ey.com/ipsas ipsas outlookfile/ey... · ipsas outlook highlights from our global ipsas update...

TRANSCRIPT

ey.com/IPSAS

August 2013

IPSAS issues for public finance management executives

IPSAS Outlook

Highlights from our global IPSAS update webcast 2

IPSASB publishes RPG 1 and RPG 2 4

IPSASB project update 7

Resources 10

In this issue ...

Highlights from our global IPSAS update webcast Read the highlights from our recent global IPSAS update webcast covering the IPSASB’s major projects and the IPSAS adoption landscape globally.

IPSASB publishes RPG 1 Long-Term Sustainability of Public Finances and RPG 2 Financial Statement Discussion and Analysis Read our summary of the recommended practice guidelines issued by the IPSASB recently.

IPSASB project update See a summary of the recent Board discussions on key projects during its June 2013 meeting.

Resources Look here for a recent list of our publications.

A message from Thomas Müller-Marqués Berger

Welcome to this month’s edition of IPSAS Outlook, which brings you insights into recent IPSAS developments and emerging issues. In addition, we bring you regular reports on IPSAS projects from around the world and we share some of the experiences of our Global IPSAS network. I hope you will find this of assistance to your organization.

We welcome your feedback on IPSAS Outlook. Please contact us at [email protected].

Thomas Müller-Marqués Berger, IPSAS Global Leader

2 IPSAS Outlook August 2013

Highlights from our global IPSAS update webcast

Back in June this year, we held our first global IPSAS update webcast and were joined by over a thousand participants spanning across the globe at this live interactive event.1 Our webcast covered the IPSASB’s latest activities; gave an update on the latest decisions made on some of the IPSASB’s high profile projects; and gave a snapshot on the IPSAS adoption landscape globally, including the latest update on the EU’s IPSAS implementation plan for EU Member States. Our special guest, Ian Carruthers, also shared with audience some of his experience when the UK went through its accounting transformation in the 1990s. After the webcast, we asked lead panelist, Thomas Mueller-Marques Berger, for his thoughts of the event.

Q: Could you share with us some of the highlights of the webcast?

A: Certainly. Let me begin by saying that I was very glad to have Ian Carruthers (CIPFA2 and IPSAS Board member) and George Higgins (EY South Africa Professional Practice Group) join us on the webcast. Their experiences in public sector accounting transformations have enriched and enlivened discussions during the event.

The timing of the webcast, a few days after the June IPSASB meeting, enabled us to share with the audience the latest decisions made by the IPSASB. At that meeting, the IPSASB approved two recommended practice guidelines, which are discussed in more details in this issue of IPSAS Outlook. The Board also considered feedback received on proposals contained in the Conceptual Framework exposure drafts Phases 2 and 3 – elements and measurement in financial statements, respectively.3 Unsurprisingly, the proposal in Phase 2 to define deferred inflows and deferred outflows as elements generated quite a lot of debate and wasn’t popular with respondents. The Board has not yet made any tentative decisions on what to do with such classes of transactions. It will be something to look out for. In my view, if it is not discussed in the Conceptual Framework, it will have to be addressed as a separate project in a separate standard.

1 The archived webcast Public Sector Accounting: IPSAS Update 2013 can be accessed at http://www.ey.com/GL/en/Issues/webcast_2013‐06‐26‐0700_public‐sector‐accounting‐ipsas‐update‐2013‐replay

2 The Chartered Institute of Public Finance and Accountancy 3 Conceptual Framework Phase 2: Elements and Recognition in Financial Statements and Conceptual Framework Phase 3: Measurement of Assets and Liabilities in Financial Statements

Q: Could you also talk us through some of the other topics covered during the webcast that were recently discussed by the Board?

