federal and california tax update for businesses and estates/media/event...

TRANSCRIPT

Federal and California Tax Update for Businesses and Estates

Annette Nellen, CPA, CGMA, JD Gary McBride, JD, LLM (Taxation), CPA

Copyri

ght 2

016-1

7

Notice to ReadersCalCPA Education Foundation programs and publications are designed to provide CPAs and financial professionals current, accurate information concerning the subject matter covered. However, the CalCPA Education Foundation gives no assurance that such information is comprehensive in its coverage of a subject matter or that it is suitable in dealing with specific client problems or business-related circumstances. Accordingly, information published or provided by the CalCPA Education Foundation should not be relied upon as a substitute for independent research to original sources of authority. The CalCPA Education Foundation does not render any accounting, legal or other professional advice, nor does it have any responsibility for updating or revising any programs or publications which it may present, distribute or sponsor.

CPE Credit Policies Course, Conference, Onsite—The California Board of Accountancy (CBA) grants one CPE credit hour for each 50 minutes of class time. To qualify for CPE, a program must be at least 50 minutes in length. The CBA tracks CPE in 25-minute segments after the first 50 minutes. For each additional 25-minute segment completed, 0.5 CPE credit hours will be granted. To accurately track participation, registrants are required to legibly sign your name on the official sign-in sheet prior to the start of the event. If you arrive late, you must note your arrival time on the sign-in sheet. If you need to leave early, you must initial and note your departure time on the sign-in sheet to receive partial credit.

The CBA requires CPE providers to closely monitor attendance during CPE. If you are not in the room during a portion of the CPE event, you will not receive credit. Your official record of attendance for the event is available via the My Events section of the website within one week. The host provider must retain the record of attendance, written educational goals and specific learning objectives, as well as a syllabus, which provides a general outline instructional objective and a summary of topics for the course for a period of five years. A copy of the educational goals, learning objectives, and course syllabus shall be made available to the CBA upon request.

Webcast—For webcast participants to receive credit, three times every hour, you will be required to respond to an attendance question that appears on the screen. If viewing the webcast as part of a group, the group leader is required to answer the attendance questions on behalf of all participants. Group attendance is verified and documented by the group attendance form the day of the event. The CalCPA Education Foundation archives attendance records as required by the CBA to verify your CPE attendance in the event your CPE records are audited.

Webcast are broadcast via the internet to those individuals who have registered for the webcast. The CalCPA Education Foundation takes all reasonable efforts to maintain the camera on the speaker, but does on occasion pan across the audience while following a speaker around the room. Furthermore, as the broadcast requires the use of microphones and other devices to amplify the speaker to both the live and webcast audience, an attendee’s voice may be broadcast during the webcast and, no attendee should have an expectation of privacy as to potentially being identifiable in the webcast.

Self-Study—An online exam is included with your purchase. After studying the materials, to take the exam please go to www.calcpa.org/MySelfStudy. You may be asked to log in. Once you have logged in, find this product and click “Take Exam.” You will have a total of (3) attempts to take the final exam. Once you have completed the online final exam, you will be notified if you have passed or failed. To pass, you need a minimum passing grade of 70% (except for California regulatory review courses where the minimum passing grade is 90% as specified in Reg. Sec. 87.9(3)). You will be able to download your certificate of completion documenting the number of CPE credits earned for the course through your CPE Tracker at www.calcpa.org/CPE_Tracker. Please monitor the time it takes to complete the course. Record your total time and your comments about the course on the evaluation e-mailed to you.

In accordance with the Standards of the National Association of State Boards of Accountancy (NASBA), one credit hour is granted for each 50 minutes of interactive self-study completed. Recommended credit hours are included in each course description. However, state boards of accountancy have final authority on the acceptance of individual courses for CPE credit. Self-study courses must be completed by one year from date of purchase. If you have any problems or questions using your online course, please e-mail [email protected]. If you move before completing this course, please contact Member Services at (800) 922-5272 with your new address.

Materials Terms and Conditions—CalCPA Education Foundation program materials, both hardcopy and electronic, are protected by U.S. copyright law. Materials are provided only for use by the participant registered for the program. You agree that you will not sell, distribute, transmit, or otherwise transfer all or any portions of the content of program materials without written permission from the author(s). Please contact the CalCPA Education Foundation course materials coordinator at [email protected] or (650) 522-3208 to obtain permission.

eBook FAQs—Visit www.calcpa.org/ebooks to view frequently asked questions. Be sure to save your annotations made throughout the course.

The CalCPA Education Foundation Guarantee—If any continuing education product fails to meet your expectations, or if you are not satisfied for any reason, you may return it within 30 days for an exchange or refund. (Shipping and handling fees are nonrefundable). Call Member Services at (800) 922-5272 for return instructions.

Copyright © 2016 Annette Nellen, CPA, CGMA, JD

Gary McBride, JD, LLM (Taxation), CPA No copyright claimed in U.S. Government materials.

TAXB _________________________________________________________________________________________________________www.calcpa.org (800) 922-5272

Copyri

ght 2

016-1

7

2016 Federal & California Tax Update: Businesses, Trusts, Estates, & Exempt Orgs

Gary McBride & Annette Nellen

California CPA Education Foundation November 2016 – January 2017

The PPT slides that accompany each chapter can be download (chapter by chapter) at: http://mntaxclass.com/files.html

Chapter 1: 2016 Legislation and Code/Regs. First Effective in 2016

Chapter 2: Expiring Provisions

Chapter 3: C Corporations

Chapter 4: S Corporations

Chapter 5: Partnerships and LLCs

Chapter 6: Credits

Chapter 7: State of California and MultiState

Chapter 8: Accounting Methods and Section 199

Chapter 9: International Tax

Chapter 10: Payroll Tax and Worker Classification

Chapter 11: ACA Update

Chapter 12: Estate, Gift, and GST Tax

Chapter 13: Income Taxation of Trusts and Estates

Chapter 14: Tax Exempts

Chapter 15: Looking Forward

©2016. These materials are copyrighted and may not be reproduced or distributed in whole or in part without permission of the authors/CalCPA Education Foundation.

Copyri

ght 2

016-1

7

2016 McBride/Nellen Federal and California Update for Businesses and Estates

Chapter 1: 2016 Legislation and Code/Regs. First Effective in 2016 Page 1-1

Chapter 1 : 2016 Legislation and Code/Regs. First Effective in 2016

Table of Contents Chapter 1 : 2016 Legislation and Code/Regs. First Effective in 2016 .................................. 1-1

2016 Legislation ............................................................................................................. 1-2

P.L. 114-125 (2/24/16), Trade Facilitation and Trade Enforcement Act of 2015 ............. 1-2

Continuing Appropriations Legislation FY2017 – P.L. 114-223 (9/29/16; H.R. 5325) ... 1-3

Prior Law First Effective in 2016 ........................................................................... 1-3

New 2016 Filing Requirements ............................................................................................. 1-3

Due Date for W-2 and 1099-MISC ....................................................................................... 1-4

Truncated SSN on Form W-2 ............................................................................................... 1-4

PATH and Deminimis Errors on Information Returns and Payee Statements ............... 1-4

Permanence and Enhancement of Food Inventory Donations .......................................... 1-5

Expensing for Live Theatrical Productions ......................................................................... 1-6

Research Credit Usable Against AMT for Eligible Small Businesses ............................... 1-6

Research Credit Available Against Payroll Taxes for Start-ups ....................................... 1-7

Work Opportunity Tax Credit Extended to Long-Term Unemployed ............................ 1-8

More Employers Are Eligible for Differential Wage Payment Tax Credit ...................... 1-9

Work Opportunity Tax Credit Extension and Modification ............................................. 1-9

Partnership Interests Created by Gift ................................................................................. 1-9

Loss Transfers Between Tax Indifferent Parties ................................................................ 1-9

Regulations First Effective in 2016 .................................................................... 1-10

Chart of All 2016 Federal Tax Regulations ....................................................................... 1-10

T.D. 9752; Reg. 1.6038D-1, -2, -6 (2/22/2016) -- Final Regulations On Specified Foreign Financial Asset (SFFA) Form 8938 Reporting By Domestic Entities ............................. 1-10

Background ....................................................................................................................... 1-10

2016 Final Regulations ..................................................................................................... 1-12

Effective Date. ................................................................................................................... 1-12

Specified Domestic Entity (SDE). .................................................................................... 1-12

Definition of SDE for Partnerships and Corporations.................................................. 1-12

Domestic Trusts ................................................................................................................ 1-16

©2016. These materials are copyrighted and may not be reproduced or distributed in whole or in part without permission of the authors/CalCPA Education Foundation.

