fixed income investor presentation may 2011 - ingenico · investors presentation - may 2011• 9....

TRANSCRIPT

Investors PresentationMay 2011

Investors presentation - May 2011• 2

Disclaimer

All forward-looking statements are Ingenico management’s present expectations of future events and are subject to a number of factors and uncertainties that could cause actual results to differ materially from those described in the forward-looking statements.

Investors presentation - May 2011• 3

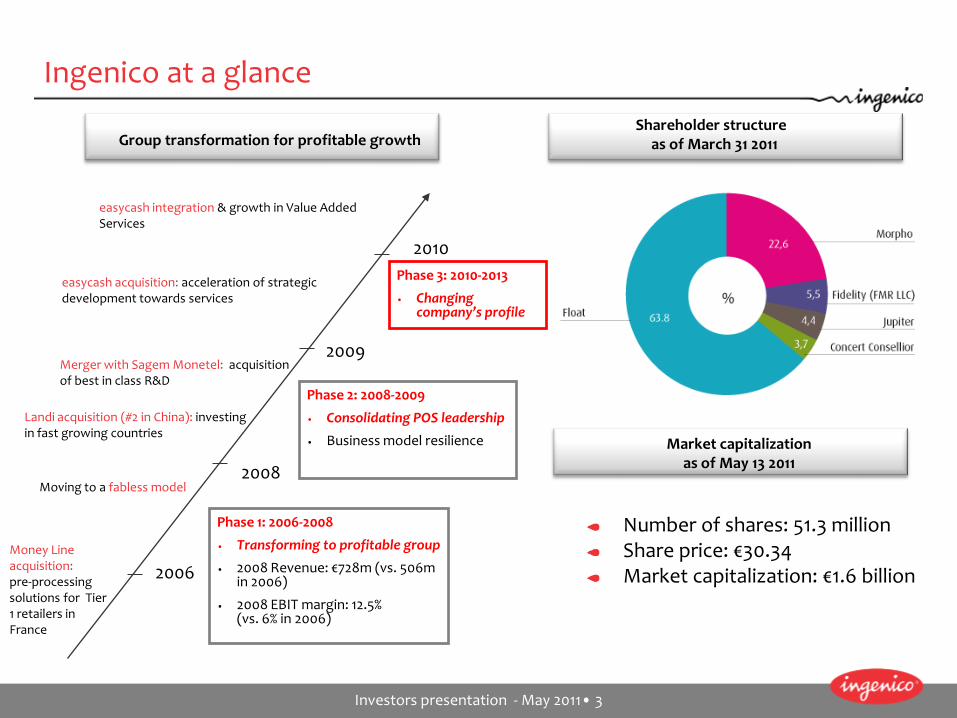

Ingenico at a glance

Number of shares: 51.3 millionShare price: €30.34Market capitalization: €1.6 billion

easycash acquisition: acceleration of strategic development towards services

Landi acquisition (#2 in China): investing in fast growing countries

Merger with Sagem Monetel: acquisition of best in class R&D

Money Line acquisition: pre-processing solutions for Tier 1 retailers in France

2009

2008

2006

Moving to a fabless model

2010

easycash integration & growth in Value Added Services

Phase 2: 2008-2009

• Consolidating POS leadership

• Business model resilience

Phase 1: 2006-2008

• Transforming to profitable group

• 2008 Revenue: €728m (vs. 506m in 2006)

• 2008 EBIT margin: 12.5% (vs. 6% in 2006)

