fast-tracking bioenergy industry development in malaysia ... · development in malaysia: feedstock...

TRANSCRIPT

Fast-Tracking Bioenergy Industry

Development in Malaysia:

Feedstock Availability, Policy

Frameworks, and Future PlansFrameworks, and Future PlansDato’ Leong Kin Mun, Technical Advisor

EU-Malaysia Biomass Sustainable Production Initiative (Biomass-SP)

2nd Biomass & Pellets Update 2012

17 February 2012, Bangkok, Thailand

The Project

• A development cooperation project funded by the European Union (EU) under the SWITCH-Asia Programme, jointly promoted by the Malaysian Industry Government Group for High Technology (MIGHT), the Association of Environmental Consultants and Companies of Malaysia (AECCOM), the European Biomass Association (EUBIA),and the Danish Technological Instituteand the Danish Technological Institute

• 1 of 16 approved projects from 350 proposal from EU and Asia under SWITCH-Asia Programme

• To assist Malaysian SMEs in the biomass industry to implement sustainable production (SP) models and link them to the EU and global value chain, as well as to contribute towards global climate change mitigation effort.

Biomass resource potential

• 4.7 million ha cultivated with oil palm (13.6% of the country’s total land area)

• 421 mills operation – only 20% crude palm oil and 3% palm kernel oil and

4%

1% 1%

Biomass resource potential

Oil palm20% crude palm oil and 3% palm kernel oil and 3% palm kernel cake, 74% by-products (wet biomass)

• Wood residues aplenty –but a lot of competing uses e.g. furniture-making & particleboard