Copyri

ght 2

016-1

7

2016 McBride/Nellen Federal and California Update for Businesses and Estates

Chapter 1: 2016 Legislation and Code/Regs. First Effective in 2016 Page 1-2

REG-163113-02 (8/4/16) Prop. Regs. 25.2701-2,-8, 25.2704-1, -2, -3, -4; IRS Issues Proposed Regulations on Gift and Estate Tax Valuations ............................................... 1-18

T.D. 9728; Regs. 1.706-1, -4, -5 (Aug. 3, 2015) -- Final Regulations on Varying Interest Rules for Partnership TYB On or After Aug. 3, 2015 ...................................................... 1-19

Variations Subject to Varying Interest Rules ................................................................ 1-19

General Rule of Segments and Proration Periods ......................................................... 1-20

Step-by-Step Approach (Ten Steps) ................................................................................ 1-21

Example of Step-by-Step Approach (Reg. 1.706-4(a)(4) Example (Modified) ............ 1-22

Exceptions (Reg. 1.706-4((b)) ........................................................................................... 1-24

Conventions (Reg. 1.706-4((c)) ........................................................................................ 1-26

Optional Regular Monthly Or Semi-Monthly Interim Closings (Reg. 1.706-4(d)) .... 1-28

Extraordinary Items (Reg. 1.706-4(e) ............................................................................. 1-29

Agreement of the Partners (Full text of Reg. 1.706-4(f)) .............................................. 1-33

Effective Date (Reg. 1.706-4(g)) ....................................................................................... 1-33

Inflation Adjustments ................................................................................................ 1-34

2017 Inflation Adjustments – Rev. Proc. 2016-55 ............................................................. 1-34

2017 Social Security Wage Base is $127,200 ...................................................................... 1-34

2016 Legislation P.L. 114-125 (2/24/16), Trade Facilitation and Trade Enforcement Act of 2015

P.L. 114-125 makes these two tax changes:

a. Increase in FTF Penalty - Increases the §6651(a) penalty for failure to file a return from $135 to $205, effective for returns required to be filed after 2015. The change is the last sentence of §6651(a):

“In the case of a failure to file a return of tax imposed by chapter 1 within 60 days of the date prescribed for filing of such return (determined with regard to any extensions of time for filing), unless it is shown that such failure is due to reasonable cause and not due to willful neglect, the addition to tax under paragraph (1) shall not be less than the lesser of $135 $205 or 100 percent of the amount required to be shown as tax on such return.”

This amount is adjusted annually for inflation.

CBO estimates this change will raise $202 million over ten years (12/10/15 cost estimate on H.R. 644).

©2016. These materials are copyrighted and may not be reproduced or distributed in whole or in part without permission of the authors/CalCPA Education Foundation.

Copyri

ght 2

016-1

7

2016 McBride/Nellen Federal and California Update for Businesses and Estates

Chapter 1: 2016 Legislation and Code/Regs. First Effective in 2016 Page 1-3

b. Made the Internet Tax Freedom Act (ITFA) moratorium permanent and, effective after June 30, 2020, removed the grandfather provision (relevant to Hawaii, New Mexico, North Dakota, Ohio, South Dakota, Texas, and Wisconsin). This moratorium was originally enacted in 1998 and renewed a few times. See further discussion in the Multistate Tax portion of the outline.

Continuing Appropriations Legislation FY2017 –

P.L. 114-223 (9/29/16; H.R. 5325) This legislation funds the government through December 9, 2016. Thus, Congress left the full funding activity until after the November elections.

