ey oil and gas pe perspective - ief oil and gas – pe perspective ... petrobras (nts), nggd and...

TRANSCRIPT

Click to edit Master title style

The better the question. The better the answer.

The better the world works.

EY Oil and Gas – PE perspective

March 2017

Click to edit Master title style

Contents

1. PE investment in the context of industry capital raising 2

2. PE as a finance ‘multiplier’ 7

3. PE as a driver of the unconventional industry 11

4. PE as a driver of behavior and change 15

Click to edit Master title style Industry structure

PE investment in the context of industry capital raising

Oil & Gas — EY’s global perspective 3

Private equity is a small proportion of the total capital invested in the industry

Source: EY Global Oil and Gas transactions review 2016, 1Derrick

62 74 63 81

248 237 246 209

362

461

366

241

28.4

19.6

19.4

15.9

4%

2% 3% 3%

2013 2014 2015 2016

PE investments

Loans

Bonds

Equity

PE as a % of overall capitalraised

Capital raised (US$b) • Capital raised by oil and gas

companies during 2016

continued to remain under

pressure

• Equity markets received a

boost, mainly from a few

sizeable new IPOs and several

follow-on offerings from US

shale companies.

• Debt market for investment-

grade bonds remained relatively

robust, albeit at lower levels

than 2015

• Surge in activity in Q4 2016

Post oil price decline, PE firms have followed a “wait-and-watch” approach for investing in the sector, accounting for approximately 2-4% of the total capital raised globally (between 2013-2016)

Note: To analyse yearly trends in deal value, mega 2016 PE deals considered as outliers and excluded from analysis, which includes PE investment in Rosneft, Petrobras (NTS), NGGD and Essar Oil.

Oil & Gas — EY’s global perspective 4

Industry structure

PE as a finance ‘multiplier’

Oil & Gas — EY’s global perspective 5

PE has the capacity to invest a great deal more than it has recently

Source: Preqin Special Report: North American Oil & Gas, November 2016

Note*: 2016 numbers are till October 2016

North America-focused oil and gas fundraising

40 43

35

19

US$39.0b

US$[VALUE]b

US$[VALUE]b

US$[VALUE]b

US$[VALUE]b

US$[VALUE]b

US$[VALUE]b

US$[VALUE]b

2013 2014 2015 2016*

No. of funds closed Aggregate Capital Raised Average ticket size

• Despite price volatility, PE oil and gas fund raising has not been impacted significantly. 2016 saw US$33.9b

of funds raised for investment in North-America alone.

• Average ticket size for each fund increased to US$1.8 b in 2016 compared with US$1b in 2013.

• Significant capital overhang in the industry from past fund-raisings, not much that has been raised could be

invested; close to US$100b still available as dry powder capital for investments.

• PE will typically use leverage of 1-1.5x equity (in the US) to magnify its investment.

