final accounts preparation - osbornebooks.co.uk · 4 incomplete records accounting layouts for the...

TRANSCRIPT

Osborne Books Tutor Zone

Final AccountsPreparationChapter activities

© Osborne Books Limited, 2016

2 f i n a l a c c o u n t s p r e p a r a t i o n t u t o r z o n e

Business organisations1

1.1 Link the type of business in the box on the left with the box on the right that best describes it.

Charity

Limited liability partnership (LLP)

Sole trader

Partnership

Limited company

1.2 Complete the following table showing how each organisation distributes its profits. Choose fromthe following options:Drawings by owner / Drawings by members / Dividends to shareholders / Drawings by partners

Profits distributed in the form of:

Limited liability partnership (LLP)

Sole trader

Partnership

Limited company

A group of individuals working together in business

An incorporated business owned by shareholders

An organisation run to fund charitable activities

An incorporated form of partnership

An individual trading in his name or a trading name

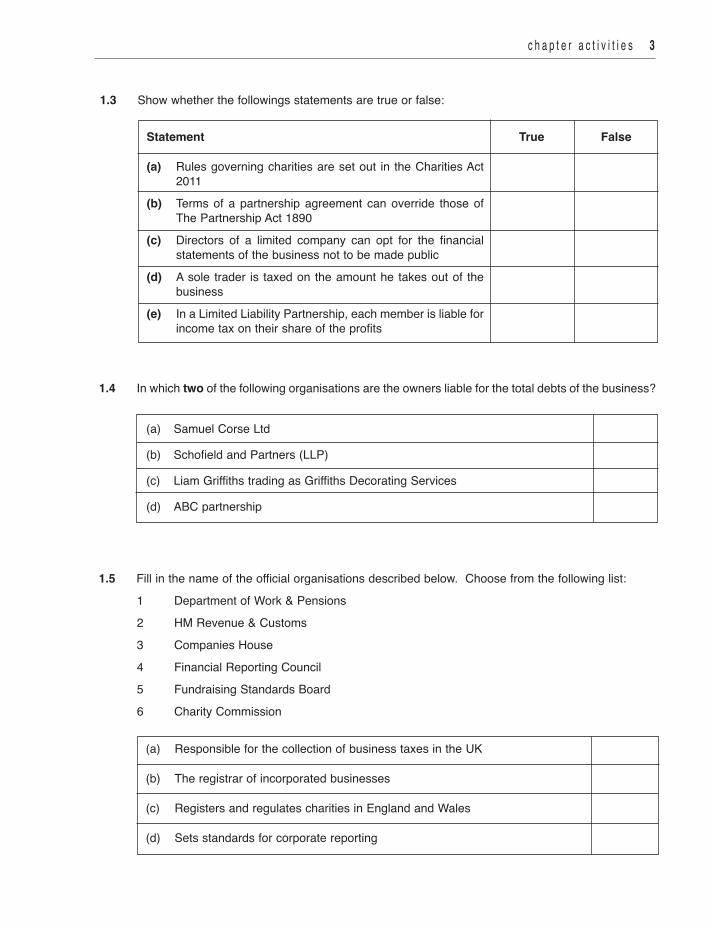

c h a p t e r a c t i v i t i e s 3

1.4 In which two of the following organisations are the owners liable for the total debts of the business?

(a) Samuel Corse Ltd

(b) Schofield and Partners (LLP)

(c) Liam Griffiths trading as Griffiths Decorating Services

(d) ABC partnership

1.3 Show whether the followings statements are true or false:

Statement True False

(a) Rules governing charities are set out in the Charities Act2011

(b) Terms of a partnership agreement can override those ofThe Partnership Act 1890

(c) Directors of a limited company can opt for the financialstatements of the business not to be made public

(d) A sole trader is taxed on the amount he takes out of thebusiness

(e) In a Limited Liability Partnership, each member is liable forincome tax on their share of the profits

1.5 Fill in the name of the official organisations described below. Choose from the following list:1 Department of Work & Pensions2 HM Revenue & Customs3 Companies House4 Financial Reporting Council5 Fundraising Standards Board 6 Charity Commission

(a) Responsible for the collection of business taxes in the UK

(b) The registrar of incorporated businesses

(c) Registers and regulates charities in England and Wales

(d) Sets standards for corporate reporting

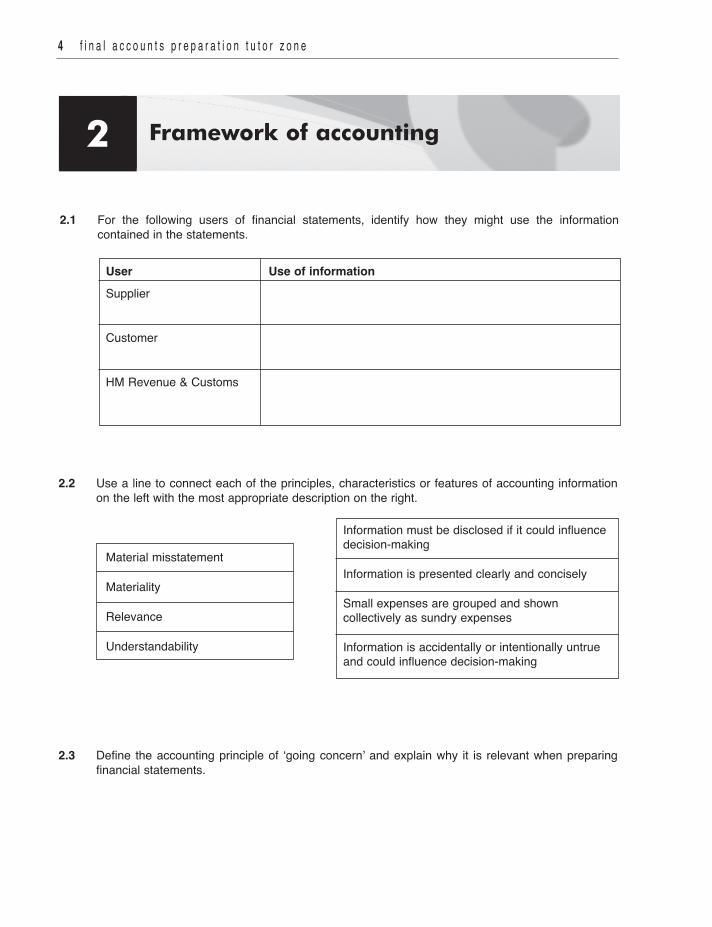

4 f i n a l a c c o u n t s p r e p a r a t i o n t u t o r z o n e

Framework of accounting2

2.2 Use a line to connect each of the principles, characteristics or features of accounting informationon the left with the most appropriate description on the right.

Material misstatement

Materiality

Relevance

Understandability

Information must be disclosed if it could influencedecision-making

Information is presented clearly and concisely

Small expenses are grouped and showncollectively as sundry expenses

Information is accidentally or intentionally untrueand could influence decision-making

2.1 For the following users of financial statements, identify how they might use the informationcontained in the statements.

User Use of informationSupplier

Customer

HM Revenue & Customs

2.3 Define the accounting principle of ‘going concern’ and explain why it is relevant when preparingfinancial statements.

c h a p t e r a c t i v i t i e s 5

2.4 Identify the five ethical principles of accounting from the following list.

(a) Security(b) Professional competence and due care(c) Faithful representation(d) Objectivity(e) Neutrality(f) Honesty (g) Integrity(h) Professional behaviour(i) Confidentiality(j) Verifiability

2.5 Which supporting qualitative characteristic of accounting information is relevant in each of thefollowing situations? Choose from: Understandability, Verifiability, Comparability, Timeliness.

