facilitating a sustainable supply chain & fuel supply

TRANSCRIPT

Facilitating a Sustainable Supply Chain & Fuel

Supply

Shah Nawaz Ahmad

Senior Adviser

India, Middle East and South-East Asia

INBP Conference

Nov 13-14, 2019

Mumbai,

Presentation TitleName, Job Title 2

Presentation TitleName, Job Title 3

°C anomalyJuly 2018

Source:NASA GISS

Extreme weather: the global summer of 2018

Presentation TitleName, Job Title

© 2015 Organisation for Economic Co-operation and Development 4

Source: International Energy Agency

IEA 2°C Scenario: Nuclear is Required to Provide the Largest Contribution to Global Electricity in 2050

Presentation TitleName, Job Title

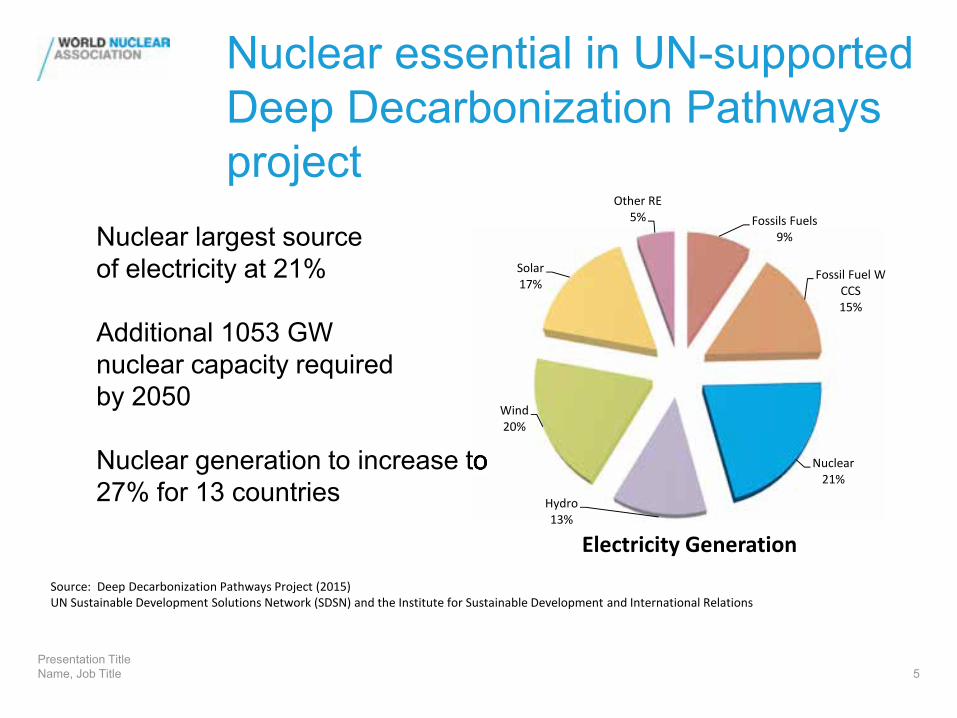

Nuclear essential in UN-supported Deep Decarbonization Pathways project

5

Nuclear largest source of electricity at 21%

Additional 1053 GWnuclear capacity required by 2050

Nuclear generation to increase to 27% for 13 countries Nuclear generation to increase to

Fossils Fuels9%

Fossil Fuel W CCS15%

Nuclear21%

Hydro13%

Wind20%

Solar17%

Other RE5%

Electricity GenerationSource: Deep Decarbonization Pathways Project (2015) UN Sustainable Development Solutions Network (SDSN) and the Institute for Sustainable Development and International Relations

Presentation TitleName, Job Title

Decarbonising electricity generation –need for low life cycle emissions:

Nuclear energy is among the best

6

Source: World Nuclear Association meta study, incl. IPCC 2014

Presentation TitleName, Job Title

Effective safety paradigm

Paul Scherrer Institut 1998: considering 1943 accidents with more than 5 fatalities

