feasibility report on acceptance of the marss rrbf · 2016-07-11 · marss– feasibility report 4...

TRANSCRIPT

PROJECT LIFE + ENV/DE/343

Action A2: Stakeholder consultancy and EU dimension

Del 9. Feasibility Report on acceptance of the MARSS RRBF

A multi-country stakeholder consultancy report looking at the chosen test cases of Germany, Italy, Greece, Czech Republic, the UK and Serbia

For more information, please visit: www.marss.rwth-aachen.de

Material advanced recovery SuStainable SySteMS

Feasibility RepoRt on acceptance oF the MaRss RRbF

A multi-country stakeholder consultancy report looking at the chosen test cases of Germany, Italy, the UK,

Greece, Czech Republic, and Serbia

this report was written and compiled in the frame of the MaRss project by c. hornsby, with significant

contributions from the country partners and experts named below who carried out the local actions and

assisted the MaRss project in this multi-cultural stakeholder consultancy action. please contact her if you

would like more information at [email protected].

We would like to thank in particular:

Germany

prof. Dr. i. Romey (WbF Gmbh); Mr M balhar (branch Manager- a.s.a. e.V.); Mr t. schulzke (UMsicht,

Fraunhofer institute); Dr. M. Monzel (Regent Gmbh); Mr h. Kugel (Regent Gmbh)

Italy

Dr. G. Fiorentino; Dr. M. Ripa; Ms c. Vassillo; prof. Dr. s. Ulgiati, (University of parthenope naples) as well as

Dr V. cigiolotti (enea); prof. Dr. M. Giampietro (Uab); Ms R. chifari (Uab); Mrs s. bukkens (Uab)

Greece

Mr J. Mardikis (envireco); prof. Dr. M. loizidou (national University of athens); Dr. K. Moustakas (national

University of athens)

Czech Republic

assistant prof. Dr. l. benesova (charles University of prague); ing. anna cidlinová (the national institute of

public health & centre for health and the environment in prague)

UK

Dr. n. head (northampton University); prof. Dr. M. bates (northampton University); Dr. c. coggins (Wamtech)

Serbia

prof. G. Vujic (University of novi sad, president of sesWa); F. J. popović ( Department for Municipal Waste

Management, belgrade); J. V. Filipović, and V. n. božanić (University of belgrade, Faculty of organizational

sciences, belgrade)

For public release

eU life plus MaRss project coordinator:

Department of processing and Recycling (i.a.R.). RWth-aachen University

project website: www.marss.rwth-aachen.de

3

The MARSS (Material Advanced Recovery Sustainable Systems) project was successful in re-

ceiving part-funding from the European Commission under the 2011 Life Plus Programme.

This demonstration project has developed an innovative process for the production of organic

biomass fuel derived from mixed rubbish from households (known as mixed Municipal Solid

Waste) in the area around Trier in Germany.

RegEnt GmbH is co-developing an innovative process (known as MARSS) for the production

of organic fuels, derived from mixed rubbish, with 4 other European partners. This EU Life plus

co-funded project is taking place on the premises of Entsorgungs- und Verwertungszentrums

(EVZ) in Mertesdorf, Germany. Additional project partners are RWTH Aachen University (acting

as Coordinator), pbo GmbH, as well as the Universitá degli Studi di Napoli and the Universitat

Autónoma de Barcelona.

All EU Life Plus funded projects are selected on the basis that they can prove to provide ben-

efits to the environment. The MARSS project has identified various direct and indirect potential

benefits to the environment:

Reduction of harmful GHG emissions

Reducing biological municipal waste going to landfill

Reducing landfilling of valuable metals and other materials suitable for recycling

Local production of electricity and heat from household waste as well as increasing

renewable energy potential for urban communities.

Prevention of soil and ground water contamination from landfill sites

This demonstration project is partly funded by the EU Life Plus Programme.

Project duration: 09.2012–12.2015

Project budget: 4,154,933 €

EU contribution: 2,073,727 €

Project location: EVZ Mertesdorf, Rheinland-Pfalz, Germany

Contact: [email protected]

Web Site: www.marss.rwth-aachen.de

MaRss– Feasibility Report

4

Developing carbon neutral technologies and making better and more rational use of energy and

other natural resources have become essential for sustainable development of our society. An

appropriate response to the gravity of climate change has been the revised targets supporting

the move away from fossil fuels to a more sustainable basis for energy production and manage-

ment of waste. The EU framework on climate and energy for 2030 proposed by the European

Commission in January 2014 presents targets that are more ambitious and aims at reducing

greenhouse gas emissions by 40% and increase the use of renewables to at least 27% by 2030.

The MARSS project is one such attempt to provide a technology that helps to remove and stabi-

lise the biogenic fraction of MSW from being landfilled, so reducing greenhouse gas emissions

and providing a renewable biomass fuel for heat and power production. This report has been

produced in the frame of the EU funded MARSS project and is intended to provide an overview

of the results of the stakeholder consultancies carried out in the six countries studies. Common

stakeholder questionnaires and a methodology were devised and set up for use in the consul-

tancy work by all experts and project partners.

The MARSS concept to demonstrate the effective separation of organic material from mixed

municipal solid waste was not intended as a solution for Germany. Rather it was intended for

those EU (and candidate countries) that are having problems fulfilling the various relevant EU

Directives, in particular the Landfill Directive [1]. Waste in one location is not the same as in

another and it constantly changes over time and with different ways of dealing with it depend-

ing on the local history, culture and level of development. Only a few countries can be said

to have a “grip” on waste in terms of reaching the targets set by different pieces of European

legislation, but even these more advanced countries (such as Germany) also acknowledge that

some decisions made in the past were not really sustainable or ecologically friendly, and maybe

would have not been taken in exactly the same form today. At the same time, Germany is

leading the field in technological development and patents also in the field of advanced waste

management and can provide valuable experience to less advance countries in their waste

management plants.

There is a pressing need to help those countries that are still relying on landfilling of waste

(including large amounts of biogenic waste) and to provide them with a tested and robust

separation technology to remove as much biomass as possible from mixed rubbish before final

disposal of the un-usable residues so aiding them in reaching the agreed targets for the land-

filling of biogenic fractions. It is also becoming increasingly clear that decisions affecting the

public domain, such as in waste management, can no longer be taken without embracing a

comprehensive stakeholder consultancy based on technical transparency, economic and social

constraints, environmental burdens and social attitudes [2].

Foreword

5

All in all, a project or proposal might be technically feasible and environmentally sound, but

might not be accepted by stakeholders for a set of reasons that have nothing to do with techni-

calities or environmental constraints. Stakeholders might have a set of convictions and values

that sets them in conflict with the proposed interventions.

The countries were chosen as they represent radically different levels of development in solid

waste management, and many have chosen or are considering different routes and methods to

deal with household rubbish. We also report on the in-depth study of Naples having recently

emerged from what is locally called the “waste emergency” where there were open heated con-

flicts between the waste managers and the general public.

Other countries, represented by their municipalities who often make the final waste manage-

ment decisions, are trying to benefit from lessons learnt, both good and bad, also finding that it

is not easy or possible to simply transfer one basket of technologies or strategies per se to other

countries due to differences in local problems, lack of funds, political preferences and popula-

tion perceptions/conflicts at the local and regional levels.

This report puts together the main findings from work carried out in the stakeholder consultan-

cies in the different countries in the frame of the Life Plus funded MARSS Project.

For more information, please contact the Coordinator at [email protected] or visit the

website at www.marss.rwth-aachen.de

MaRss – Feasibility Report

6

Foreword . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4

Contents page . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6

Executive summary . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8Background to project. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8Country Studies key results. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8Outlook for MARSS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10

Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12

Methodology . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14

Country Studies . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15Use of MBT technology . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16Outlook. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18

UK . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18Country highlights . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18Energy Management. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21UK Questionnaires results . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21Outlook. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24

Italy . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24The case of Naples . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24Municipal waste management system . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 28Identification of stakeholder groups . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 29Selection of results from the stakeholder consultancy . . . . . . . . . . . . . . . . . . . . . 29Outlook. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 32

Greece. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 33Waste management contracts in Greece . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 33Stakeholder consultancy. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 33Profile summary of Municipal Solid Waste Management in Greece . . . . . . . . . . . 34Demand & Perception of Biomass fuels in Greece . . . . . . . . . . . . . . . . . . . . . . . . 36Exploitation of biomass fuel in Greece . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 36Main barriers to market development in Greece . . . . . . . . . . . . . . . . . . . . . . . . . . 37Greek Questionnaire Analysis. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 38MBT capacity . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 38Fluidized bed combustion in Greece . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 39Outlook. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 40

Czech Republic . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 40Waste management in Czech Republic . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 40Stakeholder consultancy. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 42Outlook. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 44

MaRss – Feasibility Report

Contents page

7

Serbia . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 45Waste management in Serbia . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 46Major barriers in Serbia . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 47Outlook. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 48

Conclusion . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 49A note of thanks. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 51

Notes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 52

References . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 54References used in introduction and conclusion . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 54References used in the German study . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 55References used in the UK study . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 55References for Greek country study . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 56References for Czech Study. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 57References for Serbia Study . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 57

List of Acronyms . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 59

MaRss – Feasibility Report

8

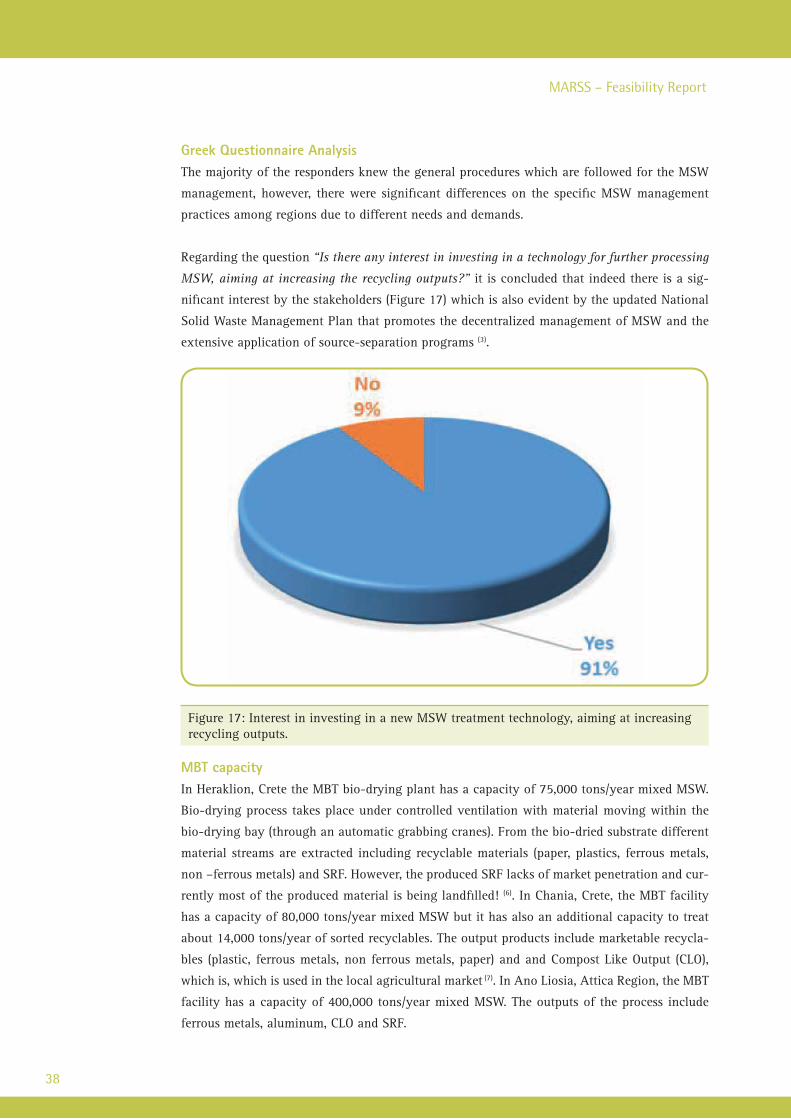

The aim of this report is to illustrate the main results of the stakeholder consultation on the ac-

ceptability and the market potential effectiveness of MARSS technology and its final produced

material in chosen countries. This report is part of the Action A2.Stakeholder consultancy and

EU dimension of the EU LIFE+ project entitled Material Advanced Recovery Sustainable System

(MARSS).

