fba fa section8 writing a financial report carlsberg casefahmi.ba.free.fr/docs/courses/hec...

TRANSCRIPT

Financial Financial StatementStatement AnalysisAnalysis

Section 8.Section 8.Section 8.Section 8.

Writing a Financial Analysis Report Writing a Financial Analysis Report An example of analysis gridAn example of analysis gridGuidance NotesGuidance NotesGolden RulesGolden RulesLimitations of Financial RatiosLimitations of Financial Ratios

Carlsberg Case StudyCarlsberg Case StudyPreliminary AnalysisPreliminary Analysis

Writing a Financial Analysis Report Writing a Financial Analysis Report An example of analysis gridAn example of analysis gridGuidance NotesGuidance NotesGolden RulesGolden RulesLimitations of Financial RatiosLimitations of Financial Ratios

Carlsberg Case StudyCarlsberg Case StudyPreliminary AnalysisPreliminary Analysis

Fahmi Ben Abdelkader ©

HEC Paris2015

Preliminary AnalysisPreliminary AnalysisGrowth AnalysisGrowth AnalysisProfitability AnalysisProfitability AnalysisIlliquidity risk: short and longIlliquidity risk: short and long--term ratiosterm ratiosSummary NoteSummary Note

Preliminary AnalysisPreliminary AnalysisGrowth AnalysisGrowth AnalysisProfitability AnalysisProfitability AnalysisIlliquidity risk: short and longIlliquidity risk: short and long--term ratiosterm ratiosSummary NoteSummary Note

5/7/2016 6:26 PM 1

Chapter Outline

Writing a Financial Analysis Report An example of analysis gridAn example of analysis gridGuidance NotesGolden RulesLimitations of Financial Ratios

Carlsberg Case StudyPreliminary AnalysisGrowth Analysis

Fahmi Ben Abdelkader © Financial Statement Analysis5/7/2016 6:26 PM 2

Growth AnalysisProfitability AnalysisIlliquidity risk: short and long-term ratiosSummary Note

How to conduct a financial analysis?

Writing a Financial Analysis Report An example of a nalysis gridGuidance NotesGolden RulesLimitations of Financial Ratios

In the long run, a company can survive only if it creates value for its shareholders and meets

A guiding principle

its commitments towards all its stakeholders

To do so, it must:

Generate wealth

Invest

Finance its investments

GrowthAnalysis

Financial Analysis

Fahmi Ben Abdelkader © Financial Statement Analysis5/7/2016 6:26 PM 3

Generate a sufficient return

Anticipate and manage illiquidity risk

ProfitabilityAnalysis

Risk Analysis

How to conduct a financial analysis?

Writing a Financial Analysis Report

(1)Strategic and

Economic Assessment

Preliminary analysis

Preliminary analysis

1.1 Understand the characteristics of the sector in which the company operates…1.2 … analyse the auditors’ report and accounting policies

The toolkit of the financial analyst

Sales, Net Income, EBITDA, Total Assets 2.1 Growth measurement

An example of analysis gridGuidance NotesGolden RulesLimitations of Financial Ratios

Financial AnalysisFinancial Analysis

2.2 How the firm uses its money? Fixed Assets, WC, Capital Employed, Cash flow from investment activities

2.3 Where does the money come from? Leverage, Equity, Net Debt, Capital Invested, Short-term debt, etc.

2.4 Analysis of the Cash Cycle WC in days’ worth of sales; Cash flow from operating, FCF

3.1 Margin analysis Profitability ratios, Cost structure

3.2 Return on Invested Capital (ROIC)ROIC = NOPAT/ Capital EmployedROIC = Oper. Margin * Asset turnoverEconomic Value Added = ROIC - WACC

(2) Growth Analysis

(3) Profitability

Fahmi Ben Abdelkader © Financial Statement Analysis

Summary note

Summary note

3.3 Return on Equity (ROE)

4.2 Solvency risk

Economic Value Added = ROIC - WACC

ROE = Net Income/ EquityROE = ROIC + Leverage effectResidual Income= ROE - re

4.1 Short-term liquidity risk Current ratioQuick ratio

Interest coverage ratio, leverage, etc.

Profitability Analysis

(4) Risk Analysis

5. Develop and communicate conclusions / recommenda tions(5)

Recommendations

Some Guidance Notes

Writing a Financial Analysis Report

There is no single indicator of good health

A rigorous Financial Analysis requires a combination and a cross-analysis of different indicators covering several aspects to “good financial health”

An example of analysis gridGuidance NotesGolden RulesLimitations of Financial Ratios

aspects to “good financial health”

Ratios are not very helpful by themselves; they nee d to be compared to something: an appropriate benchmark

Time-Trend Analysis

Comparison with competitors and industry peers

Return ratios should be compared to the required rate of return (Opportunity Cost of Capital)

Fahmi Ben Abdelkader © Financial Statement Analysis5/7/2016 6:26 PM 5

Don’t only focus on the numbers, you need to be awa re of the organisation’s business strategy and objectives

Understand the nature of the industry in which the organisation operates

Understand that the overall state of the economy may also have an impact on the performance of the organisation

There is nothing worse in FSA and valuation than fo rgetting the overall picture

Some Golden Rules

Writing a Financial Analysis Report An example of analysis gridGuidance NotesGolden RulesLimitations of Financial Ratios

Spending money does not necessarily make you poorer and neither does receiving money necessarily make you any richer .