Supporting qualitative characteristic

(a) Inventory valuation is accurate and based onIAS 2 Inventories

(b) Financial statements are ready for review andsubmission when required

(c) The layout and format of financial statementsis similar to that used in previous periods andby other businesses

(d) Clarification is given in the form of supportingnotes in the financial statements

2.6 One of the main accounting principles is that of accruals. Which of the following definitions bestdefines the accruals principle?

(a) Accounting values are estimated to give a realistic profit figure

(b) Accounting transactions are recorded in the period in which they are incurred

(c) Accounting transactions are recorded in the period in which they are paid for

(d) Accounting transactions are recorded according to the type of business involved

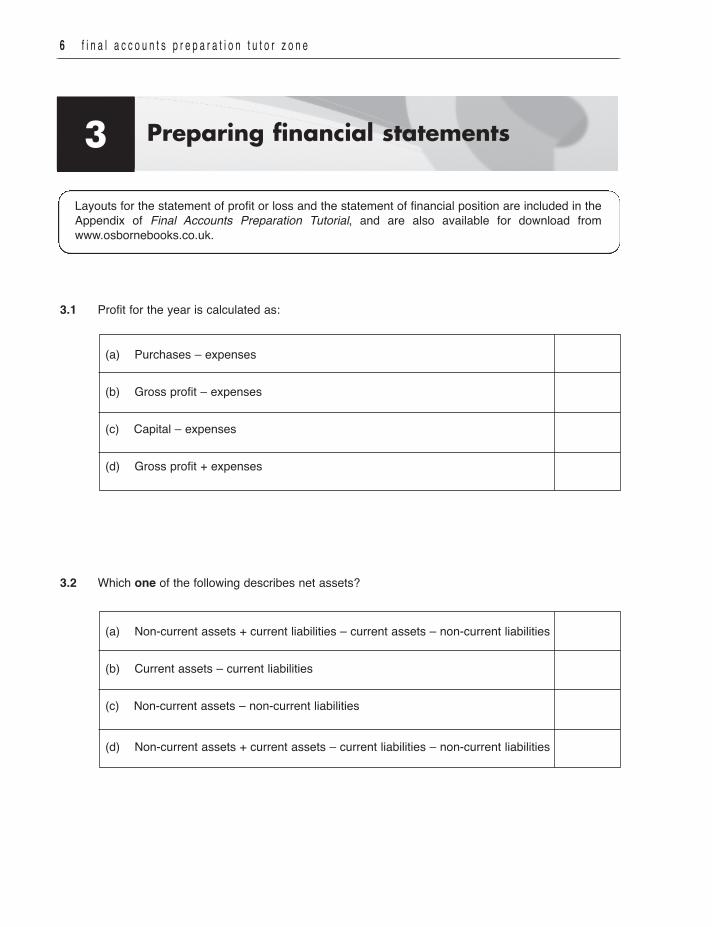

3.1 Profit for the year is calculated as:

(a) Purchases – expenses

(b) Gross profit – expenses

(c) Capital – expenses

(d) Gross profit + expenses

3.2 Which one of the following describes net assets?

(a) Non-current assets + current liabilities – current assets – non-current liabilities

(b) Current assets – current liabilities

(c) Non-current assets – non-current liabilities

(d) Non-current assets + current assets – current liabilities – non-current liabilities

6 f i n a l a c c o u n t s p r e p a r a t i o n t u t o r z o n e

Preparing financial statements3

Layouts for the statement of profit or loss and the statement of financial position are included in theAppendix of Final Accounts Preparation Tutorial, and are also available for download fromwww.osbornebooks.co.uk.

c h a p t e r a c t i v i t i e s 7

3.3 You are to fill in the missing figures for the following sole trader businesses:

Sales Opening Purchases Closing Gross Expenses Profit/loss* inventory inventory profit for year £ £ £ £ £ £ £

Business A 75,000 7,000 50,000 8,000 ........ 16,000 ........

Business B ......... 10,000 65,000 8,000 22,000 ......... 15,000

Business C 64,000 9,500 52,000 ......... 13,500 15,500 ........

Business D 44,350 6,250 ......... 7,350 26,050 ......... 13,600

Business E 49,750 ........ 26,750 9,600 23,900 18,600 ........

Business F 75,000 11,500 47,500 ........ 26,500 ......... –5,500

*Note: loss is indicated by a minus sign

8 f i n a l a c c o u n t s p r e p a r a t i o n t u t o r z o n e

3.4 This Activity is about calculating missing balances and the accounting equation.You are given the following information about a sole trader as at 1 April 20-7:The value of assets and liabilities were:

• Non-current assets at carrying amount £50,500 • Inventory £9,450 • Trade receivables £18,750 • Cash at bank £2,140 • Trade payables £11,380 There were no other assets or liabilities.

(a) Calculate the capital account balance as at 1 April 20-7.

£

(b) On 30 April 20-7, new office equipment is purchased on credit for use in the business. Tickthe boxes to show what effect this transaction will have on the balances. You must chooseone answer for each line.

Debit Credit No change

Non-current assets

Trade receivables

Trade payables

Bank

Capital

(c) Which of the following is a current asset? Select one answer.

(a) Owner’s capital

(b) A bank overdraft

(c) Trade payables

(d) Trade receivables

c h a p t e r a c t i v i t i e s 9

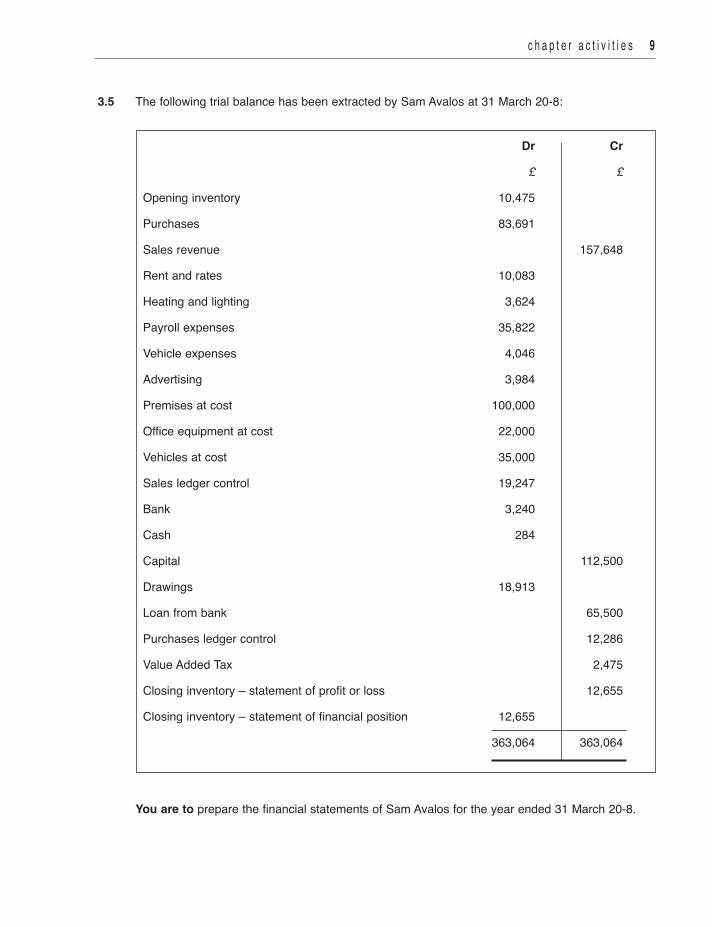

3.5 The following trial balance has been extracted by Sam Avalos at 31 March 20-8:

Dr Cr

£ £

Opening inventory 10,475

Purchases 83,691

Sales revenue 157,648

Rent and rates 10,083

Heating and lighting 3,624

Payroll expenses 35,822

Vehicle expenses 4,046

Advertising 3,984

Premises at cost 100,000

Office equipment at cost 22,000

Vehicles at cost 35,000

Sales ledger control 19,247

Bank 3,240

Cash 284

Capital 112,500

Drawings 18,913

Loan from bank 65,500

Purchases ledger control 12,286

Value Added Tax 2,475

Closing inventory – statement of profit or loss 12,655

Closing inventory – statement of financial position 12,655

363,064 363,064

You are to prepare the financial statements of Sam Avalos for the year ended 31 March 20-8.