Background to projectThe main aim of the MARSS project is to provide demonstration of an innovative solid waste

separation and biogenic stabilization system to add to a basket of options for waste manage-

ment to those countries currently not able to fulfill the Landfill Directive. This was not a

solution envisaged for Germany, as Germany already fulfills the Landfill Act and has an estab-

lished waste management structure throughout the country; and has also set in place separate

collection of bio waste from households with one exception of Rhineland Palatinate where

the MARSS plant is situated. There are specific requirements for licensing of industrial CHP

biomass plants who wish to use a waste derived RRBF fuel with significant extra costs which

also limits the uptake by CHP plants for the MARSS renewable fuel. Having said that, a special

exception has been granted to A.R.T., serving Trier and the surroundings in Rhineland Palati-

nate, to continue to operate the RegEnt MBT plant, and not to immediately adopt and enforce

separate collection of bio-waste from the households. This decision was probably taken on the

basis of the continuing success of the MBT plant for dealing with the regions’ mixed MSW, as

well as the publicity given to the MARSS plant.

Country Studies key resultsSix countries were chosen for a cross-cultural stakeholder consultancy within the time of the

MARSS project in order to try to understand the potential for replication of MARSS technol-

ogy in these countries and also to understand exactly what the barriers or opportunities are for

possible future uptake of this technology. The six countries were chosen for study due to their

different histories and country profiles, namely Germany, UK, Italy, Greece, Czech Republic and

Serbia. This report is not an in-depth study of these questions but presents the results of the

surveys carried out by chosen experts in these countries with a specific mandate to look at the

acceptability of MARSS.

Executive summary

9

| executive summary

The country studies have shown that

It is simply not easy to transpose one successfully demonstrated technology from one

country to another. The acceptability and chances for successful implementation rely on

a multiplicity of complex factors such as political climate, investment opportunities, and

state of play in the waste management systems already in place, level of infrastructures,

attitudes towards incineration/combustion, and markets for fuels.

Acceptance and uptake of the MARSS technology depends specifically on the national

regulations in force in that country, and severe restrictions are in place preventing CHP

plant operators from switching easily from one specific biomass fuel feedstock to one

coming from mixed household waste. In fact, some of the countries do not allow or au-

thorize a MARSS type product to be used or accredited for use as a biomass feedstock

for the production of renewable energy; whereas others do allow this. There is a need for

standardization and norms on a pan-European level in consultation with such bodies as

the European Committee for Standardisation (CEN)1.

Acceptance of the MARSS technology also depends on the availability of the basis tech-

nology of MBT as it is an add-on module, as well as the presence eventually of biomass

CHP units that would use the MARSS RRBF to make combined heat and power locally,

as well as improving the economics of the whole process by claiming some form of car-

bon reduction credits – the exact form of these credits depends on the national schemes

present in those countries. For example, the tariff system related to energy production (€/

MWh) from MSW biomass in Greece is still vague compared to alternative biomass feed-

stock (i.e. agricultural biomass). This is different in the UK where from 5 October 2015 all

participants generating heat (or heat and power) from biomass must comply with sustain-

ability requirements however waste or fuel wholly derived from waste is considered to

meet the sustainability requirements.

Some countries are positively encouraging ventures that produce renewable heat and

power from biomass such as the UK – for example making them exempt from the Climate

Change Levy Tax; and under the Renewables Obligation (RO) licensed electricity suppli-

ers are required to source a percentage of the electricity supplied from eligible renewable

sources, including both dedicated and co-fired biomass.

Acceptance by the main stakeholder groups, which includes the general public in those

communities, is also a very important factor, and our work has indicated that it is essen-

tial to start the consultancy actions before any decision is taken on which technology to

employ in that community.

The results of the questionnaires to the general public indicate that there is a high level or

even an over-enthusiasm about the MARSS technology being able to solve the problems

of their national/local MSW waste management; and also a willingness to pay more for

waste management, but only if it really brings benefits to the environment and reduces

health hazards to families. This finding was present in all the country studies.

1 European Committee for Standardisation, https://www.cen.eu/about/RoleEurope/Pages/default.aspx

MaRss – Feasibility Report

10

Cement industries in both Greece and Czech Republic voiced a real interest in the MARSS

RRBF in their operating processes in the case the final product complies with the national

and industrial requirements and it is financially beneficial.

Some country studies, such as in Greece, saw limitations in the uptake of MARSS technol-

ogy to use the RRBF fuel in spite of the fact that biomass (in different products) is being

used as a source for heat and power production, so that this technology based on biomass

is already accepted and used. However, due to the limitations of the MBT operations and

use of RDF/SRDs, the operation of thermal treatment plans for the energy recovery of

MSW sourced biomass fuel is not expected, at least in the near future, to be part of the

MSW management practices in Greece.

Currently in Greece there aren’t any thermal treatment units installed for the energy re-

covery of MSW biomass fuel. Additionally, the relevant policy framework as specified in

the new National Solid Waste Management Plan states that thermal energy recovery of

secondary solid fuels such as combustion, pyrolysis, gasification, etc. are considered as

high environmental impact methods and on the basis of the precautionary principle pro-

cesses they are considered as unsuitable for the treatment of MSW.

Differences came about in attitudes to incineration/combustion technologies, where the

highest resistance was found in Italy and the lowest in Czech Republic – however this

should be verified by further surveys and analysis work.

The problem of availability of finance for investment in new technologies such as MARSS

was a problem in all the countries studies, including Germany; it is forecasted that no

more MBT plants will be built in Germany (currently 48 plants) due to the small profit

margins for operators. But this should be seen against the backdrop that MBT technology

itself is on the increase in Europe as a whole as it does provide a robust sorting technol-

ogy for other countries. Italy leads the field world-wide with the greatest number of MBT

plants and there are none in the Czech Republic to date. So the differences are significant

across Europe in the solutions that local authorities chose to deal with their waste.

An interest was shown in the transfer of Best Available Practices (BAPs) by the countries

under study, and to extend the collaboration to exchange information and “lessons learnt”.

Outlook for MARSSAlthough the MARSS technology itself has been judged as a viable add-on modular technol-

ogy to MBT plants, the best chances for commercialization seems to be in those member states

which are still in the process of building up their waste management system supported by

national legislation that allows the use of waste recovered biomass fuels such as MARSS in

their tariff and benefits schemes, as well as providing some financial incentives for uptake of

new technologies, as is the case in the UK. There is also a keen interest in the MARSS technol-

ogy in Naples, and results have been presented to the Municipality for further consideration.

11

| executive summary

Consultation work must be carried out with CEN2 who works in technical cooperation with the

International Standards Organisation; certification of the MARSS RRBF will open up new busi-

ness and market opportunities, and without this accreditation, the RRBF product has very little

chances to stand alone as a biomass CHP feedstock.

The most economical way to install MARSS technology seems to be to combine the MBT plus

MARSS modules with an on-site CHP plant for heat and energy production, so reducing trans-

portation costs and maximizing the already needed environmental impact cleaning systems on

one site. The heat and power can be used on site or distributed via a heat and power distribution

gris to local communities. However a positive financial balance can be improved when there

are incentive schemes for waste sourced biomass produced heat and power offered at national

level for example to reduce tax or provide a feed-in tariff or incentive to use renewable heat

and power, such as in the UK.

Further analyses work should be carried out to investigate the potential of MARSS, not only as

an advanced sorting system to produce a biomass rich fuel which after combustion in a fluid-

ized bed combuster, acts as a concentrator phosphorus in the cyclone ash. This is of real interest

for future businesses, to recycle phosphorus to be used as a fertilizer. In addition, it might be

the MARSS technology could be adapted for use as one of the Urban Mining tools, to recover

and sort out metals, plastics and organic fractions from old landfills.

2 European Standardization plays an important role in the development and consolidation of the European Single Market.

The fact that each European Standard is recognized across the whole of Europe, and automatically becomes the national

standard in 33 European countries, makes it much easier for businesses to sell their goods or services to customers throug-

hout the European Single Market.

MaRss – Feasibility Report

12

Stakeholder concerns are growing in the area or waste management about the increasing de-

mands for valuable resources by society, and the poor way in which decision-makers have been

dealing with waste and recycling. It is clear that the times of what seemed to be abundant and

cheap natural resources is coming to an end with the growing needs of an ever increasing glob-

al population combined with concerns about the security of supply of many essential materials

and products. Often decisions are made to introduce what may be good technically-speaking

new developments of urban waste management, hydrocarbon extraction, lands use change for

new industrial infrastructures only to find that the problems have not been solved, and conflicts

are created between civil society and decision-makers.

At the same time, there is a rise in interest in understanding the importance of involving dif-

ferent stakeholder groups in decisions about sustainable management of natural resources and

the environment linking civil society’s concerns about environmental and social impacts. Some

countries, such as Germany and the UK, are leading the field in promoting public participation

in policy and public decision making in different fields such as transport planning, environ-

mental issues, and health care and is claiming the interest of academics, practitioners, regula-

tors, and governments. In fact the UK started a call in 1998 in a White Paper [1] for enhanced

public participation and a renewal of local democracy to be embedded in local authorities deci-

sions which should reflect the wishes of the community without actually stating how this can

be achieved (e.g., Leach and Wingfield 1999) [2]

The increasing use of media and social networks certainly play a role in rallying the normal

citizen to take part in local resistance initiatives which in turn leads to greater public aware-

ness about decisions for change taken at the public authority levels. Conflict prevention and

solution requires the role of stakeholders be acknowledged and valued, as a crucial early step

to build a correct relation among all interested parties to bring about lasting decisions leading

to positive sustainable development. In line with the growing number public-voiced concerns

and demands for more transparency and greater access to environmental information, the EU

Directive 2003/4/EC3 [3] deals with these issues and provides guidance on the dissemination of

environmental information to the public; and Directive 2003/35/EC [4] endorses public partici-

pation and allows a direct expression of concerns relating to decisions affecting the environ-

ment within their local community.

3 The European Commission sets rules which ensure freedom of access to, and dissemination of, information on the envi-

ronment held by public authorities and to set out the basic terms and conditions under which such information should be

made available.

