financial services regulatory authority

TRANSCRIPT

FINANCIAL SERVICES REGULATORY AUTHORITY

31 March 2018ANNUAL REPORT

FINANCIAL SERVICES REGULATORY AUTHORITY (FSRA) Annual Report 2018

FINANCIAL SERVICES REGULATORY AUTHORITY (FSRA) Annual Report 2018 01

ABBREVIATION 2

INTRODUCTION 6

THE MINISTRY IN CHARGE OF THE FSRA 7

THE FSRA MANDATE 8

ORGANISATIONAL IDENTITY AND DEFINITION 9

FSRA STATEMENT OF VALUES 10

THE REGULATORY AND LEGISLATIVE FRAMEWORK 11

CHAIRMAN’S REPORT 12

CORPORATE GOVERNANCE 13

GENERAL REVIEW OF THE ECONOMY 19

CEO’s REVIEW 23

FACTS AND FIGURES - DASHBOARD 35

FSRA HISTORIC FINANCIAL SUMMARY 39

REGULATED INDUSTRIES – DETAILED REPORTS

1. Capital Markets Institutions 40

2. Credit and Savings Institutions 57

3. Savings and Credit Cooperative Societies (SACCOs) 59

4. Credit Providers 67

5. Building Societies 72

6. Insurance, Retirement Funds and Medical Schemes 78

7. Long Term Insurance Companies 82

8. Short Term Insurance Companies 95

9. Retirement Funds 106

LEGAL SERVICES, STAKEHOLDER ENGAGEMENTS AND

CONSUMER PROTECTION 124

FSRA AUDITED FINANCIAL STATEMENTS 129

CONTENTS

FINANCIAL SERVICES REGULATORY AUTHORITY (FSRA) Annual Report 2018

AML/CFT - Anti-Money Laundering / Combating the Financing of TerrorismAUM - Assets Under ManagementAMLO - Anti-Money Laundering Officers and Compliance OfficersCIS - Collective Investment SchemesCMA - Common Monetary AreaCMD - Capital Markets Development DivisionCMI - Capital Markets InstitutionsCSI - Credit and Savings Instutions DivisionCSD - Central Securities DepositoriesCISNA - (SADC) Committee of Insurance, Securities and Non Banking Financial AuthoritiesFATCA - Foreign Accounts Tax Compliance ActFATF - Financial Action Task ForceFIP - Finance and Investment Protocol (SADC)FSB - Financial Services Board (South Africa)FSPs - Financial Services ProvidersFSRA - Financial Services Regulatory AuthorityIAIS - International Association of Insurance SupervisorsIMF - International Monetary FundIOPS - International Organisation of Pensions SupervisorsIRF - Insurance and Retirement Funds DivisionMLTPF ACT - Money Laundering and Financing of Terrorism (Prevention) ActMOU - Memorandum of UnderstandingNAMFISA - Namibia Financial Institution Supervisory AuthorityNBFIs - Non-Banking Financial InstitutionsNBFIRA - Non-Bank Financial Institutions Regulatory Authority RIRF - Registrar of Insurance And Retirement FundsSACCO - Savings and Credit Co-OperativesSADC - Southern African Development CommunitySSX - Swaziland Stock ExchangeTWG - Technical Working GroupOTC - Over The Counter

ABBREVIATIONS

02

FINANCIAL SERVICES REGULATORY AUTHORITY (FSRA) Annual Report 2018

ABBREVIATIONS PERFORMANCE OVERVIEW

03

TOTAL ASSETS

E910 Million(2017: E996 Million)

TOTAL CLAIMS

E213 Million(2017: E151 Million)

GROSS PREMIUMS

E631 Million(2017: E584 Million)

NET ASSETS

E413 Million(2017: E329 Million)

NET PROFIT

E127 Million(2017: E124 Million)

5 SHORT TERM LICENCES APPROVED (2017: 5)

SHORT TERM INSURANCE BUSINESS AT A GLANCE

TOTAL ASSETS

E3.9 Billion(2017: E3.7 Billion)

TOTAL CLAIMS

E547 Million(2017: E432 Million)

GROSS PREMIUMS

E662 Million(2017: E625 Million)

NET ASSETS

E515 Million(2017: E470 Million)

NET PROFIT

E72 Million(2017: E59 Million)

7 LONG TERM LICENCES APPROVED (2017: 7)

LONGTERM INSURANCE BUSINESS AT A GLANCE

TOTAL ASSETS

E28 Billion(2017: E27 Billion)

LOCAL INVESTMENTS

E11.9 Billion(2017: E10.2 Billion)

TOTAL CONTRIBUTIONS

E1.5 Billion(2017: E1.8 Billion)

BENEFITS PAID

E1.5 Billion(2017: E1.4 Billion)

FOREIGN INVESTMENTS

E15.9 Billion(2017: E16.8 Billion)

122RETIREMENT FUNDS LICENCES APPROVED (2017: 120)

42% LOCAL INVESTMENTS (2017:38%)

RETIREMENT FUNDS AT A GLANCE

TOTAL ASSETS UNDER REGULATION

E41.7 Billion334FINANCIAL SERVICES LICENCES APPROVED

TOTAL LICENCES AND TOTAL ASSETS UNDER REGULATION

FINANCIAL SERVICES REGULATORY AUTHORITY (FSRA) Annual Report 2018

PERFORMANCE OVERVIEW

04

TOTAL ASSETS OF SACCOS

E1.5 Billion(2017: E1.2 Billion)

TOTAL ASSETS OF BUILDING SOCIETIES

E2.4 Billion(2017: E2.0 Billion)

TOTAL ASSETS OF CREDIT PROVIDERS

E4.6 Billion(2017: E3.5 Billion)

170 LICENCES APPROVED (2017: 180)

TOTAL ASSETS UNDER MANAGEMENT

E25.8 Billion(2017: E23.3 Billion)

GROSS REVENUE

E138.4 Million(2017: E119.9 Million)

30 CAPITAL MARKETS LICENCES APPROVED (2017: 24)

TOTAL EXPENSES

E113.3 Million(2017: E103.0 Million)

CREDIT AND SAVINGS INSTITUTIONS AT A GLANCE

CAPITAL MARKETS INSTITUTIONS AT A GLANCE

FINANCIAL SERVICES REGULATORY AUTHORITY (FSRA) Annual Report 2018

POPULATION

1.14 Million People

Gross Domestic Product

E55.27 Billion

Employment to Population Ratio

41.1%

PERFORMANCE OVERVIEW KEY FIGURES ON MACRO ECONOMIC DATA

GDP Annual Growthas at 31 March 2018

US Dollar Exchange Rate as at 31 March 2018

0.2%

USD1 = E11.8108

05

Source: https://nsd.Eswatini:opendataforafrica.org/chkrctc/population

Source: https://nknoena.com/atlas/Eswatini/GDP

FINANCIAL SERVICES REGULATORY AUTHORITY (FSRA) Annual Report 2018

INTRODUCTION

The Financial Services Regulatory Authority (FSRA) hereby presents its annual report for the year ended 31 March 2018.

The FSRA is built on the energy and drive of its people. This year’s Annual Report is all about capturing the dynamic quality that permeates every department of the Authority. The passionate Board of Directors, Executive Committee, along with

dedicated colleagues, have profoundly affected the Financial Services Sector in a special way.

On every page of this report, we will introduce you to the true inner workings of the FSRA, the engines that keep the Authority running strong. You will see faces, smiles, curious and determined eyes, passionate hearts, and boundary-pushing minds. In short, our people.

06

FINANCIAL SERVICES REGULATORY AUTHORITY (FSRA) Annual Report 2018

INTRODUCTION THE MINISTRY IN CHARGE OF THE FSRA

The Ministry of Finance

The Ministry of Finance is the Ministry responsible for FSRA’s policy guidance. The Mission of the Ministry of Finance is to promote Macroeconomic stability in

Eswatini by formulating and implementing fiscal and financial policies that optimise economic growth and improve the welfare of its citizens. One of the major components of the Ministry’s mission is to:

Provide a sound regulatory framework for the country’s financial sector, hence the FSRA was established to fulfil this mandate.

Create an environment which will promote private sector development

07

FINANCIAL SERVICES REGULATORY AUTHORITY (FSRA) Annual Report 2018

THE FSRA MANDATE

a) The stability of the Eswatini financial system;b) The safety and soundness of financial services providers;c) The highest standards of conduct of business by financial services

providers;d) The promotion of fair competition between different financial service

providers for the benefit of stakeholders;e) The fairness, efficiency and orderliness of the Eswatini

non-bank financial sector, andf) The protection of the stakeholders.

The principal objects of the Authority are spelt out in the FSRA Act, as being to foster, through regulation and prudential supervision of financial services providers:

08

FINANCIAL SERVICES REGULATORY AUTHORITY (FSRA) Annual Report 2018

THE FSRA MANDATE FSRA ORGANISATIONAL IDENTITY AND DEFINITION

The FSRA Vision

The FSRA Mission

To be a world class regulator of financial services.

The following is an outline of what we do (our mission); how we do this (our values); where we want to go (our vision); and how all fits together (our strategic model).

We regulate and supervise financial services to protect stakeholders and foster a stable financial system in Eswatini.

