f il appraisal of lt upy iffco feitilizer project india

TRANSCRIPT

Report No. 591 -IN F ILAppraisal of Lt UPyIFFCO Feitilizer ProjectIndiaDecember 9, 1974

Industrial Projects Department

Not for Public Use

Document of the International Bank for Reconstruction and DevelopmentInternational Development Association

This report was prepared for official use only by the Bank Group. It may not be published,quoted or cited without Bank Group authorization. The Bank Group does not accept responsibilityfor the accuracy or completeness of the report.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

CURRENCY EQUIVALENTS WEIGHTS AND MEASURES

Rs 1.0 = US$0.133 All weights and measures are in metric unitsRs 7.50 = US$1.00 1 Metric Ton (Ton) = 1,000 Kilograms

1 Kilogram (Kg) = 2.204 Pounds (lbs)1 Kilometer (Km) = 0.62 Miles1 Hectare (Ha) = 2.47 Acres

PRINCIPAL ABBREVIATIONS AND ACRONYMS USED

CAN Calcium Ammonium NitrateDAP Diammonium Phosphate (18-46-0)FACT Fertilisers and Chemicals, Travancore Ltd.FAI Fertilizer Association of IndiaFCI Fertilizer Corporation of IndiaGOI Government of IndiaHYV High Yielding VarietyIDBI Industrial Development Bank of IndiaIFFCO Indian Farmers Fertiliser Cooperative Ltd.KW KilowattKWh Kilowatt HourK20 (Potash) Potassium Oxide Content in FertilizersMW MegawattMWh Megawatt HourN Nitrogen Content in FertilizersNPK Complex Fertilizer Containing N, P205 and K20P205 (Phosphoric Acid) Phosphorous Pentoxide Content in FertilizersSSP Single Superphosphate (0-18-0)TPD Tons per DayTPY Tons per YearTSP Triple Superphosphate (0-46-0)UP Uttar Pradesh

FISCAL YEARS

GOI and Fertilizer Statistics - April 1-March 31IFFCO (actual operations) - July 1-June 30IFFCO (projected operations) - January 1-December 31

INDIA

APPRAISAL OF THE IFFCO FERTILIZER PROJECT

Table of Contents

Page No.

SUMMARY AND CONCLUSIONS ............ ................ i-iii

I. INTRODUCTION .... . .............. . 1

II. THE IFFCO ORGANIZATION ...................... . 1

A. Description, Organization and Management .......... ...... O.. 1B. Plants under Construction . .. 0*0.6*.* ** ... **. *** * .* 2C. Financial Evaluation of Existing Operations ....... 3D. Ylortgages ......... oso***se ........ *XX... 5

III. FERTILIZER MARKET .......... o....*. ...

A. Agriculture in India and the need for Fertilizers. 5B. The Role of the Cooperative Institutions. 6C. Supply and Demand ............ . ............. . .......... 7D. IFFCO's Market Area .. ... ............ *.*.... .... o.o 9E. IFFCO's Marketing Efforts ...... **...... .. ......... . 10F. Prices ................. .......... ...... 11

IV. THE PHULPUR PROJECT ................ .. a.* .. o..... ............. 12

A. Project Location ...... .o... .. . . o.. 12B. Project Scope *. ........ o..0..e0.0.0...*. ...... 0.0.... 13C. Feedstocks and Other Needs .. o...... 13D. Technology .. oo. . 000.0.0.o....0. .. . 14E. Ecology .. .....-. 0..0.*..... ......... 0...* 14F. Employment, Training and Social Aspects .15G. Project Execution and Operation ... 15

V. CAPITAL COST ESTIMATE AND FINANCING PLAN .......... 17

A. Capital Costs. . . .. ........... .. ... .. .. . . 17B. Financing Plan . ... . ........ o. .. .. o.. 18C. Procurement and Disbursement ...............................O. 19D. Allocation and Disbursement of IBRD Loan ....... 19

This report was prepared by Messrs. Antonio S. Tarnawiecki, Christopher J.Pratt, Denis T. Carpio and Felipe A. M. de la Balze of the IndustrialProjects Department.

Table of Contents (Continued)

Page No.

VI. FINANCIAL ANALYSIS ............................ 20

A. Analysis of the Project ................. . 20B. Financial Rate of Return and

Sensitivity Analysis ......... .......... 23C. Consolidated Forecasts for IFFCO C... O06000 23D. Financial Covenants *... *.*......... 25E. Major Risks . ............... , 25

VII. ECONOMIC ANALYSIS ............................. 26

A. W4orld Fertilizer Prices ........ .......... 26B. Economic Rate of Return ........ .......... 26C. Domestic Fertilizer Supply and Food

Production ............ .. ............... 27D. Direct Foreign Exchange Savings ...... o ... 27E. Other Benefits ............... ; 27

JIII. AGREEMENTS ..,............ #...............-.-....-. 28

ANNEXES

1-1 Glossary of Terms Used in the Report1-2 Units and Conversion Factors2-1 Geographical Distribution of IFFCO's Cooperative Shareholdings2-2 IFFCO Management Chart during Phulpur Project Construction2-3 Summary of CFI-IFFCO Agreement2-4 Projected Financial Statements for the Kalol and Kandla Factories

3-1 Agriculture in India and the need for Plant Nutrients3-2 The Agricultural Cooperative System in India3-3 Flow of Products and Funds in Agricultural Cooperatives3-4 Historical Development of the Fertilizer Market3-5 Fertilizer Market Projections3-6 IFFCO's Market Area3-7 International Price Range of Urea4-1 Meteorological Data for Allahabad Area4-2 Proposed Plant Layout for IFFCO Phulpur Project4-3 Representative Data for Heavy Fuel Oil Feedstock to be used

in the Project4-4 Representative Data for Coal and Other Utilities to be used

in the Project4-5 Description of Proposed Processes to be used in the Project4-6 Integrated Process Flow Sheet for the Project4-7 Environmental and Safety Conditions4-8 Staffing and Labor Pattern for the Phulpur Urea Project4-9 IFFCO Management Chart (during Project Construction)4-10 Construction Schedule4-11 Transportation and Handling of Large Equipment4-12 IFFCO Management Chart (Operations)5-1 Capital Cost Estimate5-2 Expenditure Commitment and Price Escalation Factors5-3 Permanent Working Capital5-4 Interest during Construction5-5 Disbursement Schedule of IBRD Loan6-1 Depreciation Schedule6-2 Urea Production Cost Estimate at mid-1978 Prices6-3 Debt Service Schedule in Current Rupees6-4 Financial Forecasts6-5 Profit and Cash Breakeven Charts6-6 Calculation of Capital Costs at constant mid-1978 Rupees6-7 Assets Revalued at mid-1978 Rupees6-8 Cash Flow for Financial Rate of Return6-9 Financial Rate of Return and Sensitivity Analysis6-10 Projected Consolidated Financial Statements7-1 Annual Economic Production Costs and Foreign Exchange Savings7-2 Estimated Prices for Economic Analysis7-3 Economic Cost and Benefit Streams in Constant 1978 Rupees7-4 Economic Rate of Return and Sensitivity Analysis

MAPSIBRD 10453R - Location of Major Fertilizer Plants and Refineries in IndiaIBRD 11227 - IFFCO's Market AreasIBRD 11228 - Site of Proposed IFFCO Phulpur Project.

INDIA

IFFCO FERTILIZER PROJECT

SUMMARY AND CONCLUSIONS

i. This report deals with the appraisal of a fertilizer project inPhulpur, Uttar Pradesh (UP) comprising a 900 tons per day (TPD) ammonia unitand a 1,500 TPD urea plant based on heavy fuel oil for feedstock and coal forsteam and power generation. The project, which is expected to start commer-cial production in September 1978, is sponsored by the Indian Farmers' Fer-tiliser Cooperative Ltd. (IFFCO), owned by the Government of India and coopera-tive institutions. Although two thirds of the shares are held by the Govern-ment, IFFCO's by-laws provide for the eventual transfer of the Governmentshares to the cooperatives. The project will add 495,000 tons per year (TPY)urea capacity (equivalent to 228,000 tons of nitrogen) to two other plantsthat IFFCO is successfully building and has almost completed. These two plants,having a final product capacity of 392,000 TPY of urea and 376,000 TPY of com-plex (NPK) fertilizers, are the first venture of the Indian cooperative systeminto the large-scale manufacture of fertilizers. The Phulpur project is esti-mated to cost about US$220 million, of which US$107 million is anticipated tobe in foreign exchange including nearly US$17 million in interest during con-struction. A Bank loan of US$109 million equivalent is proposed; it would bemade to IFFCO and guaranteed by the Government.

ii. Chemical fertilizer consumption in India grew rapidly--at an averagerate of 17% annually--in the last 20 years and reached 2.8 million tons of thethree major plant nutrients 1/ in 1973/74. With 164 million hectares, Indiais the third ranking country in the world in cropped area (and the second inirrigated land). Future increases in production of foodgrain and other cropsare expected to result not so much from enlargement of the cultivated areas asfrom improved agricultural practices, including higher rates of fertilizerapplication. Recent forecasts estimate N consumption at 4.3 and 6.9 milliontons by 1978/79 and 1983/84 respectively. 2/

iii. The growth in fertilizer production in the past 20 years (16% peryear on the average) is impressive but has failed to keep pace with demand andimports have increased almost twentyfold in spite of the fact that farmers'demand has not been fully satisfied because of balance of payment problems andrecent scarcity and high prices of imported fertilizers. Domestic productionof fertilizer has been disappointing in recent years; production of N fertilizerin 1973/74 (less than 1.1 million tons) was only 67% of commercial capacity

1/ 1.83 million tons of nitrogen (N), 0.61 million tons of phosphoric acid(P2 0 5) and 0.33 million tons of potash (K2 0).