Oil & Gas — EY’s global perspective 6

Industry structure

PE as a driver of the unconventional industry

Oil & Gas — EY’s global perspective 7

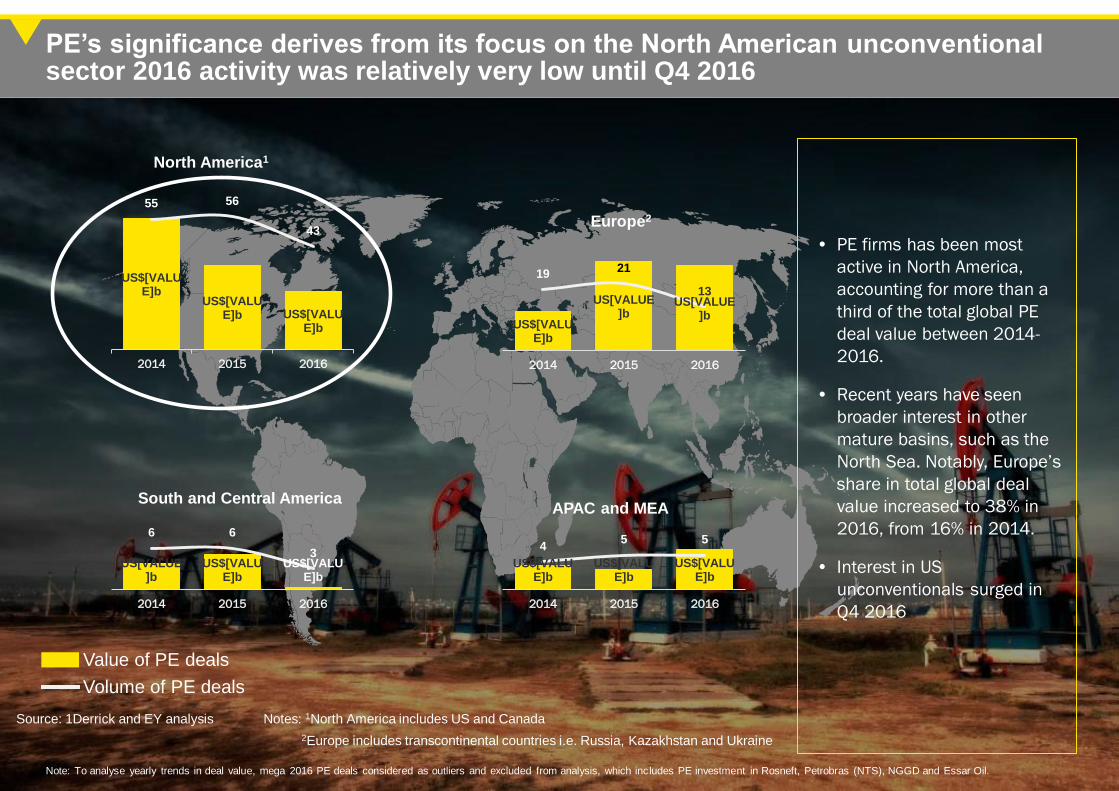

US$[VALUE]b

US$[VALUE]b US$[VALU

E]b

55 56

43

2014 2015 2016

US[VALUE]b

US$[VALUE]b

US$[VALUE]b

6 6

3

2014 2015 2016

US$[VALUE]b

US[VALUE]b

US[VALUE]b

19 21

13

2014 2015 2016

US$[VALUE]b

US$[VALUE]b

US$[VALUE]b

4 5 5

2014 2015 2016

South and Central America

Europe2

APAC and MEA

• PE firms has been most

active in North America,

accounting for more than a

third of the total global PE

deal value between 2014-

2016.

• Recent years have seen

broader interest in other

mature basins, such as the

North Sea. Notably, Europe’s

share in total global deal

value increased to 38% in

2016, from 16% in 2014.

• Interest in US

unconventionals surged in

Q4 2016

Value of PE deals

Volume of PE deals

Source: 1Derrick and EY analysis Notes: 1North America includes US and Canada

2Europe includes transcontinental countries i.e. Russia, Kazakhstan and Ukraine

PE’s significance derives from its focus on the North American unconventional sector 2016 activity was relatively very low until Q4 2016

North America1

Note: To analyse yearly trends in deal value, mega 2016 PE deals considered as outliers and excluded from analysis, which includes PE investment in Rosneft, Petrobras (NTS), NGGD and Essar Oil.