A positive cash flow is not always value creating and vice versa (Cash generated by the core business versus cash A positive cash flow is not always value creating and vice versa (Cash generated by the core business versus cash generated by non-operating activities)

Earnings are an opinion, cash is a fact

The need to assess earnings quality

A lever can become a club

In assessment of earnings quality, the analyst should consider the materiality and variability of NON-OPEARTING items of income such as non-cash items

Fahmi Ben Abdelkader © Financial Statement Analysis5/7/2016 6:26 PM 6

A lever can become a club

The impact of financial leverage cannot be analyzed independently of Risk

The value of a business depends primarily on the capacity of its assets to generate cash flows, and less on capital structure choices

A lack of liquidity may lead to loss of business op portunities and, in a worst case, bankruptcy

Limitations of Financial Ratios

Writing a Financial Analysis Report An example of analysis gridGuidance NotesGolden RulesLimitations of Financial Ratios

« les chiffres sont des êtres fragiles qui, à force d'être torturés, finissent par avouer tout ce qu'on veut leur faire dire »

Alfred Sauvy

Despite the appealing nature of financial ratios, t hey should be used with caution:

Accounting practices differ among firms and countries

Many ratios provides a snapshot of the firm’s financial position at a given point in time (e.g. Seasonality effects).

Based on historical accounting information and, thus, backward-looking

Fahmi Ben Abdelkader © Financial Statement Analysis5/7/2016 6:26 PM 7

Accounting numbers always subject to window dressing (e.g. ROE).

Inflation Effects ; mostly on balance sheet and income statement amounts.

Chapter Outline

Writing a Financial Analysis Report An example of analysis gridAn example of analysis gridGuidance NotesGolden RulesLimitations of Financial Ratios

Carlsberg Case StudyPreliminary AnalysisGrowth Analysis

Fahmi Ben Abdelkader © Financial Statement Analysis5/7/2016 6:26 PM 8

Growth AnalysisProfitability AnalysisIlliquidity risk: short and long-term ratiosSummary Note

Strategic and Economic Assessment

Carlsberg Case Study Preliminary AnalysisGrowth AnalysisProfitability AnalysisLiquidity risk: short and long-term ratiosSummary Note

Understand the Business well and identify the main characteristics of :

⇒ the sector in which the company operates…

⇒ the product

⇒ the production model⇒ the production model

⇒ distribution network

⇒ markets (local vs foreign)

Etc.

What are the potential implications of these charac teristics on :

⇒ the operating cycle

⇒ the Cash cycle

⇒

Fahmi Ben Abdelkader © Financial Statement Analysis5/7/2016 6:26 PM 9

⇒ the working capital

⇒ investment requirements

⇒ margins

⇒ risk

Etc.

Strategic and Economic Assessment

Carlsberg Case Study Preliminary AnalysisGrowth AnalysisProfitability AnalysisLiquidity risk: short and long-term ratiosSummary Note

The Carlsberg Group is the fourth largest brewer in the world . The Group employs 41,000 people and is characterized by a high degree of diversity of brands, markets, and cultures.

The business is focused in Western Europe, Eastern Europe and Asia where the firm has strong market

An extensive portfolio of more than 500 beer brands provides a beer for every occasion and palate. Their flagship brand, Carlsberg, is one of the best known beer brands in the world , and Baltika, Carlsberg, Tuborg and Kronenbourg are among the biggest brands in Europe .

The business is focused in Western Europe, Eastern Europe and Asia where the firm has strong market positions . The rest of the world is mainly serviced through export or license agreements.

Since growth estimates are expected to be somewhat stagnant in Western Europe (poor performance in Spain and Greece), Carlsberg has been engaging in a lot of acquisitions to gain market share in emerging markets, mainly Russia and Asia. However, Carlsberg has suffered from the 200% duty

Fahmi Ben Abdelkader © Financial Statement Analysis5/7/2016 6:26 PM 10

emerging markets, mainly Russia and Asia. However, Carlsberg has suffered from the 200% duty increase on beer in Russia in 2010.

A benchmark: Heineken

Both companies focus on the production and sale of beverages and they are among the top-five players in the brewery sector worldwide. From this perspective, they are comparable.

Strategic and Economic Assessment: what do we expec t to see?