2/ The Draft Fifth Five-Year Plan projected a 1978/79 consumption of 5.2million tons of N.

- li -

(i.e., excluding plants mechanically complete but not yet operating comuercial-ly). Because of uncertainty in the availability and pricing of fertilizers inthe world market, increased domestic production--through improvement in thecapacity utilization of existing plants and installation of new units--iscrucial for India's programs to increase agricultural production. The projectwill help to fill, at a satisfactory economic cost, the gap between productionand demand, thus diminishing the country's costly dependence on imported ferti-lizer and the consequent risk of interrupted supplies. Any shortfall in foodproduction resulting from lack of fertilizers would cost India many times thecost of producing them locally.

iv. The project envisages the utilization of modern but proven techno-logy (the ammonia plant will be similar to that of the Nangal fertilizer plantfor which IDA financing was approved in January 1973) and will be executed byIFFCO with the assistance of engineering firms which have experience in theconstruction of fuel oil-based ammonia and urea plants and offsites and whichwill actively participate in the procurement of equipment following Bankguidelines. IFFCO will set up a Project Implementation Unit, and to strengthenits capacity to manage the implementation of a project employing technologynot used today in India (the Nangal fertilizer plant will be the first majorplant based on fuel oil), IFFCO will arrange, if they or the Bank deem itnecessary, for qualified technical advisory services. The contracts with thelatter and the engineering firms will be subject to prior Bank approval.

v. The US$109 million loan will finance equipment and spares procuredaccording to Bank guidelines and the foreign exchange component of the feesfor expatriate engineering, licensing and advisory services. The balance ofthe project cost will be financed through long-term borrowings from the Gov-ernment and Indian banking institutions totalling Rs 258 (US$34.3) millionand by raising IFFCO's equity by Rs 580 (US$77.2) million through contributionsfrom the Government (Rs 360 million) and the cooperative institutions (Rs 220million). In view of the need to mobilize substantial resources from a largenumber of cooperatives, the Government has agreed to cover any shortfall inthe cooperatives' contribution. The project will be soundly capitalized witha debt:equity ratio of about 60:40 including some quasi equity in the form ofsubordinated debt to the Govern>;snt. As loans are repaid, IFFCO's financialposition will be strengthened and reserves built up for future expansion.

vi. Agricultural cooperatives in India, besides extending credit totheir members, share in the marketing of their crops, and are the major dis-tributors of fertilizer and other agricultural inputs. Institutional de-velopment, however, is uneven and the processing of credit applications andrecovery of loans must be improved. The prevailing high level of overdueloans does not affect fertilizer manufacturers (including eventually IFFCO)because sales are primarily financed by the banking system but correctivemeasures, many of which have already been taken, must nevertheless be firmlypursued, such as: disbursing credit largely in kind (fertilizer, seeds, etc.),tying of crop marketing with loan repayment, rejecting credit applicationsfrom defaulting borrowers and tightening accounting procedures at village-levelcooperatives. Operations of cooperatives located in the most important dis-tricts in IFFCO's marketing area are rapidly improving but the effectiveness

- iii -

of the steps taken must be kept continually under review. The proposed loanto IFFCO will reinforce the Company's capacity to strengthen cooperative in-stitutions at the grassroots level through the training of cooperative offi-cials for extension services on fertilizer application by individual farmers.

vii. Based on the present net ex-factory price of Rs 1,100 (US$147) perton of urea in India and the expected price escalation through 1978, theproposed plant's cash flow is projected to maintain a current ratio of atleast 1.5 to 1.0 and yield a financial rate of return of 10.3% after incometaxes or 13.9% before taxes. The present price paid by farmers for urea isRs 2,000 (US$267) per ton, but Rs 610 (US$81) per ton is set aside to sub-sidize higher-priced urea imports through a Government-controlled equaliza-tion fund. The Government has agreed to maintain fertilizer prices at levelsallowing efficient manufacturers to meet their expenses, service their debtout of their revenues and earn a reasonable rate of return on capital employed.

viii. On the basis of long-term international price levels for feedstock(US$65/ton of heavy fuel oil at plant site) and urea (US$175/ton landed atIndian port) expected at the time the plant starts commercial production, theproject's economic rate of return is 16.2%. Were production costs to increaseby 10%, the rate of return would decrease to 14.8%. A drop of US$20/ton inthe price for urea would depress the return by 3.6 percentage points. A one-year delay in the time required for construction would lower the rate of returnto 15.0% and a 10% capital cost overrun to 14.6%. The annual foreign exchangesavings are estimated at US$59 million annually.

ix. IFFCO has been active for three years in promotional programsadvocating balanced fertilizer application and other improved agriculturalpractices. As part of these programs IFFCO has been training its own andcooperative staff in all aspects of fertilizer application and marketingand has sold about 300,000 tons of fertilizers reaching a large number ofcooperative members "demonstration" plots. This extensive background infertilizer marketing and IFFCO's experience in building two large fertil-izer plants are expected to reduce risks to a minimum provided that imple-mentation of the project can be carried out as planned. However, delaysin delivery of equipment and cost overruns in excess of those provided forcannot be ruled out altogether in the tight equipment market situation existingat present. But even a one-year delay in project completion combined with a10% cost overrun - serious as these events would be in the attempt to getadditional fertilizer to Indian agriculture quickly and at a reasonable price- would reduce the economic rate of return only to 13.4%.

x. Based on the agreements reached with the Government and IFFCO asshown at the end of the report, the project is suitable for a Bank loan ofUS$109 million equivalent.

I. INTRODUCTION

1.01 The Government of India (GOI), on behalf of Indian Farmers FertiliserCooperative Ltd. (IFFCO or the Company), has requested a Bank loan of US$109million equivalent to help in the financing of a new fertilizer plant with acapacity of 297,000 tons per year (TPY) of ammonia and 495,000 TPY of urea,equivalent to 227,700 TPY of nitrogen (N) nutrient 1/ at Phulpur, UttarPradesh (UP). IFFCO is owned jointly by the Government and Indian cooperativeinstitutions and is about to complete the construction of two other fertili-zer plants in Gujarat, one at Kalol, for the production of ammonia and urea,and the other at Kandla, for the production of complex fertilizers (Map:IBRD 10453RI). The Company also plans to build a phosphoric acid plant at alater date.

1.02 IDA has extended four credits and IFC participated in two fertilizerprojects in India. A fifth fertilizer project, the Sindri Modernization Pro-ject of the Fertilizer Corporation of India (FCI), has been recently appraisedby IDA and is expected to be presented to the Executive Directors at the sametime as the IFFCO project. The Phulpur project is the first involving theconstruction of a new grass-roots plant. It was first reviewed by a Bankmission in October 1973, and after some additional preparatory work, appraisedin March/April 1974 by a mission consisting of Messrs. Tarnawiecki (Chief) andPratt, of the Industrial Projects Department.

II. THE IFFCO ORGANIZATION

A. Description, Organization and Management

2.01 IFFCO was registered on November 3, 1967, under the Bombay Coop-erative Societies Act and, subsequently, as a central society in New Delhi..It is owned two-thirds by the Government and one-third by a great number ofIndian cooperative institutions. Its authorized capital is Rs 1,000 millionand its paid-up capital Rs 285 million. The idea of the Indian cooperativesystem engaging in the large-scale manufacture of fertilizers was suggestedto the Government in 1964 by the Cooperative League of USA, which also offeredassistance in implementing it. The US Agency for International Development(AID) studied the plan in 1966/67, recommended building an ammonia/urea plantand a complex (NPK) fertilizer plant in Gujarat, and helped in their financing.These are the two plants which are now nearing completion (para. 1.01).

1/ A glossary of terms used in the report is contained in Annex 1-1 andunits and conversion factors common in the petroleum and fertilizerindustries are shown in Annex 1-2.

- 2 -

2.02 The contribution of the cooperative system to IFFCO's equity nowstands at Rs 105 million. About 24,000 cooperative institutions ranging fromthe national level federation to primary village cooperatives in 10 Statesare shareholders in IFFCO (Annex 2-1). Shareholders who contribute Rs 100,000or more have the right to a seat on IFFCO's Representative General Body, aform of general shareholders assembly, and every 200 societies with smallershareholders can jointly elect one representative. During the first 10 yearsof its existence (i.e., until November 1977), the Government appoints theBoard of Directors and the principal officers, and thereafter the Representa-tive General Body will select 5 members of the Board. The Managing, Financeand Marketing Directors, who are at the same time full-time officers, will beappointed by the Board with prior approval of the Government. Another 14members will be appointed by cooperative institutions, up to 5 by the Govern-ment and 3 by financial institutions. An Executive Committee has been estab-lished with adequate powers to run day-to-day operations of the Company. Thesenior corporate structure is shown in Annex 2-2.

