financial reporting fraud : a practical guide to detection

TRANSCRIPT

University of Mississippi University of Mississippi

eGrove eGrove

Guides, Handbooks and Manuals American Institute of Certified Public Accountants (AICPA) Historical Collection

2003

Financial reporting fraud : a practical guide to detection and Financial reporting fraud : a practical guide to detection and

internal control; internal control;

Charles R. Lundelius

Follow this and additional works at: https://egrove.olemiss.edu/aicpa_guides

Part of the Accounting Commons, and the Taxation Commons

Recommended Citation Recommended Citation Lundelius, Charles R., "Financial reporting fraud : a practical guide to detection and internal control;" (2003). Guides, Handbooks and Manuals. 117. https://egrove.olemiss.edu/aicpa_guides/117

This Book is brought to you for free and open access by the American Institute of Certified Public Accountants (AICPA) Historical Collection at eGrove. It has been accepted for inclusion in Guides, Handbooks and Manuals by an authorized administrator of eGrove. For more information, please contact [email protected].

Am

er

ica

n

In

st

itu

te

o

f C

er

tif

ied

P

ub

lic

A

cc

ou

nt

an

ts

F in a n c ia lR e p o r tin g

Fr a u d :A Practical Guide to

Detection and Internal Control

Charles R. Lundelius, Jr., CPA/ABV

Notice to Readers

Financial Reporting Fraud: A Practical Guide to Detection and InternalControl does not represent an official position of the American Institute ofCertified Public Accountants, and it is distributed with the understandingthat the author, editor, and publisher are not rendering legal, accounting,or other professional services in this publication. If legal advice or otherexpert assistance is required, the services of a competent professionalshould be sought.

page i 05-15-03 11:34:26

F in a n c ia lR e p o r tin g

Fr a u d :A Practical Guide to

Detection and Internal Control

Charles R. Lundelius, Jr., CPA/ABV

Copyright 2003 byAmerican Institute of Certified Public Accountants, Inc.New York, NY 10036-8775

All rights reserved. For information about the procedure for requesting permission tomake copies of any part of this work, please call the AICPA Copyright PermissionsHotline at (201) 938-3245. A Permissions Request Form for e-mailing requests is availableat www.aicpa.org by clicking on the copyright notice on any page. Otherwise, requestsshould be written and mailed to the Permissions Department, AICPA, HarborsideFinancial Center, 201 Plaza Three, Jersey City, NJ 07311-3881.

1 2 3 4 5 6 7 8 9 0 PP 0 9 8 7 6 5 4 3

ISBN 0-87051-472-5

page ii 05-15-03 11:34:26

DEDICATION

To my children, Alexandria, Christina and Trey, who taught me tolook at things from a fresh perspective.

To my wife, Patricia, who taught me to persevere until I found theanswer.

iii

page iii 05-15-03 11:34:26

page iv 05-15-03 11:34:26

ABOUT THE AUTHOR

Charles R. Lundelius, Jr., CPA/ABV, is with FTI Consulting, Inc.(NYSE:FCN), in Washington, DC. Mr. Lundelius is Senior ManagingDirector of FTI’s Securities Litigation Consulting Group, where he hasconducted numerous investigations of financial reporting fraud. His expe-rience in accounting includes securities and investment banking and anactive practice in consulting and litigation services. He has consulted andtestified in the areas of securities market pricing, investment suitability,securities fraud, accounting fraud, and compliance and due diligencepractices. He has qualified as an expert witness in securities tradingand valuations, damages, financial analysis, accounting, statistics, andeconometrics, having testified in federal and state court and before admin-istrative hearings of the Securities and Exchange Commission. Mr. Lun-delius is a frequent speaker at professional seminars and conferences ona variety of accounting and related topics. Mr. Lundelius also serveson the NASDAQ Listing Qualifications Panel, the hearing forum thatdetermines which stocks trade on NASDAQ.

The opinions expressed in this book are those of the author and donot reflect the positions of FTI Consulting, Inc. or the NASDAQ StockMarket.

v

page v 05-15-03 11:34:26

page vi 05-15-03 11:34:26

TABLE OF CONTENTS

Introduction xiii

Part A The Problem 1

Chapter 1 The Nature of Financial Reporting Fraud 3

What Constitutes Financial ReportingFraud? 3

Legal and Regulatory Guidance andStandards 4SEC Definition of Fraud 4Key Fraud Laws and Definitions 5SAS No. 82 7SAS No. 99 9Elimination of the Materiality Loophole 12Sarbanes-Oxley Act of 2002 15

Common Methods of Committing Fraud 19Conclusion 20

Chapter 2 Earnings Manipulation 21

Earnings Improvement 22Secondary Securities Markets and Insider

Trading 22New Securities Price Enhancement 24

Exchange Listing 29Conclusion 31NASDAQ Listing Standards 33

Chapter 3 Earnings Management 37

Cost of Equity 38

vii

page vii 05-15-03 11:34:26

viii Financial Reporting Fraud

Using the Capital Asset Pricing Model toDetermine the Cost of Equity 38

The Price of Volatility 39Why Manipulate Earnings? 40

Enhanced Share Value 40Using the Single-Stage Gordon Growth

Model to Determine Share Value 40The Reward of Consistency and Growth:

Price/Earnings Multiples 41Sustaining Share Price: How Fraudsters

Benefit 42Getting Around Time Restrictions 42

Flexibility in Accounting: A NumbersGame? 50Failure to Perform Punishes the Stock Price 51Four Types of Earnings Management 51

Conclusion 54

Chapter 4 Balance Sheet Manipulation 55

Growing Importance of the Balance Sheet 55Direct Methods of Balance Sheet

Manipulation: Fraudulent Entries 56Indirect Methods of Balance Sheet

Manipulation: Hiding Transactions 57Manipulation Techniques: Examples 58

Direct-Method Example: The Case of theVanishing Payables 58

Indirect Method Example: The MissingImpairment Loss 62

Conclusion 67

Chapter 5 Special Issues for Closely Held Companies 69

The Pressure to Placate OutsideShareholders 70

The Pressure to Satisfy the BankerLenders 70

The Pressure From Venture Capitalists toGo Public 71The Small Initial Public Offering Window 72Securities Law 72

Special Valuation Issues 74

page viii 05-15-03 11:34:26

Contents ix

Generally Accepted AccountingPrinciples-Basis Standard 75Cash Basis and Accrual Basis 75Tax Incentives 75

The Correlation Between Company Sizeand Fraud 76

The Audit Committee’s Role 77Conclusion 77

Chapter 6 Not-for-Profit and Government Entities 79

NPOs: Similar to and Yet Separate Fromthe For-Profit World 79Reputation Over Compensation 80Revenue Recognition 80Restricted Funds 80Expense Ratios 81

Government Entities 87The Significance of Compensation and

Reputation 87The Dangers in Greater Disclosure 87Methods for Hiding Problems 88Gray Areas in Revenue and Asset

Classification 89Conclusion 89

Part B The Fraud Battle 91

Chapter 7 Research Findings on FraudulentAccounting 93

The 1987 Treadway Report 94The 1999 Research Report 96

Operating and Financial Condition 96Quality of Internal Controls 97Nature and Duration of Fraud 100

Internal Control Report 103Conclusion 105

Chapter 8 The Role of the Audit Committee 107

Key Players in Internal Control 107Financial Management 107Senior Management 108Internal Auditors 109Audit Committees 109Outside Auditors 110

page ix 05-15-03 11:34:26

x Financial Reporting Fraud

Principal Blue Ribbon CommitteeRecommendations 111Charter and Reporting Lines 111Communications Between Auditor and Audit