The alternatives to nuclear are far more dangerous – even including accidents

7

Presentation TitleName, Job Title

Environment

Chiba refinery fire

Smog in Beijing

8

From the society perspective:Increase genuine public wellbeing

Presentation TitleName, Job Title

OECD electricity generating cost projections for year 2010 on – 5% discount rate, c/kWh

country nuclear coal coal with CCS Gas CCGT Onshore wind

Belgium 6.1 8.2 - 9.0 9.6

Czech R 7.0 8.5-9.4 8.8-9.3 9.2 14.6

France 5.6 - - - 9.0

Germany 5.0 7.0-7.9 6.8-8.5 8.5 10.6

Hungary 8.2 - - - -

Japan 5.0 8.8 - 10.5 -

Korea 2.9-3.3 6.6-6.8 - 9.1 -

Netherlands 6.3 8.2 - 7.8 8.6

Slovakia 6.3 12.0 - - -

Switzerland 5.5-7.8 - - 9.4 16.3

USA 4.9 7.2-7.5 6.8 7.7 4.8

China* 3.0-3.6 5.5 - 4.9 5.1-8.9

Russia* 4.3 7.5 8.7 7.1 6.3

EPRI (USA) 4.8 7.2 - 7.9 6.2

Eurelectric 6.0 6.3-7.4 7.5 8.6 11.3

9

Presentation TitleName, Job Title

OECD electricity generating cost projections for year 2010 on – 10% discount rate, c/kWh

country nuclear coal coal with CCS Gas CCGT Onshore wind

Belgium 10.9 10.0 - 9.3-9.9 13.6

Czech R 11.5 11.4-13.3 13.6-14.1 10.4 21.9

France 9.2 - - - 12.2

Germany 8.3 8.7-9.4 9.5-11.0 9.3 14.3

Hungary 12.2 - - - -

Japan 7.6 10.7 - 12.0 -

Korea 4.2-4.8 7.1-7.4 - 9.5 -

Netherlands 10.5 10.0 - 8.2 12.2

Slovakia 9.8 14.2 - - -

Switzerland 9.0-13.6 - - 10.5 23.4

USA 7.7 8.8-9.3 9.4 8.3 7.0

China* 4.4-5.5 5.8 - 5.2 7.2-12.6

Russia* 6.8 9.0 11.8 7.8 9.0

EPRI (USA) 7.3 8.8 - 8.3 9.1

Eurelectric 10.6 8.0-9.0 10.2 9.4 15.5

10

Presentation TitleName, Job Title

Presentation TitleName, Job TitleTitle Name 12

COUNTRY

NUCLEAR ELECTRICITY GENERATION

2018

REACTORS OPERABLE

August 2019

REACTORS UNDER

CONSTRUCTION

August 2019

REACTORS PLANNED

August 2019

REACTORS PROPOSED

August 2019

URANIUM

REQUIRED

2017

TWh % e No. MWe net No. MWe gross No. MWe

gross No. MWe gross tonnes U

Argentina 6.5 4.7 3 1702 1 27 1 1150 2 1350 195

Bangladesh 0 0 0 0 2 2400 0 0 2 2400 0

Belarus 0 0 0 0 2 2388 0 0 2 2400 0Brazil † 14.8 2.7 2 1896 1 1405 0 0 4 4000 321China 277.1 4.2 47 45,688 11 10,005 43 50,900 170 199,610 8289Finland 21.9 32.5 4 2764 1 1720 1 1250 0 0 494France 395.9 71.7 58 63,130 1 1750 0 0 0 0 9502India 35.4 3.1 22 6219 7 5400 14 10,500 28 32,000 843Japan 49.3 6.2 33 31,679 2 2756 1 1385 8 11,562 662

Korea RO (South)

127.1 23.7 24 23,231 4 5600 0 0 2 2800 4730

Pakistan 9.3 6.8 5 1355 2 2322 1 1170 0 0 217Romania 10.5 17.2 2 1310 0 0 2 1440 1 720 183Russia † 191.3 17.9 36 29,139 6 4973 24 25,810 22 21,000 5380Slovakia 13.8 55.0 4 1816 2 942 0 0 1 1200 651Slovenia 5.5 35.9 1 696 0 0 0 0 1 1000 141Spain 53.4 20.4 7 7121 0 0 0 0 0 0 1275Turkey 0 0 0 0 1 1200 3 3600 8 9500 0

Presentation TitleName, Job TitleTitle Name 13

COUNTRY

(Click name forCountry Profile)

