fasb statement 167 and consolidating variable-interest...

TRANSCRIPT

FASB Statement 167 and Consolidating

Variable-Interest EntitiesPreparing Compliant Financials: Challenges for Mid-Sized and Smaller Accounting Firms

Today’s faculty features:

1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific

WEDNESDAY, NOVEMBER 9, 2011

Presenting a live 110-minute teleconference with interactive Q&A

Today’s faculty features:

For this program, attendees must listen to the audio over the telephone.

Please refer to the instructions emailed to the registrant for the dial-in information.

Attendees can still view the presentation slides online. If you have any questions, please

contact Customer Service at1-800-926-7926 ext. 10.

Elizabeth Jones, Director, KPMG, Chicago

Ashima Jain, Director, PricewaterhouseCoopers, San Jose, Calif.

Marti Bruketta, Director, National Professional Services Group - SEC Services,

PricewaterhouseCoopers, San Jose, Calif.

Conference Materials

If you have not printed the conference materials for this program, please

complete the following steps:

• Click on the + sign next to “Conference Materials” in the middle of the left-

hand column on your screen.

• Click on the tab labeled “Handouts” that appears, and there you will see a

PDF of the slides for today's program. PDF of the slides for today's program.

• Double click on the PDF and a separate page will open.

• Print the slides by clicking on the printer icon.

Continuing Education Credits

Attendees must listen to the audio over the telephone. Attendees can still view

the presentation slides online but there is no online audio for this program.

Please refer to the instructions emailed to the registrant for additional

FOR LIVE EVENT ONLY

Please refer to the instructions emailed to the registrant for additional

information. If you have any questions, please contact Customer Service

at 1-800-926-7926 ext. 10.

Tips for Optimal Quality

Sound Quality

For this program, you must listen via the telephone by dialing 1-866-873-1442

and entering your PIN when prompted. There will be no sound over the web

connection.

If you dialed in and have any difficulties during the call, press *0 for assistance.

You may also send us a chat or e-mail [email protected] immediately so You may also send us a chat or e-mail [email protected] immediately so

we can address the problem.

Viewing Quality

To maximize your screen, press the F11 key on your keyboard. To exit full screen,

press the F11 key again.

FASB Statement 167 and Consolidating Variable-Interest Entities Seminar

Nov. 9, 2011

Ashima Jain, PricewaterhouseCoopers

Elizabeth Jones, KPMG

Marti Bruketta, PricewaterhouseCoopers

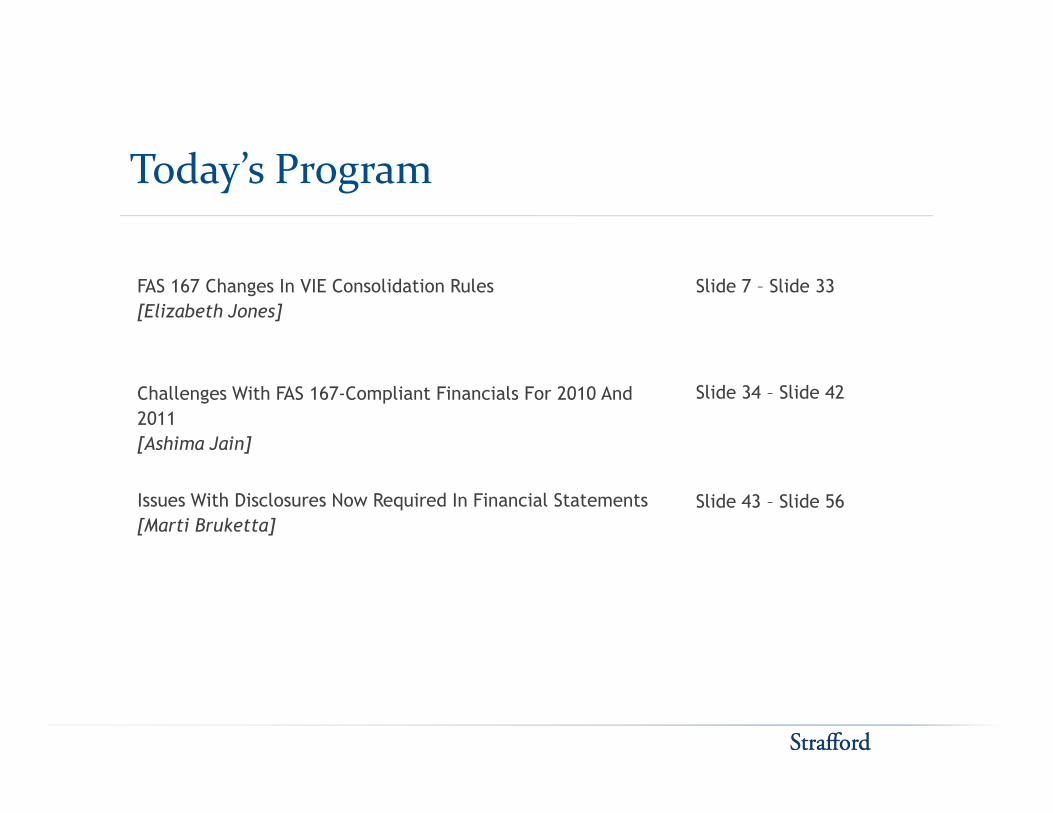

Today’s Program

FAS 167 Changes In VIE Consolidation Rules

[Elizabeth Jones]

Challenges With FAS 167-Compliant Financials For 2010 And

Slide 7 – Slide 33

Slide 34 – Slide 42

2011

[Ashima Jain]

Issues With Disclosures Now Required In Financial Statements

[Marti Bruketta]

Slide 43 – Slide 56

Elizabeth Jones, KPMG

FAS 167 CHANGES IN VIE CONSOLIDATION RULES

Elizabeth Jones, KPMG

Agenda For This Section

• Overview of FIN 46(R)

• Overview of FAS 167, including major changes from FIN 46R

• Recently proposed changes to FAS 167

• IASB IFRS 10

8

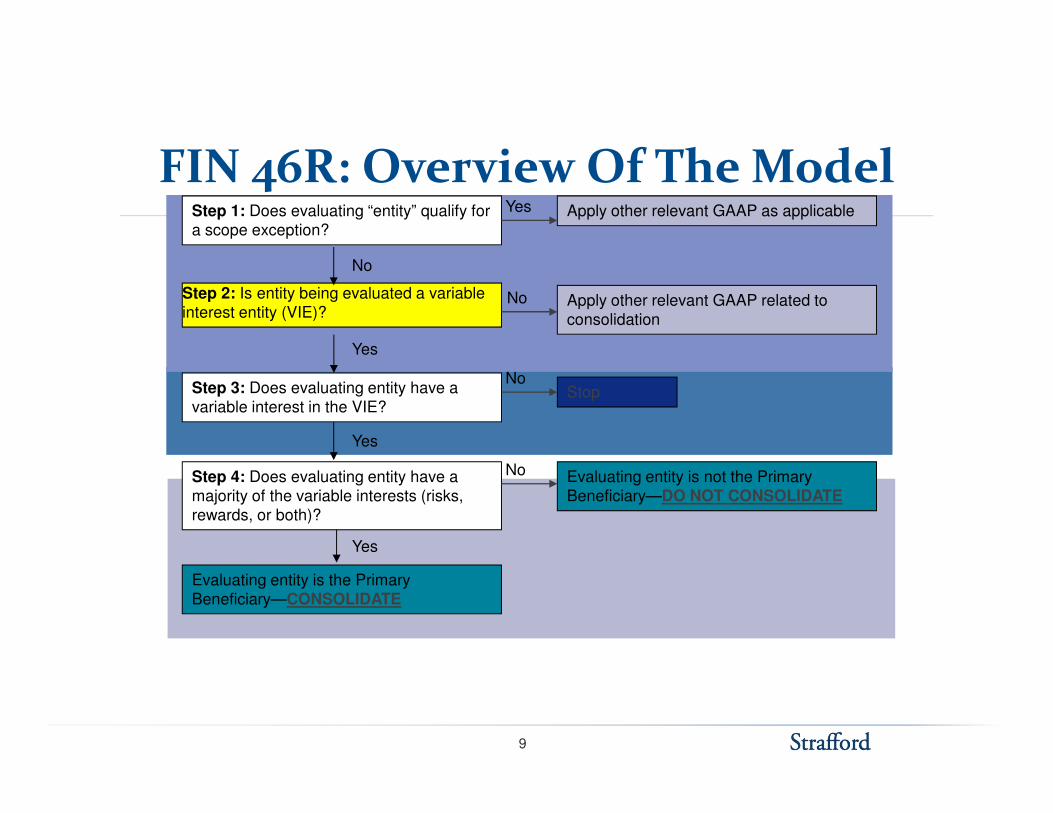

FIN 46R: Overview Of The Model

Step 3: Does evaluating entity have a variable interest in the VIE?

Step 2: Is entity being evaluated a variable interest entity (VIE)?

Apply other relevant GAAP as applicable

No

Step 1: Does evaluating “entity” qualify for a scope exception?

Apply other relevant GAAP related to consolidation

Yes

No

No

Yes

Stopvariable interest in the VIE?

Yes

Step 4: Does evaluating entity have a majority of the variable interests (risks, rewards, or both)?

Evaluating entity is not the Primary Beneficiary—DO NOT CONSOLIDATE

No

Evaluating entity is the Primary Beneficiary—CONSOLIDATE

Yes

9

FIN 46R: Equity Investment At Risk

I. Paragraph 5(a) explains that an entity is a VIE if its equity investment at risk is insufficient to allow it to finance its activities without additional subordinated financial support.

1. To be considered “at risk”, equity investment must have the following characteristics:

a. Equity under U.S. GAAPa. Equity under U.S. GAAP

b. Participate significantly in the entity’s profits and losses

c. Not issued in exchanged for subordinated interest in another VIE

d. Not provided or financed by another party involved with the entity

i. Sufficiency of equity determined through qualitative and quantitative analysis

10

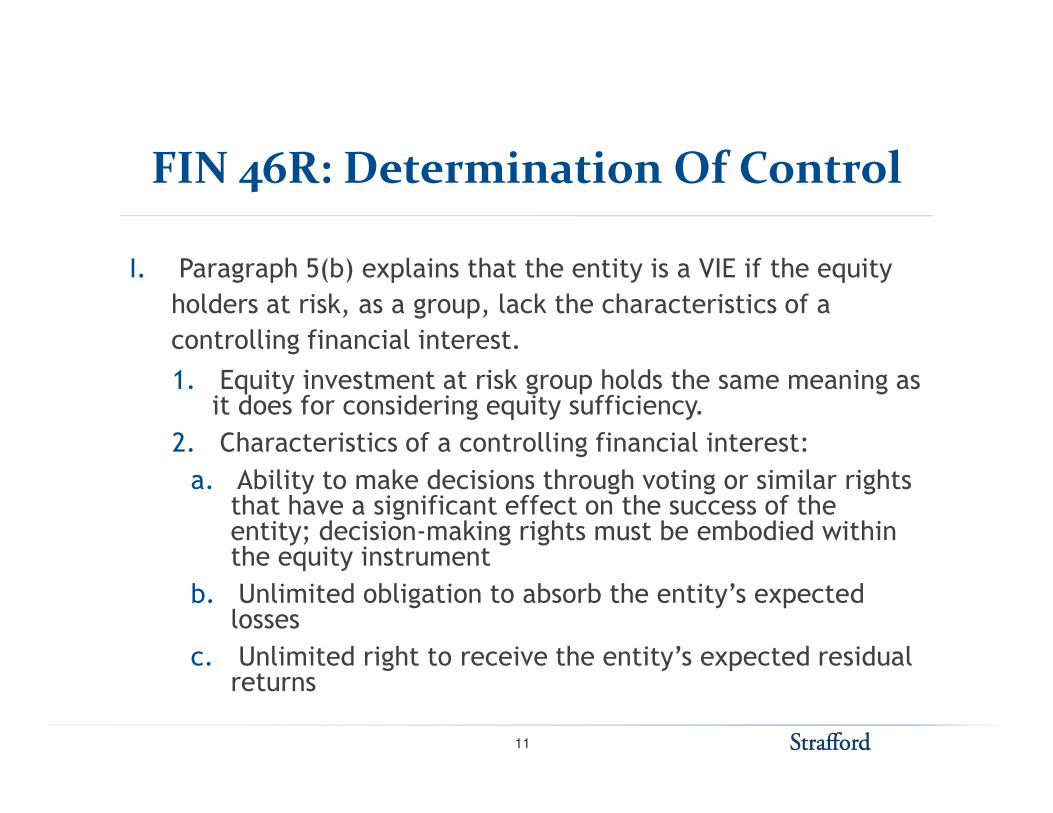

FIN 46R: Determination Of Control

I. Paragraph 5(b) explains that the entity is a VIE if the equity

holders at risk, as a group, lack the characteristics of a

controlling financial interest.

