ferroglobe plc presentation at cru silicon metal

TRANSCRIPT

- 0 -

Ferroglobe PLC Presentation at CRU Silicon Metal Conference Lisbon

November 14, 2018

Advancing Materials Innovation

NASDAQ: GSM

- 1 -

This presentation contains forward-looking statements within the meaning of Section 27A of the United States Securities Act of 1933, as amended, and Section 21E of the United States Securities Exchange Act of 1934, as amended. Forward-looking statements are not historical facts but are based on certain assumptions of management and describe our future plans, strategies and expectations. Forward-looking statements can generally be identified by the use of forward-looking terminology, including, but not limited to, "may," “could,” “seek,” “guidance,” “predict,” “potential,” “likely,” "believe," "will," "expect," "anticipate," "estimate," "plan," "intend," "forecast," or variations of these terms and similar expressions, or the negative of these terms or similar expressions. Forward-looking statements contained in this presentation are based on information currently available to Ferroglobe PLC (“we,” “our,” “Ferroglobe,” the “Company” or the “Parent”) and assumptions that we believe to be reasonable, but which are inherently uncertain. As a result, our actual results, performance or achievements may differ materially from those expressed or implied by these forward-looking statements, which are not guarantees of future performance and involve or implicate known and unknown risks, uncertainties and other factors that are, in some cases, beyond our control. We caution you that all such statements, as well as forward-looking statements made orally in the presentation hereof, involve or implicate myriad risks and uncertainties, including without limitation, risks that Ferroglobe will not successfully integrate the businesses of Globe Specialty Metals, Inc. and Grupo FerroAtlántica SAU, that we will not realize estimated cost savings and/or the value of certain tax assets, synergies and growth, and/or that such benefits may take longer to realize than expected. Important factors that may cause actual results to differ include, but are not limited to: (i) unanticipated costs of integration, including operating costs, customer loss and business disruption being greater than expected; (ii) our ability to optimize organizational and governance structure; (iii) our ability to hire and retain key personnel; (iv) regional, national or global political, economic, business, competitive, and market conditions; (v) changes in the cost and/or availability of raw materials or energy; (vi) competition in the metals and foundry industries; (vii) environmental and other regulatory risks; (viii) our ability to identify and evaluate liabilities associated with acquired assets prior to their acquisition; (ix) our ability to manage operational risks including industrial accidents and natural disasters; (x) our ability to manage international operations; (xi) changes in technology; (xii) our ability to acquire or renew permits and approvals; (xiii) changes in law and/or regulation and/or compliance costs affecting Ferroglobe; (xiv) conditions in the credit markets; (xv) risks associated with assumptions made in connection with critical accounting estimates and legal proceedings; (xvi) the risks of currency fluctuations and foreign exchange controls; and (xvii) the risks of local, regional and international unrest, economic downturn, tax assessments, tax adjustments, and changes in tax rates. The foregoing list is not exclusive or exhaustive. You should carefully consider the foregoing factors and the other risks and uncertainties that may affect our business, including those described in the “Risk Factors” section of Ferroglobe’s Registration Statement on Form F-1, Annual Reports on Form 20-F, Current Reports on Form 6-K and other documents we file from time to time with the United States Securities and Exchange Commission. We do not give any assurance (1) that we will achieve our expectations, or (2) concerning any result or the timing thereof, in each case, with respect to any regulatory action, administrative proceedings, government investigations, litigation, warning letters, consent decrees, cost reductions, business strategies, earnings or revenue trends or future financial results. Forward-looking financial information and other non-historical metrics presented herein represent our key goals and are not intended as guidance or projections for the periods presented herein or any future periods. We do not undertake or assume, and expressly disclaim, any obligation to update publicly any of the forward-looking statements in this presentation to reflect actual results, new information or future events, changes in assumptions or changes in other factors affecting forward-looking statements. If we update one or more forward-looking statements, no inference should be drawn that we will make additional updates with respect to those or other forward-looking statements. We caution you not to place undue reliance on any forward-looking statements, which are made only as of the date of this presentation. EBITDA, adjusted EBITDA, adjusted diluted profit (loss) per ordinary share and adjusted profit (loss) attributable to Ferroglobe are non-IFRS financial metrics that, we believe, are pertinent measures of Ferroglobe’s success. The Company has included these financial metrics to provide supplemental measures of its performance. We believe these metrics are useful because they eliminate items that have less bearing on the Company’s current and future operating performance and highlight trends in its core business that may not otherwise be apparent when relying solely on IFRS financial measures. For additional information, including a reconciliation of the differences between such non-IFRS financial measures and the comparable IFRS financial measures, please refer to our periodic filings with the U.S. Securities & Exchange Commission, available in the SEC Filings section under the Investors tab on our website, www.ferroglobe.com.