NUCLEAR ELECTRICITY GENERATION

2018

REACTORS OPERABLE

August 2019

REACTORS UNDER CONSTRUCTION

August 2019

REACTORS PLANNED

August 2019

REACTORS PROPOSED

August 2019

TWh % e No. MWenet No. MWe

gross No. MWegross No. MWe

grossBangladesh 0 0 0 0 2 2400 0 0 2 2400

China 277.1 4.2 47 45,688 11 10,005 43 50,900 170 199,610India 35.4 3.1 22 6219 7 5400 14 10,500 28 32,000Japan 49.3 6.2 33 31,679 2 2756 1 1385 8 11,562Korea RO (South) 127.1 23.7 24 23,231 4 5600 0 0 2 2800

Pakistan 9.3 6.8 5 1355 2 2322 1 1170 0 0Russia † 191.3 17.9 36 29,139 6 4973 24 25,810 22 21,000Turkey 0 0 0 0 1 1200 3 3600 8 9,500UAE 0 0 0 0 4 5600 0 0 0 0

WORLD* 2563 c 10.3** 444 /(167)

395,756 54/(39) 57,808 111/(

86) 121,829 330/(239) 360,782

TWh % e No. MWe No. MWe No. MWe No. MWeNUCLEAR

ELECTRICITY GENERATION

OPERABLE UNDER CONSTRUCTION PLANNED PROPOSED

Presentation TitleName, Job Title

New reactor starts in 2016-17

South Korea: Shin Kori 3China: Ningde 4China: Hongyanhe 4

USA: Watts Bar 2China: Changjiang 2China: Fangchenggang 2

Russia: Novovoronezh 2 1India: Kudankulam 2

China: Fuqing 3Pakistan: Chasnupp 3

China: Yangjiang 4Pakistan: Chasnupp 4

China: Fuqing 4China: Tianwan 3

14

Presentation TitleName, Job Title

New reactor starts in 2018-19

Russia: Rostov-4Russia: Leningrad 2-1China: Yangjiang 5China: Taishan 1China: Sanmen 1China: Haiyang 1China: Sanmen 2China: Haiyang 2China: Tianwan 4

South Korea: Shin Kori 4Russia: Novovoronezh 2-2China: Taishan 2China: Yangjiang 6

15

Presentation TitleName, Job Title

Scheduled start ups by 2020

MWe2019 Belarus Ostrovets 1 11942019 China, Fangchenggang 3 11802019 China, Fuqing 5 11502019 China, Hongyanhe 5 11192019 China, Huaneng 2102019 Russia, Pevek FNPP 70

MWe2020 Belarus, Ostrovets 2 11942020 China, Hongyanhe 6 11192020 China, Fangchenggang 411802020 China, Fuqing 6 11502020 China, Tianwan 5 11182020 China, Bohai shipyard 602020 Finland, Olkiluoto 3 17202020 India, Kalpakkam PFBR 5002020 Japan, Shimane 3 13732020 Korea, Shin Hanul 1 14002020 Russia, Leningrad II-2 11702020 Slovakia, Mochovce 3 4712020 UAE, Barakah 1 1400

16

Presentation TitleName, Job Title

Innovative nuclear energy

During 5 years, between 2016 and 2020 there are due to be:

• 47 new reactors online• Based on 20 different designs• Built in 11 countries• 2 are newcomer countries• 9 of the 20 designs being built for

the first time

17

Presentation TitleName, Job Title

Reactors reaching 50 years of operation this year

Beznau 1, Switzerland

Ginna, USA

Nine Mile Point 1, USA

18

Presentation TitleName, Job Title

Tarapur 1

Tarapur 2

19

Presentation TitleName, Job Title

Reactors perform well over entire lifetime:Mean capacity factor by age (2014-2018)

20

Presentation TitleName, Job Title

Long-Term Operation (LTO)• In principle, operating for a longer period than initially

expected should normally be economically attractive.• Nuclear power is characterized by high initial capital costs

and low fuel costs, • For well-managed plants with low O&M costs, the cost of

producing electricity can be very competitive. (Tarapur 1&2)• However the licensing requirements that need to be

completed for extending operation vary significantly • In US, some industry commentators have predicted that

over 90 percent of the US reactors could apply for and be granted licence extensions.

• A sustainable supply chain for equipment and services is most relevant for LTO

21

Presentation TitleName, Job Title

• Professor William D’haeseleer study for the European Commission suggested that extending operations for a further 20 years could typically cost less than US$ 1,000/kWe. (New Build EU Overnight cost est $5,500/kWe)

• This would suggest that long-term operation is the cheapest way of providing nuclear power over a 20-year period.

