fixed income research monthly review: september 2021

TRANSCRIPT

BondAdviser | Fixed Income Advisory and Research Market Review: September 2021

1 1

11 October 2021

Fixed Income Research

Monthly Review: September 2021

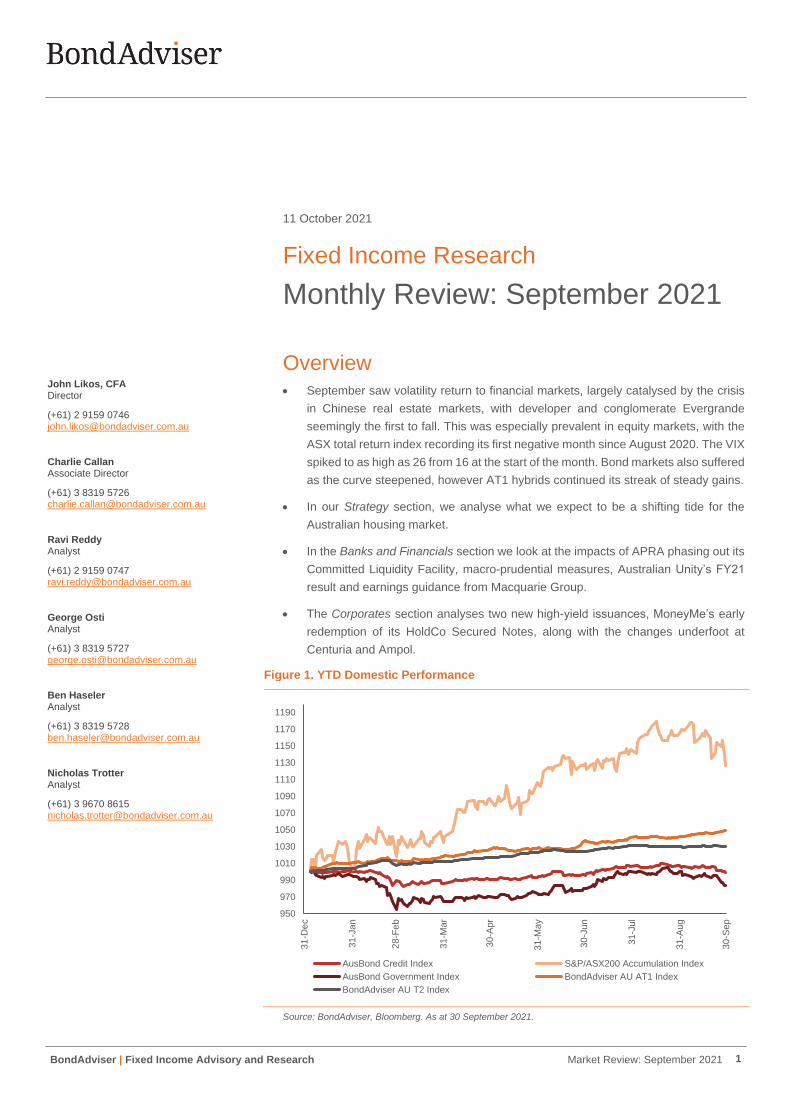

Overview • September saw volatility return to financial markets, largely catalysed by the crisis

in Chinese real estate markets, with developer and conglomerate Evergrande

seemingly the first to fall. This was especially prevalent in equity markets, with the

ASX total return index recording its first negative month since August 2020. The VIX

spiked to as high as 26 from 16 at the start of the month. Bond markets also suffered

as the curve steepened, however AT1 hybrids continued its streak of steady gains.

• In our Strategy section, we analyse what we expect to be a shifting tide for the

Australian housing market.

• In the Banks and Financials section we look at the impacts of APRA phasing out its

Committed Liquidity Facility, macro-prudential measures, Australian Unity’s FY21

result and earnings guidance from Macquarie Group.

• The Corporates section analyses two new high-yield issuances, MoneyMe’s early

redemption of its HoldCo Secured Notes, along with the changes underfoot at

Centuria and Ampol.

Figure 1. YTD Domestic Performance

Source: BondAdviser, Bloomberg. As at 30 September 2021.

950

970

990

1010

1030

1050

1070

1090

1110

1130

1150

1170

1190

31

-De

c

31

-Ja

n

28

-Fe

b

31

-Ma

r

30

-Apr

31

-Ma

y

30

-Ju

n

31

-Ju

l

31

-Aug

30

-Sep

AusBond Credit Index S&P/ASX200 Accumulation Index

AusBond Government Index BondAdviser AU AT1 Index

BondAdviser AU T2 Index

John Likos, CFA Director

(+61) 2 9159 0746 [email protected]

Charlie Callan Associate Director

(+61) 3 8319 5726 [email protected]

Ravi Reddy Analyst

(+61) 2 9159 0747 [email protected]

George Osti Analyst

(+61) 3 8319 5727 [email protected]

Ben Haseler Analyst

(+61) 3 8319 5728 [email protected]

Nicholas Trotter Analyst

(+61) 3 9670 8615 [email protected]

BondAdviser | Fixed Income Advisory and Research Market Review: September 2021 2

Performance

Market Indices

September was a rocky month for financial markets, bringing the rosy, volatility-free

environment for equities in 2021 to a crashing halt. The VIX, a measure of volatility in

US equity markets, gapped upwards as a result of Evergrande Group, a Chinese

property developer, which has failed to make interest payments on its USD bonds.

Equities were not the only markets impacted as a large sell off, especially in junk USD

denominated bonds from Chinese issuers, triggered a global spike in yields.

Our four AusBond indices (see Figure 2) all suffered losses, with the duration-less FRNs

faring better than the hard-hit AusBond Gov Index. Our T2 index recorded another

somewhat flat month, down 0.03% on 31 August levels. BondAdviser’s AT1 index was

the only positive performer in this tumultuous month of unknowns, rising 0.85% for

September.

Figure 2. Monthly Performance - Key Indices

Source: BondAdviser, Bloomberg.

Security Performance

With relatively strong and more importantly, stable performance in the AT1 index during

a month of market-wide contagion, there were some standout securities. The majority of

hybrids went somewhat unchanged for the month of September, with a select few driving

the strong gains for the month. ~70% of our hybrid coverage universe had a monthly

change in margin of less than 0.50%. CBAPE was the standout, tightening by 2.93%,

however this was a function of the security’s maturity date fast approaching (15 October

2021). OBLHA also had a positive month, tightening 1.35%. At the other end, PPCHB

was notable, widening 1.53% by the end of the month, finishing at par ($100.00) after

very slowly repricing downwards from $104.95 post its ex-distribution date of 24

September. As at close on October 6 the price was $100.00. We use this case as an

opportunity to caution investors from buying thinly traded securities in times where some

downward pressure may still be present due to liquidity issues.

-1.85%-1.68%

-1.51%

-0.79%

-0.06% -0.03%

0.85%

-2.50%

-1.50%

-0.50%

0.50%

1.50%

BondAdviser | Fixed Income Advisory and Research Market Review: September 2021 3

Strategy

That’s a nice haircut. Did you do it yourself?

The title of this piece modifies a quote from Michael Burry in the film adaptation of

Micheal Lewis’ novel ‘The Big Short’. Whilst it ties in nicely with the current lockdown

environment, it also ties in with residential housing. We are not housing experts but

sense the tide is turning. We also sense that with appropriate policy measures, there is

no cause for alarm – the alternative is a Miami housing estate and/or Japanification, so

credit investors need to remain vigilant.

Quarter Acre Block a Pipe Dream

We are not at all surprised that record low interest rates have spurred the domestic

housing market forward in 2021. Leaving the hyperbole of anecdotes outside, Australia’s

property prices have been controversial for some time, perhaps because it is easy for

the lay person to grasp the tangible effect of the compounded annual growth rate. For

some, it is a wealth effect, for others, unaffordability.

Since 2004, the ABS Residential Property Price Index has returned a geometric average

of 5.11% p.a. The ASX 200, on a price basis, has only managed 4.60% p.a. over the

same period - noting this is just analysing price, no yield, taxes, dividend return or

reinvestment is factored. It should also be unsurprising to relate such a steady increase

in housing prices, to a base interest rate that has been steadily trending downwards

since the early nineties. When interest rates fall, so do interest repayments, which means

that serviceability increases, allowing mortgagees to borrow more. Interest rates are the

biggest driver of housing prices.

Figure 3: Australian Residential Property Price Index

Source: BondAdviser ABS. As at 30 June 2021.

The explosion in housing prices in 2021 has unnerved many, including bankers at the

coal face. The most notable canaries being the CEOs at CBA and ANZ, both having

publicly opined that housing prices have run too hard.

In September, APRA released data that confirmed the shift in housing market dynamics,

which we have warned about on numerous occasions. Between 2014 and 2017 APRA,

through macro-prudential measures, targeted investor and interest only loans, and

subsequently, as seen in Figure 4, between 2017-2020 first home buyers (FHBs) have

made up an increasingly larger proportion of new home loans. Such trend has reversed

in 2021, with investor loan commitments showing a rapid take-up that is commensurate

in the fall in FHB proportions. A cursory analysis here suggests that FHBs are again

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

0

20

40

60

80

100

120

140

160

180

Resi Price Index YOY Chg (RHS)

BondAdviser | Fixed Income Advisory and Research Market Review: September 2021 4

being squeezed out of ownership by speculators. This is politically unsustainable and

does not carry favour with regulators.

In late-September, Federal Treasurer Josh Frydenberg suggested macro-prudential

measures were being considered by the Council of Financial Regulators (CFR) to reduce

potential financial risks in the banking system from rising residential property prices.

Around the same time, in a speech, RBA Assistant Governor Michele Bullock also

pointed at the risks pertaining to bank and household balance sheets from the sharp rise

in property prices and associated growth in lending. While she acknowledged the

strength of bank balance sheets and maintenance of lending standards, she noted that

risks to financial stability could be building. The matter was addressed by the CFR at its

September 2021 quarter meeting with APRA being handed the task to publish an

information paper in the next few months on the framework for implementing

macroprudential policy.