Oil & Gas — EY’s global perspective 8

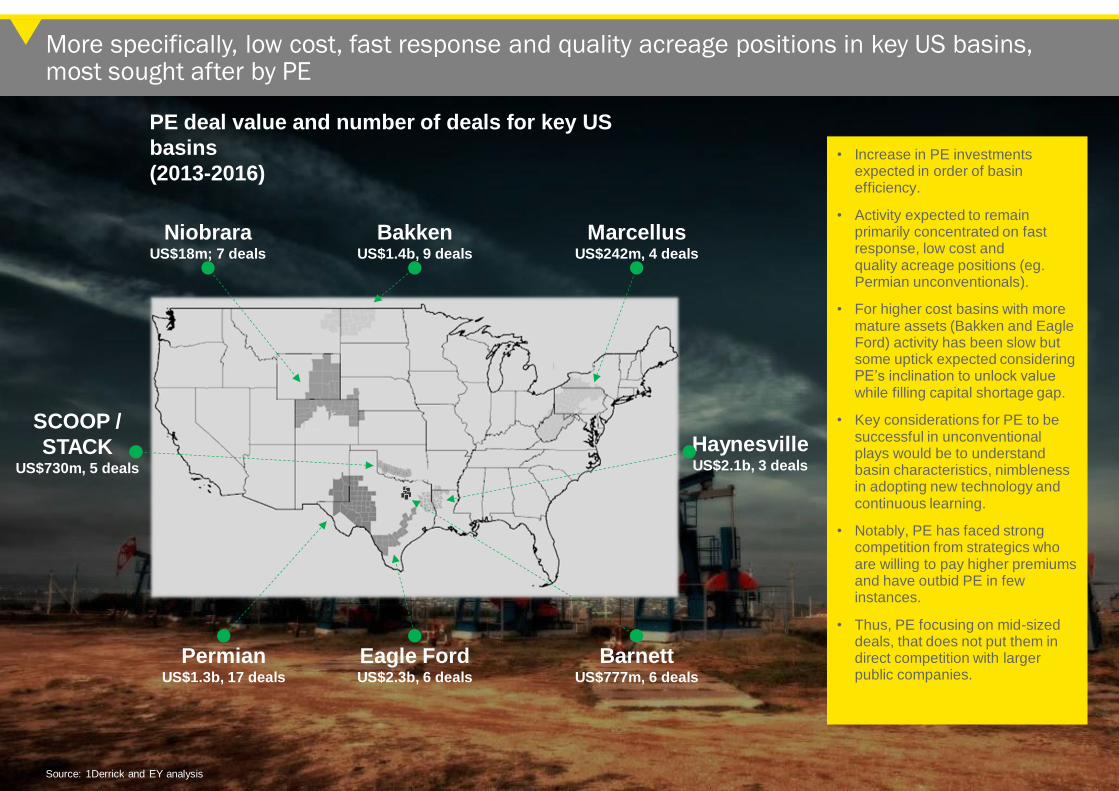

More specifically, low cost, fast response and quality acreage positions in key US basins, most sought after by PE

• Increase in PE investments expected in order of basin efficiency.

• Activity expected to remain primarily concentrated on fast response, low cost and quality acreage positions (eg. Permian unconventionals).

• For higher cost basins with more mature assets (Bakken and Eagle Ford) activity has been slow but some uptick expected considering PE’s inclination to unlock value while filling capital shortage gap.

• Key considerations for PE to be successful in unconventional plays would be to understand basin characteristics, nimbleness in adopting new technology and continuous learning.

• Notably, PE has faced strong competition from strategics who are willing to pay higher premiums and have outbid PE in few instances.

• Thus, PE focusing on mid-sized deals, that does not put them in direct competition with larger public companies.

Eagle Ford US$2.3b, 6 deals

Barnett US$777m, 6 deals

Haynesville US$2.1b, 3 deals

Marcellus US$242m, 4 deals

SCOOP /

STACK US$730m, 5 deals

Bakken US$1.4b, 9 deals

Niobrara US$18m; 7 deals

Permian US$1.3b, 17 deals

PE deal value and number of deals for key US

basins

(2013-2016)