2.03 The present Managing Director, Mr. Paul Pothen, is a highly ableand experienced fertilizer industry technologist and executive. The FinanceDirector, Mr. B.B. Singh, has been seconded to IFFCO from the Ministry ofFinance, and the General Manager, Mr. B. R. Singh, has an extensive backgroundin Indian fertilizer distribution and sales as well as in the cooperativesystem. Mr. Pothen's contract expires in January 1976 and Mr. B. B. Singh'sin July 1975. Mr. Pothen's contract can be extended for two additional yearswithout any difficulty and the Company has agreed to consult with the Bankon the appointment of a qualified successor to any vacancy in the position ofa fulltime Director. The eventual replacements for these men should beselected and trained as early as possible.

B. Plants under Construction

2.04 As mentioned previously, two IFFCO projects are being completed atKalol, near Ahmedabad, and about 325 km away, in Kandla, close to the IndianOcean where facilities for ocean-going vessels and railway connections areavailable. The Kalol plant comprises a 910 tons per day (TPD) ammonia unitand a 1,200 TPD urea unit plus storage, offsites and township. The ammoniaunit was designed and engineered by M.W. Kellogg Company (USA) in conjunctionwith Kellogg (India), and uses local natural gas, to be purchased from GOI atUS$0.45 per thousand standard cubic feet (MSCF), supplemented by about 180 TPDof naphtha. The urea unit was licensed by Stamicarbon N.V. (Holland) andengineered by Humphreys and Glasgow Ltd. (UK) in conjunction with H. & G.Consultants Private Ltd. (India), which also designed the offsites. It willconsume about 700 TPD of ammonia. The balance of approximately 200 TPD ofammonia will be transported via rail to the Kandla plant for the manufactureof complex fertilizers, with any surplus to be sold to industrial users.

2.05 The Kandla plant comprises two streams each having a design capacityof 600 TPD diammonium phosphate (DAP). The addition of potash enables avariety of NPK grades to be made according to need. The plant was designedby Dorr-Oliver Inc. (USA) in conjunction with Dorr-Oliver (India) Ltd. andtheir United Kingdom affiliate. Offsites were also designed by this group.A deep-water dock and township have been built nearby.

2.06 Project organization, procurement, construction and management atboth sites has been undertaken by IFFCO staff with the assistance of Cooperar-ative Fertilizers International (CFI), a group formed by US fertilizer co-operatives, and other expatriate staff working in conjunction with contractors'project teams. This arrangement (Annex 2-3) has been successful and indicatesthat IFFCO's management and project team are competent. Contracts for theseplants were let in July 1971 and commercial production of ammonia at Kalol isexpected to begin in November 1974, five months behind schedule. Due to de-layed shipment of the imported reactor, urea production at Kalol is not likelyto commence, until late 1974. Meanwhile, ammonia can be transported to Kandlaas well as to other plants subject to the availability of sufficient railtank-cars. While eventually IFFCO may produce its own phosphoric acid, ini-tially it will depend on imported phosphoric acid. One shipment of 15,000tons has already been received, but adequate supply from the world market maybe difficult during the next couple of years.

C. Financial Evaluation of Existing Operations

2.07 Total costs of the two plants, including contingencies and initialworking capital, are currently estimated at Rs 939 million (about US$125million), of which Kalol represents'about 72% and Kandla 28%. Sources offunds - US, UK, Netherlands, Government of India, Industrial Development Bankof India (IDBI) and other financial institutions - are detailed in Annex 2-1.

2.08 Financing of the two projects was highly leveraged and at the endof 1974 IFFCO's debt/equity ratio will be about 70:30. The Government hasagreed to subordinate its existing credit of Rs 112 million (Annex 2-1) onterms similar to those described for the Government's quasi-equity contributionfor the proposed Bank project (para. 5.05). Such a conversion would bringthe Company's debt/equity ratio to about 58:42 at the end of 1974.

2.09 IFFCO's projected financial statements without the project are shownin Annex 2-4 and summarized in the Table next page. The projections are basedon end-of-1974 costs and prices escalated by annual inflation rates of 12%during 1975, 8% during 1976, and 6% during 1977 and 1978; after start-up ofthe project they are expressed in constant mid-1978 prices. As mentionedbefore, the Kandla plant is facing difficulties in obtaining supplies ofphosphoric acid in the world market and the projected financial results arebased on the plant producing NPK at only 25% of capacity during the next twoyears. IFFCO's profitability, however, as shown in Annex 2-4, will still besatisfactory because the Kalol plant is expected to operate at 60% of capa-city in 1975, 80% in 1976, and 90% thereafter, and the ammonia productionintended for the manufacture of NPK fertilizer can be profitably sold toother users. The expected financial results from the two existing plants

- 4 -

Summary of Projected Financial Statements for theKalol and Kandla Factories./

(Rs million)

Year Ending December 31 1975 1976 1977 1978

Capacity Utilization (%): Kalol Unit 60 80 90 90Kandla Unit 25 25 60 80

Income Statement and Cash Flow(in current prices)Sales Revenues 15 680 1,121 1,388Cost of Sales 344 460 788 997Interest Charges j 69 65 61 59Income Taxes (55%) Y - 10 150 183Net Profit 2 145 122 149Depreciation 69 69 69 69Operating CasV low 139 279 252 277Debt Service Ž1 58 64 68 67Total Debt Service 67 74 86 85

Balance SheetCurrent Assets 213 231 248 262Cumulative-Funds:(a) Available for Investment - 121 265 435(b) Available for Distribution W - 10 19 29Net Fixed Assets and Spares 834 768 702 635Current Liabilities 7 130 93 98 124Long-Term Debt 519 503 487 449Equity (including quasi-equity) 339 535 648 788Total Assets or Liabilities 1,048 1,131 1,234 1,362

RatiosRegular Debt Service Coverage 2.3 4.2 3.7 4.1Total Debt Service Coverage 1.9 3.7 2.9 3.3Current Ratio 1.6 2.5 2.5 2.1Debt:Equity Ratio / 57:43 48:62 43:57 36:64

1/ Last digit discrepancies due to roundingv/ Interest oharges on all debt, including subordinated debt3/ Development rebate of Rs 139 million is used to offset taxable income

during 1975 and 1976V Net profit, depreciation and interest charges5/ Excluding debt service on subordinated debtb6/ Limited to 7% of net profit7 Including current portion of regular and subordinated debt

&Subordinated debt included in equity.

- 5 -

are favorable because the Kandla and Kalol plant capital and financing costswere largely incurred before the sharp equipment price inflation registeredduring 1973 and 1974. Furthermore, the present urea ex-factory price has beenset by the Government to provide a fair return on equity on the much higherpresent levels of capital and financial costs.

2.10 The Company has instituted comprehensive internal reporting pro-cedures and has agreed to supply to the Bank quarterly production, incomeand cash flow reports and audited annual reports satisfactory to the Bank.IFFCO wilL also prepare each quarter projected cash flows for the next 12-month period.

D. Mortgages

2.11 IFFCO's properties at Kalol and Kandla have been mortgaged tosecure the loans received by IFFCO from the Government, IDBI and other finan-cial institutions in India. The Government and IFFCO have agreed to vacatethe existing mortgages by June 30, 1975. These mortgages will be replaced bya new mortgage in favor of the Government. IDBI and other financial insti-tutions will be given Government guarantees for their loans to IFFCO.

2.12 The existing mortgages do not extend to any properties of theproposed Phulpur Unit. In addition to the proposed Bank loan, IDBI, otherfinancial institutions and possibly the Government will advance loan fundsto the new plant. Under the arrangements agreed with the Government andIFFCO, IFFCO may create certain liens on the properties of the Phulpur Unitin favor of the Government to secure loan amounts of the Bank and IDBI(including other financial institutions) which will be guaranteed by theGovernment, and to secure any direct lending by the Government for thePhulpur Unit. Arrangements will be made to ensure that the Bank will receivea part of any amounts recoverable under liens on the Phulpur Unit until itsloan is fully repaid. No other liens will be allowed except with the approvalof the Bank.

III. FERTILIZER MARKET

A. Agriculture in India and the Need for Fertilizers

3.01 With a cropped area of 164 million ha (Annex 3-1), India ranksthird in the world in area of cultivated land (after the USSR and US) andsecond in irrigated land (after Mainland China). In 1971, an estimated72% of the labor force worked the land but the agricultural sector's sharein GDP (at factor cost) was only about 43%. In the decade ending 1971-72,the growth rate for foodgrain output was 2.6% p.a. of which 0.5% can beascribed to cropped area increases and 2.1% to higher productivity. 1/ This

1/ However, for cereals alone (i.e., excluding pulses), the growth inoutput was 3.1% annually and in yields, 2.6% p.a..

- 6 -

was largely due to increased use of fertilizers and irrigation and to thespreading cultivation of high-yielding varieties (HYVs) of several crops,especially wheat and rice. During the last two years of the Fourth Five-Year Plan (1968/69 - 73/74) production failed to increase primarily becauseof the 1972/73 drought, scarcity of fertilizers, power shortages and trans-portation difficulties.

3.02 The Draft Fifth Five-Year Plan has set a target for foodgraingrowth of 4.2% annually from 1973/74 through 1978/79, of which 3.2% wouldresult from increased crop yields and 1.0% would be brought about throughan increase in area under crops of 10.2 million ha. However, the latestBank country economic report 1/ indicates that an increase in cropped areaof 5 million ha in foodgrains and 3 million ha in other crops is morelikely. The yields of the main crops are planned to increase by from 18%to 3S% in five years. To attain such increments increased availability offertilizers is indispensable but it must be complemented by proper use ofother inputs (water, seeds, pesticides and tractors), maintenance of advan-tageous crop price/input cost ratios for most crops, and improvement ofagricultural credit procedures.