Phase 3: 2010-2013

• Changing company’s profile

Group transformation for profitable growth Shareholder structure

as of March 31 2011

Market capitalization as of September 15 2010Market capitalization

as of May 13 2011

Investors presentation - May 2011• 4

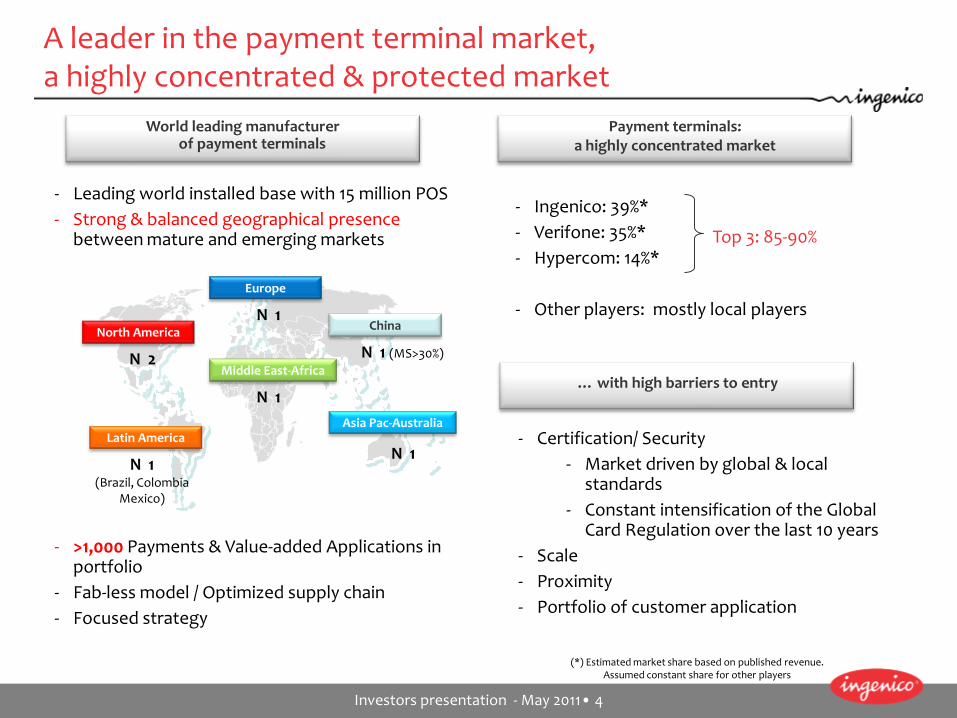

A leader in the payment terminal market, a highly concentrated & protected market

North America

Latin America

Europe

Middle East-Africa

China

Asia Pac-Australia

N 1(Brazil, Colombia

Mexico)

N 2

N 1

N 1

N 1

N 1 (MS>30%)

World leading manufacturer of payment terminals

Payment terminals: a highly concentrated market

… with high barriers to entry

- Certification/ Security- Market driven by global & local

standards- Constant intensification of the Global

Card Regulation over the last 10 years - Scale- Proximity- Portfolio of customer application

- Ingenico: 39%* - Verifone: 35%*- Hypercom: 14%*

- Other players: mostly local players

Top 3: 85-90%

(*) Estimated market share based on published revenue. Assumed constant share for other players

- Leading world installed base with 15 million POS- Strong & balanced geographical presence

between mature and emerging markets

- >1,000 Payments & Value-added Applications in portfolio

- Fab-less model / Optimized supply chain- Focused strategy

Investors presentation - May 2011• 5

Serving a worldwide blue-chip customer base

Major financial institutions and merchants are using our products and solutions all over the world (in more than 100 countries). Dual vendor policy

Our blue chip customer base includes banks, processors & acquirers, merchants, integrators, and services providers