94%

Oil palm

Wood

Rice

Sugarcane

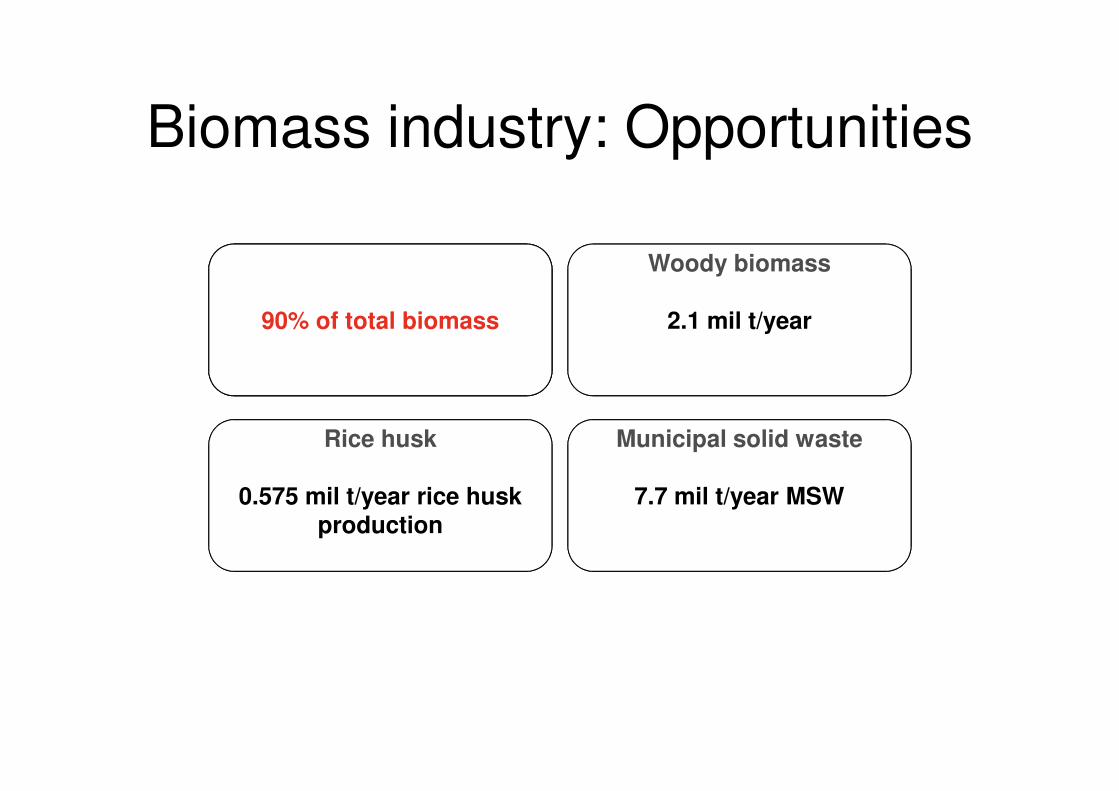

Biomass industry: Opportunities

Palm biomass Woody biomass

Palm biomass

70 mil t/year EFB, PKS, OPF, OPT,

mesocarp fibre, POME

Woody biomass

2.1 mil t/year90% of total biomass

Rice husk Municipal solid waste

Rice husk

0.575 mil t/year rice husk

production

Municipal solid waste

7.7 mil t/year MSW

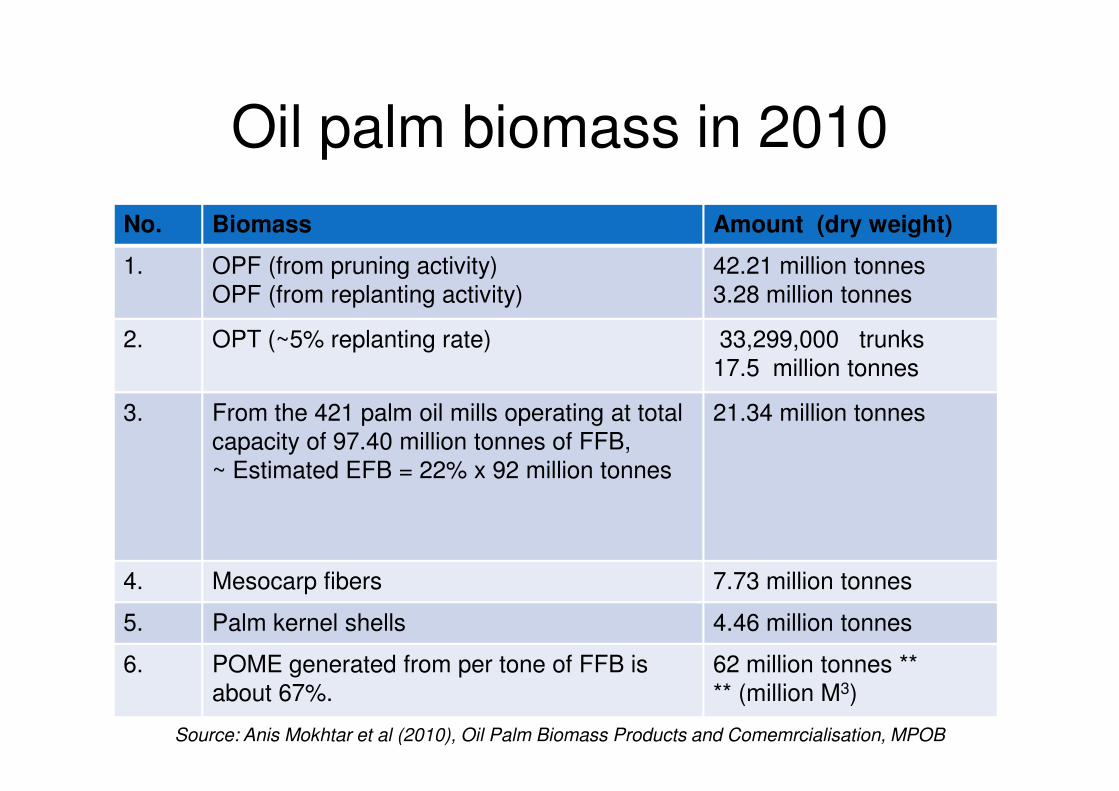

Oil palm biomass in 2010

No. Biomass Amount (dry weight)

1. OPF (from pruning activity) OPF (from replanting activity)

42.21 million tonnes 3.28 million tonnes

2. OPT (~5% replanting rate) 33,299,000 trunks 17.5 million tonnes

3. From the 421 palm oil mills operating at total capacity of 97.40 million tonnes of FFB,~ Estimated EFB = 22% x 92 million tonnes

21.34 million tonnes

4. Mesocarp fibers 7.73 million tonnes

5. Palm kernel shells 4.46 million tonnes

6. POME generated from per tone of FFB is about 67%.

62 million tonnes **** (million M3)

Source: Anis Mokhtar et al (2010), Oil Palm Biomass Products and Comemrcialisation, MPOB

Palm oil industry in Malaysia – the big picture

• Palm oil plantation - 80-85% owned by private estates and government/state-owned schemes, 10-15% by independent smallholders

• Palm oil processing - 60-65% owned by private / listed / government-linked companies, government-linked companies, 35-40% owned by independent palm oil mills

• FELDA – single largest palm oil player in Malaysia; 17.7% of total planted area, and contribute up to 20% in palm oil production

Government initiatives related to biomass/green technology

• National Green Technology Policy 2009– Green technology as driver to accelerate national economy and

promote sustainable development

• 10th Malaysia Plan 2011 – 2015– Renewable Energy (RE) Act 2011 and F-i-T mechanism– 985 MW of RE by 2015 (15.5% of energy mix)

• Economic Transformation Programme (ETP)• Economic Transformation Programme (ETP)• Developing biogas facilities at palm oil mills as part of the National Key

Economic Area (NKEA)

• Renewable Energy Roadmap– RE Act implements F-i-T and RE Fund to cover the cost of the

mechanism– Establishment of dedicated Implementation Agency - SEDA

• Malaysia Biomass Initiative (MBI)– Special Purpose Vehicle for Aggregation, Consortia, etc. Will play

crucial role of long-term sole purchaser and supplier of palm waste biomass – promoted by MIGHT, Global Science Innovation Advisory Council (GSIAC), and BiotechCorp

Recent development

National Biomass Strategy 2020• Spearheaded by Agensi Inovasi Malaysia and

MIGHT• Creation of RM 30 billion GNI impact, mobilising

up to 30 million tonnes30 million tonnes of oil palm biomass, up to 30 million tonnes30 million tonnes of oil palm biomass, 60,000 new jobs by 2020

• 4 EPPs under NKEA; – Pelletisation capacity, – Oil palm biomass centre, – Biogas at palm oil mills, and – Oleo derivatives

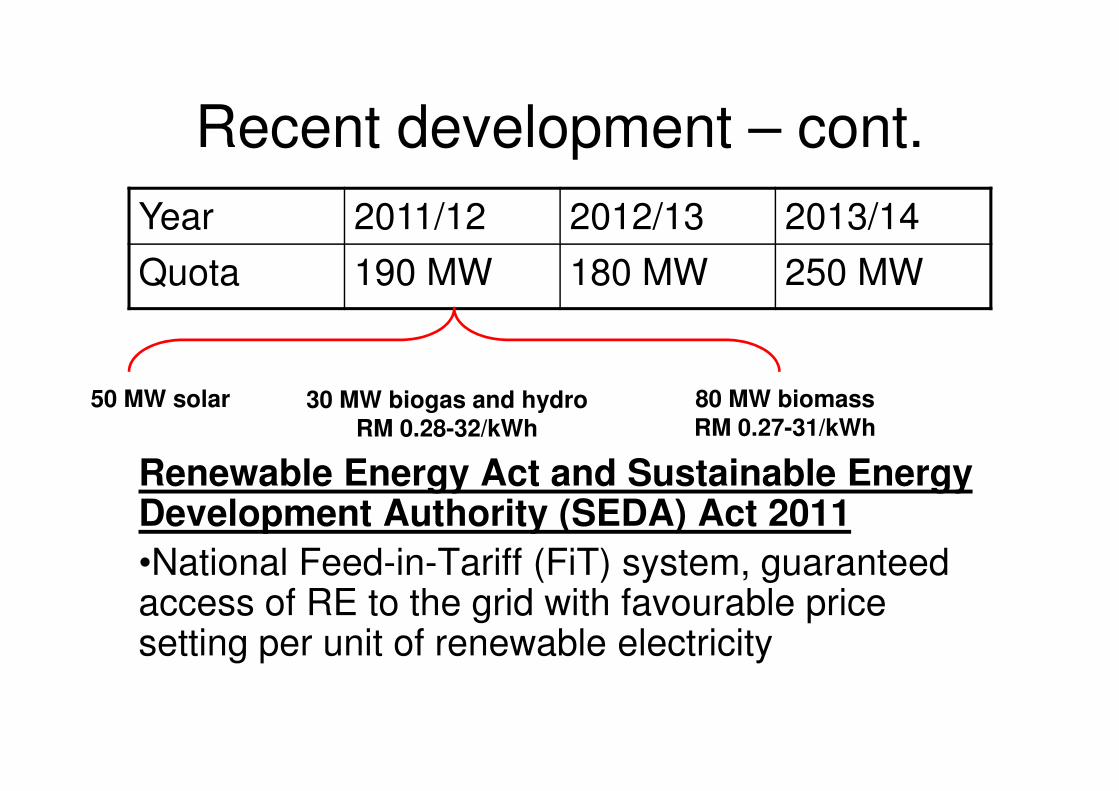

Recent development – cont.