Committee 113Audit Committee Overload 114Conclusion 116

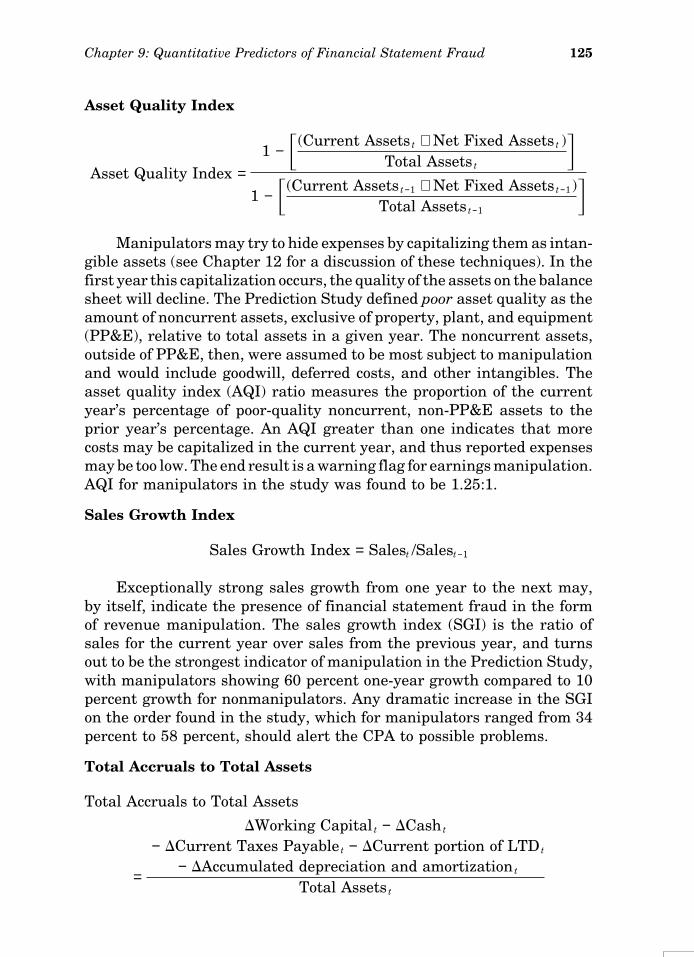

Chapter 9 Quantitative Predictors of FinancialStatement Fraud 117

COSO Research 117Size 118Amount of Misstatements 118Stock Market Listing and Industry 119Audit Committees 121

Academic Research 122Characteristics of Sample and Control

Companies 122Ratio and Index Analysis 123Application of Predictive Measures 126

Conclusion 130

Part C The CPA’s Fraud Battle 133

Chapter 10 Loss Contingencies and AssetImpairments 135

Loss Contingencies 135Warranty and Product Claims Reserves 137Estimation Issues 139

Asset Impairments 145Debt and Equity Instruments 148Conclusion 149

Chapter 11 Manipulation of Preacquisition Reserves 151

FASB Rationale for AllowingPreacquisition Contingencies 152Loss Contingencies: FASB No. 141 Versus

FASB No. 5 152Amount of the Contingency 154

Preacquisition Reserve Example 155Conclusion 159

page x 05-15-03 11:34:26

Contents xi

Chapter 12 Cost and Debt Shifting 161

Cost Shift to Related Entity 161Cost Shifting at Livent 161Fraud Detection at Livent 163Other Fraud Detection Steps 164

‘‘Hidden Debts’’ and the Special PurposeEntities 165GAAP Standards for SPEs 165SPE Fraud 169

Conclusion 172

Chapter 13 Recognizing Fictitious Revenues 173

Lack of an Agreement When BookingSales 175Standards of Evidence 176Detecting Fake Agreements 176

Nondelivery 177No Fixed Price 177

Royalties 178Side Agreements 178

Receivables Are Not Collectible 179Conclusion 188

Appendix A Proposed Rule: Disclosure inManagement’s Discussion and Analysisabout the Application of CriticalAccounting Policies 189

Appendix B SEC Staff Accounting Bulletin No. 99—Materiality 237

Appendix C SEC Staff Accounting Bulletin: No. 101—Revenue Recognition in FinancialStatements 253

Appendix D Financial Reporting Fraud SupplementalChecklist 287

page xi 05-15-03 11:34:26

page xii 05-15-03 11:34:26

INTRODUCTION

Ever since the collapse of the savings and loan industry in the 1980s,financial reporting fraud has been a topic of great discussion, not onlyamong accountants but also among regulators, legislators and the generalpublic. In a broader context, accounting fraud was one of the principalcauses listed by plaintiffs in class action suits brought by shareholdersagainst public companies over the last several years. And then cameEnron. Over the period of late 2001 through the first half of 2002, witha succession of high-profile bankruptcies of large companies related toaccounting fraud, which included Enron, Global Crossing and WorldCom,the world changed for accountants. Congress responded with the passageof the Sarbanes-Oxley Act of 2002 that restructured the accounting profes-sion and placed supervision in the hands of a government-appointedentity.

Financial Reporting Fraud: A Practical Guide to Detection and Inter-nal Control addresses the fraud issue from the practical perspective, usingillustrations and examples of fraud concepts, in addition to referencesto research findings and authoritative literature. The text draws uponfindings of professionals and academicians studying fraud in publiclytraded companies because financial information from those companies isreadily available, but the lessons learned from those studies are equallyapplicable to non-public companies, no matter the size or the industry.Furthermore, the hightened standards of corporate governance imposedon public companies by Sarbanes-Oxley and related regulations willgreatly impact private companies as well.

For instance, it would be difficult to imagine, in today’s environment,that a bank loan officer would present to a loan committee the applicationof a private company for a significant loan if that company’s board ofdirectors did not have an audit committee; should such a loan defaultdue to accounting fraud in the absence of an audit committee, banksenior management and regulators would probably not be very forgiving.Therefore, many of the reporting standards and internal controls nowbeing imposed or recommended for public companies will soon find theirway to private companies as well.

xiii

page xiii 05-15-03 11:34:26

xiv Financial Reporting Fraud

For that reason, in addition to the discussions and illustrations ofareas of financial reporting fraud, Financial Reporting Fraud: A PracticalGuide to Detection and Internal Control provides in the appendixes someof the key Securities and Exchange Commission proposed rules and staffaccounting bulletins that, while targeted at public companies, will likelybecome standards for private companies also. A CPA preparing for theworld after Sarbanes-Oxley should be well-versed in these issues, regard-less of the type of company involved.

page xiv 05-15-03 11:34:26

PART A

THE PROBLEM

1

page 1 05-15-03 11:41:58

page 2 05-15-03 11:41:58

CHAPTER 1

THE NATURE OF FINANCIAL

REPORTING FRAUD

Financial reporting fraud involves the alteration of financial statementdata, usually by a firm’s management, to achieve a fraudulent result.These altered financial statements are the tools then used by a company’sunscrupulous managers to obtain some reward. The reward may consistof direct compensation, such as receiving a bonus that otherwise wouldnot be paid without using altered, incorrect financial data to embellishmanagement’s operating performance. On the other hand, the compensa-tion may be less direct, in that managers avoid being fired for failing toachieve promised results. Compensation may also be indirect; for exam-ple, management may use fraudulent financial statements to raise addi-tional capital that, in turn, allows a firm to expand and presumablyenhance the value of shares held by management.

WHAT CONSTITUTES FINANCIAL REPORTING FRAUD?What constitutes financial reporting fraud has been the subject of muchdebate because the lines between fraud and discretion are not alwaysclear. It is easy to define fraud as a conscious effort by management toproduce financial statements with materially wrong accounting data. Itis almost as easy to identify as fraud misleading accounting entries thatmanagement cannot justify under any applicable accounting standards.Fraudulent acts become less obvious, however, when cloaked in the man-tle of accounting standards that are incorrectly applied. For example,the applicable accounting standards in the United States are generallyaccepted accounting principles (GAAP), and those principles may allowmanagement some discretion about when to recognize revenue orexpenses. Management is free to take full advantage of that discretion,but, in pushing accounting concepts to their limit, management must be

3

page 3 05-15-03 11:41:58

4 Financial Reporting Fraud

especially careful not to overstep. When operating on the edge of GAAPpermissibility, internal controls are stretched heavily, and one mistake ina seemingly small area can result in significant and drastic consequences.

Honorable people can debate the most appropriate use of a principlewhen looking at the gray or more broadly permissive areas of GAAP.Less-than-honorable people, however, might make use of these gray areasto produce financial statements that mislead. This practice is found mostoften in concert with other misleading applications of GAAP.

Those who commit fraud almost always fail to discuss their misuseof GAAP principles in the notes to financial statements. Although theaccounting for a certain transaction may appear to be supported by GAAP,failure to disclose so as not to make the financial statements misleadingmay take the reporting entity out of GAAP compliance. Without knowl-edge of the impact of GAAP gray-area judgments on the financial state-ments, unsuspecting readers may mistakenly assume that revenues andexpenses were accrued in a manner consistent with prior financial state-ments when, in fact, they were not. The end result may be that continuingoperations appear to be profitable while, in reality, there may be seriousproblems that the misuse of GAAP gray areas can cover up for a shortperiod of time.