More than 100,000 small merchants directly managed in France and Germany

Investors presentation - May 2011• 6

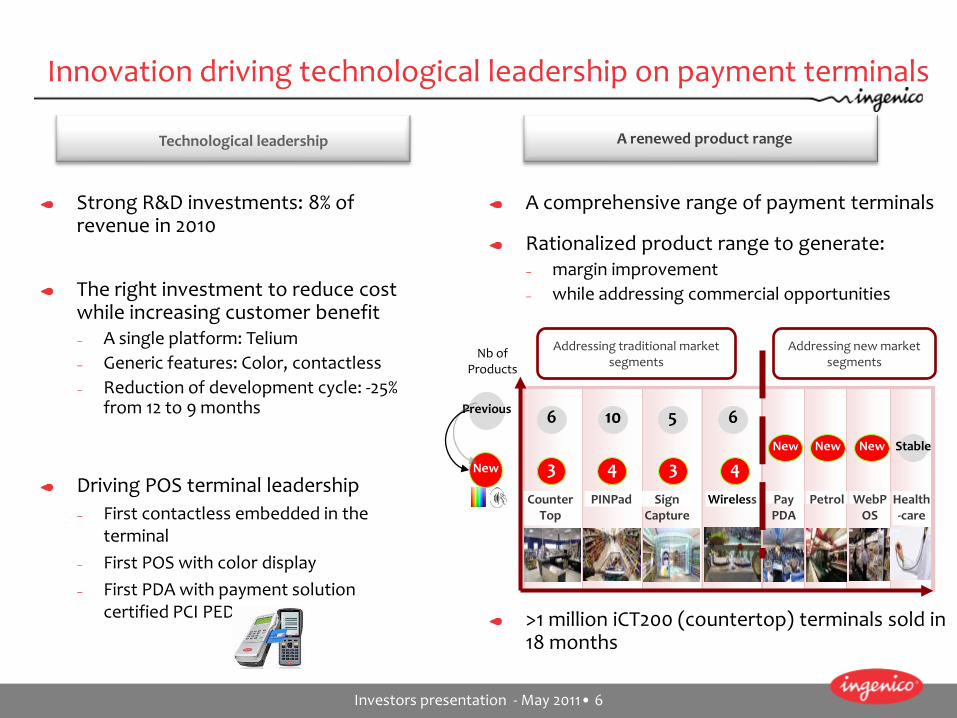

Innovation driving technological leadership on payment terminals

Strong R&D investments: 8% of revenue in 2010

The right investment to reduce cost while increasing customer benefit– A single platform: Telium– Generic features: Color, contactless– Reduction of development cycle: -25%

from 12 to 9 months

Driving POS terminal leadership– First contactless embedded in the

terminal– First POS with color display– First PDA with payment solution

certified PCI PED

A comprehensive range of payment terminals

Rationalized product range to generate:– margin improvement– while addressing commercial opportunities

>1 million iCT200 (countertop) terminals sold in 18 months

Counter Top

WirelessSign Capture

Pay PDA

WebPOS

Health-care

Petrol

Addressing traditional market segments

Addressing new market segments

PINPad

6

3

10

4

5

3

6

4New NewNew Stable

Previous

Nb ofProducts

New

Technological leadership A renewed product range

Investors presentation - May 2011• 7

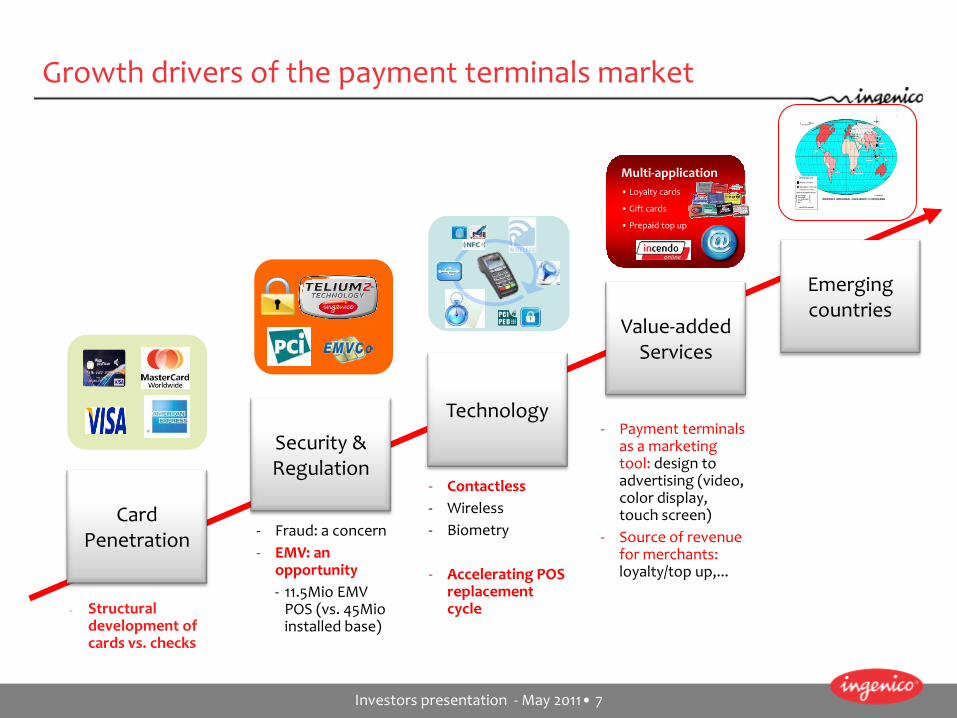

Emerging countries

Technology

Card Penetration

Multi-application• Loyalty cards

• Gift cards

• Prepaid top up

Value-addedServices

Security &Regulation

Growth drivers of the payment terminals market

- Fraud: a concern- EMV: an

opportunity- 11.5Mio EMV

POS (vs. 45Mio installed base)

- Contactless- Wireless- Biometry

- Accelerating POS replacement cycle

- Payment terminals as a marketing tool: design to advertising (video, color display, touch screen)

- Source of revenue for merchants: loyalty/top up,...