Introduction

13

| introduction

However timing is essential in this consultancy process, as Rowe et al (2005) [5] confirm, in that

it is too late when simply getting input from the public in what they call “risk arenas” such as

the decision for the siting of for example a new waste management technology or radioactive

waste facilities and not allowing public input much earlier in the discussions about the overall

suitability of the proposed strategy and approach for that local region (Rowe and Frewer 2000)

[6]. Our research investigations and results ratify the importance of involving the public at a

deep level as early as possible in the consultation process. Some EU countries such as France

have taken this one step further and enshrined the requirement for public participant in na-

tional legislation.

The role and influence of trust within the stakeholder groups is not to be under-estimated, as

is the way and means that the messages and information about the new proposal is given out.

Other surveys, including those done in the UK, have also shown that industry and government

official come very low on the trust scales (Petts 1998)4 [7] and this was endorsed by our Naples

case study results [8].

Technical transparency is considered not to be an optional requirement in this two-way com-

munication process and again great care must be taken about the content and understandability

of the messages and information given out about not only the technical innovation, its impacts

both environmental and socio--economic at both the local and regional levels, but also the

trade-offs and final beneficiaries and to avoid conflicts.

A well planned, early and well executed stakeholder consultancy based on a transparent en-

gagement strategy and information exchange can also lead to longer-term and more positive

relationships between the community members and local authority decision makers that goes

beyond the initial feasibility studies.

This cross-cultural international study has brought insights about stakeholder groupings in

that, in spite of the limitations of the questionnaires provided, it was clear that there are broad

categories of stakeholders with different opinions, regardless of their profession and role, and

these factors should be taken into account by the decision-makers. Results achieved in the case

study carried out in Naples indicate that there are significant psychological elements behind the

opinions and responses received from the different stakeholder groups.

4 Petts, J.: Barriers to participation and deliberation in risk decisions: evidence from waste management. Journal of Risk

Research, 7: 115–133 (2004)

MaRss – Feasibility Report

14

A general country analysis methodology was set up and followed in the different countries.

Focus points for the country studies were agreed with the experts. Additionally questionnaire

surveys were performed targeting the general public to illustrate people’s awareness level on

MSW management issues.

The questionnaires were designed to address three key areas: general information about the

stakeholder identity, stakeholder knowledge and perspective about waste management, and

stakeholders’ perceptions and feelings about the MARSS fuel/plant. General information about

stakeholders (gender, education, province of residence, age and job’s position) was requested

in order to establish a profile of respondents. In the general area of the survey the goal was to

understand how waste management, collection and recycling are organized locally, how stake-

holders are informed about the ways to separate and collect waste, to what extent were they

satisfied about present waste management matters in their area/region/country.

The interview guidelines and questionnaires were set up by C. Hornsby, the MARSS scientific

coordinator and with support from the partners, and agreed with the country experts who

distributed them in the country language. Web forms were put on the MARSS website for

easy access and collection of responses. Emphasis was put on face to face interviews with key

stakeholder groups and individuals. Analyses of work carried out including close attention to

the interview notes was made to ascertain the potential applicability of MARSS technology

considering the existing market conditions in the different countries.

Methodology

15

| country studies

Germany

Although Germany already fulfills the Landfill Directive and is considered one of the most ad-

vanced countries in solid waste management, the local public authority (A.R.T. with its operat-

ing company RegEnt GmbH) formed part of the original ideas task force setting up the project

proposal (known as MARSS) with RWTH Aachen University. RegEnt GmbH is co-developing

and demonstrating the innovative process (known as MARSS) for the production of refuse

renewable biomass fuels (RRBF), derived from mixed rubbish, with 4 other European partners.

This EU Life plus co-funded project is taking place on the premises of Entsorgungs- und Verw-

ertungszentrums (EVZ) in Mertesdorf, Germany. Additional project partners are of course RWTH

Aachen University (acting as Coordinator), pbo GmbH, as well as the Universitá degli Studi di

Napoli and the Universitat Autónoma de Barcelona.

This project is unique in Germany and is operated and owned by RegEnt in Mertesdorf which

houses the MARSS demonstration plant.

Germany is seen as rather leading the world in terms of effective solid waste management and

this is a result of the particular history. It is also important to understand some of the history

behind the development of the current adopted systems in Germany.

A large increase in waste volume in the 1980s, and detectable environmental damages caused

from the storage of not pre-treated urban wastes, as well as polluted leachate and the green-

house methane gas emissions, led for search of better disposal concepts. Waste experts rec-

ognised the need for pre-treatment of the waste prior to the storage in landfills besides the

requirement for a more intensified waste recovery5.

5 The road to MBT technology, ASA e. V. Arbeitsgemeinschaft Stoffspezifische Abfallbehandlung

Im Hause der Abfallwirtschaftsgesellschaft des Kreises Warendorf mbH, M. Balhar

Country Studies

MaRss – Feasibility Report

16

Use of MBT technologyGermany pretreats a total of around 25 % of urban waste using MBT technology (MBT =

Mechanical-Biological Waste Treatment). This technology is based on a material stream specific

waste treatment. It means that the material properties of residual wastes - which are varying to

a large extent - determine the selection and specification of treatment steps.

An extraordinary increase of the waste volume in the 1980s and detectable environmental

damages caused from the storage of not pre-treated urban wastes, as well as polluted leachate

and the greenhouse-effective methane gas emissions led for search of better disposal concepts.

Waste experts recognised - besides the requirement for a more intensified waste recovery - the

need for pre-treatment of the waste prior to the storage in landfills. In 1993 the Federal Council

of Germany stipulated in the Technical Instructions for Urban Waste (TASi) the pre-treatment

for biologically degradable wastes with waste incineration as the only accepted alternative op-

tion. The TASi granted the public waste disposal authorities a transitional period of 12 years

to reorganise and restructure their plants. The political stipulation on waste incineration plants

as the only technology was among experts at that time contradictorily discussed and often

couldn’t be realised and get a majority in the municipalities. The public opinion showed resist-

ance against waste incineration plants because of expectations of air pollutions (e.g. dioxins,

heavy metals).

A great many planning projects for waste incineration plants failed and country-wide planning

projects and search for sites were withdrawn. In the early 90s, a large number of landfill sites

were built due to the pressure by the Federal states on the competent local authorities to fulfil

their tasks to deal with waste fast, safe and efficiently.

Figure 1: Scientific coordinator, Kate Hornsby interviewing Mr M. Balhar, the Business Of-fice Manager of ASA (Arbeitsgemeinschaft Stoffspezifische Abfallbehandlung) which repre-sents the MBT operators in Germany

17

| country studies

The 1996 Closed Loop and Waste Management Act (“KrW-/AbfG”) underlined the new moves

towards closed loop waste management and producer responsibilities and this was compounded

by intense political discussions about which method was more suitable for pre-treatment and

final disposal of waste with a look at some new technologies (including Thermoselect etc) ,

some of which later proved not to be as useful or workable as they were claimed to be. This

led to a greater interest in one emerging technology known as Mechanical Biological waste

Treatment (MBT) where waste is generally source separated, then selected recyclables and other

fractions sorted out, and finally the biodegradable residues are stabilized or biologically treated

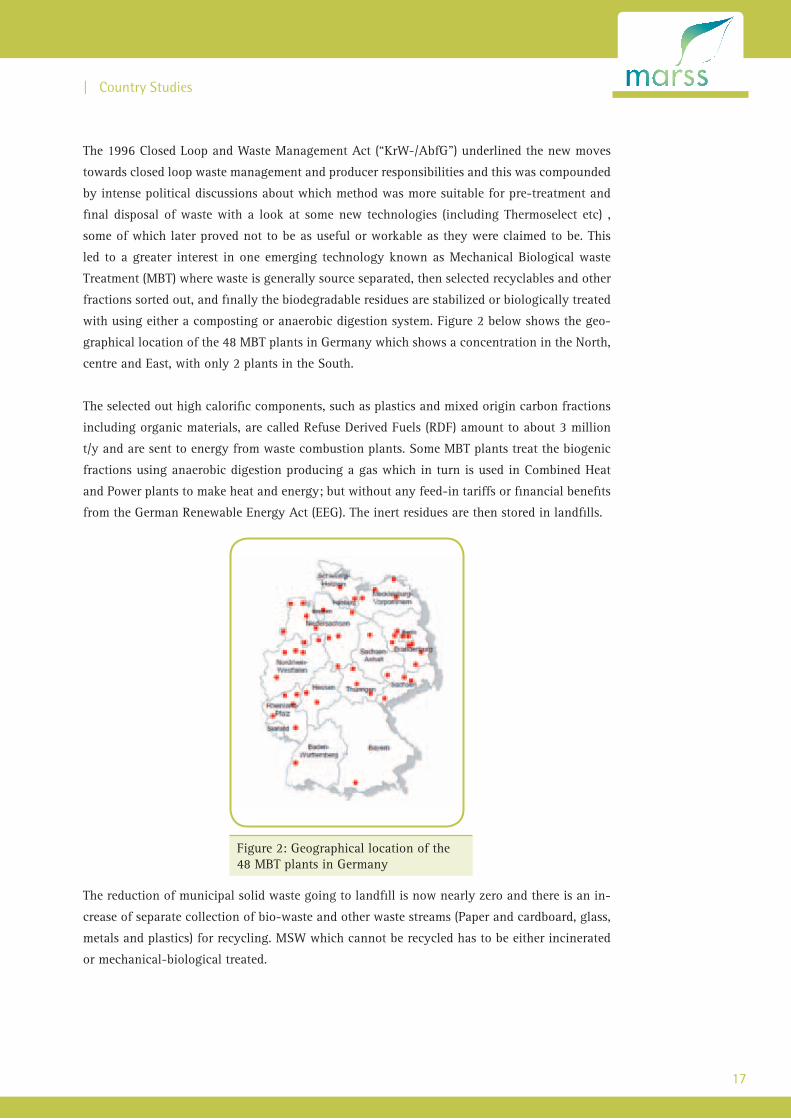

with using either a composting or anaerobic digestion system. Figure 2 below shows the geo-

graphical location of the 48 MBT plants in Germany which shows a concentration in the North,

centre and East, with only 2 plants in the South.

The selected out high calorific components, such as plastics and mixed origin carbon fractions

including organic materials, are called Refuse Derived Fuels (RDF) amount to about 3 million

t/y and are sent to energy from waste combustion plants. Some MBT plants treat the biogenic

fractions using anaerobic digestion producing a gas which in turn is used in Combined Heat

and Power plants to make heat and energy; but without any feed-in tariffs or financial benefits

from the German Renewable Energy Act (EEG). The inert residues are then stored in landfills.

The reduction of municipal solid waste going to landfill is now nearly zero and there is an in-

crease of separate collection of bio-waste and other waste streams (Paper and cardboard, glass,

metals and plastics) for recycling. MSW which cannot be recycled has to be either incinerated

or mechanical-biological treated.