3.03 Although under controlled small-scale farm trials, incrementalyields as high as 10 tons of foodgrain per ton of plant nutrient have beenobtained, in practical terms, a ratio of only about 6 to 1 is expectedunder average Indian conditions in the next few years. 2/ These are verycrude yardsticks of what actual marginal response to fertilizer applicationmay be, but indicate the magnitude of the foodgrain imports that would beneeded to cover shortfalls in fertilizer supplies.

B. The Role of the Cooperative Institutions

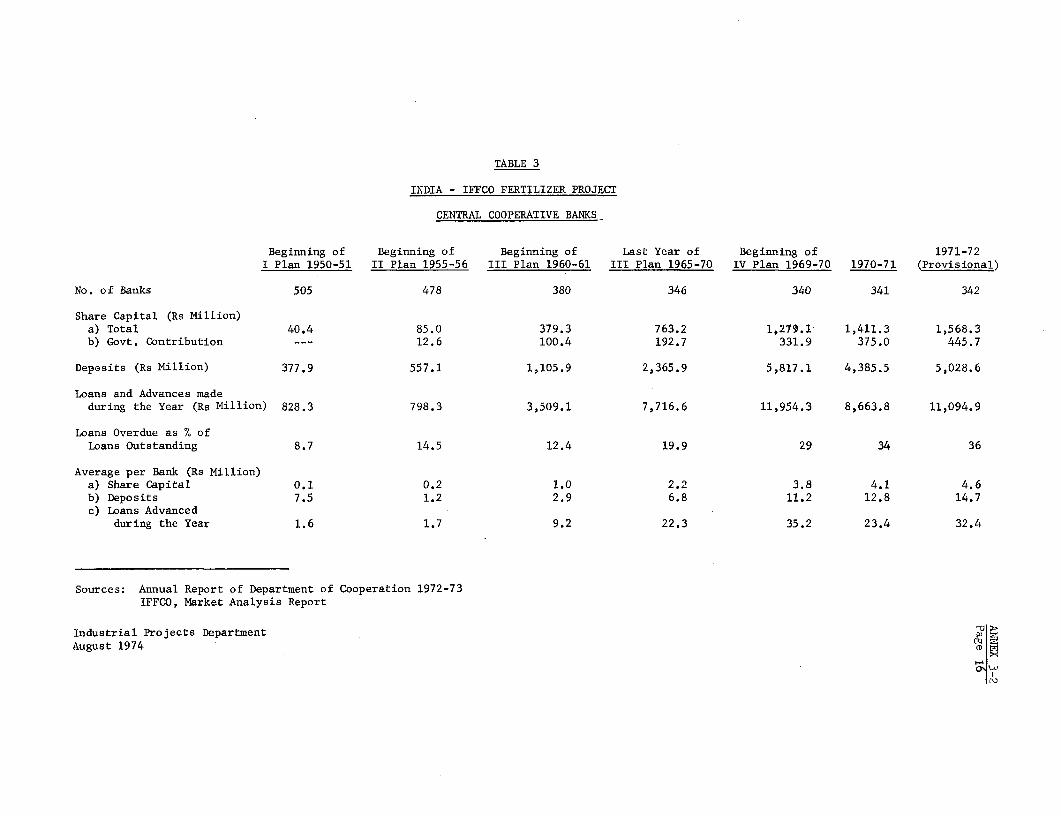

3.04 The Indian cooperative movement participates actively in agricul-tural credits, crop marketing and fertilizer distribution, and, throughIFFCO, also in the large-scale manufacture of fertilizers. The share ofthe Indian cooperative movement in agricultural credit was a meager 3% in1952, but increased rapidly during the sixties to reach about 33% of thetotal in 1969 (.Annex 3-2). In most States there is a three-tier structurefor extending short-terui eredit to individual farmers: the State-Level"Apex" cooperative bank, tile district-level central cooperative bank andthe primary (village-level) cred.aL or multi-purpose cooperative society(Annex 3-3). MIarketing of crops and distribution of fertilizers and otherinputs are also important activities of the cooperative system. The primarymarketing cooperatives handled crops valued at Rs 8.4 billion in 1971/72 andabout Rs 11 billion in 1973/74.

1/ "Economic Situation and Prospects of India" (402-IN), May 7, 1974.

2/ IBRD, Economic Situation and Prospects of India, Report No. 402-IN(May 7, 1974).

3.05 However, the primary agricultural credit cooperatives face aserious problem in the lack of sufficient well-trained full-time employeesand the large proportion of overdues: 44% of loans outstanding as of June30, 1972. This situation can be partly justified by bad crops but theGovernment and officials in the cooperative movement recognize that thelarger number of cases is due to poor management, particularly laxity inloan recovery practices (Annex 3-2, paras. 13/14). Although the problemdiminishes in relative importance as one moves up through the tiers ofthe cooperative system (Apex banks' overdues amounted to only 7% of loansoutstanding in June 1972) and it does not affect in any way the financialposition of fertilizer manufacturers (including eventually IFFCO), con-tinued improvement is of the greatest importance and the effectiveness ofsteps already taken towards this end should be kept under periodic review.These steps include disbursement of credit only to farmers who have repaidprevious loans and training of full time cooperative officials. Fortunately,some of the cooperatives most active in introducing needed reforms arelocated in the States where IFFCO will market the largest share of itsproduction.

C. Supply and Demand

3.36 In India, the cooperative institutions as well as the private andoublic sectors share in fertilizer production and distribution. One halfof the present capacity to manufacture N fertilizers--the product dealtwith in this report--is owned and operated by the public sector, mainly byFCI and Fertilisers and Chemicals, Travancore Ltd. (FACT), 1/ 31% by privatecompanies and the remaining 19% by mixed enterprises. The cooperatives willshare in production only as IFFCO's two plants come shortly on stream.Producers are allowed to market part of their straight N fertilizers 2/and the balance goes to the Central Fertilizer Pool, a public sectoragencv, wh3ich came into existence in 1942 to import N fertilizers, a func-tion it still performs.

3.71 The historical growth of fertilizer consumption and productionin In3ia is analyzed in Annex 3-4 and projections through 1983/84 aresaomn in Annex 3-5. The following paragraphs summarize the major conclu-s iOils.

3.9S Consumption of the three major plant nutrients 3/ increased atan average annual rate of 17.4% in the last 20 years, reaching 2.77 milliontons in 1973/74. Growth in consumption of N alone has been only slightly

1/ FCI was founded in 1961 to take over the management of three existingpublic sector plants (SINDRI, Nangal and Trombay) and is the largestfertilizer and the sixth largest industrial enterprise in India. FACTwas founded in 1947 as a mixed enterprise.

2/ The proportion varies in different States, but it has generally beenbetween 50% and 70% of production.

3/ Nitrogen (N), phosphorus (P205) and potash (K20).

-8-

less rapid--16.1% p.a.--and the level reached in 1973/74 was 1.83 milliontons, while consumption of P205 and K20 was 0.61 and 0.33 million tonsrespectively.

3.09 Starting from a low base, fertilizer production also increasedrapidly in the last two decades (by 16% per year) but failed to keep pacewith demand and imports have increased almost twenty-fold from 63,000 tonsof nutrients in 1953/54 to 1,220,000 tons in 1973/74. Production in 1973/74 was 1.07 million tons of N and 0.39 million tons of P205. All potassicfertilizers are imported, although some imported K20 is being incorporatedinto complex fertilizers made locally. During the last few years, the pro-nounced growth trends for consumption and production have somewhat lessenedas local plant capacity build-up was delayed, plants already completed failedto reach expected production levels, foreign exchange for imports was scarce,and imported fertilizers were increasingly more difficult to obtain or wereavailable only at rapidly increasing prices. All this has put a very heavyburden on India's balance of payments.

3.10 Present annual installed capacity to manufacture chemical fer-tilizers in India is 1.94 million tons of N and 0.57 million tons of P205(Annex 3-5). Capacity utilization of the nitrogenous fertilizer plantsaveraged only 67% in 1973/74, discounting figures for three plants whichhad either just started normal production or had not yet overcome initialproduction difficulties. - The reasons for this poor showing are many.Some--mainly power shortages and lack of foreign exchange needed for bal-ancing equipment and for operations--are not within the responsibility ofpresent plant management; others--including a good share of the responsi-bility to keep adequate stocks of spare parts and act forcefully to avoiddelays in reaching stable commercial production--are the result of poorplanninig, bureaucratic inflexibility in day-to-day operations and sometechnical shortcomings.