A: At recent meetings, the Board has also been discussing the issues around consolidation in the public sector context as part of the project on the revision of IPSASs 6-8. 4

The capital injection by governments into banks and other private sector entities, as a result of the global economic crisis, has meant that governments have, at times, effectively acquired a significant stake in these entities. And because the terms and conditions of each bail-out differ, it is often not clear whether a government truly controls the entities that it bailed out, and whether the government would be required to consolidate these entities into its balance sheet. When discussing the issue of control, the Board has often considered what ‘control’ means in a bail-out situation.

While the Board is still working towards an ED, some Board members are not certain that a full consolidation in the circumstances where governments obtain control of entities under financial distress is appropriate. During the Boards’ discussions, alternatives to full consolidation were discussed, including the use of the equity method, with extensive disclosures in such exceptional circumstances. Additionally, in many of these bail-out situations, control is presumably ‘temporal’ in nature, and the government involved has no intention and, indeed, does not demonstrate ‘control’ of the entities it bailed out by actively being involved in making operational and financial policy decisions. Once the ED is finalized, constituents will have an opportunity to respond to the proposals of the Board in due course. I would encourage everyone to give some consideration to the proposal, and respond to the ED in due course.

4 IPSAS 6 Consolidated Financial Statements, IPSAS 7 Investments in Associates, IPSAS 8 Interests in Joint Ventures

IPSAS Outlook August 2013 3

Another topic covered in the webcast was the IPSASs and statistical reporting project. The Board discussed responses to the consultation paper during their June meeting and was somewhat disappointed to receive only 25 responses. In part, this may reflect the difficulty in bringing accountants and statisticians together and for them to understand the approach the other is taking. The Board has agreed that the Task Force should consider the responses received to produce a definitive table of IPSAS and Government Finance Statistics (GFS) differences, and a brief summary of the choices needed within IPSAS, to produce GFS-compliant numbers.

The alignment of the control definitions is already being worked on through the IPSASs 6-8 revision project, but more major projects such as an update or replacement for IPSAS 22 Disclosure of Financial Information about the General Government Sector need to be considered alongside the other potential projects in the 2014 Work Plan, which the Board is starting to develop.

It is also interesting to share the feedback we received for one of the polling questions during the webcast. When we asked our audience which project would be their top priority, a majority voted for revenue recognition.

Q: Another topic that panelists discussed was on IPSAS adoption and implementation. Could you summarize what was discussed during the webcast?

A: Sure. Moving on to this discussion on the IPSAS adoption landscape globally, it is important to highlight that within each region, several countries are considering, or are in the process of, implementing IPSAS. Having said that, the starting points and implementation approaches are very heterogeneous. Many countries are starting from a cash basis, such as Austria, Brazil and Malaysia. Others are starting from an accrual basis, or even IFRS in New Zealand’s case. Looking at current adoption projects, we see quite ambitious approaches globally. For example, Brazil decided to convert all levels of government, including federal government, 26 states and more than 3000 municipalities to IPSAS with effect from 1 January 2015. The same date of transition was also chosen by Malaysia and Nigeria.

On the topic of IPSAS implementation challenges, our panelists highlighted the importance of the involvement of other functions within an entity, such as IT, legal and risk management. The political support and legislative framework are also crucial for a successful public finance transformation program. Conversion to an accrual accounting framework such as IPSAS will certainly impact areas outside of the accounting function.

For those who are interested, this webcast is currently available on-demand on our EY Thought Center Webcasts website at www.ey.com/GL/en/Issues/Thought-center-webcasts

4 IPSAS Outlook August 2013

IPSASB publishes RPG 1 Long-Term Sustainability of Public Finances and RPG 2 Financial Statement Discussion and Analysis

RPG 1 Long-Term Sustainability of Public Finances 5

In July 2013, the IPSASB issued its first Recommended Practice Guideline (RPG 1): Reporting on the Long-Term Sustainability of an Entity’s Finances. An entity that aims to be in-compliance with IPSAS is not required to apply the RPG, but is highly recommended to adopt the guidelines. On the issuance of RPG 1, IPSASB Chair, Andreas Bergmann said, “RPG 1 provides straightforward guidance on presenting information about the capacity of an entity to provide social benefits at existing levels, to maintain existing taxation revenues, and to meet its financial commitments. By developing guidance on reporting information about the long-term sustainability of an entity’s finances, RPG 1 reflects the IPSASB Conceptual Framework’s position that, in order to meet users’ needs, the scope of financial reporting is more comprehensive than the financial statements.” 6 The following is a summary of the guidelines in RPG 1.