Year 2011/12 2012/13 2013/14

Quota 190 MW 180 MW 250 MW

50 MW solar 30 MW biogas and hydro 80 MW biomass

Renewable Energy Act and Sustainable Energy Development Authority (SEDA) Act 2011

•National Feed-in-Tariff (FiT) system, guaranteed access of RE to the grid with favourable price setting per unit of renewable electricity

50 MW solar 30 MW biogas and hydro

RM 0.28-32/kWh

80 MW biomass

RM 0.27-31/kWh

Value-adding bioenergy ventures with CDM/VCS

• CDM (Clean Development Mechanism): Indirectly supports IRR/ROI of RE development projects –reduction of carbon emissions are registered and verified as certified emission reductions (CERs) and traded for with Annex 1 parties under the Kyoto Protocol/United Nations Framework for Climate Change ConventionNations Framework for Climate Change Convention

• VCS (Voluntary Carbon Standard): focuses on GHG reduction attributes only and does not require projects to have additional environmental or social benefits. The approved carbon offsets are traded as Voluntary Carbon Units (VCUs) and represent emissions reductions of 1 metric tonne of CO2

Incentives for Biomass Industry

• BioNexus Status companies enjoy attractive tax incentives, supporting programs to venture into global market, and Bills of Guarantees provided

• Green Lane Facility under SME Corp for innovative SMEs – 2% interest rebate for approved loans and tax deduction to get 1-innoCERTdeduction to get 1-innoCERT

• Green Technology Financing Scheme for producers and users of green technology

• Pioneer Status and Investment Tax Allowance – tax exemption of 100% statutory income for 10 years for biomass utilisation in energy generation or recycling of biomass to high value-added products

Funding for biomass commercialisation

• TechnoFund (MOSTI) – a bridging fund to address the funding gap between earlier basic research and commercialisation. Up to RM 5 million (RM 40 million boost for Year 2012)

• Commercialisation of R&D Fund (MTDC) for • Commercialisation of R&D Fund (MTDC) for universities – Commercialisation of R&D output from public and private universities up to RM 500k – RM 4 million

• Business Start-Up Fund (MTDC) – to fund new startup technology-based company up to a maximum of RM 5 million

Funding for biomass commercialisation (cont.)

• Cradle Investment Programme (Cradle Fund) – funds development of prototype to facilitate commercialisation -CIP Catalyst (pre-seed fund: RM500k), CIP 500 (commercialisation fund:RM500k, 2 applications/company)

• 1-innoCERT (SME Corp) – innovation certification to • 1-innoCERT (SME Corp) – innovation certification to develop innovative SMEs; opportunities for innovation coaching programme and SME Innovation Award which offers RM1 million to the Top Most Innovative SME

• Machinery loan by OCBC (4%), Project financing (Bank Pembangunan, CIMB), Soft Loan Schemes for SMEs by Agro Bank and MIDF (4%)

Funding for biomass commercialisation (cont.)

• RM500 million Commercialization Innovation Fund to assist SMEs in commercialising research products as announced in Budget 2012

• MyCreative Venture Capital initial fund of RM200 million to increase technological innovation and creativity among the youth RM200 million to increase technological innovation and creativity among the youth (Budget 2012)

• Green Technology Financing Programme (MDV) – contract financing for green certified companies from RM250k to RM2mil

• Green global supply chain opportunities for low carbon product

Funding for biomass commercialisation (cont.)

• Life Sciences Capital Fund (VC) – specialise in early stage investments in agriculture, industrial and healthcare biotechnology

• Malaysian Debts Venture Bhd – funded a large • Malaysian Debts Venture Bhd – funded a large scale CDM InnoWorks Scheme project under Inno Integrasi that promotes integrated waste management and bio-organic fertilizer plants for adoption by palm oil mills; amounting to RM100 million

Funding for biomass commercialisation (cont.)

• Bio-Technology Venture Fund – worth US$100mil (RM317.63mil) to boost the country's biotech industry, to be administered by BiotechCorp for biotech administered by BiotechCorp for biotech companies operating in Malaysia.

Challenges in the Biomass Industry

• Aggregation / collection of biomass

• Are the wastes and residues economically viable; depends on ease of collection and whether projects can be developed near source of supply – logistic costs are major barrier

• Access to financing for commercialisation• Access to financing for commercialisation

• Funding and schemes available but approval depending on Financial Institutions decision based on the 5Cs (Credit, Collateral, Capacity, Character, Condition)

• Conversion technology

• EFB pelletisation, converting biomass to sugar and ethanol yet to be commercially proven

• Projects may fail due to pricing issue for high technology

Challenges in the Biomass Industry-2

• Uncertainties of long term biomass supply (difficult to secure long term fuel supply agreement & pricing mechanism, logistic and transportation cost

• Inconsistency of biomass fuel quality –EFB requires pre-treatment to increase efficiency

• Technical & financial issues related to grid connection for biogas – methane capture projects

