financial statements year ended october 31, 2015 · these financial statements for the year ended...

TRANSCRIPT

Vision Credit Union Ltd.Financial Statements

Year Ended October 31, 2015

Independent Auditor's Report

To the Members of Vision Credit Union Ltd.

Report on the Financial Statements

We have audited the accompanying financial statements of Vision Credit Union Ltd., which comprise the statementof financial position as at October 31, 2015 and the statements of income and comprehensive income, changes inmembers' equity and cash flows for the year then ended, and a summary of significant accounting policies andother explanatory information.

Management's Responsibility for the Financial Statements

Management is responsible for the preparation and fair presentation of these financial statements in accordancewith International Financial Reporting Standards, and for such internal control as management determines isnecessary to enable the preparation of financial statements that are free from material misstatement, whether dueto fraud or error.

Auditor's Responsibility

Our responsibility is to express an opinion on these financial statements based on our audit. We conducted ouraudit in accordance with Canadian generally accepted auditing standards. Those standards require that we complywith ethical requirements and plan and perform the audit to obtain reasonable assurance about whether thefinancial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in thefinancial statements. The procedures selected depend on the auditor's judgment, including the assessment of therisks of material misstatement of the financial statements, whether due to fraud or error. In making those riskassessments, the auditor considers internal control relevant to the entity's preparation and fair presentation of thefinancial statements in order to design audit procedures that are appropriate in the circumstances, but not for thepurpose of expressing an opinion on the effectiveness of the entity's internal control. An audit also includesevaluating the appropriateness of accounting policies used and the reasonableness of accounting estimates madeby management, as well as evaluating the overall presentation of the financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our auditopinion.

Opinion

In our opinion, the financial statements present fairly, in all material respects, the financial position of Vision CreditUnion Ltd. as at October 31, 2015 and its financial performance and its cash flows for the year then ended inaccordance with International Financial Reporting Standards.

Edmonton, AlbertaDecember 12, 2015 CHARTERED ACCOUNTANTS

2

Vision Credit Union Ltd.Statement of Income and Comprehensive Income

Year Ended October 31, 2015

2015 2014

($Thousands)Interest income

Member loans $ 30,567 $ 25,887Investments 1,890 2,028

32,457 27,915

Interest expenseMember deposits 5,385 4,882

Financial margin 27,072 23,033

Other income (expense)Other income 4,959 4,202Provision for credit losses (Note 5) (151) (94)

4,808 4,108

Operating expensesPersonnel 9,969 8,419Administration 5,822 5,228Member security 1,287 968Occupancy 1,274 1,092Organization 397 306

18,749 16,013

Income before ProfitShare allocation & income taxes 13,131 11,128

ProfitShare allocation 8,627 7,292

Income before income taxes 4,504 3,836

Income taxes (Note 8)Current 774 760Deferred 230 76

1,004 836

Net income and comprehensive income for the year 3,500 3,000

See notes to financial statements

4

Vision Credit Union Ltd.Statement of Changes in Members' Equity

Year Ended October 31, 2015

Membershares

ProfitShareallocation

Retainedearnings Total

($Thousands)Balance, October 31, 2013 $ 43,956 $ 8,100 $ 34,500 $ 86,556

Net income and comprehensiveincome - - 3,000 3,000

Acquisition of Caisse HorizonCredit Union Ltd. 3,002 - 6,659 9,661

Accrual for the redemption ofCaisse Horizon Credit UnionLtd. shares (442) - - (442)

Issuance of member shares 8,101 (8,100) - 1Redemption of member shares (4,788) - - (4,788)ProfitShare allocation - 7,292 - 7,292

Balance, October 31, 2014 49,829 7,292 44,159 101,280

Net income and comprehensiveincome - - 3,500 3,500

Issuance of member shares 7,294 (7,292) - 2Redemption of member shares (5,286) - - (5,286)ProfitShare allocation - 8,627 - 8,627

Balance, October 31, 2015 $ 51,837 $ 8,627 $ 47,659 $ 108,123

See notes to financial statements

5

Vision Credit Union Ltd.Statement of Cash Flows

Year Ended October 31, 2015

2015 2014

($Thousands)Operating activities

Net income and comprehensive income for the year $ 3,500 $ 3,000Items not affecting cash:

Amortization 1,134 754Deferred taxes 230 76ProfitShare allocation 8,627 7,292

13,491 11,122

Changes in non-cash working capital:Income taxes payable (166) (50)Other assets (37) 274Accounts payable and accrued liabilities (167) 826

(370) 1,050

13,121 12,172

Investing activitiesPurchase of property and equipment, and intangible assets (2,052) (2,243)Proceeds on disposal of property and equipment 208 -Net assets acquired through business combinations - 29,165Net change in member loans receivable and accrued interest (81,052) (72,532)Net change in foreclosed properties held for resale 316 (80)Net sale of investments 19,459 27,228

(63,121) (18,462)

Financing activitiesNet change in member deposits and accrued interest 30,016 30,969Member shares issued 2 1Redemption of member shares (5,286) (4,788)

24,732 26,182

Increase (decrease) in cash flow (25,268) 19,892

Cash and cash equivalents - beginning of year 42,945 23,053

Cash and cash equivalents - end of year $ 17,677 $ 42,945

Cash flows supplementary informationInterest received $ 32,229 $ 27,298

Interest paid $ 5,444 $ 4,322

Income taxes paid $ 940 $ 810

See notes to financial statements

6

Vision Credit Union Ltd.Notes to Financial StatementsYear Ended October 31, 2015

1. Reporting entity information

Entity information

Vision Credit Union Ltd. (the "Credit Union") is incorporated under the Credit Union Act of the Province ofAlberta, and is the result of a business combination between Battle River Credit Union Ltd. and Caisse HorizonCredit Union Ltd. on May 1, 2014.

The Credit Union operates sixteen credit union branches and serves members in Camrose, Peace River, andthe surrounding areas. The address of the Credit Union's registered office is 5007 - 51st Street, Camrose,Alberta, T4V 1S6.

The Credit Union Deposit Guarantee Corporation ("CUDGC"), a Provincial Corporation, guarantees therepayment of all deposits with Alberta credit unions, including accrued interest. The Credit Union Act providesthat the Province will ensure that the Corporation carries out this obligation.

Statement of compliance

These financial statements have been prepared in accordance with International Financial ReportingStandards ("IFRS") as issued by the International Accounting Standards Board ("IASB").

Basis of measurement

These financial statements for the year ended October 31, 2015 were recommended for approval andauthorized for issue by the Board of Directors on December 12, 2015.

The financial statements have been prepared on the historic cost basis except for financial assets andfinancial liabilities classified as available for sale or as fair value with gains or losses included in the statementof income and comprehensive income.

Functional and presentation currency

These financial statements are presented in Canadian dollars, which is the functional currency of the CreditUnion.

2. Significant accounting policies

Cash and cash equivalents

Cash and cash equivalents comprise cash on hand, the current account with Credit Union Central AlbertaLimited (operating as "Alberta Central") and items in transit and are recorded at amortized cost on thestatement of financial position. These items are highly liquid financial assets with maturities of three monthsor less from the acquisition date and are used by the Credit Union in the management of short-termcommitments.

(continues)

7

Vision Credit Union Ltd.Notes to Financial StatementsYear Ended October 31, 2015

2. Significant accounting policies (continued)

Investments

Central deposits and shares

Alberta Central term deposits are accounted for as loans and receivables at amortized cost, adjusted torecognize other than a temporary impairment in the underlying value. Alberta Central shares are classified asavailable for sale and are initially recognized at fair value. There is no separately quoted market value forthese shares and the fair value could not be measured reliably. Fair value cannot be measured reliably as thetiming of redemption of these shares cannot be determined, therefore, the range of reasonable fair valueestimates is significant and the probabilities of the various estimates cannot be reasonably assessed.Therefore, they are recorded at cost.