1. Equity investment at risk group holds the same meaning as it does for considering equity sufficiency.it does for considering equity sufficiency.

2. Characteristics of a controlling financial interest:

a. Ability to make decisions through voting or similar rights that have a significant effect on the success of the entity; decision-making rights must be embodied within the equity instrument

b. Unlimited obligation to absorb the entity’s expected losses

c. Unlimited right to receive the entity’s expected residual returns

11

FIN 46R: Anti-Abuse Clause

Paragraph 5(c) explains that an entity is a VIE if:

� The voting rights of some equity investors are not proportional to their obligations to absorb the entity’s expected losses and/or rights to receive expected residual returns; AND their obligations to absorb the entity’s expected losses and/or rights to receive expected residual returns; AND

� Substantially all of the entity’s activities involve, or are conducted on behalf of, an equity-at-risk investor that has disproportionately few voting rights.

12

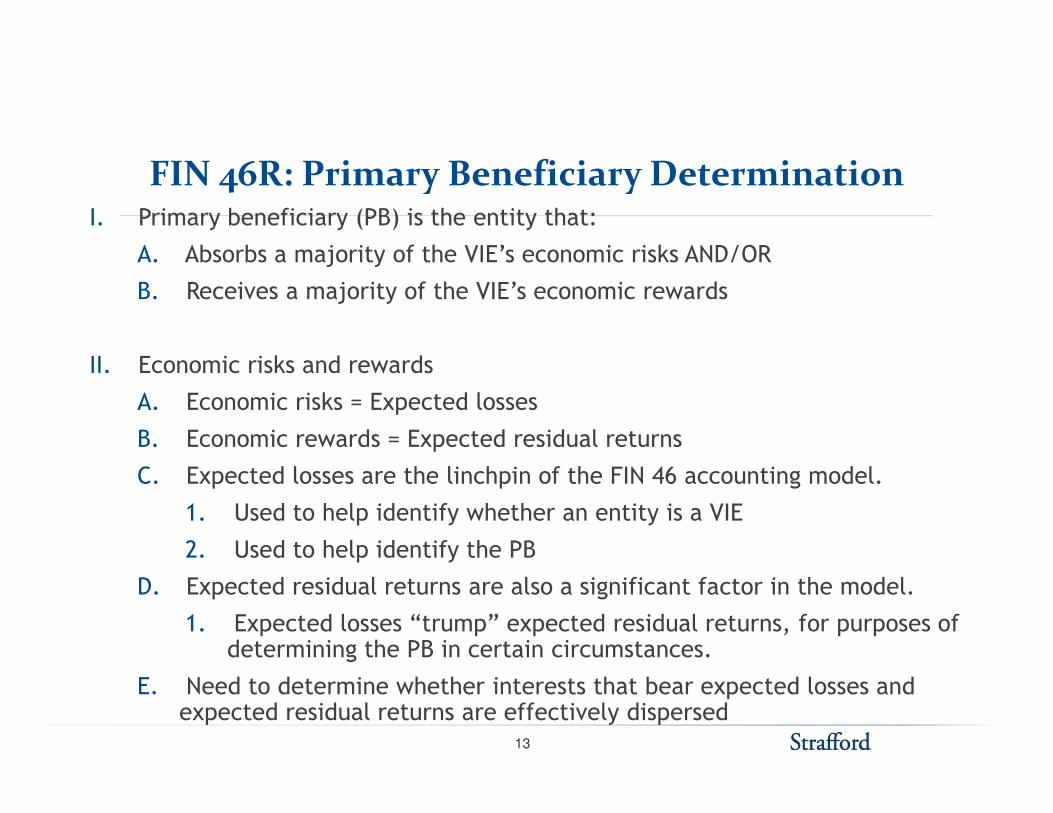

FIN 46R: Primary Beneficiary DeterminationI. Primary beneficiary (PB) is the entity that:

A. Absorbs a majority of the VIE’s economic risks AND/OR

B. Receives a majority of the VIE’s economic rewards

II. Economic risks and rewards

A. Economic risks = Expected lossesA. Economic risks = Expected losses

B. Economic rewards = Expected residual returns

C. Expected losses are the linchpin of the FIN 46 accounting model.

1. Used to help identify whether an entity is a VIE

2. Used to help identify the PB

D. Expected residual returns are also a significant factor in the model.

1. Expected losses “trump” expected residual returns, for purposes of determining the PB in certain circumstances.

E. Need to determine whether interests that bear expected losses and expected residual returns are effectively dispersed

13

FAS 167: Overview

I. Previous guidance in FIN 46R

A. Generally, the enterprise that absorbs the majority of the expected losses, residual returns, or both is the primary beneficiary (“PB”) and consolidates (quantitative assessment).

II. Objective of FAS 167

A. Address concerns raised as a result of recent market events (e.g., primary beneficiary determination and reconsideration events)

B. Improve financial reporting by entities involved with variable interest entities (“VIEs”)

III. Impact of FAS 167

A. More entities subject to FIN 46(R) (FASB ASC 810-10) consolidation assessments and reassessments

14

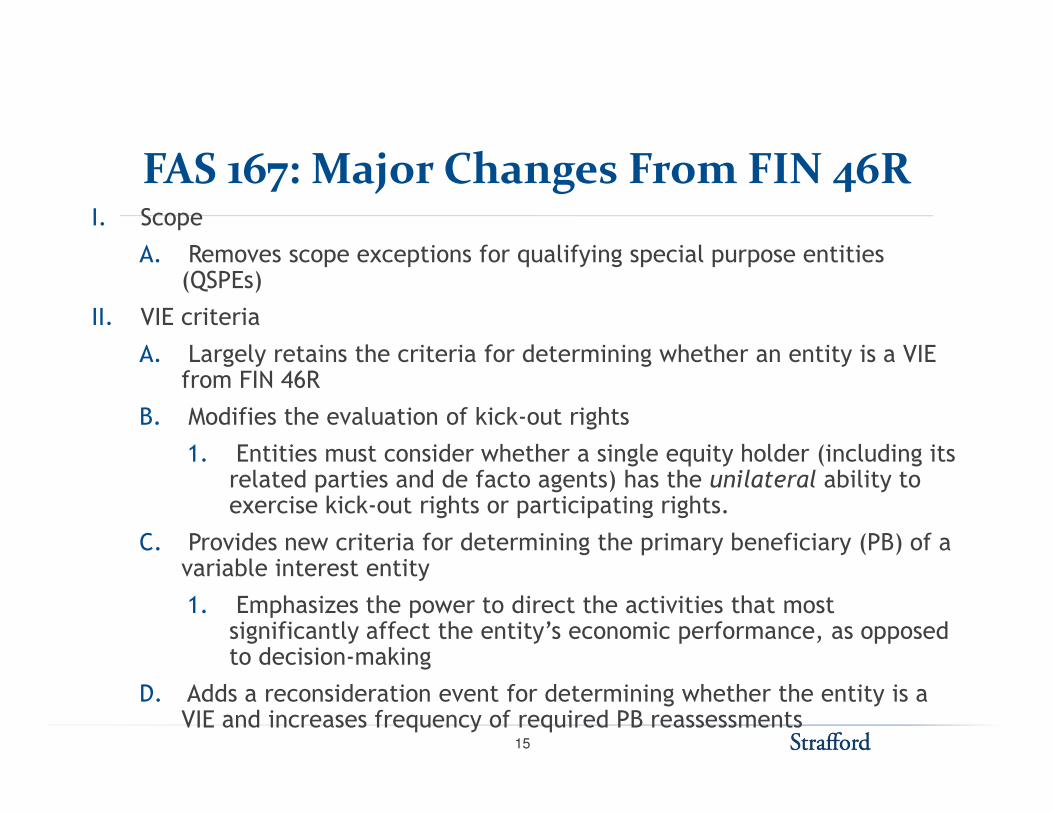

FAS 167: Major Changes From FIN 46RI. Scope

A. Removes scope exceptions for qualifying special purpose entities (QSPEs)

II. VIE criteria

A. Largely retains the criteria for determining whether an entity is a VIE from FIN 46R

B. Modifies the evaluation of kick-out rightsB. Modifies the evaluation of kick-out rights

1. Entities must consider whether a single equity holder (including its related parties and de facto agents) has the unilateral ability to exercise kick-out rights or participating rights.

C. Provides new criteria for determining the primary beneficiary (PB) of a variable interest entity

1. Emphasizes the power to direct the activities that most significantly affect the entity’s economic performance, as opposed to decision-making

D. Adds a reconsideration event for determining whether the entity is a VIE and increases frequency of required PB reassessments

15

FAS 167: Major Changes From FIN 46R (Cont.)

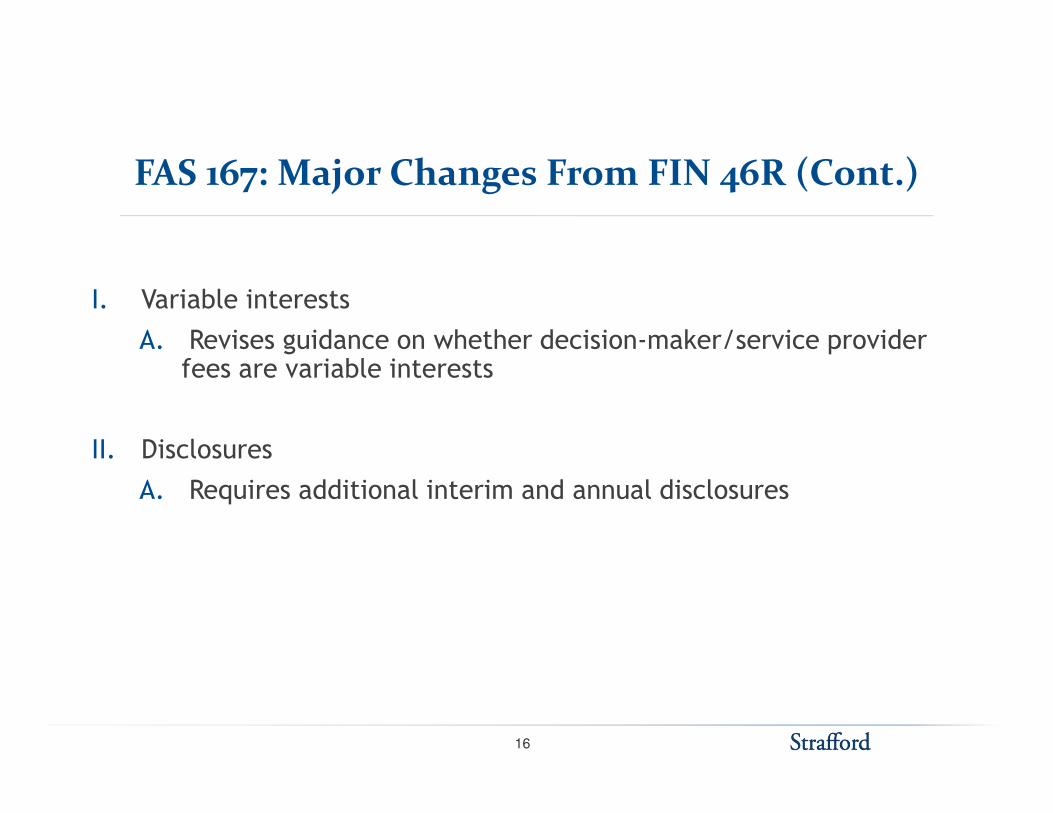

I. Variable interests

A. Revises guidance on whether decision-maker/service provider fees are variable interests

II. Disclosures

A. Requires additional interim and annual disclosures

16

FAS 167: VIE Criteria

I. Key principle

A. Kick-out rights are rarely exercised. Therefore, these rights and participating rights should not be considered in evaluating whether an entity is a VIE, unless a single party or related party group has the unilateral ability to exercise them.exercise them.