Objective, status and scope

The objective of this RPG is to provide guidance on the reporting of the long-term sustainability of a public sector entity’s finances (or the reporting of long-term fiscal sustainability information). The aim of such reporting is to provide an indication of the projected long-term sustainability of an entity’s finances over a specified time horizon in accordance with stated assumptions.

The scope of this RPG includes an entity’s projected inflows and outflows and is not limited to those flows related to programs providing social benefits. Nevertheless, the RPG acknowledges that the flows relating to programs providing social benefits, including entitlement programs that require contributions from participants, can be a highly significant component of reporting long-term fiscal sustainability information for many entities.

Although the reporting of environmental sustainability is not directly addressed in this RPG, an entity should assess the financial impacts of environmental factors and take them into account when developing its projections.

5 RPG 1 can be accessed at https://www.ifac.org/sites/default/files/publications/files/RPG%201%20Long‐term%20Sustainability%20of%20Public%20Finances%20DRAFT%20July%2016,%202013_0.pdf

6 IPSASB press release IPSASB Publishes First Recommended Practice Guideline on the Long‐Term Sustainability of Public Finances, 24 July 2013. http://www.ifac.org/news‐events/2013‐07/ipsasb‐publishes‐first‐recommended‐practice‐guideline‐long‐term‐sustainability‐p

Whether to report long-term fiscal sustainability information

In determining whether to report long-term fiscal sustainability information, an entity needs to assess whether there are potential users of forward-looking financial information. Long-term fiscal sustainability information is broader than information derived from financial statements and includes projected inflows and outflows related to the provision of goods and services and programs providing social benefits using current policy assumptions over a specified time horizon. It therefore takes into account decisions made by the entity, on or before the reporting date, that will give rise to future outflows that do not meet the definition of and/or recognition criteria for liabilities at the reporting date. Similarly, it takes into account future inflows that do not meet the definition of and/or recognition criteria for assets at the reporting date.

Policies and decisions taken today have a long-term impact on future inflows and outflows of resources. Therefore there is a need for information on the consequences of such policies and decisions that supplement information on liabilities, expenses, assets, and revenues in the financial statements. Long-term fiscal sustainability information prepared in accordance with the RPG should enable users to assess various aspects of the long-term fiscal sustainability of the entity, including the nature and extent of financial risks that the entity faces.

Reporting long-term fiscal sustainability information

The form and content of an entity’s long-term fiscal sustainability information will vary depending on the nature of the entity and the regulatory environment in which it operates. A single presentation approach is unlikely to satisfy the objectives of financial reporting. In general, long-term fiscal sustainability information would include the following components:

► Projections of future inflows and outflows, which can be displayed in tabular statements or graphical formats, and a narrative discussion explaining the projections

► A narrative discussion of the dimensions of long-term fiscal sustainability including any indicators used to portray the dimensions

► A narrative discussion of the principles, assumptions and methodology underlying the projections

IPSAS Outlook August 2013 5

Revenue Dimension

Capacity to vary existing taxation levels or introduce new revenue

sources. Vulnerable to factors such as viability of increases in taxation levels or dependence on revenue

sources outside the entity’s control.

Debt Dimension Capacity to meet financial

commitments or refinance or increase debt. Vulnerable to factors

such as market and lender confidence and interest rate risk.

