final e bulletin may18 - icmai.inicmai.in/upload/students/e-bulletin/final-ebulletin-may18.pdf ·...

TRANSCRIPT

FOLLOW US ON FOLLOW US ON

THE INSTITUTE OF COST ACCOUNTANTS OF INDIA(Statutory body under an Act of Parliament)

Headquarters: CMA Bhawan, 12, Sudder Street, Kolkata - 700 016Phone: +91-33-2252-1031/34/35/1602/1492/1619/7373/7143

Delhi office: CMA Bhawan, 3, Institutional Area, Lodhi Road, New Delhi - 110 003Phone: +91-11-2462-2156/2157/2158

BulletinBulletinBulletineee

www.icmai.in

VOL: 3, No.: 5, May , 2018 ISSUE

CMA STUDENTS’TOLL FREE 18003450092 / 1800110910TOLL FREE 18003450092 / 1800110910TOLL FREE 18003450092 / 1800110910

Behind every successful business decision, there is always a CMA

FINAL

CMA Manas Kumar ThakurCMA Manas Kumar ThakurCMA Manas Kumar Thakur

Chairman,Training & Education Facilities (T& EF)

MESSAGE FROM THE CHAIRMAN

Committee

Behind every successful business decision, there is always a CMA

Dear Students,

“Education is the kindling of a flame, not the filling of a vessel”.An investment in knowledge pays the best interest and learning is the eye of the mind. Education breeds Confidence, Confidence breeds Hope, Hope breeds Peace. The capacity to learn is a gift, the ability to learn is a skill; the willingness to learn is a choice. Intelligence plus Character is the goal of true education.Every one of you should have an aim and an aimless life is always a miserable life. To lead a successful life your aim should be high, wide target oriented and this in turn will make your life precious to yourself and to others. But whatever your ideal be, it cannot be perfectly realised unless you have realised perfection in yourself. Everything may be achieved by means of discipline and if you are not enough serious and disciplined, you may not be successful as a professional.

June term of examination is approaching and I know, everyone of you are trying hard to become successful in your examination. What I request you; please read your Study Material carefully, follow MTPs, RTPs and E-bulletins and practice to solve the problems meticulously. Work Book for Final students' has also been uploaded. I have come to know that you have enjoyed and benefitted from the Webinar Classes conducted by the Directorate of Studies.

What I suggest; Don't stress do your best. In the examination hall; follow your heart but take the brain with you! Please don't be panic stricken; “Education is learning, what you didn't even know you didn't know”

The Directorate of Studies is sincerely putting their effort to help you for coming out as a true professional and a torch bearer of the nation. Your duty is to grab the available resources, to derive the benefits given and to make you a successful professional. Academicians of repute are contributing in this bulletin despite their busy schedule; if you are having any doubts on any subject you may resolve those issues by mailing them. “Education gives you wings to fly”

“Never stop learning; for when we stop learning we stop growing”

Best of luck for your forthcoming examination,

CMA Manas Kumar Thakur

STUDENTS’ E-bulletin FinalVOL: 3, No.: 5. MAY 2018, ISSUE

i

i

1

2

6

9

12

16

21

24

27

30

32

Knowledge Update -

Message from the Chairman -

Examination Time Table -

Actionate Your Skill Set -

33

34

35

36

Practical Advice -

Submissions -

Message from the Directorate of Studies -

Snapshots -

Group : III Paper 13: Corporate Laws

Group: III Paper 15: Strategic Cost Management - Decision Making (SCMD) -

Group: III Paper 16: Direct Tax Laws and International Taxation (DTI) -

Group: IV Paper 17: Corporate Financial Reporting (CFR) -

Group: IV Paper 18: Indirect Tax Laws & Practice (ITP) -

Group: IV Paper 19: Cost & Management Audit (CMAD) -

Group: IV Paper 20: Strategic Performance Managementand Business Valuation (SPBV) -

Group: III Paper 14: Strategic FinancialManagement (SFM) -

& Compliance (CLC) -

Behind every successful business decision, there is always a CMA

STUDENTS’ E-bulletin FinalVOL: 3, No.: 5. MAY 2018, ISSUE

In this section of e-bulletin we shall have a series of discussion on each of these chapters to provide a meaningful assistance to the students in preparing themselves for the examination at the short end and equip them with suff icient knowledge to deal with real life complications at the long end.

KNOWLEDGEUpdate

Behind every successful business decision, there is always a CMA 1

STUDENTS’ E-bulletin FinalVOL: 3, No.: 5. MAY 2018, ISSUE

Your Preparation Quick TakesYour Preparation Quick TakesYour Preparation Quick Takes

CORPORATE LAWS & COMPLIANCE (CLC)

GROUP: 3 PAPER: 13

Shri Subrata Kr. RoyCompany Secretary

M.S.T.C. Ltd.He can be reached at:

C 20%

A 50%B 30%

Behind every successful business decision, there is always a CMA 2

STUDENTS’ E-bulletin FinalVOL: 3, No.: 5. MAY 2018, ISSUE

Learning Objectives:

Read the Study Material minutely. For details or if you don't understand Study Material or the section is important to identify the

topic, then refer to Bare Act, otherwise reference to Bare Act is not necessary. For Company Law, book by Avtar Singh is recommended. For other laws Institute Study Material is sufficient.

The words used in any of the texts as mentioned above should be understood by immediate reference to the Dictionary.

The main points coming out in any of the provisions should be either underlined or written in separate copy which has to be repeated again and again.

Theoretical knowledge should be adequate and clear before solving practical problems. Don't write wrong English. It changes the meaning and therefore answer may be wrong even

when the student's conception is clear. Also don't make spelling mistakes.

Behind every successful business decision, there is always a CMA

Competition Act.

1.0 Competition Act, 2003

The Monopolies & Restrictive Trade Practices Act, 1969 is the first enactment to deal with competition issues and came into effect on 1st June 1970.

The Government appointed a committee in October 1999 to

examine the existing MRTP Act for shifting the focus of the law from curbing monopolies to promoting competition and to suggest a modern competition law. Pursuant to the recommendations of this committee, the Competition Act, 2002, was enacted on 13th January 2003. It was subsequently amended in 2007.

It provides for different notifications for making different

provisions of the Act effective including repeal of MRTP Act and dissolution of the MRTP Commission.

Under the Act, Competition Commission of India and the Competition Appellate Tribunal have been established.

1.1 Competition Act notification

Certain provisions such as those relating to establishment of the Commission, appointment of Chairperson and Members, appointment of staff, undertaking of competition advocacy have been notified.

Other provisions of the Act are yet to be notified such as those relating to adjudication of anti-competitive practices and regulation of combinations.

1.2 Objectives of the Act The objectives of the Competition Act are to:

prevent anti-competitive practices, promote and sustain competition, protect the interests of the consumers and ensure freedom of trade. competition advocacy by creating awareness among various

levels at Government, industry and consumers. The objectives of the Act are sought to be achieved through the instrumentality of the Competition Commission of India (CCI) which has been established by the Central Government with effect from 14th October, 2003. 1.3 CCI is a body corporate and shall have a full time chairman with minimum 2 and maximum 6 to 7 members. Commission may appoint Secretary and other officers as may be required.

Functions of Competition Commission of India (CCI) i) CCI shall prohibit anti-competitive agreements, which determine

prices, limit or control markets, bid rigging etc.ii) Abuse of dominance, through unfair or discriminatory prices or

conditions, limiting or restricting production or development,

denying market access etc.and regulate combinations (merger or amalgamation or acquisition) which cause or likely cause an appreciable adverse effect or competition through a process of enquiry.

iii) It shall give opinion on competition issues on a reference received from an authority established under any law (statutory authority)/Central Government.

iv) CCI is also mandated to undertake competition advocacy, create public awareness, promote competition, protect interest of consumers and ensure freedom of trade and impart training on competition issues.

v) Inquiry into certain agreements and dominant position by giving notices to the parties.

“Agreement” under the Act An agreement includes any arrangement, understanding or concerted action entered into between parties. It need not be in writing or formal or intended to be enforceable in law.

1.4 Prohibition of certain agreement

A. Anti-competitive agreement shall be presumed to have appreciable adverse effect on competition and thereby deemed to be restrictive.