- Structural development of cards vs. checks

Investors presentation - May 2011• 8

Emerging markets & urbanization drive growth

Increased middle class with access to financial services

Governments pushing for tax collection

avg. 2 terminals p. 1,000 inh.

avg. 24 terminals p.1,000 inh.

Source: Euromonitor / IMF

Mature Payment Countries

Emerging Countries

Num

ber o

f PO

S te

rmin

als p

er ‘0

00 p

eopl

e

Emerging countries as key sources of growth

Investors presentation - May 2011• 9

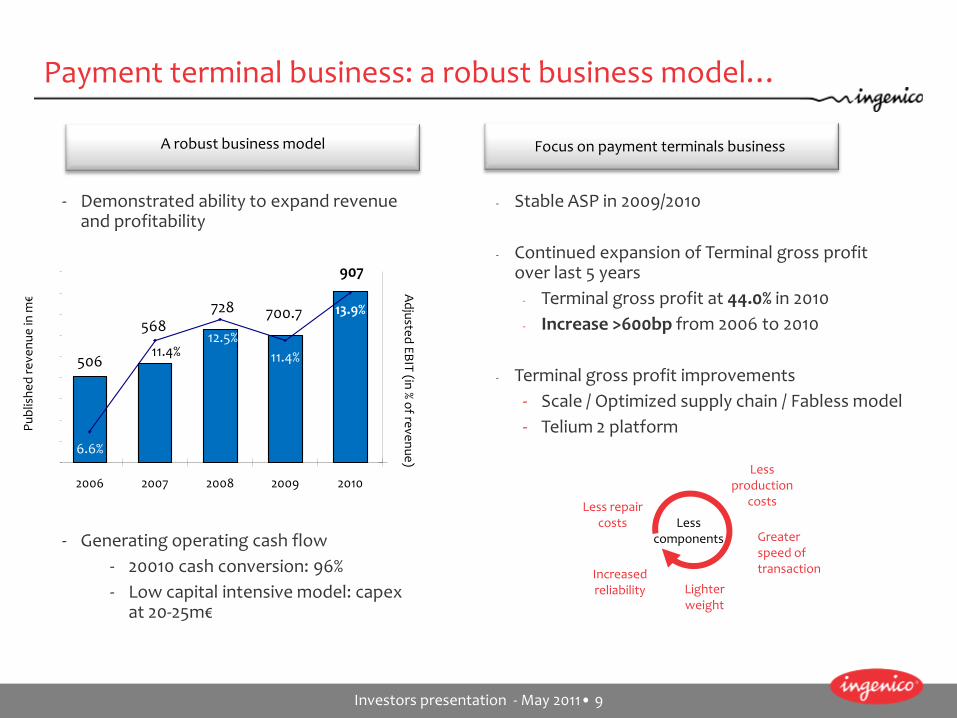

Payment terminal business: a robust business model…

- Stable ASP in 2009/2010

- Continued expansion of Terminal gross profit over last 5 years

- Terminal gross profit at 44.0% in 2010- Increase >600bp from 2006 to 2010

- Terminal gross profit improvements- Scale / Optimized supply chain / Fabless model- Telium 2 platform

A robust business model Focus on payment terminals business

Less components Greater

speed of transaction

Lighter weight

Increased reliability

Less production

costsLess repair costs

- Demonstrated ability to expand revenue and profitability

- Generating operating cash flow- 20010 cash conversion: 96%- Low capital intensive model: capex

at 20-25m€

506

568728 700.7

907

6.6%

11.4%12.5%

11.4%

13.9%

5%100

200

300

400

500

600

700

800

900

1000

2006 2007 2008 2009 2010

Publ

ishe

d re

venu

e in

m€ A

djusted EBIT (in % of revenue)