II. Impact

A. Affects analysis of FIN 46(R) ¶5(b)(1)

B. Inconsistent with guidance in EITF 04-5 (FASB ASC 810-20)

1. Inconsistent consolidation conclusions for voting interest entities and VIEs

C. Modification of kick-out rights guidance may cause more entities (e.g., LPs, LLCs) to be evaluated as VIEs.

17

FAS 167: Decision-Maker/Service Provider Fees

I. Key principles

A. A service provider that is acting solely as a fiduciary should not be required to consolidate the entity to which it is providing services.it is providing services.

B. If the fees received by a decision-maker or other service provider are variable interests, then the decision-maker or service provider is not acting solely as a fiduciary.

C. Insignificant non-fee variable interests held by a decision-maker or other service provider should not cause its fees to be considered variable interests.

18

FAS 167: Determining Primary Beneficiary1. Modifies approach to require qualitative, not quantitative, analysis

a. Entities must determine which party has a controlling financial interest in a VIE.

b. The variable interest holder with a controlling financial interest is the PB and must consolidate the VIE.

2. A variable interest holder has a controlling financial interest in a VIE if it has both of the following:

a. The power to direct the activities of a VIE that most significantly affect the entity’s economic performance

b. The right to receive benefits or obligation to absorb losses of the VIE that could potentially be significant to the VIE

3. Consider VIE purpose and design

4. Power to direct activities is not affected by kick-out rights or participating rights, unless such rights are unilaterally held by a single party (including related parties and de facto agents).

5. Protective rights held by other parties do not preclude an entity from having the power to direct activities of the VIE.

19

FAS 167: Determining Primary Beneficiary (Cont.)

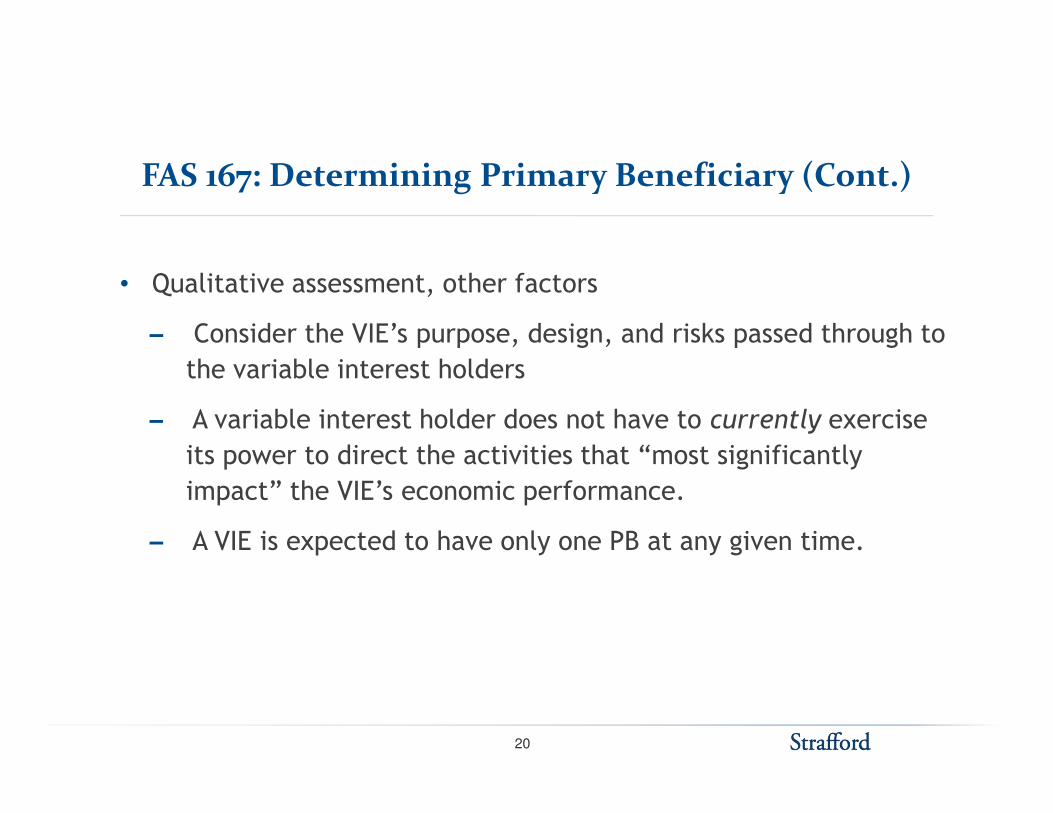

• Qualitative assessment, other factors

– Consider the VIE’s purpose, design, and risks passed through to

the variable interest holders

– A variable interest holder does not have to currently exercise – A variable interest holder does not have to currently exercise

its power to direct the activities that “most significantly

impact” the VIE’s economic performance.

– A VIE is expected to have only one PB at any given time.

20

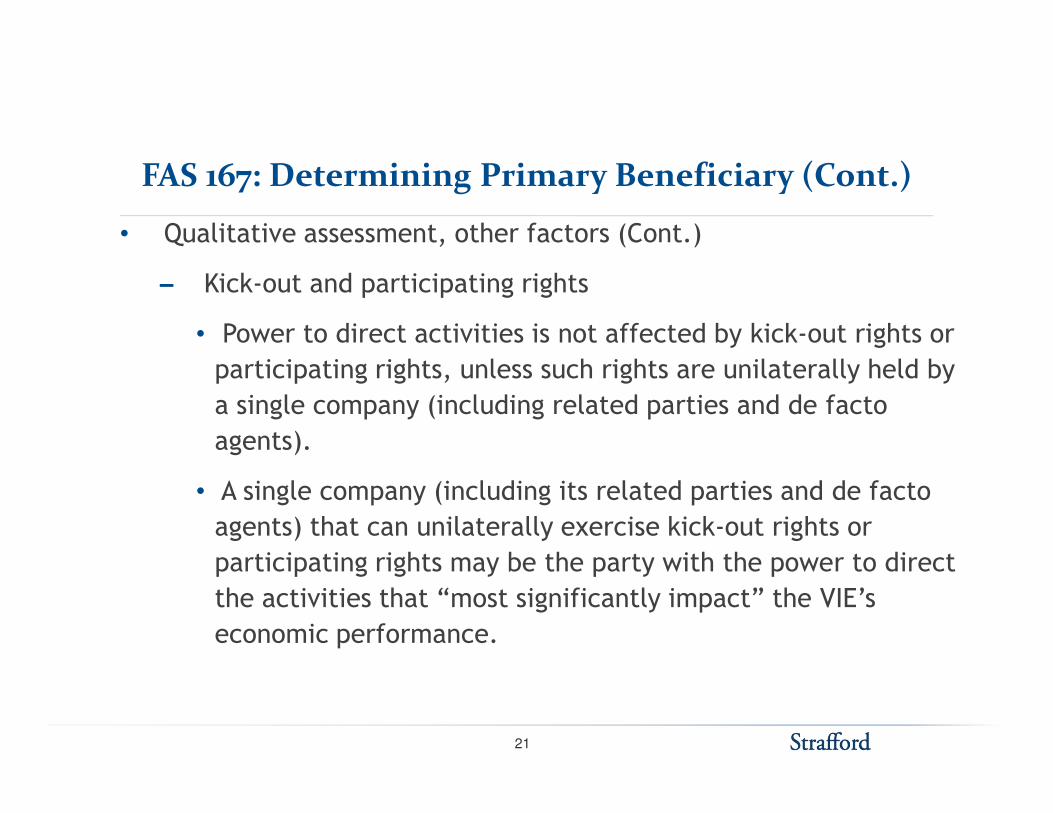

FAS 167: Determining Primary Beneficiary (Cont.)

• Qualitative assessment, other factors (Cont.)

– Kick-out and participating rights

• Power to direct activities is not affected by kick-out rights or

participating rights, unless such rights are unilaterally held by

a single company (including related parties and de facto a single company (including related parties and de facto

agents).

• A single company (including its related parties and de facto

agents) that can unilaterally exercise kick-out rights or

participating rights may be the party with the power to direct

the activities that “most significantly impact” the VIE’s

economic performance.

21

FAS 167: Determining Primary Beneficiary (Cont.)

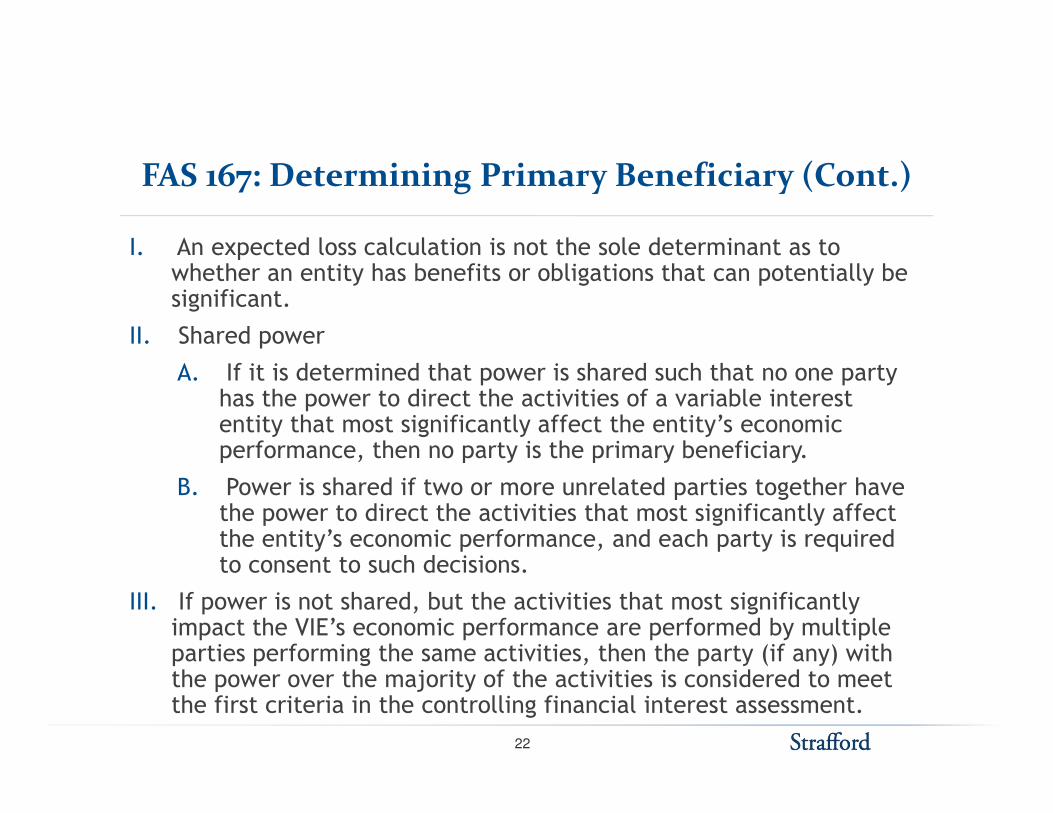

I. An expected loss calculation is not the sole determinant as to whether an entity has benefits or obligations that can potentially be significant.

