fes 2016 stakeholder feedback document - national...

TRANSCRIPT

Stakeholder Feedback

document 2016

Future Energy Scenarios

JANUARY 2016

This publication is part of our annual scenario development process. It summarises

how we have engaged with you, what you have told us since the release of FES 2015

and our initial thoughts on the new suite of scenarios for 2016. The FES Stakeholder

Feedback document is the latest of our suite of ‘Future of Energy’ documents which

also includes: Electricity Ten Year Statement (ETYS), Gas Ten Year Statement (GTYS),

System Operability Framework (SOF), Winter Outlook Report (WOR) and Summer

Outlook Report (SOR).

I am excited to be leading the team that develops the FES. Once again we have had some

really fantastic engagement with our stakeholders, which has delivered real intelligence and

insight for us to use as we build FES 2016. There are so many uncertainties regarding the

future of energy for GB; it is your views, knowledge and insight which drive the scenarios,

allowing us to better understand these uncertainties. I would like to take this opportunity to

thank you for giving us your time and energy in this engagement.

You had a lot of good things to say about FES 2015. We continue to seek improvements in

our engagement to ensure we maintain good relationships with current stakeholders and

target new stakeholders to enhance the richness of the scenarios. We plan to do even more

of this as we move forward in 2016.

I hope you find this publication useful and look forward to sharing the outcome of our 2016

work later this year.

Marcus Stewart, Energy Policy and Supply Manager

Introduction

Welcome to the Future Energy Scenarios (FES) Stakeholder Feedback

document for 2016.

National Grid’s Electricity Transmission licence standard condition (C11) requires the

submission of our proposed future energy scenarios to Ofgem by the end of January each

year. This document represents our submission. It summarises our stakeholder

engagement, how this engagement has been, and will be, taken into account in the

development of this year’s FES, and our initial thoughts on the new suite of scenarios for

2016.

These images are from the FES 2015 conference.

What does this document represent?

Section one: Executive Summary

Section two: Why we create the Future Energy Scenarios

Section three: The role of stakeholders

Section four: Stakeholder feedback and what it means for FES 2016

Section five: Overview of FES 2016

Section six: Future improvements

Section seven: Types of organisations we engaged with in this year’s consultation

Section eight: Continuing the conversation

Contents

Consistency is critical

Overwhelmingly our stakeholders told us that they want to see consistency year on year in

the FES. This has reaffirmed our approach to FES 2015 and there will not be any big

changes to our scenarios this year. We have ensured consistency is central to our

deliberations as we begin to develop this year’s scenarios. We will be maintaining the “look

and feel” of the document and make changes only where clearly justifiable.

2020 Renewable Energy Directive target

Gone Green will not be forced to meet the 2020 Renewable Energy Directive target of 15

percent of UK energy consumption coming from renewable sources. This reflects that

although significant progress has been made towards the target, with 2020 only four years

away it is very challenging to meet. Further analysis will be undertaken through the FES

2016 cycle and we will identify what needs to happen to reach the 15 percent target.

We have enhanced our stakeholder engagement activities

We have broadened our engagement activities and increased the number of stakeholders

that we engaged with.

We introduced a series of webinars this year, made our workshops more interactive, held an

extensive programme of focused bilateral sessions and enhanced our online presence. In

doing so we increased the number of organisations we engaged with from 233 to 362.

Introducing a new structured approach

During our FES 2015 consultation 45 percent of our stakeholders told us they want us to be

clearer on how the FES assumptions and inputs are created and used. For 2016 we are

introducing a more structured approach to grouping our inputs and assumptions. This will

ensure consistency across our analysis as well as allowing stakeholders to better

understand how our scenarios are developed.

More of our insight

Our stakeholders told us that they want to hear more of our insight within the FES. For

2016, we will develop and improve our signposting to contain more insight and statements

about what developments would be required to realise the different scenarios. We will also

include ‘Spotlights’ to allow us to explore key topics in more detail and consider

developments which are not yet at a maturity to be included as an input into our analysis.

Executive Summary

Sectio

no

ne

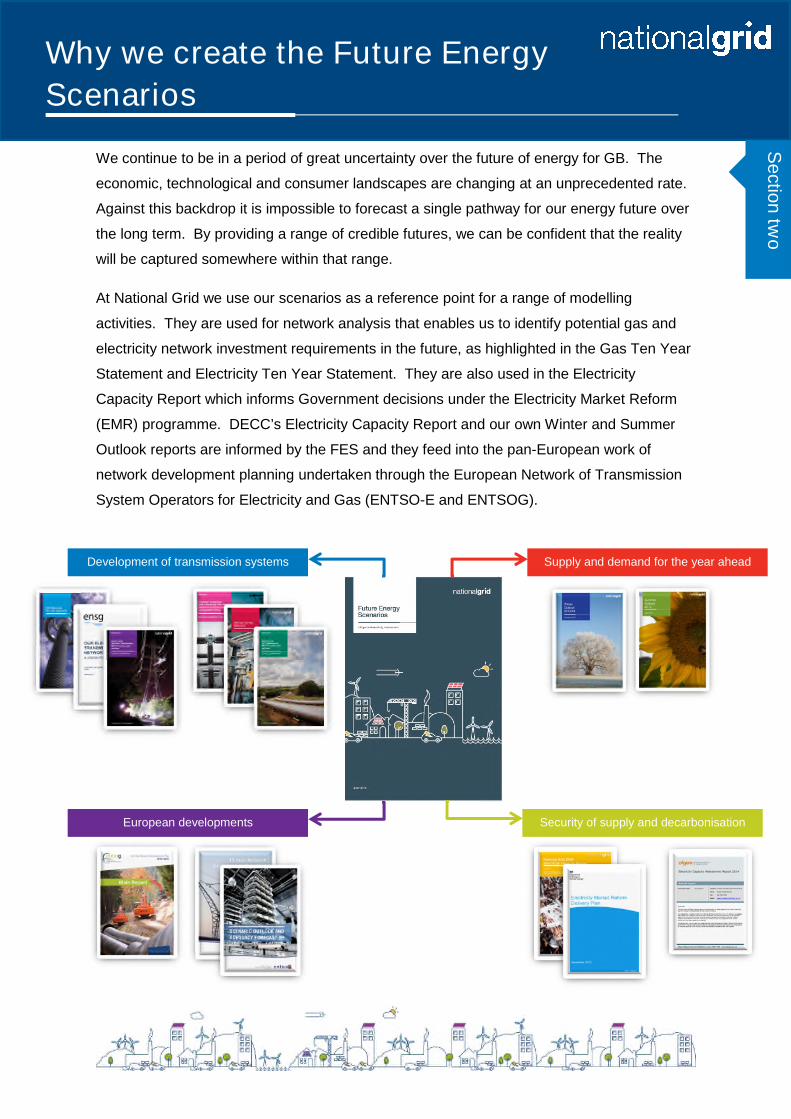

We continue to be in a period of great uncertainty over the future of energy for GB. The

economic, technological and consumer landscapes are changing at an unprecedented rate.