09

FINANCIAL SERVICES REGULATORY AUTHORITY (FSRA) Annual Report 2018

We maintain open, honest and direct relationships with our stakeholders. We treat non-public information at our disposal with utmost confidentiality in accordance with the law.

People are important to us. We work as a team to satisfy our stakeholders.

We execute our mandate and in doing so we fulfil our duties to all stakeholders. We report and take responsibility for our actions.

We are open and transparent in our dealings with stakeholders.

Our laws and regulations guide our decisions. We apply the same principles to similar events.

IntegrityWe, at FSRA, base our decisions on ethical principles and legal fairness.

THE FSRA STATEMENT OF VALUES

Confidentiality

Teamwork

Transparency

Consistency

Accountability

10

FINANCIAL SERVICES REGULATORY AUTHORITY (FSRA) Annual Report 2018

THE FSRA STATEMENT OF VALUES THE REGULATORY AND LEGISLATIVE FRAMEWORK

The FSRA Act, No.2 of 2010, is the legislative frame-work governing the operations of the Authority and the regulation and supervision of Non-Bank Financial Institutions (NBFIs) and matters inciden-tal thereto. The FSRA Act is the umbrella act of the Financial Services Laws for regulating all the NBFIs. The Act prescribes the operations, responsibilities and accountabilities of the FSRA including: Constitution of the Authority; The Board, Chief Executive Officer and Staff of

the Authority; Financial Resources of the Authority; Administration of Financial Services Laws;

Financial Services Licenses; Market Conduct of Financial Services Providers; Auditors and Actuaries; Information, Reports, Inspection and Investiga-

tion; Disciplinary Measures; Curators and Winding up of Authorised Finan-

cial Services Providers (FSPs); The Ombudsman of Financial Services; Appeals; and Miscellaneous provisions.

The regulated Financial Services Providers are listed below:

The Umbrella Act – The Financial Services Regulatory Authority Act (2010)

Name of the Industry Act Supporting Rules and Regulations Types of FSPs

INSURANCE INDUSTRY

The Insurance Act, 2005 1. Insurance Regulations, 20082. Insurance Directives, 2008

1. Reinsurers2. Insurers3. Insurance Brokers4. Corporate Agents5. Individual Agents6. Medical Aid Schemes7. Medical Aid Scheme Providers

RETIREMENT FUNDS INDUSTRY

The Retirement Funds Act, 2005 1. Retirement Funds Regulations, 2008

2. Retirement Funds Directives, 2008

1. Local Retirement Funds 2. Foreign Retirement Funds3. Beneficiary Funds4. Funds Administrators5. Trustees of Retirement Funds6. Other Fund Service Providers

CAPITAL MARKETS INDUSTRY

Securities Act, 2010 1. Industry specific sub-legislations awaiting promulgation.

1. Securities Exchanges2. Investment Advisors3. Investment Advisor Representatives4. Collective Investment Schemes5. Collective Investment Scheme Managers6. Central Securities Depositories7. Trustees and Custodians8. Dealer Representatives9. Exempt Dealers

CREDIT AND SAVINGS INDUSTRY

1. Building Societies Act, 19622. Consumer Credit Act, 20163. SACCOs Bill – under

drafting

1. Consumer Credit Regulations awaiting promulgation

1. Building Societies2. Savings and Credit Cooperative Societies

(SACCOs)3. Credit Providers4. Credit Bureaus5. Debt Counsellors

Note: Other laws applicable to all Financial Services Providers include, inter alia, the Companies Act, the Employment Act and the Income Tax Order.

11

FINANCIAL SERVICES REGULATORY AUTHORITY (FSRA) Annual Report 2018

INTRODUCTION

The Board is grateful to the Minister of Finance, for showing confidence in appointing its members to serve on the board

of the Financial Services Regulatory Authority. The end of this reporting period completes the term for the board. Therefore, the Board is grateful for the opportunity to present an update on the activities at the FSRA, which it now outlines below:

a) Attendance at meetings: Throughout its term in office, the board demonstrated commitment to the business of the Authority, in that they took attendance at board meetings very seriously, as demonstrated in the next section of this report. No meeting was postponed as a result of lack of quorum. This made decision making a lot easier.

b) No Government Subventions requested: The FSRA took a decision on operating on a shoestring budget three years ago by foregoing burdening government with requests for funding its operations. Instead, the FSRA embarked on carrying out its legislative mandate by streamlining operations to fit the resources it is collecting from the levying of regulated entities. It is worth noting that the FSRA, has not increased levy rates since its establishment. By not increasing levy rates, the effectiveness of its supervision has not been compromised.

c) Governance Policies: During its term in office, the board has been able to approve 13 policies to guide management administer the Authority in accordance with good corporate governance principles.

d) Automation of the Stock Exchange: A new stock exchange fully automated with two trading platforms (Main Board and SME platform) is to be launched soon. Management has submitted a business plan currently considered by the board aimed at turning around the stock exchange into a financially viable market. A motivation is to be submitted to the Minister proposing demutualisation of the exchange thus freeing the FSRA from funding the exchange.

e) Staff turnover: The FSRA has been experiencing a turnover of staff at an accelerated pace over the last three years largely due to attraction by better salaries in the financial sector. The board has since commissioned a job evaluation and salary review whose outcome will correctly position the remuneration structure of the Authority. It will be in the best interest of the FSRA to consider the recategorisation of the Authority to category “B” in order to improve its ability to retain competent staff.

f) Outstanding legislation, regulations and notices awaiting gazetting: The board appeals to the Minister to implore officials at the Ministry to process draft legislation, regulations and industry practice notes in order to strengthen the supervisory framework. Technical assistance has been obtained from the IMF and First Initiative to update and harmonise the FSRA Act and its subsidiary legislations such that accelerating the speed of promulgating legislation is crucial going forward.

g) Placing the Motor Vehicle Accident Fund under supervision: the FSRA has received notification from the Ministry, communicating a ministerial directive for the supervision of the MVA Fund by the Authority. The Authority appreciates this move, as the MVA Fund plays a key role in social provision for victims of road accidents. In the same spirit, the Authority also desires that the Occupational Health and Safety Fund, as well as Phalala Fund be brought under FSRA supervision, since now, these funds are bleeding government millions of Emalangeni.

h) New Strategic Plan: The FSRA has formulated a new strategic plan starting 1 April 2018 to 31 March 2021, by which it aims to focus attention on increasing FSRA intensity of supervision. The strategy incorporates the IMF-First Initiative technical assistance aimed at modernising and harmonising the legislative framework of the financial services sector as well as aligning the operations of the FSRA and complementing the efforts of the Central Bank of Eswatini in promoting financial stability.

CHAIRMAN’S REPORT

12

FINANCIAL SERVICES REGULATORY AUTHORITY (FSRA) Annual Report 2018

CHAIRMAN’S REPORT CORPORATE GOVERNANCE REPORT

ROBUST CORPORATE GOVERNANCE

As a Board, we believe that a strong corporate governance framework and culture translates to a strong Authority that delivers

for all its stakeholders. We recognise that the way we do business is critical in order for us to earn and maintain the respect and trust of all stakeholders including our regulated entities, consumers, suppliers, employees, the shareholder and the community. The FSRA directors and management are committed to conducting business in an ethical, fair and transparent manner in accordance with high standards of corporate governance. The Board, together with the management team, leads by example. We have a robust corporate governance framework in place and we are committed to fostering a culture of compliance that values personal and corporate integrity, accountability and continuous improvement. Our corporate governance framework includes:

An engaged Board of directors with a diverse range of skills and experience supported by an effective Board Committee structure.

Clear and transparent communication with our stakeholders.

Strong risk management and assurance processes and culture.

Our Values and Behaviours and supporting policies that underpin the way we behave and meet our strategic objectives.

1. Our Board

In accordance with Section 7 of the FSRA Act, 2010, the Authority is administered and managed by a Board of Directors. The composition of the Board is stipulated in the Act to consist of:a) A Chairman and not more than 4 other members,

who shall be appointed by the Minister of Finance. Members appointed by the Minister shall be persons of recognised standing and experience in the financial services sector.

b) A representative of the Swaziland Law Society;c) A representative of the Institute of Account-

ants;

d) The Principal Secretary of the Ministry of Finance, or a person authorised by the Principal Secretary in writing to act on behalf of the Principal Secretary; and

e) The Chief Executive Officer of the Authority, who shall act as secretary to the Board.

The members of the Board for the year ended 31 March 2018 comprised the following:

1. Mr Stephen L. Simelane - Chairman (Appointed 2015)2. Mr Modern B. Samketi - Member (Appointed 2015)3. Mr Nathie E. Maseko - Member (Appointed 2015)4. Amos C. Mkhatshwa - Member (Appointed 2015)5. Mr Sabelo J. Mabuza - Member (Appointed 2015)6. Mr Ntsika W. Fakudze - Member (Appointed 2015)7. Mr Nkululeko H. Dlamini - Member (Appointed 2017)

11.1 Board term of office

A member of the Board, other than the Principal Secretary and the Chief Executive Officer, shall hold office for a period not exceeding three years on such terms and conditions as the Minister may determine, and shall be eligible for reappointment.