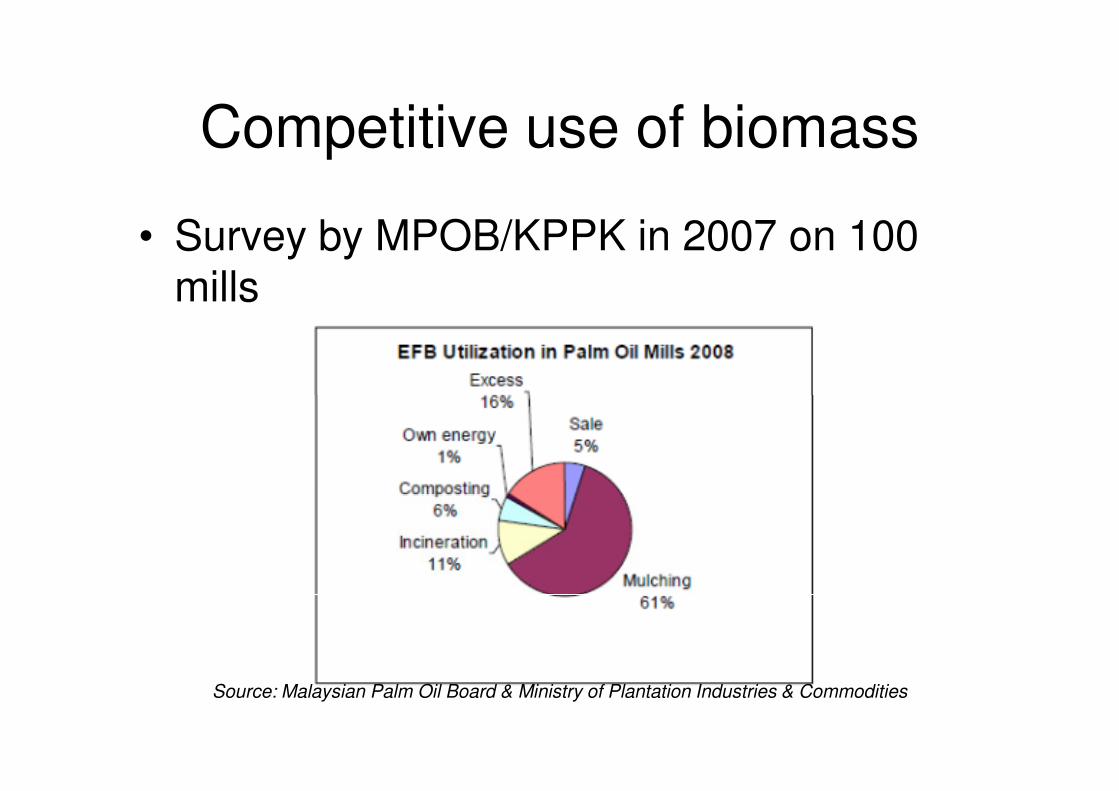

Competitive use of biomass

• Survey by MPOB/KPPK in 2007 on 100 mills

Source: Malaysian Palm Oil Board & Ministry of Plantation Industries & Commodities

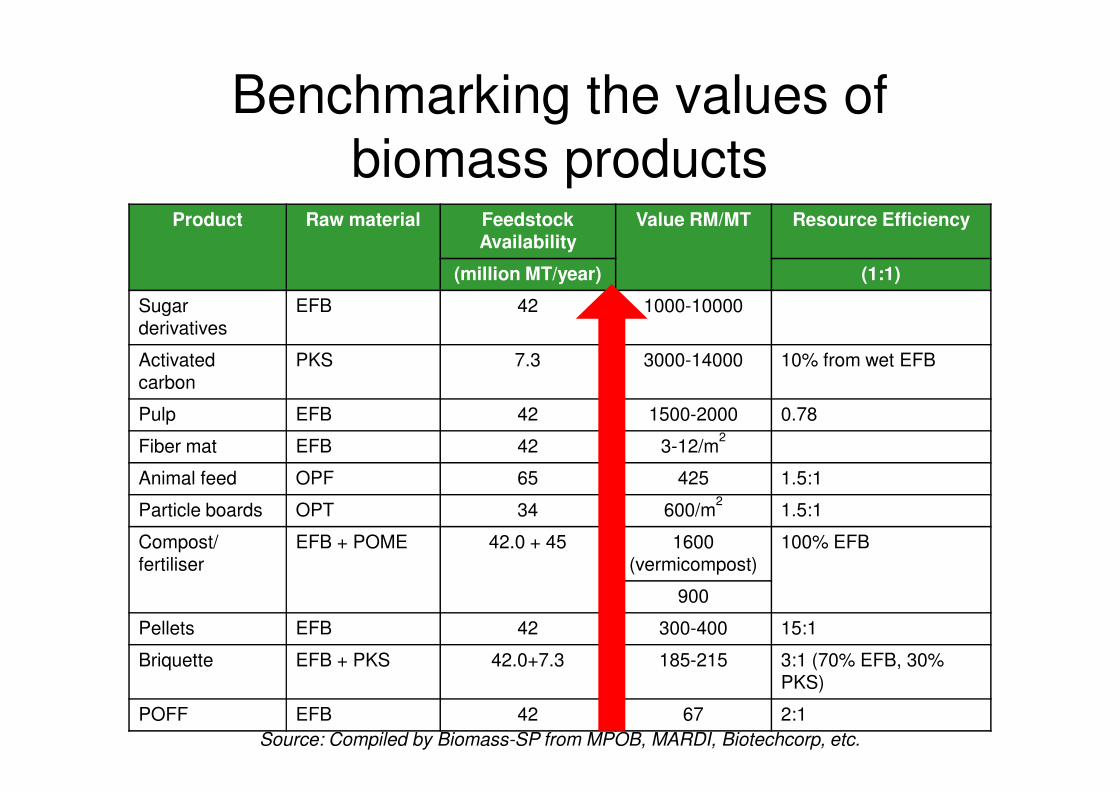

Benchmarking the values of biomass products

Product Raw material Feedstock Availability

Value RM/MT Resource Efficiency

(million MT/year) (1:1)

Sugar derivatives

EFB 42 1000-10000

Activated carbon

PKS 7.3 3000-14000 10% from wet EFB

Pulp EFB 42 1500-2000 0.78

Fiber mat EFB 42 3-12/m2

Animal feed OPF 65 425 1.5:1

Particle boards OPT 34 600/m2

1.5:1

Compost/ fertiliser

EFB + POME 42.0 + 45 1600 (vermicompost)

100% EFB

900

Pellets EFB 42 300-400 15:1

Briquette EFB + PKS 42.0+7.3 185-215 3:1 (70% EFB, 30% PKS)

POFF EFB 42 67 2:1

Source: Compiled by Biomass-SP from MPOB, MARDI, Biotechcorp, etc.