Carlsberg Case Study Preliminary AnalysisGrowth AnalysisProfitability AnalysisLiquidity risk: short and long-term ratiosSummary Note

Beer is the core product

Industrial business activity

the working capital is expected to be positive (but the company is also expected to have a strong

Relatively strong market position, but :

Heavy investments in Asia and Russia over the past 6 years

the working capital is expected to be positive (but the company is also expected to have a strong bargaining power thanks to its position in the market and its size)

Pressure on the cash cycle

High Investment requirements

Assess asset turnover

Fahmi Ben Abdelkader © Financial Statement Analysis5/7/2016 6:26 PM 11

Relatively strong market position, but :

Declining sales in Western European countries, mainly those affected by the debt crisis

The 200% duty increase on beer in Russia in 2010

margins are expected to be relatively comfortable

But high pressure on margins due to the debt crisis and an increase in taxes in Russia

Strategic and Economic Assessment

Carlsberg Case Study Preliminary AnalysisGrowth AnalysisProfitability AnalysisLiquidity risk: short and long-term ratiosSummary Note

Stock price trends (2010-2013)

Dow Jones

Heineken

Carlsberg

Fahmi Ben Abdelkader © Financial Statement Analysis5/7/2016 6:26 PM 12

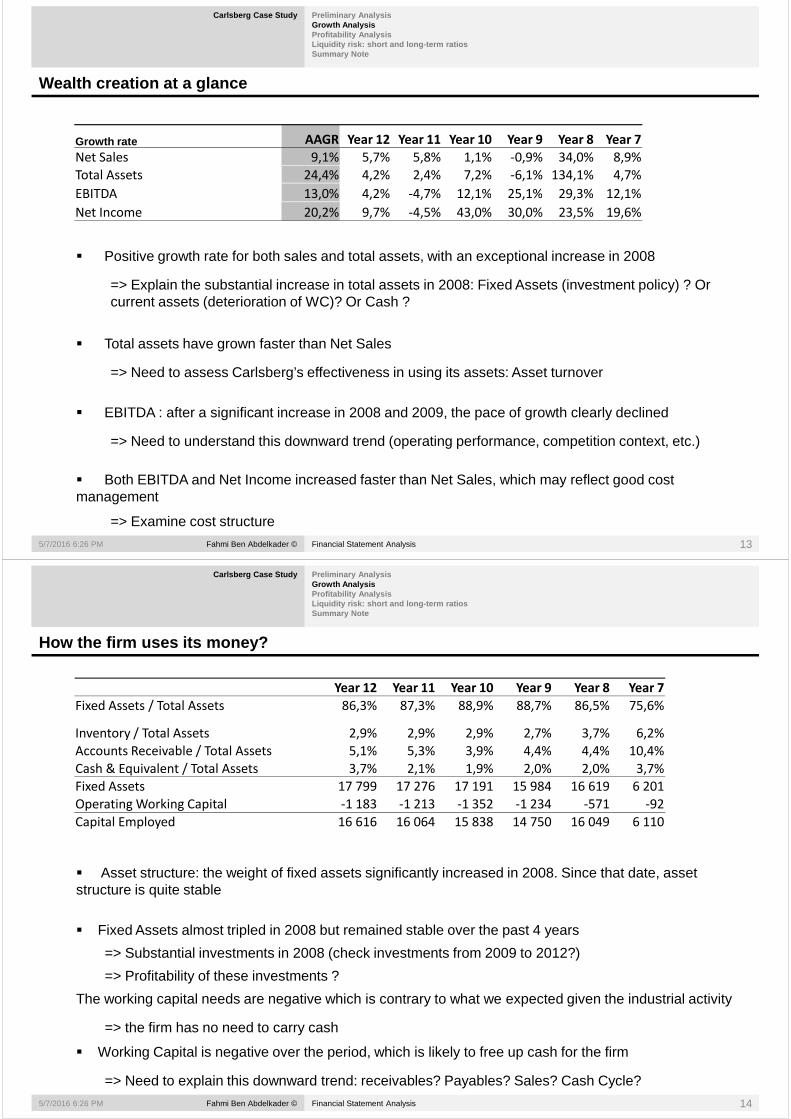

Wealth creation at a glance

Carlsberg Case Study Preliminary AnalysisGrowth AnalysisProfitability AnalysisLiquidity risk: short and long-term ratiosSummary Note

Growth rate AAGR Year 12 Year 11 Year 10 Year 9 Year 8 Year 7

Net Sales 9,1% 5,7% 5,8% 1,1% -0,9% 34,0% 8,9%

Total Assets 24,4% 4,2% 2,4% 7,2% -6,1% 134,1% 4,7%

EBITDA 13,0% 4,2% -4,7% 12,1% 25,1% 29,3% 12,1%

� Positive growth rate for both sales and total assets, with an exceptional increase in 2008

EBITDA 13,0% 4,2% -4,7% 12,1% 25,1% 29,3% 12,1%

Net Income 20,2% 9,7% -4,5% 43,0% 30,0% 23,5% 19,6%

=> Explain the substantial increase in total assets in 2008: Fixed Assets (investment policy) ? Or current assets (deterioration of WC)? Or Cash ?

� Total assets have grown faster than Net Sales

=> Need to assess Carlsberg’s effectiveness in using its assets: Asset turnover

Fahmi Ben Abdelkader © Financial Statement Analysis5/7/2016 6:26 PM 13

� EBITDA : after a significant increase in 2008 and 2009, the pace of growth clearly declined

=> Need to assess Carlsberg’s effectiveness in using its assets: Asset turnover

=> Need to understand this downward trend (operating performance, competition context, etc.)