Forward-Looking Statements and Non-IFRS Financial Metrics

- 2 -

Topics for discussion

Introduction to Ferroglobe

Near-term observations on the silicon metal market

Medium-term outlook supported by strong fundamentals

Introduction to Ferroglobe

- 4 -

Ferroglobe is a leading global player in advanced materials

Global leader in an attractive growing industry

Best in class operations with unique competitive advantages

Entrepreneurial culture with strong growth track record

Unrivaled technology development and know-how

Disciplined financial management

- 5 -

Global leader in niche, high-value markets

The leading player in silicon metals… …and one of the leading ferroalloys producers

Silicon Metal Capacity (000, mt) Other Ferroalloys Capacity (000, mt)

Pri

vat

Gro

up

Source: Ferroglobe, public filings

341

207

164

96

62 60 53 48

2,145

1,260

879 710 670

355 250

- 6 -

Diverse product mix provides exposure to a variety of end markets

- 7 -

Unparalleled global operations and diversified product offering provides Ferroglobe and its customers unique optionality

Capacity by Geography

(000, mt) Europe North America South America Africa Asia Total

Silicon 178 91 - 72 - 341

Ferrosilicon / Foundry Alloys 225 120 109 112 - 566

Manganese-based Alloys 623 - 34 - - 657

Other Silicon-Based Alloys 27 - 10 - - 37

Total - 1,601

Factories

Mining

Energy

London, UK

Broadest product range

Global customer reach

Low cost operations

Production flexibility

Production optionality

Natural F/X hedge

High barriers to entry

- 8 -

Ferroglobe has amongst the broadest range of capabilities in silicon metal and ferroalloys

Broadest range of products

Diversified and flexible production footprint

Experience in worldwide international logistics

Unrivalled quality and reliability

Track record for innovation and finding customized solutions for our customers

Near-term observations on the silicon metal market

- 10 -

Key messages

Macroeconomic picture remains positive

Trade war: more rhetoric than reality to date

Trade case ‘overhang’ has passed ― corrections to supply, demand, and pricing

Recent headlines need to be put into historical perspective

Ferroglobe will continue to remain disciplined ― swift actions as market evolves

- 11 -

Global macroeconomic view remains positive with steady growth forecasted for 2019

Real GDP Growth, by Country Group

Source: IMF, World Economic Outlook, Oct. 2018 Note: Grey area denotes projections

Global Growth Outlook (% Change in GDP)

Source: IMF, World Economic Outlook, Oct. 2018

- 12 -

Historical context for the recent evolution in SiMe prices

Price recovery in 2017 ‘amplified’ due to preliminary trade case outcome

Capacity creep as pricing

environment improved in 2017, including emerging markets benefiting from a strong USD

‘Overhang’ impact of trade case that lead to surplus inventories by customer in advance of final outcome

Silicon Metal

Source: CRU

($/t

)

