fast logistics in the b2c ecommerce: a global overview fortin… · fast logistics in the b2c...

TRANSCRIPT

FAST LOGISTICS IN THE B2C eCOMMERCE: A GLOBAL OVERVIEW

1

POLITECNICO DI MILANO

SCHOOL OF INDUSTRIAL AND INFORMATION ENGINEERING

MASTER OF SCIENCE IN MANAGEMENT ENGINEERING

FAST LOGISTICS IN THE B2C eCOMMERCE: A GLOBAL OVERVIEW

CANDIDATE: SUPERVISOR: Veronica Fortini (842408) Prof. Riccardo Mangiaracina

CO-SUPERVISORS: Dott. Samuele Fraternali Dott.ssa Denise Ronconi

Academic Year 2016/2017

FAST LOGISTICS IN THE B2C eCOMMERCE: A GLOBAL OVERVIEW

2

FAST LOGISTICS IN THE B2C eCOMMERCE: A GLOBAL OVERVIEW

3

Index

ABSTRACT 9

EXECUTIVE SUMMARY 10

1. Introduction 18

2. Literature Review 21

2.1 Methodology 21

2.1.1 Scope of the analysis 21

2.1.2 Selection process 21

2.1.3 Review method 22

2.2 Summary of review and discussion 23

2.2.1 Main characteristics of the papers examined 24

2.2.2 Research methods used 27

2.3 Discussion of themes arising from the review 29

2.3.1 Research area 30

2.3.2 First matrix classification: speed of delivery – type of activity 32

2.3.3 Second matrix classification: speed of the logistics process -field

of application 50

2.4 Conclusions from literature review and directions for future

research 58

3. Research objective and methodology 65

3.1 Objective 66

3.2 Methodology 67

4. Empirical analysis 77

4.1 First empirical analysis: single-variable classifications 77

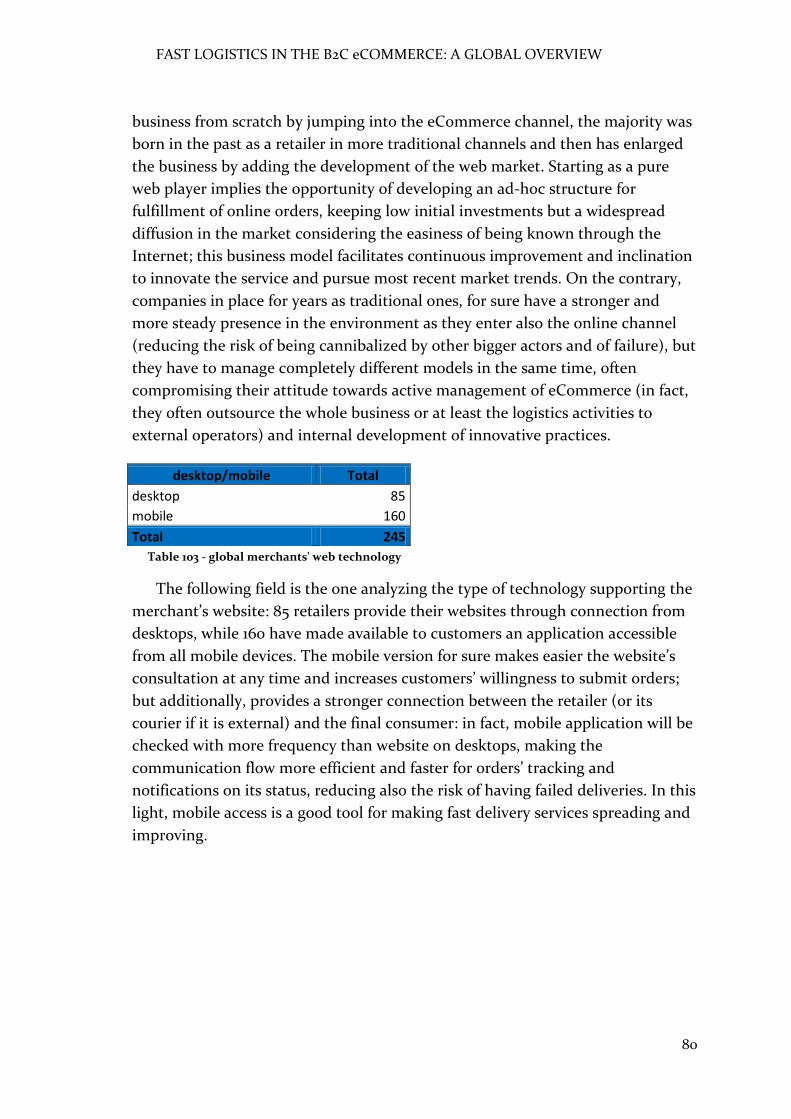

4.1.1 Global context 77

4.1.1.1 Merchants’ sample size 77

4.1.1.2 Breakdown by channel, web technology and commodity

sector 78

4.1.1.3 Split by delivery speed 80

4.1.1.4 Service providers 83

4.1.2 United States 84

4.1.2.1 Breakdown by channel, web technology and commodity

sector 85

4.1.2.2 Split by delivery speed 86

4.1.2.3 In-depth analysis of logistics providers, related cost,

coverage and type 88

FAST LOGISTICS IN THE B2C eCOMMERCE: A GLOBAL OVERVIEW

4

4.1.2.4 Logistics technologies and alternatives to last-mile

delivery 91

4.1.2.5 Additional services: real-time tracking, date/time choice

and pre-delivery contacts 92

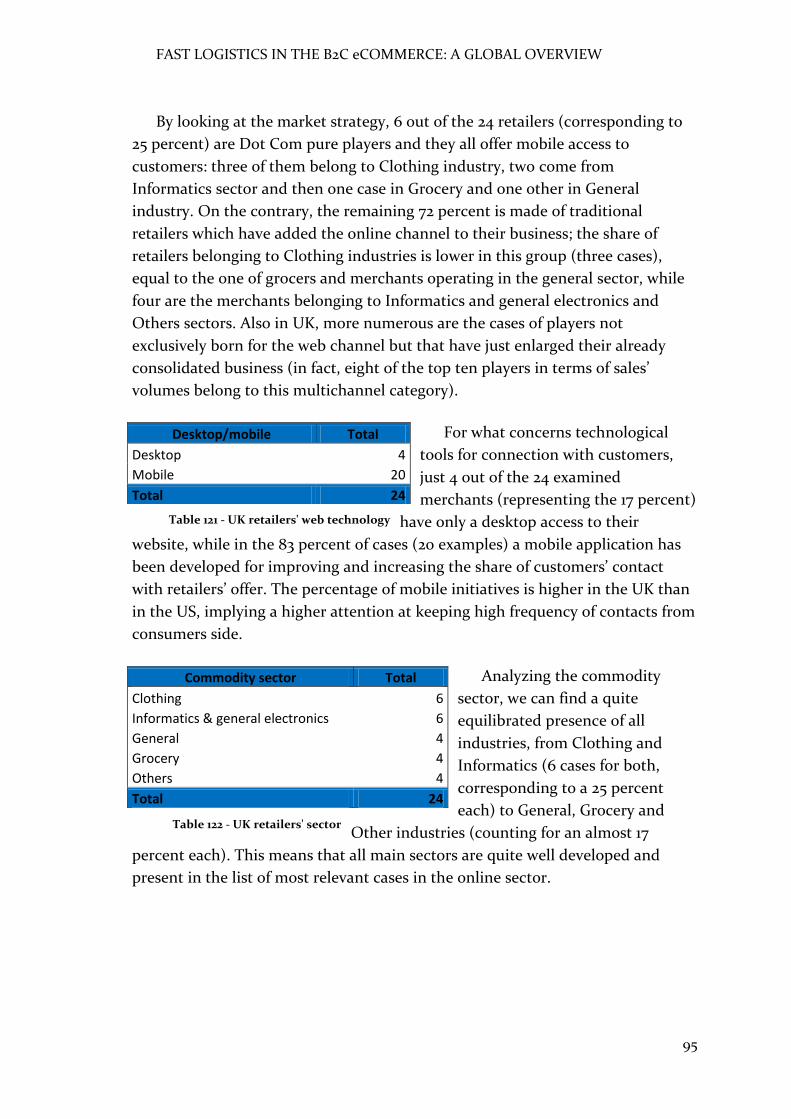

4.1.3 United Kingdom 93

4.1.3.1 Breakdown by channel, web technology and commodity

sector 94

4.1.3.2 Split by delivery speed 95

4.1.3.3 In-depth analysis of logistics providers, related cost,

coverage and type 96

4.1.3.4 Logistics technologies and alternatives to last-mile

delivery 97

4.1.3.5 Additional services: real-time tracking, date/time choice

and pre-delivery contacts 99

4.1.4 Other European countries (France, Germany, Italy , Spain) 100

4.1.4.1 Breakdown by channel, web technology and commodity

sector 101

4.1.4.2 Split by delivery speed 104

4.1.4.3 In-depth analysis of logistics providers, related cost,

coverage and type 107

4.1.4.4 Logistics technologies and alternatives to last-mile

delivery 112

4.1.4.5 Additional services: real-time tracking, date/time choice

and pre-delivery contacts 114

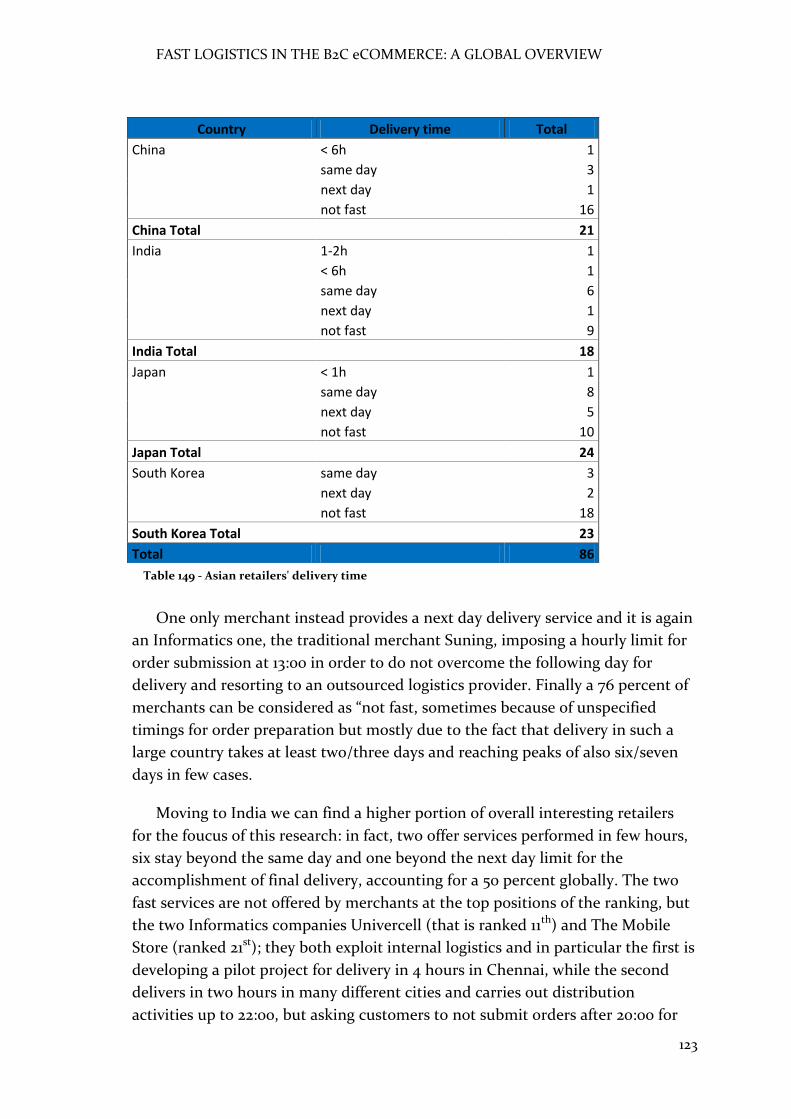

4.1.5 Asian countries (China, India, Japan and South Korea) 116

4.1.5.1 Breakdown by channel, web technology and commodity

sector 117

4.1.5.2 Split by delivery speed 120

4.1.5.3 In-depth analysis of logistics providers, related cost,

coverage and type 123

4.1.5.4 Logistics technologies and alternatives to last-mile

delivery 129

4.1.5.5 Additional services: real-time tracking, date/time choice

and pre-delivery contacts 131

4.1.6 Conclusions and insights from first empirical classifications 133

4.2 Second empirical analysis: double-variable classifications 139

4.2.1 Commodity sector – merchant’s business nature 140

4.2.1.1 Next Day 140

4.2.1.2 Same Day 143

4.2.1.3 Less than six hours 146

4.2.2 Commodity sector – geographical coverage 148

FAST LOGISTICS IN THE B2C eCOMMERCE: A GLOBAL OVERVIEW

5

4.2.2.1 Next Day 148

4.2.2.2 Same Day 148

4.2.2.3 Less than six hours 152

4.2.3 Commodity sector – type of logistics service 152

4.2.3.1 Next Day 152

4.2.3.2 Same Day 155

4.2.3.3 Less than six hours 158

4.2.4 Commodity sector – used transportation means 159

4.2.4.1 Next Day 159

4.2.4.2 Same Day 160

4.2.4.3 Less than six hours 161

4.2.5 Conclusions and insight from second empirical analysis 162

5. Final conclusions 165

BIBLIOGRAPHY 168

SITOGRAPHY 172

FAST LOGISTICS IN THE B2C eCOMMERCE: A GLOBAL OVERVIEW

6

TABLES INDEX Table 1 – main characteristics of the examined papers 31

Table 1 - Area of research of papers examined 37

Table 2 – first classification: addressed activities vs. speed of delivery 41

Table 3 - second classification: speed of logistics vs. application field 58

Table 4 - global merchants' quantity 81

Table 5 - global merchants' excluded non-interesting cases 82

Table 6 - global merchants' market channel 83

Table 7 - global merchants' web technology 83

Table 8 - global merchants' sector 84

Table 9 - global merchants' delivery time 85

Table 10 - global merchants' service providers

88

Table 11 - US merchants' market channel 89

Table 12 - US merchants' web technology 89

Table 13 - US merchants' sector 90

Table 14 - US merchants' delivery time

90

Table 15 - US merchants' service providers 92

Table 16 - US merchants' delivery cost

93

Table 17 - US merchants' geographic coverage 94

Table 18 - US merchants' logistics type 95