As with proving any type of fraud, one must generally show thatthere was scienter, meaning that the perpetrator knew that his or heractions were designed to mislead. For purposes of this book, a perpetratorwith scienter—that is, a perpetrator who intends to use incorrect financialstatements to mislead—will be referred to as a ‘‘fraudster.’’ Thus, whenaccounting decisions purportedly in conformity with GAAP produce finan-cial statements intentionally designed (with scienter) to mislead thereader, those decisions cross the line into fraud.

LEGAL AND REGULATORY GUIDANCE AND STANDARDS

There are numerous sources for guidance on the nature and standardsto establish the existence of financial reporting fraud. These sourceshelp the CPA determine what fraud is, where to look for it, and who isresponsible.

SEC Definition of Fraud

The principal concepts that govern fraud are codified in the U.S. securitieslaws and regulations, especially Securities and Exchange Commission(SEC) Rule 10b-5, which states the following:

It shall be unlawful for any person, directly or indirectly, bythe use of any means or instrumentality of interstate commerce,

page 4 05-15-03 11:41:58

Chapter 1: The Nature of Financial Reporting Fraud 5

or the mails, or of any facility of any national securitiesexchange,(a) to employ any device, scheme, or artifice to defraud,(b) to make any untrue statement of a material fact or to omit

to state a material fact necessary in order to make thestatements made, in the light of the circumstances underwhich they were made, not misleading, or

(c) to engage in any act, practice, or course of business whichoperates or would operate as a fraud or deceit upon anyperson, in connection with the purchase or sale of any secu-rity.

Publicly traded companies must conform to GAAP and to the rulesand regulations promulgated by the SEC under U.S. securities laws. TheSEC drew heavily on accounting literature when it addressed the issueof accounting gray areas for materiality and other issues. SEC standardsthat have their origin in GAAP provide substantial guidance to determinefinancial reporting fraud not only for publicly traded companies, but alsofor all firms issuing financial statements in conformity with GAAP.

Key Fraud Laws and Definitions

In addition to SEC Rule 10b-5, there are several other important lawsand accounting statements that guide the CPA in matters dealing withfraud.

The Foreign Corrupt Practices Act of 1977

One decades-old law that still carries significant weight today is theForeign Corrupt Practices Act of 1977 (FCPA). This legislation, well-known for cracking down on bribery of foreign business and officials,went further and codified the requirement that all public companiesmaintain adequate internal controls. FCPA Section 102 states that thepublic company shall:

(A) make and keep books, records, and accounts, which, inreasonable detail, accurately and fairly reflect the transac-tions and dispositions of the assets of issuer; and

(B) devise and maintain a system of internal accounting con-trols sufficient to provide reasonable assurances that—(i) transactions are executed in accordance with manage-

ment’s general or specific authorization;(ii) transactions are recorded as necessary (1) to permit

preparation of financial statements in conformity withgenerally accepted accounting principles or any othercriteria applicable to such statements . . .

Management, therefore, had to take responsibility for the firm’sfinancial statements and establish internal controls that ensured trans-

page 5 05-15-03 11:41:58

6 Financial Reporting Fraud

actions were entered in accordance with management’s instructions. Fur-ther, management had to prepare its financial statements in accordancewith GAAP or other criteria, such as regulatory accounting for regulatedindustries. The FCPA held management accountable if fraud existed inthe financial statements.

Federal Sentencing Guidelines

Another area of law, contained in the federal sentencing guidelines,addresses the steps a company may take to mitigate criminal penalties ifit is ever found to have violated U.S. law. Those steps include establishingpolicies and procedures designed to implement an ‘‘effective program toprevent and detect violations of law.’’ The sentencing guidelines requirethat a company exercise ‘‘due diligence’’ to implement an ‘‘effective pro-gram,’’ and such ‘‘due diligence’’ requires, at a minimum, that a companymust: (1) spell out its policies and procedures, (2) communicate themeffectively with its employees, and (3) designate individuals who will beresponsible for enforcing those standards. If there is a likelihood thatcertain activities of a company or certain of its personnel are known tobe at risk of violating U.S. law, as may be demonstrated by prior conduct,the federal sentencing guidelines impose heightened requirements onmanagement to take steps to discipline offenders and implement proce-dures to prevent and detect such conduct in the future. Furthermore,there must be a monitoring mechanism with:

Systems reasonably designed to detect criminal conduct by itsemployees and other agents and by having in place and publiciz-ing a reporting system whereby employees and other agentscould report criminal conduct by others within the organizationwithout fear of retribution. (FCPA Sec. 8A1.3(k)(5)).

However, even though the monitoring requirements of the federalsentencing guidelines existed for many years, many companies had beenslow to implement such a reporting system until enactment of theSarbanes-Oxley Act of 2002 (see the discussion in the section titled ‘‘TheSarbanes-Oxley Act of 2002’’) and other post-Enron reforms. Only asrecent legislation and regulations imposed greater requirements on corpo-rate audit committees and boards of directors have companies rushed toinstall fraud-reporting hotlines and other reporting systems.

More important, however, is that if a company implements the fed-eral sentencing guidelines, that company and its management can holdup these actions taken as evidence of intent to prevent fraud. When theCPA is looking at how serious an organization is about fighting fraud,whether or not the organization has implemented steps previouslydescribed is a clear indicator. Finally, failure to implement applicable

page 6 05-15-03 11:41:58

Chapter 1: The Nature of Financial Reporting Fraud 7

government standards ‘‘weighs against a finding of an effective programto prevent and detect violations of law.’’ In the case of financial reportingfraud, those standards are expressed in GAAP and SEC rules and regula-tions, among others.

Statement on Auditing Standards No. 53

In 1988, the AICPA Auditing Standards Board (ASB) issued Statementon Auditing Standards (SAS) No. 53, The Auditor’s Responsibility toDetect and Report Errors and Irregularities. This Statement, since super-seded, set out the basis for distinguishing the difference between fraudand honest error. Referring to accounting fraud as ‘‘irregularities,’’ SASNo. 53 stated:

The term ‘‘irregularities’’ refers to intentional misstatementsor omissions of amounts or disclosures in financial statements.Irregularities include fraudulent financial reporting under-taken to render financial statements misleading, sometimescalled management fraud, and misappropriation of assets,sometimes called defalcations. Irregularities may involve actssuch as the following:

• Manipulation, falsification, or alteration of accountingrecords or supporting documents from which financial state-ments are prepared

• Misrepresentation or intentional omission of events, trans-actions, or other significant information

• Intentional misapplication of accounting principles relatingto amounts, classification, manner of presentation, or disclo-sure

Fraud, then, had the element of intent that resulted in manipulationof financial statements, misrepresentation of transactions, or misapplica-tion of accounting principles.

SAS No. 82By 1997, the ASB had issued SAS No. 82, Consideration of Fraud in aFinancial Statement Audit (AICPA, Professional Standards, vol. 1, AUsec. 316), which replaced SAS No. 53 but essentially retained the SASNo. 53 definition of fraud and added the concept of how fraud affectsfinancial statement users. SAS No. 82, since superseded, used the termmisstatement to characterize fraud, and stated the following:

Misstatements arising from fraudulent financial reporting areintentional misstatements or omissions of amounts or disclo-sures in financial statements to deceive financial statementusers.

page 7 05-15-03 11:41:58

8 Financial Reporting Fraud

Now, in addition to the presence of management intent, fraud’s defini-tion was expanded to include its purpose, which was to deceive the user.

SAS No. 82 also provided a list of 25 fraud risk factors—that is, redflags—to guide auditors in assessing risk and planning for an audit. Thestatement allocated the 25 red flags among three broad categories:

1. Management characteristics and influence over the control environ-ment

2. Industry conditions3. Operating and financial stability characteristics

Examples of red flags included aggressive or unrealistic forecasts,ineffective communication and support of entity values or ethics, anddomineering management behavior or attempts to influence audit scope.