Prior Law First Effective in 2016

New 2016 Filing Requirements

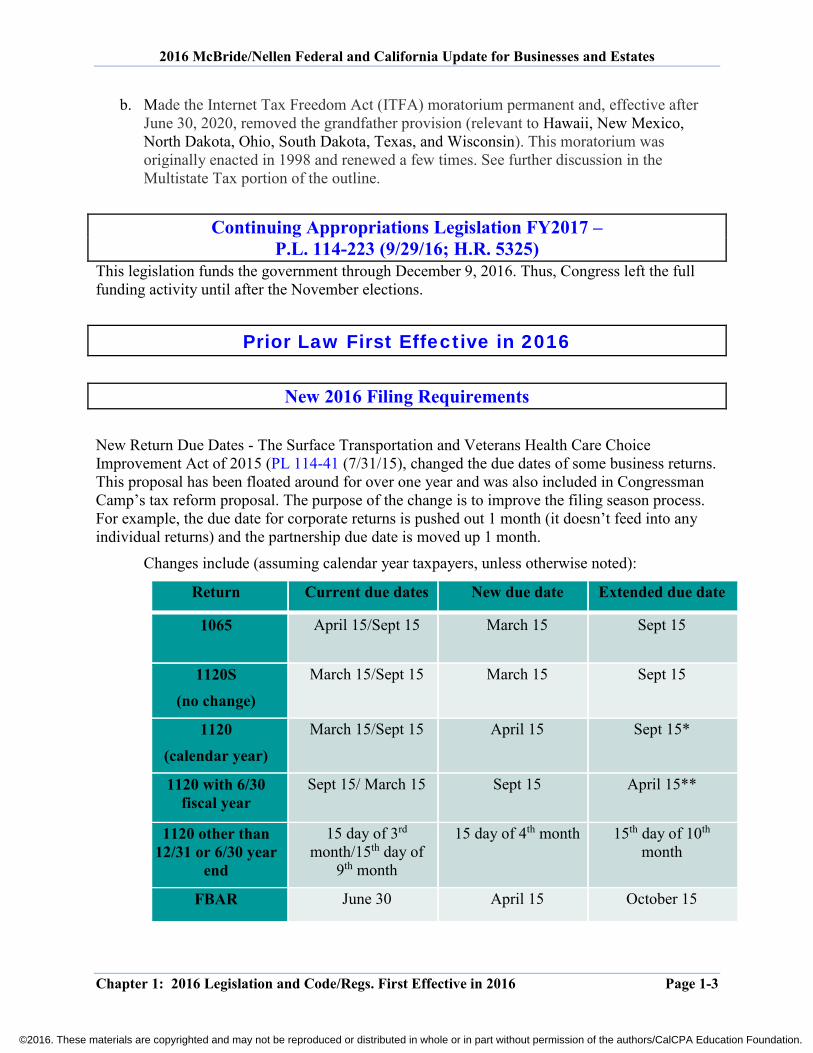

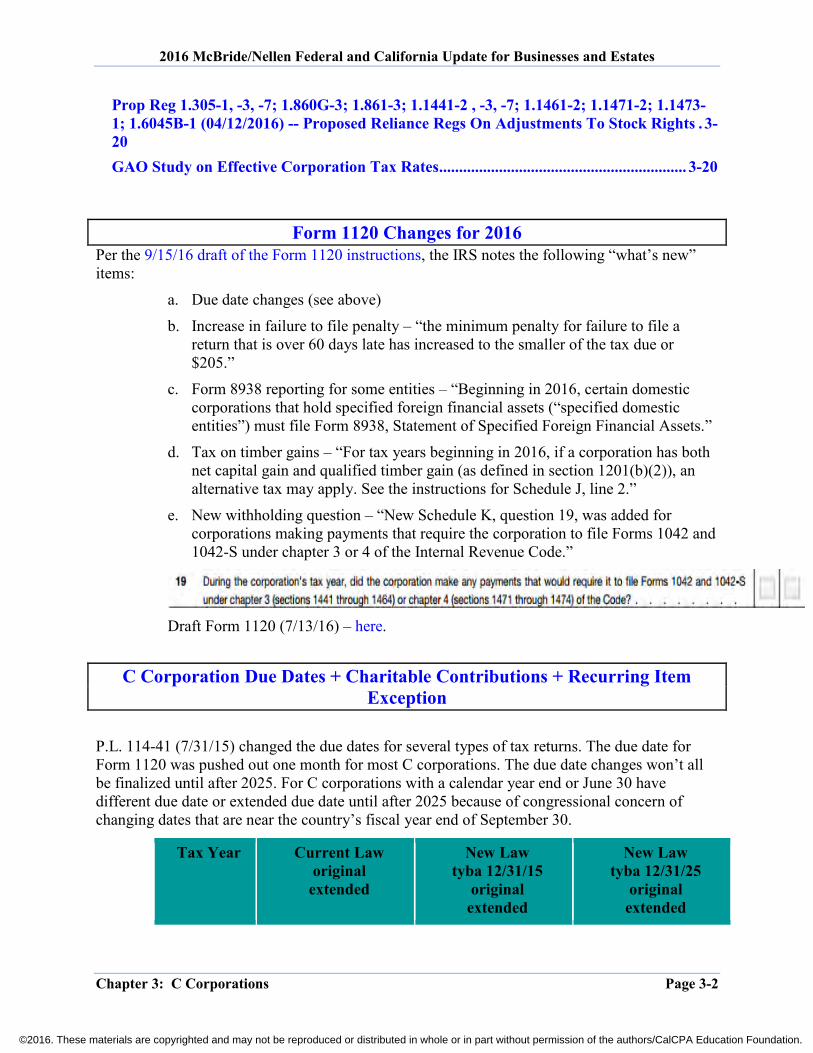

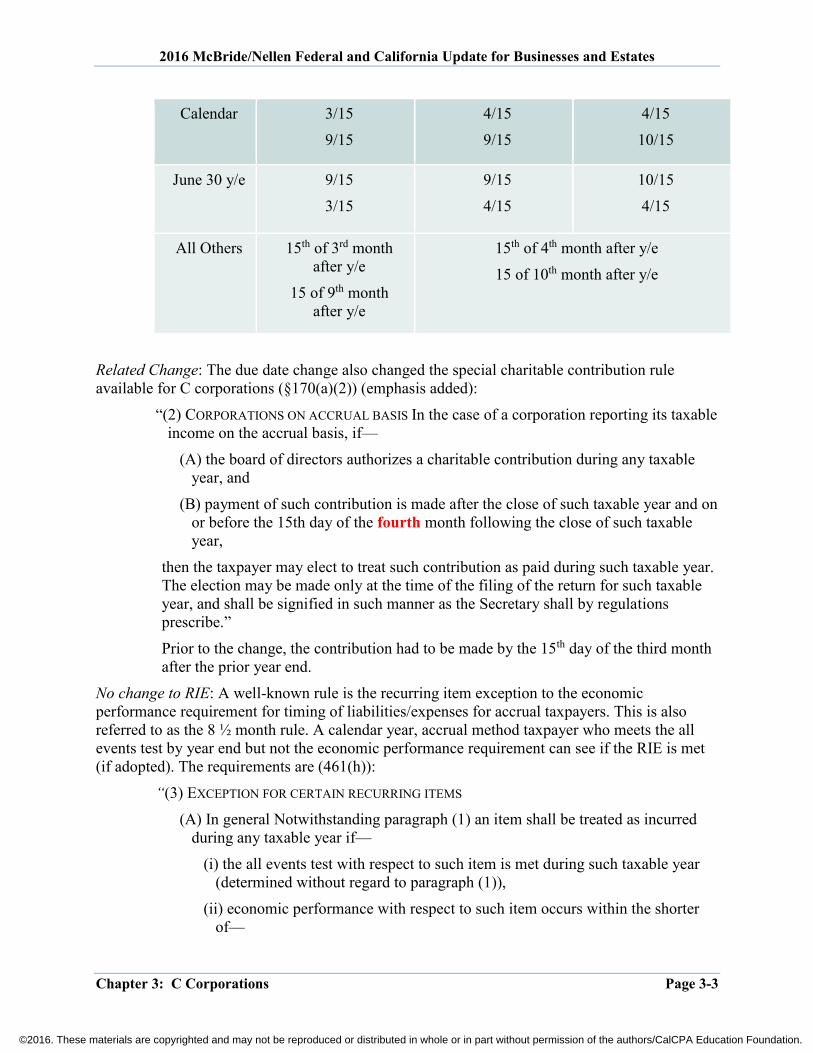

New Return Due Dates - The Surface Transportation and Veterans Health Care Choice Improvement Act of 2015 (PL 114-41 (7/31/15), changed the due dates of some business returns. This proposal has been floated around for over one year and was also included in Congressman Camp’s tax reform proposal. The purpose of the change is to improve the filing season process. For example, the due date for corporate returns is pushed out 1 month (it doesn’t feed into any individual returns) and the partnership due date is moved up 1 month.

Changes include (assuming calendar year taxpayers, unless otherwise noted):

Return Current due dates New due date Extended due date

1065 April 15/Sept 15 March 15 Sept 15

1120S (no change)

March 15/Sept 15 March 15 Sept 15

1120 (calendar year)

March 15/Sept 15 April 15 Sept 15*

1120 with 6/30 fiscal year

Sept 15/ March 15 Sept 15 April 15**

1120 other than 12/31 or 6/30 year

end

15 day of 3rd month/15th day of

9th month

15 day of 4th month 15th day of 10th month

FBAR June 30 April 15 October 15

©2016. These materials are copyrighted and may not be reproduced or distributed in whole or in part without permission of the authors/CalCPA Education Foundation.

Copyri

ght 2

016-1

7

2016 McBride/Nellen Federal and California Update for Businesses and Estates

Chapter 1: 2016 Legislation and Code/Regs. First Effective in 2016 Page 1-4

*After 12/31/2025, C corps using a calendar year will have extended returns due October 15 (rather than September 15).

**The new due dates go into effect for 6/30 C corps for tax years beginning after 12/31/2015.

Conforming amendments were also made to other Code sections as needed, such as §170(a)(2)(B).

Effective dates: Generally, to returns for tax years beginning after 12/31/15. So, for filing 2016 returns (assuming calendar year).

Additional resources:

The AICPA has a nice chart summarizing all of the changes.

Sherr, “Why new tax return due date changes are important,” AICPA CPA Insider, 10/19/15.

JCT, Overview of Selected Provisions Relating To The Financing of Surface Transportation Infrastructure, JCX-97-15 (6/23/15).

Due Date for W-2 and 1099-MISC PATH modifies the filing dates of returns and statements relating to employee wage information and nonemployee compensation to improve compliance; generally, all forms are due to the IRS by January 31 (Sections 6071 and 6402). This change applies to 2016 returns and statements (due January 2017). See AICPA Due Date chart and new IRS instructions for Form 1099-MISC. These measures aim to help reduce identity theft.

Truncated SSN on Form W-2 PATH extends IRS authority to require truncated Social Security numbers on Form W–2 (§6051(a)(2)). IRS authority at §6109(d). Effective 12/18/15. Per the JCT, this change will allow the IRS to issue regulations “requiring or permitting” a truncated SSN on Form W-2 (JCS-1-16, 3/14/16, p. 336). For overview of IRS regulations on truncation, see Nellen, “TTINs and protecting taxpayer identities,” AICPA Tax Insider, 9/11/14. PATH and Deminimis Errors on Information Returns and Payee Statements

©2016. These materials are copyrighted and may not be reproduced or distributed in whole or in part without permission of the authors/CalCPA Education Foundation.

Copyri

ght 2

016-1

7

2016 McBride/Nellen Federal and California Update for Businesses and Estates

Chapter 1: 2016 Legislation and Code/Regs. First Effective in 2016 Page 1-5

PATH (P.L. 114-113 (12/18/16)) adds a safe harbor provision to §6721 to allow taxpayers to not have to re-issue certain information returns where there is an error of $100 or less. This changes applies to returns required to be filed and payee statements required to be provided after 12/31/16 (thus for 2016 forms).

Per the Joint Committee on Taxation, General Explanation of Tax Legislation Enacted in 2015 (JCS-1-16; March 2016), page 222:

“In general, a de minimis error of an amount on the information return or statement need not be corrected if the error for any single amount does not exceed $100. A lower threshold of $25 is established for errors with respect to the reporting of an amount of withholding or backup withholding. The provision requires broker reporting to be consistent with amounts reported on uncorrected returns which are eligible for the safe harbor. If any person receiving payee statements requests a corrected statement, the penalty for failure to file a correct information return and the penalty for failure to furnish a correct payee statement would continue to apply in the case of a de minimis error.”

Permanence and Enhancement of Food Inventory Donations

PATH made permanent the enhanced donation deduction for food inventory (§170(e)(3)(C)). Permanence is effective contributions after 12/31/14. The enhancements apply for tax years beginning after 12/31/15. Per the Joint Committee on Taxation, General Explanation of Tax Legislation Enacted in 2015 (JCS-1-16; March 2016), pages 130-131:

“The provision reinstates and makes permanent the enhanced deduction for contributions of food inventory for contributions made after December 31, 2014.

For taxable years beginning after December 31, 2015, the provision also modifies the enhanced deduction for food inventory contributions by: (1) increasing the charitable percentage limitation for food inventory contributions and clarifying the carryover and coordination rules for these contributions; (2) including a presumption concerning the tax basis of food inventory donated by certain businesses; and (3) including presumptions that may be used when valuing donated food inventory.

First, the ten-percent limitation described above applicable to taxpayers other than C corporations is increased to 15 percent. For C corporations, these contributions are made subject to a limitation of 15 percent of taxable income (as modified). The general ten-percent limitation for a C corporation does not apply to these contributions, but the ten-percent limitation applicable to other contributions is reduced by the amount of these contributions. Qualifying food inventory contributions in excess of these 15-percent limitations may be carried forward and treated as qualifying food inventory contributions in each of the five succeeding taxable years in order of time.

Second, if the taxpayer does not account for inventory under section 471 and is not required to capitalize indirect costs under section 263A, the taxpayer may elect, solely for computing the enhanced deduction for food inventory, to treat the basis of any apparently wholesome food as being equal to 25 percent of the fair market value of such food.

©2016. These materials are copyrighted and may not be reproduced or distributed in whole or in part without permission of the authors/CalCPA Education Foundation.

Copyri

ght 2

016-1

7

2016 McBride/Nellen Federal and California Update for Businesses and Estates

Chapter 1: 2016 Legislation and Code/Regs. First Effective in 2016 Page 1-6

Third, in the case of any contribution of apparently wholesome food which cannot or will not be sold solely by reason of internal standards of the taxpayer, lack of market, or similar circumstances, or by reason of being produced by the taxpayer exclusively for the purposes of transferring the food to an organization described in section 501(c)(3), the fair market value of such contribution shall be determined (1) without regard to such internal standards, such lack of market or similar circumstances, or such exclusive purpose, and (2) by taking into account the price at which the same or substantially the same food items (as to both type and quality) are sold by the taxpayer at the time of the contributions (or, if not so sold at such time, in the recent past).”

Expensing for Live Theatrical Productions The 2015 PATH Act extends the election to expense qualified film and television production costs for two years, to cover productions commencing in 2015-2016. For productions commencing after 2015, the election is expanded to cover qualified live theatrical productions. Per the JCT Bluebook:

A qualified live theatrical production is defined as a live staged pro- duction of a play (with or without music) which is derived from a written book or script and is produced or presented by a commercial entity in any venue which has an audience capacity of not more than 3,000, or a series of venues the majority of which have an audience capacity of not more than 3,000. In addition, qualified live theatrical productions include any live staged production which is produced or presented by a taxable entity no more than 10 weeks annually in any venue which has an audience capacity of not more than 6,500. In general, in the case of multiple live-staged productions, each such live-staged production is treated as a separate production. Similar to the exclusion for sexually explicit productions from the present-law definition of qualified productions, qualified live theatrical productions do not include stage performances that would be excluded by section 2257(h)(1) of title 18 of the U.S. Code, if such provision were extended to live stage performances. …. The modifications for live theatrical productions apply to productions commencing after December 31, 2015. For purposes of this provision, the date on which a qualified live theatrical production commences is the date of the first public performance of such production for a paying audience.

