TREASURY ACCOUNT AND ACCOUNTING AND REPORTING OF BUDGET RECEIPTS

• The tax and securities (GPSS/CSD) system was introduced, where the Treasury is involved as a participant of the securities accounts settlement system

• The Treasury has information on transactions in primary and secondary securities market (treasury obligations and bonds)

• By means of this system state securities are used as a collateral for credits issued by the National Bank to commercial banks

Externally financed project funds management, accounting and reporting

GPSS/CSD

CONSOLIDATED TREASURY ACCOUNT AND ACCOUNTING AND REPORTING OF BUDGET RECEIPTS

• State Treasury is responsible for full and correct accounting of receipts from state, autonomous republics’, regional and local self-government budgets.

• Budget receipts are deposited to the consolidated treasury account via National and commercial banks of Georgia.

• In order to receive timely information about receipts during the day , it is possible to periodically import receipts, several times a day (for instance, every hour)

MANAGEMENT OF BUDGET RECEIPTS

Externally financed project funds management, accounting and reporting

CONSOLIDATED TREASURY ACCOUNT AND ACCOUNTING AND REPORTING OF BUDGET RECEIPTS

• In the end of the operations day, the banking day of the informational day is closed, receipts processed and then compared with the RTGS

• For the purpose of accounting and reporting of budget receipts the Treasury maintains electronic forms and registries

• Registry represents a basis for accounting, where financial transaction and its outcome are accounted and recorded

MANAGEMENT OF BUDGET RECEIPTS

Externally financed project funds management, accounting and reporting

CONSOLIDATED TREASURY ACCOUNT AND ACCOUNTING AND REPORTING OF BUDGET RECEIPTS

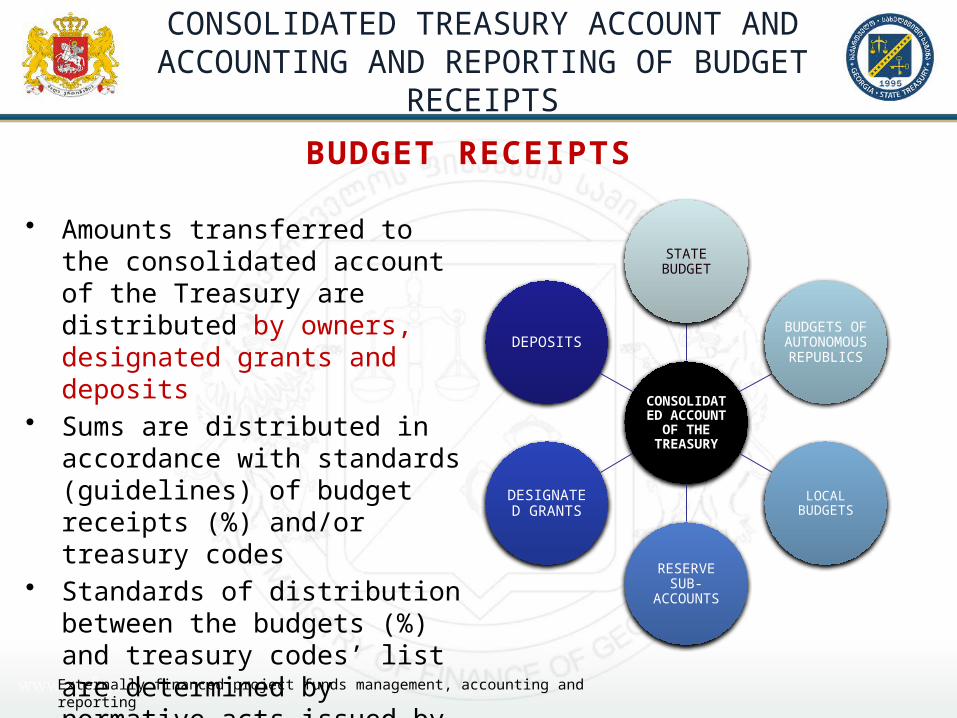

• Amounts transferred to the consolidated account of the Treasury are distributed by owners, designated grants and deposits