Investors presentation - May 2011• 10

… to fuel development towards services

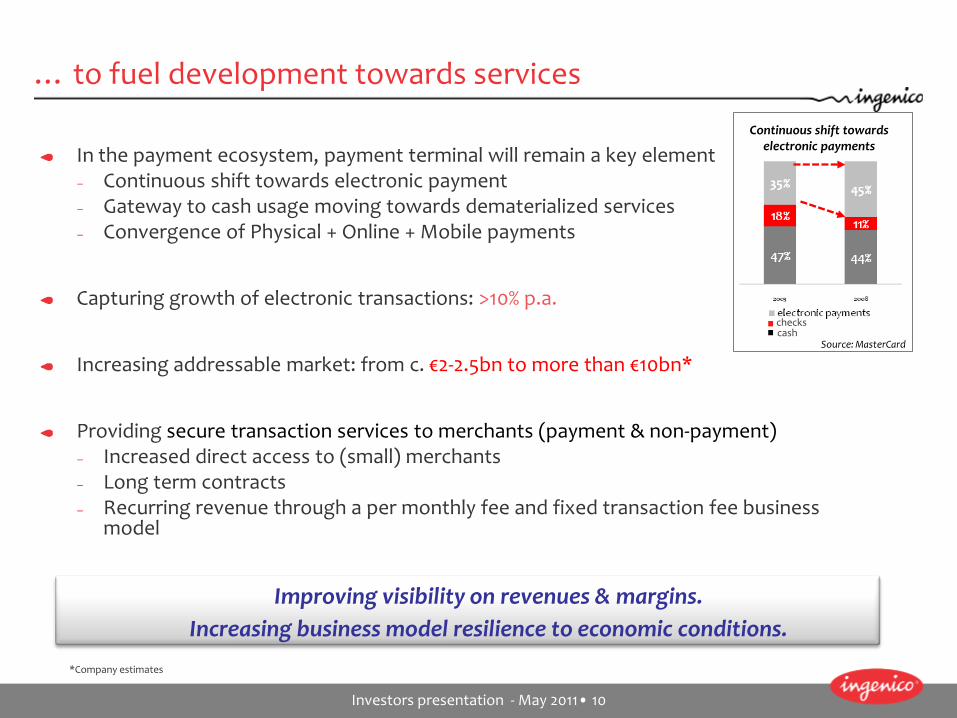

In the payment ecosystem, payment terminal will remain a key element– Continuous shift towards electronic payment– Gateway to cash usage moving towards dematerialized services– Convergence of Physical + Online + Mobile payments

Capturing growth of electronic transactions: >10% p.a.

Increasing addressable market: from c. €2-2.5bn to more than €10bn*

Providing secure transaction services to merchants (payment & non-payment)– Increased direct access to (small) merchants– Long term contracts – Recurring revenue through a per monthly fee and fixed transaction fee business

model

Improving visibility on revenues & margins.Increasing business model resilience to economic conditions.

Continuous shift towards electronic payments

checkscash

Source: MasterCard

*Company estimates

Investors presentation - May 2011• 11

Ingenico in the electronic payment value chain

POS terminal marketMarket Transaction services VAS Financial institutions

mostly

Value chain Hardware Terminal

servicesConnectivity Pre-

processing ProcessingValue-added

ServicesSettlement

Ingenico entities

Revenue type

Monthly fee

Monthly feeOne off Monthly

fee

% of transaction

in value

Monthly fee+ Fixed charge /

transaction

Fixed fee per

transaction

Merchant Services AcquirerProcessor VAS provider

Ingenico mostly provides POS terminals to either directly (large retailers) or indirectly (banks, distributors)

Revenue business model mostly relies on one off fees

Easycash operates payment & VAS services for merchants

Revenue business model relies on recurring revenue through a per transaction payment type of business

