financing the u.s. power fleet - latest oil, energy & metals … · · 2013-04-18800 mw gas...

TRANSCRIPT

Financing the U.S. Power Fleet Generation reliability and transformation of the power fleet Las Vegas, April 9th, 2013

Jorge Camina

Head of Project & Acquisition Finance U.S. Santander Global Banking & Markets

p.2 Financing the Power Industry in U.S. About Santander

A growing franchise in the U.S. Largest bank in the Eurozone by market cap and 9th in the world1: serving 100

million customers Santander in the U.S.: 1.7 million customers, $178bn assets, 777 branches

and 14,000 employees

We have financed 34 deals with either debt or equity in the North American power space in the last 24 months: 8.2 GW capacity, $14bn of EV

Among these, 11 solar - PV and CSP - (1.7GW), and 16 wind (2.6GW) Santander led 6 bank-institutional hybrid deals in 2012, raising + $2.3bn debt “Greenest Bank in the World in 2012” by Bloomberg

Committed to the Power Industry

p.3 Financing the Power Industry in U.S. Santander : Debt Provider to Power Projects in the U.S.

US 2012

US$ 756,000,000Left Lead CoordinatorJoint Lead Arranger

Joint Bookrunner

Centinela Solar

170 MW Solar PV Plant in California

CAD 2012

CAD$ 296,000,000Left Lead CoordinatorJoint Lead Arranger

Joint Bookrunner

Des Moulins Phase I

136 MW Wind Farm in Quebec

US 2012

US$ 352,000,000

Flat Ridge 2

470 MW Wind Farmin Kansas

Left Lead CoordinatorJoint Lead Arranger

Joint Bookrunner

US 2012

US$ 355,000,000Senior Managing Agent

Co-Documentation Agent

Broad River

Acquisition of 847 MW gas-fired power plant

US 2012

US$ 272,000,000Mandated Lead Arranger

Syndication Agent

Alpine Solar

68 MW Solar PV Plant in California

US 2012

US$ 444,000,000Left Lead CoordinatorJoint Lead Arranger

Joint Bookrunner

California Ridge

214 MW Wind Farm in Illinois

US 2012

US$ 476,000,000Joint Lead Arranger

Joint Bookrunner

Imperial Solar South

130 MW Solar PV Plant in California

US 2012

US$ 465,000,000Left Lead CoordinatorJoint Lead Arranger

Joint Bookrunner

Arlington Valley

127 MW Solar PV Plant in Arizona

US 2011

US$ 1,779,000,000

Joint Lead Arranger

Desert Sunlight

550 MW Solar PV Plant in California

US 2012

US$ 650,000,000Joint Lead Arranger

Co-Documentation Agent

Alta Wind VII & IX

300 MW Wind Farms in California

US 2011

US$ 631,000,000Joint Lead Arranger

Co-Documentation Agent

Alta Wind VI & VIII

Two 150 MW Wind Farms in California

US$ 422,000,000

US 2011

Joint Lead ArrangerJoint Bookrunner

Lakefield

210 MW Wind Farm in Minnesota

US 2011

US$ 796,000,000

Co-Agent

CPV Sentinel

800 MW Gas Fired Power Plant in California

US$ 144,000,000

Mandated Lead Arranger

Lost Creek

Refinancing of 150 MW Wind Farm in Missouri

US 2011

US$ 727,000,000

Co-Agent

Sharyland

300 miles Transmission Lines in Texas

US 2011

p.4 Financing the Power Industry in U.S. Santander : Equity Provider to Power Projects in the U.S.