Several years after the issuance of SAS No. 82, Barbara A. Apostolou,John M. Hassell, Sally A. Webber, and Glenn E. Sumners conductedresearch (‘‘The Relative Importance of Management Fraud Risk Factors,’’Behavioral Research in Accounting, 1/1/2001) that evaluated the weightplaced by 140 external and internal auditors on each of the three catego-ries and on the red flags in each category. The researchers found thatauditors had some fairly uniform feelings about circumstances most con-ducive to finding financial reporting fraud:

The aggregate decision model indicates that 58.2 percent of thetotal possible 100.0 percent decision weight is associated withthe group of red flags dealing with management characteristicsand influence over the control environment. Operating andfinancial stability characteristics were associated with 27.4 per-cent, while industry conditions red flags were associated with14.4 percent of the total decision weight. Thus, red flags associ-ated with management characteristics and influence over thecontrol environment were rated about twice as important asoperating and financial stability characteristics and about fourtimes as important as industry conditions red flags. The threesingle-most important red flags, which account for almost 40percent of the total decision weight, were all within the manage-ment characteristics category: (1) known history of securitieslaw violations (14.6 percent), (2) significant compensation tiedto aggressive accounting practices (12.9 percent), and (3) man-agement’s failure to display appropriate attitude about internalcontrol (12.6 percent).

Management characteristics and the control environment, then,clearly stood out among auditors as the most important indicators ofpotential fraud. Within that category, three red flags led the list: historyof violations, compensation tied to accounting, and lack of interest in

page 8 05-15-03 11:41:58

Chapter 1: The Nature of Financial Reporting Fraud 9

internal controls. Subsequent chapters of this book cover managementcharacteristics and internal controls in greater detail.

SAS No. 99

The ASB continued to refine its auditing guidance with regard to fraudand in 2002 released a new standard, SAS No. 99, Consideration of Fraudin a Financial Statement Audit (AICPA, Professional Standards, vol. 1,AU sec. 316), to supersede SAS No. 82. The new standard has a moreextensive list of red flags organized into categories that look at (1) incen-tives and pressures on management to commit fraud, (2) opportunitiesto commit fraud, and (3) the attitudes and rationalizations found amongthose who commit fraud. See Table 1.

Table 1. Risk Factors Relating to Misstatements Arising FromFraudulent Financial Reporting

Reprinted from Statement on Auditing Standards No. 99, Consideration of Fraudin a Financial Statement Audit (AICPA, Professional Standards, vol. 1, AU sec.316).

A.2 The following are examples of risk factors relating to misstatements arisingfrom fraudulent financial reporting.

Incentives/Pressures

a. Financial stability or profitability is threatened by economic, industry, or entityoperating conditions, such as (or as indicated by):— High degree of competition or market saturation, accompanied by declining

margins— High vulnerability to rapid changes, such as changes in technology, product

obsolescence, or interest rates— Significant declines in customer demand and increasing business failures in

either the industry or overall economy— Operating losses making the threat of bankruptcy, foreclosure, or hostile

takeover imminent— Recurring negative cash flows from operations or an inability to generate

cash flows from operations while reporting earnings and earnings growth— Rapid growth or unusual profitability, especially compared to that of other

companies in the same industry— New accounting, statutory, or regulatory requirements

b. Excessive pressure exists for management to meet the requirements or expecta-tions of third parties due to the following:— Profitability or trend level expectations of investment analysts, institutional

investors, significant creditors, or other external parties (particularly expecta-tions that are unduly aggressive or unrealistic), including expectations cre-ated by management in, for example, overly optimistic press releases orannual report messages

page 9 05-15-03 11:41:58

10 Financial Reporting Fraud

— Need to obtain additional debt or equity financing to stay competitive—includ-ing financing of major research and development or capital expenditures

— Marginal ability to meet exchange listing requirements or debt repaymentor other debt covenant requirements

— Perceived or real adverse effects of reporting poor financial results on signifi-cant pending transactions, such as business combinations or contract awards

c. Information available indicates that management or the board of directors’ per-sonal financial situation is threatened by the entity’s financial performance aris-ing from the following:— Significant financial interests in the entity— Significant portions of their compensation (for example, bonuses, stock

options, and earn-out arrangements) being contingent upon achieving aggres-sive targets for stock price, operating results, financial position, or cash flow1

— Personal guarantees of debts of the entity

d. There is excessive pressure on management or operating personnel to meetfinancial targets set up by the board of directors or management, including salesor profitability incentive goals.

1 Management incentive plans may be contingent upon achieving targets relating only tocertain accounts or selected activities of the entity, even though the related accounts oractivities may not be material to the entity as a whole.

Opportunities

a.The nature of the industry or the entity’s operations provides opportunities toengage in fraudulent financial reporting that can arise from the following:— Significant related-party transactions not in the ordinary course of business

or with related entities not audited or audited by another firm— A strong financial presence or ability to dominate a certain industry sector

that allows the entity to dictate terms or conditions to suppliers or customersthat may result in inappropriate or non-arm’s-length transactions

— Assets, liabilities, revenues, or expenses based on significant estimates thatinvolve subjective judgments or uncertainties that are difficult to corroborate

— Significant, unusual, or highly complex transactions, especially those closeto period end that pose difficult ‘‘substance over form’’ questions

— Significant operations located or conducted across international borders injurisdictions where differing business environments and cultures exist

— Significant bank accounts or subsidiary or branch operations in tax-havenjurisdictions for which there appears to be no clear business justification

b. There is ineffective monitoring of management as a result of the following:— Domination of management by a single person or small group (in a nonowner-

managed business) without compensating controls— Ineffective board of directors or audit committee oversight over the financial

reporting process and internal control

c. There is a complex or unstable organizational structure, as evidenced by thefollowing:— Difficulty in determining the organization or individuals that have controlling

interest in the entity

page 10 05-15-03 11:41:58

Chapter 1: The Nature of Financial Reporting Fraud 11

— Overly complex organizational structure involving unusual legal entities ormanagerial lines of authority

— High turnover of senior management, counsel, or board membersd. Internal control components are deficient as a result of the following:

— Inadequate monitoring of controls, including automated controls and controlsover interim financial reporting (where external reporting is required)

— High turnover rates or employment of ineffective accounting, internal audit,or information technology staff

— Ineffective accounting and information systems, including situationsinvolving reportable conditions

Attitudes/Rationalizations

Risk factors reflective of attitudes/rationalizations by board members, management,or employees, that allow them to engage in and/or justify fraudulent financialreporting, may not be susceptible to observation by the auditor. Nevertheless, theauditor who becomes aware of the existence of such information should consider itin identifying the risks of material misstatement arising from fraudulent financialreporting. For example, auditors may become aware of the following informationthat may indicate a risk factor:• Ineffective communication, implementation, support, or enforcement of the entity’s

values or ethical standards by management or the communication of inappropriatevalues or ethical standards

• Nonfinancial management’s excessive participation in or preoccupation with theselection of accounting principles or the determination of significant estimates

• Known history of violations of securities laws or other laws and regulations, orclaims against the entity, its senior management, or board members alleging fraudor violations of laws and regulations

• Excessive interest by management in maintaining or increasing the entity’s stockprice or earnings trend

• A practice by management of committing to analysts, creditors, and other thirdparties to achieve aggressive or unrealistic forecasts

• Management failing to correct known reportable conditions on a timely basis• An interest by management in employing inappropriate means to minimize

reported earnings for tax-motivated reasons• Recurring attempts by management to justify marginal or inappropriate

accounting on the basis of materiality• The relationship between management and the current or predecessor auditor is

strained, as exhibited by the following:— Frequent disputes with the current or predecessor auditor on accounting,

auditing, or reporting matters— Unreasonable demands on the auditor, such as unreasonable time constraints

regarding the completion of the audit or the issuance of the auditor’s report— Formal or informal restrictions on the auditor that inappropriately limit access

to people or information or the ability to communicate effectively with theboard of directors or audit committee

— Domineering management behavior in dealing with the auditor, especiallyinvolving attempts to influence the scope of the auditor’s work or the selectionor continuance of personnel assigned to or consulted on the audit engagement

page 11 05-15-03 11:41:58

12 Financial Reporting Fraud

When looking for early warning indicators, the CPA should firstfocus attention on the incentives and motives for fraud. When, for instance,in the midst of well-known industry problems, a firm in that industryprovides guidance to securities analysts that earnings will not be affected,a red flag emerges. Upon further investigation, the CPA may determinethat management has another incentive in that the firm’s compensationplan awards bonuses based on accounting results. Then, there may beopportunity to manipulate financial results because key senior managersdominate a fairly green and inexperienced staff who would not likelyquestion management’s decisions. Finally, management would rational-ize the use of fraudulent accounting because it enhances the value ofcompany stock.

