fasb 12, fasb 107, fasb 115, fair value,trading securities,maturity

TRANSCRIPT

ACCO.721

FASB 107-115

DATE: 11/04/09

JOSE CINTRON,MBA

FASB “ROCKS” the Accounting World!!

With Fair Value Accounting

for Financial Instruments

There was an Investment Community Interest in Reporting Fair Values of Financial Instruments in Financial

Statements.

The Life Of An Accountant Before 1993

Hmmm...Historical Cost…

Lower of Cost or Market…Life is good...

Objective Conservative Simple to explain

FASB Statement No. 12, Accounting for Certain Marketable Securities

Everything was not perfect. Accountant Before 1993

Net Income Trends

LOCOM Valuation Adjustments

Irregular

earnings

patterns Not

consistent with

realization

principle Cumbersome

Disclosure

(FASB 107)

Current Fair Value Reporting: FASB#107 (1991)

Is cumbersome, inconsistent, and confusing

Does not permit analysts to gauge value and risk

Does not disclose assumptions for gain on sale computations

Accountant

We need FASB #115

FASB Statement No. 115 Accounting for Certain Investments in Debt and Equity

Securities

Keep valuation

adjustments on the

balance sheet until

they are earned!

Classify financial assets according to

management intention!

Three Categories:

Trading securities

Hold to maturity

Available for sale

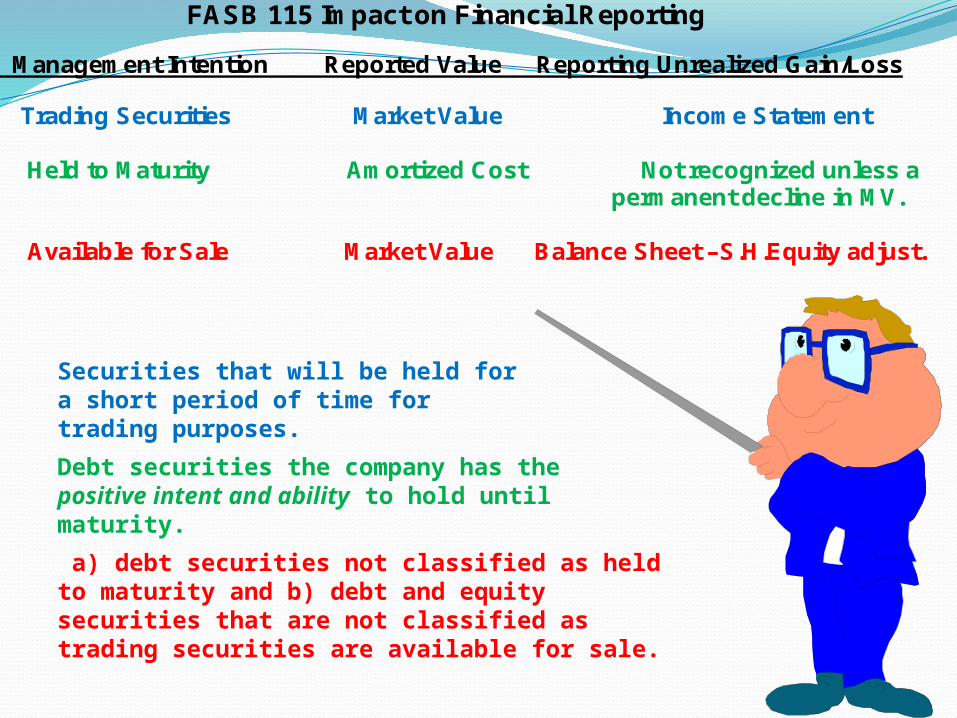

FASB 115 Impact on Financial Reporting

Management Intention Reported Value Reporting Unrealized Gain/Loss Trading Securities Market Value Income Statement Held to Maturity Amortized Cost Not recognized unless a permanent decline in MV. Available for Sale Market Value Balance Sheet –S.H.Equity adjust.

Securities that will be held for a short period of time for trading purposes.

Debt securities the company has the positive intent and ability to hold until maturity.

a) debt securities not classified as held to maturity and b) debt and equity securities that are not classified as trading securities are available for sale.

FASB 115

Market Value = Fair Value

F.V. of Trading Securities - Income Statement.

Held to Maturity – Not recognized / P.I.

F. V. of AFS Securities – SH.Equity Section

Balance Sheet (AFS)ASSETSLIABILITIESEQUITY

Adjustment to:Unrialized gain/ losses on

investments from FV.

Shareholder’s Equity seccion.

FASB 115,Securities with fair market value below cost basis are impairer.

If impairment is determined to be other than temporary, cost basis of individual security must be written down to fair value through income statements.

Fannie Mae and Freddie Mac(2008) significant decline in market price of their stock, these securities are presumed to have other-than-temporary impairment losses if their cost basis is well in excess of current market prices.

• These losses are considered realized and must be recognized in the income statement.

• Losses are capital losses for tax purposes.

The Life Of An Accountant after the Year 1993

Jose,Hmmm…Fair Value Accounting…Equity Adjustments…

Change is hard...

More accurate valuation More difficult to determine

More difficult to explain

“Change is hard, Jose.”

FASB no.115, is here to stay. You will love no. 114

REFERENCESSummary of Statement No. 115,retrieved on Nov.4, 2009 from;http://www.fasb.org/summary/stsum115.shtml

Financial Accounting Standard Board,retrieved on Nov.4, 2009 from;http://www.fasb.org/jsp/FASB/Page/03-16-09_otti.pdf

FASB 115: it's back to the future 115,retrieved on Nov.4, 2009 from;http://www.thefreelibrary.com/

FASB+115:+it's+back+to+the+future+for+market+value+accounting.-a014381134

Summary of Statement No. 107, retrieved on Nov.4, 2009 from;http://www.fasb.org/pdf/fas107.pdf