Investors presentation - May 2011• 12

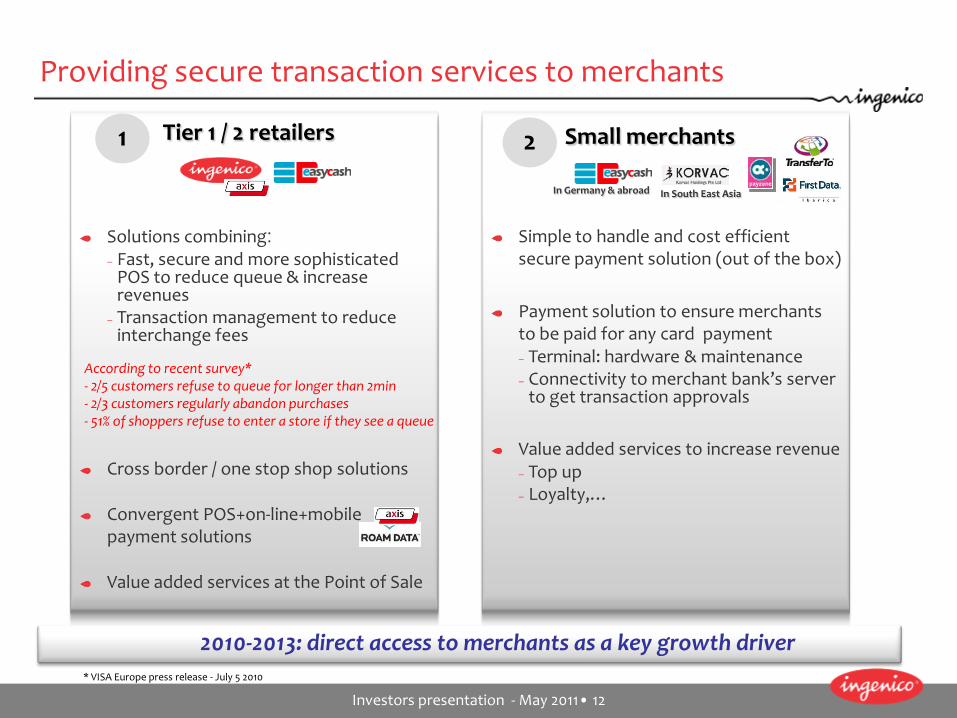

Providing secure transaction services to merchants

Tier 1 / 2 retailers

Solutions combining:– Fast, secure and more sophisticated

POS to reduce queue & increase revenues

– Transaction management to reduce interchange fees

Cross border / one stop shop solutions

Convergent POS+on-line+mobilepayment solutions

Value added services at the Point of Sale

1

According to recent survey*- 2/5 customers refuse to queue for longer than 2min- 2/3 customers regularly abandon purchases- 51% of shoppers refuse to enter a store if they see a queue

* VISA Europe press release - July 5 2010

Simple to handle and cost efficient secure payment solution (out of the box)

Payment solution to ensure merchants to be paid for any card payment– Terminal: hardware & maintenance– Connectivity to merchant bank’s server

to get transaction approvals

Value added services to increase revenue – Top up– Loyalty,…

Small merchants2

2010-2013: direct access to merchants as a key growth driver

In Germany & abroad In South East Asia

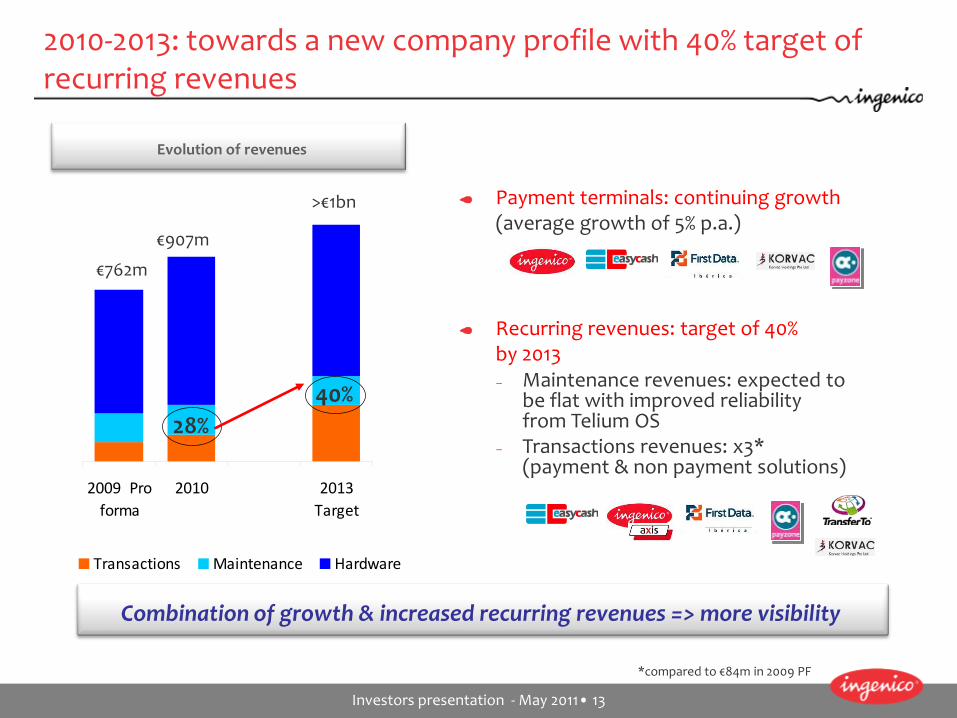

Investors presentation - May 2011• 13

Payment terminals: continuing growth (average growth of 5% p.a.)