II. Shared power

A. If it is determined that power is shared such that no one party has the power to direct the activities of a variable interest has the power to direct the activities of a variable interest entity that most significantly affect the entity’s economic performance, then no party is the primary beneficiary.

B. Power is shared if two or more unrelated parties together have the power to direct the activities that most significantly affect the entity’s economic performance, and each party is required to consent to such decisions.

III. If power is not shared, but the activities that most significantly impact the VIE’s economic performance are performed by multiple parties performing the same activities, then the party (if any) with the power over the majority of the activities is considered to meet the first criteria in the controlling financial interest assessment.

22

FAS 167: Reconsidering VIE StatusAnd PB Determinations

• Reconsidering VIE status

– Additional reconsideration event: Loss of power by the

holders of the equity at risk

– Troubled debt restructurings are no longer excluded from – Troubled debt restructurings are no longer excluded from

events that require VIE and PB reconsideration.

• Reconsidering PB determinations

– PB determinations must be reconsidered on a continuous

basis (no specific reconsideration events).

– Not limited to the end of the reporting period

23

Recently Proposed FAS 167 Changes: Overview

I. Joint project with IASB

II. Objectives

A. Converge IFRS and U.S. GAAP

B. Develop improved guidance on consolidation for all entities

III. Significant changes proposed to U.S. GAAP

A. New guidance on evaluating whether a decision-maker is a principal or

an agent

B. Eliminates deferral of ASU 2009-17 (Statement 167) for certain entities

C. Amends consolidation guidance for certain non-VIE partnerships and

similar entities

IV. During the project, the FASB decided not to fully converge with the IASB

A. Effective control

B. Potential voting rights

C. Single consolidation model for all entities

24

Proposed Principal And Agent Guidance: Summary

I. Decision-maker is a variable interest holder that has power to make decisions

about (i.e., to direct) the key activities of another entity.

A. For VIEs, the activities that most significantly affect economic performance

B. For non-VIE partnerships and similar entities, the financing and operating

decisions made in the ordinary course of business

1. General partner is presumed to have such power.1. General partner is presumed to have such power.

II. Under existing GAAP, entities are required to consider the guidance in ASC

paragraph 810-10-55-37 (formerly FIN 46R ¶B22) for purposes of both:

A. (1) Determining whether decision maker’s arrangement represents a variable

interest

B. (2) Evaluating whether decision maker is a principal or an agent

III. The FASB proposal:

A. Retains guidance in ASC 810-10-55-37 for purposes of variable interest

identification

B. Introduces judgmental model to evaluate whether decision-maker is a

principal or an agent25

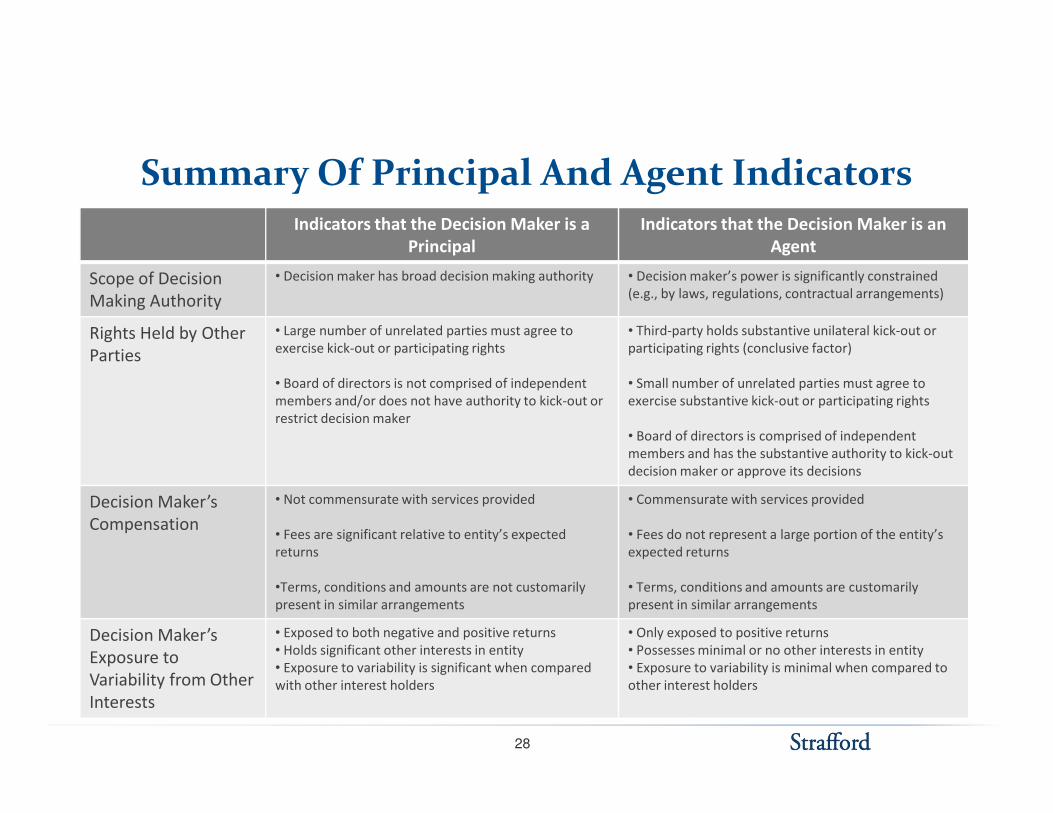

Proposed Principal And AgentGuidance: Summary (Cont.)

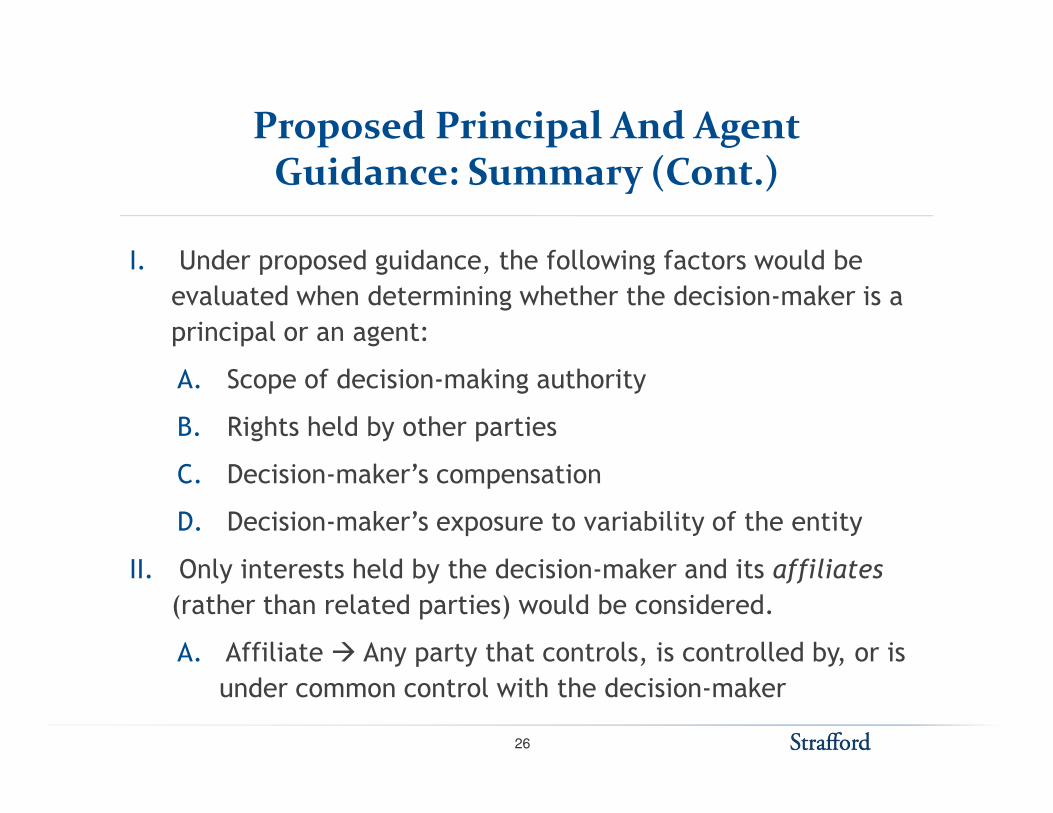

I. Under proposed guidance, the following factors would be

evaluated when determining whether the decision-maker is a

principal or an agent:

A. Scope of decision-making authority

B. Rights held by other parties

C. Decision-maker’s compensation

D. Decision-maker’s exposure to variability of the entity

II. Only interests held by the decision-maker and its affiliates

(rather than related parties) would be considered.

A. Affiliate � Any party that controls, is controlled by, or is

under common control with the decision-maker

26

Proposed Principal And AgentGuidance: Summary (Cont.)

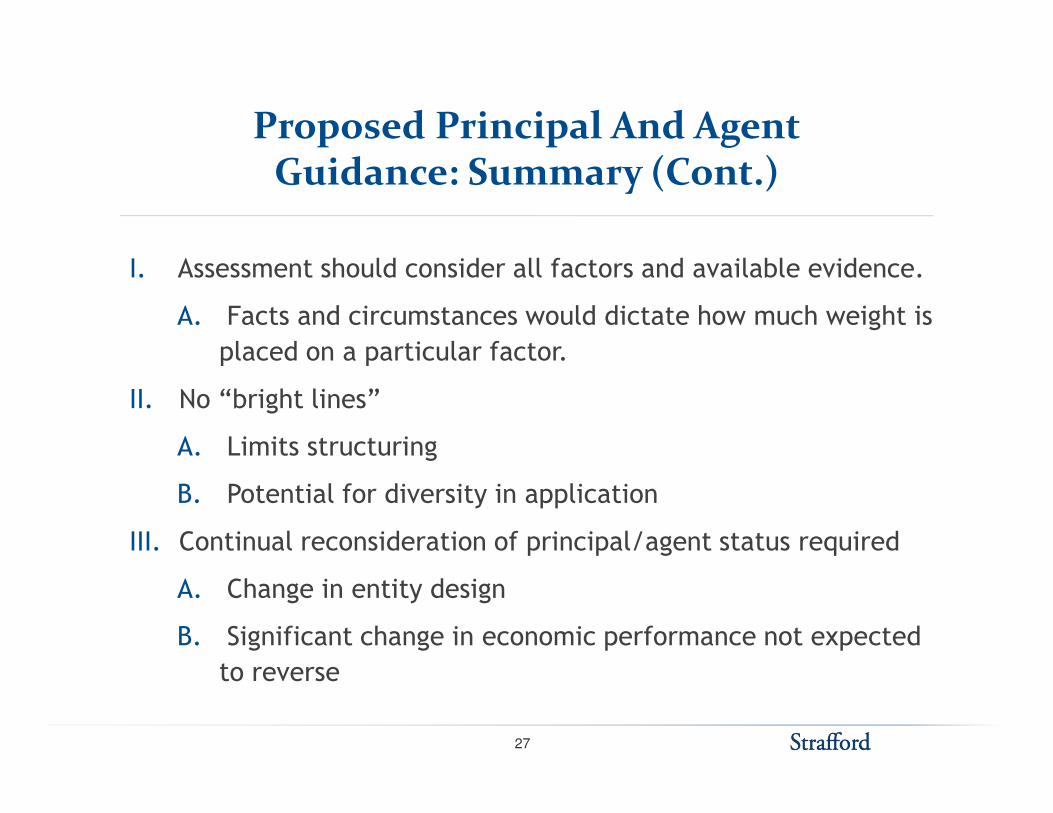

I. Assessment should consider all factors and available evidence.

A. Facts and circumstances would dictate how much weight is

placed on a particular factor.