3.11 A great number of demand and consumption projections have beenmade in the past, but actual consumption has always fallen short of pre-dictions. The latest detailed study was a joint GOI-IBRD report preparedby li.B. Donde and Dorris Brown in 1971, which, on the basis of actual datathrough1 1968/69 forecast N demand to range between 2.4 and 2.9 millionTPY ly 1973/74 and betwieen 4.0 and 5.2 million TPY by 1978/79. The DraftFifthl Plan foresees a consumption of 5.2 million tons of N, 1.8 milliontons of P2 0 and 1.0 million tons of KI20 in 1978/79. Based on actual datatLrouglh 1971/74 and recent information supplied by Government officials,IFFCO and cooperative institutions, and taking into account possible lim-itations in areas under irrigation, multiple cropping and fertilizer sup-plies, probable Et consumption projections have been revised downwards (Annex3-5). These figures, together with past data, are summarized on the nextpage. The Governmnent is making efforts to narrow the gap between supply anddemand by increasing the output from existing plants and adding new capacity.Plants under construction or for which financing is being arranged will have

an incremental capacity of 2.9 million tons of N and 0.7 million tons of P 2 05.Expected production from these plants have been included in the projectionsshown below:

- 9 -

India - Fertilizer Consumption and Supplies(million nutrient tons)

Consumption _ Production Gap /1N P205 K20 N P205 N P205

1962/63 /2 0.35 0.08 0.04 0.19 0.09 0.19 0.011968/69 1.13 0.39 0.15 0.56 0.21 0.78 0.091969/70 1.36 0.42 0.21 0.73 0.22 0.57 0.091970/71 1.49 0.46 0.23 0.83 0.28 0.48 0.031971/72 1.75 0.56 0.30 0.95 0.29 0.46 0.241972/73 1.78 0.59 0.33 1.06 0.33 0.69 0.211973/74 1.84 0.61 0.33 1.07 0.39 0.67 0.221974/75 Estimate 2.20 0.75 0.40 1.43 0.40 0.77 0.35

Projection:

1978/79 Probable 4.31 1.57 0.78 3.72 1.14 0.59 0.431978/79 Low 3.89 1.41 0.70 3.28 0.84 0.61 0.57

1983/84 Probable 6.95 2.78 1.39 6.34 1.97 0.61 0.811083/84 Low 6.26 2.51 1.25 5.01 1.48 1.25 1.03

/1 Actual imports for 1962/63 to 1973/74. (Sums of actual production andimports do not add to consumption because of stock variations).

/2 Average for 3 years centered on 1962/63.

Under Indian agricultural conditions, an average nutrient ratio of 4:2:1for N:P205:K20 is considered desirable. At present this ratio is muchhigher in N, namely 5.5:1.8:1, but for the future a gradual improvement isforeseen. It is clear from the above that India's problem is not one ofa market unable to absorb domestic production, but of ability to supplyan ever-increasing demand.

D. IFFCO's MIarket Area

3.12 Since the two States which have the largest proportion in IFFCO'scooperative shareholdings, the Punjab and UP (each with 25%), are also thelargest potential consumers of fertilizers, IFFCO's marketing strategy willbe largely directed towards these two States. IFFCO should, in principle,supply fertilizers to its cooperative members approximately in proportionto their equity contribution. However, initially IFFCO plans to sell itsproducts in predetermined areas of seven States out of the ten with sharesin IFFCO: Punjab, UP, Haryana, Madhya Pradesh, Rajasthan, Gujarat andMaharashtra (Map: IBRD 11227). The following analysis of supply anddemand in IFFCO's marlceting area is limited to N fertilizers because

- 10 -

the gap between production and consumption of P 0 is expected to be pro-portionately wider than that for N in the near Suiure and therefore marketingof phosphate fertilizer would not present great difficulties. More detailsare given in Annex 3-6.

IFFCO Marketing AreaEstimated Supply and Demand in 1978/79

(million tons of N)

UP, Haryana M. Pradesh, RajasthanPunjab and Gujarat and Maharashtra Totals

Capacity /1 0.49 1.00 0.88 2.37

Production /1- "Probable" 0.28 0.83 0.43 1.54- "Low" 0.23 0.72 0.37 1.32

Consumption in IFFCO'smarket area:- "Probable" 0.29 1.28 0.39 1.96

- "Low" 0.27 1.22 0.33 1.82

Surplus (Deficit):- "Probable" (0.01) (0.45) 0.04 (0.42)- "Low" (0.04) (0.50) 0.04 (0.50)

/1 Capacity and production figures refer to the seven states in whichIFFCO's market area extends.

It can be seen that there will be not only an overall supply deficit inIFFCO's marketing area, but that such deficit is particularly pronouncedin the two States in which the Company's nitrogen fertilizer plants aregoing to be located (U.P. and Gujarat). Based on present plans the def-icit in the area will still persist in 1983/84. At that time probableconsumption there is expected to have increased to about 3.6 million tonsof N as against maximum production of about 3.3 million tons.

E. IFFCO's Marketing Efforts

3.13 IFFCO has pioneered in the promotion of balanced fertilizerapplication, suitable farming practices (including proper timing of fertil-izer application) and prior estimation of adequate dosages according tosoil test results, crops planted, availability of water and other culti-vation conditions. This promotion has been carried out by IFFCO through-out ten States by means of "seeding" programs, in the course of which ithas sold in the last three years more than 300,000 tons of fertilizerthrough a great number of sales points (some 4,632 at the end of 1972/73).

- 11 -

During these programs IFFCO has sought the cooperation of farmers willingto buy fertilizers in prescribed quantities 1/ and follow recommended farm-ing practices in "demonstration" plots.

3.14 To reach effectively as many farmers as possible, IFFCO hasrecognized that personnel at the sales points--whether run by the coopera-tive system, private dealers or public agencies--must be accessible toIFFCO as well as to the farmers. Therefore the Company has a trainingprogram for staff in credit cooperatives and cooperative banks. This inturn requires an active in-house training effort for the about 160 em-ployees in IFFCO's Marketing Division. Since 1970, the Company has hadmore than 30 training programs for salesmen, agronomists and marketingmanagers. In summary, therefore, IFFCO appears well prepared for themarketing of its output, and while the private and public sector plantsin its marketing area will offer healthy competition, there is no dangerof supply surpluses within the area.

F. Prices

3.15 Urea and other straight nitrogenous fertilizer prices are sta-tutorily controlled by the Government. Phosphatic and complex fertilizerprices are not subject to this control, but all phosphatic fertilizer man-ufacturers abide by the prices recommended by the Fertilizer Associationof India (FAI), which includes all the major Indian fertilizer manufac-turers. The retail price for urea, which had been kept within rathernarrow bounds since the mid-sixties has experienced two important in-creases within the last 12 months as shown below. The Government hasagreed that no actions will be taken precluding efficient fertilizer man-ufacturers from obtaining revenues enabling them to meet expenses, ser-vice debt and earn a reasonable return on invested capital. This policyhas been confirmed by the Government during negotiations.

India - Development of Selected Fertilizer Retail Prices(in Rs/MT)

Ammonium NPK DAPUrea Sulphate 15-15-15 18-46

April 1967 840 492 870 1,095March 1972 959 549 912 1,335October 1973 1,050 600 1,130 1,475May 1974 2,000 925 2,900 3,005

1/ IFFCO, unlike other manufacturers, has insisted that farmers pay for thefertilizers used in their "demonstration" plots.

- 12 -

3.16 Part of the increase approved in May 1974 will compensate the manu-facturers for higher feedstock costs and part will be used to subsidize im-ports, so as to minimize the Government's losses in importing fertilizer forwhich prices have been repidly increasing since last year (Annex 3-7). Thestructure of the present urea pricing system as applied to the Phulpur plantis as follows:

India - Structure of Urea Price(in Rs/MT)

Price to farmer 2,000Deposited with GOI for price equalization 610

Retained by manufacturer 1,390Less distribution margin 80Less freight 44Less excise tax 166

Net average Phulpur ex-factory price 1,100

Although detailed analyses are not yet available, preliminary indications arethat the benefit/cost ratios justifying generally recommended fertilizerdosages have not been affected negatively by the recent changes in the pricesof fertilizers and most crops.

IV. THE PHULPUR PROJECT

A. Project Location

4.01 Bearing in mind that markets and shareholders for the project willbe largely concentrated ia the Punjab and UP, an intensive search for asuitable location was made in these States by IFFCO. A site close to Phulpurand near Allahabad (Map: IBRD 11228) was selected and the choice appears tobe an excellent one. A broad-gauge railroad runs by the northern side ofthe site and is part of the Allahabad to Jaunpur line. A meter-gauge rail-road and also the Grand Trunk Road which both connect Allahabad with Varanasiand other important cities are 15 km to the south. The site's southernboundary is the Allahabad-Shahganj road. Thus, ability to bring in heavyequipment, feedstock (heavy fuel oil), coal and labor, as well as to trans-port the bagged (or bulk) urea is reasonably assured. Furthermore, many ofthe marketing areas in northern UP and neighboring States are accessible onlyby meter-gauge track. Therefore a substantial amount of urea will be movedby the meter-gauge network, thus reducing costs of trans-shipment and theincidence of damaged bags and-material losses. Also, the substantial addi-tional rail freight load can be shared between the two rail systems.

- 13 -

4.02 The project's external power requirements are not expected to ex-ceed 3 MVA, or about 20% of needs. Nevertheless, the site is near a 33 KV,10 MVA power line, which will be enlarged to provide secure emergency suppliesas well as construction needs. The area has good ground water sources andthe proximity of lakes plus the Ganges river provides supplementary suppliesif needed. The topography allows natural drainage and except for heavy equip-ment no piling is believed necessary. The area is not in a seismic zone andits meteorological data are given in Annex 4-1. Arrangements have been madeto purchase the required 200 ha or so for the plant site, mostly consistingof barren rural land. A condition of effectiveness of the Loan is that IFFCOtakes possession of this area. Telephone and telegraph services exist atPhulpur and telex and airline facilities at Allahabad. Ample labor is avail-able in the surrounding towns and villages.