� Both EBITDA and Net Income increased faster than Net Sales, which may reflect good cost management

=> Examine cost structure

How the firm uses its money?

Carlsberg Case Study Preliminary AnalysisGrowth AnalysisProfitability AnalysisLiquidity risk: short and long-term ratiosSummary Note

Year 12 Year 11 Year 10 Year 9 Year 8 Year 7

Fixed Assets / Total Assets 86,3% 87,3% 88,9% 88,7% 86,5% 75,6%

Inventory / Total Assets 2,9% 2,9% 2,9% 2,7% 3,7% 6,2%

Accounts Receivable / Total Assets 5,1% 5,3% 3,9% 4,4% 4,4% 10,4%

� Asset structure: the weight of fixed assets significantly increased in 2008. Since that date, asset structure is quite stable

Accounts Receivable / Total Assets 5,1% 5,3% 3,9% 4,4% 4,4% 10,4%

Cash & Equivalent / Total Assets 3,7% 2,1% 1,9% 2,0% 2,0% 3,7%

Fixed Assets 17 799 17 276 17 191 15 984 16 619 6 201

Operating Working Capital -1 183 -1 213 -1 352 -1 234 -571 -92

Capital Employed 16 616 16 064 15 838 14 750 16 049 6 110

� Fixed Assets almost tripled in 2008 but remained stable over the past 4 years

Fahmi Ben Abdelkader © Financial Statement Analysis5/7/2016 6:26 PM 14

� Fixed Assets almost tripled in 2008 but remained stable over the past 4 years

=> Substantial investments in 2008 (check investments from 2009 to 2012?)

� Working Capital is negative over the period, which is likely to free up cash for the firm

=> Need to explain this downward trend: receivables? Payables? Sales? Cash Cycle?

=> Profitability of these investments ?

The working capital needs are negative which is contrary to what we expected given the industrial activity

=> the firm has no need to carry cash

Where does the money come from?

Carlsberg Case Study Preliminary AnalysisGrowth AnalysisProfitability AnalysisLiquidity risk: short and long-term ratiosSummary Note

Year 12 Year 11 Year 10 Year 9 Year 8 Year 7

Financial Leverage 68,4% 67,4% 69,8% 85,0% 99,6% 128,6%

Debt-to-capital ratio 40,6% 40,2% 41,1% 46,0% 49,9% 56,3%

Long-term debt / Total Liabilities 65,7% 65,1% 63,5% 66,7% 69,1% 58,3%

� Financial Leverage sharply decreased from 128% in 2007 to 68% in 2012

Long-term debt / Total Liabilities 65,7% 65,1% 63,5% 66,7% 69,1% 58,3%

Short-term debt / Total Liabilities 4,2% 2,5% 5,3% 4,4% 6,3% 9,4%

Accounts payable / Total Liabilities 30,1% 32,4% 31,2% 28,9% 24,6% 32,3%

Shareholders' Equity 9 869 9 598 9 330 7 972 8 141 2 672

Net Financial Debt 6 747 6 465 6 508 6 779 8 109 3 437

Invested Capital 16 616 16 064 15 838 14 750 16 249 6 110

=> This decrease is mainly the result of a constant rise in Equity, and less a debt pay-down policy

Fahmi Ben Abdelkader © Financial Statement Analysis5/7/2016 6:26 PM 15

� Investments in 2008 were funded both by Debt and Equity, which significantly increased capital invested in the firm

=> Despite a net decline in debt in 2009, the level of net debt remained stable over the past 4 years

=> Need to investigate the cost of debt and its impact on net income

Analysis of the Cash Cycle

Carlsberg Case Study Preliminary AnalysisGrowth AnalysisProfitability AnalysisLiquidity risk: short and long-term ratiosSummary Note

Working Capital Needs in days’ worth of sales

Year 12 Year 11 Year 10 Year 9 Year 8 Year 7

Inventory days 25 25 25 22 32 31

+ Receivable days 59 61 49 48 60 48+ Receivable days 59 61 49 48 60 48

- Payable Days 131 134 126 118 112 72

= Operating Working Capital days worth of sales -48 -48 -52 -47 -20 7

� Working Capital Days moved from positive to negative in 2008, and registered a notable decrease over the period

� Successful policy of rationalization of required working capital?

=> The company improved its capacity to convert inventories to account receivables

=> This decrease allowed the company to free-up cash

Fahmi Ben Abdelkader © Financial Statement Analysis5/7/2016 6:26 PM 16

=> However, we should notice the substantial increase in payable days.

=> Need to dig deeper to understand how Carlsberg can afford to wait more than 4 months before paying suppliers

=> Are these credit terms negotiated or are they the result of an out of control situation?