Table 19 - US merchants' transportation means 96

Table 20 - US merchants' last-mile alternatives

96

Table 21 - US merchants' tracking systems 97

Table 22 - US merchants' time choice 97

Table 23 - US merchants' contacts 97

Table 24 - UK retailers' market channel 98

Table 25 - UK retailers' web technology 98

Table 26 - UK retailers' sector

99

Table 27 - UK retailers' delivery time 99

Table 28 - UK retailers' service provider 100

Table 29 - UK retailers' delivery cost 100

Table 30 - UK retailers' geographic coverage

101

Table 31 - UK retailers' logistics type 101

Table 32 - UK retailers' transportation means 101

FAST LOGISTICS IN THE B2C eCOMMERCE: A GLOBAL OVERVIEW

7

Table 33 - UK retailers' last-mile alternatives 102

Table 34 - UK retailers' tracking systems 103

Table 35 - UK retailers' day/time choice 103

Table 36 - UK retailers' contacts 104

Table 37 - European merchants' market channel 105

Table 38 - European merchants' web technology 106

Table 39 - European merchants' sector 108

Table 40 - European merchants' delivery time 109

Table 41 - European merchants' service providers 112

Table 42 - European merchants' delivery cost 114

Table 43 - European merchants' geographic coverage 115

Table 44 - European merchants' logistics type 116

Table 45 - European merchants' transportation means 117

Table 46 - European merchants' last-mile alternatives 118

Table 47 - European merchants' tracking system 119

Table 48 - European merchants' day/time choice 119

Table 49 - European merchants' contacts 120

Table 50 - Asian retailers' market channel

122

Table 51 - Asian retailers' web technology 123

Table 52 - Asian retailers' sector 124

Table 53 - Asian retailers' delivery time 125

Table 54 - Asian retailers' service providers 128

Table 55 - Asian retailers' delivery cost 129

Table 56 - Asian retailers' geographical coverage

131

Table 57 - Asian retailers' logistics type 132

Table 58 - Asian retailers' transportation means 134

Table 59 - Asian retailers' last-mile alternatives 135

Table 60 - Asian retailers' tracking system

136

Table 61 - Asian retailers' day/time choice 137

Table 62 - Asian retailers' contacts 138

Table 63 - sector vs. channel next day global 145

Table 64 - sector vs. channel next day US 145

Table 65 - sector vs. channel next day UK 146

Table 66 - sector vs. channel next day Europe 147

Table 67 - sector vs. channel next day Asia 147

Table 68 - sector vs. channel same day global 148

Table 69 - sector vs. channel same day US 148

FAST LOGISTICS IN THE B2C eCOMMERCE: A GLOBAL OVERVIEW

8

Table 70 - sector vs. channel same day UK

149

Table 71 - sector vs. channel same day Europe 149

Table 72 - sector vs. channel same day Asia

150

Table 73 - sector vs. channel <6h global 150

Table 74 - sector vs. channel <6h US 151

Table 75 - sector vs. channel <6h Europe 151

Table 76 - sector vs. channel <6h Asia 152

Table 77 - sector vs. coverage next day global 152

Table 78 - sector vs. coverage same day global 153

Table 79 - sector vs. coverage same day US 153

Table 80 - sector vs. coverage same day UK

154

Table 81 - sector vs. channel same day Europe 155

Table 82 - sector vs. coverage same day Asia 156

Table 83 - sector vs. coverage <6h global 156

Table 84 - sector vs. logistics next day global 157

Table 85 - sector vs. logistics next day US 157

Table 86 - sector vs. logistics next day Europe 158

Table 87 - sector vs. logistics next day Asia 159

Table 88 - sector vs. logistics same day global 160

Table 89 - sector vs. logistics same day US 160

Table 90 - sector vs. logistics same day Europe

161

Table 91 - sector vs. logistics same day Asia 162

Table 92 - sector vs. logistics <6h global 163

Table 93 - sector vs. vehicles next day global 164

Table 94 - sector vs. vehicles same day global 165

Table 95 - sector vs. vehicles <6h global 166

FIGURES INDEX Figure 1 - two-dimensional classification along with research method 41 Figure 2 - two-dimensional classification along with research method 59

Figure 3 - extract from database: merchants' number, name, service provider,

country, market channels and web technology 70

Figure 4 - extract from database: retailers' sector, delivery time and other time

features 72

Figure 5 - extract from database: delivery cost and its characteristics 73

FAST LOGISTICS IN THE B2C eCOMMERCE: A GLOBAL OVERVIEW

9

Figure 6 - extract from database: geographic coverage and delivery area's details74

Figure 7 - extract from database: logistics service type, operator, name and

vehicles used 75

Figure 8 - extract from database: last-mile alternatives and real-time tracking 76

Figure 9 - extract from database: day/time choice and duration, contacts before

delivery and useful websites 77

FAST LOGISTICS IN THE B2C eCOMMERCE: A GLOBAL OVERVIEW

10

ABSTRACT This research aims at providing an in-depth analysis of the current initiatives

of fast delivery in the eCommerce business. Given the strong growth of the

Internet in the last decades and the corresponding development of the channel of

online sales, one of the most challenging topics that merchants have to face

regards the way in which they have to organize and manage their logistics

fulfillment processes, that are much more complex in the eCommerce with

respect to the traditional channels.