Portfolio investments

Investments, including Concentra Financial debentures and other shares and investments, are valued initiallyat fair value, adjusted to recognize other than a temporary impairment in the underlying value. Investmentsare purchased with the intention to hold them to maturity, or until market conditions cause alternativeinvestments to become more attractive. Investments in equity investments that do not have a quoted marketprice in an active market are estimated to be equal to cost.

Member loans receivable

Loans are initially recognized at their fair value and subsequently measured at amortized cost. Amortized costis calculated as the loans' principal amount, less any allowance for anticipated losses, plus accrued interest.Interest revenue is recorded on the accrual basis using the effective interest method. Loan administration feesare amortized over the term of the loan using the effective interest method. The effective interest rate is therate that exactly discounts the estimated future cash receipts through the expected life of the financial asset tothe carrying amount of the financial asset.

Foreclosed properties held for resale are carried at the lower of the amortized cost of the loan or mortgagesforeclosed, adjusted for revenues received and cost incurred subsequent to foreclosure, and the estimated netproceeds from the sale of assets.

Impairment of financial assets

The Credit Union assesses at each reporting date whether there is objective evidence that a financial asset orgroup of financial assets, other than a financial asset held at fair value through profit or loss, is impaired. Afinancial asset or group of financial assets is considered to be impaired only if there is objective evidence thatone or more events that occurred after the initial recognition of the asset(s) has had a negative effect on theestimated future cash flows of that asset and the impact can be reliably estimated.

The Credit Union first assesses whether objective evidence of impairment exists for assets that are individuallysignificant and collectively for assets that are not individually significant. If management determines that noobjective evidence of impairment exists for an individually assessed asset, the asset is assessed collectively ingroups that share similar credit risk characteristics.

(continues)

8

Vision Credit Union Ltd.Notes to Financial StatementsYear Ended October 31, 2015

2. Significant accounting policies (continued)

Member loans

The Credit Union maintains an allowance for specific and collective credit losses on member loans, which areestablished as a result of reviews at an individual loan and loan portfolio level.

A specific allowance is recognized by reviewing the creditworthiness of the individual borrowers and the valueof the collateral underlying the loan.

The amount of the allowance is measured as the difference between the loan’s carrying amount and thepresent value of estimated future cash flows discounted for fixed rate loans at the loan’s original effectiveinterest rate and for variable rate loans at the effective rate at the time of impairment. Cash flows arising fromthe recovery and sale of collateral are included, whether or not foreclosure is probable. The carrying amountof the loan is reduced through the use of an allowance account and the amount of the loss is recognized withinthe provision for credit loss expense in the statement of income and comprehensive income.

Where individual loans are not considered to be specifically impaired, they are placed into groups of loanswith similar risk profiles and collectively assessed for losses that have been incurred but not yet identified.

A collective allowance is established where the Credit Union has identified objective evidence that losses inthe loan portfolio have been incurred, but for which a specific provision cannot yet be determined. Thecollective allowance is based on observable data including the current portfolio delinquency profile, historicloss experience and management’s evaluation of other conditions existing at the reporting date which are notreflected in historical trends. Changes in the collective allowance account are recognized within the provisionfor credit loss expense in the statement of income and comprehensive income.

The methodology and assumptions used are reviewed regularly to reduce any differences between lossestimates and actual loss experience. Changes in assumptions used could result in a change in the allowancefor loan losses and have a direct impact on the provision for credit loss expense in the statement of incomeand comprehensive income.

Following impairment, interest income is recognized using the original effective rate of interest. This rate isthen used to discount the future cash flows for the purpose of measuring the potential impairment loss. If, in asubsequent period, the amount of the impairment loss decreases and the decrease can be related objectivelyto an event occurring after the impairment was recognized, the previously recognized impairment loss isreversed by adjusting the specific or general allowance. The amount of the reversal is recognized within theprovision for credit losses in the statement of income and comprehensive income.

The Credit Union writes off amounts charged to the allowance account against the carrying value of animpaired loan when there is no realistic prospect of future recovery and all collateral has been realised. TheCredit Union seeks to work with the members to bring their accounts to a current status before takingpossession of collateral.

(continues)

9

Vision Credit Union Ltd.Notes to Financial StatementsYear Ended October 31, 2015

2. Significant accounting policies (continued)

Other financial assets

For assets measured at amortized cost, an impairment loss is calculated as the difference between itscarrying amount, and the present value of the estimated future cash flows discounted at the original effectiveinterest rate. An impairment loss in respect of an available-for-sale financial asset held at cost is calculatedas the difference between its carrying value and the present value of estimated future cash flows discounted atthe current market rate of return for a similar asset.

All impairment losses are recognized in the statement of income and comprehensive income. An impairmentloss is reversed if the reversal can be related objectively to an event occurring after the impairment loss wasrecognized. For financial assets measured at amortized cost, the reversal is recognized in the statement ofincome and comprehensive income. Reversals of impairments are not recognized for available-for-salefinancial assets that are measured at cost.

Property and equipment

Property and equipment are stated at cost less accumulated amortization and impairment losses. Costincludes expenditures that are directly attributable to the acquisition of the asset. When parts of an item ofproperty and equipment have different useful lives, they are accounted for as separate items of property andequipment.

Amortization is provided using the following methods and rates intended to amortize the cost of the assetsover their estimated useful lives:

Buildings 10-40 years straight-line methodComputer hardware 3-10 years straight-line methodFurniture and equipment 3-20 years straight-line methodParking lot 14-25 years straight-line method

The useful lives of items of property and equipment are reviewed on a regular basis and the useful life isaltered if estimates have changed significantly. Gains or losses on disposal of property and equipment aredetermined as the difference between the net disposal proceeds and the carrying amount of the asset, and arerecognized in the statement of income and comprehensive income as other operating income or otheroperating costs, respectively.

Intangible assets

Intangible assets consist of certain acquired and internally developed banking software. Intangible assets arecarried at cost, less accumulated amortization and accumulated impairment losses, if any. Input costsdirectly attributable to the development or implementation of the asset are capitalized if it is probable thatfuture economic benefits associated with the expenditure will flow to the Credit Union and the cost can bemeasured reliably.

Intangible assets available for use are amortized on a straight-line basis over their useful lives (which hasbeen estimated to range from 3 years to 15 years). The method of amortization and the useful lives of theassets are reviewed annually and adjusted if appropriate.

There are no indefinite life intangible assets.

(continues)

10

Vision Credit Union Ltd.Notes to Financial StatementsYear Ended October 31, 2015

2. Significant accounting policies (continued)

Investment property

Investment property consists of land and a building in High Prairie where the Credit Union previously operateda branch. The building is now being rented. The land and building were initially recorded at cost, and afterrecognition the Credit Union has the choice to either use the fair value model or the cost model to account forits investment property. The Credit Union has chosen the cost model to account for its investment property, inwhich IAS 16 then applies.

Investment property is stated at cost less accumulated amortization and impairment losses. Cost includesexpenditures that are directly attributable to the acquisition of the asset.

Amortization is provided using the following methods and rates intended to amortize the cost of the investmentproperty over its estimated useful life:

Buildings 40 years straight-line method

The useful life of investment property is reviewed on a regular basis and the useful life is altered if estimateshave changed significantly. Gains or losses on disposal of investment property are determined as thedifference between the net disposal proceeds and the carrying amount of the asset, and are recognized in thestatement of income and comprehensive income as other operating income or other operating costs,respectively.

Impairment of non-financial assets

At the end of each reporting period, the Credit Union reviews the carrying amounts of its tangibleand intangible assets to determine whether there is any indication that those assets have suffered animpairment loss. If any such indication exists, the recoverable amount of the asset is estimated in order todetermine the extent of the impairment loss (if any). Where it is not possible to estimate the recoverableamount of an individual asset, the Credit Union estimates the recoverable amount of the cash-generatingunits (“CGU”) to which the asset belongs. Where a reasonable and consistent basis of allocation can beidentified, corporate assets are also allocated to individual CGU’s, or otherwise they are allocated to thesmallest group of CGU’s for which a reasonable and consistent allocation basis can be identified. Intangibleassets with indefinite useful lives and intangible assets not yet available for use are tested for impairment atleast annually, and whenever there is an indication that the asset may be impaired.