1.2 The role and responsibilities of the Board and management

The Board’s primary role is to ensure the protection and enhancement of long-term shareholder (Government) value taking into account the interests of other stakeholders including employees, regulated entities, consumers of financial services, suppliers and the wider community. The Board is accountable to the shareholder for the performance of the Authority. It directs and monitors the business and affairs of the Authority on behalf of Government and is responsible for the Authority’s overall corporate governance. In particular, the Board’s responsibilities include:

13

FINANCIAL SERVICES REGULATORY AUTHORITY (FSRA) Annual Report 2018

CORPORATE GOVERNANCE REPORT - continued

approving the strategic objectives and direction of the Authority and overseeing management’s implementation of those strategic objectives;

monitoring the Authority’s operational per-formance generally including its financial state and the effectiveness of the Authority’s safety and sustainability strategy;

approving major expenditures, transactions, budgets, funding plans and capital management initiatives;

monitoring the integrity, effectiveness and consistency of the Authority’s risk management framework, controls and systems;

setting the overall remuneration framework for the Authority and overseeing executive succession planning;

appointing, assessing the performance and setting the remuneration of the CEO, as well as approving the appointment and remuneration of senior management and overseeing their performance;

influencing the corporate culture, ethical standards and reputation of the Authority; and

monitoring the effectiveness of the Authority’s governance practices including overseeing shareholder reporting and engagement as well as compliance with the Authority’s continuous disclosure obligations.

1.3 Skills and Diversity of the Board

As observed in the composition of the Board above, the Act stipulates the appropriate characteristics needed by the Board to maximise its effectiveness and the blend of skills, knowledge and experience necessary for the present and future needs of the Authority. Having a range of different skills, backgrounds, experience and diversity ensures a broad range of viewpoints which facilitates effective governance and decision making.

1.4 The Chairman

The Chairman, Mr Stephen Simelane, is an inde-pendent non-executive director. He has been an independent non-executive director and Chairman of the Authority since 2015. The Chairman’s

overarching responsibilities include:1 providing leadership for the Board, 2 facilitating the effective contribution of all

directors, 3 managing the dynamics of Board discussion, 4 setting the Board agenda and ensuring adequate

time is available for discussion on all agenda items on strategic issues.

5 The Chairman is also responsible for encou-raging constructive relations between directors and between Board and management and promoting the interests of the Authority with all key external stakeholders.

Importantly, the roles of Chairman and CEO of the Authority are not fulfilled by the same person.

1.5 The Board Secretary

The role of the Board Secretary rests with the CEO, as stipulated in the Act. The Board Secretary reports directly to the Board through the Chairman, and all directors have access to the Secretary. The Board Secretary’s role in respect of matters relating to the proper functioning of the Board includes: (a) advising the Board and its Committees on

governance matters, (b) monitoring that Board and Committee

policies and procedures are followed, (c) coordinating all Board business including

the timely despatch of Board and Committee papers,

(d) acting as a point of reference for dealings between the Board and management,

(e) sourcing and retaining independent profes-sional advisors as required,

(f ) helping to organise and facilitate the induction and professional development of directors, and

(g) ensuring proper compliance with relevant statu-tory requirements relating to the Authority’s operations.

1.6 Independence of Directors and Confidentiality Oath

Directors are expected to bring independent views and judgement to the Board’s deliberations. The Board recognises the special responsibility of

14

FINANCIAL SERVICES REGULATORY AUTHORITY (FSRA) Annual Report 2018

CORPORATE GOVERNANCE REPORT - continued

non-executive directors for monitoring executive management and providing independent views. Under the Board Charter, the Board must maintain majority non-executive directors and have a non-executive independent Chairman (with different persons filling the roles of Chairman and CEO).

The Board has determined that, in respect of the 2018 financial year, the Chairman and all non-executive directors are independent of executive management and free of any business or other relationship that could materially interfere with the exercise of unfettered and independent judgement or compromise their ability to act in the best interests of the Authority. The independence of each director is considered on a case by case basis from the perspective of both the Authority and the director. All directors have signed Declaration of Interest Form as well as a Confidentiality Oath.

1.7 Board meetings

The FSRA Act stipulates that the Board shall meet as often as the business of the Authority may require, but not less frequent than once in every two months. A quorum at a meeting shall be five members, including the Chief Executive Officer or

a person acting in that capacity. The Chairperson or, in the absence of the Chairperson, the Deputy Chairperson, shall chair a meeting for the Board. Except as otherwise provided in the Act, decisions of the Board shall be determined by a majority of members present and voting, and in the event of a tie, the person chairing that meeting shall have a casting vote in addition to the deliberative vote.

Directors receive comprehensive papers, via IBoards Software, in advance of the Board meetings. The utilisation of technology in dispatching Board Papers comes with great advantages, such as;

Significant reduction in the use of paper, since there’s no longer need to print bulk papers;

Significant savings in utilisation of ink; and Time savings, since no manpower time is

required to compile, bind and drive around delivering Board Papers.

The savings derived from using IBoards Technology far outweighs the cost of hardware, and software annual license. The Directors also receive regular updates in relation to key management reports, via Board Committees, which are then presented to the Main Board by the Committee Chairmen.

Stephen Simelane

Modern Samketi

Nathie Maseko

Amos Mkhat-shwa

Sabelo Mabuza

Ntsika Fakudze

Nkululeko Dlamini

Main Board 13/13 10/13 13/13 10/13 13/13 13/13 8/13

FAR n/a n/a n/a 13 / 13 12 / 13 n/a 9 / 13

REMCO n/a n/a 14 / 14 n/a 13 / 14 13 / 14 n/a

Legal n/a 5/5 n/a 4/5 n/a 4/5 n/a

The table below indicates the number of meetings conducted in the period 2017/2018

*FAR – Finance, Audit and Risk Committee*REMCO – Remunerations and Appointments Committee*Legal – Legal and Compliance Committee

Board remuneration is in accordance with rates published by the Public Enterprise Unit (PEU).

1.8 Conflict of Interest

Directors are required to avoid conflicts of interest and immediately inform their fellow directors

should a conflict of interest arise. Directors are also required to advise the Authority of any relevant interest that may result in a conflict.

The Board has adopted the use of formal declarations of interests that are tabled at Board meetings where directors disclose any new material

15

FINANCIAL SERVICES REGULATORY AUTHORITY (FSRA) Annual Report 2018

CORPORATE GOVERNANCE REPORT - continued

personal interests or if there is any change in the nature or extent of a previously disclosed interest. This includes a director’s appointment or retirement from boards of other companies. Where a matter in which a director has a material personal interest is being considered by the Board, that director must not be present when the matter is being considered or vote on the matter unless all of the directors have passed a resolution to enable that director to do so or the matter comes within a statutory exception.

1.9 Access to management, information and professional advice

All directors have unrestricted access to the senior executives and other employees of the Authority through the Chairman, or the CEO. Directors may seek briefings from senior executives outside the regular presentations made by senior executives at Board meetings.

Subject to prior consultation with the Chairman, each director may seek independent professional advice at the Authority’s expense to assist the director in the proper exercise of powers and discharge of duties as a director or as a member of a Board Committee. Pursuant to a deed executed by the Authority and each director, a director also has the right to have access to all documents which have been presented to meetings or made available to the Board or any Board Committee whilst in office, including materials referred to in those documents.

1.10 Board and executive performance and remuneration

The Board is committed to a performance culture and to ensuring that a range of formal processes are in place to evaluate the performance of the Board, Board Committees, each director and senior executives.

Management review

The non-executive directors are responsible for regularly evaluating the performance of the CEO

based on specific criteria including the Authority’s business performance, short- and long-term strategic objectives and the achievement of personal objectives that are approved annually.

All executives are subject to an annual performance review. These reviews, involve an executive being evaluated by their immediate superior by reference to their specific performance objectives for the year, including the completion of key performance indicators and contribution to specific business and company plans. This review is aligned to the Authority’s remuneration framework and is considered for, among other things, the purposes of determining any increases to fixed remuneration and outcomes under the Authority’s short term incentive plan.