II. No “bright lines”II. No “bright lines”

A. Limits structuring

B. Potential for diversity in application

III. Continual reconsideration of principal/agent status required

A. Change in entity design

B. Significant change in economic performance not expected

to reverse

27

Summary Of Principal And Agent IndicatorsIndicators that the Decision Maker is a

Principal

Indicators that the Decision Maker is an

Agent

Scope of Decision

Making Authority

• Decision maker has broad decision making authority • Decision maker’s power is significantly constrained

(e.g., by laws, regulations, contractual arrangements)

Rights Held by Other

Parties

• Large number of unrelated parties must agree to

exercise kick-out or participating rights

• Board of directors is not comprised of independent

members and/or does not have authority to kick-out or

• Third-party holds substantive unilateral kick-out or

participating rights (conclusive factor)

• Small number of unrelated parties must agree to

exercise substantive kick-out or participating rightsmembers and/or does not have authority to kick-out or

restrict decision maker

exercise substantive kick-out or participating rights

• Board of directors is comprised of independent

members and has the substantive authority to kick-out

decision maker or approve its decisions

Decision Maker’s

Compensation

• Not commensurate with services provided

• Fees are significant relative to entity’s expected

returns

•Terms, conditions and amounts are not customarily

present in similar arrangements

• Commensurate with services provided

• Fees do not represent a large portion of the entity’s

expected returns

• Terms, conditions and amounts are customarily

present in similar arrangements

Decision Maker’s

Exposure to

Variability from Other

Interests

• Exposed to both negative and positive returns

• Holds significant other interests in entity

• Exposure to variability is significant when compared

with other interest holders

• Only exposed to positive returns

• Possesses minimal or no other interests in entity

• Exposure to variability is minimal when compared to

other interest holders

28

Other Changes To VIE Consolidation Guidance

I. Amends guidance about VIE determination

A. Characteristic regarding whether equity holders possess power

(ASC paragraph 810-10-15-14(b)(1))

B. Conformed to the revised principal-agent guidanceB. Conformed to the revised principal-agent guidance

II. Revises one of the primary beneficiary characteristics

A. Replacement of potentially significant variable interest

condition in ASC paragraph 810-10-25-38A(b) (formerly FIN 46R

¶14A(b))

B. Must be able to use power in a principal capacity

29

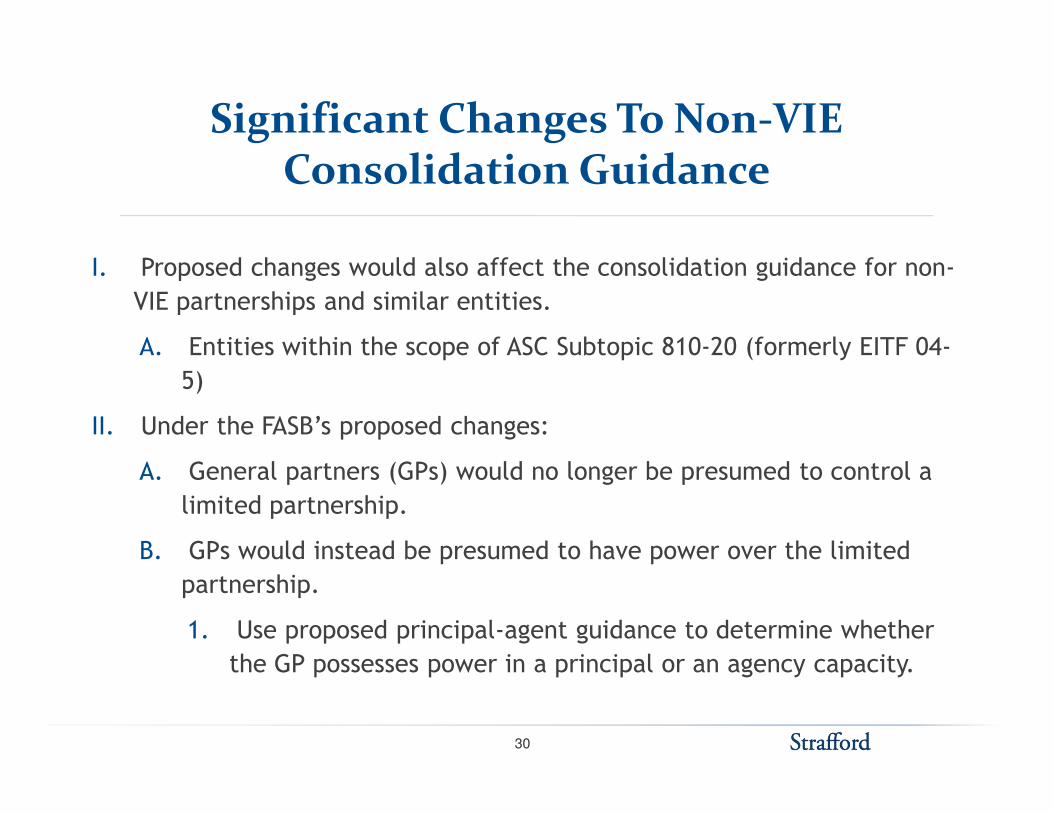

Significant Changes To Non-VIEConsolidation Guidance

I. Proposed changes would also affect the consolidation guidance for non-

VIE partnerships and similar entities.

A. Entities within the scope of ASC Subtopic 810-20 (formerly EITF 04-

5)

II. Under the FASB’s proposed changes:

A. General partners (GPs) would no longer be presumed to control a

limited partnership.

B. GPs would instead be presumed to have power over the limited

partnership.

1. Use proposed principal-agent guidance to determine whether

the GP possesses power in a principal or an agency capacity.

30

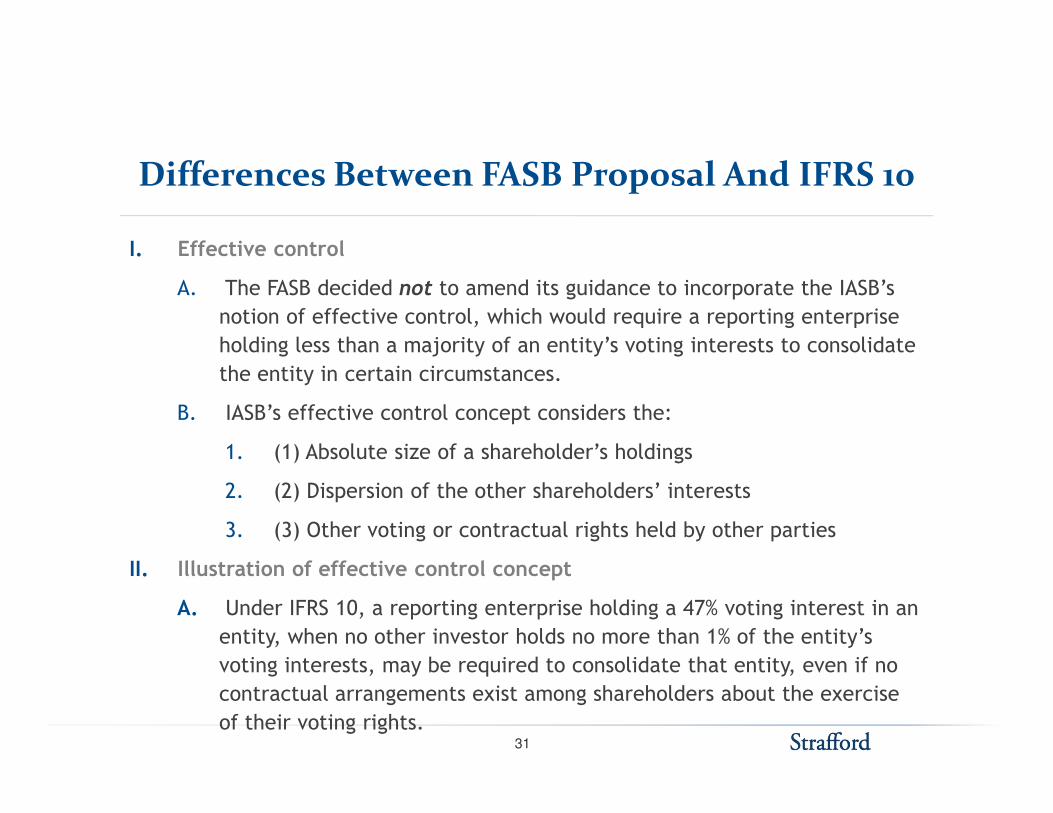

Differences Between FASB Proposal And IFRS 10

I. Effective control

A. The FASB decided not to amend its guidance to incorporate the IASB’s

notion of effective control, which would require a reporting enterprise

holding less than a majority of an entity’s voting interests to consolidate

the entity in certain circumstances.

B. IASB’s effective control concept considers the:B. IASB’s effective control concept considers the:

1. (1) Absolute size of a shareholder’s holdings

2. (2) Dispersion of the other shareholders’ interests

3. (3) Other voting or contractual rights held by other parties

II. Illustration of effective control concept

A. Under IFRS 10, a reporting enterprise holding a 47% voting interest in an

entity, when no other investor holds no more than 1% of the entity’s

voting interests, may be required to consolidate that entity, even if no

contractual arrangements exist among shareholders about the exercise

of their voting rights.31

Differences Between FASBProposal And IFRS 10 (Cont.)

I. Potential voting rights

A. IFRS 10 requires a reporting enterprise to consider potential voting

rights to determine whether it has power.

1. May arise from convertible instruments, options or forward

contracts

2. Must be substantive in nature (e.g., no significant barriers)2. Must be substantive in nature (e.g., no significant barriers)

B. The FASB’s proposed guidance does not incorporate this concept.

1. Does not provide the current ability to direct the relevant

activities that affect returns

II. Single-model approach

A. The FASB decided at this time not to pursue a single, control-based

consolidation model similar to the one set forth in IFRS 10.

1. Focus on higher-priority projects

2. Statement 167 (ASU 2009-17) is relatively new.

32

Status And Next Steps

I. Exposure draft of proposed FASB ASU expected in Q4 2011

A. Final standard expected in 2012

B. No discussion of effective date yet

C. Transition expected to be the same as for ASU 2009-17 C. Transition expected to be the same as for ASU 2009-17

(Statement 167)

II. IASB issued final guidance (IFRS 10) in May 2011

A. Effective for annual periods beginning on or after Jan. 1,

2013

33

Ashima Jain, PricewaterhouseCoopers

CHALLENGES WITH FAS 167-COMPLIANT FINANCIALS FOR 2010 AND 2011

Ashima Jain, PricewaterhouseCoopers

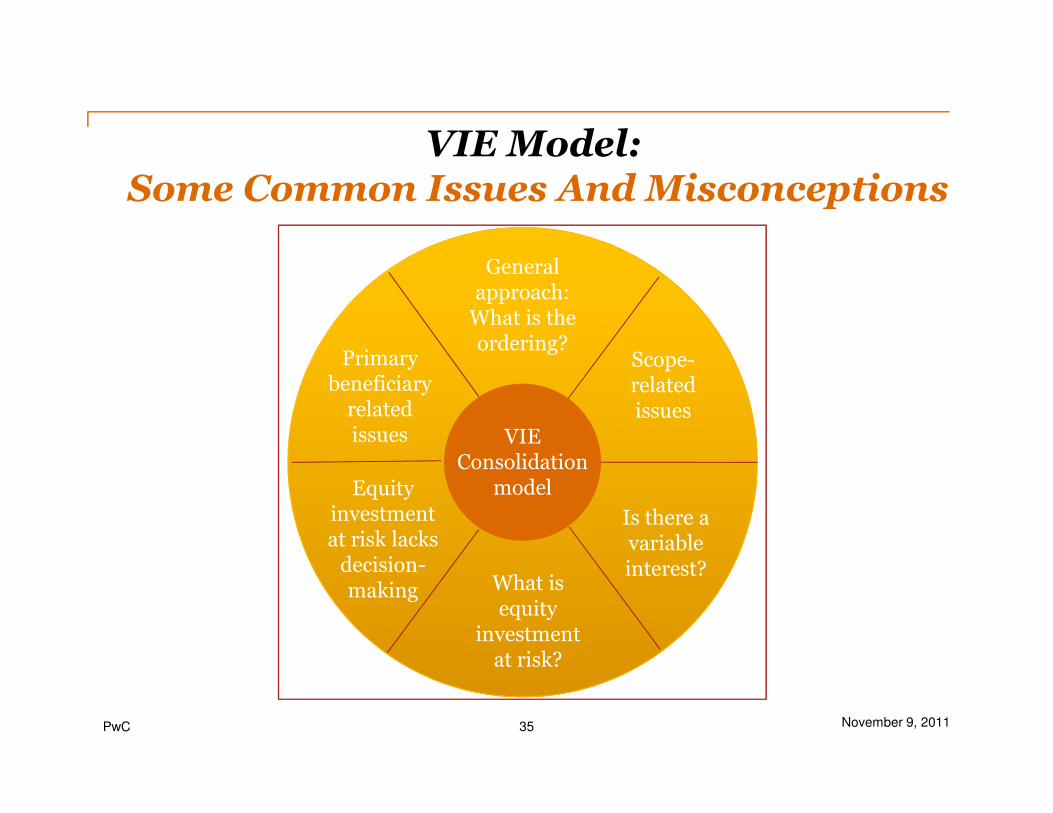

VIE Model:Some Common Issues And Misconceptions

General approach: What is the ordering?