Research Credit Usable Against AMT for Eligible Small Businesses

PL 114-113 (12/18/16) (PATH) modified the credit to allow eligible small businesses to use the research tax credit against AMT effective for credits determined for tyba 12/31/15. Following is an explanation and example from the Joint Committee on Taxation, General Explanation of Tax Legislation Enacted in 2015 (JCS-1-16; March 2016), pages 136-137.

©2016. These materials are copyrighted and may not be reproduced or distributed in whole or in part without permission of the authors/CalCPA Education Foundation.

Copyri

ght 2

016-1

7

2016 McBride/Nellen Federal and California Update for Businesses and Estates

Chapter 1: 2016 Legislation and Code/Regs. First Effective in 2016 Page 1-7

“in the case of an eligible small business (as defined in section 38(c)(5)(C), after application of rules similar to the rules of section 38(c)(5)(D)), the research credit determined under section 41 for taxable years beginning after December 31, 2015, is a specified credit. Thus, these research credits of an eligible small business may offset both regular tax and AMT liabilities.”

Example from Footnote 403: “Assume a taxpayer has a regular tax liability of $80,000, a tentative minimum tax of $100,000, and a research credit determined under section 41 of $90,000 for the taxable year (and no other credits). Under present law, the taxpayer’s research credit is limited to the excess of $100,000 over the greater of (1) $100,000 or (2) $13,750 (25% of the excess of $80,000 over $25,000). Accordingly, no research credit may be claimed ($100,000 – $100,000 = $0) for the taxable year and the taxpayer’s net tax liability is $100,000. The $90,000 research credit may be carried back or forward under the rules applicable to the general business credit.”.

Example of law change from Footnote 412: “the limitation would be the excess of $100,000 over the greater of (1) $0 or (2) $13,750. Since $13,750 is greater than $0, the $100,000 would be reduced by $13,750 such that the research credit would be limited to $86,250. Hence, the taxpayer would be able to claim a research credit of $86,250 against its $100,000 net income tax (the sum of $80,000 regular tax liability and $20,000 alternative minimum tax), which would result in $13,750 of total net tax owed ($100,000—$86,250). The remaining $3,750 of its research credit ($90,000—$86,250) may be carried back or forward, as applicable.”

Research Credit Available Against Payroll Taxes for Start-ups

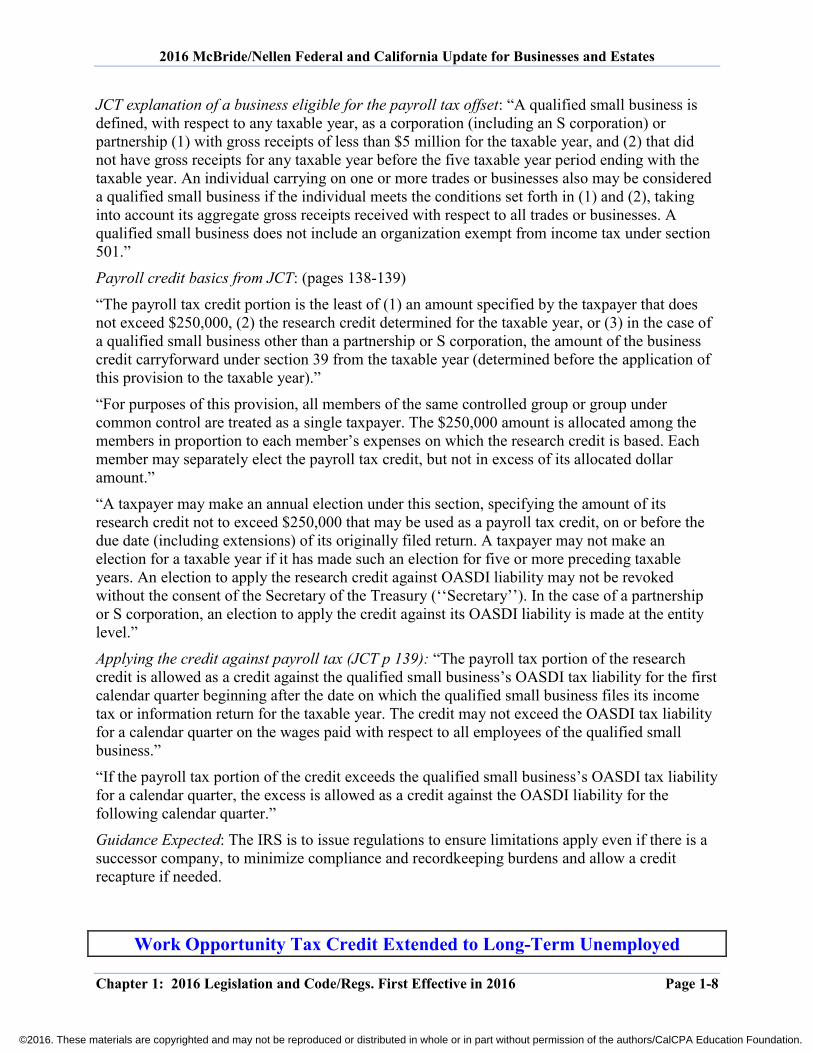

Research Credit and Payroll Taxes – PL 114-113 (12/18/16) (PATH) made the research tax credit permanent and made a few taxpayer favorable modifications. One of the modifications is to allow certain start-up businesses to use the credit against payroll taxes (limited to $250,000) for tax years beginning after 12/31/15. The draft Form 6765 for 2016 has a new Section D for this calculation, which also affects payroll returns (see Form 941 and 2017 draft form). The draft 2017 Form 941 refers to Form 8974, Qualified Small Business Payroll Tax Credit for Increasing Research Activities, which is attached to Form 941.

Interaction with §280C(c): Per the JCT Bluebook for PATH – “If a taxpayer makes an election under this provision, the amount so elected is treated as a research credit for purposes of section 280C.414

fn414 “Thus, taxpayers are either denied a section 174 deduction in the amount of the credit or may elect a reduced research credit amount. The election is not taken into account for purposes of determining any amount allowable as a payroll tax deduction.”

©2016. These materials are copyrighted and may not be reproduced or distributed in whole or in part without permission of the authors/CalCPA Education Foundation.

Copyri

ght 2

016-1

7

2016 McBride/Nellen Federal and California Update for Businesses and Estates

Chapter 1: 2016 Legislation and Code/Regs. First Effective in 2016 Page 1-8

JCT explanation of a business eligible for the payroll tax offset: “A qualified small business is defined, with respect to any taxable year, as a corporation (including an S corporation) or partnership (1) with gross receipts of less than $5 million for the taxable year, and (2) that did not have gross receipts for any taxable year before the five taxable year period ending with the taxable year. An individual carrying on one or more trades or businesses also may be considered a qualified small business if the individual meets the conditions set forth in (1) and (2), taking into account its aggregate gross receipts received with respect to all trades or businesses. A qualified small business does not include an organization exempt from income tax under section 501.”

Payroll credit basics from JCT: (pages 138-139)

“The payroll tax credit portion is the least of (1) an amount specified by the taxpayer that does not exceed $250,000, (2) the research credit determined for the taxable year, or (3) in the case of a qualified small business other than a partnership or S corporation, the amount of the business credit carryforward under section 39 from the taxable year (determined before the application of this provision to the taxable year).”

“For purposes of this provision, all members of the same controlled group or group under common control are treated as a single taxpayer. The $250,000 amount is allocated among the members in proportion to each member’s expenses on which the research credit is based. Each member may separately elect the payroll tax credit, but not in excess of its allocated dollar amount.”

“A taxpayer may make an annual election under this section, specifying the amount of its research credit not to exceed $250,000 that may be used as a payroll tax credit, on or before the due date (including extensions) of its originally filed return. A taxpayer may not make an election for a taxable year if it has made such an election for five or more preceding taxable years. An election to apply the research credit against OASDI liability may not be revoked without the consent of the Secretary of the Treasury (‘‘Secretary’’). In the case of a partnership or S corporation, an election to apply the credit against its OASDI liability is made at the entity level.”

Applying the credit against payroll tax (JCT p 139): “The payroll tax portion of the research credit is allowed as a credit against the qualified small business’s OASDI tax liability for the first calendar quarter beginning after the date on which the qualified small business files its income tax or information return for the taxable year. The credit may not exceed the OASDI tax liability for a calendar quarter on the wages paid with respect to all employees of the qualified small business.”

“If the payroll tax portion of the credit exceeds the qualified small business’s OASDI tax liability for a calendar quarter, the excess is allowed as a credit against the OASDI liability for the following calendar quarter.”

Guidance Expected: The IRS is to issue regulations to ensure limitations apply even if there is a successor company, to minimize compliance and recordkeeping burdens and allow a credit recapture if needed.

Work Opportunity Tax Credit Extended to Long-Term Unemployed

©2016. These materials are copyrighted and may not be reproduced or distributed in whole or in part without permission of the authors/CalCPA Education Foundation.

Copyri

ght 2

016-1

7

2016 McBride/Nellen Federal and California Update for Businesses and Estates

Chapter 1: 2016 Legislation and Code/Regs. First Effective in 2016 Page 1-9

The 2015 PATH Act extended the deadline for employing eligible members of targeted groups for purposes of claiming the Work Opportunity Tax Credit (WOTC), to cover hiring that occurs in 2015-2019 (section 51(c)(4)). After 2015, the PATH Act also modified the WOTC rules to benefit employers that hire qualified long-term unemployed individuals (those who have been unemployed for 27 weeks or more), with the credit amount for those individuals is equal to 40% of the first $6,000 of wages (section 51(d)).