Figure 4: New Home Loan Commitments (ex-refinance) Mix

Source: BondAdviser, RBA. As at 31 August 2021.

Figure 5 shows that housing lending debt to household disposable income has been

rising steadily for many years and stood at around 140% as at 30 June 2021. However,

due to the aforementioned low interest rates and to a lesser extent, the relatively strong

performance of the Australian economy (healthy employment levels, increased

government support) has meant that the proportion of housing loan interest payments to

household disposable income has declined rapidly since late 2019.

Figure 5: Household Housing Debt and Serviceability

Source: BondAdviser, RBA. As at 30 June 2021.

0%

10%

20%

30%

40%

50%

60%

O/Occ ex FHB First Home Buyers (FHB) Investor

4%

5%

6%

7%

8%

9%

10%

11%

80%

90%

100%

110%

120%

130%

140%

150%

Jan-0

5

Jan-0

6

Jan-0

7

Jan-0

8

Jan-0

9

Jan-1

0

Jan-1

1

Jan-1

2

Jan-1

3

Jan-1

4

Jan-1

5

Jan-1

6

Jan-1

7

Jan-1

8

Jan-1

9

Jan-2

0

Jan-2

1

Housing Loan Debt/Income Housing Int Payments/Income (RHS)

BondAdviser | Fixed Income Advisory and Research Market Review: September 2021 5

Figure 6. ADIs’ New Housing Loans - Debt to Income Ratio

Source: BondAdviser, APRA. As at 30 June 2021.

As illustrated in Figure 6, it is alarming that new loans are being granted to property

buyers with increasingly higher levels of debt relative to the purchaser’s income. Over

the June 2021 quarter, 21.4% of new loans were at least 6x the size of the borrower’s

income. As seen in Figure x, this metric has been on an exponential trajectory over the

past year especially, with the June 2020 quarter at 15.6%.

Another cause for alarm is fraud rates. According to an annual UBS survey (n=900),

41% of those that took out a mortgage over the past year submitted a factually inaccurate

loan application. In the seven years UBS has been conducting this survey on Australians,

it has never recorded such a high reading. Whilst the majority of those that provided an

inaccurate application stated the application was “mostly factual and accurate”, around

a third said the application was only “partially factual and accurate” – this was another

record. Regardless of asset class, an increase in fraud is one of the tell-tale signs of

mania. Chasing the market and falsely stretching one’s capacity limit to ensure

qualification is not sustainable and should be stamped out quickly.

Following the Treasurers speech, on 6 October, APRA surprised many by announcing

an increase in the loan serviceability buffer from 2.50% to 3.00% above the actual

mortgage interest rate that ADI’s use to assess a borrower’s ability to meet interest

repayment commitments. The impact is likely to be modest with the regulator estimating

it will reduce the borrowing capacity of the typical borrower by around 5%. More

substantial measures remain a possibility. We see this move as a signal of further action

to come, APRA’s announcement alone will not de-risk the real estate sector – in many

ways it just lowers the price-based searching criteria for property buyers. Further hard

hitting is needed, albeit gradually, as given the leverage in the system, unwinding is a

tight-rope exercise.

Macro-prudential policies have been introduced in New Zealand, with the RBNZ

reinstating LVR restrictions on home lending in February. However, it has not

significantly slowed the price growth. LVR restrictions were tightened for investor loans

in May and changes for owner occupiers come into effect in November: the 5% limit of

new lending to investors that can be at LVR’s above 60% remains while only 10%

(currently 20%) of new lending to owner occupiers can be at LVR’s greater than 80%.

For the banks, from a credit perspective we are unconcerned, however macro-prudential

tailwinds will take some steam out of earnings growth. The market environment also

stalls the likelihood of scrapping the Responsible Lending laws, as it would appear

without cause (given the boom in prices and credit) and politically unpalatable.

14%

16%

18%

20%

22%

$0b

$20b

$40b

$60b

$80b

$100b

$120b

$140b

$160b

Mar-19 Jun-19 Sep-19 Dec-19 Mar-20 Jun-20 Sep-20 Dec-20 Mar-21 Jun-21

Debt : Income < 4x Debt : Income ≥ 4x < 6x

Debt : Income ≥ 6x Debt : Income ≥ 6x % New Loans (RHS)

BondAdviser | Fixed Income Advisory and Research Market Review: September 2021 6

Banks & Financials

APRA Phases out CLF

On 10 September 2021, APRA announced that commencing 2022, it will start phasing

out the use of the RBA’s Committed Lending Facility (CLF) by ADIs to help meet their

prudential liquidity requirements (as measured by the Liquidity Coverage Ratio, “LCR”)

to zero by the end of 2022. This change was a not a surprise to us, albeit the speed of

phasing out was quicker than expected. We first opined that the excess of liquidity in the

banking sector should be used to support lower yields in January.

Senior bank paper was instantly bid 3-5bps wider on trading desks following the

announcement. We thought this was underdone, as the banks were yet to unwind their

large positions. We have been underweight on expectations of normalisation post the

TFF roll-off. Whilst we believe the TFF impact will be larger than this regulatory change,

at the time we expected closing the CLF should still crystallise 10-20bps of widening.

This has subsequently happened.

Figure 7: BA B4 Senior Unsecured Index*

Source: BondAdviser Index Platform: BAB4SU0DNTR As at 6 October 2021.

By way of background the CLF was introduced in 2015 to compensate for the lack of

available High Quality Liquid Assets (HQLA), which includes government bonds, notes

and coins, and Exchange Settlement Account (ESA) balances with the RBA, that ADIs

could access to meet liquidity requirements. The CLF allowed banks to hold Alternative

Liquid Assets (ALA) such as bank bonds and RMBS for liquidity purposes. This was

designed when Australia had little public debt, which is no longer the case.

Overall, the transition timeframe is reasonable and manageable, and we do not expect

a material deterioration in the robust liquidity profile of bank balance sheets. Importantly,

the CLF will remain available should it be required to meet shortfalls in the availability of

HQLA, which is supportive for confidence in overall sector liquidity. In terms of bank

profitability, there is likely to be pressure on net interest margins for some banks, as ALA

are replaced with lower yielding HQLA – for some time now this has been a tremendous

regulatory arbitrage for treasury desks.

0.10%

0.11%

0.12%

0.13%

0.14%

0.15%

0.16%

0.17%

0.18%

0.19%

0.20%

0.21%

0.22%

0.23%

0.24%

01

-Ju

n-2

1

15

-Ju

n-2

1

29

-Ju

n-2

1

13

-Ju

l-2

1

27

-Ju

l-2

1

10

-Aug

-21

24

-Aug

-21

07

-Sep

-21

21-S

ep

-21

05

-Oct-

21

BondAdviser | Fixed Income Advisory and Research Market Review: September 2021 7

Figure 8: B4 LCR

Source: BondAdviser, Company Reports.

The Big Four held $127 billion in average ALAs over the June 2021 quarter. Based on

their respective positions, this suggests all the major banks except ANZ would need to

replace ALA with HQLA. ANZ is the best placed, having already reduced its reliance on

the CLF. NAB would have met the 100% minimum LCR requirement solely with HQLA,

but the majors will need to continue to hold a healthy buffer above the minimum - though

possibly not as elevated as the current average LCR of around 130%.

Plummeting Iron Ore Price Puts Pressure on Fiscal Position

The slump in iron ore prices due to growing cuts in Chinese steel production has been

further impacted by weaker confidence in expected demand for steel from the property

construction sector as result of the Evergrande crisis. The spot price fell from ~U$229

per tonne in May 2021 to just under US$100 per tonne in mid-September and is now

above US$115.

Figure 9: Spot Iron Ore

Source: BondAdviser, Bloomberg. As at 28 September 2021.

$210B

$128B$143B

$123B

$10B

$44B

$38B

$36B

135%129% 129% 127%

0%

20%

40%

60%

80%

100%

120%

140%

$30B

$60B

$90B

$120B

$150B

$180B

$210B

$240B

ANZ CBA NAB WBC

100% Minimum (RHS) HQLA

ALA RBNZ

LCR % (RHS) LCR % HQLA Only (RHS)

US$75/T

US$100/T

US$125/T

US$150/T

US$175/T

US$200/T

US$225/T

US$250/T

Se

p-2

0

Oct-

20

No

v-2

0

De

c-2

0

Ja

n-2

1

Fe

b-2

1

Ma

r-2

1

Ap

r-2

1

Ma

y-2

1

Ju

n-2

1

Ju

l-2

1

Aug

-21

BondAdviser | Fixed Income Advisory and Research Market Review: September 2021 8

This will hurt the pace of Australia’s economic recovery, which has already been dented

by recent extended lockdowns, and consequently places pressure on the Federal budget

deficit. According to the 2021-22 Federal Budget Papers, a US $10 per tonne fall in the

iron price will reduce FY22 GDP by ~$6.5 billion and tax receipts ~$1.3 billion. However,

the iron ore price is still above the US$55 per tonne forecast by the end of the March

2022 quarter in the Budget.

A weaker budget position could put Australia’s sovereign credit rating at risk. We see

this risk being somewhat underappreciated in the current environment. Any changes to

the sovereign rating will also impact the ratings of the Major Banks and Macquarie Bank

as they assume government support. We note S&P upgraded Australia’s credit rating

outlook from Negative to Stable in early June 2021, given the better than expected

economic recovery and fiscal outlook, but S&P has assumed a slower pace of decline in

the iron ore price than Government forecasts.

Loan Deferrals on the Rise

APRA data to 31 August 2021 showed that $11.9 billion worth of loans were in temporary

loan repayment deferral arrangements representing 0.5% of total loans outstanding, up

from $5.6 billion at the end of July. Housing loans comprised $11.9 billion (0.7% of total

home loans) with the remaining balance, $765 million, in SME loans (0.3% of total SME

loans). Given the extended lockdown in Sydney, it is no surprise NSW had the highest

proportion of loans subject to deferral, at 1.4% per. According to the Australian Banking

Association, as at 5 September 2021 NSW made up the bulk of all deferrals by number

– 69% of home loans and 72% of business loans.