Figure 2: Geographical location of the 48 MBT plants in Germany

18

marss – Feasibility Report

OutlookGermany has fulfilled the Landfill Directive for some years, and has maintained a 50% recy-

cling level of MSW since 2006 and all signs are that this will continue. Germany has set an

ambitious target to recover all MSW including treatment residues by 2020 and some experts

consider this to be rather ambitious. The new law of separate bio-waste collection is already in

force since the beginning of 2015 so this too may have an effect on the total calorific fraction

within MSW available for energy recovery. It is already a known fact that Germany has an

over-capacity of incinerators due to long contract being given concluded and a large number

of expensive plants being built, so this too may affect the prices so raising the demand for RDF

coming from MSW. This may then reduce the rate of recycling and increase the rate of im-

ports into Germany of suitable waste derived fuels. Biogas is also a competitor for the organic

fractions found in MSW so we may see a diversion of this fraction into biogas plants so this

may raise interest in MARSS technology but this has not been investigated in this study. The

constraints set by the tight licensing and flue gas cleaning regulations in Germany for Biomass

CHP plants will also put some constraints on a market for the MARSS RRBF with a tendency

to zero, as any additional investment costs will eat into the already tight profit margins of the

CHP operators. It might be said that if we had the same incentive schemes for Renewable heat

and power production such as in the UK, the outlook would be different. However, the current

outlook is that it is predicted that some MBT plants will actually close6. This endorses the opin-

ion that MARSS may not and does not have a potential for replication in Germany apart from

the one demonstration plant in Mertesdorf, which will close at the end of the demonstration

period ion 31st December 2015.

UKCountry highlightsJacob Hayler, Executive Director of the Environmental Services Association (ESA) confirmed

the opportunities emerging in the waste sector commenting, “The UK’s waste management and

recycling sector has gone through an incredible period of transformation in the past decade.

We have moved away from a logistics and low-technology business to becoming a commodity

processing and fuel preparation industry. A legislative and regulatory push towards higher en-

vironmental standards is creating a wealth of new opportunities for waste and recycling com-

panies to thrive”. More must be done, however, if the UK is to achieve the ‘circular economy’

that the EU directives aspire to as 50% rubbish is still being landfilled. According to DEFRA,

energy from waste will remain and continue to be the main path towards diverting residual rub-

bish from landfilling. MBT technology is on the rise with over 50 plants wither running, being

constructed or planned however there remains some uncertainties which include the strength

of markets for MBT end-products such as refuse derived fuel (RDF) and biologically stabilised

products for application to land of for energy recovery.

6 April 2015 Consultation of Report preparation with ASA e.V.

19

| country studies

Significant changes are underway certainly in the UK since 2012 mainly:

significant increase in RDF exports from the UK in 2012 and 2013, supported by a matur-

ing bio-drying Biological Mechanical Treatment (BMBT) sector

market activities dominated by a small number of companies who have substantial stakes

in the UK energy from waste sector (conventional and ACT/ATT), but also a number of

smaller companies

uncertainty about the future of such exports: differences between RDF and SRF, short- or

long-term trends

it is still necessary (and planned) for MARSS to produce a short market-oriented state-

ment, with details of the product + specifications

the energy from waste landscape is growing and changing with still substantial support

for incineration with CHP but interest growing in other technologies such as MARSS.

The use of renewable energy within the market is now an obligation. Suppliers meet their

obligations by presenting Renewables Obligation Certificates (ROCs), which are issued per

MWh of energy produced and weighted according to the technology used. For example

advanced conversion of waste and anaerobic digestion receive two ROCs and energy from

waste by incineration with combined heat and power receives one. No ROCs have yet

been issued for waste derived electricity because typically 40% of municipal solid waste is

fossil-derived (or non-renewable) which has led to classification problems.

Historically the UK has relied on landfill for the management of municipal solid waste, due to a

legacy of mining and quarrying and the availability of ‘holes’ in the ground. With over 80% of

such waste being disposed of in landfill the UK was given a four-year derogation in meeting the

targets for diverting biodegradable municipal solid waste (MSW) from landfill under Directive

1999/31/EC on the landfilling of waste (LFD) based on 1995 tonnages, reduced to 75% by2006,

50% by 2009, 35% by 2016. The average biogenic content of MSW in England is 68%.

Mass burn incineration plants were first developed as ‘destructors’ to reduce volume and weight

of waste prior to disposal. Most generated electricity with a few using the waste heat. Over 30

plants were closed after 1996 due to the tighter emission limits imposed by Directive 89/369/

EEC on the Prevention of Air Pollution from New Municipal Incineration Plants and Directive

89/429/EEC on the Prevention of Air Pollution from Existing Municipal Incineration Plants.

Various revisions of the Waste Framework Directive (WFD) (Directive 75/442/EC) – emphasize

the importance of human health and the environment, focus on disposal, but refers to the waste

hierarchy and requires waste plans by Member States. Revised WFD 91/156/EEC includes re-

covery and an objective definition of waste replacing a subjective definition (‘waste’ means any

substance or object which the holder discards or intends or is required to discard).

Further revisions in WFD Directive 2008/98/EC on waste and repealing certain Directives keeps

MaRss – Feasibility Report

20

definition of waste, primacy of environment and health, a 5-stage waste hierarchy as a prior-

ity (not guidance), waste prevention plans, targets for separate collection (by 2015 for at least

paper, metal, plastic and glass), targets for recycling (by 2020 minimum of 50% reuse and re-

cycling for waste materials such as at least paper, metal, plastic and glass from households and

possibly from other origins as far as these waste streams are similar to waste from households,

and may include biowaste), energy recovery (+ efficiency equation : 65% for new plant, 60%

for existing plant).

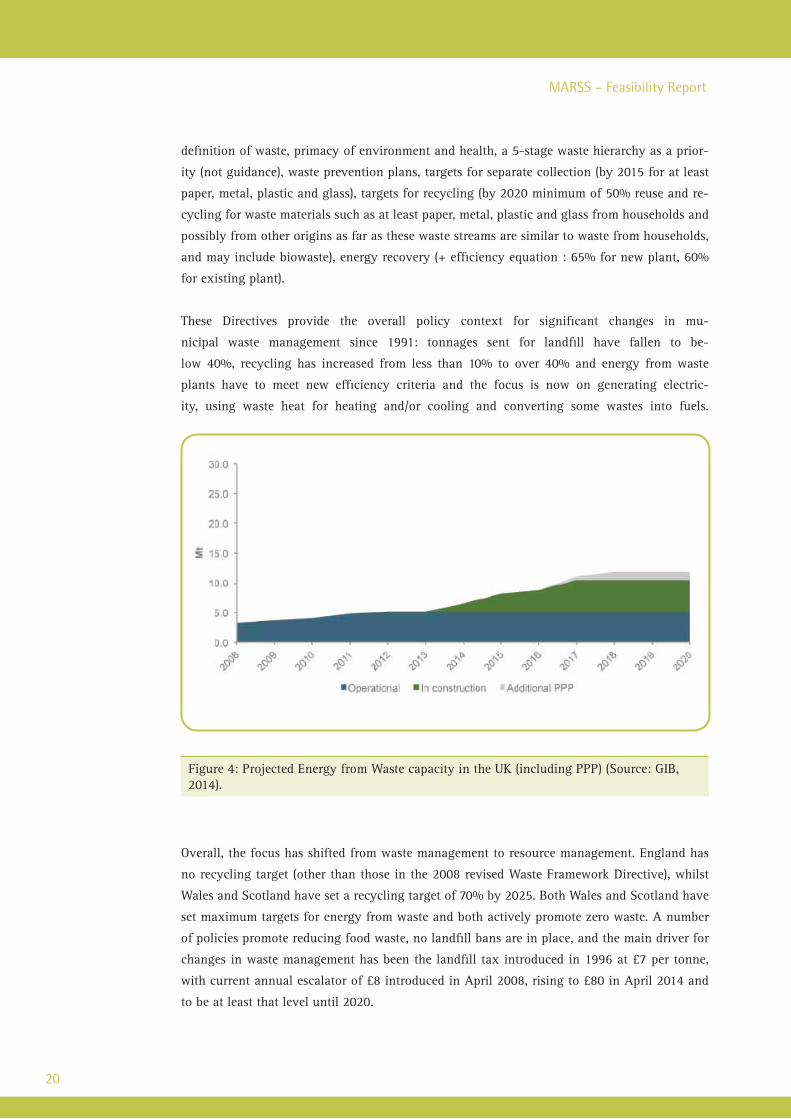

These Directives provide the overall policy context for significant changes in mu-

nicipal waste management since 1991: tonnages sent for landfill have fallen to be-

low 40%, recycling has increased from less than 10% to over 40% and energy from waste

plants have to meet new efficiency criteria and the focus is now on generating electric-

ity, using waste heat for heating and/or cooling and converting some wastes into fuels.

Overall, the focus has shifted from waste management to resource management. England has

no recycling target (other than those in the 2008 revised Waste Framework Directive), whilst

Wales and Scotland have set a recycling target of 70% by 2025. Both Wales and Scotland have

set maximum targets for energy from waste and both actively promote zero waste. A number

of policies promote reducing food waste, no landfill bans are in place, and the main driver for

changes in waste management has been the landfill tax introduced in 1996 at £7 per tonne,

with current annual escalator of £8 introduced in April 2008, rising to £80 in April 2014 and

to be at least that level until 2020.

Figure 4: Projected Energy from Waste capacity in the UK (including PPP) (Source: GIB, 2014).

21

| country studies

Energy ManagementAt the same time there have been major changes in the energy management sector. After 1945

the role of coal declined, although still accounting for 59% of energy in 1966. Oil imports in-

creased substantially, and the discovery and development of North Sea gas (total replacement

of coal gas by 1976) and North Sea Oil (allowing the UK to become an oil exporter) supported

by nuclear power led to a four-fuel energy economy. The UK is again a net importer of oil

and gas, and most nuclear power plants will close after 2020. Current energy policies promote

imported natural gas and renewables (the UK has been set a target under the Renewables Direc-

tive 2009/28/EC of 15% of energy from renewables by 2020), especially offshore wind. Overall,

energy policies stress the importance of security of supply, diversity and control over prices.

Residual waste and what to do with it remains an issue for many EU Member States in spite

of significant progress around waste management in the last two decades (e.g. England in-

creasing recycling rates from 7% in 1995/6 to more than 40% in 2014). Mechanical Biological

treatment technologies have increasingly come into the treatment matrix across the EU but

have remained a minor option within the UK, primarily related to the higher cost of facilities

compared with other options. In addition, market conditions in the UK, in the aftermath of the

economic downturn, have restricted MBT as an investment option for Local Authorities and

merchant operators.

UK Questionnaires resultsQuestionnaires were sent to Local Authority and Cross-sectoral stakeholders with a low level

response rate (8.19 and 17.5% respectively), which reflected the low level of support for MBT

among those providing additional feedback (interviewees).

However there is no doubt that there is an untapped resource in terms of biomass content in

MSW.

As the one of the key stakeholder groups in the procurement and commissioning process for

MBT technologies, it was telling that all respondents from LA’s felt the policy emphasis from

government was low. In the UK context this is not surprising as there has been a strategic com-

mitment to AD since the Waste Review (DEFRA, 2011) which has been emphasised within the

National Waste Management Plan for England (DEFRA, 2013a) as well as being highlighted as a

central feature within the Zero Waste approaches of Scotland and Wales for materials recovery

prior to final disposal (TSE, 2010; WAG, 2010).

MaRss – Feasibility Report

22

There was an overwhelmingly negative response when respondents were asked about future in-

vestment in infrastructure, with MBT being seen as the least likely investment option (alongside

landfill provisioning) during subsequent discussions. Indeed, this reluctance to consider MBT

(and thus MARSS) technologies as part of their future plans was reflected in responses when

asked if their LA was likely to consider producing a biomass fuel, with a number of respondents

indicating they already sent RDF to energy from waste (EfW) recovery operations.