- An anti-competitive agreement is an agreement having appreciable adverse effect on competition. Anti-competitive agreements include:-

agreement to limit production & supply, storage, distribution agreement to allocate markets agreement to fix price bid rigging (manipulating the bids) or collusive bidding

(bidding with understanding among the bidders) conditional purchase/sale (tie-in arrangement) e x c l u s i v e s u p p l y / d i s t r i b u t i o n a r r a n g e m e n t -

limit/restrict/withhold/allocation of an area resale price maintenance refusal to deal

The whole agreement shall be construed as “void” if it contains anticompetitive clauses. However, agreement for restriction for protection of intellectual property shall not fall under this category. 1.5 Abuse of dominance

Dominance refers to a position of strength which enables a dominant firm to operate independently in India of competitive forces or to affect its competitors or consumers or the market in its favour.

impedes fair competition between firms, exploits consumers and makes it difficult for the other

players to compete with the dominant undertaking on merit. imposing unfair conditions or price, predatory pricing,

limiting production/market, creating barriers to entry and

3

STUDENTS’ E-bulletin FinalVOL: 3, No.: 5. MAY 2018, ISSUE

Behind every successful business decision, there is always a CMA

applying dissimilar conditions to similar transactions.

1.6 Specific instances of dominanace in Competion Act

(a) directly or indirectly, imposes unfair or discriminatory conditions in purchase or sale of goods or services, including predatory price;

(b) limits, restricts production of goods/ provision of services/ technical development

(c) denial of market access(d) uses dominant positioning one market to enter into other

relevant market. 2.0 Who can make a complaint? Any person, consumer, consumer association or trade association can make a complaint against anti-competitive agreements and abuse of dominant position. A person includes an individual, Hindu Undivided Family (HUF), company, firm, association of persons (AOP), body of individuals (BOI), statutory corporation, statutory authority, artificial juridical person, local authority and body incorporated outside India. A consumer is a person who buys for personal use or for other purposes. 3.0 Orders the Commission can pass

During the course of enquiry, the Commission can grant interim relief restraining a party from continuing with anti competitive agreement or abuse of dominant position

To impose a penalty of not more than 10% of turn-over of the enterprises and in case of cartel - 3 times of the amount of profit made out of cartel or 10% of turnover of all the enterprises whichever is higher

After the enquiry, the Commission may direct a delinquent enterprise to discontinue and not to re-enter anti-competitive agreement or abuse the dominant position

To award compensation

To modify agreement

To recommend to the Central Govt. for division of enterprise in case it enjoys dominant position.

�*� Declare an agreement to be void.

*� Violation of orders may result to imprisonment. 4.0 “Combination” under the Act and regulation thereof

Combination includes acquisition of shares, acquisition of control by the enterprise over another and amalgamation between or amongst enterprises. Combination, that exceeds the threshold limits specified in the Act in terms of assets or turnover, which causes or is likely to cause an appreciable adverse effect on competition within the relevant market in India, can be scrutinized by the Commission �

4.1 In case of combination the threshold limits are- For acquisition –

Combined assets of the firms (acquirer and the enterprise) is more than Rs 1500 Cr. or turnover is more than Rs 4500 Cr. (these limits are US$ 750 millions including at least Rs.750 Cr. in India and 2250 millions including at least 2250 million in India in case one of the firms is situated outside India).

The limits are more than Rs 6000 Cr or Rs 18000 Cr and US$ 3 billion including at least Rs.750 Cr. in India and 9 billions including at least Rs.2250 Cr. in India in case acquirer is a group in India or outside India respectively.

CG has exempted enterprise whose control, shares, voting rights or assets are being acquired has assets of value of not more than Rs.250 Cr. and turnover of not more than Rs.750 Cr.

Turnover means amount on sale of product or rendering of services of similar or substitutable goods or services. Group means two or more enterprise which directly or indirectly exercise 26% or more of voting right in other enterprise or appoint more than 50%of the directors or control affairs of the other enterprise.

4.2 For merger/amalgamation –

Assets of the merged/amalgamated entity more than Rs 1500 Cr or turnover more than Rs 4500 Cr (these limits are US$ 750 millions including at least and 2250 millions including at least Rs.2250 Cr. in India in case one of the firms is situated outside India).

The limits are more than Rs 6000 Cr or Rs 18000 Cr and US$ 3 billion and 9 billions in case merged/amalgamated entity belongs to a group in India or outside India respectively

Asset means written down book value and shall include intellectual

property.

A firm proposing to enter into a combination, may, at its option, notify the Commission in the specified form disclosing the details of the proposed combination within 30 days of such proposal i.e. approval of the board of directors or execution of the agreement or other document for acquisition. No combination shall come into effect until 210 days have passed from the day on which the notice has been given to the Commission or Commission has given no objection, whichever is earlier. 5.0 Procedure for investigation of combinations If the Commission is of the opinion that a combination is likely to cause or has caused adverse effect on competition,

It shall issue a notice to show cause the parties as to why investigation in respect of such combination should not be conducted.

On receipt of the response, if Commission is of the prima facie opinion that the combination has or is likely to have appreciable adverse effect on competition, it may direct publication of details inviting objections of public and hear them, if considered appropriate.

It may invite any person, likely to be affected by the combination, to file his objections. The Commission may also enquire whether the disclosure made in the notice is correct and combination is likely to have an adverse effect on competition.

5.1 Orders the Commission can pass in case of combinations

It shall approve the combination if no appreciable adverse effect on competition is found

It shall disapprove of combination in case it forms an opinion of appreciable adverse effect on competition

M a y p r o p o s e s u i t a b l e m o d i fi c a t i o n i n t h e agreement/arrangement.

5.2 Prohibition of abuse of dominance

i) an enterprise shall be considered to be dominant in the referent market in India, if -

(a) operate independently of competitive forces;(b) affects the consumer, competitor or the relevant

4

STUDENTS’ E-bulletin FinalVOL: 3, No.: 5. MAY 2018, ISSUE

Behind every successful business decision, there is always a CMA

market in its favour.ii) abuse of dominant position shall mean using of unfair or discriminatory condition in purchase or sale or price of goods and

services or restricting quality of production, services or scientific development to prejudice customers, denial of market access, supplementary obligations or predatory pricing.

5.3 Regulation of combinations

i) no person shall enter into combination which causes or likely to cause appreciable adverse effect on competition in the relevant market in India;

ii) persons propose to enter into combination shall give notice to the Commission with 30 days of approval of the proposal by the Board or execution of any agreement;

iii) no combination shall be effective before lapse of 210 days of giving notice or getting approval of the Commission, whichever is earlier;

iv) do not apply to bank, FI, FII or venture capital fund. 7 days notice needs to be given to Commission.

5

STUDENTS’ E-bulletin FinalVOL: 3, No.: 5. MAY 2018, ISSUE

Your Preparation Quick TakesYour Preparation Quick TakesYour Preparation Quick Takes

STRATEGIC FINANCIAL MANAGEMENT (SFM)

GROUP: 3 PAPER: 14

Behind every successful business decision, there is always a CMA

Dr. Arindam DasAssociate Professor,

Department of CommerceThe University of Burdwan

He can be reached at:[email protected]

A 25%B 20%

C 25% D 30%

6

STUDENTS’ E-bulletin FinalVOL: 3, No.: 5. MAY 2018, ISSUE

Behind every successful business decision, there is always a CMA

Learning objectives:

After studying this section on Strategic Financial Management, you will be able to: compute fair price of futures contract determine if any arbitrage opportunities exist

Strategic Financial Management

Illustration 1

On 31.08.2017, the value of stock index was Rs. 2,200. The risk free rate of interest is 8% which is continuously compounded. The dividend yield on this stock index is as under:

0.01583 Find out the futures price of contract deliverable on 31.12.2017. Given e = 1.01593

Solution:

The price of futures, when dividend yield is given, is written as:(r-q)t F= S e 0

where F denotes price of the futures contract = ?S is spot price of the underlying stock = 2200o

r is the risk-free rate of interest = 8% = .0.08q = Average dividend yield of four months viz. September to December = (3+3+4+3)/ 4 = 3.25% = 0.0325T denotes time to expiry expressed in year = 4 months or 4/12 or 0.333

(0.08 – 0.0325) 0.333 0.01583 Thus, F= 2200 e = 2200 x e = 2200 x1.01593 = 2235.046

Illustration 2

The following data relates to ABC ltd's share prices:Current price per share: Rs. 180Price per share in the 6 months futures market: Rs. 195It is possible to borrow money in the market for securities transactions at the rate of 12% per annum.