Service Dimension Capacity maintain or vary services

and entitlements. Vulnerable to factors such as viability of reductions in services and

entitlements.

Can entities collect sufficient revenue to maintain current services given debt constraints?

Can current services be maintained or varied given current revenue policies and debt constraints?

How sustainable is projected debt, given current service and revenue policies?

Projections should be prepared on the basis of current policy assumptions, and assumptions about future economic and other conditions. The appropriate selection of time horizon is also crucial. As time horizon increases, the assumptions underpinning the projections become less robust and potentially less verifiable. Conversely, excessively short time horizons may increase the risk that the consequences of events outside the time horizon would be ignored, thereby reducing the relevance of projections.

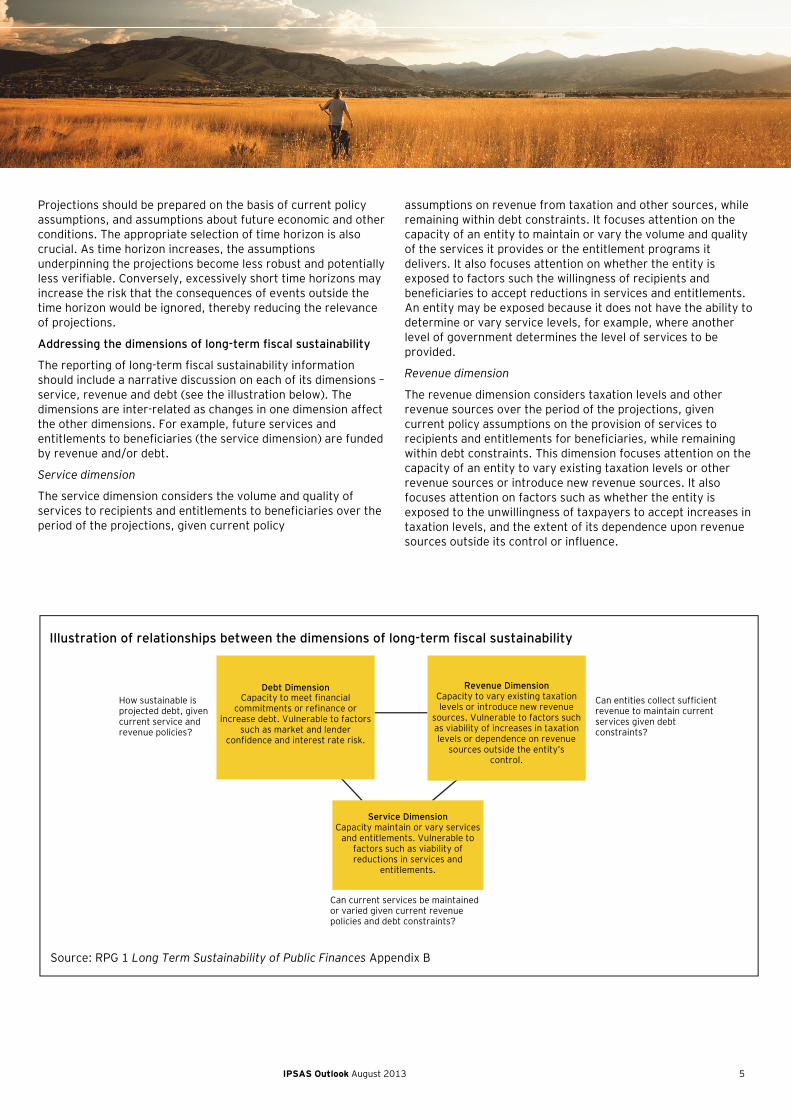

Addressing the dimensions of long-term fiscal sustainability

The reporting of long-term fiscal sustainability information should include a narrative discussion on each of its dimensions – service, revenue and debt (see the illustration below). The dimensions are inter-related as changes in one dimension affect the other dimensions. For example, future services and entitlements to beneficiaries (the service dimension) are funded by revenue and/or debt.