Recoverable amount is the higher of fair value less costs to sell and value in use. In assessing value in use,the estimated future cash flows are discounted to their present value using a pre-tax discount rate that reflectscurrent market assessments of the time value of money and the risks specific to the asset for which theestimates of future cash flows have not been adjusted.

If the recoverable amount of an asset or CGU is estimated to be less than its carrying amount, the carryingamount of the asset or CGU is reduced to its recoverable amount. An impairment loss is recognizedimmediately in the statement of income and comprehensive income.

Where an impairment loss subsequently reverses, the carrying amount of the asset or CGU is increased to therevised estimate of its recoverable amount, but so that the increased carrying amount does notexceed the carrying amount that would have been determined had no impairment loss been recognized forthe asset or CGU in prior years. A reversal of an impairment loss is recognized immediately in the statementof income and comprehensive income.

Accounts payable and accrued liabilities

Accounts payable are initially recorded at fair value and are subsequently carried at amortized cost, whichapproximates fair value due to the short term nature of these liabilities.

(continues)

11

Vision Credit Union Ltd.Notes to Financial StatementsYear Ended October 31, 2015

2. Significant accounting policies (continued)

Member deposits

Member deposits are initially recognized at fair value net of transaction costs directly attributable to issuanceand are subsequently measured at amortized cost using the effective interest method.

Member shares

Shares are classified as liabilities or member equity in accordance with their terms. Sharesredeemable at the option of the member, either on demand or on withdrawal from membership, are classifiedas liabilities. Shares redeemable at the discretion of the Credit Union board of directors are classified asequity. Shares subject to regulatory restriction are accounted for using the criteria set out in IFRIC 2 Members'Shares in Cooperative Entities and Similar Instruments.

Revenue recognition

Revenue is recognized to the extent that it is probable that the economic benefits will flow to the Credit Unionand the revenue can be reliably measured. The following specific recognition criteria must also be met beforerevenue is recognized.

Interest income is recognized in the statement of income and comprehensive income for all financial assetsmeasured at amortized cost using the effective interest rate method. The effective interest rate is the rate thatdiscounts estimated future cash flows through the expected life of the financial instrument back to the netcarrying amount of the financial asset. The application of the method has the effect of recognizing revenue ofthe financial instrument evenly in proportion to the amount of outstanding over the period to maturity orrepayment.

Investment income is recognized as interest is earned on interest-bearing investments, and when dividendsare declared on shares.

Commissions and fees that are considered an integral part of the effective interest rate are included in themeasurement of the effective interest rate. Commissions and fees that are not an integral part of the effectiveinterest rate, including insurance commissions and mortgage prepayment penalties are recognized as incomewhen charged to the members.

Account service charges are recognized as income when charged to the members.

Income taxes

Current tax and deferred tax are recognized in profit or loss except to the extent that the tax is recognizedeither in other comprehensive income or directly in equity, or the tax arises from a business combination.

Current tax assets and liabilities for the current and prior periods are measured at the amount expected to berecovered from or paid to the taxation authorities. The calculation of current tax is based on the tax rates andtax laws that have been enacted or substantively enacted by the end of the reporting period.

Deferred tax assets and liabilities are measured at the tax rates that are expected to apply to the period whenthe assets are realized or the liabilities are settled. The calculation of deferred tax is based on the tax ratesand tax laws that have been enacted or substantively enacted by the end of the reporting year. Deferred taxassets are recognized to the extent that it is probable that future taxable profit will be available against whichthe temporary differences can be utilized.

(continues)

12

Vision Credit Union Ltd.Notes to Financial StatementsYear Ended October 31, 2015

2. Significant accounting policies (continued)

Deferred tax assets and liabilities are recognized where the carrying amount of an asset or liability differs fromits tax base, except for taxable temporary differences arising on the initial recognition of goodwill andtemporary differences arising on the initial recognition of an asset or liability in a transaction which is not abusiness combination and at the time of the transaction affects neither accounting or taxable income.

Recognition of deferred tax assets for unused tax losses, tax credits and deductible temporary differences isrestricted to those instances where it is probable that future taxable profit will be available which allows thedeferred tax asset to be utilized. Deferred tax assets are reviewed at each reporting date and are reduced tothe extent that it is no longer probable that the related tax benefit will be realized.

Foreign currency translation

Transaction amounts denominated in foreign currencies are translated into their Canadian dollar equivalentsat exchange rates prevailing at the transaction dates. Carrying values of monetary assets and liabilities reflectthe exchange rates at the year end date. Translation gains and losses are recognized in the statement ofincome and comprehensive income for the current period.

Financial instruments

Financial assets and financial liabilities, including derivatives, are recognized on the statement of financialposition when the Credit Union becomes a party to the contractual provisions of a financial instrument or non-financial derivative contract. The Credit Union recognizes financial instruments at the trade date. All financialinstruments are initially measured at fair value. Subsequent measurement is dependent upon the financialinstrument’s classification. Transaction costs relating to financial instruments designated as fair value throughprofit or loss are expensed as incurred. Transaction costs for other financial instruments are capitalized oninitial recognition.

The financial instruments classified as fair value through profit or loss are measured at fair value withunrealized gains and losses recognized in the statement of income and comprehensive income.

Available for sale financial assets are measured at fair value with unrealized gains and losses recognized inother comprehensive income. The Credit Union classifies its shares in Alberta Central as available for sale.

The financial assets classified as loans and receivables are initially measured at fair value, then subsequentlycarried at amortized cost using the effective interest method less any accumulated impairment losses. Loansand receivables include cash and cash equivalents, term deposits, accounts receivable and members' loansand accrued interest.

Other financial liabilities are initially measured at fair value, then subsequently carried at amortized cost.Accounts payable and accrued liabilities and member deposits and accrued interest are classified as otherfinancial liabilities.

De-recognition of financial assets

De-recognition of a financial asset occurs when:

l The Credit Union does not have rights to receive cash flows from the asset;

l The Credit Union has transferred its rights to receive cash flows from the asset or has assumed anobligation to pay the received cash flows in full without material delay to a third party under a “pass-through" arrangement; and either:

l The Credit Union has transferred substantially all the risks and rewards of the asset, or

(continues)

13

Vision Credit Union Ltd.Notes to Financial StatementsYear Ended October 31, 2015

2. Significant accounting policies (continued)

l The Credit Union has neither transferred nor retained substantially all the risks and rewards of theasset, but has transferred control of the asset.

When the Credit Union has transferred its rights to receive cash flows from an asset or has enteredinto a pass-through arrangement, and has neither transferred or retained substantially all of the risksand rewards of the asset nor transferred control of the asset, the asset is recognized to the extent that theCredit Union’s continuing involvement in the asset, in that case, the Credit Union also recognizes anassociated liability. The transferred asset and the associated liability are measured on a basis that reflects therights and obligations that the Credit Union has retained.

A financial liability is derecognized when the obligation under the liability is discharged, cancelled or expires.Where an existing financial liability is replaced by another from the same lender on substantially differentterms, or the terms of the existing liability are substantially modified, such an exchange or modification istreated as a derecognition of the original liability and the recognition of a new liability, and the difference inthe respective carrying amount is recognized in the statement of income and comprehensive income.

Comprehensive income (loss)

Comprehensive income (loss) includes all changes in equity of the Credit Union, except those resulting frominvestments by members and distributions to members. Comprehensive income is the total of net income andother comprehensive income. Other comprehensive income comprises revenues, expenses, gains and lossesthat, in accordance with International Financial Reporting Standards, require recognition, but are excludedfrom net income. The Credit Union does not have any items giving rise to other comprehensive income, nor isthere any accumulated balance of other comprehensive income. All gains and losses, including those arisingfrom measurement of all financial instruments, have been recognized in the statement of income andcomprehensive income for the year.