1 0 f i n a l a c c o u n t s p r e p a r a t i o n t u t o r z o n e

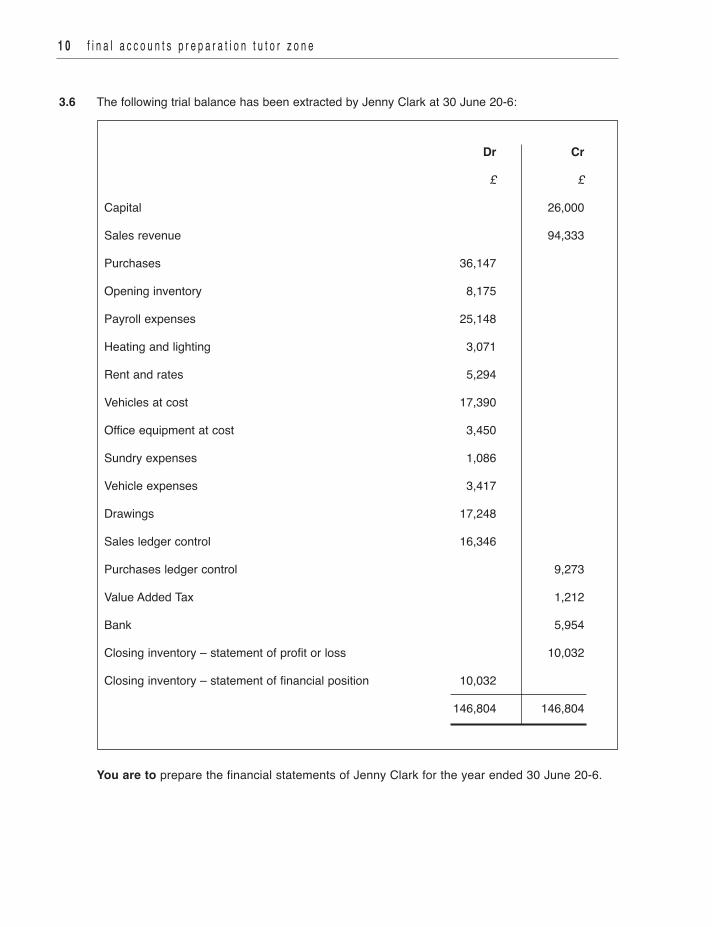

3.6 The following trial balance has been extracted by Jenny Clark at 30 June 20-6:

Dr Cr

£ £

Capital 26,000

Sales revenue 94,333

Purchases 36,147

Opening inventory 8,175

Payroll expenses 25,148

Heating and lighting 3,071

Rent and rates 5,294

Vehicles at cost 17,390

Office equipment at cost 3,450

Sundry expenses 1,086

Vehicle expenses 3,417

Drawings 17,248

Sales ledger control 16,346

Purchases ledger control 9,273

Value Added Tax 1,212

Bank 5,954

Closing inventory – statement of profit or loss 10,032

Closing inventory – statement of financial position 10,032

146,804 146,804

You are to prepare the financial statements of Jenny Clark for the year ended 30 June 20-6.

c h a p t e r a c t i v i t i e s 1 1

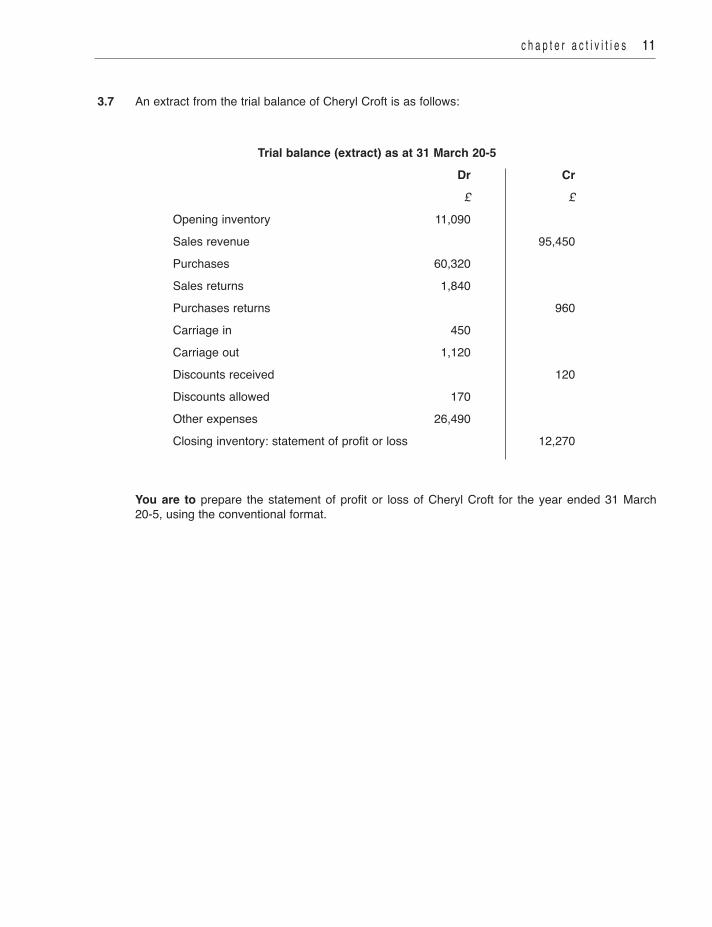

3.7 An extract from the trial balance of Cheryl Croft is as follows:

Trial balance (extract) as at 31 March 20-5 Dr Cr £ £ Opening inventory 11,090 Sales revenue 95,450 Purchases 60,320 Sales returns 1,840 Purchases returns 960 Carriage in 450 Carriage out 1,120 Discounts received 120 Discounts allowed 170 Other expenses 26,490 Closing inventory: statement of profit or loss 12,270

You are to prepare the statement of profit or loss of Cheryl Croft for the year ended 31 March

20-5, using the conventional format.

1 2 f i n a l a c c o u n t s p r e p a r a t i o n t u t o r z o n e

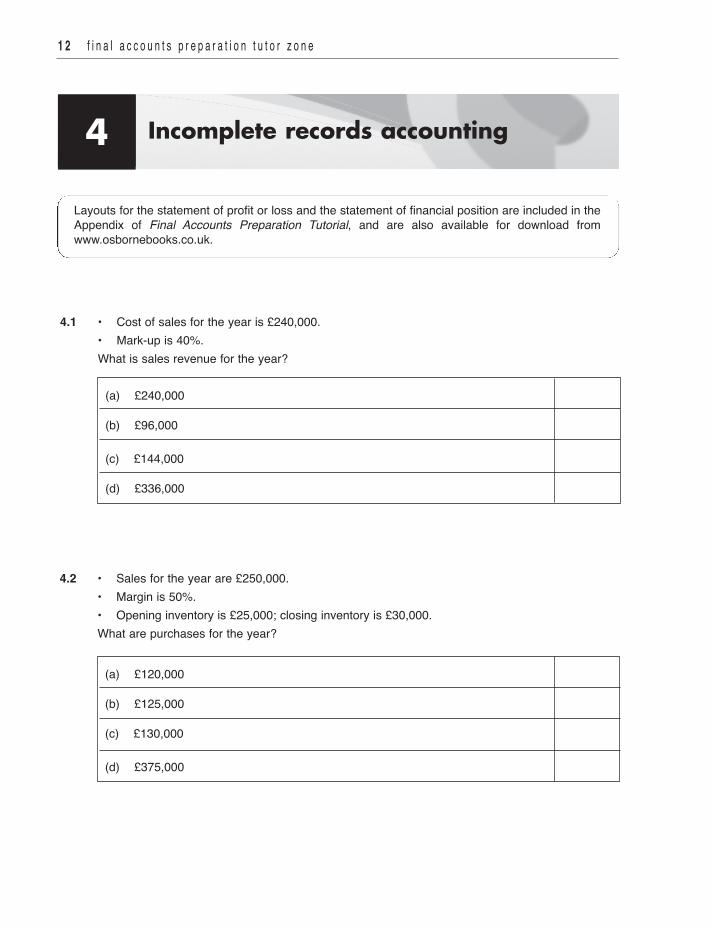

4.1 • Cost of sales for the year is £240,000.• Mark-up is 40%.What is sales revenue for the year?