Against this backdrop it is impossible to forecast a single pathway for our energy future over

the long term. By providing a range of credible futures, we can be confident that the reality

will be captured somewhere within that range.

At National Grid we use our scenarios as a reference point for a range of modelling

activities. They are used for network analysis that enables us to identify potential gas and

electricity network investment requirements in the future, as highlighted in the Gas Ten Year

Statement and Electricity Ten Year Statement. They are also used in the Electricity

Capacity Report which informs Government decisions under the Electricity Market Reform

(EMR) programme. DECC’s Electricity Capacity Report and our own Winter and Summer

Outlook reports are informed by the FES and they feed into the pan-European work of

network development planning undertaken through the European Network of Transmission

System Operators for Electricity and Gas (ENTSO-E and ENTSOG).

Supply and demand for the year aheadDevelopment of transmission systems

Security of supply and decarbonisationEuropean developments

Why we create the Future Energy

Scenarios

Sectio

ntw

o

As we strive to deliver value to all of our stakeholders, it is important that we understand how

our stakeholders use the FES. We explored this question across our engagement activities

this year. Our stakeholders told us that they use the FES in a variety of ways. Over ten

percent of our stakeholders told us that they use it as a reference document throughout the

year, whilst 15 percent use it as a benchmarking tool.

PlanningInformation source for market analysis

Horizon scanning using case studies

Compare models and analysisProvides an overall market view

Future pathways for technology innovations

“Sustainability First makes use of the FES scenarios as a

key reference document, for example, to underpin the

modelling for our GB Electricity Demand project. We have a

cross-sector interest, but are particularly interested in

household load projections. We would find more robust

analysis helpful on some aspects of future household load

and its innate flexibility, for example, uptake of household

electric heat, including new generation storage heaters.

Also, likely uptake rates and impact of LED lighting on peak

load are very important.”

Judith Ward, Sustainability First

2.1 How do our stakeholders use the FES?

Sectio

ntw

o

We continue to maintain

our relationships with

those from the energy

industry, whilst also

increasing our stakeholder

base.

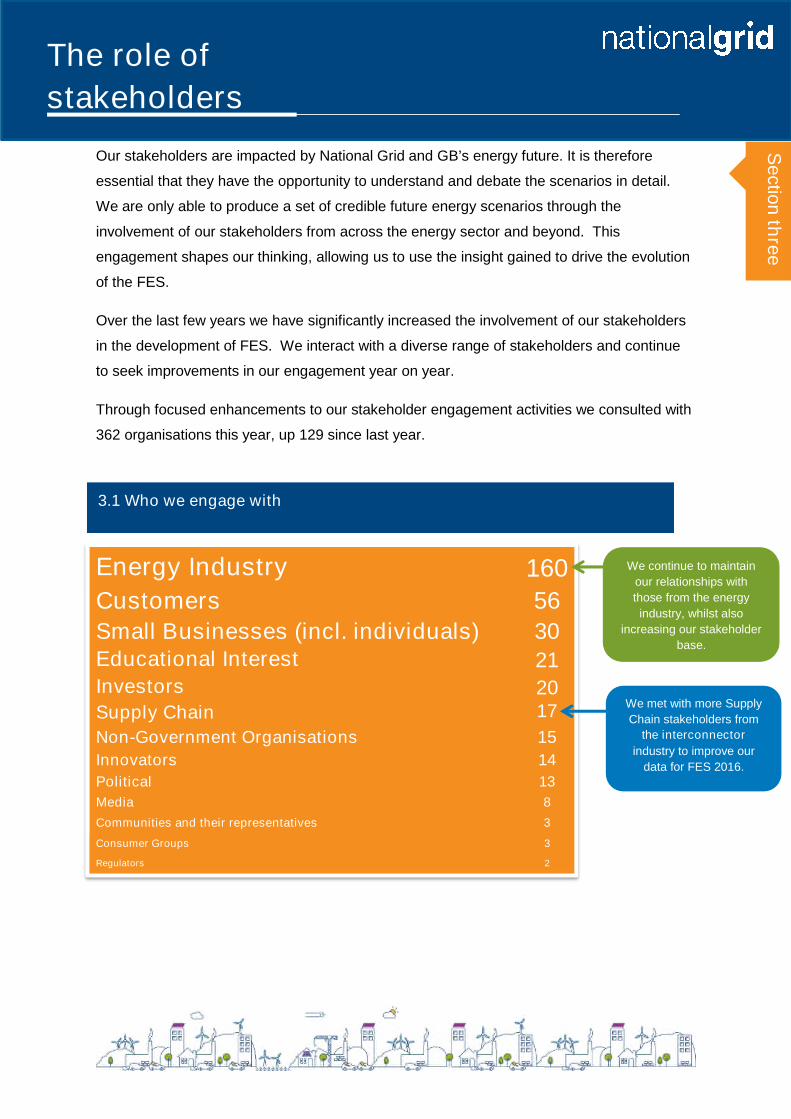

Our stakeholders are impacted by National Grid and GB’s energy future. It is therefore

essential that they have the opportunity to understand and debate the scenarios in detail.

We are only able to produce a set of credible future energy scenarios through the

involvement of our stakeholders from across the energy sector and beyond. This

engagement shapes our thinking, allowing us to use the insight gained to drive the evolution

of the FES.

Over the last few years we have significantly increased the involvement of our stakeholders

in the development of FES. We interact with a diverse range of stakeholders and continue

to seek improvements in our engagement year on year.

Through focused enhancements to our stakeholder engagement activities we consulted with

362 organisations this year, up 129 since last year.

Energy Industry 160

Customers 56

Small Businesses (incl. individuals) 30Educational Interest 21Investors 20Supply Chain 17

Non-Government Organisations 15

Innovators 14

Political 13

Media 8

Communities and their representatives 3

Consumer Groups 3

Regulators 2

We met with more Supply

Chain stakeholders from

the interconnector

industry to improve our

data for FES 2016.

The role of

stakeholders

Sectio

nth

ree

3.1 Who we engage with

Each year we run an engagement process where we consult with our stakeholders, analyse

feedback and then create and launch the next round of scenarios. We are always looking to

improve our engagement and enhance the accessibility of FES.

We run a whole suite of engagement activities to allow our stakeholders to get involved in a

way that suits them. As well as the FES launch event and our extensive programme of

bilateral engagement, this year we enhanced our engagement activities by:

Introducing webinars.