Service dimension

The service dimension considers the volume and quality of services to recipients and entitlements to beneficiaries over the period of the projections, given current policy

assumptions on revenue from taxation and other sources, while remaining within debt constraints. It focuses attention on the capacity of an entity to maintain or vary the volume and quality of the services it provides or the entitlement programs it delivers. It also focuses attention on whether the entity is exposed to factors such the willingness of recipients and beneficiaries to accept reductions in services and entitlements. An entity may be exposed because it does not have the ability to determine or vary service levels, for example, where another level of government determines the level of services to be provided.

Revenue dimension

The revenue dimension considers taxation levels and other revenue sources over the period of the projections, given current policy assumptions on the provision of services to recipients and entitlements for beneficiaries, while remaining within debt constraints. This dimension focuses attention on the capacity of an entity to vary existing taxation levels or other revenue sources or introduce new revenue sources. It also focuses attention on factors such as whether the entity is exposed to the unwillingness of taxpayers to accept increases in taxation levels, and the extent of its dependence upon revenue sources outside its control or influence.

Source: RPG 1 Long Term Sustainability of Public Finances Appendix B

Illustration of relationships between the dimensions of long-term fiscal sustainability

6 IPSAS Outlook August 2013

Debt dimension

The debt dimension considers debt levels over the period of the projections, given current policy assumptions on the provision of services to recipients and entitlements for beneficiaries, and revenue from taxation and other sources. This dimension focuses attention on the capacity of the entity to meet its financial commitments as they come due or to refinance or increase debt as necessary. It also focuses attention on whether the entity is exposed to market and lender confidence and interest rate risk.

The level of net debt is important for an assessment of the debt dimension, as, at any reporting date, it represents the amount expended on the past provision of goods and services that has to be financed in the future. Therefore, this indicator is likely to be relevant for many entities. By projecting current policy assumptions for the provision of goods and services, and for revenue from taxation and other sources, projected levels of net debt can be presented. This information assists users in assessing the entity’s ability to meet its financial commitments as they come due or to maintain, refinance or increase its levels of debt and thereby evaluate the sustainability of the entity’s debt.

RPG 2 Financial statement discussion and analysis 7

A couple of days after issuing RPG 1, the IPSASB published a second recommended practice guideline, RPG 2 Financial Statement Discussion and Analysis. The following is a summary of the guidelines in RPG 2.

The draft of this RPG 2 was finalized with some minor amendments at the last IPSASB meeting in June 2013. The aim of RPG 2 is to help users understand the financial position, financial performance, and cash flows presented in an entity’s general purpose financial statements. As it is a guideline and not a mandatory standard, entities that apply IPSAS are not obliged to adopt it. Similar to RPG 1, the IPSASB strongly recommends the implementation of RPG 2. It not only enables users to gain further insights into the operations of the entity, from the perspective of the entity itself, but also provides guidance for presenting such information.

7 RPG 2 can be accessed at https://www.ifac.org/sites/default/files/publications/files/RPG%202%20Financial%20Statement%20Discussion%20and%20Analysis%20July%2016,%202013%20DRAFT.pdf

Financial statement discussion and analysis should always include:

► An overview of the entity’s operations and the environment in which it operates

► Information about the entity’s objectives and strategies that relate to the financial statements

► An analysis of the entity’s financial statements including significant changes and trends

► Risks and uncertainties related to the financial statements

However, the form and content of the information depends on the nature of the entity and its regulatory environment.

In its press release on the publication of RPG 2, Bergmann explains, “Financial statement discussion and analysis presented in accordance with RPG 2 represents good practice. It sets out the status, scope, and reporting boundary for the information. RPG 2 is intended to encourage more public sector entities to provide users with financial statement discussion and analysis.” Furthermore, he commented on the advantage of comparability and flexibility of application, “it will promote comparability across entities that present financial statement discussion and analysis; at the same time, its flexible application will benefit entities in jurisdictions that have local requirements or regulations. The issuance of RPG 2 is an important step for the IPSASB, because it further extends our pronouncements on presentation of information beyond presented in general purpose financial statements.”