B. Project Scope

4.03 As no major natural gas reserves have yet been found in India andlong-term additional naphtha supplies at prices low enough for fertilizerproduction are unlikely to be available, the Government is encouraging theuse of heavy fuel oil as a feedstock for ammonia production, plus coal forthe generation of steam and power. The first plant in India using thesefuels is already under construction at Nangal (FCI) and more installationsof this type are either ready for construction or planned (Sindri, Trombay V,Delhi Cloth Mills, Bathinda). The proposed Phulpur ammonia unit will closelyresemble the Nangal plant, both as to scope and design.

4.04 IFFCO plans to convert all of the ammonia to be produced at Phulpurin its 900 TPD (297,000 TPY) ammonia unit into prilled urea, as none will beneeded for other purposes and ample by-product carbon dioxide will be avail-able from the gas-producing section. The ammonia will be fed to a 1,500 TPD(495,000 TPY) urea unit, which will add an equivalent of 228,000 TPY of N toIndia's fertilizer capacity. At first all of the output will be packed inplastic lined jute bags to be purchased in the country but, if opportune,some urea may be bulk-shipped and other types of packaging may be used in thefuture. The project will include all necessary offsites such as railroadsidings, oil and coal storage and handling, ash disposal, water and effluenttreatment, cooling towers, product storage and shipping, maintenance shops,offices and personnel facilities. The envisaged plant layout is shown inAnnex 4-2.

C. Feedstocks and Other Needs

4.05 lieavy fuel oil will be brought from existing domestic refineries(primarily the one at Barauni, some 200 km away), the planned one at Mathura,in UP south of Delhi (at a distance of about 500 km), or be imported; annualconsumption will be of up to 250,000 tons. Representative chemical and physi-cal specifications and price data are given in Annex 4-3. The project's annualcoal requirements of about 400,000 tons will be moved by rail from mines inBihar and Madhya Pradesh, over a mean distance of some 400 km. Main speci-fications and typical price data for coal, power and water are shown in

- 14 -

Annex 4-4 and requirements of raw materials, utilities and other needs inAnnex 4-5. Methanol needed for gas purification and chemicals for watertreatment are available from Indian producers, as are jute bags and plasticliners.

4.06 IFFCO has agreed to enter, by December 31, 1975 into long-term con-tracts for the provision of the required supplies of heavy fuel-oil, coal andpower. The Government has assured the Bank that arrangements will be madefor the adequate supply of all materials required to operate the project atfull capacity, and promised to send letters, not later than the end of thepresent year, to the supplying agencies (Barauni refinery, the UP StateElectricity Board and coal mines). The Government has also agreed to takeall steps necessary to ensure that a sufficient number of railway cars areavailable for the transportation of raw materials and products.

D. Technology

4.07 For ammonia plants using heavy fuel oil feedstocks, experiencedlicensors for the fuel oil partial oxidation process are Shell (Holland) andTexaco (USA). Additionally, purification of the snythesis gas produced fromheavy fuel oil is most efficiently achieved by absorption type processes.For this project, sulfur and carbon dioxide removal together with carbonmonoxide conversion using the technology offered by Lurgi (F. R. Germany) isproposed.

4.08 Processes for air separation, nitrogen wash, ammonia and urea syn-theses are more widely available. Accordingly, invitations on an internationalbasis are being sent to several major engineering firms who have appropriateexperience in building large ammonia and urea plants in conjunction with theabove licensed technologies. Evaluations and selections will be made on thebasis of technical competence as well as optimum capital and discounted operat-ing costs, technical preferences, completion times and successful experience.

4.09 The ammonia plant will be a single-train installation using threepartial oxidation units and one air-separation unit. The urea plant willbe of single-train design, using one prill tower. All technology and equip-ment for these plants as well as for ancillary units and offsites will be ofproven design and construction. The proposed processes are described inmore detail in Annex 4-5 and a material flowsheet is shown in Annex 4-6.

E. Ecology

4.10 IFFCO has agreed to take all measures necessary to ensure that theammonia and urea plants plus their offsites will be designed and operatedaccording to environmental and safety standards approved by the Bank. About7,000 TPY of sulfur will be released from the heavy oil feedstock; this willbe recovered as elemental sulfur and sold. Carbon produced in the partialoxidation units will be continuously collected and used along with coal toproduce steam. Process water contaminated with methanol and other compoundsfrom the gas purification process as well as by urea plant wash-down water,

- 15 -

will be sent to an effluent-treatment unit prior to disposal. Urea dust fromthe prilling tower will be reduced to very low proportions by suitable arres-tors, to minimize product loss as well as air pollution. Coal ash, amountingto some .400 TPD will be disposed of in local ravines and some may possiblybe used locally to produce building materials. More details on environmentalprotection are given in Annex 4-7.

F. Employment, Training and Social Aspects

4.11 The project will provide employment for some 600 people, as shownin Annex 4-8. Many of these will be drawn from the town of Phulpur andnearby villages. Senior new production and maintenance staff will be giventraining in the IFFCO ammonia/urea plant at Kalol and elsewhere, prior tostart-up. They will be supplemented by experienced Kalol people during plantcommissioning and initial production stages. New technicians will be giventraining on the site during construction and start-up by IFFCO and contractors'personnel. The Company has already established an extensive training programfor its personnel at Kandla and Kalol.

4.12 The project will provide other benefits besides an annual additionof about 230,000 tons of N to India's fertilizer production. It will be aboon to the Phulpur area by creating many new direct and indirect jobs.Being a cooperative, IFFCO is very conscious of its social role. Ithas in the past, and will continue, to assist local communities and coopera-tives in many ways and mainly through training in industrial skills, marketingand improved farming methods. Constructing the project will employ for aboutfour years some 2,000 skilled and unskilled people drawn from the local areaand other parts of India. In addition, an estimated US$40 million worth ofequipment made by Indian manufacturers is likely to be purchased, provideddelivery times permit it.

G. Project Execution and Operation

4.13 IFFCO's plants at Kalol and Kandla have been constructed under theoverall management of the Company's project group. Close adherence toschedules in these projects indicates the IFFCO project team has provencompetent, with the assistance of a few experienced expatriates and in con-junction with major engineering firms, to manage the construction of a largefertilizer plant (para. 2.06).

4.14 IFFCO proposes to undertake the Phulpur project with the assistanceof engineering firms, of which two would be foreign having the necessaryexperience in urea and in ammonia based on fuel oil feedstock (para. 4.08)and the others would be Indian firms in charge of design and engineering foroffsites. The engineering firms would be coordinated and managed by a ProjectImplementation Unit within IFFCO (Annex 4-9), to be staffed essentially withthe Kalol and Kandla project groups after the start-up of these plants. How-ever, availability of this personnel could be delayed and, more importantly,they will have experience in a gas and naphtha-based ammonia plant, but not

- 16 -

in the more complex technology used in fuel oil-based plants. IFFCO hastherefore agreed to engage the services of qualified technical advisors assoon as IFFCO or the Bank deem such services necessary for the timely andefficient execution of the project.

4.15 The starting date for the construction of the Phulpur project isJanuary 1, 1975, when all necessary financial agreements are expected to havebeen reached. However, in view of the high costs of any delays in the pre-sent tight market for fertilizer plant equipment, some advanced contractingfor engineering services and process licensing, and placing orders for somelonglead items of equipment are envisaged. Under these conditions, start-upby August 1978 is anticipated. This timing will be reviewed with the engin-eering firms scheduled to be selected in November 1974, who, with IFFCO, willdevelop detailed critical path networks covering all aspects of the project.A preliminary overall schedule is shown in Annex 4-10. To ensure that sched-ules can be fulfilled, the Government has agreed to process and issue promptlyall import licenses, make available the foreign exchange and allocate locallyproduced materials as needed for the execution of the project.

4.16 The selected engineering firms will agree to furnish IFFCO withcomplete design and purchasing data within specified periods. Failure tomeet these deadlines will subject the firms to penalty payments. Plant per-formance guarantees in terms of capacity, product quality, and feedstockand utility requirements will be obtained from each process licensor andengineering firm. Inability to meet these guarantees will trigger penalties,unless effective corrections are made in the field without cost to IFFCO.It is planned to use experienced Indian contractors to undertake civilengineering design and construction, under the overall supervision and coordi-nation of the IFFCO Project Implementation Unit. Plant erection will alsobe undertaken by Indian contractors under the supervision of the firms chosento supply process and design engineering. Requirements for the movement ofsome heavy equipment are described in Annex 4-11.

4.17 Project operation during commissioning and initial production willbe undertaken by trained Indian staff under the supervision of IFFCO seniorpersonnel on loan from the Kalol plant working in conjunction with special-ists from the ammonia and urea plant licensors and engineers. Thereafter,should it not be possible to build up production as now envisaged or maintainit, IFFCO has agreed to secure the outside expertise needed to overcome suchoperational difficulties. When full-scale production has been attained, plantoperations and management will be integrated within the IFFCO corporatestructure as shown in Annex 4-12.

- 17 -

V. CAPITAL COST ESTIMATE AND FINANCING PLAN

A. Capital Costs

5.01 The total cost of the project is estimated at US$220.5 (Rs 1,655)million of wlhich US$107.3 (Rs 805) million is foreign exchange. The estimateis summarized below and shown in detail in Annex 5-1. The estimate is basedon present prices, whicli have been arrived at in consultation withi generalcontractors currently building similar factories in India and elsewhere.Physical contingencies have been estimated at about 10% of the base estimatedproject cost. Provisions for price escalation are based on the end-of-1974cost estimate including phlysical contingencies and projected price escalationrates of 11'a during 1975 and 7.5%a annually thereafter for equipment andforeign exchange costs and 10% and 8% respectively for civil works and otherlocal currency costs. Derivation of the escalation factors is shown inAnnex 5-2.