Creating a dedicated FES website and increasing our online presence.

Tailoring the content of our workshops and making them more interactive.

Publishing the ‘FES in 5’ to complement the full FES document.

3.2 How we engage

Sectio

nth

ree

Launch event 201 stakeholder organisations

We trialled a panel approach to hear the voice of various experts.

We held a bigger exposition to allow more engagement with our team.

We were oversubscribed so this year we have chosen a larger venue.

When asked “how valuable was the conference to you”, our average score was 7.8/10 (up

from 7.4 in 2014).

Publications

‘FES in 5’ was a new publication introduced in 2015 aimed at stakeholders who use

the key messages from our analysis.

This year we will be printing more copies of our FES document as our stakeholders

have told us they find a hard copy useful.

This is a screen shot of our ‘FES in 5’ post on LinkedIn which includes the engagement

statistics:

“It is a good opportunity to get an overviewfrom specialists on where they think the‘envelope’ of possibilities is for energy

development and transmission.”

“I would like to seemore interaction withthe audience in the

auditorium e.g. Q&A”

“I find the A5 [FES] book really usefulas a reference document instead of

having to look online”

“The printedoutput [is]fantastic”

Sectio

nth

ree

Workshops 116 stakeholder organisations

We expanded our locations, holding them in Edinburgh, Nantwich, Warwick and

London as well as holding a dedicated 2050 workshop.

We tailored the content of our workshops to the subjects stakeholders told us they

wanted to discuss.

We made them more interactive, providing the opportunity to visit six focused

stations exploring the structure and content of the FES.

This year we will look to hold workshops in Cardiff and Brussels based on feedback.

When asked “how valuable was the event to you”, our average score was 7.4/10. This is our

benchmark and we will aim for a higher score for FES 2016.

Webinars 118 stakeholder organisations

We trialled a series of webinars to explore if our stakeholders would find this a useful

way to engage with us. We hosted three webinars covering topics of electricity

supply, gas supply and electricity demand.

We were clear on the specific webinar focus to allow the audience to be tailored.

This allowed us to share information and gather input into specific FES topics (e.g.

air conditioning).

We asked the webinar attendees to provide us feedback online. We have gathered

qualitative data both on FES specific topics and on how the webinars were run,

which we will take into account for FES 2016.

“It was useful to go round the sixdifferent ‘stations’ to have a chance to

feedback on those areas of the scenarioformulation. The round table discussions

were also very useful.”

“Very interesting range of peopleand opinions. Interesting to

understand how National Gridoperates. Really enjoyed talking

'energy modelling' with people whounderstood these things!”

Feedback helpful for our next round ofwebinars: “I recommend USB

microphones - happy to share bestpractice in what we have trialled for

our webinars.”

“[It was] useful to stopand hear commentary

and questions.”

Sectio

nth

ree

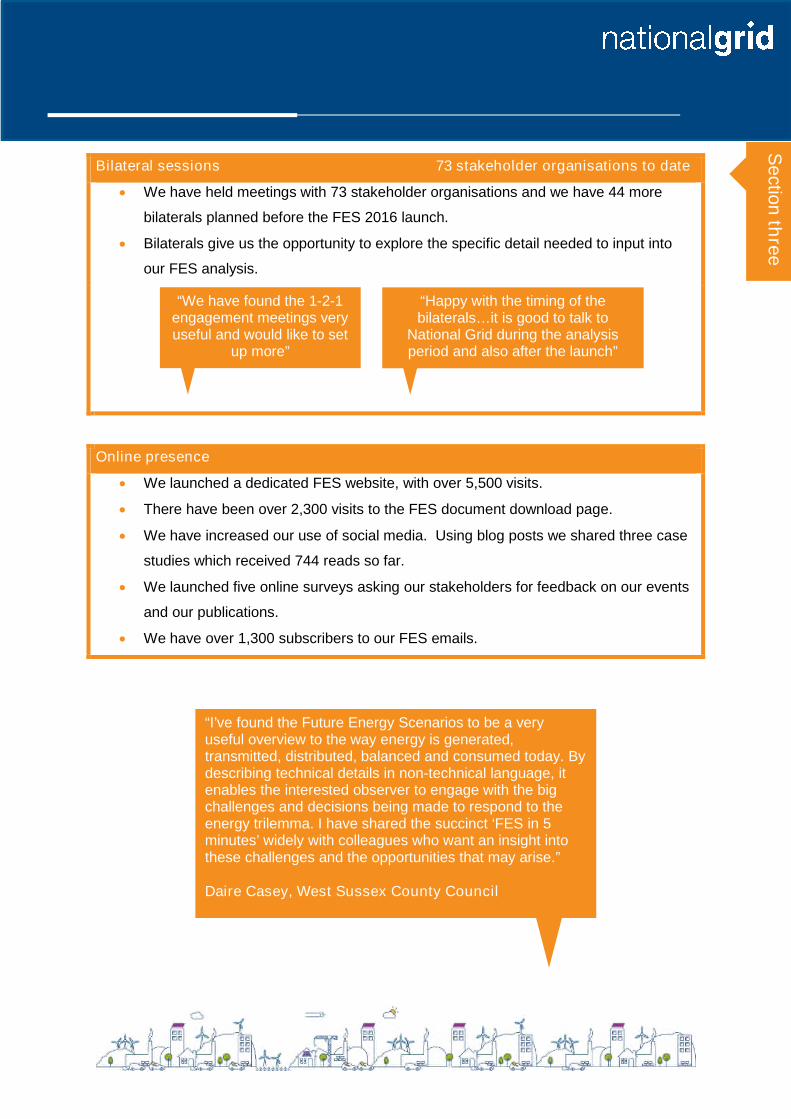

Bilateral sessions 73 stakeholder organisations to date

We have held meetings with 73 stakeholder organisations and we have 44 more

bilaterals planned before the FES 2016 launch.

Bilaterals give us the opportunity to explore the specific detail needed to input into

our FES analysis.

Online presence

We launched a dedicated FES website, with over 5,500 visits.

There have been over 2,300 visits to the FES document download page.

We have increased our use of social media. Using blog posts we shared three case

studies which received 744 reads so far.

We launched five online surveys asking our stakeholders for feedback on our events

and our publications.

We have over 1,300 subscribers to our FES emails.

“We have found the 1-2-1engagement meetings veryuseful and would like to set

up more”

“Happy with the timing of thebilaterals…it is good to talk to

National Grid during the analysisperiod and also after the launch”

“I’ve found the Future Energy Scenarios to be a veryuseful overview to the way energy is generated,transmitted, distributed, balanced and consumed today. Bydescribing technical details in non-technical language, itenables the interested observer to engage with the bigchallenges and decisions being made to respond to theenergy trilemma. I have shared the succinct ‘FES in 5minutes’ widely with colleagues who want an insight intothese challenges and the opportunities that may arise.”