This is well below the peak of above $250 billion of loans subject to deferral in 2020, but

with parts of Australian still in lockdown, we expect these numbers will rise. Importantly

though, we believe the banks are well placed to cope with any higher impairments as a

result of these lockdowns, given strong CET1 levels and loss provisions being held

above pre-pandemic levels despite some unwinding that has occurred this year.

Changes in the Australian LMI Landscape

Westpac (ASX: WBC) has completed the $350m sale of Westpac Lenders Mortgage

Insurance to Arch Capital Group. The sale is consistent with the Bank’s strategy of

focussing on its core business. This will increase CET1 capital by ~7bps. WBC’s pro-

forma CET1 as at 30 June 2021 was 12.5% post announced and completed asset sales,

placing it well above the unquestionably strong benchmark of 10.5%. WBC is the only

one of the Big Four that has not announced capital management initiatives, though at

the 3Q21 update the potential of a buy-back was raised, with a decision likely to be

revealed at the FY21 results in November 2021.

There is more competitive tension in the LMI market now with the recent entry of Arch

Capital. QBE Insurance Group (ASX: QBE) and Genworth Financial Mortgage Insurance

(ASX: GMA) are the other two players. We expect Arch Capital will be looking to bulk up

its LMI insurance book and as such is likely to be a keen bidder for Commonwealth

Bank’s LMI contract. The contract is currently with Genworth and expires at the end of

December 2022. The potential loss of this contract is a key earnings risk for Genworth

as it represented 57% of FY20 gross written premium. Wholesale and institutional

subscribers can click here for our research on Genworth Subordinated Notes II.

AYU FY21 Result – Credit Positive

We maintained a Stable view on Australian Unity’s (ASX: AYU) credit outlook after the

FY21 result. Overall, it was a sound performance in a challenging environment as

COVID-19 continued to have impacts across the Group. The result was positive for the

Group’s credit profile given the stronger earnings performance and generally improved

balance sheet metrics.

BondAdviser | Fixed Income Advisory and Research Market Review: September 2021 9

Segment adjusted EBITDA was up 19% to $180.2 million, driven by stronger

performances across Independent & Assisted Living and Retail, which outweighed

weakness in Wealth and Capital Markets. After Group corporate costs, Group adjusted

EBITDA rose 29% to $98.9 million.

No FY22 earnings guidance was provided but the business is well placed to leverage

favourable demographic dynamics of a growing and aging population over the long-term.

MQG Guides for Another Strong Result

Macquarie Group (ASX: MQG) provided first time guidance for 1H22 – it is expected to

be slightly down on 2H21 (NPAT: $2.03 billion). Regardless, it still points to another

bumper result, noting it will be well up on 1H21 ($985 million) and 2H20 ($1.27 billion).

This reflects advantageous operating conditions that have led to a stronger than

expected performance in the Commodities and Global Markets segment along with the

sale of the UK commercial and industrial smart meter businesses. As always, the

guidance is subject to a range of factors, including market conditions and the timing of

transactions. Importantly, given the risks from COVID-19, market volatility and

geopolitical issues, the Group reiterated its focus on maintaining conservative capital,

funding and liquidity settings.

BondAdviser | Fixed Income Advisory and Research Market Review: September 2021 10

Corporates

Centuria Continue Expansion with CIP’s Investment Grade

On 22 September 2021, Moody’s assigned the Centuria Industrial REIT (ASX: CIP) a

Baa2 credit rating at the Issuer level. CIP upstreams distributions to Centuria’s HoldCo

Issuer (Centuria Capital No. 2 Fund, “C2F”), which owns a ~17% stake in CIP. In

obtaining a credit rating, we expect CIP to transition towards a more traditional REIT

capital structure, given it now has the size to facilitate larger capital market transactions.

In time, we suspect CIP will issue bonds that will repay revolving bank facilities. Whilst

there may be an incremental increase in leverage (we estimate about $150 million of

debt headroom against the gearing rating metric), we see the funding diversity benefits

as somewhat offsetting.

The next day, CIP announced it would conduct an equity raising worth ~$325 million

(successfully raised $300 million) to partially assist in the funding of a new portfolio

acquisition worth ~$351 million, initially yielding 4.1% on average, across eight assets.

The portfolio will also help to reduce the cap rate for CIP which has consistently fallen

each half since 1H16 at ~7.4%. Whilst WALEs will incrementally fall, this positively

continues the trend of funding any new acquisitions with a large equity component. This

equity raise is positive both in terms of a growth narrative for the Trust, and from a

creditor perspective as we originally expected to see increased leverage following the

investment grade credit rating. That said, the news was taken poorly by shareholders,

with the price of CIP stock falling 6% in a day and has since declined further. Our

Centuria bond recommendations remain unchanged.

Getting MeMoney Back Early

On 27 September 2021, MoneyMe (ASX: MME) announced it had secured a $50 million

funding commitment from Pacific Equity Partners (PEP), by way of a four-year secured

hybrid funding instrument. This facility will be used to repay the existing $22 million

HoldCo Secured Notes.

The facility is a senior secured HoldCo loan, which has a variable step-up coupon that

is contingent on an increase in market valuation, subject to a ceiling of 4.5%. In addition,

PEP will receive warrants which entitle issuance or cash settlement of up to a maximum

of 5 million shares (3.4% of total shares today). The equity upside embedded within the

facility decreases the nominal interest rate.

We highlighted in August that we expected additional capital would be needed by

November and whilst the new structure is somewhat unique, it has crystallised our

opinion that the bonds were underpricing the likelihood of new capital.

The HoldCo Secured Notes settled in April 2021 and following our initial Subscribe

recommendation, we have maintained a Buy. Assuming the bonds are redeemed on 27

October 2021, at 105% of par, the IRR will be 19.0% from our initial Subscribe and

an impressive 36.6% since our latest Buy recommendation.

Latitude Not Yet Off into the Horizon

Latitude Group Holdings (ASX: LFS) launched an Offer for Latitude Capital Notes (ASX:

LFSPA) on September 2. The issuance was in high demand, raising $150 million ($25

million in excess of the original $125 million target) and pricing at the lower bound of the

4.75-5.00% margin range. The Notes commenced trading on 29 September and

experienced some weakness in its first few days, trading up to 25bps wider than at

issuance. At launch, LFSPA priced 99, 179, and 221bps above the respective

Challenger, regional bank, and Big Four bank curves. Those margins are now

significantly wider at 119, 199 and 238bps.

BondAdviser | Fixed Income Advisory and Research Market Review: September 2021 11

Figure 10: AT1 and LFSPA Trading Margin

Source: BondAdviser, ASX, Bloomberg, as at 30 September 2021.

New Issue - CAIG

On 28 September, Capital Alliance Investment Group, through Capital Alliance Au Pty

Ltd launched an offer for fixed rate HoldCo Secured Notes at an initial margin range of

9.00-10.00%. CAIG are looking to raise $50 million to increase working capital for

general corporate purposes and funding the Group’s development pipeline. Being a

developer, manager and owner of both commercial and residential property provides the

Group with a diverse stream of cashflows. CAIG’s historical operating model has been

to develop a mixed-use property with both commercial features such as a hotel or offices

along with residential apartments. Post-development, the Group has maintained

ownership of the commercial assets and typically sold the apartments. This provides for

smoother earnings compared to a typical developer that will sell all assets once

developed, whereby CAIG receives income both from management and from asset

sales.

Figure 11: Yield - USD Lodging Curves (CAIG ASW to USD)

Source: BondAdviser, Bloomberg, as at 27 September 2021. CAIG based on 9% coupon, cross-currency asset swap into USD.

As the majority of the Group’s income is expected to be sourced from 5-star hotel

tenancies in the medium-term, we view the earnings of the Group most comparable to

the lodging universe. Below in Figure [x] it can be seen that at the lower bound of IPT,

the Notes sit at a clear premium to the B-rated lodging curve. As the delta between the

CBAPJ, 2.47%

CBAPI, 2.53%

NABPF, 2.25%WBCPJ, 2.43%

MQGPD, 2.77%

MQGPE, 2.79%

MBLPC, 2.55% SUNPH, 2.71%

AMPPB, 4.90%

BOQPF, 2.89%

BENPH, 2.86%

CGFPC, 3.56%

LFSPA, 4.80%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

5.0%

5.5%

4 4.2 4.4 4.6 4.8 5 5.2 5.4 5.6 5.8 6

Tra

din

g M

arg

in

Term to Expected Call

CAIG

CCC

Represents $500m Issuance

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

0 1 2 3 4 5 6 7 8 9 10

Op

tio

n A

dju

ste

d S

pre

ad

Term to Call

BBB Curve BB Curve B Curve

BondAdviser | Fixed Income Advisory and Research Market Review: September 2021 12

2- and 4-year markers for both the BBB and BB curves is 24bps, we view the 79bps for

an additional 1.5 years against the outstanding CCC bonds to be a suitable term

premium compensation. Click here to read the full IPO Report.

Bartering Taking Longer Than Expected at Ampol

Z Energy (NZX: ZEL) provided an update on 27 September with regards to the

acquisition proposal from Ampol (ASX: ALD), which was first announced at the release

of ALD’s FY21 results on 23 August. The news provided by Z Energy was that there was

no news. Z advised investors that the original four-week exclusivity period provided to

Ampol had been extended by two weeks. Ampol and Z have been unable to yet address

outstanding matters or agree on key transaction terms. The two parties have announced

there isn’t any certainty that the acquisition will go ahead but a market update can be

expected on or before 11 October.