IPSAS Outlook August 2013 7

IPSASB project update

What’s new? The following table shows new publications issued by the IPSASB:

Projects Publication

RPG 1 Reporting on the Long-Term Sustainability of an Entity’s Finances

At the June 2013 IPSASB meeting, the Board approved for issuance RPG 1 Reporting on the Long-Term Sustainability of an Entity’s Finances. This RPG was issued on 24 July 2013. See page 4 of this Outlook for further details.

RPG 2 Financial Statement Discussion and Analysis

The Board also approved for issuance RPG 2 Financial Statement Discussion and Analysis at the June 2013 meeting. This RPG was published on 26 July 2013. See page 5 of this Outlook for further details.

Preface to the Conceptual Framework for General Purpose Financial Reporting by Public Sector Entities

The IPSASB has published the Preface to the Conceptual Framework for General Purpose Financial Reporting by Public Sector Entities as a preliminary Board view. The Preface highlights characteristics of the public sector that underpin the development of IPSASs and RPGs. It can be accessed at www.ifac.org/public-sector

The IPSASB June 2013 Meeting – current discussions

Topic Current discussion

Conceptual Framework

As there are concerns about pressure on the timetable for the finalization of the Conceptual Framework, the IPSASB agreed that the timetable should be considered further at the September meeting.

Given that the International Accounting Standards Board’s (IASB) reinitiated its Framework project, the IPSASB discussed the relationship between the IASB and IPSASB’s Framework projects at this meeting, in light of the projected issuance of the IASB’s Discussion Paper (DP) in July 2013. The IPSASB reaffirmed that the IPSASB’s Conceptual Framework is a public sector-critical project that needs to respond to public-sector specific characteristics. The IPSASB staff will review the IASB’s DP in order to avoid differences in definitions and terminology that are unwarranted by public sector circumstances.

It was agreed that it should be communicated clearly why the IPSASB Framework will differ from the IASB Framework within the IPSASB’s Conceptual Framework.

As part of this communication, the IPSASB agreed to publish the Preface as a preliminary Board view in July 2013.

Conceptual Framework Phase 2 Elements and Recognition in Financial Statements

The comment period for the Exposure Draft (ED) Elements and Recognition in Financial Statements ended in April 2013. The IPSASB received 40 responses during the public consultation and staff presented feedback received at this meeting.

The most controversial aspect in the ED is the Board’s proposal to define deferred inflows and deferred outflows as elements. A majority of the respondents do not support the proposal. From the feedback received, a wide range of approaches were suggested by respondents on dealing with flows that contain timing restrictions, the IPSASB directed staff to undertake an analysis of financial performance and financial position for the September meeting.

Further discussions were about assets and liabilities. The IPSASB tentatively reaffirmed that the definition of an asset should include control as an essential characteristic rather than treating control as recognition criterion, and that the definition of both an asset and a liability should include a past event(s) as an essential characteristic.

The discussion about the definitions of revenue and expenses were deferred as these are largely dependent on decisions on deferred inflows and deferred outflows.

8 IPSAS Outlook August 2013

Topic Current discussion

Conceptual Framework Phase 3 Measurement of Assets and Liabilities in Financial Statements

The public consultation of the Measurement of Assets and Liabilities in Financial Statements ED also ended in April. Thirty-seven responses were received. The IPSASB reviewed and discussed the staff’s analysis of comments received at this meeting.

The IPSASB tentatively reaffirmed that fair value would not be adopted as a measurement basis for the public sector largely because of the specific meaning of the term ‘fair value’ in IFRS 13 Fair Value Measurement. However, the extent to which market value is applicable to non-specialized operational assets should be made clearer. In response to feedback received, the IPSASB tentatively decided that while some of the perspectives in both the fair value and deprival value models should be retained, the models themselves would not be included in the final guidance.