- 13 -

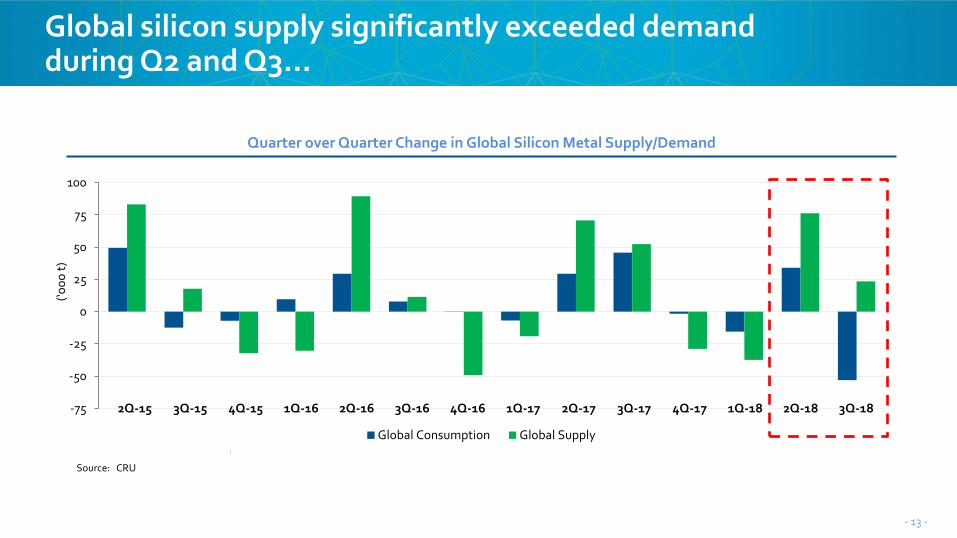

Global silicon supply significantly exceeded demand during Q2 and Q3…

Source: CRU

Quarter over Quarter Change in Global Silicon Metal Supply/Demand

-75

-50

-25

0

25

50

75

100

Global Consumption Global Supply

(‘0

00

t)

1Q-17 2Q-17 3Q-17 4Q-17 1Q-18 2Q-18 3Q-18 1Q-16 2Q-16 3Q-16 4Q-16 2Q-15 3Q-15 4Q-15

- 14 -

1,750

1,950

2,150

2,350

2,550

2,750

2,950

3,150

3,350

3,550

3,750O

ct. 2

00

8

Fe

b. 2

00

9

Jun

. 20

09

Oct

. 20

09

Fe

b. 2

010

Jun

. 20

10

Oct

. 20

10

Fe

b. 2

011

Jun

. 20

11

Oct

. 20

11

Fe

b. 2

012

Jun

. 20

12

Oct

. 20

12

Fe

b. 2

013

Jun

. 20

13

Oct

. 20

13

Fe

b. 2

014

Jun

. 20

14

Oct

. 20

14

Fe

b. 2

015

Jun

. 20

15

Oct

. 20

15

Fe

b. 2

016

Jun

. 20

16

Oct

. 20

16

Fe

b. 2

017

Jun

. 20

17

Oct

. 20

17

Fe

b. 2

018

Jun

. 20

18

Oct

. 20

18

US (98.5% Si, 5-5-3 EXW) 10 Year Average

…coupled with stockpiled inventory, the index price in the U.S. reached near historical averages in recent months

Source: CRU

($/t

)

Silicon Metal Pricing ― U.S.

- 15 -

1,750

1,950

2,150

2,350

2,550

2,750

2,950

3,150

3,350

3,550

3,750O

ct. 2

00

8

May

20

09

Dec

. 20

09

Jul.

20

10

Fe

b. 2

011

Sep

t. 2

011

Ap

r. 2

012

No

v. 2

012

Jun

. 20

13

Jan

. 20

14

Au

g. 2

014

Mar

. 20

15

Oct

. 20

15

May

20

16

Dec

. 20

16

Jul.

20

17

Fe

b. 2

018

Sep

t. 2

018

EU (98.5% Si, 5-5-3 DDP) 10 Year Average

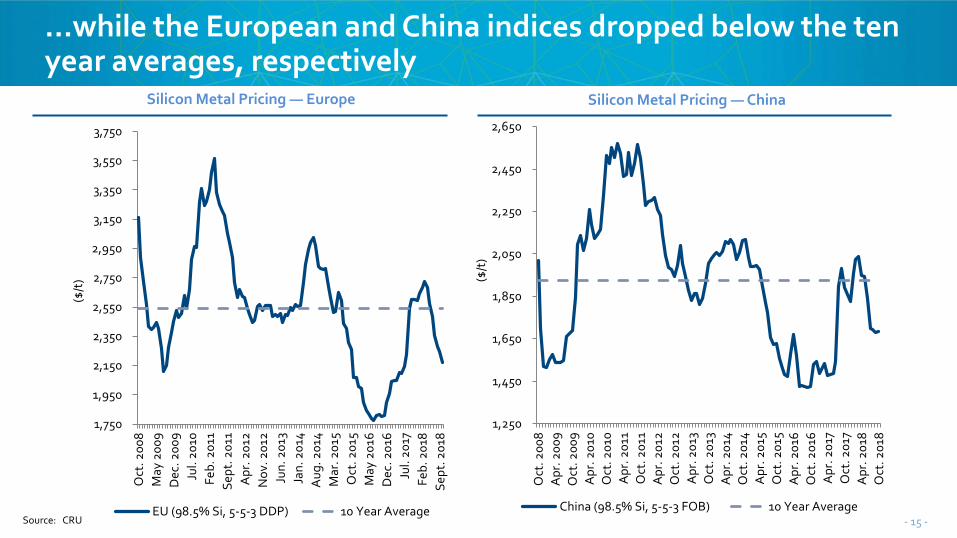

…while the European and China indices dropped below the ten year averages, respectively