Qantas Tap $200 Million Excess in Early Refinance

On 16 September, Qantas Airways Ltd (ASX: QAN) raised $500 million with a 7-year

senior unsecured issuance, refinancing the outstanding $300 million Note that matures

in May 2022. As the maturing bonds are unable to be called early, we view the early

timing of the raise to be supportive of the Group in this constricted operating

environment. The 2028 Notes priced 20 basis points below initial price talks at 3.15%

and will help significantly reduce QAN’s cost of debt given the coupon of 7.75% for the

2022 Notes.

Moody’s reiterated Qantas’ Baa2 credit rating on 18 September, taking a similar stance

to that of its view on fellow struggling Australian business, Crown Resorts (ASX: CWN)

- that the current operating pressures are not permanent, Qantas are established as a

dominant market leader and the Group has a strong balance sheet to support it through

likely the final stretch of COVID-induced struggles. As at June 30, Qantas’ debt to

EBITDA ratio was already in excess of Moody’s threshold before downgrading the credit

rating, and as such the Outlook held for QAN was Negative. We are not concerned by

the long-run implications of an additional $200 million in debt, however, leverage will be

high as at 1H22 should no further changes be made to the capital structure as both the

2022 and 2028 Notes will be outstanding. Given the low rate of the 2028 Notes we would

be pleased to see the Group use the excess $200 million to pay down bank debt.

In response to the Federal Government’s announcement for international travel bans to

be uplifted on 14 November 2021 for states with greater than 80% of its population

double vaccinated, Qantas announced its return to London and Los Angeles. Given

management’s expectation was 1 December 2021 this has little impact on our earnings

expectations. Unfortunately, 1H22 will likely be the hardest Qantas are hit as a result of

the pandemic. We believe credit rating agencies will continue to look through this, given

the Group’s lion share of the domestic air travel market in combination with the revenge

spend upon borders reopening sure to provide for a sharp rebound in earnings.

BondAdviser | Fixed Income Advisory and Research Market Review: September 2021 13

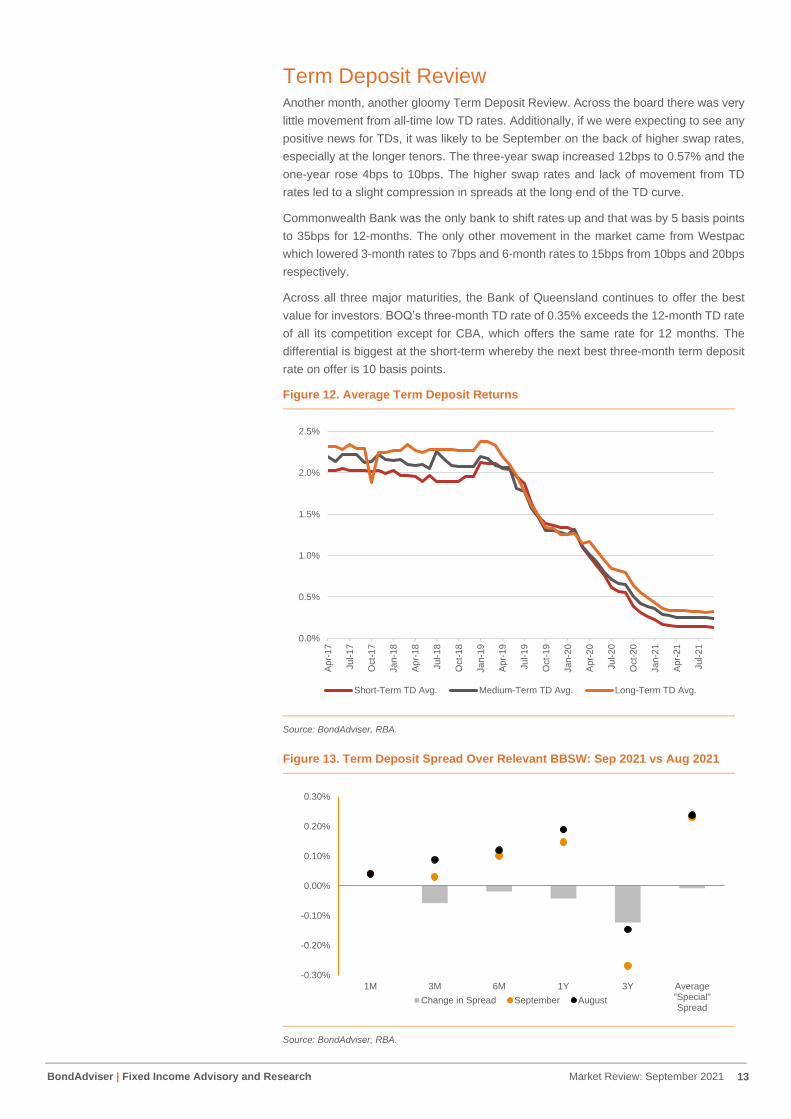

Term Deposit Review Another month, another gloomy Term Deposit Review. Across the board there was very

little movement from all-time low TD rates. Additionally, if we were expecting to see any

positive news for TDs, it was likely to be September on the back of higher swap rates,

especially at the longer tenors. The three-year swap increased 12bps to 0.57% and the

one-year rose 4bps to 10bps. The higher swap rates and lack of movement from TD

rates led to a slight compression in spreads at the long end of the TD curve.

Commonwealth Bank was the only bank to shift rates up and that was by 5 basis points

to 35bps for 12-months. The only other movement in the market came from Westpac

which lowered 3-month rates to 7bps and 6-month rates to 15bps from 10bps and 20bps

respectively.

Across all three major maturities, the Bank of Queensland continues to offer the best

value for investors. BOQ’s three-month TD rate of 0.35% exceeds the 12-month TD rate

of all its competition except for CBA, which offers the same rate for 12 months. The

differential is biggest at the short-term whereby the next best three-month term deposit

rate on offer is 10 basis points.

Figure 12. Average Term Deposit Returns

Source: BondAdviser, RBA.

Figure 13. Term Deposit Spread Over Relevant BBSW: Sep 2021 vs Aug 2021

Source: BondAdviser, RBA.

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

Ap

r-1

7

Ju

l-1

7

Oct-

17

Ja

n-1

8

Ap

r-1

8

Ju

l-1

8

Oct-

18

Ja

n-1

9

Ap

r-1

9

Ju

l-1

9

Oct-

19

Ja

n-2

0

Ap

r-2

0

Ju

l-2

0

Oct-

20

Ja

n-2

1

Ap

r-2

1

Ju

l-2

1Short-Term TD Avg. Medium-Term TD Avg. Long-Term TD Avg.

-0.30%

-0.20%

-0.10%

0.00%

0.10%

0.20%

0.30%

1M 3M 6M 1Y 3Y Average"Special"Spread

Change in Spread September August

BondAdviser | Fixed Income Advisory and Research Market Review: September 2021 14

Figure 14. Δ Annual LT TD Rates

7 7

Source: BondAdviser, Company Websites, RBA. Note Long-Term ~12m.

Figure 15. LT Deposit Rates

7 7

Source: BondAdviser, Company Websites, RBA. Note Long-Term ~12m.

Figure 16. MT Deposit Rates

Source: BondAdviser, Company Websites, RBA. Note Medium-Term ~6m.

Figure 17. ST Deposit Rates

Source: BondAdviser, Company Websites, RBA. Note Short-Term ~3m.

-0.45% -0.45%

-0.55%

-0.45%-0.50%

-0.40%

-0.8%

-0.6%

-0.4%

-0.2%

0.0%

ANZ CBA NAB WBC BEN BOQ

0.20%0.25%

0.15% 0.15%0.20%

0.40%

0.00%

0.20%

0.40%

ANZ CBA NAB WBC BEN BOQ

1 Yr Swap Spread over 1Yr Swap

0.15% 0.15% 0.15%0.10%

0.25%

0.35%

0.00%

0.20%

0.40%

ANZ CBA NAB WBC BEN BOQBBSW6M Spread over BBSW6M

0.08% 0.06% 0.08%0.05%

0.08%

0.33%

0.00%

0.20%

0.40%

ANZ CBA NAB WBC BEN BOQ

BBSW3M Spread over BBSW3M

BondAdviser | Fixed Income Advisory and Research Market Review: September 2021 15

Key Events

Date Description

3 September Moody’s places AGL onto a negative outlook citing risks of the

announced demerger to AGL’s credit profile.

APRA publishes a report outlining its Climate Vulnerability

Assessment which it is undertaking with the Big 5.

7 September RBA releases its monthly Monetary Policy Decision, holding the

cash rate target at 10bps and announcing it will maintain its

government bond purchase program at $4bn a week until at least

Feb 2022.

Reports indicate that Qantas has progressed the process to sell

$550m of undeveloped Sydney property, having shortlisted bidders.

8 September Evergrande’s share price falls below its IPO price following a

second downgrade in two days as it announces that a default

seems probable.

9 September In its Annual Report, Crown’s auditor KPMG issues a formal notice

that there is a ‘material uncertainty’ that Crown will be able to

continue as a ‘going concern’.

10 September APRA announces it will require ADIs to end their reliance on the

CLF by the end of 2022, subject to market conditions.

Santos and Oil Search finalise their merger agreement to form a

$21bn, top 20 global oil and gas company.

14 September US August CPI is weaker than expected with headline CPI rising

0.3% MoM (expected: 0.4%; prior: 0.5%) and core CPI rising 0.1%

MoM (expected: 0.3%; prior: 0.3%).

Perth Airport has commenced legal proceedings in WA Supreme

Court against Qantas, claiming it is owed ~$17m in unpaid fees for

aeronautical services provided in 2018.

15 September WBC updates the market on the sale of its Pacific business,

reporting the PNG’s Competition Commission provided its final

determination to deny approval to Kina Bank to purchase the

business.

16 September Telstra provides a number of strategic updates at its Investor Day,

revealing its T25 strategy. Notable announcements include an

expectation for mid-single digit EBITDA growth between FY21-

FY25.

17 September Wesfarmers revises its non-binding offer to acquire Australian

Pharmaceutical Industries to $1.55 per share, up from $1.38.

BondAdviser | Fixed Income Advisory and Research Market Review: September 2021 16

Date Description

20 September AusNet Services receives an indicative, non-binding offer from

Brookfield Asset Management at $2.50 cash per share. AusNet’s

Board has granted Brookfield exclusive due diligence.

22 September APA Group announces it has made a non-binding offer of $2.60

cash per share to acquire AusNet Services.