Required:

a) Calculate the theoretical minimum price of a 6-month futures contract.b) Explain if any arbitrage opportunities exist

Solution:

a) Theoretical minimum price of a 6-month futures contract= Spot price + Cost of Carry - Dividend

Month Dividend paid (%)

January 3

February 4

March 3

April 3

May 4

June 3

July 3

August 4

September 3

October 3

November 4

December 3

7

STUDENTS’ E-bulletin FinalVOL: 3, No.: 5. MAY 2018, ISSUE

Behind every successful business decision, there is always a CMA

= 180 + (180 x o.12 x 0.5) – 0= 190.80

Thus we see that futures price by calculation is Rs. 190.80 and is quoting at Rs. 195 in the exchange.a) Since the fair value of futures contract is less than actual futures price, the futures contract is overvalued. Hence one can sell the

contract and do arbitrage by buying stock in cash market.Step IBuy ABC Ltd. stock at Rs. 180 by borrowing at 12% for 6 months. Therefore, the outflow will be:Cost of stock� � � � � � � Rs. 180.00Add: Interest@12%for 6 months (i.e., 180 x 0.12 x 0.5)� Rs. 10.80Total outflows (A)� � � � � � Rs. 190.80Step IISell 6-month futures contract at Rs. 195. Hence the inflows will be:Sale proceeds of futures contract� � � � Rs. 195.00Add: Dividend received � � � � � � 00Total inflows (B)� � � � � � Rs. 195.00Profit earned by arbitrageur = Inflows – Outflows = 195 – 190.80 = Rs. 4.20 per share.Note: Transactions costs like commission, margin etc. have been ignored.

Illustration 3

Calculate the theoretical price of 3-month ACC futures, if ACC (FV Rs. 10) quotes Rs 520 on NSE, and the 3-month futures price quotes at Rs. 532, and the borrowing rate is given as 15% and the expected dividend is 25% payable before expiry. Is there any arbitrage opportunities? If the market price of futures is Rs. 542, do arbitrage opportunities still exist?

Solution:

Theoretical price of a 3-month futures contract= Spot price + Cost of Carry - Dividend = 520 + (520 x 0.15 x 0.25) – (25% of FV Rs.10)= 537

Actual futures price: Rs. 532Since the fair value of futures contract is more than actual futures price, the futures contract is undervalued in the market. Hence arbitrageur would buy the futures contract and sell stock in cash market.

No dividend is received as stock was sold. Margins, commissions and all transactions costs are ignored.Actual futures price: Rs. 542Since the fair value of futures contract is less than actual futures price, the futures contract is overvalued in the market. Hence arbitrageur would sell the futures contract and buy stock in cash market.

Margins, commissions and all transactions costs are ignored.

Arbitrageurs make profit in either situation. The things are not so rosy in practical life. In practice, however, transactions costs like margin funding, commissions, brokerage, securities transaction tax etc. kill the arbitrage opportunities.

Activity today Rs. Activity at expiry Rs. Net

Buy futures 532 Sell futures FT F -532T

Sell stock 520 Buy stock ST 520 - ST

Deposit sale proceeds Received 19.50(=520 x 0.15x 0.25)

19.50

Net gain at expiry = F -532 + 520 - S + 19.50; since F would converge with S , at expiry, T T T T

they would cancel out7.50

Activity today Rs. Activity at expiry Rs. Net

Sell futures 532 Buy futures FT 542 -FT

Buy stock 520 Sell stock ST S - 520T

Dividend received On or before expiry 2.50 2.50

Paid 19.50 -19.50

Net gain at expiry = 542 -F + S – 520 + 2.50 - 19.50; since F would converge with S , at T T T T

expiry, they would cancel out5.00

Fund stock purchase

8

STUDENTS’ E-bulletin FinalVOL: 3, No.: 5. MAY 2018, ISSUE

Your Preparation Quick TakesYour Preparation Quick TakesYour Preparation Quick Takes

STRATEGIC COST MANAGEMENT - DECISION

(SCMD)MAKING

GROUP: 3 PAPER: 15

Behind every successful business decision, there is always a CMA

CMA (Dr.) Sreehari ChavaCost & Management Consultant,

Nagpur, Maharastra,He can be reached at:

B 50%

C 30%A 20%

A Cost Management 20%B Strategic Cost Management Tools and Techniques 50%C Strategic Cost Management - Application of Statistical Techniques in Business Decisions 30%

9

STUDENTS’ E-bulletin FinalVOL: 3, No.: 5. MAY 2018, ISSUE

Behind every successful business decision, there is always a CMA

Learning Objectives:

The Strategic cost management framework provides a clear plan of attack for addressing costs and decisions that affect them. It helps to get answers on: Is there a plan for strategic cost management? Have the controlling functions for each significant cost in the organization been

identified? Are there resources devoted to finding or obtaining new approaches to breaking cost

barriers? Is cost modelling being used or is there an active effort to develop or buy cost

modelling capability?

An Introduction to Linear Programming

01.00 Linear programming (LP)Linear programming (LP), also called linear optimization) is a method to achieve the best outcome - such as maximum profit or lowest cost - in a mathematical model whose requirements are represented by linear relationships. More formally, linear programming is a technique for the optimization of a linear objective function, subject to linear equality and linear inequality constraints.

It is “a technique for specifying how to use limited resources or capacities of a business to obtain a particular objective, such as least cost, highest margin or least time, when those resources have alternate uses”. The situation which require a search for “best” values of the variables, subject to certain constraints, are amenable to programming analysis. These situations cannot be handled by the usual tools of calculus or marginal analysis.

A linear programming problem has two basic parts. The first part is the objective function, which describes the primary purpose of the formulation – to maximize some return (for example, profit) or to minimize some cost (for example, production cost or investment cost). The second part is the constraint set. It is the system of equalities and/or inequalities, which describes the restrictions (conditions or constraints) under which optimization is to be accomplished.

02.00 An Example

Consider a chocolate manufacturing company which produces only two types of chocolates – A and B. Both the chocolates require Milk and Choco only. To manufacture each unit of A and B, following quantities are required:

Each unit of A requires 1 unit of Milk and 3 units of Choco Each unit of B requires 1 unit of Milk and 2 units of Choco

The company's kitchen has a total of 5 units of Milk and 12 units of Choco. On each sale, the company makes a profit of

Rs 6 per unit of A Rs 5 per unit of B

How many units of A and B should the company produce to maximize its profit?

SolutionThe first step is to represent the problem in a tabular form for better understanding.

The second step is formulating the problem as a mathematical model. Let the total number of units produced of A be = X; the total number of units produced of B be = Y; and the total profit be represented by Z

The company has to produce as many units of A and B to maximize the profit. The total profit is derived by the total number of units of A and B produced multiplied by their per unit profit of Rs 6 and Rs 5 respectively. Thus, the objective formulation may be stated as:

Max Z = 6X+5Y

But the resources of Milk and Choco are available in limited quantity. As per the above table, each unit of A and B requires 1 unit of Milk. The total amount of Milk available is 5 units. This constraint may be formulated mathematically as:

X+Y ≤ 5

Also, each unit of A and B requires 3 units & 2 units of Choco respectively. The total amount of Choco available is 12 units. This constraint may be formulated mathematically as:

3X+2Y ≤ 12

Further, the values for units of A can only be integers. So we have two more constraints, i.e. X ≥ 0 & Y ≥ 0.

For the company to make maximum profit, the above inequalities have to be satisfied. Hence the final mathematical formulation would be put as:

Max Z = 6X+5Y

Subject to

X+Y ≤ 5

3X+2Y ≤ 12

Where X ≥ 0 & Y ≥ 0.

03.00 Common Terminologies Decision Variables: Decision variables are the variables which will decide the output. They represent the ultimate solution. To solve any problem, we first need to identify the decision variables. For the above example, the total number of units for A and B denoted by X & Y respectively are the decision variables.

Objective Function: Objective Function is defined as the objective of making decisions. In the above example, the company wishes to maximise the total profit represented by Z. So, profit is the objective function.

Constraints: The constraints are the restrictions or limitations on the decision variables. They usually limit the value of the decision variables. In the above example, the limit on the availability of resources, i.e. Milk and Choco are theconstraints.

Non-negativity: For all linear programs, the decision variables should always take non-negative values. Which means the values for decision variables should be greater than or equal to zero.

04.00 The Process of Formulation1. Identify the decision variables2. Write the objective function3. Mention the constraints4. Explicitly state the non-negativity restriction

For a problem to be a linear programming problem, the decision variables, objective function and constraints all have to be linear

Product Milk Choco Profit per unit

A 1 3 Rs 6

B 1 2 Rs 5

Total 5 12

10

STUDENTS’ E-bulletin FinalVOL: 3, No.: 5. MAY 2018, ISSUE

Behind every successful business decision, there is always a CMA

functions. If the all the three conditions are satisfied, it is called a .Linear Programming Problem

05.00 Applications of Linear ProgrammingIn practice linear programming has proved to be one of the most widely used technique of managerial decision making in business, industry and numerous other fields. Linear programming and Optimization are used in various industries. Manufacturing and service industry uses linear programming on a regular basis.