More Employers Are Eligible for Differential Wage Payment Tax Credit The PATH Act made permanent the tax credit for employers that provide differential pay to employees while they serve in the military. The credit equals 20% of differential pay of up to $20,000 paid to each qualifying employee during the applicable year. In addition, beginning in 2016, the PATH Act makes the credit available to employers of any size, rather than just small employers with 50 or fewer workers. The credit applies to differential wage payments to qualifying employees for periods that they are called to active duty with U.S. uniformed services for more than 30 days. (section 45P)

Work Opportunity Tax Credit Extension and Modification PATH extended and modified the WOTC (51(c)(4)) to include “qualified long-term unemployment recipients.” The extension is effective for individuals who starts work after 12/31/14. The modification applies for those who start work after 12/31/15. See Notice 2016-22 and Notice 2016-40 for guidance and transition relief. Form 8850, Pre-Screening Notice and Certification Request for the Work Opportunity Credit, has been updated.

Partnership Interests Created by Gift P.L. 114-74 (11/2/15) – Bipartisan Budget Act of 2015 - Modifies §761 for partnership interests created by gift. For partnership TYBA 12/31/15.

Loss Transfers Between Tax Indifferent Parties Section 267(d) was modified by PATH for sales and other dispositions of property acquired after 12/31/15 in a sale or exchange to which §267(a)(1) applied. Per the Joint Committee on Taxation, General Explanation of Tax Legislation Enacted in 2015 (JCS-1-16; March 2016), page 313:

“The provision provides that the general rule of section 267(d) does not apply to the extent gain or loss with respect to property that has been sold or exchanged is not subject to Federal income

©2016. These materials are copyrighted and may not be reproduced or distributed in whole or in part without permission of the authors/CalCPA Education Foundation.

Copyri

ght 2

016-1

7

2016 McBride/Nellen Federal and California Update for Businesses and Estates

Chapter 1: 2016 Legislation and Code/Regs. First Effective in 2016 Page 1-10

tax in the hands of the transferor immediately before the transfer but any gain or loss with respect to the property is subject to Federal income tax in the hands of the transferee immediately after the transfer. Thus, the basis of the property in the hands of the transferee will be its cost for purposes of determining gain or loss, thereby precluding a loss importation result.”

“The provision applies to sales and other dispositions of property acquired after December 31, 2015, by the taxpayer in a sale or exchange to which section 267(a)(1) applied.”

Regulations First Effective in 2016

Chart of All 2016 Federal Tax Regulations For a complete list of regulations issued by the IRS and Treasury in 2016, see http://www.sjsu.edu/people/annette.nellen/website/2016regs.html. T.D. 9752; Reg. 1.6038D-1, -2, -6 (2/22/2016) -- Final Regulations On Specified

Foreign Financial Asset (SFFA) Form 8938 Reporting By Domestic Entities

Background Section 6038D, enacted as part of The Hiring Incentives to Restore Employment Act in 2010, requires certain individuals and specified domestic entities to report information about specified foreign financial assets (SFFAs). SFFAs are reported, as an attachment to the income tax return, on Form 8938. "Specified foreign financial assets," include financial accounts held at foreign financial institutions, and stocks, securities, financial instruments, contracts, or interests issued or held by a foreign person or entity. Section 6038D(f) extends SFFA reporting, to the extent provided in regulations, to domestic entities such as U.S. partnerships, corporations, and trusts; therefore, the regulations declare that a “specified person” subject to Form 8938 reporting is a “specified individual or a specified domestic entity.” Reg. 1.6038D-1(a)(1). Specified individuals include U.S. citizens and resident aliens of the United States for any portion of the tax year. Regarding specified individuals, the IRS issued temporary regulations on Dec. 19, 2011 (TD 9567) addressing the Form 8938 reporting requirements and those rules were finalized on Dec. 12, 2014 (TD 9706). On Dec. 19, 2011 (REG-130302-10) the IRS published proposed regulations addressing the reporting requirements for specified domestic entities (SDEs); however, the 2014 final regulations covered only SFFA reporting by individuals and reserved coverage of reporting by domestic entities. Notice 2013-10 clarified that reporting by domestic entities of interests in SFFAs would not be required before the date specified by final regulations.

©2016. These materials are copyrighted and may not be reproduced or distributed in whole or in part without permission of the authors/CalCPA Education Foundation.

Copyri

ght 2

016-1

7

2016 McBride/Nellen Federal and California Update for Businesses and Estates

Chapter 1: 2016 Legislation and Code/Regs. First Effective in 2016 Page 1-11

The 2014 final regulations did specify the applicable reporting threshold for SDEs: The section 6038D requirement would only apply to domestic entities if the aggregate value of a domestic entity’s SFFAs exceeds: (1) $50,000 on the last day of the taxable year, or (2) $75,000 at any time during the taxable year. (Reg. 1.6038D-2(a)(1)). With respect to entities, the 2014 final regulations further explain that:

A “specified person is not treated as having an interest in any specified foreign financial assets held by a corporation, partnership, trust, or estate solely as a result of the specified person's status as a shareholder, partner, or beneficiary of such entity.” (Reg. 1.6038D-2(b)(4)(i)) A “specified person that is treated as the owner of a trust or any portion of a trust under sections 671 through 679 [a grantor trust]” with limited exceptions, “is treated as having an interest in any specified foreign financial assets held by the trust or the portion of the trust.” (Reg. 1.6038D-2(b)(4)(ii)) A specified person that owns a foreign or domestic disregarded entity “is treated as having an interest in any specified foreign financial assets held by the disregarded entity.” (Reg. 1.6038D-2(b)(4)(iii))

Specified persons are not required to report an SFFA on Form 8938 if the specified person reports the asset on at least one of the following IRS Forms:

3520, “Annual Return To Report Transactions With Foreign Trusts and Receipt of Certain Foreign Gifts” (“in the case of a specified person that is the beneficiary of a foreign trust”);

5471, “Information Return of U.S. Persons With Respect To Certain Foreign Corporations”;

Form 8621, “Return by a Shareholder of a Passive Foreign Investment Company or Qualified Electing Fund”;

Form 8865, “Return of U.S. Persons With Respect To Certain Foreign Partnerships”; For taxable years beginning after March 18, 2010, and ending on or before December 31,

2013, Form 8891, “U.S. Information Return for Beneficiaries of Certain Canadian Registered Retirement Plans”

Instead of reporting the SFFA on Form 8938, the specified person reports on Form 8938 the form (above) on which the SFFA was reported. (Reg. 6038D-7(a)(1)(i) and (ii)) A specified person treated as the owner of a foreign trust or any portion of a foreign trust under sections 671 through 679 is not required to report any SFFAs held by the foreign trust on Form 8938, provided—

(i) The specified person reports the trust on a Form 3520 timely filed; (ii) The trust timely files Form 3520-A, “Annual Information Return of Foreign Trust With

a U.S. Owner,”; and (iii) The Form 8938 filed by the specified person reports the filing of the Form 3520 and

Form 3520-A. (Reg. 6038D-7(a)(2))

©2016. These materials are copyrighted and may not be reproduced or distributed in whole or in part without permission of the authors/CalCPA Education Foundation.

Copyri

ght 2

016-1

7

2016 McBride/Nellen Federal and California Update for Businesses and Estates

Chapter 1: 2016 Legislation and Code/Regs. First Effective in 2016 Page 1-12

Observation: The Form 8938 filing requirement in IRC section 6038D is in addition to the Report of Foreign Bank and Financial Accounts (FBAR) reporting requirement imposed by Title 31 (not the Internal Revenue Code which is Title 26). Per the IRS website:

“The new Form 8938 filing requirement does not replace or otherwise affect a taxpayer’s obligation to file FinCEN Form 114 (Report of Foreign Bank and Financial Accounts). Unlike Form 8938, the FBAR (FinCEN Form 114) is not filed with the IRS. It must be filed directly with the office of Financial Crimes Enforcement Network (FinCEN), a bureau of the Department of the Treasury, separate from the IRS.”

IRS Chart: Comparison of Form 8938 and FBAR Requirements

2016 Final Regulations Effective Date. The final regulations are effective for tax years that begin after Dec. 31, 2015.

Specified Domestic Entity (SDE). “A specified domestic entity is a domestic corporation, a domestic partnership, or a trust described in section 7701(a)(30)(E), if such corporation, partnership, or trust is formed or availed of for purposes of holding, directly or indirectly, specified foreign financial assets. Whether a domestic corporation, a domestic partnership, or a trust described in section 7701(a)(30)(E) is a specified domestic entity is determined annually.” (Reg. 1.6038D-6(a))

Definition of SDE for Partnerships and Corporations The 2016 final regulations set forth two objective conditions to establish if a corporation or partnership is “formed or availed of” for the purpose of holding SFFAs thus making the entity a “specified domestic entity” (SDE). To be an SDE:

1) The entity must be closely held. For corporations, closely held means that a specified individual owns directly,

indirectly or constructively, at least 80 percent (by vote or value) of the corporation, on the last day of the corporation’s tax year.

For partnerships, closely held means that a specified individual holds directly, indirectly or constructively, at least 80 percent of the capital or profits interest on the last day of the partnership’s tax year.