However, 5 respondents (36%) did indicate the presence of biomass CHP plants within their

areas, but given the small number of LA’s responding this cannot be taken as representative.

Indeed, EfW with CHP is becoming increasingly prevalent, with a number of such facilities

coming through the planning pipeline currently.

Those questioned were then asked to give an indication of the impact on their decision-making

that a number of considerations may have, see Figure 6. They were asked to classify these con-

siderations on a scale relating to the seriousness of the impact on decision-making (e.g. very

serious through to not relevant. None of those questioned ranked any consideration within the

‘very serious’ category.

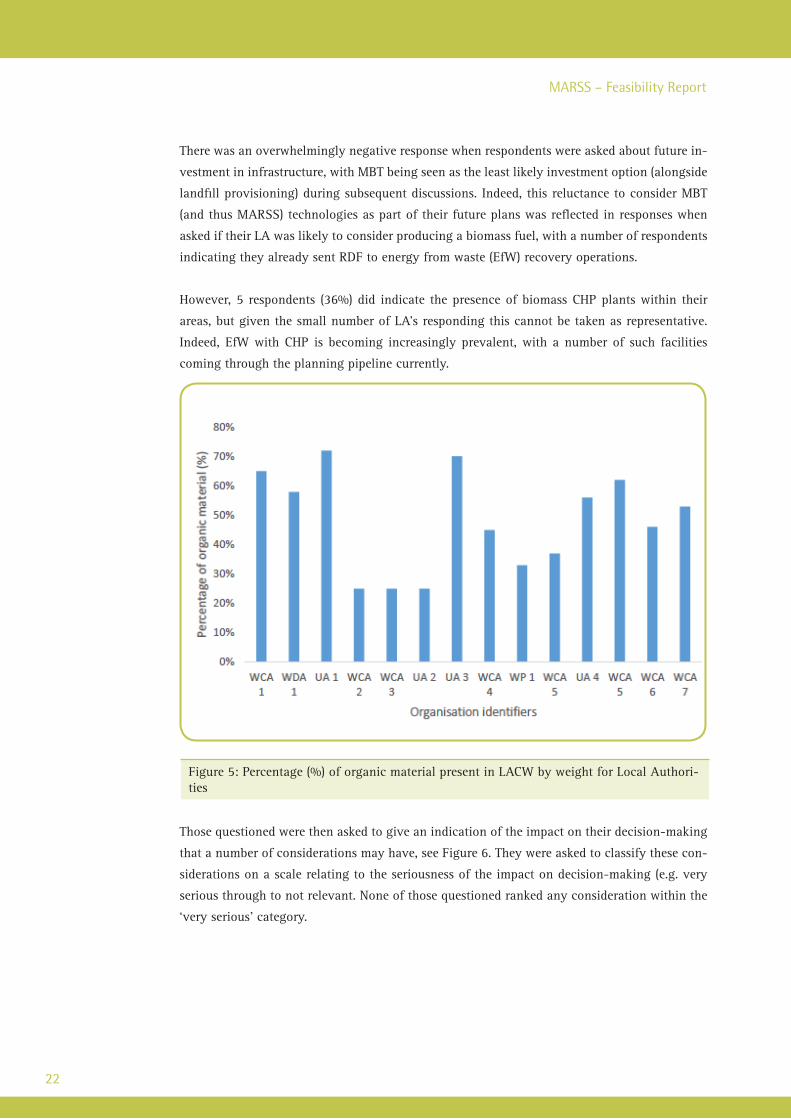

Figure 5: Percentage (%) of organic material present in LACW by weight for Local Authori-ties

23

| country studies

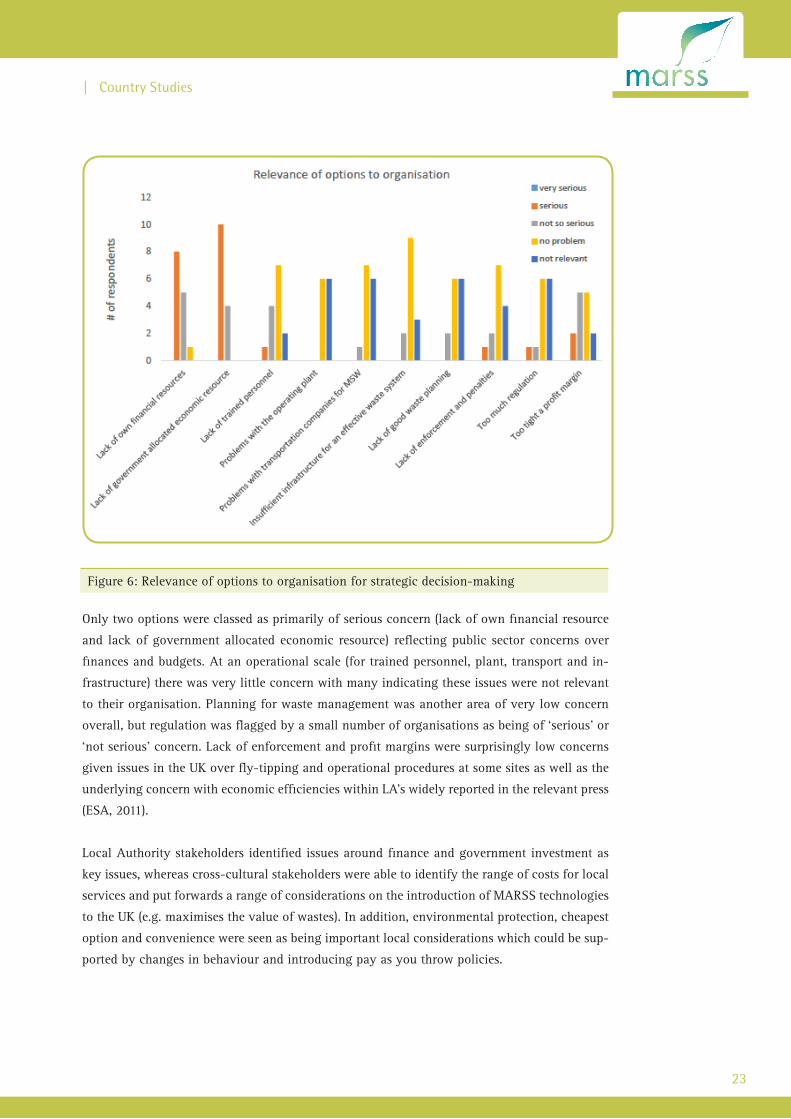

Figure 6: Relevance of options to organisation for strategic decision-making

Only two options were classed as primarily of serious concern (lack of own financial resource

and lack of government allocated economic resource) reflecting public sector concerns over

finances and budgets. At an operational scale (for trained personnel, plant, transport and in-

frastructure) there was very little concern with many indicating these issues were not relevant

to their organisation. Planning for waste management was another area of very low concern

overall, but regulation was flagged by a small number of organisations as being of ‘serious’ or

‘not serious’ concern. Lack of enforcement and profit margins were surprisingly low concerns

given issues in the UK over fly-tipping and operational procedures at some sites as well as the

underlying concern with economic efficiencies within LA’s widely reported in the relevant press

(ESA, 2011).

Local Authority stakeholders identified issues around finance and government investment as

key issues, whereas cross-cultural stakeholders were able to identify the range of costs for local

services and put forwards a range of considerations on the introduction of MARSS technologies

to the UK (e.g. maximises the value of wastes). In addition, environmental protection, cheapest

option and convenience were seen as being important local considerations which could be sup-

ported by changes in behaviour and introducing pay as you throw policies.

MaRss – Feasibility Report

24

OutlookThere is a significant amount of biomass available within the residual waste stream across the

UK, which currently goes to EfW within the UK and has recently been subject to export (mainly

to EfW in Europe). Recent reporting has indicated there is a large amount of EfW infrastructure

to come on-stream which could offer a route for MBT outputs over the long-term. In addition,

pre-treatment is expected to offer another potential route but this is not of significant scale.

This suggests the scope for MARSS technology penetration into the UK waste sector is limited

as policy focus is generally in other areas which impacts considerably on where future invest-

ments will be made.

The scale of organic fraction which remains within the residual waste stream in the UK would

indicate there is potential for applying a technological innovation such as MARSS. In general

stakeholders were positive about the credentials of MARSS but had more pressing concerns

over issues with waste at the local scale, which contrasts with the strategic benefit which may

be obtained from MBT in delivering regulatory targets. However, a combination of financial

constraints impacting Local Authority waste planning, other policy priorities to deliver on

waste hierarchy commitments and the emphasis on value and quality through transitioning to-

wards a circular business model, means realistically that the UK provides a limited opportunity

for MARSS market penetration currently.

ItalyDue to the fact that Naples has just been going through a period of “emergency” in their waste

collection and management and much publicity has been given to the on-going problems in the

city and region, it was chosen in the MARSS project for an in-depth study.

The case of NaplesItaly as a country is extremely diverse in its profile of MSW management and has enormous

regional difference in approaches, success in reaching targets and some have specific problems

of control of operations in the waste area. The case of Naples was considered in depth within

the MARSS project and a summary of the results are found in this and other publications7.

According to ISPRA (2012), there are considerable differences between the regions in MSW

generation and landfilling has been the main form of disposal. However landfilling is on the

decrease from 19.7 to 15.4 million tonnes in absolute terms; but the range is drastic with Lom-

bady landfilling about 8% whereas Sicily landfilled 93% MSW (ISPRA 2012).

The level of separate collection is increasing in all the Italian regions, but Italy as a whole,

with 35 % of MSW separate collection in 2010, equal to 11.4 million tonnes, is still far from

achieving the national separate collection targets, introduced by Legislative Decree 152/2006

(the 2008 target was 45 %)8.