Manufacturing industries use linear programming for . Their motive is to analyzing their supply chain operationsmaximize efficiency with minimum operation cost. As per the recommendations from the linear programming model, the manufacturer can reconfigure their storage layout, adjust their workforce and reduce the bottlenecks.

Linear programming is a used in organized retail for . Since the number of products in the market shelf space optimizationhave increased in leaps and bounds, it is important to understand what does the customer want. Optimization is aggressively used in stores like Walmart, Hypercity, Reliance, Big Bazaar, etc. The products in the store are placed strategically keeping in mind the customer shopping pattern. The objective is to make it easy for a customer to locate & select the right products. This is subject to constraints like limited shelf space, the variety of products, etc.

Optimization is used for . This is an extension of the popular traveling salesman problem. Service optimizing Delivery Routesindustry uses optimization for finding the best route for multiple salesmen traveling to multiple cities. With the help of clustering and greedy algorithm the delivery routes are decided by companies like FedEx, Amazon, etc. The objective is to minimize the operation cost and time.

Optimization is used in . Supervised Learning works on the fundamental of linear programming. A system is Machine Learningtrained to fit on a mathematical model of a function from the labeled input data that can predict values from an unknown test data.

6.00 Quick Take

The applications of Linear programming can be extended to many many real-world like situations by multiple stakeholders such as Entrepreneurs, Managers, Scientists, Shareholders, Sports, Stock Markets, etc. And, the exploration continues…

11

STUDENTS’ E-bulletin FinalVOL: 3, No.: 5. MAY 2018, ISSUE

Your Preparation Quick TakesYour Preparation Quick TakesYour Preparation Quick Takes

DIRECT TAX LAWS AND INTERNATIONAL

(DTI)TAXATION

GROUP: 3 PAPER: 16

Behind every successful business decision, there is always a CMA

CA Vikash Mundhra He can be reached at:

A 50%C 20%

B 30%

12

STUDENTS’ E-bulletin FinalVOL: 3, No.: 5. MAY 2018, ISSUE

Behind every successful business decision, there is always a CMA

Learning Objectives:

To develop basic idea about the problem of International double taxation

To get acquainted with the methods of reliefs To have acquaintance with the basic provisions of the provisions of

the Indian Income-tax Act regarding reliefs for double taxation.

Tax on Dividend

Sec. 10(34) provides that any income by way of dividend referred to in sec. 115-O (stated below) shall be exempted. Accordingly, dividend from a domestic company, except dividend u/s 2(22)(e), shall be exempted in hands of the recipient.

Tax on distributed profits by a Domestic Company [Sec. 115-O]

A domestic company for any amount declared as dividends [other than dividend specified u/s 2(22)(e)] shall be charged to additional income tax @ 15% + surcharge + education cess & SHEC.

Taxpoint

a) Dividend may be interim or otherwise and distributed out of current or accumulated profits.

b) Such tax shall be in addition to income tax for which no deduction is available.

c) Dividend distribution tax is applicable even if the company has declared dividend out of its exempted income.

d) A shareholder does not get any credit of tax for the tax paid by the company.

Exception: Corporate dividend tax is not required to be paid on:i. The amount of dividend, if any, received by the domestic company during the financial year, from its subsidiary company and such:

Taxpoint: A company shall be a subsidiary of another company, if such other company, holds more than half in nominal value of the equity

share capital of the company. The same amount of dividend shall not be taken into account for reduction more than once.

i. The amount of dividend, if any, paid to the New Pension System Trust referred to sec. 10(44).ii. Any dividend paid by the specified domestic company to a business trust out of its current income on or after the specified date.

Specified domestic company means a domestic company in which a business trust has become the holder of whole of the nominal value of equity share capital of the company (excluding the equity share capital required to be held mandatorily by any other person in accordance with any law for the time being in force or any directions of Government or any regulatory authority, or equity share capital held by any Government or Government body);

Specified Date means the date of acquisition by the business trust of such holding as is referred above.

iii. Dividend paid by a company, being a unit of an International Financial Services Centre deriving income solely in convertible foreign exchange, out of its current income.

Case Tax Treatment

Dividend from a domestic companies -

a) Dividend excluding dividend u/s 2(22)(e)

- Where aggregate divided exceeds � 10 lakh in the total income of the resident specified assessee

"Specified assessee" means a person other than:

i. a domestic company; or

ii. a fund or institution or trust or any university or other educational institution or any hospital or other medical institution referred to in sec. 10(23C)(iv) or (v) or (vi) or (via); or

a trust or institution registered u/s 12A or 12AA.

Taxable in the hands of recipient @ 10% [Sec. 115BBDA]

- In any other case Exempted u/s 10(34)

b) Deemed dividend u/s 2(22)(e) Taxable

Dividend from a non-domestic company Taxable in the hands of recipient

Dividend from a co-operative society Taxable in the hands of recipient

Subsidiary Company is Condition

a domestic company Subsidiary company has paid the tax which is payable u/s 115-O on such dividend

a foreign company The tax is payable by the domestic company u/s 115BBD on such dividend

13

STUDENTS’ E-bulletin FinalVOL: 3, No.: 5. MAY 2018, ISSUE

Behind every successful business decision, there is always a CMA

Tax on such dividend is neither paid by the company nor by the person receiving such dividend

Tax Rates

Tax on distributed profit shall be computed after grossing up the tax by using following formula:

Rate of Dividend Distribution Tax before surcharge and cess = Amount Distributed x 15% = 17.647%

� � � � � 85%

Surcharge + Cess is also applicable on aforesaid calculated rate.

Other Procedure

The principal officer of the domestic company and the company shall be liable to pay such tax to the credit of the Central Government within 14 days from the date of:

(a) declaration of any dividend; or

(b) distribution of any dividend; or

(c) payment of any dividend,

- whichever is earlier.

Where the principal officer and the company fails to pay the whole or any part of the tax on distributed profits within the time allowed, he or it shall be liable to pay simple interest at the rate of 1% for every month or part thereof on the amount of such tax for the period beginning on the date immediately after the last date on which such tax was payable and ending with the date on which the tax is actually paid [Sec. 115P]

Deemed to be in default [Sec. 115Q]: If any principal officer of a domestic company and the company does not pay tax on distributed profits, then, he or it shall be deemed to be an assessee in default.

Penalty [Sec. 271C]: If any person fails to pay (the whole or any part of the above tax), then such person shall be liable to pay, by way of penalty, a sum equal to the amount of tax which such person failed to pay.

Prosecution [Sec. 276B]: If a person fails to pay to the credit of the Central Government the tax payable by him, he shall be punishable with rigorous imprisonment for a term which shall not be less than 3 months but which may extend to 7 years and with fine.

Illustration H Ltd. has received dividend of � 5,00,000 from its subsidiary company S Ltd. Further H Ltd. declares dividend of � 12,00,000 to its shareholders; dividend distribution tax will be paid as under:

Tax on Distributed Income to Shareholders [Sec. 115QA]Section 115-O provides for levy of Dividend Distribution Tax (DDT) on the company at the time when company distributes, declares or pays any dividend to its shareholders. Consequent to the levy of DDT the amount of dividend received by the shareholders is not included in the total income of the shareholder (subject to sec. 115BBDA).

The consideration received by a shareholder on buy-back of shares by the company is not treated as dividend but is taxable as capital gains u/s 46A.

A company, having distributable reserves, has two options to distribute the same to its shareholders either by declaration and payment of dividends to the shareholders, or by way of purchase of its own shares (i.e. buy back of shares) at a consideration fixed by it. In the first case, the payment by company is subject to DDT and income in the hands of shareholders is exempt. In the second case the income is taxed in the hands of shareholder as capital gains.

Unlisted Companies, as part of tax avoidance scheme, are resorting to buy back of shares instead of payment of dividends in order to avoid payment of tax by way of DDT particularly where the capital gains arising to the shareholders are either not chargeable to tax or are taxable at a lower rate.

In order to curb such practice following provisions are made:

(1) The asseessee is a Domestic company

(2) Its shares are not listed on any recognised stock exchange.

(3) The assessee-company has distributed income on buy back of its own shares from its shareholders

“Buy-back” means purchase by a company of its own shares in accordance with the provisions of any law for the time being in force relating to companies

“Distributed income” means the consideration paid by the company on buy-back of shares as reduced by the amount, which was

Particulars S Ltd. H Ltd.