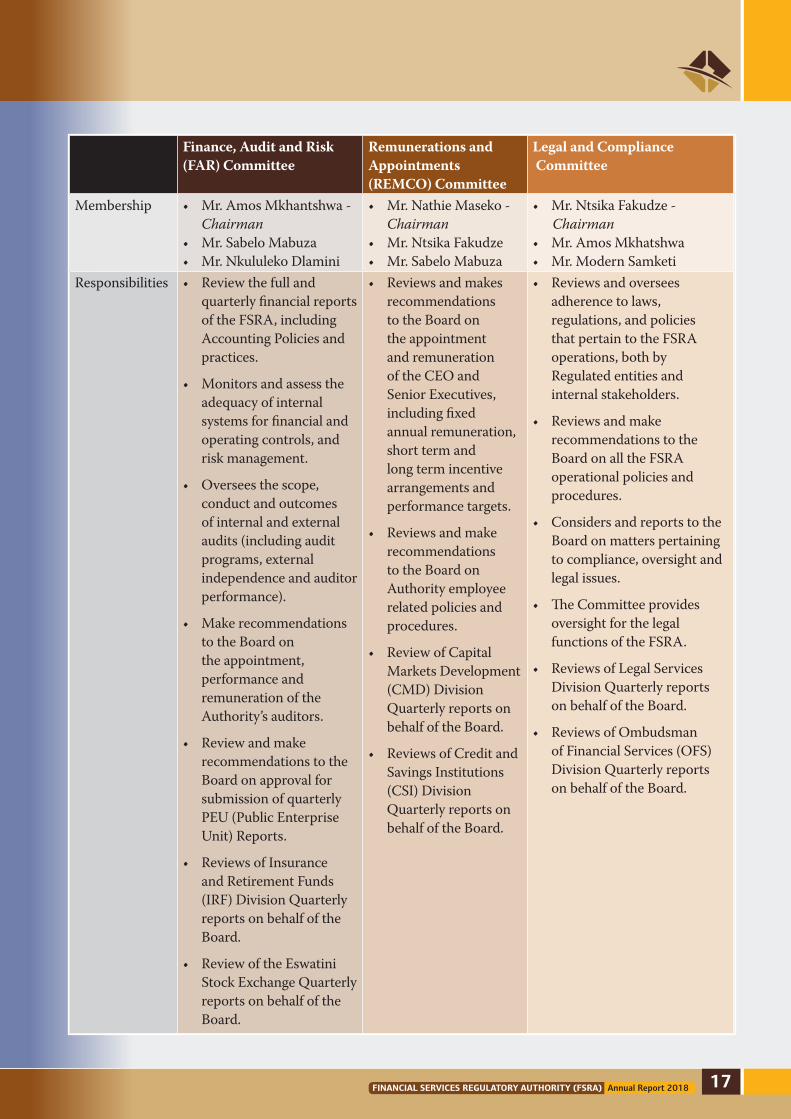

2. Our Board Committees The Board has three standing Committees that play an important role in assisting the Board perform its role and discharge its responsibilities. The following Committees assist the Board by focussing in more detail on specific areas of FSRA’s operations and governance framework: i. Finance, Audit and Risk (FAR) Committee; ii. Remunerations and Appointments Committee

(REMCO); iii. Legal and Compliance (LEGAL) Committee.

Separate charters were approved for each Commi-ttee. The Board Committees, generally, review matters on behalf of the Board and refer matters to the Board for decision with a recommendation from the Committee. The Committee papers, including minutes of meetings, are circulated to the Board members. Additionally, joint Committee meetings are convened where matters overlap and need Committees’ consensus before they are tabled to the main Board.

An overview of the membership, composition and responsibilities of each standing Committee as at the date of this statement is as follows:

16

FINANCIAL SERVICES REGULATORY AUTHORITY (FSRA) Annual Report 2018

Finance, Audit and Risk (FAR) Committee

Remunerations and Appointments (REMCO) Committee

Legal and Compliance Committee

Membership • Mr.AmosMkhantshwa-Chairman

• Mr.SabeloMabuza• Mr.NkululekoDlamini

• Mr.NathieMaseko-Chairman

• Mr.NtsikaFakudze• Mr.SabeloMabuza

• Mr.NtsikaFakudze- Chairman• Mr.AmosMkhatshwa• Mr.ModernSamketi

Responsibilities • Reviewthefullandquarterly financial reports of the FSRA, including Accounting Policies and practices.

• Monitorsandassesstheadequacy of internal systems for financial and operating controls, and risk management.

• Overseesthescope,conduct and outcomes of internal and external audits (including audit programs, external independence and auditor performance).

• Makerecommendationsto the Board on the appointment, performance and remuneration of the Authority’s auditors.

• Reviewandmakerecommendations to the Board on approval for submission of quarterly PEU (Public Enterprise Unit) Reports.

• ReviewsofInsuranceand Retirement Funds (IRF) Division Quarterly reports on behalf of the Board.

• ReviewoftheEswatiniStock Exchange Quarterly reports on behalf of the Board.

• Reviewsandmakesrecommendations to the Board on the appointment and remuneration of the CEO and Senior Executives, including fixed annual remuneration, short term and long term incentive arrangements and performance targets.

• Reviewsandmakerecommendations to the Board on Authority employee related policies and procedures.

• ReviewofCapitalMarkets Development (CMD) Division Quarterly reports on behalf of the Board.

• ReviewsofCreditandSavings Institutions (CSI) Division Quarterly reports on behalf of the Board.

• Reviewsandoverseesadherence to laws, regulations, and policies that pertain to the FSRA operations, both by Regulated entities and internal stakeholders.

• Reviewsandmakerecommendations to the Board on all the FSRA operational policies and procedures.

• ConsidersandreportstotheBoard on matters pertaining to compliance, oversight and legal issues.

• TheCommitteeprovidesoversight for the legal functions of the FSRA.

• ReviewsofLegalServicesDivision Quarterly reports on behalf of the Board.

• ReviewsofOmbudsmanof Financial Services (OFS) Division Quarterly reports on behalf of the Board.

CORPORATE GOVERNANCE REPORT - continued

17

FINANCIAL SERVICES REGULATORY AUTHORITY (FSRA) Annual Report 2018

3. Our Risk Management Practices

Effective assurance and risk management practices help the Authority to achieve its strategic objectives, ensure compliance with its legal obligations and protect the best interests of its stakeholders.

3.1 Integrity of Reporting

The Board and management have established controls that are designed to safeguard the company’s interests and the integrity of its reporting. These include accounting, financial reporting, and other internal control policies and procedures which are directed at monitoring whether the Authority complies with approved policies.

In accordance with standards set by the Board, prior to approval of its financial statements, the Finance, Audit and Risk Committee reviews and provides assurance to the Board that, having made appropriate enquiries, in their opinion;

The financial records of the FSRA have been properly maintained; and

The financial statements comply with the appropriate accounting standards and gives a true and fair view of the financial position and performance of the Authority.

In addition, comprehensive practices have been adopted, in compliance with the Public Procurement Act, to require that:

Capital expenditure, transactions and other commitments above a certain size obtain CEO and Board approval (as required under the Authority’s formal delegation of authority).

Business transactions are properly authorised and executed.

The Authority’s financial statements are subject to an external audit by an independent auditor. The FSRA currently engages PricewaterhouseCoopers (PwC) as its independent external auditors. In accordance with PEU requirements, the Authority is expected to rotate /reappoint Auditors every three years.

The Finance, Audit and Risk Committee is responsible for overseeing the audit process on behalf of the Board.

3.2 Risk Identification and Management

The Board is still in the process of establishing policies for the oversight and management of material business risks and internal controls. The Finance, Audit and Risk Committee has been mandated to oversee the development of policies, internal controls and procedures that the FSRA will use to identify business and regulatory risks. The design and implementation of the risk management and internal controls systems to manage the Authority’s business risks is the responsibility of management.

4. Our Code of Ethics

The FSRA regards integrity and high ethical standards on the part of all its employees as non-negotiable. For that reason, the Authority has adopted a code of ethics and conduct outlining its commitment to society, regulated entities, suppliers and its stakeholders. Employees are required to:a) Desist from involving themselves in any form of

dishonesty.b) Be loyal to the employer, promote its interests

and assist it to achieve its purpose and goals and all business decisions must be made in the best interest of the employer.

c) Perform their duties diligently and in the most effective and efficient manner.

d) Desist from misusing their position to obtain personal benefits on terms which are not available to the general public.

e) Act honestly with integrity at all times towards colleagues, the employer and members of the public.

f) Obtain the employer’s approval before hand if they wish to work for or be associated with another organisation or business where there is conflict with the employer’s business.

g) Not waste the employer’s time, money, or other resources.

h) Not give confidential information about the employer, stakeholders or employees to any other person, or make improper use of it.

i) Use the appropriate channels for making known grievances or complaints they may have.

The FSRA does not tolerate any corrupt or dishonest practice such as bribery and corruption. Employees shall not directly or indirectly request, accept, offer, or grant a personal advantage in connection with a business activity, regardless of whether the other party to the transaction is an individual, company or a government agency.

CORPORATE GOVERNANCE REPORT - continued

18

FINANCIAL SERVICES REGULATORY AUTHORITY (FSRA) Annual Report 2018

CORPORATE GOVERNANCE REPORT - continued

GENERAL OVERVIEW OF THE ECONOMY- ECONOMY OVERVIEW

A small, landlocked kingdom, Eswatini is bordered in the north, west and south by the Republic of South Africa and by

Mozambique in the east. Eswatini depends on South Africa for 60% of its exports and for more than 90% of its imports. Eswatini’s currency is pegged to the South African Rand, effectively relinquishing Eswatini’s monetary policy to South Africa. The government is dependent on customs duties from the Southern African Customs Union (SACU) for 49% of revenue; income tax accounts for 27% and a valued added tax for 19% of revenues. Eswatini is a lower middle income country, but its income distribution is highly skewed, with an estimated 20% of the population controlling 80% of the nation’s wealth.

Subsistence agriculture employs approximately 70% of the population. The manufacturing sector diversified in the 1980s and 1990s, but manufacturing has grown little in the last decade. Sugar and soft drink concentrate are the largest foreign exchange earners. Mining has declined in importance in recent years. Coal, gold, diamond, and quarry stone mines are small scale, and the only iron ore mine closed in 2014. With an estimated 28% unemployment rate, Eswatini’s need to increase the number and size of small and medium enterprises and to attract foreign direct investment is acute. On 1 January 2015, Eswatini lost its eligibility for benefits under the US African Growth and Opportunity Act after failing to meet benchmarks relating to workers’ rights.