Summary of Capital Cost Estimates

in Rs million in US$ millionForeign Local Foreign LocalExchange Currency Total Exchange Currency Total %

Land Acouisition, SiteDevelopment and Township 4 23 27 o.6 3.1 3.7 2.6

Equipment, Supplies & Spares 380 210 590 50.6 28.1 78.7 56.6Freight, Insurance, Handlingand Duties 20 146 166 2.7 19.4 22.1 15.9

Licenses and Engineering 72 11 83 9.6 1.5 11.1 8.0Erection and Supervision 22 40 62 2.9 5.4 8.3 6.oCivil Works 13 52 65 1.7 7.0 8.7 6.2Project Management Services 11 19 30 1.5 2.5 4.0 2.9Pre-operating Expenses - 19 19 - 2.5 2.5 1.8Base Cost Estimate (BCE) 522 520 1,042 69.6 69.5 139.1 100.0

Physical Contingencies(10% of BCE) 53 53 106 7.0 7.0 14.0 10

Price Escalation (18.4% ofBCE plus physical contin- 106 105 211 14.1 14.0 28.1 20.2gencies)]

Installed Cost 681 678 1,359 90.7 90.5 181.2 130.2Working Capital - 98 98 - 13.0 13.0 9.3Expected Project Cost 681 776 1,457 90.7 103.5 194.2 139a5

Interest during Construction 125 73 198 16.6 9.7 26.3 -

Total Financing Required 806 849 1,655 107.3 113.2 220.5 -

1/ 18.5% on all the equipment and foreign exchange costs, and 18.0% onCivil Works and other local costs.

- 18 -

5.02 The initial working capital is estimated at about US$13.0 (Rs 98)million, all in local currency (Annex 5-3). The interest during constructionfor the project has been estimated at US$26.3 (Rs 197) million in Annex 5-4and is based on the disbursement schedule shown in Annex 5-5 and a 10-1/4,interest rate on all loans, i.e. those from the Bank and Industrial Develop-ment Bank of India (IDBI) as well as the subordinated loan (quasi-equity)from the Government.

B. Financing Plan

5.03 The proposed financing plan for the project is as follows:

Financing Plan-------- million Rs ------ …- -------- million US$…Foreign Local Foreign Local % oExchange Currency Total Exchange Currency Total Tot

EquityCooperatives - 220 220 - 29.2 29.2 13GOI 360 360 - 48.0 48.0 21

Sub-total - 580 580 - 77.2 77.2 35

Subordinated DebtGOI - 83 83 - 11.0 11.0 5

Long-Term DebtIBRD 817 - 817 109.0 - 109.0 49,IDBI _ 175 175 23.3 23.3 10.

Sub-total 817 175 992 109.0 23.3 132.3 60

TOTAL FINANCING 817 838 1.655 109.0 111.5 220.5 100.

5.04 The Bank has stressed its support of maintaining the participationof the cooperative institutions in IFFCO's equity as high as possible. TheBank has therefore agreed to permit the Government's equity contribution tobe reduced by an amount equal to the Company's internal resources that--al-though not counted upon in the above financing plan--could be made availableby IFFCO during project implementation provided that all the financial covenantsagreed upon (para. 6.09) are kept. However, since, on the other hand, thecollection of funds from a large number of cooperatives towards their equitycontribution may not proceed in step with the project's requirements, a backupguarantee has been obtained from the Government to make promptly available toIFFCO any difference between the expected and the actual equity contributionmade by cooperative institutions.

5.05 The proposed IBRD loan to IFFCO will be guaranteed by the Govern-ment and is assumed to be for 16 years (starting December 1974) including

- 19 -

5 years of grace at an assumed annual interest rate of 8% plus a 2-1/4%

guarantee fee payable to the Government. The other long-term loans (from

the Government and IDBI) are assumed to be made to IFFCO at 10-1/4% interest

rate and for a term of 15 years including a 5 year grace period, except that

the subordinated loan from the Government will only be repaid -- both as

regards interest and principal -- to the extent that after such payments theCompany can meet a minimum current ratio test, as discussed further below(paras 6.04 and 6.10). The prompt availability of these loans has been con-

firmed during negotiations. Under these assumptions and considering the

subordinated debt as quasi-equity, the project will be financed 60% by debt

and 40% by equity.

5.06 Should there be any cost overrun on the project and IFFCO be unable

to provide the necessary funds when needed and in a form satisfactory to the

Bank, it will be the responsibility of the Government to make any shortfall

available to IFFCO whether in local or foreign currency.

C. Procurement and Disbursement

5.07 International competitive bidding procedures in accordance with

Bank Guidelines will be used for equipment and materials estimated to cost

about US$66 million. Proprietary equipment essential to the process and

items in limited supply, which are critical to the timely completion of the

project and which are estimated to cost about US$8 million, may be procured

following bidding from restricted lists of qualified suppliers, with prior

approval of the Bank. Small items, costing less than US$50,000 equivalent,

with a total estimated cost of about US$2 million, may be purchased from

manufacturers and local representatives of foreign suppliers on the basis

of suitability, availability and price considerations following approval by

the Bank of the list of items involved. A preference of 15% or the customs

duty, whichever is lower, will be allowed to Indian manufacturers for the

purDose of evaluating international competitive bids. Bid evaluation will

be IFFCO's responsibility with the assistance, as required, from the engineering

firms to be contracted (para 4.08). The short-lists of prequalified suppliers

for long-lead items as well as thieir names of engineering firms (para 4.08and 4.14) and the terms of their contracts will be subject to prior Bankapproval. To expedite deliveries in a tight equipment supply position,

IFFCO will send its own procurement officers to the consultants' or to

potential suppliers' main offices.

5.08 Of the total estimated cost of about US$10n million for equipment and

materials, it is estimated that, following Bank guidelines, about US$61 million

will be imported and about US$15 million would be won through international com-'

petitive bidding by local suppliers. The balance of about US$25 million would

be procured locally and not financed from the proceeds of the Bank loan.

D. Allocation and Disbursement of IBRD Loan

5.09 The proceeds of the IBRD loan will cover the estimated cost ofinternationally bid equipment and spares, including the estimated value of

- 20 -

local equipment contracts awarded after such international bidding, pro-perietory or long-lead items procured, with prior approval of the Bank, fromselected bidders, and the foreign exchange cost of licenses, engineeringand technical services, as well as interest during construction on the Bankloan. Expected price escalation has been included in the allocated cate-gories of the loan as shown below.

Allocation of IBRD Loan(US$ million)

Equipment, Freight, Supplies and Spares 67.3Licenses and Engineering 11.4Project Management, Erection and Supervision 5.2Interest during Construction 16.6Unallocated (physical contingencies) 8.5

109.0

5.10 Quarterly disbursement forecasts for the Bank loan are containedin section C of Annex 5-5.

VI. FINANCIAL ANALYSIS

A. Analysis of the Project

6.01 The financial analysis of the project is based on a projectionextending from the expected start of commercial operations, in September1978, to the end of 1990. with the plant depreciated over the same periodof abou-t 12 years on a straight line basis (Annex 6-1) and production build-ing up from 60% capacity utilization through December 1979 to 90% in 1981.Operating costs and urea sales have been based on estimated end-of-1974prices escalated through mid-1978 assuming annual domestic inflation ratesof 12% during 1975, 8% during 1976 and 6% afterwards. 1/ As noted earlier,the Government controls ex-factory and retail prices for urea as well asthe prices for coal and heavy fuel oil. The appraisal assumes that, in linewith a recent general policy decision, confirmed during negotiations, theGovernment will allow prices for urea to rise with feedstock, coal and othercosts, leaving prices in real terms unchanged, and leading to 1978 ex-factoryprices of Rs 1,450 (US$193) per ton of urea and Rs 561 (US$75) per ton ofheavy fuel oil.

1/ These rates which yield a compound factor of 1.32 for the periodconsidered, are consistent with country economic projections.

- 21 -

6.02 The production cost structure of the project, in 1978 prices, isshown in Annex 6-2 and summarized below, for a 90% capacity utilization.

Cost per Ton of Urea (Bagged)

Project Production Costs (1978 Prices)Unit per Ton Annual

US$ Rs US$ RsMillion Million

Fuel Oil 38.40 288 17.09 128.2Coal 12.00 90 5.37 40.3Bags 15.87 119 7.07 53.0

Other Variable Costs 6.00 45 2.69 20.2

Sub-total Variable Costs 72.27 542 32.23 241.7

Fixed Costs except Depreciation 16.93 127 7.53 56.5Depreciation 36.53 274 16.28 122.1

Total Cost 125.73 943 56.04 420.3

6.03 The long-term debt service schedule for the project is shown inAnnex 6-3. The project's forecast financial statements through 1990 andthe major assumptions used are contained in Annex 6-4. A summary of theinitial five years (1978-1982) is shown on the following page.