7 Please refer to the MARSS website for additional publications and results at www.marss.rwth-aachen.de

8 EEA Municipal waste in Italy, Feb 2013 Report

25

| country studies

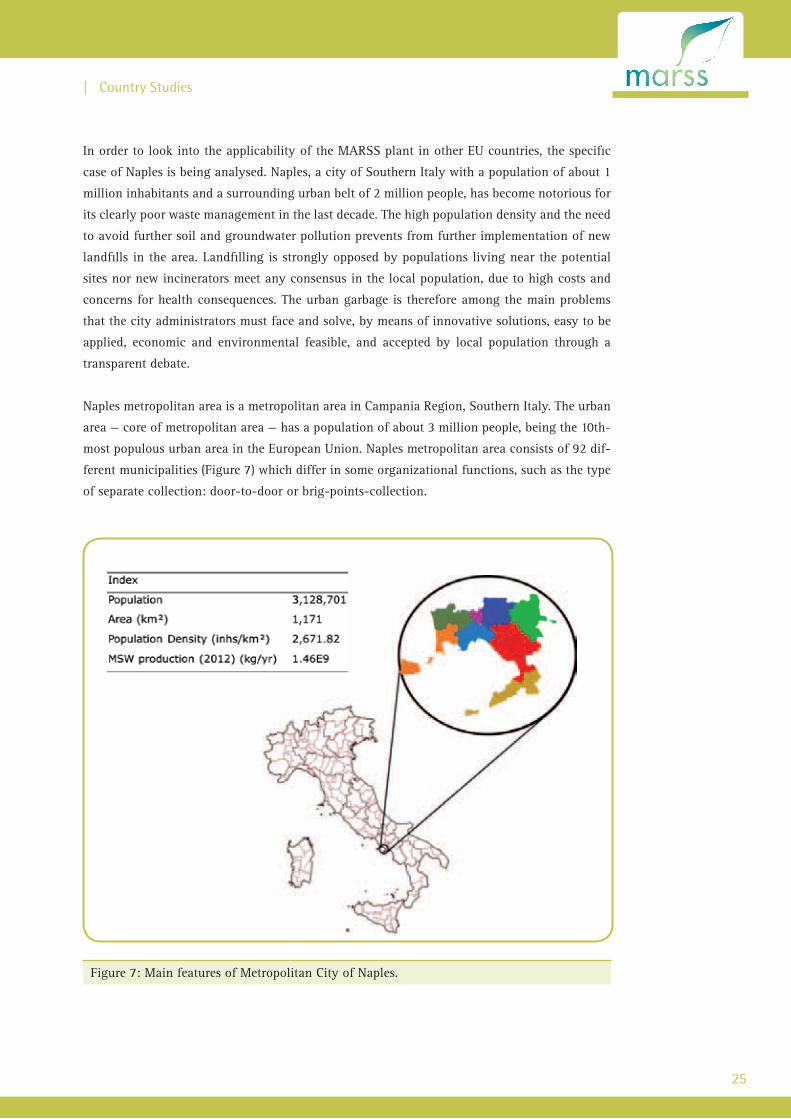

In order to look into the applicability of the MARSS plant in other EU countries, the specific

case of Naples is being analysed. Naples, a city of Southern Italy with a population of about 1

million inhabitants and a surrounding urban belt of 2 million people, has become notorious for

its clearly poor waste management in the last decade. The high population density and the need

to avoid further soil and groundwater pollution prevents from further implementation of new

landfills in the area. Landfilling is strongly opposed by populations living near the potential

sites nor new incinerators meet any consensus in the local population, due to high costs and

concerns for health consequences. The urban garbage is therefore among the main problems

that the city administrators must face and solve, by means of innovative solutions, easy to be

applied, economic and environmental feasible, and accepted by local population through a

transparent debate.

Naples metropolitan area is a metropolitan area in Campania Region, Southern Italy. The urban

area — core of metropolitan area — has a population of about 3 million people, being the 10th-

most populous urban area in the European Union. Naples metropolitan area consists of 92 dif-

ferent municipalities (Figure 7) which differ in some organizational functions, such as the type

of separate collection: door-to-door or brig-points-collection.

Figure 7: Main features of Metropolitan City of Naples.

MaRss – Feasibility Report

26

The critical nature of the situation that has led to the crisis in MSW collection and treatment in

Naples may be attributed, besides social factors, to the following factors:

separate collection is not widespread and makes up for a too small proportion of overall

waste production;

lack of local biological treatment plants. This forces the municipalities that achieve high

percentages of separate collection of the organic fraction to export it to other regions at

high cost;

separate collection fractions are not 100% recyclable. Thus, when such fractions are recy-

cled, a non-negligible quantity of residues is produced, which must be diverted to landfill.

large amounts of hazardous organic and inorganic substances are illegally landfilled and

stored with unknown future consequences;

communication and information to citizens is lacking both in quantity and quality and,

when present, very seldom occurs with advance notice. This contributes to strengthening

across-the-board opposition, which is also intensified by inaccurate or partial news.

The last two aspects touch the social side of the waste emergency in Campania: the lack of ac-

ceptance for today’s situation, the long-lasting complaints due to odor, air, and soil pollution

and bad management, the broken promises of changing the present situation. Even though they

are not discussed here, it is evident that these aspects are of high and crucial importance.

Figure 8: Schematic flow chart of MSW collection and treatment in Naples

27

| country studies

Naples Municipality shows the highest waste generation in 2011 (Figure 9) among Campania

Municipalities due the high population density and large tourist flows. Environmental issues of

the current waste management system have received great attention because since the mid-90s,

the city of Naples and surrounding provinces have struggled with waste management policies

and disposal emergency has not been totally resolved yet. At the same time the implementation

of new landfills was opposed by local population causing a strong social conflict. Political and

scientific analyses of the waste crisis indicate the emergency situation was created by inappro-

priate waste management policy and practice (Commissione Parlamentare, 2007). Illegal waste

activities have increased considerably in the last years, among which the case of the Naples

crisis (2008) in which the European Court of Justice condemned Italy for the late and incorrect

application of EU directives (Hazardous Waste Directive and the Landfill Directive) on prevent-

ing negative environmental impacts from waste dumps, including sites for dangerous waste.

The overall production of municipal solid waste (MSW) in Naples in 2011, as estimated by the

official Italian authority, was about 5.16E+08 kg of urban waste (i.e. around 540 kilograms per

inhabitant per year [kg inh-1 year-1]). In the last ten years, the MSW generation trend shows a

constant growing rate except for 2009-2010 where a decreasing pattern became evident (Figure 9).

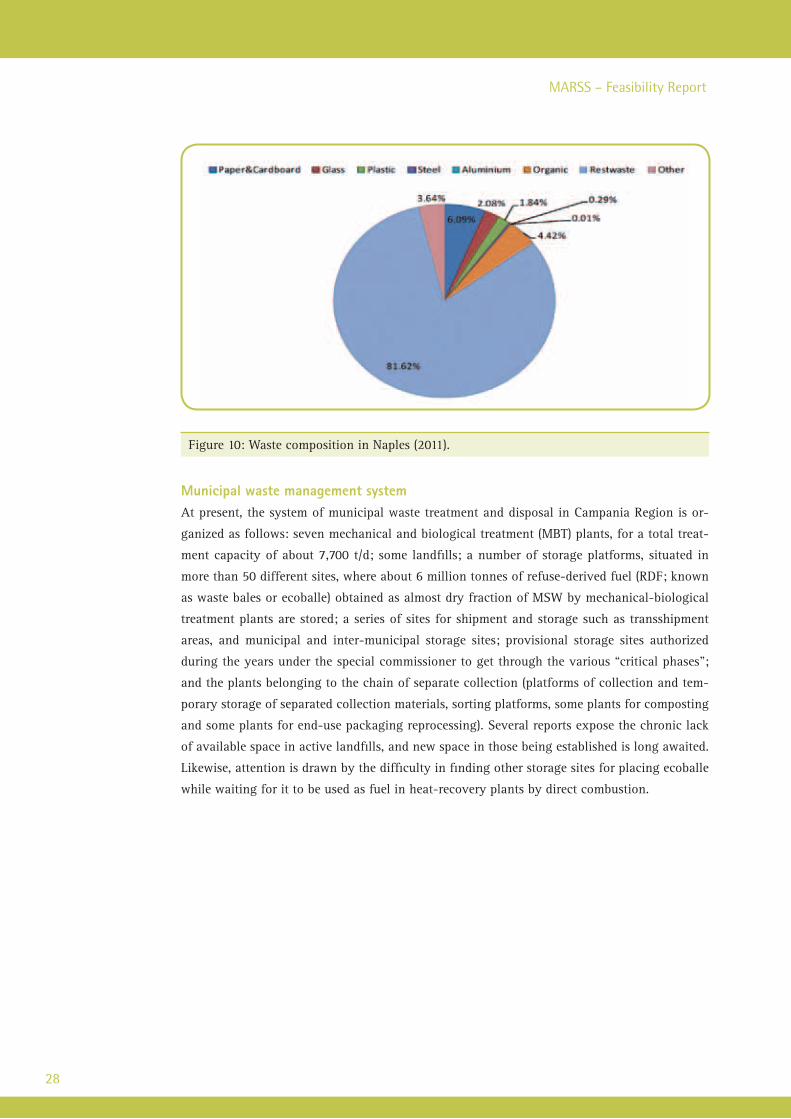

The production of 5.16E+08 kg municipal waste (Figure 10) is subdivided into the following:

4.22E+08 kg of unsorted mixed collection sent to treatment and disposal, 7.62E+07 kg of sepa-

rate collection sent to recycling or organic treatment; 1.88E+07 kg (representing less that 4%

of total waste generation) of ‘others’ including batteries, clothes, bulky waste is not included in

the analysis due to the lack of reliable data.

Figure 9: Waste production in Naples in the last decades. Data provided by Arpac, 2013

MaRss – Feasibility Report

28

Municipal waste management systemAt present, the system of municipal waste treatment and disposal in Campania Region is or-

ganized as follows: seven mechanical and biological treatment (MBT) plants, for a total treat-

ment capacity of about 7,700 t/d; some landfills; a number of storage platforms, situated in

more than 50 different sites, where about 6 million tonnes of refuse-derived fuel (RDF; known

as waste bales or ecoballe) obtained as almost dry fraction of MSW by mechanical-biological

treatment plants are stored; a series of sites for shipment and storage such as transshipment

areas, and municipal and inter-municipal storage sites; provisional storage sites authorized

during the years under the special commissioner to get through the various “critical phases”;

and the plants belonging to the chain of separate collection (platforms of collection and tem-

porary storage of separated collection materials, sorting platforms, some plants for composting

and some plants for end-use packaging reprocessing). Several reports expose the chronic lack

of available space in active landfills, and new space in those being established is long awaited.

Likewise, attention is drawn by the difficulty in finding other storage sites for placing ecoballe

while waiting for it to be used as fuel in heat-recovery plants by direct combustion.

Figure 10: Waste composition in Naples (2011).

29

| country studies

Identification of stakeholder groupsA number of carefully selected stakeholders in Naples and Campania Region were identified,

out of a preliminary list, broken down into 10 categories9. Ten groups of about 300 stakeholders

were extracted, who were invited to answer to an online questionnaire. An explanation of the

MARSS project’s goal and scope and the reasons underlying the stakeholders’ consultancy were

provided, together with some technical information about the proposed solution.

The biomass extraction from MSW technology was presented as one of the possible options in

order to provide a means for the Municipality to comply with the Landfill Directive, and in turn,

leading to a more sustainable waste management for this municipality. Special attention was

given in the questionnaires to see how respondents perceive the reasons and responsibilities of

the waste emergency in Naples and in Campania Region in the past years. In the technical area,

a first explanation about the proposed plant and how it works was provided, before raising

questions about stakeholders’ knowledge of the different waste management options; finally,

50 questions (39 open and 11 closed) were listed about stakeholders’ judgment on the way the

waste emergency was addressed. Some questions were repeated under different points of view,

in order to purposefully introduce some redundancy in the form of “double-check” questions.

In so doing, the real point of view of the stakeholders involved could likely be understood.

Selection of results from the stakeholder consultancyA selection of achieved results is shown in the diagrams of 11, 12, 13 and 14. Questions offered

the possibility to the stakeholders to identify causes, responsibilities, risks; to express fears and

expectations; to provide a preliminary evaluation of the proposed technology, about which they

only knew what was told them in the survey. It is important to note that a third party did not

provide the information, but by the project proponents and therefore some lack of trust and

uncertainty were expected.

9 National Ministry, Local Authorities, Local Waste Management Authority, Local Waste Management Authority, Emergency

Commissioner, Companies in charge of collection and recycling urban waste, Professional Associations, Environmental

Associations and social groups, Local Actors, Academic Research institutions, Mass media.