23 September IAG announces it has received 435 claims relating to the Victorian

earthquake. Suncorp reports it has received minimal claims and

does not expect a big expense impact.

29 September Australia’s Council of Financial Regulators (RBA, ARPA, ASIC,

Treasury) announce they have formally discussed the possibility of

tightening macro-prudential policy and that APRA will publish a

paper setting out a framework in the coming months.

30 September APRA reports that loan deferrals remained very low ($12bn)

through to August compared to 2020.

BondAdviser | Fixed Income Advisory and Research Market Review: September 2021 17

New Issue Monitor

ISIN / ASX Code Issue Date Issuer Structural Position

Coupon Term (Yrs)

Issue Size ($m)

1 Month Δ Price

AU3CB0277077 15/01/2021 European

Investment Bank Sr

Unsecured 0.75% 7 1,250 1.09%

AU3CB0277036 15/01/2021 Australia Pacific Mortgage Fund

Ltd Secured 7.00% 2 15 0.02%

AU3CB0277168 20/01/2021 University of Melbourne

Sr Unsecured

1.97% 10 150 2.57%

AU3FN0058103 21/01/2021 Heartland

Australia Group Pty Ltd

Sr Unsecured

2.11% 2 75 0.06%

AU3CB0277291 27/01/2021 European

Investment Bank Sr

Unsecured 1.30% 10 300 2.71%

AU3CB0277234 27/01/2021 Asian

Development Bank

Sr Unsecured

1.30% 10 200 2.80%

AU3FN0058129 29/01/2021 Westpac

Banking Corp Subordinated 1.56% 10 1,250 0.08%

AU3CB0277432 4/02/2021 Inter-American Development

Bank

Sr Unsecured

1.00% 8 300 1.82%

AU3FN0058244 17/02/2021 Defence Bank

Ltd Subordinated 3.16% 10 15 0.66%

AU3CB0277796 19/02/2021 European

Investment Bank Sr

Unsecured 1.90% 15 200 4.14%

AU3CB0277960 23/02/2021 Australia Pacific Mortgage Fund

Ltd Secured 6.75% 1 13 0.09%

AU3FN0058343 24/02/2021 Suncorp-

Metway Ltd Sr

Unsecured 0.46% 5 750 0.27%

AU3CB0278174 26/02/2021 UBS

AG/Australia Sr

Unsecured 1.10% 5 300 0.81%

AU3FN0058608 26/02/2021 UBS

AG/Australia Sr

Unsecured 0.53% 5 700 0.20%

AU3FN0058699 4/03/2021

Newcastle Permanent

Building Society Ltd

Sr Unsecured

0.66% 5 225 0.10%

AU3CB0278380 9/03/2021 Aurizon Finance

Pty Ltd Sr

Unsecured 3.00% 7 500 1.97%

AU3FN0059200 17/03/2021 Liberty Financial

Pty Ltd Sr

Unsecured 2.48% 4 200 0.08%

AU0000136442 17/03/2021 Macquarie Group Ltd

AT1 2.91% 7 725 0.40%

AU3CB0278653 18/03/021 Mirvac Group Finance Ltd

Sr Unsecured

2.60% 9 300 2.19%

AU3CB0278869 23/03/2021 Verizon

Communications Inc

Sr Unsecured

2.35% 7 600 1.26%

AU3CB0278877 23/03/2021 Verizon

Communications Inc

Sr Unsecured

3.00% 7 500 2.67%

BondAdviser | Fixed Income Advisory and Research Market Review: September 2021 18

ISIN / ASX Code Issue Date Issuer Structural Position

Coupon Term (Yrs)

Issue Size ($m)

1 Month Δ Price

AU3CB0278885 23/03/2021 Verizon

Communications Inc

Sr Unsecured

3.85% 20 150 4.79%

AU3CB0278893 24/03/2021 Stockland Trust Sr

Unsecured 2.30% 7 300 1.54%

AU3FN0059424 26/03/2021 MUFG Bank Ltd/Sydney

Sr Unsecured

0.51% 4 750 0.14%

AU3CB0278711 31/03/2021 Lendlease

Finance Ltd Sr

Unsecured 3.70% 10 300 2.65%

AU3CB0279057 31/03/2021 WestConnex

Finance Co Pty Ltd

Secured 3.15% 10 650 2.76%

AU0000138927 1/04/2021 Commonwealth

Bank of Australia

AT1 2.76% 6 1,180 0.04%

AU3FN0059531 7/04/2021

Australia & New Zealand

Banking Group Ltd

Sr Unsecured

0.18% 1 200 0.06%

AU3FN0059523 7/04/2021

Australia & New Zealand

Banking Group Ltd

Sr Unsecured

0.14% 1 1200 0.02%

AU3FN0059549 9/04/2021 Macquarie Bank

Ltd Sr

Unsecured 0.22% 1 150 0.04%

AU0000140014 15/04/2021 NAOS Emerging

Opportunities Company Ltd

Sr Unsecured

4.50% 5 23 -

AU0000143364 20/04/2021 Centuria Capital

No 2 Fund Secured 4.29% 5 190 0.09%

AU3FN0059994 21/04/2021 Victoria Power

Networks Finance Pty Ltd

Sr Unsecured

0.84% 5 175 0.04%

AU3CB0279651 21/04/2021 Victoria Power

Networks Finance Pty Ltd

Sr Unsecured

1.60% 5 325 0.55%

AU3CB0279644 21/04/2021 Victoria Power

Networks Finance Pty Ltd

Sr Unsecured

2.13% 7 200 1.79%

AU3CB0279560 21/04/2021 CHC Finance

Pty Ltd Sr

Unsecured 3.09% 10 250 2.72%

AU3FN0059721 22/04/2021 Credit Union Australia Ltd

Sr Unsecured

0.72% 5 100 0.10%

AU3CB0279578 23/04/2021 NSW Electricity

Networks Finance Pty Ltd

Secured 2.73% 10 300 1.93%

AU3CB0279891 28/04/2021 Australian Gas Networks Ltd

Secured 2.15% 7 250 1.60%

AU3CB0279883 28/04/2021 Australian Gas Networks Ltd

Secured 2.82% 10 200 2.77%

AU3FN0060091 29/04/2021 Bank of

Queensland Ltd Subordinated 1.64% 10 250 0.01%

AU3CB0279925 29/04/2021 MoneyMe Ltd Secured 8.25% 4 15 0.46%

AU3CB0280402 4/05/2021 IMB Ltd Subordinated 2.54% 10 70 0.38%

BondAdviser | Fixed Income Advisory and Research Market Review: September 2021 19

ISIN / ASX Code Issue Date Issuer Structural Position

Coupon Term (Yrs)

Issue Size ($m)

1 Month Δ Price

AU3FN0060448 5/05/2021 Network

Finance Co Pty Ltd

Secured 2.58% 7 350 0.04%

AU3FN0060406 5/05/2021 Transurban Queensland

Finance Pty Ltd Secured 3.25% 10 300 0.12%

AU3FN0060182 6/05/2021 Bank of

Queensland Ltd Sr

Unsecured 0.67% 5 425 0.80%

AU3CB0279958 6/05/2021 Bank of

Queensland Ltd Sr

Unsecured 1.40% 5 225 2.57%

AU3CB0280295 20/05/2021 Woori

Bank/Sydney Sr

Unsecured 0.31% 1 100 2.93%

AU3CB0280394 20/05/2021 Barclays PLC Sr

Unsecured 2.06% 6 150 4.29%

AU3CB0280287 20/05/2021 Barclays PLC Sr

Unsecured 3.38% 11 200 0.89%

AU3FN0060463 20/05/2021 Barclays PLC Sr

Unsecured 1.29% 6 250 0.00%

AU3CB0280006 24/05/2021 PACCAR

Financial Pty Ltd Sr

Unsecured 0.75% 3 150 1.68%

AU3CB0280030 25/05/2021 Liberty Financial

Pty Ltd Sr

Unsecured 2.59% 5 200 0.72%

AU3CB0280634 2/06/2021 NBN Co Ltd Sr

Unsecured 2.15% 7 350 1.77%

AU3FN0060638 4/06/2021 Peet Ltd Sr

Unsecured 4.88% 5 75 1.48%

AU3FN0060737 8/06/2021 Avanti Finance

Ltd Sr Secured 4.77% 4 70 0.25%

AU3CB0280915 15/06/2021 Aurizon Network

Pty Ltd Sr

Unsecured 3.29% 11 75 4.39%

AU3FN0061016 16/06/2021 Teachers Mutual

Bank Ltd Sr

Unsecured 0.70% 5 100 0.05%

AU3FN0061024 16/06/2021 MyState Bank

Ltd Sr

Unsecured 0.67% 4 50 0.28%

AU3FN0061065 17/06/2021 Macquarie Bank

Ltd Subordinated 1.57% 10 750 0.04%

AU3CB0280956 17/06/2021 Charter Hall LWR Pty Ltd

Sr Unsecured

2.66% 9 200 2.66%

AU3FN0061081 18/06/2021 Bendigo &

Adelaide Bank Ltd

Sr Unsecured

0.67% 5 225 0.08%

AU3CB0281053 23/06/2021 Wesfarmers Ltd Sr

Unsecured 2.55% 10 350 2.94%

AU3CB0281046 23/06/2021 Wesfarmers Ltd Sr

Unsecured 1.94% 7 650 1.80%

AU3CB0281145 24/06/2021 AGI Finance Pty

Ltd Sr Secured 2.12% 6 450 0.92%

BondAdviser | Fixed Income Advisory and Research Market Review: September 2021 20

ISIN / ASX Code Issue Date Issuer Structural Position

Coupon Term (Yrs)

Issue Size ($m)