Reporting on the Long-Term Sustainability of an Entity’s Finances

After reviewing a further version of draft RPG Reporting on the Long-Term Sustainability of a Public Sector Entity’s Finances and some minor modifications, the RPG was issued at the end of July. See our summary of the guideline on page 4.

Financial Statement Discussion and Analysis

The IPSASB reviewed a draft RGP, Financial Statement Discussion and Analysis. The final version was published as RPG 2 at the end of July. See our summary of the guideline on page 6.

Reporting Service Performance Information

The Board decided that Reporting Service Performance Information will be developed as a RPG as well. Despite being a RPG, and not an authoritative standard, the Board thought that it should acknowledge that some selection of services will always be necessary, and guidance on how this should be done should be provided and the relevant factors or criteria for such selection be included. Furthermore, the RPG should also provide guidance on the types of performance indicators to be chosen and the guidance should tie the choice of indicators back to objectives, encourage reporting that goes beyond outputs to outcomes, and note the circumstances in which an entity is reporting.

It is anticipated that an ED of this RPG will be further developed for consideration at the IPSASB’s September 2013 meeting.

Government Business Enterprises (GBEs)

A survey conducted with Board members in December 2012 revealed a wide spectrum of entities being treated as GBEs across jurisdictions. During this meeting, the IPSASB considered that there are four options on the way forward:

(i) Not to define GBEs, leaving jurisdictions to make their own decisions on which entities are profit-oriented and should apply IFRS or national private sector GAAP

(ii) Clarify the existing definition for easier application and achieve greater consistency (iii) Narrow the existing definition to reduce current diversity in practice (iv) Redefine GBEs based on services or objectives

IPSASB staff will prepare a draft consultation paper (CP) proposing the characteristics of entities to be considered when deciding whether to apply IPSASs to public sector entities.

First-Time Adoption of Accrual Basis IPSASs

During this meeting, the IPSASB discussed an analysis of the transitional accounting issues for IPSAS 28 Financial Instruments: Presentation, IPSAS 29 Financial Instruments: Recognition and Measurement and IPSAS 30 Financial Instruments: Disclosure. It was agreed that a first-time adopter should have a three-year relief period for the recognition of financial instruments that were not recognized before. First-time adopters that already have known financial instruments may adopt a three-year relief period for the measurement of such financial instruments.

In addition, the IPSASB discussed various overarching issues (e.g., deemed cost, recognition of finance lease liabilities or the recognition and/or measurement of certain items) that impact the finalization of the proposed ED. The first draft of the proposed ED was reviewed during the meeting and an updated version would be considered at the September 2013 meeting.

IPSASs and GFS Reporting Guidelines

A high-level review of responses received on the CP IPSASs and Government Finance Statistics Reporting Guidelines was carried out.

The next steps include a further more detailed review and analysis in order to: refine the table that tracks progress on the reduction of differences between IPSAS and GFS; develop proposals on guidance of choice of options within IPSASs; and develop proposals for the IPSASB’s future work plan consultation (GFS difference reductions, approach to considering options that reduce differences and the future of IPSAS 22 Disclosure of Financial Information about the General Government Sector).

IPSAS Outlook August 2013 9

Topic Current discussion

Revision of IPSASs 6-8

After considering a range of issues associated with the development of the five EDs that will be issued as part of this project at earlier meetings, the focus of this meeting was on which reporting entities should be required to comply with the consolidation requirements in the ED, based on IFRS 10 Consolidated Financial Statements. The IPSASB agreed to propose that investment entities be required to recognize their controlled investments at fair value, as required by IFRS 10.