New IFRS standards and interpretations not applied

Certain new standards have been published that are mandatory for the Credit Union's accounting periodsbeginning on or after October 31, 2015 or later periods that the Credit Union has decided not to early adopt.The new IFRS standards not yet applied include:

IFRS 7 Financial Instruments: Disclosures

This amendment aligns with the deferral of the effective date of IFRS 9. Instead of requiring restatement ofcomparative financial statements, entities are either permitted or required to provide modified disclosures ontransition from IAS 39 to IFRS 9 on the basis of the entity's date of adoption and if the entity chooses torestate prior periods. The amendment is effective for annual periods beginning on or after January 1, 2015.

IFRS 9 Financial Instruments

The new standard is the first phase of the project to replace IAS 39 Financial Instruments: Recognition andMeasurement. The standard simplifies the current financial asset classifications contained in IAS 39 bycreating two classifications – amortized cost and fair value. In addition the standard will require that allequity instruments are measured at fair value. The new standard has a mandatory effective date for periodsbeginning on or after January 1, 2018, with earlier application permitted. The second and third phases of theproject dealing with financial asset impairment and hedging remain in development and so the full impact ofthe standard on the Credit Union will be unknown until the completion of the project.

(continues)

14

Vision Credit Union Ltd.Notes to Financial StatementsYear Ended October 31, 2015

2. Significant accounting policies (continued)

IFRS 15 Revenue from Contracts with Customers

IFRS 15 is based on the core principle to recognize revenue to depict the transfer of goods or servicesto customers in an amount that reflects the consideration to which the entity expects to be entitled in exchangefor those goods or services. IFRS 15 focuses on the transfer of control. IFRS 15 replaces all of the revenueguidance that previously existed in IFRSs. The effective date for IFRS 15 is January 1, 2017, with earlierapplication permitted.

IAS 1 Presentation of Financial Statements

The amendments to IAS 1 are a part of a major initiative to improve disclosure requirements in IFRS financialstatements. The amendments clarify the application of materiality to note disclosure and the presentation ofline items in the primary statements provide options on the ordering of financial statements and additionalguidance on the presentation of other comprehensive income related to equity accounted investments. Theeffective date for these amendments is January 1, 2016, with earlier application permitted.

3. Significant accounting judgments, estimates and assumptions

As the precise determination of many assets and liabilities is dependent upon future events, the preparation offinancial statements for a period necessarily involves the use of estimates and approximations which havebeen made using careful judgment. These estimates are based on management's best knowledge of currentevents and actions that the Credit Union may undertake in the future. The resulting accounting estimates will,by definition, seldom equal the resulted actual results, and actual results may ultimately differ from theseestimates.

Allowance for impaired loans

The Credit Union reviews its individually significant loans at each reporting date to assess whether animpairment loss should be recognized. In particular, judgment by management is required in the estimation ofthe amount and timing of future cash flows when determining the impairment loss.

In estimating these cash flows, the Credit Union makes judgments about the borrower’s financial situation andthe net realizable value of collateral. These estimates are based on assumptions about a number of factorsand actual results may differ, resulting in future changes to the allowance.

Member loans receivable that have been assessed individually and found not to be impaired and allindividually insignificant loans are then assessed collectively, in groups of assets with similar riskcharacteristics, to determine whether provision should be made due to incurred loss events for which there isobjective evidence but whose effects are not yet evident. The collective provision assessment takes account ofdata from the loan portfolio such as credit quality, delinquency, historical performance and industry economicoutlook. The impairment loss on member loans receivable is disclosed in more detail in Note 5.

Financial instruments not traded on active markets

For financial instruments not traded in active markets, fair values are determined using valuation techniquessuch as the discounted cash flow model that rely on assumptions that are based on observable active marketsor rates. Certain assumptions take into consideration liquidity risk, credit risk and volatility.

(continues)

15

Vision Credit Union Ltd.Notes to Financial StatementsYear Ended October 31, 2015

3. Significant accounting judgments, estimates and assumptions (continued)

Impairment of non-financial assets

At each reporting date, the Credit Union assesses whether there are any indicators of impairment for non-financial assets. Non-financial assets that have an indefinite useful life or are not subject to amortization, suchas goodwill, are tested annually for impairment. Other non-financial assets are tested for impairment if thereare indicators that their carrying amounts may not be recoverable.

Income taxes

The Credit Union periodically assesses its liabilities and contingencies related to income taxes for all yearsopen to audit based on the latest information available. For matters where it is probable that an adjustmentwill be made, the Credit Union records its best estimate of the tax liability including the related interest andpenalties in the current tax provision. Management believes that they have adequately provided for theprobable outcome of these matters; however, the final outcome may result in a materially different outcomethan the amount included in the tax liabilities.

4. Cash and cash equivalents2015 2014

Cash held with Alberta Central, including items in transit $ 14,310 $ 39,899Cash on hand 3,367 3,046

$ 17,677 $ 42,945

16

Vision Credit Union Ltd.Notes to Financial StatementsYear Ended October 31, 2015

5. Member loans

2015

RecordedLoans

SpecificAllowance

CollectiveAllowance

Net CarryingValue

Gross ImpairedLoans

($Thousands)Agricultural 137,461 - 5 137,456 -Commercial 160,909 338 259 160,312 1,000Consumer 77,331 102 69 77,160 147Residential 352,076 14 176 351,886 229

727,777 454 509 726,814 1,376

Accrued interest 3,763 - - 3,763 4

731,540 454 509 730,577 1,380

2014

RecordedLoans

SpecificAllowance

CollectiveAllowance

Net CarryingValue

Gross ImpairedLoans

($Thousands)Agricultural 122,251 10 10 122,231 16Commercial 132,935 226 212 132,497 350Consumer 73,273 178 132 72,963 213Residential 318,670 105 138 318,427 229

647,129 519 492 646,118 808

Accrued interest 3,407 - - 3,407 5

650,536 519 492 649,525 813

Loan allowance details

2015 2014

($Thousands)Balance, beginning of year $ 1,011 $ 874Less: Accounts written off, net of recoveries (199) 81

812 955Provision for impaired loans 151 56

Balance, end of year $ 963 1,011

(continues)

17

Vision Credit Union Ltd.Notes to Financial StatementsYear Ended October 31, 2015

5. Member loans (continued)

Loans past due but not impaired

A loan is considered past due when a counterparty has not made a payment by the contractual due date.The table that follows presents the carrying value of loans at year end that are past due but not classified asimpaired because they are either i) less than 60 days past due, or ii) fully secured and collection efforts arereasonably expected to result in repayment.

2015

30-59 days 60-89 days90 days and

greater Total

($Thousands)Agricultural 403 - - 403Commercial 508 - 837 1,345Consumer 621 8 5 634Residential 1,067 119 537 1,723

2,599 127 1,379 4,105

2014

30-59 days 60-89 days90 days and

greater Total

($Thousands)Agricultural 167 6 361 534Commercial 608 - 280 888Consumer 166 25 193 384Residential 677 229 559 1,465

1,618 260 1,393 3,271

The principal collateral and other credit enhancements the Credit Union holds as security for loans include (i)insurance, mortgages over residential lots and properties, (ii) recourse to business assets such as realestate, equipment, inventory and accounts receivable, (iii) recourse to commercial real estate propertiesbeing financed, and (iv) recourse to liquid assets, guarantees and securities. Valuations of collateral areupdated periodically depending on the nature of the collateral. The Credit Union has policies in place tomonitor the existence of undesirable concentration in the collateral supporting its credit exposure. Inmanagement's estimation, the fair value of the collateral is sufficient to offset the risk of loss on the loanspast due but not impaired.