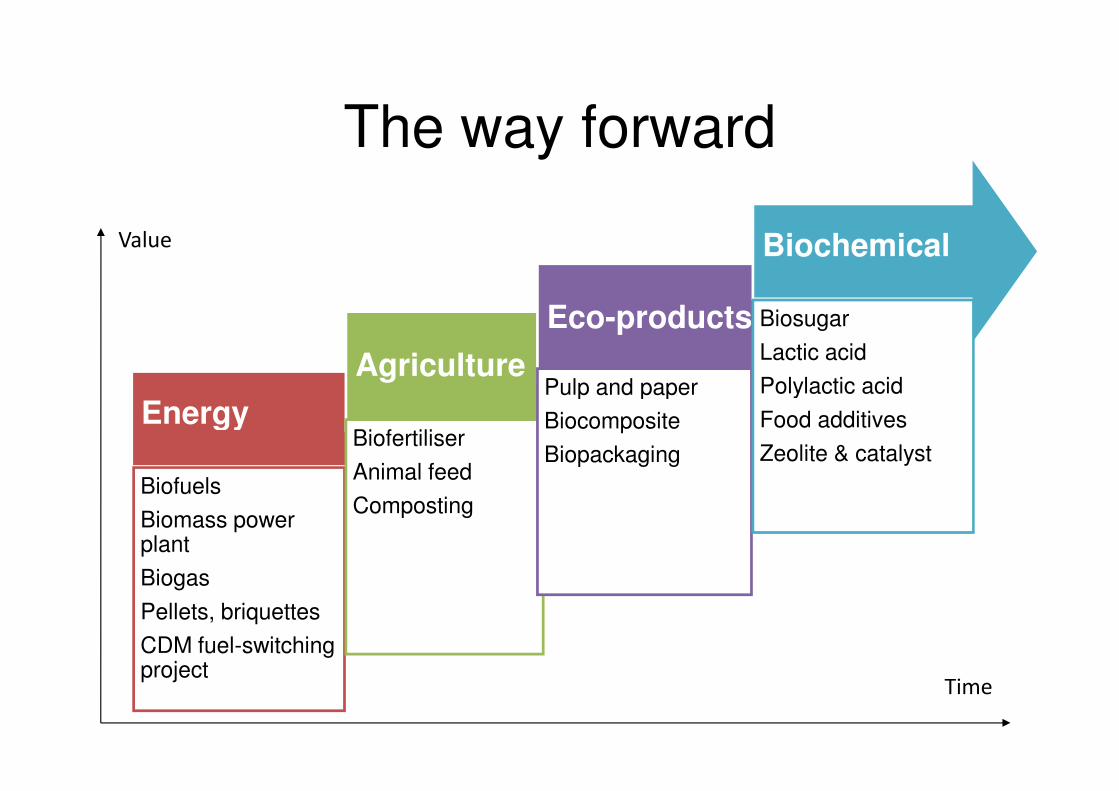

The way forward

Energy

Agriculture

Eco-products

Pulp and paper

Biochemical

Biosugar

Lactic acid

Polylactic acid

Value

Energy

Biofuels

Biomass power plant

Biogas

Pellets, briquettes

CDM fuel-switching project

Biofertiliser

Animal feed

Composting

Pulp and paper

Biocomposite

Biopackaging

Polylactic acid

Food additives

Zeolite & catalyst

Time

Thank You

Q&A Session

EU-Asia Biomass Best Practices and

Business Partnering Conference 2012

• 7-10 May 2012 at Putra World Trade Centre (PWTC)

• Invited 100 regional speakers

• Areas of focus: biomass as energy, biomass as high value chemicals, and biomass as eco-products

• Business Matching Event• Business Matching Event

• Participation from more than 300 biomass stakeholders during the official launching!

• Serious EU biomass companies (investors, buyers, technology providers etc) looking for business collaboration with Malaysia will be granted Travel Incentive EUR 800 (travel from Europe to Malaysia)