Scope-related issues

Primary beneficiary related

PwC 35 November 9, 2011

issues

Is there a variable interest?

What is equity

investment at risk?

Equity investment at risk lacks decision-making

related issues VIE

Consolidation model

General Consolidation Approach: VIE Model First

Determine if the investee should be consolidated under the variable interest entity (VIE) model

• Discussed earlier in this session; an entity may be consolidated even if the investor controls less than 50% of the voting shares of the investee

Determine if the investee should be consolidated under the “voting interest” model

• >50% ownership? • Minority shareholder veto rights? • Partnerships/certain LLCs consolidation model? • By contract model?

For example …

PwC 36 November 9, 2011

Determine if equity method of accounting should be applied

• 20-50% ownership (>3-5% for LPs/some LLCs)?• Common stock, in-substance common stock? • Ability to exercise significant influence (board seats,

commercial arrangements, dependency of investee on investor, inter-company transactions, key source of financing, etc.)?

Determine if cost method of accounting should be applied

• <20% ownership (<3-5% for LPs/some LLCs)?• How much less than 20% ownership?• Ability to exercise significant influence?

Common Scope-Related Issues

• The entity is not a special-purpose entity.

• The entity is a business.

• The entity is a joint venture.

Misconception:

The VIE model does not apply because …

PwC 37 November 9, 2011

Is There A Variable Interest?Does the relationship create or absorb risk?

Variable Interest Not a Variable Interest

PwC 38 November 9, 2011

Risk absorbers Risk creators

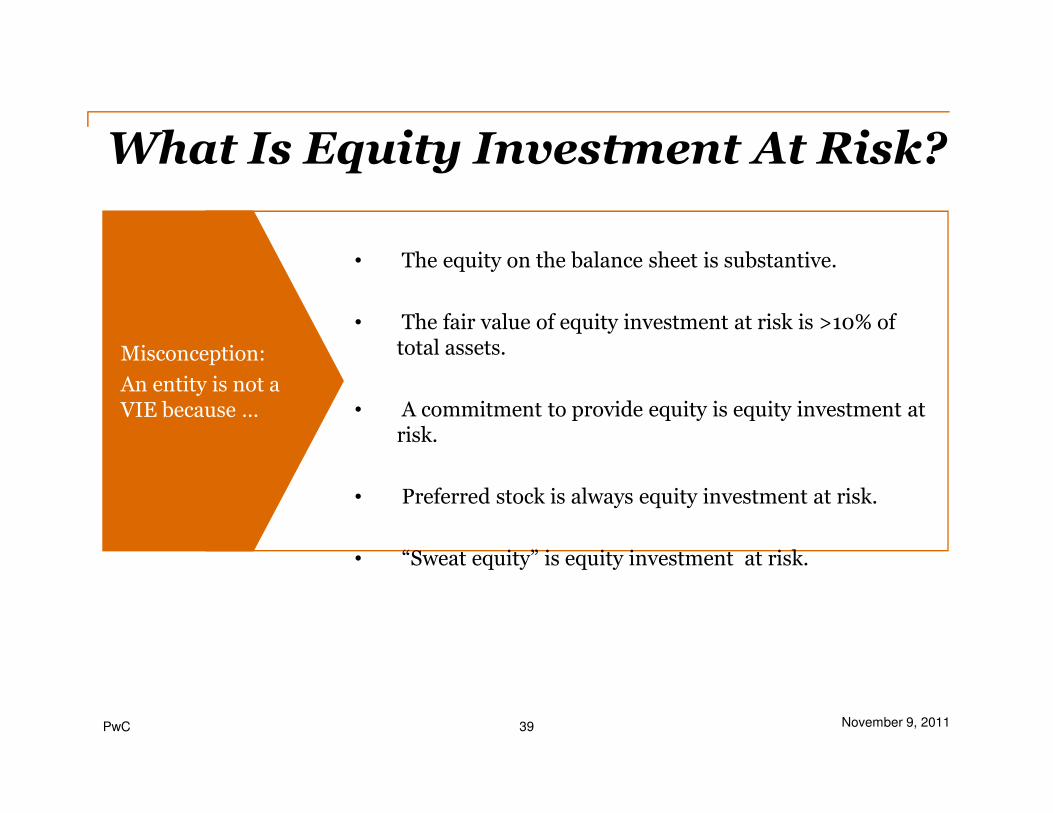

What Is Equity Investment At Risk?

• The equity on the balance sheet is substantive.

• The fair value of equity investment at risk is >10% of total assets.

• A commitment to provide equity is equity investment at

Misconception:

An entity is not a VIE because …

PwC 39 November 9, 2011

• A commitment to provide equity is equity investment at risk.

• Preferred stock is always equity investment at risk.

• “Sweat equity” is equity investment at risk.

VIE because …

Equity Investment At Risk Lacks Decision-Making:Kick-Out Rights In A Partnership

Substantive kick-out rights held by one limited partner investor

Substantive kick-out rights held by multiple limited partner investors

No substantive kick-out rights

General partner

Not a VIE under decision-making

Not a VIE under decision-making

Not a VIE under decision-making

PwC 40 November 9, 2011

partner equity consideredat risk

decision-making characteristic

decision-making characteristic

decision-making characteristic

General partner equity notconsidered at risk

Not a VIE under decision-making characteristic

VIE under decision-making characteristic

VIE under decision-making characteristic

Some Common Primary Beneficiary Related Issues

• If the entity is a VIE, will there always be a PB?

• At which level does power have to be analyzed -board/managing committee, or some other level?

• If a party within a related party group is the PB on a Some common

PwC 41 November 9, 2011

• If a party within a related party group is the PB on a stand-alone basis, but another party within that groups receives a majority of the economics, should the related party tiebreaker rule be applied?

• If there is a change in PB during a reporting period, from what date should the change apply?

Some common questions

Thank you

This publication has been prepared for general guidance on matters of interest only, and does not constitute professional advice. You should not act upon the information contained in this publication without obtaining specific professional advice. No representation or warranty (express or implied) is given as to the accuracy or completeness of the information contained in this publication, and, to the extent permitted by law, Pricewaterhouse Coopers, LLP., its members, employees and agents do not accept or assume any liability, responsibility or duty of care for any consequences of you or anyone else acting, or refraining to act, in reliance on the information contained in this publication or for any decision based on it.

© 2011 Pricewaterhouse Coopers, LLP. All rights reserved. In this document, “PwC” refers to PricewaterhouseCoopers, LLP which is a member firm of PricewaterhouseCoopers International Limited, each member firm of which is a separate legal entity.

ISSUES WITH DISCLOSURES Marti Bruketta, PricewaterhouseCoopers

ISSUES WITH DISCLOSURES NOW REQUIRED IN FINANCIAL STATEMENTS

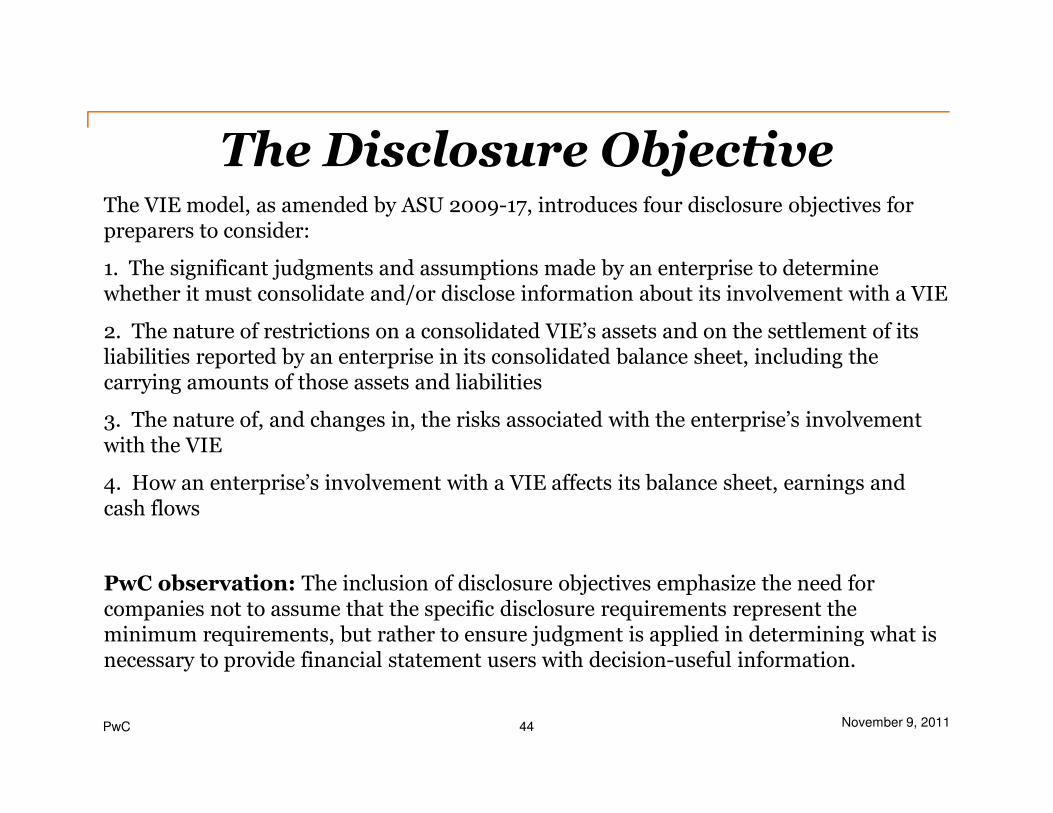

The Disclosure ObjectiveThe VIE model, as amended by ASU 2009-17, introduces four disclosure objectives for preparers to consider:

1. The significant judgments and assumptions made by an enterprise to determine whether it must consolidate and/or disclose information about its involvement with a VIE

2. The nature of restrictions on a consolidated VIE’s assets and on the settlement of its liabilities reported by an enterprise in its consolidated balance sheet, including the carrying amounts of those assets and liabilities

PwC 44 November 9, 2011

3. The nature of, and changes in, the risks associated with the enterprise’s involvement with the VIE

4. How an enterprise’s involvement with a VIE affects its balance sheet, earnings and cash flows

PwC observation: The inclusion of disclosure objectives emphasize the need for companies not to assume that the specific disclosure requirements represent the minimum requirements, but rather to ensure judgment is applied in determining what is necessary to provide financial statement users with decision-useful information.

The Aggregation Principle

• Aggregation of the new disclosures for similar entities is allowed, if separate reporting would not provide more useful information to financial statement users.

• At a minimum, the disclosures should be made in such a way that financial statement users are able to distinguish between VIEs that are not consolidated because the enterprise is not the primary beneficiary of the entity (but holds only a significant variable interest), and those VIEs that are consolidated.