=> The company improved its capacity to convert inventories to account receivables

The decrease in WC is less the result of a better management of inventory and receivable but more related to the stretching of payable

Analysis of the Cash Cycle

Carlsberg Case Study Preliminary AnalysisGrowth AnalysisProfitability AnalysisLiquidity risk: short and long-term ratiosSummary Note

Year 12 Year 11 Year 10 Year 9 Year 8 Year 7

Year 12 Year 11 Year 10 Year 9 Year 8 Year 7

Operating Working Capital -1 183 -1 213 -1 352 -1 234 -571 -92

Year 12 Year 11 Year 10 Year 9 Year 8 Year 7

Cash From Operating Activities (I) 1 323 1 181 1 477 1 827 1 047 648

Cash From Investing Activities (II) -533 -654 -783 -413 -7 659 -660

Free Cash Flow (I+II) 790 527 694 1 414 -6 612 -12

� Except 2007 and 2008, FCF is positive

=> Carlsberg generated enough cash from operations to cover investment needs

=> Negative FCF in 2008 is mainly due to heavy investments

Fahmi Ben Abdelkader © Financial Statement Analysis5/7/2016 6:26 PM 17

� Working Capital rationalization was extremely profitable by improving the cash flows of Carlsberg

=> Substantial cash savings (in 2012, cash generated thanks to WC represents almost 90% of operating cash flow)

=> Positive cash from operations

=> Thanks to Working Capital rationalization from 2009 to 2012, investments were entirely covered by cash from operations

Margin analysis (Common-size analysis - income state ment)

Carlsberg Case Study Preliminary AnalysisGrowth AnalysisProfitability AnalysisLiquidity risk: short and long-term ratiosSummary Note

Profit & expenses % of Net Revenue Year 12 Year 11 Year 10 Year 9 Year 8 Year 7

Net Revenue 100% 100% 100% 100% 100% 100%

Cost of sales 50% 50% 48% 51% 52% 50%

Gross Margin 50% 50% 52% 49% 48% 50%

Operating expenses 29% 29% 28% 28% 31% 33%Operating expenses 29% 29% 28% 28% 31% 33%

EBITDA Margin or Operating Margin 21% 21% 23% 21% 17% 17%

Depreciation & amortization 6% 6% 7% 6% 6% 6%

EBIT Margin 15% 15% 17% 15% 11% 11%

Net financial expenses 3% 3% 4% 5% 6% 3%

Pretax Income 12% 12% 13% 10% 5% 8%

- Corporate income tax 3% 3% 3% 3% -1% 2%

Net Profit Margin 9% 9% 10% 7% 5% 6%

NOPAT (Net Operating Profit After Tax) 11% 11% 13% 11% 12% 8%

Fahmi Ben Abdelkader © Financial Statement Analysis5/7/2016 6:26 PM 18

� The weight of cost of sales is relatively stable over the period, the weight of operating expenses has decreased

=> Net sales and cost of sales have increased at the same pace: a good cost management

� Operating margin registered an interesting increase after 2008

=> Thanks to a better control of operating expenses

=> Investments made in 2008 seem to be profitable

Margin analysis (Common-size analysis - income state ment)

Carlsberg Case Study Preliminary AnalysisGrowth AnalysisProfitability AnalysisLiquidity risk: short and long-term ratiosSummary Note

Profit & expenses % of Net Revenue Year 12 Year 11 Year 10 Year 9 Year 8 Year 7

Net Revenue 100% 100% 100% 100% 100% 100%

Cost of sales 50% 50% 48% 51% 52% 50%

Gross Margin 50% 50% 52% 49% 48% 50%

Operating expenses 29% 29% 28% 28% 31% 33%Operating expenses 29% 29% 28% 28% 31% 33%

EBITDA Margin or Operating Margin 21% 21% 23% 21% 17% 17%

Depreciation & amortization 6% 6% 7% 6% 6% 6%

EBIT Margin 15% 15% 17% 15% 11% 11%

Net financial expenses 3% 3% 4% 5% 6% 3%

Pretax Income 12% 12% 13% 10% 5% 8%

- Corporate income tax 3% 3% 3% 3% -1% 2%

Net Profit Margin 9% 9% 10% 7% 5% 6%

NOPAT (Net Operating Profit After Tax) 11% 11% 13% 11% 12% 8%

Fahmi Ben Abdelkader © Financial Statement Analysis5/7/2016 6:26 PM 19

� Net profit margin doubled from 2008 to 2010

=> The improvement of the operating margin

=> The continuous reduction in the proportion of net financial expenses

Return analysis

Carlsberg Case Study Preliminary AnalysisGrowth AnalysisProfitability AnalysisLiquidity risk: short and long-term ratiosSummary Note

Year 12 Year 11 Year 10 Year 9 Year 8 Year 7

NOPAT (Net Operating Profit After Tax) 11% 11% 13% 11% 12% 8%

ROIC (Return On Invested Capital)

* Turnover rate of Capital employed 54% 53% 51% 54% 50% 98%

= ROIC (Return On Invested Capital) 6,1% 6,0% 6,4% 5,8% 5,9% 7,6%

� ROIC was quite stable over the period (around 6%)

=> The increase in NOPAT in 2008 was not sufficient to offset the sharp decline in asset turnover