19

FINANCIAL SERVICES REGULATORY AUTHORITY (FSRA) Annual Report 2018

The IMF forecasted that Eswatini’s economy will grow at a slower pace in 2017 because of a region-wide drought, which is likely to hurt Eswatini’s revenue from sugar exports and other agricultural products; tourism and transport sectors will also decline. Overgrazing, soil depletion, drought, and floods are persistent problems. Eswatini’s revenue from SACU receipts also are projected to decline in 2017, making it harder for the government to maintain fiscal balance.

Captured from the Minister’s Budget Speech

In March 2018, the Minister of Finance delivered the 2018/2019 Budget Speech. The following write-up is captured from the Minister’s Speech for the benefit of our readers. The Minister highlighted that the widening of the budget deficits without adequate financing is exerting pressures on the domestic economy. Government spending continues to outpace its ability to raise enough revenues resulting in cash flow challenges and accumulation of arrears. The 7 cash flow challenges experienced in 2016/17 continued into 2017/18, and this has negatively affected local businesses. It is therefore, very important that Government restores fiscal sustainability to ensure macroeconomic stability and unlock the country’s potential to place growth on a higher growth path. Increased government recurrent expenditure in the context of severely diminished SACU revenue largely explains the deterioration in the fiscal balance. The widening deficit poses risks to sound public debt management and government’s ability to meet its statutory obligations.

RECENT ECONOMIC PERFORMANCE AND

OUTLOOK

The economic developments, which affected the domestic economy are highlighted as follows.

i) International Developments

The global economy continued to strengthen in 2017. The IMF estimated that global output increased by 3.7 percent in 2017, up from the 3.2 percent estimate for 2016. All major economies across the world contributed to strong growth,

notably, economies in Asia and Europe performed better than initially expected. The 2017 growth for emerging markets and developing countries was 4.7 percent, while advanced economies grew by 2.3 percent.

Global output is expected to maintain the upward momentum experienced in the last two years. Global growth is expected to increase by 3.9 percent annually in 2018 and 2019, respectively. It is expected that this would result in a surge in global investment that will particularly benefit large exporting countries. Furthermore, the U.S. tax reforms are expected to temporarily increase growth in the U.S., an effect that will spill-over to its major trading partners.

ii) Regional Developments

Sub-Saharan Africa grew at a slower pace when compared to other emerging and developing regions in 2017 with GDP growth estimated at 2.7 percent. However, this growth was stronger than the growth rate of 1.4 percent that the region experienced in 2016. The GDP growth rates varied significantly among countries in the region. Oil exporting countries grew at much lower rates relative to non-oil exporting countries mainly due to low oil prices. As these countries continue to recover, growth in the region overall is expected to continue to pick up into 2018 and 2019, at 3.3 percent and 3.5 percent respectively. The South African economy was affected by structural bottlenecks that constrained growth in 2017. The IMF estimates indicate that South Africa’s economy grew by 0.9 percent in 2017 which will be maintained in 2018 and 2019 respectively.

iii) Domestic Developments

Real GDP Growth

The domestic economy is projected to have grown by 1.9 percent in 2017 from 1.4 percent in 2016 mainly benefiting from a faster recovery in crop production on both Swazi Nation Land and individual tenure farms. Maize and sugarcane production in particular, returned to pre-drought production levels. As a result, crop production grew by 17.2 percent in 2017. However, the

ECONOMY REVIEW - continued

20

FINANCIAL SERVICES REGULATORY AUTHORITY (FSRA) Annual Report 2018

livestock population was significantly reduced due to the drought, leading to low output in 2017. Furthermore, there has been a decline in the construction sector as implementation of various construction projects slowed largely due to the current fiscal challenges. On balance, both the primary and secondary sectors grew by 0.7 percent in 2017. The tertiary sector led output growth in 2017, with a projected growth rate of 2.7 percent driven mainly by the wholesale, retail, and the financial services sub sectors.

Economic performance in 2018 is anticipated to be 1.3 percent, followed by an increase to over

2 percent per year in the medium term as the primary and secondary sectors gain from the full recovery of the agriculture sector. The negative risks surrounding the current fiscal challenges will need to be managed effectively to mitigate the impact on growth. In the tertiary sector, growth will be driven by the demand for services to support developments in the primary and secondary sectors.

Inflation

Inflationary pressures eased in 2017 following a tighter monetary policy stance and recovery.

Month 31-Mar-2018 31-Mar-2017 31-Mar-2016 31-Mar-2015 31-Mar-2014April 7,8 8,5 4,9 5,3 5,6May 7,1 8,0 5,4 5,5 5,5June 6,9 7,5 5,7 5,3 5,6July 6,7 7,4 4,9 6,2 6,0August 5,9 8,0 4,8 6,0 5,9September 5,4 8,3 4,5 6,2 5,7October 5,4 8,2 4,6 6,3 4,7November 4,9 8,6 4,5 6,6 4,4December 4,7 8,7 4,9 6,2 4,4January 4,6 8,2 5,6 5,6 4,7February 4,0 6,8 7,3 5,0 4,7March 4,0 6,0 7,8 4,7 5,1Annual Average 5,6 7,9 5,4 5,7 5,2

Eswatini Inflation Trends for the Past Five Years

AprilM

ayJu

neJu

ly

August

Septe

mber

October

November

Decem

ber

Januar

y

Febru

ary

Mar

ch

INFL

ATIO

N R

ATE

S

10,0

9,0

8,0

7,0

6,0

5,0

4,0

3,0

2,0

1,0

0,0

8,5

7,0

5,65,34,9

8,0

7,1

5,45,5

7,5 7,48,0

8,3 8,28,6 8,7

8,2

7,36,8

5,04,74,0 4,0

4,75,1

6,0

7,0

5,6

4,74,6

6,2

4,94,74,4

6,6

4,94,54,4

6,3

5,44,74,6

6,25,75,4

4,5

5,95,96,0

4,8

6,76,26,0

4,9

6,9

5,75,65,3

31-Mar-14 31-Mar-15 31-Mar-16 31-Mar-17 31-Mar-18

Eswatini Inflation Trends for the Past Five Years

ECONOMY REVIEW - continued

21

FINANCIAL SERVICES REGULATORY AUTHORITY (FSRA) Annual Report 2018

Inflation figures over the past 5 years show a drastic decline in inflation rates. When looking at the current financial year alone, inflation rate was 8.5% in April 2017, and closed with 4% on 31 March 2018. The decline in the inflation rate means that the price of Eswatini goods are increasing at a slower rate than before, and because the trend has remained almost flat from month to month, it means prices will change less frequently, and firms can spend less time and energy updating prices. When inflation falls to a very low rate, then real interest rates can be higher than predicted. This increases the real debt burden of citizens and can lead to slower economic growth.

Balance of Payments

Preliminary figures indicate that the current account recorded a surplus of E8.6 billion in 2017, however, declining from the E9.5 billion registered in 2016. Our export earnings in 2017 amounted to E24.1 billion, showing a marginal decline of 1.3 percent compared to the E24.4 billion in 2016. The financial account posted a deficit of E7.2 billion in 2017 from a surplus of

E8.5 billion in 2016. The deficit in the financial account was due to a net decline in Foreign Direct Investment coupled with net increases in foreign portfolio assets and “other investment” assets.

Real Gross domestic product in constant prices growth rate

In 2018, real GDP growth for Eswatini was 0.2%. Though Eswatini real GDP growth fluctuated substantially in recent years, it tended to decrease through 1999 - 2018 period ending at 0.2 % in 2018.

What is real GDP growth?

Real GDP growth represents annual percentage growth rate of GDP at market prices, based on constant local currency. GDP is the sum of gross value added by all resident producers in the economy plus any product taxes and minus any subsidies not included in the value of the products. It is calculated without making deductions for depreciation of fabricated assets or for depletion and degradation of natural resources.

ECONOMY REVIEW - continued

22

PE

RC

EN

TAG

E

20

17.5

15

12.5

10

7.5

5

2.5

0

-2.5

-51980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016 2018

ESWATINI REAL GDP GROWTH

FINANCIAL SERVICES REGULATORY AUTHORITY (FSRA) Annual Report 2018

ECONOMY REVIEW - continued

CEO’S REVIEW- STRATEGIC REVIEW

D uring the year under review, the FSRA embarked on its Strategy development exercise. The Authority aims to achieve

its strategic goals within the strategic period of 1 April 2018 to 31 March 2021.

Our Mission is to be an effective regulator, which is supported by harmonised legislation, efficient processes, and operating in a low risk environment by 2021.

Strategic Focus Areas

In order to ensure relevance of the FSRA to its stakeholders, we developed three (3) strategic focus areas, namely:

High performance organisation Risk responsive environment Conducive Legislation

STRATEGIC PROJECTS

HighPerformanceOrganisation

Risk ResponsiveEnvironment

ConduciveLegislation

23

FINANCIAL SERVICES REGULATORY AUTHORITY (FSRA) Annual Report 2018

CEO’s REVIEW - continued

1

PROJECT

To integrate our core processes to effectively regulate and supervise the financial services industry.