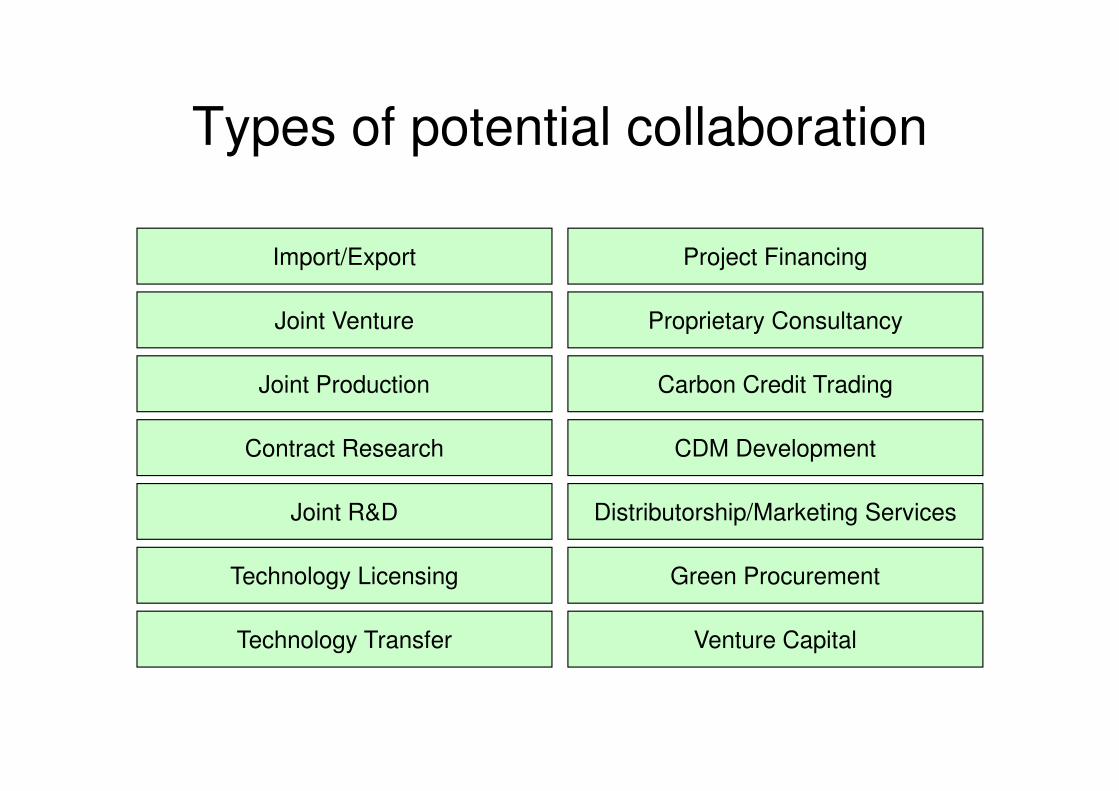

Import/Export

Proprietary ConsultancyJoint Venture

Joint Production

Project Financing

Carbon Credit Trading

Types of potential collaboration

Joint Production

Contract Research

Joint R&D

Technology Licensing

Technology Transfer

Carbon Credit Trading

Distributorship/Marketing Services

Venture Capital

CDM Development

Green Procurement

Potential areas of collaboration

� Buyers meet Sellers

� Consultants meet Clients

� Entrepreneurs meet Venture Capitalists

� Exporters meet Importers

� Researchers meet Marketers

� Researchers meet Researchers

� SMEs meet Multi-� Exporters meet Importers

� Foreign Investors meet Government Officers

� Investors meet Marketers

� Vendors meet Procurement Officers, etc.

� SMEs meet Multi-National Companies

� SMEs meet SMEs

� Suppliers meet Distributors

� Traders meet Manufacturers

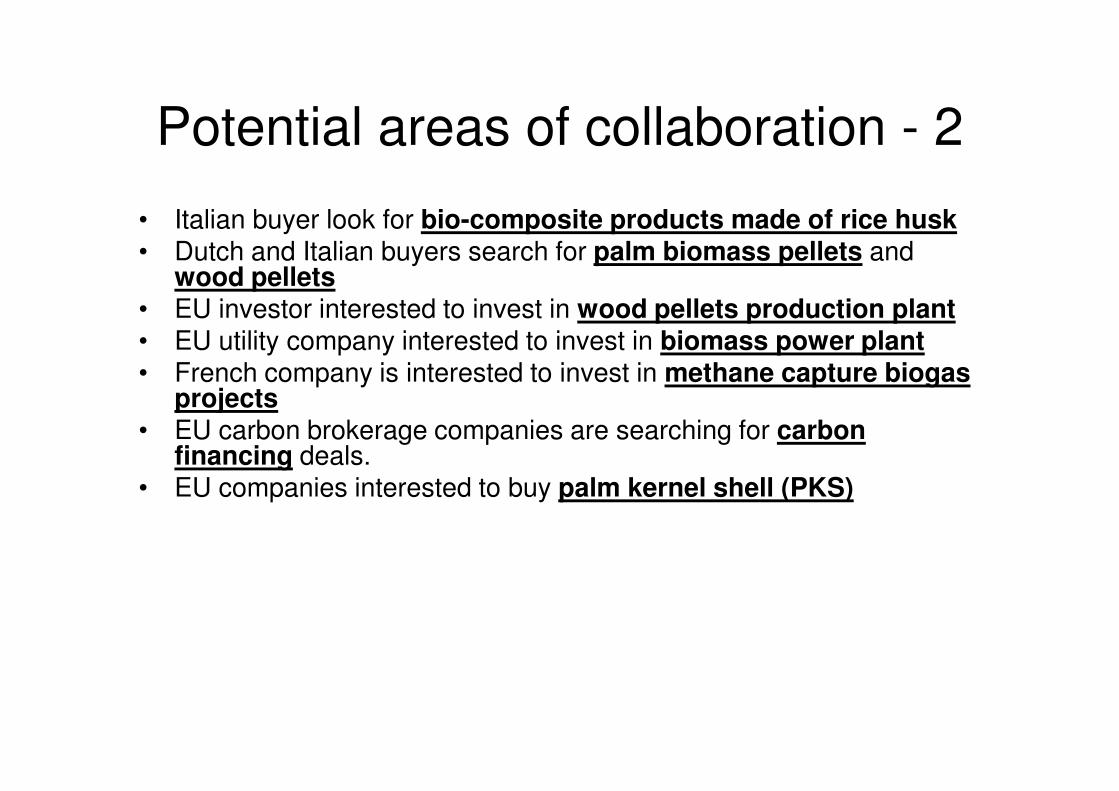

Potential areas of collaboration - 2

• Italian buyer look for bio-composite products made of rice husk• Dutch and Italian buyers search for palm biomass pellets and

wood pellets• EU investor interested to invest in wood pellets production plant• EU utility company interested to invest in biomass power plant• French company is interested to invest in methane capture biogas

projects projects • EU carbon brokerage companies are searching for carbon

financing deals. • EU companies interested to buy palm kernel shell (PKS)