=> Despite a slight improvement in asset turnover during the three past years, its level remains significantly lower than the highest level reached in 2007

Fahmi Ben Abdelkader © Financial Statement Analysis5/7/2016 6:26 PM 20

significantly lower than the highest level reached in 2007

=> The huge amount of investments in 2008 has weighed heavily on the operating performance

Carlsberg Case Study Preliminary AnalysisGrowth AnalysisProfitability AnalysisLiquidity risk: short and long-term ratiosSummary Note

Analyzing ROIC: Economic Value Added

Return on invested capital for Carlsberg Versus WAC C

8,0%

2,0%

3,0%

4,0%

5,0%

6,0%

7,0% WACC=7%

Fahmi Ben Abdelkader © Financial Statement Analysis5/7/2016 6:26 PM 21

Carlsberg is only creating value for its shareholders and lenders in 2007

0,0%

1,0%

2005 2006 2007 2008 2009 2010 2011 2012

Carlsberg Case Study Preliminary AnalysisGrowth AnalysisProfitability AnalysisLiquidity risk: short and long-term ratiosSummary Note

Analyzing ROIC: Economic Value Added

Return on invested capital for Carlsberg and Heinek en

20,0%

ROIC Carlsberg

6,0%

8,0%

10,0%

12,0%

14,0%

16,0%

18,0%ROIC Carlsberg

ROIC Heineken

Fahmi Ben Abdelkader © Financial Statement Analysis5/7/2016 6:26 PM 22

Carlsberg is only able to generate a ROIC that exceeds Heineken’s in 2008

Carlsberg’s level of profitability is generally below Heineken’s in the period examined

0,0%

2,0%

4,0%

2005 2006 2007 2008 2009 2010 2011 2012

Carlsberg Case Study Preliminary AnalysisGrowth AnalysisProfitability AnalysisLiquidity risk: short and long-term ratiosSummary Note

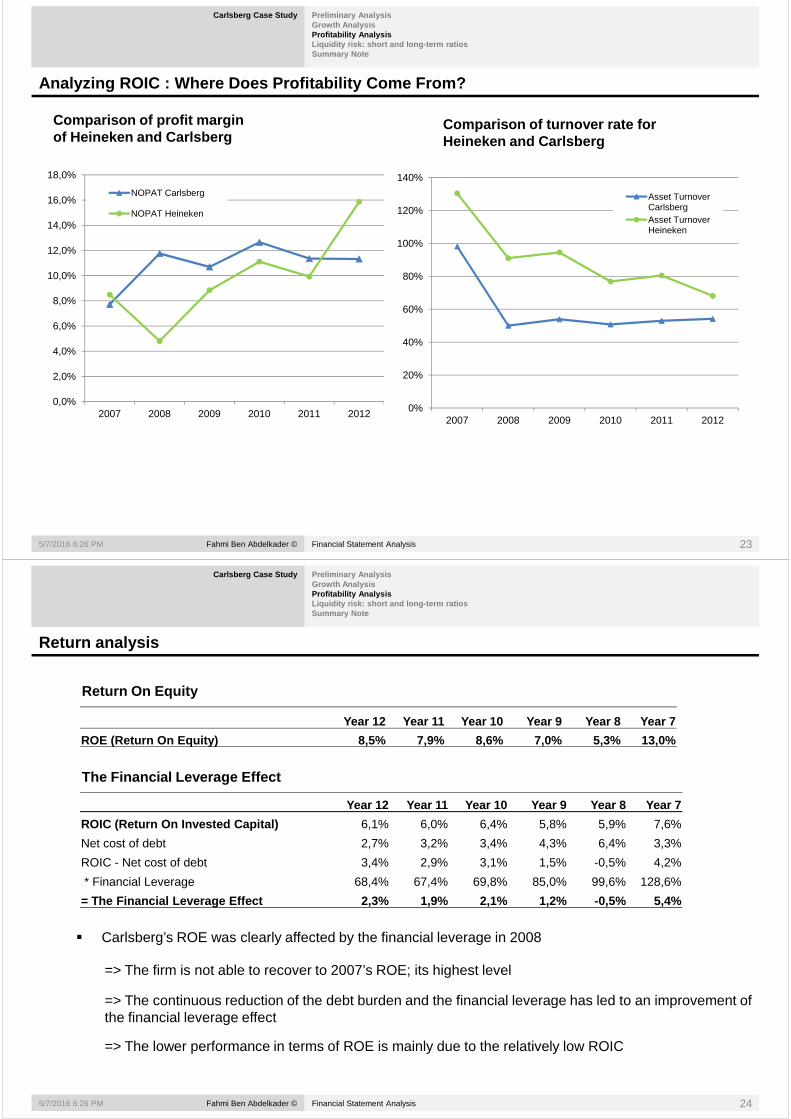

Analyzing ROIC : Where Does Profitability Come From ?