Figure 11: Perception of the main reasons underlying the recent waste emergency in Naples and Campania Region

MaRss – Feasibility Report

30

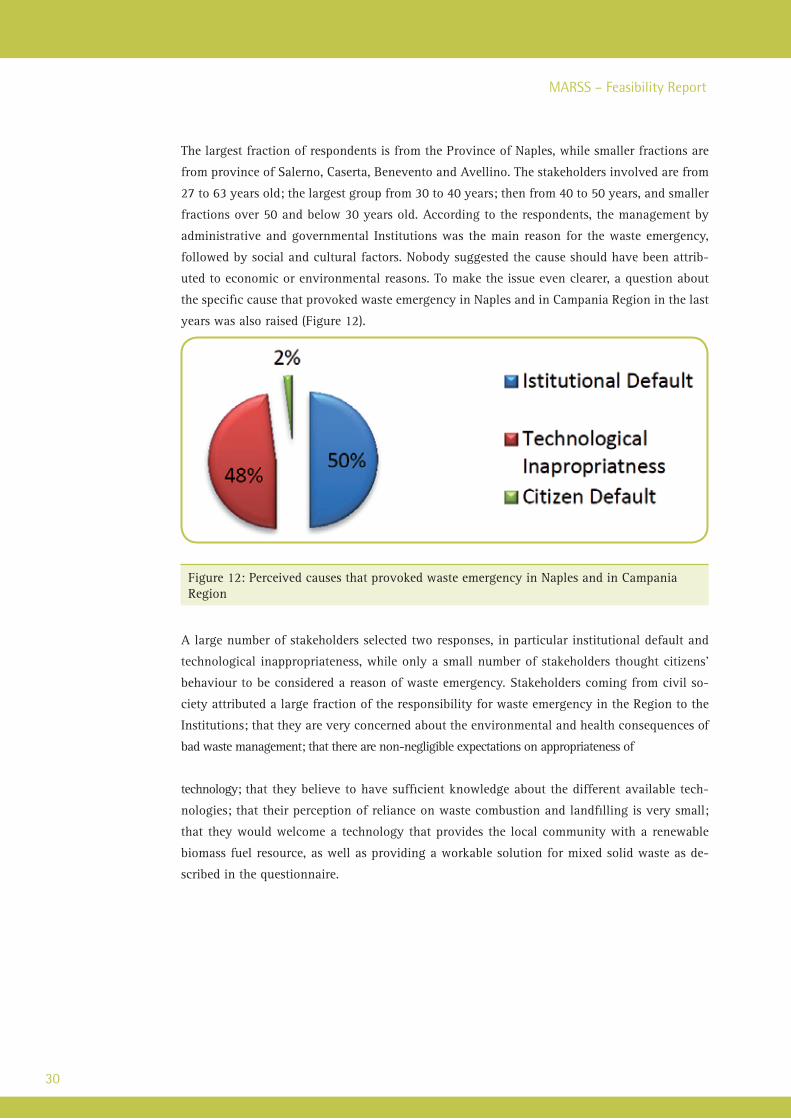

The largest fraction of respondents is from the Province of Naples, while smaller fractions are

from province of Salerno, Caserta, Benevento and Avellino. The stakeholders involved are from

27 to 63 years old; the largest group from 30 to 40 years; then from 40 to 50 years, and smaller

fractions over 50 and below 30 years old. According to the respondents, the management by

administrative and governmental Institutions was the main reason for the waste emergency,

followed by social and cultural factors. Nobody suggested the cause should have been attrib-

uted to economic or environmental reasons. To make the issue even clearer, a question about

the specific cause that provoked waste emergency in Naples and in Campania Region in the last

years was also raised (Figure 12).

A large number of stakeholders selected two responses, in particular institutional default and

technological inappropriateness, while only a small number of stakeholders thought citizens’

behaviour to be considered a reason of waste emergency. Stakeholders coming from civil so-

ciety attributed a large fraction of the responsibility for waste emergency in the Region to the

Institutions; that they are very concerned about the environmental and health consequences of

bad waste management; that there are non-negligible expectations on appropriateness of

technology; that they believe to have sufficient knowledge about the different available tech-

nologies; that their perception of reliance on waste combustion and landfilling is very small;

that they would welcome a technology that provides the local community with a renewable

biomass fuel resource, as well as providing a workable solution for mixed solid waste as de-

scribed in the questionnaire.

Figure 12: Perceived causes that provoked waste emergency in Naples and in Campania Region

31

| country studies

The main risks perceived by the larger fraction of respondents are those related to negative

impacts on environment and human health, while social and economic risks are given much

smaller importance. The largest fraction of stakeholders who responded to the survey thinks

that the situation in Naples and in Campania Region is not stable, and that there will probably

be a new emergency in the near future. In general, the majority of respondents are convinced

that the past emergency had a bad impact not only on the reputation of the city that could

result in the loss of tourists and foreign investments, but had also worsened the environmental

quality of the city and the entire province of Naples.

From these preliminary results it clearly appears that all the interviewed stakeholders are not

satisfied of the waste management in Naples and in Campania Region, with a level of satisfac-

tion around 1 and 2 (over a range from 1 to 5, being 1 the lowest level of satisfaction and 5

the highest level of satisfaction), and think it is urgent and mandatory to change the entire

management system. The majority of respondents seem to know about the technologies that

are presently used for waste collection and disposal in Naples and in Campania Region. The

largest three groups10 of stakeholders, out of the 10 groups involved in this preliminary survey,

seem to be well informed and care about waste management, even if not directly working on it.

After all the questions about the possible risks and the level of experience of each plant, we

asked if respondents would be favorable or adverse to the construction of the new plant. The

largest amount of the stakeholders responded in a favorable way (97% favorable; only 3%

against).

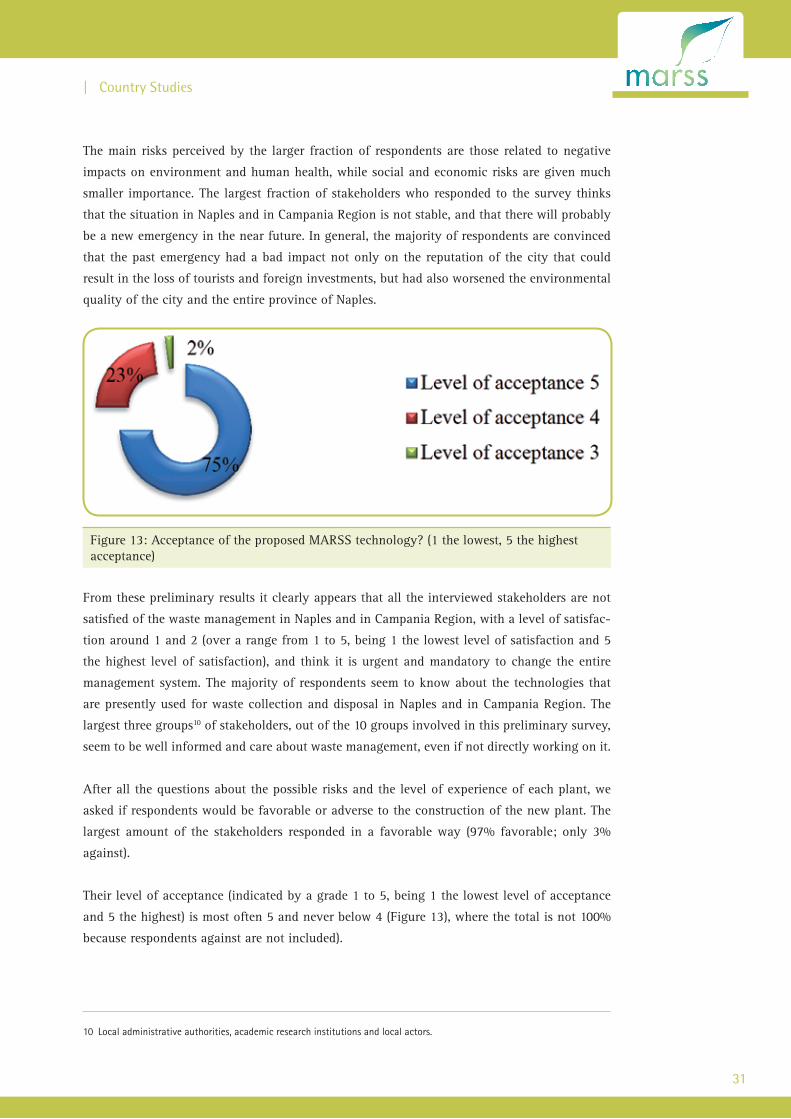

Their level of acceptance (indicated by a grade 1 to 5, being 1 the lowest level of acceptance

and 5 the highest) is most often 5 and never below 4 (Figure 13), where the total is not 100%

because respondents against are not included).

10 Local administrative authorities, academic research institutions and local actors.

Figure 13: Acceptance of the proposed MARSS technology? (1 the lowest, 5 the highest acceptance)

MaRss – Feasibility Report

32

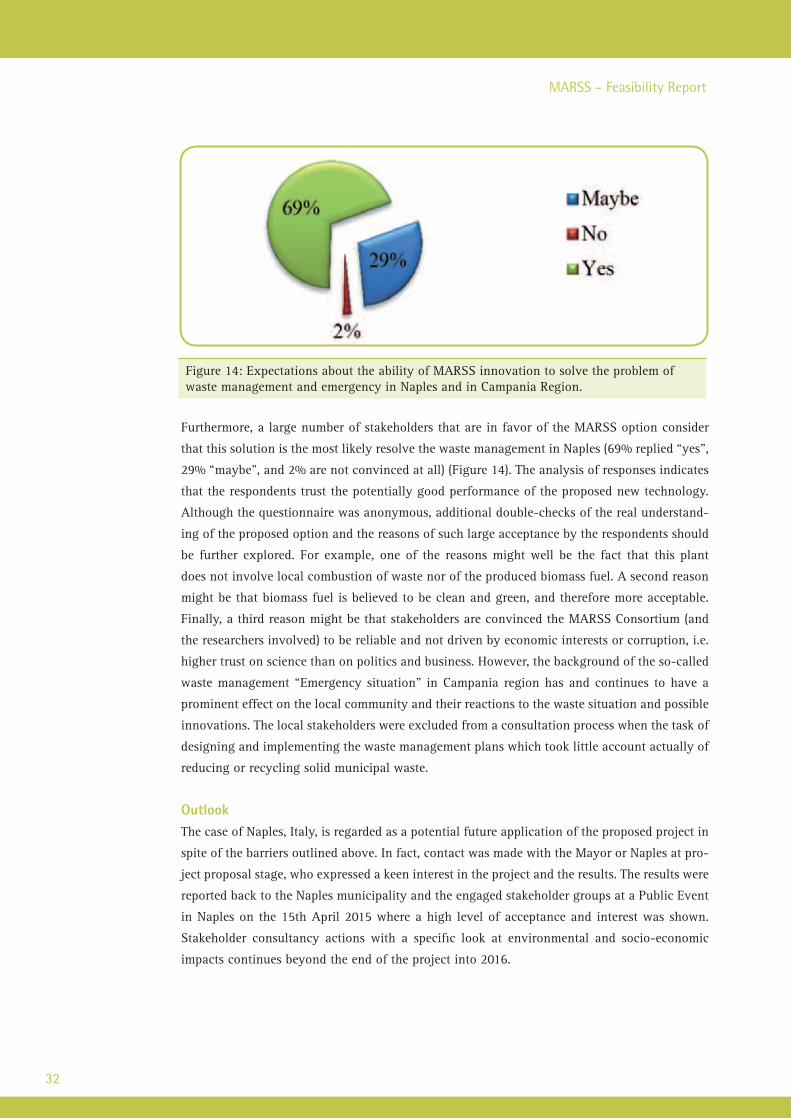

Furthermore, a large number of stakeholders that are in favor of the MARSS option consider

that this solution is the most likely resolve the waste management in Naples (69% replied “yes”,

29% “maybe”, and 2% are not convinced at all) (Figure 14). The analysis of responses indicates

that the respondents trust the potentially good performance of the proposed new technology.