(a) £240,000

(b) £96,000

(c) £144,000

(d) £336,000

4.2 • Sales for the year are £250,000.• Margin is 50%.• Opening inventory is £25,000; closing inventory is £30,000.What are purchases for the year?

(a) £120,000

(b) £125,000

(c) £130,000

(d) £375,000

Incomplete records accounting4

Layouts for the statement of profit or loss and the statement of financial position are included in theAppendix of Final Accounts Preparation Tutorial, and are also available for download fromwww.osbornebooks.co.uk.

c h a p t e r a c t i v i t i e s 1 3

4.3 You are preparing accounts from incomplete records. Trade receivables at the start of the year were£20,400. During the year sales on credit total £90,300, bank receipts from trade receivables total£85,600, sales returns total £1,400, and discounts allowed total £700.What is the trade receivables figure at the end of the year?

(a) £13,600

(b) £27,200

(c) £23,000

(d) £24,400

4.4 The following figures are extracted from the accounts of Wyvern Systems Limited for the yearended 30 June 20-8:• sales for the year, £300,000• opening inventory, £20,000• closing inventory, £40,000• purchases for the year, £260,000

You are to calculate:(a) cost of sales for the year(b) gross profit for the year(c) gross profit mark up %(d) gross sales margin %

1 4 f i n a l a c c o u n t s p r e p a r a t i o n t u t o r z o n e

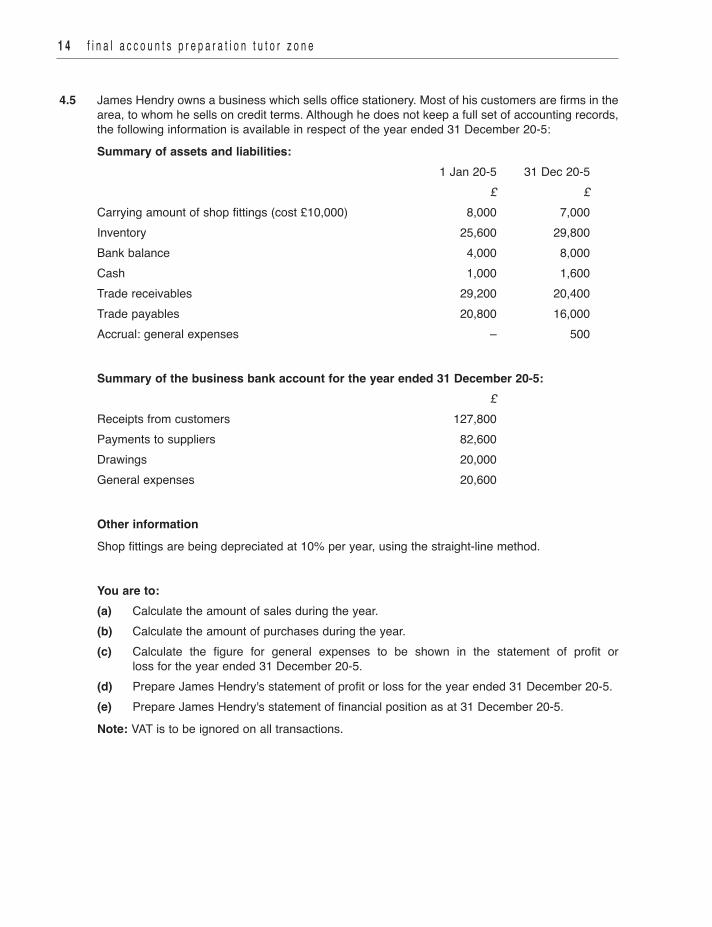

4.5 James Hendry owns a business which sells office stationery. Most of his customers are firms in thearea, to whom he sells on credit terms. Although he does not keep a full set of accounting records,the following information is available in respect of the year ended 31 December 20-5:Summary of assets and liabilities: 1 Jan 20-5 31 Dec 20-5 £ £Carrying amount of shop fittings (cost £10,000) 8,000 7,000Inventory 25,600 29,800Bank balance 4,000 8,000Cash 1,000 1,600Trade receivables 29,200 20,400Trade payables 20,800 16,000Accrual: general expenses – 500

Summary of the business bank account for the year ended 31 December 20-5: £Receipts from customers 127,800Payments to suppliers 82,600Drawings 20,000General expenses 20,600

Other informationShop fittings are being depreciated at 10% per year, using the straight-line method.

You are to:(a) Calculate the amount of sales during the year.(b) Calculate the amount of purchases during the year.(c) Calculate the figure for general expenses to be shown in the statement of profit or loss for the year ended 31 December 20-5.(d) Prepare James Hendry's statement of profit or loss for the year ended 31 December 20-5.(e) Prepare James Hendry's statement of financial position as at 31 December 20-5.Note: VAT is to be ignored on all transactions.

c h a p t e r a c t i v i t i e s 1 5

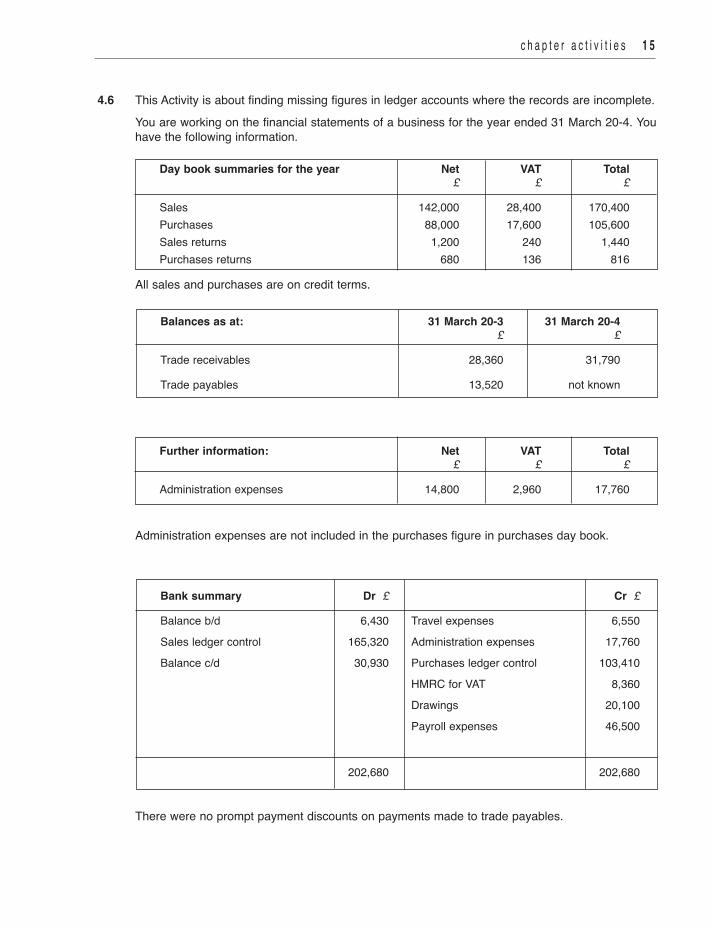

4.6 This Activity is about finding missing figures in ledger accounts where the records are incomplete.You are working on the financial statements of a business for the year ended 31 March 20-4. Youhave the following information.