US 2012

US$ 2,000,000,000

US 2012

CONFIDENTIAL

US 2012

CONFIDENTIAL

US 2011

US$ 21,000,000

US 2012

US$ 138,000,000

US 2011

US$ 1,000,000,000 CONFIDENTIAL

US 2011US 2011

US$ 123,000,000 US$ 123,000,000

US 2011

CONFIDENTIAL

US 2010

Shiloh III

102 MW Wind Farm

Solana

280 MW CSP

Mountain Air

138 MW Wind Farm

Punta Lima

23.4 MW Wind Farm

SPP Project

4.4 MW Solar PV

Project Arranger Tax Equity Investor

Project Arranger Equity Investor

Project Arranger Equity Investor

Project Arranger Tax Equity Investor

Project Arranger Equity Investor

Project Arranger Equity Investor

Palm Valley Solar

4.5 MW Solar PV

Project Arranger Equity Investor

Tonopah Solar

110 MW CSP

Project Arranger Equity Investor

Flatt Water

60 MW Wind Farm

Equity Provider

Austin Solar

35 MW Solar PV

Equity Provider

PRIVATE CLIENT

Macho Springs

50 MW Wind Farm

p.5 Financing the U.S. Power Fleet 2013: Slow down in financing pipeline in the power Industry (Supply)

Supply U.S. Electricity Demand down 0.3% in 2012 (10.6 Bn KW/hr/d) Slow down after a period of unprecedented support to the Renewable Energy

industry through various programs: DOE, ITC Cash Grant, etc. Diminishing stock of PPAs in the wind & solar industry: getting closer to the

RPS targets in California Tailwinds from the manufacturer cost curve in Solar PV: improving success

ratio of aggressive PPA pricings and accelerating RPS compliance Mostly Generation driving the need of debt. Transmission not yet demanding

significant private capital, with exceptions like the CREZ program in Texas Coal Retirement will drive growth but may not happen as quickly and may be

semi-merchant driven

p.6 Financing the U.S. Power Fleet 2013: The IPP Power sector has been a key driver of Project Finance Lending in the last 5 yrs

Power represented 86% of the Project Finance Market in 2011, 54% in 2012

U.S. Project Finance market volumes have remained stable at $ 35 Bn

12.2 8.0 8.1

17.4

6.6

7.9

6.7 11.6

18.3

14.1

6.0

6.8

5.5

1.2

8.2 3.9

6.1 4.7

2.0 1.9 1.4

3.9

2.0

3.9

0

5

10

15

20

25

30

35

40

2008 2009 2010 2011 2012

Conventional Power Renewable Energy Oil and Gas Transportation - Infra. Other

The Project Finance Market in the U.S. 2008 - 2012

p.7

Demand Strong demand for financing contracted power: traditional PF Banks, LifeCos

and Bond Market (ie Topaz) Low Default track record in contracted power Relative Value with Corporate Credits: $15 Bn of the Heinz acquisition facility

were flexed-down this month (6/7 Yrs Term Loan B @ L+225 / 275 Bps) High Yield Investors chasing yield in the Infrastructure space: Sabine Pass 1.5

Bn trading at 5% yield (BB-; 5 year construction) European banks are mostly back (French & German) Japanese lenders targeting to maintain volume in a weaker pipeline:

tightening pricing & increasing appetite for semi-merchant deals Growing appetite for power assets and presence of U.S. regional banks

Financing the U.S. Power Fleet 2013: Debt appetite is strong (Demand)

p.8 Financing the U.S. Power Fleet Power: key driver of Project Finance Lending in the last 5 yrs

Yield of non-IG credits continued dropping, reaching below 6% levels. Appetite for yield is driving more assets managers from more traditional HY

structures to the power & infrastructure space

5.0

5.5

6.0

6.5

7.0

7.5

8.0

8.5

9.0

9.5

10.0

Jan-11 Jul-11 Jan-12 Jul-12 Jan-13

JPMorgan High Yield Bond Index YTW (%)

7 to 10 yrs 10+ yrs

JPM High Yield Index (YTW %)

p.9 Financing the Power Industry in U.S. Supply / Demand Imbalance

Competition in pricing and tenors in the short term, despite capital regulatory constraints kicking in full by 2018

Increased interest in other power asset categories, from purely utility scale contracted power with commercially proven technologies to:

– Increasing interest in Distributed Generation, Commercial & Residential – Merchant & Semi-merchant projects will get more attention: Term Loan B

players will find more competition from Commercial Banks – Less commercially proven technologies (ie CSP)

Partially alleviated by strong demand from multibillion LNG Exporting facilities (estimated in >15 Bn debt needs in the U.S for the next 12 months)

The end of the cash grant era leads to the comeback of ITC Bridges Back to UW to capture deal-flow?