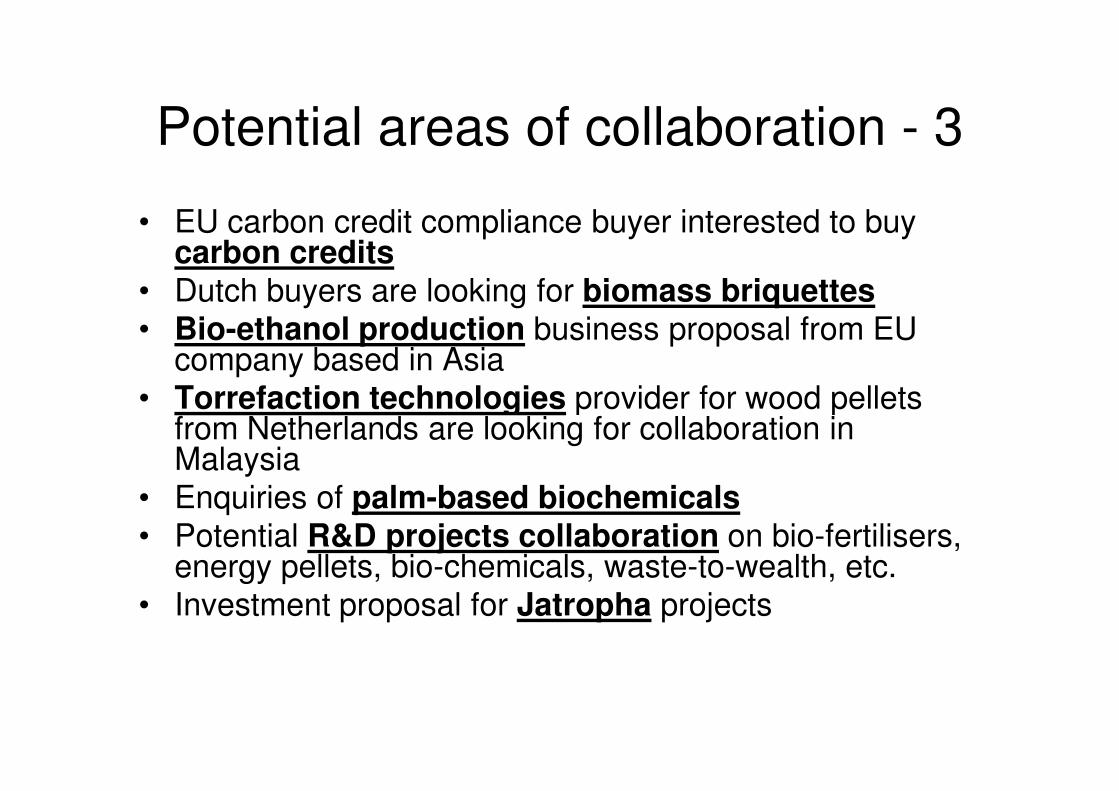

Potential areas of collaboration - 3

• EU carbon credit compliance buyer interested to buy carbon credits

• Dutch buyers are looking for biomass briquettes• Bio-ethanol production business proposal from EU

company based in Asia• Torrefaction technologies provider for wood pellets • Torrefaction technologies provider for wood pellets

from Netherlands are looking for collaboration in Malaysia

• Enquiries of palm-based biochemicals• Potential R&D projects collaboration on bio-fertilisers,

energy pellets, bio-chemicals, waste-to-wealth, etc.• Investment proposal for Jatropha projects

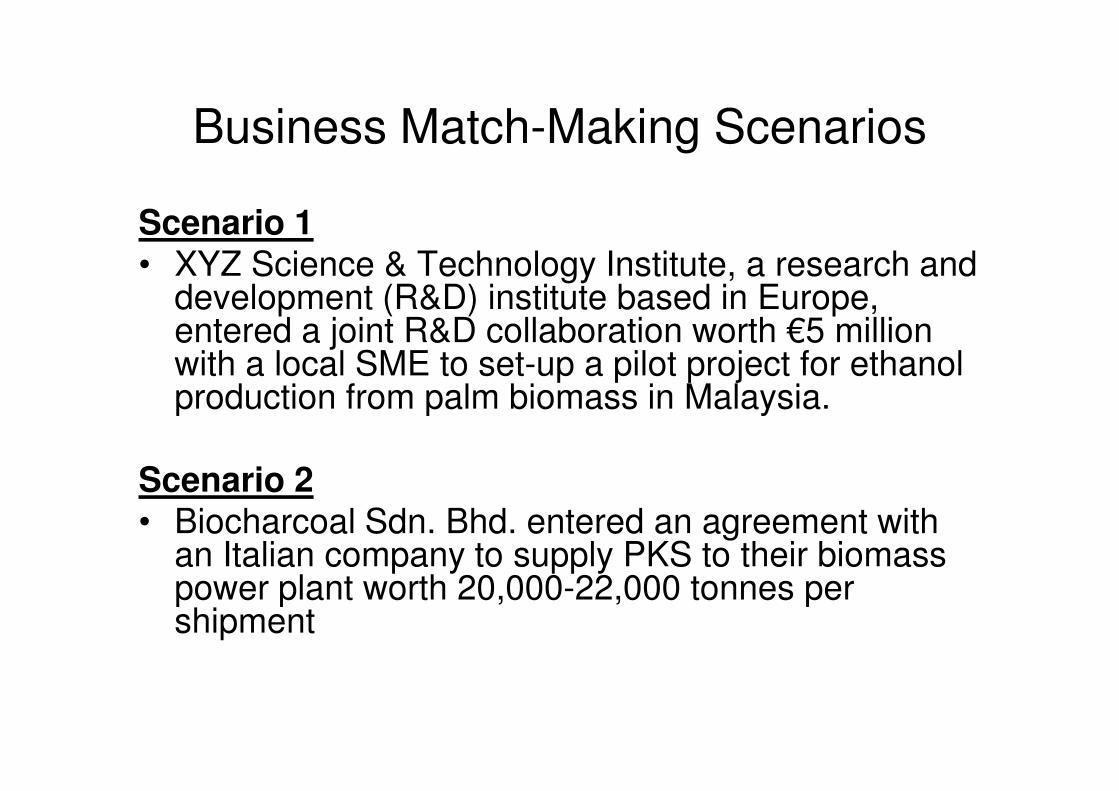

Business Match-Making Scenarios

Scenario 1• XYZ Science & Technology Institute, a research and

development (R&D) institute based in Europe, entered a joint R&D collaboration worth €5 million with a local SME to set-up a pilot project for ethanol production from palm biomass in Malaysia. production from palm biomass in Malaysia.

Scenario 2• Biocharcoal Sdn. Bhd. entered an agreement with

an Italian company to supply PKS to their biomass power plant worth 20,000-22,000 tonnes per shipment