Source: 1Derrick and EY analysis

Oil & Gas — EY’s global perspective 9

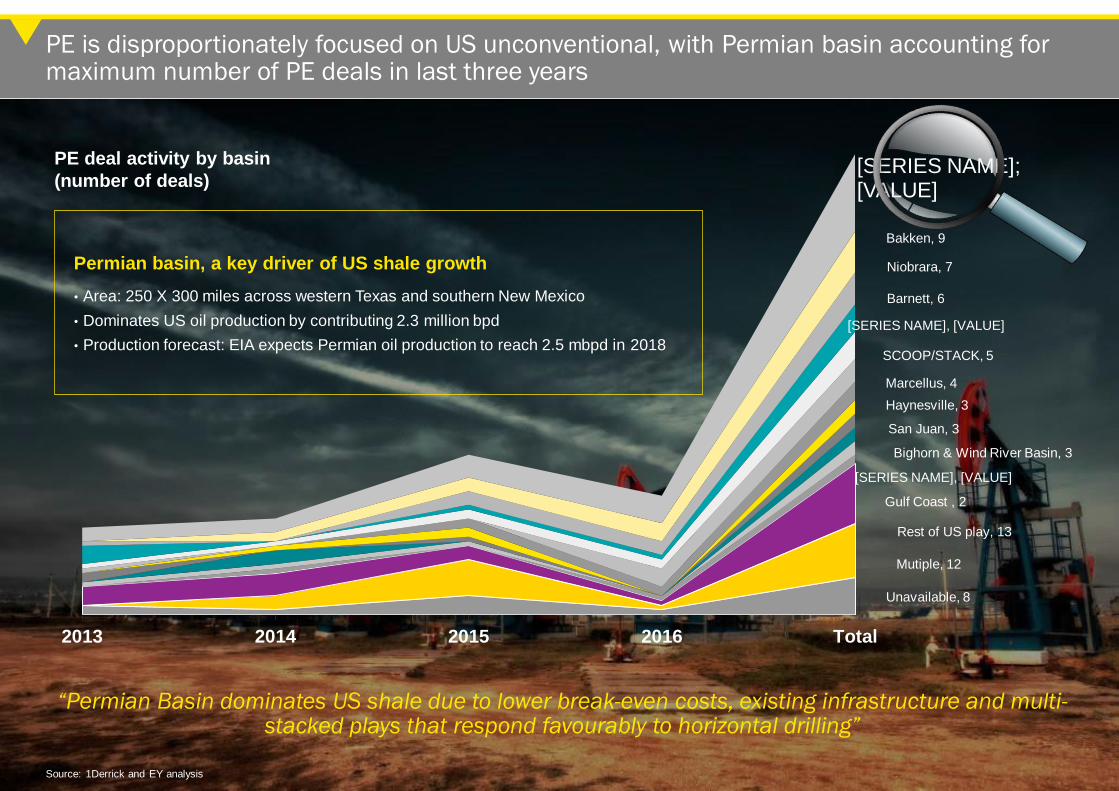

PE is disproportionately focused on US unconventional, with Permian basin accounting for maximum number of PE deals in last three years

Unavailable, 8

Mutiple, 12

Rest of US play, 13

Gulf Coast , 2

[SERIES NAME], [VALUE]

Bighorn & Wind River Basin, 3

San Juan, 3

Haynesville, 3

Marcellus, 4

SCOOP/STACK, 5

[SERIES NAME], [VALUE]

Barnett, 6

Niobrara, 7

Bakken, 9

[SERIES NAME]; [VALUE]

2013 2014 2015 2016 Total

Permian basin, a key driver of US shale growth

• Area: 250 X 300 miles across western Texas and southern New Mexico

• Dominates US oil production by contributing 2.3 million bpd

• Production forecast: EIA expects Permian oil production to reach 2.5 mbpd in 2018

PE deal activity by basin

(number of deals)

Source: 1Derrick and EY analysis

“Permian Basin dominates US shale due to lower break-even costs, existing infrastructure and multi-stacked plays that respond favourably to horizontal drilling”

Oil & Gas — EY’s global perspective 10

Asset level deals, specifically producing assets/ development asset, remain favorite with PE firms

0.2

2.9 1.9

4.9

3.7

0.9

0.1

0.5

0.1

1.6

2013 2014 2015 2016

Breakup of deal type by value (US$b)

Corporate deals Producing assets Developing assets

1

6 2 2

15

12 20

14

3 3

12

10

2013 2014 2015 2016

Breakup of deal type by number

Corporate deals Producing assets Developing assets

Key points

Asset type deals dominate PE transaction landscape. Key drivers include:

► Majors and independents coring down their portfolio of assets (not necessarily bad assets)

► Either they need capital to shore up their balance sheets, or

► Drill down to focus on one or two areas (basins or offshore/onshore) resulting in divestiture of the assets in

other regions/ segment

► Distressed asset deals from operators in need to boost liquidity and pay down debt.

► Relatively lesser technical/ exploration risk in producing assets compared with developing or underdevelopment

assets.

US$2.3b

US$8.2b

US$3.8b

US$2.6b

19 21

34

26

Source: 1Derrick and EY analysis

Note: To analyse yearly trends in deal value, mega 2016 PE deals considered as outliers and excluded from analysis, which includes PE investment in Rosneft, Petrobras (NTS), NGGD and Essar Oil.