The methodology adopted for providing this overview comprehends a first

analysis of the existing literature about this topic: articles have been collected

from the most utilized scientific libraries and they have been analyzed first

according to their area of research, then through a matrix in which the speed of

the delivery process they described was crossed with the type of activities tackles;

lastly, another matrix have been provided in order to match again the speed of

the logistics process subject of the article with the main field of application of the

contribution.

Having then outdrawn comments on findings, from the main gaps

highlighted in the literature review a second analysis have been performed

having as subject of research the sample of main merchants actually working in

the eCommerce; rankings on top players in the sector have allowed to find which

the most important players were and the an extensive research on the most

common web browsers have been performed for each of them in order to collect

a huge amount of data about the delivery services they offered, which have been

collected in a database.

Data have been previously analyzed by considering one single field of the

database at a time and then have been crossed together in some double-variable

classifications in which mainly similarities and differences according to the

commodity sector of belonging of the merchants have been investigated.

All the analyses made on real examples have provided a complete overview of

the up-to-date online market for what concerns fast and non-fast delivery

options, providing some interesting insights for practitioners’ development.

FAST LOGISTICS IN THE B2C eCOMMERCE: A GLOBAL OVERVIEW

11

EXECUTIVE SUMMARY

Premise

This research aims at providing an in-depth analysis of the up-to-date

situation in relation to initiatives of fast delivery in the eCommerce business.

Given the strong growth of the Internet in the last decades and the

corresponding high development of the channel of online sales, one of the most

challenging topics that merchants have to face regards the way in which they

have to organize and manage their logistics fulfillment processes, that are much

more complex in the eCommerce with respect to the traditional channels made

of physical stores. As next day delivery initiatives have almost become a common

trend at a worldwide level, the disruption resulting from same day delivery

services’ diffusion will be even greater, having the potential of fundamentally

changing the way online shopping is performed. Therefore, the trend of fast

deliveries is under development in these years and it represents a rich source of

cases.

Research objective

The objective of the research is the one of collecting and classifying most

interesting initiatives in order to provide not only directions for future research

to academicians, but also to allow market practitioners to get insights from

existing cases for their own services’ development, increasing more and more the

diffusion of such practices in the actual context and improving the service level.

In an attempt to provide a complete picture of the current situation for what

concerns fast logistics in business-to-consumer eCommerce, the objective of the

thesis has been formalized in the following questions:

1) Which are the most relevant real examples of merchants operating in the

eCommerce at a worldwide level?

2) How many of these merchants carry out their e-fulfillment process not

going beyond the next day from order reception? And how many among

them offer even faster options?

3) Which commonalities and/or differences exist among initiatives belonging

to different geographical areas?

4) Which commodity sectors are interested by this kind of initiatives? Are

there any commonalities and/or differences in the initiatives’ feature

among the industries?

5) What are the latest trends about the main features of logistics activities

and about the technologies employed for the provision of this kind of

services?

FAST LOGISTICS IN THE B2C eCOMMERCE: A GLOBAL OVERVIEW

12

Methodology

The first action taken for taking an updated picture has been a literature

review focused on a set of 52 selected papers published from 2001 to 2017 in 39

international journals. Among these contributions, some other literature reviews

dealing with internet shopping and home deliveries were found, but the majority

of them presented a number of limitations related either to their put in writing

time (i.e. lack of recent contributions, e.g. Lee and Whang, 2001) or to their

content (i.e. focus on last-mile shipment only and its impact on city logistics,

without addressing the whole process from order receipt; e.g. Visser et al., 2014;

Savelsbergh and Van Woensel, 2016). Just one paper proposed a recent review

(2016) and tackled all supply chain management activities in eCommerce, from

order picking to final delivery, but it was providing a set of practices

implemented by real companies without addressing fast delivery issue in a

comprehensive manner (Yu et al., 2016). So this review was carried out in order to

overcome the above-mentioned limitations and was organized into three main

sub-sections: discussion of main characteristics (i.e. year of publication, journal

title and type, regions addressed), research method and content of each paper.

This review presented a number of gaps not adequately addressed yet or not

considered at all.

First, the analyzed literature refers primarily to few industries such as grocery,

food in general and consumer electronics, while other sectors such as clothing,

books, cosmetics have not been examined at all. This represents a gap, especially

for what concerns clothing industry, because it is the one having seen the highest

growth in sales in the last years and also having experienced a significant growth

of companies approaching same day or next day deliveries, especially in big cities

and in case of last-minute orders (e.g. on Christmas or other holiday occasions);

additionally, its supply chain is of relevant complexity.

Second, most attention is paid to the management of the delivery activity

alone, from the moment in which the order leaves the distribution center to the

end customer’s reception of it; even if it is surely a very complex activity to be

performed and its last portion, the one occurring inside cities and having the

name of last-mile, is complex and the one representing the service performance

directly experienced by the customer, other activities are part of the delivery

process too and should be tackled with more attention: picking has an impact too

on the overall order cycle time and for sure a comprehensive approach which

considers both picking and delivery could get to larger benefits.

Third, while contributions about cycle times of more than two days are

common, a little has been written about faster processes. Longer delivery options

have now been overcome by same day and next day deliveries, which are

becoming (or already are, in more developed areas) industry standards

FAST LOGISTICS IN THE B2C eCOMMERCE: A GLOBAL OVERVIEW

13

(Hausmann et al., 2014); this means that a lot of cases are spreading and these

practices need to be deeply studied and carefully analyzed as they could provide

very interesting insights and drive future development of the business-to-

consumer eCommerce field.

Lastly, too much space is occupied by empirical contributions (i.e. case

studies and surveys), especially for what concerns fast and same day delivery

classes: a wider investigation in the field will allow academics to gather a relevant

number of data and examples so as to develop articles of more general validity,

which could be used by practitioners as frameworks in order to guide their

operative strategies.

All these gaps have been useful in order to formalize the research questions.

Then starting from these highlighted gaps, a depth research has been

performed by investigating examples of delivery options offered by real

merchants operating in the eCommerce channel through the access to the digital

edition of a guide on top 2013 e-retailers; it is called “Internet retailer – portal to

eCommerce intelligence” and it provides profiles, statistics, contacts and analyses

of the largest retailers in a certain geographical area; in particular its versions

split by continent have been utilized, having so one ranking for European

countries, one for Asian continent and the third dedicated to United States

situation only. For Asian and European countries, top 25 players in the ranking

were identified for further research (with the exception of Spain, which was a bit

poorer in terms of relevant online players and the ranking only involved 14

retailers); for US instead, the field was so big that the analysis was extended to

the group of first 60 actors in the national ranking. So for each nation, all

websites belonging to the group of identified top merchants were searched on the

Internet and deeply studied, with a particular attention to the process of orders’

fulfillment and final delivery to customers. Then, all collected information have

been inserted in a database organized according to the following fields:

number in the national ranking: allowing to have an idea of merchants’

relevance inside their country of belonging in terms of sales;

merchant name;

service provider name;

country of belonging of the merchant;

Dot Com/traditional player;

pure player/multichannel retailer;

desktop/mobile website;

commodity sector: sector in which the player operates, identifying in a

precise manner the type of products sold and moved during the service’

supply; we have Clothing, Cosmetics & Perfumery, General, Grocery,

Home & Furniture, Informatics & general electronics, Publishing sectors

FAST LOGISTICS IN THE B2C eCOMMERCE: A GLOBAL OVERVIEW

14

and then other industries of minor presence among which we can find

Childcare, Drugs, Eyewear, Flowers, Music stores and Office supplies;

time for the delivery service: considering services which take more time

than what represents our interest area, we can find different hours’ ranges

surpassing the 24 hours for service provision (e.g. web retailers delivering

in between 48 and 96 hours, others in 48 hours, others between 24 and 72

hours or between 24 and 48 hours); moving instead towards faster

services, we first find merchants operating within the next day or the next

morning (if they are able to assure delivery within lunch time of the day

after order submission); then we have same day operators; in the end,

there is a cluster of websites offering deliveries which do not overcome 6

hours for the whole service provision (some declare of taking less than 6

hours for delivery but without specifying a fixed time, while some others

assure services operating in between 1 and 2 hours or even taking less than

1 hour to be performed). Among all the websites examined, we found also

merchants not offering express services at all (i.e. typically serving

customers in not less than 2 or 3 days and even more), that have been

classified as “non fast” and for which data collection activity has stopped at

this stage as they do not represent the focus of the research. In addition,

there were also websites which were impossible to access and about which

no information could be found even searching through the more

traditional web browsers, together with sites of retailers providing services

and not physical items (and so not arranging any picking and delivery

activity for their business’ nature) and finally websites shut down (it could

be because after some test time they closed the online channel resorting to

more traditional ones or because they went bankrupt); all these cases were

obviously immediately excluded from the database;

additional time information;

hour limit in order to get on-time delivery;

delivery timeframes;