Dividend Paid 5,00,000 12,00,000

Less: Dividend received from subsidiary company Nil 5,00,000

Balance 5,00,000 7,00,000

Tax u/s 115-O [(((Balance Amount x 15 / 85) 112%) x 103%)] 1,01,788 1,42,504

14

STUDENTS’ E-bulletin FinalVOL: 3, No.: 5. MAY 2018, ISSUE

Behind every successful business decision, there is always a CMA

received by the company for issue of such shares, determined in the manner as may be prescribed.

(4) Such company shall be liable to pay additional income-tax @ 20% (+ surcharge + cess) on the distributed income. Such tax is irrespective of the fact that the company is not liable for paying income tax on its income.

(5) The principal officer of the domestic company and the company shall be liable to pay the tax to the credit of the Central Government within 14 days from the date of payment of any consideration to the shareholder on buy-back of shares.

(6) The tax on the distributed income by the company shall be treated as the final payment of tax in respect of the said income and no further credit therefor shall be claimed by the company or by any other person in respect of the amount of tax so paid.

(7) No deduction under any other provision of this Act shall be allowed to the company or a shareholder in respect of the income which has been charged to tax under this section or the tax thereon.

Interest Payable for Non-payment of Tax by Company [Sec. 115QB] Where the principal officer of the domestic company and the company fails to pay the tax on the aforesaid distributed income within 14 days, he or it shall be liable to pay simple interest @ 1% for every month or part thereof on the amount of such tax for the period beginning on the date immediately after the last date on which such tax was payable and ending with the date on which the tax is actually paid.

When Company is Deemed to be Assessee in Default [Sec. 115QC]

If any principal officer of a domestic company and the company does not pay tax on distributed income in accordance with the provisions of section 115QA, then, he or it shall be deemed to be an assessee in default in respect of the amount of tax payable by him or it and all the provisions of this Act for the collection and recovery of income-tax shall apply.

Tax on distributed income to unit holders [Sec. 115R]

Any amount of income distributed by the specified company or a Mutual Fund to its unit holders shall be chargeable to tax and such specified company or Mutual Fund shall be liable to pay additional income-tax on such distributed income at the rate of:(i) 5% on income is distributed by a mutual fund under an infrastructure debt fund scheme to a non-resident (not being a company)

or a foreign company (ii) 25% on income distributed to any person being an individual or a Hindu undivided family;(iii) 30% on income distributed to any other person

Tax on distributed profit shall be computed after grossing up the tax

However, the above provision shall not apply in respect of any income distributed:

a) by the Administrator of the specified undertaking (i.e., Unit Scheme, 1964) to the unit holders; or

b) to a unit holder of equity oriented funds in respect of any distribution made from such funds.

The person responsible for making payment of the income distributed by the Unit Trust of India or a Mutual Fund and the Unit Trust of India or the Mutual Fund, as the case may be, shall be liable to pay tax to the credit of the Central Government within 14 days from the date of distribution or payment of such income, whichever is earlier.

No deduction under any other provision of this Act shall be allowed to the Unit Trust of India or to a Mutual Fund in respect of the income, which has been charged to tax u/s 115R(2).

Redemption or repurchase of units or allotment of additional units by way of bonus units would not be subject to levy of additional income tax u/s 115R [Circular 6/2014 dated 11-02-2014]

Interest payable for non-payment of tax [Sec. 115S]

Where the person responsible for making payment of the income distributed by the specified company or a Mutual Fund and the specified company or the Mutual Fund, as the case may be, fails to pay the whole or any part of the tax within the time allowed, he or it shall be liable to pay simple interest at the rate of 1% every month or part thereof on the amount of such tax for the period beginning on the date immediately after the last date on which such tax was payable and ending with the date on which the tax is actually paid.

Unit Trust of India or Mutual Fund to be assessee in default [Sec. 115T]

If any person responsible for making payment of the income distributed by the specified company or a Mutual Fund and the specified company or the Mutual Fund, as the case may be, does not pay such tax, then, he or it shall be deemed to be an assessee in default.

15

STUDENTS’ E-bulletin FinalVOL: 3, No.: 5. MAY 2018, ISSUE

Your Preparation Quick TakesYour Preparation Quick TakesYour Preparation Quick Takes

DIRECT TAX LAWS AND INTERNATIONAL

(DTI)TAXATION

GROUP: 4 PAPER: 17

Behind every successful business decision, there is always a CMA

A 30%E 15%

D 15%

C 20% B 20%

A GAAP and Accounting Standards 30%B Accounting if Business Comminations & Restructuring 20%C Consolidated Financial Statements 20%D Developments in Financial Reporting 15%E Government Accounting in India 15%

Shri Sumit Kumar MajiAssistant Professor,

Department of Commerce,The University of Burdwan,

He can be reached at:[email protected]

16

STUDENTS’ E-bulletin FinalVOL: 3, No.: 5. MAY 2018, ISSUE

Behind every successful business decision, there is always a CMA

Learning Objectives:

After studying the present section of Corporate Financial Reporting you will be able to: Understand the concept of intangible assets as per AS 26. Learn the initial and subsequent recognition criteria for intangible assets as

per AS 26. Grasp the method for charging amortization.

Intangible Assets

An asset is a resource within the control of an enterprise (as a result of any past event) from which future economic benefits are expected to flow to that enterprise. Intangible asset can be defined as the identifiable nonmonetary asset which does not have any physical substance. The essential features of an Intangible Assets are:

No Physical Substance: One of the most important features of an intangible asset is that it does not have any physical substance or even if it has, the cost of the physical substance must be very negligible as compared to the total value of the intangible asset. Following this logic the software contained in a compact disc or pen drive is considered as intangible asset. Let us assume that the cost of the software is Rs. 100000 which is contained in a CD. The value of CD is Rs. 8. Thus the CD value is negligible as a proportion of the total value of the software. Thus even if the software has physical substance it would be assumed that it does not have any physical substance.

Nonmonetary: The asset should be nonmonetary in nature i.e. the value of the asset is not fixed by the contractual commitments. Example of monetary assets are debtors, bills receivables etc. In respect of these assets the amount to be received is fixed by the contractual obligation whereas the value of nonmonetary assets such as plant, property and equipment is not determined by any kind of contractual commitments. The value of intangible assets also is not determined by any kind of fixed contractual obligation.

Identifiable: The intangible assets should be separately identifiable or in other words it should be separate from the value of goodwill arising out of synergistic effect business combination. If the purchase consideration exceeds the value of net assets taken over in case of a business combination, goodwill arises. The intangible assets must be separate from this goodwill. For example the purchase consideration is Rs. 500000 and the value of net assets (including patent of Rs. 50000) taken over is Rs. 200000 then the value of goodwill is Rs. 300000 (500000-150000-50000). Under this situation the patent of Rs. 50000 is to be recorded as the identifiable intangible asset which is separate from the tangible trading assets worth Rs. 150000.

Future Economic Benefit: Future economic benefit must flow to the enterprise as a result of the productive use of such intangible asset either through cost savings or by generating revenue. For example a license to use a new production system may result in the reduction of cost or by using a patented formula; a pharmaceutical company may be able to generate revenue by selling the medicines. Thus both the license and the patented formula are intangible assets.

Control: An intangible asset is said to be within the control if it has the legal right to enjoy the future economic benefits arising out of the use of the asset and it can restrict any other enterprise to enjoy such benefits. To put it in a different way, if the enterprise can sell, rent, give the intangible on lease, allow other enterprises to use the asset then it is within the control of the enterprise. Following this logic customer list or employees are not recorded as intangible asset as the enterprise do not have adequate control over the employees or the customers. Cost Measurement: To recognise an intangible asset in the books of account the cost of the intangible asset should be capable of being reliably measured. If the cost cannot be reliably measured, it cannot be recorded in the books of account. Following this principle the internally generated intangibles are not recorded in the books of account. For example brand such as Samsung has been created for years and different factors such as product quality, post-sale services, appropriate marketing strategy etc are responsible for the creation of the brand. However cost of these factors cannot be reliably measured thus the internally generated brands are not recorded as intangible asset in the books of accounts.