2

PROJECT

To achieve a working environment that attracts and retains people who reflect the values of the FSRA.

3

PROJECT

To create a low risk financial service provider environment for effective supervision.

4

PROJECT To have a harmonised regulatory framework that will

enable the FSRA to effectively regulate and supervise the financial sector.

STRATEGIC PROJECTS

To achieve the above focus areas, we have identified four strategic projects:

At the FSRA, the Board of Directors owns the strategy, while the Executive team executes it. Our plan is to achieve our strategic goals, within a strategic period, which will begin on 01 April 2018, and will end on 31 March 2021. In so doing, we aim to fully develop our systems and infrastructure, within this time frame. We will achieve this goal, through the strategic programmes, and process targets, as set out in the Strategy document.

Prior to crafting our strategy, we first defined our core business process. This gave us a nodal point from where we could analyse our strengths; weaknesses; opportunities; and threats. In our task to regulate and supervise financial services within Eswatini, a precis of our core process is as follows:

24

FINANCIAL SERVICES REGULATORY AUTHORITY (FSRA) Annual Report 2018

CEO’s REVIEW - continued

From this process, the FSRA’s primary concern is to licence and monitor financial services providers. Moreover, where problems or conflicts arise, the Authority must remedy such to ensure that the financial system of Eswatini is safe and stable. This is our primary task. To support this task, the Authority must also continuously manage good relations with our stakeholders, and we must review and propose legislation that will enable this task.

To express the Authority’s primary task, we have created a mission that will enable our processes, and a vision that will drive our strategy. And to understand this task, we have created a process construct that clearly indicates how our core processes interact with each other. Further to this, we have also developed values that will direct our behaviour.

To drive our strategy, we have created a strategic ladder that we refer to as the V5 system. This system will show how we aim to achieve our ultimate vision; and, it also indicates what our super goal is, for this strategic period.

To put our mission, and vision into action, we pose four strategic programmes, and ten operational targets. We view our strategic programs, as the non-repetitive action that we must take, to stay relevant. We run and measure these programmes

through project management methods. Our operations, on the other hand, are the repetitive action that we must take to perform efficiently. To measure these operations, we have created core targets. Also, we have quantified these targets so that they show the capacity with which we aim to run our processes. Therefore, we have split our strategic initiative from our current operational action. To measure and monitor our strategy we have created a strategic scorecard where we can view our progress without effort.

To stay relevant, we have opted to engage in a rolling strategy, as opposed to a static one. This means that our goal will stay permanent, but that we will engage in different projects to achieve this goal. These projects have different durations, and will be completed at different time intervals. And if our stakeholders demand so, we will close current projects, and engage in new ones. Our three-year goal is to be an effective regulator, which is supported by harmonised legislation; efficient processes; and operating in a low risk environment by 2021. We will do what it takes to achieve this. Whilst we complete our strategic programmes, we will constantly work to achieve our operational process targets. In this way we will stay relevant, whilst we optimally perform.

Stakeholder Relations

Legislative Review

License Monitor Remedy

25

FINANCIAL SERVICES REGULATORY AUTHORITY (FSRA) Annual Report 2018

CHIEF EXECUTIVE OFFICER’S REVIEW - continued

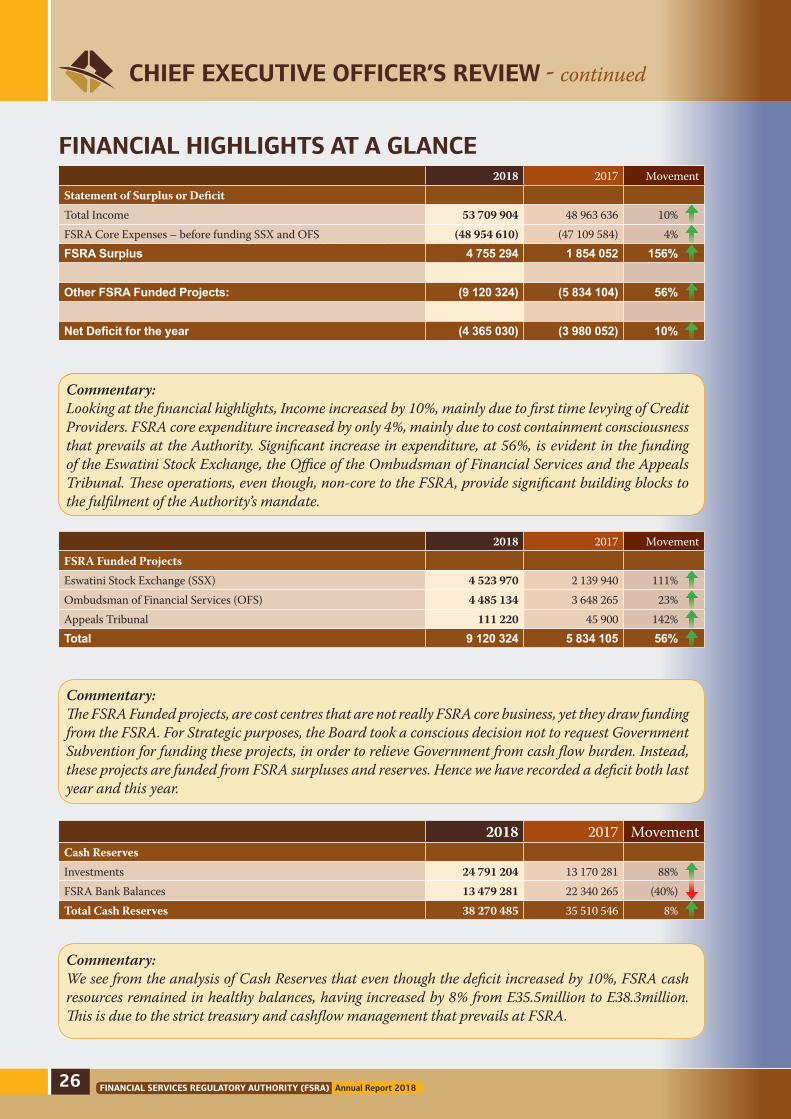

FINANCIAL HIGHLIGHTS AT A GLANCE

2018 2017 MovementFSRA Funded ProjectsEswatini Stock Exchange (SSX) 4 523 970 2 139 940 111%Ombudsman of Financial Services (OFS) 4 485 134 3 648 265 23%Appeals Tribunal 111 220 45 900 142%Total 9 120 324 5 834 105 56%

2018 2017 MovementCash ReservesInvestments 24 791 204 13 170 281 88%FSRA Bank Balances 13 479 281 22 340 265 (40%)Total Cash Reserves 38 270 485 35 510 546 8%

2018 2017 MovementStatement of Surplus or DeficitTotal Income 53 709 904 48 963 636 10%FSRA Core Expenses – before funding SSX and OFS (48 954 610) (47 109 584) 4%FSRA Surplus 4 755 294 1 854 052 156%

Other FSRA Funded Projects: (9 120 324) (5 834 104) 56%

2018 2017 MovementStatement of Surplus or DeficitTotal Income 53 709 904 48 963 636 10%FSRA Core Expenses – before funding SSX and OFS (48 954 610) (47 109 584) 4%FSRA Surplus 4 755 294 1 854 052 156%

Other FSRA Funded Projects: (9 120 324) (5 834 104) 56%

Net Deficit for the year (4 365 030) (3 980 052) 10%

Commentary:Looking at the financial highlights, Income increased by 10%, mainly due to first time levying of Credit Providers. FSRA core expenditure increased by only 4%, mainly due to cost containment consciousness that prevails at the Authority. Significant increase in expenditure, at 56%, is evident in the funding of the Eswatini Stock Exchange, the Office of the Ombudsman of Financial Services and the Appeals Tribunal. These operations, even though, non-core to the FSRA, provide significant building blocks to the fulfilment of the Authority’s mandate.

Commentary:The FSRA Funded projects, are cost centres that are not really FSRA core business, yet they draw funding from the FSRA. For Strategic purposes, the Board took a conscious decision not to request Government Subvention for funding these projects, in order to relieve Government from cash flow burden. Instead, these projects are funded from FSRA surpluses and reserves. Hence we have recorded a deficit both last year and this year.

26

Commentary:We see from the analysis of Cash Reserves that even though the deficit increased by 10%, FSRA cash resources remained in healthy balances, having increased by 8% from E35.5million to E38.3million. This is due to the strict treasury and cashflow management that prevails at FSRA.

FINANCIAL SERVICES REGULATORY AUTHORITY (FSRA) Annual Report 2018

CHIEF EXECUTIVE OFFICER’S REVIEW - continued

27

Operating Highlights

Since the FSRA was founded in 2006 (first as the Office of the Registrar of Insurance and Retirement Funds (RIRF)), we’ve seen first hand the speed and breadth of change in the Financial Services Sector. We have learned the importance of adaptability. As a matter of operating philosophy, we seek to make continuous improvement an integral part of our organisational culture.

That is why, across the Authority, we are accele-rating the development of systems and processes, capabilities and solutions for our stakeholders, especially our regulated entities and consumers of financial services products. In so doing, we believe we can improve the way we approach regulation and deliver regulatory value to all stakeholders.