Silicon Metal Pricing ― China

Source: CRU

($/t

)

Silicon Metal Pricing ― Europe

($/t

)

1,250

1,450

1,650

1,850

2,050

2,250

2,450

2,650

Oct

. 20

08

Ap

r. 2

00

9

Oct

. 20

09

Ap

r. 2

010

Oct

. 20

10

Ap

r. 2

011

Oct

. 20

11

Ap

r. 2

012

Oct

. 20

12

Ap

r. 2

013

Oct

. 20

13

Ap

r. 2

014

Oct

. 20

14

Ap

r. 2

015

Oct

. 20

15

Ap

r. 2

016

Oct

. 20

16

Ap

r. 2

017

Oct

. 20

17

Ap

r. 2

018

Oct

. 20

18

China (98.5% Si, 5-5-3 FOB) 10 Year Average

- 16 -

Catalysts for near-term pricing recovery

Trade case impact has passed ― lower inventory stockpiles by end users

Strong demand fundamentals across the chemical, aluminum and photovoltaic sectors

Limited new capacity to enter the market

Increasing input costs pressuring margins ― provides an inherent pricing floor

Quicker market discipline and reactivity ― curtailments, idling capacity

Continued environmental shutdowns in China; greater internal consumption

- 17 -

Global Silicon Metal ― Surplus / (Deficit)

After surplus inventory overhang in 2018, CRU is projecting a global balance deficit in early 2019…

Global Silicon Metal ― Production vs. Consumption

Source: CRU

699

776 799 738

693

772 813 790

723 757

704 720 707 769 773 765

600

700

800

900

1Q-18 2Q-18 3Q-18e 4Q-18e 1Q-19e 2Q-19e 3Q-19e 4Q-19e

Global Production Global Consumption

-24

19

95

19

-14

4

40 25

-50

0

50

100

150

1Q-18 2Q-18 3Q-18 4Q-18 1Q-19 2Q-19 3Q-19 4Q-19

(‘0

00

t)

(‘0

00

t)

- 18 -

…however, CRU underestimates the capacity changes made by Ferroglobe

218

127

72

178

91

72

0

50

100

150

200

250

Europe North America Africa

March 2018 Pro Forma for planned changes

Ferroglobe Silicon Metal Capacity

Silicon Metal capacity reductions: • Selma, AL (2 furnaces) • Beverly, OH (1 furnace) • Château-Feuillet, France: 2 furnaces • Laudun, France: 1 furnace

-40k tons

-36k tons

(‘0

00

t)

- 19 -

90

95

100

105

110

115

1Q-16 2Q-16 3Q-16 4Q-16 1Q-17 2Q-17 3Q-17 4Q-17 1Q-18 2Q-18 3Q-18

Increasing input and production costs will tend to force price increases

Coal

Quartz

Oil /

Natural Gas

Electrodes

Estimated world SiMe Production Cost Index

Ind

ex =

10

0 (

1Q-1

6)

SiMe Pricing vs Production Cost Index

Ind

ex =

10

0 (

1Q-1

6)

80

90

100

110

120

130

140

150

1Q-16 2Q-16 3Q-16 4Q-16 1Q-17 2Q-17 3Q-17 4Q-17 1Q-18 2Q-18 3Q-18

CRU - US Spot Price ($/t)

SiMe Production Cost Index ($/t)

Medium-term outlook for silicon metal

- 21 -

Steady global silicones consumption growth at levels beyond GDP

Recent growth from global economic expansion expected to continue

Recent consumption gains constrained by production capacity

Announced expansions support additional growth expectations

New applications and product

developments

World Silicon Demand Driven by Silicones Production

2.9% 5.8% 6.7% 7.5% 7.3% 5.7% YoY

Growth

(‘0

00

s)