1 Month Δ Price

AU3CB0281152 24/06/2021 AGI Finance Pty

Ltd Sr Secured 2.94% 10 125 2.81%

AU3FN0061099 24/06/2021 Judo Bank Pty

Ltd Subordinated 4.53% 10 50 2.05%

AU3CB0281251 29/06/2021 Llitst Finance

Pty Ltd Sr

Unsecured 2.85% 9 200 2.76%

AU3CB0281293 2/07/2021 Emeco Pty Ltd Sr

Unsecured 6.25% 5 250 0.41%

AU3FN0061172 2/07/2021 Victoria Power

Networks Finance Pty Ltd

Sr Unsecured

0.93% 10 50 0.31%

AU3FN0061289 9/07/2021 Heartland

Australia Group Pty Ltd

Company Guarnt

2.03% 3 45 0.05%

AU3FN0061404 15/07/2021 Banco

Santander SA Sr

Unsecured 0.88% 5 425 0.64%

AU3CB0281608 15/07/2021 Banco

Santander SA Sr

Unsecured 1.65% 5 100 0.21%

AU3CB0281582 15/07/2021 Edith Cowan

University Sr

Unsecured 2.74% 12 150 2.88%

AU3CB0281590 15/07/2021 Edith Cowan

University Sr

Unsecured 3.40% 20 100 4.60%

AU3FN0061412 15/07/2021 Commonwealth

Bank of Australia

Sr Unsecured

0.33% 5 20 0.01%

AU3CB0281681 23/07/2021 Pallas FM Trust Sr Secured 7.00% 1 9 -

AU3CB0281418 7/08/2021 CNH Industrial

Capital Australia Pty Ltd

Sr Unsecured

1.75% 3 200 0.04%

AU3SG000253 12/08/2021 Northern Territory Treasury

Sr Unsecured

3.00% 30 80 6.74%

AU3SG000254 16/08/2021 South Australian

Government Sr

Unsecured 0.089% 1 500 0.03%

AU3CB028234 18/08/2021 Export Finance

& Insurance Sr

Unsecured 1.465% 10 250 2.94%

AU3CB028233 18/08/2021 Victoria Power

Networks Finance

Sr Unsecured

2.195% 10 50 2.91%

AU3FN006252 19/08/2021 ING Bank

Australia Ltd Secured 0.412% 5 625 0.05%

AU3CB028235 19/08/2021 ING Bank

Australia Ltd Secured 1.10% 4 120 0.98%

AU3FN006264 23/08/2021 Victoria Power

Networks Finance

Sr Unsecured

0.51% 3 300 0.03%

AU0000170284 27/08/2021 Macquarie Bank

Ltd AT1 2.91% 7 655 0.01%

AU3FN006276 30/08/2021 Cooperative

Rabobank UA Sr Preferred 0.072% 1 100 0.04%

BondAdviser | Fixed Income Advisory and Research Market Review: September 2021 21

ISIN / ASX Code Issue Date Issuer Structural Position

Coupon Term (Yrs)

Issue Size ($m)

1 Month Δ Price

AU3FN0062816 7/09/2021 United Energy Distribution Pty

Ltd

Sr Unsecured

0.48% 3 130 -

AU3CB0282945 9/09/2021 Toyota Finance

Australia Ltd Sr

Unsecured 0.85% 3 275 -

AU3FN0062824 9/09/2021 Toyota Finance

Australia Ltd Sr

Unsecured 0.44% 3 425 -

AU3FN0062964 15/09/2021 Suncorp-

Metway Ltd Sr

Unsecured 0.49% 5 750 -

AU3FN0062998 15/09/2021 Toyota Finance

Australia Ltd Sr

Unsecured 0.36% 2 100 -

AU0000172470 15/09/2021 Westpac

Banking Corp AT1 2.91% 8 1,750 -

AU3FN0062915 16/09/2021 Australian

Central Credit Union Ltd

Subordinated 2.41% 10 75 -

AU3CB0283059 21/09/2021 VER Finco Pty

Ltd Sr

Unsecured 2.4% 7 200 -

AU3FN0063103 23/09/2021 Commonwealth

Bank of Australia

Sr Unsecured

0.43% 5 500 -

AU0000173551 23/09/2021 Suncorp-

Metway Ltd AT1 2.91% 7 405 -

AU3CB0283224 24/09/2021

Shopping Centres

Australasia Property Retail

Trust

Sr Unsecured

2.45% 8 250 -

AU3SG0002587 24/09/2021 Northern Territory

Treasury Corp

Sr Unsecured

2.75% 20 100 -

AU3FN0063095 24/09/2021 Woori

Bank/Sydney Sr

Unsecured 0.20% 1 50 -

AU3CB0283182 27/09/2021 Qantas Airways

Ltd Sr

Unsecured 3.15% 7 500 -

AU3CB0283356 27/09/2021 Commonwealth

Bank of Australia

Sr Unsecured

1.09% 5 50 -

AU0000176901 28/09/2021 Latitude Group

Holdings Subordinated 4.76% 5 150 -

BondAdviser | Fixed Income Advisory and Research Market Review: September 2021 22

AT1 Curve and Data

Figure 18. ASX AT1 Trading Margin

Arial

Figure 19. AT1 Primary & Weighted Average Secondary Yield to Call**

Last 1m 3m YTD 1y 3y 5y Inception^

Yield to Call 3.06% 2.85% 2.85% 3.05% 3.22% 5.49% 5.95% 7.26%

%Δ 7.37% 7.37% 0.33% -4.97% -44.26% -48.57% -57.85%

Trading Margin 2.31% 2.33% 2.24% 2.79% 3.01% 3.12% 4.02% 0.79%

%Δ -0.86% 3.13% -17.20% -23.26% -25.96% -42.54% 192.41%

Source: BondAdviser Index Platform: BAAUAT1DFTR ** Weighted average based on market capitalisation. BAAUAT1DFTR is a franked, total return index that is rebalanced on a daily basis. Yield to call based on BondAdviser estimates. ^Inception of BAAUAT1DFTR is 16/5/2007.

WBCPG

AMPPA

ANZPE

CBAPF

CGFPA

SUNPF

NABPD

WBCPE

CBAPD

ANZPF

CGFPB

IAGPD

ANZPG

CBAPH

BENPG

SUNPGWBCPI

BOQPE

MQGPCANZPH

CBAPG

WBCPH

AMPPB

MBLPC

CGFPC

SUNPH

MQGPD

CBAPJ

WBCPJ

CBAPI

BOQPF

BENPHMQGPE

NABPHANZPI

SUNPI WBCPK

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

0 1 2 3 4 5 6 7 8

0%

2%

4%

6%

8%

10%

12%

14%

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

Yield to Call** AMP SUN/SBK MQG/MBL BEN BOQ CGF

IAG SGB ANZ CBA NAB WBC

BondAdviser | Fixed Income Advisory and Research Market Review: September 2021 23

T2 Curve and Data

Figure 20. T2 Trading Margin

Figure 21. T2 Primary & Weighted Average Secondary Yield to Call**

Last 1m 3m YTD 1y 3y 5y Inception^

Yield to Call 1.98% 1.84% 2.02% 2.14% 2.43% 3.90% 3.89% 7.05%

%Δ 7.61% -1.98% -7.48% -18.52% -49.23% -49.10% -71.91%

Trading Margin 1.31% 1.31% 1.35% 1.80% 2.13% 1.53% 1.99% 0.60%

%Δ 0.00% -2.96% -27.22% -38.50% -14.38% -34.17% 118.33%

Source: BondAdviser Index Platform: BAAUT20DNTR ** Weighted average based on market capitalisation. BAAUT20DNTR is a total return index that is rebalanced on a daily basis. Yield to call based on BondAdviser estimates. ^Inception of BAAUT20DNTR is 16/5/2007.

BEN 2.8%

WBC 4.43%

ANZ 4.63%

AAI 3.15%

CGF 2.09%

AMP 1.84%

WBC 1.4%

BOQ 1.84%

WBC 4.52%

WBC 1.78%

NABPE

AMP 2.85%

BEN 2.38%

SBS 3.73%

SUN 2.1%

NAB 2.1%

IAG 2.07%

ANZ 1.97%

WBC 4.01%

WBC 1.93%

Mac 2.76%

IAG 2.29%

Her 3.38%

Gen 4.68%

MyS 4.12%

Com 1.77%

Cle 5.76%

NAB 1.68%

SUN 2.19%

WBC 1.55%

ANZ 1.82%

QBE 2.65%

NAB 1.96%

NAB 3.1%

IAG 2.37%

NAB 4.45%

ANZ 4.24%

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

0 1 2 3 4 5 6 7

0%

2%

4%

6%

8%

10%

12%

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

Yield to Call** AMP SUN/SBK SBS BEN

BOQ CGF IAG GMA ANZ

CBA NAB WBC AAI HBS

ME MY MBL CLV

BondAdviser | Fixed Income Advisory and Research Market Review: September 2021 24

Corporate Curves

Figure 22. AAA-A Band

Source: BondAdviser; Bloomberg.

Figure 23. BBB Band

Source: BondAdviser; Bloomberg.

Figure 24. Sub IG Band / Unrated Curve

Source: BondAdviser; Bloomberg.