Daire Casey, West Sussex County Council

Sectio

nth

ree

The feedback we receive from our stakeholders drives the development of our FES. In

considering this feedback we explore each comment and consider it against the themes we

are hearing from across our stakeholder engagement. There may be outliers that go against

the majority of what our stakeholders are saying or feedback that cannot be allocated to the

framework by which we develop our scenarios. In this section we will explore the feedback

and demonstrate what it means for FES 2016. We split the feedback into two categories:

structural and content specific.

You said…. For FES 2016 we will….

You want consistency

between iterations of the

FES.

We will maintain consistency with FES

2015. We will maintain the look and feel

of the FES and throughout development

we will keep the desire for consistency in

mind, making changes where

demonstrably required.

You like the security of

supply rules and the use of

four scenarios in a 2X2

matrix.

We will continue using the security of

supply rules and the four scenarios in a

2X2 matrix with the same axes titles.

The Levy Control Framework

(LCF) should not be a fixed

rule as it can change and is

short term.

We will make the LCF an assumption.

“It’s important to haveconsistency and track how

the scenarios havechanged overtime.”

“Isn’t the LCF just an input?”

Stakeholder feedback and what it

means for FES 2016

Sectio

nfo

ur

4.1 Structural feedback and what it means for FES 2016

You like how we used the

PESTE structure to give an

overview of the four

scenarios, but found our

secondary assumptions

unclear.

We will use a more structured approach

to FES development (the Scenario

Framework) and PEST* structure to

group and display our assumptions.

You want us to be clearer on

our use of terminology

(‘power’, ‘energy’,

‘electricity’).

We will ensure clarity and consistency in

our definitions.

You would like to hear more

of our insight in the FES.

We will develop our signposting to

contain more insight and statements

about what developments would be

required for key elements within a

scenario to be realised. We will also

include ‘Spotlights’ to allow us to

explore and offer our insight on key

topics.

You like the names ‘Gone

Green’ and ‘Slow

Progression’, but you would

like ‘Consumer Power’ and

‘No Progression’ changed.

We balanced this up against the desire

for consistency and will not change any

of the scenario names for FES 2016.

Instead we will include greater narrative

to support the names.

“You should tieup the

connectionbetween

assumptions andPESTE.”

*This year we are using the shortened PEST model as we believe environmental factors feature in all the other elements of PEST.

“[It is] interesting toknow more about

National Grid's ownthoughts on questions.”

“Which power? Electricityor gas, the word power is

confusing.”

“If the principle of thescenario fundamentallychanges then changethe name. If changesto the scenarios areevolutions then don’tchange the name.”

75% of stakeholders want to keep the names ‘Gone Green’ and 57%

want to keep ‘Slow Progression’;

59% of stakeholders said to change ‘Consumer Power’; and 66% to

change ‘No Progression’.

Sectio

nfo

ur

Theme: Technological.

Assumption: Deployment Rateof Smart Meters. Set at High in Gone Green;

Medium in Consumer Powerand Slow Progression; Low inNo Progression.

Model lever: The specificnumber of smart meters deployedeach year in each scenario.

*Th

isye

ar

we

are

usi

ng

the

sho

rte

ned

PE

ST

mo

delas

we

belie

vee

nvi

ron

me

nt

fea

ture

sin

all

the

oth

er

ele

me

nts

ofP

ES

T.

We

will

inclu

de

na

rra

tive

with

inth

eF

ES

tosu

ppo

rtth

is.

The Scenario Framework introduces a more structured approach, providing a single

reference document to group all the inputs and assumptions that we use to build our

scenarios.

We believe this approach will ensure consistency across all of our analysis. It allows us to

identify and group all the inputs into understandable and clear themes. Stakeholder

feedback is central to the discussion of each element of the framework. We hope that as well

as driving more consistency in our approach it will meet our stakeholders’ desire to

understand better how we develop our scenarios.

P E

ST

Assumptions

Fixed rules

Scenario world

Model leversThe numbers used in the analysis

Set at high/medium/low

for each scenario

The matrix,

scenario

names and

fixed rules Themes

4.2 The Scenario Framework

Scenario FrameworkExample

Central to the Scenario Framework is the scenario world. This effectively captures the core

elements which are fixed in each of our scenarios: the matrix, scenario names and fixed rules.

The next layer introduces the scenario themes: Political, Economic, Social and Technological

(PEST*). The themes were chosen as our stakeholders told us that they like and understand

the use of PEST.

Sitting beneath each theme are all the assumptions which feed into the scenarios. Each

assumption will be set at High, Medium or Low for each of the four scenarios.

The final layer of the framework is the specific model levers which are input into the analysis in

line with the level set for each assumption.

Sectio

nfo

ur

In this section we explore the key themes emerging from our stakeholder engagement with

regards to the content of our scenarios and what this means for FES 2016. Obviously our

stakeholders provide a whole wealth of detailed information that is used in our scenarios;

this section reflects a summary of this.

You said…. For FES 2016 we will….

Interconnectors

Consumer Power should have more

interconnection.

We have a developed a new capacity model for the

analysis of interconnectors. Using this we have validated

what our stakeholders have told us and for FES 2016

Consumer Power will have more interconnection.

Last year we said we were going to

improve our interconnector methodology,

have we done this? For example, we

don’t take into account what is happening

across the EU in terms of interconnection

flows.

For FES 2016 we have implemented a more robust

method and introduced a generic timeline for

interconnector development so we can understand the

minimum time it takes to connect.

We have commissioned Baringa to undertake European

modelling work to deliver FES 2016 annuals and peaks

which considers flows across Europe. We are currently

out to tender for the enduring European model which will

be used from FES 2017 onwards.

“This year we have consulted with 25% more stakeholders including thosefrom the supply chain, political, regulatory and customer groups. As a

result of this we will be changing a number of our modelling inputs,including building rate (offshore cable jointing changed from 2 days to 5

days, offshore cable laying rate changed from 10km/day to 5km/day) andinputs associated with assumed build type.”

Dave Wagstaff, Balancing Analyst

4.3 Content specific feedback and what it means for FES 2016

Sectio

nfo

ur

Electricity Supply

It would be really useful to understand

how load factors will change over the

study period.

We will consider how we might be able to show load factors

within our scenarios and aim to include this in FES 2016.

We should be more aggressive in how

deployment of new technologies is

reflected, e.g. marine.

We base our technology projections after engaging with a

variety of stakeholders and include those technologies which

demonstrate clear evidence of deployment. Within FES 2016

we will include a number of ‘Spotlights’ for technologies

where there is currently insufficient data to include as a direct

input to our analysis.