1,591 1,637 1,732

1,848 1,987

2,133 2,253

1,000

1,200

1,400

1,600

1,800

2,000

2,200

2,400

2017 2018e 2019e 2020e 2021e 2022e 2023e

Global population growth

Housing and commercial construction

Growth in automotive and transportation

Increasing consumer electronics

Personal care and consumer products

Advancements in medical equipment

Source: CRU

Major Silicones Demand Drivers

- 22 -

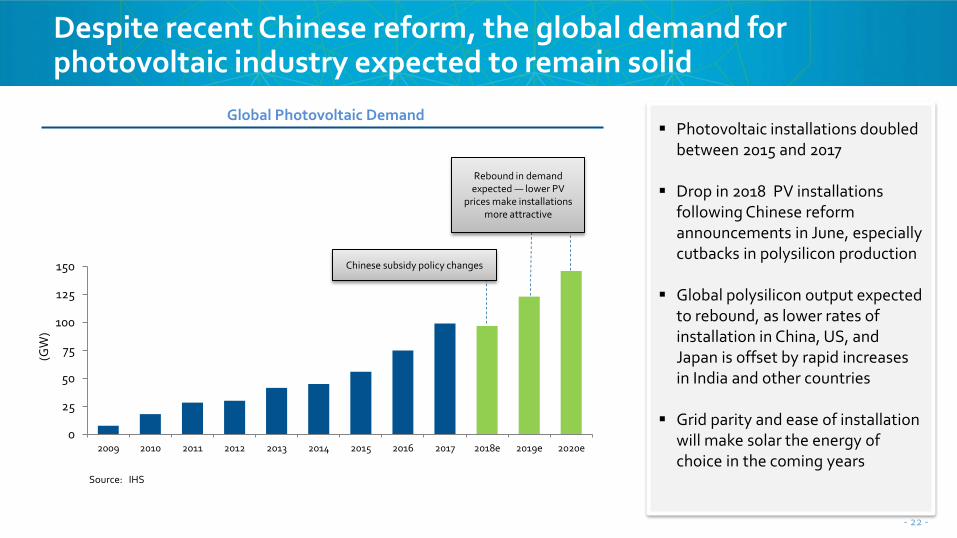

Despite recent Chinese reform, the global demand for photovoltaic industry expected to remain solid

0

25

50

75

100

125

150

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018e 2019e 2020e

Photovoltaic installations doubled between 2015 and 2017

Drop in 2018 PV installations following Chinese reform announcements in June, especially cutbacks in polysilicon production

Global polysilicon output expected to rebound, as lower rates of installation in China, US, and Japan is offset by rapid increases in India and other countries

Grid parity and ease of installation will make solar the energy of choice in the coming years

Global Photovoltaic Demand

(GW

)

Chinese subsidy policy changes

Rebound in demand expected ― lower PV

prices make installations more attractive

Source: IHS

- 23 -

Aluminum demand expected to continue delivering steady growth for silicon metal

Lowest stocks to consumption ratio since Sept.2008

Global Finished Aluminum Demand Outlook

Source: AME Metals & Mining

Global stocks as days of consumption

2017 2018e 2019e 2020e

North America (mm, tons) 6.8 6.8 6.9 7.1

(Y/Y Growth) -0.5% 2.5% 1.8%

Europe (mm, tons) 9.2 9.5 9.6 9.8

(Y/Y Growth) 3.0% 1.7% 1.5%

China (mm, tons) 34.9 36.7 38.4 40.0

(Y/Y Growth) 5.2% 4.5% 4.1%

World (mm, tons) 63.8 66.7 69.0 71.3

(Y/Y Growth) 4.5% 3.5% 3.3%

Trade war impact: more rhetoric than reality

Despite the imposition of wide-ranging tariffs and large anti-dumping duties on Chinese foil and sheet, Chinese aluminium exports have increased substantially in 2018 (year-over-year)

- 24 -

Chinese domestic demand growth coupled with supply curtailments is favorable to the global landscape

25%

27%

29%

31%

33%

35%

37%

39%

41%

43%

45%

2016 2017 2018e 2019e 2020e 2021e 2022e 2023e

Export share of production (%)

Chinese Silicon Production and Exports Chinese Exports as % of Production

(‘0

00

t)

- 25 -

Final remarks

Overall fundamentals for silicon metal are strong worldwide:

― Solid demand momentum

― Supply tightness

― Cost inflation impacting marginal producers

At current prices certain producers (specifically new entrants) unlikely to cover true cost of production, including depreciation and financing costs

Ferroglobe is uniquely positioned to serve a variety of customers, products and geographies and will apply this flexibility to switch production of products to the most profitable locations

Producing at a loss is not an option!

Producers forced to remain disciplined and react to changing market dynamics: balancing production vs. commercial strategies vs. profitability

- 26 -

Ferroglobe PLC Presentation at CRU Silicon Metal Conference Lisbon

November 14, 2018

Advancing Materials Innovation

NASDAQ: GSM