Oil & Gas — EY’s global perspective 11

Industry structure

PE as a driver of behavior and change

Oil & Gas — EY’s global perspective 12

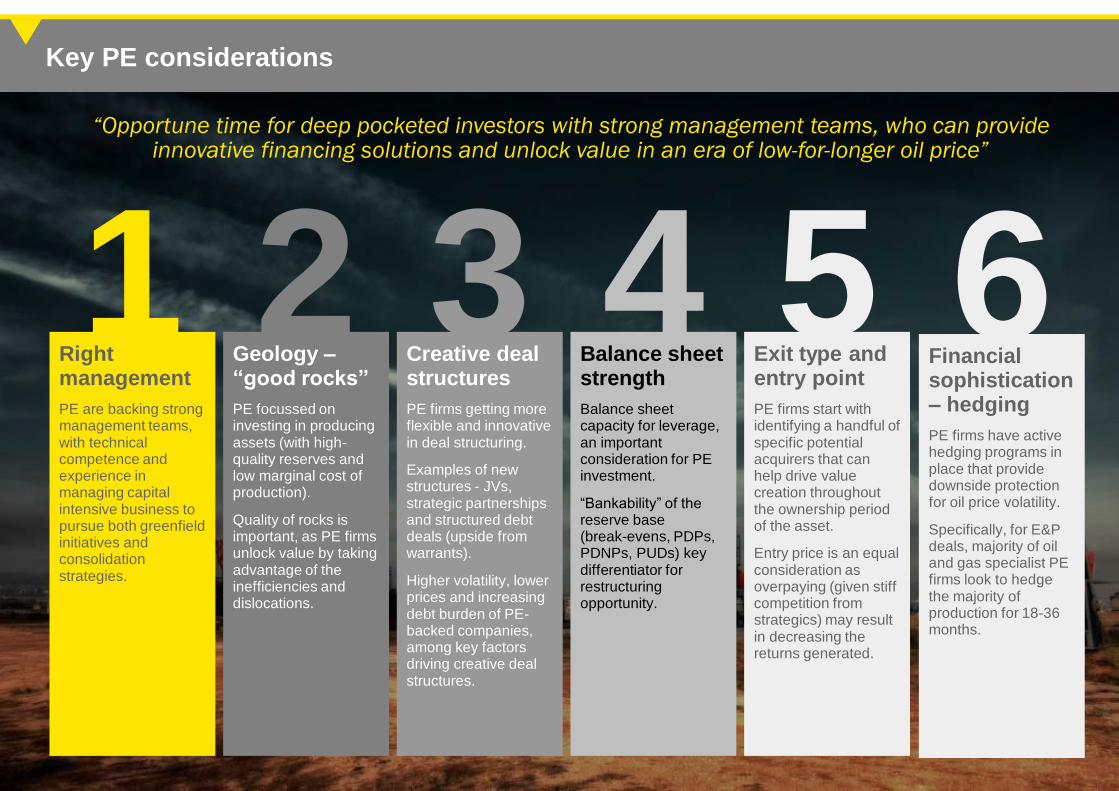

“Opportune time for deep pocketed investors with strong management teams, who can provide innovative financing solutions and unlock value in an era of low-for-longer oil price”

Right management

PE are backing strong management teams, with technical competence and experience in managing capital intensive business to pursue both greenfield initiatives and consolidation strategies.

1 Geology – “good rocks”

PE focussed on investing in producing assets (with high-quality reserves and low marginal cost of production).

Quality of rocks is important, as PE firms unlock value by taking advantage of the inefficiencies and dislocations.

2 Creative deal structures

PE firms getting more flexible and innovative in deal structuring.

Examples of new structures - JVs, strategic partnerships and structured debt deals (upside from warrants).

Higher volatility, lower prices and increasing debt burden of PE-backed companies, among key factors driving creative deal structures.

3 Balance sheet strength

Balance sheet capacity for leverage, an important consideration for PE investment.

“Bankability” of the reserve base (break-evens, PDPs, PDNPs, PUDs) key differentiator for restructuring opportunity.

Exit type and entry point

PE firms start with identifying a handful of specific potential acquirers that can help drive value creation throughout the ownership period of the asset.

Entry price is an equal consideration as overpaying (given stiff competition from strategics) may result in decreasing the returns generated.

5 4 Financial sophistication – hedging

PE firms have active hedging programs in place that provide downside protection for oil price volatility.

Specifically, for E&P deals, majority of oil and gas specialist PE firms look to hedge the majority of production for 18-36 months.