We should take into consideration the

increasing influence of small-scale

generation on the electricity supply mix.

We should consider a fully decentralised

scenario.

FES 2015 saw Consumer Power reach 40 percent small-scale

decentralised generation by 2035, doubling from today’s level.

The Government has signed multiple large-scale generation

contracts going 15-35 years out; as such none of our

scenarios will be fully decentralised. We are working on

improvements in our understanding of the volume and type of

small-scale generation and the interactions with large-scale

generation. We aim to include more on this in FES 2016.

“We will be using the results of our webinar in order to validate our 2016analysis. Stakeholders mostly agreed with our projected range for onshore

and offshore wind. Most stakeholders felt that our solar projections don’treflect current market conditions so we will revisit our solar assumptions.

Most stakeholders felt coal would close earlier than in our 2015 scenarios –we will also revisit our plant closure profile.”

Janet Coley, Electricity Supply Analyst

Sectio

nfo

ur

Electricity demand

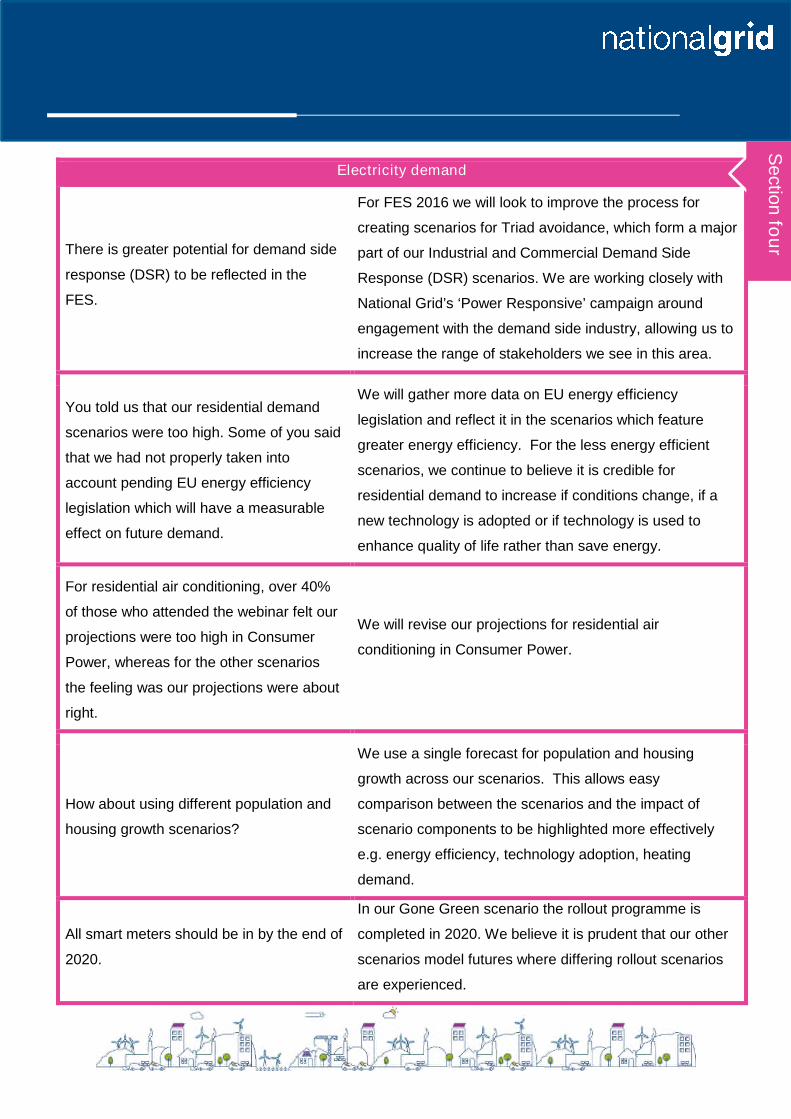

There is greater potential for demand side

response (DSR) to be reflected in the

FES.

For FES 2016 we will look to improve the process for

creating scenarios for Triad avoidance, which form a major

part of our Industrial and Commercial Demand Side

Response (DSR) scenarios. We are working closely with

National Grid’s ‘Power Responsive’ campaign around

engagement with the demand side industry, allowing us to

increase the range of stakeholders we see in this area.

You told us that our residential demand

scenarios were too high. Some of you said

that we had not properly taken into

account pending EU energy efficiency

legislation which will have a measurable

effect on future demand.

We will gather more data on EU energy efficiency

legislation and reflect it in the scenarios which feature

greater energy efficiency. For the less energy efficient

scenarios, we continue to believe it is credible for

residential demand to increase if conditions change, if a

new technology is adopted or if technology is used to

enhance quality of life rather than save energy.

For residential air conditioning, over 40%

of those who attended the webinar felt our

projections were too high in Consumer

Power, whereas for the other scenarios

the feeling was our projections were about

right.

We will revise our projections for residential air

conditioning in Consumer Power.

How about using different population and

housing growth scenarios?

We use a single forecast for population and housing

growth across our scenarios. This allows easy

comparison between the scenarios and the impact of

scenario components to be highlighted more effectively

e.g. energy efficiency, technology adoption, heating

demand.

All smart meters should be in by the end of

2020.

In our Gone Green scenario the rollout programme is

completed in 2020. We believe it is prudent that our other

scenarios model futures where differing rollout scenarios

are experienced.

Sectio

nfo

ur

Gas demand

The Natural Gas Vehicle (NGV) market is

heading towards pure gas vehicles rather than

hybrids.

For FES 2016, we will review our NGV analysis to

focus on pure gas vehicles.

You would like to see more depth to our district

heat analysis.

We have a district heat model, created in

collaboration with Buro Happold, that explores

opportunities for district heat giving a richer picture of

deployment in the UK. For FES 2016, we will advance

this project to allow an extra layer of depth to be

included in our analysis.

You believe that the 20 percent reduction of gas

demand per house identified in Gone Green and

Slow Progression through a Home Energy

Management System (HEMS) is too ambitious.

We will review the gas demand reduction associated

with a HEMS for FES 2016. We will continue to

gather more data on new technologies to enhance the

inputs to our analysis.

You are surprised that low carbon heating

uptake is not more prevalent in Slow

Progression; you would expect it to be closer to

Consumer Power.

We will re-evaluate the assumptions in our heating

technology model.

“Our stakeholders told us they wanted to see more detail in our district heatinganalysis in the FES. This year we started an innovation project working with Buro

Happold to investigate suitable locations for district heating in Great Britain. Havingthis information will give us a better view on gas and electricity demand in our

scenarios. Recently we shared our findings with the Energy NetworksAssociation's Gas Futures group to get their thoughts.”