• Sums are distributed in accordance with standards (guidelines) of budget receipts (%) and/or treasury codes

• Standards of distribution between the budgets (%) and treasury codes’ list are determined by normative acts issued by competent bodies

BUDGET RECEIPTS

Externally financed project funds management, accounting and reporting

CONSOLIDATED ACCOUNT OF THE

TREASURY

STATE BUDGET

BUDGETS OF AUTONOMOUS

REPUBLICS

LOCAL BUDGETS

RESERVE SUB-ACCOUNTS

DESIGNATED GRANTS

DEPOSITS

Externally financed project funds management, accounting and reporting

NATIONAL BANK OF GEORGIA

HQCommercial

Bank №1

HQCommercial

Bank №2

Commercial Bank Branch

Commercial Bank Branch

Tax / Non-Tax Payers

RTGS

Budget Institution

TREASURY SINGLE ACCOUNT

REVENUE SERVICE

Budget Organization Local Budget

CONSOLIDATED TREASURY ACCOUNT

CONSOLIDATED MULTI - CURRENCY ACCOUNT MANAGEMENT

• The State Treasury had opened a unified multi-currency account at the National Bank of Georgia in 2009

• Budgetary organizations effect payments in foreign currency in the consolidated multi-currency account

• External debts are served and paid from the same account

• Donor organizations and grants and credits of foreign countries are also directed to the multi-currency account

• Budget and other deposit payments effected by natural or legal entities

Externally financed project funds management, accounting and reporting

CONSOLIDATED MULTI - CURRENCY ACCOUNT MANAGEMENT

• State Treasury is a member of the World inter-banks financial telecommunications association system (SWIFT).

• Currency transaction accounting system assigns the currency code (sub-account) to organizations or investment projects.

• Currency code (sub-account) contains 9 symbols:

1st symbol determines type of transaction (current, special, deposit); 4th – designations (investment project, designated funding, fine, fee, etc.) 5th – form (loan, grant, etc)

Externally financed project funds management, accounting and reporting

1 2 3 4 5 6 7 8 9

TYPE OF TRANSACTION DONOR DESIGNATION FORM UNIQUE CODE OF THE ORANIZATION OR PROJECT

Externally financed project funds management, accounting and reporting

• BUDGETARY

ORGANIZATION

• STATE TREASURY

• BENEFICIARIES

• CURRENCY ACCOUNT

• SWIFT• CONSOLIDAT

ED ACCOUNT

• NBG• SWIFT MESSAGE

• CASH DEMAND

• CURRENCY ORDER

(DEMAND)