This book examines incentives and motives in some detail, andthrough the use of examples and illustrations, it looks at opportunitiesand rationalizations as well.

Elimination of the Materiality LoopholeQualitative Materiality

With the publication of SEC Staff Accounting Bulletin (SAB) No. 99 in1999, the SEC staff made clear that fraudulent accounting entries knownto senior management could not be left unadjusted if they were deemed‘‘immaterial’’ using some mechanical, quantitative standard, such as apercentage of net income. Relying purely on a quantitative basis, whichwas a common practice before the publication of SAB No. 99, was nolonger acceptable. With the publication of SAB No. 99, qualitative materi-ality clearly took first position when the SEC staff stated, ‘‘Materialityconcerns the significance of an item to users of a registrant’s financialstatements. A matter is ‘material’ if there is a substantial likelihood thata reasonable person would consider it important.’’ Therefore, any itemthat could alter a reader’s perception of the financial condition of a com-pany could be considered material. (Chapter 3 provides further analysisof materiality from the perspective of the users of financial statements,and the entire text of SAB No. 99 is found in Appendix B.)

The SEC staff provided examples.

Among the considerations that may well render material aquantitatively small misstatement of a financial statementitem are—• whether the misstatement arises from an item capable of

precise measurement or whether it arises from an estimateand, if so, the degree of imprecision inherent in the estimate

• whether the misstatement masks a change in earnings orother trends

page 12 05-15-03 11:41:58

Chapter 1: The Nature of Financial Reporting Fraud 13

• whether the misstatement hides a failure to meet analysts’consensus expectations for the enterprise

• whether the misstatement changes a loss into income or viceversa

• whether the misstatement concerns a segment or other por-tion of the registrant’s business that has been identified asplaying a significant role in the registrant’s operations orprofitability

• whether the misstatement affects the registrant’s compli-ance with regulatory requirements

• whether the misstatement affects the registrant’s compli-ance with loan covenants or other contractual requirements

• whether the misstatement has the effect of increasing man-agement’s compensation—for example, by satisfyingrequirements for the award of bonuses or other forms ofincentive compensation

• whether the misstatement involves concealment of anunlawful transaction

For example, the following illustrates the first bullet point. Supposemanagement legitimately had to book an estimate of a patent asset’svalue when it was acquired (along with some other assets that wereequally hard to value). Later in the reporting period, though, as thepatented technology was licensed, the value of the patent became clearer,and that value was less than the originally booked amount. If the differ-ence between the original and the correct value was less than the firm’squantitative materiality threshold, say 5 percent of assets, then, applyingjust a quantitative standard, management was able to argue that noadjustment would be required. SAB No. 99, though, most likely wouldrequire management to make the adjustment because a more precisevalue is obtainable.

Likewise, when looking at income statement items, the SEC viewedthe practice of indulging fraudulent and clearly erroneous entries up tosome arbitrary percentage limit as a license for management to mislead:

The staff believes that investors generally would regard assignificant a management practice to over- or under-state earn-ings up to an amount just short of a percentage threshold inorder to ‘‘manage’’ earnings. Investors presumably also wouldregard as significant an accounting practice that, in essence,rendered all earnings figures subject to a management-directedmargin of misstatement.

page 13 05-15-03 11:41:58

14 Financial Reporting Fraud

Undoubtedly, auditors would continue to use quantitative standardswhen planning an audit, but when examining financial statementaccounts, in most cases detected fraudulent intentional misstatementswould be deemed material according to SAB No. 99. Any loophole thatfraudsters may have had before the issuance of SAB No. 99 to rely purelyon a mechanical application of quantitative materiality as a means ofjustifying fraudulent entries was effectively closed.

Quantitative Materiality

In addition to imposing qualitative standards for materiality, the SECpursued other steps to lower the triggers for quantitative materiality. Inthe matter of W. R. Grace (SEC Accounting and Auditing EnforcementRelease No. 1141, June 30, 1999), Grace management set up and usedreserves (called ‘‘Cookie Jar Reserves’’; see Chapter 3) to manage thereported earnings of its principal health care subsidiary, National MedicalCare, Inc. (NMC). In 1991 and 1992, NMC earned profits in excess oftargets given to securities analysts, and NMC took the excess profits toa reserve account that had no stated purpose. In 1993 and 1994, NMC’sactual profits were under the announced targets, so management drewdown on the reserve to increase reported earnings. This technique iscalled ‘‘earnings smoothing’’ and is done to show consistent growth overseveral reporting periods (the rationale for smoothing earnings is dis-cussed in detail in Chapter 3). W. R. Grace’s outside auditors knew aboutthe reserve, recognized that it violated GAAP (see Chapter 12 for a discus-sion of reserve accounting), and proposed adjusting entries. Grace man-agement refused to make the adjustments, though, and the auditorspassed on the adjustments because, when looked at from the perspectiveof Grace’s consolidated financial statements, the NMC subsidiary adjust-ments did not appear to be material.

The SEC disagreed. Grace management had focused the attentionof securities analysts on the performance of NMC and believed that NMC’sperceived steady, consistent growth in earnings was important enoughto Grace’s stock value that management was justified in using reservesto manage NMC’s earnings. In the SEC’s decisions issued in this matter,the SEC bootstrapped materiality up from Grace’s Health Care Group,mostly consisting of NMC, to the overall company:

The inclusion of the excess reserves in the Health Care Groupsegment information for the period 1991 through 1994 resultedin a material misstatement of segment information which, inturn, was material to Grace’s consolidated financial statementstaken as a whole for one or more periods during the relevantperiod.

page 14 05-15-03 11:41:58

Chapter 1: The Nature of Financial Reporting Fraud 15

In other words, because NMC was material to the Health Care Groupand the Health Care Group was material to Grace, improper use ofreserves to manage NMC earnings was material to Grace. Setting asidethe fact that the reserve account itself would fail the qualitative material-ity test because it was not set up in accordance with GAAP, the quantita-tive materiality test was lowered from the consolidated company leveldown to the segment level and even further to the level of a specificsubsidiary in the W. R. Grace case. In the SEC’s view, then, if managementtouts the performance of a specific subsidiary and then manages itsearnings, Grace would apply quantitative materiality at the subsidiarylevel.

Sarbanes-Oxley Act of 2002

When accounting frauds were tied to the collapse of Enron Corp., GlobalCrossing Ltd., and WorldCom, Inc., all occurring within the few monthsfrom December 2001 to June 2002, Congress reacted rapidly by passingthe Sarbanes-Oxley Act of 2002, which was signed by President Bush onJuly 30, 2002. The Act created the Public Company Accounting OversightBoard (PCAOB) to oversee the audit and auditors of public companies(referred to as ‘‘issuers’’ in the Act because those companies issue sharesthat are publicly traded).

Among the duties of the PCAOB, Congress wanted the newly formedentity to ‘‘establish auditing, quality control, ethics, independence, andother standards relating to the preparation of audit reports for issuers.’’(Sarbanes-Oxley, Sec. 101(c)(2).) With regard to auditing, quality control,and ethics, Congress mandated that auditors describe in each audit reportthe testing of the internal control structure and the procedures used bythe company to implement those controls. Specifically, the Act states thatthe audit report must present:

(I) the findings of the auditor from such testing;(II) an evaluation of whether such internal control structure

and procedures(aa) include maintenance of records that in reasonable

detail accurately and fairly reflect the transactionsand dispositions of the assets of the issuer;

(bb) provide reasonable assurance that transactions arerecorded as necessary to permit preparation of finan-cial statements in accordance with generallyaccepted accounting principles, and that receipts andexpenditures of the issuer are being made only inaccordance with authorizations of management anddirectors of the issuer; and

page 15 05-15-03 11:41:58

16 Financial Reporting Fraud

(III) a description, at a minimum, of material weaknesses insuch internal controls, and of any material noncompliancefound on the basis of such testing. (Sec. 103(a)(2)(A)(iii).)

Thus, with Sarbanes-Oxley, the record-keeping requirements of theFCPA are set out in greater detail, and the auditors are charged withtesting and reporting on the adequacy of controls relating to the mainte-nance of those records. Auditors are also required to report materialweaknesses or ‘‘any material noncompliance’’ relating to internal controls.Although one could argue that these steps are already required undergenerally accepted auditing standards, the requirements for these proce-dures now carry the force of federal law (and enhanced penalties underthe Act).