PwC 45 November 9, 2011

Also, disclose method used to aggregate the disclosures

• ASC 810-10-50 provides guidance regarding what qualitative and quantitative information should be considered in determining whether to aggregate disclosures.

PwC observation: Different users prefer different levels of information. Although certain users may naturally prefer the most disaggregated level of information available, others may find that same level of information unwieldy and excessive. In deciding whether to disclose disaggregated or aggregated information, companies should use judgment to determine the information that will be most useful to financial statement users and accomplish the objectives of the disclosure principles.

Specific Required Disclosures About VIEs:Primary Beneficiary (Consolidator)

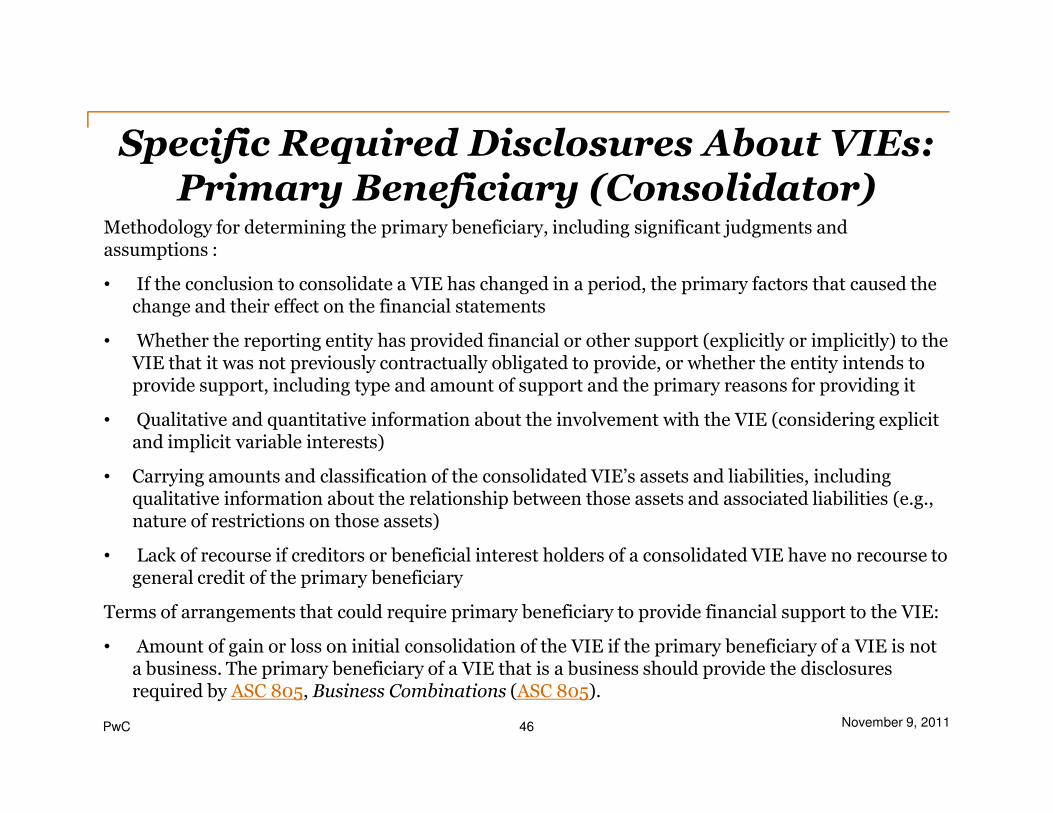

Methodology for determining the primary beneficiary, including significant judgments and assumptions :

• If the conclusion to consolidate a VIE has changed in a period, the primary factors that caused the change and their effect on the financial statements

• Whether the reporting entity has provided financial or other support (explicitly or implicitly) to the VIE that it was not previously contractually obligated to provide, or whether the entity intends to provide support, including type and amount of support and the primary reasons for providing it

PwC 46 November 9, 2011

• Qualitative and quantitative information about the involvement with the VIE (considering explicit and implicit variable interests)

• Carrying amounts and classification of the consolidated VIE’s assets and liabilities, including qualitative information about the relationship between those assets and associated liabilities (e.g., nature of restrictions on those assets)

• Lack of recourse if creditors or beneficial interest holders of a consolidated VIE have no recourse to general credit of the primary beneficiary

Terms of arrangements that could require primary beneficiary to provide financial support to the VIE:

• Amount of gain or loss on initial consolidation of the VIE if the primary beneficiary of a VIE is not a business. The primary beneficiary of a VIE that is a business should provide the disclosures required by ASC 805, Business Combinations (ASC 805).

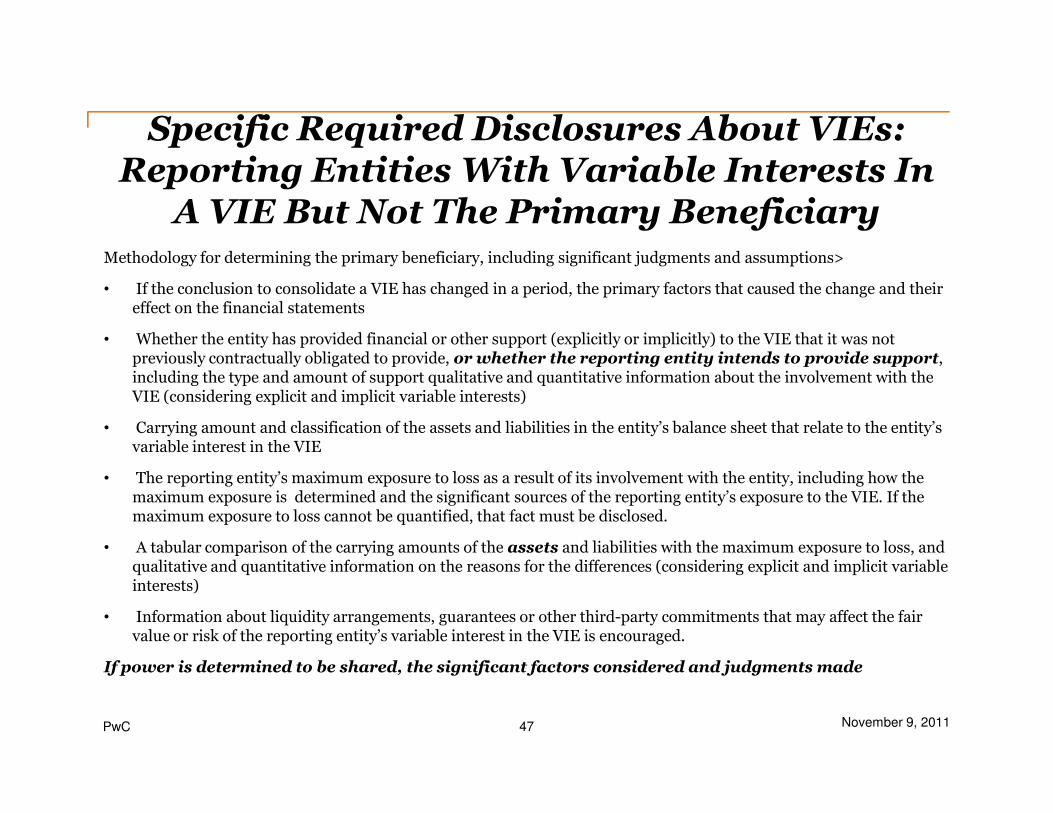

Specific Required Disclosures About VIEs: Reporting Entities With Variable Interests In A VIE But Not The Primary Beneficiary

Methodology for determining the primary beneficiary, including significant judgments and assumptions>

• If the conclusion to consolidate a VIE has changed in a period, the primary factors that caused the change and their effect on the financial statements

• Whether the entity has provided financial or other support (explicitly or implicitly) to the VIE that it was not previously contractually obligated to provide, or whether the reporting entity intends to provide support, including the type and amount of support qualitative and quantitative information about the involvement with the VIE (considering explicit and implicit variable interests)

PwC 47 November 9, 2011

• Carrying amount and classification of the assets and liabilities in the entity’s balance sheet that relate to the entity’s variable interest in the VIE

• The reporting entity’s maximum exposure to loss as a result of its involvement with the entity, including how the maximum exposure is determined and the significant sources of the reporting entity’s exposure to the VIE. If the maximum exposure to loss cannot be quantified, that fact must be disclosed.

• A tabular comparison of the carrying amounts of the assets and liabilities with the maximum exposure to loss, and qualitative and quantitative information on the reasons for the differences (considering explicit and implicit variable interests)

• Information about liquidity arrangements, guarantees or other third-party commitments that may affect the fair value or risk of the reporting entity’s variable interest in the VIE is encouraged.

If power is determined to be shared, the significant factors considered and judgments made

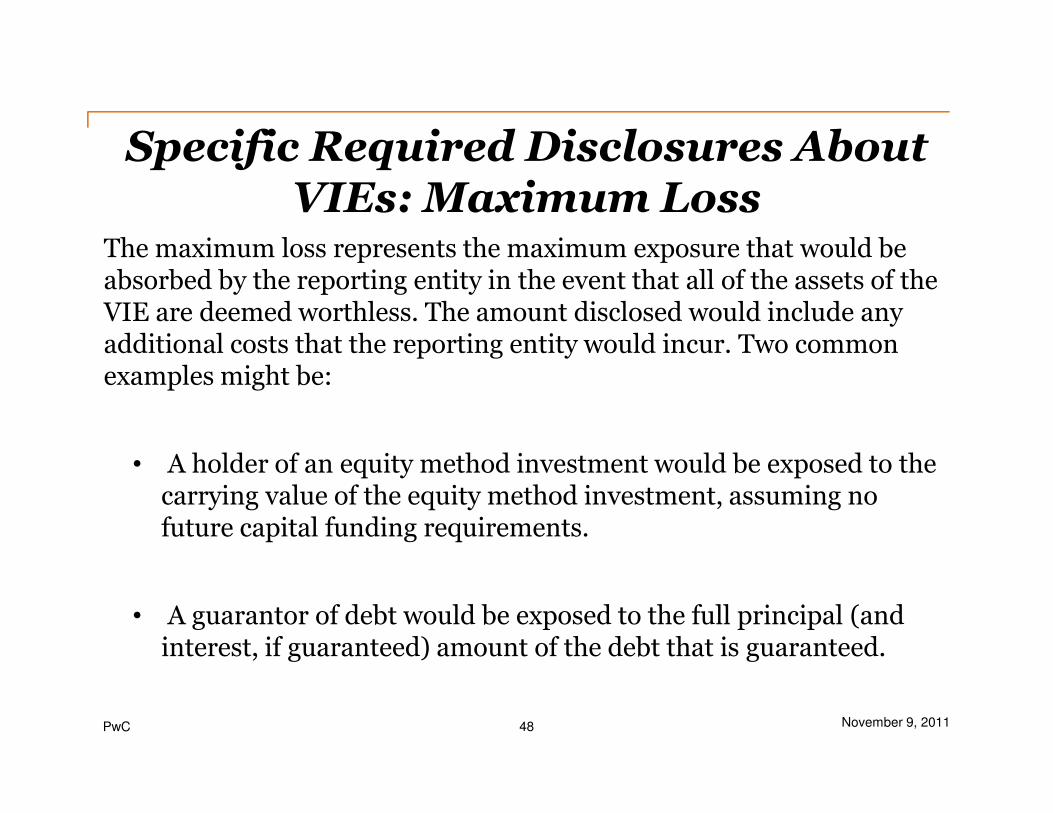

Specific Required Disclosures AboutVIEs: Maximum Loss

The maximum loss represents the maximum exposure that would be absorbed by the reporting entity in the event that all of the assets of the VIE are deemed worthless. The amount disclosed would include any additional costs that the reporting entity would incur. Two common examples might be:

PwC 48 November 9, 2011

• A holder of an equity method investment would be exposed to the carrying value of the equity method investment, assuming no future capital funding requirements.