Human Capital

Our people are at the heart of what we do, and we recognise that our investment in them, along with instilling a positive culture, leads to better business outcomes. That is why the authority and Board has spent quality time during the year, reviewing the Staff terms and conditions of service, as well all other staff related policies as follows:

Recruitment and Selection Policy and Procedure; Education, Training and Development

Policy and Procedure; Health and Safety Policy and Procedure Code of Ethics; Disciplinary Code and Procedure; Incapacity Counselling Policy and

Procedure; Grievance Procedure; Sexual Harassment Policy and

Procedure.

In the year under review, we continued to implement a range of initiatives to support a culture that values performance, innovation, professional development, flexibility and wellbeing.

Manager Development Programmes

At FSRA, we recognise that effective leadership is key to building a positive culture and strong employee engagement, so in the year under review, all our Managers successfully enrolled and graduated for Manager Development Programmes offered by Wits Business School and Stellenbosch Business School.

Encouraging Lateral Movement

As an integrated business, and as a retention strategy, the FSRA offers huge scope for people to make lateral moves within the Authority whenever vacancies become available. A few staff members took advantage of this opportunity during the year.

Employee Engagement

Measuring our employee engagement gives the Authority a valuable insight into the quality of our workplace and culture, and helps us to better understand how we can continue to create a positive work environment for our people.

During the year under review, and as part of our employee engagement objective, an employee survey was conducted. The results of some of the variables that were measured are demonstrated in the charts below:

Personal Growth

Question 1. What attracted them to join the FSRA?

Most participants cited opportunities for growth as the attracting factor to the organisation. 35% of the respondents mentioned they were attracted by the potential of growth opportunities and/or career advancement for themselves. The industry and organisational culture of the Authority follows at 28% and 14%, respectively. A relatively small 3% of the respondent cited passion as an attraction to the FSRA. Overall, the response generated were positive for this question.

FINANCIAL SERVICES REGULATORY AUTHORITY (FSRA) Annual Report 2018

Question 2. How happy are you with working for the FSRA?

Generally, FSRA employees are happy. 50% of the respondents indicated that they are happy whilst only over 6.7% are very happy. 23.3% of the respondents are somewhat happy. When combined these figures display an 80% level of contentment with working for the FSRA

compared to a paltry 20% of unhappy and somewhat unhappy respondents. There is a positive ambience amongst personnel of the Authority and it can be concluded that the staff morale is high. Literature review suggest that the level of happiness of employees is directly linked to their productivity. Figure 2 shows a graphical representation of the happiness level of the Authority’s employees.

CHIEF EXECUTIVE OFFICER’S REVIEW - continued

FIGURE 1: MAIN ATTRACTING FACTORS

FIGURE 2: HAPPINESS LEVEL OF RESPONDANTS

Salary3%

Nature of Work 10%

Industry 28%

Organisational Culture 14%

Position3%

Growth Opportunities/

Career Advancement

35%

Happy50%

Great Team7%

Very Happy7%

Unhappy10%

Somewhat Unhappy

10%

Somewhat Happy

23%

28

FINANCIAL SERVICES REGULATORY AUTHORITY (FSRA) Annual Report 2018

From the chart above you can deduce that there is a small clique of employees who are unhappy, and this represent a small fraction of the Authority employees. With the necessary retention, wellness strategies or policies such can be changed.

Question 3. Do you feel you receive adequate training to help you in your scope of work?

The Education and Training policy clearly spells out the terms of training to be afforded to employees of the Authority. As per the respondent’s views, 46.7% feel they receive adequate training whilst a slightly less 33.3% feel the training provided is inadequate in helping them in their scope of work. 20 % of the respondents elected to remain neutral.

Since the Authority spends over 10% of its entire budget on conferences and training, it is apparent that emphasis have been placed on the importance of continuous development. However, by virtue of the 33.3% who feel they receive inadequate training there needs to be an even balance on how the training provided is structured and evaluated for effectiveness.

Emphasis should be placed on upskilling junior or entry officers in order to fully develop their skills. In essence, training employees will reinforce their sense of value. The nature of training availed by the Authority could achieve employee satisfaction and a higher retention rate for the Authority. Below is a chart representation of the respondent’s responses.

Employee Satisfaction

Question 4. Is there anything in particular that you like most about working here?

From the below chart we can deduce that the nature of job is what employees like most about

working here at the FSRA. The nature of work at 68% is an important component in the retention of employees. The respondents mentioned training, experience and exposure, opportunity of career advancement which are factors that the Authority must ensure are availed going forward.

CHIEF EXECUTIVE OFFICER’S REVIEW - continued

FIGURE 3: ADEQUATE TRAINING BAROMETER

Yes 47%

May be20%

No33%

29

FINANCIAL SERVICES REGULATORY AUTHORITY (FSRA) Annual Report 2018

FIGURE 5: RESPONDANTS ON WHAT THEY LIKE MOST ABOUT WORKING FOR THE AUTHORITY

FIGURE 6: MOTIVATIONAL FACTORS TO GO ABOVE YOUR SCOPE OF WORK

CHIEF EXECUTIVE OFFICER’S REVIEW - continued

Question 5: What can motivate you to go above and beyond your scope of work here at the FSRA?

Simply said, most employees require increased pay for them to go above and beyond their scope of work. 93% of the respondent answered this question. A lesser

percentage just require recognition for work done which can serve as motivation enough for them. It is crucial that supervisors and managers understand the importance of showing appreciation to one’s work. A simple thank you or well done means a lot to an employee.

Nature ofWork68%

Perks8%

Staff and Relations

22%

MonetaryIncentives

49%

Recognition31%

Growth, Trainingand Environment

20%

30

FINANCIAL SERVICES REGULATORY AUTHORITY (FSRA) Annual Report 2018

CHIEF EXECUTIVE OFFICER’S REVIEW - continued

Compensation

Question 6. Hypothetically, if you were to resign / leave FSRA tomorrow what would be the main reason?

This was the crux of the survey. The main reason solicited here is a factor and forms the basis of

which the retention strategy ought to address. 97% of the respondents attempted this question. The two main factors cited as reason for leaving the Authority were dissatisfaction with pay and career advancement. See below a chart of the results.

Evidently, the two main factors contributing to employee turnover is the lack of career advancement / promotion and dissatisfaction with pay. These two are inter-related. Career advancement or promotion comes with an improved pay whilst dissatisfaction with pay is self-explanatory. Combined this adds up to 72.4% of monetary related hence it being the

two absolute factors for employees resigning or leaving FSRA. It seems the Authority needs to timely address or adjust the pay scale. The Authority should also consider creating growth opportunities for its employees. The good news is that the Board has already commissioned a Job Evaluation and Salary review exercise in response to the high turnover problem.

FIGURE 7: MAIN REASON FOR RESIGNING OR LEAVING THE AUTHORITY’S EMPLOY

Dissatisfaction with benefits package

4%

Career advancement/promotion

41%

Dissatisfaction with pay

39%

Dissatisfaction with Management

3%

Nature of job/job satisfaction

4%

Insufficient Challenge4%

Work environment

3%

UnsolicitedOffer 4%

31

FINANCIAL SERVICES REGULATORY AUTHORITY (FSRA) Annual Report 2018

Information and Communication Technology (ICT)

Bank Supervision Application (BSA) System

In order to improve the usage of the Electronic Regulatory System (BSA) by the regulated entities and FSRA staff, the Authority received a two weeks training from a BSA Consultant, Mr. Samuel Mwale from the Reserve Bank of Zimbabwe. The training was also meant to sensitise staff on the features of the new version of BSA, version 4.0 and what to expect from it and to further enable them to use the current version to produce the reports needed on the non-bank financial sector when needed.

Legislative Highlights

SACCO Bill, 2018

The leading consultant who had been engaged to develop the SACCO Policy and the SACCO Bill returned to the country to present both documents to the industry and other stakeholders. Mr. Dave Grace from Dave Grace and Associates conducted a stakeholder workshop on 28 February 2018 at Royal Villas where the SACCO policy and Bill were discussed extensively, and a lot of progress was made. The deadlines for sending comments and reviews on these documents was 14 March 2018. These were incorporated into the final draft of the SACCO Bill which is currently with the Microfinance Unit: Centre for Financial Inclusion (CFI).

Insurance (Amendment) Regulations

The Authority has drafted the Insurance (Amendment) Regulations which aim to increase the local investment criteria for insurers from 30% to 50%. The amendments were sent to the industry for comments and the industry was given the 9th February 2018 as the deadline for submission of comments. Comments received are now being incorporated into the final draft regulations.

The amendments apply to both the short-term and the long-term insurers.

Retirement Funds (Amendment) Regulations

The Authority has drafted the Retirement Funds (Amendment) Regulations. These regulations aim to increase the local investment criteria for retirement funds from 30% to 50%. The regulations were sent to the industry for comments and the industry was given the 9th February 2018 as the deadline for submission of comments. Comments received are being incorporated into the final draft rules regulations

Building Societies (Amendment Bill)

The object of the Bill is to amend the Building Societies Act, 1962 in order to provide for the conversion of a Building Society into a Company incorporated in terms of the Companies Act, 2009, and to provide for incidental matters. The Authority has received the copy of the Bill and is in the process of compiling comments to the Bill for onward transmission to the Ministry of Finance.