Comparison of profit margin of Heineken and Carlsberg

Comparison of turnover rate for Heineken and Carlsberg

18,0%

NOPAT Carlsberg

140%

4,0%

6,0%

8,0%

10,0%

12,0%

14,0%

16,0%NOPAT Carlsberg

NOPAT Heineken

20%

40%

60%

80%

100%

120%Asset Turnover CarlsbergAsset Turnover Heineken

Fahmi Ben Abdelkader © Financial Statement Analysis5/7/2016 6:26 PM 23

0,0%

2,0%

2007 2008 2009 2010 2011 2012 0%

20%

2007 2008 2009 2010 2011 2012

Return analysis

Carlsberg Case Study Preliminary AnalysisGrowth AnalysisProfitability AnalysisLiquidity risk: short and long-term ratiosSummary Note

Year 12 Year 11 Year 10 Year 9 Year 8 Year 7

ROE (Return On Equity) 8,5% 7,9% 8,6% 7,0% 5,3% 13,0%

Return On Equity

Year 12 Year 11 Year 10 Year 9 Year 8 Year 7

ROIC (Return On Invested Capital) 6,1% 6,0% 6,4% 5,8% 5,9% 7,6%

Net cost of debt 2,7% 3,2% 3,4% 4,3% 6,4% 3,3%

ROIC - Net cost of debt 3,4% 2,9% 3,1% 1,5% -0,5% 4,2%

* Financial Leverage 68,4% 67,4% 69,8% 85,0% 99,6% 128,6%

= The Financial Leverage Effect 2,3% 1,9% 2,1% 1,2% -0,5 % 5,4%

The Financial Leverage Effect

� Carlsberg’s ROE was clearly affected by the financial leverage in 2008

Fahmi Ben Abdelkader © Financial Statement Analysis5/7/2016 6:26 PM 24

� Carlsberg’s ROE was clearly affected by the financial leverage in 2008

=> The firm is not able to recover to 2007’s ROE; its highest level

=> The continuous reduction of the debt burden and the financial leverage has led to an improvement of the financial leverage effect

=> The lower performance in terms of ROE is mainly due to the relatively low ROIC

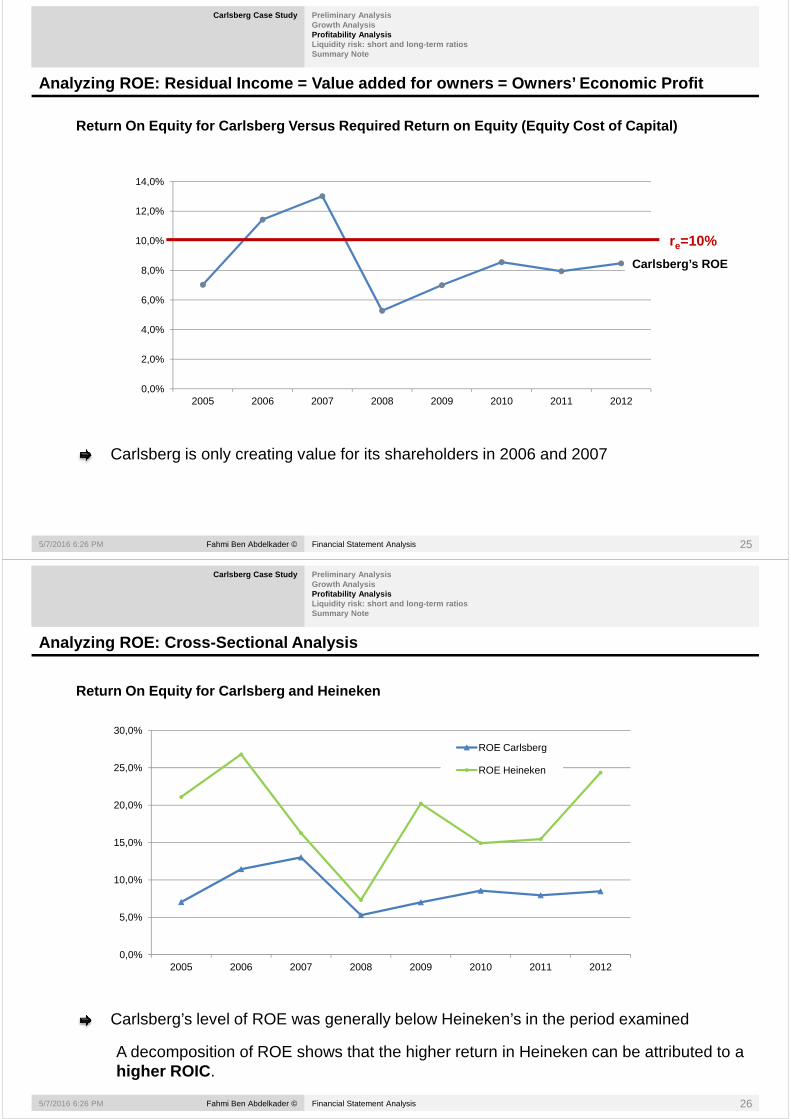

Analyzing ROE: Residual Income = Value added for ow ners = Owners’ Economic Profit

Carlsberg Case Study Preliminary AnalysisGrowth AnalysisProfitability AnalysisLiquidity risk: short and long-term ratiosSummary Note