Constructive Ownership: “[S]ections 267(c) and (e)(3) apply for the purpose of determining the constructive ownership of a specified individual in a corporation or partnership, except that section 267(c)(4) is applied as if the family of an individual includes the spouses of the individual's family members.” Per section 267(c)(4): “[t]he family of an individual shall include only his brothers and sisters (whether by

©2016. These materials are copyrighted and may not be reproduced or distributed in whole or in part without permission of the authors/CalCPA Education Foundation.

Copyri

ght 2

016-1

7

2016 McBride/Nellen Federal and California Update for Businesses and Estates

Chapter 1: 2016 Legislation and Code/Regs. First Effective in 2016 Page 1-13

the whole or half blood), spouse, ancestors, and lineal descendants.” Therefore, the spouses of ancestors, lineal descendants, and brothers and sisters are also included. (Reg. 1.6038D-6(b)(2)(iii))

2) At least 50% of the entity’s gross income for the tax year must be passive income or at

least 50% of the entity’s assets must produce or be held for the production of passive income. Passive income and assets generally include dividends, interests, rents and royalties

(unless the rents and royalties are “derived in the active conduct of a trade or business conducted, at least in part, by employees of the corporation or partnership), annuities, the excess of gains over losses from the sale or exchange of assets that generate passive income. (See Reg. 1.6038D-6(b)(3))

For purposes of applying the 50% passive income and asset thresholds “all domestic corporations and domestic partnerships that are closely held by the same specified individual … and that are connected through stock or partnership interest ownership with a common parent corporation or partnership are treated as owning the combined assets and receiving the combined income of all members of that group.” (See Reg. 1.6038D-6(b)(3)(iii))

The percentage of passive assets held by a corporation or partnership for a tax year is “the weighted average percentage of passive assets (weighted by total assets and measured quarterly), and the value of assets of a corporation or partnership is the fair market value of the assets or the book value of the assets that is reflected on the corporation's or partnership's balance sheet (as determined under either a U.S. or an international financial accounting standard).” Reg. 1.6038D-6(b)(1).

Observation: The final regulations eliminated the subjective principal purpose test for determining SDE status that was contained in the proposed regulations that included a corporation or partnership in which only 10% of the income or assets are passive where the entity was formed for the principal purpose of avoiding Form 8938 reporting based upon all of the facts and circumstances.

Reporting Threshold Aggregation Rule for SDEs. An SDE is only required to File Form 8938 if it also meets the reporting threshold: SFFAs exceeding either $50,000 on the last day of the taxable year, $75,000 at any time during the taxable year. (Reg. 1.6038D-2(a)(1)). For purposes of determining if an SDE meets the reporting threshold, the following aggregation rule applies:

“The value of any specified foreign financial asset in which a specified domestic entity has an interest and that is excluded from reporting on Form 8938 pursuant to § 1.6038D-7(a) (concerning certain assets reported on another form) is excluded for purposes of determining the aggregate value of specified foreign financial assets. For purposes of determining the aggregate value of specified foreign financial assets, a specified domestic entity that is a corporation or partnership and that has an interest in any specified foreign financial asset is treated as owning all the specified foreign financial assets (excluding specified

©2016. These materials are copyrighted and may not be reproduced or distributed in whole or in part without permission of the authors/CalCPA Education Foundation.

Copyri

ght 2

016-1

7

2016 McBride/Nellen Federal and California Update for Businesses and Estates

Chapter 1: 2016 Legislation and Code/Regs. First Effective in 2016 Page 1-14

foreign financial assets excluded from reporting on Form 8938 pursuant to § 1.6038D-7(a)) held by all domestic corporations and domestic partnerships that are closely held by the same specified individual as determined under §1.6038D-6(b)(2).” (Reg. 1.6038D-2(a)(6)(ii)) (Emphasis added)

Example. Individual: Facts. L is a specified individual. After considering family attribution, L owns a 90% capital interest in a family limited partnership (FLP). L does not own any other closely held businesses. 50% of FLP’s gross income is passive. The FLP assets include SFFAs with a maximum value of $90,000 during the tax year. Analysis. Because FLP is closely held by a specified individual and 50% of the gross income is passive, FLP is a specified domestic entity (SDE). Conclusion: Because FLP is an SDE with SFFAs exceeding the filing threshold ($75,000 maximum value during the year), FLP must file Form 8938 as an attachment to Form 1065. Observation: The broad aggregation rule applicable to the reporting threshold should not be confused with the narrower aggregation rule applicable to the passive income or assets test. Example (1) in Reg. 1.6038D-6(b)(3)(iii) -- Closely Held and Constructive Ownership. Facts DC1 is a domestic corporation the total value of the stock of which is owned 60% by A, a

specified individual, 30% by B, a member of A's family for purposes of section 267(c)(2) who is not a specified individual, and 10% by FC1, a foreign corporation.

DC1 owns 90% of the total value of the stock of DC2, a domestic corporation. FC2, a foreign corporation, owns 10% of DC2.

Neither A nor B owns, directly, indirectly, or constructively, any stock in FC1 or FC2. Closely held ownership determination A is considered to own 90% and 81% of the total value of DC1 and DC2, respectively, by

application of the rules of section 267(c) and this section. DC1 and DC2 are closely held by A because A, a specified individual, is considered to own

more than 80% of their total value. Example (2) in Reg. 1.6038D-6(b)(3)(iii) (modified)-- Application of Aggregation Rule and Reporting Threshold. Facts L is a specified individual. In Year X, L wholly owns DC1, a domestic corporation, and also owns a 90% capital interest

in DP, a domestic partnership. DC1 owns 80% of the sole class of stock of DC2, a domestic corporation. DC1 has no assets other than its interest in DC2. DC2's only assets are assets that produce passive income, with a maximum value in Year X

of $40,000 on October 12. DC2's assets are comprised in relevant part of SFFAs with a maximum value in Year X of

$15,000 on October 12. DP's only assets are assets that produce passive income and that are SFFAs with a maximum

value of $90,000 in Year X on October 12.

©2016. These materials are copyrighted and may not be reproduced or distributed in whole or in part without permission of the authors/CalCPA Education Foundation.

Copyri

ght 2

016-1

7

2016 McBride/Nellen Federal and California Update for Businesses and Estates

Chapter 1: 2016 Legislation and Code/Regs. First Effective in 2016 Page 1-15

Specified domestic entity status DC1 and DC2. DC1 and DC2 are closely held by a specified individual. DC1 and DC2 are considered related entities that are connected through stock ownership

with a common parent corporation, because DC1 and DC2 are closely held by L, and DC2 is connected with DC1 through DC1's ownership of stock of DC2 representing at least 80% of the voting power or value of DC2.

As a result, each of DC1 and DC2 is considered as owning the combined assets, and receiving the combined income, of both DC1 and DC2; however, DC1's equity interest in DC2 is disregarded for this purpose.

Therefore, DC1 and DC2 each satisfies the passive asset threshold, because 100 percent of each company's assets is passive.

DC1 and DC2 are specified domestic entities for Year X. DP DP is closely held by a specified individual. DP is not considered a related entity with DC1 and DC2, because DC1 and DP are not owned

by a common parent corporation or partnership. As a result, whether the 50% passive income or passive asset threshold is met with respect to

DP is determined solely by reference to DP's separately earned passive income and separately held passive assets.

DP holds only passive assets during Year X and therefore DP is a specified domestic entity for Year X.

Reporting requirements DC1 Under Sec. 1.6038D-2(a)(6)(ii), DC1 is not treated as owning the SFFAs held by DC2 and

DP for purposes of applying the reporting threshold, because DC1 does not have an interest in any SFFAs.

DC1 is not required to file Form 8938 because DC1 does not satisfy the reporting threshold. DC2 and DP Under Sec. 1.6038D-3, DC2 and DP each has an interest in SFFAs. For purposes of applying the reporting threshold, DC2 is treated as owning in addition to its

own assets the assets of DP, and DP is treated as owning in addition to its own assets the assets of DC2.

As a result, DC2 and DP each satisfies the reporting threshold of Sec. 1.6038D-2(a)(1), because the value of the SFFAs each is considered as owning is $105,000 on October 12, Year X, which exceeds DC2's and DP's $75,000 reporting threshold.

DC2 and DP must each file Form 8938 for Year X to report their respective SFFAs in which they have an interest and disclose their maximum values as provided in Sec. 1.6038D-4 ($15,000 in the case of DC2 and $90,000 in the case of DP).

Example (3) in Reg. 1.6038D-6(b)(3)(iii) (modified) -- Application of Aggregation Rule and Entity with an Active Trade Or Business. Facts The facts are the same as in Example 2 above, except that DC2 also owns an active business. The assets attributable to the business are not passive assets and constitute at least 60% of the

value of DC2's assets at all times during Year X.

©2016. These materials are copyrighted and may not be reproduced or distributed in whole or in part without permission of the authors/CalCPA Education Foundation.

Copyri

ght 2

016-1

7

2016 McBride/Nellen Federal and California Update for Businesses and Estates

Chapter 1: 2016 Legislation and Code/Regs. First Effective in 2016 Page 1-16

The income from the business is not passive income and constitutes at least 60% of the gross income generated by DC2 in Year X.

Specified domestic entity status. DC1 and DC2 DC1 and DC2 are considered related entities that are connected through stock ownership

with a common parent corporation because DC1 and DC2 are closely held by L, and DC2 is connected with DC1 though DC1's ownership of stock of DC2 representing at least 80% of the voting power or value of DC2.

As a result each of DC1 and DC2 is treated as owning the combined assets, and receiving the combined income, of both DC1 and DC2; however, DC1's equity interest in DC2 is disregarded.