Iain Shepherd, Energy Demand Analyst

Sectio

nfo

ur

Gas supply

Locally produced shale gas should be

greener in terms of overall lifecycle carbon

emissions than liquefying gas in the Middle

East, shipping it several thousand miles to

the UK and re-gasifying it.

We do not reflect lifecycle carbon emissions as an

input to our analysis as current carbon accounting

does not include emissions incurred from activities

outside the UK. For FES 2016, we will look to explore

this further in a ‘Spotlight’.

It is unrealistic to say that no infrastructure

will close; by 2035 some of the facilities will

be quite old.

We acknowledge this can be seen as a limitation in

our analysis, however we do not assume a facility will

close when the owner of the facility has not made

such a decision public. However, for FES 2016 we will

consider whether an objective means of reducing

capacity, possibly based on age of facility, can be

developed.

We should consider alternative sources of

gas supply such as bio-synthetic natural gas

(SNG) or hydrogen from electricity to gas

schemes.

We will investigate this further in a ‘Spotlight’ for FES

2016. We already consider biomethane, principally

from anaerobic digestion, but have not so far

considered bio-SNG, gas from waste or hydrogen

from electricity to gas schemes. These are all

potential sources that are more likely to connect to the

distribution networks than the transmission network

and we are in dialogue with the gas distribution

networks to understand the maturity of these

technologies.

The balance between LNG and continental

gas is ‘unknowable’ and we should not

demonstrate any sort of split as this would

imply an unwarranted level of confidence.

Market intelligence at the moment, both from our

stakeholders and commercial sources, is that LNG

availability is likely to be high for at least the next 5

years. There may be some scope for increasing the

LNG minimum level slightly and reducing, but not

removing, the ‘generic import’ category. We will

continue to engage with our stakeholders on this and

review for FES 2016.

Sectio

nfo

ur

Electricity storage

We should include electricity storage in the

scenarios – Gone Green and Consumer

Power provide the best environments for

electricity storage to prosper.

We have engaged with developers and the value

proposition has improved for storage, therefore, we will

include electricity storage penetration in the FES 2016

analysis – focusing growth in Gone Green and Consumer

Power. This will cover transmission, distribution and

behind the meter electricity storage.

2050

We should include further analysis on

aviation and shipping as they will dominate

emissions in 2050.

For FES 2016 we will enhance our 2050 analysis regarding

shipping and aviation emissions.

There should be more than one scenario

meeting the 2050 carbon target.

Whilst Gone Green is the only scenario to meet the carbon

target, for FES 2016 we will share sensitivities that

demonstrate there are other ways of meeting them.

Simon Durk, Gas Supply Manager

“Engaging with stakeholders allows us to check our modelling against otherindustry players, experts in their field, and confirm that our assumptions are

reasonable. Stakeholders have given us useful pointers to new sources ofinformation. We believe that by engaging with stakeholders we produce gas

flow scenarios that are more credible than would otherwise be the case.”

Sectio

nfo

ur

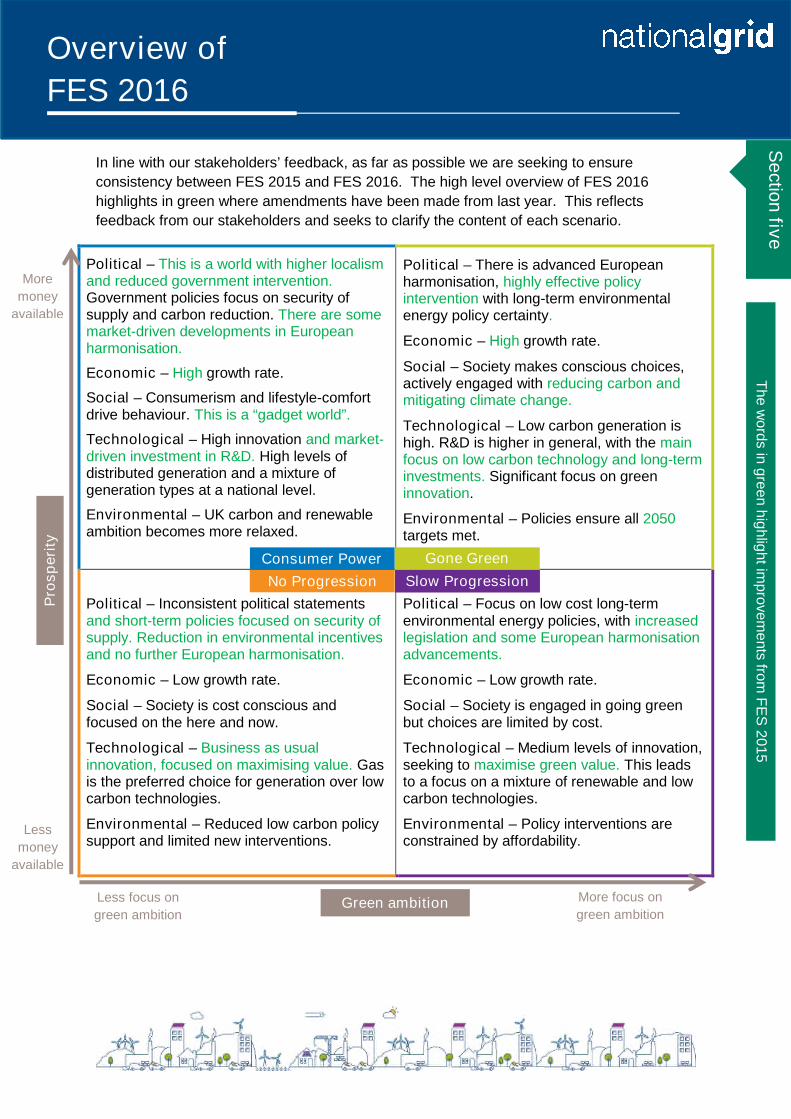

In line with our stakeholders’ feedback, as far as possible we are seeking to ensure

consistency between FES 2015 and FES 2016. The high level overview of FES 2016

highlights in green where amendments have been made from last year. This reflects

feedback from our stakeholders and seeks to clarify the content of each scenario.

Political – This is a world with higher localismand reduced government intervention.Government policies focus on security ofsupply and carbon reduction. There are somemarket-driven developments in Europeanharmonisation.

Economic – High growth rate.

Social – Consumerism and lifestyle-comfortdrive behaviour. This is a “gadget world”.

Technological – High innovation and market-driven investment in R&D. High levels ofdistributed generation and a mixture ofgeneration types at a national level.

Environmental – UK carbon and renewableambition becomes more relaxed.