Securities Exchange Rules 2018

The Authority is involved in the drafting and finalising the Securities Exchange Rules 2018. The rules are expected to come into operation on the 1 April 2018.

Local, Regional and International Cooperation

Local CooperationMoU with the National Industrial Corporation of Eswatini (NIDCS)

The Authority has received a request from the National Industrial Corporation of Eswatini (NIDCS) to enter into a Memorandum of Understanding (MoU). The objective of NIDCS is to contribute to the sustainable economic development through investing

CHIEF EXECUTIVE OFFICER’S REVIEW - continued

32

FINANCIAL SERVICES REGULATORY AUTHORITY (FSRA) Annual Report 2018

in projects that are economically and financially viable. The parties to the MOU will collaborate and cooperate with each other in supporting fund raising initiatives for economically viable projects.

Participation in Financial Sector Development Implementation Plan

The FSRA is part of the Financial Sector Development Implementation Plan (FSDIP). During the year under review working group meetings were held and FSRA staff members participated in the meetings.

Anti-Money Laundering National Risk Assessment (NRA)

The FSRA also participates in the NRA by reviewing the regulated sectors’ exposure to money laundering and the controls that the sector has in place to mitigate their exposure and vulnerability to money laundering. As at 31 March 2018, the Authority had submitted a draft report on our sector’s exposure to money laundering to the AML Task Force.

International Cooperation

IMF First Initiative Technical Assistance

During the year under review, the FSRA received the approval of Technical Assistance, themed IMF- First Initiative Strengthening the Supervision of the NBFIs.

The purpose of the technical assistance (TA) project is to develop the capacity of the FSRA to effectively regulate and supervise the non-bank financial institutions (NBFIs) sector in Eswatini, with a view to ensuring its stability and that of the entire financial system.

In more specific terms, the aim of the proposed project is to assist the FSRA to achieve its mandate, in accordance with the Financial Services Regulatory Authority Act, 2010 (FSRA Act) of ensuring the soundness and stability of the NBFI sector by enhancing risk-focused supervision in three industry

subsectors: insurance and retirement funds (IRFs); capital market institutions (CMIs); and credit and savings institutions (CSIs).

Through ensuring the stability of the NBFI sector, the project also aims to lay the basis for the further development of the sector and contribute to expanding financial inclusion in Eswatini, and in that context, it is closely aligned with Eswatini’s Financial Sector Development Implementation Plan (FSDIP) 2017 – 2019. It is intended that the project will support the FSRA to implement its component of the FSDIP.

IOSCO (International Organisation of Securities Commissions) Self-Assessment

Following the admission of the FSRA as an Associate member of IOSCO, the IMF is assisting the FSRA to achieve ordinary membership status. The FSRA self-assessment with the 38 IOSCO principles is still in progress and a final report is due to be presented to the Assessment committee in December 2018.

Participation in the IAIS (International Association of Insurance Supervisors) Accounting and Audit Working Group

The Authority has deployed a staff member who actively participates in the mandate of the IAIS Accounting and Audit Working Group (AAWG). The AAWG is responsible for: The IAIS’ external relationships with Account-

ing and Auditing bodies around the world. Monitoring relevant developments in inter-

national accounting, auditing, financial reporting or valuation requirements and in public disclosures made by insurers and more widely.

Preparing comment letters and other papers to external bodies in relation to the above, for approval by the Policy Development Committee.

Developing, updating or providing input into the development or updating of IAIS high-level principles-based supervisory and supporting material relevant to:o accounting of insurance companies;

CHIEF EXECUTIVE OFFICER’S REVIEW - continued

33

FINANCIAL SERVICES REGULATORY AUTHORITY (FSRA) Annual Report 2018

o auditing of insurance companies;o valuation for solvency purposes;o audit assurance required for information provided to insurance supervisors;o reporting to supervisors; ando public disclosures of insurers.

Looking Ahead

The major highlight when looking ahead will impact the Insurance Companies in as far as changes in International Financial Reporting Standards for Insurance Accounting is concerned. On 18 May 2017, the International Accounting Standards Board (IASB or Board) issued IFRS 17 Insurance Contracts (The Standard). The Standard will be first applied for reporting periods starting on or after 1 January 2022. IFRS 17 represents the most significant change to Insurance Accounting requirements in over 20 years – it demands a complete overhaul of insurers’ financial statements.

This major change to implement IFRS 17 will extend beyond the finance and actuarial functions of insurers — with a large impact across Data, Systems and Processes (DSP). Its business impacts need to be understood and communicated to a wide range of internal and external stakeholders. Given the scale of this change, investors and other stakeholders will want to understand the likely impact as early as possible. Different jurisdictions around the globe are busy preparing for the implementation of IFRS 17. The FSRA will be initiating an urgent action plan for Eswatini and SADC Committee of Insurance, Securities, and Non-Bank Financial Authorities towards the preparation for implementation of IFRS 17.

RECOMMENDED ACTION PLAN

1. Organise Internal IFRS 17 training for all Insurance regulatory staff to sensitise them on extensive reporting changes coming with the Standard.

2. Design (at CISNA level) a survey targeting to receive responses from Insurance Companies, Actuaries, and Auditors on level of awareness of the standard and preparatory work being done on the ground.

3. Conduct compulsory extensive regional trainings focusing on getting Insurers, Actuaries, and auditors up to speed with IFRS 17.

4. At FSRA design IFRS compliant reporting returns forms, in conjunction with Capital Adequacy Requirements forms.

5. Recommend an IFRS 17 Working group for CISNA to track progress by member countries.

SANDILE DLAMINI (MR)

Chief Executive Officer

CHIEF EXECUTIVE OFFICER’S REVIEW - continued

34

FINANCIAL SERVICES REGULATORY AUTHORITY (FSRA) Annual Report 2018

FACTS AND FIGURES - DASHBOARDCHIEF EXECUTIVE OFFICER’S REVIEW - continuedN

ON

-BA

NK

ING

FIN

AN

CIA

L IN

STIT

UT

ION

S vs

TO

TAL

FIN

AN

CIA

L SY

STE

M A

SSE

TS

AS

AT

31

MA

RC

H

20

1820

1720

1620

1520

14G

DP

Estim

ate

55 2

70 0

00 0

0061

740

000

000

56 2

18 9

05 4

72 5

4 92

0 40

2 82

0

53 5

80 8

80 8

00

NO

N-B

ANK

ING

FIN

ANC

IAL

INST

ITU

TIO

NS

(NBF

Is)

67 4

78 5

89 3

7663

086

959

423

59 4

21 1

77 8

07 4

9 85

0 49

6 25

6 4

5 43

8 61

0 58

1

EXC

LUD

ING

CIS

– A

SSET

S U

ND

ER M

AN

AG

EMEN

T 41

712

031

265

39 7

40 5

23 5

0336

439

203

478

30 3

59 7

51 2

8228

493

615

553

Retir

emen

t Fun

ds28

145

849

255

27 2

63 8

77 1

0625

550

918

962

22

319

605

062

20

442

962

359

Lo

ng te

rm In

sura

nce

3 90

8 63

3 63

33

724

220

329

3 30

4 42

6 11

4

2 5

67 7

05 1

86

2

359

953

026

Sh

ort t

erm

insu

ranc

e91

0 15

5 08

399

5 86

1 77

461

9 29

3 20

7

28

3 79

8 03

4

29

7 44

8 16

8 Ca

pita

l Mar

kets

Inst

itutio

ns35

1 67

5 29

435

1 67

5 29

431

2 78

7 19

5D

ATA

NO

T Y

ET C

OLL

ECT

EDCo

llect

ive I

nves

tmen

t Sch

emes

(CIS

) – A

UM

/AUA

25 7

66 5

58 1

1123

346

435

920

22 9

81 9

74 3

29 1

9 49

0 74

4 97

4

16 9

44 9

95 0

28

SACC

Os

1 46

8 00

3 00

01

318

164

000

1 17

8 58

1 00

0

75

2 62

4 00

0

1 0

23 8

07 0

00

Cred

it on

ly in

stitu

tions

4 57

1 14

3 00

03

859

288

000

3 49

1 96

0 00

0

2 6

44 4

71 0

00

2

643

597

000

Bu

ildin

g So

ciet

ies

2 35

6 57

2 00

02

227

437

000

1 98

1 23

7 00

0

1 7

91 5

48 0

00

1

725

848

000

CO

MM

ERC

IAL

AN

D D

EVEL

OPM

ENT

BA

NK

S21

500

000

000

18 3

00 0

00 0

0015

800

000

000

12

770

591

000

13

437

973

000

FIN

AN

CIA

L R

EGU

LATO

RS

10 1

85 3

44 2

1810

184

844

769

10 2

52 7

65 8

24

9 41

3 94

5 80

1

9 26

6 11

9 93

9 Ce

ntra

l Ba

nk o

f Es

wat

ini (

CBS

)10

128

352

000

10 1

28 3

52 0

0010

192

107

000

9

366

311

000

9 2

23 4

78 0

00

Fina

ncia

l Ser

vice

s Reg

ulat

ory A

utho

rity (

FSRA

)56

992

218

56 4

92 7

6960

658

824

47

634

801

42

641

939

TOTA

L FI

NA

NC

IAL

SYST

EM99

163