Recurring revenues: target of 40% by 2013– Maintenance revenues: expected to

be flat with improved reliability from Telium OS

– Transactions revenues: x3* (payment & non payment solutions)

Combination of growth & increased recurring revenues => more visibility

2010-2013: towards a new company profile with 40% target of recurring revenues

2009 Proforma

2010 2013Target

Transactions Maintenance Hardware

*compared to €84m in 2009 PF

>€1bn

€762m

40%28%

Evolution of revenues

€907m

Investors presentation - May 2011• 14

2010: an outstanding year

Strong top line growth– 2010 revenue: €907.0m– Year-on year: +29%– Like-for-like: +10%

… while significantly fueling profitability & demonstrated operating leverage– Adjusted current operating income*: 13.9% (+250 basis points)– EBITDA margin at 18.3%– Doubled net operating cash flow to €158.9m– Strong cash conversion driven by operating leverage and tight

management of working capital

Paving ground to accelerate 2013 strategic plan– Deployment of Telium2 platform – Successful integration of easycash– Targeted acquisitions in value-added services

*Adjusted current operating income is defined as adjusted profit from ordinary activities

Investors presentation - May 2011• 15

Management priorities for 2011: delivering our 2013 strategic plan

Terminals: maintain product leadership– iPA 280 (PayPDA) is taking off– Mobile POS (iWL) is clearly ahead of competition– Unattended range to capture market potential of vending machines

Transactions: enlarged offering and enhanced footprint– Front-end processing for Tier 1 retailers– Rolling out easycash internationally

– Obtained “institution payment” license in Q1’11– Opening at least 2 countries in 2011

– Capturing mobile payment emergence opportunities

VAS: developing and deploying integrated portfolio of services– Transfer To: capturing air time growth through new routes

Investors presentation - May 2011• 16

Q1 2011: a very good start of the year (1/2)

Sustained growth– Q1’11 revenue of: €204.9m (+18% year-on-year)– Like-for-like: +9%

Strong performance of both terminals (+6.4%*) and Transactions (+25%*)– Terminals: Specific market dynamics / More contactless, more mobile

terminals– Transactions: growth on all segments: development of AXIS solutions,

acquiring services in Germany and Value-Added-Services

Continuation of trends observed at the end of 2010– Very strong quarter in Latin America (Brazil) and Asia Pacific (China)– Asia Pacific: 2nd largest region for the second quarter in a row– Still a strong momentum in Europe SEPA (Spain, UK, France)– Activity down in EMEA & North America where low anticipated performance

was accentuated by an unfavorable basis of comparaison

* Before Price Purchase Allocation

Investors presentation - May 2011• 17

Q1 2011: a very good start of the year (2/2)

2011 revenue target revised upwards– Like-for-like revenue (at constant group perimeter & FX) ≥ 985m€ (as against

965-985m€)– Like-for-like growth: ≥ 6.3%

Continuous profitability improvement confirmed– Adjusted profit from ordinary activities* ≥ 13.9% – EBITDA: ≥ 18.3%

Enhanced financial flexibility– €250m raised through convertible bonds (OCEANE) due 1 January 2017

* Before Price Purchase Allocation

Investors presentation - May 2011• 18

Ingenico investment case

Investors presentation - May 2011• 19

Appendix

Investors presentation - May 2011• 20

Glossary

POS: Point of Sale / e-payment terminal

VAS: Value-added Services

SEPA: Single Euro Payment Area. 27 European Union members, Island, Liechtenstein, Norwayand Switzerland

Acquirer: financial institution responsible for the underlying transactions (authorization, clearing & settlement) with its merchant-customers

Issuer: Cardholder’s bank

Processor: a technical operator providing infrastructure to support acquirer functions, such as authorization, clearing and settlement services. In practice, acquirers outsourced merchant acquiring services to processor

PSP: A Payment Service Provider is a company performing all or part of electronic payment services and potentially including settlement as per Payment Service Directive in Europe. In the US, settlement is always performed by financial institutions

Scheme: provides a payments mechanism through the existing (debit or credit) card payment infrastructure