• A guarantor of debt would be exposed to the full principal (and interest, if guaranteed) amount of the debt that is guaranteed.

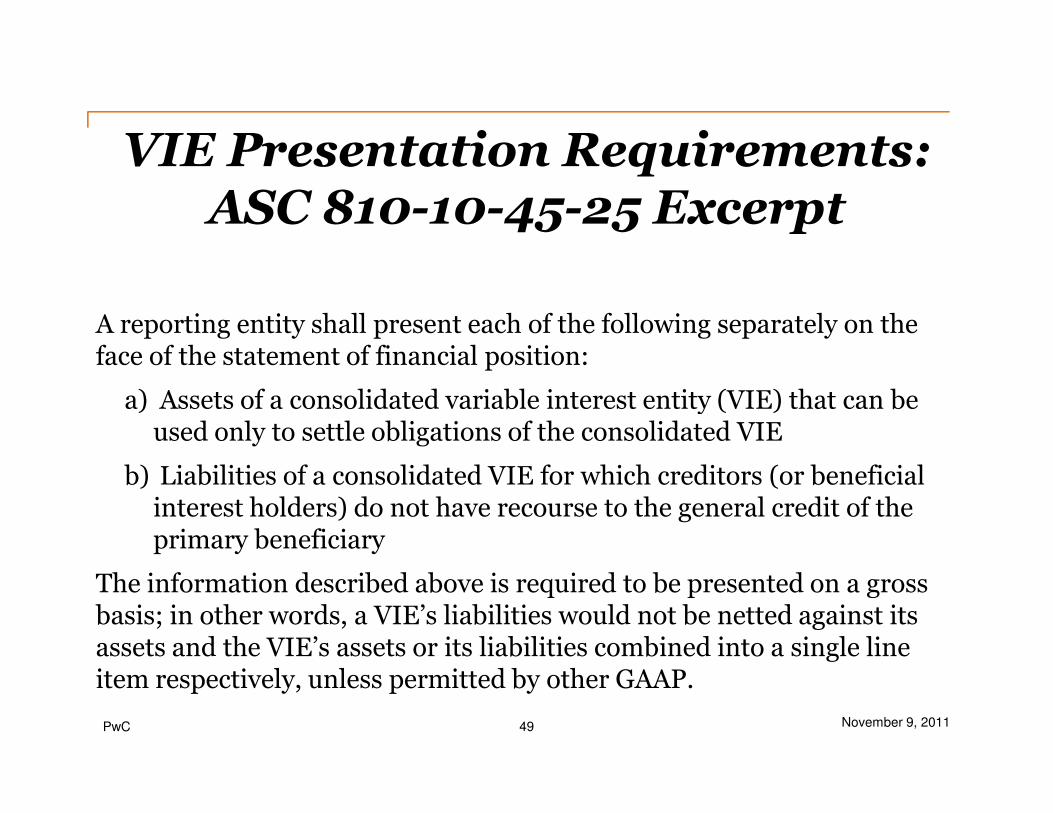

VIE Presentation Requirements:ASC 810-10-45-25 Excerpt

A reporting entity shall present each of the following separately on the face of the statement of financial position:

a) Assets of a consolidated variable interest entity (VIE) that can be

PwC 49 November 9, 2011

a) Assets of a consolidated variable interest entity (VIE) that can be used only to settle obligations of the consolidated VIE

b) Liabilities of a consolidated VIE for which creditors (or beneficial interest holders) do not have recourse to the general credit of the primary beneficiary

The information described above is required to be presented on a gross basis; in other words, a VIE’s liabilities would not be netted against its assets and the VIE’s assets or its liabilities combined into a single line item respectively, unless permitted by other GAAP.

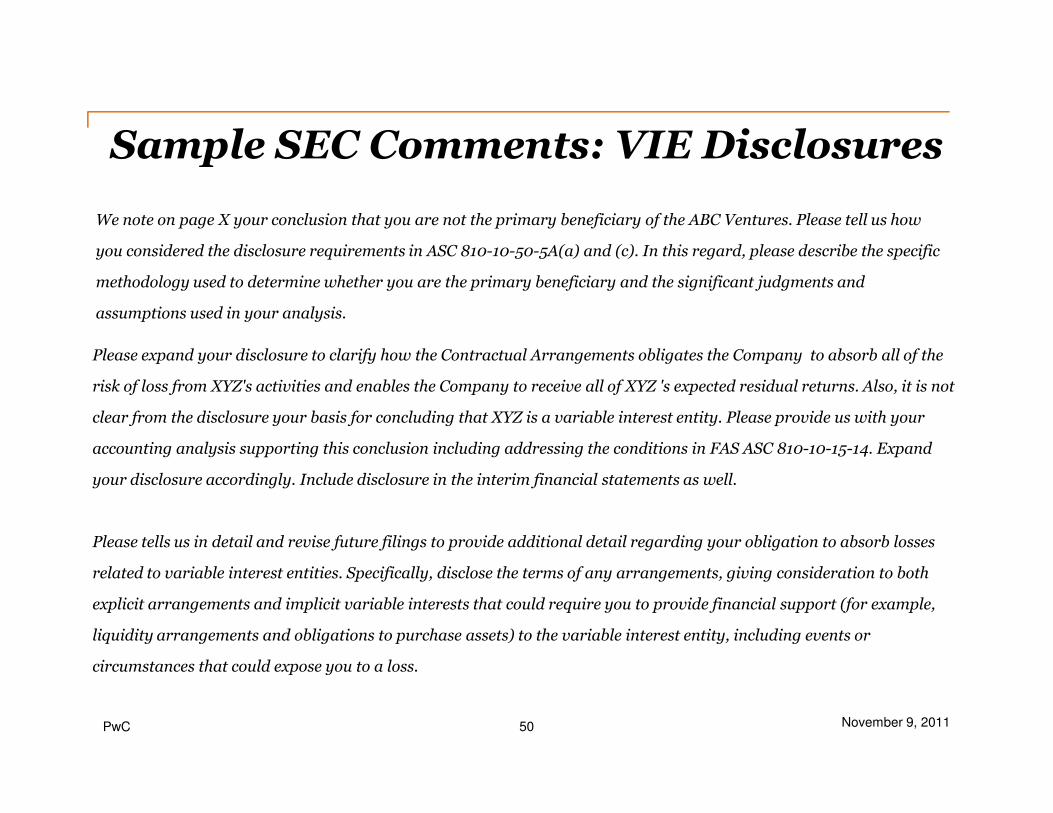

Sample SEC Comments: VIE Disclosures

We note on page X your conclusion that you are not the primary beneficiary of the ABC Ventures. Please tell us how

you considered the disclosure requirements in ASC 810-10-50-5A(a) and (c). In this regard, please describe the specific

methodology used to determine whether you are the primary beneficiary and the significant judgments and

assumptions used in your analysis.

Please expand your disclosure to clarify how the Contractual Arrangements obligates the Company to absorb all of the

risk of loss from XYZ's activities and enables the Company to receive all of XYZ 's expected residual returns. Also, it is not

PwC 50 November 9, 2011

clear from the disclosure your basis for concluding that XYZ is a variable interest entity. Please provide us with your

accounting analysis supporting this conclusion including addressing the conditions in FAS ASC 810-10-15-14. Expand

your disclosure accordingly. Include disclosure in the interim financial statements as well.

Please tells us in detail and revise future filings to provide additional detail regarding your obligation to absorb losses

related to variable interest entities. Specifically, disclose the terms of any arrangements, giving consideration to both

explicit arrangements and implicit variable interests that could require you to provide financial support (for example,

liquidity arrangements and obligations to purchase assets) to the variable interest entity, including events or

circumstances that could expose you to a loss.

Sample SEC Comments: VIE Disclosures (Cont.)

We note your disclosure on page X with respect to the various entities you evaluated as potential variable interest

entities (VIEs). We further note your disclosure that for the two VIEs which were consolidated that "...equity investors

in the entity do not have the characteristics of a controlling financial interest or do not have sufficient equity at risk

for the entity to finance its activities without additional subordinated financial support." For the two entities that

PwC 51 November 9, 2011

for the entity to finance its activities without additional subordinated financial support." For the two entities that

were not determined to be VIEs and therefore not consolidated, please tell us the basis for your conclusion and revise

your disclosures accordingly.

Please explain to us the equity relationship you have with your foreign subsidiary in China and what relationships it

has in turn with other Chinese variable interest entities or equity related subsidiaries.

Sample SEC Comments: VIE Disclosures (Cont.)

You note that you own a 50% equity investment in the ABC joint venture, and you further disclose

that you are required to recognize 100% of any losses for those companies which represent ABC.

Please provide a detailed analysis on your consideration of the ABC joint venture under FASB ASC

810, specifically whether the ABC joint venture would be considered a variable interest entity and if

so, the determination of the primary beneficiary. Please provide this analysis both prior to and after

PwC 52 November 9, 2011

so, the determination of the primary beneficiary. Please provide this analysis both prior to and after

the amendment to the standard under Accounting Standards Update No. 2009-17.

Sample SEC Comments: VIE Disclosures (Cont.)

We refer to your 50-50 joint venture. We note that you have determined that based upon the level of

equity at risk, the venture is a variable interest entity and that you are not the primary beneficiary.

Please revise to disclose the significant factors considered and judgments made in determining that

the power to direct the activities of a VIE that most significantly impact the VIE's economic

performance is shared in accordance with the guidance in paragraph 810-10-25-38D. Please refer to

ASC 810-10-50-4(e). In your response, please provide us with your proposed disclosures.

PwC 53 November 9, 2011

We refer to your investment in the 50-50 joint venture and related guarantee of operating

performance for the venture. You state that the maximum exposure to loss under this guarantee was

below $X million at December 31, 2010 and that you believe "the likelihood is remote

that the performance guarantee will not be achieved and, therefore, will not have a material

adverse impact on the Company's financial position, operating results or cash flows." Please

revise to disclose how the maximum exposure to loss was determined and the period of

time over which this guarantee will be in effect. In your response, please provide us with

your proposed disclosures.

Sample SEC Comments: VIE Disclosures (Cont.)

You indicate that other than through certain contractual rights, you have a limited ability control

ABC. Please provide us with a detailed outline of these contractual rights and how they impact your

ability to control ABC. In addition, since it appears that such contractual rights may provide you

with the ability to control ABC, please tell us what consideration was given to the possibility that ABC

may represent a variable interest which should be consolidated in accordance with ASC Topic 810.

We note your disclosure that you determined XYZ Company was a variable interest entity (VIE)

PwC 54 November 9, 2011

We note your disclosure that you determined XYZ Company was a variable interest entity (VIE)

based on the $X million outstanding line of credit you provided them as of June 30, 2010. In addition,

we note your disclosure on page XX of the Form 10-K that you also provide ABC Holding Company,

another affiliate, with a $X million committed line of credit with an outstanding balance of $XX

million at December 31, 2009. Please explain to us how you determined that XYZ Company was a

VIE and ABC was not though additional financial support was provided by you to both entities. We

note your reference to ASC 810-10-50-12 and 50-13, respectively. Please refer to any additional

guidance you used in your determination and provide sufficient details supporting your current

accounting.

PwC 55 November 9, 2011

This publication has been prepared for general guidance on matters of interest only, and does not constitute professional advice. You should not act upon the information contained in this publication without obtaining specific professional advice. No representation or warranty (express or implied) is given as to the accuracy or completeness of the information contained in this publication, and, to the extent permitted by law, Pricewaterhouse Coopers, LLP., its members, employees and agents do not accept or assume any liability, responsibility or duty of care for any consequences of you or anyone else acting, or refraining to act, in reliance on the information contained in this publication or for any decision based on it.

© 2011 Pricewaterhouse Coopers, LLP. All rights reserved. In this document, “PwC” refers to PricewaterhouseCoopers, LLP which is a member firm of PricewaterhouseCoopers International Limited, each member firm of which is a separate legal entity.