Recognition Criteria

17

STUDENTS’ E-bulletin FinalVOL: 3, No.: 5. MAY 2018, ISSUE

Behind every successful business decision, there is always a CMA

Let us consider the following illustration for better understanding:

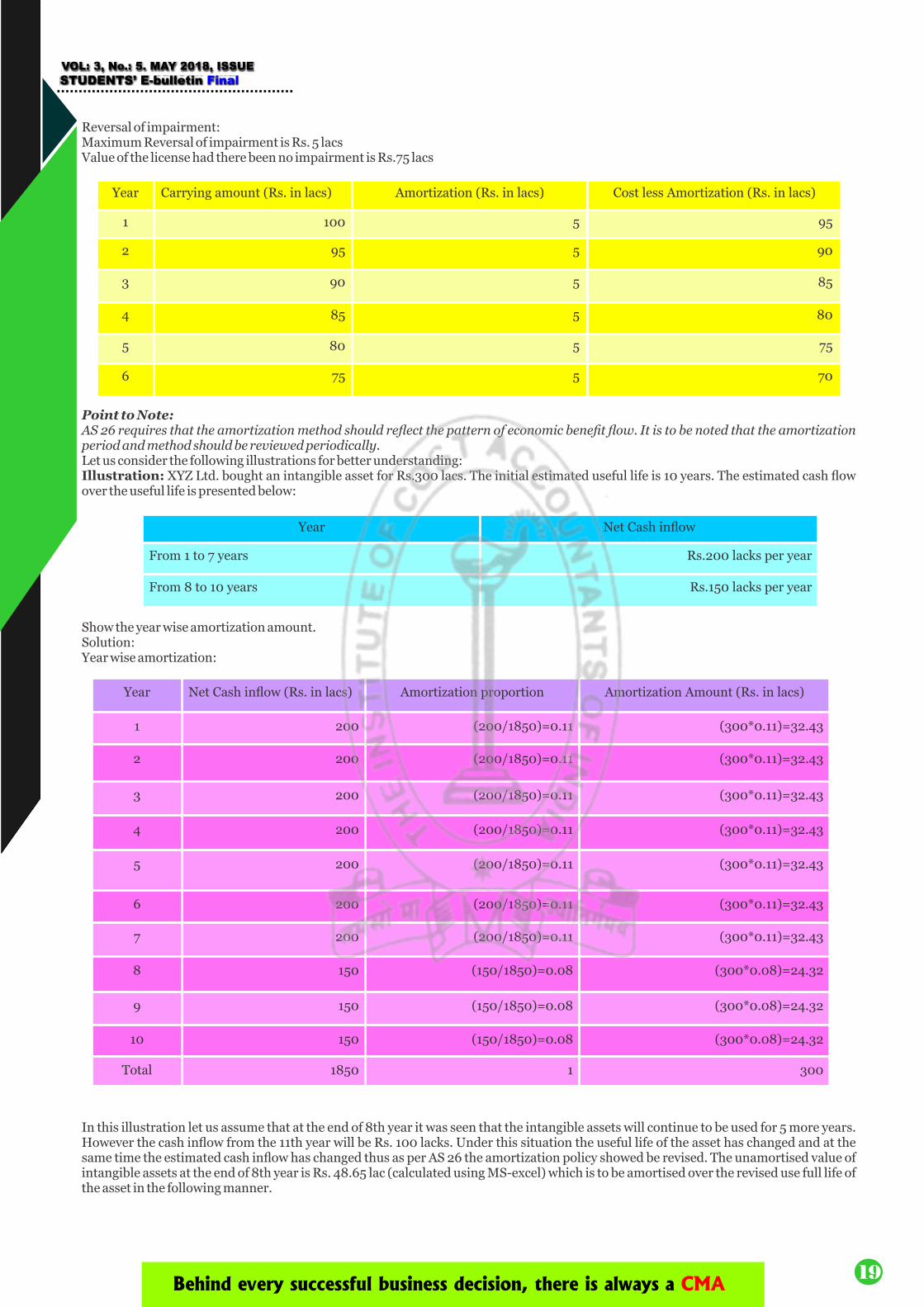

Illustration: ABC Ltd purchased a license for Rs. 100 lacs for an agreed period of 20 years. The amortization should be made using straight line basis. Company does not follow the practice of showing the asset at revalued amount.The Recoverable Amount of the license for the end of first 4 years is given below:

Show the accounting for intangible for the useful life of the asset.Solution: Statement showing the accounting for the license

Year end Recoverable Amount (Rs. in lacs)

1 97

2 91

3 80

4 70

5 80

Year Carrying Amount(Rs. in lacs)

Amortization(Rs. in lacs)

Cost less Amortization

(Rs. in lacs)

Recoverable Amount

(Rs. in lacs)

Impairment loss(Rs. in lacs)

Reversal of Impairment loss

(Rs. in lacs)

1 100 5 95 97 - -

2 95 5 90 91 - -

3 90 5 85 80 5 -

4 80 4.71 75.29 70 5.29 -

5 70 4.375 65.62 80 - 5

6 75 5 70 NA - -

7 70 5 62.4 NA - -

8 65 5 60 NA - -

9 60 5 55 NA - -

10 55 5 50 NA - -

11 50 5 45 NA - -

12 45 5 40 NA - -

13 40 5 35 NA - -

14 35 5 30 NA - -

15 30 5 25 NA - -

16 25 5 20 NA - -

17 20 5 15 NA - -

18 15 5 10 NA - -

19 10 5 5 NA - -

20 5 5 0 NA - -

18

STUDENTS’ E-bulletin FinalVOL: 3, No.: 5. MAY 2018, ISSUE

Behind every successful business decision, there is always a CMA

Reversal of impairment:Maximum Reversal of impairment is Rs. 5 lacsValue of the license had there been no impairment is Rs.75 lacs

Point to Note:AS 26 requires that the amortization method should reflect the pattern of economic benefit flow. It is to be noted that the amortization period and method should be reviewed periodically.Let us consider the following illustrations for better understanding:Illustration: XYZ Ltd. bought an intangible asset for Rs.300 lacs. The initial estimated useful life is 10 years. The estimated cash flow over the useful life is presented below:

Show the year wise amortization amount.Solution:Year wise amortization:

In this illustration let us assume that at the end of 8th year it was seen that the intangible assets will continue to be used for 5 more years. However the cash inflow from the 11th year will be Rs. 100 lacks. Under this situation the useful life of the asset has changed and at the same time the estimated cash inflow has changed thus as per AS 26 the amortization policy showed be revised. The unamortised value of intangible assets at the end of 8th year is Rs. 48.65 lac (calculated using MS-excel) which is to be amortised over the revised use full life of the asset in the following manner.

Year Carrying amount (Rs. in lacs) Amortization (Rs. in lacs) Cost less Amortization (Rs. in lacs)

1 100 5 95

2 95 5 90

3 90 5 85

4 85 5 80

5 80 5 75

6 75 5 70

Year Net Cash inflow

From 1 to 7 years Rs.200 lacks per year

From 8 to 10 years Rs.150 lacks per year

Year Net Cash inflow (Rs. in lacs) Amortization proportion Amortization Amount (Rs. in lacs)

1 200 (200/1850)=0.11 (300*0.11)=32.43

2 200 (200/1850)=0.11 (300*0.11)=32.43

3 200 (200/1850)=0.11 (300*0.11)=32.43

4 200 (200/1850)=0.11 (300*0.11)=32.43

5 200 (200/1850)=0.11 (300*0.11)=32.43

6 200 (200/1850)=0.11 (300*0.11)=32.43

7 200 (200/1850)=0.11 (300*0.11)=32.43

8 150 (150/1850)=0.08 (300*0.08)=24.32

9 150 (150/1850)=0.08 (300*0.08)=24.32

10 150 (150/1850)=0.08 (300*0.08)=24.32

Total 1850 1 300

19

STUDENTS’ E-bulletin FinalVOL: 3, No.: 5. MAY 2018, ISSUE

Behind every successful business decision, there is always a CMA

Year Net Cash inflow (Rs. in lacs) Amortization proportion Amortization Amount (Rs. in lacs)

9 150 (150/600)=0.25 (48.65*0.25)=12.16

10 150 (150/600)= 0.25 (48.65*0.25)= 12.16

11 100 (100/600)= 0.17 (48.65*0.17)= 8.11

12 100 (100/600)=0.17 (48.65*0 .17)= 8.11

13 100 (100/600)=0.16 (48.65*0 .16)= 8.11

Total 600 1 48.65

20

STUDENTS’ E-bulletin FinalVOL: 3, No.: 5. MAY 2018, ISSUE

Your Preparation Quick TakesYour Preparation Quick TakesYour Preparation Quick Takes

INDIRECT TAX LAWS & PRACTICE (ITP)

GROUP: 4 PAPER: 18

Behind every successful business decision, there is always a CMA

A Advanced Indirect Tax - Laws & Practice 80%B Tax Practice and Procedures 20%

B 20%

A 80%

Shri Abhik Kr. MukherjeeAssistant Professor,

Dep. of Business AdmisitrationThe University of Burdwan

He can be reached at:[email protected]

21

STUDENTS’ E-bulletin FinalVOL: 3, No.: 5. MAY 2018, ISSUE

Behind every successful business decision, there is always a CMA

Learning objectives:

After studying this section, you will having an understanding of:

Concept of cancellation of GST Registration; Who can initiate cancellation of GST registration; Approaches for cancellation of GST registration; Who can cancel GST Registration; Circumstances under which GST registration has to be cancelled; Forms used for cancellation of GST registration; Procedure adopted for the cancellation of GST registration; Impact of cancellation of GST registration; Revocation of cancellation of GST registration and the procedure involved.