In addition, Section 404 of the Act required management to submitto the SEC an ‘‘internal control report’’ with the company’s annually filedfinancial statements and disclosures. That internal control report would:

(1) state the responsibility of management for establishing andmaintaining an adequate internal control structure andprocedures for financial reporting; and

(2) contain an assessment, as of the end of the most recentfiscal year of the issuer, of the effectiveness of the internalcontrol structure and procedures of the issuer for financialreporting. (Sarbanes-Oxley, Sec. 404(a).)

In addition to the auditor’s evaluation of internal controls underSection 103 of the Act described here, under Section 404(b), outside audi-tors are required to ‘‘attest to, and report on,’’ management’s assessmentof company internal controls as well.

More noteworthy, though, are the requirements relating to auditcommittees. The audit committee is defined as:

(A) a committee (or equivalent body) established by andamongst the board of directors of an issuer for the purposeof overseeing the accounting and financial reporting pro-cesses of the issuer and audits of the financial statementsof the issuer; and

(B) if no such committee exists with respect to an issuer, theentire board of directors of the issuer. (Sarbanes-Oxley,Sec. 2(a)(3).)

At least one member of the audit committee must be a ‘‘financialexpert’’ (or the company must disclose why it does not have such anexpert). The financial expert is a person who has:

(1) an understanding of generally accepted accounting princi-ples and financial statements;

page 16 05-15-03 11:41:58

Chapter 1: The Nature of Financial Reporting Fraud 17

(2) experience in(A) the preparation or auditing of financial statements of

generally comparable issuers; and(B) the application of such principles in connection with

the accounting for estimates, accruals, and reserves;(3) experience with internal accounting controls; and(4) an understanding of audit committee functions. (Sec.

407(b).)

Section 202 of the Act requires the audit committee to approve allaudit (and non-audit) services, effectively giving the audit committee thepower to hire and fire auditors. Section 204 spells out the minimumcontent of reports that the auditor must provide to the audit committee,which consist of:

(1) all critical accounting policies and practices to be used;(2) all alternative treatments of financial information within

generally accepted accounting principles that have beendiscussed with management officials of the issuer, ramifica-tions of the use of such alternative disclosures and treat-ments, and the treatment preferred by the registered publicaccounting firm; and

(3) other material written communications between the regis-tered public accounting firm and the management of theissuer, such as any management letter or schedule of unad-justed differences.

In short, the Act requires identification and discussion of the treat-ment of ‘‘critical accounting policies,’’ including any differences of opinion(‘‘alternative treatments’’) by and among company management and itsoutside auditors. Congress, then, wanted to encourage a frank discussionbetween the audit committee, company management, and outside audi-tors of the use of accounting principles with material impact that weresubject to different interpretations. However, in no place does the Actdefine critical accounting policies. For help with the term, one must lookto SEC pronouncements, and in particular the proposed rules containedin Release Nos. 33-8098; 34-45907, which set out the SEC’s criteria fordetermining critical accounting policies and estimates. This book exam-ines those criteria in detail, building upon the actual examples used inthe SEC’s proposed rules.1

1 These examples are expanded from examples contained in Securities and Exchange Commis-sion (SEC) Releases No. 33-8098 and No. 34-45907, Disclosure in Management’s Discussionand Analysis about the Application of Critical Accounting Policies to illustrate certainaspects of financial reporting fraud. Additional assumptions are added to the SEC examples.Subsequently, the SEC-recommended disclosures to the audit committee are presented toillustrate how those disclosures would have increased the likelihood of fraud detection. Theexamples, as shown, reflect the opinions of the author and not the SEC. The reader isencouraged to read the SEC releases, which are included as an appendix to this book.

page 17 05-15-03 11:41:58

18 Financial Reporting Fraud

Clearly, Sarbanes-Oxley places tremendous reliance on the auditcommittee as the last line of defense within the firm against financialfraud. If, as Congress intended, management and auditors make fulldisclosure to the audit committee of the material accounting policies mostsubject to differing interpretation, the audit committee becomes the finalarbiter before release of the financial statements of any judgment calls.

The Act, though, also makes clear that the audit committee is notthe only party responsible for overseeing the audit process and the ade-quacy of internal controls. Just to make sure that senior managementunderstands its responsibilities, Section 302 of the Act requires the ‘‘prin-cipal executive officer’’ and the ‘‘principal financial officer’’ to certify thatthe financial statements are fairly presented and that:

(4) the signing officers—(A) are responsible for establishing and maintaining inter-

nal controls;(B) have designed such internal controls to ensure that

material information relating to the issuer and its con-solidated subsidiaries is made known to such officersby others within those entities, particularly during theperiod in which the periodic reports are being prepared;

(C) have evaluated the effectiveness of the issuer’s internalcontrols as of a date within 90 days prior to the report;and

(D) have presented in the report their conclusions aboutthe effectiveness of their internal controls based ontheir evaluation as of that date;

(5) the signing officers have disclosed to the issuer’s auditorsand the audit committee of the board of directors (or personsfulfilling the equivalent function)(A) all significant deficiencies in the design or operation

of internal controls which could adversely affect theissuer’s ability to record, process, summarize, andreport financial data and have identified for the issuer’sauditors any material weaknesses in internal controls;and

(B) any fraud, whether or not material, that involves man-agement or other employees who have a significant rolein the issuer’s internal controls; and

(6) the signing officers have indicated in the report whetheror not there were significant changes in internal controlsor in other factors that could significantly affect internalcontrols subsequent to the date of their evaluation, includ-ing any corrective actions with regard to significant defi-ciencies and material weaknesses. (Sec. 302(a).)

By requiring that principal officers certify they have disclosed mate-rial internal control weaknesses to the auditor and the audit committee,

page 18 05-15-03 11:41:58

Chapter 1: The Nature of Financial Reporting Fraud 19

Congress has emphasized the officers’ role in communicating materialweaknesses and forced those officers to make a public declaration (subjectto significant penalties for perjury) to that effect. In summary, Congresshas placed responsibility for internal controls squarely on the shouldersof senior management. This book also discusses in detail the role of seniormanagement in the act of and prevention of financial reporting fraud.

While Sarbanes-Oxley principally applies to public companies, theAct and related reform measures will likely set the tone for corporategovernance in private companies as well. Concerns about financialreporting fraud among those who provide capital to private entities, suchas banks and venture capitalists, will drive implementation of publiccompany standards into the non-public sectors. Therefore, whether theCPA works with public or non-public entities, knowledge of all the rele-vant standards is essential.

COMMON METHODS OF COMMITTING FRAUD

Research carried out for the Committee of Sponsoring Organizations(COSO) of the Treadway Commission, found that, when it came to execut-ing financial reporting fraud, the most common kinds of fraud methodswere the following:

1. Overstatement of earnings2. Fictitious earnings3. Understatement of expenses4. Overstatement of assets5. Understatement of allowances for receivables6. Overstatement of the value of inventories by not writing down the

value of obsolete goods7. Overstatement of property values and creation of fictitious assets

These methods tend to fall into three broad categories:

1. Earnings manipulation2. Earnings management2

3. Balance-sheet manipulation

These three topics will be covered in each of the next three chapters.

2 There is no distinction in accounting literature between earnings management and earningsmanipulation. The author makes this distinction, however, for ease in explaining differentconcepts of financial reporting fraud affecting the income statement.

page 19 05-15-03 11:41:58

20 Financial Reporting Fraud

CONCLUSION

The following chapters in Part A cover the various kinds of financialreporting fraud for each of the three categories and corresponding motivesfor each kind. The early indicators of financial reporting fraud (bothquantitative and qualitative) are discussed in Part B, and the meansto detect some of the most difficult-to-find kinds of fraud are covered inPart C.

page 20 05-15-03 11:41:58

CHAPTER 2

EARNINGS MANIPULATION

Earnings manipulation is the direct alteration of accounting data for thepurpose of fraudulently changing reported income. For example, bookinga sale that clearly does not meet the requirements for revenue recognitionincreases revenues. Conversely, capitalizing marketing costs as an asset,contrary to guidance in generally accepted accounting principles (GAAP),decreases current period expenses. Notice also that both examples affectthe balance sheet as well: Recognizing fictitious sales inflates accountsreceivable; deferring marketing expenses creates some type of amortiz-able asset. Because the primary intent of these manipulations is, however,to increase earnings rather than create assets, these practices are classi-fied as earnings manipulation.