Political – There is advanced Europeanharmonisation, highly effective policyintervention with long-term environmentalenergy policy certainty.

Economic – High growth rate.

Social – Society makes conscious choices,actively engaged with reducing carbon andmitigating climate change.

Technological – Low carbon generation ishigh. R&D is higher in general, with the mainfocus on low carbon technology and long-terminvestments. Significant focus on greeninnovation.

Environmental – Policies ensure all 2050targets met.

Political – Inconsistent political statementsand short-term policies focused on security ofsupply. Reduction in environmental incentivesand no further European harmonisation.

Economic – Low growth rate.

Social – Society is cost conscious andfocused on the here and now.

Technological – Business as usualinnovation, focused on maximising value. Gasis the preferred choice for generation over lowcarbon technologies.

Environmental – Reduced low carbon policysupport and limited new interventions.

Political – Focus on low cost long-termenvironmental energy policies, with increasedlegislation and some European harmonisationadvancements.

Economic – Low growth rate.

Social – Society is engaged in going greenbut choices are limited by cost.

Technological – Medium levels of innovation,seeking to maximise green value. This leadsto a focus on a mixture of renewable and lowcarbon technologies.

Environmental – Policy interventions areconstrained by affordability.

Gone Green

Slow ProgressionNo Progression

Consumer Power

Less

money

available

More

money

available

Less focus on

green ambition

More focus on

green ambitionGreen ambition

Pro

sp

eri

ty

The

word

sin

gre

en

hig

hlig

htim

pro

vem

ents

from

FE

S2015

Sectio

nfiv

e

Overview of

FES 2016

5.1 What are the key changes?

We have increased the economic growth rate in Gone Green and Consumer Power in

line with intelligence we have gathered. This was also validated by feedback from our

stakeholders.

We have highlighted the approach and drivers of innovation across the scenarios.

There is lower policy intervention in the scenarios which have less focus on green

ambition.

We have explicitly identified the level of expected European harmonisation across the

scenarios as our stakeholders felt this was an important aspect.

Gone Green will continue to meet the 2050 carbon reduction target. However, it will

not be forced to meet the 2020 Renewable Energy Directive target of 15 percent of UK

energy coming from renewable sources. This reflects that although significant

progress has been made towards the target, with 2020 only four years away it is very

challenging to meet. This is consistent with feedback from our stakeholders which

questioned the credibility of Gone Green meeting this target and is reflected in the

summary of the Gone Green scenario. Further analysis will be undertaken through the

FES 2016 cycle and we will identify what needs to happen to reach the 15 percent

target.

Comm

“It’s important to haveconsistency and track how thescenarios have changed over

time.”

“Scenarios are too GBfocused and not international.”

“A high growth economic caseis needed.”

Sectio

nfiv

e

5.1 What are the key changes in the FES 2016 overview matrix?

Comments from stakeholders at the autumn workshops:

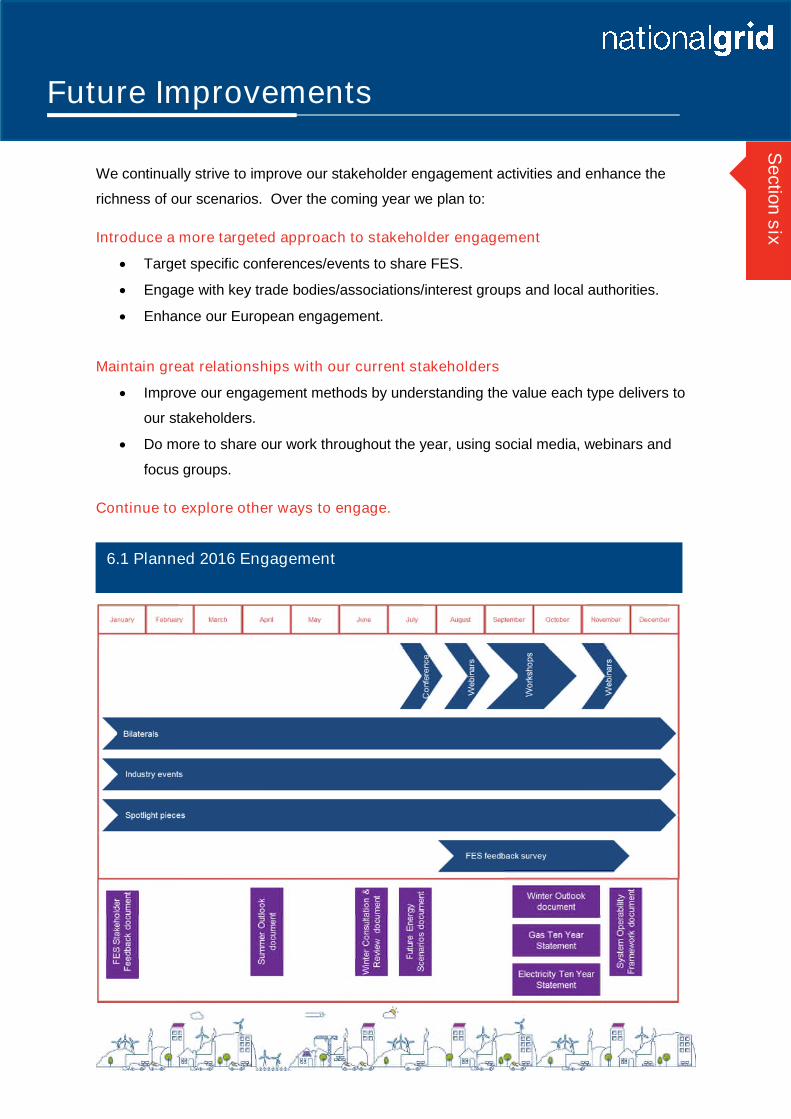

We continually strive to improve our stakeholder engagement activities and enhance the

richness of our scenarios. Over the coming year we plan to:

Introduce a more targeted approach to stakeholder engagement

Target specific conferences/events to share FES.

Engage with key trade bodies/associations/interest groups and local authorities.

Enhance our European engagement.

Maintain great relationships with our current stakeholders

Improve our engagement methods by understanding the value each type delivers to

our stakeholders.

Do more to share our work throughout the year, using social media, webinars and

focus groups.

Continue to explore other ways to engage.