Although the questionnaire was anonymous, additional double-checks of the real understand-

ing of the proposed option and the reasons of such large acceptance by the respondents should

be further explored. For example, one of the reasons might well be the fact that this plant

does not involve local combustion of waste nor of the produced biomass fuel. A second reason

might be that biomass fuel is believed to be clean and green, and therefore more acceptable.

Finally, a third reason might be that stakeholders are convinced the MARSS Consortium (and

the researchers involved) to be reliable and not driven by economic interests or corruption, i.e.

higher trust on science than on politics and business. However, the background of the so-called

waste management “Emergency situation” in Campania region has and continues to have a

prominent effect on the local community and their reactions to the waste situation and possible

innovations. The local stakeholders were excluded from a consultation process when the task of

designing and implementing the waste management plans which took little account actually of

reducing or recycling solid municipal waste.

OutlookThe case of Naples, Italy, is regarded as a potential future application of the proposed project in

spite of the barriers outlined above. In fact, contact was made with the Mayor or Naples at pro-

ject proposal stage, who expressed a keen interest in the project and the results. The results were

reported back to the Naples municipality and the engaged stakeholder groups at a Public Event

in Naples on the 15th April 2015 where a high level of acceptance and interest was shown.

Stakeholder consultancy actions with a specific look at environmental and socio-economic

impacts continues beyond the end of the project into 2016.

Figure 14: Expectations about the ability of MARSS innovation to solve the problem of waste management and emergency in Naples and in Campania Region.

33

| country studies

GreeceWaste management contracts in GreeceWaste management situation in Greece has improved in the last decade but it is still recog-

nized as a pressing problem. In Greece the collection and transportation of MSW are mainly

performed by the cleaning services of the municipalities. In rare occasions private companies

are assigned to collect and transport MSW. A significant part of MSW management authorities,

have assigned the collection and transportation of solid waste as well as their management to

inter-municipal companies where more municipalities are participating in the scheme. How-

ever, no particular policy is followed concerning the type and duration of the contracts with

the private companies/enterprises.

Stakeholder consultancyFindings from the interviews with the stakeholders demonstrated that cement industries have

the capacity and could potentially apply MARSS technology. They would adopt the use of MSW

biomass as fuel material in their operating process in case the final product complies with the

national and industrial requirements and it is financially beneficial. The general public would

fully support an innovative technology such as MARSS in case it was applied in a sustainable

manner, meaning that the technology is sustainable in terms of environmental, economic and

social aspects.

In Greece three large cement industries are operating, namely Titan Group, Halyps Cement

(Italcementi Group) and Lafarge Holcim Group. The main supply fuel that is currently used for

the operating process in the cement industries is petroleum coke (petcoke). The petcoke is a

carbonaceous solid delivered from oil refinery coker units or other cracking processes (16). In

order to reduce the harmful environmental impacts and significant financial cost from petcoke,

cement industries have been oriented to use alternative fuels for their operating processes. The

most important factors for the selection of the combustible material in cement industries are:

lower calorific value

low levels of moisture

low levels of chlorine and mercury content(17) (18) (19)

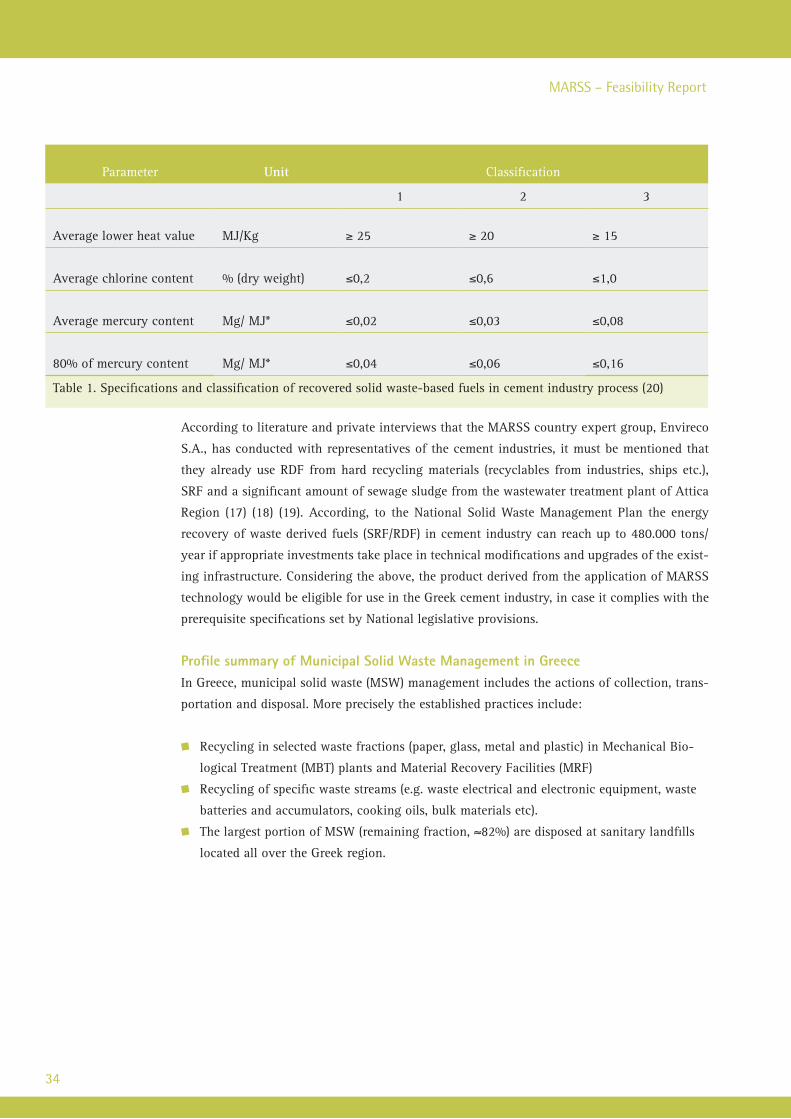

According to the national legislation (MD 56366/4351/2014), the use of waste materials as

alternative fuel for energy recovery in the cement industry should follow specific require-

ments that are given in Table 1. Additionally, the cement industries shall periodically (every

six months) perform analysis to waste derived fuels in order to determine its biomass content,

volatile matter, moisture, ash content and calorific value, chlorine content and mercury con-

centration following the corresponding European analysis standards.

MaRss – Feasibility Report

34

According to literature and private interviews that the MARSS country expert group, Envireco

S.A., has conducted with representatives of the cement industries, it must be mentioned that

they already use RDF from hard recycling materials (recyclables from industries, ships etc.),

SRF and a significant amount of sewage sludge from the wastewater treatment plant of Attica

Region (17) (18) (19). According, to the National Solid Waste Management Plan the energy

recovery of waste derived fuels (SRF/RDF) in cement industry can reach up to 480.000 tons/

year if appropriate investments take place in technical modifications and upgrades of the exist-

ing infrastructure. Considering the above, the product derived from the application of MARSS

technology would be eligible for use in the Greek cement industry, in case it complies with the

prerequisite specifications set by National legislative provisions.

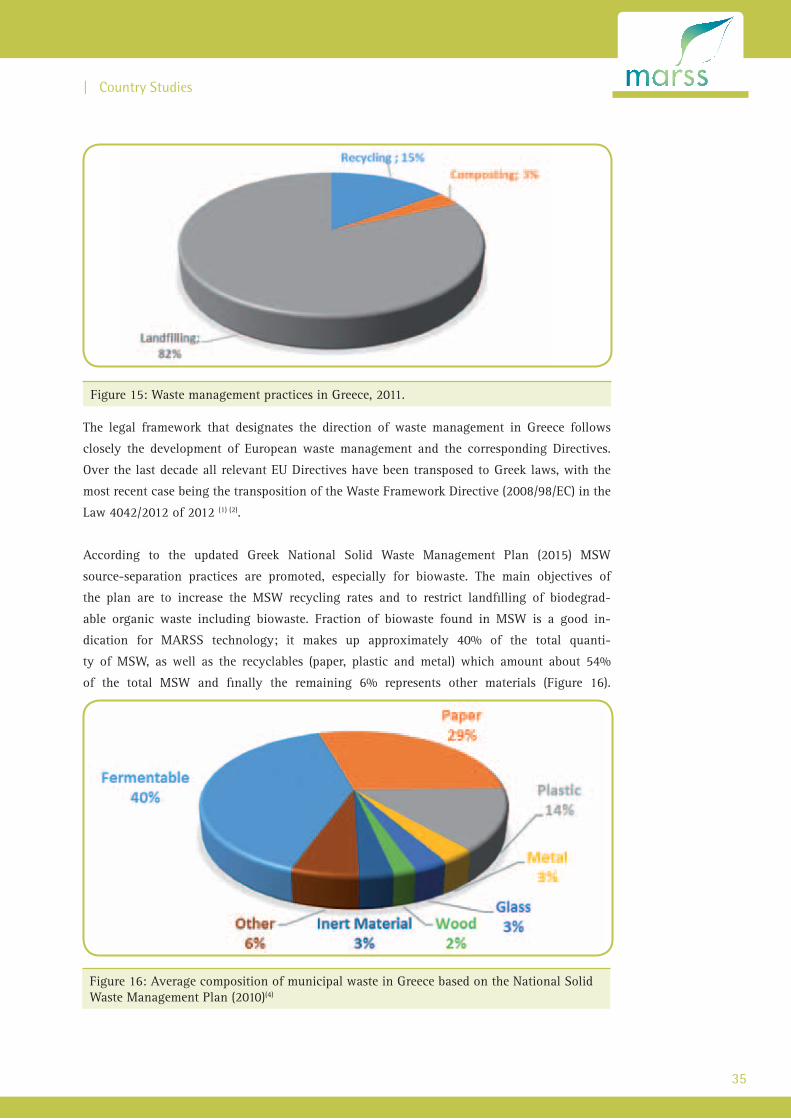

Profile summary of Municipal Solid Waste Management in GreeceIn Greece, municipal solid waste (MSW) management includes the actions of collection, trans-

portation and disposal. More precisely the established practices include:

Recycling in selected waste fractions (paper, glass, metal and plastic) in Mechanical Bio-

logical Treatment (MBT) plants and Material Recovery Facilities (MRF)

Recycling of specific waste streams (e.g. waste electrical and electronic equipment, waste

batteries and accumulators, cooking oils, bulk materials etc).