cost type: the delivery service has usually an own cost which adds up to

the one of bought items; this cost can be fixed, variable, fixed but

becoming free once reached a certain expense for the goods (and the same

can happen in case of variable cost) or in few cases offered for free no

matter the expense’s amount;

criteria taken into consideration for variable cost;

exact value of the delivery expense;

exact value of items’ expense to be reached in order to get free delivery;

minimum expense imposed for order submission;

price peculiarities: filled only if some peculiarities exist (e.g. a phone

number is provided and only by calling it the customer can know the exact

FAST LOGISTICS IN THE B2C eCOMMERCE: A GLOBAL OVERVIEW

15

delivery expense or money-back guarantee is assured to customers if the

order is not delivered by the promised time window or if a maximum

number of articles which can be bought within one order exist, etc.);

international coverage;

national coverage;

local coverage;

coverage area;

logistics type (internal/outsourcing/crowd-sourcing): variable identifying

if all the logistics activities are performed internally by the retailer itself

(or at most by a logistics spin-off appositely created for serving a specific

e-retailer and belonging to the same owning group) or if they are left to an

external operator found on the logistics market or lastly, if they are

performed according to the crowd-sourcing model (i.e. there is an external

entity which doesn’t operate as a physical distributor owning assets and

fleets and having couriers working under its direct dependence, but it only

works as an inter-change platform, collecting independent couriers who

work autonomously with their own transportation means and connecting

them with retailers in search of someone to perform home delivery);

preferred logistics operator;

service name;

transportations means’ peculiarity: filled in case a web merchant (or in its

place the provider of the logistics service) resorts to a very specific type of

means only. We can find cases in which more traditional means as vans or

refrigerated vans only are adopted; then we have cases in which the

preferred vehicle utilized is the car. Moving to two-wheeled vehicles we

can find retailers employing indiscriminately bicycles and motorbikes,

while others provide their couriers exclusively with bicycles; there is also

the eco-friendly option in which couriers use electric bicycles for

performing final delivery. In the end moving to air transportation we have

cases in which the airplane is the only mean utilized or innovative

merchants putting in place delivery by drones;

click & collect in-store (as first last-mile delivery alternative);

parcel locker’s pickup (as second last-mile delivery alternative);

other collection point (additional diverse last-mile alternatives);

additional information on last-mile alternative: descriptive variable in

which all information regarding every delivery alternative offered by a

retailer (and explained in its website) are collected; it provides the

alternative description (in case it doesn’t involve in-store collection and/or

parcel locker) (e.g. convenience stores agreed upon collection service with

the retailer and having a terminal dedicated to collection of online orders;

or terminals belonging to a particular logistics operator allied with the

FAST LOGISTICS IN THE B2C eCOMMERCE: A GLOBAL OVERVIEW

16

retailer such as UPS, Colissimo, Chronopost, Hermes points, etc.; or again

delivery in the store’s car park or directly inside vehicle’s trunk; etc.), the

hourly limit for order submission in order to get the alternative or the

specific time window taken by the alternative to be performed;

real-time tracking;

choice of the day/timeframe of delivery;

chosen timeframe duration;

pre-delivery contacts: descriptive variable in which, if present (otherwise

the value is “no”), the moment in which customers have the opportunity of

being directly in contact with the courier carrying their order with

him/her is identified. It could be just a notification to confirm that an

order has been received or a notification of goods pickup in the warehouse

and then of shipment; or it can be the opportunity of speaking with the

courier before he/she starts its delivery tour in order to arrange all the

details for an efficient delivery; or it can even be the option of receiving,

together with delivery details, also courier’s name and image to make the

delivery process always easier;

information on pre-delivery contacts: it reports the nature of contacts with

logistics operators and the technological mean utilized for the

communication (e.g. call, e-mail, text or notification on the website and

details about the exact time in which this communication takes place); of

course this field is filled in only when a pre-delivery contact occurs;

useful websites.

With the data collected in the database, some classifications and analyses

have been performed.

First of all single-variable classifications have been carried out by considering

one database’s field at a time and giving a first overview at a worldwide level,

then deeply investigated by splitting for different geographies of interest.

A second analysis have been carried out by crossing two variables: the first

one was always the commodity sector and the second ones have been selected in

order to find out if some commonalities and/or differences existed among

merchants belonging to different industries; they are the merchant’s business

nature (Dot Com pure player/traditional multichannel actor), the geographic

coverage of the service, the logistics’ type of the provider and lastly the

peculiarity (if any) of vehicles utilized for performing the distribution activity.

FAST LOGISTICS IN THE B2C eCOMMERCE: A GLOBAL OVERVIEW

17

Results

All the aforementioned analyses got to the formalization of the following

answers to the research questions:

1) The most relevant cases of actual merchants operating in the eCommerce

nowadays belong to United States, immediately followed by United

Kingdom and then, some steps away, by France and Germany. The rest of

the European continent and the Asian countries represent a still too

under-developed context with respect to the first players (especially in

comparison with the United States). The worldwide market is still in

general strongly characterized by traditional retailers having added

eCommerce as their secondary or even third business, in an attempt of

implementing a multichannel strategy in order to increase their often

already stable market share; however, most of them have already

understood the potential of mobile devices’ diffusion and have developed

applications to increase the degree of pervasiveness into the market. Most

relevant actors in the actual context still belong to already strongly web

developed sectors of Clothing and Informatics, but other more recent

industries such as General and Grocery sectors are moving forward.

2) The portion of merchants performing deliveries in which the e-fulfillment

process lasts less than twenty-four hours at worldwide level corresponds

to an almost 46 percent of all the eCommerce merchants; of course this

value changes depending on the geography: it is a bit higher in the US

continent (52 percent), balanced a lower value in the Asian continent (38

percent). The European context, if United Kingdom is excluded, reports an

amount of cases not far from the one of oriental countries (37 percent),

but if adding the British merchants (which provide fast services in the 88

percent of national cases) the overall situation of Europe moves close to

the worldwide average value (reaching a 48 percent). Again United

Kingdom and United States provide the highest quantity of cases of

interest. However splitting these cases into more precise time windows

needed for delivery service provision, we find out that most of really fast

initiatives (i.e. the ones taking less than six hours) do not have a precise

country of belonging as they mainly are few sporadic cases or pilot

projects spread in almost all the global territory; instead interesting to

notice is the fact that while most of initiatives in American and European

countries relate to next day options, the most developed trend in the

Asian geographies is the one of same day deliveries.

3) Some of the insights got in order to answer to this question have been

already reported below. We can add that while for next day deliveries no

significant differences among countries can be found (excepted for the fact

FAST LOGISTICS IN THE B2C eCOMMERCE: A GLOBAL OVERVIEW

18

that Dot Com next day players are in limited number in Asia and in the

US, while they constitute a more significant portion of the European

market), same day deliveries differentiate themselves according to the

country of development: indeed, while United States and Europe see a

limited diffusion of these delivery options, Asian countries led by India

report a huge development of same day services. In addition, while almost

all cases of interest can reach only a local coverage, in the United Kingdom

and in some Asian countries (mainly China and Japan) some merchants

are able to offer also more spread options that reach a more national

coverage.

4) The main sectors interested by fast initiatives in general are Clothing and

Informatics, but we can observe some dedicated trends according to the

country and the delivery timing. In fact, for what regards same day

deliveries, while in the US and Europe overall we can mainly find projects

in commodity sectors of recent development (such as Grocery and Others)

Asia provides a higher amount of examples belonging to sectors such as

Informatics and General, that in the other countries have experienced a

precedent development but then have often remained stuck to the next

day delivery timings. Additionally, some sectors comprehend merchants

that are able to cover higher distances with their fast delivery services

(maybe due also to the peculiarity of items transported), which are

Grocery sector in the UK context and Informatics industry in the Asian

continent.

5) The most delivery services increase their speed, the most we can observe

that retailer leave the recourse to outsourced logistics operators in favor of

internal infrastructures properly developed for providing a more

personalized and controlled service; another interesting trend which

ensures a certain speed of the overall e-fulfillment process avoiding big

investments is represented by the crowd-sourcing model application, but

it remains quite under-developed, with a relevant presence only in the

United States. For what concerns vehicles utilized in transportation, vans

(or refrigerated vans in the case of grocers) are leaving the ground to

lighter and faster means such as bicycles and/or motorbikes, especially

individually owned ones for the crowd-sourcing cases. Few cases of major

interest can be found (one of use of electric bicycles and the other project

with drones), but they only represent an almost irrelevant amount of pilot

and testing projects under development.

FAST LOGISTICS IN THE B2C eCOMMERCE: A GLOBAL OVERVIEW

19

1. Introduction In the last decades, the Internet has emerged as a dynamic medium for

channeling transactions between customers and firms in a virtual

marketplace. The growth of the Internet has been phenomenal, and there has

been a corresponding growth in eCommerce market (i.e. the online market

channel). (Cho et al., 2008). The rise of online Internet sales and eCommerce

gave a big boost to retail companies’ sales and gave rise to new and different

business models. According to the “Euromonitor” the global non-store internet

retail sales or internet shopping reported a 14.8% growth from 2007 to 2012, while

the total retail growth was just 0.9% over the same period (Visser et al., 2014).

Estimates reported by the ECommerce Foundation (2015) show that business-to-

consumer (B2C) eCommerce sales worldwide reached $1.9 trillion in 2014,

representing a doubling in sales compared to 2011 (Savelsbergh and Van Woensel,

2016). Mainly following the spread of IT systems such as laptops, tablets, smart

phones and other technologies, today about 45% of all European consumers shop

online (Morganti et al., 2014). The market share of internet shopping will

continue to grow and will substitute traditional shopping. This is more evident by

the fact that by 2020 up to one third of the total shops at shopping centers in

European developed countries like the Netherlands will be closed down due to

the economic crisis and competition from web shops (Visser et al., 2014).