All sales and purchases are on credit terms.

Administration expenses are not included in the purchases figure in purchases day book.

There were no prompt payment discounts on payments made to trade payables.

Day book summaries for the year Net VAT Total £ £ £

Sales 142,000 28,400 170,400 Purchases 88,000 17,600 105,600 Sales returns 1,200 240 1,440 Purchases returns 680 136 816

Balances as at: 31 March 20-3 31 March 20-4 £ £

Trade receivables 28,360 31,790

Trade payables 13,520 not known

Further information: Net VAT Total £ £ £

Administration expenses 14,800 2,960 17,760

Bank summary Dr £ Cr £

Balance b/d 6,430 Travel expenses 6,550 Sales ledger control 165,320 Administration expenses 17,760 Balance c/d 30,930 Purchases ledger control 103,410 HMRC for VAT 8,360 Drawings 20,100 Payroll expenses 46,500

202,680 202,680

1 6 f i n a l a c c o u n t s p r e p a r a t i o n t u t o r z o n e

(a) Using the figures given on the previous page, prepare the sales ledger control account forthe year ended 31 March 20-4. Show discounts allowed as the balancing figure.

Sales ledger control account

(b) Using the figures given on the previous page, prepare the purchases ledger control accountfor the year ended 31 March 20-4. Show clearly the trade payables figure at the end of theyear as the balancing figure.

Purchases ledger control account

(c) Find the closing balance for VAT by preparing the VAT control account for the year ended31 March 20-4. Use the figures given on the previous page, and in the answer to (a) above.

Note: The business is not charged VAT on its travel expenses.

VAT control account

Balance b/d 3,460

c h a p t e r a c t i v i t i e s 1 7

5.1 A statement of profit or loss shows a loss for the year of £5,800. It is discovered that no allowancehas been made for payroll expenses accrued of £550 and rent prepaid of £250 at the year end.What is the adjusted loss for the year?

(a) £6,600

(b) £5,000

(c) £6,100

(d) £5,500

5.2 Identify whether the following items will be stated in the year end statement of profit or loss asincome or expense by selecting the relevant column of the table below.

Item Income Expense

Loss on disposal of non-current asset

Increase in allowance for doubtful debts

Irrecoverable debts

Discounts received

Depreciation charges

Carriage out

Sole trader financial statements5

Layouts for the statement of profit or loss and the statement of financial position are included in theAppendix of Final Accounts Preparation Tutorial, and are also available for download fromwww.osbornebooks.co.uk.

1 8 f i n a l a c c o u n t s p r e p a r a t i o n t u t o r z o n e

5.3 A statement of profit or loss shows a profit for the year of £15,240. The owner of the businesswishes to decrease the allowance for doubtful debts by £600 and to write off irrecoverable debts of£200. What is the adjusted profit for the year?

(a) £15,640

(b) £14,840

(c) £16,040

(d) £14,440

c h a p t e r a c t i v i t i e s 1 9

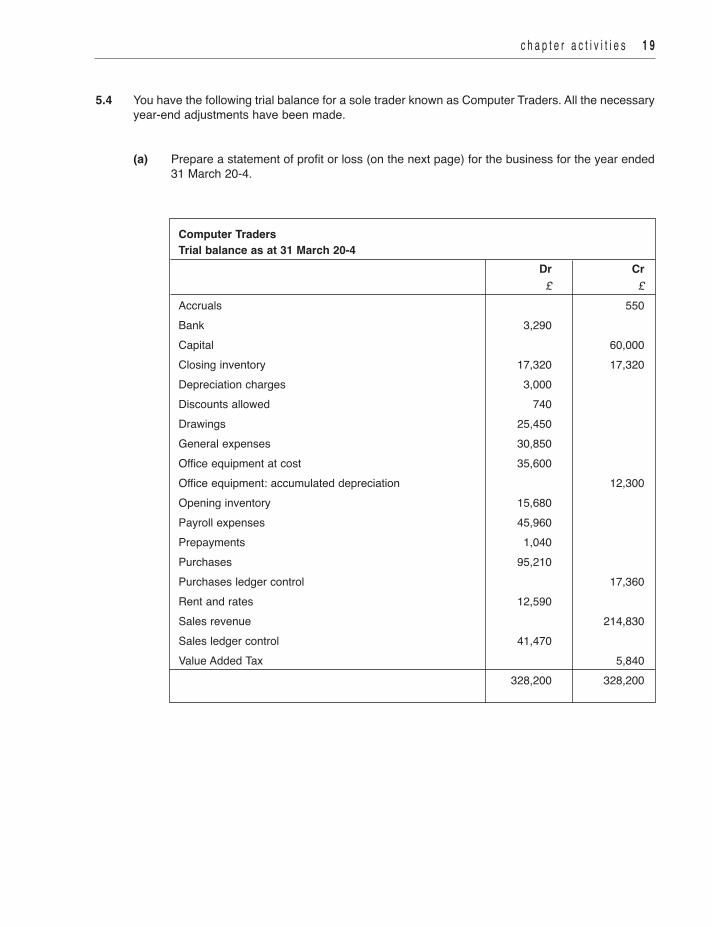

5.4 You have the following trial balance for a sole trader known as Computer Traders. All the necessaryyear-end adjustments have been made.

(a) Prepare a statement of profit or loss (on the next page) for the business for the year ended31 March 20-4.

Computer Traders Trial balance as at 31 March 20-4 Dr Cr £ £ Accruals 550 Bank 3,290 Capital 60,000 Closing inventory 17,320 17,320 Depreciation charges 3,000 Discounts allowed 740 Drawings 25,450 General expenses 30,850 Office equipment at cost 35,600 Office equipment: accumulated depreciation 12,300 Opening inventory 15,680 Payroll expenses 45,960 Prepayments 1,040 Purchases 95,210 Purchases ledger control 17,360 Rent and rates 12,590 Sales revenue 214,830 Sales ledger control 41,470 Value Added Tax 5,840 328,200 328,200

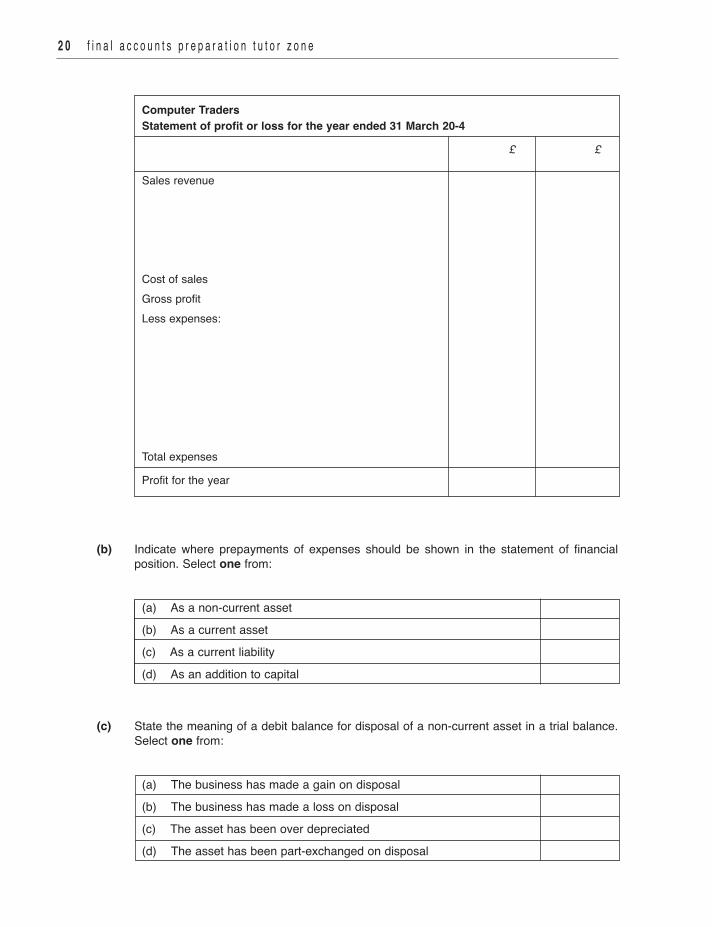

2 0 f i n a l a c c o u n t s p r e p a r a t i o n t u t o r z o n e

Computer Traders Statement of profit or loss for the year ended 31 March 20-4

£ £

Sales revenue Cost of sales Gross profit Less expenses:

Total expenses

Profit for the year

(b) Indicate where prepayments of expenses should be shown in the statement of financialposition. Select one from:

(a) As a non-current asset (b) As a current asset (c) As a current liability (d) As an addition to capital

(c) State the meaning of a debit balance for disposal of a non-current asset in a trial balance.Select one from:

(a) The business has made a gain on disposal (b) The business has made a loss on disposal (c) The asset has been over depreciated (d) The asset has been part-exchanged on disposal

c h a p t e r a c t i v i t i e s 2 1

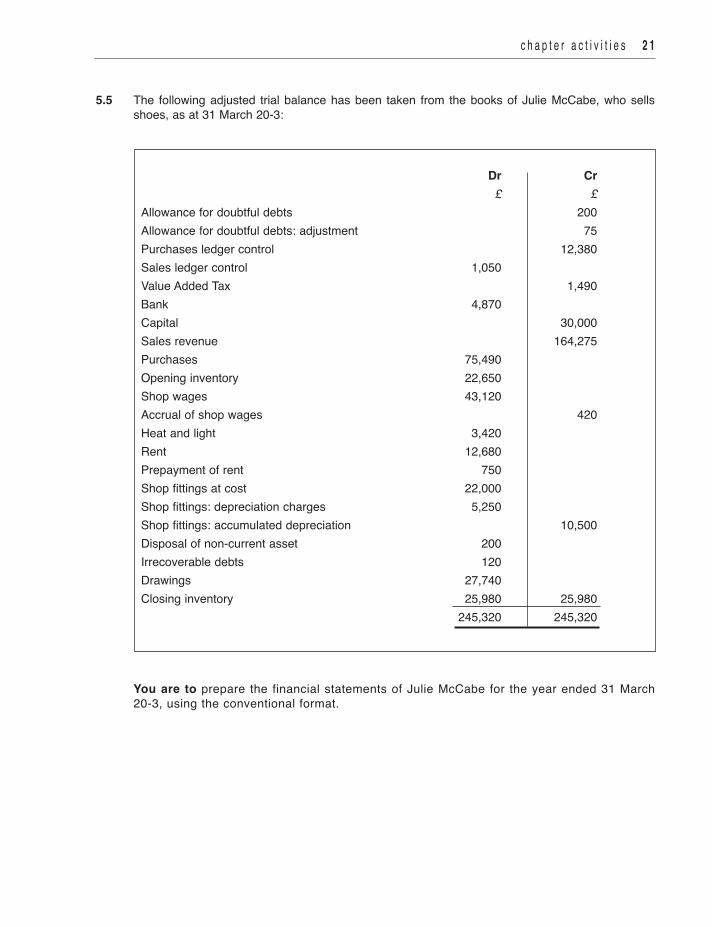

5.5 The following adjusted trial balance has been taken from the books of Julie McCabe, who sellsshoes, as at 31 March 20-3:

Dr Cr £ £ Allowance for doubtful debts 200 Allowance for doubtful debts: adjustment 75 Purchases ledger control 12,380 Sales ledger control 1,050 Value Added Tax 1,490 Bank 4,870 Capital 30,000 Sales revenue 164,275 Purchases 75,490 Opening inventory 22,650 Shop wages 43,120 Accrual of shop wages 420 Heat and light 3,420 Rent 12,680 Prepayment of rent 750 Shop fittings at cost 22,000 Shop fittings: depreciation charges 5,250 Shop fittings: accumulated depreciation 10,500 Disposal of non-current asset 200 Irrecoverable debts 120 Drawings 27,740 Closing inventory 25,980 25,980 245,320 245,320

You are to prepare the financial statements of Julie McCabe for the year ended 31 March20-3, using the conventional format.

2 2 f i n a l a c c o u n t s p r e p a r a t i o n t u t o r z o n e

6.1 Profits of a two-person partnership are £24,600 before the following are taken into account:• interest on partners’ capital accounts, £2,200• salary of one partner, £12,500• interest on partners’ drawings £500

If the remaining profits are shared equally, how much will each partner receive?

(a) £12,300

(b) £7,400

(c) £5,200

(d) £6,900

Partnership financial statements6

Layouts for the statement of profit or loss and the statement of financial position are included in theAppendix of Final Accounts Preparation Tutorial, and are also available for download fromwww.osbornebooks.co.uk.

c h a p t e r a c t i v i t i e s 2 3

6.2 You have the following information about a partnership business:• The financial year ends on 31 March• The partners are Joe, Kit and Liz• Partners’ annual salaries: Joe £12,600 Kit £20,900 Liz £5,350• Partners’ capital account balances as at 31 March 20-7: Joe £40,000 Kit £30,000 Liz £20,000• Interest on partners’ capital for the year: Joe £1,200 Kit £900 Liz £600• Interest charged on partners’ drawings: Joe £120 Kit £310 Liz £90• The partners share the remaining profit of £22,000 as follows: Joe 40% Kit 35% Liz 25%• Partners’ drawings for the year: Joe £16,350 Kit £26,490 Liz £12,600Prepare the current accounts for the partners for the year ended 31 March 20-7. Show clearly thebalances carried down. You must enter zeros where appropriate. Do not use brackets, minus signsor dashes.

Current accounts

Joe £ Kit £ Liz £ Joe £ Kit £ Liz £Balance b/d 200 0 0 Balance b/d 0 600 1,000

2 4 f i n a l a c c o u n t s p r e p a r a t i o n t u t o r z o n e

6.3 This Activity is about preparing a partnership statement of financial position.You are preparing the statement of financial position for the JK Partnership as at 31 March 20-5.The partners are Jon and Kim.All the necessary year-end adjustments have been made, except for the transfer of profit to thecurrent accounts of the partners.Before sharing profits the balances of the partners’ current accounts are:• Jon £750 debit• Kim £400 creditEach partner is entitled to £6,500 profit share.

(a) Calculate the balance of each partner’s current account after sharing profits. Indicatewhether these balances are DEBIT or CREDIT.

Current account: Jon £ DEBIT / CREDIT

Current account: Kim £ DEBIT / CREDIT

Note: these balances will need to be transferred into the statement of financial position ofthe partnership which follows.

c h a p t e r a c t i v i t i e s 2 5

You have the following trial balance. All the necessary year end adjustments have been made.

(b) Prepare a statement of financial position for the partnership as at 31 March 20-5. You needto use the partners’ current account balances that you have just calculated. Do not usebrackets, minus signs or dashes.