18

Vision Credit Union Ltd.Notes to Financial StatementsYear Ended October 31, 2015

6. Investments2015 2014

($Thousands)Held to maturity

Term deposits held with Alberta Central $ 93,820 $ 103,770Other 9,517 16,785Accrued interest 159 284

103,496 120,839Available for sale

Alberta Central common shares 8,500 8,172Other investments 3,543 5,984Accrued interest 4 7

12,047 14,163

$ 115,543 $ 135,002

As required by the Credit Union Act, the Credit Union holds investments in Alberta Central to maintain itsliquidity level.

Term deposits held with Alberta Central earn interest at rates ranging from 0.48% to 0.69%. The term depositmaturities range from November 2015 to December 2015.

Term deposits and Guaranteed Investment Certificates ("GICs") included in other above earn interest at ratesranging from 2.01% to 2.25%. The term deposit maturities range from May 2015 to April 2018.

Other investments above also include corporate bonds, mortgage pools and debentures held with variousfinancial institutions.

7. Other assets2015 2014

($Thousands)Prepaid expenses $ 209 $ 174Accounts receivable 3 1

$ 212 $ 175

19

Vision Credit Union Ltd.Notes to Financial StatementsYear Ended October 31, 2015

8. Income taxes

The total provision for income taxes in the statement of income and comprehensive income is at a ratediffering from the combined federal and provincial statutory income tax rates for the following reasons:

2015 2014

Combined federal and provincial statutory income tax rates 48.50 % 48.00 %Reduction for Credit Unions and general tax reduction (26.01) % (25.40) %Non-deductible and other items (0.21) % (0.73) %

Income taxes as reported 22.28 % 21.87 %

The tax effects of temporary differences which give rise to the deferred income tax asset reported in thebalance sheet, are due to differences between amounts deducted for accounting and income tax purposes withregards to property and equipment, investment property, intangible assets, the allowance for impaired loansand accounts payable and accrued liabilities.

Net deferred income tax assets are comprised of the following:

2015 2014

($Thousands)Property and equipment, intangible assets and investmentproperty $ (327) $ (134)Cumulative Eligible Capital 757 754Allowance for impaired loans 29 28Accounts payable and accrued liabilities - 41

$ 459 $ 689

9. Investment property2015 2014

($Thousands)Cost - Land and buildingOpening balance $ 325 $ -Additions from business combination - 325

325 325Accumulated amortization - buildingOpening balance $ 9 -Amortization 18 9

27 9

$ 298 $ 316

The investment property was previously operated as a branch in High Prairie. This building is currently beingrented to an unrelated party, the High Prairie School Division No. 48. The lease agreement is effective untilAugust 31, 2016 and the annual rent of $28,800 is received monthly and included in other income on thestatement of income and comprehensive income.

20

Vision Credit Union Ltd.Notes to Financial StatementsYear Ended October 31, 2015

10. Intangible assets2015 2014

($Thousands)CostOpening balance $ 1,468 $ 1,131Additions 447 692Write offs - (355)

1,915 1,468

Accumulated amortizationOpening balance $ 594 $ 756Amortization 258 193Write offs - (355)

852 594

Net book value $ 1,063 $ 874

11. Derivative financial assets and liabilities

The Credit Union has entered into option agreements with Alberta Central to offset the exposure related to theperformance of the underlying index on equity-linked products offered to members. The embedded derivativein the product as well as the option derivative is marked to market each year end, and amounted to $8,157(2014 - $52,510) as shown on the statement of financial position. At the end of the term, the Credit Union willreceive payment from Alberta Central which will offset the amount that will be paid to the members based onthe performance of the underlying index of the product.

The Credit Union has $2,349,354 (2014 - $2,349,354) outstanding of equity-linked deposits owed to itsmembers at year end. These deposits mature in February 2016 and February 2018.

The option agreements with Alberta Central are recorded in member deposits at cost less accumulatedamortization. Amortization is calculated on a straight-line basis over the term of the products and amounted to$37,268 (2014 - $18,634) for the year. Due to the business combination between Battle River Credit UnionLtd. and Caisse Horizon Credit Union Ltd. on May 1, 2014 to form Vision Credit Union Ltd., the 2014comparative balance for amortization includes only 6 months of operations of Caisse Horizon Credit UnionLtd. The comparative balance is $37,268 if a full year of operations for Caisse Horizon Credit Union Ltd. isincluded. The balance of the option agreements included in member deposits as at year end is $50,412 (2014- $87,680).

21

Vision Credit Union Ltd.Notes to Financial StatementsYear Ended October 31, 2015

12. Property and equipment

Land BuildingsComputerhardware

Furnitureand

equipmentParking

lot Total

($Thousands)CostBalance atOctober 31, 2013 582 7,310 1,970 2,950 315 13,127

Additions 832 4,163 603 496 7 6,101Disposals - - - - - -Write offs - - (1,572) (2,193) - (3,765)

Balance atOctober 31, 2014 1,414 11,473 1,001 1,253 322 15,463

Additions 288 578 399 109 - 1,374Disposals (24) (3) - (9) - (36)Write offs - - - - - -

Balance atOctober 31, 2015 1,678 12,048 1,400 1,353 322 16,801

Accumulated amortizationBalance atOctober 31, 2013 - 3,143 1,704 2,522 140 7,509

Additions - 293 100 173 14 580Disposals - - - - - -Write offs - - (1,572) (2,193) - (3,765)

Balance atOctober 31, 2014 - 3,436 232 502 154 4,324

Additions - 403 245 185 15 848Disposals - - - - - -Write offs - - - - - -

Balance atOctober 31, 2015 - 3,839 477 687 169 5,172

Net book value

At October 31,2014 1,414 8,037 769 751 168 11,139

At October 31,2015 1,678 8,209 923 666 153 11,629

22

Vision Credit Union Ltd.Notes to Financial StatementsYear Ended October 31, 2015

13. Member deposits

The repayment of all deposits, including accrued interest, is guaranteed by Credit Union Deposit GuaranteeCorporation, for which the Credit Union pays a deposit guarantee assessment fee.

2015 2014

($Thousands)Demand deposits $ 471,093 $ 457,752Term deposits 220,070 210,403Registered plans 73,380 66,313

764,543 734,468Accrued interest 3,889 3,948

$ 768,432 $ 738,416

Member deposits are subject to the following terms:

l Demand deposits are due on demand and bear interest at rates up to 2.00% for the year endedOctober 31, 2015.

l Term deposits are subject to fixed and variable rates of interest ranging from 0.20% to 4.50%, withinterest payments due monthly, annually or on maturity.

l Registered plans are subject to fixed and variable rates of interest ranging from 0.30% to 4.15%, withinterest payments due monthly, annually or on maturity.