One of the challenging questions that online retailers now face is how to

organize the logistics fulfillment processes during and after order receipt.

Compared with traditional retailers, online retailers are at a disadvantage in that

when a shopper purchases an item from a physical store, the product can

immediately be taken home. However, in the case of online retailers, the

customer must wait for the shipment to arrive (Gong and de Koster, 2008). Jeff

Bezos of Amazon.com notes: “The logistics and the customer service – the

non‐glamorous parts of the business – are the biggest problem with

e‐commerce. A lot of these companies that are coming online spend all their

money and effort building a beautiful website and then they can't get the

stuff to the customer” (US News & World Report, 1999). In line with Bezos’

thought, in a research carried out by European consumers' organizations, it was

found that logistics aspects such as delivery lead times were not met by a

substantial part of the investigated Internet companies (de Koster, 2003). This is

due to the fact that eCommerce requires a new logistics approach in which

small order size, increased daily order volumes, small parcel shipments, and

same‐day shipments are common. Getting goods delivered to a customer's

doorstep in a timely manner is a complicated task and the success of firms in

the eCommerce market depends on the efficiency of their distribution

networks. The effective and efficient movement of goods is critical in the

FAST LOGISTICS IN THE B2C eCOMMERCE: A GLOBAL OVERVIEW

20

eCommerce logistics supply chain (Cho et al., 2008) and this has generated

significant demand for dedicated delivery services to the end customers.

All the aforementioned requirements have resulted in an increasing

fragmentation of shipments into different parts, with a strong attention paid to

the “last-mile” - the final leg in a business-to-consumer delivery service whereby

the consignment is delivered to the recipient, either at the recipient's home or at

a collection point (Ducret R.,2014) and a tremendous innovation in how this last-

mile delivery takes place (Morganti et al., 2014). Today, algorithm-driven delivery

models and analytics enable urban customers to get products delivered faster,

more flexibly, and sometimes less expensively than in the past. Options will

continue to proliferate in the future, with innovative delivery vehicles such as

drones, robots, and driverless vehicles, reducing or perhaps eliminating someday

the need for delivery personnel (Lee et al., 2016). This sector is also seeing the

diffusion of alternative pickup and delivery options (e.g., locker-boxes and parcel

shops) and speed will be the main push in this evolution (Hausmann et al., 2014).

There is an increasing requirement for punctuality and efficiency of express

delivery services. Due to the fact that all customers may have different time

schedules, it is especially important for an express company to deliver goods

punctually as customers expect. At the same time, the express companies

certainly hope to minimize the total travel time for a courier. Therefore, a courier

is facing a though problem and he needs to design the task schedule reasonably

at the beginning of a day’s work, which should not only satisfy all the customers’

appointment times but also make the total time minimized (Sun et al., 2016).

Customers tend to order more frequently, in smaller quantities, and they require

customized services. Companies tend to accept late orders while still

needing to provide rapid and timely delivery within tight time windows (thus the

time available for single preparation activities, such as order picking, is shorter).

In general, lead times are under pressure (Gong and de Koster, 2008). In addition,

the consumer is allowed more and more to take part in defining the e-logistics

that suits him/her, in terms of price, quality, time, green and/or fair practices.

That is, the “logsumer” has more and more power to dictate how the last-mile

needs to be organized (Savelsbergh and Van Woensel, 2016). Now that

eCommerce catches on as a favorable way of making purchases, customers have

increased the pressure they put on retailers and merchants to rapidly supply

products. In such a market, filling orders within a 24 hours time window has

become a standard since some years in many industries, including the

pharmaceutical, food and beverage, office supply and furniture industries

(Gagliardi et al., 2008). Nevertheless, consumers are demanding even more

convenience when delivery is concerned. They want to have multiple delivery options

to choose from, and to receive their products as fast as possible. Once consumers have

experienced a superior service level, they are usually reluctant to return to the

FAST LOGISTICS IN THE B2C eCOMMERCE: A GLOBAL OVERVIEW

21

previous inferior level. Few people would be willing to wait four days for a digital

camera they have ordered online if they can get Amazon to deliver it the next day

(assuming both options are free). Judging from recent survey results, younger

generations (e.g., “millennial”), people living in small households, those working long

hours and consumers with higher incomes are among those particularly willing to pay

for more convenience and speed (Hausmann et al., 2014).

Next day or two-days delivery is currently the industry standard in all developed

countries, but the next evolutionary step is affordable same day delivery. With same

day delivery, orders are delivered within a few hours after purchasing them, or in a

chosen time window on the same day. The Senior Vice President of a logistics

company stated that: “Same day delivery is a game changer because it combines

the immediate product availability of retail with the convenience of ordering

from home” (Hausmann et al., 2014). In recent years, many e-tailers have started

to offer their customers a same day delivery option, sometimes even going down

to 1-hour or 2-hour delivery options (see, e.g., Amazon Prime in selected US

cities) (Savelsbergh and Van Woensel, 2016). Since many online purchases are

impulse buys and, as customers can change their minds and legally cancel the

order within a certain time horizon, a fast response is critical, next day delivery is

no longer enough and different retailers (e.g. the Datch operators Centraal

Boeekhuis, Wehkamp and Albert) had to put in place same day delivery services

in order to stay competitive. Additionally, often the customer specifies a certain

time window for delivery and retailers use different pricing schemes according to

different windows (Gong and de Koster, 2008). As groundbreaking as the

emergence of leading online retailers was in the 1990’s, the impending disruption

that will result from same day delivery will be greater. Same day delivery, if

executed correctly, can provide expansive options for consumers and brands

hoping to grow their business. While critics may see same day delivery as a

downfall for smaller retailers, it can potentially offer competitive advantage for

businesses of all sizes. The logistics required for making same day delivery a

reality are daunting. Supply chain, delivery, customer support, advanced

eCommerce software and warehouse facilities are all crucial to make the new

tactic a reality (Sareen, 2013). Same day delivery has the potential to fundamentally

change the way we shop. It integrates the convenience of online retail with the

immediacy of bricks-and-mortar stores. In recent years an increasing number of

companies have started piloting and operating new models of same day delivery,

including incumbent logistics providers such as DHL, DPD, FedEx, and UPS.

Demand is expected to increase significantly given the compelling value proposition

of same day delivery for consumers because consumers clearly attach a value to it.

The availability of same day delivery is actually expected to further support

eCommerce adoption and drive the online sales of product categories not yet bought

online on a large scale (such as groceries) (Hausmann et al., 2014).

FAST LOGISTICS IN THE B2C eCOMMERCE: A GLOBAL OVERVIEW

22

2. Literature review Coherently with the above premises, the present literature review aims to analyze and

categorize the articles on fast delivery options in B2C eCommerce from an up-to-date

perspective, including more recent contributions to the topic. The objective of this

chapter is twofold: first, to classify researches on this topic made by practitioners and

academics and second, to identify gaps in the research in order to propose directions

for future studies.

2.1 Methodology

2.1.1 Scope of the analysis

This review concerns the examination of the literature related to business-to-

consumer eCommerce with a particular focus on fast deliveries. More specifically,

the viewpoint is that of retailers and merchants which operate in such a fast

delivery context, in order to understand how they decide to organize and conduct

their activities in order to be able to meet customers’ expectations. The main

activities which are investigated are picking after order receipt and delivery of the

goods to the end customer, with a particular attention to the last “leg” of the

delivery process, called “last-mile”. Furthermore, for what concerns order lead

time, not only articles about same day or even faster timings (e.g. about a few

hours) are taken into consideration, but also literature on deliveries made in 24

hours or more, if they are considered to significantly contribute to the topic of

operations’ optimization and activities’ time minimization.

2.1.2 Selection process

First, we established the classification context used to categorize the

material (i.e. logistics management of fast deliveries in the eCommerce

industry);

then the unit of analysis was identified as a single scientific paper or a

white paper published on an international journal;

we consequently conducted a search by keywords using library databases

(e.g. Science Direct, Scopus, Emerald Insights, Google Scholar, etc.). This

search has been carried out using keywords and strings (e.g. “fast picking

eCommerce”, “last-mile delivery”, “same day delivery”, “fast logistics

eCommerce”, “next day delivery”, etc.) and their combinations, that have

been sought in the abstract, title and main body of the scientific papers. In

order to avoid the omission of other potentially significant papers, the

majority of the contributions were also cross-referenced. This method

allowed to analyze the main logistics and transportation journals, as well

FAST LOGISTICS IN THE B2C eCOMMERCE: A GLOBAL OVERVIEW

23

as journals about environment, information systems and computer

science, social and behavioral sciences (e.g. International Journal of

Physical Distribution and Logistics Management, International Journal of

Production Research, International Journal of Production Economics,

International Journal of Logistics Research and Applications, Journal of

Operations Management, Logistics Information Management,

Transportation Research Method, Transportation Science, European

Journal of Operational Research, Business and Information Systems

Engineering, Industrial Management and Data Systems, Information

Technology Journal, Production Planning and Control, Mathematical

Problems in Engineering, Studies in Computational Intelligence, etc.). In

this way, it was possible to assure adequate coverage of the actual body of

research in the field;

we first selected all the papers that in some way dealt with picking and

delivery activities’ management in the context of eCommerce, in order to

collect as many contributions as possible. Then, from this wide base, only

the papers specifically focused on activities’ optimization in terms of order

cycle time minimization and/or provision of a fast delivery offer to

customers where deeply analyzed. As such, the subset of contributions

lastly selected and considered for an in-depth investigation was made of 52

papers published from 2001 to 2017. The number of publications reviewed

in this study can be considered adequate given the fact that this topic has

been particularly developed in the last few years, so it is quite recent and it

is not easy to find many significant contributions on this field;

at this point, the literature was analyzed and categorized. During this

stage, a two-dimensional approach was chosen in order to provide a clear

classification of the examined papers.