Telstra 4.00% 2022

Stockland 4.50% 2022

GPT 3.591% 2023

Stockland 3.30% 2024

Vicinity 2.60% 2025

Vicinity FRN 1.42% 2025

Optus 1.60% 2025

NBN Co 1.00% 2025

GPT Office Fund 2.525% 2026

Victoria Power Networks 1.603% 2026

Victoria Power Networks FRN 0.80% 2026

GPT 3.657% 2026

Telstra 4.00% 2027

Stockland 2.30% 2028

Victoria Power Networks 2.132% 2028

NBN Co 2.15% 2028

Wesfarmers SLB 1.941% 2028

Optus 2.50% 2030

NBN Co 2.20% 2030

Wesfarmers SLB 2.550% 2031

0.00%

0.20%

0.40%

0.60%

0.80%

1.00%

1.20%

1.40%

1.60%

0 1 2 3 4 5 6 7 8 9 10

AGL 5.00% 2021

Qantas 7.75% 2022

Mirvac 3.50% 2023

Qantas 4.40% 2023

APA Group 3.75% 2023

Ausgrid FRN 1.10% 2024

Woolworths 2.85% 2024

SCA 3.90% 2024

Aurizon 4.00% 2024

Woolworths 1.85% 2025

Coles FRN 0.97% 2025

AusNet Subordinated FRN 3.1% 2080

Ampol Subordinated FRN 2080

Downer 3.70% 2026

Qantas 4.75% 2026

Coles 2.20% 2026

Ausgrid 1.814% 2027

Port Brisbane 2.30% 2027

Goodman Australia 2.20% 2027

Lend Lease 3.4% 2027

Origin 2.65% 2027

Qantas 3.15% 2028

SCA 2.45% 2029

Coles 2.65% 2029

Woolworths 2.80% 2030

LLITST 2.85% 2030

Coles 2.10% 2030

Qantas 5.25% 2030

Aurizon 2.90% 2030

Port Brisbane 2.85% 2031

Lend Lease 3.70% 2031

Pacific National 3.80% 2031

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

0 1 2 3 4 5 6 7 8 9 10

OBLHA

KITT Notes

PPCHB

Civmec Secured Notes

Centuria Notes II FRN 4.25% 2023

SEEK Subordinated Notes

QUBHA

Centuria 5.00% 2024

Peet Wholesale Notes

Avanti Finance Senior Secured Notes

MME HoldCo Secured Notes

Avanti Finance Senior Secured Notes 2

IMF Jan 2026 5.65%

C2FHA

Emeco 6.25% 2026

Peet Wholesale Notes 2

LFSPA

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

7.00%

8.00%

0 1 2 3 4 5 6

BondAdviser | Fixed Income Advisory and Research Market Review: September 2021 25

Credit and Money Markets Charts

Figure 25. Monthly Δ in Trading Margins (ASX Listed Debt & Hybrid Securities)

Source: BondAdviser, Bloomberg as at 30 September 2021.

Figure 26. 3m OIS Spreads

Source: BondAdviser, Bloomberg as at 30 September 2021.

Figure 27. Bank Bill Swap Rates

Source: BondAdviser, Bloomberg as at 30 September 2021.

-2.00%

-1.00%

0.00%

1.00%

2.00%

3.00%

-1.00%

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

7.00%

8.00%

3M AU OIS 3M US OIS 3M EU OIS

0.00%

0.25%

0.50%

0.75%

1.00%

1.25%

1.50%

1.75%

2.00%

2.25%

2.50%

2015 2016 2017 2018 2019 2020 2021

1MBBSW 3MBBSW 6MBBSW

BondAdviser | Fixed Income Advisory and Research Market Review: September 2021 26

Listed Data Tracker

Description Valuation Income Change in Trading Margin Risk

Ticker Issue Size

Expected Maturity

Term Sector Last Price

Accrued YTM Trading Margin

Fixed/Floating Interest Margin

Frequency Current

Rate Cash

Payment Ex-Date

Payment Date

1 month 3 months 6

months 12

months Modified Duration

Credit Duration

Additional Tier 1 (AT1) Hybrids

Major Banks

ANZPE 1610 24/03/2022 0.5 Banks 100.7 0.054 1.99% 1.94% Floating 3.25% Semi-Annual 2.30% $1.14 15/03/2022 24/03/2022 0.02% 0.47% -0.53% -0.61% 0.48 0.48

ANZPF 970 24/03/2023 1.5 Banks 102.9 0.060 1.85% 1.65% Floating 3.60% Semi-Annual 2.54% $1.26 15/03/2022 24/03/2022 -0.08% -0.33% -0.91% -0.85% 0.49 1.44

ANZPG 1622 20/03/2024 2.5 Banks 107.3 0.129 2.15% 1.72% Floating 4.70% Quarterly 3.30% $0.82 9/12/2021 20/12/2021 -0.40% -0.38% -0.88% -1.43% 0.30 2.33

ANZPH 931 20/03/2025 3.5 Banks 105.8 0.104 2.76% 2.09% Floating 3.80% Quarterly 2.67% $0.67 9/12/2021 20/12/2021 -0.03% 0.07% -0.53% -0.97% 0.31 3.22

CBAPD 3000 15/12/2022 1.2 Banks 101.0 0.116 2.22% 2.08% Floating 2.80% Quarterly 1.97% $0.49 6/12/2021 15/12/2021 0.11% 0.14% -0.49% -0.76% 0.21 1.18

CBAPE 1450 15/10/2021 0.0 Banks 100.0 0.214 1.25% 1.20% Floating 5.20% Quarterly 3.65% $0.91 2/12/2021 15/12/2021 -2.93% 0.22% -0.93% -1.44% -0.52 -0.68

CBAPF 1640 31/03/2022 0.5 Banks 101.2 0.161 1.67% 1.62% Floating 3.90% Quarterly 2.74% $0.68 6/12/2021 15/12/2021 0.82% 0.32% -0.68% -0.93% 0.21 0.45

CBAPG 1365 15/04/2025 3.5 Banks 104.1 0.140 2.89% 2.20% Floating 3.40% Quarterly 2.39% $0.60 6/12/2021 15/12/2021 0.02% -0.10% -0.50% -0.97% 0.27 3.23

CBAPH 1590 26/04/2024 2.6 Banks 104.6 0.152 2.29% 1.84% Floating 3.70% Quarterly 2.60% $0.65 6/12/2021 15/12/2021 -0.15% -0.24% -0.70% -1.21% 0.26 2.34

CBAPI 1650 20/04/2027 5.6 Banks 102.5 0.124 3.63% 2.53% Floating 3.00% Quarterly 2.11% $0.53 6/12/2021 15/12/2021 -0.05% -0.05% -0.30% -0.60% 0.27 4.97

CBAPJ 1180 20/10/2026 5.1 Banks 101.4 0.113 3.49% 2.47% Floating 2.75% Quarterly 1.93% $0.48 6/12/2021 15/12/2021 -0.06% -0.09% - - 0.24 4.59

NABPD 1499 07/07/2022 0.8 Banks 102.6 -0.095 1.56% 1.48% Floating 4.95% Quarterly 3.48% $0.88 28/09/2021 7/10/2021 -0.25% 0.09% -0.78% -1.02% 0.03 0.76

NABPF 1874 17/06/2026 4.7 Banks 107.8 0.143 3.20% 2.25% Floating 4.00% Quarterly 2.81% $0.70 8/12/2021 17/12/2021 -0.28% -0.06% -0.34% -0.97% 0.37 4.22

NABPH 2386 17/12/2027 6.2 Banks 105.0 0.125 3.83% 2.63% Floating 3.50% Quarterly 2.46% $0.61 8/12/2021 17/12/2021 -0.10% -0.02% -0.31% - 0.34 5.40

WBCPE 1311 23/09/2022 1.0 Banks 101.6 0.059 1.56% 1.46% Floating 3.05% Quarterly 2.15% $0.54 14/12/2021 23/12/2021 -0.42% -0.30% -0.87% -1.41% 0.24 0.97

WBCPH 1690 22/09/2025 4.0 Banks 103.7 0.070 3.02% 2.23% Floating 3.20% Quarterly 2.25% $0.56 13/12/2021 22/12/2021 -0.09% -0.16% -0.51% -0.95% 0.29 3.68

WBCPI 1423 31/07/2024 2.8 Banks 105.2 0.102 2.29% 1.76% Floating 3.70% Quarterly 2.60% $0.65 9/12/2021 20/12/2021 -0.32% -0.23% -0.82% -1.27% 0.28 2.58

WBCPJ 1723 22/03/2027 5.5 Banks 104.9 0.075 3.51% 2.43% Floating 3.40% Quarterly 2.39% $0.60 13/12/2021 22/12/2021 -0.14% -0.12% -0.38% - 0.34 4.87

WBCPK 1750 21/09/2029 8.0 Banks 101.0 0.120 4.22% 2.78% Floating 2.90% Quarterly 2.04% $0.54 10/12/2021 21/12/2021 - - - - 0.25 6.73

BondAdviser | Fixed Income Advisory and Research Market Review: September 2021 27

Listed Data Tracker

Description Valuation Income Change in Trading Margin Risk

Ticker Issue Size Expected Maturity

Term Sector Last Price

Accrued YTM Trading Margin

Fixed/Floating Interest Margin

Frequency Current

Rate Cash

Payment Ex-Date Payment Date 1 month

3 months

6 months

12 months Mod. Dur. Credit

Duration

Additional Tier 1 (AT1) Hybrids

Other Financials

AMPPA 268 22/12/2021 0.2 Diversified Financials

100.6 0.146 4.45% 4.43% Floating 5.10% Quarterly 5.12% $1.28 13/12/2021 22/12/2021 1.42% -0.16% -0.10% -0.93% 0.23 0.23

AMPPB 275 16/12/2025 4.2 Diversified Financials

99.0 0.225 5.74% 4.90% Floating 4.50% Quarterly 4.51% $1.13 7/12/2021 16/12/2021 -0.23% 0.13% 0.10% -0.11% 0.18 3.73

BENPG 322 13/06/2024 2.7 Banks 103.8 0.175 2.86% 2.37% Floating 3.75% Quarterly 2.63% $0.66 30/11/2021 13/12/2021 0.20% -0.45% -0.42% -1.14% 0.25 2.55

BENPH 502 15/06/2027 5.7 Banks 105.0 0.157 3.98% 2.86% Floating 3.80% Quarterly 2.67% $0.67 6/12/2021 15/12/2021 -0.15% 0.06% -0.28% - 0.33 4.99

BOQPE 350 15/08/2024 2.9 Banks 104.0 0.464 3.01% 2.48% Floating 3.75% Quarterly 2.64% $0.66 27/10/2021 15/11/2021 -0.19% 0.18% -0.41% -1.12% 0.17 2.70

BOQPF 260 14/05/2027 5.6 Banks 105.0 0.470 4.00% 2.89% Floating 3.80% Quarterly 2.67% $0.67 27/10/2021 15/11/2021 -0.13% -0.05% -0.09% - 0.24 4.91

CGFPA 345 25/05/2022 0.6 Diversified Financials

100.6 0.335 3.05% 2.99% Floating 3.40% Quarterly 2.39% $0.60 16/11/2021 25/11/2021 0.25% -0.59% -0.42% -9.34% 0.15 0.64