CANCELLATION OF REGISTRATION UNDER GOODS AND SERVICES TAX

LAW

Introduction Registration happens to be a very important procedure under the GST laws. Most persons or entities who supply goods and/or services in India have a GST registration. After obtaining GST registration, sometimes a GST registration may need to be cancelled. It is known that the registration certificate once granted is permanent unless surrendered, cancelled or revoked.

Concept of Cancellation under GST lawCancellation, in the context of GST registration, simply means that the tax payer will not remain a registered person under the GST law. This cancellation of registration happens to be a procedural exercise in the context of GST registration. The provisions regarding cancellation of registration are provided under Sec. 29 of the Central Goods and Services Tax Act, 2017.

NB: It is to be noted that the cancellation of registration under the State Goods and Services Tax (SGST) Act or the Union Territory Goods and Services Tax (UTGST) Act shall be deemed to be a cancellation of registration under the Central Goods and Services Tax Act.

Who can initiate the cancellation of registration under GST law

As per the provisions laid out u/s 29 of the CGST Act, 2017, any one of the following three entities can initiate the cancellation of registration under GST: The proper officer (Superintendent of Central Tax); The registered person; or Any legal heir of the registered person (in the event of death

of such registered person).

Approaches for cancellation of registration

The GST statute clearly specifies two ways or approaches for cancellation of registration: Suo moto cancellation: The proper officer of GST can on his

own motion cancel the registration; or On the basis of application filed: Cancellation for registration

can also be done on the basis of application filed either by the registered person, or by any legal heir of a registered person.

Thus, the GST Registration cancellation can either be initiated by the department on their own motion or the registered person can apply for cancellation of their GST registration.

Who can cancel GST registration It is only the proper officer of GST who can cancel the registration in such manner and within such period as may be prescribed. However, it is to be noted that the proper officer shall not cancel the registration without giving the person an opportunity of being heard.

Circumstances under which GST registration has to be cancelled

The registration granted under GST can be cancelled for specified reasons. The GST registration can be cancelled for the following reasons:

the business has been discontinued, transferred fully for any reason including death of the proprietor, amalgamated with other legal entity, demerged or otherwise disposed of;

there is any change in the constitution of the business; the taxable person (other than the person who has vol-

untarily taken registration u/s 25(3) of the CGST Act, 2017) is no longer liable to be registered;

a registered person has contravened prescribed provisions of the Act or the rules made thereunder;

a person paying tax under Composition levy scheme has not furnished returns for three consecutive tax periods;

any registered person (other than a person paying tax under Composition levy scheme) has not furnished returns for a continuous period of six months;

any person who has taken voluntary registration under Sec. 25(3) of the CGST Act, 2017 has not commenced business within six months from the date of registration;

registration has been obtained by means of fraud, willful misstatement or suppression of facts

Forms used for cancellation of GST registration

The procedure of cancellation of registration involves the use of different types of forms. These forms are briefly discussed hereunder:

GST REG 16: This form is applicable only when the taxpayer itself applies for the cancellation of registration. Thus, it is basically an application form.

GST REG 17: This form is required to be used when the cancellation of registration is initiated by the authorized officer. By issuing the GST REG 17 form to the taxpayer the proper officer can ask to show cause as why the registration should not be cancelled. Thus, this form is used for issuance of show cause notice.

GST REG 18: The reply to the show cause notice is to be made by furnishing GST REG 18 form under the specified time period. The taxpayer or the concerned party must reply to the notice within 7 working days of issuance of the notice giving the explanation of safeguarding the cancellation of registration. Thus, this form is basically the reply to the show cause notice.

GST REG 19: The GST REG 19 form is for the usage of GST officer for issuing a formal order for the cancellation of GST registration. The order for sending the notice must be under 30 days from the date of application or the response date in GST REG 18 form. This form is the Cancellation Order.

GST REG 20: On being satisfied, the GST officer can direct for the revocation of any proceedings towards the cancellation of the registration. In that case, the proper officer should pass the order in the Form GST REG 20. Thus, this form is basically the Revocation Order.

22

STUDENTS’ E-bulletin FinalVOL: 3, No.: 5. MAY 2018, ISSUE

Behind every successful business decision, there is always a CMA

Procedure for cancellation of GST registration

Portal: To cancel a GST registration, application must be submitted on the GST Common Portal in FORM GST REG-16.

Documents: Along with FORM GST REG-16, documents disclosing the following need to be submitted:

Details of inventories viz.: o inputs held in stock; or o inputs contained in semi-finished; or o finished goods held in stockon the date from which cancellation of registration is sought.

Details of capital goods held in stock on the date from which cancellation of registration is sought.

Details of any tax liability.

Details of any GST payment, made against such liability.

Time limit for submission: If a GST registration is cancelled involuntarily, then the above documents along with the application for GST Registration Cancellation and other relevant documents must be submitted on the GST Common Portal within 30 days.

Time limit for issuance of order: On submission of an application for cancellation of GST registration, the GST officer is required to verify the application and issue an order in FORM GST REG-19, within 30 days from the date of application.

Impact on cancellation of GST registration

The impact of cancellation of GST registration can be discussed as under:

On liability to pay tax and other dues: The cancellation of registration shall not affect the liability of the person to pay tax and other dues (under this Act) or to discharge any obligation (under this Act or rules made thereunder) for any period prior to the date of cancellation (whether or not such tax and other dues are determined before or after the date of cancellation).

Payment of input tax credit: The registered person whose registration is cancelled shall pay an amount equivalent to the credit of input tax in respect of inputs held in stock and inputs contained in semi-finished or finished goods held in stock or capital goods or plant and machinery on the day immediately preceding the date of such cancellation or the output tax payable on such goods, whichever is higher. Such amount is required to be paid either by way of debit in the electronic credit ledger or electronic cash ledger.

NB: In case of capital goods or plant and machinery, the taxable person shall pay an amount equal to the input tax credit taken on the said capital goods or plant and machinery, reduced by such percentage points as may be prescribed or the tax on the transaction value of such capital goods or plant and machinery under section 15, whichever is higher.

Filing of Final Return: When the GST registration of a registered person (other than an Input Service Distributor or a non-resident taxable person or a person paying tax under the composition scheme or TDS/TCS) has been cancelled, the person has to file a final return within 3 months of the date of cancellation or date of order of cancellation, whichever is later.

NB: Such Final Return has to be filed electronically (in FORM GSTR-10) through the GST common portal either directly or through a Facilitation Centre notified by the Commissioner.

Revocation of Cancellation of GST Registration

In case the GST registration has been cancelled by the Department there exists detailed provision for revocation of the cancellation. These are provided under Sec. 30 of the Central Goods and Services Tax Act, 2017. The provisions regarding revocation of registration are highlighted hereunder:

In case a GST registration application is cancelled involuntarily by a GST Officer, an application for revocation (in form GST REG 21) of cancellation of registration can be filed.

Such application for revocation of cancellation of registration is required to be filed to the Proper Officer (Assistant or Deputy Commissioners of Central Tax).

The application for revocation of cancellation of GST registration must be filed within a period of 30 days from the date of the service of the order of cancellation of registration at the GST common portal, either directly or through a Facilitation Centre notified by the Commissioner.

However, if the GST registration has been cancelled for failure to furnish returns, application for revocation shall be filed, only after such returns are furnished and any amount due as tax, in terms of such returns, has been paid along with any amount payable towards interest, penalty and late fee in respect of the said returns.

On examination of the application if the Proper Officer is satisfied, for reasons to be recorded in writing, that there are sufficient grounds for revocation of cancellation of GST registration, then he shall revoke the cancellation of registration by an order in FORM GST REG 22 within a period of 30 days from the date of the receipt of the application and communicate the same to the applicant.

However, if on examination of the application for revocation, if the Proper Officer is not satisfied then he will issue a notice in FORM GST REG 23 requiring the applicant to show cause as to why the application submitted for revocation should not be rejected and the applicant has to furnish the reply within a period of 7 working days from the date of the service of the notice in FORM GST REG 24.