CONSOLIDATED MULTI - CURRENCY ACCOUNT MANAGEMENT

1. Conversion of the sum into foreign currency from the cash account;2. Transfers.

MULTI-CURRENCY ACCOUNT TRANSACTIONS

Externally financed project funds management, accounting and reporting

CONSOLIDATED MULTI - CURRENCY ACCOUNT MANAGEMENT

3. Accounting of transfers to the account;4. Conversion into national currency of budget receipts

MULTI-CURRENCY ACCOUNT TRANSACTIONS

BUDGETARY ORGANIZATION

CURRENCY ACCOUNT

SWIFTE-TREASURY

NBG DONORS & TAXPAYERS

SWIFT MESSAGE

CONVERSION MESSAGE

CONSOLIDATED ACCOUNT

STATE TREASURY

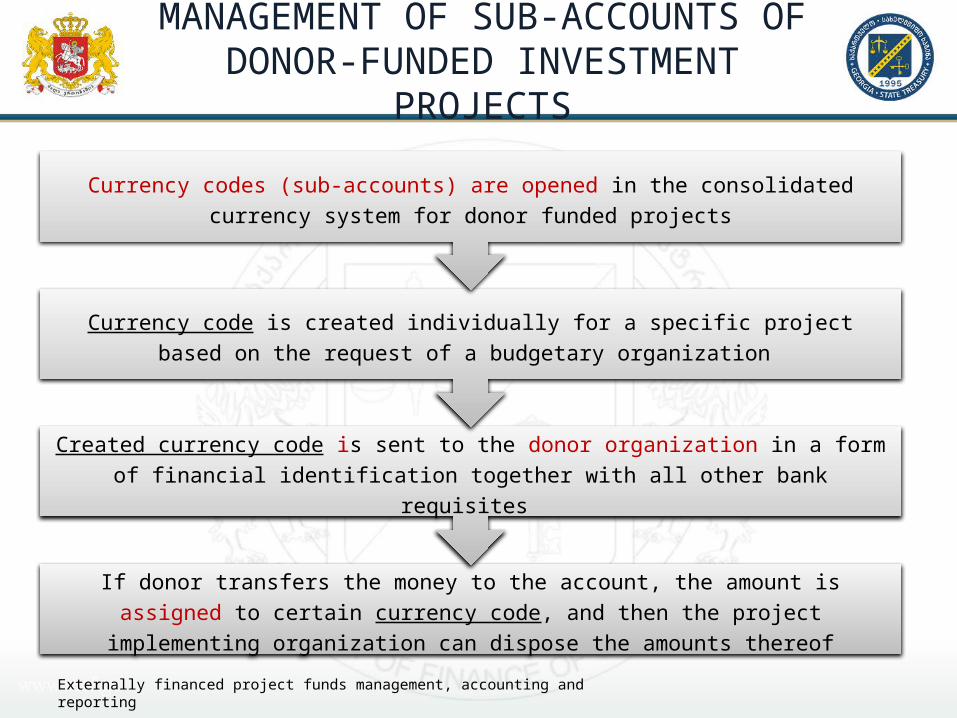

If donor transfers the money to the account, the amount is assigned to certain currency code, and then the project implementing organization can dispose the amounts thereof

Created currency code is sent to the donor organization in a form of financial identification together with all other bank requisites

Currency code is created individually for a specific project based on the request of a budgetary organization

Currency codes (sub-accounts) are opened in the consolidated currency system for donor funded projects