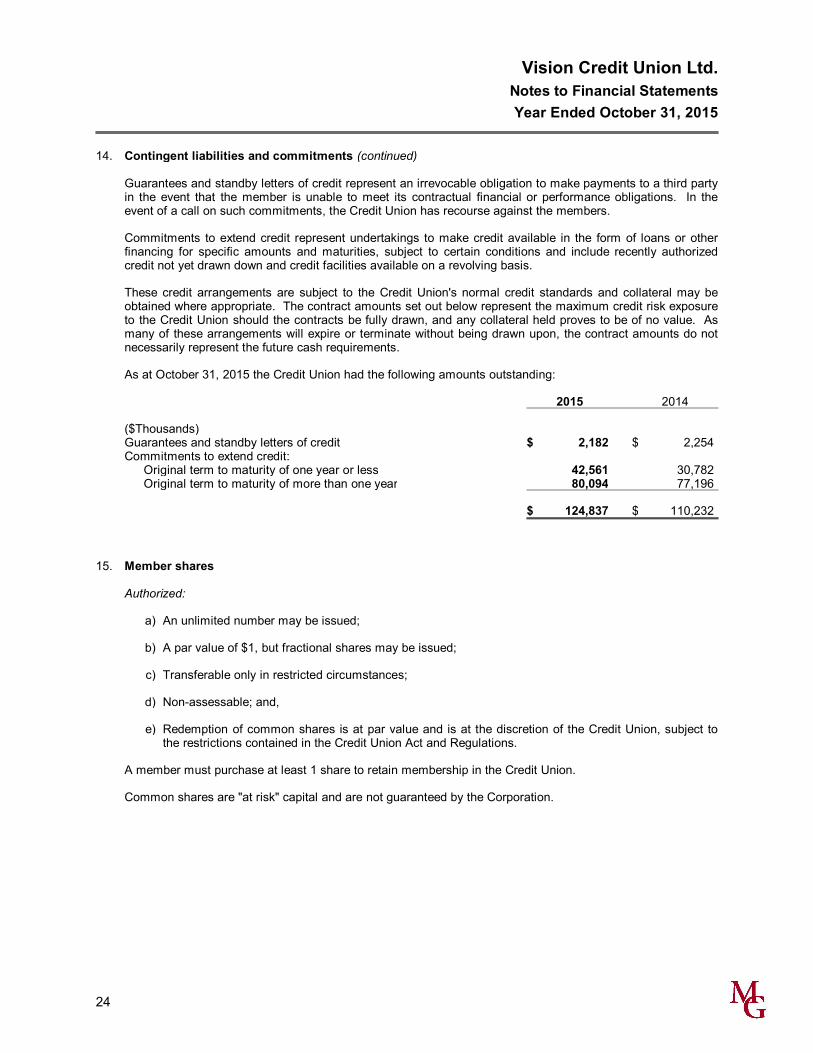

14. Contingent liabilities and commitments

Line of Credit

To finance short-term cash needs, the Credit Union has two operating lines of credit with Alberta Central. Thefirst operating line of credit has a ceiling of $38,600,000 CDN (2014 - $19,400,000 CDN), is payable ondemand, bears interest at Alberta Central’s Canadian prime rate less 0.5% (2014 - Alberta Central's Canadianprime rate less 0.5%) and is secured by a demand promissory note, a general assignment of book debts anda hypothecation of the Credit Union’s shares, investments and deposits with Alberta Central.

The second operating line of credit has a ceiling of $1,000,000 USD (2014 - $500,000 USD) and a maximumcomponent equivalent of $1,400,000 CDN, is payable on demand, bears interest at Alberta Central’s US primerate plus 0.5% (2014 - Alberta Central's US prime rate plus 0.5%) and is secured by a demand promissorynote, a general assignment of book debts and a hypothecation of the Credit Union’s shares, investments anddeposits with Alberta Central.

The operating lines of credit avoid the need to maintain on hand large sums of cash for short-term purposes.The operating lines of credit are used generally on a day-to-day basis. There is no balance outstanding as atOctober 31, 2015 (2014 - $nil).

Credit Commitments

In the normal course of business, the Credit Union enters into various commitments to meet the creditrequirements of its members. These include credit commitments, letters of credit, letters of guarantee andloan guarantees, which are not included on the statement of financial position.

(continues)

23

Vision Credit Union Ltd.Notes to Financial StatementsYear Ended October 31, 2015

14. Contingent liabilities and commitments (continued)

Guarantees and standby letters of credit represent an irrevocable obligation to make payments to a third partyin the event that the member is unable to meet its contractual financial or performance obligations. In theevent of a call on such commitments, the Credit Union has recourse against the members.

Commitments to extend credit represent undertakings to make credit available in the form of loans or otherfinancing for specific amounts and maturities, subject to certain conditions and include recently authorizedcredit not yet drawn down and credit facilities available on a revolving basis.

These credit arrangements are subject to the Credit Union's normal credit standards and collateral may beobtained where appropriate. The contract amounts set out below represent the maximum credit risk exposureto the Credit Union should the contracts be fully drawn, and any collateral held proves to be of no value. Asmany of these arrangements will expire or terminate without being drawn upon, the contract amounts do notnecessarily represent the future cash requirements.

As at October 31, 2015 the Credit Union had the following amounts outstanding:

2015 2014

($Thousands)Guarantees and standby letters of credit $ 2,182 $ 2,254Commitments to extend credit:

Original term to maturity of one year or less 42,561 30,782Original term to maturity of more than one year 80,094 77,196

$ 124,837 $ 110,232

15. Member shares

Authorized:

a) An unlimited number may be issued;

b) A par value of $1, but fractional shares may be issued;

c) Transferable only in restricted circumstances;

d) Non-assessable; and,

e) Redemption of common shares is at par value and is at the discretion of the Credit Union, subject tothe restrictions contained in the Credit Union Act and Regulations.

A member must purchase at least 1 share to retain membership in the Credit Union.

Common shares are "at risk" capital and are not guaranteed by the Corporation.

24

Vision Credit Union Ltd.Notes to Financial StatementsYear Ended October 31, 2015

16. Related party transactions

Key management personnel ("KMP") consists of the CEO, Senior Vice Presidents, Vice Presidents, Managers,Branch Managers, and the Board of Directors.

Loans made to KMP are approved under the same lending criteria applicable to members. KMP may receiveconcessional rates of interest on their loans and facilities. These benefits are subject to tax with the total valueof the benefit included in the compensation figures below.

There are no loans that are impaired in relation to loan balances with KMP or directors.

There are no benefits or concessional terms and conditions applicable to the family members of KMP. Thereare no loans that are impaired in relation to the loan balances with family or relatives of KMP.

At year end, the total of loans outstanding to KMP amounted to:

2015 2014

($Thousands)Aggregate of loans to KMP $ 5,564 $ 6,003Total value of revolving credit facilities to KMP 1,057 1,400

Net balance available $ 6,621 $ 7,403

During the year, the interest earned on loans and interest paid on deposits for KMP amounted to:

2015 2014

($Thousands)Interest and other revenue earned on loans to KMP $ 169 $ 213Interest paid on deposits to KMP 5 5

Due to the business combination between Battle River Credit Union Ltd. and Caisse Horizon Credit Union Ltd.on May 1, 2014 to form Vision Credit Union Ltd., the 2014 comparative balance includes only 6 months ofoperations of Caisse Horizon Credit Union Ltd. The comparative balances are $230,000 and $7,000 forinterest and other revenue earned on loans to KMP and interest paid on deposits to KMP respectively, if a fullyear of operations for Caisse Horizon Credit Union Ltd. is included.

At year end, the total value of member deposits from KMP amounted to:

2015 2014

($Thousands)Aggregate of deposits from KMP $ 1,212 $ 1,520

During the year, aggregate compensation of KMP amounted to:

2015 2014

($Thousands)Salary, bonuses and short term benefits $ 3,535 $ 3,120

(continues)

25

Vision Credit Union Ltd.Notes to Financial StatementsYear Ended October 31, 2015

16. Related party transactions (continued)

Due to the business combination between Battle River Credit Union Ltd. and Caisse Horizon Credit Union Ltd.on May 1, 2014 to form Vision Credit Union Ltd., the 2014 comparative balance for salary, bonuses and shortterm benefits includes only 6 months of operations of Caisse Horizon Credit Union Ltd. The comparativebalance is $3,414,000 if a full year of operations for Caisse Horizon Credit Union Ltd. is included.

Transactions with the Board of Directors, committee members, management and staff are at terms andconditions as set out in the loan policies of the Credit Union.

Payments made for honoraria and per diems amounted to $25,901 (2014 - $18,850) and reimbursement ofexpenses amounted to $8,730 (2014 - $5,703). Amounts paid to directors ranged from $400 to $3,550 withan average of $2,158. Due to the business combination between Battle River Credit Union Ltd. and CaisseHorizon Credit Union Ltd. on May 1, 2014 to form Vision Credit Union Ltd., the 2014 comparative balance fortransactions with the Board of Directors includes only 6 months of operations of Caisse Horizon Credit UnionLtd. The comparative balance is $53,503 for payments made for honoraria and per diems if a full year ofoperations for Caisse Horizon Credit Union Ltd. is included.