Near term outcome 2013-2014

p.10

:

1. There is no carve-out in Basel III in the treatment of Project Finance

2. Commercial Banks will see their appetite for long tenors significantly reduced

3. Pricing & Return pressures: Increase in pricing and pressure en ROA

48%

38%

25%

16% 12%

8% 5%

PrivateEquity

Equity Property Credit 10years

Credit 7years

Credit 5years

Credit 3years

Financing the Power Industry in U.S The Project Finance Business Model is in the middle of a transition

Basel III – increased costs for long term financings challenging for PF business

The new capital regulations kick-in full by 2018

Capital requirements by asset class under Basel III

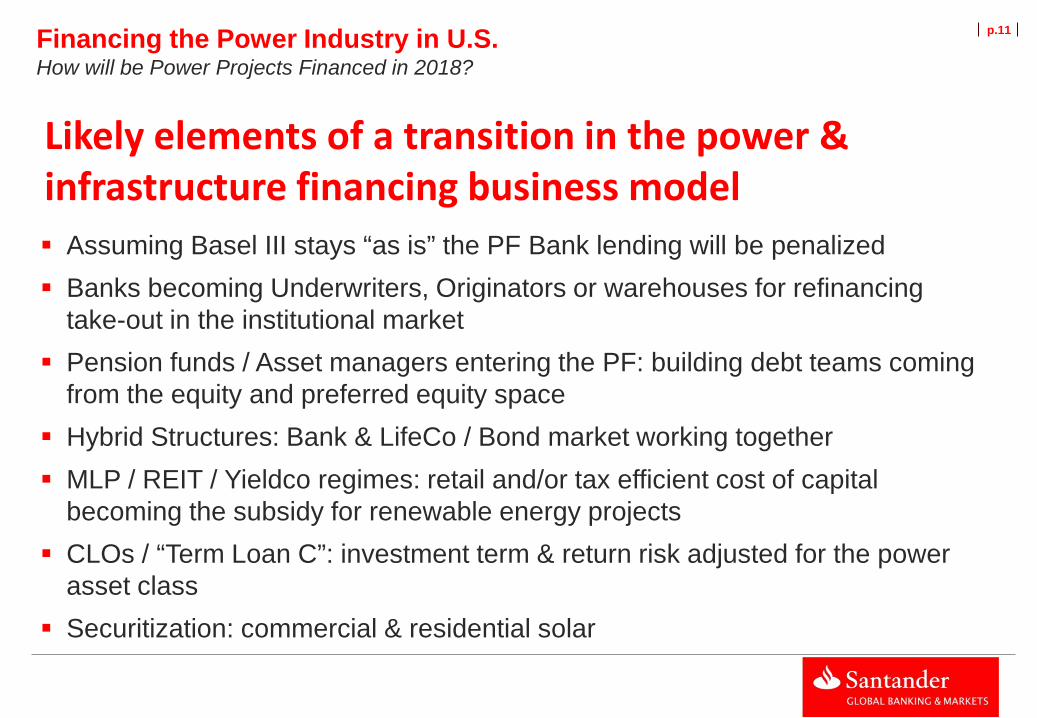

p.11 Financing the Power Industry in U.S. How will be Power Projects Financed in 2018?

Likely elements of a transition in the power & infrastructure financing business model Assuming Basel III stays “as is” the PF Bank lending will be penalized Banks becoming Underwriters, Originators or warehouses for refinancing

take-out in the institutional market Pension funds / Asset managers entering the PF: building debt teams coming

from the equity and preferred equity space Hybrid Structures: Bank & LifeCo / Bond market working together MLP / REIT / Yieldco regimes: retail and/or tax efficient cost of capital

becoming the subsidy for renewable energy projects CLOs / “Term Loan C”: investment term & return risk adjusted for the power

asset class Securitization: commercial & residential solar