factors affecting oil and product prices - trala 2015 annual meeting... · factors affecting oil...

TRANSCRIPT

Factors Affecting Oil and Product Prices

Rayola Dougher

API Senior Economic Advisor

0

20

40

60

80

100

120

140

160

Iran/Iraq war

Gulf War OPEC

cuts 4.2

million

9/11

Low spare

capacity

Recession

Libyan

Uprising

Supply

surplus

The price of oil has fluctuated sharply before

Inflation-adjusted 2014 $/barrel

Sources: Inflation-adjusted average refiners acquisition price for crude oil

PDVSA strike

Iraq War

Asian Growth

$0.00

$1.00

$2.00

$3.00

$4.00

$5.00

Mar-08 Mar-09 Mar-10 Mar-11 Mar-12 Mar-13 Mar-14 Mar-15

Crude Oil $1.18 Gasoline $2.46 Diesel $2.93

Changes in gasoline and diesel prices closely

track changes in crude oil prices

Average prices as of March 6, 2015

Sources: NYMEX (WTI crude oil) and AAA (gasoline and diesel)

Many factors affect the price of oil, but in the end

it comes down to supply and demand

Source: EIA

Growth in Global Oil Supply

Disruptions (mmb/d)

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

Ja

n 2

01

2

Ju

l 20

12

Ja

n 2

01

3

Ju

l 20

13

Ja

n 2

01

4

Ju

l 20

14

Ja

n 2

01

5

OPEC

Non-

OPEC

Growth in U.S. Crude Oil

Production* (mmb/d)

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

Ja

n-2

012

Ju

l-2

01

2

Ja

n-2

013

Ju

l-2

01

3

Ja

n-2

014

Ju

l-2

01

4

Ja

n-2

015

Growth in U.S. oil production has largely offset

the growth in global oil supply disruptions

Source: EIA * Includes hydrocarbon gas liquids, biofuels, and refinery processing gains.

0

0.5

1

1.5

2

2.5

2014 2015 2016

Production

Consumption

World growth in crude oil production surged

ahead of growth in consumption in 2014

Source: EIA, Short-term Energy Outlook, February 2015

(mill

ion

ba

rre

ls p

er

da

y)

U.S. oil production is increasing as a result of

technological innovations

4

5

6

7

8

9

10

1970

1975

1980

1985

1990

1995

2000

2005

2010

2015

U.S. Crude Oil Production (millions of barrels per day)

Source: EIA

>73% growth

2008 to 2014

SHALE ENERGY PROVIDES A NATIONAL OPPORTUNITY

Current and prospective resources and basins in the continental US

Source: EIA based on data from various published studies – updated May 9, 2011

Current Shale Resources

Prospective Shale Resources

Basins

Shallowest/ Youngest

Mid-Depth/ Mid-Age

Deepest/Oldest

Shale Resources, Lower 48 States

Stacked Resources

-0.5

0

0.5

1

1.5

2

2014 2015 2016OPEC North America

Russia and Caspaian Sea Latin America

North Sea Other Non-OPEC

World crude oil and liquid fuels production growth

Mill

ion

ba

rre

ls p

er

da

y

Source: EIA, Short-term Energy Outlook, February 2015

-1

0

1

2

3

4

United

Sta

tes

Cana

da

Bra

zil

Chin

a

Om

an

Austr

alia

Ma

laysia

Ind

ia

Norw

ay

Sud

an

/S.

Sud

an

Oth

er

Nort

h S

ea

Kaza

khsta

n

Vie

tnam

Gab

on

Co

lom

bia

Russia

Syria

Egyp

t

Azerb

aija

n

Mexic

o

Un

ited

Kin

gd

om

2016

2015

2014

Non-OPEC crude oil and liquid fuels production

growth

(mill

ion

ba

rre

ls p

er

da

y)

Source: EIA, Short-term Energy Outlook, February 2015

0%

10%

20%

30%

40%

50%

60%

70%

Crude oil and petroleum product imports have

declined as a share of consumption

Source: EIA

Why does diesel fuel cost what it does?