As a result, no more than 40 percent of the value of DC1's and DC2's assets at all times during Year X are passive and no more than 40 percent of DC1's and DC2's gross income for Year X is passive.

DC1 and DC2 do not satisfy the passive income or passive asset threshold for Year X. DC1 and DC2 are not specified domestic entities for Year X.

DP For the reasons described in Example 2 above, DP is a specified domestic entity for Year X.

Reporting requirements DC1 and DC2 DC1 and DC2 are not specified domestic entities for Year X, and are not required to file

Form 8938. DP Under Sec. 1.6038D-3, DP has an interest in SFFAs.

Under Sec. 1.6038D-2(a)(6)(ii), DP is treated as owning in addition to its own assets the assets of DC2.

As a result, DP satisfies the reporting threshold of Sec. 1.6038D-2(a)(1) because the value of the specified foreign financial assets it is considered to own for purposes of Sec. 1.6038D-2(a)(1) is $105,000 on October 12, Year X, which exceeds DP's $75,000 reporting threshold.

DP must file Form 8938 for Year X to report the specified foreign financial assets in which it has an interest and disclose their maximum values as provided in Sec. 1.6038D-4, which is $90,000.

Domestic Trusts As a general rule a trust described in section 7701(a)(30)(E) is formed or availed of for purposes of holding, directly or indirectly, specified foreign financial assets (thus is an SDE) if and only if the trust has one or more specified persons as a current beneficiary. A “current beneficiary” is:

1) “any person who at any time during such taxable year is entitled to, or at the discretion of any person may receive, a distribution from the principal or income of the trust (determined without regard to any power of appointment to the extent that such power remains unexercised at the end of the taxable year).”

2) “any holder of a general power of appointment, whether or not exercised, that was exercisable at any time during the taxable year, but does not include any holder of a general power of appointment that is exercisable only on the death of the holder.” Reg. 1.6038D-6(c).

©2016. These materials are copyrighted and may not be reproduced or distributed in whole or in part without permission of the authors/CalCPA Education Foundation.

Copyri

ght 2

016-1

7

2016 McBride/Nellen Federal and California Update for Businesses and Estates

Chapter 1: 2016 Legislation and Code/Regs. First Effective in 2016 Page 1-17

The determination of whether a domestic trust is an SDE is made annually for each taxable year of the trust. A trust is described in Section 7701(a)(30)(E) as “any trust if--(i) a court within the United States is able to exercise primary supervision over the administration of the trust, and (ii) one or more United States persons have the authority to control all substantial decisions of the trust.” Exception Where Domestic Trust Not Required to File Form 1041. The preamble to the final regulations explains the issue:

Proposed §1.6038D-6(d) excepts certain entities from being treated as a specified domestic entity. A commenter recommended that the final regulations expand proposed §1.6038D-6(d) to also except certain domestic trusts that are not required to file a Form 1041, "U.S. Fiduciary Income Tax Return," or any information returns. The Treasury Department and the IRS do not adopt this comment because the 2014 final regulations already address the commenter's concerns. The 2014 final regulations provide in §1.6038D-2(a)(7) that a specified person, including a specified domestic entity, is not required to file Form 8938, "Statement of Specified Foreign Financial Assets," with respect to a taxable year if the specified person is not required to file an annual return with the IRS with respect to that taxable year. In the case of a specified domestic entity, the term "annual return" means an annual federal income tax return or information return filed with the IRS, including returns required under section 6012. See §1.6038D-1(a)(11). A Form 1041 is an annual return for purposes of §1.6038D-1(a)(11) of the final regulations. (TD 9752)

Excepted Domestic Entities. Grantor Trusts. A domestic trust or any portion of the trust that is treated as owned by one or more specified persons under sections 671 through 678 (the grantor trust rules) and the regulations issued under those sections is not considered to be a specified domestic entity.

Observation: A “specified person that is treated as the owner of a trust or any portion of a trust under sections 671 through 679 [a grantor trust]” with limited exceptions, “is treated as having an interest in any SFFAs held by the trust or the portion of the trust.” (Reg. 1.6038D-2(b)(4)(ii)). Therefore, the grantor, rather than the grantor trust, is subject to Form 8938 reporting of SFFAs owned by the grantor trust.

Other Exceptions:

A domestic entity is not considered to be an SDE if it is described in section 1473(3) and the regulations as excepted from the definition of the term “specified United States person”. This exception does not apply to any trust that is exempt from tax under section 664(c)--a charitable remainder annuity trust and a charitable remainder unitrust.

©2016. These materials are copyrighted and may not be reproduced or distributed in whole or in part without permission of the authors/CalCPA Education Foundation.

Copyri

ght 2

016-1

7

2016 McBride/Nellen Federal and California Update for Businesses and Estates

Chapter 1: 2016 Legislation and Code/Regs. First Effective in 2016 Page 1-18

A domestic trust is not considered an SDE if the trustee is a bank, financial institution, or domestic corporation that is subject to certain examination, oversight or registration requirements, has supervisory authority over or fiduciary obligations with regard to the trust’s specified foreign financial assets, and files income tax returns and information returns on behalf of the trust.

REG-163113-02 (8/4/16) Prop. Regs. 25.2701-2,-8, 25.2704-1, -2, -3, -4; IRS Issues Proposed Regulations on Gift and Estate Tax Valuations

IRS proposes significant changes to Reg. 25.2701 and 25. 2704-2 and -3.

Per the preamble to the regulations: “these proposed regulations concern the treatment of certain lapsing rights and restrictions on liquidation in determining the value of the transferred interests. These proposed regulations affect certain transferors of interests in corporations and partnerships and are necessary to prevent the undervaluation of such transferred interests.”

Among other things, the proposed rules disregard certain restrictions on the liquidation or redemption of interests if such restrictions may be removed by the transferor or the transferor's family after the transfer. In addition, restrictions that defer the payment of liquidation proceeds for more than six months or permit payment in any manner other than cash or other property will be disregarded. The regulations, if finalized, eliminate valuation discounts (such as due to lack of control) for gift and estate tax purposes on transfers of interests in family entities.

A public hearing is scheduled for 12/1/16. If finalized, a few provisions would not be effective until 30 days afterwards. With the current administration coming to an end, there may be a rush to get the regulations finalized soon after the hearing.

Why issued: Per the White House, “reduces tax avoidance by making it more difficult for the wealthiest Americans to exploit this loophole and avoid contributing their fair share. The tax avoiding activity that this action addresses is quite significant.”

Proposed Effective Date. The regulations are proposed to apply to rights created after 10/8/1990, where the lapse occurs on or after the date the regulations are finalized. In addition, the rules are proposed to apply to property restrictions created after 10/8/1990, where the transfer occurs 30 days or more after the date the regulations are finalized.

Planning: Taxpayers with significant assets to transfer inter-family should consider accelerating setting up appropriate entities and making transfers before the regulations are finalized as well as evaluating timing of transfers in existing entities.

Legislation Introduced to Stop the Proposed Valuation Discount Regulations:

H.R. 6042, To nullify certain proposed regulations relating to restrictions on liquidation of an interest with respect to estate, gift, and generation-skipping transfer taxes – Introduced by Congressman Sensenbrenner (R-WI). See 9/15 press release. The text is as follows:

“Regulations proposed for purposes of section 2704 of the Internal Revenue Code of 1986 relating to restrictions on liquidation of an interest with respect to estate, gift, and generation-skipping transfer taxes, published on August 4, 2016

©2016. These materials are copyrighted and may not be reproduced or distributed in whole or in part without permission of the authors/CalCPA Education Foundation.

Copyri

ght 2

016-1

7

2016 McBride/Nellen Federal and California Update for Businesses and Estates

Chapter 1: 2016 Legislation and Code/Regs. First Effective in 2016 Page 1-19

(81 Fed. Reg. 51413), and any substantially similar regulations hereafter promulgated, shall have no force or effect.”

Protect Family Farms and Business Act – introduced by Congressman Davidson (D-OH) – see text (no bill number as of 9/23/16) and explanation (9/21 press release). The text of the bill is as follows:

“The proposed regulations under section 2704 of the Internal Revenue Code of 1986 relating to restrictions on liquidation of an interest with respect to estate, gift, and generation-skipping transfer taxes, published on August 4, 2016, in the Federal Register (81 Fed. Reg. 51413) shall have no force or effect. No Federal funds may be used to finalize, implement, administer, or enforce such proposed regulations or any substantially similar regulations.”

Resources:

REG-163113-02 (8/4/16)

AICPA Resources

White House, Closing an Estate Tax Loophole for the Wealthiest Few: What You Need to Know, 8/3/16

Treasury blog post of 8/2/16

“The Controversial Way Wealthy Americans Are Lowering Their Estate Taxes,” Saunders, Wall Street Journal, 8/19/16.

T.D. 9728; Regs. 1.706-1, -4, -5 (Aug. 3, 2015) -- Final Regulations on Varying

Interest Rules for Partnership TYB On or After Aug. 3, 2015 IRS issued final regulations on the determination of a partner's distributive share of partnership items of income, gain, loss, deduction, and credit when a partner's interest varies during a partnership tax year. The final regulations also modify the existing regulation on the required tax year of a partnership.

Variations Subject to Varying Interest Rules A Variation. Reg. 1.706-4 provides rules for determining the partners' distributive shares of partnership items when a partner's interest in a partnership varies during the taxable year as a result of:

the disposition of a partial or entire interest in a partnership as described in reg. 1.706-1(c)(2) (sale, exchange or liquidation of entire interest or death of partner closing the tax year with respect to the partner) and (3) (sale or exchange of less than entire interest which does not close the tax year with respect to the partner) or

with respect to a partner whose interest in a partnership is reduced as described in reg. 1.706-1(c)(3), including by the entry of a new partner (collectively, a "variation").