• However, low gas prices in North America have undermined the case for long-term operation, although these cannot be assumed to last indefinitely. (In some projections natural gas prices increase within the time frame of building new nuclear plants).

• The total value of work for long-term operation could amount to some US$ 50-100 billion (depending on the amount of refurbishment deemed necessary by the regulatory body).

• This could amount to around US$ 4 billion a year of international procurement

22

Presentation TitleName, Job Title

Nuclear Power Market • The the market is not a ‘sellers’ market’; however neither is

it a ‘buyers’ market’.

• The main technical barriers to trade are the licensing requirements imposed by the nuclear regulatory bodies for the protection of health and safety and to safeguard materials and know-how from misuse.

• Although a number of technology vendors have obtained regulatory approval for their reactor models across several jurisdictions, no vendor is able to offer its technology everywhere.{Cooperation in Design Evaluation & Licencing (CORDEL)/ Multinational Design Evaluation Programme (MDEP)}

23

Presentation TitleName, Job Title

• There are today eleven consolidated technology vendors offering their technology and services across much of the nuclear fuel cycle.

• While the industry remains weighted towards domestic markets, most vendors are, internationally diversified in terms of their corporate make-up and their supplier base.

• International trade in nuclear components has the potentialto reach nearly US$ 30 billion a year, according to World Nuclear Association reference scenario estimates.

• The value of the investment in new nuclear build to 2035 is of the order of US$ 1.5 trillion, with significant international procurement of US$ 24 to $ 30 billion a year after 2025 (up from about $6-10 billion a year currently).

• About US$ 730 billion will consist of equipment purchases.

24

Presentation TitleName, Job Title

• Competitive pressures are encouraging the localization of manufacturing, joint ventures and international procurement.

• As a result, production is located in several jurisdictions with materials, semi-processed and finished fabrications perhaps crossing several borders prior to reaching the final destination for assembly and installation.

• Services are also performed in different countries either as a result of subcontracting or through the participation of specialist divisions of the same transnational corporation or industrial group.

• Globalization, in short, is as much a part of the civil nuclear scene as it is in other industries.

• The World Nuclear Association believes that the system for import and export between countries should be reviewed to streamline procedures while preserving a sound safeguards regime.

25

Presentation TitleName, Job Title

• A competitive global market exists for the construction and procurement of nuclear power plants.

• Around a decade ago, there were concerns that some ‘choke points’ existed along the supply chain, for instance in terms of heavy forging capacity.

• However, a combination of factors, including i) the cancellation of some planned plants, which followed the March 2011 Fukushima Daiichi accident, ii) investment by existing suppliers and iii) the transfer of technology and localization of manufacturing (especially to China), means there are now sufficient suppliers available to fabricate key reactor components under currently known plans.

• Potentially bottlenecks could re-emerge in the event of multiple reactor orders being issued at the same time as an upturn in capital investment.

26

Presentation TitleName, Job Title

Localization • Localization supports the transfer of technology and raises productivity

in the host country, but needs significant additional efforts. (Need for vendor oversight)

• It creates employment, especially in professional and skilled occupations, directly and indirectly as local companies develop their capabilities and relationships with global companies.

• Direct employment is created from the ‘backward linkages’ in the supply chain through the processing and manufacture of basic inputs and intermediate products and services.

• Jobs may also be stimulated indirectly by helping local suppliers upgrade their capacities so that they are more competitive in international markets, although economic evidence pertaining to its impact is inconclusive.

• Localization attempts to capture some of the investment in electrification for national economic development by raising productivity among local firms and moving their product portfolio ‘up the value chain’.

• Care needs to be taken that localization should not impact project schedules & cost

• A local supply base can provide a convenient service during plant operation and maintenance. The procurement policies for spare parts, supplies and maintenance by plant operators are another important factor

27

Presentation TitleName, Job Title

Export Control • Growing international technical exchange, trade and

investment is presenting a challenge to the existing regime of export control, which was developed at a time of much more limited international business interaction.

• Most export control authorities do not issue general export licences for nuclear-related items, even though they do issue such licences for certain non-nuclear dual-use items,

• This places the nuclear industry at a disadvantage in comparison with the aerospace and defence industries.

• The degree of scrutiny accorded to nuclear technology should be risk-based.