JK Partnership Trial balance as at 31 March 20-5

Dr £ Cr £ Accruals 590 Administration expenses 23,850 Allowance for doubtful debts 760 Allowance for doubtful debts: adjustment 150 Bank 4,680 Capital account – Jon 30,000 Capital account – Kim 20,000 Cash 570 Closing inventory 12,630 12,630 Current account – Jon 750 Current account – Kim 400 Depreciation charges 3,000 Disposal of non-current asset 220 Machinery at cost 40,000 Machinery: accumulated depreciation 12,500 Opening inventory 11,220 Payroll expenses 43,260 Purchases 73,840 Purchases ledger control 14,750 Sales revenue 155,910 Sales ledger control 36,230 Value Added Tax 2,860 Total 250,400 250,400

2 6 f i n a l a c c o u n t s p r e p a r a t i o n t u t o r z o n e

JK Partnership Statement of financial position as at 31 March 20-5

Cost Accumulated Carrying amount depreciation Non-current assets £ £ £

Current assets

Current liabilities

Net current assets

Net assets

Financed by: Jon Kim Total

c h a p t e r a c t i v i t i e s 2 7

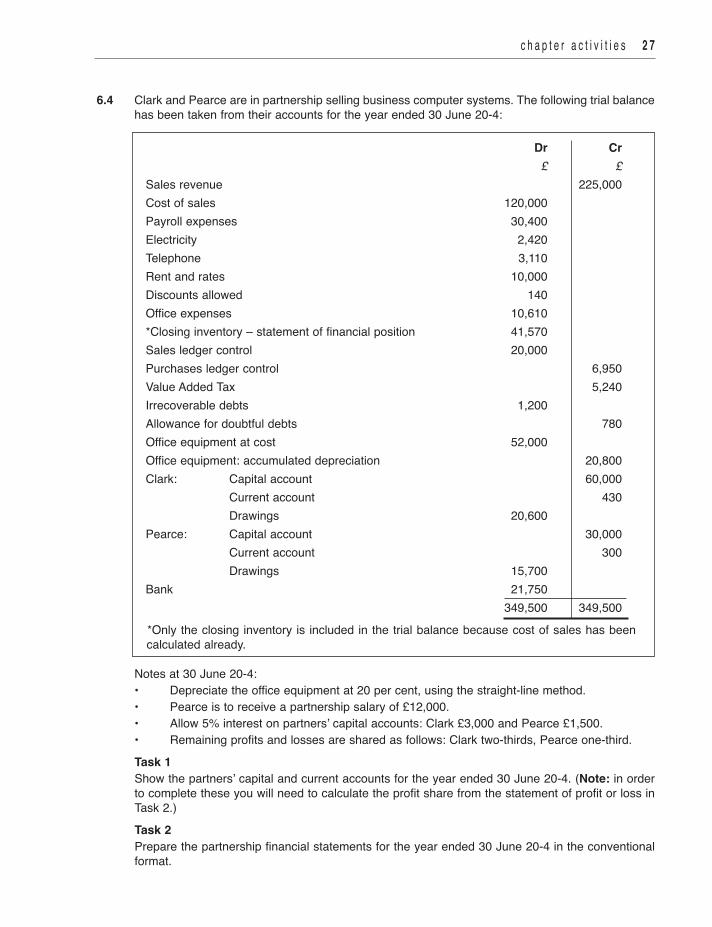

6.4 Clark and Pearce are in partnership selling business computer systems. The following trial balancehas been taken from their accounts for the year ended 30 June 20-4:

Dr Cr £ £ Sales revenue 225,000 Cost of sales 120,000 Payroll expenses 30,400 Electricity 2,420 Telephone 3,110 Rent and rates 10,000 Discounts allowed 140 Office expenses 10,610 *Closing inventory – statement of financial position 41,570 Sales ledger control 20,000 Purchases ledger control 6,950 Value Added Tax 5,240 Irrecoverable debts 1,200 Allowance for doubtful debts 780 Office equipment at cost 52,000 Office equipment: accumulated depreciation 20,800 Clark: Capital account 60,000 Current account 430 Drawings 20,600 Pearce: Capital account 30,000 Current account 300 Drawings 15,700 Bank 21,750 349,500 349,500*Only the closing inventory is included in the trial balance because cost of sales has beencalculated already.

Notes at 30 June 20-4:• Depreciate the office equipment at 20 per cent, using the straight-line method.• Pearce is to receive a partnership salary of £12,000.• Allow 5% interest on partners’ capital accounts: Clark £3,000 and Pearce £1,500.• Remaining profits and losses are shared as follows: Clark two-thirds, Pearce one-third.Task 1Show the partners’ capital and current accounts for the year ended 30 June 20-4. (Note: in orderto complete these you will need to calculate the profit share from the statement of profit or loss inTask 2.)Task 2

Prepare the partnership financial statements for the year ended 30 June 20-4 in the conventionalformat.

2 8 f i n a l a c c o u n t s p r e p a r a t i o n t u t o r z o n e

7.2 Rachel and Sonia are in partnership sharing profits equally. Each has a capital account with abalance of £40,000. Trish joins as a new partner. The profit share will be Rachel 60%, Sonia 30%and Trish 10%. An adjustment is made for goodwill on the admission of Trish to the value of£30,000, but no goodwill is to be left in the accounts. What will be the balance of Rachel’s capitalaccount after the creation and write off of goodwill?

(a) £43,000

(b) £55,000

(c) £37,000

(d) £22,000

7.1 Anne, Beth and Carol are in partnership sharing profits equally. Anne is to retire and it is agreedthat goodwill is worth £24,000. After Anne’s retirement, Beth and Carol will continue to run thepartnership and will share profits equally. What will be the goodwill adjustments to Carol’s capitalaccount?

(a) Debit £8,000; credit £12,000

(b) Debit £12,000; credit £8,000

(c) Debit £8,000; credit £8,000

(d) Debit £12,000; credit £12,000

Changes in partnerships 7

c h a p t e r a c t i v i t i e s 2 9

7.3 You have the following information about a partnership:The partners are Dan and Eve.

• Fay was admitted to the partnership on 1 April 20-5 when she paid £30,000 into the bankaccount as her capital.

• Profit share, effective until 31 March 20-5: – Dan 40% – Eve 60%• Profit share, effective from 1 April 20-5: – Dan 30% – Eve 50% – Fay 20%• Goodwill was valued at £20,000 on 31 March 20-5.

• Goodwill is to be introduced into the partners’ capital accounts on 31 March and theneliminated on 1 April.

(a) Prepare the goodwill account of the partnership, showing clearly the transactions on theadmission of Fay, the new partner.

Goodwill account

(b) Prepare the capital account for Fay, the new partner, showing clearly the balance carrieddown as at 1 April 20-5.

Capital account – Fay

Balance b/d 0

3 0 f i n a l a c c o u n t s p r e p a r a t i o n t u t o r z o n e

(c) Identify whether the following statements about the partnership of Dan, Eve and Fay aretrue or false by putting a tick in the relevant column of the table below.

Statement True False

Fay has paid a premium to join the existing partnership of Dan and Eve

The balances of Dan and Eve’s capital accounts will increase because goodwill has been charged to Fay

Dan and Eve have each paid money to Fay when she joined the partnership

After the admission of Fay, the bank account of the partnership will have £30,000 extra minus the amount paid by Fay for goodwill

c h a p t e r a c t i v i t i e s 3 1

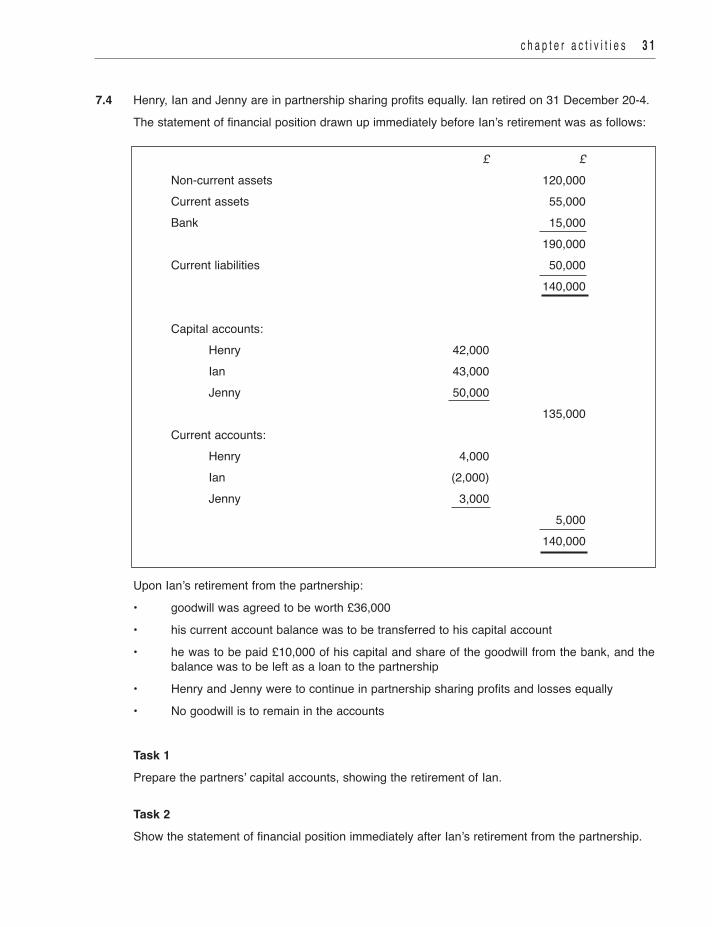

7.4 Henry, Ian and Jenny are in partnership sharing profits equally. Ian retired on 31 December 20-4.The statement of financial position drawn up immediately before Ian’s retirement was as follows:

£ £ Non-current assets 120,000 Current assets 55,000 Bank 15,000 190,000 Current liabilities 50,000 140,000

Capital accounts: Henry 42,000 Ian 43,000 Jenny 50,000 135,000 Current accounts: Henry 4,000 Ian (2,000) Jenny 3,000 5,000 140,000

Upon Ian’s retirement from the partnership: • goodwill was agreed to be worth £36,000 • his current account balance was to be transferred to his capital account • he was to be paid £10,000 of his capital and share of the goodwill from the bank, and the

balance was to be left as a loan to the partnership • Henry and Jenny were to continue in partnership sharing profits and losses equally • No goodwill is to remain in the accounts

Task 1 Prepare the partners’ capital accounts, showing the retirement of Ian.

Task 2 Show the statement of financial position immediately after Ian’s retirement from the partnership.

3 2 f i n a l a c c o u n t s p r e p a r a t i o n t u t o r z o n e

7.5 Gil and Hal are in partnership. Profit for the year ended 31 March 20-7 is £51,300 beforeappropriation of profit. The partnership allows for the following:• Partnership commission – Gil £18,000 – Hal £12,000• Profit share – Gil two thirds – Hal one third• Interest on capital – Gil £400 – Hal £500• Drawings for the year – Gil £24,000 – Hal £20,000

Task 1Prepare the partnership appropriation account for Gil and Hal for the year ended 31 March 20-7.

Gil and HalPartnership appropriation account for the year ended 31 March 20-7

Total Gil Hal £ £ £

Profit for the year

Commission

Interest on capital

Profit available for distribution

Profit share:

Gil

Hal

Total profit distributed

c h a p t e r a c t i v i t i e s 3 3

Task 2Update the current accounts for the partnership for the year ended 31 March 20-7. Show clearly thebalances carried down.

Dr Partners’ current accounts Cr Gil Hal Gil Hal £ £ £ £ 1 Apr 20-6 Balance b/d – 2,000 1 Apr 20-6 Balance b/d 4,500 –

7.6 Partners Deb and Maj shared profits and losses 60:40 until 30 September 20-1 when their capitalaccounts showed credit balances of: Deb £45,000; Maj £50,000. From 1 October 20-1 they agreeto share profits equally. Goodwill is valued at £40,000 and is introduced into their capital accountsand then eliminated. What is the balance of Maj’s capital account after the creation and write-off ofgoodwill?

(a) £54,000 credit

(b) £46,000 credit

(c) £49,000 credit

(d) £46,000 debit

3 4 f i n a l a c c o u n t s p r e p a r a t i o n t u t o r z o n e

Introduction to company financialstatements8

8.1 Fill in the gaps in the following sentences. Choose from the words below.

IAS 1 ……………………………. of Financial Statements sets out the ……………………………

contents for financial statements of …………………………………. and the accounting

…………… on which the statements should be prepared. These concepts include

………………………………. and ……………………… basis of accounting.

equity maximumprinciples partnershipsproduction going concern accruals minimum companies presentation

8.2 Link the items on the left with the description on the right that best defines them.

IAS 2 Inventories Guidance on how to determine the carrying amount ofnon-current assets

IFRSs The primary source of UK company law

IAS 16 Property,Plant & Equipment

Established so that business accounts can beunderstood from company to company and from countryto country

Companies Act Guidance on the acceptable methods of valuing goodsheld in stock

c h a p t e r a c t i v i t i e s 3 5

8.3 (a) Indicate in which financial statement of a company the following summarised items willappear.

Item Statement of Statement of profit or loss financial position

(a) Cost of sales

(b) Tax liabilities

(c) Goodwill

(d) Issued share capital

(e) Distribution costs

(f) Inventories

(b) Give two examples of accounting information that might be included in each of the followingsummarised items:

1 Distribution costs 2 Cost of sales 3 Trade and other receivables

8.4 Which of the following are obligations of the directors of a limited company? 1 To report to shareholders on how the company has been been run 2 To file annual statements with the Registrar of Companies. 3 To disclose the company’s financial position in the financial statements

(a) 1 only

(b) 1 and 2

(c) 1 and 3

(d) All of them

3 6 f i n a l a c c o u n t s p r e p a r a t i o n t u t o r z o n e

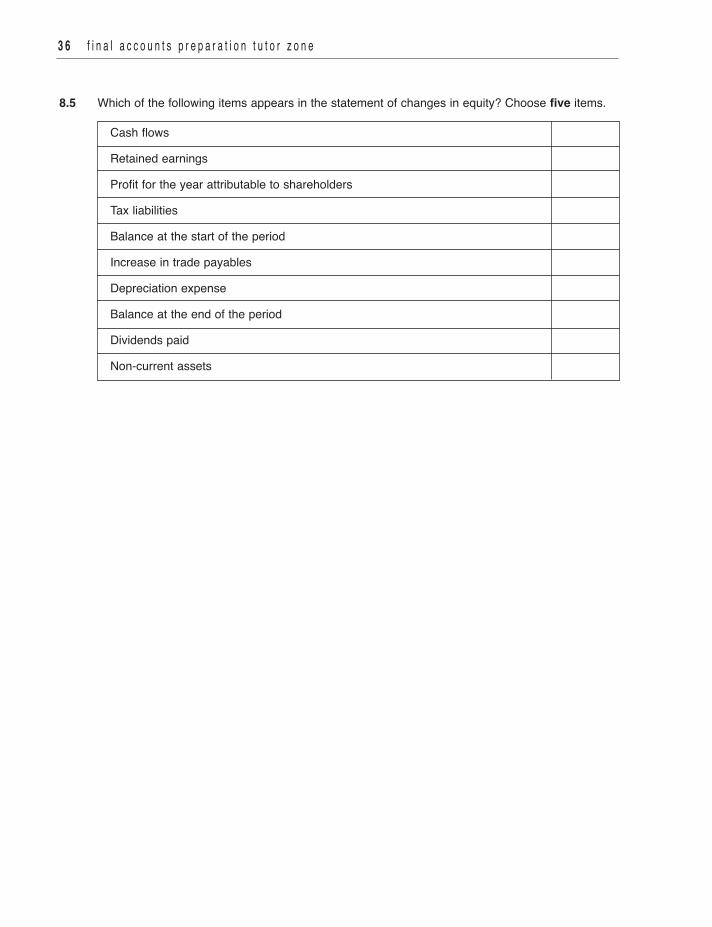

8.5 Which of the following items appears in the statement of changes in equity? Choose five items.

Cash flows

Retained earnings

Profit for the year attributable to shareholders

Tax liabilities

Balance at the start of the period

Increase in trade payables

Depreciation expense

Balance at the end of the period

Dividends paid

Non-current assets