6

Key PE considerations

Oil & Gas — EY’s global perspective 13

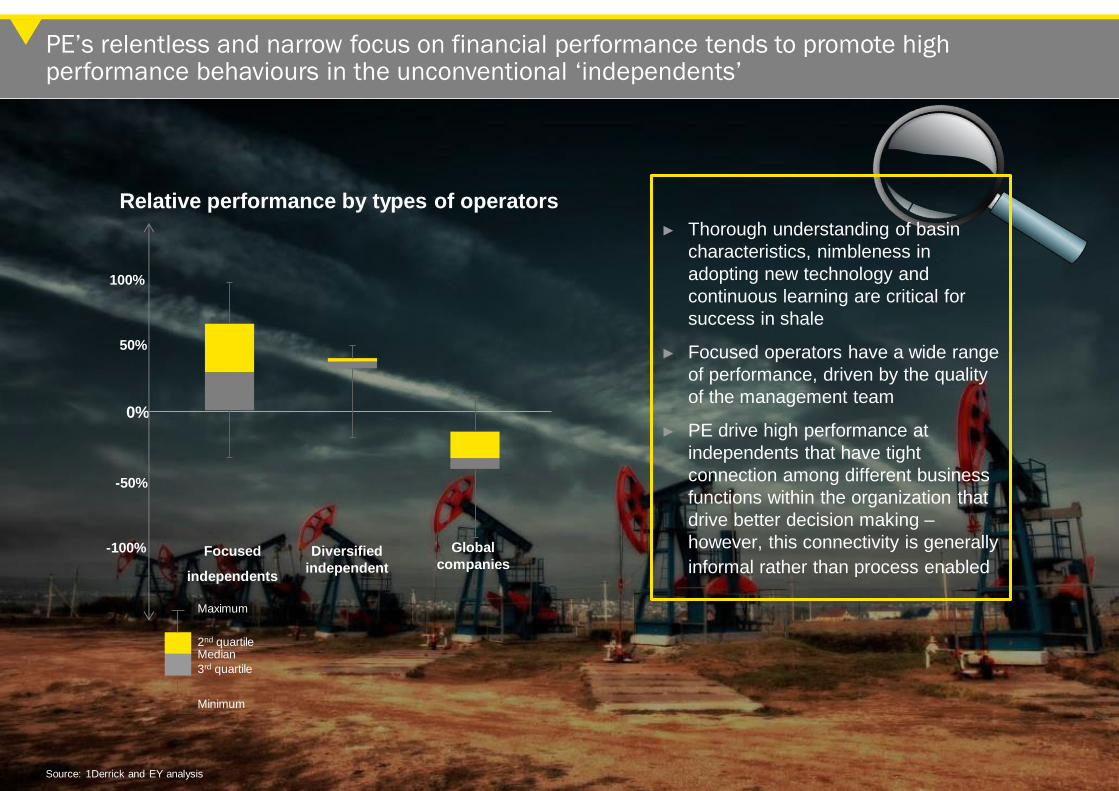

PE’s relentless and narrow focus on financial performance tends to promote high performance behaviours in the unconventional ‘independents’

Source: 1Derrick and EY analysis

0%

Diversified

independent

100%

-100%

-50%

50%

Focused

independents

Global

companies

2nd quartile

3rd quartile

Median

Maximum

Minimum

Relative performance by types of operators

► Thorough understanding of basin

characteristics, nimbleness in

adopting new technology and

continuous learning are critical for

success in shale

► Focused operators have a wide range

of performance, driven by the quality

of the management team

► PE drive high performance at

independents that have tight

connection among different business

functions within the organization that

drive better decision making –

however, this connectivity is generally

informal rather than process enabled

Oil & Gas — EY’s global perspective 14

EY

Assurance | Tax | Transactions | Advisory

About EY

EY is a global leader in assurance, tax, transaction and advisory services. Worldwide, our

230,000 people are united by our shared values and an unwavering commitment to quality.

We make a difference by helping our people, our clients and our wider communities achieve

their potential.

For more information, please visit

www.ey.com.

EY refers to the global organization of

member firms of EY Global Limited, each of

which is a separate legal entity. EY Global

Limited, a UK company limited by guarantee, does not

provide services to clients. For more information about

our organization.

EY LLP is a client-serving member firm of

EY Global and of EY Americas

operating in the US.

© 2017 EYGM Limited. All Rights Reserved.

This publication contains information in summary form and is therefore intended for general guidance only. It is not

intended to be a substitute for detailed research or the exercise of professional judgment. Neither EYGM Limited nor

any other member of the global EY organization can accept any responsibility for loss occasioned to any person acting

or refraining from action as a result of any material in this publication. On any specific matter, reference should be

made to the appropriate advisor.