CGFPB 460 22/05/2023 1.6 Diversified Financials

103.3 0.459 2.86% 2.63% Floating 4.40% Quarterly 3.09% $0.77 11/11/2021 22/11/2021 -0.46% 0.43% -0.53% -1.76% 0.17 1.58

CGFPC 385 25/05/2026 4.6 Diversified Financials

104.8 0.453 4.49% 3.56% Floating 4.60% Quarterly 3.23% $0.81 16/11/2021 25/11/2021 -0.18% 0.24% 0.07% - 0.24 4.09

IAGPD 404 15/06/2023 1.7 Insurance 105.0 0.277 2.40% 2.15% Floating 4.70% Quarterly 4.71% $1.17 6/12/2021 15/12/2021 -0.38% -0.52% -1.06% -1.07% 0.24 1.63

MQGPC 1000 16/12/2024 3.2 Diversified Financials

104.8 0.154 3.10% 2.49% Floating 4.00% Quarterly 3.43% $0.85 2/12/2021 16/12/2021 -0.22% 0.05% -0.12% -0.76% 0.28 2.99

MQGPD 905 10/09/2026 4.9 Diversified Financials

106.5 0.228 3.76% 2.77% Floating 4.15% Quarterly 3.55% $0.89 29/11/2021 10/12/2021 -0.04% 0.20% 0.09% -0.57% 0.33 4.38

MQGPE 725 18/09/2027 6.0 Diversified Financials

100.7 0.080 3.95% 2.79% Floating 2.90% Quarterly 2.49% $0.62 7/12/2021 20/12/2021 -0.07% -0.06% -0.14% - 0.24 5.29

SUNPF 375 17/06/2022 0.7 Diversified Financials

101.6 0.147 2.12% 2.04% Floating 4.10% Quarterly 2.88% $0.72 2/12/2021 17/12/2021 0.37% 0.39% -0.41% -0.77% 0.22 0.70

SUNPG 375 17/06/2024 2.7 Insurance 104.9 0.130 2.33% 1.84% Floating 3.65% Quarterly 2.56% $0.64 2/12/2021 17/12/2021 -0.78% -0.56% -0.89% -1.47% 0.27 2.57

SUNPH 389 17/06/2026 4.7 Insurance 101.4 0.107 3.65% 2.71% Floating 3.00% Quarterly 2.11% $0.53 2/12/2021 17/12/2021 -0.12% 0.07% -0.34% -0.56% 0.24 4.29

SUNPI 405 19/06/2028 6.7 Insurance 99.9 0.056 4.21% 2.92% Floating 2.90% Quarterly 2.04% $0.48 6/12/2021 17/12/2021 - - - - 0.21 5.84

MBLPC 641 22/12/2025 4.2 Insurance 108.5 0.116 3.40% 2.55% Floating 4.70% Quarterly 4.02% $1.00 9/12/2021 21/12/2021 -0.12% -0.04% -0.12% -0.86% 0.37 3.79

MBLPD 655 07/09/2028 6.9 Insurance 100.3 0.271 4.22% 2.89% Floating 2.90% Quarterly 2.48% $0.69 19/11/2021 7/12/2021 0.03% - - - 0.19 5.99

BondAdviser | Fixed Income Advisory and Research Market Review: September 2021 28

Listed Data Tracker

Description Valuation Income Change in Trading Margin Risk

Ticker Issue Size

Expected Maturity

Term Sector Last Price

Accrued YTM Trading Margin

Fixed/Floating Interest Margin

Frequency Current

Rate Cash

Payment Ex-Date

Payment Date

1 month 3 months 6 months 12

months Mod. Dur.

Credit Duration

Additional Tier 1 (AT1) / T2 Hybrids / Bonds

Other Financials

BENHB 75 Perpetual - Banks 99.5 0.105 2.74% 1.02% Floating 1.00% Quarterly 1.02% $0.26 12/11/2021 30/11/2021 0.00% -0.16% -0.66% -0.66% - -

NABPE 943 20/02023 2.0 Banks 101.1 0.061 1.97% 1.66% Floating 2.20% Quarterly 2.21% $0.55 9/12/2021 20/12/2021 0.05% 0.19% 0.47% 0.47% 0.23 1.92

SBKHB 200 Perpetual - Insurance 99.7 0.071 2.59% 0.76% Floating 0.75% Quarterly 0.78% $0.20 16/08/2021 2/09/2021 0.01% -0.32% -0.49% -0.49% - -

Corporate Hybrids

CWNHB 630 23/07/2022 0.8 Consumer

Discretionary 85.50 0.2 27.63% 27.55% Floating 4.00% Quarterly 4.01% $1.00 3/12/2021 14/12/2021 4.60% 20.09% 19.64% 19.64% 0.15 0.66

C2FHA 199 20/04/2026 4.6 Real Estate 105.00 0.8 4.16% 3.24% Floating 4.25% Semi-Annual 4.27% $1.08 13/10/2021 20/10/2021 0.00% -0.07% - - 0.14 4.03

LFSPA 150 Perpetual - Diversified Financials

99.80 0.0 5.82% 4.80% Floating 4.75% Semi-Annual 3.34% $1.11 18/01/2022 27/01/2022 - - - - - -

NFNG 251 Perpetual - Chemicals 87.50 1.8 6.81% 4.88% Floating 3.90% Semi-Annual 4.00% $2.00 6/10/2021 15/10/2021 0.08% 0.05% -0.43% -0.43% - -

RHCPA 260 Perpetual - Health Care 103.80 -0.3 6.52% 4.59% Floating 4.85% Quarterly 3.46% $1.74 27/09/2021 20/10/2021 -0.11% -0.03% -0.04% -0.04% - -

Listed Bonds / Convertibles / Preference Equity

AYUHC 115 15/12/2024 3.2 Diversified Financials

100.63 0.4 2.55% 1.93% Floating 2.00% Quarterly 2.03% $0.51 5/10/2021 14/10/2021 -0.16% 0.11% -0.74% -0.74% 0.04 2.90

AYUHD 207 15/12/2026 5.2 Diversified Financials

100.00 0.5 3.29% 2.25% Floating 2.15% Semi-Annual 2.18% $0.55 5/10/2021 14/10/2021 -0.23% -0.16% -0.44% -0.44% 0.03 4.62

AYUPA 120 Perpetual - Diversified Financials

107.10 3.3 6.88% 4.94% Fixed 7.14% Semi-Annual 5.00% $2.51 6/10/2021 15/10/2021 -0.21% 0.07% 0.51% 0.51% - -

CVCG 60 22/06/2023 1.7 Diversified Financials

96.20 0.0 6.68% 6.43% Floating 3.75% Quarterly 3.77% $0.95 9/12/2021 31/12/2021 0.18% 0.40% 0.27% 0.27% 0.22 1.44

NCCGA 23 30/09/2026 5.0 Diversified Financials

100.95 0.0 4.29% 3.28% Fixed 4.50% Quarterly 4.50% $2.25 22/03/2022 31/03/2022 -0.25% -0.20% - - 4.44 4.44

OBLHA 76 8/01/2022 0.3 Diversified Financials

100.00 0.0 4.22% 4.20% Floating 4.20% Quarterly 4.22% $1.06 20/12/2021 31/12/2021 -1.35% 2.01% -1.35% -1.35% 0.25 0.25

PPCHB 50 5/10/2022 1.0 Real Estate 100.00 -0.1 4.69% 4.58% Floating 4.65% Quarterly 4.68% $1.18 24/09/2021 5/10/2021 1.53% 0.07% 1.28% 1.28% 0.01 0.99

QUBHA 305 5/10/2023 2.0 Industrials 103.98 -0.1 2.16% 1.85% Floating 3.90% Quarterly 3.93% $0.99 24/09/2021 5/10/2021 -0.56% -0.48% -0.38% -0.38% 0.06 1.93

URFHC 175 24/12/2021 0.2 Real Estate 99.50 1.3 8.99% 8.39% Fixed 7.75% Quarterly 7.75% $1.95 17/09/2021 30/09/2021 1.00% 1.40% 1.01% 1.01% 1.45 1.45

BondAdviser | Fixed Income Research and Advisory Market Review: September 2021

General Disclosures

BondAdviser has acted on information provided to it and our research is subject to

change based on legal offering documents. This research is for informational purposes

only.

This information discusses general market activity, industry or sector trends, or other

broad-based economic, market or political conditions and should not be construed as

research or investment advice.

The content of this report is not intended to provide financial product advice and must

not be relied upon as such. The Content and the Reports are not and shall not be

construed as financial product advice. The statements and/or recommendations on this

web application, the Content and/or the Reports are our opinions only. We do not

express any opinion on the future or expected value of any Security and do not explicitly

or implicitly recommend or suggest an investment strategy of any kind.

The content and reports provided have been prepared based on available data to which

we have access. Neither the accuracy of that data nor the methodology used to produce

the report can be guaranteed or warranted. Some of the research used to create the

content is based on past performance. Past performance is not an indicator of future

performance. We have taken all reasonable steps to ensure that any opinion or

recommendation is based on reasonable grounds. The data generated by the research

is based on methodology that has limitations; and some of the information in the reports

is based on information from third parties.

We do not guarantee the currency of the report. If you would like to assess the currency,

you should compare the reports with more recent characteristics and performance of the

assets mentioned within it. You acknowledge that investment can give rise to substantial

risk and a product mentioned in the reports may not be suitable to you.

You should obtain independent advice specific to your circumstances, make your own

enquiries and satisfy yourself before you make any investment decisions or use the

report for any purpose. This report provides general information only. There has been

no regard whatsoever to your own personal or business needs, your individual

circumstances, your own financial position or investment objectives in preparing the

information.

We do not accept responsibility for any loss or damage, however caused (including

through negligence), which you may directly or indirectly suffer in connection with your

use of this report, nor do we accept any responsibility for any such loss arising out of

your use of, or reliance on, information contained on or accessed through this report.

© 2021 Bond Adviser Pty Ltd. All rights reserved.