Though there is no distinction in accounting literature between earn-ings management and earnings manipulation, to better explain theimpact of financial reporting fraud on the income statement, earningsmanagement is treated as a subset of earnings manipulation and isdiscussed separately in Chapter 3, ‘‘Earnings Management.’’ Earningsmanagement generally involves the manipulation of a series of earningsdata to achieve a perception of profitability and/or growth in earnings,as illustrated in W. R. Grace (Securities and Exchange Commission (SEC)Accounting and Auditing Enforcement Release No. 1141, June 30, 1999),discussed in Chapter 1. The focus of this chapter is on the type of earningsmanipulation designed to give a one-shot boost to earnings.

Recent research has shed much light on the motives for earningsmanipulation. The Committee of Sponsoring Organizations of theTreadway Commission sponsored research published in 1999 (the COSOReport) that examined SEC enforcement actions for the period of 1987through 1997 (see Chapter 7 for a more complete discussion of thefindings). The COSO Report found that motives for fraud generally fellinto the following three broad categories. Firms or individuals attemptedto:

21

page 21 05-09-03 10:47:46

22 Financial Reporting Fraud

1. Increase the stock price to increase the benefits of insider trading andto obtain higher cash proceeds when issuing new securities.

2. Obtain national stock exchange listing status or maintain minimumexchange listing requirements to avoid delisting.

3. Avoid reporting a pretax loss and bolster other financial results.

A fourth motive, to cover up assets misappropriated for personalgain, does not involve earnings manipulation and is not discussed in thisbook.

EARNINGS IMPROVEMENT

Secondary Securities Markets and Insider Trading

The motive to improve earnings usually works in concert with othermotives; rarely does it stand alone. For example, one of the most commonancillary motives for earnings manipulation may be found in a firm’smanagement compensation plan. Such plans generally reward manage-ment based on reported earnings performance and, therefore, set thestage for potential manipulation. To compound the motive for fraud, theform of compensation paid to management for performing well is not justcash; stock (or some equivalent such as options, stock appreciation rights,or deferred compensation plans) is frequently a large component of com-pensation that increases in value if senior managers can fraudulentlyincrease reported earnings before selling their shares.

Stock Compensation

Over the last several decades, management consultants, compensationcommittees, and academicians have advocated the use of stock as a compo-nent of compensation to align the interests of management with those ofthe firm’s shareholders. Without significant share ownership, the advo-cates claimed, management was free to pursue its own self-interests,granting itself ever-higher cash salaries, benefits, and perquisites, andin a period of placid boards stocked with friends of management, the onlyrecourse for unhappy shareholders was to sell their shares. The cost ofpaying for management was referred to as ‘‘agency cost’’ because manage-ment served as the agent for shareholders, and management was empow-ered to run the company on their behalf. Agency cost was presumablyhigher if management did not have significant equity ownership, hencethe push for equity-based compensation plans.

Once management received stock (or equivalent) awards under thecompensation plan, however, managers immediately began to look foropportunities to sell some or all of their shares. The reasons behind

page 22 05-09-03 10:47:46

Chapter 2: Earnings Manipulation 23

managers’ desire to dispose of their equity varied, but most had to dowith lack of diversification. Typically, a manager compensated with stockquickly finds his or her personal portfolio dominated with employershares. Further, given that the source of the manager’s cash earnings isthe same source as the major securities holding in his or her portfolio, asignificant amount of financial security for that manager rests in justone firm: the manager’s employer. Therefore, the manager has everyincentive to diversify as soon as possible.

For senior management, though, who may have significant portionsof their net worth reflected in employer shares and who may also have theability to manipulate earnings (due to lax internal controls, for example),there is tremendous incentive to maximize net worth by fraudulentlyincreasing reported earnings to increase share price long enough to allowthem to dispose of their shares. Due to the price/earnings (P/E) multiplierused to value securities, a small, fraudulent increase in earnings pershare translates into a much greater increase in stock price—on the orderof 15 to 40 times as much, or more. When a senior executive is trying toliquidate large numbers of shares, such an increase is meaningful. If,though, the fraudulent increase in reported earnings helps meet stockanalysts’ expectations or changes negative earnings to positive, theimpact on share price may be much greater. During the late 1990s’Internet boom market, then-SEC Chairman Arthur Levitt observed thatcompanies missing street earnings per share (EPS) expectations by aslittle as one penny per share were hammered. Senior executives wishingto avoid such a drop in share price would push hard to find the extrapenny, probably through some type of manipulation.

Stock compensation, then, provides a powerful motivator for incomestatement manipulation and subsequent illegal insider trading. A man-ager who is heavily compensated in stock needs to sell to diversify. If thestock is volatile such that small changes in reported earnings have asignificant impact on market price and if actual earnings do not appearto be meeting expectations, the manager will come under pressure fromthe perspective of personal net worth and from colleagues in similarsituations to manipulate earnings. If the manager gives in to the pressureand then sells shares, that manager likely trades on material nonpublicinformation—information that the books are cooked—and is guilty ofillegal insider trading.

Contingent Compensation

In addition to the drive to pay management in stock, compensation expertsadded the requirements that pay (whether cash or stock) be made contin-gent upon performance. This contingency was also designed to alignmanagement’s interests with those of shareholders. Management com-

page 23 05-09-03 10:47:46

24 Financial Reporting Fraud

pensation agreements, for instance, may require the achievement of someabsolute level of net income or an increase in net income over somebenchmark to trigger bonus payments. Also, to give the contingent com-pensation plan the power to motivate managers, consultants urged com-pensation committees to make bonuses a significant part of totalcompensation. The end result was that managers certainly were moti-vated to increase reported earnings, but some managers, faced with theprospect of seeing their compensation fall significantly if they failed tohit their goals, succumbed to the temptation to manipulate earnings. Forthose managers, the increase in reported earnings was not necessarilyan accurate reflection of their business performance. Even though thecompensation experts may have been correct and justified, in theory, totry to align management’s interests with shareholders’, they may haveunwittingly set up strong motivators for financial statement fraud. Cer-tainly incentive compensation is a valid concept, but it must be imple-mented with well-designed and rigorously enforced internal controls.

New Securities Price Enhancement

The discussion of stock and insider trading thus far has largely centeredon the impact of earnings manipulation on shares trading in the secondarysecurities markets, that is, the trading of previously issued shares on theregulated exchanges and markets. In contrast, the primary securitiesmarkets consist of that group of investors (principally institutions andinvestment banks) who purchase newly issued stock; those investors thenbegin trading that stock in the secondary markets after shares are issued.The primary markets, though, present yet another opportunity for finan-cial statement fraud, especially for earnings manipulation, because sharevalues are usually a function of projected future income.

When most people think about newly issued securities, they thinkof initial public offerings (IPOs) of shares of companies that were notpreviously publicly traded. True, IPOs constitute a part of the primarysecurities markets, but so do the sales of new shares by firms that alreadyhave other identical shares trading publicly. The latter are referred toas seasoned equity offerings (SEOs) because, at the time of the sale of newshares, there are other, seasoned, shares outstanding that are alreadytrading. Both IPOs and SEOs present unique opportunities for fraudsters,but in either case, the fraudsters’ objective is usually the same: to raisemore capital than they could if they told the truth about their firm’sfinancial condition. With the extra capital, the fraudsters can then awardthemselves larger compensation packages, acquire related entities atovervalued prices, or simply stay afloat longer while incurring operatinglosses.

page 24 05-09-03 10:47:46

Chapter 2: Earnings Manipulation 25

IPOs

Companies preparing to go public are under intense pressure to cleanup their books and, if actual results are insufficient, to enhance historicalearnings to be published in the offering prospectus through fraudulentmethods. For firms that were privately held for some period of yearsbefore the IPO, there are numerous fraud motives and methods. (Chapter5 also covers the special pressures exerted on private firms by venturecapitalists.) In the privately held environment, a firm’s primary reportingresponsibilities are to banks and tax authorities; shareholders and man-agement are typically closely aligned (if not one and the same), makingtheir reporting needs secondary (see Chapter 5). For public companies,however, the reporting priority shifts to shareholders, especially thosenot in management, who do not have access to financial informationabout the firm beyond its published financial statements.