6.04 Forecast financial statements show that, if the project performsas expected, the results will be satisfactory. Considering subordinateddebt as equity, debt service coverage 1/ would be at least 1.7, the currentratio 1.5:1.0 or higher, and the debt:equity ratio, which is projected to be61:39 at the end of 1978, would rapidly improve thereafter. In fact, theproject would generate enough cash to enable repayment of tile subordinateddebt in 10 years as shown in Annex 6-3, while at the same time maintaining atotal debt service coverage 2/ of not iess than 1.6 (except for the firstfew nonths of operation) and meeting all other financial covenants. There-fore, the financial forecasts indicate that all debt service including that

on subordinated debt can be met by the project.

6.05 The breakeven charts for the project are shown in Annex 6-5. Exceptfor the initial months of operations less than 64% and 53% capacity utiliza-tion are required for the plant to breakeven on a profit and a cash basisrespectively.

1/ Excluding the debt service on subordinated debt.

2/ Including the debt service on subordinated debt.

- 22 -

Summary Financial Forecast for the Project(Rs million) ]/

Year Ending December 31 1978 / 1979 1980 1981 1982

Capacity Utilization (%) 60 60 80 90 90

Income Statement and Cash FlowFertilizer Sales 78 431 574 646 646Cost of Sales (Net) / 69 338 391 418 418Interest Charges Y 37 110 107 99 91Income Taxes (55%) - - 16 71 75Net Profit (Loss) (28) (18) 60 58 62Depreciation 41 122 122 122 122Operating Cash Flow 50 215 289 279 275Debt Service Ž1 34 102 165 162 159Total Debt Service Y 37 110 181 178 174

Balance SheetCurrent Assets 132 145 151 158 165Cumulative Cash / - 91 193 288 382Net Fixed Assets and Spares 1,516 1,394 1,271 1,149 1,027Current Liabilities / 22 97 101 105 110Long-Term Debt 992 926 856 781 702Quasi Equity (subordinated debt) 82 74 66 58 50Equity 551 533 593 651 712Total Assets or Liabilities 1,648 1,630 1,615 1,594 1,573

RatiosDebt Service Coverage 1.5 2.1 1.7 1.7 1.7Total Debt Service Covs:,ageY 1.3 1.9 1.6 1.6 1.6Current Ratio 6. o 1.5 1.5 1.5 1.5Debt Equity Ratio / 61:39 60:40 56:44 52:48 48:52Net Profit/Sales (%) (36) (4) 10 9 10

In 1978 prices. Last digit discrepancies are due to roundingE Four months of operation onlyT Cost of sales (Annex 6-4) less sales of by-product sulfur

Including interest charges on subordinated debtNet income after taxes plus depreciation and interest charges on all debt

7/Excluding debt service on subordinated debtB Including debt service on subordinated debtv Funds not required for working capital

Including current portion of the subordinated long-term debtSubordinated debt included in equity.

- 23 -

B. Financial Rate of Return and Sensitivity Analysis

6.06 For purposes of calculating the financial rate of return of theproject, capital costs are converted to constant 1978 rupees (Annexes 6-6and 6-7) and the cost and benefit streams are shown in Annex 6-8. The returnis 10.3%, after taxes or 13.9%1' before taxes. Several factors contribute tothis relatively low return: high capital costs reflecting the sharp priceescalations recently experienced and expected during project implementationas wzell as the absence of existing infrastructure at the project site; theneed to lengthen the construction period on account of tight equipmentsupplies: and tile high income tax rate of 55%, which depresses the aftertax rate of return by about 3.6 percentage points.

6.07 Sensitivitv tests are shonm in Annex 6-9 and summarized below forthe base case ex-factory price of Rs 1,450 (US$193) per ton of urea in 1978prices, corresponding to a 1974 price of Rs 1,100 per ton (para 3.16). Therate of return is also shown for ex-factory prices 10% above and below thebase case price (As 1,595 and 1,305 per ton respectively). 'l'hese pricesare in line wit,] estinated long-term economic prices (para 7.02) and con-siderably below current world prices.

Financial Rate of Return (%)

Ex-factory Urea Price, Rs/ton 1,305 1,450 I 9,US$/ton 174 193 21K

(a) Base Case 8.5 10.3 11.9(h) Base Case before Taxes 10.7 13.9 16.8(c) Operating Cost up 10% 7.6 9.5 11.2(d) Operating Cost down 10% 9.4 11.1 12.7(e) Slower Capacity Build-up 7.6 9.3 10.8(f) One-year delay in Construction 8.0 9.6 11.0(g) 10%0 Cost Overrun 7.6 9.2 10.3(1h) 10% Cost Overrun and One-Year Delay in

Construction 7.1 8.6 10.0

C. Consolidated Forecasts for IFFCO

6.08 As mentioned before, the financial forecasts for the project aremore than adequate. The Bank loan, lhowever, will be made to IFFCO and notto the Pnulpur Project Unit. IFFCO's existing plants are expected to showvery satisfactory profitability and liquidity by the time the Phulpur plantbegins operations. Therefore, the consolidated income and cash flow pro-jections for the existing and the new facilities--shown in detail in Annex 6-10and summarized below--are also very favorable. Debt service coverage (exclud-ing subordinated debt) will be 2.2 or better and total debt service coverage(including subordinated debt), at least 1.9. Since all financial covenantscan be met, the consolidated financial forecasts include annual payments onboth the existing and the new subordinated debt to the Government beginningin 1977 and 1980 respectively and both are expected to be fully repaid by theend of 1989.

- 24 -

Summary of Projected Consolidated Financial Statementsj/(Rs million)

Year Ending December 31 1978 1979 1980 1981 1982

Capacity Utilization (%)Project (Phulpur) 60 60 80 90 90Kalol Unit 90 90 90 90 90Kandla Unit 80 90 90 90 90

Income Statement and Cash Flow (1978 Prices)Sales 1,466 1,919 2,063 2,135 2,135Cost of Sales (Net) 1,067 1,423 1,476 1,503 1,503Interest Charges ?i 95 161 146 133 121Profit before Taxes 304 336 441 499 511Income Taxes (55%) 167 184 243 274 281Net Income (Loss) after Taxes 137 151 198 224 230Depreciation 109 191 191 191 191Operating Cash Flow j 343 503 535 549 542Debt Service 4/ 101 183 246 239 232Total Debt Service -/ 121 208 278 270 261

Balance SheetCurrent Assets 397 397 397 398 404Cumulative Cash:(a) Available for Investment 450 733 977 1,2 1,(b) Available for Distribution W 28 39 53 69 85Net Fixed Assets and Spares 2,150 1,960 1,769 1,578 1,387Current Liabilities 7/& 146 231 235 240 244Long-Term Debt 1,441 1,327 1,208 1,085 958Quasi Equity 169 149 131 114 96Equity 1,271 1,423 1,620 1,845 2,075Total Assets ow Liabilitiss 3,025 3,129 3,195 3,283 3,373

RatiosDebt Service Coverage 3.4 2.7 2.2 2.3 2.3Total Debt Service Coverage 2.8 2.4 1.9 2.0 2.0Current Ratio 2.7 1.7 1.7 1.7 1.6Debt Equity Ratio / 50:50 46:64 41:59 35:65 30:70

j/ Last digit discrepancies due to rounding2 Interest charges on all debt, including subordinated debt

Net income after taxes plus depreciation and interest charges/ Excluding debt service on subordinated debtJ/ Including debt service on subordinated debtP/ Limited to 7% of net income'T Current portion of regular and subordinated debt includedvK Subordinated debt included in equity.

- 25 -

D. Financial Covenants

6.09 The estimated consolidated financial position of IFFCO by the timethe project commences commercial operation appears satisfactory. To ensurethat the project, and IFFCO in general, will operate in a financially satis-factory manner, the following covenants have been agreed upon by IFF0O:

(a) The project will be operated as a separate profit centerwith its own income, cashflow and balance sheet accountsfor control purposes;

(b) The project entity will maintain a current ratio of atleast 1.5:1.0 and IFFCO will maintain for itself a currentratio of not less than 1.1:1.0 through December 31, 1976,and of not less than 1.5:1.0 afterwards;

(c) Additional investments in fixed assets in excess of US$3million per year will be subject to prior Bank approval;

(d) IFFCO will take all necessary actions not to exceed a debt:equity ratio of 60:40 including the subordinated debt asequity;

(e) IFFCO will not incur any additional debt, if by so doingit could not maintain a debt service coverage of at least1.4 in any of the succeeding fiscal years;

(f) No dividend distribution nor debt service payments forinterest, principal or both on the subordinated debt willbe paid by IFFCO unless such payments are covered by currentearnings and subject to maintaining a current ratio of atleast 1.5 after such payments; and

(g) Completion date for the project will be understood tomean the date on which the facilities included in theproject have been tested and proven to be satisfactory inaccordance with sound engineering procedures and practicesand have maintained daily production averaging 80% of fullcapacity for a period of at least 60 consecutive days.

E. Major Risks

6.10 The project capital cost estimate includes US$28 million for priceescalation. This provision should be adequate but in the present strongsellers' market and under unprecedented inflation pressure in India, a priceescalation beyond that provided for cannot be ruled out. The project isbased on a conservative time schedule and the capital cost estimate providesfor project management assistance, which, combined with IFFCO's projectimplementation experience, should reduce risks in the project execution andoperation. However, unexpected delays in equipment deliveries from heavilybooked suppliers and inadequate fuel oil and coal supplies could also affect

- 26 -

the project. On the other hand, the financial position of IFFCO as a wholeis protected by the cash flow of its two existing plants which are nowmechanically complete and are expected to start production in a few weeks.

VII. ECONOMIC ANALYSIS

A. World Fertilizer Prices