2.1.3 Review method

For the purpose of this review, the selected contributions were classified

based on: their main characteristics (i.e. year of publication, journal title and

type, countries addressed), the research methods adopted, and the content area.

All of the papers were categorized according to these review criteria, in order to

identify patterns suggesting possible gaps and themes of interest for future

contributions (Perego et al., 2011; Mangiaracina et al., 2015).

FAST LOGISTICS IN THE B2C eCOMMERCE: A GLOBAL OVERVIEW

24

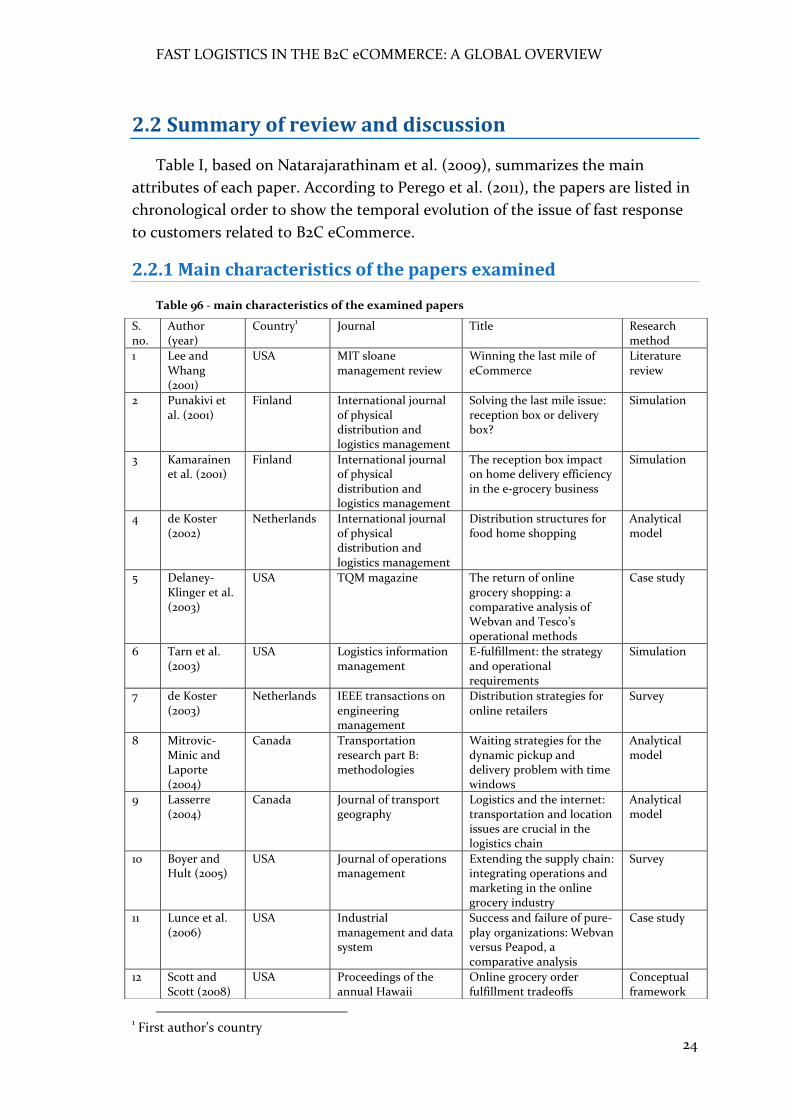

2.2 Summary of review and discussion

Table I, based on Natarajarathinam et al. (2009), summarizes the main

attributes of each paper. According to Perego et al. (2011), the papers are listed in

chronological order to show the temporal evolution of the issue of fast response

to customers related to B2C eCommerce.

2.2.1 Main characteristics of the papers examined

Table 96 - main characteristics of the examined papers

1 First author’s country

S. no.

Author (year)

Country1 Journal Title Research

method

1 Lee and Whang (2001)

USA MIT sloane management review

Winning the last mile of eCommerce

Literature review

2 Punakivi et al. (2001)

Finland International journal of physical distribution and logistics management

Solving the last mile issue: reception box or delivery box?

Simulation

3 Kamarainen et al. (2001)

Finland International journal of physical distribution and logistics management

The reception box impact on home delivery efficiency in the e-grocery business

Simulation

4 de Koster (2002)

Netherlands International journal of physical distribution and logistics management

Distribution structures for food home shopping

Analytical model

5 Delaney-Klinger et al. (2003)

USA TQM magazine The return of online grocery shopping: a comparative analysis of Webvan and Tesco’s operational methods

Case study

6 Tarn et al. (2003)

USA Logistics information management

E-fulfillment: the strategy and operational requirements

Simulation

7 de Koster (2003)

Netherlands IEEE transactions on engineering management

Distribution strategies for online retailers

Survey

8 Mitrovic-Minic and Laporte (2004)

Canada Transportation research part B: methodologies

Waiting strategies for the dynamic pickup and delivery problem with time windows

Analytical model

9 Lasserre (2004)

Canada Journal of transport geography

Logistics and the internet: transportation and location issues are crucial in the logistics chain

Analytical model

10 Boyer and Hult (2005)

USA Journal of operations management

Extending the supply chain: integrating operations and marketing in the online grocery industry

Survey

11 Lunce et al. (2006)

USA Industrial management and data system

Success and failure of pure-play organizations: Webvan versus Peapod, a comparative analysis

Case study

12 Scott and Scott (2008)

USA Proceedings of the annual Hawaii

Online grocery order fulfillment tradeoffs

Conceptual framework

FAST LOGISTICS IN THE B2C eCOMMERCE: A GLOBAL OVERVIEW

25

international conference on system sciences

13 Gagliardi et al. (2008)

Canada International journal of production economics

Space allocation and stock replenishment synchronization in a distribution center

Case study

14 Cho et al. (2008)

USA International journal of physical distribution and logistics management

Logistics capability, logistics outsourcing and firm performance in an eCommerce market

Survey

15 Gong and de Koster (2008)

Netherlands IIE transactions A polling-based dynamic order picking system for online retailers

Simulation

16 Song et al. (2009)

UK Transportation research method

Addressing the last mile problem: transport impacts of collection and delivery points

Case study

17 Ghiani et al. (2009)

Italy Transportation research part E: logistics and transportation review

Anticipatory algorithms for same day courier dispatching

Analytical model

18 Hu and Chang (2009)

China Journal of the Chinese institute of industrial engineers

An innovative logistics model for multi-channel retailing

Analytical model

19 Hu and Chang (2010)

China International journal of advanced manufacturing technology

An innovative automated storage and retrieval system for B2C eCommerce logistics

Analytical model

20 Agatz et al. (2011)

Netherlands Transportation science

Time slot management in attended home delivery

Analytical model

21 Runciman (2011)

UK ITNOW: Oxford journals

Do IT yourself? Case study

22 Durand and Gonzalez-Feliu (2012)

France Procedia – social and behavioral sciences

Urban logistics and e-grocery: have proximity delivery services a positive impact on shopping trips?

Simulation

23 Xiao et al. (2013)

China Information technology journal

B2C eCommerce vehicle delivery model and simulation

Simulation

24 Vanelslander et al. (2013)

Belgium International journal of logistics research and applications

Commonly used eCommerce supply chains for fast moving consumer goods: comparison and suggestions for improvement

Conceptual framework

25 Sareen (2013) USA Wired Once refined, same day delivery will be commonplace

Conceptual framework

26 Morganti et al. (2014)

France Transportation research procedia

The impact of eCommerce on final deliveries: alternative parcel delivery services in France and Germany

Case study

27 Morganti et al. (2014)

France Research in transportation business and management

Final deliveries for online shopping: the deployment of pickup point networks in urban and suburban areas

Case study

28 Wang et al. (2014)

China Mathematical problems in engineering

How to choose “last mile” delivery modes for e-fulfillment

Simulation

29 Gruber et al. Germany Research in A new vehicle for urban Simulation

FAST LOGISTICS IN THE B2C eCOMMERCE: A GLOBAL OVERVIEW

26

(2014) transportation business and management

freight? An ex-ante evaluation of electric cargo bikes in courier services

30 Cleophas and Ehmke (2014)

Germany Business and information systems engineering

When are deliveries profitable?: considering order value and transport capacity in demand fulfillment for last-mile deliveries in metropolitan areas

Case study

31 Ehmke and Campbell (2014)

USA European journal of operational research

Customer acceptance mechanisms for home deliveries in metropolitan areas

Simulation

32 Visser et al. (2014)

Netherlands Procedia – social and behavioral sciences

Home delivery and the impacts on urban freight transport: a review

Literature review

33 Ducret (2014) France Research in transportation business and management

Parcel deliveries and urban logistics: changes and challenges in the courier express and parcel sector in Europe – the French case

Case study

34 Hausmann et al. (2014)

Germany McKinsey & company Same day delivery: the next evolutionary step in parcel logistics

Conceptual framework

35 Xu et al. (2014)

China Proceedings of the 2014 IEEE 18th International Conference on Computer Supported Cooperative Work in Design, CSCWD 2014