Upon receipt of the information or clarification in FORM GST REG 24, the Proper Officer shall dispose of the application within a period of 30 days from the date of the receipt of such information or clarification from the applicant. In case the information or clarification provided is satisfactory, the Proper Officer shall dispose the application as per para (iii) above. In case it is not satisfactory, the applicant will be mandatorily given an opportunity of being heard, after which the Proper Officer after recording the reasons in writing may by an order in FORM GST REG 05, reject the application for revocation of cancellation of registration and communicate the same to the applicant.

The revocation of cancellation of GST registration under the State Goods and Services Tax Act or the Union Territory Goods and Services Tax Act, as the case may be, shall be deemed to be a revocation of cancellation of registration under Central Goods and Services Tax Act.

23

STUDENTS’ E-bulletin FinalVOL: 3, No.: 5. MAY 2018, ISSUE

Your Preparation Quick TakesYour Preparation Quick TakesYour Preparation Quick Takes

COST & MANAGEMENT AUDIT (CMAD)

GROUP: 4 PAPER: 19

Behind every successful business decision, there is always a CMA

A Cost Audit 35%B Management Audit 15%C Internal Audit, Operational Audit and other related issues 25%D Case Study on Performance Analysis 25%

A 35%D 25%

B 15%C 25%

CMA S S SonthaliaPracticing Cost Accountant,

BhubaneswarHe can be reached at:

24

STUDENTS’ E-bulletin FinalVOL: 3, No.: 5. MAY 2018, ISSUE

Behind every successful business decision, there is always a CMA

Learning Objectives:

To verify the correctness of the cost accounting records. To find out whether the principles of cost accountancy have

been fully and correctly applied in maintaining cost records. To search for the deficiencies in the cost record system of the

company. To attain efficiency in cost accounting systems and procedures

Reporting on Performance Analysis

The Cost Auditor has to provide his observations and suggestions under Para 2 of the Cost Audit Report as per CRA – 3 format. It is not specifically mentioned anywhere about the areas / points to be covered under this para. But, it can be assumed that the matters that are covered under this para should be in regards to those issues that affect the cost of the product / service.Therefore observation and suggestions are given by the auditor under this para based on the 'Performance Analysis' of the operations of the company related to its production process keeping in mind cost optimisation and/or cost reduction to enable company to be cost competitive.

The Cost Auditor has the power and authority as per the power given by the section 143 (1) and 143 (14) of The Companies Act 2013. So, for the requirements of Para 2 of the CRA – 3, the Cost Auditor is entitled to cover any area of activities of the company including for earlier years for fulfilment of his duty.

In this article, emphasis has been to cover those areas that the Cost Auditor can provide in the observations and suggestions in the Cost Audit Report after doing the 'Performance Analysis'.

The basic objective of Performance Analysis is to provide an actionable insight into costs and profitability for the management in the strategic and operational context. It aims at discovering various drivers of costs and profitability and their impact on the selected performance variables. This shall require understanding the unique industry specific factors that govern the operations of the company. This is important because the factors affect the company vary from industry to industry. For example, the companies that makes non-homogenous products like a Boiler for a Thermal Generation of Electricity shall have unusual amount of variable costs every year as the projects may differ in technical specification. Similarly for an electricity company who generate/transmit/distribute the electricity the issues are different. Therefore, the Cost Auditor should have a thorough knowledge about the industry and the operations.

However, there are some indicative contents that can be included in the observations that reflect about the costs. The following are the areas:

1. Production / Capacity Utilization Analysis2. Productivity / Efficiency Analysis3. Utilities efficiency Analysis4. Manpower Analysis5. Key costs and Contribution analysis6. Product Profitability Analysis7. Market Profitability Analysis8. Working Capital and Inventory Management Analysis

The above points are also discusses in the Study Note 7 of the Paper – 19 study materials. However it is explained below considering the importanceof above analysis.

1. Production / Capacity Utilization Analysis

The production and capacity utilisation information is provided in the Annexure 1 Part B & C of CRA – 3. This information does not provide the information about the

normative capacity that can be achieved. The capacity utilization can only be correctly determined when the normative capacity is established. For normative capacity determination, an average of 3 / 5 years of capacity maintained can be taken into consideration. This may vary with the technical specification. The Cost Auditor should consider the various factors responsible for the difference between them and arrive at the capacity to be taken as 100% capacity. The capacity is crucial for the determination of effect of fixed costs and variable costs that has link to the cost of the product / service.

The Auditor can refer to the CAS-2 stating about the determination of capacity to properly determining the capacity of the company.

2. Productivity / Efficiency Analysis

The productivity analysis refers to the efficient usage of the resources / inputs for product and services. Since around 80% of the cost is accounted for the raw-materials consumed, this needs for a strict monitoring of the efficiency of usage of raw-materials. Since most of the organisations have a budget for usage of materials, the Cost Auditor should observe for the basis of such budget. One of the method to notice any significant losses in usage of materials is observing the trends of input-output ratio or yield ratio and raw-materials consumed to finished product of previous years. Further this also needs to compared with the norms provided by machinery supplier and also the quality/purity of input materials. Higher ratio shall result in increase in costs.

The performance measures in respect of this area could be:o inputs utilised (material, man, machine, capital etc)

per unit of output or output obtained per unit ofan input variable

o Wastages as percentage of inputo Indices could be developed for Single Factor

Productivity (SFP), Multi-Factor Productivity (MFP), TotalFactor Productivity (TFT)

o Inter-relationships in various productivity measures e.g. output per man-hour may have increase, butif it is accompanied by higher wastage per man hour, then there is no real benefit.

3. Utilities efficiency Analysis

The production process requires usage of utilities for continuous production process. After the direct costs, the cost of utilities are the most important costs that the company has to incur. The utilities can be in form of electricity, air, steam,internet and / or any other material that plays an integral part of production process which is not found in the finished goods / services. In other words they are a substantial part of conversion cost. For the measurement of efficiency, the Cost Auditor should arrive at the standard cost of utilities per unit and the trends of last three to four years.

4. Manpower Analysis

The cost of manpower is reflected in the financial

25

STUDENTS’ E-bulletin FinalVOL: 3, No.: 5. MAY 2018, ISSUE

Behind every successful business decision, there is always a CMA

statements as Employee Costs for the company as a whole. But in the case of Cost Statements, the manpower is segregated in categories like Direct Labour, Other Production Overheads, Administrative Overheads, and Quality Control Overheads etc. This segregation is for each and every cost centre and for each product / service. Availability of such data can help the company for the planning of the manpower requirements or Human Resource planning and thus the estimation of costs to be incurred in recruitment and training. The performance of the employees is directly connected to the profitability of the company. These kind of data can be very helpful to establish an incentive scheme to motivate the employees. The Cost Auditor should critically analyse the costs to find out any idle time – normal / abnormal. The normal idle time are to be included in the cost whereas the abnormal are to be excluded and are to be targeted to be reduced. The Cost Auditor should also focus on the Labour turnover. The higher the turnover, the higher the cost to the company.

5. Key Costs and Contribution Analysis

The recovery of variable cost is significant for the long term sustainability of the company. Variable cost deducted from Sales provides for Contribution. This calculation also helps in calculation of Breakeven Point and Margin of Safety. This has impact on profitability. The Cost Auditor should view the trend of contribution relating to key costs and highlight any significant variation during those periods. Again, the relevance of Capacity Utilisation comes to the picture for deciding the fixed cost to be adopted. The fixed cost during the maintenance of Normative Capacity should be taken into consideration for calculation of Breakeven Point or Margin of Safety.

The scope of this analysis is only possible in the cost statements as the financial statements does not provide for the variable and fixed costs of each and every product / service. The Cost Auditor based on the nature and his judgement classify and accumulate the costs as fixed and variable to enable such analysis.

6. Product Profitability Analysis

The Cost Statements are prepared for each and every product / service. The companies that have multiple products or those that provide multiple services need to know the profitability of each and every product / service. The future sustainability of the company depends upon the profitability of each product / service. This can also help the management decide which product / service is to continue and which ones to discontinue and which one provides for maximum contribution to the company as a whole. Moreover, the company can take decisions regarding pricing of the products / services to retain the competitive edge in the market. The profitability can be found out at various stages of cost like – Cost of Production and Cost of

Sales that enables the company to identify the efficiency in each stages.

To provide for such an analysis, the Cost Auditor has to have a keen knowledge of the production process and also the accounting policy and system of the company.

7. Market Profitability Analysis