Externally financed project funds management, accounting and reporting

MANAGEMENT OF SUB-ACCOUNTS OF DONOR-FUNDED INVESTMENT PROJECTS

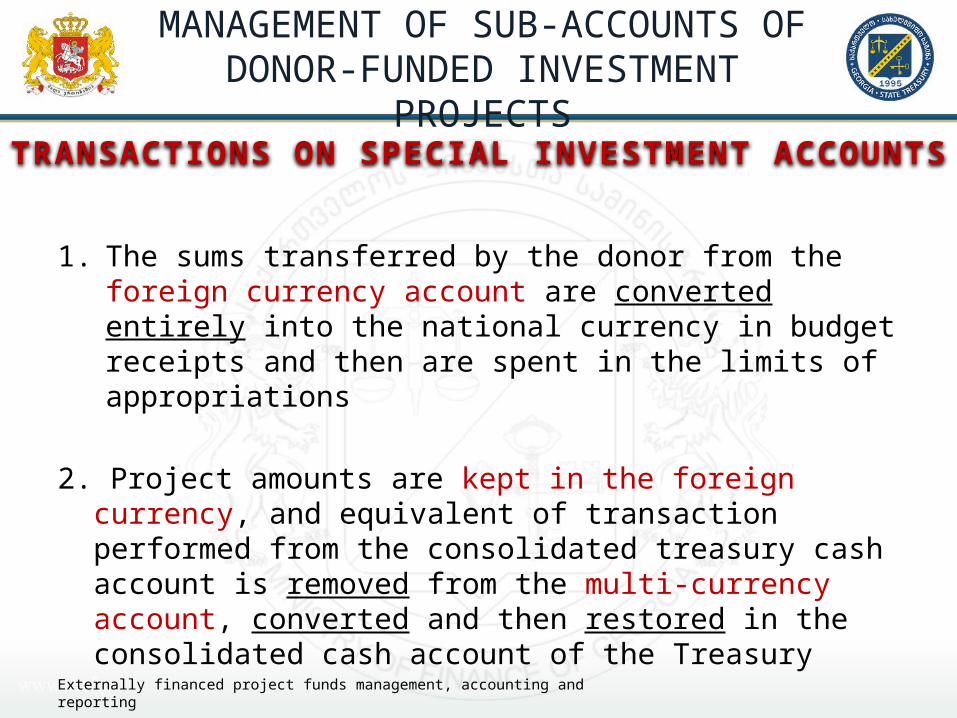

1. The sums transferred by the donor from the foreign currency account are converted entirely into the national currency in budget receipts and then are spent in the limits of appropriations

2. Project amounts are kept in the foreign currency, and equivalent of transaction performed from the consolidated treasury cash account is removed from the multi-currency account, converted and then restored in the consolidated cash account of the Treasury

Externally financed project funds management, accounting and reporting

MANAGEMENT OF SUB-ACCOUNTS OF DONOR-FUNDED INVESTMENT PROJECTS

TRANSACTIONS ON SPECIAL INVESTMENT ACCOUNTS

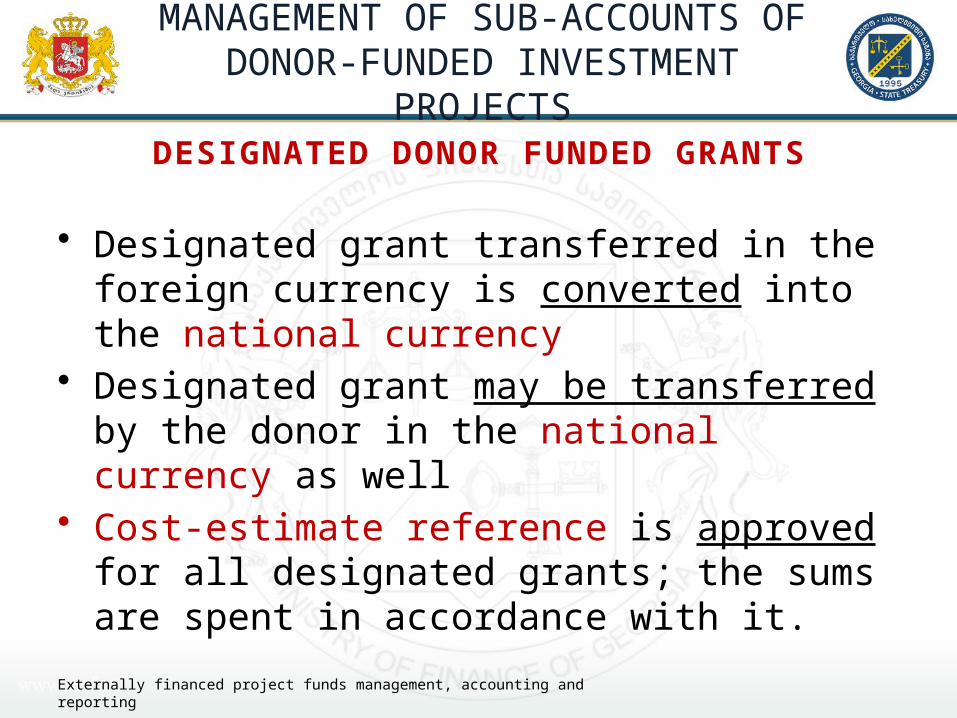

• Designated grant transferred in the foreign currency is converted into the national currency

• Designated grant may be transferred by the donor in the national currency as well

• Cost-estimate reference is approved for all designated grants; the sums are spent in accordance with it.

Externally financed project funds management, accounting and reporting

MANAGEMENT OF SUB-ACCOUNTS OF DONOR-FUNDED INVESTMENT PROJECTS

DESIGNATED DONOR FUNDED GRANTS

Thank you for attention!

www.mof.gewww.treasury.gov.ge

Zaza RukhaiaFebruary, 2012

EXTERNALLY FINANCED PROJECT FUNDS MANAGEMENT, ACCOUNTING AND REPORTING