The Credit Union Deposit Guarantee Corporation

The Credit Union Deposit Guarantee Corporation ("CUDGC") was incorporated for the purpose of protectingthe members of credit unions from financial loss in respect of their deposits with credit unions and to establishsound procedures and controls for credit unions. CUDGC provides a safeguard for all savings and deposits ofmembers of Alberta credit unions.

Transactions with the CUDGC included assessments of $1,187,105 (2014 - $868,565) and are recorded asmember security expense on the statement of income and comprehensive income. Due to the businesscombination between Battle River Credit Union Ltd. and Caisse Horizon Credit Union Ltd. on May 1, 2014 toform Vision Credit Union Ltd., the 2014 comparative balance for CUDGC assessments includes only 6 monthsof operations of Caisse Horizon Credit Union Ltd. The comparative balance is $989,392 if a full year ofoperations for Caisse Horizon Credit Union Ltd. is included. There was $300,641 (2014 - $248,464) includedin accounts payable and accrued liabilities at year end.

The Credit Union Central Alberta Limited

The Credit Union is a member of the Alberta Central which acts as a depository for surplus funds, and makesloans to credit unions. Alberta Central also provides other services for a fee to the Credit Union and acts in anadvisory capacity.

Transactions with Alberta Central included income earned on investments referred to in Note 6 in the amountof $1,317,119 (2014 - $1,460,336), and fees assessed by Alberta Central which include annual affiliation duesin the amount of $230,969 (2014 - $207,950) recorded as organization expense in the statement of incomeand comprehensive income. Due to the business combination between Battle River Credit Union Ltd. andCaisse Horizon Credit Union Ltd. on May 1, 2014 to form Vision Credit Union Ltd., the 2014 comparativebalance for transactions with Alberta Central includes only 6 months of operations of Caisse Horizon CreditUnion Ltd. The comparative balances are $1,777,521 and $244,993 for income earned on investments andannual affiliation dues respectively, if a full year of operations for Caisse Horizon Credit Union Ltd. is included.

Celero Solutions

The Credit Union has entered into an agreement with Celero Solutions to provide the maintenance of theinfrastructure needed to ensure uninterrupted delivery of such banking services.

Celero Solutions is a company formed as a joint venture by the Credit Union Centrals of Alberta,Saskatchewan and Manitoba along with Concentra Financial Services and Credit Union Electronic TransactionServices.

26

Vision Credit Union Ltd.Notes to Financial StatementsYear Ended October 31, 2015

17. Director and officer indemnification

The Credit Union indemnifies its directors and officers against any and all claims or losses reasonablyincurred in the performance of their service to the Credit Union to the extent permitted by law.

18. Fair value of financial instruments

The amounts are designed to approximate the fair values of the Credit Union's financial instruments using thevaluation methods and assumptions described below. Since many of the Credit Union's financial instrumentslack an available trading market, the fair values represent estimates of the current market value ofinstruments, taking into account changes in market rates that have occurred since their origination. Due to theestimation process and the need to use judgment, the aggregate fair value amounts should not be interpretedas being necessarily realizable in an immediate settlement of the instruments.

Fair values have not been determined for property and equipment or any other asset or liability that is not afinancial instrument. The fair value of cash, variable rate loans and deposits, and accounts payable andaccrued liabilities are assumed to equal their book values due to their short term nature. The fair values offixed rate loans and deposits are determined by discounting the expected future cash flows at the estimatedcurrent market rates for loans and deposits with similar characteristics.

The following methods and assumptions were used to estimate the fair value of financial instruments:

a) The fair values of cash and cash equivalents, short-term investments, other assets and other liabilitiesare assumed to approximate book values, due to their short-term nature.

b) The estimated fair value of floating rate investments, member loans and member deposits areassumed to equal book value as the interest rates automatically reprice to market.

c) The estimated fair value of fixed rate member loans and fixed rate member deposits is determined bydiscounting the expected future cash flows of these loans and deposits at current market rates forproducts with similar terms and credit risks.

Estimated fair values of financial instruments are summarized as follows:

2015 2014

BookValue

FairValue

Fair ValueDifference

Fair ValueDifference

($Thousands)Assets Cash $ 17,677 17,677 - - Investments 115,543 116,546 1,003 968 Member loans 730,577 735,845 5,268 1,699 Other assets 14,251 14,252 - -Less:Liabilities Member deposits 768,432 770,744 (2,312) (2,587) Other liabilities 1,493 1,493 - -

$ 108,123 112,083 3,959 80

(continues)

27

Vision Credit Union Ltd.Notes to Financial StatementsYear Ended October 31, 2015

18. Fair value of financial instruments (continued)

Fair value measurements

The Credit Union classifies fair value measurements recognized on the balance sheet using a three-tier fairvalue hierarchy, which prioritizes the inputs used in measuring fair values as follows:

- Level 1: Quoted prices (unadjusted) are available in active markets for identical asset or liabilities.

- Level 2: Inputs other than quoted prices in active markets that are observable for the asset or liability,either directly or indirectly.

- Level 3: Unobservable inputs in which there is little or no market data, which require the Credit Union todevelop its own assumptions.

The carrying value of cash and cash equivalents approximate their fair value as they are short term in natureor are receivable on demand. Member loans and member deposits have been classified as Level 2 as fairvalues are primarily due to change in interest rates. There have been no transfers between Level 1 and 2during the year.

Fair value measurements are classified in the fair value hierarchy base on the lowest level input that issignificant to that fair value measurement. This assessment requires judgment, considering factors specificto an asset or a liability and may affect placement within the fair value hierarchy.

19. Capital management

The Credit Union’s objectives when managing capital are:

l To ensure the long-term viability of the Credit Union and the security of member deposits by holding alevel of capital deemed sufficient to protect against unanticipated losses; and,

l To comply at all times with the capital requirements set out in the Credit Union Act of Alberta (“theAct”). The Credit Union complied with these capital requirements throughout the year ending October31, 2015.

The Credit Union is required under the Act to hold total capital equal to or exceeding the greater of:

l 4% of total assets. As at October 31, 2015, this amounted to $35,121,939;

l 8% of risk weighted assets. Under this method, the Credit Union reviews each loan and other assetsand assigns a risk weighting using definitions and formulas set out in the Act and by the Credit UnionDeposit Guarantee Corporation. The more risk associated with an asset, then the higher the assignedweighting. The balance of each asset is multiplied by the risk weighting with the result then addedtogether. This method allows the Credit Union to measure capital relative to the possibility of loss withmore capital required to support assets that are seen as being higher risk. As at October 31, 2015, thisamounted to $43,620,915.

Additionally, the Credit Union is required to have a regulatory capital buffer of 2.5% of risk weightedassets for the year ended October 31, 2015. Further to this requirement, the Credit Union is expectedto hold a self-identified internal buffer equal to 2% of risk weighted assets. As at October 31, 2015, theCredit Union exceeds all capital requirements and holds total capital of 19.6% of risk weighted assets.

The Credit Union management ensures compliance with capital adequacy through the following:

l Establishing policies for capital management, monitoring and reporting;

(continues)

28

Vision Credit Union Ltd.Notes to Financial StatementsYear Ended October 31, 2015

19. Capital management (continued)

l Establishing policies for related areas such as asset liability management;

l Reporting to the Board of Directors and the Audit & Finance Committee regarding financial results andcapital adequacy;

l Reporting to the Credit Union Deposit Guarantee Corporation on its capital adequacy; and,

l Establishing budgets and reporting variances to those budgets.

Under the Act, total capital as at October 31, 2015 includes:

2015 2014

($Thousands)Retained earnings $ 47,659 $ 44,159Member shares 51,837 49,829ProfitShare allocation 8,627 7,292Collective allowance of credit losses 509 492Less: Deferred tax recoverable (459) (689)Less: Intangible assets (1,063) (874)

$ 107,110 $ 100,209

Therefore, the Credit Union has exceeded its minimum capital requirements at October 31, 2015.