Note: The above variations may result in a closure of the tax year with respect to the partner, but they do not result in a closure of the partnership tax year for the entire partnership.

©2016. These materials are copyrighted and may not be reproduced or distributed in whole or in part without permission of the authors/CalCPA Education Foundation.

Copyri

ght 2

016-1

7

2016 McBride/Nellen Federal and California Update for Businesses and Estates

Chapter 1: 2016 Legislation and Code/Regs. First Effective in 2016 Page 1-20

The following items, subject to allocation under other rules, are not subject to the rules of Reg. 1.706-4:

special allocation rules for certain items from the discharge or retirement of debt in sections 108(e)(8) and 108(i)

relating to the determination of partners' distributive shares of allocable cash basis items in section 706(d)(2)

relating to the determination of partners' distributive share of any item of an upper tier partnership attributable to a lower tier partnership in section 706(d)(3)

“In all cases, all partnership items for each taxable year must be allocated among the partners, and no partnership items may be duplicated, regardless of the particular provision of section 706 (or other Code section) which applies, and regardless of the method or convention adopted by the partnership.”

General Rule of Segments and Proration Periods The preamble describes the general rule of segments and proration periods as follows:

For purposes of accounting for the partners' varying interests in the partnership, the 2009 proposed regulations required the partnership to maintain, for each partner whose interest changes in the taxable year, segments to account for such changes. Under the 2009 proposed regulations, a segment was a specific portion of a partnership's taxable year created by a variation, regardless of whether the partnership used the interim closing method or the proration method for that variation. The final regulations continue to rely on the concept of segments; however, because the final regulations now permit partnerships to use both the interim closing method and the proration method in the same taxable year, the final regulations also contain a new concept of proration periods. Under the final regulations, segments are specific periods of the partnership's taxable year created by interim closings of the partnership's books, and proration periods are specific portions of a segment created by a variation for which the partnership chooses to apply the proration method. The partnership must divide its year into segments and proration periods, and spread its income among the segments and proration periods according to the rules for the interim closing method and proration method, respectively. Under the final regulations, the first segment commences with the beginning of the taxable year of the partnership and ends at the time of the first interim closing of the partnership's books. Any additional segment shall commence immediately after the closing of the prior segment and ends at the time of the next interim closing. However, the last segment of the partnership's taxable year ends no later than the close of the last day of the partnership's taxable year. If there are no interim closings, the partnership has one segment, which corresponds to its entire taxable year.

©2016. These materials are copyrighted and may not be reproduced or distributed in whole or in part without permission of the authors/CalCPA Education Foundation.

Copyri

ght 2

016-1

7

2016 McBride/Nellen Federal and California Update for Businesses and Estates

Chapter 1: 2016 Legislation and Code/Regs. First Effective in 2016 Page 1-21

Under the final regulations, the first proration period in each segment begins at the beginning of the segment, and ends at the time of a variation for which the partnership uses the proration method. The next proration period begins immediately after the close of the prior proration period and ends at the time of the next variation for which the partnerships uses the proration method. However, each proration period ends no later than the close of the segment. Thus, segments close proration periods. Therefore, the only items subject to proration are the partnership's items attributable to the segment containing the proration period.

Step-by-Step Approach (Ten Steps) The final regulations provide the following step-by-step approach to determining the distributive share of partnership items (reg. 1.706-4(a)(3)(i) through (x)):

1) Determine whether either of the exceptions in reg. 1.706-4(b) for contemporaneous partners and partnerships for which capital is not a material income-producing factor applies (detail below).

2) Determine which of its items are subject to allocation under the special rules for extraordinary items in reg. 1.706-4(e) and allocate those items accordingly (detail below).

3) Determine with respect to each variation whether it will apply the interim closing method or the proration method. Absent an agreement of the partners (within the meaning of reg. 1.706-4(f)) to use the proration method, the partnership shall use the interim closing method. The partnership may use different methods (interim closing or proration) for different variations within each partnership tax year; however, the IRS “may place restrictions on the ability of partnerships to use different methods during the same taxable year in guidance published in the Internal Revenue Bulletin.”

4) Determine when each variation is deemed to have occurred under the partnership's selected convention (as described in 1.706-4(c), detail below).

5) Determine whether there is an agreement of the partners (within the meaning of 1.706-4(f)) to perform regular monthly or semi-monthly interim closings (as described in 1.706-4(d)). If so, then the partnership will perform an interim closing of its books at the end of each month (in the case of an agreement to perform monthly closings) or at the end and middle of each month (in the case of an agreement to perform semi-monthly closings), regardless of whether any variation occurs. Absent an agreement of the partners to perform regular monthly or semi-monthly interim closings, the only interim closings during the partnership's taxable year will be at the deemed time of the occurrence of variations for which the partnership uses the interim closing method.

6) Determine the partnership's segments, which are specific periods of the partnership's taxable year created by interim closings of the partnership's books. The first segment

©2016. These materials are copyrighted and may not be reproduced or distributed in whole or in part without permission of the authors/CalCPA Education Foundation.

Copyri

ght 2

016-1

7

2016 McBride/Nellen Federal and California Update for Businesses and Estates

Chapter 1: 2016 Legislation and Code/Regs. First Effective in 2016 Page 1-22

starts with the beginning of the tax year of the partnership and ends at the time of the first interim closing. Any additional segment begins immediately after the closing of the prior segment and ends at the time of the next interim closing. However, the last segment of the partnership's tax year ends no later than the close of the last day of the partnership's tax year. “If there are no interim closings, the partnership has one segment, which corresponds to its entire tax year.”

7) Apportion the partnership's items for the year among its segments. The partnership determines the items of income, gain, loss, deduction, and credit of the partnership for each segment. In general, a partnership treats each segment as though the segment were a separate distributive share period. “For example, a partnership may compute a capital loss for a segment of a taxable year even though the partnership has a net capital gain for the entire taxable year. For purposes of determining allocations to segments, any special limitation or requirement relating to the timing or amount of income, gain, loss, deduction, or credit applicable to the entire partnership taxable year will be applied based upon the partnership's satisfaction of the limitation or requirement as of the end of the partnership's taxable year. For example, the expenses related to the election to expense a section 179 asset must first be calculated (and limited if applicable) based on the partnership's full taxable year, and then the effect of any limitation must be apportioned among the segments in accordance with the interim closing method or the proration method using any reasonable method.”

8) “[D]etermine the partnership's proration periods, which are specific portions of a segment created by a variation for which the partnership chooses to apply the proration method. The first proration period in each segment begins at the beginning of the segment, and ends at the time of the first variation within the segment for which the partnership selects the proration method. The next proration period begins immediately after the close of the prior proration period and ends at the time of the next variation for which the partnerships selects the proration method. However, each proration period shall end no later than the close of the segment.”

9) “[P]rorate the items of income, gain, loss, deduction, and credit in each segment among the proration periods within the segment.”

10) [D]etermine the partners' distributive shares of partnership items under section 702(a) by taking into account the partners' interests in such items during each segment and proration period.”

Example of Step-by-Step Approach (Reg. 1.706-4(a)(4) Example (Modified)

At the beginning of 2016, PRS, a calendar year partnership, has three equal partners, A, B, and C.

o On April 16, 2016, A sells 50% of its interest in PRS to new partner D. o On August 6, 2016, B sells 50% of its interest in PRS to new partner E.

During 2016, PRS generated: o $75,000 of ordinary income,

©2016. These materials are copyrighted and may not be reproduced or distributed in whole or in part without permission of the authors/CalCPA Education Foundation.

Copyri

ght 2

016-1

7

2016 McBride/Nellen Federal and California Update for Businesses and Estates

Chapter 1: 2016 Legislation and Code/Regs. First Effective in 2016 Page 1-23

o $33,000 of ordinary deductions, o $12,000 of capital gain in the ordinary course of its business, o <$9,000> of capital loss in the ordinary course of its business.

Within that year, PRS earned $60,000 of ordinary income, incurred $24,000 of ordinary deductions, earned $12,000 of capital gain, and sustained $6,000 of capital loss between January 1, 2016, and July 31, 2016, and

PRS earned $15,000 of gross ordinary income, incurred $9,000 of gross ordinary deductions, and sustained $3,000 of capital loss between August 1, 2016, and December 31, 2016.

None of PRS's items are extraordinary items. Capital is a material income producing factor for PRS. For 2016, PRS determines the distributive shares of A, B, C, D, and E as follows. First, PRS determines that none of the exceptions in paragraph (b) apply because capital

is a material-income producing factor and no variation is the result of a change in allocations among contemporaneous partners.

Second, PRS determines that none of its items are extraordinary items subject to allocation under paragraph (e).

Third, the partners of PRS agree to apply the proration method to the April 16, 2016, variation, and PRS accepts the default application of the interim closing method to the August 6, 2016, variation.

Fourth, PRS determines the deemed date of the variations for purposes of this section based upon PRS's selected convention.

Because PRS applied the proration method to the April 16, 2016, variation, PRS must use the calendar day convention with respect to the April 16, 2016, variation. Therefore, the variation that resulted from A's sale to D on April 16, 2016, is deemed to occur for purposes of this section at the end of the day on April 16, 2016.

Further, the partners of PRS agree to apply the semi-monthly convention to the August 6, 2016, variation.