Return On Equity for Carlsberg Versus Required Retu rn on Equity (Equity Cost of Capital)

14,0%

re=10%

2,0%

4,0%

6,0%

8,0%

10,0%

12,0%

Carlsberg’s ROE

Fahmi Ben Abdelkader © Financial Statement Analysis5/7/2016 6:26 PM 25

Carlsberg is only creating value for its shareholders in 2006 and 2007

0,0%2005 2006 2007 2008 2009 2010 2011 2012

Analyzing ROE: Cross-Sectional Analysis

Carlsberg Case Study Preliminary AnalysisGrowth AnalysisProfitability AnalysisLiquidity risk: short and long-term ratiosSummary Note

Return On Equity for Carlsberg and Heineken

30,0%

ROE Carlsberg

5,0%

10,0%

15,0%

20,0%

25,0%

ROE Carlsberg

ROE Heineken

Fahmi Ben Abdelkader © Financial Statement Analysis5/7/2016 6:26 PM 26

Carlsberg’s level of ROE was generally below Heineken’s in the period examined

A decomposition of ROE shows that the higher return in Heineken can be attributed to a higher ROIC .

0,0%2005 2006 2007 2008 2009 2010 2011 2012

Illiquidity risk: short and long-term ratios

Carlsberg Case Study Preliminary AnalysisGrowth AnalysisProfitability AnalysisLiquidity risk: short and long-term ratiosSummary Note

Short-term liquidity ratios

Year 12 Year 11 Year 10 Year 9 Year 8 Year 7

Current ratio 77% 71% 59% 61% 74% 87%Current ratio 77% 71% 59% 61% 74% 87%Quick ratio 60% 54% 43% 46% 54% 65%Cash ratio 21% 54% 43% 46% 54% 65%

Cash flow from operations to short-term debt ratio 36% 33% 40% 55% 30% 28%

� Short term liquidity ratios show that the firm’s current assets are not able to cover current liabilities

=> The sharp decline in cash ratio could be cause of concern. Need to investigate the reasons of this brutal drop

=> CFO to short-term debt ratio registered also a significant decrease compared to its level in 2009

Fahmi Ben Abdelkader © Financial Statement Analysis5/7/2016 6:26 PM 27

=> CFO to short-term debt ratio registered also a significant decrease compared to its level in 2009

Illiquidity risk: short and long-term ratios

Carlsberg Case Study Preliminary AnalysisGrowth AnalysisProfitability AnalysisLiquidity risk: short and long-term ratiosSummary Note

Long-term liquidity risk

Year 12 Year 11 Year 10 Year 9 Year 8 Year 7Long-term debt / Total Liabilities 65,7% 65,1% 63,5% 66,7% 69,1% 58,3%Short-term debt / Total Liabilities 4,2% 2,5% 5,3% 4,4% 6,3% 9,4%Short-term debt / Total Liabilities 4,2% 2,5% 5,3% 4,4% 6,3% 9,4%Financial Leverage 68,4% 67,4% 69,8% 85,0% 99,6% 128,6%Solvency ratio 47,8% 48,5% 48,3% 44,2% 42,0% 32,6%Interest Coverage ratio 5,57 4,73 4,64 2,91 1,83 4,03Interest Coverage ratio (Cash) 5,57 4,37 5,11 4,56 2,26 4,03Debt to EBITDA 3,62 3,62 3,47 4,06 6,07 3,33Debt to Cash flow from operations ratio 5,10 5,47 4,41 3,71 7,75 5,30

� Financial Leverage sharply decreased from 128% in 2007 to 68% in 2012

=> This decrease is mainly the result of a constant rise in Equity, and less a debt pay-down policy

Fahmi Ben Abdelkader © Financial Statement Analysis5/7/2016 6:26 PM 28

� Interest Coverage ratios registered a substantial improvement over the period

=> This decrease is mainly the result of a constant decrease in net financial expenses

� Debt to EBITDA ratio has also registered a positive evolution

=> however, we should notice the stagnation of this ratio over the past 2 years, the debt stopped decreasing !

Summary Notes: the strengths and weaknesses

Carlsberg Case Study Preliminary AnalysisGrowth AnalysisProfitability AnalysisLiquidity risk: short and long-term ratiosSummary Note

The strengths

Net sales are growing faster than costs: good management of operating costs leading to a positive evolution of operating margin

The weaknesses

Successful policy of rationalization of required working capital: substantial cash savings

Thanks to Working Capital rationalization over the past 4 years, investments have been entirely covered by cash from operations: money generated thanks to the core business activities

evolution of operating margin

Net Assets are growing faster than net sales: heavy investments have considerably affected asset turnover

Fahmi Ben Abdelkader © Financial Statement Analysis5/7/2016 6:26 PM 29

Recommendations

The significant increase in payables could be cause of concern: perhaps indicating the firm is becoming a bad payer ?!

Need to assess the quality of investments (i.e. assets)

ROIC is not high enough to compensate for lower asset turnover

Operating performance is not sufficient to create value for shareholders