20. Financial instruments risk management

The Credit Union, as part of its operations, carries a number of financial instruments which result in exposureto the following risks: credit risk, market risk, foreign currency risk and liquidity risk.

The Credit Union, as part of operations, has established avoidance of undue concentrations of risk andrequirements for collateral to mitigate credit risk as risk management objectives. In seeking to meet theseobjectives, the Credit Union follows a risk management policy approved by its Board of Directors.

The Credit Union's risk management policies and procedures include the following:

a) Ensuring all activities are consistent with the mission, vision and values of the Credit Union;

b) Balancing risk and return by:

l Managing credit, market and liquidity risk through preventative and detective controls;

l Ensuring credit quality is maintained;

l Ensuring credit, market, and liquidity risk is maintained at acceptable levels;

l Diversifying risk in transactions, member relationships and loan portfolios;

l Pricing according to risk taken; and,

l Using consistent credit risk exposure tools.

(continues)

29

Vision Credit Union Ltd.Notes to Financial StatementsYear Ended October 31, 2015

20. Financial instruments risk management (continued)

Various Board of Directors committees are involved in financial instrument risk management oversight,including the Audit & Finance Committee. The risk policies, procedures and objectives have not changedmaterially from the prior year.

Credit risk

Credit risk is the risk of a financial loss in the event of failure by a borrower to completely honour its financialobligation to the Credit Union, such as interest and/or principal payments due on member loans. Credit riskarises principally as a result of the Credit Union’s lending activities with members.

Management and the Board of Directors review and update the credit risk policy annually. The Credit Union'smaximum credit risk exposure before taking into account any collateral held is the carrying amount of loans asdisclosed on the balance sheet. See Note 5 for further information.

Concentration of credit risk exists if a number of borrowers are engaged in similar economic activities or arelocated in the same geographical region, and indicate the relative sensitivity of the Credit Union's performanceto developments affecting a particular segment of borrowers or geographical region. Geographical risk existsfor the Credit Union due to its primary service area being Camrose, Peace River and surrounding areas.

Credit risk management

The Credit Union uses a risk management process for its credit portfolio. The risk management process startsat the time of a member credit application and continues until the loan is fully repaid. Management of creditrisk is established in policies and procedures by the Board of Directors.

The primary credit risk management policies and procedures include the following:

a) Loan security (collateral) requirements;

b) Security valuation processes, including methods used to determine the value of real property andpersonal property when that property is subject to a mortgage or other charge;

c) Maximum loan to value ratios where a mortgage or other charge on real or personal property is takenas security;

d) Borrowing member capacity (repayment ability) requirements;

e) Borrowing member character requirements;

f) Limits on aggregate credit exposure per individual and/or related parties;

g) Limits on concentration to credit risk by loan type, industry and economic sector;

h) Limits on types of credit facilities and services offered;

i) Internal loan approval processes;

j) Loan documentation standards;

k) Loan re-negotiation, extension and renewal processes;

l) Processes that identify adverse situations and trends, including risks associated with economic,geographic and industry sectors;

(continues)

30

Vision Credit Union Ltd.Notes to Financial StatementsYear Ended October 31, 2015

20. Financial instruments risk management (continued)

m) Control and monitoring processes including portfolio risk identification and delinquency tolerances;

n) Timely loan analysis processes to identify, assess and manage delinquent and impaired loans;

o) Collection processes that include action plans for deteriorating loans;

p) Overdraft control and administration processes; and

q) Loan syndication processes.

Market risk

Market risk is the risk of a loss in value of financial instruments that may arise from changes in market factorssuch as interest rates, equity prices and credit spreads. The Credit Union's exposure changes depending onmarket conditions. Market risks that have a significant impact on the Credit Union include fair value risk andinterest rate risk.

Fair value risk

Fair value risk is the potential for loss from an adverse movement in the value of a financial instrument. TheCredit Union incurs fair value risk on its loans, term deposits and investments held. The Credit Union does nothedge its fair value risk, with the exception of the exposure of the equity-linked products offered to membersas discussed in Note 11. See Note 18 for further information on fair value of financial instruments.

Interest rate risk

Interest rate risk is the risk that the value of a financial instrument might be adversely affected by a change inthe interest rates. Changes in market interest rates may have an effect on the cash flows associated withsome financial assets and liabilities, known as cash flow risk, and on the fair value of other financial assets orliabilities, known as price risk. The Credit Union incurs interest rate risk on its loans and other interest bearingfinancial instruments.

Foreign currency risk

Foreign currency risk exposure results if financial assets or financial liabilities are denominated in a currencyother than Canadian dollars. The Credit Union holds US dollars. The balances held are relatively lowtherefore the currency risk is low. The Credit Union follows a policy of holding US dollars in an amountslightly below the US dollar deposit account levels. These levels are monitored and recorded daily. The buyand sell rates are also monitored and recorded daily. Excess US cash holdings are converted into Canadianfunds.

Liquidity risk

Liquidity risk is the risk that the Credit Union will not be able to pay obligations when they fall due or not beable to repay depositors when funds are withdrawn. To mitigate this risk, the Credit Union Act (the “Act”)requires that the Credit Union maintain, at all times liquidity that is adequate in relation to the business carriedon. The Credit Union calculates its liquidity position on a monthly basis to assess compliance with statutoryand mandatory liquidity requirements. These balances are communicated to the Board of Directors regularlythroughout the year. The Credit Union manages liquidity by continuously monitoring actual daily cash flows,monitoring the maturity dates of financial assets and financial liabilities, and maintaining adequate cashreserves.

(continues)

31

Vision Credit Union Ltd.Notes to Financial StatementsYear Ended October 31, 2015

20. Financial instruments risk management (continued)

The Act requires credit unions to maintain eligible assets for adequate liquidity. Assets held by the CreditUnion for such purposes are outlined below:

2015 2014

($Thousands)Credit Union Central statutory investments 58,820$ 55,570Credit Union Central common shares 8,500 8,172

Total assets held for liquidity 67,320$ 63,742

21. Comparative figures

Some of the comparative figures have been reclassified to conform to the presentation adopted in the currentyear. The reclassification of certain balances has no impact on retained earnings.

32

Vision Credit Union Ltd.Notes to Financial StatementsYear Ended October 31, 2015

22. Interest rate risk

Interest rate risk is the risk that the value of a financial instrument might be adversely affected by a change inthe interest rates. Changes in market interest rates may have an effect on the cash flows associated withsome financial assets and liabilities, known as cash flow risk, and on the fair value of other financial assets orliabilities, known as price risk. The Credit Union incurs interest rate risk on its loans and other interest bearingfinancial instruments.

2015($Thousands)

VariableRate

Within 1 Year

1 to 5Years

Non-rateSensitive Total

Assets

Cash and cashequivalents

$ 16,990 - - 687 17,677

Effective Yield 0.25% 0.00% 0.00% 0.00% 0.24%

Investments - 94,815 11,912 8,816 115,543

Effective Yield 0.00% 0.61% 3.56% 0.00% 0.87%

Member loans 205,220 190,677 331,880 2,800 730,577

Effective Yield 4.24% 4.33% 4.46% 0.00% 4.35%

Other - - - 14,251 14,251

$ 222,210 285,492 343,792 26,554 878,048

Liabilities and Equity

Member deposits $ 298,751 131,837 153,815 184,029 768,432

Effective Yield 0.25% 1.98% 1.66% 0.00% 0.77%

Capital andretained earnings

- - - 108,123 108,123

Other - - - 1,493 1,493

$ 298,751 131,837 153,815 293,645 878,048

Net gap $ (76,541) 153,655 189,977 (267,091) -

% of assets -8.72% 17.50% 21.64% -30.42% 0.00%

2014

Net gap $ (5,317) 162,054 167,338 (324,075) -

% of assets -0.63% 19.26% 19.89% -38.51% 0.00%

33