ISO: Independent Sales Offices

Investors presentation - May 2011• 21

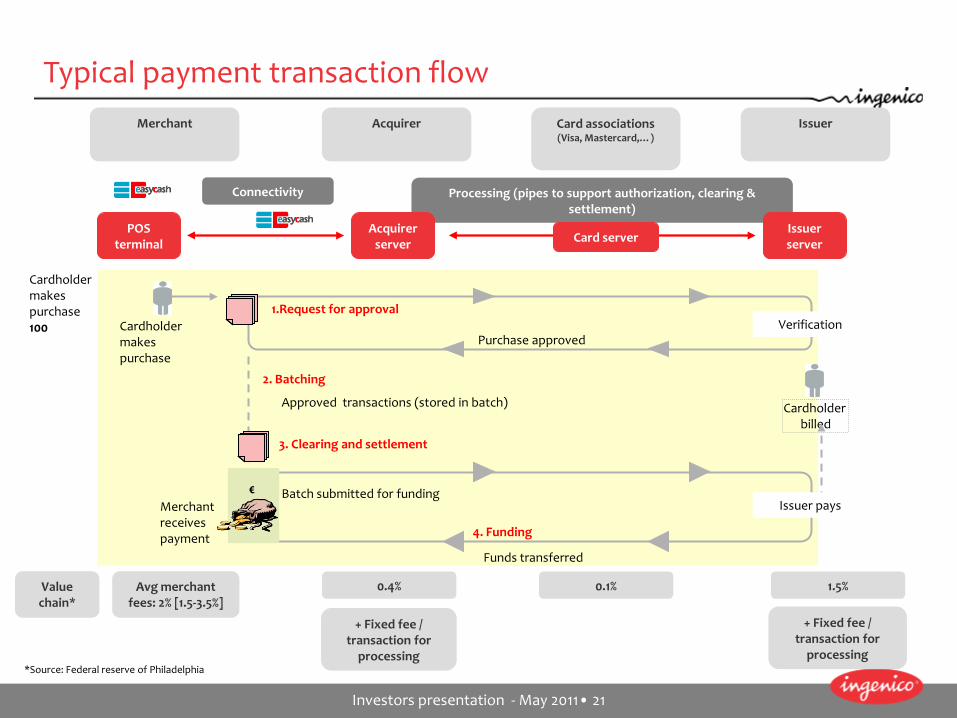

Processing (pipes to support authorization, clearing & settlement)

Merchant

Connectivity

Acquirer server

Acquirer Card associations (Visa, Mastercard,…)

Issuer

Issuer server

POS terminal

Value chain*

Avg merchant fees: 2% [1.5-3.5%]

0.4% 0.1% 1.5%

+ Fixed fee / transaction for

processing

+ Fixed fee / transaction for

processing

Card server

Cardholder makes purchase100

2. Batching

3. Clearing and settlement

4. Funding

1.Request for approval

Purchase approvedCardholder makes purchase

Cardholder billed

Approved transactions (stored in batch)

Batch submitted for fundingMerchant receives payment

Funds transferred

Verification

€Issuer pays

Typical payment transaction flow

*Source: Federal reserve of Philadelphia

Investors presentation - May 2011• 22

Large customers

+ Fixed fee / transaction

easycash business model at a glance

Hardware Terminal services

Connectivity ProcessingValue-added

Services

Settlement

Merchant Services AcquirerProcessor

Small customers

OLV Visa ZKA

% of transaction in value (1.5-3.5%)*

One-off + monthly charge + fee

(based on volume)

One-off

Monthly rental fee

and and and and and

and/or

VAS provider

Monthly charge

Revenue type

and and and/orand/or or

or

N/A

N/A

Monthly (variable)

charge

Revenue type

*Source: Federal reserve of Philadelphia

One-off + monthly charge + fee

(based on volume)

% of transaction in value (1.5-3.5%)*

+ Fixed fee / transaction

Investors presentation - May 2011• 23

easycash integration accelerating the evolution towards services

2009 revenue at 2010

perimeter*

2009 revenue**

2009 combined revenue

One off & fee per month

Revenue business

model

One off & fee per transaction

15%

16%

22%

2009 EBITDA* margin

652 m€

* Excluding Sagem Danemark, Manison and Moneyline Business Systems starting January 1 2009** IFRS based revenue

20%

28%

84%

2009 Revenue * profile % of revenue

from services

17 m€

€762m

€93m

€669m

2009 Adj. EBIT margin

11%

17%

12%

TransactionServices

Hardware & Maintenance Services

€17m€652m

€67m€26m

€84m€678m