IPSASB staff was directed to proceed to draft an ED based on IFRS 10 which

(i) Requires that investment entities account for their controlled investments at fair value (ii) Sets out the possibility of permitting the retention of fair value investment entity accounting

by a non-investment controlling entity

Work Plan 2013-2014

The work program for 2013-2014 including potential projects to be added to the work program was discussed. Given current resources and existing project commitments, the IPSASB agreed to add two projects to the work program. Following the July 2012 consultation, it was agreed that a project on social benefits as well as a project on emissions trading schemes should be added to the work program. These projects should commence sometime during 2013-2014. A number of potential projects will be further considered when the IPSASB undertakes its broader strategic review for the period post 2014. There will be a consultation process with the goal of approving and issuing a CP for comment in March 2014.

10 IPSAS Outlook August 2013

Resources

The publications below are available on ey.com/ipsas

IPSAS Explained

We have published an updated second edition of our practical guide to IPSAS, IPSAS Explained. This guide provides decision-makers in the public sector with an overview of IPSAS and the International Public Sector Accounting Standards Board. Opening with an examination of the objectives of the standards, the book goes on to give an overview of the principles relevant to key topics such as the accrual basis of accounting as against the cash basis, fair value, present value, cost and measurement bases. It contains a summary of each IPSAS and recently-issued exposure drafts. This book is available for purchase from Wiley, at www.ey.com/ipsas.

Toward transparency

EY has undertaken a study to assess the current state of public sector accounting from a global perspective. This new research provides a better understanding of what governments are doing well, and where there is scope for improvement.

A snapshot of GAAP differences between IPSAS and IFRS

This publication summarizes the key differences between IPSAS and IFRS. It further explains the sources and reasons for differences between the two frameworks.

www.publicfinanceinternational.org

���������������������������������������������������������������������������������������������������Visit Public Finance International, www.publicfinanceinternational.org, a website supported by EY and developed in conjunction with the Chartered Institute of Public Finance and Accountancy to provide informed news and comment on ���������������������������������������������������������������developments in public financial management internationally, raise awareness of the need for good governance and connect a global community of like-minded public financial management professionals.

IPSAS Outlook August 2013 11

.

Archived webcast

EY’s Public Sector Accounting: IPSAS Update 2013

In this webcast, our panel provides an overview on the background, structure and due process of the IPSASB. It also provides an update on key projects on the IPSASB's agenda, including the Conceptual Framework, and outlines some of the current developments on IPSAS adoption and implementation around the world.

This webcast aims to provide public sector finance managers with the latest developments on the IPSASB's projects and IPSAS implementation globally. This archived webcast can be accessed at http://www.ey.com/GL/en/Issues/webcast_2013-06-26-0700_public-sector-accounting-ipsas-update-2013-replay

12 IPSAS Outlook August 2013

EY | Assurance | Tax | Transactions | Advisory About EY EY is a global leader in assurance, tax, transaction and advisory services. The insights and quality services we deliver help build trust and confidence in the capital markets and in economies the world over. We develop outstanding leaders who team to deliver on our promises to all of our stakeholders. In so doing, we play a critical role in building a better working world for our people, for our clients and for our communities. EY refers to the global organization and may refer to one or more of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients. For more information about our organization, please visit ey.com. About EY’s International Public Sector Accounting Standards Group The move to International Public Sector Accounting Standards (IPSAS) is an important initiative in public sector accounting, the impact of which stretches far beyond accounting to affect every key decision you make, not just how you report it. We have developed the global resources — people and knowledge — to support our client teams. And we work to give you the benefit of our broad sector experience, our deep subject matter knowledge and the latest insights from our work worldwide. It’s how EY makes a difference.

© 2013 EYGM Limited. All Rights Reserved. EYG no. AU1790 ED None In line with EY’s commitment to minimize its impact on the environment, this document has been printed on paper with a high recycled content.

This material has been prepared for general informational purposes only and is not intended to be relied upon as accounting, tax, or other professional advice. Please refer to your advisors for specific advice.

ey.com