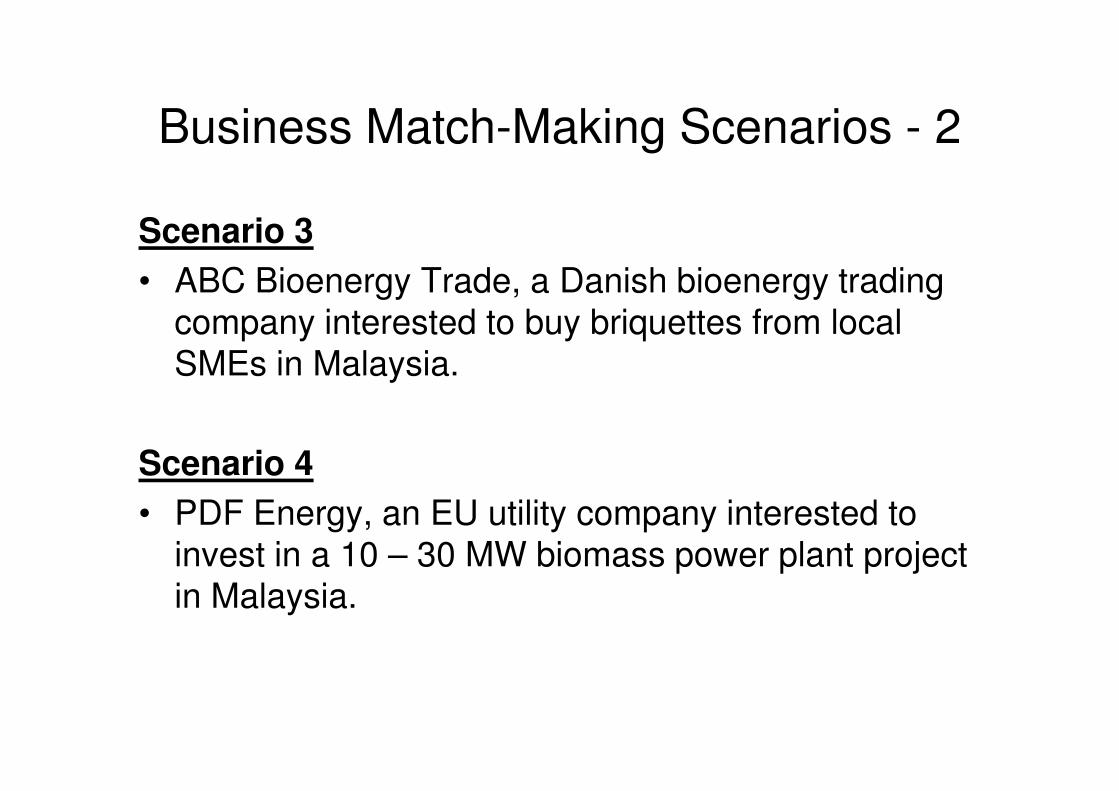

Business Match-Making Scenarios - 2

Scenario 3

• ABC Bioenergy Trade, a Danish bioenergy trading company interested to buy briquettes from local SMEs in Malaysia.

Scenario 4

• PDF Energy, an EU utility company interested to invest in a 10 – 30 MW biomass power plant project in Malaysia.

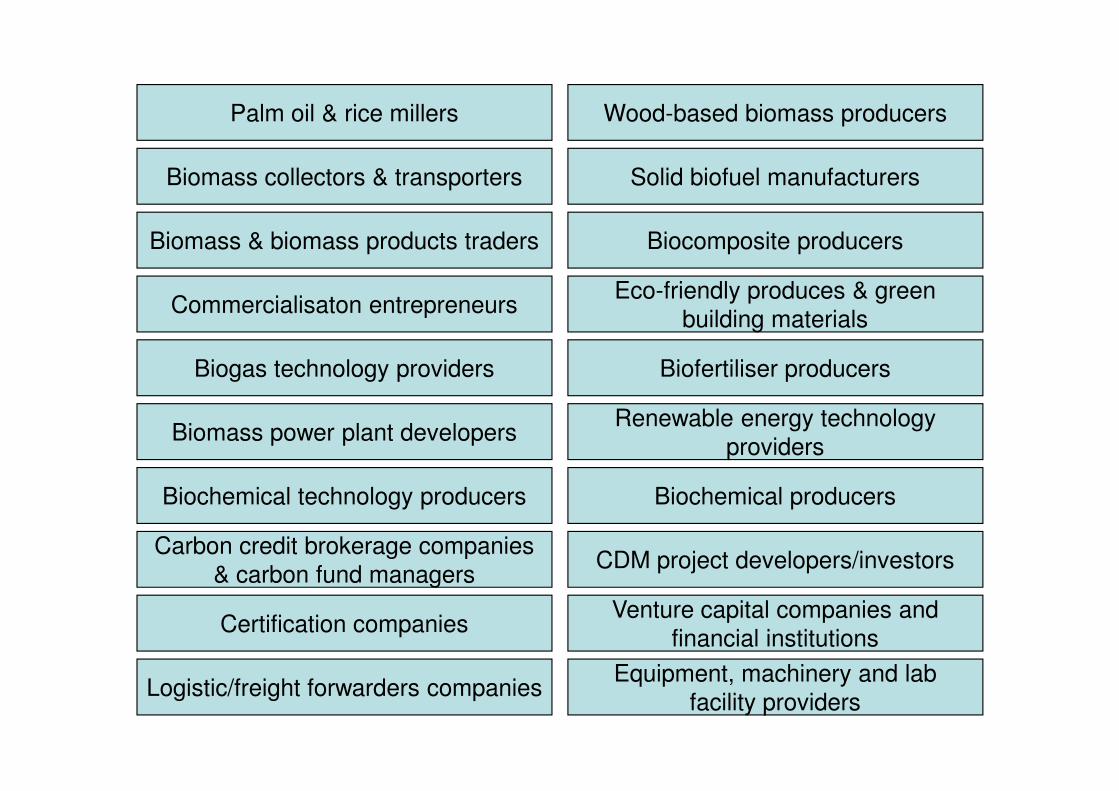

Palm oil & rice millers

Solid biofuel manufacturersBiomass collectors & transporters

Biomass & biomass products traders

Commercialisaton entrepreneurs

Biogas technology providers

Wood-based biomass producers

Biocomposite producers

Biofertiliser producers

Eco-friendly produces & green building materials

Biomass power plant developers

Biochemical technology producers

Carbon credit brokerage companies & carbon fund managers

Certification companies

Biochemical producers

Renewable energy technology providers

Venture capital companies and financial institutions

CDM project developers/investors

Logistic/freight forwarders companiesEquipment, machinery and lab

facility providers

For further information

Serious EU biomass buyers/traders/technology providers/investors may consult Biomass-SP as your focal

point to trade biomass in Malaysia: EFB, pellets, PKS, woodchips, biocharcoal, briquettes, investments in

biomass power plants, etc.

For further information

T: 603-88848882

F: 603-88848838

www.biomass-sp.net