• A nuclear power reactor poses a relatively low technology risk with respect to proliferation

28

Presentation TitleName, Job Title

Uranium• Production from world uranium mines now supplies 90% of the

requirements of power utilities. • Primary production from mines is supplemented by secondary

supplies, formerly most from ex-military material but now the products of recycling and stockpiles built up in times of reduced demand.

• World mine production has expanded significantly since about 2005.• Each GWe of increased new capacity will require about 150 tU/yr of

extra mine production routinely, and about 300-450 tU for the first fuel load.

• Because of the cost structure of nuclear power generation, with high capital and low fuel costs, the demand for uranium fuel is much more predictable than with probably any other mineral commodity.

• Once reactors are built, it is very cost-effective to keep them running at high capacity and for utilities to make any adjustments to load trends by cutting back on fossil fuel use.

• Demand forecasts for uranium thus depend largely on installed and operable capacity, regardless of economic fluctuations.

• However, this picture is complicated by policies which give preferential grid access to subsidised wind and solar PV sources

29

Presentation TitleName, Job Title

Uranium Prices (Graph courtesy of UxC)

(

The reasons for fluctuation in mineral prices relate to demand and perceptions of scarcity. The price cannot indefinitely stay below the cost of production, nor will it remain at very high levels for longer than it takes for new producers to enter the market and anxiety about supply to subside.

30

Presentation TitleName, Job Title

U Purchase Strategies• Govt to Govt Contracts

• Market based purchase✓ Spot Purchase✓ Short / Long Term Contracts

(Most trade is via 3-15 year term contracts with producers selling directly to utilities sometimes at a significantly higher price than the spot market, reflecting the security of supply).

• Market Based Security of Supply ✓ Individual Contract✓ Above contract backed by industry consortium✓ IAEA Fuel Bank

31

Presentation TitleName, Job Title

Conversion• The uranium conversion sector is characterized by a small

number of companies producing UO2 for those reactors fuelledwith natural uranium and UF6 for those using enriched uranium.

• For the last eight years the market was in oversupply caused by reduced conversion requirements and the accumulation of sizeable UF6 stockpiles.

• Excess capacity resulted in the reduction, suspension and even closure of conversion production.

• Today, annual primary production is far lower than annual conversion requirements.

• The market has begun a period of rebalancing, largely absorbing inventories in the near term.

• In the medium term idled capacity is expected to be resumed, while in the long term (towards the end of the next decade in the Reference Scenario), capacity expansion is expected to be needed

32

Presentation TitleName, Job Title

Enrichment • Excess global enrichment capacity has resulted in the

indefinite postponement of new US projects and extensive use of existing capacity for underfeeding and tails re-enrichment.

• Of the major suppliers of enrichment services, CNNC will be the only one to significantly expand its capacity over the forecast period due to the Chinese target of achieving self-sufficiency.

• The three other major suppliers will not need to expand their capacity through to 2040 in the Reference Scenario.

• In the Upper Scenario, additional capacity might be needed as early as in the first half of the next decade.

• However, given the modular nature of centrifuge technology and the construction times for nuclear power reactors, enrichment capacity expansion can take place in a timely way, and supply challenges should be avoided

33

Presentation TitleName, Job Title

Fabricated Fuel • The fuel fabrication market differs from the other stages of

nuclear fuel cycle due to the specificity of the product. • Fuel assemblies are highly engineered and technological

products. • Moreover, the market itself is more regional in character

than global, but this is changing.• Localization can assure long term supply. • At present, existing fuel fabrication capacities are sufficient

to cover anticipated demand for both first cores and reloads; however, in some circumstances it is still possible that supply bottlenecks could occur for certain designs.

34

Presentation TitleName, Job Title

Harmony programme 2016-2050Cumulative 1000 GW new nuclear capacity to 2050

Construction rate doubled from trend of less than 5GW/y to 10GW/y

Then we need to triple from today’s level

35

Presentation TitleName, Job Title

Harmony Programme

The Harmony programme provides a framework for action, helping industry reach out to key stakeholders so that barriers to growth can be removed.

36

Presentation TitleName, Job Title

Level playing field

37

Markets should be reformed to:

• support capital investments• include grid system costs• eliminate nuclear-only taxes• reform subsidies• give credit for low carbon

emissions• value 24/7 reliability• support innovative finance

solutions