Sectio

nsix

Future Improvements

6.1 Planned 2016 Engagement

Stakeholder GroupNo. of

organisationsconsulted

National Grid’s corporate stakeholdergroups

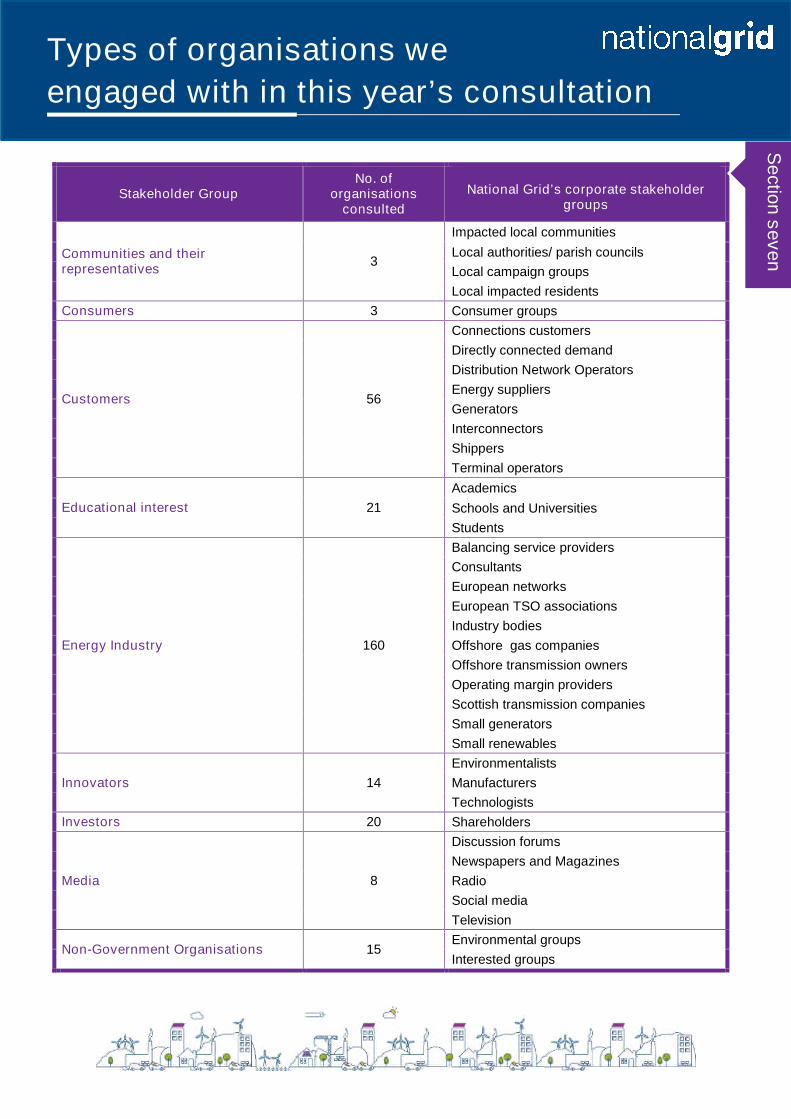

Communities and theirrepresentatives

3

Impacted local communities

Local authorities/ parish councils

Local campaign groups

Local impacted residents

Consumers 3 Consumer groups

Customers 56

Connections customers

Directly connected demand

Distribution Network Operators

Energy suppliers

Generators

Interconnectors

Shippers

Terminal operators

Educational interest 21

Academics

Schools and Universities

Students

Energy Industry 160

Balancing service providers

Consultants

European networks

European TSO associations

Industry bodies

Offshore gas companies

Offshore transmission owners

Operating margin providers

Scottish transmission companies

Small generators

Small renewables

Innovators 14

Environmentalists

Manufacturers

Technologists

Investors 20 Shareholders

Media 8

Discussion forums

Newspapers and Magazines

Radio

Social media

Television

Non-Government Organisations 15Environmental groups

Interested groups

Sectio

nseven

Types of organisations we

engaged with in this year’s consultation

Stakeholder GroupNo. of

organisationsconsulted

National Grid’s corporate stakeholdergroups

Political 13

Devolved administrations

European administration

Members of European Parliament

Members of Parliament

UK government

UK government bodies

Regulators 2European regulatory bodies

UK regulatory bodies

Small Businesses 30Individuals

Local community businesses

Supply Chain 17Partners

Suppliers

Types of organisations we

engaged with in this year’s consultation

Sectio

nseven

“In the last two years or so, we have used the FES documents as the starting

point for our analyses of the long term GB power market. We have found that

the four scenarios provide a good range of potential demand and

generation/energy mix with their supporting stories to reinforce our message

to client that the outlook is extremely uncertain and that they should adopt a

sufficiently flexible strategy or other risk mitigation measures. We have

tended to focus most on the implications for generation capacity of various

scales and types, as well as DSR and storage, however we have also used

the FES views on heat for examining district heat and System Marginal Price

(SMP) options. Our clients seem to be reassured that the projections in FES

have been developed through a broad stakeholder consultation process and

therefore are grounded, rather than being too academic.”

Guy Doyle, Mott MacDonald

National Grid UK

@nationalgriduk

NationalGridUK

Get involved in the debate on the future

of energy on Twitter, tweeting us

@nationalgriduk and join our LinkedIn

group ‘Future of Energy by National Grid’

Email us with your views on this

document or the FES at

one of our experts will get in touch

Access our current and past FES documents,

Stakeholder Feedback documents, data and

multimedia at http://fes.nationalgrid.com

Write to us at:

SO Strategy

Energy Insights

National Grid House

Warwick Technology Park

Gallows Hill

Warwick

CV34 6DA

Continuing the

conversation

Sectio

neig

ht

Disclaimer

For the purpose of this statement, National Grid Gas plc and National Grid Electricity Transmission plc willtogether be referred to as National Grid. The information contained within the Future Energy ScenariosStakeholder Feedback document (“the Document”) is disclosed voluntarily and without charge to you in order tofacilitate and encourage discussion of the scenarios used by National Grid in its electricity and gas planningprocesses.

The Document does not replace the Gas Ten Year Statement (GTYS) or the Electricity Ten Year Statement(ETYS) (or any other document published by National Grid containing substantially the same information asthose documents) published in accordance with the relevant licence conditions.

While National Grid have not sought to mislead any party as to the content of the Document and, whilst thecontent represents National Grid’s best views as of 22 January 2016, readers should not place any reliance onthe content of the Document. The Document (including, without limitation, information as regards capacityplanning, future investment and the resulting capacity) must be considered as illustrative only and no warrantycan be or is made as to the accuracy and completeness of such Document, nor shall anything within theDocument constitute an offer capable of acceptance or form the basis of any contract. Other than in the event offraudulent misstatement or fraudulent misrepresentation, National Grid does not accept any responsibility forany use which is made of the information contained within this Document.

Copyright National Grid 2016, all rights reserved. No part of the Document may be reproduced in any materialform (including photocopying and storing in any medium or electronic means and whether or not transiently orincidentally) without the written permission of National Grid except in accordance with the provisions of theCopyright, Designs and Patents Act 1988.