Logistics scheduling based on cloud business workflows

Analytical model

36 Kumagai (2014)

USA IEEE spectrum A day in the life of digi-key Case study

37 Wang and Xiao (2015)

China Journal of transport geography

Co-evolution between etailing and parcel express industry and its geographical imprints: The case of China

Conceptual framework

38 Koster et al. (2015)

Germany Transportation research procedia

Cooperative traffic control management for city logistic routing

Conceptual framework

39 Li et al. (2015)

China Lecture Notes in Computer Science

Towards fast and accurate solutions to vehicle routing in a large-scale and dynamic environment

Analytical model

40 Zu and Sun (2015)

China Lecture Notes in Computer Science

Optimization of order picking work flow at the eCommerce logistics centers

Conceptual framework

41 Tsamis et al. (2015)

UK Studies in Computational Intelligence

Adaptive storage location assignment for warehouses using intelligent products

Simulation

42 Wang et al. (2016)

China Transportation Research Part E: Logistics and Transportation Review

Towards enhancing the last-mile delivery: An effective crowd-tasking model with scalable solutions

Analytical model

43 Sun et al. (2016)

China Proceedings - 2016 IEEE International Conference on Web Services, ICWS 2016

A personalized service for scheduling express delivery using courier trajectories

Analytical model

FAST LOGISTICS IN THE B2C eCOMMERCE: A GLOBAL OVERVIEW

27

The 52 papers examined where published in 39 different journals, with a mean

value of about 1.3 contributions per journal. We found different types of journals,

i.e. engineering operations and activity management journals (28 percent),

logistics and transportation journals (20 percent), computer and system sciences

journals (20 percent), information and communication technologies journals(9

percent), business

management, accounting and consulting journals (9 percent), applied

mathematics journals (7 percent), social and behavioral sciences journals (5

percent) and environmental sciences journals (2 percent).

Focusing on the year of publication, we can see a pretty stable trend with one,

two or at maximum three papers published each year from 2001 (with the

exception of 2007 in which there were no contributions to consider); but year

2014 brought a dramatic change: in fact, the big majority of the papers, almost 70

percent, were published from that year on. The reasons that justify this pattern

might be explained as follows. On the one hand, since the emergence of the

Internet as a powerful medium to channel customers and firms in a virtual

marketplace in the last 1990s, there has been a continuous, although moderate,

interest in the optimization of the activities in the B2C eCommerce. The whole

44 Savelsbergh and Van Woensel (2016)

USA Transportation Science

City logistics: Challenges and opportunities

Literature review

45 Schrotenboer et al. (2016)

Netherlands International Journal of Production Research

Order picker routing with product returns and interaction delays

Analytical model

46 Liu et al. (2016)

China Engineering Optimization

A capacitated vehicle routing problem with order available time in eCommerce industry

Analytical model

47 Harrington et al. (2016)

UK Production Planning and Control

Identifying design criteria for urban system last-mile solutions -A multi-stakeholder perspective

Conceptual framework

48 Saskia et al. (2016)

Germany Transportation research Procedia

Innovations in e-grocery and Logistics Solutions for Cities

Case study

49 Van Duin et al. (2016)

Netherlands Transportation research Procedia

Improving Home Delivery Efficiency by Using Principles of Address Intelligence for B2C Deliveries

Conceptual framework

50 Yu et al. (2016)

China Procedia CIRP ECommerce Logistics in Supply Chain Management: Practice Perspective

Literature review

51 Lee et al. (2016)

USA Stanford business school

Technological disruption and innovation in last-mile delivery

Conceptual framework

52 Li et al. (2017)

China International Journal of Production Research

Joint optimisation of order batching and picker routing in the online retailer’s warehouse in China

Analytical model

FAST LOGISTICS IN THE B2C eCOMMERCE: A GLOBAL OVERVIEW

28

supply chain have been investigated: algorithms have been developed in order to

optimize activities inside the firms’ warehouses/plants (addressing stock

allocation, stock replenishment and order picking) but also outside plants’ walls

(delivery scheduling and courier routing, with a particular attention to the last-

mile of the delivery process); business models of different operators’ have been

analyzed and compared, to understand which ones were better able to answer to

more and more challenging customers’ needs, especially in terms of speed; the

daily schedule of couriers operating for online merchants has been addressed in

order to optimize routes, minimize delivery times and maximize the number of

points touched in one tour; additionally, new solutions have been studied to

improve the efficiency of home deliveries. But the real revolution towards same

day or faster delivery services has started in 2014 with the first ground-breaking

pilot projects of Amazon: they have pushed a lot of other online retailers or

logistics companies to invest in such projects, leading a wave in which everybody

was trying to keep the pace and follow this new trend in order to stay competitive

in the market.

Finally, looking at the countries addressed, the number of papers in which the

first author is from China is 13 (corresponding to 25 percent), followed by 12

contributions of researchers from USA (i.e. 23 percent) and 7 contributions of

researchers from the Netherlands (i.e. 13 percent). Then other papers were

written by authors from Germany (five), France (four), UK (four), Canada (three),

Finland (two), Belgium (one) and Italy (one). This result is consistent with the

current fast growing adoption of eCommerce in China, which represents the

most promising emerging market, and the leading position kept by USA in this

industry for years. Interesting also to notice the relevance of contributions from

Netherlands, Germany, France and UK as most innovative and developed

European countries in this field.

2.2.2 Research methods used

Contributions were also classified on the basis of their research methodology.

Categories used for this classification belong to a study by Meixell and Norbis

(2008) who identified seven research methods: analytical/mathematical models,

conceptual models or frameworks, case studies, interviews, surveys, simulations

and others.

As shown in Table I, many papers present analytical or mathematical models

(14), but there are also many based on case studies (11) or presenting conceptual

models and frameworks (10) or simulations (10). For what concerns the remaining

methodologies, some papers are literature reviews aimed at representing the

state-of-the-art of scientific research on a certain topic in the moment they were

written (4), while some others are based on data collected from surveys (3).

FAST LOGISTICS IN THE B2C eCOMMERCE: A GLOBAL OVERVIEW

29

First, the possibility of finding a link between the research method and the

year of publication was investigated: results show that contributions based on

surveys are the less recent ones and no significant papers following this method

have been written after 2008; on the contrary, writings reporting conceptual

models and frameworks follow the opposite trend, because no contributions were

made before 2008 and the large majority of papers (90 percent) belong to the

years from 2013 on. The first pattern could be explained by the fact that the

practices of fast and same day delivery in B2C eCommerce are quite recent and

not already widespread as customers’ requests; this could make hard the job of

submitting surveys and collecting a so relevant number of responses allowing to

draw significant and generally valid conclusions. Instead, the second trend of

conceptual frameworks may be justified by the interest of researchers in

developing theoretical models with a wide-ranging relevance, so that they could

be considered valuable and be studied and applied by a lot of different operators

that want to be competitive.

Then, a possible connection between the type of research method and the

theme addressed was investigated. A specific relationship could not be identified,

but some prevailing themes were found according to the research method. For

example, empirical papers (i.e. case studies or surveys) often address the theme

of supply chain structure, analyzing the whole operations’ chain of one (e.g.

Kumagai J., 2014), two (e.g. Delaney-Klinger K. et al., 2003; Lunce S.E. et al., 2006)

or more firms’ realities (de Koster R., 2003; Boyer K.K. and Hult G.T.M., 2005).

For what concerns case studies alone, they present also the theme of last-mile

delivery in the 36 percent of papers (e.g. Song R. et al., 2009; Runciman B., 2011;

Morganti E. et al., 2014; Cleophas C. and Ehmke J.F., 2014); the interest is mainly

got by failed first-time home deliveries and the study of cases in which alternative

delivery methods are applied, such as pickup points and automatic lockers, in

order to reduce the risk of failure. Analytical and mathematical models in almost

65 percent of cases deal with the theme of delivery scheduling and routing

arrangement for couriers. Some models and algorithms are developed in order to

solve dynamic vehicle dispatching or vehicle routing problem, to minimize time

and cost spent for delivery and maximize the number of touch-points in one

courier’s tour (e.g. Ghiani G. et al., 2009; Agatz N. et al., 2011; Sun Y. et al., 2016);

in some cases these algorithms are also time dependent (i.e. a certain time

window is set as a constraint and specifies the order available time) (e.g. Xu R. et

al., 2014; Li Y. et al., 2015;; Liu L. et al., 2016), while in other cases they focus on

the implementation of a specific delivery technology, such as air cargo (e.g.

Lasserre F., 2004). Then we find some models aimed at solving dynamic pickup

problems to optimize pickers’ activity for orders’ preparation (e.g. Schrotenboer

A.H. et al., 2016); finally, some other papers address both pickup and delivery

issues (e.g. Mitrovic-Minic S., Laporte G., 2004). Interesting to notice the

FAST LOGISTICS IN THE B2C eCOMMERCE: A GLOBAL OVERVIEW

30

significant contribution made by Chinese authors in this field of mathematical

modeling (57 percent of the total). Dealing with simulations, a notable portion

(40 percent) of papers addresses the theme of last-mile delivery: most of them

simulate scenarios in which alternative technologies to attended home delivery

are exploited (i.e. reception box, delivery box and collection-and-delivery points)

in order to compare their performance in terms of cost and service levels (e.g.

Punakivi M. et al., 2001; Kamarainen V. et al., 2001; Wang X. et al., 2014); some

others compare performances of different transportation means, e.g. assessing

the outstanding value of electric and traditional bikes (e.g. Gruber J. et al., 2014).