57% 18% 13%

Crude Oil Excise

Taxes Transportation

and Retailing Refining

12%

Source: EIA, based on average 2014 price of $3.83 per gallon

Combined local, state and federal (cents per gallon) as of January 1,2015

One reason the price of diesel fuel varies by state

is that taxes vary

2013

2014

2015

Projected

2016

Projected

WTI Crudea

($/barrel) 97.91 93.26 55.02 71.00

Brent Crude

($/barrel) 108.64 99.02 57.56 75.00

Gasolineb

($/gallon) 3.51 3.36 2.33 2.73

Dieselc

($/gallon) 3.92 3.83 2.83 3.24

Heating Oil

($/gallon) 3.78 3.73 2.74 3.03

Natural Gasd

($/mcf) 10.30 10.91 10.28 10.56

Electricity

(cents/kwh) 12.12 12.49 12.63 12.85

EIA price forecast

a West Texas Intermediate b Average regular pump price c On-highway retail d Residential average

Source: EIA, Short-term Energy Outlook, February 2015.

Power and Politics

Expanding alternative fuels for transportation:

current laws

The Congressional

Budget Office

predicts the price

of diesel could rise

by up to 51 cents

per gallon and

gasoline by up to

26 cents per

gallon by 2017.

Save consumers up

to $5.8 billion a year

in lower fuel costs

Add 300,000 jobs to

U.S. economy in

2020

Reduce America’s

trade deficit by $22

billion in 2020

Why export crude oil?

Crude oil exports yield economic benefit across all 50 states

Source: ICF International and EnSys Energy,

87% of federal offshore acreage is off-limits to

development

Development of Canadian oil sands would benefit

the U.S. economy

Filling America’s tank Within 10 years Canada and U.S. can provide all our liquid fuel needs

U.S. Oil

Production

Oil from Canada

Biofuels

Oil from

Rest of World

Sources of liquid

fuel supply

in 10 years

53%

13%

10%

24%

72%

18%

10%

EIA Forecast Potential Sources: EIA; Wood Mackenzie

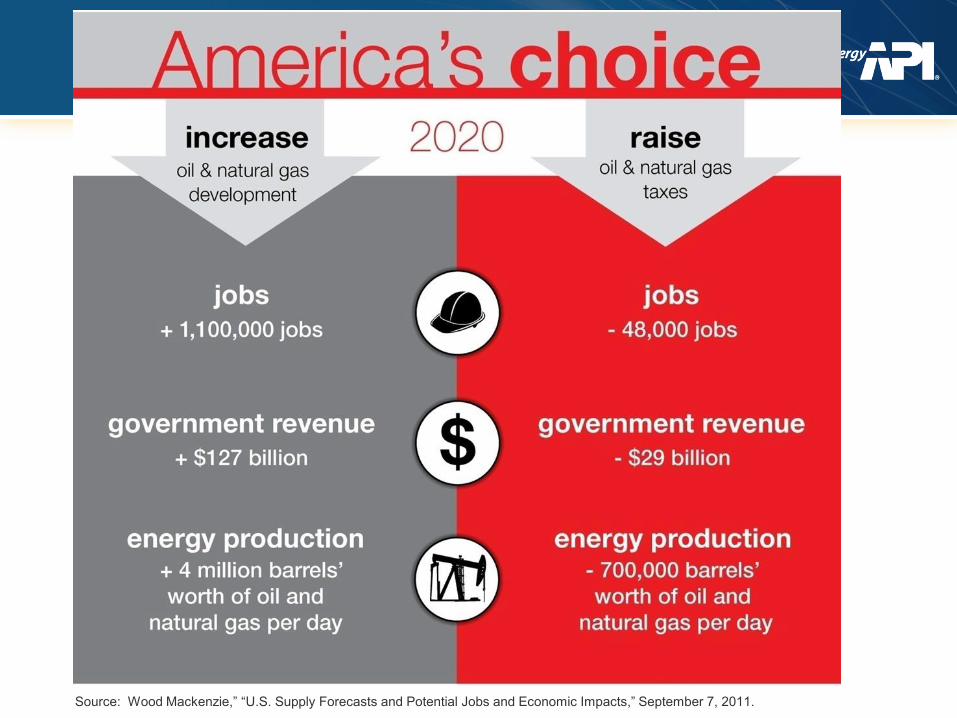

Source: Wood Mackenzie,” “U.S. Supply Forecasts and Potential Jobs and Economic Impacts,” September 7, 2011.

90% 86% 86% 85%

83%

72% 70%

65%

Lead to morejobs

Helpstrengthen

energysecurity

Helpstimulateeconomy

Help lowerenergy costs

SupportO&NG

development

SupportKeystone XL

pipeline

Supportoffshore

development

Increasingenergy taxes

may hurtconsumers

Harris Poll Results on Increased U.S. Oil and Natural Gas Development

Voters voice strong support for increased

domestic oil and natural gas development

Source: Harris Interactive telephone poll, November 5, 2014

For more information visit: www.api.org

www.energytomorrow.org

www.energycitizens.org