As discussed in Chapter 5, one area of greatest concern for potentialfraud in private firms is related party transactions. If one company outof a group of related companies planned to go public, the expense sharingand revenue allocations among the related entities, done most likely fortax minimization, need careful review as well as thorough documentation.A tax fraud scheme probably has elements of financial fraud as well,except the financial fraud may not become effectuated until other people(investors) begin to rely on those financial statements. For example, saythat two related firms shared manufacturing plant facilities in a numberof locations, but, due to heavy development costs, one firm’s marginalincome tax rate was only 10 percent and the other firm’s rate was 35percent. When management, which was essentially the same for bothfirms, began to allocate rent expense for the shared facilities, manage-ment devised a fraudulent expense-sharing arrangement that allocateddeductions away from the firm with a low marginal tax rate to the firmincurring a higher marginal tax rate. That scheme would violate variousprovisions of the Internal Revenue Code (see Revenue Procedure 2002-18 for a discussion of IRS-imposed reallocations used to correct suchschemes). However, should the low marginal rate firm later go public,its historical financial statements would not reflect an accurate share ofits expenses; rent expense would be too low. An investor or investmentbanker, then, relying on those financial statements to value the shares,may underestimate future rent expense. The end result is financial state-ment fraud arising from tax fraud and an overvaluation of the IPO shares.

SEOs

Academic research over the last decade has found several curious eventssurrounding firms that issue new shares in an SEO. Michael Gombola,Hei Wai Lee, and Feng-Ying Liu cited research that found share prices

page 25 05-09-03 10:47:46

26 Financial Reporting Fraud

declined only slightly, about 3 percent, after a firm announced an SEO.1

Some price decline is expected because the firm is increasing its outstand-ing shares, thus diluting earnings, at least in the near term; in thelong run, the firm hopes new capital provided in the SEO will provideadditional earnings that make up for and eventually reverse any near-term dilution. Reviewing other research, however, Gombola, Lee, and Liufound that actual performance after an SEO did not meet expectations:

Despite the price decline at the announcement, Loughran andRitter (1995) show further substantial declines after the SEOannouncement. Their findings suggest that to account fully forthe post-offering stock price underperformance over a five-yearhorizon, the price decline accompanying the announcementshould be as large as 44 percent. Their research indicates thatthe stock of firms offering seasoned equity remains substan-tially overvalued long after the announcement is made public.Similarly, McLaughlin, Safieddine, and Vasudevan (1996) showa significant decline in profitability during the three years fol-lowing the announcement. This finding is also consistent withthe hypothesis that firms offering seasoned equity issues areoverpriced following the offering.2

Clearly, something is amiss. The market may be consistently overop-timistic, hoping for quicker, higher returns from the new capital infusionthan actually occurs, or the share prices at the time of the announcementmay be inflated by fraudulent financial statements. The latter possibilityappears to be aided by the fact that the fraud resulted in raising morecapital that, in turn, could have been invested to produce earnings thatcover up the fraud in later periods. The following example illustrateshow.

Example Scenario. The Operating System Co., a publicly traded com-pany, designs and sells software that enhances the data processingperformance of mainframe computers. Operating System recentlyacquired, in a purchase transaction, the assets of Data Mover Corp.,a firm that develops and distributes software designed to improvedistributed processing capabilities through quicker data transfers. Thetransaction was financed by junk bonds placed with institutional inves-tors. Operating System management believed that Data Mover’s prod-uct would complement their own and that, since the target market forboth products was the same—mainframe users—there was an opportu-

1 ‘‘Evidence of Selling by Managers after Seasoned Equity Offering Announcements,’’ Finan-cial Management, September 22, 1997.

2 Ibid.

page 26 05-09-03 10:47:46

Chapter 2: Earnings Manipulation 27

nity to reduce redundancies in the combined sales forces and achievea synergistic benefit from the acquisition. In other words, only onesalesperson was now needed to call on an Operating System/DataMover customer instead of two.

Operating System’s chief financial officer (CFO) recognized thattrimming the sales force could have potentially adverse consequencesfor some customer relationships, so she set up loss contingencies forpossible early contract cancellations, write-offs of accounts receivable,and product discounts to accommodate unhappy customers. The losscontingencies were set up under a balance sheet account titled ‘‘Acquisi-tion Reserves.’’ The charge for these reserves went to goodwill (seeChapter 11 for a discussion on setting up acquisition reserves).

Soon after the acquisition, Operating System decided to float anoffering of new shares and secured, at the company’s annual meeting,the approval of its shareholders to issue the shares. Proceeds from theoffering, net of offering expenses and underwriters’ fees, would be usedto pay down the high-interest rate acquisition debt. When OperatingSystem’s CFO contacted the firm’s investment bankers who wouldmanage the offering, the investment bankers noted that OperatingSystem’s stock price had slumped after the Data Mover acquisitionbecause the market did not believe that synergies from the acquisitionwould be significant. ‘‘You’re going to have to prove to the Street thatyou will indeed have synergies from this acquisition in your next quar-terly filing, or we will have to discount the offering price severely,’’said the managing director of the investment banking firm. This putthe CFO under significant pressure because she had assured seniormanagement that she believed the price the new shares would fetchwould be close to the current price of shares already trading on themarket. Her pricing assumption was important because managementdid not want to see significant dilution.

The next quarterly filing with the SEC was due in two weeks; thequarter had ended one month earlier. The CFO had to think fast. Sheknew that in the weeks after the acquisition, senior sales managersdecided to have Data Mover sales personnel pair up with OperatingSystem salespeople to make joint calls on common customers to mini-mize customer defections to competitors. As a result of this executivedecision, the hoped-for redundancy reductions were not showing up asquickly as planned. On the other hand, though, the joint sales callshad so far resulted in fewer unhappy customers, so the acquisitionreserves went largely untapped, though it was still too early to tellwhether they would be needed.

The CFO concluded, then, that she could, in her words, ‘‘recharac-terize’’ the acquisition reserves to include redundant sales salaries as an

page 27 05-09-03 10:47:46

28 Financial Reporting Fraud

acquisition expense. Even though anticipated personnel terminationswere accounted for in a separate charge, she rationalized that carryingthe extra sales personnel on the payroll was an expense incurred inlieu of the expected losses from unhappy customers. The CFO instructedthe controller to charge the redundant salaries to acquisition reservesinstead of payroll expense. The controller, when asked why he did notquestion the CFO’s instruction, said that he believed that because theaccount title for the reserves was so broadly worded, ‘‘the acquisitionreserves could be used for just about any acquisition-related expensethat came up.’’

By running the expense for redundant personnel through the bal-ance sheet account, the CFO was able to show a reduced payroll cost,compared to the combined payroll of both Operating System and DataMover before the acquisition, in the quarterly income statement filedwith the SEC. The investment bankers were pleased and priced theoffering of new shares with only a small discount from quoted priceson shares already trading. As an added bonus, when the market sawthat payroll cost had declined due to perceived synergies in the acquisi-tion, the price of Operating System’s stock increased, covering most ofthe underwriting costs of the seasoned equity offering.

Example Analysis. While this example deals with loss contingencies,as discussed in Financial Accounting Standards Board (FASB) State-ment of Financial Accounting Standards No. 5, Accounting for Contin-gencies, and FASB Statement No. 141, Business Combinations, thefacts here do not require much analysis in that area (however, seeChapter 11 for a more detailed discussion of reserves). Essentially, theCFO attempts to justify debiting salary costs against reserves set upfor other purposes, which violates GAAP; moreover, it is not likely thatredundant salary costs would even qualify as a loss contingency. Thefact that the account title is ambiguous is irrelevant; the stated pur-poses for the reserves were to absorb anticipated financial consequencesof unhappy customers. The fact that management spent more moneythan originally planned to keep the customers happy does not allowthe company to access those reserves.

Furthermore, to use the reserves to effectively hide salary expenseto give the appearance of improved operating results is deceptive with-out adequate disclosure, which was pointedly missing in the example.Materiality may not even be a workable defense in this situation. Theamount of the payroll costs squirreled away in reserves may not havebeen large relative to overall net income from the perspective of quanti-tative materiality, but the fact that investment bankers and their

page 28 05-09-03 10:47:46

Chapter 2: Earnings Manipulation 29