In conclusion, literature reviews in 75 percent of cases are based on the state-of-

the-art analysis of trends in the couriers and logistics operators’ industry, often

grouped by continent or nation, in order to keep the pace with the last practices

and get useful insights about future possible developments (e.g. Visser J. et al.,

2014; Savelsbergh M. and Van Woensel T., 2016; Yu Y. et al., 2016).

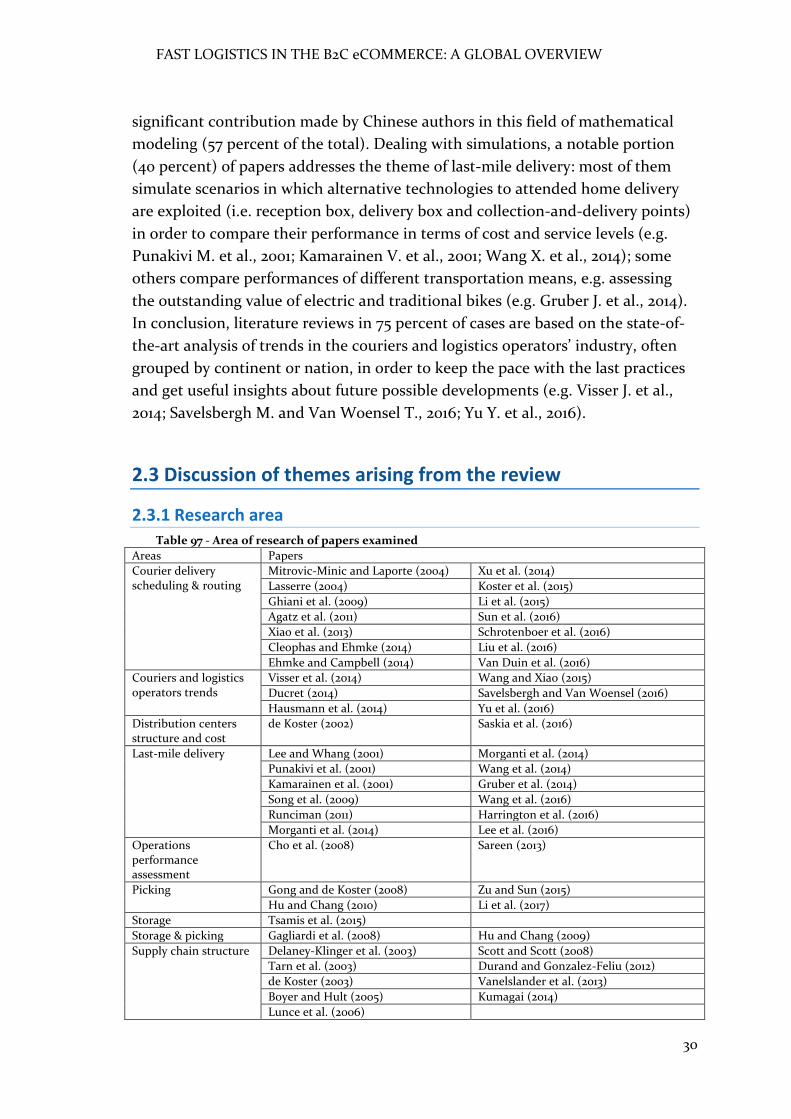

2.3 Discussion of themes arising from the review

2.3.1 Research area

Table 97 - Area of research of papers examined

Areas Papers

Courier delivery scheduling & routing

Mitrovic-Minic and Laporte (2004) Xu et al. (2014)

Lasserre (2004) Koster et al. (2015)

Ghiani et al. (2009) Li et al. (2015)

Agatz et al. (2011) Sun et al. (2016)

Xiao et al. (2013) Schrotenboer et al. (2016)

Cleophas and Ehmke (2014) Liu et al. (2016)

Ehmke and Campbell (2014) Van Duin et al. (2016)

Couriers and logistics operators trends

Visser et al. (2014) Wang and Xiao (2015)

Ducret (2014) Savelsbergh and Van Woensel (2016)

Hausmann et al. (2014) Yu et al. (2016)

Distribution centers structure and cost

de Koster (2002) Saskia et al. (2016)

Last-mile delivery Lee and Whang (2001) Morganti et al. (2014)

Punakivi et al. (2001) Wang et al. (2014)

Kamarainen et al. (2001) Gruber et al. (2014)

Song et al. (2009) Wang et al. (2016)

Runciman (2011) Harrington et al. (2016)

Morganti et al. (2014) Lee et al. (2016)

Operations performance assessment

Cho et al. (2008) Sareen (2013)

Picking Gong and de Koster (2008) Zu and Sun (2015)

Hu and Chang (2010) Li et al. (2017)

Storage Tsamis et al. (2015)

Storage & picking Gagliardi et al. (2008) Hu and Chang (2009)

Supply chain structure Delaney-Klinger et al. (2003) Scott and Scott (2008)

Tarn et al. (2003) Durand and Gonzalez-Feliu (2012)

de Koster (2003) Vanelslander et al. (2013)

Boyer and Hult (2005) Kumagai (2014)

Lunce et al. (2006)

FAST LOGISTICS IN THE B2C eCOMMERCE: A GLOBAL OVERVIEW

31

The papers were also analyzed on the basis of their content (i.e. the issues

they tackle). By looking only at the area of research, we can see that 14 of them

(corresponding to the 27 percent) deal with the theme of delivery scheduling &

routing arrangement in order to optimize couriers’ daily job; as previously stated,

most of them (64 percent) are analytical or mathematical models, but we find

also some conceptual models and some simulations. Their aims are multiple:

finding the best delivery technology able to squeeze at maximum delivery time

(e.g. Lasserre F., 2004); managing the fleet in real-time, without recurring to an a-

priori data preparation phase, to solve problems of optimization of vehicles’ load

(i.e. have vehicles as fully-loaded as possible), assign requests and state routings

for each vehicle (e.g. Mitrovic-Minic S. and Laporte G., 2004; Ghiani G. et al.,

2009; Xiao H. et al., 2013; Cleophas C. and Ehmke J.F., 2014; Ehmke J.F. and

Campbell A.M., 2014; Xu R. et al., 2014; Li Y. et al., 2015; Sun Y. et al., 2016; Liu L.

et al., 2016); selecting the time slots to be assigned to each zip code delivery area

in order to reach cost-effectiveness while, at the same time, keeping an adequate

service performance for customers (e.g. Agatz N. et al., 2011); studying solutions

of traffic control management (i.e. TM) allowing courier express and parcel

services (i.e. CEP) to integrate management of their last mile deliveries with city

traffic conditions (e.g. Koster F. et al., 2015); developing routing decisions for

pickers inside the warehouse, for both activities of simultaneous picking of

ordered products and putting away of returned items and considering also

interactions among pickers working in the same time (e.g. Schrotenboer et al.,

2016); finally, investigating modeling techniques that apply address intelligence

in order to use historical delivery data for identifying and predicting potential

improvements in the choice of zip code delivery areas (e.g. van Duin J.H.R. et al.,

2016).

Then, 12 papers (corresponding to the 23 percent of the total) face different

aspects of last-mile delivery; the research methods they present are numerous,

but case studies and simulations constitute a relevant portion. In many of them,

the issue of unattended and failed first-time home delivery is tackled and

advantages and disadvantages of alternative network designs (such as the

introduction of the reception box, the delivery box, consolidation centers, pickup

points, automatic lockers or the recourse to a crowd-tasking model with a pool of

citizen workers who complete the delivery) are analyzed in order to find a way to

minimize the cost of failure (i.e. cost of repeated delivery for the carrier and/or

cost of customer trips to retrieve the item from depots) (e.g. Punakivi M. et al.,

2001; Kamarainen et al., 2001; Song R. et al., 2009; Morganti E. et al., 2014; Wang

X. et al., 2014; Harrington T.S. et al., 2016; Wang Y. et al., 2016). In other

contributions, the theme of optimization of the last-mile delivery (i.e. pursuing

cost and time reduction while keeping a high service level) is addressed by

looking at the means of transportation and assessing the convenience of

FAST LOGISTICS IN THE B2C eCOMMERCE: A GLOBAL OVERVIEW

32

alternative means that are already in use nowadays and/or which will encounter a

widespread diffusion in the future; examples of these are bikes and electric cargo

bikes, drones, robots and driverless vehicles (e.g. Gruber J. et al., 2014; Lee H.L. et

al., 2016). In the end, one paper (Runciman B., 2011) is focused on analyzing the

positive impact, in terms of last-mile delivery time reduction, of a cloud

infrastructure that operates as a platform to integrate the API web service with

eCommerce, point of sales, mobile and telephone channels of different retailers;

this tool is analyzed in the case of a specific operator (i.e. Shutl) which is now

able to serve its customers within a very short time window.

Moving on with the classification, we can find 9 papers out of the total 52 (so,

the 17 percent of them) dealing with the theme of supply chain structure, taking a

look at the operations strategy and/or the business model applied by one or more

operators along the whole chain. The majority of contributions is made of

frameworks or simulations which propose general logistics models and discuss

typical e-fulfillment strategies, without referring to real cases (e.g. Tarn J.M. et

al., 2003; Scott J.E. and Scott C.H., 2008; Durand B. and Gonzalez-Feliu J., 2012);

one of them analyzes the supply chain not only in terms of activities’

management and operations, but its main aim is to find out the distribution of

logistics costs along the chain (Vanelslander T. et al., 2013). Some papers take

data from case studies or surveys of online retailers in order to investigate

strategies of these different types of retailers; the focus is especially on the choice

of where to fulfill customer orders (from existing stores or dedicated warehouses